Embed Size (px)

Citation preview

RECT

ICEL

annu

al re

port

200

3R

ectic

el i

n a

nuts

hell

1

Recticel in a nutshell

> Recticel is a Belgian Group with a strong European dimension, but also operates in the restof the world. Recticel has some one hundred establishments in 20 countries.

> Recticel contributes to daily comfort, with foam filling for seats, mattresses and slat bases,insulation material, interior comfort for cars and an extensive range of other industrial anddomestic applications.

> Recticel is the Group behind the best known bedding brands, including Beka, Lattoflex,Literie Bultex, Schlaraffia, Sembella, Swissflex, Superba, Epeda, Merinos and Ubica.

> Recticel is driven by technological progress and innovation, which has led to a revolutionarybreakthrough at the biggest names in the car industry.

> Recticel has over 11,000 employees, who contributed to the Group achieving sales to a value of 1.2 billion euros in 2003.

what really matters is

trust>

RECT

ICEL

annu

al re

port

200

3Co

nten

ts

2R e c t i c

Key figures: FRONT INSIDE COVER

Organization chart: BACK INSIDE COVER

Useful addresses and financial calendar: BACK COVER FLAP

4 > Financial section

50 Notes on the consolidated annual accounts56 Consolidated balance sheet58 Consolidated income statement60 Consolidated statement of cash62 Notes to the consolidated income statement68 Summary of the accounting and consolidation principles70 Exchange rates70 List of consolidated subsidiaries73 Litigation74 Group six-year financial record75 Annual accounts of Recticel SA/NV80 Auditor’s report

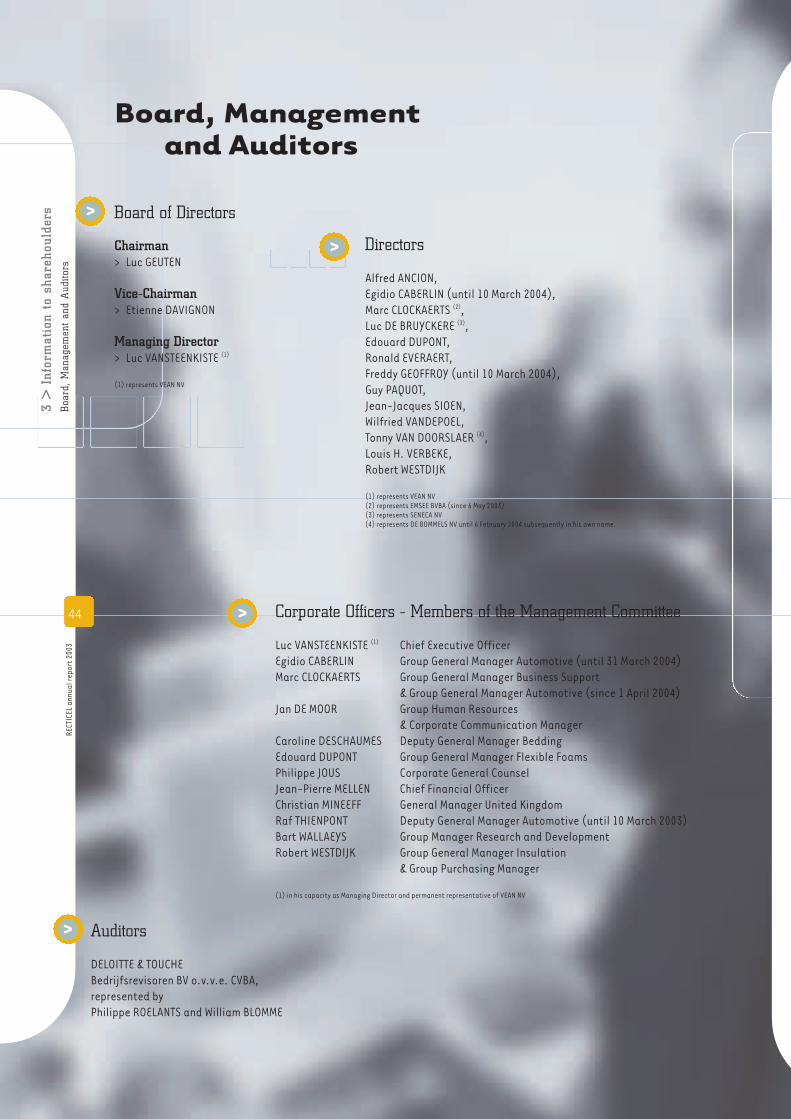

1 Recticel in a nutshell3 Highlights of 20034 Letter to the shareholders6 Report by the Board of Directors

0 > Introduction

3 > Information to shareholders

40 Share information43 Switch to IAS/IFRS44 Board, management and auditors45 Corporate Governance

10 Mission statement11 Strategy12 Synergy13 Human Resources14 Research and Development15 Safety and environmental protection16 Quality policy

1 > The Recticel Group

2 > Business lines

18 Polyurethane foam: production scheme19 Production plants20 Flexible foams26 Bedding30 Insulation34 Automotive

Contents

RECT

ICEL

annu

al re

port

200

3H

ighl

ight

s of

200

3

3e l

Highlights of 2003

01/2003>

Recticel and Pikolin, Spain’s leadingmattress manufacturer, announcedthe establishment of a new jointventure. Recticel, which holds a 51%stake in the new structure, has contributed its French beddingactivities, including the Literie Bultexbrand, to this venture.

January 2003

BEDDING IN FRANCE

08/2003> 10/2003>

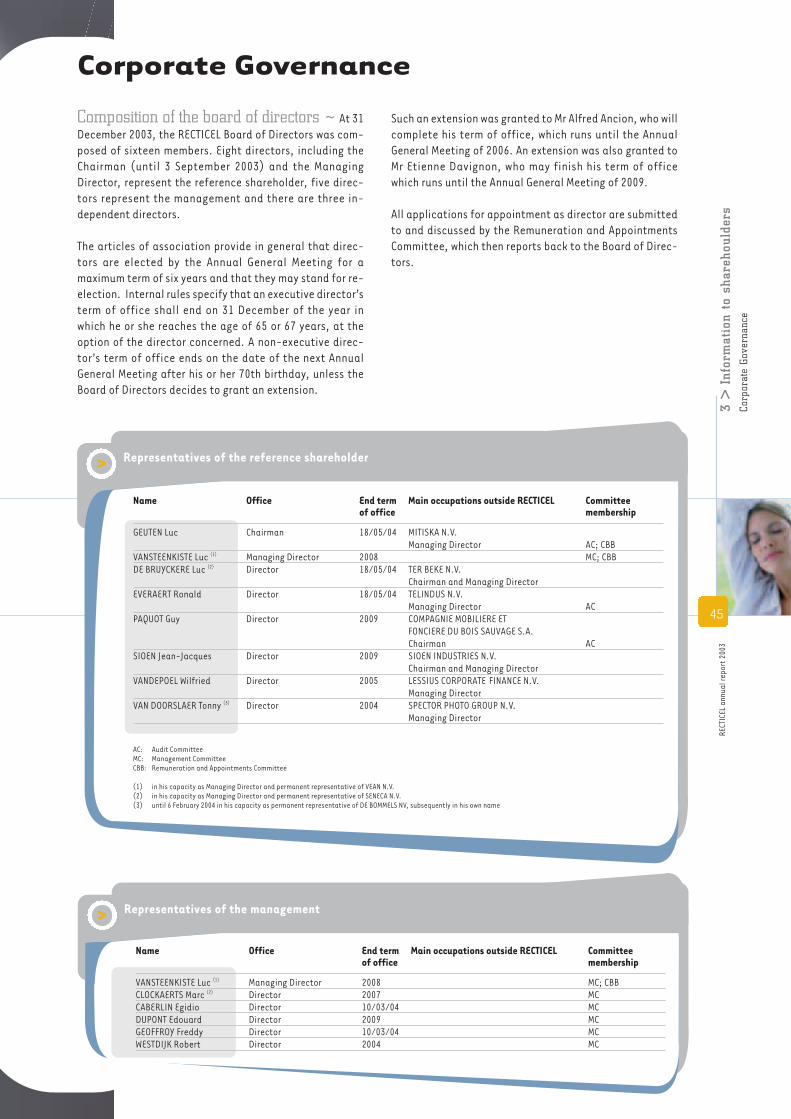

Recticel’s shareholder structure,since 1998 organized around the holding company Rec-Hold, was revised. The exclusive control byRec-Hold was converted into jointcontrol by the leaner Rec-Hold(27.3%), Mercator Bank enVerzekeringen (18.9%) and Lessius(14.75%). Within Rec-Hold, the Compagnie du Bois Sauvage, with 62.8%, is the majorityshareholder. The new commitmentruns until end-2005 (see CorporateGovernance section).

August 2003

RENEWAL OF SHAREHOLDER CONFIDENCE

Recticel and Woodbridge of Canadaannounced their intention to extendtheir joint venture by accommodatingall their respective seat cushionproduction activities in ContinentalEurope in a new group of companies.The largest manufacturer of seatcushions in moulded foam in Europeis the outcome of the extension.

October 2003

RECTICEL AND WOODBRIDGE

04/2002>

Recticel established a new company,Corpura, which is to focus on the production of innovative types of foam for specific, high-qualityapplications for use in the medicalsector, cosmetics and personalhygiene. Corpura is a full subsidiaryof Recticel which will operate fromEtten-Leur in the Netherlands (see technical foams section).

April 2003

CORPURA

09/2002>

Disappointing interim figures led to the announcement of newrestructurings. Two more plants wereclosed, bringing the total to four.In addition to the 500 jobs alreadylost in 2002, some 1000 furtherredundancies were implemented in 2003 (see Report by the Board ofDirectors and the Human Resourcessection).

September 2003

RESTRUCTURINGS

RECT

ICEL

annu

al re

port

200

3Le

tter

to t

he s

hare

hold

ers

4

Letter to the shareholders

Iraq ~ At the beginning of 2003, the eyes of the worldwere focused on Iraq, where a second Gulf War seemedinevitable and hopes were pinned on a rapid, favourableoutcome. However, the economic recovery expected im-mediately after the fall of the Iraqi regime failed to ma-terialize. The economy trickled along only hesitantly,following the flow of international events. There was noquestion of general growth. Some countries still managedto make limited economic progress over the year as awhole, but others, including a number of European heavy-weights, even experienced slightly negative growth.

Restructurings ~ For Recticel, it was already ap-parent at the end of the first six months that 2003 wouldconstitute a break in the positive trend of the past years.Sales were stable, but the combination of the economicdownturn and a number of specific phenomena in ourgrowth markets were already making it clear that theexpected results would not be attained. Recticel saw pro-fitability decline in most of its activities, with the excep-tion of the insulation business line, which took the bene-fits of its strong and professionally organized productionmachinery, in conjunction with a wide sales network.

The Group immediately decided to launch an ambitiousrestructuring plan, building on the efforts already madepreviously to secure the profitability and the future of theGroup. Four plants were closed and others were restruc-tured. The savings plan, which cost the Group some EUR 9million, was largely implemented at the beginning of 2004and gives Recticel renewed breathing space and scope forthe future. The Group is expecting a significant impro-vement in the results for this year and even further advan-ces in 2005.

Outlook ~ The improvement cannot result from asavings plan alone. For 2004, the Group consequentlyhopes for some natural growth, however small. In addition,the existing joint ventures in the bedding business line(with Pikolin of Spain) and automotive business line (withWoodbridge of Canada) are ready for strong development,based on technological efficiency, thorough knowledge ofthe market and innovative and flexible sales strategies.The insulation business line received positive impetus fromstricter insulation standards in a number of neighbouringcountries and again displays the potential of the sector.The Group is closely monitoring the development of thismarket in Central Europe.As regards the flexible foam business line, the Group in-tends to concentrate increasingly on high-quality appli-cations for its products.The automotive industry shows that the activities becomeprofitable as soon as the start-up phases are over. Sincethe number of new programmes going into production from2004 is approached with the necessary caution, the Groupexpects a positive trend in this market too, in which itspresence includes its own patented technology.

