Embed Size (px)

Citation preview

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

IPO Statistics &

Readiness Discussion

ASC 606 (IFRS 15) Adoption Trends

SEC Comment Letters, SAB 74 Disclosures, Early Adopters

January 2018

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

Executive Summary

1

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

➢ Connor Group has reviewed SEC comment letters issued to date as of December 29, 2017 regarding the adoption or

implementation of ASC 606 Revenue from Contracts with Customers (or its IFRS equivalent, IFRS 15).

➢ This population of relevant SEC comment letters was determined and the filings were retrieved via searches within

CompanyIQ™¹ based on the following criteria:

• SEC Comment letters issued and closed as of December 29, 2017. Please note that SEC only publishes

comment letters that have been fully addressed and closed.

• Comment letter language includes “Topic 606”, “ASC 606” or “ASU 2014-09”.

A total of 31 companies have been issued comment letters, 4 of which are early adopters of the new revenue standard.

Those comment letters contain 42 comments pertaining to either the adoption or implementation of the standard.

➢ A summary of the findings is presented below:

a) Over half of the comments request companies to expand their disclosures related to the evaluation and

implementation status.

b) For companies that are yet to adopt the standard, no comments were noted concerning specific technical

issues in SAB 74 disclosures.

c) On the other hand, in letters to early adopters, comments consist of both inquiries about rationale in reaching

certain technical conclusions and requests to expand disclosure for specific technical areas. Those account for

35% of the total comments reviewed. Notable ones include:

❖ Disclose why cost-to-cost measure is a faithful depiction of transfer of control

❖ Disclose significant payment terms and how the timing of satisfaction of performance obligations relates

to the timing of payment and the effect on the contract asset and liability balances

❖ Whether a significant financing component exists in certain long-term arrangements

❖ Rationale for concluding point-in-time recognition for customized construction contracts

2SEC Comment Letters

¹ CompanyIQ™ is a product of (http://www.mylogiq.com/), a provider of SEC compliance and public company intelligence products. CompanyIQ™ identifies, extracts,

and collates information from relevant public sources to create an 360° company profile and access SEC disclosures and SEC comments linked with responses.

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

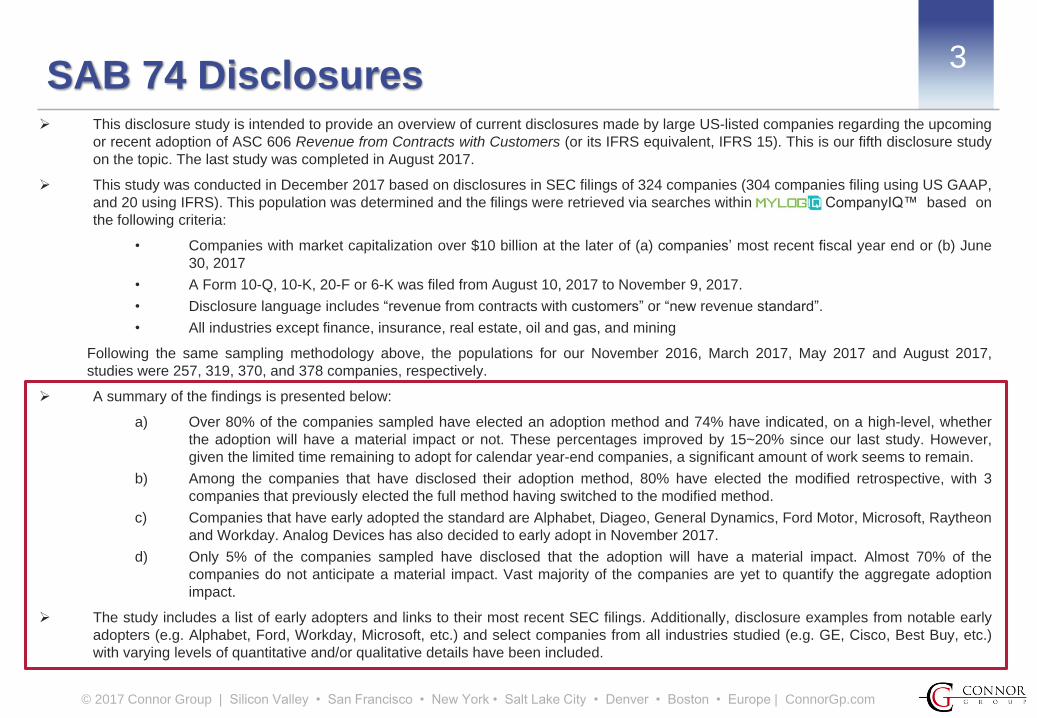

➢ This disclosure study is intended to provide an overview of current disclosures made by large US-listed companies regarding the upcoming

