Embed Size (px)

Citation preview

Reserving for Periodical Payments under the

Courts Act

Anthony Carus

© Carus Consulting Actuaries Ltd. 2005 2

Governing Principles

• FSA’s Prudential Sourcebook (PRU)– http://fsahandbook.info/FSA/handbook.jsp?doc=/handbook/PRU

• International Accounting Standards Board: IFRS 4

• Institute /Faculty Guidance Notes– http://www.actuaries.org.uk/files/pdf/map/Contents.pdf

• Company philosophy and practice

© Carus Consulting Actuaries Ltd. 2005 3

PRU

• PRU 1.2.26 R – A firm must carry out regular assessments of

the adequacy of its financial resources using processes and systems which comply with PRU 1.2.27 R.

• PRU 1.2.27 R – The processes and systems required by PRU

1.2.26 R must be proportionate to the nature, scale and complexity of the firm's activities.

© Carus Consulting Actuaries Ltd. 2005 4

PRU – cont.

• PRU 1.2.31 R – The processes and systems required by PRU 1.2.26R

must enable the firm to identify the major sources of risk to its ability to meet its liabilities as they fall due, including the major sources of risk in each of the following categories:

– (1) credit risk; – (2) market risk; – (3) liquidity risk; – (4) operational risk; and – (5) insurance risk.

© Carus Consulting Actuaries Ltd. 2005 5

PRU – cont.

• PRU 1.2.35 R – For each of the major sources of risk identified in

accordance with PRU 1.2.31 R, the firm must carry out stress tests and scenario analyses that are appropriate to the nature of those major sources of risk, as part of which the firm must:

– (1) take reasonable steps to identify an appropriate range of realistic adverse circumstances and events in which the risk identified crystallises; and

– (2) estimate the financial resources the firm would need in each of the circumstances and events considered in order to be able to meet its liabilities as they fall due.

© Carus Consulting Actuaries Ltd. 2005 6

Example

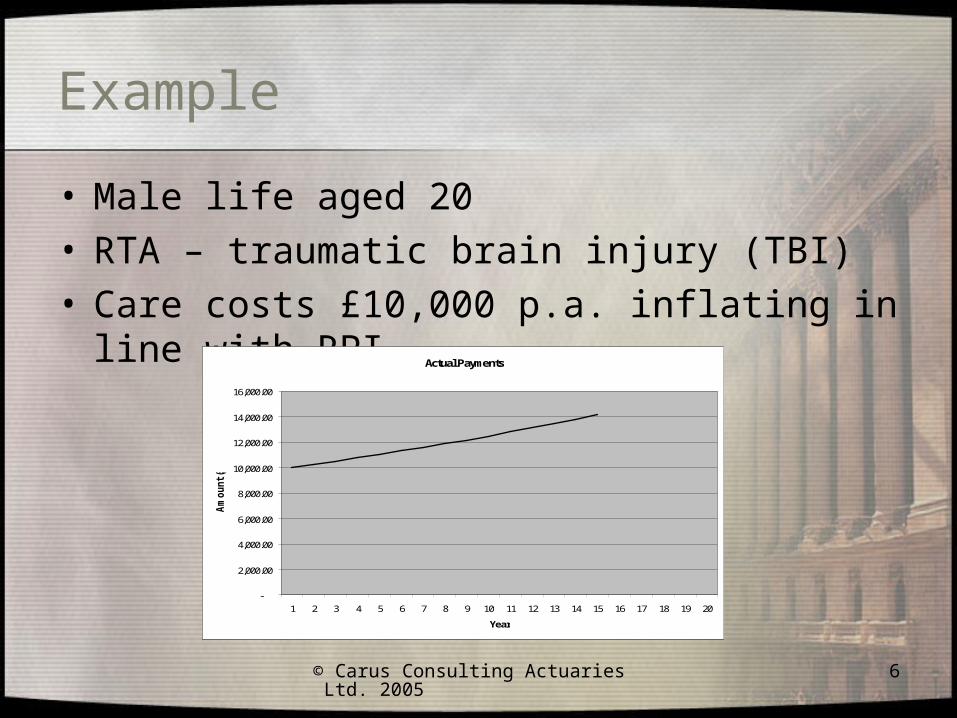

• Male life aged 20• RTA – traumatic brain injury (TBI)• Care costs £10,000 p.a. inflating in line with RPI

Actual Payments

-

2,000.00

4,000.00

6,000.00

8,000.00

10,000.00

12,000.00

14,000.00

16,000.00

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Year

Am

ount (£

)