Central and Eastern Europe ~ Recticel is nowdelighted that strong development has occurred in Centraland Eastern Europe in the past decade. The Group’s ac-tivities there have long extended beyond the production ofbulk foam for the furniture sector and now already includea large number of high-tech applications, for example forthe car industry.

2003 will go down in history as a year of great uncertainty. This is hardly surprising, given the impactwhich the international tensions and all their negative side-effects have already had on our societyand economic development for several years.

2003, uncertainty and economic slowdown

RECT

ICEL

annu

al re

port

200

3Le

tter

to t

he s

hare

hold

ers

5

Moreover, the growth in the local activities not only makesup for the decline on the Western European market, whichseemed to be more sensitive than ever to phenomena suchas relocation and importation from low-wage countries,but has also created a growing local demand which coinci-des with the rise in the standard of living.

In general, Central Europe offers very high potential for thefuture, which Recticel has every intention of followingclosely. Accordingly, the Group expects that in the comingyears its activities in all business lines will continue todevelop especially rapidly in these countries, compared toother growth markets.

Level of debt ~ Reducing the level of debt remainsone of the Group’s top priorities. On account of the growthin the automotive business line and the start-up phases ofthe planned new contracts, it was already announced pre-viously that it was not feasible to reduce the level of debtin the short term. Recticel is counting on being able to setto work on actively reducing its debt from 2005. The drivingforces here are the review of the investment requirementsin the automotive sector (inter alia by gran-ting licences) and greater attention beingpaid to control of the necessary workingcapital.

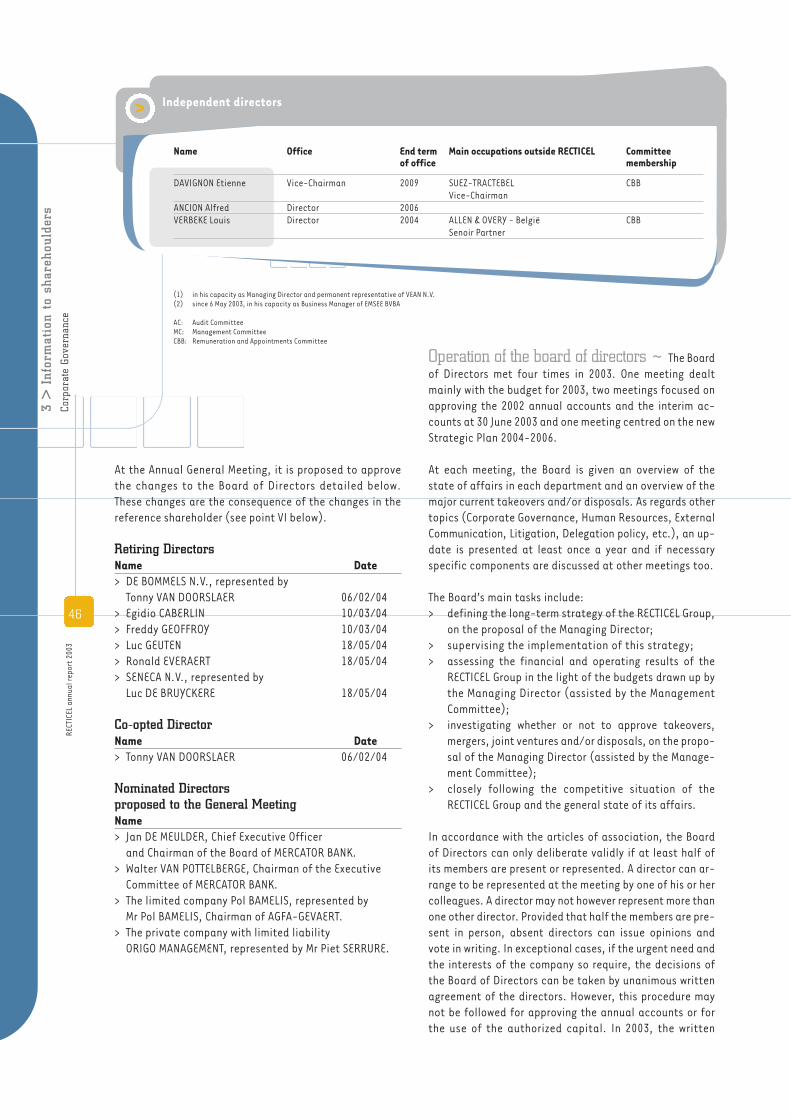

Shareholder structure ~The five-year period since the takeover of amajority of the Recticel shares by Rec-Holdended in 2003. The Group is proud that themajority of shareholders have extendedtheir commitment for an additional two-year period. This provides Recticel with an-other opportunity to continue to work on itsdevelopment as a group and on its long-term vision and ambitions, with the backingof stable shareholders.

2004 is possibly becoming a transitional year. If the hopedfor economic recovery does in fact become reality, the re-structuring carried out bears fruit and the start-up phasesin the automotive business line go according to plan, theGroup is certain that it will be once more on the road toprofit in 2004. 2003 has not been an easy year and we have had to callmore than ever on your efforts and patience. We should liketo express our thanks for this to you all, both employeesand shareholders.

Luc Vansteenkiste Luc Geuten

Luc Vansteenkiste Luc Geuten

RECT

ICEL

annu

al re

port

200

3R

epor

t by

the

boa

rd o

f D

irec

tors

6

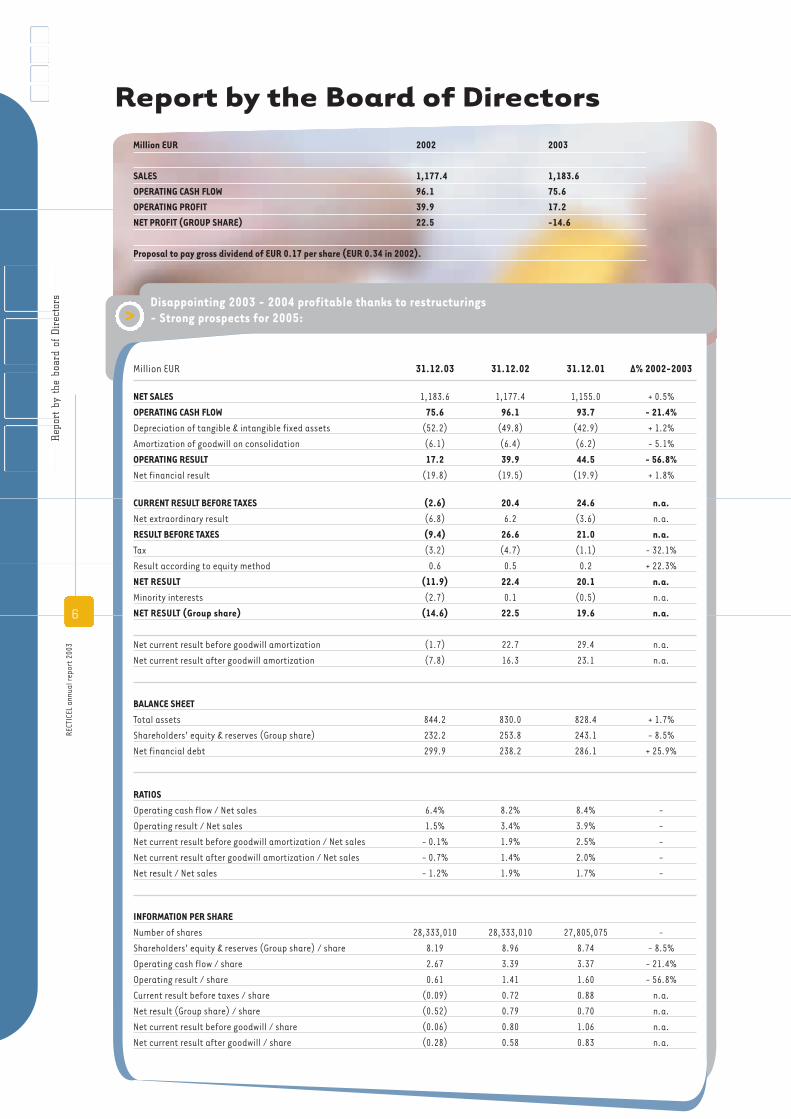

Million EUR 2002 2003

SALES 1,177.4 1,183.6OPERATING CASH FLOW 96.1 75.6OPERATING PROFIT 39.9 17.2NET PROFIT (GROUP SHARE) 22.5 -14.6

Proposal to pay gross dividend of EUR 0.17 per share (EUR 0.34 in 2002).

Million EUR 31.12.03 31.12.02 31.12.01 ∆% 2002-2003

NET SALES 1,183.6 1,177.4 1,155.0 + 0.5%OPERATING CASH FLOW 75.6 96.1 93.7 - 21.4%Depreciation of tangible & intangible fixed assets (52.2) (49.8) (42.9) + 1.2%Amortization of goodwill on consolidation (6.1) (6.4) (6.2) - 5.1%OPERATING RESULT 17.2 39.9 44.5 - 56.8%Net financial result (19.8) (19.5) (19.9) + 1.8%

CURRENT RESULT BEFORE TAXES (2.6) 20.4 24.6 n.a.Net extraordinary result (6.8) 6.2 (3.6) n.a.RESULT BEFORE TAXES (9.4) 26.6 21.0 n.a.Tax (3.2) (4.7) (1.1) - 32.1%Result according to equity method 0.6 0.5 0.2 + 22.3%NET RESULT (11.9) 22.4 20.1 n.a.Minority interests (2.7) 0.1 (0.5) n.a.NET RESULT (Group share) (14.6) 22.5 19.6 n.a.

Net current result before goodwill amortization (1.7) 22.7 29.4 n.a.Net current result after goodwill amortization (7.8) 16.3 23.1 n.a.

BALANCE SHEETTotal assets 844.2 830.0 828.4 + 1.7%Shareholders’ equity & reserves (Group share) 232.2 253.8 243.1 - 8.5%Net financial debt 299.9 238.2 286.1 + 25.9%

RATIOSOperating cash flow / Net sales 6.4% 8.2% 8.4% -Operating result / Net sales 1.5% 3.4% 3.9% -Net current result before goodwill amortization / Net sales - 0.1% 1.9% 2.5% -Net current result after goodwill amortization / Net sales - 0.7% 1.4% 2.0% -Net result / Net sales - 1.2% 1.9% 1.7% -

INFORMATION PER SHARENumber of shares 28,333,010 28,333,010 27,805,075 -Shareholders’ equity & reserves (Group share) / share 8.19 8.96 8.74 - 8.5%Operating cash flow / share 2.67 3.39 3.37 - 21.4%Operating result / share 0.61 1.41 1.60 - 56.8%Current result before taxes / share (0.09) 0.72 0.88 n.a.Net result (Group share) / share (0.52) 0.79 0.70 n.a.Net current result before goodwill / share (0.06) 0.80 1.06 n.a.Net current result after goodwill / share (0.28) 0.58 0.83 n.a.

Disappointing 2003 - 2004 profitable thanks to restructurings- Strong prospects for 2005:>

Report by the Board of Directors

RECT

ICEL

annu

al re

port

200

3R

epor

t by

the

boa

rd o

f D

irec

tors

7

Review of sales and profit ~The sales of the Group rose in 2003 by 0.5% to EUR 1,183.6million.

