Embed Size (px)

Citation preview

Report

of

Commodity Futures Trading Subcommittee

Industrial Structure Council

-Establishing an Open, Sound, Active and Attractive Market, Aiming to Enhance Competitive Edge of the Japanese Economy-

August 21, 2012

1

Table of Contents Chapter 1: Introduction・・・・・・・・・・・・・・・・・・・・・・・・2 Chapter 2: Framework for Establishing Comprehensive Exchange

1. Background and objectives・・・・・・・・・・・・・・・・・・・・・・4 2. Comprehensive exchanges that will deal with securities, financial instruments and

commodities in an integrated manner・・・・・・・・・・・・・・・・・・

4 3. Bill for the Partial Revision of the Financial Instruments and Exchange

Act・・・・・・5 Chapter 3: Possible Actions for the Revitalization and Sound Development of the

Commodity Futures Market I. Revitalization of Commodity Trading

1. Improving services available from commodity exchanges・・・・・・・・・・7 2. Improving operational efficiency of commodity exchanges・・・・・・・・・9 3. Enhancing clearing functions (clearing capabilities)・・・・・・・・・・・・10

II. Expansion of diversified market participants

1. Expanding market participants・・・・・・・・・・・・・・・・・・・・10 2. Framework for improving user-friendliness and credibility・・・・・・・・・12 3. Spreading out proper understanding on commodity futures market・・・・・・13

III. Coping with Globalized Commodity Futures Market

1. Collaborating with overseas markets・・・・・・・・・・・・・・・・・・13 2. Enhancing market surveillance functions・・・・・・・・・・・・・・・・14 3. Expanding over-the-counter (OTC) trading・・・・・・・・・・・・・・・15

IV. Solicitation Rules

1. Ban on unsolicited offers・・・・・・・・・・・・・・・・・・・・・・15 2. Possible approach on solicitation rules・・・・・・・・・・・・・・・・・16

Conclusion・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・18

2

3

Chapter 1: Introduction 1. With the wild fluctuation of energy prices for recent years as well as a steep rise in

metal resource prices, the commodity futures market serves as an important industrial infrastructure in trading-related risk hedging and price formation and is expected to play a significant role to enhance the competitive edge of Japan’s economy. Through successively enhancing consumer protection schemes, Japan’s commodity futures market has been seeing a steady decrease in consumer complaints, leading to a healthier market. However, trading volumes have been shrinking in the market. The government’s market revitalization efforts have been finally showing effect, halting the further decrease in trading volume. On the other hand, drastic changes are necessary if Japan is to serve as a main market in Asia.

2. In such a situation, stakeholders are increasingly interested in what comprises a

comprehensive market. Aiming to set up a new framework for attaining such a comprehensive market that would handle securities, financial instruments and commodities in an integrated manner, the government has had two measures, “Realizing the New Growth Strategy 2011” and the “Basic Strategy for Revitalizing Japan” approved as a cabinet decision. In November 2011, the Tokyo Stock Exchange and the Osaka Stock Exchange announced that they were aiming at business integration. With these conditions, in addition to the 2009 amendments that allowed commodity exchanges under the same holding firm as stock and financial exchanges, it has become necessary to create an appropriate legal framework to smoothly set up and operate comprehensive markets that will deal with securities, financial instruments and commodities in an integrated manner.

3. In addition, at the end of May 2012, related parties agreed that the agricultural

products market of the Tokyo Grain Exchange will be transferred to the Tokyo Commodity Exchange and the Kansai Commodities Exchange. Smoother transfer will lead to the enhancement of consumer protection, which will in turn revitalize Japan’s commodity market under a new market framework.

4. In addition, for the revitalization and sound development of Japan’s commodity

market, the government should, in addition to efforts for developing a healthier

4

market by protecting consumers, launch its active efforts for improving market liquidity, such as improving services available from exchanges and expanding the number and type of diversified market participants. Exchanges around the world have been pushing ahead with international collaborations and international trading volume to mitigate cost burdens and improve their user-friendliness for customers. Paying attention to avoid brakes on the formation of comprehensive markets, Japan should examine how to appropriately respond to globalized commodity futures markets as mentioned above.

5. In response to questions raised by the Minister of Agriculture, Forestry and Fisheries

and the Minister of Economy, Trade and Industry about constructing a commodity market capable of addressing environmental changes in February 2012, this subcommittee has held meetings six times in total and has compiled this report, while paying attention to the aforementioned trends.

