Embed Size (px)

Citation preview

REPORT OF THE AUDIT OF THE LIVINGSTON COUNTY

FISCAL COURT

For The Fiscal Year Ended June· 30, 2006 ·

EXECUTIVE SUMMARY

AUDIT EXAMINATlON OF THE LIVINGSTON COUNTY FISCAL COURT

June 30, 2006

Romaine & Associates, PLLC has completed the audit of the Livingston County Fiscal Court for fiscal year ended June 30, 2006. We have issued an unqualified opinion, on the governmental activities, business-type activities, each major fund, and aggregate remaining fund information financial statements of Livingston County, Kentucky.

Financial Condition:

The county had net assets of $6,736,392 as of June 30, 2006. The county had unrestricted net assets of $2,385,590 in its governmental activities as of June 30, 2006, with total net assets of $6,728,543. In its business-type activities, total cash and cash equivalents were $2,169 with total net assets of $7,849.

Deposits:

The county's deposits were insured and collateralized by bank securities.

~ONTENTS PAGE

INDEPENDENT AUDITOR'S REPORT ......................................................................................................... 1

LIVINGSTON COUNTY OFFICIALS ............................................................................................................ 3

STATEMENT OF NET ASSETS MODIFIED CASH BAsiS ................... ; ................................................................. 5

STATEMENT OF ACTIVITIES - MODIFIED CASH BASIS ...................................................................................... 7

BALANCE SHEET- GOVERNMENTAL fuNDS - MODIFIED CASH BASIS ..•.•.••..••.•.•.•••..••.••...•..•.......••..•...•••••.••••....•. 10

STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES

IN FuND BALANCES- GOVERNMENTAL FuNDS- MODIFIED CASH BASIS ............................................................. 13

RECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES, AND

CHANGES IN FuND BALANCES OF GOVERNMENTAL FUNDS TO THE

STATEMENT OF ACTIVITIES- MODIFIED CASH BASIS .. ~ ......... ; ..... , ................................................................... 16

STATEMENT OF NET ASSETS- PROPRIETARY FuND- MODIFIED CASH BASIS ....................................................... 18

STATEMENT OF REVENUES, EXPENSES, AND CHANGES IN FuND NET ASSETS-

PROPRIETARYFuND MODIFIEDCASHBASIS ................................................................................................ 20

STATEMENT OF CASH FLOWS PROPRIETARY FuND- MODIFIED CASH BASIS ...................................................... 22

NOTES TO FINANCIAL STATEMENTS ....................................................................................................... 25

BUDGETARY COMPARISON SCHEDULES ..•.•.....•...•...••..•••.....•.•..•..•.......•.....••..•.••...•.•.......•........•...............•...... 3 9

NOTES TO REQUIRED SUPPLEMENTARY INFORMATION~ .......................................................................... 43

COMBINING BALANCE SHEET-

NON-MAJOR GOVERNMENTAL FUNDS- MODIFIED CASH BASIS ......................................................................... 45

COMBINING STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES

IN FuND BALANCES- NON-MAJOR GOVERNMENTAL FUNDS - MODIFIED CASH BASIS ........................................... 4 7

REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND

ON COMPLIANCE AND OTHER MA TIERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS

PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDHING STANDARDS ............................................ 49

APPENDIX A:

CERTIFICATION OF COMPLIANCE LOCAL GOVERNMENT ECONOMIC ASSISTANCE PROGRAM

't:.,·

Krista Romaine, CPA, Member Charlotte Clark, Member

'

. '. ssocwtes p££c

CERTIFIED PUBLIC ACCOUNTANTS

To the People of Kentucky Honorable Emie Fletcher, Govemor Jolm R. Farris, Secretary Finance and Administration Cabinet Honorable ChristopherK. Lasher, Livingston County Judge/Executive Members of the Livingston Cmmty FiscaLCourt

h1dependent Auditor's Report

William Erwin, CPA Van R. Prince, CPA

We have audited the accompanying financial statements of the govemrnental activities, the businesstype activities, each major fund, and the aggregate remaining fund information of Livingston County, Kentucky, as of and for the year ended June 30, 2006, which collectively comprise the County's basic financial statements, as listed in the table of contents. These financial statements are the responsibility of the. Livingston County Fiscal Court. Our responsibility is to express opinions on these fmancial statements based on our audit.

We conducted our audit in accordance with auditing standards generally accepted in the United States of Ame1ica, the standards applicable to fmancial audits contained in Govemrnent Auditing Standards issued by the Comptroller General of the United States, and the Audit Guide for Fiscal Court Audits issued by the Auditor of Public Accounts, Co11llllonwealth of Kentucky. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the fmancial statements are free of material misstatement. ·An audit includes exarn:i:n:i:ng, on a test basis, evidence suppmiing the an1ol.1nts and disclosures :in the fmancial statements. An audit also includes assessing the accounting prinCiples used and significant estimates ·made QY management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinions.

As described in Note 1, Livingston County, Kentucky, prepares its financial statements on a prescribed basis . of accounting that demonstrates complia,nce . with the modified cash basis, which is a comprehensive basis of account:ing other :than accounting principles generally accepted in the United States of Ame1ica.

In our op:inion, the fmancial statements refened to above present fairly, in all material respects, the respective financial .position of the govemmental activities, the business-type activities, each major fm1d, and the aggregate remaining fund infonnat:i:on of Livingston County, Kentucky, as of June 30, 2006, and the respective changes in fmancial position and cash flows, where applicable, thereof for the year then ended in confomlity with the basis of accounting described in Note 1.

The county has not presented the managemenfs discus~ion ·and analysis that the Govermnenta1 Accounting Standards Board (GASB) has detennined is necessary to supplement, although not required to be part of the basic financial statement. The budgetary comparison information is not a required pa.rt of the basic financial statements but is supplementary infom1ation required by the Govenm1ental Accounting Standards Board. We have applied certain lin:rited proc:::dures, which consisted principally of inquiries of management regarding the methods of measurement and presentation of the budgetary comparison info:·rx_·::cm. Hmvever, we did nm audit the :i:nfonnation and express no opinion 011 it.

s Road- Suite 341 -P.O. Box 488- Mayfield, Kentucky 42066 Phone: 270-247-8050 Fax: 270-247-7749

AICPA KSCPA TSCPA

To the People of Kentucky Honorable Ernie Fletcher, Governor John R. Farris, Secretary Finance and Administration Cabinet Honorable Christopher K. Lasher, Livingston County Judge/Executive Members of the Livingston County Fiscal Court

Page 2

Our audit was conducted for the purpose of forming opmwns on the financial statements that collectively comprise Livingston County,. Kentucky's basic fmancial statements. The accompanying supplementary information, combining ·fund financial statements, are presented for purpose of additional analysis and are not a required part of the basic fmancial statements. The combining fund financial statements have been subjected to the auditing procedures applied in the audit of the basic financial statements and, in our opinion, are fairly stated in all material respects in relation of the basic financial statements taken as a whole.

In accordance with Government Auditing Standards, we have also issued our report dated June 12, 2007 on our consideration of Livingston County, Kentucky's internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose ofthat report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards and should be considered in assessing the results of our audit.

June 12, 2007

Respectfully submitted,

Krista L Romaine, CPA Romaine & Associates, PLLC

Fiscal Court Members:

Christopher K. Lasher

Terry Stringer

William "Jerry" Deatherage

Ivus Crouch

Delmer Joe O'Bryan

Other Elected Officials:

Billy N. Riley

Benjamin Guill

Carroll D. Walker

Jackie Doom

Tommy Williams

Sue Ann Carver

Jeff Armstrong

Appointed Personnel:

Tracie Belcher

Tracy Mitchell

TanaDoom

Cindy Mifflin

Paul Quertermous

Hershel Evans

Debbie Willbanks

LIVINGSTON COUNTY OFFICIALS

For 1)1eYear EndedJune 30, 2006

County Judge/Executive

Magistrate

Magistrate

. Magistrate

Magistrate

County Attorney

Jailer*

County Clerk

Circuit Court Clerk

Sheriff

Property Valuation Administrator

Coroner

County Treasurer

Occupational Tax Collector

Finance Officer

Human Resource

Road Supervisor

911 Administrator

Jail Administrative Assistant

*The Livingston County Jail discontinued housing inmates as of May 16,2005.