On a comparable basis, sales would have risen by 2.2%.However, part of the growth was neutralized by exchangedifferences (an amount of EUR 26.7 million), especially withregard to the American dollar and pound sterling.

In addition, the scope of consolidation was changed asfollows:- the integration of the remaining 50% of the Greek Ri-

comex (flexible foam), which represents sales amount-ing to EUR 2.5 million;

- the integration of 51% of the activities of the plant inTrilport, France (automotive), accounting for EUR2.6 million;

- the integration of 50% of the Japanese Inorec, whichwas still not consolidated in 2002, for EUR 1.9 million;

Operating cash flow fell by 21.4% to EUR 75.6 million. TheInsulation and Flexible Foam business lines showed strongperformances and declined only slightly in spite of thedifficult market. Automotive and Bedding were faced withlower profitability.

The decline is primarily attributable to a wide variety ofexternal factors, such as the lower volumes of the FordMondeo, the delayed start-up of various contracts in theautomotive industry and the persistent pressure on con-sumption in the bedding sector.

8,1%

34,2%

30,9%

26,8%

>

2003 % 2002 %

Flexible foam (1) 29.8 39.4 33.8 34.9Bedding 19.5 25.8 24.2 25.0Automotive (1) 16.0 21.1 28.4 29.4Insulation 10.3 13.7 10.4 10.7

75.6 96.1

Operating cash flow (in million EUR)

(1) The sales and operating cash flow of the American subsidiary Soundcoat, which were hitherto included in the ‘automotive’ business line, have beenintegrated in the ‘flexible foam’ business line since the beginning of 2003. The 2002 figures have been adjusted to this situation to make them comparablewith those of 2003.

2003 Breakdown of sales by business line

Flexible foam> 34.2%

Bedding> 30.9%

Insulation> 8.1%

Automotive> 26.8%

2000 2001 2002 2003

1070

1155

1999

1023

1177 1184

Sales [in million EUR]

39,4%

25,8%

21,1%

13,7%

2003 Breakdown of cash flow by business line

Flexible foam> 39.4%

Bedding> 25.8%

Insulation> 13.7%

Automotive> 21.1%

RECT

ICEL

annu

al re

port

200

3R

epor

t by

the

boa

rd o

f D

irec

tors

8

The operating profit fell from EUR 39.9 million to EUR 17.2million.

Financial expenditure increased slightly from EUR 19.5million to EUR 19.8 million. Net interest charges amountedto EUR 15.4 million (EUR 17.5 million in 2002), showing areduction mainly as a result of lower prevailing interestrates and a lower average outstanding debt. The net im-pact of foreign exchange differences resulted in a chargeof EUR 1.7 million.

Net extraordinary charges amounted to EUR 6.8 million.The most important extraordinary factor was the sub-stantial cost of the additional restructuring announced inSeptember 2003 and carried out in the meantime. After 500 jobs were already lost in 2002, it was decided in2003 to implement some 1,000 more redundancies, the ma-jority of which have now occurred.

In Germany and the Netherlands, two plants in the beddingsector were closed. In addition, a further two conversionunits are being closed in Germany, restructuring was carriedout in ten other plants, including the headquarters of theGroup, and the general administration costs and researchand development costs were slashed. The costs of and provisions for these operations amountedto EUR 9 million and were booked to the 2003 accounts.

All these measures yield structural savings estimated atEUR 16.3 million for 2004 and EUR 19.3 million for 2005.

Tax fell to EUR 3.2 million.

The minority interests amounted to EUR 2.7 million andcomprise the joint ventures with Copirel of France (bed-ding) and JR Interiors of Germany (automotive).

Under the impact of all these factors, the Group recorded anet loss (Group share) of EUR 14.6 million.

(*) added by written decision of the Board of Directors of 30 April 2004.

Market sectors ~ For a report on the individual business lines and the com-ments on them included in the report of the Board of Di-rectors, please refer to the sections on the business lineslater in this report.

Level of financial debt ~ Recticel respects the maximum debt level within thecontext of the syndicated loan. The lower than foreseencash flow for 2003 leads to a temporary overrun of one ofthe conditions.

On the basis of the current discussions with the banks, theGroups trusts that the situation will soon be corrected.

On 26 April 2004, the Board of Directors was informed that thesyndicate of banks has agreed to allow Recticel a waiver from some ofits commitments until 30 September 2004. (*)

Prospects for the future ~ The Group will return to profit again from 2004 and haseven better prospects for 2005.

1

1 > The Recticel Group 2 > Business lines 3 > Information to shareholders 4 > Financial section

10 Mission Statement11 Strategy12 Synergy13 Human Resources14 Research and Development15 Safety and environmental protection16 Quality policy

Finding balance in time to come

The Recticel Group

RECT

ICEL

annu

al re

port

200

3

10

> Mission Statement

• to meet everyone’s desire for greater comfort in everyday life;

• to be a coherent group consisting of four business lines (Flexible Foams,Bedding, Automotive and Insulation), strengthened by long experience incomfort marketing and technology and by outstanding knowledge of polyurethane foam, materials and production processes;

• to create added value for its customers and its shareholders;

• to offer all employees the opportunity to develop their individual talents,within the framework of the group strategy;

• to assume its responsibilities as an organization within the community, witha strong emphasis on quality, safety, health and environmental protection.

Group values

• Team spirit

• Entrepreneurship

• Creativity and innovation

• Respect for the environment and the individual

• Transparency and openness

1 >

The

Rec

tice

l G

roup

Mis

sion

sta

tem

ent

/ Gr

oup

valu

es

Recticel wishes :

RECT

ICEL

annu

al re

port

200

31

> T

he R

ecti

cel

Gro

upSt

rate

gy

11

StrategyThe Recticel Group’s global strategy focuses on three important components:

Volume ~ Recticel wishes to play a leading role in thesupply of block foam. The supply is large, especially in theflexible foams sector, and more specifically the foamfillings for seats, and the entry threshold for new ma-nufacturers is quite low. The Group wishes to secure itsmarket share and profitability through good control of itsown productivity and optimum utilization of its productionmachinery.

Brand policy ~ To stand out more clearly within anoften very competitive market and to secure its own pro-ducts against the resultant price pressure, Recticel hasopted for a strong brand policy. The Group uses strongbrand names, especially in the bedding sector. Some areknown mainly in a local market (Schlaraffia in Germany,Beka in Belgium, Ubica in the Netherlands, Superba inSwitzerland, Epeda-Merinos in France, etc.). Other brandsform typical examples of a pan-European approach andare distributed in several countries (Swissflex, Lattoflex,Literie Bultex, etc.).

Technology ~ Research and development, creativityand technological innovation form the structure of theGroup’s further expansion. The most important break-through in this field is undoubtedly the unique Spraytechnology. By using the ‘Colofast Spray’ technology,Recticel was the first to be able to supply colourfastcomponents in polyurethane, which has permitted a re-volutionary modernization of the interior finish for cars.

In addition, a large number of new types of technicalfoams were the result of sustained efforts in the field ofresearch and development, just like Tau foam, which gavenew impetus to the application of PU as an insulationmaterial in the construction industry, through its light-ness, great strength and improved fire-resistance.

> POLYURETHANE PRODUCTION> flexible and rigid foams

> BRAND POLICY> bedding

> HIGH-TECH APPLICATIONS> automotive

Control of

RECT

ICEL

annu

al re

port

200

3

12

1 >

The

Rec

tice

l G

roup

Syne

rgy

SynergyRecticel operates in four different sectors. Nevertheless, there are a number of areas where thesevarious activities overlap, which the Group has fused together soundly.

RECTICEL OPERATES IN FOUR

DIFFERENT SECTORS.

NEVERTHELESS, THERE ARE

A NUMBER OF AREAS WHERE THESE

VARIOUS ACTIVITIES OVERLAP,

WHICH THE GROUP HAS FUSED

TOGETHER SOUNDLY

Technology ~ Technologically, polyurethane formsthe leitmotiv for the Group’s highly diverse activities.Polyurethane technology, in both manufacturing andconversion, forms the basis for new, innovative appli-cations and for improving the quality of existing products.

Purchasing power ~ There is a centralizedpurchasing policy for chemical raw materials. This hasenabled Recticel to acquire an important position as buyerof these raw materials, the second largest in the world. Allplants benefit from this. The Group has also taken steps tocombine purchases of other strategic raw materials, suchas latex, textiles and metal components, for the beddingbusiness line.

Overlapping of the business lines ~ Althoughthe Group’s joint activities have been divided into fourdifferent business lines, it is sometimes difficult to drawfirm lines between them and to mark off all the appli-cations strictly. A large number of products of the tech-nical foams business line, for example, are used in theautomotive industry. Clearly there is overlapping betweenthe various sectors which in a large number of cases cantherefore be considered as complementary.

In this way, certain business lines derive benefit fromthe possibilities offered by others, which is a clear illus-tration of the economies of scale which this comple-mentarity entails.

Marketing ~ All business lines are characterized bythe need for their own specific marketing strategy. Forall that, there are also parallels. For instance, the large-scale advertising campaign in the bedding business linefor Literie Bultex also paved the way for the brand nameComfort Bultex becoming better known. ‘Comfort Bultex’has grown in the flexible foams business line since 1995to become the only filling material able to gain a com-petitive advantage from its brand name and its visibility.

Recycling ~ Off-cuts of foam left over from the con-version process are recycled. In this way, the trim foamfrom various activities is manufactured into new, reboundfoam which in turn is used for applications in all thebusiness lines.

RECT

ICEL

annu

al re

port

200

31

> T

he R

ecti

cel

Gro

upH

uman

Res

ourc

es

13

Human Resources

Whilst the human resources policy developed further at group level within the framework defined inprevious years, 2003 was marked by a number of specific challenges. On account of the economicdownturn, disappointing results and the failure of the expected recovery to materialize, the Groupfound itself obliged to adapt to economic reality and to implement a whole series of restructurings.

2003 saw the closure of four plants. In the Netherlands, theDeventer plant was shut down and mattress productionwas transferred to Hulshout (Belgium). The German slatbase production plant in Holzwickede was also closed. Theactivities are being started up again in the Czech Republic.In addition, a further two flexible foam conversion units inGermany are being closed.

In addition to the closure of the above-mentioned plants,some ten other plants underwent fundamental restruc-turing and additional efforts were made to cut generaloperating costs.

All these measures resulted in some 1000 job losses in 2003,implemented mainly during the second half of the year. Asa result of adapting the general structures, the number ofGroup senior executives was also reduced by 30 (or 20%)during 2002-2003. The total cost of all these operations for2003 comes to EUR 9 million.

The restructurings will allow Recticel to save at least EUR16.3 million in 2004. For 2005, this figure is estimated atEUR 19.3 million.

As a result of the development of the Group in the UnitedStates and the growth markets of Central and EasternEurope, 375 new jobs were created in 2004, thus confiningthe total reduction in the workforce to 5%.

The Group is aware that the reductions have increased thepressure on the present structures. It is nevertheless con-vinced that the past efforts were essential to form thenecessary basis to face the future of the Group with re-newed confidence.

> Key figures

Workforce 2003 11,421

(full-time and part-time employees, excluding temporary workers and those medically unfit for work and including all employees of jointventures in which Recticel has 50% control)

Closures: Wabern (D)Bad Ditzenbach (D)Deventer (NL)Holzwickede (D)

Redundancies 2003: approximately 1000 members of staff

Recruitments 2003: approximately 375 members of staff

Restructuring costs: EUR 9 million

Estimated savings: 2004: EUR 16,3 million2005 — : EUR 19,3 million

RECT

ICEL

annu

al re

port

200

3

14

1 >

The

Rec

tice

l G

roup

Res

earc

h an

d D

evel

opm

ent

Research and Development: the IDCOne of the Group’s greatest advantages is the availability of a centralized research centre. The IDC islocated in Wetteren (Belgium), gathers together the experience and knowhow of the Group in a singlelocation and is available to all plants and business lines.

