Embed Size (px)

Citation preview

aicpa.org/FRC

November 2011

AICPA Technical Practice Aids

TIS Section 9530, Service Organization Controls Reports .01 Reporting on Controls at a Service Organization Relevant to Subject Matter Other Than User Entities’ Internal Control Over Financial Reporting

Inquiry—Is authoritative guidance available for reporting under AT section 101, Attest Engagements (AICPA,

Professional Standards), on a service organization’s controls relevant to subject matter other than user

entities’ internal control over financial reporting (ICFR)?

Reply—Yes. The AICPA has developed an authoritative guide, Reporting on Controls at a Service Organization

Relevant to Security, Availability, Processing Integrity, Confidentiality, or Privacy (SOC 2) (SOC 2 guide), to

assist practitioners in reporting under AT section 101 on an examination of controls at a service organization

relevant to the security, availability, or processing integrity of a system or the confidentiality, or privacy of

the information processed by the system.

[Issue Date: November 2011.]

aicpa.org/FRC

.02 Service Organization Controls Reports

Inquiry—What does the acronym "SOC" stand for?

Reply—The acronym SOC stands for service organization controls, as in "service organization controls

reports." The AICPA introduced this term to make practitioners aware of the various professional standards

and guides available to them for examining and reporting on controls at a service organization relevant to

user entities and to help practitioners select the appropriate standard or guide for a particular engagement.

The following are the designations for the three engagements included in the SOC report series and the

source of the guidance for performing and reporting on them:

SOC 1: Statement on Standards for Attestation Engagements (SSAE) No. 16, Reporting on Controls at

a Service Organization (AICPA, Professional Standards, AT sec. 801), and AICPA Guide Service

Organizations: Applying SSAE No. 16, Reporting on Controls at a Service Organization (SOC 1)

SOC 2: AICPA Guide Reporting on Controls at a Service Organization Relevant to Security,

Availability, Processing Integrity, Confidentiality, or Privacy (SOC 2) and AT section 101

SOC 3: TSP section 100, Trust Services Principles, Criteria, and Illustrations for Security, Availability,

Processing Integrity, Confidentiality, and Privacy, and AT section 101

[Issue Date: November 2011.]

.03 Authority of SOC 1 and SOC 2 Guides

Inquiry—What is the authority of the SOC 1 and SOC 2 guides?

Reply—The SOC 1 and SOC 2 guides have been cleared by the AICPA’s Auditing Standards Board. AT section

50, SSAE Hierarchy (AICPA, Professional Standards), classifies attestation guidance included in an AICPA guide

as an interpretive publication and indicates that a practitioner should be aware of and consider interpretive

publications applicable to his or her examination. If a practitioner does not apply the attestation guidance

included in an applicable interpretive publication, the practitioner should be prepared to explain how he or

she complied with the SSAE provisions addressed by such attestation guidance.

[Issue Date: November 2011.]

aicpa.org/FRC

.04 SOC 3 Engagements

Inquiry—What is a SOC 3 engagement?

Reply—A SOC 3 engagement is similar to a SOC 2 engagement in that the practitioner reports on whether an

entity (any entity, not necessarily a service organization) has maintained effective controls over its system

with respect to security, availability, processing integrity, confidentiality, or privacy. Like a SOC 2

engagement, a SOC 3 engagement uses the criteria in TSP section 100. Unlike a SOC 2 engagement, a SOC 3

report (1) does not contain a description of the practitioner’s tests of controls and results of those tests and

(2) is a general-use report rather than a restricted use report. (The term general use refers to reports for

which use is not restricted to specified parties.)

[Issue Date: November 2011.]

.05 Types of Reports for SOC 2 Engagements

Inquiry—Are there type 1 and type 2 reports for SOC 2 engagements?

Reply—Yes. In a SOC 2 engagement, like a SOC 1 engagement, the practitioner has the option of providing

either a type 1 or a type 2 report. In both reports, management of the service organization prepares a

description of its system. In a type 1 report, the service auditor expresses an opinion on whether the

description is fairly presented (that is, does it describe what actually exists) and whether the controls

included in the description are suitability designed. Controls that are suitably designed are able to achieve

the related control objectives or criteria if they operate effectively. In a type 2 report, the service auditor’s

report contains the same opinions that are included in a type 1 report, and also includes an opinion on

whether the controls were operating effectively. Controls that operate effectively do achieve the control

objectives or criteria they were intended to achieve. Both SOC 1 and SOC 2 reports are examination reports,

which means the practitioner obtains a high level of assurance.

