Embed Size (px)

Citation preview

Retail Competition in theU.S.: Is It Working?

Theresa Flaim, Ph.D.Vice President, Strategic Planning

Niagara_Mohawk-Harvard Electricity Policy GroupCambridge, MassachusettsMay 22-23, 2000

Outline of Presentation

Fewmassmarketcustomersare switchingsuppliersDoesthe lackof switchingmeanmarketsareworkingor failing?Alternativeapproachesare beingadoptedThe emergingconsensus:the designof defaultsupplyis the criticalissue

2

1

- ---- - --

Few mass market customers

are switching suppliers

In many states where retail access has.beenenacted (California, Massachusetts, New York,etc.), fewer than 2% of customers haveswitched suppliersEven in Pennsylvania, where switching is beingheavily subsidized,* only 10-12% of customershave switched suppliers.

*Whencustomers switch commodity suppliers, they receive a creditthat is 0.6 to 1.3 cents/kWh more than it actually costs the utility toserve them. This subsidy is called "headroom."

3

Why are so few mass marketcustomers switching suppliers?

Wildlyunrealistic expectationsCirca1994: "Retail competition in electricity willspread much more rapidly than it did in natural gas"

Problems in wholesale marketsImmaturewholesalemarketsmakeit difficult andexpensivefor someretailersto acquirecommoditysupplies

Conflicting public policy goals in designingtransition plansUnderlyingeconomics of commodity retailing

4

2

Most states are trying toachieve conflicting goals:

Protect customers from "undue" price volatilityduring the transitionLower prices for all customers, not just thosewho switch

Promote customer switchingCreate an efficient market

These goals willdictate different designs fordefault service

5

Economics of CommodityResellers

Haveto lookat underlyingeconomicsto get areal sense of what is happeningand whyOverallproblem: the priceof default service inmost states has been capped, makingit hard fornew entrants to add value through pricehedgingTwofeatures of commodityretailingareimportant:

cost and ability to hedge the commoditytransaction costs

6

3

--------

- --

Economics of commodityretailing for small customers

"'C- i-. -#_a:'; , '".",,_._,,>

There are four widely recognizedpr5blems thafrifake itdifficult to profitably serve mass market (residential andsmall commercial) customers:

Smallvolumes:an averageresidentialcustomerconsuming 1000 kWh per month would have a commoditybill=$30jmonth (if commodity prices average 3 cjkWh)Thin margins:marginsare squeezedby defaultsupplyprices, but competition willalso yield low margins (3-7%for other retail commodities); 5% of $30 =$1.50jmonth;gross profit on a single pack of cigarettes = $1.00

High transaction costsHard to offer value-added hedging services whendefault supplies are already hedged

7

Transaction costs are high relative toavailable margin for small customers

BackOfficeCosts (aka Customer Account ManagementServices (CAMS»

billingcentralpaymentprocessingcollectionscallcentermeter readingand meter services

Sales and MarketingCostsgeneral &administrative costsdistribution channel

offer (acquisitioncost)fulfillment

8

4

-- - -

Transaction costsoil

Incumbent utilitieshave two cost advantagesrelativeto ESCosin terms of transaction costs

Scope economies in billing,central payment, andcollections processing due to the fact that theyalready provide these services for delivery (T&D)andcan extend those functions to the commodity withnegligible marginal costAs a default provider (commodity purchased throughthe spot market) there is no need to invest incustomer acquisition, a key cost driver for newentrants

9

Customers need a reason to switch. . .CortldentlaDRAFT

. When value can't be offered in other ways, price discounts areneeded to induce most customers to switch.

Price Discounts Required to Cause Customers to Switch

L8goClicu.......,.... .....

""

%kWhf1a

b

....'''''"

0.0... 2 5.0... 7 to." 12 '1.0'11o

PriDeDEal" f'e",,,,,ofTotilBiI) Pro Osca.lft f'e1t81tOfTOtai BiI)

. Big custaners switch for lower discounts.Bil discounts are easier to produce for big custaners (3040% of bill is commodity).Only 20% of total bill is commodity for typical resi:lential customer_u u__.

10

5

If few customers switch, aremarkets working or failing?

One view: markets are workingIf there are no barriers to entry, and customers don'tswitch, then you have success by definition.If default supply is the unhedged wholesale spotmarket price of electricity, and customers are notwillingto buy from retailers, they are simply sayingthe value they would derive isn't worth the priceretailers need to charge to cover their costs.Regulators shouldn't try to manage outcomes. Theyshould let customers decide what is best for them.

11

If few customers switch, aremarkets failing? . . .

