Embed Size (px)

Citation preview

ReinsuranceFinancial Concerns

Frank J. Maffa, CFE, CIE

Vice President

American Re-Insurance

Company

22

AgendaAgenda Reinsurance

Regulatory Concerns

Reinsurance Program

Reinsurance Contracts

Credit for Reinsurance

Reinsurance Accounting

Reinsurance Reporting

Reinsurance Collateral

Reinsurance Audit

Security Analysis

33

ReinsuranceReinsurance

Reinsurance is Management tool.• Manage Underwriting Risk

•Capacity / Spreading RiskAbility to write more premium while

maximizing principle of insurance.•Loss Control / Catastrophe Protection

Minimize financial impact from losses.

• Manage Financial Aspects•Financing

Providing financial resources for growth.•Stabilization

Minimize variations in financial results.

44

Regulatory ConcernsRegulatory ConcernsReinsurance is International

Many participants all over the world.Who are the participants? How financially strong are they? Is the risk, and the funds, retroceded and re-retroceded? How do we know who has the ultimate responsibility/obligation?Do the insurance laws of foreign countries/jurisdictions equally protect the claimants, the policyholder, and the regulator?

Reinsurance ContractsContracts are not of standard form.Are all safeguards included in the contract?Will reinsurer be able to deny coverage through technicality?Who will reside over disputes and which laws will govern?Is the regulator protected in the event of liquidation?

55

Regulatory Concerns (continued)Regulatory Concerns (continued)Collection of reinsurance / Credit risk

Reinsurance is a long term commitment.Is the reinsurer financially strong?

Affiliated reinsurance transactionsRisk remains within the groupCeding company is still responsible to pay obligation.Funds are transferred to affiliate possibly in a different country or jurisdiction.

How are funds invested? Safeguards on assets.

66

Reinsurance ProgramReinsurance Program

Understand Company’s Objectives• Spreading of Risk / Capacity

- Working Covers - Quota Share• Loss Control - Limitation of Risk

- Excess of Loss Covers- Catastrophe Protection

• Protection of Net Retention- Stop Loss Covers- Aggregate Covers

77

Reinsurance Program (Continued)Reinsurance Program (Continued)• Selection of Reinsurers

- Due Diligence- Financial Statements- Rating Agency Reports- IRIS Ratio Results

• Structure of Reinsurance Program- Beneficial Order of Contracts- Lines of Business Covered- Limits of Coverage

