Embed Size (px)

Citation preview

RMIT University

Econometric Modelling and the Effectiveness of Hedging

Exposure to Foreign Exchange Risk

This paper aims to test the efficiencies of four econometric models at determining an optimal hedge ratio. We will specifically be demonstrating the abilities of each model to outperform each other. The econometric models that we will test include: the (i) Conventional Model (levels), the (ii) Conventional Model (first difference), the (iii) Quadratic Model, and the (iv) Error Correction Model. These four models will be applied to both a money market hedge and a cross currency hedge using the base currency of the Australian Dollar (AUD), an exposure currency of the Canadian Dollar (CAD), and a third currency of the Swiss Franc (CHF). The results will show, that though there is merit in financial hedging; the effectiveness of the hedge is not dependent upon the econometric model chosen.

ii

Disclaimer: All remaining errors and omissions are entirely those of the author.

iii

Table of Contents

1. INTRODUCTION ....................................................................................................................... 1

1. LITERATURE REVIEW ............................................................................................................. 2

1.1 Hedging Techniques ............................................................................................................ 2

1.2 Hedge Ratios ......................................................................................................................... 3

1.3 Econometric Techniques ...................................................................................................... 3

1.4 Measure of Effectiveness and Variance Ratio (VR)/ Variance Reduction (VD) ............. 5

3. METHODOLOGY ....................................................................................................................... 5

3.1 Identification of Currencies and Variable .................................................................................. 6

3.2 Estimating the Money Market Hedge Ratio ............................................................................. 6

3.2.1 Conventional Model (Levels) ............................................................................................... 6

3.2.2 Conventional Model (First Differences).............................................................................. 6

3.2.3 Quadratic Model ................................................................................................................... 6

3.2.4 Error Correction Model ........................................................................................................ 7

3.3 Estimating the Cross Currency Hedge Ratio ............................................................................ 7

3.3.1 Conventional Model (Levels) ............................................................................................... 7

3.3.2 Conventional Model (First Differences).............................................................................. 7

3.3.3 Quadratic Model ................................................................................................................... 7

3.3.4 Error Correction Model ........................................................................................................ 7

3.4 Estimating VR and VD ......................................................................................................... 7

4. DATA AND EMPIRICAL RESULTS ......................................................................................... 8

4.1 Money Market Hedge Results .................................................................................................... 8

4.2 Cross Currency Hedge Results ................................................................................................... 9

4.3 Data and Statistical Outputs ..................................................................................................... 10

5. CONCLUSION ........................................................................................................................... 12

REFERENCES ................................................................................................................................... 14

APPENDICES .................................................................................................................................... 16

Appendix 1: EViews for Money Market Hedge ............................................................................ 16

Appendix 2: EViews Output for Cross Currency Hedge .............................................................. 17

1

1. INTRODUCTION

The objective of this project is to find out if the econometric modelling of the hedge ratio makes

any difference for the effectiveness of money market and cross currency hedging of exposure to

foreign exchange risk.

A major question in finance is the effectiveness of the econometric models being used. It seems

financial types of many kinds put blind faith in the outputs of econometric models, but is this

faith justified? The amount of risk a portfolio manager or CFO is willing to take on is more

often than not based on these models. With the sheer amount of money being wagered by these

money managers, it is essential that these models represent what they promise to.

It was Meese & Rogoff (1983) who showed us that the random walk model often perform better

than any forecast will, but still econometricians believe in their models. In finance and

particularly in the academics it is believed without second thought that a normal distribution is

present, and that the variables follow a random walk. That is to say they are completely random,

and therefore quite impossible to forecast. Still, these econometric models promise to do exactly

this. An entire position and its hedge may very well be based on an econometric model.

The fact that Mark & Choi (1997)and Chinn & Meese (1995) refuted the fact, especially when

forecasts where on a long horizon; provides econometricians with the belief that they can

improve upon the random walk model.

The objective of this study is to test the efficiency of the econometric models when compared

with one another. We will test the (i) Conventional Model (Levels), (ii) Conventional Model

(First Difference), (iii) Quadratic Model, and (iv) Error Correction Model. These models will use

variables derived from the exchange rates between the Canadian Dollar, the Australian Dollar,

and the Swiss Franc. This work is original as the question of effectiveness of hedge ratio

effectiveness based on econometric model has never been approached with these currencies. It

would be recommended that a continuation of the empirical work is undertaken to develop

conclusive answers.

The findings in this study are that none of the econometric models perform better than another.

It is apparent that hedging and using a hedge ratio is advisable, but selection between which

econometric models to use is too little benefit.