5

Chapter 2: Framework for Establishing Comprehensive Exchanges 1. Background and objectives

As a part of market revitalization projects, analysts point out the importance of establishing a comprehensive exchange. The 2009 law amendment mentioned above already created a new framework that allowed the mutual entry of commodity exchanges and financial instruments exchanges (i.e., stock/financial instruments exchanges coexisting with commodity exchanges under the same holding firm), but this time the government further intends to establish a new framework for establishing/operating comprehensive exchanges dealing with securities, financial instruments and commodities in an integrated manner (e.g., integrating the commodity exchange with the financial instruments exchange through merger or business transfer), aiming to further improve user-friendliness and liquidity in the commodity market as a whole. 2. Comprehensive exchanges that will deal with securities, financial instruments and commodities in integrated manner

To establish comprehensive exchanges, policymakers should, while paying attention to the legal amendments to date, integrate regulatory and supervisory programs for comprehensive exchanges dealing with securities, financial instruments and commodities (except for some commodities, such as rice) in an integrated manner (e.g., integrating the commodity exchange with the financial instruments exchange through merger or business transfer) for the near term and should have in mind the following framework to maintain mutual collaborations among such comprehensive exchanges. (1) Exchanges

1) As several authorities will exercise their supervisory powers over the aforementioned exchanges at the same time, these overlapping supervisory powers should be unified. In this process, policymakers should establish a new framework in accordance with Financial Instruments and Exchange Act, which covers a wide variety of financial products.

2) On the other hand, METI should keep serving as the ministry responsible for commodities to certain extent from the commodity market’s industrial policy perspectives: appropriately coping with product characteristics, including product

6

deliveries at the time of petroleum trades, taking emergency responses to sharp commodity price fluctuations that might pose adverse impacts on people’s daily life, and working on screening commodities that will get listed at the said commodities exchange.

(2) Regulations on business operators

1) Commodity futures business operators that tap into the said exchange are regarded as financial instruments business operators as set forth in Financial Instruments and Exchange Act in the same manner as securities firms dealing with financial products.

2) However, policymakers should set up necessary special measures for business operators only handling commodity futures so that the present commodity futures business operators will be able to smoothly join the said exchange and continue engage in their trading practices.

3) Commodity futures traders only engaging in self-account trading should keep a similar status as set forth in the Commodity Derivatives Act so that they will able to continue smooth trading in the future.

(3) Others

1) As for clearing organizations for the said exchange, policymakers should basically examine the feasibility of integrating securities/financial instruments clearing practices with commodity futures clearing practices into a single framework from the viewpoint of user friendliness for investors. However, as these two trading categories have different a mix of clearing services participants and clearing practices, the present commodity futures clearing organizations will continue providing clearing services for commodity trading at the said exchanges.

2) As for the insurance cap for trading at the said exchanges, policymakers should basically create a new framework as an investor protection fund as set forth in the Financial Instruments and Exchange Act. However, since such a framework will require market participants to redundantly join two protection funds, there should be a temporary special measure to exempt commodity futures business operators from joining the investor protection fund if they have already joined the consumer protection fund.

7

3. Bill for Partial Revision of Financial Instruments and Exchange Act

At its second meeting, the Commodity Futures Trading Subcommittee has released the report “Possible Framework for Comprehensive Exchanges” as its interim opinion on comprehensive exchanges dealing with securities, financial instruments and commodities in an integrated manner. Based on such an interim opinion, the government submitted the “Bill for Partial Revision of Financial Instruments and Exchange Act” to the Diet on March 9, 2012.

8

Chapter 3: Possible Actions for the Revitalization and Sound Development of the Commodity Futures Market

Through successively enhancing consumer protection schemes, the number of consumer complaints and counseling cases in trading on the commodity futures market and the foreign commodity market decreased by half in 2010 from a peak in 2004. As it further decreased by 50% on a year-on-year basis (or 1/4 from the peak level) in 2011 after the most recent law amendment (effective on January 1, 2011), troubles in the market are diminishing. In particular, the number of consumer complaints and counseling cases on trading at exchanges at home is falling sharply. On the other hand, trading volume in the commodity futures market has been decreasing for seven consecutive years since 2003. The government’s market revitalization efforts have been finally showing effect, with trading volume taking an upturn to rise in 2011, but it is urgently necessary to revitalize and soundly develop the commodity futures market. To be specific, policymakers should take appropriate consumer protection measures as mentioned below and also work on market revitalization efforts by improving services available from commodity exchanges or expanding diversified market participants. I. Revitalization of Commodity Trading 1. Improving services available from commodity exchanges (1) Listing new commodities

