Embed Size (px)

Citation preview

© OECD/IEA, 2016

Renewable energy markets and global climate goals

Nordic cleantech cooperation in Africa:

Needs, opportunities, challenges and solutions COP22, Marrakech November 9, 2016

Liwayway Adkins

Environment and Climate Change Unit International Energy Agency

© OECD/IEA, 2016

The IEA works around the world to support an

accelerated clean energy transition that is

enabled by real-world SOLUTIONS

supported by ANALYSIS

and built on DATA

© OECD/IEA 2015

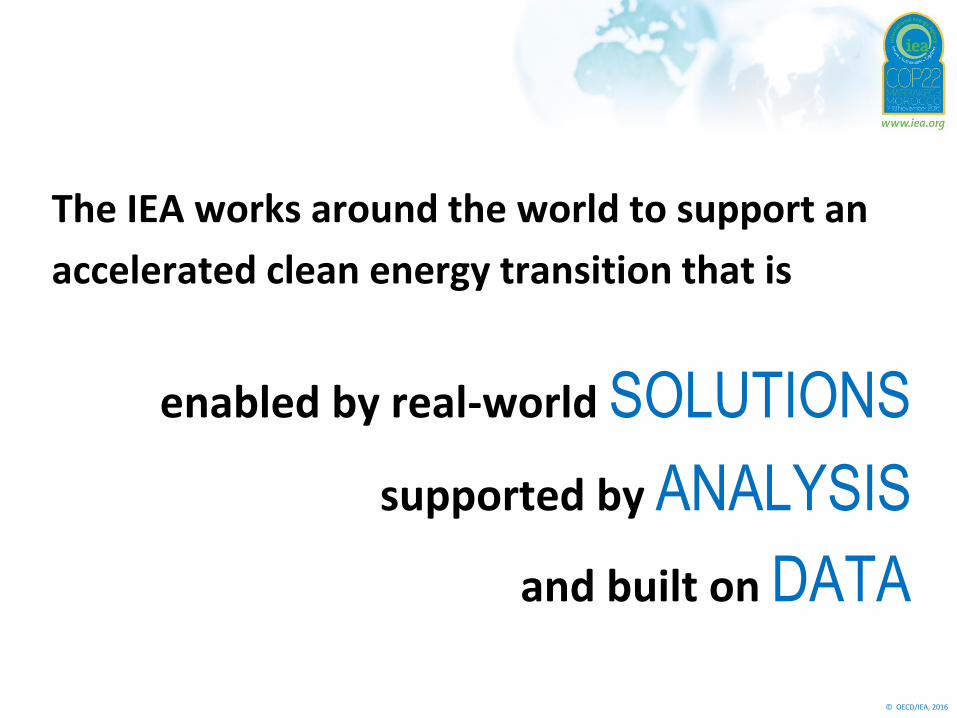

IEA strategy to raise climate ambition Peak in emissions (Bridge Scenario)

Global energy-related GHG emissions

20

25

30

35

40

2000 2014 2020 2025 2030

Gt

CO

2-e

q

Bridge Scenario

INDC Scenario

49%

17%

15%

10%

Savings by measure, 2030

Energy efficiency

Reducing inefficient coal

Renewables investment

Upstream methane reductions

Fossil-fuel subsidy reform

9%

Five measures – shown in a “Bridge Scenario” – achieve a peak in emissions around 2020, using only proven technologies & without harming economic growth