© Carus Consulting Actuaries Ltd. 2005 7

Mortality

• General Population

• By age

• Male / Female

• Pension policyholder / no policy

• Annuity policyholder / no policy

• Traumatic Brain Injury / well

© Carus Consulting Actuaries Ltd. 2005 8

Population

• Ogden Tables• Projected or not?• Projected

– 2002-based– Calculated as at 2005– England and Wales

• Source data: http://www.gad.gov.uk/Population/2002/engwal/wew02mort.xls

• Manipulation required

© Carus Consulting Actuaries Ltd. 2005 9

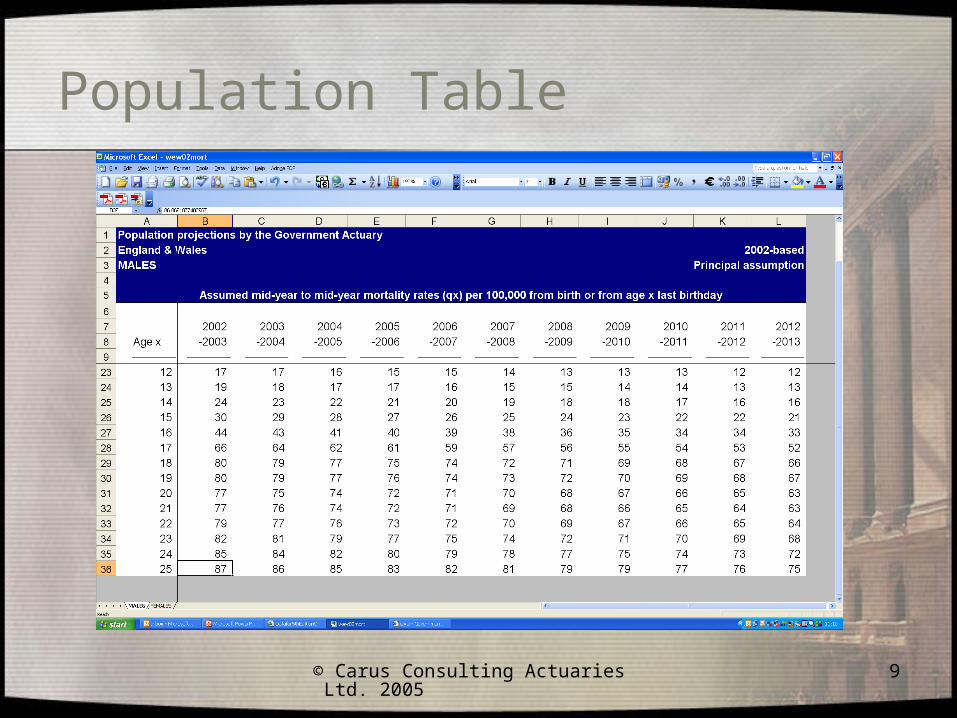

Population Table

© Carus Consulting Actuaries Ltd. 2005 10

Annuity / Pensioner

• Which?• ’92 Series• Adjusted• Continuous Mortality Investigation

Working Paper 1– http://www.actuaries.org.uk/Display_Page.cgi?url=/cmi/cmi_workingpapers.html

• New ’00 Series• Say:

– IMA92 Select– Base projected as CMIR 17– Scaled at younger ages tapering to no scaling at older ages

© Carus Consulting Actuaries Ltd. 2005 11

Discount Rate

• Is discounting permitted?• Close matching

– PRU 4.2.57 to 4.2.61

• Only applicable to long-term business funds– Arising through the definition of “index-linked

liabilities”

• But how much risk do you want to assume?

© Carus Consulting Actuaries Ltd. 2005 12

Investment

• ILGS– Limited spread of maturity dates– Longest currently 2035– Speculation surrounding the issue of an ultra-

long (50 year) ILGS in 3rd quarter 2005

• Derivatives– Inflation swap

• Something else?