To cope with risk hedging and investment needs for commodities at home and enhance overall liquidity, commodity exchanges should examine and put into effect the listing of new commodities. Concretely speaking, they should actively list the following commodities: Industrial or agricultural products not yet listed at home but actively traded at overseas exchanges, commodities traded for future delivery in the domestic market, commodities that were listed in the past and expected to get listed again due to changes in trading conditions, or commodities with potential needs.

As for risk hedging needs, policymakers should, while paying attention to recent

9

discussions on power utility system reforms, examine the feasibility and needs of listing power-generating fuels and, furthermore, electric power itself (electricity).

For example, they should provide transactions easily traded/delivered in small lots so that Japanese citizens will feel more comfortable and familiar with commodity trading.

(2) Developing new products attractive to individual investors

Forex (FX) and stock price index futures are actively traded online via the Internet in the financial instruments field. In the commodity futures field, it is also necessary to develop new products attractive to individual investors.

For example, these commodities would include options trading (including binaries forecasting whether or not the preset conditions will be met in a certain time period), contract day trading of gold (a commodity without the last trading day) or indexed trading (precious metals, etc.).

Programming-based automatic trading is used for forex purposes or for commodity futures self-account trading at proprietary trading firms. In addition, policymakers should create a new framework in which individual investors will be able to use programming-based automatic trading for their trading entrusted with commodity futures business operators.

(3) Flexible spot commodity delivery program

Commodities are basically delivered at designated delivery location (a specified warehouse, etc.), but policymakers should address diversified delivery needs to encourage use of Japan’s futures market.

For example, some commodities are imported from overseas nations, unloaded in Tokyo and then re-exported to a third nation. However, if they are able to receive these commodities at overseas warehouses and directly export them to a third nation, they will be able to reduce their transportation cost.

To allow commodity deliveries overseas, Tokyo Commodity Exchange’s delivery terms adjustment program and Tokyo Grain Exchange’s agreement early delivery program1 should cover more diversified commodities and employ more flexible delivery terms and procedures.

1 Some overseas exchanges have put in place their programs that deliver commodities on terms other than the predetermined delivery terms if contracting parties successfully form consensus (such a program is called Alternative Delivery Procedure).

10

(4) Extending trading hours at exchanges

Tokyo Commodity Exchange has extended its nighttime trading hours several times from 2008 to 2010, with the day session from 9:00 a.m. to 3:30 p.m. and the night session from 5:00 p.m. to 4:00 a.m. in the next morning. As a result, the night session accounts for approximately 40% of overall trading, while trading with overseas markets is increasing to about 30%, yielding some positive impacts leading to revitalization as well as globalization of Japan’s futures market. In addition, overseas commodity exchanges are further extending their trading hours for recent years.

To expand market participants at home and abroad, commodity exchanges should examine feasibility of further extending their trading hours, while paying attentions to specific needs, such as system services, clearing services and market participants’ needs.

(5) Trading in foreign currencies Trading in foreign currencies should be put into practice so that market participants will be able to smoothly trade with overseas markets (see III. 1.(3)).

2. Improving and upgrading operational efficiency of commodity exchanges (1) Smoothly transferring listed commodities for trading at commodity exchanges

Related parties have agreed that agricultural products market of the Tokyo Grain Exchange will be transferred to the Tokyo Commodity Exchange and Kansai Commodities Exchange. Smoother transfer will lead to enhancing consumer protection, which will in turn revitalize Japan’s commodity market under a new market framework.

As commodity markets have been seeing an upward trend in gold trading volume, it is important to revitalize oil and agricultural markets as well, aiming to yield stable business performance.

(2) Improving operational efficiency of commodity exchanges

In addition to making efforts to send up trading volume and revenues through listing new commodities and other programs as stated above, policymakers should also enhance systems operational capabilities at commodity exchanges to further reduce their trading systems cost. By clearly indicating specific quantitative indicators,

11

such as trading volume, revenues or cost when preparing or revising their medium-term plans, commodity exchanges should work on further improving their operational efficiency, including their operational cost.

