Embed Size (px)

Citation preview

© 2012 United Air Lines, Inc. All rights reserved.

September 10, 2012

CEO Kaiser Leads UATP

Tech Overhaul16

Judge Won’t Dismiss AA

Antitrust Suit4

GlobalStar’s Van Iersel

Talks Change12

Ringing in The new

Some new brands rise in the ranks in BTN’s Annual Hotel Chain

Survey. Page 18

Issue Date

aD ClosIng

MaterIal Due Features show

DIstrIbutIon

Jan 21 Jan 7 Jan 9• 25 Most Influential Executives

In the Business Travel Industry, 2012

Feb 4 Jan 18 Jan 23 • Risk Management

Mar 4 Feb 15 Feb 20 • Videoconferencing

april 1 Mar 18 Mar 20 • Premium ClassACTE Global Education Conference, New York, April 21-23

May 13 April 29 May 1 • Emerging Markets Tech Talk 2013

June 10 May 27 May 29 • Meetings

July 8 June 21 June 24• 10th Annual Expense Manager

Survey

aug 5 July 18 July 22• 30th Annual Travel Manager Salary

& Attitude Study GBTA Int’l Convention & Expo, Aug 4-7, San Diego

sept 2 Aug 19 Aug 21 • Travel Manager of the Year

oct 14 Sept 30 Oct 2 • Hotel Chain SurveyACTE Global Education Conference

nov 25 Nov 11 Nov 13 • 16th Annual Airline Survey

Dec 16 Dec 2 Dec 4 • European Travel Management Study

BTN RECuRRING DEPARTMENTSOn The Horizon • News pages • Perspective, ‘On The Record’ • Special Section • Metrics • Travel Management • Distribution • Lodging • Transportation • Procurement • Payment & Expense • Multinational • Meetings Management • Blueprint

.com

METRICS

8 JULY 23, 2012

Ancillary Revenue Growth SlowsSystemwide Ancillary Revenue* Collected Per Passenger Segment Flown, With Year-Over-Year Change

Source: Travel Leaders Corporate, based on "nearly 625,000 business travel bookings in the first quarter of 2012" and "roughly 600,000 bookings" from the first quarter of 2011

Smartphone Functions Used by Business TravelersResponsibilities Of Travel ManagementFunction Regarding Mobile Travel Tools, Apps

Hotel Tiers Experience Modest Q1 Rate HikesAverage Cost Per Night By Category, With Year-Over-Year Increases

Source: AirPlus April-May 2012 survey of 92 corporate travel buyers in North America and Europe

Research/recommend tools for possible purchase

Contribute to strategic plans for using tools

Educate self/company about apps and how travelers use them

Implement and manage use of sanctioned tools

Source, negotiate and purchase tools

Damage control

Other

No responsibilities

32% 23%

27% 23%

27% 16%

24% 18%

20% 16%

5% 4%

5% 9%

52% 55%

2012 2011Receive travel alerts (e.g., flight delays) 84%

Check weather conditions, directions or restaurants at the destination 81%

Serve as boarding pass 67%

Change existing travel plans (e.g., rebook a flight) 46%

Provide GPS information for traveler tracking systems 38%

Capture data for reimbursement of the business trip 35%

Communicate with the travel manager or other travelers via social media 28%

Pay small travel expenses directly via mobile 6%

Other 5%

2009 2010 2011 2012**

$8.60 +36%

$9.52+11%

$9.68 +2%

$9.97 +3%

* Includes bags, priority access, onboard cabin sales, ticketing/service charges, change fees, minor fees and pet fees** Through AprilSources: Airlines for America analysis of data provided by Alaska, American, Delta, JetBlue, Southwest/AirTran, United and US Airways

Upper Upscale $163.91 <1%

Upscale $132.10 +4.1%

Upper Midscale $108.19 <1%

Midscale $103.06 +1.7%

10 OCTOBER 8, 2012 .com

COVER STORY

Predicting corporate travel demand and future pricing trends never is an easy task. Each year seems to present an ever more challenging set of circum-stances for prognosticators to analyze, and it’s no di� erent entering 2013.

Unease around Europe’s economic prospects, volatile jet fuel costs, the U.S. presidential election and unrest in North Africa and the Middle East are just some conditions to consider. To assist in forecasting, it’s instructive to review how demand has been trending, but on that front, recent indicators may be as inconsistent as ever.

