-

Research ArticleInventory Control by Multiple Service Levels

underUnreliable Supplying Condition

Byungsoo Na,1 Jinpyo Lee,2 and Hyung Jun Ahn2

1Division of Business Administration, Korea University, Sejong,

Republic of Korea2College of Business Administration, Hongik

University, Seoul, Republic of Korea

Correspondence should be addressed to Jinpyo Lee;

[email protected]

Received 28 March 2016; Accepted 31 July 2016

Academic Editor: Francisco Gordillo

Copyright © 2016 Byungsoo Na et al. This is an open access

article distributed under the Creative Commons Attribution

License,which permits unrestricted use, distribution, and

reproduction in any medium, provided the original work is properly

cited.

We consider an inventory system where there is random demand

from customers as well as unreliable supplying capacity

fromsupplier. In many real-world cases, supplier might fail to

satisfy the amount of order from retailers or producers so that

onlypartial proportion of order is satisfied or even fail to

deliver all of the order. Moreover, recently a concern regarding

unreliablesupplying capacity has been increasing since the

globalizationmakes the retailer or producer face the extended

supply network withcomplicated and risky supplying capacity. Also,

we consider two classified customers, of which one is willing to

pay extra charge forexpedited delivery service but the other is not

reluctant to delay the delivery without any extra charge. We show

that there exists anoptimal threshold for inventory and price for

each service level in the following sense: if the inventory level

is less than the predeter-mined threshold, then the retailer or

producer needs to order up to the threshold level and offer

threshold price corresponding to ser-vice level. Otherwise, the

retailer does not need to order.The risk of stockout due to

unreliable supplying capacity can bemitigated bythe dynamic pricing

and inventory control with multiple service levels.

1. Introduction

Coordination of dynamic inventory and pricing control hasbeen

used as main strategy for many companies such asAmazon, Dell, and

J. C. Penny [1]. In many traditional worksfor inventory control

problem, how to maximize the profitand control the uncertainty of

demand from customers hasbeen a stark issue, in which the optimal

policy has been pro-vided using either ordering quantity or pricing

of each prod-uct. Even some works show the optimal inventory

controlpolicy using multiple pricing on single product dependingon

the service levels. However, in addition to the randomdemand from

customers, it is not well addressed that mostfirms experience the

unreliable supplying capacity fromsupplier, which is another

randomness carried from supplier.For example, suppose that

Amazon.com orders 100 books toa publisher. However, the publisher

might fail to fulfill theorder and it may deliver only some of the

ordered books(i.e., 80 books) for its own supplying capacity

problem. Somerecent works address this unreliable supply issue

which is

incorporated with pricing on the product and

replenishmentdecisions but only addresses the pricing policy on a

productwith a single-service level [2]. However, as shown in

manyonline stores, each product is delivered with more than

asingle-service level where faster service can be suggestedto the

customer willing to pay an extra charge. So, how tobalance the

demand and supply by incorporating multiplepricing corresponding to

the service level is an importantissue faced by many firms,

especially online firms. In thispaper, we show that there can be an

optimal policy toan inventory control problem in which each product

ispriced depending on the service level and the supplyingcapacity

from the supplier is also random in addition to therandomness of

demand from the customer.

2. Literatures Review

Two streams of literatures are related to this paper:(1) The

inventory/production or pricing control problem

under reliable supplying capacity.

Hindawi Publishing CorporationMathematical Problems in

EngineeringVolume 2016, Article ID 1534580, 10

pageshttp://dx.doi.org/10.1155/2016/1534580

-

2 Mathematical Problems in Engineering

(2) The inventory/production or pricing control problemunder

unreliable supplying capacity.

There are many literatures that study the inventory orpricing

control problem under reliable supplying capacity.Reference [1]

gives a comprehensive survey on this problem,in which only a

single-service level is considered. Refer-ences [3, 4] address a

single-period problem under riskneutrality, which is addressed

using Newsvendor Model.Reference [5] suggests optimal replenishment

and pricingpolicy of a single-period model under risk aversion.

Formultiperiod system, when total ordering cost is a linearfunction

of ordering quantity, a base stock list price isshown to be optimal

for single-service level in [6] and formultiple service level in

[7]. References [8, 9] show that,for multiperiod system, there is

an optimal inventory andpricing policy when a fixed ordering cost

is considered andbacklogging is allowed. Reference [10] provides an

optimalinventory and pricing policy for multiperiod system when

afixed ordering cost is considered and lost-sales are

allowed.Reference [11] addresses joint inventory and pricing

modelwhere there is a single item with stochastic demand subjectto

reference effects and the random demand is a functionof the current

price and the reference price is acting as abenchmark with which

customers compare the current price.Reference [12] suggests the

joint pricing and inventorymodelfor a stochastic inventory system

with perishable products,where the inventory system under random

demand andreliable supplying capacity is modeled by a

continuous-timestochastic differential equation. Reference [13]

considers jointpricing and inventory replenishment decision problem

overan infinite horizon where sequentially arriving customers

areforward-looking to the price of a product sold by a seller.

Intheir model, so-called strategic customers wait and monitorprices

offered from the seller and then anticipate a lowerfuture price.

Reference [14] addresses a joint pricing andproduction decision

problem for perishable items sold toprice-sensitive customers,

assuming that shortages are notallowed.

The other stream of literature relevant to our paper isthe

inventory/production or pricing control problem underunreliable

supplying capacity. Reference [15] surveys theliterature on how to

quantitatively determine lot sizes whenproduction or procurement

yields are uncertain. Reference[16] addresses an inventory control

model for a periodicreview with unreliable production capacity,

random yields,and uncertain demand but does not consider the

dynamicpricing by considering the price as exogenous and

thusminimizing the total discounted expected costs which

areproduction, holding, and shortage costs. References [17,

18]address the joint inventory and pricing decision problemwith

random demand and unreliable suppling capacity, inwhich there are

no multiple service levels. Reference [19]addresses the inventory

(but no pricing) decision modelfor production-inventory systems in

which the stock candeteriorate with time and supplying capacity

from multiplesuppliers is unreliable. Reference [20] investigates

an optimalinventory strategy for a risk-averse retailer facing

demanduncertainty and unreliable supply in which the price is

given

and is exogenous. Reference [21] considers a

risk-neutralmonopolist manufacturer ordering a key component

fromseveral suppliers using a single-period model, in which

somesuppliers might face risks of complete supplying

disruptions,which are called unreliable suppliers. Reference [22]

suggestsoptimal sourcing strategies without pricing decision

whenthere are a perfectly reliable supplier and an

unreliablesupplier.

3. Assumptions and Notations

In this paper, the following notations are used:

(1) 𝑐: per unit marginal cost,(2) 𝑝𝑅,𝑡: price charged for

regular service in period 𝑡,

(3) 𝑝𝐸,𝑡: price charged for express service in period 𝑡,

(4) 𝑝𝑡= 𝑝𝐸,𝑡

−𝑝𝑅,𝑡: extra charge for the express service in

period 𝑡 on [0, 𝑝],(5) 𝜖𝑡: random uncertainty term of demand

which had a

known distribution,(6) 𝐷

𝐸,𝑡(𝑝𝑅,𝑡

, 𝑝𝐸,𝑡

): demand for the express service,(7) 𝐷𝑅,𝑡

(𝑝𝑅,𝑡

): demand for the regular service,(8) 𝑥𝑡: inventory level at the

beginning of each period 𝑡

before ordering,(9) 𝑦𝑡: inventory level at the beginning of each

period 𝑡

after ordering,(10) ℎ

𝑡(𝐼): inventory cost (holding or backlogging) at the

end of each period 𝑡.