© Carus Consulting Actuaries Ltd. 2005 13

If ILGS

• Discount rate set according to returns available

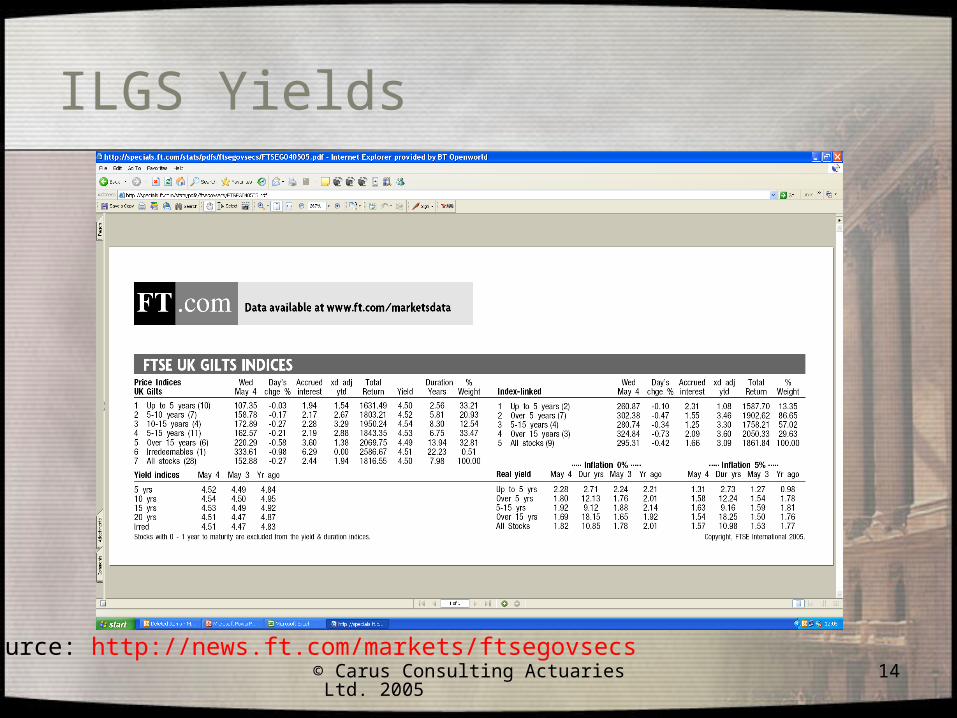

© Carus Consulting Actuaries Ltd. 2005 14Source: http://news.ft.com/markets/ftsegovsecs

ILGS Yields

© Carus Consulting Actuaries Ltd. 2005 15

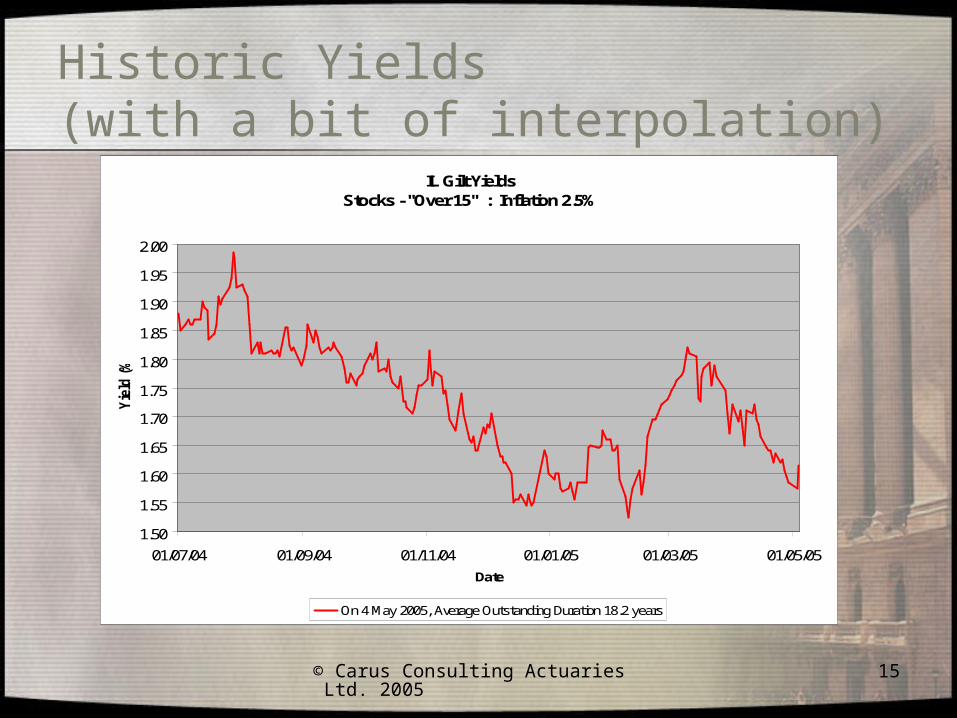

Historic Yields (with a bit of interpolation)

IL Gilt YieldsStocks - "Over 15" : Inflation 2.5%

1.50

1.55

1.60

1.65

1.70

1.75

1.80

1.85

1.90

1.95

2.00

01/07/04 01/09/04 01/11/04 01/01/05 01/03/05 01/05/05

Date

Yie

ld (%

)