Erratic Demand Trends, Economic Jitters Complicate 2013 Forecasting By David Jonas

CONTINUED ON PAGE 12

FACTS & FORECASTS

12 OCTOBER 8, 2012 .com

COVER STORY

Where We’ve Been, Where We’re Going� ere is a wide array of demand indicators to assess in determining whether corporate travel is strengthening or weakening, and by how much. Airlines all year have reported very strong or modestly strong corporate business, though some have cut second-half capacity amid macroeconomic concerns. Hoteliers have been even more bullish on the corporate market, o� ering a steady stream of commentary on their strong transient business travel trends, and strengthening group trends.

Data from travel management companies is mixed. Some in recent months have reported sustained or stronger corporate travel activity, while the likes of American Express and Hogg Robinson Group for their second quarters reported weaker activity. Sabre, meanwhile, described as strong the global growth in its global distribution system segments, but noted that U.S. growth lags that of the rest of the world.

Taken together, no trend from the past year is evident. Perhaps one of the better indicators of corporate travel demand is the growth (or decline) in the total num-ber of transactions processed through ARC by mega

travel agencies. But that metric has been rollercoaster-ing throughout 2012, with as many down months as up months. � e trend line hasn’t experienced more than two consecutive months in either direction since the � rst quarter of 2011. Including American Express, BCD Travel, Carlson Wagonlit Travel, Egencia, HRG and Omega World Travel, mega agencies in August had an aggregate transaction volume decrease of 0.7 per-cent, slightly more than the 0.15 percent decline that ARC reported for all U.S. agencies (see chart above).

Describing that trend line as a seismograph, GDSX vice president Tom Wilkinson during � e Beat Quar-terly webinar conducted in September by � e BTN Group said, “If you paid attention to economic indica-tors over the past two years, it kind of feels right. Every month we are getting some great news on interest rates, or housing or whatever, all which drives the economy, but then Europe goes into crisis, and then things sta-bilize. � e markets do respond to that. Travel is one of the great leading indicators of business, certainly in the United States and Europe.”

Many industry observers and constituents don’t expect business travel activity to pick up much more

steam through the end of 2012 and into next year. Some anticipate an outright decline, though such projections depend heavily on geography and many other factors.

Among 63 companies surveyed by BTN with annual U.S.-booked air volumes of at least $30 million, aver-age total T&E spending this year is expected to be $234 million, down from $242 million in 2011.

BCD Travel consultancy Advito in its 2013 forecast wrote that global economic jitters will “slow growth in travel for the rest of this year and 2013.”

North America Pricing ForecastsForecasting corporate travel demand is even more dif-� cult than tracking it as it happens. Forecasting prices is more di� cult still.

“Anybody who has been in the business travel in-dustry for a while has learned to be pretty skeptical of some of these predictions,” Wilkinson said. In noting expectations for oil prices speci� cally and global eco-nomic performance generally he added that “the odds of all those predictions coming true are pretty remote.” � row in unforeseen natural disasters, epidemics and civil unrest, and forecasts simply “cannot account for volatility in the market.” Instead, he suggested travel managers “ought to be thinking about a price-demand curve sort of like what is indicated on the ARC chart.”

However, should unforeseen events with wide impact be few, assumptions on global economies generally be accurate and the U.S. economy grow at about 1.5 per-cent next year, as it has this year, then price forecasts, Wilkinson said, may prove to be close to the mark.

Carlson Wagonlit Travel in July was the � rst of the usual bunch to publish a 2013 corporate travel pricing forecast. It expected modest global growth next year for most corporate travel prices, with demand growth—despite hesitancy by some companies—outpacing very limited airline and hotel supply growth.

A more recent forecast by Advito, issued in Septem-ber, also projected moderate corporate demand growth next year. It too expected airfares and hotel rates next year paid by corporate travelers to rise generally by low-to-mid single-digit percentages around the world, “either in line with or a little faster than in� ation.”

North American airfares on average will rise be-CONTINUED ON PAGE 16

CONTINUED FROM PAGE 10

U.S. Mega Travel Agency TransactionsYear-Over-Year Changes

Note: Mega agencies include American Express, BCD Travel, Carlson Wagonlit Travel, Expedia's Egencia, Hogg Robinson Group and Omega World Travel.

Source: Airlines Reporting Corp.