88

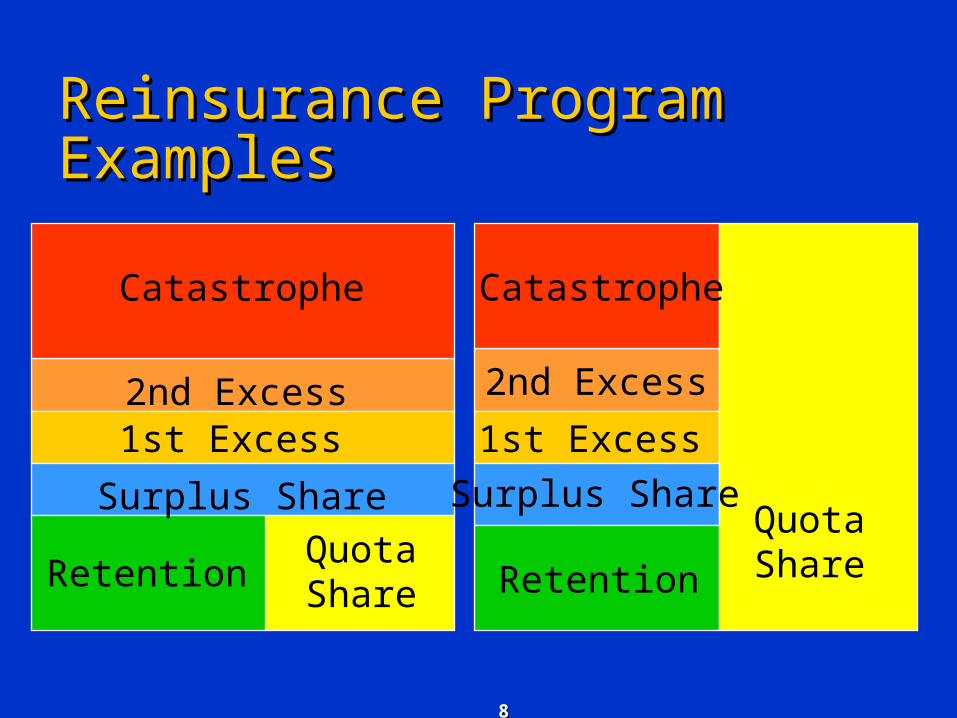

Reinsurance Program ExamplesReinsurance Program Examples

Catastrophe

2nd Excess1st Excess

Surplus Share

RetentionQuotaShare

Catastrophe

2nd Excess

1st Excess

Retention

Surplus ShareQuotaShare

99

Reinsurance ContractsReinsurance Contracts

• Should Include: Name(s) of ReinsurerPeriod of ContractBusiness CoveredLimits of CoveragePremium / CommissionReporting / SettlementsOffsetService Of SuitInsolvencyIntermediaryArbitrationGoverning LawsTermination

1010

Regulatory Contract RequirementsRegulatory Contract Requirements

Insolvency ClauseReinsurance is payable without diminution regardless of the financial status of the ceding company.

Intermediary ClauseCredit risk for the intermediary is the responsibility of the reinsurer. Payment from the ceding company to the broker is deemed paid to the reinsurer. Payment to the broker from the reinsurer does not relieve the obligations of the reinsurer to the ceding company.

Service of Suit ClauseUnauthorized reinsurers must designate the Insurance Commissioner as the legal agent for the process of suit.

Credit for reinsurance is denied if contract is missing above provisions.

1111

Timely execution of Reinsurance contractsTimely execution of Reinsurance contracts

Nine Month Rule - Nine Month Rule - NAIC’s Accounting PracticesNAIC’s Accounting PracticesIf a contract is not finalized, reduced to written form and signed within nine months, the arrangement is presumed to be retroactive and must be accounted for as retroactive contract.

Retroactive means that the loss experience under the contract is known. The purpose of the contract is possibly for adverse loss development or other reasons such as finance.

NAIC accounting rules do not allow insurance reserves to be decreased by Retroactive reinsurance contracts.

1212

Credit for ReinsuranceCredit for ReinsuranceUS Statements of Statutory Accounting PrinciplesNational Association of Insurance Commissioners (NAIC)

SSAP 62 – Property and Casualty ReinsuranceAppendix A-785 – Credit for Reinsurance

AccountingA ceding company is allowed to decrease its insurance

reserves (take credit for reinsurance) if: a. The reinsurance is prospective – covers future insurable

events.b. Reinsurance is transacted with an approved/authorized

reinsurer, orc. The reinsurer has provided collateral equal to the

amount of the reinsurance.Otherwise ceding company is not allowed to decrease its

insurance reserves.

