Embed Size (px)

Citation preview

April, 2014

For Financial Representatives’ General Information only. Not for inspection by, distribution or quotation to the general public. This document reflects the views of AllianceBernstein and sources

believed by AllianceBernstein L.P. to be reliable as of the dates cited. No representation or warranty is made concerning the accuracy of cited data. Nor is there any guarantee that any projection, forecast or

opinion will be realized. The views expressed may change at any time. References to stocks, securities or investments should not be considered recommendations to buy or sell. The value of investments,

and the income from them, can fall as well as rise and you may not get back the original amount invested. Past performance is not a guide to future performance. The value of overseas securities will be

subject to exchange-rate fluctuations. Under no circumstances should this information be construed as investment advice nor should it be construed as sales or marketing material for any financial

instrument, product or service sponsored or provided by AllianceBernstein or its affiliates or agents.

©2014 AllianceBernstein L.P.

Relatively Stable Value in a Relatively Unstable World AllianceBernstein Fixed Income

Hayden Briscoe

Senior Vice President—Director Asia Pacific Fixed Income

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public 1

Video

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

Despite Bad Press, China Provides Stability to the Region

2

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

China Reform: Rebalancing, Not Hard Landing

3

20

25

30

35

40

45

50

55

79 83 87 91 95 99 03 07 11 15 19

(% of GDP)

Investment Rate

Consumption Ratio

Saving Rate

3

Current analysis does not guarantee future results

As of September 30, 2013

Source: CEIC Data, AllianceBernstein and Bernstein Research

0

10

20

30

40

50

60

70

80

90

60 65 70 75 80 85 90 95 00 05 10 15 20 25 30 35 40

(%)

China

South Korea

Taiwan

Japan

Economic Structure Evolvement

Rural Workers’ Share of Total

Employment

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

China Big Trend: Urbanization and Construction

4

The project is on the street ! Jinmao Palace(金茂府) Near Park Hyatt in Beijing Best-selling project last year, by Franshion

2015

2005

2025

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

Vanke 3%

Greenland 2%

Wanda 2%

POLY Real Estate 2%

China Overseas 2%

Country Garden 2%

Evergrande 2%

China Resources Land 1%

Shimao 1%

Greentown 1%

Other 20,000+ 83%

Predictable Path in a Maturing Market

5

Xingrun is a private developer.

90% of Xingrun’s development

is in Fenghua or surrounding

counties.

Only 0.1% share of CNY

6,769.5 billion market.

Source: CEIC, Alliance Bernstein, as of January 30, 2014

Other 20,000+,

83%

Chinese Developers and % Share of Market

Headline: “China Developer Xingrun Can’t Pay Debt”

Top 10 Developers, 17%

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

China’s Role is Changing from a World Manufacturer to a World Banker

6

* Based on data year-to-Oct 2013

As of 17 March 2014.

Source: : ANZ Bank, PBOC Monetary Policy Report, SWIFT and AllianceBernstein

RMB as an International (and Ultimately Reserve) Currency

Central Banks

Announced Plans

to Hold CNY Assets

22 Countries

CNY Bilateral

Cross Currency

Swap Lines

24 banks

CNY2,568 billion

Offshore RMB’s

Role as a “Trade

Currency”

Starting to Grow

Transactions*

8.7%

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

China: On the Road to Becoming a Big World Consumer Market

7

China’s Share of Total Exports of Key Trading Partners

As of 17 March 2014

Source: CEIC and AllianceBernstein

2001 2013

0

5

10

15

20

25

30

35

40

World IN ID KR MY PH SG TW TH AU JP

Pe

rcen

t o

f im

po

rts to

Chin

a

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

History Repeats Itself

8

From Bank of England… …to the Fed… …to PBOC?

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public 9

Asian Countries are Relatively Stable

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

The Biggest Risks In Emerging Markets Are Political

10

What does the future hold for Ukraine and

Russia?

Will Maduro maintain his iron

grip on Venezuela?

Will Argentina

ever reform?

Will scandal push Turkey

in a new direction?

Will World Cup 2014 be a

success or failure for Brazil?

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

Asia Lessons Learnt From Their Own Crisis

11

Historical analysis and current estimates do not guarantee future results.