LIVINGSTON COUNTY. STATEMENT OF NET ASSETS- MODIFIED CASH BASIS

June 30, 2006

Page 5 LIVINGSTON COUNTY

STATEMENT OF NET ASSETS~ MODIFIED CASH BASIS

June 30, 2006

Primary Government Governmental Business~ Type

Activities Activities Totals ASSETS Current Assets:

Cash and Cash Equivalents $ 2,385,590 $ 2,169 $ 2,387,759 Notes Receivable 80,000 80,000

Total Current Assets 2,465,590 2,169 2,467,759

Noncurrent Assets: Note Receivable $ 4,173,000 $ $ 4,173,000 Land & Land Improvement 989,514 989,514 Capital Assets -Net of Accumulated

Depreciation Buildings 1,041,330 1,041,330 Vehicles and Equipment 1,292,7'2:6- 5,680 1,298,406

Infrastructure Assets -Net of Depreciation 1,019,383 1,019,383

Total Noncurrent Assets 8,515,953 5,680 8,521,633 Total Assets 10,981,543 7,849 10,989,392

LIABILITIES Current Liabilities:

Financing Obligations Payable 80,000 80,000 Total Current Liabliities ··. 80,000 80,000

Noncurrent Liabilities Financing Obligations Payable 4,173,000 4,173,000

Total Noncurrent Liabilities 4,173,000 4,173,000 Total Liabilities 4;253,000 4,253,000

NET ASSETS Invested in Capital Assets,

Net of Related Debt $ 4,342,953 . $ 5,680 $ 4,348,633 Unrestricted 2,385,590 2,169 2,387,759

Total Net Assets $ 6,728,543 $ 7,849 $ 6,736,392

The accompanying notes are an integral part of the financial statements.

LIVINGSTON-COUNTY STATEMENT OF ACTIVITIES- MODIFIED CASH BASIS

For The Year Ended June 30, 2006

Page 7 LIVINGSTON COUNTY

STATEMENT OF ACTIVITIES- MODIFIED CASH BASIS

For The Year Ended June 30,2006

Functions/Programs Expenses·

Governmental Activities:

General Government $ 1,369,459

Protection to Persons and Property 1,256,047

General Health and Sanitation 159,062

Social Services 60,270

Recreation and Culture 34,507

Roads 678,428

Interest on short-term debt 7,465

Total Governmental Activities 3,565,238

Business-type Activities:

Jail Canteen 895 Total Business-type Activities 895

Total Primary Government $ 3,566,133

Program Revenues Received

Operating

Charges for Grants and

Services Contributions

$ 17,915 $

342,862

49,865

100

410,742

$ 410,742 $

General Revenues: Taxes:

Real Property Taxes

Motor Vehicle Taxes

Occupational Taxes

In-Lieu-ofT ax

Other Taxes

Excess Fees

Miscellaneous Revenues

Interest Received

Total General Revenues

Change in Net Assets

Net Assets -Beginning

Net Assets - Ending

218,579

62,652

986,560

1,267,791

1,267,791

Capital

Grants and

Contributions

$

644,355

644,355

$ 644,355

The accompanying notes are an integral part of the financial statements.

LIVINGSTON COUNTY STATEMENT OF ACTIVITIES- MODIFIED CASH BASIS For The Year Ended June 30, 2006 (Continued)

Net (Expenses) Revenues and Changes in Net Assets

Primary Government

$

$

Governmental Activities

(1, 132,965) $

(850,533)

(109, 197)

(60,270)

(34,507)

952,587

(7,465)

(1,242,350)

(1,242,350) $

405,652

55,485

900,646

236,432

226,976

36,110

454,341

81,468

2,397,110

1,154,760

5,573,783

$ 6,728,543 $

Business-Type Activities

(895)

(895)

$

Totals

(1,132;965). ... (850,533)

(109,197)

(60,270)

(34,507)

952,587

(7,465)

(1,242,350)

(895)

(895)

(895) _$ __ (.:....1';_24_3,;_,2_45.:..)

405,652

55,485

900,646

236,432

226,976

36,110

454,341

. 81,468

2,397,110

(895) 1,153,865

8,744 5,582,527

7,849 $ 6,736,392

The accompanying notes are an integral part of the financial statements.

Page 8

LIVINGSTON COUNTY BALANCE SHEET- GOVERNMENTAL FUNDS- MODIFIED CASH BASIS

June 30, 2006

Page 10

LIVINGSTON COUNTY BALANCE SHEET- GOVERNMENTAL FUNDS- MODIFIED CASH BASIS

June 30, 2006

Occupational General Road LGEA Tax

Fund Fund Fund Fund ASSETS

Cash and Cash Equivalents $ 394,371 $ 528,738 $ 692,080 $ 731,614 Total Assets 394,371 528,738 692,080 731,614

FUND BALANCES Reserved for:

Encumbrances 14,486 46,534 8,176 738 Unreserved:

General Fund 379,885 Special Revenue Funds 482,204 683,904 730,876

Total Fund Balances $ 394,371 $ 528,738 $ 692,080 $ 731,614

The accompanying notes are an integral part of the financial statements.

$

$

:iSTON COUNTY llCE SHEET- GOVERNMENTAL FUNDS -MODIFIED CASH BASIS 0, 2006 nued)

Non-Major Funds

38,787 38,787

7,147

31,640

Total Governmental

$

Funds

2,385,590 2,385,590

77,081

379,885 1,928,624

3 8, 78 7 =$==2=,3::::85=,5=9=0=

Total Fund Balances Amounts Reported For Governmental Activities In The Statement

Of Net Assets Are Different Because: Notes Receivable Used in Governmental Activities Are Not Financial Resources Capital Assets Used in Governmental Activities Are Not Financial Resources

And Therefore Are Not Reported in the Funds.

AccumU:Iaied Depreciation . . . Long-term debt is not due and payable in the current period and, therefore, is not

reported in the funds. Financing Obligations Payable

Net Assets Of Governmental Activities

$

$

The accompanying notes are an integral part of the financial statements.

Page 11

2,385,590

4,253,000

5,654,906 (1,31 1,953)

(4,253,000)

6,728,543

LIVINGSTON COUNTY STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES

IN FUND BALANCES- GOVERNMENTAL FUNDS- MODIFIED CASH BASIS . .

For The Year Ended June JO, 2006

Page 13 LIVINGSTON COUNTY

STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES- GOVERNMENTAL FUNDS- MODIFIED CASH BASIS

For The Year Ended June 30,2006

Occupational General Road LGEA Tax

Fund Fund Fund Fund

REVENUES Taxes $ 650,411 $ $ 34,748 $ 900,646 In Lieu Tax Payments 236,432 Excess Fees 36,110 Licenses and Permits 17,915 50 Intergovernmental 2i4,106 1,253,254 380,479 10,017 Charges for Services 21,021 50 301,216 Miscellaneous 43,734 39,807 339,704 37,740 Interest 22,902 22,476 13,624 22,004

Total Revenues 1,242,631 I ,315,587 768,605 1,271,623

EXPENDITURES General Government $ 4,787,004 $ $ 60,641 $ 50,567 Protection to Persons and Property 48,527 .. 16,118 773,022 General Health and Sanitation 20,417 23,887 91,871 17,865 Social Services 5,190 43,972 Recreation and Culture 10,872 20,357 Roads 442,521 58,469 Capital Outlay 92,514 547,143 67,610 135,520 Debt Service 6,786 679 Administration 372,913 228,416 4,786

Total Expenditures 5,344,223 1,242,646 363,824 976,974

Excess (Deficiency) of Revenues Over Expenditures Before Other Financing Sources (Uses) (4, 101 ,592) 72,941 404,781 294,649

Other Financing Sources (Uses) Financing Obligation Proceeds 4,300,000 Transfers From Other Funds 135,000 Transfers To Other Funds ~333,5002 (138,189)

Total Other Financing Sources (Uses) 4,101,500 (138,189)

Net Change in Fund Balances (92) 72,941 404,781 156,460 Fund Balances - Beginning 394,463 455,797 287,299 575,154 Fund Balances -Ending $ 394,371 $ 528,738 $ 692,080 $ 731,614

The accompanying notes are an integral part of the financial statements.

Page 14

LIVINGSTON COUNTY STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES- GOVERNMENTAL FUNDS- MODIFIED CASH BASIS For The Year Ended 2006 (Continued)

$

$

$

NonMajor Funds

37,635

71,053 3,930

11,225 462

124,305

59,285 344,182

7,588

89 364 500,419

(376,114)

336,689

336,689

(39,425) 78,212 38,787

Total Governmental

Funds

$ 1,623,440 236,432

36,110 17,965

1,928,909 326,217 472,210

81 468 4,722,751

$ 4,957,497 1,181,849

154,040 49,162 31,229

500,990 850,375

7,465 695 479

8,428,086

(3,705,335)

4,300,000 471,689

(471,689) 4,300,000

594,665 1,790,925

$ 2,385,590

The accompanying notes are.an integral part of the financial statements.