or recent adoption of ASC 606 Revenue from Contracts with Customers (or its IFRS equivalent, IFRS 15). This is our fifth disclosure study

on the topic. The last study was completed in August 2017.

➢ This study was conducted in December 2017 based on disclosures in SEC filings of 324 companies (304 companies filing using US GAAP,

and 20 using IFRS). This population was determined and the filings were retrieved via searches within CompanyIQ™ based on

the following criteria:

• Companies with market capitalization over $10 billion at the later of (a) companies’ most recent fiscal year end or (b) June

30, 2017

• A Form 10-Q, 10-K, 20-F or 6-K was filed from August 10, 2017 to November 9, 2017.

• Disclosure language includes “revenue from contracts with customers” or “new revenue standard”.

• All industries except finance, insurance, real estate, oil and gas, and mining

Following the same sampling methodology above, the populations for our November 2016, March 2017, May 2017 and August 2017,

studies were 257, 319, 370, and 378 companies, respectively.

➢ A summary of the findings is presented below:

a) Over 80% of the companies sampled have elected an adoption method and 74% have indicated, on a high-level, whether

the adoption will have a material impact or not. These percentages improved by 15~20% since our last study. However,

given the limited time remaining to adopt for calendar year-end companies, a significant amount of work seems to remain.

b) Among the companies that have disclosed their adoption method, 80% have elected the modified retrospective, with 3

companies that previously elected the full method having switched to the modified method.

c) Companies that have early adopted the standard are Alphabet, Diageo, General Dynamics, Ford Motor, Microsoft, Raytheon

and Workday. Analog Devices has also decided to early adopt in November 2017.

d) Only 5% of the companies sampled have disclosed that the adoption will have a material impact. Almost 70% of the

companies do not anticipate a material impact. Vast majority of the companies are yet to quantify the aggregate adoption

impact.

➢ The study includes a list of early adopters and links to their most recent SEC filings. Additionally, disclosure examples from notable early

adopters (e.g. Alphabet, Ford, Workday, Microsoft, etc.) and select companies from all industries studied (e.g. GE, Cisco, Best Buy, etc.)

with varying levels of quantitative and/or qualitative details have been included.

3SAB 74 Disclosures

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

List of Early Adopters4

❖ Below list includes companies that have adopted ASC 606 (IFRS 15) as of their most recent SEC filing date.

❖ This list is identified through key word search within SEC.gov and CompanyIQ™ and therefore might

not represent the complete population of early adopters.