September2011

October November December January2012

February March April May June July August

+1.7%+0.2%

+1.3%-0.5%

-4.6%

-0.7%

+4.3% +3%

+2.1%

+4.2%

-5.8% -6.5%

Expected 2013 Negotiated Hotel RatesChange Versus 2012

Source: AirPlus International Aug. 2-Sept. 8 survey of 133 corporate travel buyers from North America and Europe

Increase 10% or more

Increase 5%–10%

Increase 1%–5%

Stay the same

Decrease 1%–5%

Decrease more than 5%

1%

24%

9%

52%

11%

3%

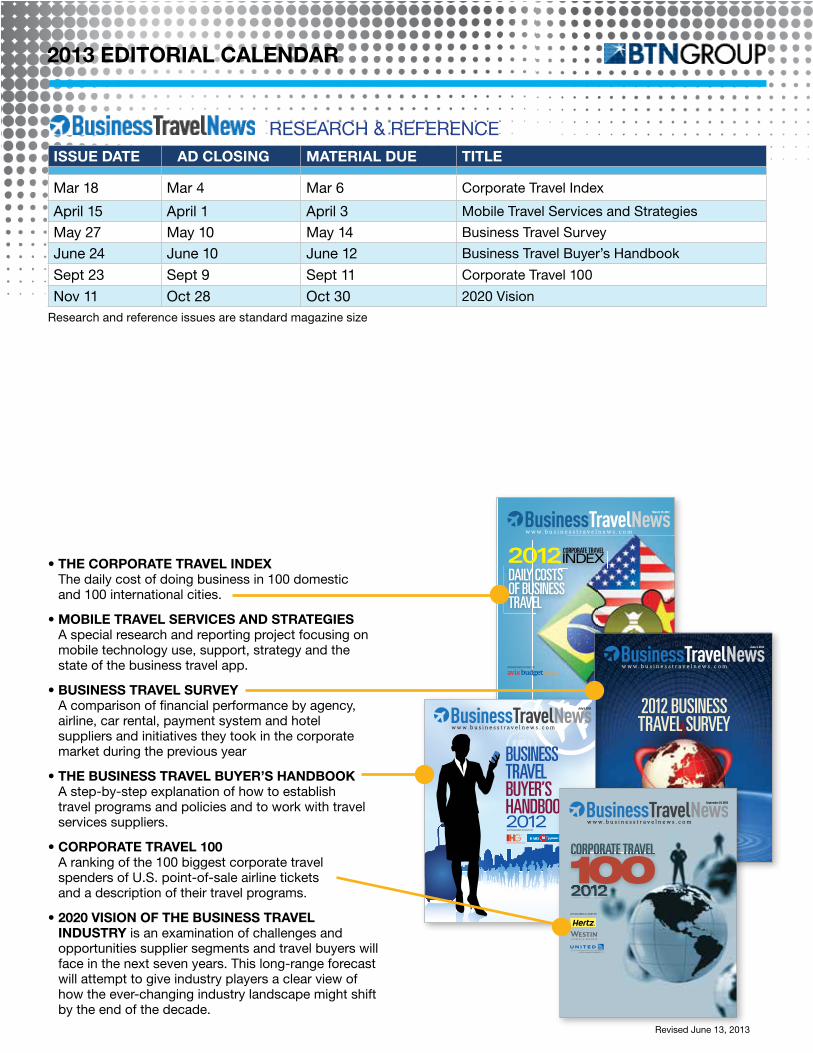

2013 eDItorIal CalenDar

Revised June 13, 201318 september 10, 2012 .com .com september 10, 2012 19

2012 Hotel Chain Survey

By Michael B. Baker

LUXURYQuality of Sales Staff

Consistency of Offering

Arrange Group Travel/

Meetings

Meetings Facilities

Corporate Rate

Programs

Quality of Food

Helpful, Courteous

Staff

Physical Appearance of Hotels

Quality of Business Center

In-Room Business Amenities

In-Room Amenities

Overall Price/Value Relationship

Average Total

St. Regis/Luxury Collection 5.27 5.40 5.04 5.04 4.52 5.33 5.70 5.80 5.50 5.50 5.60 5.05 5.31

Ritz-Carlton 5.06 5.24 5.11 5.15 4.49 5.18 5.49 5.59 5.34 5.32 5.48 4.77 5.19

Waldorf Astoria 5.18 5.47 5.19 5.31 4.94 5.44 5.25 5.25 5.08 4.92 5.08 4.75 5.16

Mandarin Oriental 5.05 5.15 4.89 4.89 4.58 5.05 5.40 5.60 5.40 5.20 5.40 4.87 5.12

Four Seasons 5.05 5.33 4.88 5.00 4.43 5.20 5.18 5.55 5.32 5.11 5.42 4.82 5.11

Fairmont 4.82 4.79 4.84 4.84 3.91 5.00 5.04 5.46 5.08 4.92 5.12 4.75 4.88

Several relatively new hotel brands have made strong inroads with travel buyers in Business Travel News’ 2012 Hotel Chain Survey, with some introduced within the past two decades beating out legacy brands.