On 4 May 2005, Average Outstanding Duration 18.2 years

© Carus Consulting Actuaries Ltd. 2005 16

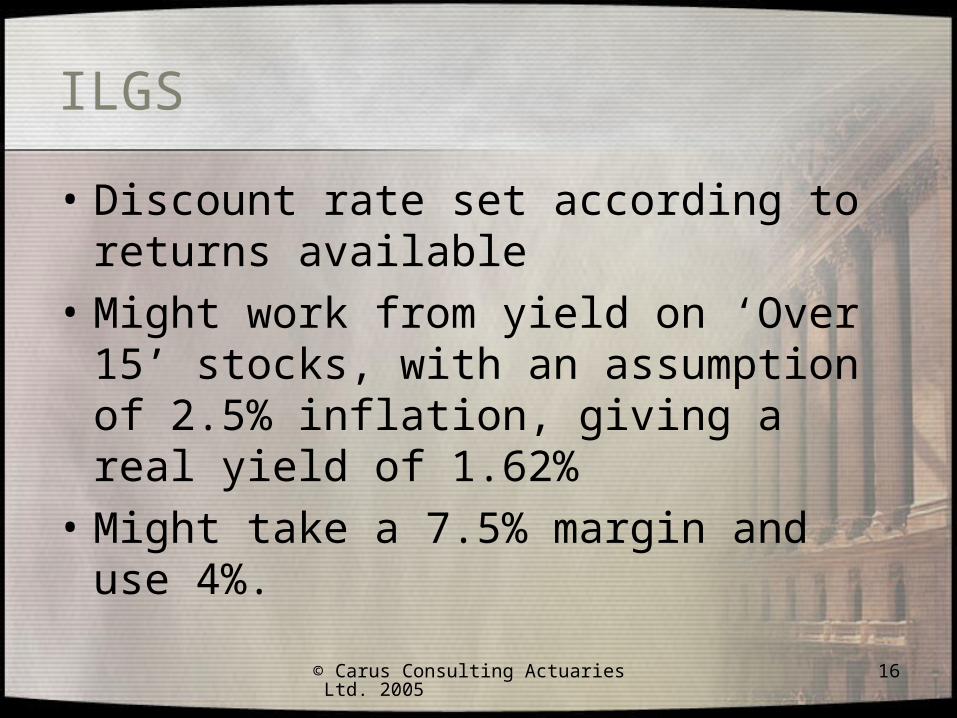

ILGS

• Discount rate set according to returns available

• Might work from yield on ‘Over 15’ stocks, with an assumption of 2.5% inflation, giving a real yield of 1.62%

• Might take a 7.5% margin and use 4%.

© Carus Consulting Actuaries Ltd. 2005 17

Other bases

• Expenses– £75 p.a. ?

• Tax– Gross ?