In addition, commodity exchanges should also work on active sales efforts to intermediate agents and investors.

3. Enhancing clearing functions (clearing capabilities)

Japan Commodity Clearing House, Co., Ltd. (JCCH) has been working on enhancing its clearing function; strengthening its operational revenue sources or financial positions; reexamining its financial eligibility requirements for keeping high-level credibility of clearing service participants; and beefing up its risk management capability.2

With clearing organizations are widely used for over-the-counter (OTC) trading on an international scale to prevent systemic risks from getting actualized, BIS and IOSCO has revised their “Recommendations for Central Counterparties (2004 version)” and announced these recommendations as “Principles for Financial Market Infrastructures” in April 2012.3 In line with the said principles, JCCH should examine the feasibility of risk-based clearing deposit programs as anti-noncompliance revenue sources, work on further enhancing risk management capabilities, such as addressing a sharp rise in risks during trading hours, and should make efforts to further beef up their financial positions to expand business operations, including OTC trading-related clearing services in the future. II. Expansion of diversified market participants 1. Expanding market participants 2 As for anti-noncompliance revenue sources, if a clearing service participant with the largest risks for losses falls into insolvency, necessary funds will be provided from a settlement non-performance reserve in which retained earnings are reserved (approximately ¥ 2.2 billion) as well as reserve fund for the commodity exchange’s compensation for loss (about ¥ 2.6 billion), and clearing deposits put by clearing service participants for guaranteeing the performance of obligations (approximately ¥ 9.5 billion). 3 The principles call for further enhancement of the clearing organization’s risk management capabilities. If the clearing organization provides a wide variety of diversified clearing services, the principles require the clearing organization to maintain anti-noncompliance revenue sources at a higher level than in the past and to appropriately address the sharp fluctuation of risks during trading hours.

12

(1) Commodity futures traders

To improve the user-friendliness for commodity futures traders that engage in commodity trading-related risk hedging, it is necessary to provide more flexible delivery terms/procedures, including actualizing commodity deliveries overseas (to reprint).

As the present applicable laws prohibit discretionary account transactions, commodity futures business operators have no choice but assigning full-time staff exclusively responsible for placing orders in terms of trading volume, prices, and timing. To mitigate such burdens on commodity futures traders, policymakers should reexamine the current framework to help professional commodity futures traders easily put comprehensive orders.

In addition, it is also necessary to improve the knowledge of sales staff regarding risk hedging transactions.

(2) Overseas business operators

Policymakers should work on the following projects: Actualizing direct market access in which overseas business operators are directly connecting with the exchange’s systems (see III.1.(2)); examining the feasibility of trading in foreign currencies (see III.1.(3)); and attracting overseas major commodity futures traders, financial instruments traders, institutional investors, and other investors.

Japan’s commodity market needs to improve its credibility in order to attract overseas business operators. In this sense, policymakers should work on strengthening business management capabilities and financial positions of traders and clearing service participants.

(3) Market entry from securities/financial markets

To mitigate financial instruments business operator’s market entry to the commodity futures market,4 it is necessary to mitigate paperwork burdens as set forth in the Commodity Derivatives Act, such as providing more flexible formats for submitted documents.

In addition, policymakers should also work on expanding ETFs/investment mutual 4 Customers for high-leverage financial derivatives are expected to invest in commodity futures, but there are some tough facts, with some web-based securities firms withdrawing from commodity futures market due to decreased liquidity in the commodity futures market.

13

trusts referring to prices at commodity markets. (4) Individual investors

1) To make investors are reassured, policymakers should maintain appropriate market operations by intensifying compliance among business operators, making clearer the government’s legal interpretations, and intensifying supervisory tasks through on-site inspections.

2) Sales staff in touch with individual investors protect consumers through compliance and enhance liquidity in the commodity futures market to bring out its full potential. In addition to intensifying compliance, policymakers should improve the quality of sales staff so that they will be able to appropriately respond to consumers’ questions on market conditions or asset management.

(5) Institutional investors

Many institutional investors in Japan, such as pension funds, are only investing in equities or bonds as their asset management approach.5

To pension funds, prop houses, funds and other institutional investors, policymakers should make appropriate explanations on the advantages of asset management through commodity futures, such as explanations on the fact that asset management in commodity futures (including ETFs) will show different price movements from equities or bonds and will be helpful as diversified investments.