The IDC has a team of some 160 researchers. Of the 2003budget, amounting to EUR 17.2 million, more than 75% wasallocated to research in the automotive sector.

In the more traditional sectors, the IDC succeeded inboosting the quality of existing products further and indeveloping new variants. One example is the introductionof Bulfast derived products, the light-stable foam whichhas made a breakthrough particularly in the textiles sector(especially in bra cup fillings). Another example is thedevelopment of ‘moulded re-bound foam’ technology,which enables recycled foam off-cuts to be converted intomore complex finished components. In the recycling field,a great deal of attention focused on new sound-insulatingunderlays for parquet floors.

The research centre succeeded in rendering the use of allHCFCs superfluous in insulation materials through theintroduction of alternative blowing agents. This break-through is confirmation of the Group’s concern to play aleading role in the protection of the living world and theenvironment through research and development.

The major part of the budget was allocated to the auto-motive sector. This is the area on which Recticel focuses tosafeguard its leading position, through its single-mindedefforts to achieve technological and chemical advances.

2%

19%

2%

77%

>

1999 2000 2001 2002 2003

Net sales of Group 1 023.2 1 069.6 1 155.0 1 177.4 1 183.6R&D expenditure 10.7 11.0 12.6 14.9 17.2R&D as %of net sales 1.04% 1.03% 1.09%1 1.27% 1.45%

Trend in R&D budget (Million EUR)

In Spray technology, attention focused on both techno-logical aspects and the development of new designs. TheGroup has made significant progress towards the indepen-dent production of components of the mixing and measu-ring system of the Spray robots, for own use, which safe-guards the patented technology even more effectively. Atthe same time, products were developed which differ inappearance from the traditional leather structure andoffer manufacturers the opportunity to introduce inno-vative designs in the car interior.

In general, it can be stated that the research centrealready has a number of possibilities ready for applicationwhich are currently awaiting commercial development. Toencourage the commercialization of these new products, itis now a matter of being involved in the discussions withthe car manufacturers at the earliest stage of prototyping.

Budget 2003: EUR 17.2 million

Flexible foam> 19%

Other> 2%

Insulation> 2%

Automotive> 77%

RECT

ICEL

annu

al re

port

200

31

> T

he R

ecti

cel

Gro

upSa

fety

and

the

Env

iron

men

t

15

Safety and the EnvironmentThe Group continued to pay particular attention to safety, health and the environment in 2003. Ineach of these three fields, efforts focused primarily on improving the results of past years stillfurther. New initiatives were also developed to strengthen the safety, health and environment policyor to adapt it to the latest trends.

Safety ~ The safety aspect was already selected theprevious year by the European Works Council (EWC) as oneof the most important topics. The ensuing dialogue has ledto concrete action plans. Reports are made on these planswithin the EWC and they have already been the subject of afirst evaluation. As a result, alongside general, very fun-damental safety provisions, new points for attention havealso appeared on the agenda, such as ergonomics, andaction plans have been drawn up to prevent, for example,back complaints and other ailments caused by repetitivemovements. In most countries, these measures have al-ready yielded conspicuous results.

Health ~ Recticel has already been identifying sub-stances which are proactively banned from its own pro-duction process for over five years. In this way, the Groupaims not only to anticipate possible future legislation, butalso to play an active role in preventing any potential riskfor the end-user.The list drawn up by Recticel is currently being discussed bythe European umbrella associations of polyurethane pro-ducers, where a great deal of support can be counted onfor the principle. The Group is proud to be able to play aleading role and to make a significant contribution to thesafety of the workers and end-users at this level too.

Environment ~ Care of the environment is nothingnew and continues unabated. Although the majority ofactions are not confined to just one year and call for con-tinuous monitoring, there is always scope for new initia-tives or changes in emphasis. In 2003, together with theIDC, considerable efforts were made to confine possibleemissions to an absolute minimum through optimization ofthe chemical formulas. A great deal of attention is alsopaid to energy-saving, with a view to limiting consumptionof electricity, gas and mineral fuels to a minimum.

Health, safety and environment are a daily concern,calling for continuous monitoring and promotion. It is nota matter of shifting attention constantly and completelyto new actions all the time. The Group is convinced that thebest results tend to be achieved through far-reaching,sustained efforts with respect to the traditional, everrecurring themes, supplemented where appropriate withuseful extensions to fields where there is the greatestpotential for improvement. Although the points on whichthis policy focuses will possibly be less spectacular inthemselves, the results, which can only be achieved in thisway, will prove that the Group is successful in fulfilling itsleading role in these fields too.

RECT

ICEL

annu

al re

port

200

3

16

1 >

The

Rec

tice

l G

roup

Qua

lity

polic

y

Quality policyThe daily concern for quality and the efforts to step up the Group’s performance as far as possiblewere underpinned in 2003 by a number of new initiatives, which allow Recticel to keep track of thelatest trends in quality policy.

The success of the ‘6 Sigma’ methodology in the carindustry led to the Group gradually introducing specificprinciples of this working method into its own system. Itsaim is not only to ensure the quality of the derivedproducts, but also to further optimize the actual produc-tion processes.

The ‘6 Sigma’ method was initially started up in the Group’sAmerican plants, but since 2003 it has also been intro-duced in other countries. The principles of the methodo-logy are applied mainly in the automotive business line andare also used by customers, such as Volvo, with whomRecticel has cooperated actively to define specific needsand the potential of this method.

The introduction of the ‘6 Sigma’ method allows betteridentification of certain areas of risk in the productionprocess, which can then be adjusted in order, for example,to limit waste as far as possible. At the same time, this im-proves the delivery performance to the customer (throughlower ppm).

The ‘6 Sigma’ method fulfilled its objective and conspi-cuous results have already been achieved in the fields inwhich the principles are implemented.

In the meantime, the ideas of the new method have alsobeen transferred to the supporting Shared Service func-tions of the Group, where they are applied to the admini-strative processes. This entails defining the expectationsof primarily the internal customers in Service LevelAgreements, mapping out the administrative processesand determining the results hoped for. Monitoring is car-ried out by means of Key Performance Indicators, which arethe subject of regular evaluations.

Although quality care is an established component ofeveryday policy and is based on fixed, unchanging prin-ciples, the Group is very enthusiastic about the metho-dology which it introduced in 2003 as extra support. It isconvinced that the improvement in the internal processeswill inevitably also benefit the quality of the goods andservices supplied.

Business lines

2

18 Polyurethane foam: production diagram19 Production plants21 Flexible foams26 Bedding30 Insulation34 Automotive

Creating real life experiences

1 > The Recticel Group 2 > Business lines 3 > Information to shareholders 4 > Financial section

RECT

ICEL

annu

al re

port

200

3

2 >

Bus

ines

s li

nes

Poly

uret

hane

foa

m:

the

prod

uctio

n di

agra

m

18

Polyurethane foam: the production diagram

Recticel’s PU production process yields rigid or flexiblefoam according to the formula used. Rigid foams are usedprimarily for insulation and can be produced in panels, butalso in larger blocks which can later be cut into morecomplex components.

Recticel’s other business sectors mainly use moreflexible types of foam. Most flexible foams are produced inblock form (slabstock) and then cut into various shapesand sizes (conversion) (for example, for the furniture in-dustry). Flexible foams can also be manufactured in spe-cific moulded shapes; this process is applied especially inthe production of car seat cushions.

Recticel’s research and development expertise has ena-bled it to produce polyurethane foams with new finishesand properties. For example, Colofast and Colofast Spraytechnology, both used with great success in the auto-motive industry, were the result of this.

CRUDE OIL

> >

>

> >

> >

>>

> >

> >>

>>

> >> > >

5% Residue

Flexible foams SprayRigid foams

Polyhydroxy compounds

MouldingBlocksPanelsBlocks

Conversion

Isocynates

95% Naphtha

POLYURETHANE FOAMS

FLEXIBLE FOAMS AUTOMOTIVEBEDDINGINSULATION

Conversion

The petrochemical industry refines some 95% of the crude oil it processes into naphtha and alliedproducts. Various other chemicals can be distilled from the 5% residue from the refining process,including polyhydroxy compounds and isocynates, the main raw materials used in the production ofpolyurethane foam (PU).

World production of plastics: 150 million tonnesWorld production of polyurethane (PU): 7.5 million tonnesEuropean production of polyurethane: 2.5 million tonnesEuropean production of flexible foam: 750,000 tonnesRecticel’s production of flexible foam: 200,000 tonnes

PU applications:Furniture, Automotive industry, Shoes, Construction and industry, Adhesives, Paints, Polymers, …The estimated annual growth of the European furniture market amounts to 3%, or 10,000 tonnes of PU

>

Flexible Foams InsulationBelgium: Wevelgem

TurnhoutBelgium: Hulshout

GeeraardsbergenFrance: Langeac

LimogesMassevauxRouenBelfortNoyen

Germany: WattenscheidJöhstadtHassfurt

Austria: TimelkamSwitzerland: Büron

FlühPoland: Lodz

Czech Republic: Jablonec

BeddingBelgium: Wetteren

HulshoutFrance: Trilport

Germany: RheinbreitbachWackersdorfEspelkampMallersdorfRüsselsheimUnterriexingen

UK: CorbyCzech

Republic: TepliceMlada Boleslaw

USA: Fountain Inn, SCAuburn Hills, MIClarkston, MITuscaloosa, AL

Japan: Nagoya

Automotive

In addition to the above-mentioned production plants,Recticel has some 60 other conversion units or sales offices in 20 countries.

Production plants

RECT

ICEL

annu

al re

port

200

32

> B

usin

ess

line

sPr

oduc

tion

plan

ts

19

Belgium: WetterenFrance: Langeac

LouviersThe Netherlands: Kesteren

Germany: BexbachBurkhardtsdorfDüsseldorfEbersbach

UK: AlfretonSweden: GislavedAustria: Kremsmünster

Italy: Gorla MinoriGreece: Aspropyrgos

Spain: Ciudad RodrigoPolyniaCataroja

Poland: ZgierzHungary: Sajobabony

Romania: Sibiú

Embracing tomorrows expectations

2 >

Bus

ines

s li

nes

FLEX

IBLE

FO

AM

S

Flexible foams

Facts & Figures ~

> The turnover of the European furniture market amounts tosome EUR 12.5 million.

> Italy and German account for approximately 53% of thistotal market.

> Of the total furniture imports into the EU, 50% come fromPoland.

> The European market in foam for the furniture sectorcomes to approximately 747,500 tonnes.

> The European technical foams market comes to approxi-mately 92,000 tonnes.

> There is a link between GDP and consumption of polyu-rethane foam per head of the population. In the EuropeanCommunity, 1.2 kg of foam is produced each year per headof the population, whereas in Romania only 0.3 kg is pro-duced at present.

Operating cash flow = operating profit (before financial result, extraordinary result,tax and minority interests) + depreciation on intangible and tangible assets +amortization of consolidation differences Operating cash flow is not equal to the gross variation in cash from operatingactivities, as indicated on page 61.