[Issue Date: November 2011.]

.06 Minimum Period of Coverage for SOC 2 Reports

Inquiry—Does the SOC 2 guide require that a type 2 report cover a minimum period?

Reply—The SOC 2 guide does not prescribe a minimum period of coverage for a SOC 2 report, however,

paragraph 2.09 of the SOC 2 guide states that one of the relevant factors to consider when determining

whether to accept or continue a SOC 2 engagement is the period covered by the report. The guide presents

an example of a service organization that wishes to engage a service auditor to perform a type 2 engagement

for a period of less than two months. The guide states that in those circumstances, the service auditor should

consider whether a report covering that period will be useful to users of the report, particularly if many of

the controls related to the applicable trust services criteria are performed on a monthly or quarterly basis. A

practitioner would use professional judgment in determining whether the report covers a sufficient period.

[Issue Date: November 2011.]

aicpa.org/FRC

.07 Placement of Management’s Assertion in a SOC 2 Report

Inquiry—In a SOC 2 engagement, does management’s assertion need to accompany the service

organization’s description of its system?

Reply—Paragraph 2.13(b) of the SOC 2 guide states, in part, that a service auditor ordinarily should accept or

continue an engagement to report on controls at a service organization only if management of the service

organization acknowledges and accepts responsibility for "providing a written assertion that will be attached

to management’s description of the service organization’s system and provided to users." The

recommendation in the SOC 2 guide is that the assertion be attached to the description rather than included

in the description to avoid the impression that the practitioner is reporting on the assertion rather than on

the subject matter.

[Issue Date: November 2011.]

.08 Illustrative Assertion for Management of a Service Organization in a SOC 2 Engagement

Inquiry—Where can I find an illustrative management assertion for a SOC 2 engagement?

Reply—Appendix C, "Illustrative Management Assertions and Related Service Auditor’s Reports on Controls at

a Service Organization Relevant to Security, Availability, Processing Integrity, Confidentiality, and Privacy," of

the SOC 2 guide contains illustrative assertions by management of a service organization for type 2 SOC 2

engagements.

[Issue Date: November 2011.]

.09 Illustrative Assertion for Management of a Subservice Organization in a SOC 2 Engagement

Inquiry—The SOC 2 guide contains illustrative management assertions for management of a service

organization. Is an illustrative assertion for management of a subservice organization available in the SOC 2

guide?

Reply—No. However, the illustrative assertions in appendix C of the SOC 2 guide can be used to construct the

subservice organization’s assertion. Paragraphs 2.13–2.15 of the SOC 2 guide address the requirement for an

assertion by management of a subservice organization when the inclusive method is used.

[Issue Date: November 2011.]

aicpa.org/FRC

.10 Management of a Subservice Organization Refuses to Provide a Written Assertion in a SOC 1 or SOC 2 Engagement

Inquiry—When using the inclusive method, if management of a subservice organization will not provide a

written assertion, what should the service auditor do?

Reply—Paragraph .A8 of AT section 801 indicates that the subservice organization’s refusal to provide the

service auditor with a written assertion precludes the service auditor from using the inclusive method.

However, the service auditor may instead use the carve-out method. Paragraph 2.15 of the SOC 2 guide

contains similar guidance for SOC 2 engagements.

[Issue Date: November 2011.]

.11 Determining Whether Management of a Service Organization Has a Reasonable Basis for Its Assertion (SOC 1 and SOC 2 Engagements)

Inquiry—Paragraph .09(c)(ii) of AT section 801 states that one of the requirements for a service auditor to

accept or continue a type 1 or type 2 engagement is that management acknowledge and accept responsibility

for having a reasonable basis for its assertion. Paragraph .A17 of AT section 801 indicates that the service

auditor’s report on controls is not a substitute for the service organization’s own processes to provide a

reasonable basis for its assertion. How does the service auditor determine whether management has a

reasonable basis for its assertion?