As of 31 December 2013

Source: IMF and AllianceBernstein

(10)

(5)

0

5

10

15

20

Bela

rus

Tu

rkey

Ukra

ine

Moro

cco

Georg

ia

South

Afr

ica

Peru

Sri

Lan

ka

Ch

ile

India

Indo

nesia

Bra

zil

Co

lom

bia

Pola

nd

US

Egypt

Rom

ania

Mexic

o

Arg

entina

Th

aila

nd

Alg

eria

Hu

ng

ary

Chin

a

Phili

ppin

es

Vene

zuela

Russia

Mala

ysia

Kore

a

Vie

tnam

Ta

iwan

Sin

gapore

% GDP

US EEMEA

Latam Asia

Asian Countries Tend to have Current Account Surpluses

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

Which Countries Are Better Off Today Than 10 Years Ago?

12

Comm. Exporters Comm. Importers

Ch

an

ges i

n F

un

dam

en

tals

Better

Colombia

Peru

Indonesia

Mexico

Kazakhstan

Brazil

Turkey

Thailand

Poland

Romania

Philippines

Korea

Hungary

Singapore

No

Change

Chile

China, India, Taiwan

Worse

Russia

Malaysia

South Africa

Argentina

Venezuela

Ukraine

Egypt

Pakistan

Czech Republic

Based on a weighted average of indicators showing improvement or deterioration during 2003-13 in trend growth, national savings rate, net public debt to GDP, GEFR to FX reserves, institutional

quality and ease of doing business.

Source: AllianceBernstein

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

Asia Currency Basket Is Remarkably Stable

13

40

50

60

70

80

90

100

110

120

130

0

50

100

150

200

250

300

350

400

450

03 04 05 06 07 08 09 10 11 12 13 14

Currency Index and Commodity Price 2003–2014

Asia

LatAm

EMEA

Commodity Price (Left Scale)

Asia Currency

Moves in a Range

Historical analysis and current estimates do not guarantee future results.

As of 28 February 2014. Asia Currency index and LatAm Currency index are respectively represented by JP Morgan Asia and Latin America Currency Index. EMEA index is represented by

BOAML EMEA Currency Index.

Source: Bloomberg and AllianceBernstein

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

Currency Butterfly Strategy—to Further Manage the Volatility

14

Lower Beta

• CNH

• TWD

• HKD

Middle

• MYR

• THB

• SGD

• KRW

• PHP

Higher Beta

• IDR

• INR

Past analysis does not guarantee future results.

As of 13 March 2014

Source: Bloomberg and AllianceBernstein

Asia Currency Index 2012-2014

Reduce

Neutral

Take

104

106

108

110

112

114

116

118

120

122

Jun09 Dec09 Jun10 Dec10 Jun11 Dec11 Jun12 Dec12 Jun13 Dec13

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

0

2

4

6

8

10

12

US

Sin

gap

ore

Ho

ng

Ko

ng

Ta

iwa

n

Au

str

alia

Ne

w Z

ea

land

Ma

laysia

So

uth

Ko

rea

Chin

a

Th

aila

nd

Ph

ilip

pin

es M

id

Ind

ia

Ind

on

esia

Sri L

an

ka

Pa

kis

tan

Vie

tna

m

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Jan11 Jul11 Jan12 Jul12 Jan13 Jul13 Jan14

Annualiz

ed Y

ield

Asia Local Market Strategy: Positive Carry Is a Sweetener

15

Interest Rate Differentials: Asia Pacific vs. US

FX Forwards: Implied Annualized Interest Carry

Past analysis does not guarantee future results.

As of 28 February 2014

Source: Bloomberg and AllianceBernstein

FX Forward Annualized Yield

(Carry) Rolling 2 years

Carry from Interest

rate differentials

Historical Average

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

0

100

200

300

400

500A

AA

AA

+

AA

AA

–

A+ A

A–

BB

B+

BB

B

BB

B–

BB

+

BB

BB

–

B+ B

B–

CC

C+

CC

C

CC

C–

South Korea

Asia Is Not an Emerging Market Any Longer

16

1 basis point = 1/100 of a percent

Pre-Crisis data is as of 31 Dec. 2005.