© Carus Consulting Actuaries Ltd. 2005 18

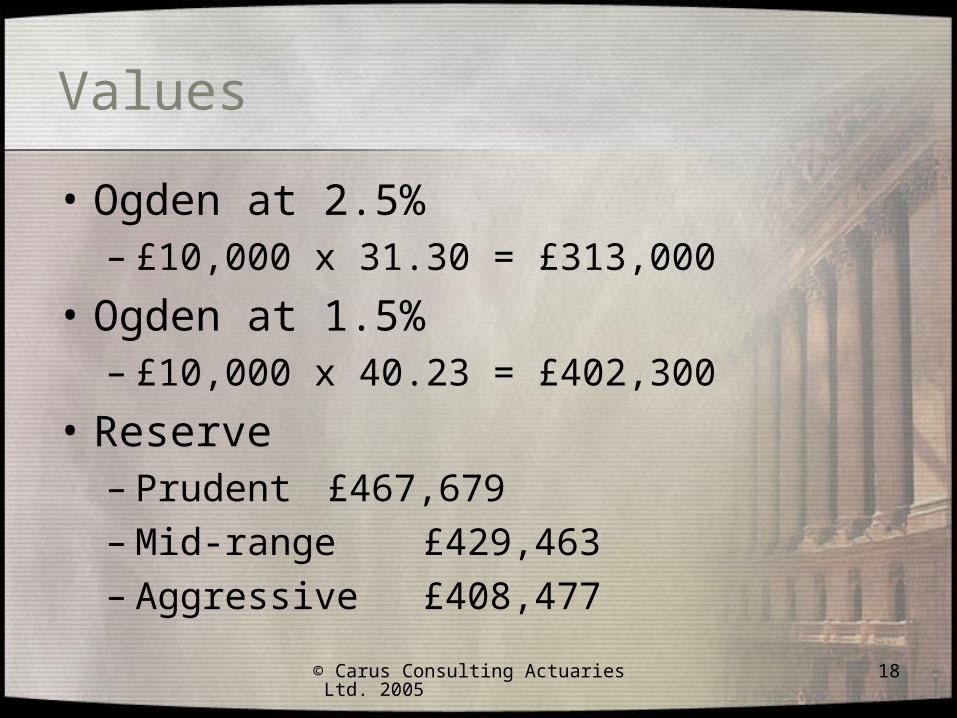

Values

• Ogden at 2.5%– £10,000 x 31.30 = £313,000

• Ogden at 1.5% – £10,000 x 40.23 = £402,300

• Reserve– Prudent £467,679– Mid-range £429,463– Aggressive £408,477

© Carus Consulting Actuaries Ltd. 2005 19

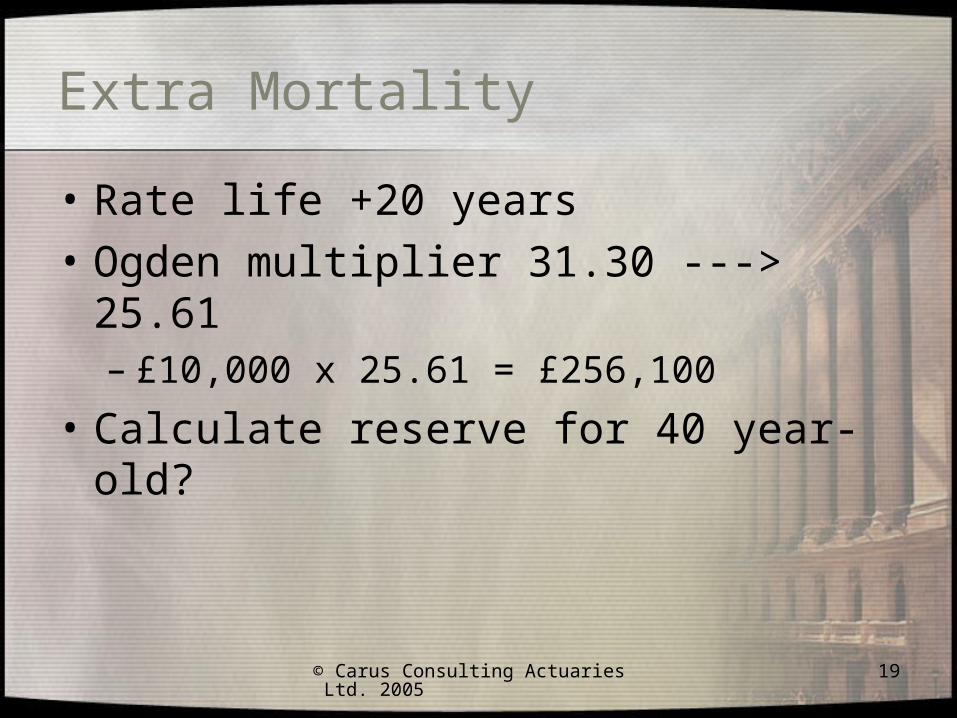

Extra Mortality

• Rate life +20 years

• Ogden multiplier 31.30 ---> 25.61– £10,000 x 25.61 = £256,100

• Calculate reserve for 40 year-old?