Reply—AT section 801 indirectly describes how the service auditor makes this determination. First, paragraph

.14(a)(vii) of AT section 801 indicates, in part, that the service organization’s description of its system should

include the service organization’s monitoring activities. Because a service auditor is required to determine

whether the description is fairly stated, in doing so the service auditor would determine whether the section

of the description that describes monitoring controls is fairly stated. Second, paragraph .A17 of AT section

801, shown subsequently, defines the term monitoring of controls and indicates that management’s

monitoring activities may provide evidence of the design and operating effectiveness of controls in support of

management’s assertion. Similar guidance for SOC 2 engagements is included in appendix A, "Information for

Management of a Subservice Organization," of the SOC 2 guide, in the section titled "Providing a Written

Assertion."

[Issue Date: November 2011.]

aicpa.org/FRC

.12 Reasonable Basis for Management of a Subservice Organization’s Assertion (SOC 1 and SOC 2 Engagements)

Inquiry—In an inclusive SOC 1 engagement, is the service auditor required to determine whether

management of the subservice organization has a reasonable basis for its assertion?

Reply—Paragraph .09(c)(ii) of AT section 801 states that one of the requirements for a service auditor to

accept or continue a type 1 or type 2 engagement is that management acknowledge and accept responsibility

for having a reasonable basis for its assertion. Paragraph .A7 of AT section 801 states that when the inclusive

method is used, the requirements of AT section 801 also apply to the services provided by the subservice

organization, including the requirement to acknowledge and accept responsibility for the matters in

paragraph .09(c)(i)–(vii) of AT section 801 as they relate to the subservice organization. Paragraph .09(c)(vii)

requires a service organization to provide a written assertion; therefore, a subservice organization would also

be required to provide a written assertion and have a reasonable basis for its assertion.

In determining whether a subservice organization has a reasonable basis for its assertion, the service auditor

would analogize the requirements and guidance in AT section 801 to the subservice organization. Paragraph

.14(a)(vii) of AT section 801 would require that the subservice organization’s description of its system include

the subservice organization’s monitoring activities. Because a service auditor is required to determine

whether the subservice organization’s description is fairly stated, in doing so the service auditor would

determine whether the section of the description that describes monitoring controls is fairly stated.

Paragraph .A17 of AT section 801 defines the term monitoring of controls and indicates that management’s

monitoring activities may provide evidence of the design and operating effectiveness of controls in support of

management’s assertion. Similar guidance on this topic for a SOC 2 engagement is included in paragraphs

2.13(b)–(c) and 2.15 of the SOC 2 guide.

[Issue Date: November 2011.]

.13 Point in a SOC 1 or SOC 2 Engagement When Management Should Provide Its Written Assertion

Inquiry—At what point in a SOC 1 or SOC 2 engagement should management provide the service auditor with

its written assertion?

Reply—Management may provide its written assertion to the service auditor at any time after the end of the

period covered by the service auditor’s type 2 report and, for a type 1 report, at any time after the as of date

of the type 1 report. The date of the service auditor’s report should be no earlier than the date on which

management provides its written assertion.

[Issue Date: November 2011.]

aicpa.org/FRC

.14 Implementing Controls Included in Management’s Description of the Service Organization’s System (SOC 1 and SOC 2 Engagements)

Inquiry—In a type 1 report for a SOC 1 or SOC 2 engagement, do the controls included in management’s

description of the service organization’s system need to be implemented?

Reply—Yes. In order for the description of the service organization’s system to be fairly presented, the

controls included in the description would have to be placed in operation (implemented). See paragraph

4.01(b) of the SOC 1 guide and paragraph 3.13 of the SOC 2 guide.

[Issue Date: November 2011.]

.15 Responsibility for Determining Whether a SOC 1, SOC 2, or SOC 3 Engagement Should Be Performed

Inquiry—Who determines whether a SOC 1, SOC 2, or SOC 3 engagement should be performed—the service

auditor or management of the service organization?

Reply—SOC 1 engagements address a service organization’s controls relevant to user entities’ ICFR, whereas

SOC 2 and SOC 3 engagements address a service organization’s controls relevant to the security, availability,

or processing integrity of a system or the confidentiality or privacy of the information the system processes.

