Embed Size (px)

Citation preview

MATTHEW KLEGER AND TONY WU

Realizable and Realized Pay:

A new world order

APRIL 29, 2013

2© 2013 Hay Group. All Rights Reserved

Agenda

Introduction: Why is this important?

Optimizing disclosure: What are the considerations?

What’s on the horizon: What to expect in 2013

Q&A

1

2

3

4

01Introduction

Presenters

Matthew Kleger, CPA, CECP

Hay Group, Philadelphia

Senior Consultant, Executive Compensation

Office: 215.861.2341

Email: [email protected]

and

Tony Wu

Hay Group, Metro New York

Consultant, Executive Compensation

Office: 201.557.8431

Email: [email protected]

5© 2013 Hay Group. All Rights Reserved

About Hay Group

85Offices in 48

countries

2600Employees

worldwide

9000International clients

Hay Group consults with

9,000 clients worldwide in a

wide variety of areas,

including:

Organizational

effectiveness

Managerial and

executive assessment

Compensation

and benefits

Performance

management

Executive remuneration

and corporate governance

Employee and customer

attitude research

WE HELP ORGANIZATIONS WORK

6© 2013 Hay Group. All Rights Reserved

Introduction

Driven by the advent of “Say on Pay”, corporate issuers, investors (shareholders) and

proxy advisory firms are trying to answer the following key questions:

WHY ARE WE TALKING ABOUT REALIZABLE / REALIZED PAY DISCLOSURES TODAY?

PAY-FOR-

PERFORMANCE

LINKAGE?

Support compensation philosophy?

What is pay?

Support business strategy?

Shareholder

communication?

Does the pay program and design support the

philosophy and pay levels / mix?

Does the pay program align / support the

business strategy?

How do we disclose in

the proxy statement?

How do we define pay if

not SCT?

7© 2013 Hay Group. All Rights Reserved

Introduction

Focus on pay-for-performance becoming more acute

Companies are starting to change the way they speak to their shareholders about it

Realizable / realized pay is an alternative to the SEC disclosure rules

Counterpoint to ISS’ pay-for-performance methodology

A realizable / realized pay analysis is a “snapshot” of estimated actual / potential pay

delivery over a select time horizon (not accounted for in the SCT)

Attempts to measure the value of the largest pay element over the selected time

horizon

WHY USE REALIZABLE / REALIZED PAY DISCLOSURES?

So what’s the problem?...misalignment between performance period

(TSR) and the amount of compensation which will actually be delivered at

a future point in time!

8© 2013 Hay Group. All Rights Reserved

Introduction

WHO WILL UTILIZE REALIZABLE / REALIZED PAY DISCLOSURES?

Utilization of

realizable /

realized pay?

Shareholders

Proxy Advisory Firms

(ISS, Glass Lewis, etc.)