© Carus Consulting Actuaries Ltd. 2005 20

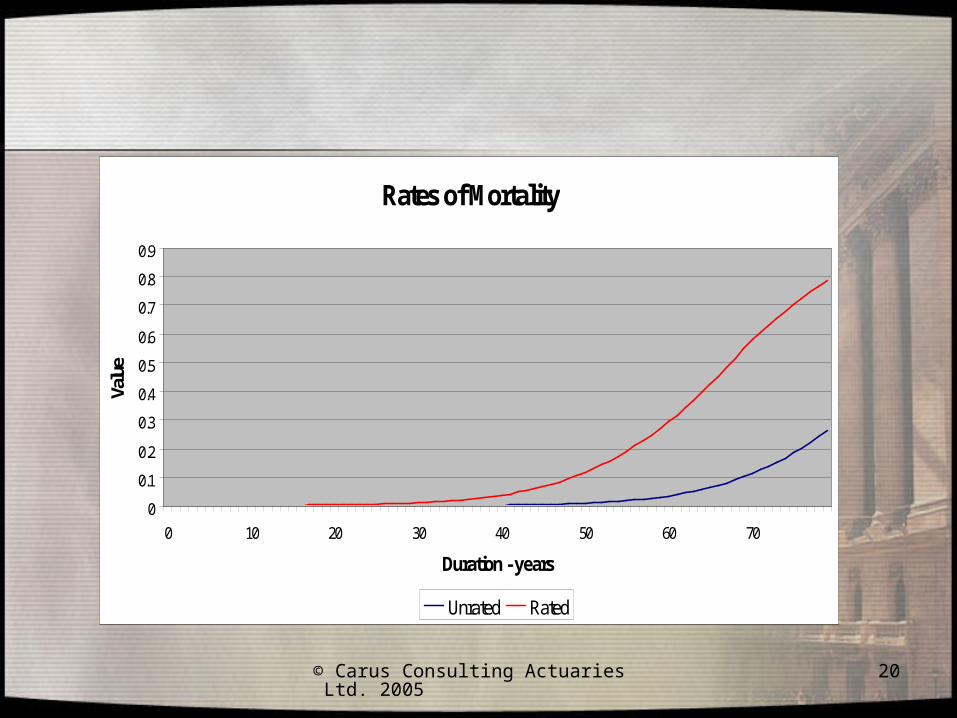

Rates of Mortality

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0 10 20 30 40 50 60 70

Duration - years

Valu

e

Unrated Rated

© Carus Consulting Actuaries Ltd. 2005 21

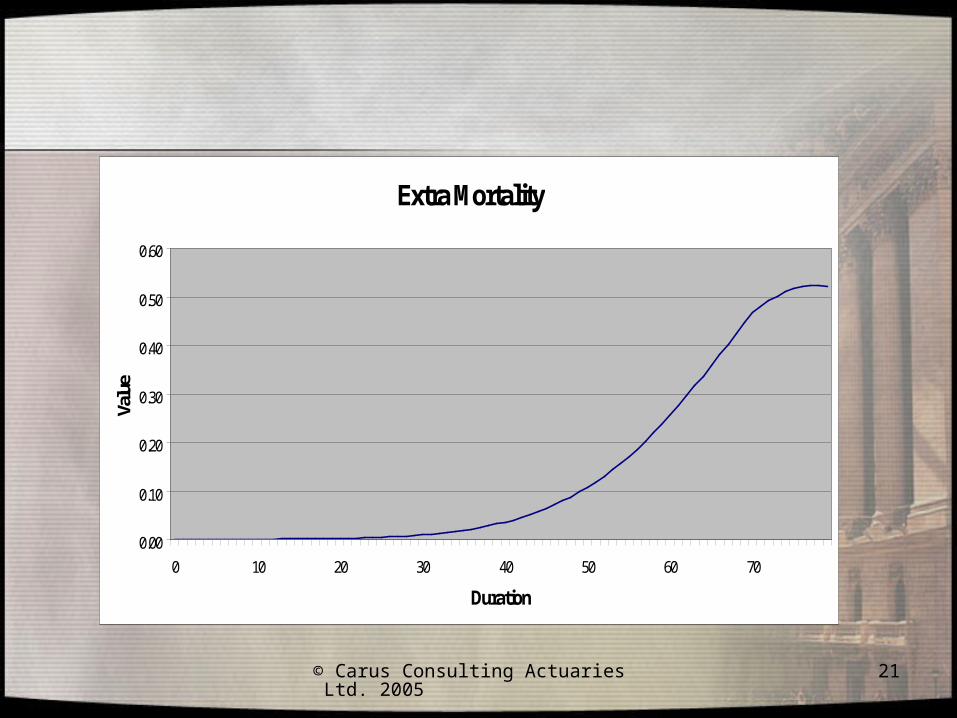

Extra Mortality

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0 10 20 30 40 50 60 70

Duration

Valu

e

© Carus Consulting Actuaries Ltd. 2005 22

Extra Mortality

• Maybe rate life +20 years• Ogden multiplier 31.30 ---> 25.61

– £10,000 x 25.61 = £256,100

• Calculate reserve for 40 year-old?• Calculate the current extra rate of mortality and