# Company Name Adoption Date Adoption Method IndustryLink to most

recent filing

1 Alphabet, Inc. March 30, 2017 Modified Technology 10-Q

2 AquaBounty Technologies, Inc March 15, 2017 No historical revenue Life science S-1

3 Aradigm Corporation April 1, 2016 Modified Life science 10-Q

4 Bsquare Corporation March 7, 2016 Modified Technology 10-Q

5Catabasis

Pharmaceuticals, Inc.January 1, 2017 No historical revenue Life science 10-Q

6 CBOE Holdings, Inc. January 1, 2017 Full Finance, Insurance & Real Estate 10-Q

7 Commvault Systems, Inc April 1, 2017 Full Technology 10-Q

8 Ecoark Holdings, Inc April 1, 2017 Modified Consumer products 10-Q

9 Ener-Core, Inc January 1, 2017 No historical revenueIndustrial products, chemicals, and

manufacturing10-Q

10 EnerNoc, Inc. January 1, 2017 Modified Technology 10-Q

11 Extreme Networks, Inc July 1, 2017 Full Technology 10-Q

12 First Solar, Inc. January 1, 2017 Full Technology 10-Q

13 Ford Motor Company January 1, 2017 ModifiedIndustrial products, chemicals, and

manufacturing10-Q

14 General Dynamics Corporation January 1, 2017 FullIndustrial products, chemicals, and

manufacturing10-Q

15 Lipocine, Inc. January 1, 2017 No historical revenue Life science 10-Q

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

List of Early Adopters (Cont’d)5

# Company Name Adoption Date Adoption Method IndustryLink to most

recent filing

16 Microsoft Corporation July 1, 2017 Full Technology 10-Q

17 Mirati Therapeutics, Inc. January 1, 2017 No historical revenue Life science 10-Q

18 Nutanix, Inc. August 1, 2017 Full Technology 10-Q

19 Pluristem Therapeutics, Inc. July 1, 2017 Modified Life science 10-Q

20 Power Integrations, Inc. January 1, 2017 Full Technology 10-Q

21 Pure Cycle Corporation September 1, 2017 Modified Transportation and utilities 10-Q

22 R1 RCM Inc. January 1, 2017 ModifiedWholesale/retailer trade,

services and others10-Q

23 Radius Health, Inc. April 1, 2017 No historical revenue Life science 10-Q

24 Raytheon Company January 1, 2017 FullIndustrial products, chemicals,

and manufacturing10-Q

25 Sage Therapeutics, Inc. January 1, 2017 No historical revenue Life science 10-Q

26 Solid Biosciences, Llc January 1, 2017 No historical revenue Life science S-1

27 Strongbridge Bipharma April 1, 2017 No historical revenue Life science 6-K

28 Tesaro, Inc. January 1, 2017 Full Life science 10-Q

29Ultragenyx Pharmaceutical,

Inc.January 1, 2017 Full Life science 10-Q

30 UnitedHealth Group January 1, 2017 ModifiedFinance, Insurance & Real

Estate10-Q

31Vanguard Natural Resources,

IncAugust 1, 2017 Modified

Oil, mining and other energy

related10-Q

32 Workday, Inc. February 1, 2017 Full Technology 10-Q

33 Zafgen, Inc January 1, 2017 No historical revenue Life science 10-Q

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

SEC Comment Letters

ASC 606 (IFRS 15) Adoption and

Implementation

6

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

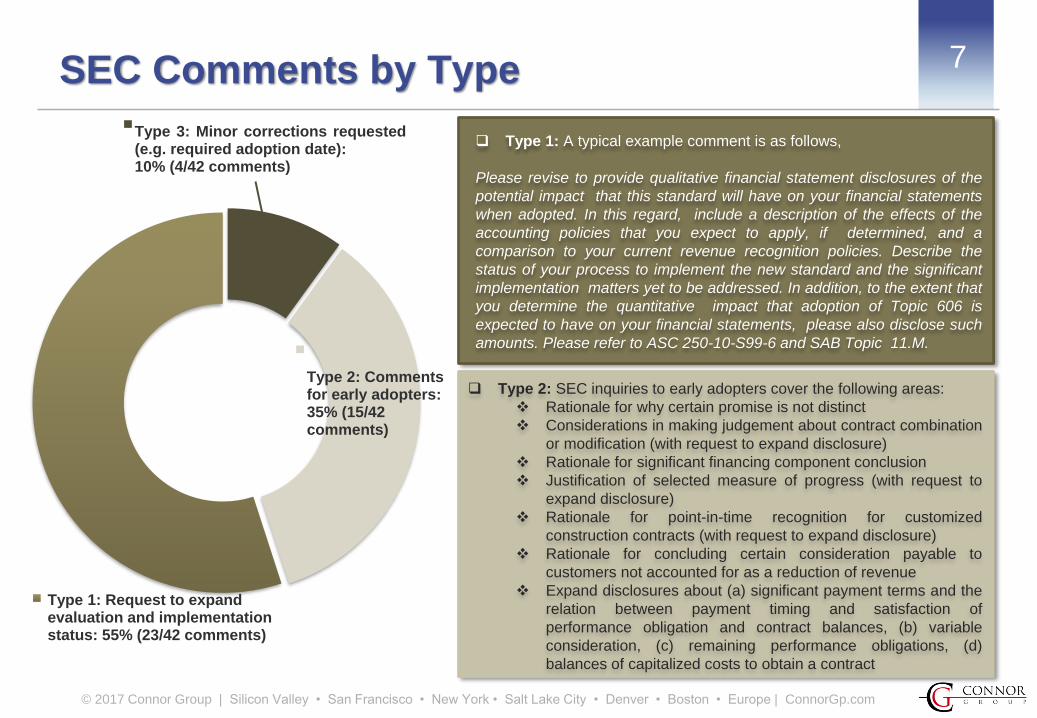

Type 2: SEC inquiries to early adopters cover the following areas:

❖ Rationale for why certain promise is not distinct

❖ Considerations in making judgement about contract combination

or modification (with request to expand disclosure)

❖ Rationale for significant financing component conclusion