© OECD/IEA, 2016

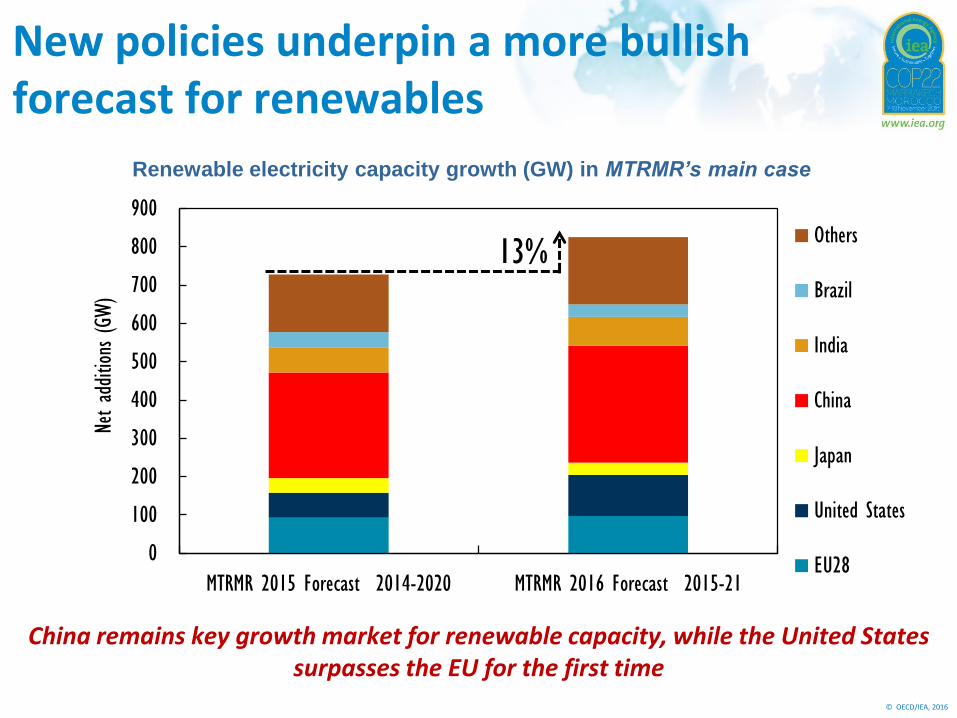

New policies underpin a more bullish forecast for renewables

China remains key growth market for renewable capacity, while the United States surpasses the EU for the first time

Renewable electricity capacity growth (GW) in MTRMR’s main case

13%

0

100

200

300

400

500

600

700

800

900

MTRMR 2015 Forecast 2014-2020 MTRMR 2016 Forecast 2015-21

Net ad

ditio

ns (GW

)