1313

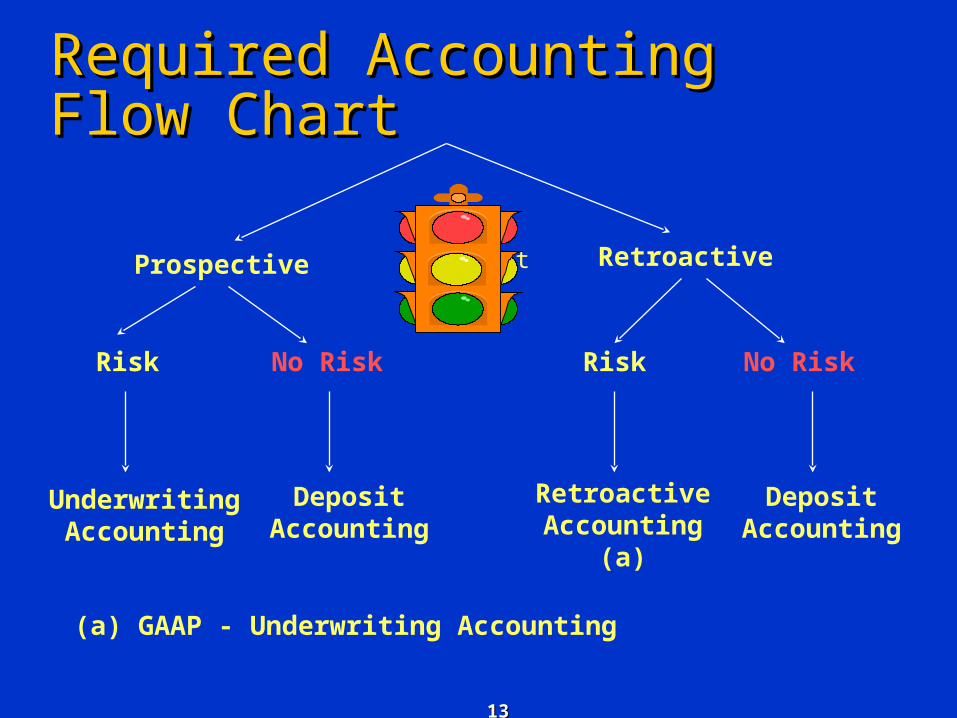

Required AccountingRequired AccountingFlow Chart Flow Chart

Contract

Risk

RetroactiveProspective

No RiskRiskNo Risk

DepositAccounting

UnderwritingAccounting

DepositAccounting

RetroactiveAccounting

(a)

(a) GAAP - Underwriting Accounting

1414

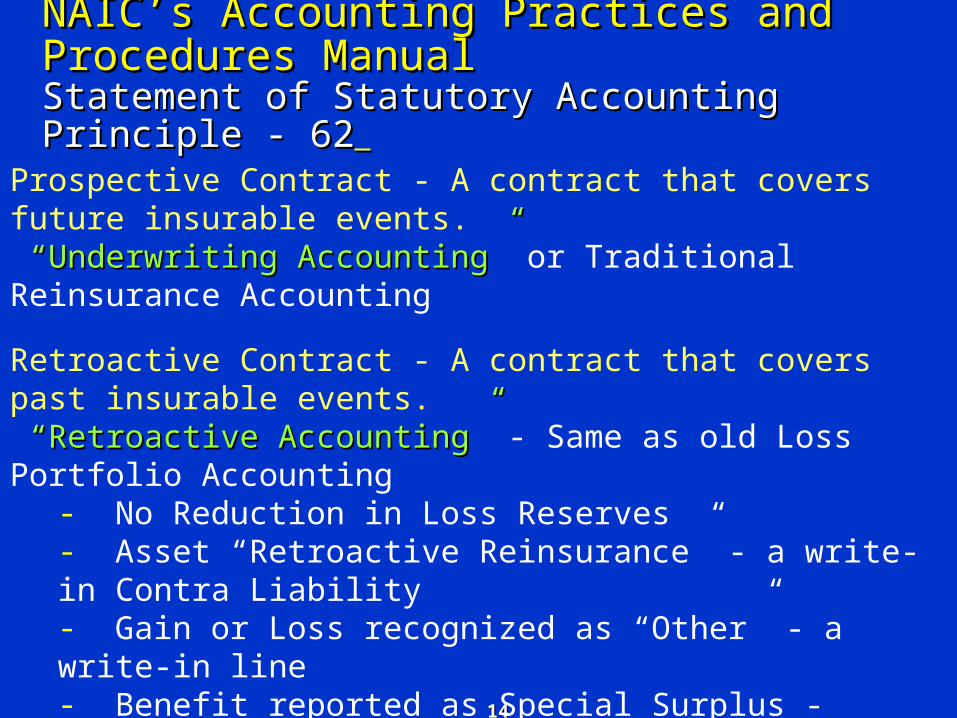

Reinsurance AccountingReinsurance AccountingNAIC’s Accounting Practices and Procedures ManualNAIC’s Accounting Practices and Procedures ManualStatement of Statutory Accounting Principle - 62Statement of Statutory Accounting Principle - 62

Prospective Contract - A contract that covers future insurable events. ““Underwriting Accounting”Underwriting Accounting” or Traditional Reinsurance Accounting

Retroactive Contract - A contract that covers past insurable events. ““Retroactive Accounting”Retroactive Accounting” - Same as old Loss Portfolio Accounting

- No Reduction in Loss Reserves- Asset “Retroactive Reinsurance” - a write-in Contra Liability- Gain or Loss recognized as “Other” - a write-in line- Benefit reported as Special Surplus - restricted