In SOC 2 and SOC 3 engagements, the service auditor uses the criteria in TSP section 100 for evaluating and

reporting on controls relevant to the security, availability, or processing integrity of a system, or the

confidentiality or privacy of the information processed by the system. In TSP section 100, these five attributes

of a system are known as principles. A service auditor may be engaged to report on a description of a service

organization’s system and the suitability of the design and operating effectiveness of controls relevant to one

or more of the trust services principles The criteria in TSP section 100 that are applicable to the principle(s)

being reported on are known as the applicable trust services criteria.

If management of the service organization is not knowledgeable about the differences among these three

engagements, the service auditor may assist management in obtaining that understanding and selecting the

appropriate engagement. Determining which engagement is appropriate depends on the subject matter

addressed by the controls and the risk management and governance needs of the user entities, and it often

involves discussion with the user entities regarding their needs.

[Issue Date: November 2011.]

aicpa.org/FRC

.16 Criteria for SOC 2 and SOC 3 Engagements

Inquiry—Are there a prescribed set of control objectives for SOC 2 and SOC 3 engagements?

Reply—In SOC 1 engagements, the service auditor determines whether controls achieve specified control

objectives. In SOC 2 and SOC 3 engagements, the service auditor determines whether controls meet the

applicable trust services criteria. Although the terminology is different in these engagements (control

objectives versus criteria), the control objectives in a SOC 1 engagement serve as criteria for evaluating the

design and, in a type 2 report, the operating effectiveness of controls. Unlike SOC 1 engagements, in which

management of the service organization determines the service organization’s control objectives based on

the nature of the service provided and how the service is performed, in all SOC 2 and SOC 3 engagements,

the service organization’s controls must meet all of the criteria in TSP section 100 that are applicable to the

principle(s) being reported on. The applicable trust services criteria serve as a prescribed set of criteria.

[Issue Date: November 2011.]

.17 Using Existing Set of Controls for a New SOC 2 or SOC 3 Engagement

Inquiry—In the past, many IT service organizations provided their user entities with SAS No. 70 reports (SAS

No. 70, Service Organizations [AICPA, Professional Standards, AU sec. 324]), covering the IT services. If a

service organization plans to undergo a SOC 2 or SOC 3 examination for the first time and has a fully defined

set of controls and control objectives related to its IT services, does the service organization need to adopt a

new set of controls to meet the applicable trust services criteria?

Reply—The SOC 2 guide and appendix C of TSP section 100 require the service organization to establish

controls that meet all of the applicable trust services criteria. A service organization that is planning to

undergo a SOC 2 or SOC 3 engagement for the first time may have controls in place that address all of the

applicable trust services criteria. However, the service organization will need to determine whether its

existing control objectives align with the applicable trust services criteria and whether its controls address all

of the applicable trust services criteria. If not, it will need to implement or revise certain controls to meet all

of the applicable trust services criteria.

[Issue Date: November 2011.]

aicpa.org/FRC

.18 Reporting on Compliance With Other Standards or Requirements in SOC 2 or SOC 3 Engagements

Inquiry—May a SOC 2 or SOC 3 report cover compliance with other standards or authoritative requirements

that are substantially similar to the applicable trust services criteria, for example, requirements in Special

Publication 800-53, Recommended Security Controls for Federal Information Systems, issued by the National

Institute of Standards and Technology (NIST) or in Payment Card Industry (PCI) Security Standards issued by

the PCI Security Counsel?

Reply—Yes. A service organization may request that a SOC 2 or SOC 3 report address additional subject

matter that is not specifically covered by the applicable trust services criteria. An example of such subject

matter is the service organization’s compliance with certain criteria established by a regulator, for example,

security requirements under the Health Insurance Portability and Accountability Act of 1996 or compliance

with performance criteria established in a service-level agreement. Paragraph 1.38 of the SOC 2 guide states

that in order for a service auditor to report on such additional subject matter, the service organization

provides the following:

An appropriate supplemental description of the subject matter

A description of the criteria used to measure and present the subject matter

If the criteria are related to controls, a description of the controls intended to meet the control-

related criteria

An assertion by management regarding the additional subject matter

Paragraph 1.39 of the guide states

The service auditor should perform appropriate procedures related to the additional subject matter, in

accordance with AT section 101 and the relevant guidance in this guide. The service auditor’s description

of the scope of the work and related opinion on the subject matter should be presented in separate

paragraphs of the service auditor’s report. In addition, based on the agreement with the service

organization, the service auditor may include additional tests performed and detailed results of those

tests in a separate attachment to the report.

