Embed Size (px)

Citation preview

Volume 4, Number 3, July – September’ 2015

ISSN (Print):2279-0977, (Online):2279-0985

PEZZOTTAITE JOURNALS SJIF (2012): 3.23, SJIF (2013): 5.057, SJIF (2014): 5.871

International Journal of Applied Services Marketing Perspectives© Pezzottaite Journals. 1747 |P a g e

RETAIL BANKING MODEL AND THE RESPONSIBILITY OF BANK BRANCHES:

WITH SPECIAL REFERENCE TO ICICI BANK

Dr. Farhina S. Khan19 Dr. Syed Shahid Mazhar20 Mohd. Ariz Siddiqui21

ABSTRACT

Retail Banking is purely an individual-centric activity of commercial banks meant for individual customers only, which

comprises all class of customer groups such as businessmen, academicians, pensioners, housewives, students, service class

and professionals. However, the concept of retail banking the expanded its concept by including High Net Worth Individuals

(HNW), non-individual groups and associations like small and medium businesses in its conceptual frame in the later years.

The pillars of its operations are viz. Multiple Products, Multiple Channels of Distribution and Multiple Customer Groups.

Analyses of ICICI Bank based on perception and views of the existing customers to have a holistic view of the organisations.

To understand the perception of customers towards ICICI offerings at the branch level a structured, disguised questionnaire

has been prepared to collect information regarding the customer‟s perception regarding the CRM policy of ICICI Bank at the

time of branch visit. The response of the customers has been measured on „Five-Point Likert Scale‟, starting from „Highly

Satisfied‟, „Satisfied‟, „Moderately Satisfied‟, „Dissatisfied‟ and ending on „Highly Dissatisfied‟ and the interpretation has

been done on the basis of „Percentage Analysis‟.

KEYWORDS

Retail Banking Model, Bank Branches, ICICI Bank etc.

INDIAN BANKING OUTLINE

It is the Financial System in an economy, through which the efficient movement of funds takes place. It facilitates capital from the

various surplus sectors of the economy to the deficient sectors and accelerates the pace of development and welfare of the

economy as a whole. The Financial system is a composition of complex and interconnected set of Money Market, Capital Market,

Central Bank, Financial Intermediaries and Financial Instruments.

Chart-1

Sources: Authors Compilation

19Assistant Professor, Faculty of Management & Research, Integral University, Uttar Pradesh, India, [email protected] 20Associate Professor, Faculty of Management & Research, Integral University, Uttar Pradesh, India, [email protected] 21 Assistant Professor, Faculty of Management & Research, Integral University, Uttar Pradesh, India,

Volume 4, Number 3, July – September’ 2015

ISSN (Print):2279-0977, (Online):2279-0985

PEZZOTTAITE JOURNALS SJIF (2012): 3.23, SJIF (2013): 5.057, SJIF (2014): 5.871

International Journal of Applied Services Marketing Perspectives© Pezzottaite Journals. 1748 |P a g e