Others

Brazil

India

China

Japan

United States

EU28

© OECD/IEA, 2016

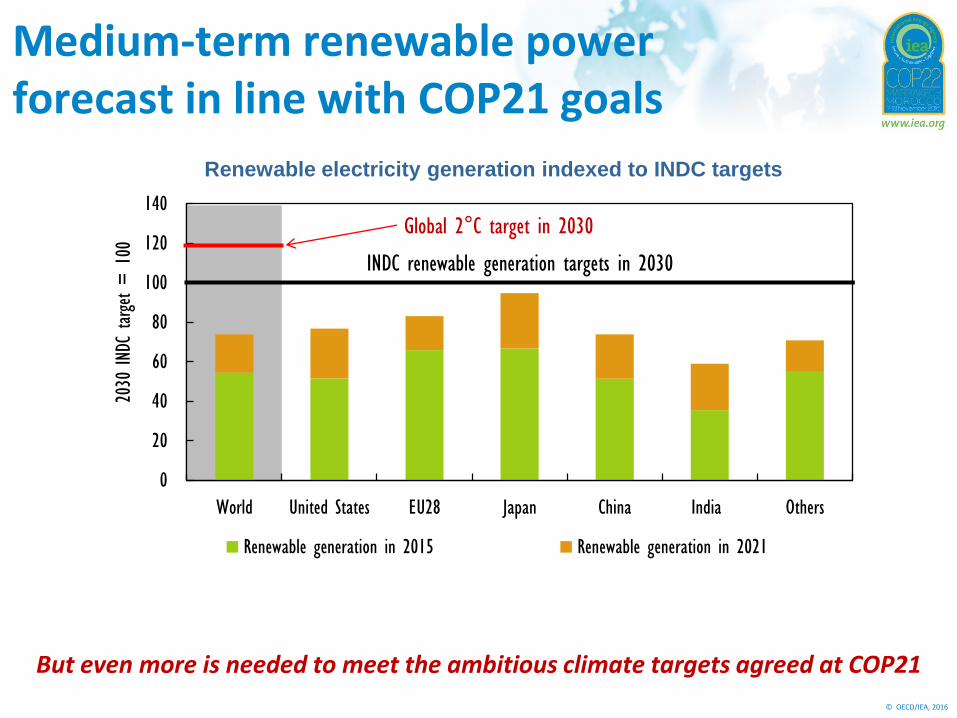

Medium-term renewable power forecast in line with COP21 goals

But even more is needed to meet the ambitious climate targets agreed at COP21

Renewable electricity generation indexed to INDC targets

0

20

40

60

80

100

120

140

World United States EU28 Japan China India Others

2030

IND

C target =

100

Renewable generation in 2015 Renewable generation in 2021

INDC renewable generation targets in 2030

Global 2°C target in 2030

© OECD/IEA, 2016

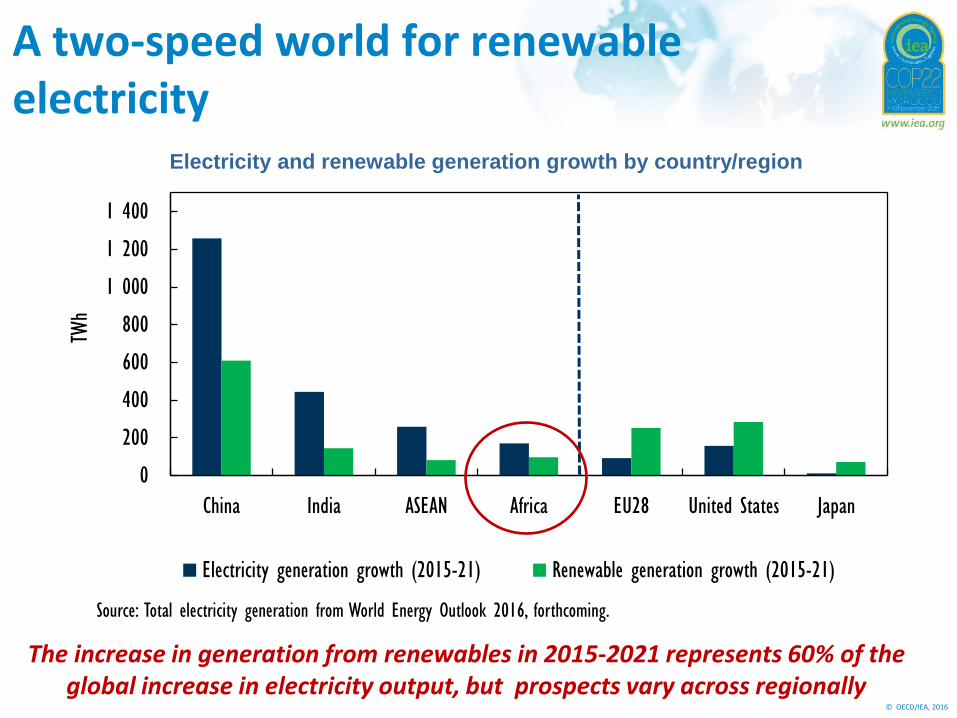

A two-speed world for renewable electricity

The increase in generation from renewables in 2015-2021 represents 60% of the global increase in electricity output, but prospects vary across regionally

Electricity and renewable generation growth by country/region

0

200

400

600

800

1 000

1 200

1 400

China India ASEAN Africa EU28 United States Japan

TWh

Electricity generation growth (2015-21) Renewable generation growth (2015-21)

Source: Total electricity generation from World Energy Outlook 2016, forthcoming.

© OECD/IEA, 2016

0

20

40

60

80

100

120

140

2009-15 2015-21

Gene

ratio

n grow

th (TW

h)