Assumption 1. Backlogging is allowed.

Assumption 2. Replenishment after ordering becomes avail-able

instantaneously.

Traditionally, in operations research literatures, the

cus-tomer’s demand is assumed to be decreasing concave functionor

simply a decreasing linear function with the price as aninput

variable. Also, the expected demand value is assumed tobe finite

and strictly decreasing as the price increases, which isgenerally

acceptable and reasonable.This decreasing propertyof demand can be

negative if the value of price is sufficientlylarge. Thus, we need

to make another assumption such thata feasible price should be

selected on the restricted range inorder to be nonnegative valued

[6, 9, 23, 24].

Assumption 3. In each period 𝑡 = 1, 2, . . . , 𝑇, the

demandfunction for regular service 𝐷

𝑅,𝑡(𝑝𝑅,𝑡

, 𝑝𝐸,𝑡

) = 𝑑𝑅,𝑡

(𝑝𝑡), where

𝑑𝑅,𝑡

(𝑝𝑡) is given by 𝑑

𝑅,𝑡(𝑝𝐸,𝑡

− 𝑝𝑅,𝑡

), and nondecreasinglinear function in 𝑝

𝑡(=𝑝𝐸,𝑡

− 𝑝𝑅,𝑡

) ∈ [0, 𝑝]. The demandfunction for express service 𝐷

𝐸,𝑡(𝑝𝑅,𝑡

, 𝑝𝐸,𝑡

) = 𝑑𝐸,𝑡

(𝑝𝑅,𝑡

, 𝑝𝑡),

where 𝑑𝐸,𝑡

(𝑝𝑅,𝑡

, 𝑝𝑡) is given by 𝑎(𝑝

𝑅,𝑡, 𝜖𝑡) − 𝐷

𝑅,𝑡(𝑝𝑅,𝑡

, 𝑝𝐸,𝑡

) =

𝑎(𝑝𝑅,𝑡

, 𝜖𝑡) − 𝑑𝑅,𝑡

(𝑝𝑡), which is nonincreasing linear function

in 𝑝𝑅,𝑡

∈ [𝑝𝑅, 𝑝𝑅] and 𝑝

𝑡∈ [0, 𝑝]. Moreover, 𝑎(𝑝

𝑅,𝑡, 𝜖𝑡) is the

possible maximum demand and nonincreasing and linearfunction of

𝑝

𝑅,𝑡∈ [𝑐, 𝑝

𝑅]. Moreover, values for 𝑝 and 𝑝

𝑅are

taken such that 𝑎(𝑝𝑅, 𝜖𝑡) −𝐷𝑅,𝑡

(𝑝𝑅,𝑡

, 𝑝𝐸,𝑡

) is nonnegative withprobability 1.

-

Mathematical Problems in Engineering 3

Assumption 3 came up from the following insight. Thenumber of

customers using the express service woulddecrease as the price

difference 𝑝

𝑡between regular and

express service increases. For example, when you try to buysome

product from an online store, the higher the pricedifference

between regular shipping and express shippingservice are, the more

you are reluctant to select the expressshipping service. Thus, as

the price difference 𝑝

𝑡between

regular and express service increases, the customers who

arereluctant to select express service will become the customersfor

regular service.

Assumption 4. The revenue in each period 𝑡 = 1, 2, . . . , 𝑇

isgiven by

𝑝𝑅,𝑡

𝐸 [𝐷𝑅,𝑡

(𝑝𝑅,𝑡

, 𝑝𝐸,𝑡

)] + 𝑝𝐸,𝑡

𝐸 [𝐷𝐸,𝑡

(𝑝𝑅,𝑡

, 𝑝𝐸,𝑡

)]

= 𝑝𝑅,𝑡

𝐸 [𝑑𝑅,𝑡

(𝑝𝑡)] + 𝑝

𝐸,𝑡𝐸 [𝑑𝐸,𝑡

(𝑝𝑅,𝑡

, 𝑝𝑡)]

(1)

and is finite and concave for 𝑝𝑅,𝑡

∈ [𝑝𝑅, 𝑝𝑅] and 𝑝

𝑡∈ [0, 𝑝],

where 𝑝𝑡= 𝑝𝐸,𝑡

− 𝑝𝑅,𝑡.

Assumption 5. 𝐻𝑡(𝐼) = 𝐸[ℎ

𝑡(𝐼)] is convex in 𝐼 and 𝐻

𝑡(0) = 0

in each 𝑡 = 1, . . . , 𝑇.

Assumption 6. lim𝑦→±∞

𝐻𝑡(𝑦 − 𝐷

𝐸,𝑡(𝑝𝑅,𝑡

, 𝑝𝐸,𝑡

)) =

lim𝑦→±∞

(𝑐𝑦+𝐻𝑡(𝑦−𝐷

𝐸,𝑡(𝑝𝑅,𝑡

, 𝑝𝐸,𝑡

))) = ∞ for any𝑝𝑅,𝑡

∈ [𝑝𝑅,

𝑝𝑅] and 𝑝

𝑡∈ [0, 𝑝].

4. Mathematical Formulation

We consider an additive demand model, where the

demanduncertainty for regular and express service is represented

byan additive random noise 𝜖

𝑡, respectively,

𝐷𝑅,𝑡

(𝑝𝑅,𝑡

, 𝑝𝐸,𝑡

) = 𝑑𝑅,𝑡

(𝑝𝑡) = D

𝑅,𝑡(𝑝𝑡) + 𝜖𝑡,

𝐷𝐸,𝑡

(𝑝𝑅,𝑡

, 𝑝𝐸,𝑡

) = 𝑑𝐸,𝑡

(𝑝𝑅,𝑡

, 𝑝𝑡) = D

𝐸,𝑡(𝑝𝑅,𝑡

, 𝑝𝑡) + 𝜖𝑡.