BTN this year changed its scor-ing system in the hotel chain sur-vey, switching to a six-point scale from the five-point scale it had used for several years. The criteria also changed slightly. Non-resort and re-sort meetings facilities were merged into a single category, and the rating of commission payment systems was dropped. One new criterion was add-ed: consistency of a brand’s offering.

This makes year-over-year com-parisons difficult in terms of overall buyer satisfaction levels. Comparing surveys does, however, show a shift

in buyers’ preferences, with only one brand that was at the top of its tier in last year’s survey repeating that feat this year and several other top brands from last year falling considerably in their rankings.

Of the multibrand hotel companies, Starwood Hotels & Resorts Worldwide, Hilton Worldwide and Hyatt Hotels Corp. each had two brands top their tiers, and Marriott International had one. Hyatt Place, the youngest of the mostly young select-service category entrants, this year earned its first num-ber-one finish, as did Starwood’s Luxu-ry Collection and St. Regis brand.

Two luxury hotel brands that sprung from iconic New York hotels were travel buyers’ favorites across all criteria in the 2012 Hotel Chain Survey. Starwood Hotels & Resorts’ St. Regis and Luxury Collection brands earned the highest overall score in the luxury tier, breaking the years-long hold that Four Seasons and Ritz-Carlton had in BTN’s survey.

Astoria is a bit smaller—22 hotels open and 13 under construction, including properties in Panama City, Berlin, Am-sterdam, Beijing and Dubai, according to Hilton global head of luxury and life-style brands John Vanderslice. Between it and the Conrad Hotels & Resorts brand, Hilton aims to be the “fastest-growing luxury hotel company in the world,” he said.

On the ropes in the austere post-

recession days of 2008, luxury hotels have rebounded powerfully, with av-erage U.S. occupancy during the first seven months of 2012 reaching pre-re-cession levels at 72.5 percent, accord-ing to STR. The average January-July luxury rate increased by 4.8 percent year over year, the highest of any tier, though it still remains below pre-reces-sion levels. Rates are poised to go even higher, considering U.S. luxury hotel demand was up 3 percent year over year through July while supply actually decreased by 0.5 percent.

“Properties had a very short, sharp bounce in terms of occupancy, though rate took longer to recover,” James said. “The luxury, urban hotels were places

where people needed to do business again, and if you add in the core inter-national travel group, they were back and we were soon supplemented by boom economies in China and Brazil.”

Corporate group business at luxury hotels also has rebounded following the days of media scrutiny and the AIG ef-fect, Vanderslice said.

“For a while, people had dropped down and were having meetings at lower-tier hotels because of economic reasons, but now they’re all bouncing back to luxury,” he explained. “Our travel partners have realized there’s ac-tually an efficiency to having a meeting

or event at a luxury hotel because of the facilities and services we provide.”

At St. Regis, those services include butler service, and Waldorf Astoria properties provide personal concierges for transient guests. Having such ser-vices across brands is the true mark of “consistency” in the luxury tier, where hotels now pride themselves on cre-ating unique designs and facilities, Vanderslice said.

They also are how luxury hotels can continue to show their value to high-level corporate travelers, James said.

“Our customers tend to be the CEOs of their business, and there is no ‘on-duty’ and ‘off-duty,’ ” he said. “The butlers can wrestle the mundane out

of their agenda: getting their boarding passes printed, having a cup of coffee or tea ready in the morning or know-ing their tastes in food so they can edit their stay.”

James attributed the St. Regis/Lux-ury Collection’s high score in physi-cal appearance to the relative newness of the portfolio. It also is investing in upgrades where necessary, such as the recent $40 million renovation at the St. Regis Aspen Resort, the second-oldest St. Regis property that had been con-verted in 1998 from a Ritz-Carlton.

Food is a major part of Waldorf As-toria’s history—the original hotel’s cu-linary inventions include veal Oscar, red velvet cake and, of course, Waldorf salad—and Vanderslice said “extraordi-nary restaurants” led to the brand’s top score for food this year. The restaurant at the brand’s Rome Cavelieri hotel, for example, is the city’s only three-Mi-chelin-starred eatery.