1515

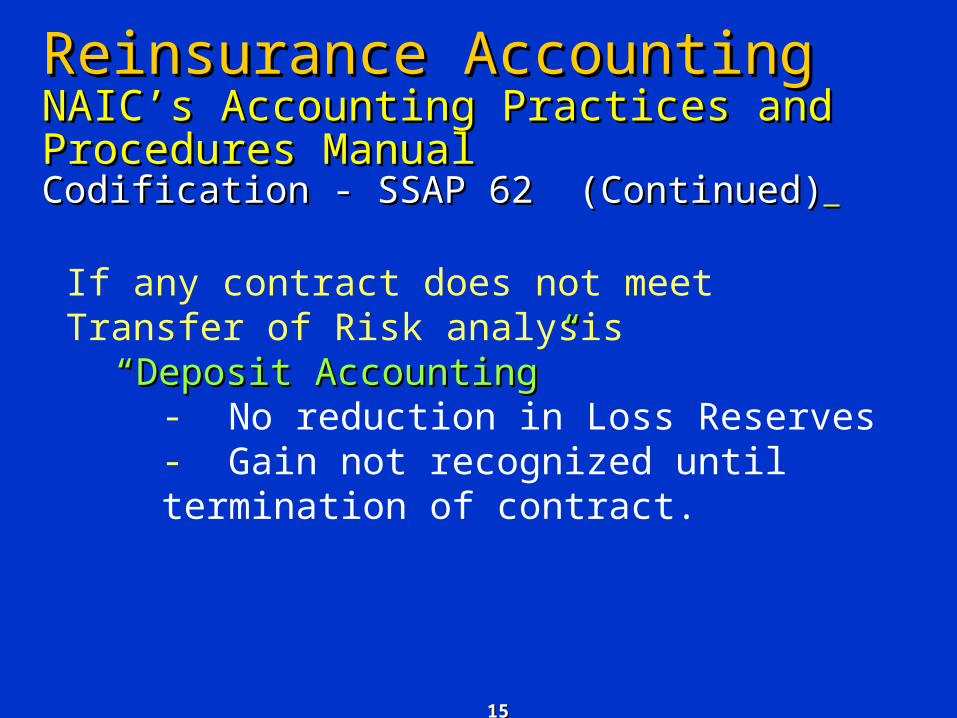

Reinsurance AccountingReinsurance AccountingNAIC’s Accounting Practices and Procedures ManualNAIC’s Accounting Practices and Procedures ManualCodification - SSAP 62 (Continued)Codification - SSAP 62 (Continued)

If any contract does not meet Transfer of Risk analysis

““Deposit Accounting”Deposit Accounting”- No reduction in Loss Reserves- Gain not recognized until termination of contract.