The rating is calculated as the highest of the S&P and Moody’s ratings.

Source: Bloomberg, S&P and Moody’s

Indonesia

Pre-Crisis Credit Spreads and Ratings

Indonesia

Malaysia

China

Thailand

Philippines

Australia

Japan

Russia

Turkey

5 Y

ear

CD

S in B

asis

Poin

ts

Ireland Germany US Spain

France The Netherlands UK

Austria

Portugal Italy

Hungary Greece

Mexico Poland

India

Hong Kong

Developed Markets Emerging Markets

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

0

100

200

300

400

500A

AA

AA

+

AA

AA

–

A+ A

A–

BB

B+

BB

B

BB

B–

BB

+

BB

BB

–

B+ B

B–

CC

C+

CC

C

CC

C–

Australia

Russia

Turkey

5 Y

ear

CD

S in B

asis

Poin

ts

Ireland Germany US Spain

France The Netherlands UK

Austria

Portugal Italy

Hungary Greece

Mexico Poland

Thailand

Asia Is Not an Emerging Market Any Longer

17

Today’s data is as of 13 Mar. 2014.

The rating is calculated as the lowest of the S&P and Moody’s ratings.

Source: Bloomberg, S&P and Moody’s

Credit Spreads and Ratings Today

5 Y

ear

CD

S in B

asis

Poin

ts

Developed Markets Emerging Markets

Indonesia

Malaysia

China South Korea

Australia

Russia

Turkey

Ireland Germany US Spain

France The Netherlands UK

Austria

Portugal Italy

Hungary Greece

Mexico Poland

Philippines

Japan

Hong Kong

India

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public 18

Capturing Asian Opportunities in an Unstable World

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

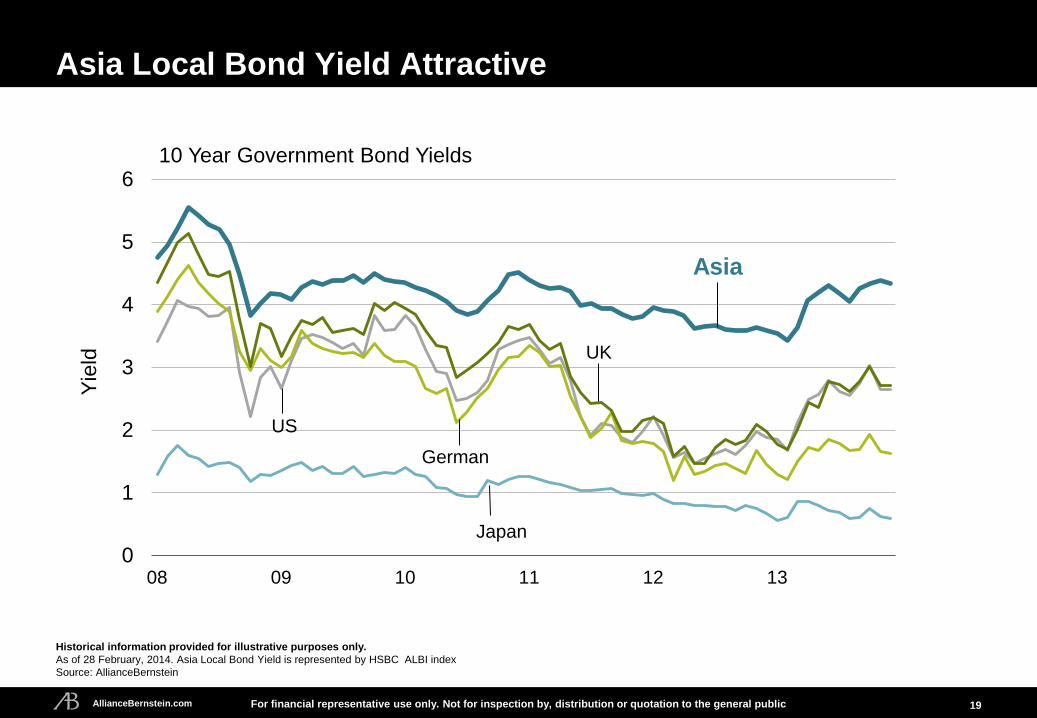

0

1

2

3

4

5

6

08 09 10 11 12 13

Yie

ld

Japan

Asia Local Bond Yield Attractive

19

Historical information provided for illustrative purposes only.