❖ Justification of selected measure of progress (with request to

expand disclosure)

❖ Rationale for point-in-time recognition for customized

construction contracts (with request to expand disclosure)

❖ Rationale for concluding certain consideration payable to

customers not accounted for as a reduction of revenue

❖ Expand disclosures about (a) significant payment terms and the

relation between payment timing and satisfaction of

performance obligation and contract balances, (b) variable

consideration, (c) remaining performance obligations, (d)

balances of capitalized costs to obtain a contract

7SEC Comments by Type

Type 3: Minor corrections requested(e.g. required adoption date):10% (4/42 comments)

Type 2: Comments for early adopters: 35% (15/42 comments)

Type 1: Request to expand evaluation and implementation status: 55% (23/42 comments)

Type 1: A typical example comment is as follows,

Please revise to provide qualitative financial statement disclosures of the

potential impact that this standard will have on your financial statements

when adopted. In this regard, include a description of the effects of the

accounting policies that you expect to apply, if determined, and a

comparison to your current revenue recognition policies. Describe the

status of your process to implement the new standard and the significant

implementation matters yet to be addressed. In addition, to the extent that

you determine the quantitative impact that adoption of Topic 606 is

expected to have on your financial statements, please also disclose such

amounts. Please refer to ASC 250-10-S99-6 and SAB Topic 11.M.

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

Comment Letter Examples8

Company Name Response Date Link to response letter and Question #

1. First Data Corp April 17, 2017 Question 5

2. NASDAQ, Inc April 13, 2017 Question 1

❖ Example of Type 1 - Request to expand evaluation and implementation status

❖ Other companies received similar Type 1 comments:

✓ Mastec, Inc.

✓ Legget & Platt, Inc.

✓ Monster Beverage Corp

✓ IAC/InterActive Corp

✓ ONEOK Partners LP

✓ Vermillion, Inc.

✓ ONEOK, Inc.

✓ MKS Instruments, Inc.

✓ Guaranty Bancshares, Inc.

✓ United Therapeutics Corp

✓ Community Health Systems, Inc.

✓ Integer Holdings Corporation

✓ Ctrip.com International, Ltd

✓ Roku, Inc.

✓ Snap, Inc.

✓ Black Knight, Inc.

✓ SenesTech, Inc.

✓ Altice USA, Inc.

✓ RYB Education, Inc.

✓ AGM Group Holdings, Inc.

✓ Co-Diagnostics, Inc.

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

Comment Letter Examples (Cont’d)9

Company Name Response Date Link to response letter and Question #

1. General Dynamics CorpSeptember 7, 2017 Question 1 - 6

October 19, 2017 Question 1

2. First Solar, Inc. August 17, 2017 Question 7 - 10

3. Workday, Inc. August 8, 2017 Question 1 - 2

4. CBOE Global Markets, Inc. September 1, 2017 Question 1 - 2

❖ Full list of Type 2 – Comments to early adopters

Company Name Response Date Link to response letter and Question #

1. BioLargo, Inc. March 30, 2017 Question 17

2. Veritone, Inc. March 15, 2017 Question 3

3. BeautyKind Holdings, Inc. April 1, 2016 Question 12

4. QMC Systems, Inc. March 7, 2016 Question 4*

❖ Full list of Type 3 – Minor corrections requested

❖ * Response letter to this SEC letter is not available on SEC.gov as of the date of this study.