This journal will read in the following manner in chapter 1, the introduction, I will introduce the

topic and brief the reader. In chapter 2, I will conduct a literature review and offer an in depth

look into the research available on the topic. Chapter 3 is a discussion on the methodology of the

2

paper and in chapter 4 I will discuss these findings. My conclusions and findings will be

summarised in chapter 5.

1. LITERATURE REVIEW

There are countless studies on the topics discussed, therefore they have been broken up into

distinct sections. This way we can focus on the importance of each to this study, and in the end

see how they are all related. The sections will be as follows: Hedging Techniques, Hedge Ratios,

Econometric Techniques, and measures of effectiveness; specifically Variance Ratio and

Variance Reduction.

1.1 Hedging Techniques

Financial hedging is an important tool in any money management position or position in which

one is taking on risk. There are two types of hedging; both operational and financial.

Operational hedging deals with reducing any exposure to foreign exchange risks, while financial

hedging is the act of taking an opposite position in a holding, to offset the risk that the holdings

move in an unexpected direction. Carter, Pantzalis & Simkins (2003) found that the combined

use of operational and financial hedges is associated with decreased exchange rate exposure. But

the two are complementary of each other, rather than dependent on each other. With operational

hedging having more of a long term focus and financial the short term (Kim, Mathur & Nam

2006). In this study we will be focusing on financial hedging techniques. Yao & Wu (2012),

explain that through financial hedging we can ultimately avoid and resolve the systemic risks that

the position of the original holdings undergo.

In this paper we will be focusing on two types of financial hedging: the money market hedge and

the cross-currency hedge.

In our study the three currencies (AUD, CAD, CHF) were assigned to x, y, and z. These

represented the base currency, exposed currency, and the currency in which would we would

attempt to create a cross rate hedge. Therefore an unhedged position would simply be the

exchange rate between the two, or (x/y). By remaining unhedged any fluctuation in this exchange

rate puts the holder at risk. We also used the interest rates from both our x and y currency, let ix

and iy represent these.

The money market hedge aims to achieve a synthetic forward situation, where the contract rate

would be equal to the interest parity rate (Benet 1992). By borrowing in our base currency and

lending in another we can achieve a money market hedge.

3

To do a cross currency hedge one must take a position on another currency whose exchange rate

against the base currency is correlated with the exchange rate between the base currency and the

exposure currency (Moosa 2011). This is represented by (x/z). Typically these hedges will

involve some form of a futures contract as a hedging tool. Therefore when the spot position and

the futures contract are in the same asset, we can theoretically eliminate a lot of the risk. When

the futures contract and the spot position are in the same asset a high proportion of the risk of

the spot position can be eliminated.

1.2 Hedge Ratios

When trying to create an effective hedge it is common practice that one develops a hedge ratio

(HR). This hedge ratio explains how much of the offsetting position it will require to effectively

hedge the original position. A naïve model assumes that a hedge ratio is equal to one, and it is

considered best practice to start with this assumption. When a hedge ratio is equal to one, the

entire position is hedged. As opposed to either the random walk model or implied model; we use

the naïve model, or a hedge ratio of one (Moosa 2011).

The estimation of the HR is crucial for a successful hedge, but the methods to do so are not

agreed upon. The HR can be explained as the ratio between the total value of one holding

versus’ the total value of the opposite positon (Yao & Wu 2012). Therefore it is essential that

the optimal hedge ratio is estimated, otherwise the risk may not be reduced by the hedge.

Without an optimal hedge ratio we are liable to be over or under hedged, with the potential for

worse losses than an unhedged position.

We measure the optimal hedge ratio through the slope coefficient of the rate of return on the

unhedged position against the rate of return of the hedging tool. The optimal hedge ratio

estimated by OLS will be identical to the hedge ratio estimated from conditional moments.

1.3 Econometric Techniques

A crucial decision made by traders is at what ratio they hedge their spot position at. This is the

problem of choosing an optimal hedge ratio. When trading commodities it a frequently

recommended solution is to set the hedge ratio equal to the ratio of the covariance between spot

and futures prices to the variance of the futures price (Benninga, Eldor & Zilcha 1984). The

estimation of the optimal hedge ratio has undergone a great deal of study in academia. Using the

ideas drawn from portfolio optimization the modern portfolio hedging theory suggested using

the OLS model and a minimum risk profile. Howard & D’Antonio (1984) presented the optimal

Sharpe hedge ratio under the condition of the maximization of the utility function. Junkus & Lee

4

(1985) empirically analysed four kinds of the hedging strategies in light of the maximizing profits,

eliminating risk, minimizing risk as well as maximizing utility(Yao & Wu 2012).