let that – or a proportion – continue as the extra mortality throughout

• In the example; current extra (ultimate) mortality is 0.000222

• I would take 50% / 75% / 90% of this

© Carus Consulting Actuaries Ltd. 2005 23

Values

• Ogden at 2.5%– £10,000 x 25.61 = £256,100

• Ogden at 1.5% – £10,000 x 30.95 = £309,500

• Reserve– Prudent £466,133– Mid-range £427,434– Aggressive £406,224

© Carus Consulting Actuaries Ltd. 2005 24

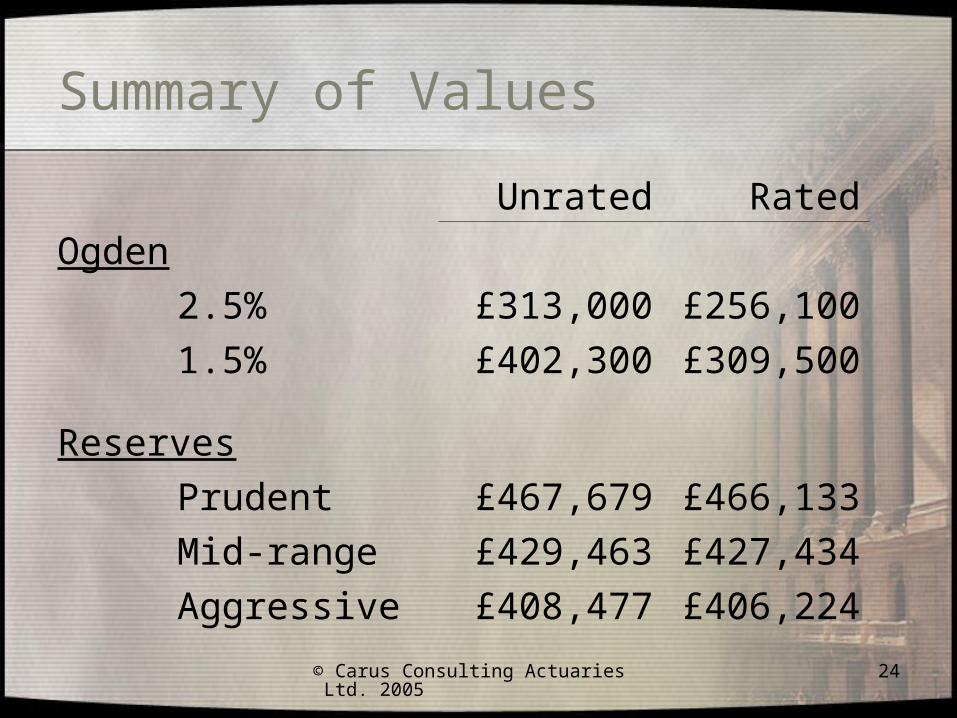

Summary of Values

Unrated Rated

Ogden

2.5% £313,000 £256,100

1.5% £402,300 £309,500

Reserves

Prudent £467,679 £466,133

Mid-range £429,463 £427,434

Aggressive £408,477 £406,224

© Carus Consulting Actuaries Ltd. 2005 25

Other Issues

• Variation Order

• Reinsurance

© Carus Consulting Actuaries Ltd. 2005 26

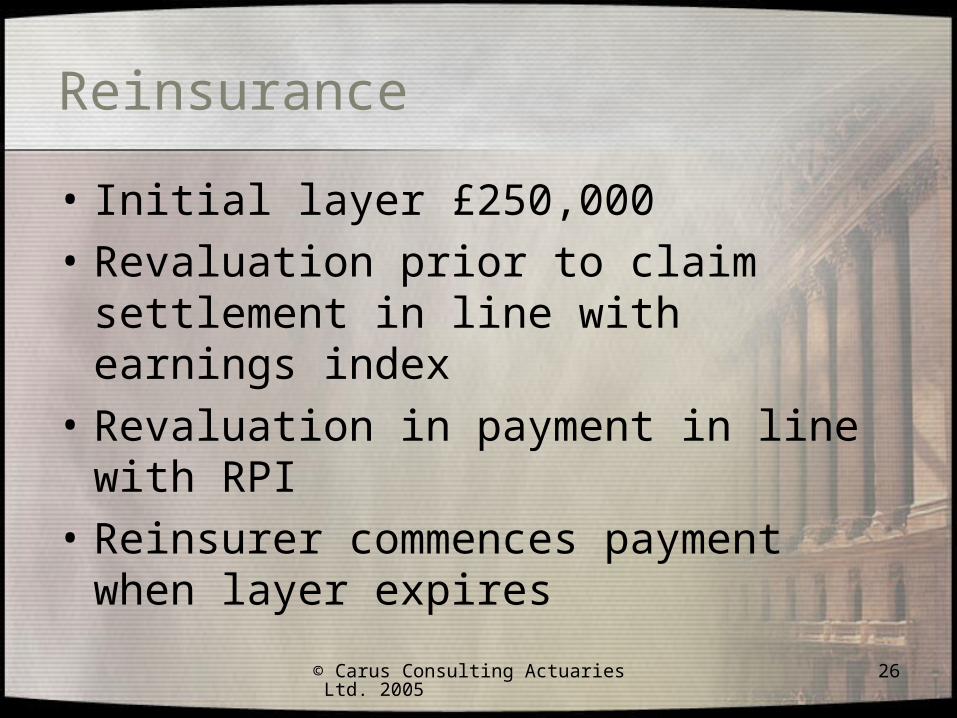

Reinsurance

• Initial layer £250,000

• Revaluation prior to claim settlement in line with earnings index

• Revaluation in payment in line with RPI

• Reinsurer commences payment when layer expires

© Carus Consulting Actuaries Ltd. 2005 27

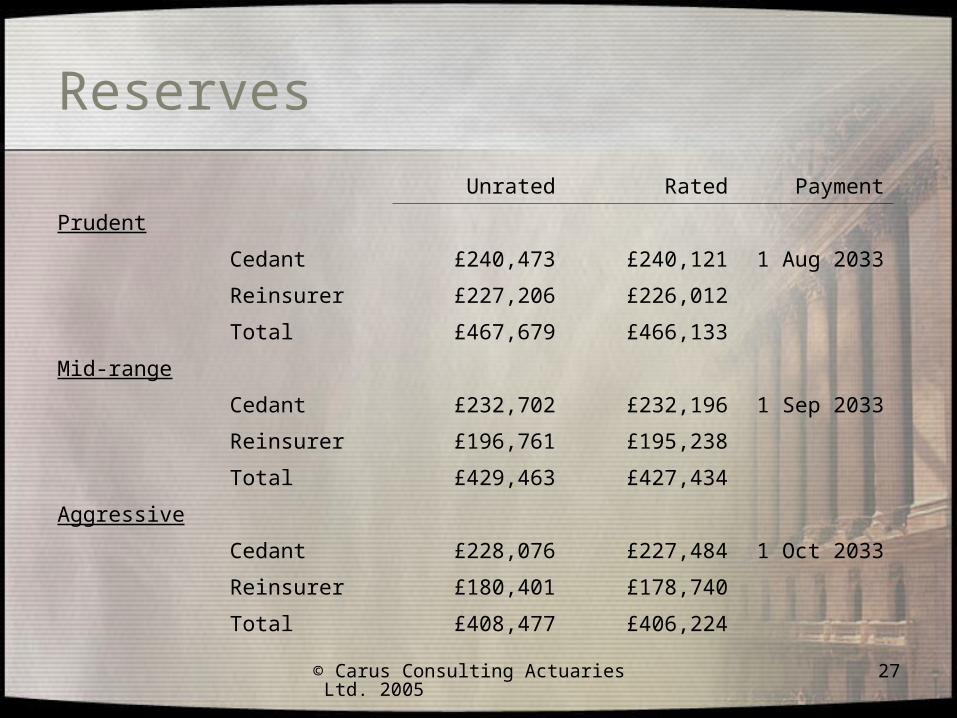

Reserves

Unrated Rated Payment

Prudent

Cedant £240,473 £240,121 1 Aug 2033

Reinsurer £227,206 £226,012

Total £467,679 £466,133

Mid-range

Cedant £232,702 £232,196 1 Sep 2033

Reinsurer £196,761 £195,238

Total £429,463 £427,434

Aggressive

Cedant £228,076 £227,484 1 Oct 2033

Reinsurer £180,401 £178,740

Total £408,477 £406,224

© Carus Consulting Actuaries Ltd. 2005 28