2000 2001 2002 2003

371.3

396.2

1999

346.7

402.2 404.5

RECT

ICEL

annu

al re

port

200

32

> B

usin

ess

line

sFL

EXIB

LE F

OA

MS

The flexible foams business line covers the manufacture, conversion and marketing of flexible po-lyurethane foam. The business line is the common denominator for three sub-sectors, which are eachdistinguished by the typical properties of the types of foam, the individual character of the pro-duction process or the typical possible applications of the foam.Most types of foam coming under this business line are manufactured in the form of slabstock and thenconverted by cutting into smaller components or finished products.Depending on their use, types of flexible foam are classified under ‘comfort’, which focuses mainly onthe furniture and mattress industry, or ‘technical foams’, which covers a large number of types offoam for domestic or industrial use, often in high-tech applications. The third business line sub-sector is that of ‘composite foams’, which is the result of Recticel’s active contribution in the fieldof recycling.

2003 ~ not a bad year in a difficult market

Sales rose by 0.6% to EUR 404.5 million(*). Lower volumes in the Western European furniture industrywere partially offset by increased production in Central Europe and the growth of sales in the‘technical foams’ business segment. Sales in ‘composite foams’ suffered from the low trim foamselling prices.The operating cash flow fell by 12.0% to EUR 29.8 million, mainly as a result of the low trim foamselling prices and the competitive climate which had a negative impact on the margins of the threebusiness segments. The fall was cushioned somewhat by raw materials prices returning at the end of2003 to their 2002 level.To further improve the profitability the Group decided to close two conversion units in Germany(Wabern and Bad Ditzenbach) during 2003. Fixed production costs were reduced and the Groupinvests in new markets and niches with a high added value.

(*) The sales and operating cash flow of the American subsidiary Soundcoat, which were hitherto included in the ‘automotive’ business line, have beenintegrated in the ‘flexible foam’ business line since the beginning of 2003. The 2002 figures have been adjusted to this situation to make them comparablewith those of 2003. 21

Sales (EUR million)

Flexible foams 2001 2002 2003

Growth in sales 6.7% 1.5% 0.6%Operating cash flow (million EUR) 24.9 33.8 29.8Operating cash flow margin 6.3% 8.4% 7.4%Investments in intangible 9.0 10.0 13.5(excluding goodwill) and tangible fixed assets (million EUR)Investments as % of net sales 2.3% 2.5% 3.3%

RECT

ICEL

annu

al re

port

200

3

22

2 >

Bus

ines

s li

nes

FLEX

IBLE

FO

AM

S

Comfort>Activities and products ~ Recticel’s comfortbusiness sector manufactures and converts flexible polyu-rethane foam which is used as filling for all kinds of seatingand mattresses.

The long slabstock resulting from the production pro-cess is cut into smaller, transportable pieces. These smallerfoam blocks are either delivered directly to customers orare cut to shape to customer specifications in one ofRecticel’s many conversion plants. The finished products(seat pads, backs, arm-rests, mattress centres) are sup-plied directly to the furniture or mattress industry.

In a number of cases, specific components for the fur-niture industry are produced in moulds, so that subsequentcutting is unnecessary.

This wide production network has spread during the pastdecade to far beyond the boundaries of Western Europe.The activities in Central and Eastern Europe, which takeplace through the Eurofoam joint venture, have grownenormously during the same period.

2003 ~ Net sales amounted to EUR 240.3 million, 0.6%down on the 2002 figure. This shows that this sector isholding its own in terms of sales, thanks to the trend inCentral Europe.

Profits were showing the first signs of recovery at the endof the second half of the year.

Competitive situation ~ The production of PU foamhas a low entry threshold, as a result of which the Europeanmarket is highly fragmented, with a large number ofsmaller manufacturers. However, on account of the risingdemand for customized solutions and quality, the onlygroups which will remain in the future will be those withpan-European ambitions. It is therefore expected that theglobal market will consolidate further. Today, only threegroups operate at European level. Recticel and British Vitaare in the lead, each with a market share of some 20%. TheAmerican Carpenter, the third group, also plays a signi-ficant role. These three groups are characterized by thespread of their manufacturing and conversion plantsthroughout a number of European countries. The rest of themarket is divided among a large number of smaller manu-facturers. At best, they play a role in their local markets,such as Olmo in Italy and Icoa in Spain, for example.

> La Ola - by Bretz Brothers

RECT

ICEL

annu

al re

port

200

32

> B

usin

ess

line

sFL

EXIB

LE F

OA

MS

Strategy and prospects: advantages for thefuture ~ The Group wishes to secure its position and toensure further growth in its sales and profitability. Variousfactors play a role here:

Internal growthIt is generally expected that the European furniture sectoras a whole will grow by an annual average of 3%, which boilsdown to 10,000 tonnes of foam per year. This means thatthere are continued prospects for limited internal growth.Recticel’s main advantages are its technological edge inthe field of manufacturing and conversion techniques, itsoptimum logistical structure and its adapted marketingapproach, focused on its own European brand, ComfortBultex.

Consolidation and reorganization The concentration movement in the European PU sector iscontinuing. The number of foam manufacturers in Europehas already fallen in recent years from 120 to around 60,which was mainly at the expense of the smaller, locally or-ganized companies. Recticel is closely examining any op-portunities for takeovers or new alliances.

Geographical expansionThe Group is trying to secure its growth through geograph-ical expansion. Eastern Europe is still important, since theannual consumption of polyurethane there is still far belowthe Western European average (in Romania, for example,annual consumption of polyurethane is a mere 300 gram-mes per head of the population, whilst the Western Euro-pean average is 1.2 kilogrammes). At the same time, Recticelis building up a strong position in Southern Europe, a marketwith enormous potential. The takeover of Inespo in Spain isa striking example of this.

InnovationFinally, Recticel also expects growth through the intro-duction of types of foam with new properties, such asFramefoam (a foam with a support function which offersan excellent alternative to traditional furniture-buildingmaterials, such as wood), Sensus (a visco-elastic foamwhich ensures outstanding distribution of pressure),Foam4Care (which is used mainly in medical applicationsand which increases patient comfort, both in hospital andat home) and Dryfeel (which repels water well and is hencewell suited for use in garden furniture).

23

> Modern shapes in seating

RECT

ICEL

annu

al re

port

200

3

24

2 >

Bus

ines

s li

nes

FLEX

IBLE

FO

AM

S

Activities and products ~ Recticel manufacturesseveral hundred technical foam types, often intended forrelatively smaller and specialized applications. The mainapplications for technical foams are in filtration, asairtight and watertight seals, in acoustic insulation, pack-aging material, sponges, etc. Rolls of technical foam arealso used to laminate other materials, such as textiles,leather, etc. Just like the flexible foams for comfort appli-cations, technical foams are manufactured in the form ofslabstock which is then cut. On account of the very specificapplications and the strict specifications which the typesof foam must meet, extra post-treatment is sometimesnecessary (reticulation, impregnation, etc.), which adaptsthe physical or chemical properties to the customer’srequirements.

2003 ~Sales rose by 3.0% to EUR 148.1 million.

The establishment of Corpura in The Netherlands (medicalapplications, inter alia) shows that Recticel is capable offurther development towards high-quality foam techno-logies, which is entirely in keeping with the Group’s stra-tegy.

Technical Foams>Competitive situation ~ The manufacture oftechnical foams demands the greatest precision. The che-mical know-how is consequently particularly important.Furthermore, the post-treatment which technical foamsundergo in many cases is also a complex affair. The con-sequence of all these factors is that the production oftechnical foams requires substantial investments in bothR&D and the technological infrastructure. It is precisely forthis reason that there are few manufacturers of technicalfoams. Within Europe, the sector is dominated by two majorgroups, Recticel and British Vita.

Local groups, such as Otto Bock and Reisgies, also playan important role in the German market. The Italian marketis dominated mainly by Orsafoam (in which Recticel has a33% stake) and Olmo, while Inespo (100% Recticel) andIcoa are the market leaders in Spain.

Strategy and prospects: advantages for thefuture ~ Recticel anticipates a further potentialannual growth of 5% in its technical foam activities, notincluding possible takeovers. The basis for this growth liesin creativity and innovation, which will ensure that types offoams are developed or adapted for new applications.

At the same time, there are possibilities for geographicalexpansion here too. The takeover of Inespo in Spain, forexample, opened the door in 2001 to a significant marketfor technical foams. Recticel investigates all opportuni-ties for takeovers capable of allowing the business line togrow at a faster rate.

> The “loop splitter” converts slabstock into continuous rolls.

2 >

Bus

ines

s li

nes

FLEX

IBLE

FO

AM

S

RECT

ICEL

annu

al re

port

200

3

> Composite foams

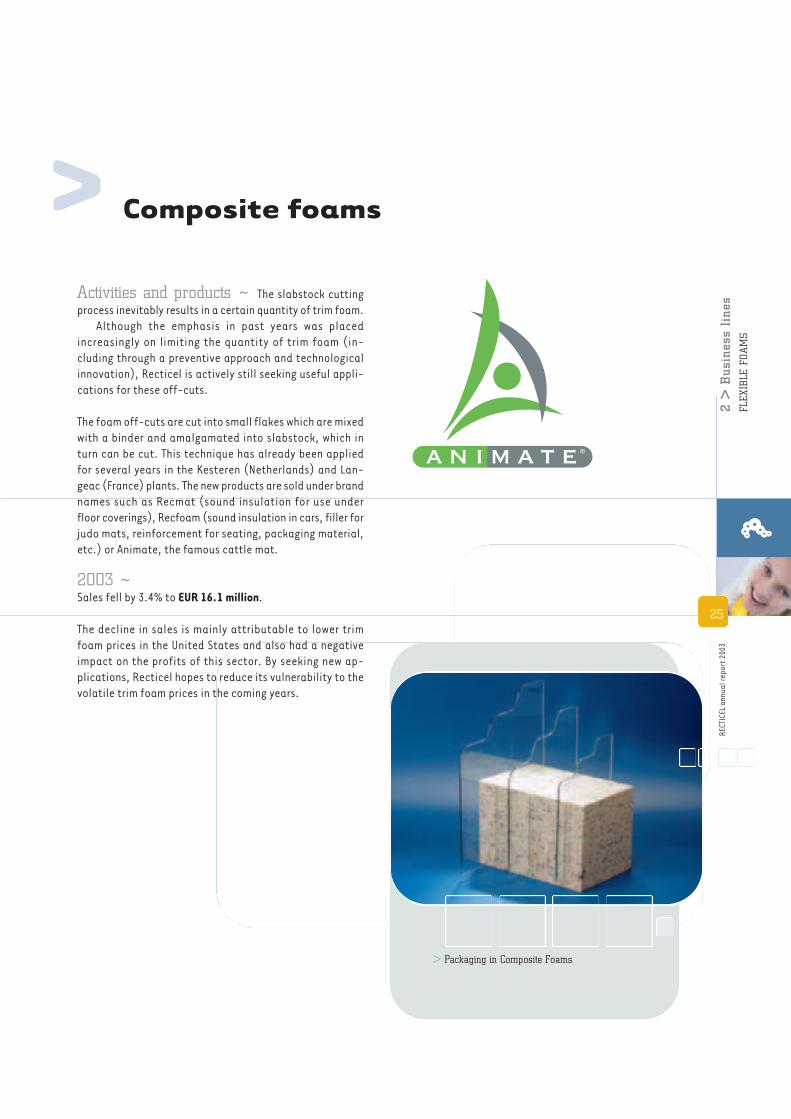

Activities and products ~ The slabstock cuttingprocess inevitably results in a certain quantity of trim foam.

Although the emphasis in past years was placedincreasingly on limiting the quantity of trim foam (in-cluding through a preventive approach and technologicalinnovation), Recticel is actively still seeking useful appli-cations for these off-cuts.

The foam off-cuts are cut into small flakes which are mixedwith a binder and amalgamated into slabstock, which inturn can be cut. This technique has already been appliedfor several years in the Kesteren (Netherlands) and Lan-geac (France) plants. The new products are sold under brandnames such as Recmat (sound insulation for use underfloor coverings), Recfoam (sound insulation in cars, filler forjudo mats, reinforcement for seating, packaging material,etc.) or Animate, the famous cattle mat.