As financial econometricians strive to create a more sophisticated model to estimate hedge ratio,

we are left to use the tools currently available to us. In our study we used the conventional model

or OLS. Citing Myers & Thompson (1989) and note that the use of conventional OLS

estimation implies the use of unconditional sample moments to estimate the optimal hedge ratio

rather than their conditional alternatives.

The OLS does have its downfalls and these come into the fact it may not consider time varying

distributions, serial correlation, heteroskedasticity and cointegration (Poterba & Summers 1987).

We also used the conventional first difference model, also called the simple model and the

historical model. This model amounts to estimating the hedge ratio from historical data by

employing a linear OLS regression at the first difference. When doing this the h is the hedge

ratio and the R2 of the regression measures its effectiveness. Therefore the coefficient is

measuring the speed that deviations from long run values are effectively eliminated. Lien (2004)

argues that the estimation of the hedge ratio and hedging effectiveness may change significantly

when the possibility of cointegration between prices is ignored.

Error correction models have also been suggested, nonlinearity in this case is achieved by

including a polynomial in the error term. Hendry & Ericsson (1991) estimated that a polynomial

to the third degree would be adequate in capturing this adjustment process. The main purpose of

error-correction models is to capture the time series properties of variables, through the complex

lag structures allowed, whilst at the same time incorporating an economic theory of the

equilibrium type (Granger & Weiss 1983). (Lien 2004) provides a theoretical analysis of this

proposition, and ends by saying that a hedger who neglects the cointegrating relationship will not

be taking a big enough offsetting position in the hedge. The empirical results that are resultant of

an error correction model are typically not significantly different from those using either a first

difference or levels model (Moosa 2003).

However, this method has suffered various criticisms. It was shown by Poterba and Summers

(1986) that stocks returns typically exhibit time-varying conditional heteroskedasticity and

because of this the assumption that covariance matrix remains constant. To improve upon past

hedge ratio estimations it may worth considering time variance of second moments (Casillo

2004). It is for this reason that recent studies have suggested attempting to use the GARCH

method for hedge ratio estimation (Hatemi-J & Roca 2006). The GARCH method allows the

conditional variances and covariances used as inputs to the hedge ratio to be time-varying.

5

Though there are more complex and time consuming methods, many authors have mentioned

that the more advanced techniques have the potential to exhibit a better performance, they do

not come without some downfalls. Some of these methods can be very problematic to estimate

and can potentially create even more costs (Lien 2004). When it comes down to it, the simple

methods like OLS can achieve results that are just as good (Myers & Thompson 1989).

1.4 Measure of Effectiveness and Variance Ratio (VR)/ Variance Reduction (VD)

When we have a perfect correlation between the prices of the hedged exchange rate and that of

the hedging instrument we achieve a hedge ratio of 1. Therefore a lot of the hedging

effectiveness is related to the correlation between the prices.

The effectiveness of the hedge ratios to foreign exchange risk can be measured by using the

variance ratio (VR) and variance reduction (VD) measures. By testing the equality of the variance

of the rates of return on both the hedged and unhedged position we can measure the VR and

VD (Moosa 2011).

The variance ratio test can be conducted to compare the effectiveness of two hedging positions

resulting from the use of different hedge ratios or different hedging instruments. If the prices of

the two currencies are not perfectly correlated than we should see that the hedge ratio will not be

equal to one. Because of this we can measure the effectiveness of the hedge by the correlation

we see between the prices. Therefore the smaller the variance the more effective the hedge is. It

must also be put through a formal test and the equality between the two must be put to a test.

The effectiveness of the hedge is therefore measured by the variance of the rate of return on the

hedged position compared with the variance of the rate of return on the unhedged position. As

the variance got smaller we would know that the hedge is becoming more effective. The VD on

the helps explain the reduction in variance when using a hedge.

Another method when using any of the models is the coefficient of determination or R2 to help

to determine the effectiveness. If the R2 was equal to one, then we could hope for a perfect

hedge. This could only happen if the prices were deemed to be perfectly correlated; in either a

positive or negative direction. Therefore if the coefficient of determination (R2) is equal to one

than we have achieved a perfect hedge.

3. METHODOLOGY

As the methods to measure the predictive accuracy of econometric modelling and their

effectiveness on hedge ratios involve the estimation and testing of the four models using EViews

6

8 and Microsoft Excel 2013, this chapter is best divided into subsections identifying each stage

of testing and or estimation procedure.

In this chapter the “variables‟, which are often referred to, are those which have been derived

from the manipulation of the original data set sourced from Bloomberg. These variables include

the exchange rates of the countries and their respective interest rates.