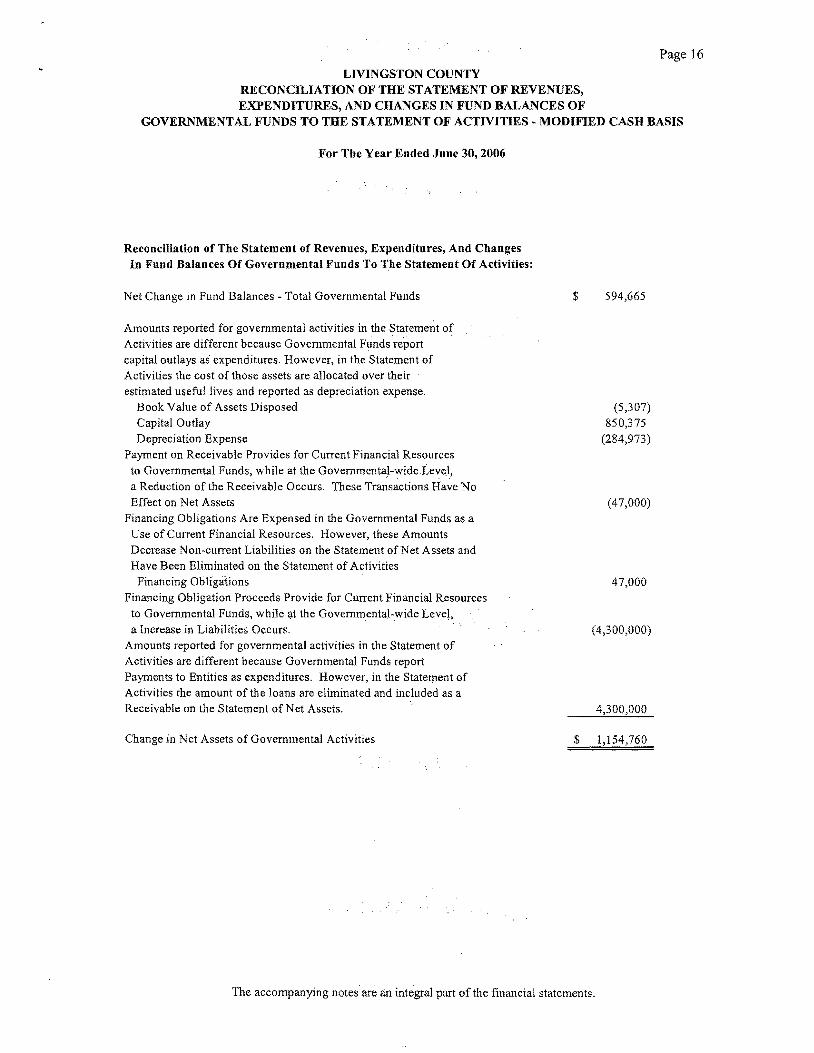

LIVINGSTON COUNTY RECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES OF

GOVERNMENTAL FUNDS TO THE STATEMENT OF ACTIVITIES- MODIFIED CASH BASIS

For The Year Ended Jun~ 30, 2()06

Page 16

LIVINGSTON COUNTY RECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES OF

GOVERNMENTAL FUNDS TO THE STATEMENT OF ACTIVITIES- MODIFIED CASH BASIS

For The Year Ended June 30, 2006

Reconciliation of The Statement of Revenues, Expenditures, And Changes In Fund Balances Of Governmental Funds To The Statement Of Activities:

Net Change in Fund Balances -Total Governmental Funds

Amounts reported for governmental activities in the Statement of Activities are different because Governmental Funds report capital outlays as expenditures. However, in the Statement of Activities the cost of those assets are allocated over their estimated useful lives and reported as depreciation expense.

Book Value of Assets Disposed Capital Outlay Depreciation Expense

Payment on Receivable Provides for Current Financial Resources to Governmental Funds, while at the Governmental-wide Level, a Reduction of the Receivable Occurs. These Transactions Have No Effect on Net Assets

Financing Obligations Are Expensed in the Governmental Funds as a Use of Current Financial Resources. However, these Amounts Decrease Non-current Liabilities on the Statement of Net Assets and Have Been Eliminated on the Statement of Activities

Financing Obligations Financing Obligation Proceeds Provide for Current Financial Resources

to Governmental Funds, while at the Governmental-wide Level, a Increase in Liabilities Occurs.

Amounts reported for governmental activities in the Statement of Activities are different because Governmental Funds report Payments to Entities as expenditures. However, in the Statement of Activities the amount of the loans are eliminated and included as a Receivable on the Statement of Net Assets.

Change in Net Assets of Governmental Activities

$ 594,665

(5,307) 850,375

(284,973)

(47,000)

47,000

(4,300,000)

4,300,000

$ 1,154,760

The accompanying notesare a:n integral part of the financial statements.

LIVINGSTON COUNTY STATEMENT OF FUND NET ASSETS- PROPRIETARY FUND- MODIFIED CASH BASIS

June 30, 2006

Page 18 LIVINGSTON COUNTY

STATEMENT OF FUND NET ASSETS- PROPRIETARY FUND- MODIFIED CASH BASIS

June 30,2006

Assets Current Assets:

Cash and Cash Equivalents Total Current Assets

Noncurrent Assets: Capital Assets:

Vehicles and Equipment Less Accumulated Depreciation

Total Noncurrent Assets Total Assets

Net Assets Invested in Capital Assets,

Net of Related Debt Unrestricted

Total Net Assets

Business-Type Activities -Enterprise

Fund

$

$

Jail Canteen

Fund

2,169 2,169

7,900 (2,220) 5,680 7,849

5,680 2,169 7,849

The accompanying notes are an integral part of the financial statements.

LIVINGSTON COUNTY STATEMENT OF REVENUES, EXPENSES, AND CHANGES IN FUND NET ASSETS~

PROPRIETARY FUND~ MODIFIED CASH BASIS

For The Year Ended June 30, 2006

LIVINGSTON COUNTY STATEMENT OF REVENUES, E~ENSES,.AND CHANGES IN FUND NET ASSETS

PROPRIETARY FUND- MODIFIED CASH BASIS

For The Year Ended June 30,2006

Operating Revenues Canteen Receipts

Total Operating Revenues

Operating Expenses Educational and Recrel).tional Depreciation Miscellaneous

Total Operating Expenses Operating Income (Loss)

Change In Net Assets Total Net Assets -Beginning Total Net Assets- Ending

Business-Type Activities -Enterprise

Fund

$

$

·Jail Canteen

Fund

!50 740

5 895

(895)

(895) 8,744 7,849

The accompanying notes are an integral part of the financial statements.

Page 20

LIVINGSTON COUNTY STATEMENT OF CASH FLOWS.:. PROPRIETARY, FUND- MODIFIED CASH BASIS

For The Year Ended June. 30, 2006

LIVINGSTON COUNTY STATEMENT OF CASH FLOWS- PROPRIETARY FUND- MODIFIED CASH BASIS

For The Year Ended. June 30, 2006

Cash Flows From Operating Activities Educational and Recreational

Miscellaneous Net Cash Provided By

Operating Activities

Net Increase (Decrease) in Cash and Cash Equivalents

Cash and Cash Equivalents - July 1

Cash and Cash Equivalents- June 30

Business-Type Activities -Enterprise

Fund

$

$

Jail Canteen

Fund

(150) (5)

(155)

(155) 2,324

2,169

The accompanying notes are ail integnil part ()f the financial statements.

Page 22

LIVINGSTON COUNTY STATEMENT OF CASH FLOWSPROPRIETARY FUND- MODIFIED CASH BASIS For The Year Ended June 30,2006 (Continued)

Reconciliation of Operating Income to Net Cash Provided (Used) by Operating Activities

Operating Income (Loss) Adjustments to Reconcile Operating Income To Net Cash Provided (Used) By Operating Activities

Depreciation Expense

Net Cash Provided By Operating Activities

Business-Type Activities -Enterprise

Fund

$

$

. Jail Canteen .. ·

Fund

(895)

740

(155)

The accompanying notes are an integral part of the financial statements.

Page 23

NOTE 1.

NOTE2.

NOTE3.

NOTE4.

NOTES.

NOTE6.

NOTE7.

NOTE8.

NOTE9.