1616

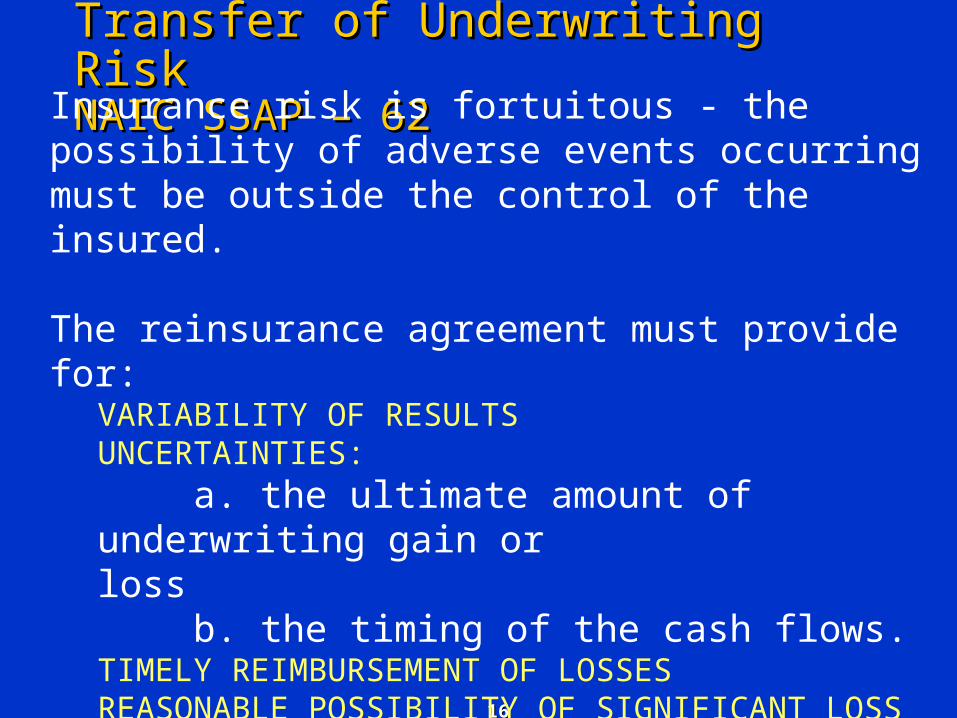

Transfer of Underwriting RiskTransfer of Underwriting RiskNAIC SSAP – 62NAIC SSAP – 62

Insurance risk is fortuitous - the possibility of adverse events occurring must be outside the control of the insured.

The reinsurance agreement must provide for:VARIABILITY OF RESULTSUNCERTAINTIES:

a. the ultimate amount of underwriting gain or loss

b. the timing of the cash flows.TIMELY REIMBURSEMENT OF LOSSESREASONABLE POSSIBILITY OF SIGNIFICANT LOSS

1717

NAIC - SSAP 62NAIC - SSAP 62Transfer of Risk (Continued)Transfer of Risk (Continued)

CASH FLOW ANALYSIS - Present value of all future cash flows.

Under “REASONABLY POSSIBLE OUTCOMES”Includes - Commissions, interest, margin fees, and

experience refunds.If exposure to reinsurance risk is remote, the contract must be accounted for as a deposit.

All cash flows processed through a deposit account.Gain recognized at termination.

1818

Reinsurance ReportReinsurance ReportUS – Schedule “F”US – Schedule “F”

• List of all reinsurers• Summary of all transactions with each reinsurer• Receivable on PAID LOSSES & LAE

Reconciles to amount on Balance SheetAged for 90 days overdue

• Receivable on UNPAID LOSSES & LAESplit between Case Reserves and IBNRReconciles to Underwriting Exhibits

• Collateral for reinsuranceBy type: Funds Held, LOC’s, Trust Agree.Funds Held reconciles to Balance Sheet

Provides:

Deficiencies: • Summary of all reinsurance with reinsurer. • No rating on financial ability of reinsurer.

1919

Reinsurance CollateralReinsurance CollateralFunds Held by ceding companyFunds Held by ceding company

• Used as a vehicle to collateralize the obligations of the

reinsurer.• Emanates from premium records of ceding company.

Letters of Credit - LOC’sLetters of Credit - LOC’s• Must be issued by NAIC approved bank.• Evergreen Clause - prior notice of termination.• Clean & Unconditional - no contingencies on draw downs.

Trust AccountsTrust Accounts• Review underlying trust agreement.• Proper beneficiary clause.• Valuation of securities under trust.

•Collateral is a substitute for financial analysis of reinsurer.

2020

Reinsurance AuditReinsurance AuditCritical ElementsCritical Elements

• Reinsurance Program- Company’s Objectives- Type of Reinsurance- Selection of Reinsurers

• Audit of Reinsurance- Review of Contracts- Reinsurance Accounting- Transfer of Risk

2121

Reinsurance AuditReinsurance AuditCritical ElementsCritical Elements (Continued) (Continued)

• Reinsurance Report - Schedule “F” U.S.- Authorized / Unauthorized- Affiliates / Non Affiliates- Aging of Recoverable- Provisions for:

• Unauthorized Reinsurance• Overdue Reinsurance

2222

Reinsurance AuditReinsurance AuditCritical ElementsCritical Elements (Continued) (Continued)

• Collateral for Reinsurance Report – Part of Schedule “F”

- Funds Held- Letters of Credit- Trust Agreements- Reciprocity (Setoff)

2323

Security AnalysisCompany Background -Company Background -

History of company/reinsurerAbility of management.

Profitability -Profitability -Underwriting PerformanceInvestment PerformanceOverall profitability

Capitalization -Capitalization - Cushion for rainy days.Base for growth.Quality of assets.

2424

Security Analysis (Continued)

Leverage -Leverage - Premiums - underwriting riskLoss Reserves - strength to absorb

adverse events.Reinsurance Recoverable - credit riskInvestments - asset riskFinance / Debt - ability to repay

Liquidity -Liquidity - Balance SheetCash Flow

UnderwritingOverall