Both Vanderslice and James said their brands also benefit from being a part of multibrand companies, as does Ritz-Carlton, which is part of Marriott. While there was a time when luxury travelers turned their noses up at re-wards programs, modern executives relish being part of them, partly be-cause they also benefit when they stay at lower-tier properties, James said.

“CEOs born in the dot-com boom are more relaxed, less likely to wear a tie and are very comfortable moving across a portfolio of hotels,” he said. “If their business takes them to Cincinnati or Oshkosh, that’s where a Four Points is, and being a part of the Starwood Preferred Guest program gives them much more control over their stay.”

St. Regis/Luxury Collection Garners Top Scores In Luxury Tier

The Starwood brands’ overall joint score was more than a tenth of a point higher than the second-ranked brand, Ritz-Carlton. They had near-perfect scores for their physical appearance and hotel staff, and also were the top-scoring brands for their sales staff, business cen-ter, business and in-room amenities and overall price/value relationship.

Although the overall score for Wal-dorf Astoria Hotels & Resorts was slightly lower than Ritz-Carlton’s, the Hilton brand topped several criteria: consistency, arranging group travel, meetings facilities, corporate rate pro-grams and food quality. Four Seasons, last year’s top brand, dropped to fifth.

Although owned by two different companies, St. Regis and Waldorf As-toria have common roots. The two New York hotels that bear their original names were companion hotels owned in the early 20th century by the Astor family. In recent decades, Starwood and Hilton decided to expand them into luxury brands covering the globe.

“It’s only recently that we’ve had enough hotels to be seriously measured in this survey,” said Paul James, Star-wood’s global brand leader for St. Regis and the Luxury Collection. “In 2007, we had 13 St. Regis hotels and some-where in the low 60s for the Luxury Collection, heavily focused in Europe. Now, we have 31 St. Regis hotels open, and that will double again in about a five year-cycle.”

Launched as a brand in 2006, Waldorf

Luxury hotels have rebounded powerfully, with average U.S. occupancy during the first seven months of 2012 reaching pre-recession

levels at 72.5 percent, according to STR.

2013 eDItorIal CalenDar

w w w . b u s i n e s s t r a v e l n e w s . c o m

2012CORPORATE TRAVELCORPORAATTEE TTRRAAVVEELLINDEX

March 19, 2012

SPONSORED IN PART BY

DAILY COSTS OF BUSINESS TRAVEL

June 4, 2012

2012 BUSINESS TRAVEL SURVEY

w w w . b u s i n e s s t r a v e l n e w s . c o m

July 9, 2012

BUSINESSTRAVELBUYER’SHANDBOOK2012SPONSORED IN PART BY

SPONSORED IN PART BY

CORPORATE TRAVEL

2012100

September 24, 2012

• the Corporate travel InDex The daily cost of doing business in 100 domestic and 100 international cities.

• MobIle travel servICes anD strategIes A special research and reporting project focusing on mobile technology use, support, strategy and the state of the business travel app.

• busIness travel survey A comparison of financial performance by agency, airline, car rental, payment system and hotel suppliers and initiatives they took in the corporate market during the previous year

• the busIness travel buyer’s hanDbook A step-by-step explanation of how to establish travel programs and policies and to work with travel services suppliers.

• Corporate travel 100 A ranking of the 100 biggest corporate travel spenders of u.S. point-of-sale airline tickets and a description of their travel programs.

• 2020 vIsIon oF the busIness travel InDustry is an examination of challenges and opportunities supplier segments and travel buyers will face in the next seven years. This long-range forecast will attempt to give industry players a clear view of how the ever-changing industry landscape might shift by the end of the decade.

Issue Date aD ClosIng MaterIal Due tItle

Mar 18 Mar 4 Mar 6 Corporate Travel Index

April 15 April 1 April 3 Mobile Travel Services and Strategies

May 27 May 10 May 14 Business Travel Survey

June 24 June 10 June 12 Business Travel Buyer’s Handbook

Sept 23 Sept 9 Sept 11 Corporate Travel 100

Nov 11 Oct 28 Oct 30 2020 Vision

Research and reference issues are standard magazine size

RESEARCH & REFERENCE

Revised June 13, 2013

2013 eDItorIal CalenDar

Issue Date aD ClosIng

MaterIal Due show DIstrIbutIon

February January 17 January 22

May March 28 April 2

august June 27 July 2 GBTA International Convention & Expo, Aug 4-7, San Diegonovember Sept 26 Oct 1