2. Framework for improving user-friendliness and credibility (1) Setting up unified taxation system and accounts

Aiming at improving user-friendliness to encourage individual investors to invest in securities, financial instruments and commodities in a cross-sectional manner and participate in the commodity futures market, the government should unify tax rates for commodity futures trading and listed equities so that they will be able to calculate their aggregate profit/loss. In addition, the government should also work on the

5 The Government Pension Investment Fund (GPIF), which manages the reserve fund of the Welfare Pension and National Pension Plans, does not invest in commodity futures. Corporate pension plans are investing only a limited portion of their assets in the commodity future market. As of the end of March 2008, commodities accounted for only 0.14% of the total assets of 1088 members of the Pension Fund Association (reported by Bloomberg on March 12, 2009).

14

centralization of trading accounts. (2) Hedge accounting suitable for actual conditions

Some analysts point out that the current guideline has insufficient descriptions on specific cases on commodity futures trading. METI should encourage CPA associations, etc. to revise their hedge trading accounting systems to make them more suitable to actual commodity futures trading.

3. Promoting proper understanding on commodity futures market

To promote proper understanding of the commodity futures market, it is necessary to work on PR activities in news programs, newspapers or magazines, publish introductory guidebooks, and expand endowed chairs at universities, aiming to arouse further interest in investment-oriented people.

In particular, for citizens seldom recognizing the utility and potential for investment provided by the commodity futures market, it is necessary to make the current program widely understood and give easily comprehensible and careful explanations on important points to avoid potential trouble.

Policymakers should also examine the feasibility of providing market information possibly helpful for commodity investment mainly for individual investors. III. Coping with the Globalized Commodity Futures Market 1. Collaborating with overseas markets (1) International collaboration among exchanges

With the higher speeds and cost of trading systems as well as stronger needs for enhancing clearing functions, cross-border integrations and collaborations among exchanges beyond the national borders (such as standardizing systems, collaborating in clearing services, jointly listing commodities, taking a stake in partner exchanges, etc.) continue to progressing.6

6 In the financial derivatives field, international collaborations are progressing more than in the commodity futures fields in Japan. Some stock price index futures in Japan are listed at overseas markets as well, while overseas stock price index futures are also listed at domestic exchanges in Japan. In addition, overseas trading of Japan’s stock price index futures accounts for more than 50%;

15

Japan’s commodity exchanges are also seeing an increasing tendency of trading from overseas. To serve as a major market in Asia, Japan should put a high priority on enhancing relationships with overseas exchanges. The government should explore/seek international collaboration, including capital alliances, aiming at jointly listing commodities and enhancing clearing functions.

Stakeholders should keep in mind that this kind of international collaboration will not prevent our efforts to push ahead with comprehensive exchanges in Japan.

(2) Entry of overseas business operators (such as direct market access) To encourage overseas business operators to tap into trading at exchanges in Japan,

it is necessary to achieve, as soon as possible, and expand direct market access so that overseas business operators are capable of direct connection with commodity the exchange’s system.

Concretely speaking, the Tokyo Commodity Exchange is in the process of filing an application for direct market access to the Hong Kong and Dubai authorities. The exchange is also preparing to file applications to the U.S. and Singapore. These agendas are expected be fulfilled soon.

(3) Trading in foreign currencies

Trading in foreign currencies should be accepted to facilitate smoother trading with overseas markets. Since account transfer payments within the same bank branch are treated as overseas remittances under the current banking system, market participants and clearing organizations must bear the time lag burden between the bank’s acceptance of remittances and actual cash transfers in the process of fund settlements, such as receiving/sending margins. For this reason, policymakers should request banks to improve their systems and expand market participants with stronger financial positions capable of assuming such time lags.

2. Enhancing market surveillance functions

Due to stronger needs for market surveillance services on an international scale, the Ministry of Agriculture, Forestry and Fisheries (MAFF) and the Ministry of Economy, Trade and Industry (METI) are making efforts, such as signing multilateral MOUs that make it possible to set up a market surveillance unit and share information among

furthermore, foreign shareholders occupy more than 50% of all shares in commodity exchanges.