(2)

We assume that 𝜖𝑡has mean zero and support [𝜖, 𝜖]. For

any feasible choice of 𝑝𝑅,𝑡

∈ [𝑝𝑅, 𝑝𝑅] and 𝑝

𝐸,𝑡∈ [𝑝𝐸, 𝑝𝐸],

the demand is positive with probability one and the

averagedemands 𝐸[𝐷

𝑅,𝑡(𝑝𝑅,𝑡

, 𝑝𝐸,𝑡

)] and 𝐸[𝐷𝐸,𝑡

(𝑝𝑅,𝑡

, 𝑝𝐸,𝑡

)] are finite.Given the inventory level 𝐼

𝑡in period 𝑡, the inventory level

𝐼𝑡+1

in period 𝑡 + 1 is given as follows:

𝐼𝑡+1

= 𝐼𝑡+ (𝑦𝑡− 𝐼𝑡) ∧ 𝑘 − 𝑑

𝐸,𝑡(𝑝𝑅,𝑡

, 𝑝𝑡) , (3)

where 𝑘 ∈ [0, 𝑦𝑡− 𝐼𝑡] in period 𝑡 and 𝑎 ∧ 𝑏 = min[𝑎, 𝑏]. Let

𝑔𝑡(𝐼, 𝑥) be the optimal profit function in period 𝑡 when the

inventory level is 𝐼 and the demand from period 𝑡 − 1 is 𝑥.Then,

the optimality equation is given by

𝑔𝑡 (𝐼, 𝑥) = max

𝑦≥𝐼,𝑝𝑅≤𝑝𝑅≤𝑝𝑅,𝑝≤𝑝≤𝑝

𝜋𝑡(𝐼; 𝑦, 𝑝

𝑅, 𝑝) , (4)

where𝜋𝑡(𝐼; 𝑦, 𝑝

𝑅, 𝑝)

= 𝑝𝑅𝐸 [𝑑𝑅(𝑝)] + 𝑝

𝐸𝐸 [𝑑𝐸(𝑝𝑅, 𝑝)]

− 𝑐𝐸 [(𝐼 + 𝑘) ∧ 𝑦 − 𝐼]

− 𝐸 [𝐻 ((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝))]

+ 𝛼𝐸 [𝑔𝑡+1

((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝) , 𝑑

𝑅(𝑝))] .

(5)

From Lemma 7, we can expect a dynamic programmingmodel with

single state as an input variable which is equiva-lent to (4).

Moreover, we can see that the optimal solution tothe equivalent

dynamic programmingmodel with single statecan be translated into

the optimal solution to (4).

Lemma7. Let 𝐼 and𝑦 be defined as 𝐼−𝑥 and𝑦−𝑥, respectively.Then,

(𝑦∗

𝑡+ 𝑥, 𝑝

∗

𝑅,𝑡, 𝑝∗

𝑡) is the set of optimal solutions to (4) if

and only if (𝑦∗𝑡, 𝑝∗

𝑅,𝑡, 𝑝∗

𝑡) is the set of optimal solutions to

G𝑡(𝐼) = max

𝑦≥𝐼,𝑝𝑅≤𝑝𝑅≤𝑝𝑅,𝑝≤𝑝≤𝑝

Π𝑡(𝐼 : 𝑦, 𝑝

𝑅, 𝑝) , (6)

where

Π𝑡(𝐼 : 𝑦, 𝑝

𝑅, 𝑝)

= 𝑝𝑅𝐸 [𝑑𝑅(𝑝)] + 𝑝

𝐸𝐸 [𝑑𝐸(𝑝𝑅, 𝑝)]

− 𝑐𝐸 [(𝐼 + 𝑘) ∧ 𝑦 − 𝐼]

− 𝐸 [𝐻 ((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝))]

+ 𝛼𝐸 [G𝑡+1

((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝) − 𝑑

𝑅(𝑝))] .

(7)

Proof. It is enough to show that, for all period 𝑡,

𝜋𝑡(𝐼; 𝑦, 𝑝

𝑅, 𝑝) = Π

𝑡(𝐼 : 𝑦, 𝑝

𝑅, 𝑝) ∀𝐼, 𝑥, 𝑦, 𝑝

𝑅, 𝑝. (8)

Since

(𝐼 + 𝑘) ∧ 𝑦 = (𝐼 − 𝑥 + 𝑘) ∧ (𝑦 − 𝑥)

=

{

{

{

𝐼 − 𝑥 + 𝑘, if 𝐼 − 𝑥 + 𝑘 ≤ 𝑦 − 𝑥

𝑦 − 𝑥, otherwise

= (𝐼 + 𝑘) ∧ 𝑦 − 𝑥,

(9)

for all period 𝑡, the first four terms of 𝜋𝑡(𝐼; 𝑦, 𝑝

𝑅, 𝑝) andΠ

𝑡(𝐼 :

𝑦, 𝑝𝑅, 𝑝) are equal to each other as follows:

𝑝𝑅𝐸 [𝑑𝑅(𝑝)] + 𝑝

𝐸𝐸 [𝑑𝐸(𝑝𝑅, 𝑝)]

− 𝑐𝐸 [(𝐼 + 𝑘) ∧ 𝑦 − 𝐼]

− 𝐸 [𝐻 ((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝))]

= 𝑝𝑅𝐸 [𝑑𝑅(𝑝)] + 𝑝

𝐸𝐸 [𝑑𝐸(𝑝𝑅, 𝑝)]

− 𝑐𝐸 [(𝐼 + 𝑘) ∧ 𝑦 − 𝐼]

− 𝐸 [𝐻 ((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝) − 𝑥)] .

(10)

-

4 Mathematical Problems in Engineering

In period 𝑇, trivially 𝑔𝑇(𝐼, 𝑥) = G

𝑇(𝐼) = 0. In period 𝑇 − 1,

𝜋𝑇−1

(𝐼; 𝑦, 𝑝𝑅, 𝑝)

= 𝑝𝑅𝐸 [𝑑𝑅,𝑇−1

(𝑝)] + 𝑝𝐸𝐸 [𝑑𝐸(𝑝𝑅,𝑇−1

, 𝑝)]

− 𝑐𝐸 [(𝐼 + 𝑘) ∧ 𝑦 − 𝐼]

− 𝐸 [𝐻 ((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸,𝑇−1(𝑝𝑅, 𝑝) − 𝑥)]

= 𝑝𝑅𝐸 [𝑑𝑅,𝑇−1

(𝑝)] + 𝑝𝐸𝐸 [𝑑𝐸,𝑇−1

(𝑝𝑅, 𝑝)]

− 𝑐𝐸 [(𝐼 + 𝑘) ∧ 𝑦 − 𝐼]

− 𝐸 [𝐻 ((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸,𝑇−1

(𝑝𝑅, 𝑝))]

= Π𝑇−1

(𝐼 : 𝑦, 𝑝𝑅, 𝑝) .

(11)

So, 𝑔𝑇−1

(𝐼, 𝑥) = G𝑇−1

(𝐼)with 𝐼 = 𝐼−𝑥. By induction, supposethat, for any 𝐼, 𝑥 with 𝐼

= 𝐼 − 𝑥,

𝑔𝑛 (

𝐼, 𝑥) = G𝑛 (𝐼) , 𝑛 = 𝑇, 𝑇 − 1, . . . , 𝑡 + 1. (12)

Then

𝜋𝑡(𝐼; 𝑦, 𝑝

𝑅, 𝑝)

= 𝑝𝑅𝐸 [𝑑𝑅(𝑝)] + 𝑝

𝐸𝐸 [𝑑𝐸(𝑝𝑅, 𝑝)]

− 𝑐𝐸 [(𝐼 + 𝑘) ∧ 𝑦 − 𝐼]

− 𝐸 [𝐻 ((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝) − 𝑥)]

+ 𝛼𝐸 [𝑔𝑡+1

((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝) − 𝑥, 𝑑

𝑅(𝑝))]

= 𝑝𝑅𝐸 [𝑑𝑅(𝑝)] + 𝑝

𝐸𝐸 [𝑑𝐸(𝑝𝑅, 𝑝)]

− 𝑐𝐸 [(𝐼 + 𝑘) ∧ 𝑦 − 𝐼]

− 𝐸 [𝐻 ((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝))]

+ 𝛼𝐸 [G𝑡+1

((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝) − 𝑑

𝑅(𝑝))] .