9© 2013 Hay Group. All Rights Reserved

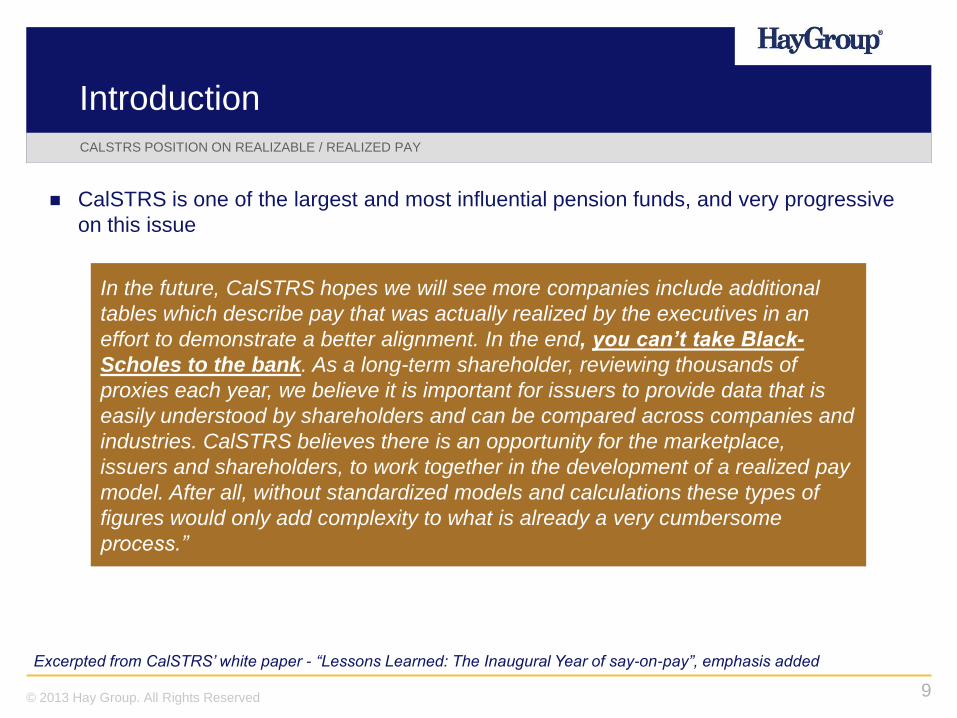

Introduction

CalSTRS is one of the largest and most influential pension funds, and very progressive

on this issue

CALSTRS POSITION ON REALIZABLE / REALIZED PAY

In the future, CalSTRS hopes we will see more companies include additional

tables which describe pay that was actually realized by the executives in an

effort to demonstrate a better alignment. In the end, you can’t take Black-

Scholes to the bank. As a long-term shareholder, reviewing thousands of

proxies each year, we believe it is important for issuers to provide data that is

easily understood by shareholders and can be compared across companies and

industries. CalSTRS believes there is an opportunity for the marketplace,

issuers and shareholders, to work together in the development of a realized pay

model. After all, without standardized models and calculations these types of

figures would only add complexity to what is already a very cumbersome

process.”

Excerpted from CalSTRS’ white paper - “Lessons Learned: The Inaugural Year of say-on-pay”, emphasis added

10© 2013 Hay Group. All Rights Reserved

Introduction

According to the 2012 Hay Group / Wall Street Journal CEO Compensation Study,

almost 15% of companies provided some form of realizable / realized pay disclosure,

up from almost none in 2010

Some of these companies include:

COMPANIES CURRENTLY USING REALIZABLE/REALIZED PAY DISCLOSURES

02Optimizing disclosure

12© 2013 Hay Group. All Rights Reserved

Optimizing disclosure

Plenty of disclosure flexibility today

What tells the most effective story to

shareholders?

Guidance being delivered from all relevant

parties potentially creating more confusion and

approaches

Proxy advisors (i.e., ISS, Glass Lewis)

Compensation consultants

Internal HR

PRESENT FLEXIBILITY

Proxy Advisors

Hint of a standard may emerge at the

conclusion of the 2013 proxy season

At this time, there is no “right” answer

– the right answer for some companies

may be non-disclosure

But, for those companies brave enough to

disclose, a series of decisions await…

13© 2013 Hay Group. All Rights Reserved

Optimizing disclosure

The definition of “pay” continues to be a widely debated topic

SCT values was considered the most widely recognized and accepted definition of “pay”

– and it still is, but…purely theoretical in nature and not ideal for pay-for-performance

MARKET GUIDANCE

Base SalaryAnnual

Incentives

Grant Date Fair Value of Long-

Term Incentives

Total Direct

Compensation

A disconnect is evident in the LTI

portion – the largest and most

critical portion of pay!

Realizable / realized pay attempts to redefine and revalue the LTI piece to better

reflect and convey what is earned or could be earned based on current / actual

performance

14© 2013 Hay Group. All Rights Reserved

Optimizing disclosure

Some early guidance from the experts…

MARKET GUIDANCE CONT’D

ISS Compensation Consultants Public Companies

Cash Compensation

Base Salary Base Salary Base Salary

Annual Incentives Annual Incentives Annual Incentives

Long-Term Incentives (for awards granted during the measurement period)

Time-Vested Full-Value Awards

Current value of outstanding

awards

Time-Vested Full-Value Awards

Current value of outstanding

awards

Time-Vested Full-Value Awards

Current value of outstanding

awards

Stock Options

Gains realized on options

exercised

BS value of outstanding options

Stock Options

ITMV of outstanding options

BS value of outstanding options

Stock Options

ITMV of outstanding options

BS value of outstanding options

Gains realized on options

exercised

Performance-Based Awards

Current value of earned awards;

and

Current value of outstanding

awards at target

Performance-Based Awards

Current value of outstanding

awards at target

Performance-Based Awards

Current value of outstanding

awards at target

Current value of expected awards

earned

Current value of pro-rata

outstanding awards at target

Ge

ne

ral A

gre

em

en

tV

ary

ing

Op

inio

ns

15© 2013 Hay Group. All Rights Reserved

Optimizing disclosure

External guidance is helpful (but also causes confusion)…but before you begin to craft a

disclosure, let’s ask ourselves the following:

Does a realizable / realized pay disclosure make sense? For the company? For

shareholders?