2003 ~Sales fell by 3.4% to EUR 16.1 million.

The decline in sales is mainly attributable to lower trimfoam prices in the United States and also had a negativeimpact on the profits of this sector. By seeking new ap-plications, Recticel hopes to reduce its vulnerability to thevolatile trim foam prices in the coming years.

25

> Packaging in Composite Foams

2 >

Bus

ines

s li

nes

BED

DIN

G

Treasuring the cheerful nightlife

3

RECT

ICEL

annu

al re

port

200

32

> B

usin

ess

line

sB

EDD

ING

Bedding

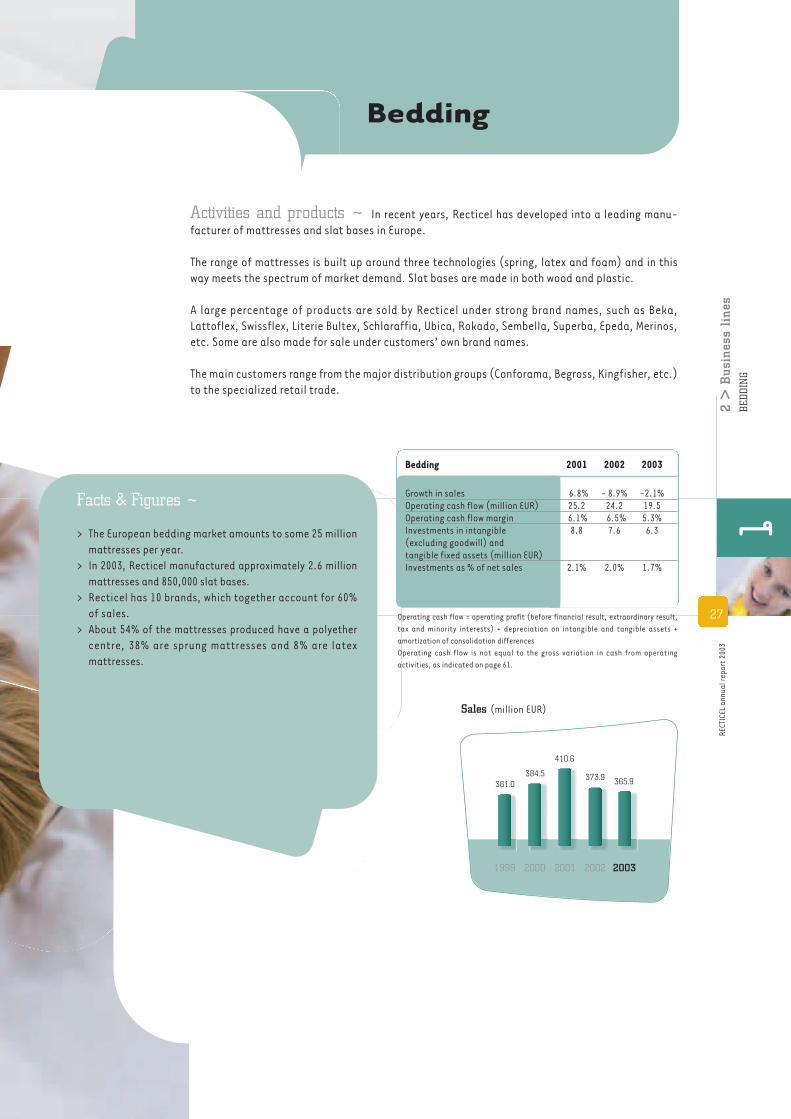

Activities and products ~ In recent years, Recticel has developed into a leading manu-facturer of mattresses and slat bases in Europe.

The range of mattresses is built up around three technologies (spring, latex and foam) and in thisway meets the spectrum of market demand. Slat bases are made in both wood and plastic.

A large percentage of products are sold by Recticel under strong brand names, such as Beka,Lattoflex, Swissflex, Literie Bultex, Schlaraffia, Ubica, Rokado, Sembella, Superba, Epeda, Merinos,etc. Some are also made for sale under customers’ own brand names.

The main customers range from the major distribution groups (Conforama, Begross, Kingfisher, etc.)to the specialized retail trade.

27

Facts & Figures ~

> The European bedding market amounts to some 25 millionmattresses per year.

> In 2003, Recticel manufactured approximately 2.6 millionmattresses and 850,000 slat bases.

> Recticel has 10 brands, which together account for 60%of sales.

> About 54% of the mattresses produced have a polyethercentre, 38% are sprung mattresses and 8% are latexmattresses.

2000 2001 2002 2003

384.5

410.6

1999

361.0373.9 365.9

Operating cash flow = operating profit (before financial result, extraordinary result,tax and minority interests) + depreciation on intangible and tangible assets +amortization of consolidation differencesOperating cash flow is not equal to the gross variation in cash from operatingactivities, as indicated on page 61.

Bedding 2001 2002 2003

Growth in sales 6.8% - 8.9% -2.1%Operating cash flow (million EUR) 25.2 24.2 19.5Operating cash flow margin 6.1% 6.5% 5.3%Investments in intangible 8.8 7.6 6.3(excluding goodwill) and tangible fixed assets (million EUR)Investments as % of net sales 2.1% 2.0% 1.7%

Sales (million EUR)

RECT

ICEL

annu

al re

port

200

3

28

2 >

Bus

ines

s li

nes

BED

DIN

G

2003 ~growth of market sharein a declining market

Recticel, which achieved sales in its bedding business lineamounting to EUR 365.9 million, succeeded in limiting thefall to 2.1%. The performance of France and Austria wasrelatively stronger.

Because of the unfavourable market conditions, operatingcash flow declined by 19.4% to EUR 19.5 million.

To secure its competitiveness in this sector, the Groupembarked upon a far-reaching restructuring plan. Manu-facturing was closed down in the Netherlands and trans-ferred to Belgium. A German slat base manufacturing plantis being closed and started up in the Czech Republic.

Furthermore, actions are taken in certain countries for astronger positioning of the brands through specific marke-ting strategies (shop-in-the-shop).

> The Lattoflex Winx system

> Swissflex, top quality in bedding

RECT

ICEL

annu

al re

port

200

32

> B

usin

ess

line

sB

EDD

ING

29

Strategy and prospects: advantages for thefuture ~ Recticel anticipates slight growth in thebedding sector at European level. The competitive pressurewill however result in slight price erosion. Further opti-mization of the product mix should enable Recticel to finda suitable solution to this.

Growth in profitabilityThe production process for mattresses is undergoing fur-ther optimization and automation in a number of plants. Itis intended through ‘plant dedication’ to arrive at op-timum utilization of the production machinery, with someplants concentrating solely on brand products and otherson products without brand name.

Recticel has also taken steps to centralize its purchasingpolicy further as regards strategic raw materials (latex,springs and textiles).

Strategic cooperation The most important link in the growth of the sector is un-doubtedly the development of the strategic alliance withPikolin, Spain. The new group, with its 1000-strong work-force and 8 plants, is the absolute market leader in Francewith brands such as Literie Bultex, Epeda and Merinos.

It is now a matter of capitalizing to the full on thecooperation between the Spanish and French partners andall potential synergies, in both France and Spain itself.

Competitive situation ~ The European beddingmarket is dominated by two European groups. Apart fromRecticel, the Swedish Hilding Anders (Crown Bedding, Pull-man, Slumberland, Wifor, etc.) also plays a prominent role.

In addition, a number of other manufacturers, most ofthem originally family companies, are firmly entrenched inlocal markets. For instance, Sumitomo of Japan, with itsbrands Treca and Dunlopillo, still has strong presence onthe French market.

Recticel has a market share of at least 15% in all thecountries where it is present.

> The new ‘Shop-in-the-shop’-concept

2 >

Bus

ines

s li

nes

INSU

LATI

ON

Ensuring a feeling of well-being

RECT

ICEL

annu

al re

port

200

32

> B

usin

ess

line

sIN

SULA

TIO

N

Insulation

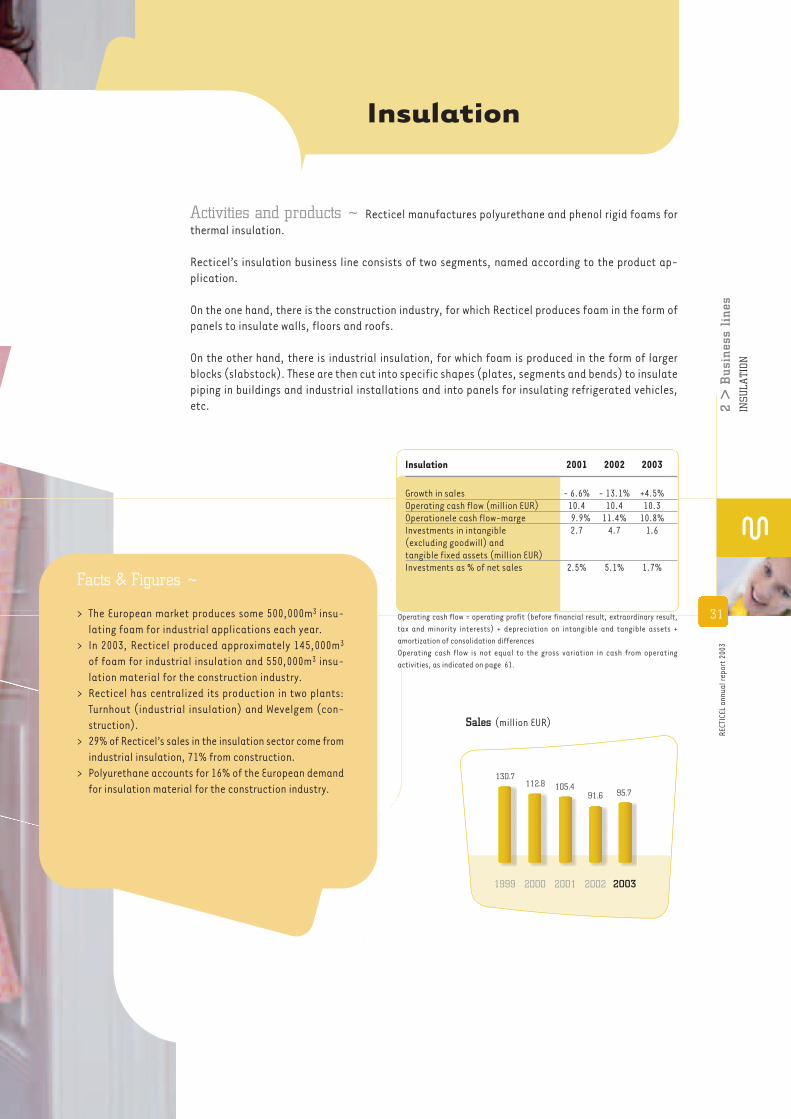

Activities and products ~ Recticel manufactures polyurethane and phenol rigid foams forthermal insulation.

Recticel’s insulation business line consists of two segments, named according to the product ap-plication.

On the one hand, there is the construction industry, for which Recticel produces foam in the form ofpanels to insulate walls, floors and roofs.

On the other hand, there is industrial insulation, for which foam is produced in the form of largerblocks (slabstock). These are then cut into specific shapes (plates, segments and bends) to insulatepiping in buildings and industrial installations and into panels for insulating refrigerated vehicles,etc.

31

Facts & Figures ~

> The European market produces some 500,000m3 insu-lating foam for industrial applications each year.

> In 2003, Recticel produced approximately 145,000m3

of foam for industrial insulation and 550,000m3 insu-lation material for the construction industry.