3.1 Identification of Currencies and Variable

As mentioned before, in our study the three currencies (AUD, CAD, CHF) were assigned to x, y,

and z. Each currency represented the base currency, exposed currency, and the currency in

which would we would attempt to create a cross rate hedge. The exchange rate between the two

(AUD/CAD) is represented by x/y. By remaining unhedged any fluctuation in this exchange rate

puts the holder at risk. Other variables used included the interest rates of Australia and Canada;

represented as ix and iy respectively.

3.2 Estimating the Money Market Hedge Ratio

To estimate the money market hedge ratio between x and y we used the following formula:

y

x

i

iyxSyxF

1

1)/(),( [1]

This estimation is representative of the interest parity forward rate between the two.

3.2.1 Conventional Model (Levels)

The conventional model used the following formula:

ttt fhs [2]

In equation 2 the variables are equal to fyxF ))/(log( and syxS ))/(log( .

3.2.2 Conventional Model (First Differences)

The first difference estimates with a lag of one, the formula is as follows:

ttt fhs [3]

3.2.3 Quadratic Model

The Quadratic Model equation is equal to:

tttt ffhs 2 [4]

7

3.2.4 Error Correction Model

The Error Correction Model (ECM) is as follows:

tttttt ffhss 111 [5]

3.3 Estimating the Cross Currency Hedge Ratio

Again in the cross currency hedge ratio we will use an unhedged position and a hedging tool which

will be equal to (x/y) and function of (x/z) where 1))/(log( syxS and 2))/(log( szxS ,

respectively. We will use the following models once again to estimate the hedge ratios.

3.3.1 Conventional Model (Levels)

The conventional model uses the following formula:

ttt hss 21 [6]

3.3.2 Conventional Model (First Differences)

The first differences model uses the following formula:

ttt shs 21 [7]

3.3.3 Quadratic Model

The quadratic model used the following formula:

tttt shss 2

221 [8]

3.3.4 Error Correction Model

The ECM used the following formula:

tttttt sshss 11,221,11 [9]

3.4 Estimating VR and VD

Calculating the VR and VD for the estimated hedge ratios is the next step, and our attempt to

measure the estimations successes. The variance ratio is equal to the ratio of the variance of the

return of the unhedged position to the variance of the rate of return on hedged position. To

calculate VR we will use one of the following equations:

)(

)(2

2

fhs

sVR

[10]

Or:

8

)(

)(

21

2

1

2

shs

sVR

[11]

In this calculation )()( 1

22 ss is equal to the variance of the rate of return on the

unhedged positon and ( )(2 fhs or )( 21

2 shs ) is equal to the variance of the rate of

return on the hedged position. When calculating VR, we can then decide if it is and effective

hedge by using this equation:

)1,1( nnFVR [12]

VD is simply calculated as:

VRVD

11 [13]

4. DATA AND EMPIRICAL RESULTS

In this study we estimated the hedge ratio from four different econometric models across two

different hedging techniques. The intention of the study was to discover whether the model used

makes any difference for the effectiveness of the hedge. The objective is to find out whether the

estimation method or model specification makes any difference for hedging effectiveness. The

two hedging techniques used will be the money market hedging and cross currency hedging.

Many studies have attempted a similar study, but with different econometric models such as

(Longo et al. 2007).

Figure 1 plots the rates of return for the unhedged position against the hedged positions for the

money market hedge. In Figure 2 we can see the results of the unhedged position versus that of

the hedged position in the cross currency hedge. Table 1 shows the estimations results from the

EViews outputs. From these outputs we can see the hedge ratio, the t-statistic, and the R2 or

coefficient of determination. In Table 2 are the variance ratio and variance reduction as well as

the variance of the unhedged position.

4.1 Money Market Hedge Results

Figure 1 looks at the rates of return of the unhedged versus the hedged rates of return; against

each econometric model for the purpose of a money market hedge. As we can see, regardless of

which method is used we see a success with the hedge. As the variance of the hedge approaches

zero, we are getting closer to a perfect hedge. In Table 2, we also see the variance ratio is

statistically significant in every case.

9

Figure 1: Variance of Rates of Return on the Unhedged and Hedged Positions (Money

Market Hedging)

Levels First Difference

Quadratic Error Correction

4.2 Cross Currency Hedge Results

We now assess the success of the cross currency hedge. Though the variance is much higher

than what we saw with the money market hedge, we still achieved a lower variance ratio than the

unhedged position achieved. But between econometric models the success was consistent

between them. Consider now cross currency hedging. The difference between the results

achieved under money market hedging and cross currency hedging is correlation (Moosa 2011).