INDEX FOR NOTES TO TaE FINANCIAL STATEMENTS

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES ......................................................... 25

DEPOSITS ............................................................................................................................ 31

CAPITAL ASSETS .................................. ········ ...................................................................... 32

SHORT-TERM DEBT ...................... ;; .................. ; ................................................................. 34

INTEREST ON SHORT-TERM DEBT ..................................................................................... 34

LONG-TERM DEBT .................................. •.• .............. ······ .............................................................. 34

EMPLOYEE RETIREMENT SYSTEM, .. : ...... ;; .... , ..... , ................................................................ 36

DEFERRED COMPENSATION ............................................................................................... 36

INSURANCE ........................................................................................................................... 36

NOTE 10. SUBSEQUENT EVENTS ........................................................................................................ 37

LIVINGSTON COUNTY NOTES TO FINANCIAL STATEMENTS

June 30, 2006

Note 1. Summary of Significant Accounting Policies

A. Basis of Presentation

Page 25

The county presents its government-wide and fund financial statements in accordance with a modified cash basis of accounting, which is a comprehensive basis of accounting other than accounting principles generally accepted in the United States of America. Under this basis of accounting, assets, liabilities, and related revenues and expenditures are :r.ecorded when they result from cash transactions, with a few exceptions. This modified cash basis recognizes revenues whenreceived and expenditures when paid. Notes receivable are recognized on the Statement of Net Assets, but notes receivable are not included and recognized on Balance Sheet - Governmental Funds. Property tax receivables, accounts payable, compensated absences, and donated assets are not reflected in the financial statements.

Encumbrances lapse at year-end and are not reflected on the Statement of Net Assets and Statement of Activities; however encumbrances are reflected on the Balance Sheet- Governmental Funds as part of the fund balance (Reserved for Encumbrances).

The State Local Finance Officer does not require the county to report capital assets and infrastructure; however the value of these assets is included in the Statement of Net Assets and the corresponding depreciation expense is included on the Statement of Activities.

B. Reporting Entity

The fmancial statements of Livingston County include the funds, agencies, boards, and entities for which the fiscal court is financially accountable. Financial accountability, as defined by Section 2100 of the Governmental Accounting Standards Board (GASB) Codification of Governmental Accounting and Financial Reporting Standards, as amended by GASB 14 and GASB 39, was determined on the basis of the government's ability to significantly influence operations, select the governing authority, participate in fiscal management and the scope of public service. Consequently, the reporting entity includes organizations that are legally separate from the primary government. Legally separate organizations are reported as component units if either the county is financially accountable or the organization's exclusion would cause the county's financial statements to be misleading or incomplete. Component units may be blended or discretely presented. Blended component units either provide their services exclusively or almost entirely to the primary government, or their governing bodies are substantively the same as the primary government. All other component units are discretely presented. The County has no blended or discretely presented component units. ·

LIVINGSTON COUNTY NOTES TO FINANCIAL STATEMENTS JUNE 30, 2006 (Continued)

Note 1. Summary of Significant Accounting Policies (Continued)

C. Livingston County Elected Officials

Page 26

Kentucky law provides for election of the officials below from the geographic area constituting Livingston County. Pursuant to state statute, these officials perform various services for the Conunonwealth of Kentucky, its judicial courts, the fiscal court, various cities and special districts within the county, and the board of education .. In exercising. these responsibilities, however, they are required to comply with state laws. Audits ·or their financial, statements are issued separately and individually and can be obtained from their respective administrative offices. These financial statements are not required to be included in the financial statements of Livingston County, Kentucky.

• Circuit Court Clerk • County Attorney • Property Valuation Administrator • County Clerk • County Sheriff

D. Government-wide and Fund Financial Statements

The government-wide financial statements (i.e., the statement of net assets and the statement of activities) report information on all of the non.,fiduciary activities of the primary government and its non-fiduciary component units. For the most part, the effect of interfund activities has been removed from these statements. Governmental activities, which normally are supported by taxes and intergovernmental revenues, are reported separately from business-type activities, which rely to a significant extemton sales, fees, and charges for support. Business-type revenues come mostly from fees charged to external parties for goods or services. Fiduciary funds are not included in these financial statements due to the unavailability of fiduciary funds to aid in the support of government programs. The County has no fiduciary funds.

The statement of net assets presents the reporting entity's non-fiduciary assets and liabilities, the difference between the two being reported as net assets. Net assets are reported in three categories: 1) invested in capital assets, net of related debt - consisting of capital assets, net of accumulated depreciation and reduced by outstanding balances for debt related to the acquisition, construction, or improvement of those assets; 2) restricted net assets -resulting from constraints placed on net assets by creditors, grantors, contributors, and other external parties, including those constraints imposed by law through constitutional provisions or enabling legislation; and 3) unrestricted net assets - those assets that do not meet the definition of restricted net assets or invested in capital assets.

LIVINGSTON COUNTY NOTES TO FINANCIAL STATEMENTS JUNE 30, 2006 (Continued)

Note 1. Summary of Significant Accounting Policies (Continued)

D. Government-wide and Fund Financial Statements (Continued)

Page 27

The statement of activities demonstrates the degree to which the direct expenses of a given function are offset by program revenues. Direct expenses are those that are clearly identifiable with a specific function. Program revenues include: 1) charges to customers or applicants who purchase, use, or directly benefit from goods, services, or privileges provided by a given function; 2) operating grants and contributions; and 3) capital grants and contributions thatare restricted to meeting the operational or capital requirements of a particular function. l:nterna:Ily · dedicated resources such as taxes and unrestricted state funds are reported as general revenues.

Funds are characterized as either major or non-major. Major funds are those whose assets, liabilities, revenues, or expenditures/expenses are at least ten percent of the corresponding total (assets, liabilities, etc.) for all funds or type (governmental or proprietary) and whose total assets, liabilities, revenues, or expenditures/expenses are at least five percent of the corresponding total for all governmental and enterprise funds combined. The fiscal court may also designate any fund as major.

Separate financial statements are provided for governmental funds and proprietary funds. Major individual governmental funds and major enterprise funds are reported as separate columns in the financial statements.

Governmental Funds

The primary government reports the following major governmental funds:

General Fund - This is the primary operating fund of the fiscal court. It accounts for all financial resources of the general government, except ·where the Governor; s ·office for Local Development requires a separate fund or where management requires that a separate fund be used for some function.

Road Fund - This fund is for road and bridge construction and repair. The primary source of revenue for this fund is state payments for truck licenses distribution, municipal road aid, and transportation grants. The Governor's Office for Local Development requires the fiscal court to maintain these receipts and expenditures separately from the General Fund.

Local Government Economic Assistance Fund (LGEA) - The purpose of this fund is to account for grants received from the Local Government Economic Assistance Program to be used to improve the environment for new industry and to improve the quality of life for the residents. The Governor's Office for Local Development requires the fiscal court to maintain these receipts and expenditures separately from the General Fund.

Occupational Tax Fund - The purpose of this fund is to account for payroll tax receipts and expenses. The occupational tax fund may be used for general purpose expenses which the county budgeted for general government, protection to persons and property, general health and sanitation, roads, and administration for the fiscal year. The Governor's .Office for Local Development requires the fiscal court to maintain these receipts and expenditUres separately from the General Fund.

LIVINGSTON COUNTY . . . NOTES TO FINANCIAL STATEMENTS. JUNE 30, 2006 (Continued)

Note 1. Sunuuary of Significant Accounting Policies (Continued)

D. Government-wide and Fund Financial Statements (Continued)

Governmental Funds (Continued)

Page 28

The primary government also has the following non-ll).ajor funds: Jail Fund, 911 Fund, Tourism Fund, and Kentucky Land Heritage Fund.

Special Revenue Funds:

The Road Fund, Jail Fund, Local Government Economic Assistance Fund, Occupational Tax Fund, 911 Fund, Tourism Fund, and Kentucky Land Heritage Fund are presented as special revenue funds. Special revenue funds are to account forthe proceeds of specific revenue sources and expenditures that are legally restricted for specific putposes.

Proprietary Funds

Proprietary funds distinguish operating revenues and expenses from non-operating items. Operating revenues and expenses generally result from providing services and producing and delivering goods in connection with proprietary funds' principal ongoing operations. All revenues and expenses not meeting this defmition are reported as non-operating revenues and expenses. The principal operating revenues of the county's enterprise funds are charges to customers for sales in the Jail Canteen Fund. Operating expenses for the enterprise funds include the cost of sales and services, administrative expenses, and depreciation on capital assets.

The primary government reportS the following major proprietary fund:

Jail Canteen Fund- The canteen operations are authorized pursuant to KRS 441.135(1), which allows the jailer to sell snacks, sodas, and other items to inmates. The profits generated from the sale of those items are to be used for the benefit or recreation of the itimates. KRS 441.135(2) requires the jailer to maintain accounting records and report anriually to the county treasurer the receipts and disbursements of the Jail Canteen Fund.

E. Deposits and Investments

The government's cash and cash equivalents are considered to be cash on hand, demand deposits, certificates of deposit, and short-term investments with original maturities of three months or less from the date of acquisition.