The opposing view: markets are failing

If customers aren't switching, then by definition themarket can't be working, (number of customers whoswitch is the measure of success)

Something must be done to "fix"the market

12

6

Alternative approaches torestructuring retail markets

Eliminate barriers, then let markets work (CA,MA, NY etc. are close to this approach)

Subsidize entry by establishing back out creditshigher than the utility's cost of providing thecommodity (PA, NJ, etc.)

Bid out the right to serve customers (customersmayor may not be allowed to "opt out") (ME,CT, PA, NJ, etc.)

Completely separate the wires function from theretailing function (TX)

13

If customers are forced to buy fromcommodity retailers, what will itcost?

Assume the commodity is the spot market so we canfocus on transaction costs

Actual transaction costs willvary, depending the firm'sscale of operations, sales and marketing costs andcustomer switching ratesA conservative estimate is $50-$100 per mass marketcustomer per year assuming market maturity. Ifaverage monthly consumption is (1000 kWh/month) andtotal average residential prices are:

7 c/kWh, total billwould increase by 6 to 12%5 c/kWh, total billwould increase by 8 to 17%

14

7

..

Why isn't the answer to justincrease the utility back-out credit?

,,',," ,'}7,-;,~'~t. .~~

New entrants argue that back-out creditsShou1acovertheir retail transactions costs

If E5Cosbill for both delivery and commodity, some costsmay be saved, but others are increased, and the bulk ofthe costs can't be eliminated

50 long as delivery servicesare billed on a volumetric,per customer basis, the utility must maintain systemsand databasesto support "retail-level" billingThis is true, even if the E5Cohas primary contact withcustomer and even if utility is not the default providerUtilities don't have incentive costs (delivery is amonopoly service)

15

Confirming EconomicEvidence is Emerging . . .

ME recently conducted an auction and rejected bids for2 of the 3 utilities becausethey were "too high"GPUrecently conducted an auction for their first block ofcustomers; nobody submitted a bid to serve them

In Pennsylvania,people are beginning to realize thatnon-switching customers will pay billions of dollars morethan they should have to due to the subsidizedshoppingcredits

Texas utilities are proceedingwith restructuring andinvesting tens of millions of dollars in duplicate customercare systems (call center, billing, collections, paymentprocessing,etc.)

16

8

-

The design of default supplyis the critical issue

We continue to believe that default supply should bebased on the un-hedged wholesale spot market price ofelectricity

This is what willactually happen in the physical marketThe ISO price is the efficient (market determined) priceIt provides an appropriate benchmark against whichcustomers can evaluate the benefits of price hedgingservices

Some load response is necessary to have a well-functioning wholesale spot market (avoiding price spikesand the need to resort to command and control measuresto balance load and supply in real time markets)

17

Design of default supply iskey to retail markets . . .

In this default supply model:The ISO procures the supply through a competitiveauction

The distribution utilityacts as a settlement agent forthe ISO. It can provide this service at the lowestadministrative cost because it has scope economiesbetween retailing delivery and retailing thecommodity

The major concern expressed about this model has beenprice volatility--willit be too much or too little topromote efficient retail markets?