> Recticel has centralized its production in two plants:Turnhout (industrial insulation) and Wevelgem (con-struction).

> 29% of Recticel’s sales in the insulation sector come fromindustrial insulation, 71% from construction.

> Polyurethane accounts for 16% of the European demandfor insulation material for the construction industry.

Operating cash flow = operating profit (before financial result, extraordinary result,tax and minority interests) + depreciation on intangible and tangible assets +amortization of consolidation differencesOperating cash flow is not equal to the gross variation in cash from operatingactivities, as indicated on page 61.

2000 2001 2002 2003

112.8 105.4

1999

130.7

91.6 95.7

Insulation 2001 2002 2003

Growth in sales - 6.6% - 13.1% +4.5%Operating cash flow (million EUR) 10.4 10.4 10.3Operationele cash flow-marge 9.9% 11.4% 10.8%Investments in intangible 2.7 4.7 1.6(excluding goodwill) and tangible fixed assets (million EUR)Investments as % of net sales 2.5% 5.1% 1.7%

Sales (million EUR)

RECT

ICEL

annu

al re

port

200

3

32

2003 ~ stable and strong

Sales came out at EUR 95.7 million, 4.5% up on the 2002figures. The increase is mainly attributable to a rise in in-dustrial insulation and to the sale of insulation materialfor construction in the United Kingdom.

The operating cash flow remained stable at EUR 10.3 million.

ConstructionWhereas sales in this sector declined slightly in most Wes-tern European countries, in the United Kingdom they grewstrongly, easily compensating for the fall in the othercountries. Profit rose slightly thanks to a strong secondhalf of the year.

Industrial insulation (Tarec)Tarec’s sales rose slightly, mainly on account of the ful-filment of a number of export contracts. In spite of someextraordinary factors, such as the bankruptcy of a majorFrench customer and reorganization costs for the plant inTurnhout, the profit ended up only just below that of 2002.

2 >

Bus

ines

s li

nes

INSU

LATI

ON

> The Exhibition Center in Bilbao. 11.000 m2 Powerdeck roof insulation.

RECT

ICEL

annu

al re

port

200

32

> B

usin

ess

line

sIN

SULA

TIO

N

33

Three measures are to ensure that the profit from theinsulation sector will rise again in 2004. The Group will takeall the necessary steps for the business activities of thissector to reach breakeven point in Germany, to boost theproductivity of the Turnhout plant further and to draw themaximum synergy from the new Benelux organization.

Strategy and prospects: advantages for the future ~

Growth through product innovationRecticel has achieved a real breakthrough with its Taufoam products, Powerdeck and Powerline. Both productsare characterized by their low weight, their high com-pressive strength and their outstanding fire-resistantproperties. Tau foam is therefore a fully-fledged alterna-tive to mineral wool (Rockwool), which still has the largestmarket share within thermal insulation material for theconstruction sector.

Tarec developed VacPac in the past, a super-insulatingtype of foam for cold insulation (e.g. refrigerators) and al-so new high-density support rings which are used for theinsulation of piping. These products will be marketed byTarec.

Growth thanks to environmental standardsThe problems surrounding the greenhouse effect, CO2 emis-sions and global warming are ensuring that the importanceof good insulation is kept constantly in the news. A largeproportion of the standards the industrialized countrieshave set themselves as targets to prevent all these un-wanted effects can be achieved through better insulation.

In most cases, better insulation means using largerthicknesses of traditional materials. However, the increa-sed weight and volume associated with greater thicknesseslimit their practical application. Because it provides betterinsulation for an equal thickness and is extremely light,polyurethane foam offers a solution here. Recticel expectsthe polyurethane foam market to expand by some 2% to 3%per annum over the next few years.

Competitive situation ~ The market for insulationfor the construction industry is highly fragmented. On theone hand, there are various alternative products, amongwhich mineral wool is undoubtedly the best known. Withinthis range of insulation materials, polyurethane has atotal market share of 16%. This market share is distributedamong a large number of suppliers. Alongside Recticel,some of the best known names are Kingspan, Ecotherm andEfisol. The majority however are smaller, locally organizedmanufacturers, who have difficulties in meeting the everkeener competition and the demand for high-qualityproducts.

Recticel also has a presence in industrial insulation via itssubsidiary Tarec Insulation, which trades in a specialistmarket. Its products are especially suitable for cold in-sulation, while the majority of other usual materials tendto be used for warm insulation. Tarec plays a leading role inthis market segment at world level.

> the new packaging robot in the Wevelgem plant.

2 >

Bus

ines

s li

nes

AU

TOM

OTI

VE

Appreciating first-class refinement

RECT

ICEL

jaar

vers

lag

2003

2 >

Bus

ines

s li

nes

AU

TOM

OTI

VE

Automotive

Activities and products ~ Recticel’s automotive business line has proved to be the Group’sfastest-growing sector in recent years. One of the reasons is that polyurethane foam is usedincreasingly in the automotive industry. Moreover, Recticel has developed revolutionary technologyfor the production of innovative, high-quality interior trim. Recticel’s automotive business line concentrates not only on the more traditional applications forPU in cars, but also on three strategic activities:

> manufacturing moulded seat cushions > window encapsulation> manufacturing interior trim components or ‘Spray’,

named after the unique, patented technology.

Facts & Figures ~

> 54 million cars were sold worldwide in 2003. Europe is res-ponsible for about 1/3 of the total production.

> The European market is expected to grow in the comingyears by 16 to 18 million cars, mainly on account of growthin Central Europe.

> The average length of a contract in the automotive in-dustry is 6 to 7 years.

> Recticel has 13 patents on its Colofast Spray technology,protecting both the chemical properties and the techno-logy. In addition, the procedure is under way for 10 newpatents.

2000 2001 2002 2003

201.0

242.8

1999

184.9

309.8 317.5

41,8%

6,9%

27,4%

23,9%

Seating27.4%

Window Encapsulation23.9%

Spray41.8%

Traditional applications6.9%

Automotive 2001 2002 2003

Growth in sales 20.8% 27.6% 2.5%Operating cash flow (million EUR) 33.2 27.7 16.0Operating cash flow margin 13.7% 8.9% 5.0%Investments in intangible 44.3 44.1 78.1(excluding goodwill) and tangible fixed assets (million EUR)Investments as % of net sales 18.2% 14.2% 24.6%

Operating cash flow = operating profit (before financial result, extraordinary result,tax and minority interests) + depreciation on intangible and tangible assets +amortization of consolidation differences.Operating cash flow is not equal to the gross variation in cash from operatingactivities, as indicated on page 61.

Sales (million EUR)

35

RECT

ICEL

annu

al re

port

200

3

36

2 >

Bus

ines

s li

nes

AU

TOM

OTI

VE

2003 ~foundations of improvement laidafter a difficult year

In spite of the 1.7% decline in European car production,sales of the automotive business line rose by 2.5% to EUR317.5 million(*).

Operating cash flow dropped by 43.8% to EUR 16.0 million.

SeatingSales rose by about 3.0% to EUR 86.9 million, reversing thetrend of the first six months. Increased activity in Espelkamp(Germany) and the start-up of the new plant in Trilport,France (Peugeot and Citroën) compensated for the delay ina number of programmes and lower than forecasted vo-lumes for a number of car models (the most important ofwhich was the Ford Mondeo) during the second half of theyear.

The delayed contracts and the fall in volumes,combined with the raw materials price rises of the first halfof the year which put the margins under pressure, depres-sed operating cash flow.

(*) The sales and operating cash flow of the American subsidiary Soundcoat, whichwere hitherto included in the ‘automotive’ business line, have been integrated inthe ‘flexible foam’ business line since the beginning of 2003. The 2002 figures havebeen adjusted to this situation to make them comparable with those of 2003.

To withstand this situation, the Group finds itself obligedto carry out radical restructuring in the Hulshout plant(with the stoppage of two of the three production lines asa result).

In the meantime, Recticel’s and Woodbridge’s six Con-tinental European plants were united in the joint ventureRecticel Woodbridge Moulded Foam, which as a result isdeveloping into the leading independent European manu-facturer of moulded foam seating, with a 25% market share.The new structure is 70% controlled by Recticel and 30% byWoodbridge.

As a result of the start-up of new programmes for VW(Passat and Golf) and Opel (Astra), the joint venture ex-pects to be able to boost its total sales in 2004 to some EUR140 million and to improve its profitability considerably.

Car windows (‘exteriors’)In the ‘exteriors’ segment (both ‘window encapsulation’ or‘converting’ and the sale of ready-for-use compounds or‘compounding’), sales rose by 2.2% to EUR 78.2 million.

A number of new programmes were running into quality andproductivity problems in the ‘converting’ sector, which ledto a fall in profitability. The problems have now been sortedout.

The ‘compounding’ activity gave evidence of healthy growthin sales and profitability. China is becoming an importantnew sales market.

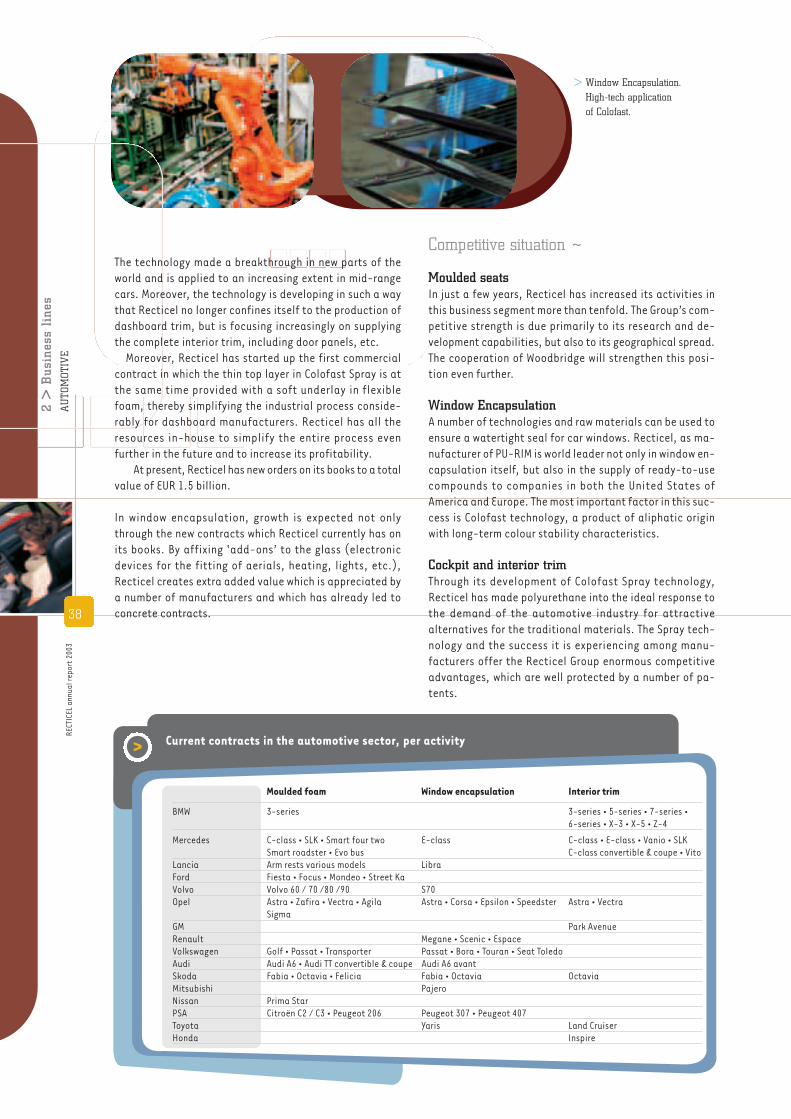

> The dashboard of the Mercedes E-class in Colofast Spray, Recticel’s contribution to comfortable driving in a top-class car.