-8

-6

-4

-2

0

2

4

6

8

10

12

Unhedged Vs. First Difference

Unhedged Conventional (First)

-10

-5

0

5

10

15

Unhedged Vs. Conventional

Unhedged Coventional

-8

-6

-4

-2

0

2

4

6

8

10

12

Unhedged Vs.Quadratic

Unhedged Quadratic

-8

-6

-4

-2

0

2

4

6

8

10

12

Unhedged Vs. ECM

Unhedged ECM

10

Figure 2: Variance of Rates of Return on the Unhedged and Hedged Positions (Cross

Currency Hedging)

Levels First Difference

Quadratic Error Correction

4.3 Data and Statistical Outputs

When analysing Table 1 and Table 2, a few things become apparent. Each econometric model

was successful at improving on the variance of an unhedged position. But they were all

successful to virtually the same degree of success. More testing could be done to see if the small

differences are significant or not. Also all numbers where statistically significant.

-8

-6

-4

-2

0

2

4

6

8

10

12

Unhedged Vs. Conventional

Unhedged Coventional

-8

-6

-4

-2

0

2

4

6

8

10

12

Unhedged Vs. First Difference

Unhedged Conventional (First)

-8

-6

-4

-2

0

2

4

6

8

10

12

Unhedged Vs. Quadratic

Unhedged Quadratic

-8

-6

-4

-2

0

2

4

6

8

10

12

Unhedged Vs. ECM

Unhedged ECM

11

Table 1: The Estimated Hedge Ratios

Hedging Method/Model Estimated h t Statistics 2R

Money Market

Levels

1.003197 746.4471 0.999758

First Differences

1.002283 1438.408 0.999935

Quadratic

.999667 213.0824 0.999759

Error Correction

1.002324 1470.821 0.999759

Cross Currency

Levels

.321832 4.925604 0.152338

First Differences

.313633 5.196754 0.167734

Quadratic

.189193 1.190871 0.157613

Error Correction

.342645 5.644652 0.211682

12

Table 2: Report the estimated VD and VR as in Table 2.

Hedging Method/Model Variance

(Unhedged)

Variance

(Hedged)

VR VD

Money Market

Levels

7.547234806 0.000498175 15217.71525 0.999934287

First Differences

7.547234806 0.000490837 15445.22682 0.999935255

Quadratic

7.547234806 0.000539529 14051.31754 0.999928832

Error Correction

7.547234806 0.000490896 15443.36927 0.999935247

Cross Currency

Levels

13.19446762 6.306547179 1.20209876 0.168121594

First Differences

13.19446762 6.305088259 1.202376911 0.168314036

Quadratic

13.19446762 6.50072812 1.166191295 0.142507748

Error Correction

13.19446762 6.318217792 1.199878319 0.166582157

5. CONCLUSION

The objective of this study was to measure the effectiveness of econometric models to estimate

the hedge ratio. And more specifically is one model better than the next. We tested the

Conventional Model, the Conventional Model with first differences, the Quadratic model, and

the Error Correction Model.

Though econometric models are a popular tool in finance, this paper shows that they might not

hold as much power as financial minds like to think. The four models tested to estimate a hedge

ratio are essentially useless when compared against one another. The amount of time spent

researching and developing these models may have been for naught.

With the money market hedge the study was able to create an almost perfect hedge. This is

possible because of a high correlation between the spot and interest parity rates. Because the

currencies for the cross currency hedge are not as highly correlated we do not achieve as

effective of a hedge. Because of this, a hedge ratio of one produces a cross currency hedge that is

less effective than with the money market hedge. That is why by using the correlation coefficient

between the two spot rates, we are able to create an effective hedge.

13

Based on this study, we can be confident that a hedging technique will help you minimize the

variance of the rate of returns, but the econometric model chosen to derive this does not matter.

It was Moosa (2003) who said it best, “Although the theoretical arguments for why model

specification does matter are elegant…what really matters for the success or failure of a hedge is

the correlation between the prices of the unhedged position and the hedging instrument”. And

this issue in correlation is why we see the difference with the money market hedge and the cross

currency.

Some considerations need to be made. As a follow up to this study a test of more econometric

models would be recommended. ARCH, GARCH, and ARIMA models may be considered and

tested. Though Casillo (2004) found that a multivariate GARCH model is only ‘marginally better’

than other. These marginal differences would need to be tested for significance. Moosa (2003)

found similar results to Casillo. However, in a study by Byström (2003) in a study of the hedging

effectiveness of the electricity futures contracts in Norway from January 1996 to October 1999,

he found that the OLS performed slightly better. It is because of this that I recommend the

GARCH method be attempted, but would not expect drastically different results.

14

REFERENCES

Benet, BA 1992, ‘Hedge period length and Ex-ante futures hedging effectiveness: The case of foreign-exchange risk cross hedges’, Journal of Futures Markets, vol. 12, no. 2, pp. 163–175.