18

9

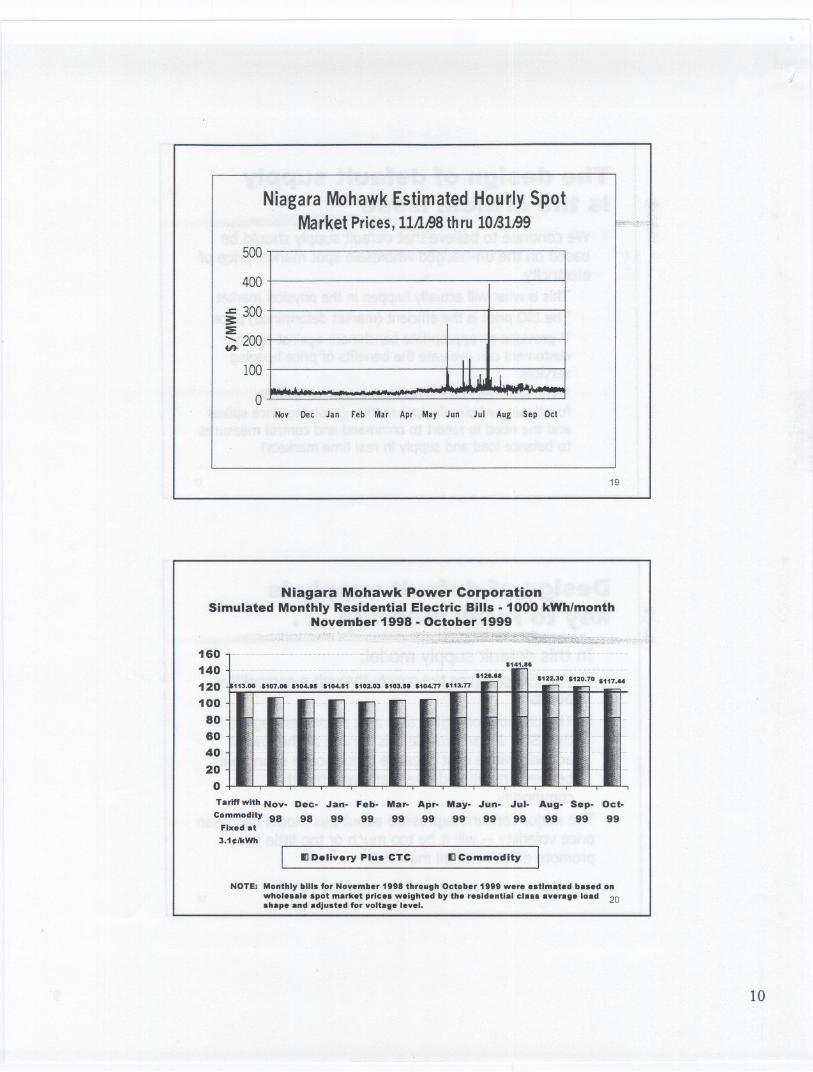

Niagara Mohawk Power CorporationSimulated Monthly Residential Electric Bills -1000 kWh/month

November 1998 - October 1999

160140

120100

8060

4020

oTanH with Nov-

Commodity 98Fixed at

3.1j1kWh

Dec- .Jan- Feb- Mar- Apr- May- .Jun- .Jul- Aug- Sep- Oct-98 99 99 99 99 99 99 99 99 99 99

IJ Delivery Plus CTC IJ Commodity

NOTE: Monthly bill. for November 1188 through October 1111 were e.tlmated ba.ed onwhole.ale .pot market price. weighted by the re.ldentlal cia.. average load 20.hape and adju.ted for voltage level.

10

Niagara MohawkEstimated Hourly SpotMarketPrices,111.1,98thru 10131,99

500

400

-= 3003::e...... 200

100II

1.1 dLII I.L

0Noy Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct

19

'1.1.".12.... '122.30'120.70.117....113... '107'" .1..... .1....1 "02.D3'103.88'1"'77 '113.77

-- -- ._- \--

Niagara Mohawk Power CorporationSimulated Monthly Electric Bills -Large Industrial

November 1998 - October 1999

400,000

350,000

300,000

250,000

200,000

150,000

100,000

50,000

o

an....--12",f17

12&4,411 8212,111 1241,217

Nov- Dec- Jan- Feb- Mar- Apr- May- Jun- JuJ- Aug- Sep- Oct-98 98 99 99 99 99 99 99 99 99 99 99

8T&D II CTC [) Commodity

NOTE: Monthly bill. for Nov. 1998 through Oct. 1199 were e.tlmated ba.ed on a 7MW, 80%load factor cu.tomer on SC3A (TOU) rate.. Commodity costs were ba.ed onwhole.ale .pot market prices adjusted for voltage level. 21

Design of default supply iskey to retail markets . . .

Everyother alternative model for default supply we canthink of has many more problems. For example, ifdefault supply continues to be offered at a relativelylow, fixed (hedged) price, it will:

interfere with the development of an efficient retailmarket and

pose many additional problems and risks

22

11

-

Design of default supply iskey to retail markets . . .

If default supply continues to be hedged:Which customers are eligible for default supply andunder what circumstances?

Who decides what supplies should be acquired andhow to acquire them? How will supply costs becollected and from whom?

Who is at risk if new stranded costs are created?

Who is at risk if insufficient supplies are acquired?

23

Summary Observations

We need rules about default supply becauseofthe nature of the network

Among the choicesavailable to retail customersshould be the option of buying wholesale at thelow administrative costs utilities can offer

It is not a good idea impose a structural changewhose immediate impact will be to increase thecost of serving residential customers 10-20%without any market evidence that real value isbei ng created

24

12

Summary Observations . . .

Should billing be made competitive?issues and problems are widely misunderstoodallowing ESCosto issue a combined commodity anddelivery bill is notthe samething as outsourcingcustomer preference for a single bill is a symptom of amuch larger problem: sufficient value isn't being createdto make it worth someone'swhile to write out anothercheck

the extent to which moving retailing functions to thecompetitive sector can reduce cost duplication dependslargely on whether delivery servicesare billedvolumetrically

25

13

- -