TRAVEL PROCuREMENT RECuRRING DEPARTMENTSIndicators • Leading Practices • Case Studies • Procurement Profiles • Supply Chain • Technology • Meetings Management • Payment • Perspective • News

SPORTS AUTHORITY

AUGUST 2012

Capturing Bookings In Nonpreferred Channels

University of Texas travel manager Kevin Maguire’s solutions apply far beyond the football fi eld

Goodman Networks’ Rapid Program Rollout

Entertainment Companies Fight For Respect

24 | Travel ProcuremenT | august 2012 www.businesstravelnews.com/procurement

Cover story

www.businesstravelnews.com/procurement august 2012 | Travel ProcuremenT | 25

ports travel carries its own sets of challenges and needs not seen in most corporate travel pro-grams. Former corporate travel buyer Kevin Maguire has spent the past few years clearing those hurdles as travel manager for intercolle-

giate athletics at the University of Texas at Austin—man-aging ground transportation and charter air travel, han-dling group airport check-ins and contending with inflated hotel rates due to citywide events.

Maguire joined UT’s travel team in late 2007 and since has created “a very consolidated program, very succinct in procedure and widely accepted by coaches and travelers,” he said. The university had a travel program when Maguire took the position, but athlet-ics was not included in that, and the department largely acted on its own when it came to travel. Maguire esti-mated that cost avoidance is 30 per-cent to 40 percent higher than when he first began to roll out the program.

Travel management at UT supports between 600 and 700 travelers spend-

ing $10 million to $20 million per year, depending on how well various teams perform during the respective seasons. Many standard solutions in-cluding online booking tools do not make sense for athletic travel pro-grams, but the department does use an agency—Anthony Travel, which specializes in university and sports travel management—for hotel and chauffeured car bookings.

Prior to taking his position at the university, Maguire had racked up a few decades in the travel industry, in-cluding travel manager or consultant

roles at Waste Management, Applied Materials and Tokyo Electron. He also has served as the Global Busi-ness Travel Association’s president (followed by his current term as its vice president) and led the develop-ment of GBTA’s sports committee. These experiences have helped Ma-guire inject procurement acumen into his university’s program, which has become something of a bench-mark not just among college athletics travel programs, but also college and professional sports programs across the country.

Consolidating Ground, Charter AirOne of Maguire’s recent initiatives was consolidating to a single sourc-ing company his department’s ground transportation program. He partnered with technology supplier Go Ground to develop that program from the ground up, as he found much of the existing technology for managing >

University of Texas at Austin travel manager for intercollegiate athletics Kevin Maguire