As of 28 February, 2014. Asia Local Bond Yield is represented by HSBC ALBI index

Source: AllianceBernstein

10 Year Government Bond Yields

Asia

US

UK

German

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

3

4

5

6

7

8

9

10 11 12 13 14

Asian Local Bond Opportunity: Indonesia

20

Drastic Swing in Trade Account to

Surplus Position Trade Balance

Historical analysis and current forecasts do not guarantee future results.

As of 21 February 2014

Source: CEIC and AllianceBernstein

-3

-2

-1

0

1

2

3

4

09 10 11 12 13

CPI Correction Will Provide

Room for Rate Easing Policy Rate vs. CPI

US

D B

illio

ns

Perc

ent

Policy Rate

CPI

Forecast

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

Asian Investment Grade Credit: Underappreciated Government and Corporate Linkages

21

1 basis point = 1/100 of a percent

Past performance does not guarantee future results.

As of 21 March 21 2014

Global Investment Grade Credit is Barclays Global Aggregate Credit Index, Asia Investment Grade Credit is J.P. Morgan JACI Investment Grade

Source: Barclays, J.P. Morgan, Moody’s, Morgan Stanley and AllianceBernstein

Investment Grade Credit Spread Historical Average 10 Year

Cumulative Default Rates

2 3 7

19

36

54

0 1 2 6

16

35

Aa A Baa Ba B Caa–C

Global 1920–2011 APAC 1993–2011

0

100

200

300

400

500

600

700

800

05 06 07 08 09 10 11 12 13

Spre

ad (

Basis

Poin

ts)

Barclays Global Agg Corp

JACI Corp IG

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

5.9

6.0

6.1

6.2

6.3

6.4

6.5Ja

n-1

2

Mar

-12

May

-12

Jul-

12

Sep

-12

No

v-1

2

Jan

-13

Mar

-13

May

-13

Jul-

13

Sep

-13

No

v-1

3

Jan

-14

Mar

-14

Spot Rate

Lower Band

Upper Band

USD/CNY

Band Widening in 2012

(from +/-0.5% to +/-1%) Band Widening in 2014

(from +/-1% to +/-2%)

China Exchange Rates: If History Is A Guide, The Change in Fixing Will Reverse To Appreciation

22

As of March 18, 2014

Source: CEIC, Alliance Bernstein

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

0

5

10

15

20

25

30

35

40

45

0

500

1,000

1,500

2,000

2,500

3,000

3,500

05 06 07 08 09 10 11 12 13 14

Perc

ent C

hange

US

D B

illio

n

FX Reserves*

RMB/USD*

(right scale)

China RMB Currency Appreciation 33%, BUT FX Reserves Up +500% Since 2005

23

Historical analysis does not guarantee future results.

*China changed FX regime to a managed float from a 10-year straight peg in July 2005. As of 31 December 2013

**As of 31 January 2014.

Source: CEIC Data and AllianceBernstein

Current Account Surplus** Cumulative Change of FX

Reserves and RMB/USD

China Trade surplus

(12-month rolling sum)

100

150

200

250

300

350

06 07 08 09 10 11 12 13 14

US

D B

illio

n

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

0

1

2

3

4

5

Dec 10 Apr 11 Aug 11 Dec 11 Apr 12 Jul 12 Nov 12 Mar 13 Jul 13 Oct 13 Feb 14

Yie

ld

China Bond Strategy: Dim Sum Market Yields Normalization

24

China Onshore Government Bond Yield

Dim Sum Government Bond Yield

As of 21 March 2014

Source: HSBC , Bloomberg

Today’s Challenge: Dim Sum yields low relative to onshore

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

* China Income Portfolio Characteristics 3 Years Duration, Government & Policy Bank Exposure

Yield 5.20%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

JG

B's

US

Govt

bo

nds

Euro

Agg

.(g

ovt/cre

dit)

US

Ag

g. (g

ovt/cre

dit)

UK

Ag

g. (g

ovt/cre

dit)

Asia

n L

oca

l B

on

ds

CH

INA

Inco

me

US

Hig

h Y

ield

EM

Bon

ds (

Plu

s)

Build Income in China

0

1

2

3

4

5

6

2008 2009 2010 2011 2012 2013

Yie

ld

US Japanese German

UK Chinese

Chinese Onshore Bonds: Attractive Yields and You’re Not Invested!