RECT

ICEL

annu

al re

port

200

32

> B

usin

ess

line

sA

UTO

MO

TIV

E

37

Interior trim (‘interiors’)Total sales came out at EUR 132.8 million, a 15% increase.During the first half of the year, the Group launched newprojects for Honda in Japan and for BMW (the new 5-seriesand the X3). During the second half of the year, there wasthe new project for the Mercedes Vito.

Because of the postponement on the one hand and theacceleration on the other hand of two different projects inone plant, start-up costs increased. Apart from that, theGroup incurred a non-recurring development cost to en-sure its future technological progress.

The profitability of the plants where the start-up pha-ses have been completed has improved substantially com-pared to 2002. Apart from that, licensing revenues fromthe activities in Japan for a Toyota project had a positiveimpact on the profitability.

In the future, the Group will start up a number of projectsfor both existing customers (new Mercedes A in 2004, newBMW3 in 2005) and new customers (VW Passat in 2005).Among other factors, these contracts will permit the salesof 2002 in this activity to double by 2006, which clearlyshows that the Group’s patented technology is today thebenchmark in the market.

To solve the problems of the past once and for all, anew management structure was chosen, which will concen-trate mainly on the control of all the operational and in-dustrial risks.

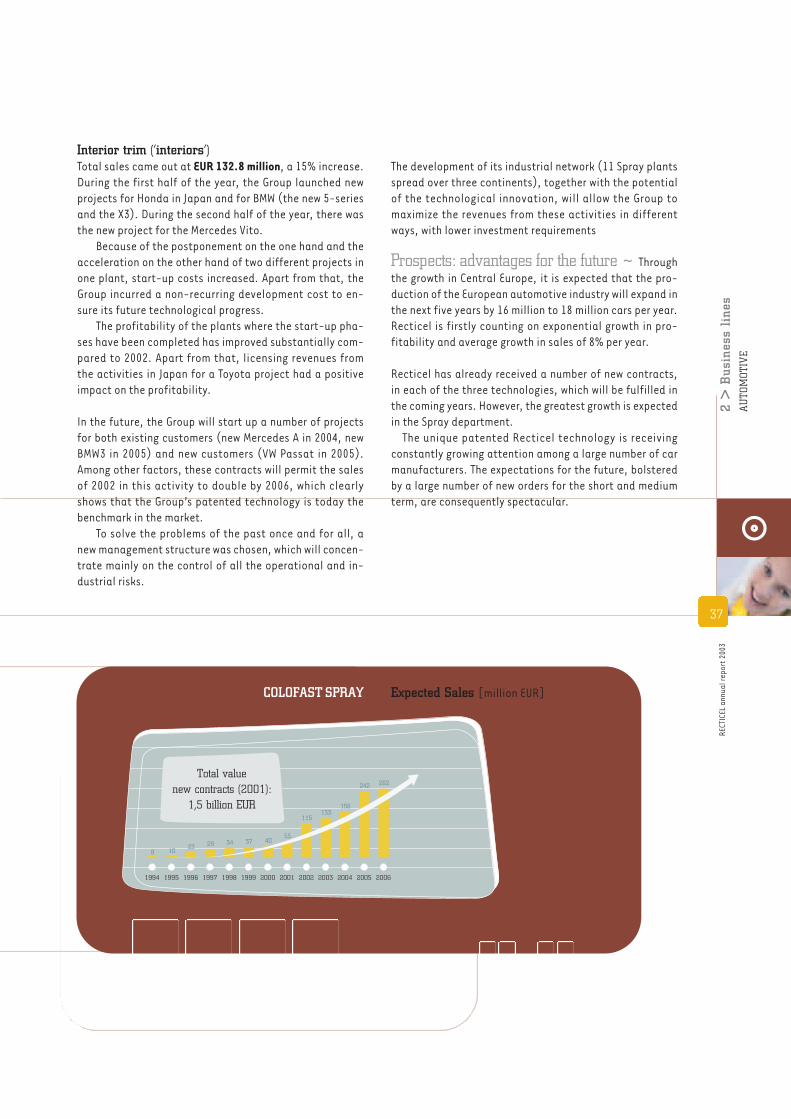

The development of its industrial network (11 Spray plantsspread over three continents), together with the potentialof the technological innovation, will allow the Group tomaximize the revenues from these activities in differentways, with lower investment requirements

Prospects: advantages for the future ~ Throughthe growth in Central Europe, it is expected that the pro-duction of the European automotive industry will expand inthe next five years by 16 million to 18 million cars per year.Recticel is firstly counting on exponential growth in pro-fitability and average growth in sales of 8% per year.

Recticel has already received a number of new contracts,in each of the three technologies, which will be fulfilled inthe coming years. However, the greatest growth is expectedin the Spray department.

The unique patented Recticel technology is receivingconstantly growing attention among a large number of carmanufacturers. The expectations for the future, bolsteredby a large number of new orders for the short and mediumterm, are consequently spectacular.

8

1994

10

1995

23

1996

29

1997

34

1998

37

1999

40

2000

55

2001

115

2002

133

2003

156

2004

242

2005

262

2006

COLOFAST SPRAY Expected Sales [million EUR]

Total value new contracts (2001):

1,5 billion EUR

RECT

ICEL

annu

al re

port

200

3

38

2 >

Bus

ines

s li

nes

AU

TOM

OTI

VE

The technology made a breakthrough in new parts of theworld and is applied to an increasing extent in mid-rangecars. Moreover, the technology is developing in such a waythat Recticel no longer confines itself to the production ofdashboard trim, but is focusing increasingly on supplyingthe complete interior trim, including door panels, etc.

Moreover, Recticel has started up the first commercialcontract in which the thin top layer in Colofast Spray is atthe same time provided with a soft underlay in flexiblefoam, thereby simplifying the industrial process conside-rably for dashboard manufacturers. Recticel has all theresources in-house to simplify the entire process evenfurther in the future and to increase its profitability.

At present, Recticel has new orders on its books to a totalvalue of EUR 1.5 billion.

In window encapsulation, growth is expected not onlythrough the new contracts which Recticel currently has onits books. By affixing ‘add-ons’ to the glass (electronicdevices for the fitting of aerials, heating, lights, etc.),Recticel creates extra added value which is appreciated bya number of manufacturers and which has already led toconcrete contracts.

Competitive situation ~

Moulded seats In just a few years, Recticel has increased its activities inthis business segment more than tenfold. The Group’s com-petitive strength is due primarily to its research and de-velopment capabilities, but also to its geographical spread.The cooperation of Woodbridge will strengthen this posi-tion even further.

Window EncapsulationA number of technologies and raw materials can be used toensure a watertight seal for car windows. Recticel, as ma-nufacturer of PU-RIM is world leader not only in window en-capsulation itself, but also in the supply of ready-to-usecompounds to companies in both the United States ofAmerica and Europe. The most important factor in this suc-cess is Colofast technology, a product of aliphatic originwith long-term colour stability characteristics.

Cockpit and interior trimThrough its development of Colofast Spray technology,Recticel has made polyurethane into the ideal response tothe demand of the automotive industry for attractivealternatives for the traditional materials. The Spray tech-nology and the success it is experiencing among manu-facturers offer the Recticel Group enormous competitiveadvantages, which are well protected by a number of pa-tents.

> Current contracts in the automotive sector, per activity

Moulded foam Window encapsulation Interior trim

BMW 3-series 3-series • 5-series • 7-series •6-series • X-3 • X-5 • Z-4

Mercedes C-class • SLK • Smart four two E-class C-class • E-class • Vanio • SLKSmart roadster • Evo bus C-class convertible & coupe • Vito

Lancia Arm rests various models LibraFord Fiesta • Focus • Mondeo • Street KaVolvo Volvo 60 / 70 /80 /90 S70Opel Astra • Zafira • Vectra • Agila Astra • Corsa • Epsilon • Speedster Astra • Vectra

SigmaGM Park AvenueRenault Megane • Scenic • EspaceVolkswagen Golf • Passat • Transporter Passat • Bora • Touran • Seat ToledoAudi Audi A6 • Audi TT convertible & coupe Audi A6 avantSkoda Fabia • Octavia • Felicia Fabia • Octavia OctaviaMitsubishi PajeroNissan Prima StarPSA Citroën C2 / C3 • Peugeot 206 Peugeot 307 • Peugeot 407Toyota Yaris Land CruiserHonda Inspire

> Window Encapsulation.High-tech application of Colofast.

Informationto sharehoulders

3

40 Share information43 Switch to IAS/IFRS44 Board, management and auditors45 Corporate Governance

Adding more value to life

1 > The Recticel Group 2 > Business lines 3 > Information to shareholders 4 > Financial section

RECT

ICEL

annu

al re

port

200

3

40

3 >

Inf

orm

atio

n to

sha

reho

ulde

rsSh

are

info

rmat

ion

Number of shares ~ The number of Recticel sharesin issue as at 31 December 2003 came to 28,333,010, thesame number as the previous year. The shares are quotedon Euronext (Brussels) and are distributed as follows:

The shares are either bearer (in denominations of 1, 10, 100or 1,000 shares), or registered.

Type Number % Market segment Code ISIN number

Ordinary: 27,900,695 98.47 Continuous market REC BE0003656676VVPR: 432,315 1.53 Spot market RECV BE0005121778

Total: 28,333,010 100.00

Reuters code: RECTt.BRBloomberg code: REC BB

>

Shareholder Ordinary shares1 VVPR shares1 Total1

Rec-Hold2 11,742,148 175,733 42.06%Mercator Verzekeringen 5,497,710 79,043 19.68%Rec-Man 1,354,783 0 4.78%Public 9,306,054 177,539 33.47%Total 27,900,695 432,315 100.00%

(1) Since each share confers one voting right, the percentages also tally with the voting control.(2) For new situation as from 7 May 2004 see page 48 (Relations with the reference shareholders)

Distribution among shareholders (by category at 31 December 2003)

Rec-Hold and Rec-Man ~ Rec-Hold, Recticel’sreference shareholder, is the holding company set up inJuly 1998 in the context of the takeover of the stake inRecticel held by Société Générale de Belgique. Followingthe reorganization of 2003, the investors of Rec-Hold areLessius, Compagnie du Bois Sauvage, VEAN NV (the invest-ment partnership of Luc Vansteenkiste (CEO)), Sinvest NVand Lennart NV.

Rec-Man is the ad hoc company set up by 40 owner-mana-gers of Recticel in 1998 after the takeover by Rec-Hold ofthe Société Générale’s shares.

(Also see additional information on page 48: “Relations withthe reference shareholders’)

Trend in the share ~ Between 31 December 2002and 31 December 2003, the ordinary Recticel share fellfrom EUR 9.20 to EUR 7.20, down 21.7%. The share reacheda high of EUR 9.40 on 16 January 2003 and a low of EUR 6.90on 11 December 2003.

The months in which the greatest volumes were tradedwere September (165,819 shares), June (156,943 shares),August (156,746 shares), December (134,978 shares) andOctober (127,585 shares). The mean monthly volume tra-ded during 2003 came to 92,977 shares. The mean daily vo-lume traded came to 4,481 shares. The VVPR share, which isfar less liquid, fell during the same period from EUR 9.20 toEUR 7.61, down 17.3%. The VVPR share reached a high ofEUR 9.70 on 13 January 2003. Its low of EUR 7.61 was recor-ded on 24 December 2003.

On 31 December 2003, the market capitalization ofRecticel came to EUR 204.2 million, as opposed to EUR260.7 million one year previously.

Share information

RECT

ICEL

annu

al re

port

200

33