(13)

The second equality holds since (𝐼+𝑘)∧𝑦−𝑑𝐸(𝑝𝑅, 𝑝)−𝑑

𝑅(𝑝) =

(𝐼+𝑘)∧𝑦−𝑑𝐸(𝑝𝑅, 𝑝)−𝑥−𝑑

𝑅(𝑝). Therefore, the result holds.

4.1. Optimal Inventory Control Policy. Now, we will show

thefollowing optimal inventory control policy: if the

inventorylevel at each period 𝑡 before ordering is less than a

predeter-mined level, then we need to order such that the

inventorylevel is increased up to the predetermined level.

Otherwise,no ordering will be made.

Lemma 8. Suppose that G𝑡+1

(⋅) is concave function and, forgiven 𝑝

𝑅and 𝑝, let 𝑦∗(𝑝

𝑅, 𝑝) be the maximizer of

𝑝𝑅𝑑𝑅(𝑝) + 𝑝

𝐸𝑑𝐸(𝑝𝑅, 𝑝) − 𝑐 (𝑦 − 𝐼)

− 𝐻 (𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝))

+ 𝛼G𝑡+1

(𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝) − 𝑑

𝑅(𝑝)) ,

(14)

where 𝑝𝐸= 𝑝𝑅+ 𝑝. Then, 𝑦∗(𝑝

𝑅, 𝑝) is also the maximizer of

𝑝𝑅𝐸 [𝑑𝑅(𝑝)] + 𝑝

𝐸𝐸 [𝑑𝐸(𝑝𝑅, 𝑝)]

− 𝑐𝐸 [(𝐼 + 𝑘) ∧ 𝑦 − 𝐼]

− 𝐸 [𝐻 ((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝))]

+ 𝛼𝐸 [G𝑡+1

((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝) − 𝑑

𝑅(𝑝))]

(15)

for any 𝐼 and, moreover,

𝑝𝑅𝐸 [𝑑𝑅(𝑝)] + 𝑝

𝐸𝐸 [𝑑𝐸(𝑝𝑅, 𝑝)] − 𝑐𝐸 [(𝐼 + 𝑘)

∧ (𝑦∗(𝑝𝑅, 𝑝) ∨ 𝐼) − 𝐼] − 𝐸 [𝐻 ((𝐼 + 𝑘)

∧ (𝑦∗(𝑝𝑅, 𝑝) ∨ 𝐼) − 𝑑

𝐸(𝑝𝑅, 𝑝))]

+ 𝛼𝐸 [G𝑡+1

((𝐼 + 𝑘) ∧ (𝑦∗(𝑝𝑅, 𝑝) ∨ 𝐼)

− 𝑑𝐸(𝑝𝑅, 𝑝) − 𝑑

𝑅(𝑝))]

(16)

is jointly concave in (𝐼, 𝑝𝑅, 𝑝), where 𝑎 ∨ 𝑏 = max[𝑎, 𝑏].

Proof. Given𝑝𝑅and𝑝,𝑝

𝑅𝑑𝑅(𝑝)+𝑝

𝐸𝑑𝐸(𝑝𝑅, 𝑝) is just constant

and thus wewill not consider them for a while. Since𝐻(⋅)

andG𝑡+1

(⋅) are concave,

𝑝𝑅𝑑𝑅(𝑝) + 𝑝

𝐸𝑑𝐸(𝑝𝑅, 𝑝) − 𝑐𝑦 − 𝐻 (𝑦 − 𝑑

𝐸(𝑝𝑅, 𝑝))

+ 𝛼G𝑡+1

(𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝) − 𝑑

𝑅(𝑝))

(17)

is jointly concave in (𝑦, 𝑝𝑅, 𝑝). Now, take any 𝛿 > 0 such

that

𝑦+𝛿 < 𝑦∗(𝑝𝑅, 𝑝) and we have 𝑦∧ (𝐼+𝑘) ≤ (𝑦+𝛿)∧ (𝐼+𝑘) <

𝑦∗(𝑝𝑅, 𝑝). So,

− 𝑐 (𝑦 ∧ (𝐼 + 𝑘) − 𝐼) − 𝐻((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝))

+ 𝛼 (G𝑡+1

((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝) − 𝑑

𝑅(𝑝)))

≤ −𝑐 ((𝑦 + 𝛿) ∧ (𝐼 + 𝑘) − 𝐼) − 𝐻((𝐼 + 𝑘) ∧ (𝑦

+ 𝛿) − 𝑑𝐸(𝑝𝑅, 𝑝)) + 𝛼 (G

𝑡+1((𝐼 + 𝑘) ∧ (𝑦 + 𝛿)

− 𝑑𝐸(𝑝𝑅, 𝑝) − 𝑑

𝑅(𝑝)))

(18)

for any 𝑘. Thus,

𝐸 [−𝑐 (𝑦 ∧ (𝐼 + 𝑘) − 𝐼) − 𝐻((𝐼 + 𝑘) ∧ 𝑦

− 𝑑𝐸(𝑝𝑅, 𝑝)) + 𝛼G

𝑡+1((𝐼 + 𝑘) ∧ 𝑦 − 𝑑

𝐸(𝑝𝑅, 𝑝)

− 𝑑𝑅(𝑝))] ≤ 𝐸 [−𝑐 ((𝑦 + 𝛿) ∧ (𝐼 + 𝑘) − 𝐼)

− 𝐻((𝐼 + 𝑘) ∧ (𝑦 + 𝛿) − 𝑑𝐸(𝑝𝑅, 𝑝))

+ 𝛼G𝑡+1

((𝐼 + 𝑘) ∧ (𝑦 + 𝛿) − 𝑑𝐸(𝑝𝑅, 𝑝)

− 𝑑𝑅(𝑝))] .

(19)

-

Mathematical Problems in Engineering 5

Therefore,

− 𝑐𝐸 [(𝐼 + 𝑘) ∧ 𝑦 − 𝐼]

− 𝐸 [𝐻 ((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝))]

+ 𝛼𝐸 [G𝑡+1

((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝) − 𝑑

𝑅(𝑝))]

(20)

is increasing in 𝑦 when 𝑦 ≤ 𝑦∗(𝑝𝑅, 𝑝). By the similar

argument,

− 𝑐𝐸 [(𝐼 + 𝑘) ∧ 𝑦 − 𝐼]

− 𝐸 [𝐻 ((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝))]

+ 𝛼𝐸 [G𝑡+1

((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝) − 𝑑

𝑅(𝑝))]

(21)

is decreasing in 𝑦 when 𝑦 ≥ 𝑦∗(𝑝𝑅, 𝑝). The first result

holds.