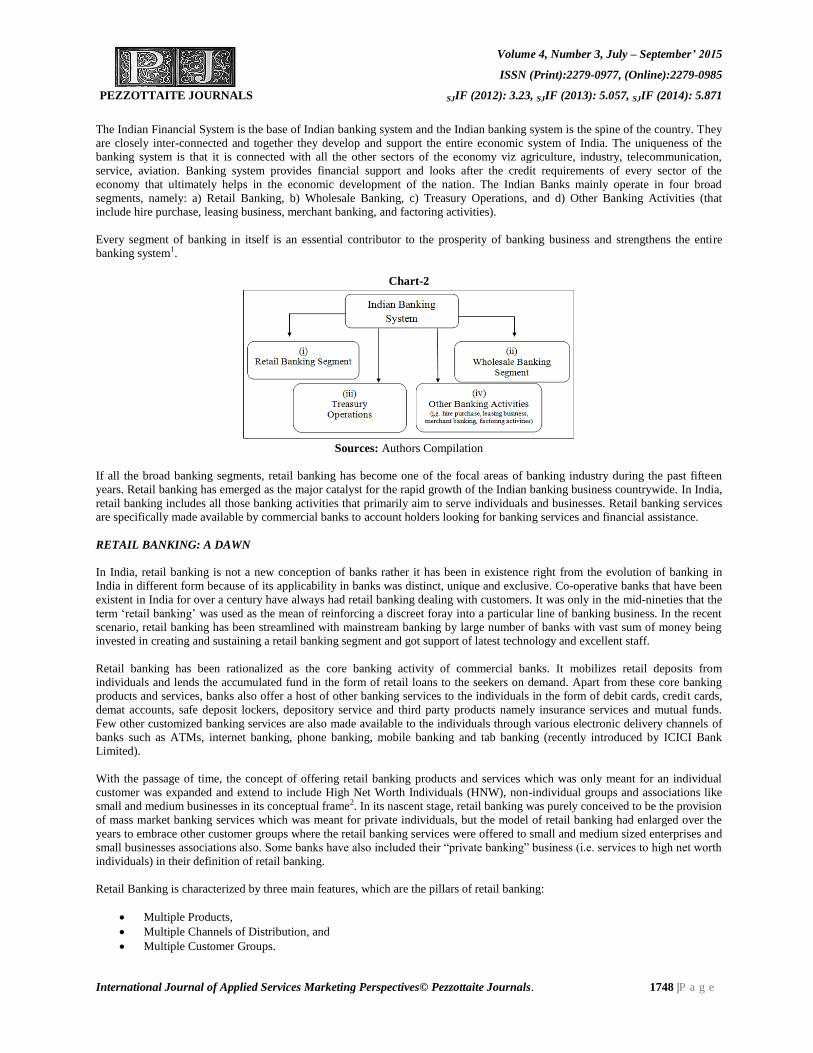

The Indian Financial System is the base of Indian banking system and the Indian banking system is the spine of the country. They

are closely inter-connected and together they develop and support the entire economic system of India. The uniqueness of the

banking system is that it is connected with all the other sectors of the economy viz agriculture, industry, telecommunication,

service, aviation. Banking system provides financial support and looks after the credit requirements of every sector of the

economy that ultimately helps in the economic development of the nation. The Indian Banks mainly operate in four broad

segments, namely: a) Retail Banking, b) Wholesale Banking, c) Treasury Operations, and d) Other Banking Activities (that

include hire purchase, leasing business, merchant banking, and factoring activities).

Every segment of banking in itself is an essential contributor to the prosperity of banking business and strengthens the entire

banking system1.

Chart-2

Sources: Authors Compilation

If all the broad banking segments, retail banking has become one of the focal areas of banking industry during the past fifteen

years. Retail banking has emerged as the major catalyst for the rapid growth of the Indian banking business countrywide. In India,

retail banking includes all those banking activities that primarily aim to serve individuals and businesses. Retail banking services

are specifically made available by commercial banks to account holders looking for banking services and financial assistance.

RETAIL BANKING: A DAWN

In India, retail banking is not a new conception of banks rather it has been in existence right from the evolution of banking in

India in different form because of its applicability in banks was distinct, unique and exclusive. Co-operative banks that have been

existent in India for over a century have always had retail banking dealing with customers. It was only in the mid-nineties that the

term „retail banking‟ was used as the mean of reinforcing a discreet foray into a particular line of banking business. In the recent

scenario, retail banking has been streamlined with mainstream banking by large number of banks with vast sum of money being

invested in creating and sustaining a retail banking segment and got support of latest technology and excellent staff.

Retail banking has been rationalized as the core banking activity of commercial banks. It mobilizes retail deposits from

individuals and lends the accumulated fund in the form of retail loans to the seekers on demand. Apart from these core banking

products and services, banks also offer a host of other banking services to the individuals in the form of debit cards, credit cards,

demat accounts, safe deposit lockers, depository service and third party products namely insurance services and mutual funds.

Few other customized banking services are also made available to the individuals through various electronic delivery channels of

banks such as ATMs, internet banking, phone banking, mobile banking and tab banking (recently introduced by ICICI Bank

Limited).

With the passage of time, the concept of offering retail banking products and services which was only meant for an individual

customer was expanded and extend to include High Net Worth Individuals (HNW), non-individual groups and associations like

small and medium businesses in its conceptual frame2. In its nascent stage, retail banking was purely conceived to be the provision

of mass market banking services which was meant for private individuals, but the model of retail banking had enlarged over the

years to embrace other customer groups where the retail banking services were offered to small and medium sized enterprises and

small businesses associations also. Some banks have also included their “private banking” business (i.e. services to high net worth

individuals) in their definition of retail banking.

Retail Banking is characterized by three main features, which are the pillars of retail banking:

Multiple Products,

Multiple Channels of Distribution, and

Multiple Customer Groups.