16

national regulatory authorities of the International Organization of Securities Commissions (IOSCO). In addition, these ministries are continuing to participate in discussions at the IOSCO Task Force on Commodity Futures Markets. They should make further efforts to improve their market supervision/surveillance functions and make the market more transparent. 3. Expanding over-the-counter (OTC) trading (1) Collaboration between trading at exchanges and OTC trading According to a recent survey, trading firms and other market participants are

engaging in OTC trading in energy and metal sectors on a large scale. Energy-related OTC trading mainly consists of crude oil, jet fuel and light oil, while metal-related OTC trading includes gold, copper, aluminum and silver.

Policymakers should analyze how commodities actively traded on OTC are related with similar commodities traded at commodity exchanges.

(2) Improving environment for OTC trading Overseas clearing organizations are employed for OTC trading in Japan in most

cases. METI should continue hearing sessions to further examine how much overseas clearing organizations are employed, and if or not similar clearing organizations are necessary in Japan.

(3) Taking actions from international perspectives At international arena, such as the G20, national authorities are expected to make

efforts for improving the transparency of OTC trading markets and mitigating systemic risks. It is beneficial to continue specifically and quantitatively identifying OTC trading in Japan.

IV. Solicitation Rules 1. Ban on unsolicited offers

As the number of consumer complaint cases on commodity futures trading has been steadily decreasing, successive legal amendments on solicitation rules, including the

17

ban on unsolicited offers, as well as stakeholder compliance efforts are showing effects to a certain extent.

Since the ban on unsolicited offers has been effective only for a year and a half, it is rather difficult to identify the relationship between the decrease in counseling/harmful cases and the ban on unsolicited offers. In this context, METI should analyze possible effects as much as possible, while keeping paying careful attention to actual conditions.

Then, before reexamining prohibited acts under the ban on unsolicited offers, policymakers should check that intensifying consumer protection has been taking root in reality and that additional restrictions other than the ban on unsolicited offers are unlikely to lead to an increase in the number of harmful cases.

When introducing the ban on unsolicited offers, lawmakers in both the House of Representatives and Councilors passed an additional resolution that policymakers should reexamine the rules set forth in government ordinances as necessity and expand the ban to all trading with individual customers in general about one year after the ban is put into practice, while paying attention to effects of regulations and actual conditions of harmful cases. As of this moment, it is unnecessary to expand the ban in this way, and policymakers should continue to monitor the effects of the restriction and actual circumstances of harmful cases. 2. Possible approach on solicitation rules

To apply legal restrictions more efficiently and effectively, it is necessary to set up appropriate restrictions suitable to individual cases as mentioned below.

(1) Making clear operational rules

1) METI should strive to actively make the ban on unsolicited offers widely known to commodity futures business operators as well as consumers.

2) In line with analysts’ opinions that they need clearer details on solicitation rules, METI will accumulate and analyze specific cases and need to address specific needs of consumers and commodity futures business operators about clarifying the solicitation rules. In this process, METI should make clearer responses than in the past and suggest easily understandable solicitation rules as necessary.

(2) Enhancing voluntary regulations

1) To apply the solicitation rules, including the ban on unsolicited offers, more

18

effectively, the government should serve as a regulatory agency, while self-regulatory organizations should also take active efforts, such as giving instructions and supervisory services for preventing trouble. Based on these actions, commodity futures business operators should also improve their compliance practices.

2) In particular, policymakers should, for example through the central government’s inspection-related basic policy documents, get across the fact it is important to intensify compliance awareness among sales staff because they play important roles in actual solicitation activities. It is also necessary to check out at the central government’s inspections whether or not they are actually intensifying compliance awareness among sales staff. In addition, self-regulatory organizations should take further actions to improve the quality of sales staff.

(3) Solicitation practices suitable to customer’s knowledge level or experiences

1) As for persons with experience in commodity futures trading or similar trading, it is appropriate to put in place solicitation rules more suitable to actual conditions. In other words, with comprehensive exchanges coming in sight as well as the number of business operators anticipated to expand, policymakers should clarify the ban on unsolicited offers applicable to customers that have already engaged in trading of investment products with certain risks.

2) When checking out the principle of suitability, METI should make it clear that holistic decision-making is acceptable in line with specific factors, such as age, revenues and assets. In addition, commodity futures business operators should have an internal administrative section to carefully double-check such holistic decisions.