KRS 66.480 authorizes the county to invest in the following, including but not limited to, obligations of the United States and of its agencies and instrumentalities, obligations and contracts for future delivery or purchase of obligations backed by the full faith and credit of the United States, obligations of any corporation of the United States government, bonds or certificates of indebtedness of this state, and certificates of deposit issued by or other interest-bearing accounts of any bank or savings and loan institution which are insured by the Federal Deposit Insurance Corporation (FDIC) or which are collateralized, to the extent uninsured, by any obligation permitted by KRS 41.240( 4).

LIVINGSTON COUNTY NOTES TO FINANCIAL STATEMENTS JUNE 30, 2006 (Continued)

Note 1. Summary of Significant Accounting Policies (Continued)

F. Capital Assets

Page 29

Capital assets, which include land, land improvements, buildings, furniture and office equipment, building improvements, machinery, equipment, and infrastructure assets (roads and bridges) that have a useful life of more than one reporting period based on the government's capitalization policy, are reported in the applicable governmental or business-type activities of the government-wide fmancial statements. Such assets are recorded at historical cost or estimated historical cost when purchased or constructed.

Cost of normal maintenance and repairs that do not add to the value of the asset or materially extend the asset's life are not capitalized. Land and Construction In Progress are not depreciated. Interest incurred during construction is not capitalized. Capital assets and infrastructure are depreciated using the straight-line method of depreciation over the estimated useful life of the asset.

Capitalization Useful Life Threshold (Years)

Land $ 12,500 10-60 Land hnprovements $ 7,500 10-60 Buildings and Building hnprovements $ 7,500 10-75 Machinery and Equipment $ 2,500 3-25 Vehicles $ 2,500 3-25 Infrastructure $ 10,000 10-50

G. Long-term Obligations

In the government-wide financial statements and proprietary fund types in the fund financial statements, long term debt and other long-term obligations are. reported as liabilities in the applicable fmancial statements. The principal amount of bonds, notes and fmancing obligations are reported.

In the fund financial statements, governmental fund types recognize bond interest, as well as bond issuance costs when received or when paid; during the current period. The principal amount of the debt and interest are reported as expenditures. Issuance costs, whether or not withheld from the actual debt proceeds received, are reported as expenditures. Debt proceeds are reported as other financing sources.

H. Fund Equity

In the fund financial statements, the difference between the assets and liabilities of governmental funds is reported as fund balance. Fund balance is divided into reserved and unreserved components, with unreserved considered available for new spending. Unreserved fund balances may be divided into designated and undesignated portions. . Designations represent fiscal court's intended use of the resources and should reflect actual plans approved by the fiscal court.

LIVINGSTON COUNTY NOTES TO FINANCIAL STATEMENTS JUNE 30, 2006 (Continued)

Note 1. Summary of Significant Accounting Policies (Continued)

H. Fund Equity (Continued)

Page 30

Governmental funds report reservations of fund balance for amounts that are legally restricted by outside parties for use for a specific purpose, long-term receivables, and encumbrances.

"Reserved for Encumbrances" are purchase orders that will be fulfilled in a subsequent fiscal period. Although the purchase order or contract creates a legal commitment, the fiscal court incurs no liability until performance has occurred on the part of the party with whom the fiscal court has entered into the arrangement. When a government intends to honor ·outstanding commitments in subsequent periods, such amounts are encumbered. Encumbrances lapse at year-end and are not reflected on the Statement of Net Assets and Statement of Activities; however, encumbrances are reflected on the Balance Sheet Governmental Funds as part of the fund balance.

I. Budgetary Information

Annual budgets are adopted on a cash basis of accounting and according to the laws of Kentucky as required by the State Local Finance Officer.

The County Judge/Executive is required to submit estimated receipts and proposed expenditures to the fiscal court by May 1 of each year. The budget is prepared by fund, function, and activity and is required to be adopted by the fiscal court by July 1. ·

The fiscal court may change the original budget by transferring appropriations at the activity level; however, the fiscal court may not i:qcrease the totalbudgeJwithout approval by the.State Local Finance Officer. Expenditures may not exceed budgeted appropriations at the activity level.

J. Related Organizations and Jointly Governed Organizations

A related organization is an entity for which the county is not financially accountable. It does not impose will or have a fmancial benefit or burden relationship, even if the county appoints a voting majority of the related organization's governing board. Based on these criteria, the following is considered to be a related organization of Livingston County Fiscal Court: Senior Citizens Center.

A jointly governed organization is a regional government or other multi-governmental arrangement that is governed by representatives from each of the governments that created the organization, but that is not a joint venture because the participants do not retain an ongoing finar~cial interest or responsibility. Based upon these criteria, the Crittenden-Livingston Water District and the Ballard, Carlisle, & Livingston Public Library are considered to be jointly governed organizations of the Livingston County Fiscal Court.

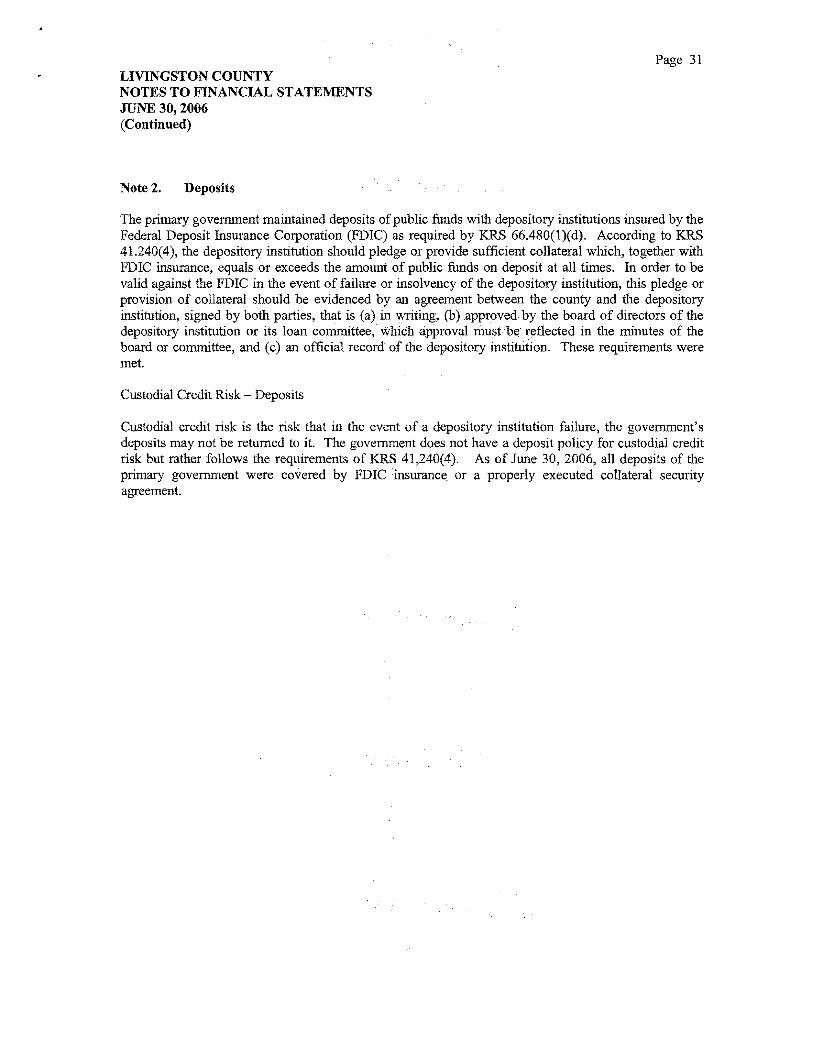

LIVINGSTON COUNTY NOTES TO FINANCIAL STATEMENTS JUNE 30, 2006 (Continued)

Note 2. Deposits

Page 31

The primary government maintained deposits of public funds with depository institutions insured by the Federal Deposit Insurance Corporation (FDIC) as required by KRS 66.480(l)(d). According to KRS 41.240(4), the depository institution should pledge or provide sufficient collateral which, together with FDIC insurance, equals or exceeds the amount of public funds on deposit at all times. In order to be valid against the FDIC in the event of failure or insolvency of the depository institution, this pledge or provision of collateral should be evidenced by an agreement between the county and the depository institution, signed by both parties, that is (a) in writing, (b )..approved by the board of directors of the depository institution or its loan committee,· which apprbvalmust be reflected in the minutes of the board or committee, and (c) an official record of the depository institution. These requirements were met.