Fossil

Fuels/Other

Hydropower

Other

Renewables

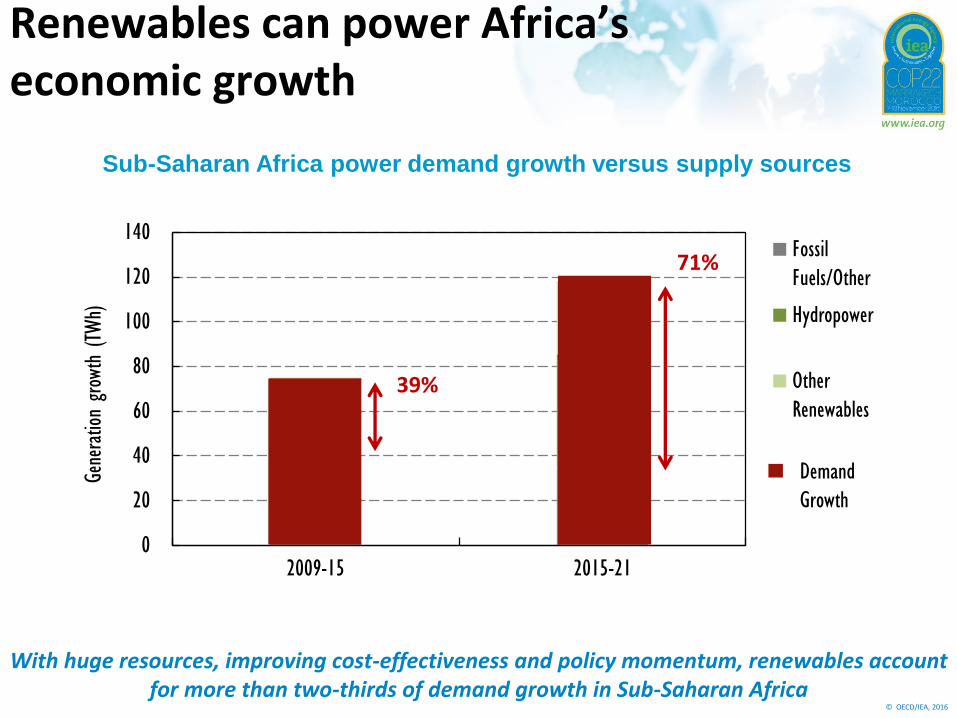

Renewables can power Africa’s economic growth

With huge resources, improving cost-effectiveness and policy momentum, renewables account for more than two-thirds of demand growth in Sub-Saharan Africa

Sub-Saharan Africa power demand growth versus supply sources

Demand

Growth

39%

71%

© OECD/IEA, 2016

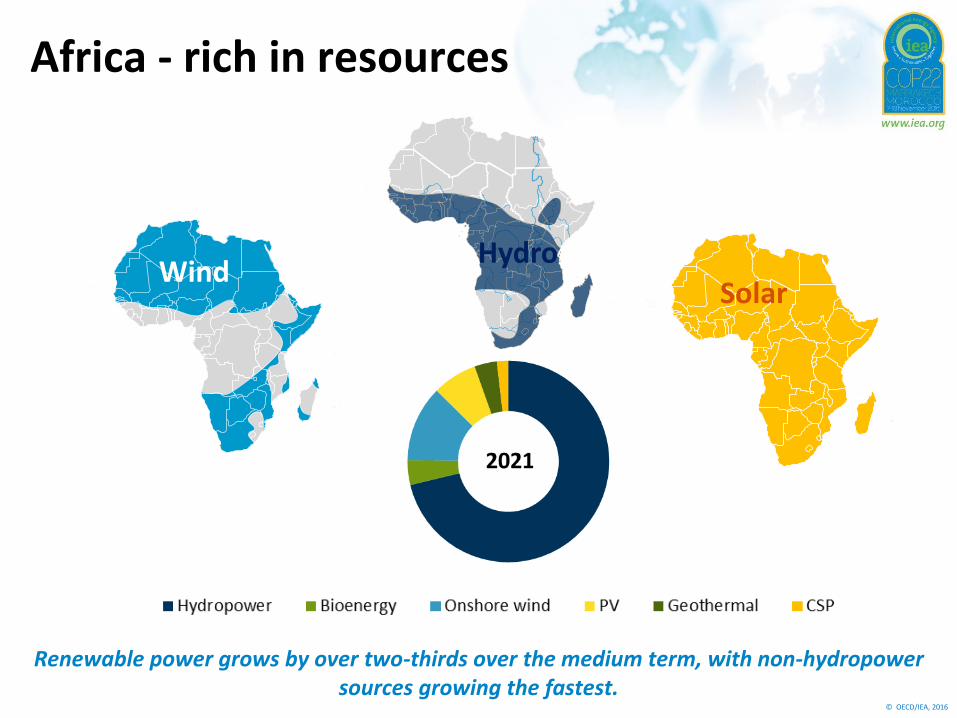

Africa - rich in resources

Hydro Wind

Solar

Renewable power grows by over two-thirds over the medium term, with non-hydropower sources growing the fastest.