19

Conclusion As for suggestions included in this report, the subcommittee will examine possible actions in detail, such as revitalizing the commodity market or expanding OTC trading, from professional perspectives, make decisions on specific actions, and hold the subcommittee meeting within this fiscal year to report on specific actions taken.

20

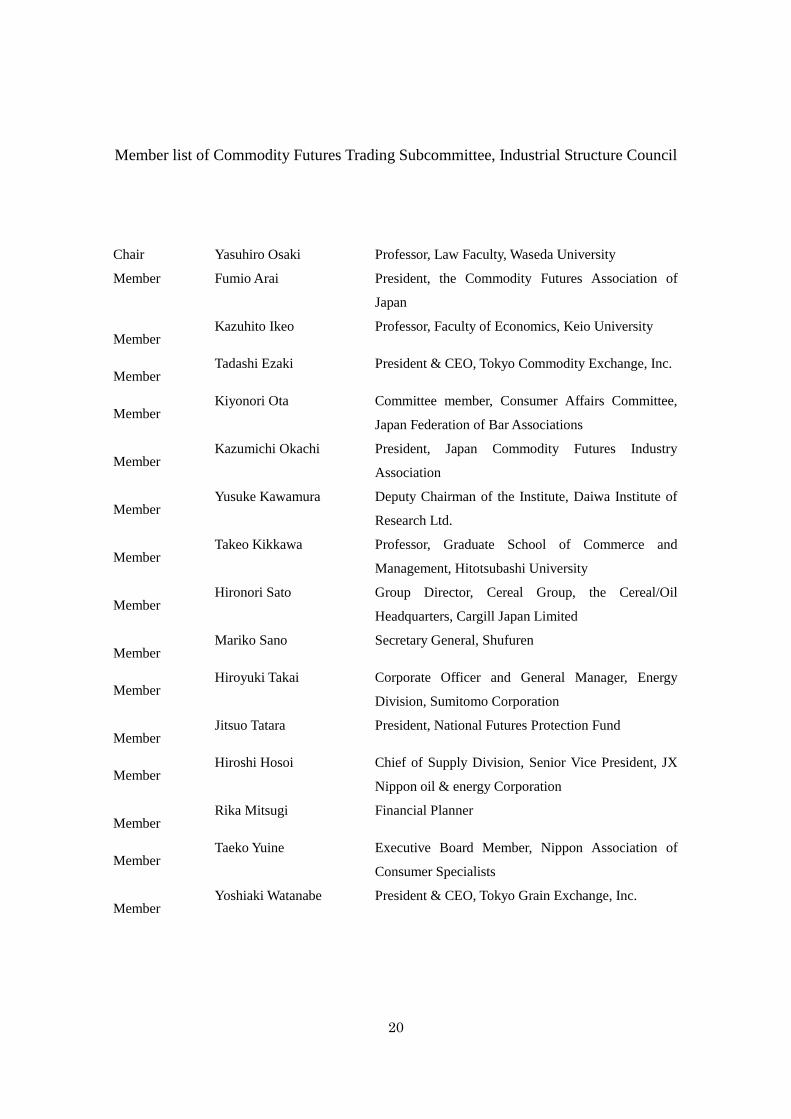

Member list of Commodity Futures Trading Subcommittee, Industrial Structure Council

Chair Yasuhiro Osaki Professor, Law Faculty, Waseda University

Member Fumio Arai President, the Commodity Futures Association of

Japan

Member Kazuhito Ikeo Professor, Faculty of Economics, Keio University

Member Tadashi Ezaki President & CEO, Tokyo Commodity Exchange, Inc.

Member Kiyonori Ota Committee member, Consumer Affairs Committee,

Japan Federation of Bar Associations

Member Kazumichi Okachi President, Japan Commodity Futures Industry

Association

Member Yusuke Kawamura Deputy Chairman of the Institute, Daiwa Institute of

Research Ltd.

Member Takeo Kikkawa Professor, Graduate School of Commerce and

Management, Hitotsubashi University

Member Hironori Sato Group Director, Cereal Group, the Cereal/Oil

Headquarters, Cargill Japan Limited

Member Mariko Sano Secretary General, Shufuren

Member Hiroyuki Takai Corporate Officer and General Manager, Energy

Division, Sumitomo Corporation

Member Jitsuo Tatara President, National Futures Protection Fund

Member Hiroshi Hosoi Chief of Supply Division, Senior Vice President, JX

Nippon oil & energy Corporation

Member Rika Mitsugi Financial Planner

Member Taeko Yuine Executive Board Member, Nippon Association of

Consumer Specialists

Member Yoshiaki Watanabe President & CEO, Tokyo Grain Exchange, Inc.