[Issue Date: November 2011.]

.19 Issuing Separate Reports When Performing Both a SOC 1 and SOC 2 Engagement for a Service Organization

Inquiry—Going forward, will service organizations that include control objectives relevant to user entities

ICFR along with control objectives that are not relevant to user entities’ ICFR in their descriptions need to

request two separate reports—SOC 1 and SOC 2?

Reply—Yes. Service organizations will now need to request two separate SOC reports if the service

organization would like to address control objectives relevant to user entities’ ICFR and control objectives

(criteria) that are not relevant to user entities’ ICFR. See paragraph 1.23 of the SOC 2 guide.

[Issue Date: November 2011.]

aicpa.org/FRC

.20 Deviations in the Subject Matter (SOC 1 and SOC 2 Engagements)

Inquiry—In a SOC 1 or SOC 2 engagement, if the service auditor identifies deviations in the subject matter

(that is, the fairness of the presentation of the description, the suitability of the design of the controls, and

the operating effectiveness of the controls) and qualifies the report because of these deviations, does

management need to revise its assertion to reflect these deviations?

Reply—If management of the service organization agrees with the service auditor’s findings regarding the

deviations, management would be expected to revise its assertion to reflect the deviations identified in the

service auditor’s report. If management does not revise its assertion, the service auditor should add an

explanatory paragraph to the report indicating that the deficiencies identified in the service auditor’s report

have not been identified in management’s assertion. Similar guidance for a SOC 2 engagement is included in

paragraph 3.105 of the SOC 2 guide.

[Issue Date: November 2011.]

.21 Use of a Seal on a Service Organization’s Website

Inquiry—Will there be a SOC seal that can be displayed on a service organization’s website indicating that the

service organization has undergone a SOC1, SOC 2, or SOC 3 engagement?

Reply—A seal is available only for SOC 3 engagements. A SOC 3 SysTrust for Service Organization Seal (seal)

may be issued and displayed on a service organization's website. All practitioners who wish to provide this

registered seal must be licensed by the Canadian Institute of Chartered Accountants (CICA). Typically the seal

is linked to the report issued by the practitioner. For more information on licensure, go to

http://www.webtrust.org. It is important to note that a practitioner can perform a SOC 3 engagement and

issue a SOC 3 report without issuing a SOC 3 seal. In such cases the practitioner does not need to be licensed

by the CICA. The license is only for the issuance of a seal.

In addition, SOC logos are available for use by (a) CPAs for marketing and promoting SOC services and (b)

service organizations that have undergone a SOC 1, SOC 2, or SOC 3 engagement within the prior 12 months.

These logos are designed to make the public aware of these SOC services and do not offer or represent

assurance that an organization obtained an unqualified (or clean) opinion. For additional information about

logos, go to http://www.aicpa.org/interestareas/frc/assuranceadvisoryservices/pages/soclogosinfo.aspx.

[Issue Date: November 2011.]