PH

OTO

GR

AP

H B

Y M

ICH

AE

L S

EX

TON

How American Airlines’ Bankruptcy Affects You

Rockwell Automation Behaves And Saves

The industry debates the true value of negotiated corporate airline deals

Inside The New Industry Certifi cations

CONTRACTING AT A CROSSROADS

FEBRUARY 2012

Revised June 13, 2013

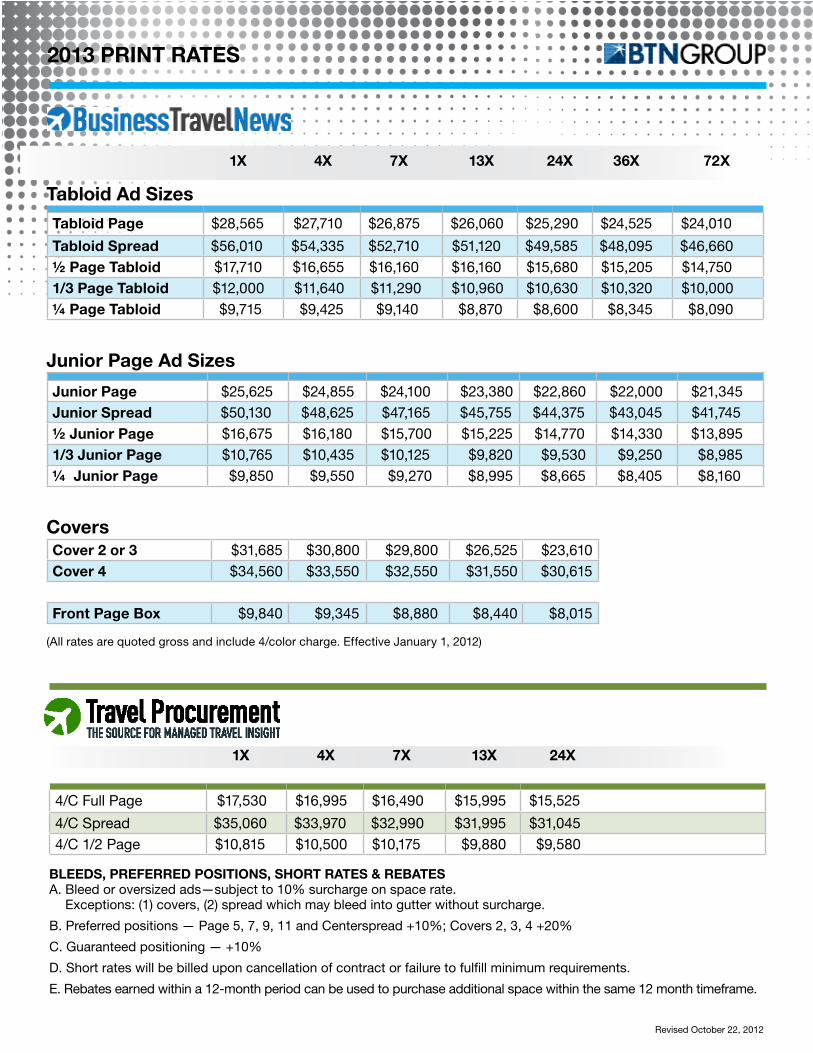

(All rates are quoted gross and include 4/color charge. Effective January 1, 2012)

1x 4x 7x 13x 24x 36x 72x tabloid ad sizes

tabloid page $28,565 $27,710 $26,875 $26,060 $25,290 $24,525 $24,010

tabloid spread $56,010 $54,335 $52,710 $51,120 $49,585 $48,095 $46,660½ page tabloid $17,710 $16,655 $16,160 $16,160 $15,680 $15,205 $14,7501/3 page tabloid $12,000 $11,640 $11,290 $10,960 $10,630 $10,320 $10,000¼ page tabloid $9,715 $9,425 $9,140 $8,870 $8,600 $8,345 $8,090

Junior page ad sizes

Junior page $25,625 $24,855 $24,100 $23,380 $22,860 $22,000 $21,345Junior spread $50,130 $48,625 $47,165 $45,755 $44,375 $43,045 $41,745½ Junior page $16,675 $16,180 $15,700 $15,225 $14,770 $14,330 $13,8951/3 Junior page $10,765 $10,435 $10,125 $9,820 $9,530 $9,250 $8,985¼ Junior page $9,850 $9,550 $9,270 $8,995 $8,665 $8,405 $8,160

Covers Cover 2 or 3 $31,685 $30,800 $29,800 $26,525 $23,610Cover 4 $34,560 $33,550 $32,550 $31,550 $30,615

Front page box $9,840 $9,345 $8,880 $8,440 $8,015

1x 4x 7x 13x 24x

4/C Full Page $17,530 $16,995 $16,490 $15,995 $15,525

4/C Spread $35,060 $33,970 $32,990 $31,995 $31,0454/C 1/2 Page $10,815 $10,500 $10,175 $9,880 $9,580

bleeDs, preFerreD posItIons, short rates & rebates A. Bleed or oversized ads—subject to 10% surcharge on space rate.

Exceptions: (1) covers, (2) spread which may bleed into gutter without surcharge.