IFRS 4

• Is this an insurance contract?– “A contract under which one party (the insurer)

accepts significant insurance risk from another party (the policyholder) by agreeing to compensate the policyholder if a specified uncertain future event (the insured event) adversely affects the policyholder.”

• Some insurance contracts cover events that have already occurred, but whose financial effect is still uncertain… In such contracts, the insured event is the discovery of the ultimate cost of those claims. APPENDIX B4

© Carus Consulting Actuaries Ltd. 2005 29

IFRS 4

• Is there an embedded derivative that must be identified and measured at fair value?– Is the embedded derivative itself an insurance

contract?

• See Implementation Guidance Example 2.16 …– Contractual feature that provides a return

contractually linked (with no discretion) to the return on specified assets

– Treatment: the embedded derivative is not an insurance contract and is not closely related to the contract. Fair value measurement is required.See also para. AG30(h) of IAS 39

© Carus Consulting Actuaries Ltd. 2005 30

Contact Details

Carus Consulting ActuariesPound House23 Shottery VillageStratford-upon-AvonWarwickshire CV37 9HD

T: 01789 290066F: 01789 290077E: [email protected]: www.carus-actuaries.co.uk

![[I. N. Herstein] Noncommutative Rings (Carus Mathe(Bookos.org)](https://img.pdfslide.us/doc/110x75/546040b2b1af9ff5588b5257/i-n-herstein-noncommutative-rings-carus-mathebookosorg.jpg)