Benninga, S, Eldor, R & Zilcha, I 1984, ‘The optimal hedge ratio in unbiased futures markets’, Journal of futures markets, vol. 4, no. 2, pp. 155–159.

Byström, HN 2003, ‘The hedging performance of electricity futures on the Nordic power exchange’, Applied Economics, vol. 35, no. 1, pp. 1–11.

Carter, D, Pantzalis, C & Simkins, B 2003, ‘Asymmetric exposure to foreign exchange risk: financial and real option hedges implemented by US multinational corporations’, in Proceedings from the 7th Annual International Conference on Real Options: Theory Meets Practice. Washington, DC, accessed October 13, 2014, from <http://realoptions.org/papers2003/SimkinsMNC_Paper.pdf>.

Casillo, A ‘Model Specification for the Estimation of the Optimal Hedge Ratio with Stock Index Futures: an Application to the Italian Derivatives Market’, accessed October 7, 2014, from <http://jamesgoulding.com/Research_II/Hedging%20Concepts/Hedging%20(Equity%20Index%201).pdf>.

Chinn, MD & Meese, RA 1995, ‘Banking on currency forecasts: How predictable is change in money?’, Journal of International Economics, vol. 38, no. 1, pp. 161–178.

Granger, CW & Weiss, AA 1983, ‘Time series analysis of error-correction models’, Studies in Econometrics, Time Series, and Multivariate Statistics, pp. 255–278.

Hatemi-J, A & Roca, E 2006, ‘Calculating the optimal hedge ratio: constant, time varying and the Kalman Filter approach’, Applied Economics Letters, vol. 13, no. 5, pp. 293–299.

Hendry, DF & Ericsson, NR 1991, ‘Modeling the demand for narrow money in the United Kingdom and the United States’, European Economic Review, vol. 35, no. 4, pp. 833–881.

Howard, CT & D’Antonio, LJ 1984, ‘A risk-return measure of hedging effectiveness’, Journal of Financial and Quantitative Analysis, vol. 19, no. 01, pp. 101–112.

Junkus, JC & Lee, CF 1985, ‘Use of three stock index futures in hedging decisions’, Journal of Futures Markets, vol. 5, no. 2, pp. 201–222.

Kim, YS, Mathur, I & Nam, J 2006, ‘Is operational hedging a substitute for or a complement to financial hedging?’, Journal of Corporate Finance, vol. 12, no. 4, pp. 834–853.

Lien, D 2004, ‘Cointegration and the optimal hedge ratio: the general case’, The Quarterly Review of Economics and Finance, vol. 44, no. 5, pp. 654–658.

Longo, C, Manera, M, Markandya, A & Scarpa, E 2007, ‘Evaluating the empirical performance of alternative econometric models for oil price forecasting’, accessed October 14, 2014, from <http://works.bepress.com/matteo_manera/2/>.

15

Mark, NC & Choi, D-Y 1997, ‘Real exchange-rate prediction over long horizons’, Journal of International Economics, vol. 43, no. 1, pp. 29–60.

Meese, RA & Rogoff, K 1983, ‘Empirical exchange rate models of the seventies: Do they fit out of sample?’, Journal of international economics, vol. 14, no. 1, pp. 3–24.

Moosa, I 2003, ‘The sensitivity of the optimal hedge ratio to model specification’, Finance Letters, vol. 1, no. 1, pp. 15–20.

Moosa, IA 2011, ‘The Failure of Financial Econometrics: Estimation of the Hedge Ratio as an Illustration’, The Capco Institute Journal of Financial Transformation, vol. 31, pp. 67–71.

Myers, RJ & Thompson, SR 1989, ‘Generalized Optimal Hedge Ratio Estimation’, American Journal of Agricultural Economics, vol. 71, no. 4, pp. 858–868.

Poterba, JM & Summers, LH 1987, The persistence of volatility and stock market fluctuations, National Bureau of Economic Research Cambridge, Mass., USA, accessed October 13, 2014, from <http://www.nber.org/papers/w1462>.

Yao, Z & Wu, H 2012, ‘Financial Engineering Estimation Methods of Minimum Risk Hedge Ratio’, Systems Engineering Procedia, vol. 3, pp. 187–193.