Since, for given 𝑝𝑅and 𝑝, 𝑦∗(𝑝

𝑅, 𝑝) is the maximizer of

− 𝑐 ((𝐼 + 𝑘) − 𝐼) − 𝐻((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝))

+ 𝛼G𝑡+1

((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝) − 𝑑

𝑅(𝑝))

(22)

for any 𝑦 ∈ R, for given 𝑝𝑅and 𝑝, (𝑦∗(𝑝

𝑅, 𝑝) ∨ 𝐼) ∧ (𝐼 + 𝑘) is

the maximizer of

− 𝑐 ((𝐼 + 𝑘) − 𝐼) − 𝐻((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝))

+ 𝛼G𝑡+1

((𝐼 + 𝑘) ∧ 𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝) − 𝑑

𝑅(𝑝))

(23)

for 𝑦 ∈ [𝐼, 𝐼 + 𝑘]. Now, take (𝐼1, 𝑝𝑅,1

, 𝑝1), (𝐼2, 𝑝𝑅,2

, 𝑝2), and

𝛾 ∈ [0, 1]. Then

𝛾 (−𝑐 ((𝐼1+ 𝑘) ∧ (𝑦

∗(𝑝𝑅,1

, 𝑝1) ∨ 𝐼1) − 𝐼1) − 𝐻((𝐼

1

+ 𝑘) ∧ (𝑦∗(𝑝𝑅,1

, 𝑝1) ∨ 𝐼1) − 𝑑𝐸(𝑝𝑅,1

, 𝑝1))

+ 𝛼 (G𝑡+1

((𝐼1+ 𝑘) ∧ (𝑦

∗(𝑝𝑅,1

, 𝑝1) ∨ 𝐼1)

− 𝑑𝐸(𝑝𝑅,1

, 𝑝1) − 𝑑𝑅(𝑝𝑅,1

, 𝑝1)))) + (1 − 𝛾)

⋅ (−𝑐 ((𝐼2+ 𝑘) ∧ (𝑦

∗(𝑝𝑅,2

, 𝑝2) ∨ 𝐼2) − 𝐼2)

− 𝐻((𝐼2+ 𝑘) ∧ (𝑦

∗(𝑝𝑅,2

, 𝑝2) ∨ 𝐼2)

− 𝑑𝐸(𝑝𝑅,2

, 𝑝2)) + 𝛼G

𝑡+1((𝐼2+ 𝑘)

∧ (𝑦∗(𝑝𝑅,2

, 𝑝2) ∨ 𝐼2) − 𝑑𝐸(𝑝𝑅,2

, 𝑝2)

− 𝑑𝑅(𝑝𝑅,2

, 𝑝2))) ≤ −𝑐 (𝛾 [(𝐼

1+ 𝑘)

∧ (𝑦∗(𝑝𝑅,1

, 𝑝1) ∨ 𝐼1)] + (1 − 𝛾) [(𝐼

2+ 𝑘)

∧ (𝑦∗(𝑝𝑅,2

, 𝑝2) ∨ 𝐼2)] − 𝐼

𝛾) − 𝐻(𝛾 [(𝐼

1+ 𝑘)

∧ (𝑦∗(𝑝𝑅,1

, 𝑝1) ∨ 𝐼1)] + (1 − 𝛾) [(𝐼

2+ 𝑘)

∧ (𝑦∗(𝑝𝑅,2

, 𝑝2) ∨ 𝐼2)] − 𝑑

𝐸(𝑝𝑅,𝛾

, 𝑝𝐸,𝛾

))

+ 𝛼G𝑡+1

(𝛾 [(𝐼1+ 𝑘) ∧ (𝑦

∗(𝑝𝑅,1

, 𝑝1) ∨ 𝐼1)] + (1

− 𝛾) [(𝐼2+ 𝑘) ∧ (𝑦

∗(𝑝𝑅,2

, 𝑝2) ∨ 𝐼2)]

− 𝛾 [𝑑𝐸(𝑝𝑅,1

, 𝑝1) − 𝑑𝑅(𝑝𝑅,1

, 𝑝1)] − (1 − 𝛾)

⋅ [𝑑𝐸(𝑝𝑅,2

, 𝑝2) − 𝑑𝑅(𝑝𝑅,2

, 𝑝2)]) = −𝑐 (𝛾 [(𝐼

1+ 𝑘)

∧ (𝑦∗(𝑝𝑅,1

, 𝑝1) ∨ 𝐼1)] + (1 − 𝛾) [(𝐼

2+ 𝑘)

∧ (𝑦∗(𝑝𝑅,2

, 𝑝2) ∨ 𝐼2)] − 𝐼

𝛾) − 𝐻(𝛾 [(𝐼

1+ 𝑘)

∧ (𝑦∗(𝑝𝑅,1

, 𝑝1) ∨ 𝐼1)] + (1 − 𝛾) [(𝐼

2+ 𝑘)

∧ (𝑦∗(𝑝𝑅,2

, 𝑝2) ∨ 𝐼2)] − 𝑑

𝐸(𝑝𝑅,𝛾

, 𝑝𝐸,𝛾

))

+ 𝛼G𝑡+1

(𝛾 [(𝐼1+ 𝑘) ∧ (𝑦

∗(𝑝𝑅,1

, 𝑝1) ∨ 𝐼1)] + (1

− 𝛾) [(𝐼2+ 𝑘) ∧ (𝑦

∗(𝑝𝑅,2

, 𝑝2) ∨ 𝐼2)] − 𝑑

𝐸(𝑝𝑅,𝛾

,

𝑝𝛾) − 𝑑𝑅(𝑝𝑅,𝛾

, 𝑝𝛾)) ≤ −𝑐 ((𝐼

𝛾+ 𝑘)

∧ (𝑦∗(𝑝𝑅,𝛾

, 𝑝𝛾) ∨ 𝐼𝛾) − 𝐼𝛾) − 𝐻((𝐼

𝛾+ 𝑘)

∧ (𝑦∗(𝑝𝑅,𝛾

, 𝑝𝛾) ∨ 𝐼𝛾) − 𝑑𝐸(𝑝𝑅,𝛾

, 𝑝𝛾))

+ 𝛼G𝑡+1

((𝐼𝛾+ 𝑘) ∧ (𝑦

∗(𝑝𝑅,𝛾

, 𝑝𝛾) ∨ 𝐼𝛾)

− 𝑑𝐸(𝑝𝑅,𝛾

, 𝑝𝛾) − 𝑑𝑅(𝑝𝑅,𝛾

, 𝑝𝛾)) ,

(24)

where 𝐼𝛾

= 𝛾𝐼1+ (1 − 𝛾)𝐼

2, 𝑝𝑅,𝛾

= 𝛾𝑝𝑅,1

+ (1 − 𝛾)𝑝𝑅,2

, and𝑝𝛾

= 𝛾𝑝1+ (1 − 𝛾)𝑝

2. The first inequality holds due to the

concavity of𝐻𝑡andG

𝑡+1, the second equality holds due to the

linearity of demand functions, and the last inequality

holdssince, for given 𝑝

𝑅,𝛾and 𝑝

𝛾, 𝑦 = (𝐼

𝛾+ 𝑘) ∧ 𝑦

∗(𝑝𝑅,𝛾

, 𝑝𝛾) ∨ 𝐼𝛾

is the maximizer of

− 𝑐 (𝑦 − 𝐼) − 𝐻 (𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝))

+ 𝛼G𝑡+1

(𝑦 − 𝑑𝐸(𝑝𝑅, 𝑝) − 𝑑

𝑅(𝑝))

(25)

for 𝑦 ∈ [𝐼𝛾, 𝐼𝛾+ 𝑘]. So, we need to verify that

𝛾 [(𝐼1+ 𝑘) ∧ (𝑦

∗(𝑝𝑅,1

, 𝑝1) ∨ 𝐼1)]

+ (1 − 𝛾) [(𝐼2+ 𝑘) ∧ (𝑦

∗(𝑝𝑅,2

, 𝑝2) ∨ 𝐼2)]

(26)

is within [𝐼𝛾, 𝐼𝛾+ 𝑘].