25

Erin

Fuller

* A model portfolio for illustration purpose only.

Historical analysis does not guarantee future results.

Through 31 March 2014. Emerging Market Bonds (Plus) is represented by JP Morgan EMBI+ index. Others bond index are represented by responding Barclays bond index.

Source: Barclays, JPMorgan, Alliance Bernstein, Bloomberg and Citi Group

Yields Are Attractively Priced: 5 Year Government Bond Yields

0

1

2

3

4

5

6

2008 2009 2010 2011 2012 2013

Yie

ld

Build Income in China

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

JG

B's

US

Govt

bo

nds

Euro

Agg

.(g

ovt/cre

dit)

US

Ag

g. (g

ovt/cre

dit)

UK

Ag

g. (g

ovt/cre

dit)

Asia

n L

oca

l B

on

ds

CH

INA

Inco

me

US

Hig

h Y

ield

EM

Bon

ds (

Plu

s)

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public 26

A Word About Risk

Fixed-Income Securities Risk. Investment in the fixed-income portfolios entails certain risks. Past performance is

not a guide to future performance. Investment returns and principal value of these funds will fluctuate so that an

investor’s shares, when redeemed, may be worth more or less than their original cost. The value of underlying

fixed-income investments of a portfolio can vary dramatically, in response to the activities and results of individual

companies or because of general market and economic conditions and changes in currency exchange rates. The

value of a portfolio’s investments may decline over short- or long-term periods. Specific fixed-income risks include

interest rate risk, lower-rated and unrated investments risk, prepayment risk, sovereign debt obligations risk,

corporate debt risk. These and other risks are described in a fund’s prospectus. Prospective investors should read

the prospectus carefully and discuss risk and the portfolio’s fees and charges with their financial adviser to

determine if the investment is appropriate for them.

This document is provided for informational purposes only and is not intended to be an offer or solicitation, or the

basis for any contract to purchase or sell any security or other instrument, or for AllianceBernstein to enter into or

arrange any type of transaction as a consequence of any information contained herein. Under no circumstances

may any information contained herein be construed as investment advice.

The information herein reflects prevailing market conditions and our judgments as of the date of the presentation,

which are subject to change. In preparing this presentation, we have relied upon and assumed, without

independent verification, the accuracy and completeness of all information available from public sources. No

representation or warranty is made concerning the accuracy of cited data. Opinions and estimates may be

changed without notice and involve a number of assumptions which may not prove valid. In addition, there can be

no guarantee that any projection, forecast or opinion in these materials will be realised. Neither this presentation

nor any of its contents may be used for any purpose without the consent of AllianceBernstein.

AllianceBernstein.com For financial representative use only. Not for inspection by, distribution or quotation to the general public

Disclosures and Important Information

27

Past performance is not a guide to future performance. The value of investments and the income from them can fall as well as rise and you may not get back the original amount invested. The value of non-domestic securities may be subject to exchange-rate fluctuations. The views and opinions expressed in this presentation are based on AllianceBernstein’s internal forecasts and should not be relied upon as an indication of future market performance or any guarantee of return from an investment in any AllianceBernstein services. Disclosure on Security Examples References to specific securities are presented to illustrate the application of our investment philosophy only and are not to be considered recommendations by AllianceBernstein. The specific securities identified and described in this presentation do not represent all of the securities purchased, sold or recommended for the portfolio, and it should not be assumed that investments in the securities identified were or will be profitable. AllianceBernstein® and the AB logo are registered trademarks and service marks used by permission of the owner, AllianceBernstein L.P. ©2014 AllianceBernstein L.P. www.alliancebernstein.com

AllianceBernstein ® and the AB logo are registered trademarks and service marks used by permission of the owner, AllianceBernstein L.P.

© 2014 AllianceBernstein L.P.

www.alliancebernstein.com 14-0022