Custodial Credit Risk- Deposits

Custodial credit risk is the risk that in the event of a depository institution failure, the government's deposits may not be returned to it. The government does not have a deposit policy for custodial credit risk but rather follows the requirements of KRS 41,240(4). As of June 30, 2006, all deposits of the primary government were covered by FDIC insurance or a properly executed collateral security agreement.

LIVINGSTON COUNTY NOTES TO FINANCIAL STATEMENTS JUNE 30, 2006 (Continued)

Note 3. Capital Assets

Capital asset activity for the year ended June 30, 2006 was as follows:

Reportin~ Enti~ ·Beginning

Balance Increases Decreases Governmental Activities:

Capital Assets Not Being Depreciated: Land and Land Improvements $. . 973,854- $ 15,660 . $

Total Capital Assets Not Being Depreciated $ 973,854 $ 15,660 $

Capital Assets, Being Depreciated: Buildings $ 1,413,256 $ $ Vehicles and Equipment 1,674,382 360,033 (33,690) Infrastructure 776,729 474,682

Total Capital Assets Being Depreciated $ 3,864,367 $ 834,715 $ (33,690)

Less Accumulated Depreciation For: Buildings $ (346,613) $ (25,313) Vehicles and Equipment (593,659) (142,723) $ 28,383 Infrastructure {115,091} (116,9372

Total Accumulated Depreciation $ {1,055,3632 $ (284,9732 $ 28,383 Total Capital Assets, Being

Depreciated, Net $ 2,809,004 $ 5492742 $ (5,3072 Governmental Activities Capital

Assets, Net $ 3,782,858 $ 565,402 $ (5,3072

Page 32

Ending Balance

$ 989,514

$ 989,514

$ 1,413,256 2,000,725 1,251,411

$ 4,665,392

$ (371,926) (707,999) {232,0282

$ {1,311,9532

$ 3,353,439

$ 4,342,953

LIVINGSTON COUNTY NOTES TO FINANCIAL STATEMENTS JUNE 30, 2006 (Continued)

Note 3. Capital Assets (Continued)

Reporting Entity Beginning )3alance .Increases Decreases

Business-T~ Activities:

Capital Assets, Being Th:preciated: Vehicles and Equipment $ 7,900 .. $. $

Total Capital Assets Being Depreciated $ 7,900 $ $

Less Accumulated Th:preciation For: Vehicles and Equipment $ ~1,480) $ {740} $

Total Accumulated Depreciation $ (1,480) $ (740) $ Total Capital Assets, Being

Depreciated, Net $ 6,420 $ {7402 $ Business-Type Activities Capital

Assets, Net $ 6,420 '$ {7402 $ 0

Depreciation expense was charged to functions of the primary government as follows:

Governmental Activities: General Government Protection to Persons and Property General Health and Sanitation Social Services Recreation and Culture Roads, Including Depreciation of General Infrastructure Assets

Total Depreciation Expense- Governmental Activities

Business-Type Activities Jail Canteen

Total Depreciation Expense- Business-Type Activities

$

$

$

$

Page 33

Ending Balance

$ 7,900

$ 7,900

$ ~2,220)

$ (2,220)

$

$

13,929 74,198

5,022 11,108 3,278

177,438

284,973

740

740

5,680

5,680

LIVINGSTON COUNTY NOTES TO FINANCIAL STATEMENTS JUNE 30, 2006 (Continued)

Note 4. Short-term Debt

Page 34

On June 16, 2005, Livingston County voted. to participated in the • Kentucky Association of Counties Advance Revenue Program (KARP) for the purchase of tax andrevenue anticipation notes for the 2005-2006 fiscal year in both the General Fund and Road Fund by issuing notes in the amount of $385,500 and $38,600 respectively, with principal and interest being due in January 2006. For the fiscal year, the County earned interest of $8,552 and $856 and paid interest of $6,786 and $679 respectively. As of June 30, 2006, all principal and interest amounts associated with the notes had been paid.

Changes In Short-term Liabilities

.Kentucky Advanced Revenue Program

Governmental Activities Short-term liabilities

$

$

Beginning Balance

Note 5. Interest On Short-term Debt ·

Additions Reductions Ending Balance

Due Within One Year

$ 424,100 $ 424,100 .....;$ _____ $;.._ __ _

$ 424,100 $ 424,100 =$'====== =$====

Interest on Short-term debt on the Statement of Activities includes $7,465 in interest on short term debt.

N()te 6. Long-term Debt

A. Financing Agreement- Ledbetter Sewer System

On July 1, 2005, Livingston County entered into, a filiancirig agreement with the Kentucky Association of Counties Leasing Trust Program (KACoL T) for the fmancing of a sewer system project for the Ledbetter Water District, Livingston County, Kentucky. The principal of the lease is $3,300,000 with repayment to be made over a fourteen year period starting in August 2005. Principal payments are due annually on January 20th, in variable amounts; interest at a rate of 4.25 percent plus associated fees are due monthly in various amounts. The Ledbetter Water District has pledge their revenues for repayment of the note and are repaying the note to KACoLT. As of June 30, 2006 the balance on the note was $3,255,000. A maturity schedule is as follows:

Fiscal Year Ended June 30

2007 $ 2008 2009 2010 2011 2012 2013-2017 2018-2019 Totals $

Principal

50,000 50,000 .55,000 60,000 60,000 65,000

.380,000 2,5351000 31255,000

Interest &Fees

$ 128,582 126,741 124,586 122,311 119,846 117,507 547,638 159,715

$ 1,318,344

LIVINGSTON COUNTY NOTES TO FINANCIAL STATEMENTS JUNE 30, 2006 (Continued)

Note 6. Long-term Debt- (Continued)

B. Financing Agreement Hospital and Health Care Services Project

Page 35

In May 2006, Livingston County entered into a financing agreement with the Kentucky Association of Counties Leasing Trust Program (KACoLT) to finance the renovation of the Livingston Hospital and Health Care Services facility. The principal of the lease is $1,000,000 with repayment to be made over a twenty-year period starting in June 2006. Livingston County has entered into an agreement with Livingston Hospital and Health Care Services, Inc for repayment of the note with KACoLT and has filed a lien on the property until note is retired. Livingston Hospital and Health Care Services, Inc are repaying the note and as of June 30,2006 the balance vvas $998,000.

Fiscal Year Ended June 30 Principal Interest

2007 $ 30,000 $ 48,321 2008 36,000 47,645 2009 36,000 46,292 2010 . 36,000 44,490 2011 36,000 42,662 2012 36,000 40,911 2013-2017 225,000 173,278 2018-2022 285,000 93,576 2023-2026 278,000 30,051

Totals $ 998,000 $ 567,226

C. Changes in Long-Term Debt

Beginning. Ending Balance Additions Reductions Balance

Governmental Activities:

Financing Obligations $ ·.· $ . 4,300,000 $ 47,000 $ 4,253,000

Governmental Activities Long-term Debt $ 0 $ 4,300,000 $ 47,000 $ 4,253,000

LIVINGSTON COUNTY NOTES TO FINANCIAL STATEMENTS JUNE 30, 2006 (Continued)

Note 7. Employee Retirement System

Page 36

The county has elected to participate in the County Employees Retirement System (CERS), pursuant to KRS 78.530 administered by the Board of Trustees of the Kentucky Retirement Systems. This is a cost sharing, multiple-employer defined benefit pension pl!Ul, which covers all eligible full-time employees and provides retirement, disability, and death benefits to plan members. Benefit contributions and provisions are established by statute. Nonhazardous covered employees are required to contribute 5 percent of their salary to the plan. The county's contribution rate for nonhazardous employees was 10.98 percent. Hazardous covered employees are required to contribute 8 percent of their salary to the plan. The county's contribution rate for hazardous employees was 25.01 percent.

Benefits fully vest on reaching five years of service for nonhazardous employees. Aspects of benefits for nonhazardous employees include retirement after 27 years of service or age 65. Aspects of benefits for hazardous employees include retirement after 20 years of service or age 55.

Historical trend ·information showing the CERS' progress in accumulating sufficient assets to pay benefits when due is presented in the Kentucky Retirement Systems' annual fmancial report. This report may be obtained by writing the Kentucky Retirement Systems, 1260 Louisville Road, Frankfort, KY 40601-6124, or by telephone at (502) 564-4646.

Note 8. Deferred Compensation

The Livingston County Fiscal Court voted. to allow ·all eligible ·employees to participate in deferred compensation plans administered by The Kentucky· Public Employees' Deferred Compensation Authority. The Kentucky Public Employees' Deferred Compensation Authority is authorized under KRS 18A.230 to 18A.27 5 to pnwide administration of tax sheltered supplemental retirement plans for all state, public school and university employees and employees of local political subdivisions that have elected to participate.