21

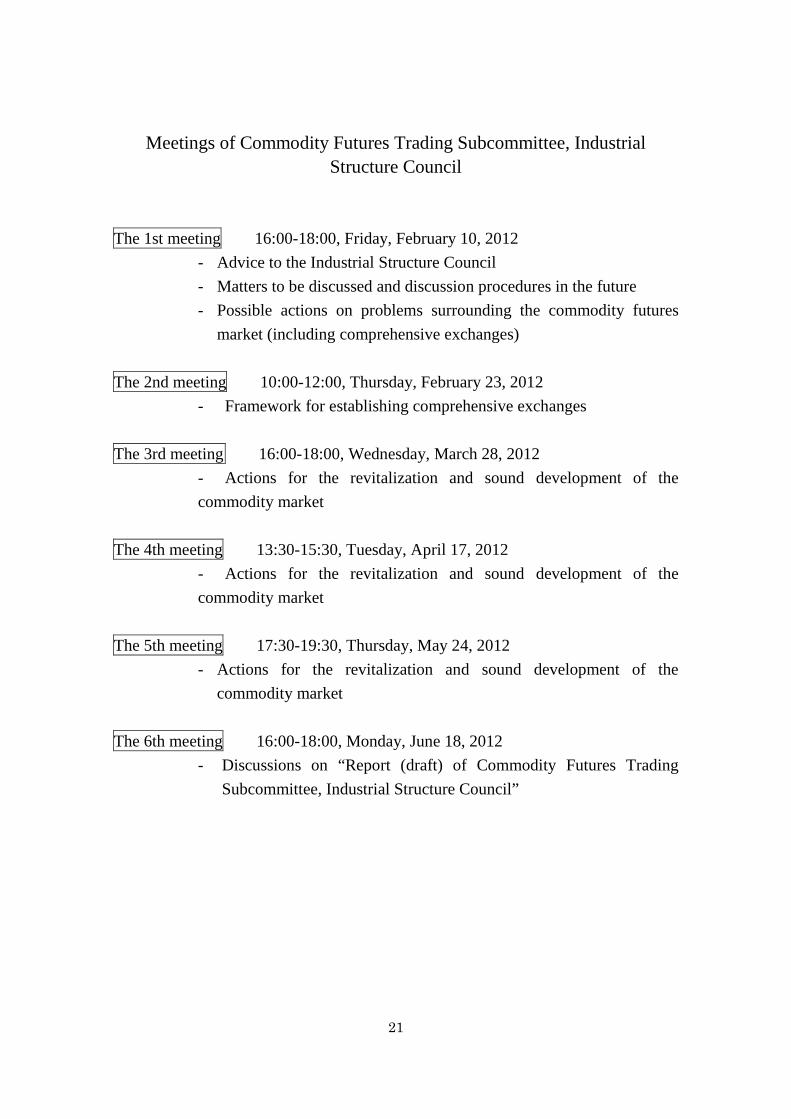

Meetings of Commodity Futures Trading Subcommittee, Industrial Structure Council

The 1st meeting 16:00-18:00, Friday, February 10, 2012

- Advice to the Industrial Structure Council - Matters to be discussed and discussion procedures in the future - Possible actions on problems surrounding the commodity futures

market (including comprehensive exchanges) The 2nd meeting 10:00-12:00, Thursday, February 23, 2012

- Framework for establishing comprehensive exchanges The 3rd meeting 16:00-18:00, Wednesday, March 28, 2012

- Actions for the revitalization and sound development of the commodity market

The 4th meeting 13:30-15:30, Tuesday, April 17, 2012

- Actions for the revitalization and sound development of the commodity market

The 5th meeting 17:30-19:30, Thursday, May 24, 2012

- Actions for the revitalization and sound development of the commodity market

The 6th meeting 16:00-18:00, Monday, June 18, 2012

- Discussions on “Report (draft) of Commodity Futures Trading Subcommittee, Industrial Structure Council”