Volume 4, Number 3, July – September’ 2015

ISSN (Print):2279-0977, (Online):2279-0985

PEZZOTTAITE JOURNALS SJIF (2012): 3.23, SJIF (2013): 5.057, SJIF (2014): 5.871

International Journal of Applied Services Marketing Perspectives© Pezzottaite Journals. 1749 |P a g e

Table-1

Retail Deposits Retail Loans Ancillary Services

Savings Account Home Loans Credit Cards

Current Account Auto Loans Debit Cards

Fixed Deposit Account Two-Wheeler Loans Telephone Banking

Recurring Deposits Educational Loans Internet Banking

Others Short Term Deposits Personal Loans Mobile Banking

Gold Loans Online Bill Payment

Zero Balance Account For Salaried People Event Loans Investment

No frills Account Credit Cards Loans Mutual Funds

Senior Citizen Deposit Account Consumer Loans Insurance Policies

Pension Small Trade Related Advances

To Individuals Safe Deposit Lockers

Crop Loans Demat Account

Advisory Services

Sources: Authors Compilation

Chart-3

Sources: Authors Compilation

Chart-4

Sources: Authors Compilation

REVIEW OF LITERATURE

“Retail banking in changing scenario” N. S. Gujral. The article discusses on the rapid changes seen in the Indian banking sector.

The author has discussed about the concept of Retail Banking and the various product and services offered by the banks like

personal loans, insurance products, advisory services, deposit accounts. The author has elaborated on the impact of retail banking

and makes suggestion for the banks that are providing retail services. The author has made an honest attempt to outline a

methodology by which success could be achieved by the banks. The author is of the opinion that a systematic and calculated

approach is a prerequisite for the success in long run.

Volume 4, Number 3, July – September’ 2015

ISSN (Print):2279-0977, (Online):2279-0985

PEZZOTTAITE JOURNALS SJIF (2012): 3.23, SJIF (2013): 5.057, SJIF (2014): 5.871

International Journal of Applied Services Marketing Perspectives© Pezzottaite Journals. 1750 |P a g e

“Retail Banking: Retail Marketing of Banking Services” by P. K. Pradhan. The article focuses on concept emergence and growth

of retail banking in India and discusses the factors that led to the retail banking. The article makes a comparative study of the

Retail banking performance of SBI and ICICI and concludes that the performance of ICICI was much better than SBI even

through ICICI has been performing for a short period. The various ratios indicate the performance in respect to the return on asset,

equity and profit per employee.

“Retail Banking in India” by K. M. Nayak. In the article the author has made a comprehensive study of the performance of Retail

banks in the article of advanced branches, transactions, ATMs, etc. The author has discussed the opportunities and challenges of

Retail Banking like entry of foreign player, information technology frequent changes in regulatory requirements network

management challenges. The author has used secondary information to show the performance of banks using retail facilities.

“Retail banking - hotter than Vindaaloo”. Natika P. Jain. In an article, the author has tried to study the needs of consumer for retail

products of different income groups. The study has tried to bring out the driving factors for retail banking and its effect on

banking system. The article outlines the various retail banking growth phases in Indian scenario and discusses the future

challenges in retail banking.

OBJECTIVES OF THE STUDY

To study the conceptual framework of retail banking in modern society.

To know the satisfaction of customers of ICICI Bank about the services offered to them at the time of branch visit at

Lucknow district.

To identify the challenging issues for ICICI Bank to attract potential customers.

To suggest measures that can help the bank to improve its performance in retail banking segment.

RESEARCH METHODOLOGY

Collection of Data

Data was collected from both primary and secondary sources. The secondary data has been compiled from newspapers, books,

journals, magazines, e-magazines, various websites and official website of ICICI bank limited. To collect primary data and

information about the behavior, intentions, attitude, awareness, demographic and satisfaction level of ICICI retail customer, a

survey has been executed. For which, a structured non-disguised questionnaire was administered. The questionnaire was

constructed on a five point Likert Scale method. Questions were direct and close ended and pre-arranged in a simple manner.

Area and Time of Survey

The area selected to conduct the survey is Lucknow city. The time of survey execution was April 2015 to July 2015.

Size of the Sample & Sampling Procedure

The researcher had administered 200 questionnaires out of which 150 respond were received. Different location of branch has

been taken as a stratification variable to form a stratum (location-wise) and by using stratified random sampling a sample was

drawn from each branch to acquire information regarding customer‟s products and services usage pattern and their satisfaction

level from it.

DATA ANALYSIS

To find out the view of the customer, data on satisfaction has been collected on the parameters selected by the researcher. It deals

with the response of ICICI customers from the services they receive at the time they visited the bank branch. „Branch Visit‟ is one

of the most important parameter to know the satisfaction of customer as bank is the place where a customer and a bank employee

meet in person to each other.