aicpa.org/FRC

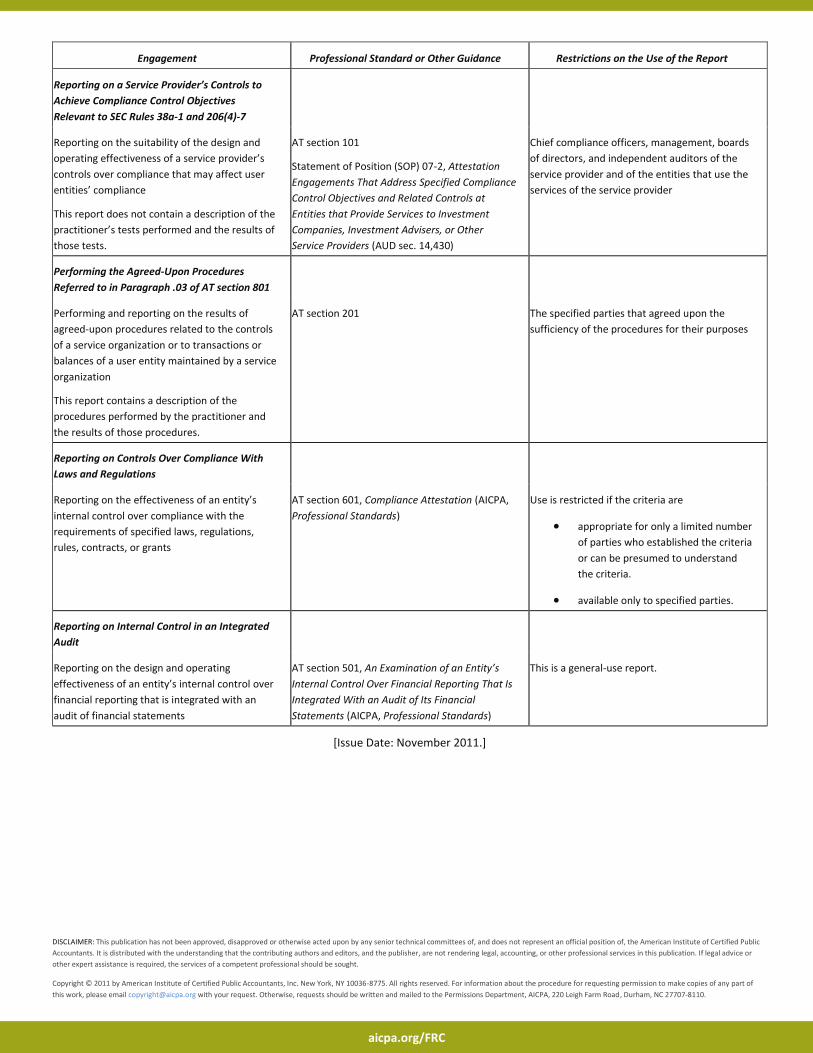

.22 Attestation Standards and Interpretive Guidance for Reporting on a Service Organization’s Controls Relevant to User Entities and for Reporting on an Entity’s Internal Control

Inquiry—AICPA professional literature includes a variety of attestation standards and interpretive guidance

for reporting on a service organization’s controls relevant to user entities and for reporting on an entity’s

internal control. How does a practitioner determine the applicable attestation standard and interpretive

guidance for these engagements?

Reply—The following table identifies a variety of attestation engagements that involve reporting on a service

organization’s controls relevant to user entities, or reporting on an entity’s internal control. The table also

identifies the appropriate attestation standard or interpretive guidance to be used in the circumstances.

Engagement Professional Standard or Other Guidance Restrictions on the Use of the Report

Reporting on Controls at a Service

Organization Relevant to User Entities’

Internal Control Over Financial Reporting:

Controls were not designed by the service

organization; management of the service

organization will not provide an assertion

regarding the suitability of the design of the

controls

Reporting on

the fairness of the presentation of

management’s description of the

service organization’s system and

Report on the fairness of the presentation of the

description under AT section 101, Attest

Engagements (AICPA, Professional Standards),

using the description criteria in paragraph .14 of

AT section 801, Reporting on Controls at a

Service Organization (AICPA, Professional

Standards), and adapting the relevant

requirements and guidance therein

Management of the service organization, user

entities, and the auditors of the user entities’

financial statements

the operating effectiveness of the

service organization’s controls

relevant to user entities internal

control over financial reporting. Such

a report may include a description of

tests of the operating effectiveness of

the controls and the results of the

tests.

Report on the operating effectiveness of controls

under AT section 101 or AT section 201, Agreed-

Upon Procedures Engagements (AICPA,

Professional Standards)

The specified parties that agreed upon the

sufficiency of the procedures for their purposes

Reporting on Controls at a Service Organization

Relevant to User Entities’ Internal Control Over

Financial Reporting: Controls were not

designed by the service organization;

management of the service organization

provides an assertion regarding the suitability

of design of controls

AT section 801 Management of the service organization, user

entities, and the auditors of the user entities’

financial statements

aicpa.org/FRC

Engagement Professional Standard or Other Guidance Restrictions on the Use of the Report

Reporting on Controls at a Service Organization

Relevant to Security Availability, Processing

Integrity, Confidentiality, or Privacy: Includes

Description of Tests and Results

Reporting on the fairness of the presentation of

management’s description of a service

organization’s system; the suitability of the

design of controls at a service organization

relevant to security, availability, processing

integrity, confidentiality, or privacy; and in a

type 2 report, the operating effectiveness of

those controls

A type 2 report includes a description of tests of

the operating effectiveness of controls

performed by the service auditor and the results

of those tests.