If yes, then consider the following primary inputs:

Absolute vs. relative

Measurement period

Performance context

Comparison to SCT / GDFV

Pay elements

Additional consideration may be given to select inputs as certain challenges / pitfalls

exist based on decisions made

IS NOW THE RIGHT TIME?

16© 2013 Hay Group. All Rights Reserved

Optimizing disclosure

Additional consideration should be given to other factors that may impact the validity of

the initial pay-for-performance results

DISCLOSURE CONSIDERATIONS

Primary Inputs Overview Additional Considerations

Absolute vs. Relative Measuring realizable / realized pay

against yourself or against proxy peers

Relative disclosure may require intensive analyses

Lag in reporting of peer pay data prevents a

“current” disclosure

Measurement Period 1-, 3-, or 5-year period – a period that

reflects a “longer-term” outlook may be

appropriate

A measurement period that aligns with the

company’s business strategy may be considered

Consider alternative ending periods / dates for

TSR calculations

Performance Context Inclusion of TSR at a minimum or

performance implied by realizable /

realized pay levels relative to SCT / GDFV

Broadening the performance context may provide

a “fuller” performance picture as operational and

strategic performance may not always show up in

stock price performance

Comparison to SCT /

GDFV

Comparison of realizable / realized to

SCT / GDFV pay would be consistent with

ISS’s approach

Usually included if electing to disclose a more

“basic” disclosure

Pay Elements A more comprehensive pay disclosure or

isolation of LTI

Adjustments to LTI may be made to ensure a

balanced approach

Valuation?

Grant timing?

17© 2013 Hay Group. All Rights Reserved

Optimizing disclosure

EVOLVING DISCLOSURES – ACM

2011 Approach Highlights:

4-year absolute comparison to

GDFV

Includes TDC and LTI

Includes stock price

performance

Equity valuation based on each

fiscal year’s closing share price

Hybrid approach to valuing

performance-based equity

(earned and at target)

Realizable pay also examined

vs. EBITDA and EPS

performance

Initial realizable pay disclosure

exhibits absolute TDC and LTI

over a 4-year period

18© 2013 Hay Group. All Rights Reserved

Optimizing disclosure

EVOLVING DISCLOSURES – ACM CONT’D

In 2012, ACM transitions to an absolute 3-year look and isolates LTI

2012 Approach Highlights:

3-year absolute

comparison to GDFV

Isolation of LTI

Equity valuation based

on FYE12 closing share

price

Performance-based

equity valued at expected

payout as a percentage

of target (1st cycle) and at

target (remaining cycles)

19© 2013 Hay Group. All Rights Reserved

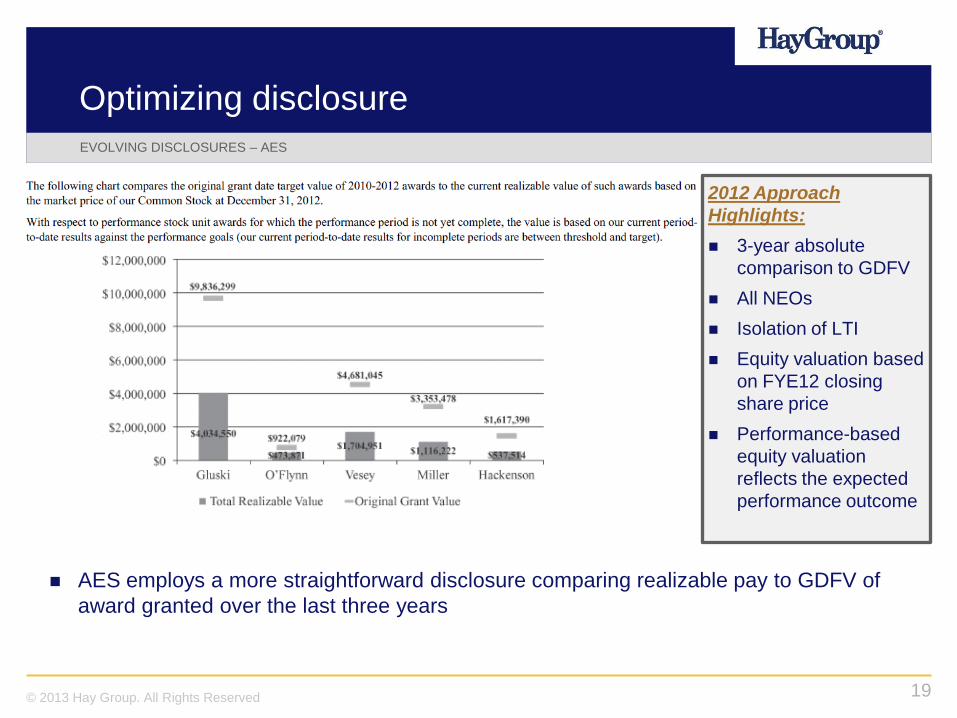

Optimizing disclosure

EVOLVING DISCLOSURES – AES

AES employs a more straightforward disclosure comparing realizable pay to GDFV of