Apart from the type of banking services being offered, the manner in which the services are offered to a customer is another very

significant aspect, which makes a big difference amongst banks. A branch visit of a customer can be turned into a productive

business deal by the bank staff, if they would be able to create an impression on customer by their approach of dealing.

The second objective of the paper is to find out the satisfaction level of customers of ICICI Bank concerning the branch visit.

Percentage of Satisfaction Level of Customers of ICICI Bank at the time of branch visit at Lucknow

Volume 4, Number 3, July – September’ 2015

ISSN (Print):2279-0977, (Online):2279-0985

PEZZOTTAITE JOURNALS SJIF (2012): 3.23, SJIF (2013): 5.057, SJIF (2014): 5.871

International Journal of Applied Services Marketing Perspectives© Pezzottaite Journals. 1751 |P a g e

Table-2

Sources: Authors Compilation

In spite of technological revolution and electronic banking expansion, many people still consider bank branch to be the primary

customer relationship channel. Customer still seems to have a strong affinity to branches even though they may visit them less. In

context to India, a branch visit is the most preferred way of customers to execute banking transactions, reason being, and customer

wants more control and security of his funds; moreover, majority of people in India are not much technically skilled to perform

online banking transaction, which is the basic requirement to use e-banking service.

Therefore, customers are usually inclined to visit a branch to satisfy their banking needs, as it is the touch point for a customer to

meet bank employees and discuss their issues with them directly in person. Therefore, at the branch level, with the help of

technology, bank should provide the best possible service to customers.

The collected data and its analysis shows that the factors like employees behaviour, their communication skill and knowledge,

prompt response and service delivery, grievance and query handling needs attention and care to strengthen up their CRM policy.

Besides, banking hours and other routine transactions carried on in banks, rest variables selected requires bank to put in efforts to

change the view of customers and make them satisfied by employing corrective measures.

Absolute Value of the Customers and their Responses

Table-3

Sources: Authors Compilation

Volume 4, Number 3, July – September’ 2015

ISSN (Print):2279-0977, (Online):2279-0985

PEZZOTTAITE JOURNALS SJIF (2012): 3.23, SJIF (2013): 5.057, SJIF (2014): 5.871

International Journal of Applied Services Marketing Perspectives© Pezzottaite Journals. 1752 |P a g e

The Challenging Issues for ICICI Bank to Attract Potential Customers

The banks in India are working on the same pattern of operations. Various products, processes, services deployed in banks are

almost. There is a very thin line which marks the differences prevails amongst Indian banks. This thin line comprises various add-on

customized services offered by bank, approach towards customers, CRM policy and so on yet one of the most important factor that

plays an influential role is the CRM policy of bank.

FINDINGS

The relevant information attained from the survey revealed the fact that although maximum numbers of customers of ICICI bank are

satisfied from its retail products and services yet there are substantial numbers of customers who are just moderately satisfied with

the same and some are dissatisfied too. This appeared to be a challenge for the bank to convert those moderately satisfied and

dissatisfied customers into satisfied one because if bank fails, then it may lose its customers to other banks. It has been found out that

there are few banking products and services that need to be improved by the bank to retain customers:

The customers of ICICI are satisfied by the routine banking transactions at the branch such as cash deposit / cash

withdrawal/fund transfer/cheque deposit.

The customers of ICICI bank seem slightly unhappy by sometimes-unfriendly behavior of the employees towards

customers. The customers have the view that bank staff shall behave with more courtesy and graciously.

During the survey, it was found that ICICI customers were with the opinion that bank should recruit staff with an

impressive communication skill and comprehensive knowledge about the banking products and services. The data

reflected that although there were customers who were satisfied by the communication skill and knowledge of the

banking staff yet there are relatively more customers who were not completely satisfied with the same.

The customers of the bank are unsatisfied by the response of employee and promptness towards customer‟s queries and

delivery of product and services at the right time. Customers of ICICI feel that the bank staff is quite not promptly and

quickly delivers services on time.

In case of employees‟ proper product information dissemination, customers are of the perception that the banking staffs

lack quality of proper imparting of information to the customers / public.

The customers of ICICI bank are discontented from the query handling by bank staff at the bank counter. In customers‟

view, bank staff is not sincere enough to handle customers‟ query at the counter. They take it extremely casually and

frustratingly.