AT section 101

AICPA Guide Reporting on Controls at a Service

Organization Relevant to Security, Availability,

Processing Integrity, Confidentiality, or Privacy

(SOC 2)

Parties that are knowledgeable about

the nature of the service provided by

the service organization

how the service organization’s system

interacts with user entities,

subservice organizations, and other

parties

internal control and its limitations

the criteria and how controls address

those criteria

complementary user entity controls

and how they interact with related

controls at the service organization

Reporting on Controls at a Service Organization

Relevant to Security Availability, Processing

Integrity, Confidentiality, or Privacy: No

Description of Tests and Results

Reporting on whether an entity has maintained

effective controls over its system with respect to

security, availability, processing integrity,

confidentiality, or privacy

If the report addresses the privacy principle, the

report also contains an opinion on the service

organization’s compliance with the

commitments in its privacy notice.

This report does not contain a description of the

service auditor’s tests performed and the results

of those tests.

AT section 101

AICPA/Canadian Institute of Chartered

Accountants Trust Services Principles, Criteria,

and Illustrations (TSP section 100, Trust Services

Principles, Criteria, and Illustrations for Security,

Availability, Processing Integrity, Confidentiality,

and Privacy)

This is a general-use report.1

1 The term general use refers to reports for which use is not restricted to specified parties.

aicpa.org/FRC

Engagement Professional Standard or Other Guidance Restrictions on the Use of the Report

Reporting on a Service Provider’s Controls to

Achieve Compliance Control Objectives

Relevant to SEC Rules 38a-1 and 206(4)-7

Reporting on the suitability of the design and

operating effectiveness of a service provider’s

controls over compliance that may affect user

entities’ compliance

This report does not contain a description of the

practitioner’s tests performed and the results of

those tests.

AT section 101

Statement of Position (SOP) 07-2, Attestation

Engagements That Address Specified Compliance

Control Objectives and Related Controls at

Entities that Provide Services to Investment

Companies, Investment Advisers, or Other

Service Providers (AUD sec. 14,430)

Chief compliance officers, management, boards

of directors, and independent auditors of the

service provider and of the entities that use the

services of the service provider

Performing the Agreed-Upon Procedures

Referred to in Paragraph .03 of AT section 801

Performing and reporting on the results of

agreed-upon procedures related to the controls

of a service organization or to transactions or

balances of a user entity maintained by a service

organization

This report contains a description of the

procedures performed by the practitioner and

the results of those procedures.

AT section 201 The specified parties that agreed upon the

sufficiency of the procedures for their purposes

Reporting on Controls Over Compliance With

Laws and Regulations

Reporting on the effectiveness of an entity’s

internal control over compliance with the

requirements of specified laws, regulations,

rules, contracts, or grants

AT section 601, Compliance Attestation (AICPA,

Professional Standards)

Use is restricted if the criteria are

appropriate for only a limited number

of parties who established the criteria

or can be presumed to understand

the criteria.

available only to specified parties.

Reporting on Internal Control in an Integrated

Audit

Reporting on the design and operating

effectiveness of an entity’s internal control over

financial reporting that is integrated with an

audit of financial statements

AT section 501, An Examination of an Entity’s

Internal Control Over Financial Reporting That Is

Integrated With an Audit of Its Financial

Statements (AICPA, Professional Standards)

This is a general-use report.

[Issue Date: November 2011.]

DISCLAIMER: This publication has not been approved, disapproved or otherwise acted upon by any senior technical committees of, and does not represent an official position of, the American Institute of Certified Public

Accountants. It is distributed with the understanding that the contributing authors and editors, and the publisher, are not rendering legal, accounting, or other professional services in this publication. If legal advice or

other expert assistance is required, the services of a competent professional should be sought.

Copyright © 2011 by American Institute of Certified Public Accountants, Inc. New York, NY 10036-8775. All rights reserved. For information about the procedure for requesting permission to make copies of any part of

this work, please email [email protected] with your request. Otherwise, requests should be written and mailed to the Permissions Department, AICPA, 220 Leigh Farm Road, Durham, NC 27707-8110.