B. Preferred positions — Page 5, 7, 9, 11 and Centerspread +10%; Covers 2, 3, 4 +20%

C. Guaranteed positioning — +10%

D. Short rates will be billed upon cancellation of contract or failure to fulfill minimum requirements.

E. Rebates earned within a 12-month period can be used to purchase additional space within the same 12 month timeframe.

2013 prInt rates

Revised October 22, 2012

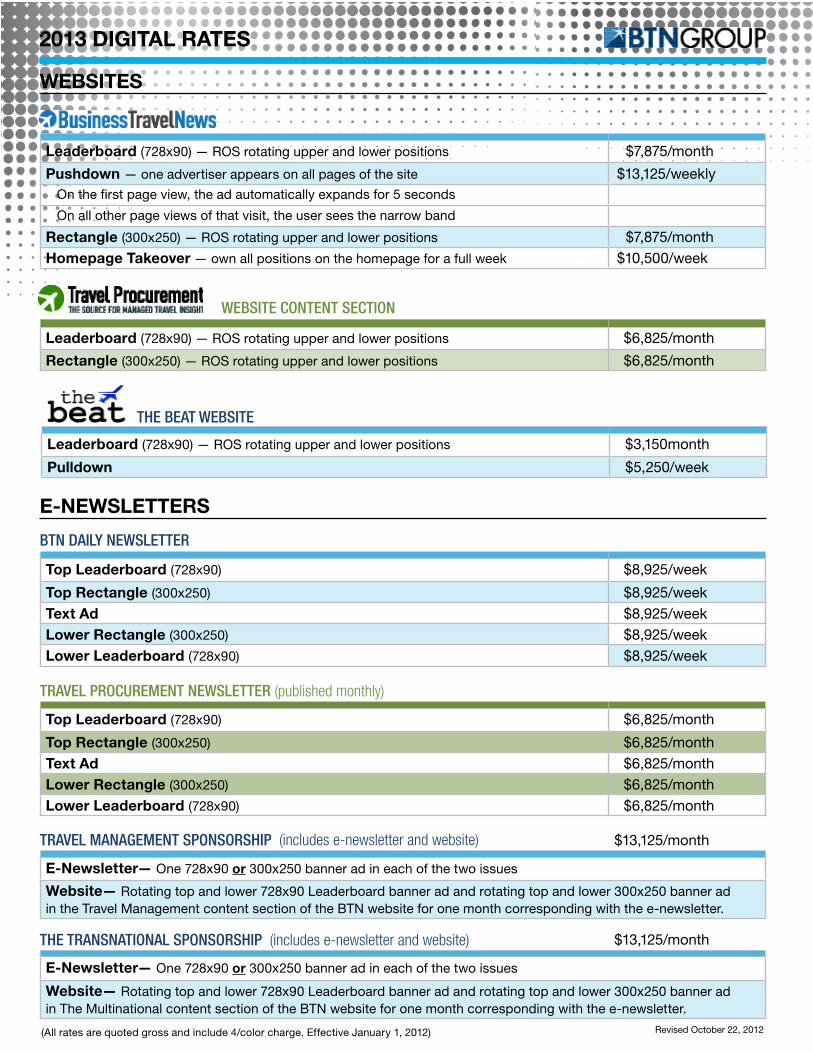

websItes

e-newsletters

(All rates are quoted gross and include 4/color charge. Effective January 1, 2012)

BTN Daily NewsleTTer

top leaderboard (728x90) $8,925/week

top rectangle (300x250) $8,925/weektext ad $8,925/weeklower rectangle (300x250) $8,925/weeklower leaderboard (728x90) $8,925/week

leaderboard (728x90) — ROS rotating upper and lower positions $3,150month

pulldown $5,250/week

Travel procuremeNT NewsleTTer (published monthly)

top leaderboard (728x90) $6,825/month

top rectangle (300x250) $6,825/monthtext ad $6,825/monthlower rectangle (300x250) $6,825/monthlower leaderboard (728x90) $6,825/month

Travel maNagemeNT spoNsorship (includes e-newsletter and website) $13,125/month

e-newsletter — One 728x90 or 300x250 banner ad in each of the two issues

website— Rotating top and lower 728x90 Leaderboard banner ad and rotating top and lower 300x250 banner ad in the Travel Management content section of the BTN website for one month corresponding with the e-newsletter.

The TraNsNaTioNal spoNsorship (includes e-newsletter and website) $13,125/month

e-newsletter— One 728x90 or 300x250 banner ad in each of the two issues

website— Rotating top and lower 728x90 Leaderboard banner ad and rotating top and lower 300x250 banner ad in The Multinational content section of the BTN website for one month corresponding with the e-newsletter.

leaderboard (728x90) — ROS rotating upper and lower positions $7,875/month

pushdown — one advertiser appears on all pages of the site $13,125/weekly On the first page view, the ad automatically expands for 5 seconds

On all other page views of that visit, the user sees the narrow band

rectangle (300x250) — ROS rotating upper and lower positions $7,875/monthhomepage takeover — own all positions on the homepage for a full week $10,500/week

weBsiTe coNTeNT secTioN

leaderboard (728x90) — ROS rotating upper and lower positions $6,825/month

rectangle (300x250) — ROS rotating upper and lower positions $6,825/month

The BeaT weBsiTe

Revised October 22, 2012

2013 DIgItal rates