The data reflect that the customers of ICICI are unhappy with response of employees towards solving their grievances.

The data reveals that the customers are unsatisfied by the bank‟s clause of holding / maintaining a monthly balance in

the bank account. In their view, it is discouraging for the customers and compels customers to switch their account to

other public sector bank with lower limit.

A considerable percentage of customers in ICICI bank are unsatisfied by the friendliness and behavior of the employees

towards customers. If bank staffs do not rectify this adopt good behavior then it would create a bad image of the bank in

market.

The collected data shows that substantial percentage of customers is not happy by the communication skill and

promptness of bank employee in their public dealing. It may be a cause of customer dissatisfaction and finding another

bank for banking purpose.

The survey results display that improper product information dissemination can result in unfavorable perception about

the knowledge of employee and create a doubt on its competency, which would degrade the brand image and standard

quality of bank recruitment policy.

The data analysis shows that customers are unsatisfied by the grievance handling system of bank. If this key point

would not be fixed by bank then there would be a major chance that bank would lose its customers to peer banks.

SUGGESTIONS

Every customer is valuable asset and an opportunity for bank. A satisfied customer may work as a visiting card of bank

through which other people can get attracted towards bank. Thus, bank staff should be much polite and welcoming to

Volume 4, Number 3, July – September’ 2015

ISSN (Print):2279-0977, (Online):2279-0985

PEZZOTTAITE JOURNALS SJIF (2012): 3.23, SJIF (2013): 5.057, SJIF (2014): 5.871

International Journal of Applied Services Marketing Perspectives© Pezzottaite Journals. 1753 |P a g e

customers and behave in friendly and good manner towards customer especially because a customer whether a new one

or existing one treated unimportantly will create dissatisfaction among them. Therefore, bank should try to develop

affinity with its customer that may result in customer loyalty.

Bank should deploy talented, skilled employee with has extremely well and fluent speaking and communication skill in

English and Hindi both. Further, enhance the capability and skill of concerning employee/s by proper and adequate

training programs.

Customer grievances require cordial attention of bank because handling customer issues grievance and problems

properly is something that creates long-term relationship, confidence and consistency amongst customers. Thus,

handling customer grievances by bank staff should be high on cards for ICICI bank.

Customer wants simplification in process and procedure of banking process. Complicated and lengthy procedure can be

result in trouble for customers and they might feel dissatisfied by the cumbersome criteria of loan sanctioning.

Therefore, banks should try to implement easy, understandable and less complicated procedure for providing loan to

customers.

In future, if the bank incorporates the measures necessary for increasing the positive perception and takes steps to

reduce the negative perception it would move at a much higher pace towards growth, expansion, development at a faster

pace helping present as well as prospective customers more efficiently and effectively.

REFERENCES

1. Retrieved from http://online.wsj.com/article/SB10001424127887323699704578326894146325274.html

2. Retrieved from http://www.cnbc.com/id/100627815

3. Bisht, H. (2005). Innovations in Banks, Indian Banks: Investing Innovatively in Technology. The ICFAI University

Press.

4. Retrieved from http://businesstoday.intoday.in/story/best-banks-2012-future-of-branch-banking-in-india/1/189927.html

5. Retrieved from http://ezinearticles.com/?Role-of-Information-Technology-in-Growth-of- Business&id=344198

6. Retrieved from http://online.wsj.com/article/SB10001424127887324504704578410550229440438.html

7. Retrieved from http://www.bain.com/publications/articles/future-of-the-bank-branch-in-asia-redesigning-footprint-and-

format.aspx

8. Mark Schofield and Seow-Chien Chew, „Future of the bank branch in Asia: Redesigning footprint and format‟, March

18, 2013.

9. Marous, Jim. (2012, October). The Digital Challenge to Retail Banks. Bain & Company. Retrieved from

http://www.bain.com/publications/articles/digital-challenge-to-retail-banks.aspx

10. Mehra, D. (2007). Commercial Banking Today. Agra: Arvind Vivek Prakashan Publishers.

11. Pradhan, P. K. (2007-08). Retail Banking: Retail Market of Banking Services. The Utkal Business Review, XX, 148-

162.

12. Prasad S. D., & Lavanya, K. S. L. (2005). Innovations in Banks, Technology Management in Banks. The ICFAI

University Press

13. Veenstra, & Auke Douwe. (2012, October 09). Is There A Future For Bank Branches?. Reterieved from

http://blogs.forrester.com/blog/39066

14. The bank branch of the future. Retrieved from www.microsoft.com/financialservices,

*****