16

APPENDICES

Appendix 1: EViews for Money Market Hedge Dependent Variable: S Method: Least Squares Date: 08/30/14 Time: 11:33 Sample: 1 137 Included observations: 137

Variable Coefficient Std. Error t-Statistic Prob. C -0.001860 0.000180 -10.33411 0.0000

F 1.003197 0.001344 746.4471 0.0000 R-squared 0.999758 Mean dependent var 0.116152

Adjusted R-squared 0.999756 S.D. dependent var 0.064452 S.E. of regression 0.001007 Akaike info criterion -10.94955 Sum squared resid 0.000137 Schwarz criterion -10.90692 Log likelihood 752.0441 Hannan-Quinn criter. -10.93223 F-statistic 557183.3 Durbin-Watson stat 0.048938 Prob(F-statistic) 0.000000

Dependent Variable: DS Method: Least Squares Date: 08/30/14 Time: 11:37 Sample (adjusted): 2 137 Included observations: 136 after adjustments

Variable Coefficient Std. Error t-Statistic Prob. C -1.69E-05 1.90E-05 -0.888554 0.3758

DF 1.002283 0.000697 1438.408 0.0000 R-squared 0.999935 Mean dependent var -0.000290

Adjusted R-squared 0.999935 S.D. dependent var 0.027424 S.E. of regression 0.000222 Akaike info criterion -13.97760 Sum squared resid 6.58E-06 Schwarz criterion -13.93477 Log likelihood 952.4767 Hannan-Quinn criter. -13.96019 F-statistic 2069018. Durbin-Watson stat 2.001766 Prob(F-statistic) 0.000000

Dependent Variable: S Method: Least Squares Date: 08/30/14 Time: 11:38 Sample: 1 137 Included observations: 137

Variable Coefficient Std. Error t-Statistic Prob. C -0.001696 0.000276 -6.145730 0.0000

F 0.999667 0.004691 213.0824 0.0000 F2 0.014002 0.017828 0.785409 0.4336

R-squared 0.999759 Mean dependent var 0.116152

Adjusted R-squared 0.999755 S.D. dependent var 0.064452 S.E. of regression 0.001008 Akaike info criterion -10.93954 Sum squared resid 0.000136 Schwarz criterion -10.87560 Log likelihood 752.3587 Hannan-Quinn criter. -10.91356 F-statistic 277801.3 Durbin-Watson stat 0.051132 Prob(F-statistic) 0.000000

17

Dependent Variable: DS Method: Least Squares Date: 08/30/14 Time: 11:39 Sample (adjusted): 3 137 Included observations: 135 after adjustments

Variable Coefficient Std. Error t-Statistic Prob. C -1.57E-05 1.86E-05 -0.844800 0.3998

DS(-1) 0.008016 0.084707 0.094637 0.9247 DF 1.002324 0.000681 1470.821 0.0000

DF(-1) -0.006047 0.084904 -0.071216 0.9433 EC(-1) -0.027964 0.018697 -1.495684 0.1372

R-squared 0.999941 Mean dependent var -0.000268

Adjusted R-squared 0.999939 S.D. dependent var 0.027525 S.E. of regression 0.000216 Akaike info criterion -14.01080 Sum squared resid 6.04E-06 Schwarz criterion -13.90319 Log likelihood 950.7287 Hannan-Quinn criter. -13.96707 F-statistic 546418.0 Durbin-Watson stat 2.059779 Prob(F-statistic) 0.000000

Appendix 2: EViews Output for Cross Currency Hedge

Dependent Variable: S Method: Least Squares Date: 08/30/14 Time: 11:53 Sample: 1 137 Included observations: 137

Variable Coefficient Std. Error t-Statistic Prob. C 0.087549 0.007721 11.33908 0.0000

S2 0.321832 0.065339 4.925604 0.0000 R-squared 0.152338 Mean dependent var 0.116152

Adjusted R-squared 0.146059 S.D. dependent var 0.064452 S.E. of regression 0.059559 Akaike info criterion -2.789205 Sum squared resid 0.478884 Schwarz criterion -2.746577 Log likelihood 193.0605 Hannan-Quinn criter. -2.771882 F-statistic 24.26157 Durbin-Watson stat 0.176500 Prob(F-statistic) 0.000002

Dependent Variable: DS Method: Least Squares Date: 08/30/14 Time: 12:13 Sample (adjusted): 2 137 Included observations: 136 after adjustments

Variable Coefficient Std. Error t-Statistic Prob. C -0.000313 0.002153 -0.145210 0.8848

DS2 0.313633 0.060352 5.196754 0.0000 R-squared 0.167734 Mean dependent var -0.000290

Adjusted R-squared 0.161523 S.D. dependent var 0.027424 S.E. of regression 0.025111 Akaike info criterion -4.516392 Sum squared resid 0.084498 Schwarz criterion -4.473559 Log likelihood 309.1147 Hannan-Quinn criter. -4.498986 F-statistic 27.00625 Durbin-Watson stat 2.201068 Prob(F-statistic) 0.000001