𝛾 [(𝐼1+ 𝑘) ∧ (𝑦

∗(𝑝𝑅,1

, 𝑝1) ∨ 𝐼1)]

+ (1 − 𝛾) [(𝐼2+ 𝑘) ∧ (𝑦

∗(𝑝𝑅,2

, 𝑝2) ∨ 𝐼2)]

≥ 𝛾 [(𝐼1+ 𝑘) ∧ 𝐼

1] + (1 − 𝛾) [(𝐼

2+ 𝑘) ∧ 𝐼

2]

= 𝛾𝐼1+ (1 − 𝛾) 𝐼

2= 𝐼𝛾,

-

6 Mathematical Problems in Engineering

Table 1: Parameters for numerical analysis.

𝑎 𝑏𝑅

𝑏𝐸

Marginal cost Holding cost Backlog cost Salvage price Range for

regular price (𝑝𝑅) Range for extra charge (𝑝)

250 5 6 30 0.3 28 20 25–65 0–30

𝛾 [(𝐼1+ 𝑘) ∧ (𝑦

∗(𝑝𝑅,1

, 𝑝1) ∨ 𝐼1)]

+ (1 − 𝛾) [(𝐼2+ 𝑘) ∧ (𝑦

∗(𝑝𝑅,2

, 𝑝2) ∨ 𝐼2)]

≤ 𝛾 (𝐼1+ 𝑘) + (1 − 𝛾) (𝐼

2+ 𝑘) = 𝐼

𝛾+ 𝑘.

(27)

By taking the expectation, we can obtain the second result.

Proposition 9. For all 𝑡 = 1, 2, . . . , 𝑇, G𝑡(⋅) is concave

function.

Proof. Since we consider the 𝑇−period problem, G𝑇+1

(𝐼) =

0 and G𝑇+1

(𝐼) is concave in 𝐼. By induction, suppose thatG𝑡+1

(⋅) is concave. Let 𝑦∗(𝑝𝑅, 𝑝) be defined as in Lemma 8.

By Assumption 4 and Lemma 8,

Π𝑡(𝐼 : 𝑦∗(𝑝𝑅, 𝑝) ∨ 𝐼, 𝑝

𝑅, 𝑝) = 𝑝

𝑅𝐸 [𝑑𝑅(𝑝)]

+ 𝑝𝐸𝐸 [𝑑𝐸(𝑝𝑅, 𝑝)] − 𝑐𝐸 [(𝐼 + 𝑘) ∧ (𝑦

∗(𝑝𝑅, 𝑝)

∨ 𝐼) − 𝐼] − 𝐸 [𝐻 ((𝐼 + 𝑘) ∧ (𝑦∗(𝑝𝑅, 𝑝) ∨ 𝐼)

− 𝑑𝐸(𝑝𝑅, 𝑝))] + 𝛼𝐸 [G

𝑡+1((𝐼 + 𝑘)

∧ (𝑦∗(𝑝𝑅, 𝑝) ∨ 𝐼) − 𝑑

𝐸(𝑝𝑅, 𝑝) − 𝑑

𝑅(𝑝))]

(28)

is jointly concave in (𝐼, 𝑝𝑅, 𝑝). So,

G𝑡(𝐼) = max

𝑝𝑅≤𝑝𝑅≤𝑝𝑅,𝑝≤𝑝≤𝑝

Π𝑡(𝐼 : 𝑦∗(𝑝𝑅, 𝑝) ∨ 𝐼, 𝑝

𝑅, 𝑝) (29)

is concave in 𝐼. Therefore, for all 𝑡 = 1, 2, . . . , 𝑇, G𝑡(⋅)

is

concave.

Proposition 10. Suppose that, in period 𝑡, the inventory levelis

𝐼𝑡and the advanced demand from period 𝑡 − 1 which is for

regular service is 𝑥𝑡−1

.Then, in period 𝑡, there is some finite pair(𝑦∗

𝑡, 𝑝∗

𝑡, 𝑝∗

𝑅,𝑡) such that if 𝐼

𝑡− 𝑥𝑡−1

≤ 𝑦∗

𝑡, it is optimal to place

positive number (𝑦∗𝑡−𝐼𝑡+𝑥𝑡−1

) of order and to charge the prices𝑝∗

𝑅,𝑡+𝑝∗

𝑡for the express service and 𝑝∗

𝑅,𝑡for the regular service.

Otherwise, no ordering will take place.

Proof. As seen in Lemma 8, the optimal solution pair(𝑦∗

𝑡, 𝑝∗

𝑅,𝑡, 𝑝∗

𝑡) does not depend on 𝐼

𝑡and 𝑥

𝑡−1but 𝑦∗𝑡depends

on (𝑝∗𝑅, 𝑝𝑡) which is 𝑦∗

𝑡= 𝑦∗

𝑡(𝑝∗

𝑅,𝑡, 𝑝∗

𝑡). So, if 𝐼

𝑡− 𝑥𝑡−1

≤ 𝑦∗

𝑡,

it is optimal to place 𝑦∗𝑡− 𝐼𝑡+ 𝑥𝑡−1

of orders. Otherwise, theoptimal order up to level is 𝐼

𝑡− 𝑥𝑡−1

which is not to order.Now, we need to verify that there exists

finite solution pair ineach period 𝑡. In each period 𝑡, the

feasible sets for 𝑝

𝑅,𝑡and 𝑝

𝑡

are bounded so that the optimal pricing 𝑝∗𝑅,𝑡

and 𝑝∗𝑡are finite.

𝑦∗

𝑡= 𝑦∗

𝑡(𝑝∗

𝑅,𝑡, 𝑝∗

𝑡) is solution to

𝑝∗

𝑅,𝑡𝑑𝑅(𝑝∗

𝑡) + (𝑝

∗

𝑅,𝑡+ 𝑝∗

𝑡) 𝑑𝐸(𝑝∗

𝑅,𝑡, 𝑝∗

𝑡) − 𝑐 (𝑦 − 𝐼)

− 𝐻(𝑦 − 𝑑𝐸(𝑝∗

𝑅,𝑡, 𝑝∗

𝑡))

+ 𝛼G𝑡+1

(𝑦 − 𝑑𝐸(𝑝∗

𝑅,𝑡, 𝑝∗

𝑡) − 𝑑𝑅(𝑝∗

𝑡)) .

(30)

By Assumption 6, in each period 𝑡,

lim𝑦→±∞

− 𝑐𝑦 − 𝐻(𝑦 − 𝑑𝐸(𝑝∗

𝑅,𝑡, 𝑝∗

𝑡)) = −∞. (31)

Thus, as 𝑦 → ±∞

(𝑝∗

𝑅,𝑡𝑑𝑅(𝑝∗

𝑡) + (𝑝

∗

𝑅,𝑡+ 𝑝∗

𝑡) 𝑑𝐸(𝑝∗

𝑅,𝑡, 𝑝∗

𝑡) − 𝑐 (𝑦 − 𝐼)

− 𝐻(𝑦 − 𝑑𝐸(𝑝∗

𝑅,𝑡, 𝑝∗

𝑡))) + 𝛼G

𝑡+1(𝑦

− 𝑑𝐸(𝑝∗

𝑅,𝑡, 𝑝∗

𝑡) − 𝑑𝑅(𝑝∗

𝑡))

(32)

will go to ∞, and thus the solution 𝑦∗𝑡

= 𝑦∗

𝑡(𝑝∗

𝑅,𝑡, 𝑝∗

𝑡) should

be finite. Therefore, the result holds.