award granted over the last three years

2012 Approach

Highlights:

3-year absolute

comparison to GDFV

All NEOs

Isolation of LTI

Equity valuation based

on FYE12 closing

share price

Performance-based

equity valuation

reflects the expected

performance outcome

20© 2013 Hay Group. All Rights Reserved

Optimizing disclosure

EVOLVING DISCLOSURES – SYMC

Symantec elects a realizable / realized hybrid as its initial disclosure

2012 Approach Highlights:

3-year absolute comparison to

GDFV

Includes all elements of TDC

Earned cash-LTIP

Equity valuation based on

FYE12 closing share price

and vesting date share price

Performance-based equity

valuation reflects the expected

performance outcome

21© 2013 Hay Group. All Rights Reserved

Optimizing disclosure

Additional examples of first-time and repeat disclosures by early filers are provided

below for reference…

EVOLVING DISCLOSURES

New Disclosures Repeat Disclosures Type Highlights

Air Products RealizableSensitivity of absolute realizable pay based on

varying TSR scenarios compared to GDFV

Archer-Daniels-

MidlandRealizable

5-year absolute realizable pay compared to

GDFV with SP performance

Deere Realizable3-year realizable pay and TSR relative to proxy

peer group. Revised valuation of PSUs in 2012

Johnson Controls Realizable3-year realizable pay and TSR relative to proxy

peer group

Pantry, Inc Realized

Transition from 1- and 3-year realized vs target

pay graphical disclosure to 1-year realized pay

vs. target tabular disclosure

Supervalu Realized 3-year absolute realized pay compared to GDFV

22© 2013 Hay Group. All Rights Reserved

Optimizing disclosure

A realizable / realized pay disclosure may not always be a great companion to the

CD&A…

Consider the quality of the message delivered to shareholders – what are we really

trying to prove? Don’t just do it because ISS is doing it

Depending on the type of disclosure, may require time-intensive calculations

Do we want to add to an already lengthy CD&A? No regulatory requirement of such

disclosure at this time

Once you start, you likely can’t stop

DISCLOSURE CHALLENGES

While a realizable / realized pay disclosure will likely become the norm

within the next two years, public companies today have more than one

opportunity to get it “right” and continue to learn from each other to set

the market standard

03What’s on the horizon?

24© 2013 Hay Group. All Rights Reserved

What’s on the horizon

We expect to see continuing trend, interest and discussion, and potential

legislation on this topic:

Continued momentum

Realizable / realized pay will gain further prominence in the Board room

Jumping on the band-wagon

Institutional shareholders and proxy advisory firms have already begun to consider

realizable / realized pay to determine SOP vote recommendations

Regulatory involvement

SEC to provide clarity on disclosures – a requirement under Dodd-Frank?

Uniformity of disclosures to emerge

This proxy season or next?

Lengthier CD&As

Realizable / realized pay disclosures will expand on an already extensive CD&A

WHAT TO EXPECT IN 2013

25© 2013 Hay Group. All Rights Reserved

What’s on the horizon

HOW SHOULD COMPANIES BE PREPARING FOR 2014?

1. Assess the need for realizable / realized pay disclosure

SOP issues?

Current or historical pay-for-performance concerns?

2. Educate the Board and compensation committee

Current market trends

Company pay program designs and potential risk exposure

3. Establish process for evaluating alternative pay-for-performance definitions

Partner with compensation consultants, counsel, and investor relations

Gather data inputs

4. Test alternative pay definitions to examine impact of varying inputs

Which approach conveys the “right” message and is defensible from a shareholder

and proxy advisor perspective

04Q&A

27© 2013 Hay Group. All Rights Reserved

Q&A

QUESTIONS

Matthew Kleger, CPA, CECP

Office: 215.861.2341

Email: [email protected]

Tony Wu

Office: 201.557.8431

Email: [email protected]