18

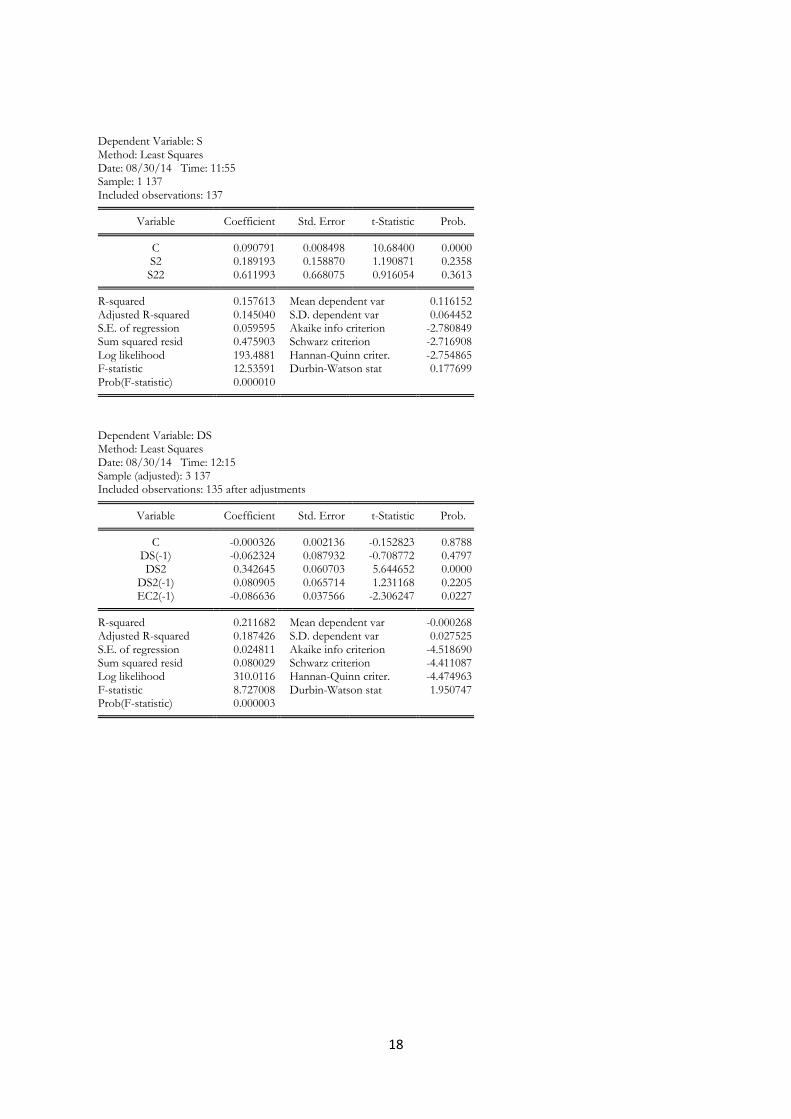

Dependent Variable: S Method: Least Squares Date: 08/30/14 Time: 11:55 Sample: 1 137 Included observations: 137

Variable Coefficient Std. Error t-Statistic Prob. C 0.090791 0.008498 10.68400 0.0000

S2 0.189193 0.158870 1.190871 0.2358 S22 0.611993 0.668075 0.916054 0.3613

R-squared 0.157613 Mean dependent var 0.116152

Adjusted R-squared 0.145040 S.D. dependent var 0.064452 S.E. of regression 0.059595 Akaike info criterion -2.780849 Sum squared resid 0.475903 Schwarz criterion -2.716908 Log likelihood 193.4881 Hannan-Quinn criter. -2.754865 F-statistic 12.53591 Durbin-Watson stat 0.177699 Prob(F-statistic) 0.000010

Dependent Variable: DS Method: Least Squares Date: 08/30/14 Time: 12:15 Sample (adjusted): 3 137 Included observations: 135 after adjustments

Variable Coefficient Std. Error t-Statistic Prob. C -0.000326 0.002136 -0.152823 0.8788

DS(-1) -0.062324 0.087932 -0.708772 0.4797 DS2 0.342645 0.060703 5.644652 0.0000

DS2(-1) 0.080905 0.065714 1.231168 0.2205 EC2(-1) -0.086636 0.037566 -2.306247 0.0227

R-squared 0.211682 Mean dependent var -0.000268

Adjusted R-squared 0.187426 S.D. dependent var 0.027525 S.E. of regression 0.024811 Akaike info criterion -4.518690 Sum squared resid 0.080029 Schwarz criterion -4.411087 Log likelihood 310.0116 Hannan-Quinn criter. -4.474963 F-statistic 8.727008 Durbin-Watson stat 1.950747 Prob(F-statistic) 0.000003