© OECD/IEA, 2016

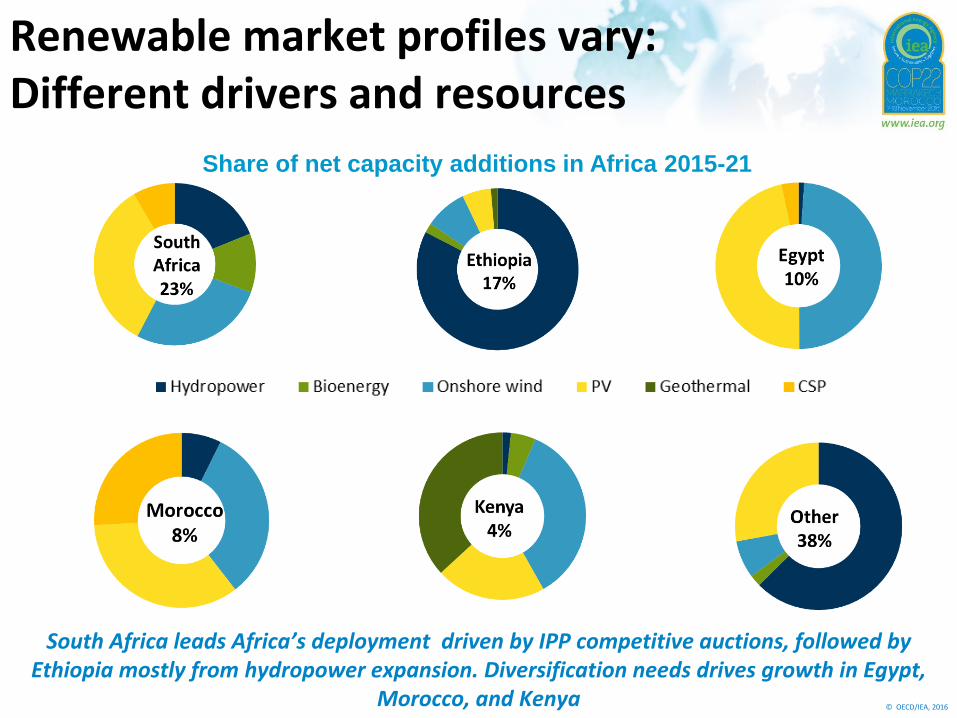

Renewable market profiles vary: Different drivers and resources

South Africa leads Africa’s deployment driven by IPP competitive auctions, followed by Ethiopia mostly from hydropower expansion. Diversification needs drives growth in Egypt,