5. Numerical Analysis

In this section, we provide a report on a numerical

analysiscarried on to obtain insights into the structure of

optimalpolicies and their sensitivity and quantitative

comparisonwith the traditional policy (single-pricing policy).

Among themain questions, we focus on

(1) the benefits of a multiple pricing strategy comparedto a one

pricing strategy in settings with continuousinventory replenishment

opportunities,

(2) the sensitivity of the optimal base stock and listprices

with respect to the degree of variability and theseasonality in the

demands,

(3) the comparison of profit with the traditional single-pricing

policy.

Our numerical study is based on data in Table 1. As men-tioned

in Assumption 3, the demand function is a linearfunction of the

regular price and extra charge. That is,

𝑑𝐸(𝑝𝑟, 𝑝) = 𝑎 × 𝛾 − 𝑏

𝑅𝑝𝑅− 𝑏𝐸𝑝 + 𝜖. (33)

The random term 𝜖 is assumed to be normally distributedwith mean

0. However, it is truncated to avoid the negativevalue of demand

such that the minimum of 𝜖 is −1 × (𝑎 −𝑏𝑅𝑝𝑅−𝑏𝐸𝑝). Also, to capture

the degree of demand variability,

we have used [c.v. × (𝑎 − 𝑏𝑅𝑝𝑅− 𝑏𝐸𝑝)]2 as the variance of 𝜖,

-

Mathematical Problems in Engineering 7

Time

1.510.5

02 3 4 51

50

100

150

200

250

300

Opt

imal

bas

e sto

ck

(a) Nonseasonal case

0

50

100

150

200

250

300

350

400

Opt

imal

bas

e sto

ck

Time2 3 4 51

1.510.5

(b) Seasonal case

Figure 1: Optimal base stock levels for varying demand

uncertainty.

30

35

40

45

50

55

List

regu

lar p

rice

Time2 3 4 51

1.510.5

(a) Nonseasonal case

30

35

40

45

50

55

60

65

70

75

80

54321

List

regu

lar p

rice

Time

1.510.5

(b) Seasonal case

Figure 2: Price for regular service for varying demand

uncertainty.

where c.v. is the coefficient for the variability in demand. 𝛾

isthe randomly generated number for the demand seasonality.

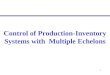

Figure 1 shows the base stock for both nonseasonal andseasonal

demand cases. As you can see in this figure, as thedemand variation

increases, the base stock tends to increase.This might be from the

fact that more demand fluctuationcan increase the possibility of

inventory shortage. So, in orderto decrease the shortage cost, the

base stock would increase.Figures 2 and 3 show the threshold price

predetermined for

regular service and express service in each time for eachdemand

variation (c.v.).

The inventory controlling strategy by multiple servicelevels can

provide the retailer or producer with the one-period advanced

information regarding demand since somecustomers, who select

regular service, are willing to delayshipment for their order. This

one-period advanced infor-mation can be useful in managing the

inventory in thenext period in the sense that inventory can be

controlled

-

8 Mathematical Problems in Engineering

Time2 3 4 51

1.510.5

30

35

40

45

50

55Li

st ex

pres

s pric

e

(a) Nonseasonal case

30

35

40

45

50

55

60

65

70

75

80

54321

List

expr

ess p

rice

Time

1.510.5

(b) Seasonal case

Figure 3: Price for express service for varying demand

uncertainty.

0

5

10

15

20

25

1.510.5(a) Nonseasonal case

0

5

10

15

20

25

1.510.5(b) Seasonal case

Figure 4: Profit comparison between inventory control by

multiple service levels and traditional inventory control by

single-service level.

more efficiently and moreover there is chance to reduce thecost

which is induced from holding too much inventory orshortage

inventory.

Figure 4 shows the benefits of an inventory controlthrough

multiple service levels compared to traditionalinventory control by

single-service level. In both nonseasonaland seasonal case, you can

see that our model under unreli-able supplying capacity is more

profitable than the traditionalsingle-service and single-pricing

model. Moreover, at higherlevel of demand uncertainty (c.v.), the

profit increase fromour model for seasonal demand case is higher

than thenonseasonal case. Thus, we can see that the benefit

frominventory control strategy by multiple service levels canbe

relatively large in the environment where the inventorysystem

experiences higher demand uncertainty and season-ality: inventory

control by multiple service levels under theunreliable supplying

capacity, which provides the system

with one-period advanced information regarding

demand,efficiently captures the demanduncertainty in order to

reducethe cost compared to traditional controlling model by

single-service level, thus giving more profit. From this

numericalanalysis, we can see that the proposed model provides

betterstrategy for the inventory controlling problem even under

theunreliable supplying capacity.

6. Conclusion

We study dynamic pricing and inventory replenishmentproblems

under unreliable supplying condition.This researchwas initiated by

the following practical intuition; that is,if customers are willing

to expedite the service for theirorder, then they are willing to

pay extra charge. In thispaper, we have verified this intuition

through constructinga reasonable demand model (Assumption 3) and by

the

-

Mathematical Problems in Engineering 9

mathematical dynamic programming model where productcan be

provided to the customers with multiple (two) pricescorresponding

to the service level, either express service orregular service. It

is shown in this paper that there exist apair of threshold levels

for inventory ordering up to leveland prices corresponding to

service levels in the followingstrategy: if the inventory level

before ordering in each periodwhich is subtracted by the regular

demand advanced fromthe previous period is less than the

predetermined threshold,then it is optimal to make ordering

decision and increaseinventory level up to the predetermined

threshold level andoffer threshold price for each service level.

Otherwise, noordering is optimal.

We can extend our model in the following possibleresearch

directions. First, we can extend the result to the caseof infinite

horizon. Considering an infinite horizon modelwith stationary

parameters with some practical assumptions,some optimality result

similar to one from the finite horizonmodel might be extended.

Second, we assume the depen-dency of demand in a period only on the

price in the sameand current period. However, the demand function

mightbe extended to depend not only on the current period butalso

on the current and the historical prices, which are theprices in

past periods. Even though it would be complex toanalyze, it would

be interesting to incorporate these moregeneral demand settings

into the model and examine thecorresponding optimal policies.

Third, our assumption inwhich the backlogging is allowed can be

modified such thatthe backlogging is not allowed but lost-sales are

assumed.Finally, it would be interesting and important to

incorporatea fixed ordering cost into our model. Analysis of

suchextensions can be more complicated to analyze but would beworth

further exploration.

Competing Interests

The authors declare that there are no competing

interestsregarding the publication of this paper.

Acknowledgments

This research was supported by 2014 Hongik UniversityResearch

Fund and also partially supported by the NationalResearch

Foundation of Korea Grant funded by the KoreanGovernment

(NRF-2015R1C1A1A02037096). These researchfunds do not lead to any

competing interests regarding thepublication of this

manuscript.