These deferred compensation plans permits all full time employees to defer a portion of their salary until future years. The deferred compensation is not available to employees until termination, retirement, death, or unforeseeable emergency~ Participation by eligible employees in the deferred compensation plans is voluntary. ·

Historical trend information showing The Kentucky Public Employees' Deferred Compensation Authority's progress in accumulating sufficient assets to pay benefits when due is presented in The Kentucky Public Employees' Deferred Compensation Authority's annual financial report. This report may be obtained by writing Kentucky Public Employees' Deferred Compensation Authority at 105 Sea Hero Road, Suite 1, Frankfort, KY 40601-8862, or by telephone at (502) 573-7925.

Note 9. Insurance

For the fiscal year ended June 30, 2006, Livingston County was a member of the Kentucky Association of Counties' All Lines Fund (KALF). KALF is a self-insurance fund and was organized to obtain lower cost coverage for general liability, property damage, public officials' errors and omissions, public liability, and other damages. The basic nature of a self-insurance program is that of a collectively shared risk by its members. If losses incurred for covered claims exceed the resources contributed by the members, the members are responsible for payment of the excess losses.

LIVINGSTON COUNTY NOTES TO FINANCIAL STATEMENTS JUNE 30, 2006 (Continued)

Note 10. Subsequent Events

Financing Agreement - Judicial Center Project

Page 37

On May 18, 2006, Livingston County passed Ordinance No. 2006-5-18-03 General Obligation Bond Anticipation Notes Series 2006. The ordinance .is fot short-t~nn financing of the Judicial Building Project. As of June 30, 2006 no money had been received from the bond issuance.

LIVINGSTON COUNTY. BUDGETARY COMPAIUSON SCHE:tiULES

Required Supplementarylnfor~~tion ~ M~difi~d Cash Basis

For The Year Ended June 30,2006

Page 39

LIVINGSTON COUNTY BUDGETARY COMPARISON SCHEDULES

Required Supplementary Information - Modified Cash Basis

For The Year Ended June 30, 2006

GENERAL FUND

Actual Variance with Amooots, Final Budget

Bud~eted Amooots (Budgetary Positive Original Final Basis) (Ne~ative)

REVENUES Taxes $ 573,250. $ 640,493 $ 650,411 $ 9,918 In Lieu Tax Paymmts 209,900 236,432 236,432 Excess Fees 4,810 35,886 36,ll0 224 Licenses and Permits 10,250 14,995 17,915 2,920 Intergovernrn;mtal Revenue 218,016 231,794 214,106 (17,688) Charges for Services 28,500 28,500 21,021 (7,479) Miscellaneous 73,930 124,766 43,734 (81,032) Interest 19,645 19,645 22,902 3,257

Total Revenues $ 1,138,301 $ 1,332,511 $ 1,242,631 $ (89,880)

EXPENDITURES General Governrn;mt $ 651,692 $ 720,845 $ 4,787,004 $ (4,066, 159) Protection to Persons and Property 6,350 48,804 48,527 277 General Health and Sanitation 17,900 26,917 20,417 6,500 Social Services 4,000 5,190 5,190 Recreation and Culture 8,000 16,622 10,872 5,750 Debt Service 640,689 640,689 6,786 633,903 Capital Outlay 92,514 (92,514) Administration 658;702 .. 722,476 372,913 349,563

Total Expenditures $ 1,987,333 ·$ 2,181,543 $ 5,344,223 $ (3,162,680)

Excess (Deficiency) of Revenues Over Expenditures Before Other Financing Sources (Uses) $ . (849,032) $ (849,032) $ (4,101,592) $ (3,252,560)

OTHER FINANCING SOURCES (USES) Financing Obligation Proceeds $ 633,800 $ 633,800 $ 4,300,000 $ 3,666,200 Transfers From Other Foods 177,550 177,550 135,000 (42,550) Transfers To Other Foods . ~368,318) . (368,318) p33,5002 34,818

Total Other Financing Sources (Uses) $ 443,032 $ 443,032 $ 4,101,500 $ 3,658,468

Net Changes in Food Balance $ . (406,000) $ (406,000) $ (92) $ 405,908 Food Balance - Beginning 406,000 406,000 394,463 !1l,53Z}

Food Balance - Ending $ 0 $ 0 $ 394,371 $ 394,371

Page 40

LIVINGSTON COUNTY BUDGETARY COMPARISON SCHEDULES Required Supplementary Information - Modified Cash Basis For The Year Ended June 30,2006 (Continued)

ROAD FUND

Actual Variance with Anxmnts, Final Budget

Budgeted Amounts (Budgetary Positive Original Final Basis} (Negative)

REVENUES Intergovernmental Revenue $ 858,051 $ 1,285,818 $ 1,253,254 $ (32,564) Charges for Services 750 750 50 (700) Miscellaneous 16,500 36,447 39,807 3,360 Interest 14;655 17,397 22,476 5,079

Total Revenues $ 889,956 $ 1;340,412 $ 1,315,587 $ (24,825)

EXPENDITURES General Health and Sanitation $ 22,500 $ 28,451 $ 23,887 $ 4,564 Roads 691,150 1,132,937 442,521 690,416 Debt Service 131,015 131,015 679 130,336 Capital Outlay 547,143 (547,143) Administration 494,891 633,916 228,416 405,500

Total Expenditures $ .. 1,339,556 .$ 1,926,319 $ 1,242,646 $ 683,673

Excess (Deficiency) of Revenues Over Expenditures Before Other Financing Sources (Uses) $ (449,600} $ (585,907) $ 72,941 $ 658,848

OTHER FINANCING SOURCES (USES) Financing Obligation Proceeds $ 129,600 $ 129,600 $ $ p29,600}

Total Other Financing Sources (Uses) $ 129,600 $ . 129,600 $ (129,600)

Net Changes in Fund Balance $ (320,000) $ (456,307) $ 72,941 $ 529,248 Fund Balance Beginning 320,000 456,307 455,797 (510)

Fund Balance -Ending $ 0 $ 0 $ 528,738 $ 528,738

Page41

LIVINGSTON COUNTY BUDGETARY COMPARISON SCHEDULES Required Supplementary Information - Modified Cash Basis For The Year Ended June 30,2006 (Continued)

LOCAL GOVERNMENT ECONOMIC ASSISTANCE FUND

Actual Variance with Amounts, Final Budget

Bud~eted Amounts (Budgetary Positive Original Final Basis) (Negative)

REVENUES Taxes $ 32,000 $ 32,000 $ 34,748 $ 2,748 Licenses and Permits 50 50 Intergovernmental Revenue 215,000 380,702 380,479 (223) Miscellaneous 1,000 331,209 339,704 8,495 Interest 3,750 7,634 13,624 5,990

Total Revenues $ 251,750 $ 751,595 $ 768,605 $ 17,010

EXPENDITURES General Government $ 52,426 $ 68,070 $ 60,641 $ 7,429 Protection to Persons and Property 15,000 28,420 16,118 12,302 General Health and Sanitation 122;675 135,817 91,871 43,946 Social Services . 13,100 . 44,192 43,972 220 Recreation and Culture 16,250 24,977 20,357 4,620 Roads 85,000. 118,876. 58,469 60,407 Capital Outlay 67,610 (67,610) Administration 197,699 609,143 4,786 604,357

Total Expenditures $ 502,750 $ 1',029,495 $ 363,824 $ 665,671

Excess (Deficiency) of Revenues Over Expenditures Before Other Financing Sources (Uses) $ . (251,000) $ (277,900) $ 404,781 $ 682,681

Net Changes in Fund Balances $ (251,000) $ (277,900) $ 404,781 $ 682,681 Fund Balances - Beginning 251,000 277,900 287,299 9,399

Fund Balances - Ending $ 0 $ 0 $ 692,080 $ 692,080

Page 42

LIVINGSTON COUNTY BUDGETARY COMPARISON SCHEDULES Required Supplementary Information - Modified Cash Basis For The Year Ended June 30,2006 (Continued)

OCCUPATIONAL TAX FUND

Actual Variance with Amounts, Final Budget

Budgeted Amounts (Budgetary Positive Original Final Basis) (Negative)

REVENUES Taxes $ 750,000 $ 750,000 $ 900,646 $ 150,646 Intergovernmental Revenues 11,600 11,600 10,017 (1,583) Charges for Services 280,000 286,226 301,216 14,990 Miscellaneous 11,400 41,900 37,740 (4,160) Interest 9,500 15,943 22,004 6,061

Total Revenues $ 1,062,500 $ 1,105,669 $ 1,271,623 $ 165,954

EXPENDITURES General Government $ 53,025 $ 59,558 $ 50,567 $ 8,991 Protection to Persons and Property 721,513 985,628 773,022 212,606 General Health and Sanitation 10,000 17,865 17,865 Roads 196,975 38,427 38,427 Capital Outlay 135,520 (135,520)

Administration 478,437 408,190 408,190 Total Expenditures $ 1,459,950 $ 1,509,668 $ 976,974 $ 532,694

Excess (Deficiency) of Revenues Over Expenditures Before Other Financing Sources (Uses) $ (397,450) $ (403,999) $ 294,649 $ 698,648

OTHER FINANCING SOURCES (USES) Transfers To Other Funds $ ~177,550) . $ ~177,550) $ ~138,189) $ 39,361

Total Other Financing Sources (Uses) $ (177,550) $ (177,550) $ (138,189) $ 39,361

Net Changes in Fund Balances .$ (575,000) $ (581,549) $ 156,460 $ 738,009 Fund Balances - Beginning 575,000 581,549 575,154 (6,395)

Fund Balances - Ending $ 0 $ 0 $ 731,614 $ 731,614

Page 43 LIVINGSTON COUNTY

NOTES TO REQUIRED SUPPLEMENTARY INFORMATION

June 30, 2006

Budgetary Information

Annual budgets are adopted on a cash basis of accounting and according to the laws of Kentucky as required by the State Local Finance Officer.