Morocco, and Kenya

Share of net capacity additions in Africa 2015-21

© OECD/IEA, 2016

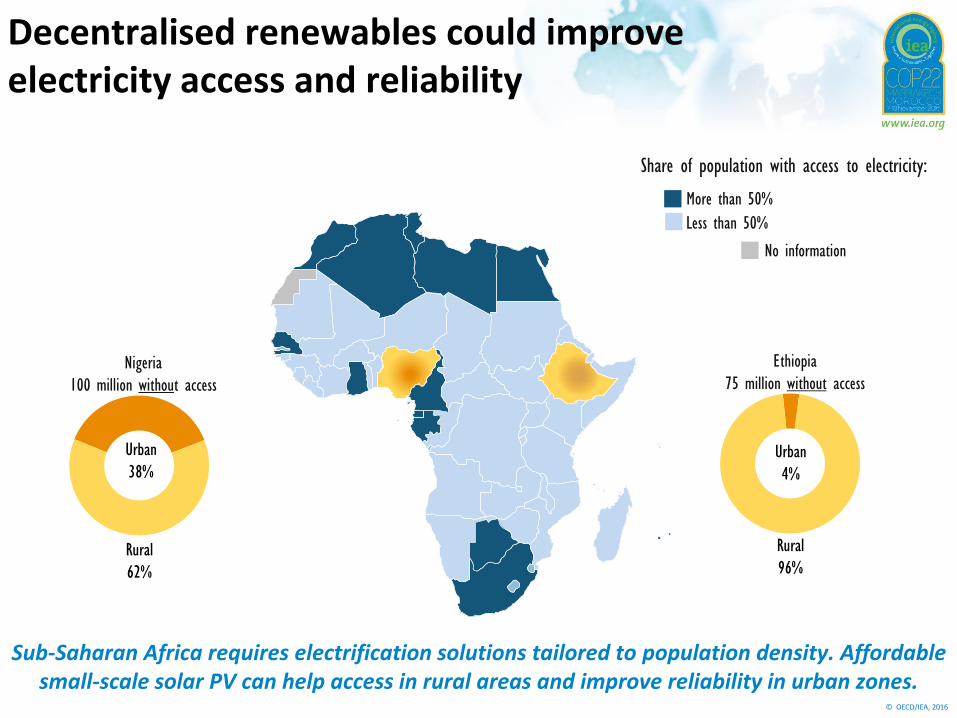

Decentralised renewables could improve electricity access and reliability

Sub-Saharan Africa requires electrification solutions tailored to population density. Affordable small-scale solar PV can help access in rural areas and improve reliability in urban zones.

Less than 50%

More than 50%

No information

Share of population with access to electricity:

Urban

38%

Rural

62%

Urban

4%

Rural

96%

Nigeria

100 million without access

Ethiopia

75 million without access

© OECD/IEA, 2016

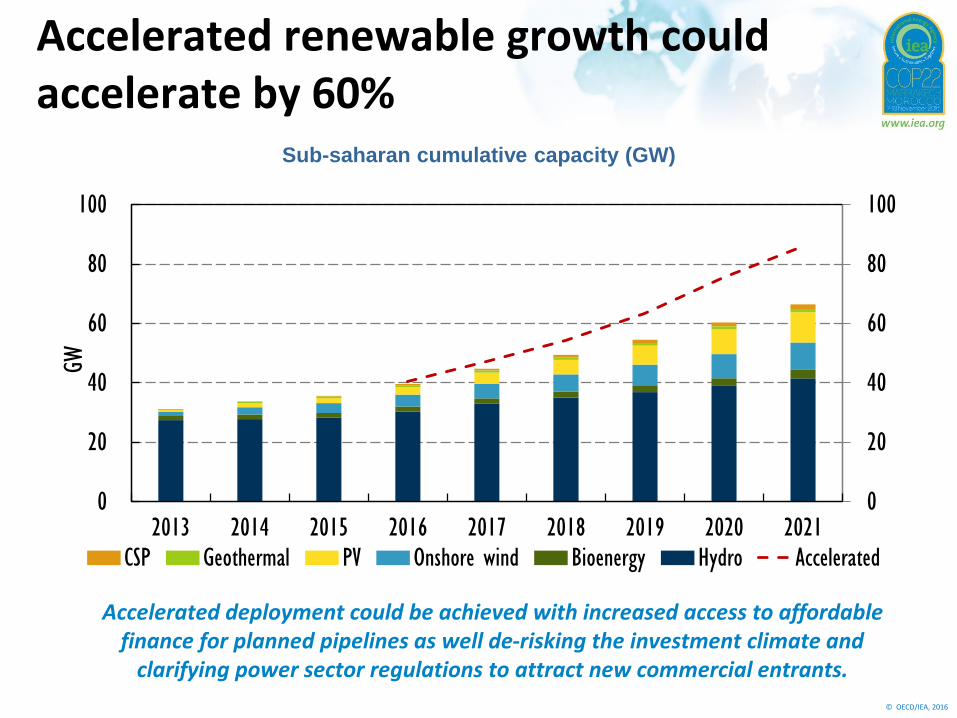

Accelerated renewable growth could accelerate by 60%

Accelerated deployment could be achieved with increased access to affordable finance for planned pipelines as well de-risking the investment climate and

clarifying power sector regulations to attract new commercial entrants.

Sub-saharan cumulative capacity (GW)

0

20

40

60

80

100

0

20

40

60

80

100

2013 2014 2015 2016 2017 2018 2019 2020 2021

GW

CSP Geothermal PV Onshore wind Bioenergy Hydro Accelerated

© OECD/IEA, 2016

Thank you