References

[1] W. Elmaghraby and P. Keskinocak, “Dynamic pricing in

thepresence of inventory considerations: research overview,

cur-rent practices, and future directions,”Management Science,

vol.49, no. 10, pp. 1287–1309, 2003.

[2] Q. Feng, “Integrating dynamic pricing and replenishment

deci-sions under supply capacity uncertainty,”Management

Science,vol. 56, no. 12, pp. 2154–2172, 2010.

[3] S. Karlin and C. R. Carr, “Prices and optimal inventory

policy,”in Studies in Applied Probability and Management Science,

vol.4, pp. 159–172, 1962.

[4] N. C. Petruzzi and M. Dada, “Pricing and the

newsvendorproblem: a reviewwith extensions,”Operations Research,

vol. 47,no. 2, pp. 183–194, 1999.

[5] V. Agrawal and S. Seshadri, “Impact of uncertainty and

riskaversion on price and order quantity in the newsvendor

prob-lem,” Manufacturing and Service Operations Management, vol.2,

no. 4, pp. 410–423, 2000.

[6] A. Federgruen and A. Heching, “Combined pricing and

inven-tory control under uncertainty,”Operations Research, vol. 47,

no.3, pp. 454–475, 1999.

[7] J. Lee, “Inventory control by different service levels,”

AppliedMathematical Modelling, vol. 35, no. 1, pp. 497–505,

2011.

[8] X. Chen and D. Simchi-Levi, “Coordinating inventory

controland pricing strategies with random demand and fixed

orderingcost: the finite horizon case,”Operations Research, vol.

52, no. 6,pp. 887–896, 2004.

[9] X. Chen and D. Simchi-Levi, “Coordinating inventory

controland pricing strategies with random demand and fixed

orderingcost: the infinite horizon case,” Mathematics of

OperationsResearch, vol. 29, no. 3, pp. 698–723, 2004.

[10] J. Lee, “Dynamic pricing inventory control under fixed cost

andlost sales,” Applied Mathematical Modelling, vol. 38, no. 2,

pp.712–721, 2014.

[11] M. Güray Güler, T. Bilgiç, and R. Güllü, “Joint

pricing andinventory control for additive demand models with

referenceeffects,” Annals of Operations Research, vol. 226, no. 1,

pp. 255–276, 2015.

[12] S. Li, J. Zhang, and W. Tang, “Joint dynamic pricing

andinventory control policy for a stochastic inventory systemwith

perishable products,” International Journal of ProductionResearch,

vol. 53, no. 10, pp. 2937–2950, 2015.

[13] Y. Chen and C. Shi, “Joint pricing and inventory

managementwith strategic customers,” 2016.

[14] L. Feng, J. Zhang, andW. Tang, “Optimal inventory control

andpricing of perishable items without shortages,” IEEE

Transac-tions on Automation Science and Engineering, vol. 13, no.

2, pp.918–931, 2016.

[15] C. A. Yano and H. L. Lee, “Lot sizing with random yields:

areview,” Operations Research, vol. 43, no. 2, pp. 311–334,

1995.

[16] Y. Wang and Y. Gerchak, “Periodic review production

modelswith variable capacity, random yield, and uncertain

demand,”Management Science, vol. 42, no. 1, pp. 130–137, 1996.

[17] Q. Li and S. Zheng, “Joint inventory replenishment and

pricingcontrol for systems with uncertain yield and demand,”

Opera-tions Research, vol. 54, no. 4, pp. 696–705, 2006.

[18] X. Chao, H. Chen, and S. Zheng, “Joint replenishment

andpricing decisions in inventory systems with

stochasticallydependent supply capacity,” European Journal of

OperationalResearch, vol. 191, no. 1, pp. 142–155, 2008.

[19] P. Ignaciuk, “Discrete-time control of

production-inventorysystems with deteriorating stock and unreliable

supplies,” IEEETransactions on Systems, Man, and Cybernetics:

Systems, vol. 45,no. 2, pp. 338–348, 2015.

[20] L. Shu, F. Wu, J. Ni, and L. K. Chu, “On the

risk-averseprocurement strategy under unreliable supply,” Computers

&Industrial Engineering, vol. 84, pp. 113–121, 2015.

[21] B. Hu and D. Kostamis, “Managing supply disruptions

whensourcing from reliable and unreliable suppliers,” Production

andOperations Management, vol. 24, no. 5, pp. 808–820, 2015.

[22] K. Park and K. Lee, “Distribution-robust single-period

inven-tory control problem with multiple unreliable suppliers,”

ORSpectrum, 2016.

-

10 Mathematical Problems in Engineering

[23] F. Chen, “Market segmentation, advanced demand

information,and supply chain performance,”Manufacturing &

Service Oper-ations Management, vol. 3, no. 1, pp. 53–67, 2001.

[24] L. Li, “A stochastic theory of the firm,” Mathematics of

Opera-tions Research, vol. 13, no. 3, pp. 447–466, 1988.

-

Submit your manuscripts athttp://www.hindawi.com

Hindawi Publishing Corporationhttp://www.hindawi.com Volume

2014

MathematicsJournal of

Hindawi Publishing Corporationhttp://www.hindawi.com Volume

2014

Mathematical Problems in Engineering

Hindawi Publishing Corporationhttp://www.hindawi.com

Differential EquationsInternational Journal of

Volume 2014

Applied MathematicsJournal of

Hindawi Publishing Corporationhttp://www.hindawi.com Volume

2014

Probability and StatisticsHindawi Publishing

Corporationhttp://www.hindawi.com Volume 2014

Journal of

Hindawi Publishing Corporationhttp://www.hindawi.com Volume

2014

Mathematical PhysicsAdvances in

Complex AnalysisJournal of

Hindawi Publishing Corporationhttp://www.hindawi.com Volume

2014

OptimizationJournal of

Hindawi Publishing Corporationhttp://www.hindawi.com Volume

2014

CombinatoricsHindawi Publishing

Corporationhttp://www.hindawi.com Volume 2014

International Journal of

Hindawi Publishing Corporationhttp://www.hindawi.com Volume

2014

Operations ResearchAdvances in

Journal of

Hindawi Publishing Corporationhttp://www.hindawi.com Volume

2014

Function Spaces

Abstract and Applied AnalysisHindawi Publishing

Corporationhttp://www.hindawi.com Volume 2014

International Journal of Mathematics and Mathematical

Sciences

Hindawi Publishing Corporationhttp://www.hindawi.com Volume

2014

The Scientific World JournalHindawi Publishing Corporation

http://www.hindawi.com Volume 2014

Hindawi Publishing Corporationhttp://www.hindawi.com Volume

2014

Algebra

Discrete Dynamics in Nature and Society

Hindawi Publishing Corporationhttp://www.hindawi.com Volume

2014

Hindawi Publishing Corporationhttp://www.hindawi.com Volume

2014

Decision SciencesAdvances in

Discrete MathematicsJournal of

Hindawi Publishing Corporationhttp://www.hindawi.com

Volume 2014 Hindawi Publishing Corporationhttp://www.hindawi.com

Volume 2014

Stochastic AnalysisInternational Journal of