The County Judge/Executive is required to submit estimated receipts and proposed expenditures to the fiscal court by May 1 of each year. The budget is prepared by fund, function, and activity and is required to be adopted by the fiscal court by July 1.

The fiscal court may change the original budget by transferring appropriations at the activity level; however, the fiscal court may not increase the total budget withcmt approval by the State Local Finance Officer. Expenditures may not exceed budgeted appropriations at the activity level.

LIVINGSTON COUNTY COMBINING BALANCE SHEET-

NON-MAJOR GOVERNMENTAL FUNDS -MODIFIED CASH BASIS Other Supplementary Information

June 30, 2006

Page 45

LIVINGSTON COUNTY COMBINING BALANCE SHEET -

NON-MAJOR GOVERNMENTAL FUNDS- MODIFIED CASH BASIS Other Supplementary Information

June 30, 2006

Kentucky Total Land Non-Major

Jail 911 ·Heritage Tourism Governmental Fund Fund Fund Fund Funds

ASSETS Cash and Cash Equivalents $ 4,347 $ . 3,847 $ 20,061 $ 10,532 $ 38,787

Total Assets $ 4,347 $ 3,847 $ 20,061 $ 10,532 $ 38,787

FUND BALANCES Reserved for: Encumbrances $ 591. $ 2,682 $ 3,874 $ $ 7,147 Umeserved: Special Revenue Funds 3,756 1,165 16,187 10,532 31,640

Total Fund Balances $ 4,347 $ 3,847 $ 20,061 $ 10,532 $ 38,787

..

LIVINGSTON COUNTY COMBINING STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES

IN FUND BALANCES- NON-MAJOR GOVERNMENTAL FUNDS- MODIFIED CASH BASIS Other Supplementary Information

For The Year Ended June 30, 2006

Page47 LIVINGSTON COUNTY

COMBINING STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES- NON-MAJOR GOVERNMENTAL FUNDS- MODIFIED CASH BASIS

Other Supplementary Information

For The Year Ended June 30, 2006

Kentucky Total land Non-Major

Jail 911 Heritage Tourism G>vermrmtal Fund . Fund Fund. Fund Funds

REVENUES Taxes $ $ $ $ 37,635 $ 37,635 Intergovernrrental 66,553 4,500 71,053 OJarges for Services 3,772 158 3,930 Miscellaneous 7,8ffi 3,422 11,225 Interest 403 59 462

Total Revenues $ 78,128 $ 3,983 $ 4,500 $ 37,694 $ 124,305

EXPENDITlJRFS General Governrrent $ $ $ 21,934 $ 37,351 $ 59,285 Protection to Persons and Property 170,954 173,228 344,182 Capital Outlay 7,588 7,588 Administration 24,145 65,219 89,364

Total Expenditures $ 2fJ2,687 $ 238,447 $ 21,934 $ 37,351 $ 500,419

Excess (D:mciency) ofRevenues Over Expenditures $ (124,559) $. (234,464) $· (17,434). $ 343 $ (376,114)

OOI.er Nnancing Sources (Uses) Transfers From Ofuer Fllllds $ 128,000 $ 198,500 $ $ 10,189 $ 336,689

Total Ofuer Financing Sources (U;es) $ 128,000 $ 198,500 $ $ 10,189 $ 336,689

Net Change in Fund Balances $ 3,441 $ (35,964) $ (17,434) $ 10,532 $ (39,425) Fund Balances- Beginning 906 39,811 37,495 78,212 Fund Balances- Ending $ 4,347 $ 3,847 $ 20,061 $ 10,532 $ 38,787

REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS

PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

Krista Romaine, CPA, Member Charlotte Clark, Member

·. .. .· ., ' ... ssoctafts p££c

CERTIFIED PUBLIC ACCOUNTANTS

TI1e Honorable Christopher K. Lasher, Livingston County Judge/Executive Members of the Livingston County Fiscal Court·. · ·

Report On Internal Control Over Financial Reporting And On Compliance And Other Matters Based On An Audit Of Financial Statements

Perfonned In Accordance With Government Auditing Standards

William Erwin, CPA Van R. Prince, CPA

We have audited the financial statements of the govenm1ental activities, the business-type activities, each major fund, and the aggregate remaining fund information of Livingston County, Kentucky, as of and for the year ended June 30, 2006, which collectively comprise the County's basic fmancial ~statenients, as listed in the table of contents· and have issued our report thereon dated June 12, 2007. 'Livingston County presents its financial statements on the modified cash basis of accounting which is a

· · coi-r;prehensive basis of accounting other than generally accepted accounting principles. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and

· · the standards applicable to fmancial audits contained in Government Auditing Standards issued by the ComP:troller General ofthe United States.

h1ternaJ Control Over Financial Reporting

,. · Inplahning and perforll1ing our audit, we co11si:d.ered ~ivil~gstoP. County's internal control over financial reporti11g in order to deterll1ine our auditing procedures for the purpose of expressing our opinions on

.. tl1e ftfiancial statements and not to provide an opinionon the i11temal control over fina.ncial reporting . . . bur 'consideration of the intemal control over fmancial reporting would not necessarily disclose all

matt~:<rs in the i11ternal control over financial reporting that might be a material weakness. A material weillmess is a reportable condition i11 which the design or operation of one or more of the internal control components does not reduce to a relatively low level the risk that misstatements caused by error 'or ftaud in an1otmts that would be material in relation to the fmancial statements being audited may occur;and not be detected within a timely period by employees in the nornml course ofperforll1ing their

vassigried functions. We noted no matters involving the internal control over financial reporting and its operation that we consider to be material weala.1esses. · · ·

~ .

Compliance And Other Matters

As part of obtaining reasonable assurance about whether Livi11gston County's fmancial statements are free cif material misstatement, we perfom1ed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the detem1i11ation of financial statement an1ounts. However, providing an opinion on compliance with those provisions was not an objective of om audit, ·and accordingly, we do not express

. such an opinion. TI1e results of our tests disclosed no instances of noncomplia.."'lce or other nmtters that · are required to be reported under Govemmem Auditing Standards.

1011 Paris Road- Suite 341 - P:o. Box488- Mayfield, Kentucky 42066 Phone: 270-247-8050 Fax: 270-247-7749

AICPA ~~SCPA TSCPA

Report On Internal Control Over Financial Reporting And On Compliance And Other Matters Based On AnAuditOfFinancial Statements Performed In Accordance With Government Auditing Standards (Continued) · ·

Page 50

This report is intended solely for the information and use of management, and the Governor's Office for Local Development and is not intended to be and should not be used by anyone other than the specified parties.

June 12,2007

Respectfully submitted,

Krista L. Romaine, CPA Romaine & Associates, PLLC

CERTIFICATION OF COMPLIANCE-LOCAL GOVERNMENT ECONOMIC ASSISTANCE PROGRAM

LIVINGSTON COUNTY FISCAL COURT

For The Fiscal Year Ended June 30, 2006

Appendix A

CERTIFICATION OF COMPLIANCE

LOCAL GOVERNMENT ECONOMIC ASSISTANCE PROGRAM

LNINGSTON COUNTY FISCAL COURT

For The Fiscal Year Ended June 30,2006

The Livingston County Fiscal Court hereby certifies that assistance received from the Local Government Economic Assistance Program was expended for the purpose intended as dictated by the applicable Kentucky Revised Statutes.

~a Name County udge!Executive

I

County Treasurer