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

SAB 74 Disclosure Trend

ASC 606 (IFRS 15)

Methods, Dates, and Anticipated Impact

10

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

11Sampled Companies by Industry

90

5852

3631 30

27

0

20

40

60

80

100

a b c d e f g

16%

11%10%

9%8%

28%

18%

From left to right:

a. Transportation and utilities

b. Technology

c. Industrial products, chemicals and manufacturing

d. Life sciences (biotechnology, pharmaceuticals, medical devices)

e. Wholesale, retail, services and other

f. Consumer products

g. Entertainment, media and communications

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

12Anticipated Adoption Method

4% 5%

91%

11%

29%

60%

14%

34%

52%

17%

49%

34%

18%

65%

17%

0%

20%

40%

60%

80%

100%

Full Retrospective Modified Retrospective Still Assessing

Nov'16 Study Mar'17 Study May'17 Study Aug'17 Study Dec'17 Study (Current)

▪ 59/324 companies

▪ Notable companies:

- Raytheon (adopted)

- General Dynamics (adopted)

- Workday (adopted)

- Microsoft (adopted)

- Apple

- GE

- Oracle

- Boeing

- American Airline

- Intuitive Surgical

▪ 209/324 companies

▪ Notable companies:

- Alphabet (adopted)

- Ford (adopted)

- Nike

- Amazon

- AT&T

- Priceline

- IBM

- Dow Chemical

- AbbVie

Full Retrospective = recast all comparative periods presented in the post-adoption financial statements; Modified Retrospective = cumulative-effect

adjustment to retained earnings in the period of adoption for prior periods’ effects

The percentage of companies that have determined an adoption method has increased by 17% since our last study. Approximately 80% of the companies

that disclosed an adoption method have elected to use the modified retrospective method.

Three companies (Netflix, International Paper, and Sherwin-Williams) have switched the adoption method previously elected from full retrospective to

modified retrospective over the past two quarters. 1 company (Yum! Brands) has switched from full retrospective to still assessing. Some companies who

have elected full retrospective have continued to indicate that their ability to apply full retrospective method depends on system readiness and the completion

of the analysis of information necessary to restate prior periods.

There are 16 companies that expect a material adoption impact and also have elected an adoption method. Over 60% of them (10 companies) have chosen

the full retrospective. On the other hand, there are 199 companies that expect that the adoption will not be material and also have determined an adoption

method. Over 80% of them (161 companies) have chosen the modified retrospective.

For early adopters, 5 out of 7 companies elected the full retrospective method.

▪ 56/324

companies

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

13Anticipated Adoption Date

2%

35%

63%

2%

85%

13%

2%

93%

5%2%

96%

2%2%

97%

1%0%

20%

40%

60%

80%

100%

120%

Early Adoption Standard Adoption Not Specified

Nov'16 Study Mar'17 Study May'17 Study Aug'17 Study Dec '17 Study (Current)

▪ 7/324 companies:

- Alphabet (adopted)

- General Dynamics (adopted)

- Ford (adopted)

- Raytheon (adopted)

- Workday (adopted)

- Microsoft (adopted)

- Analog Devices (early adopt in Nov. 17)

▪ 315/324 companies

7 companies that issued SEC filings during our current study date range have elected to early adopt the new standard. Among the 6

companies that have adopted the standard, 5 of them disclosed an immaterial impact.

The “not specified” group has decreased by 1% since our last study. This is an expected trend as currently the early adoption is essentially

only available for a small subset of companies that have an off-calendar year-end date.

Among the 315 companies within the “standard adoption” group,

▪ 66% (209 companies, comprising of 68% of US GAAP companies sampled and 10% of IFRS companies sampled) have disclosed both

the high-level adoption impact and an adoption method. This percentage has increased by 15~20% per quarter for the past 2 quarters.

▪ 9% (28 companies, comprising of 6% of US GAAP companies sampled and 50% of IFRS companies sampled) have not determined the

high-level adoption impact nor an adoption method. Such percentage has decreased by approximately 10~15% per quarter for the past 2

quarters.

▪ 2/324

companies

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

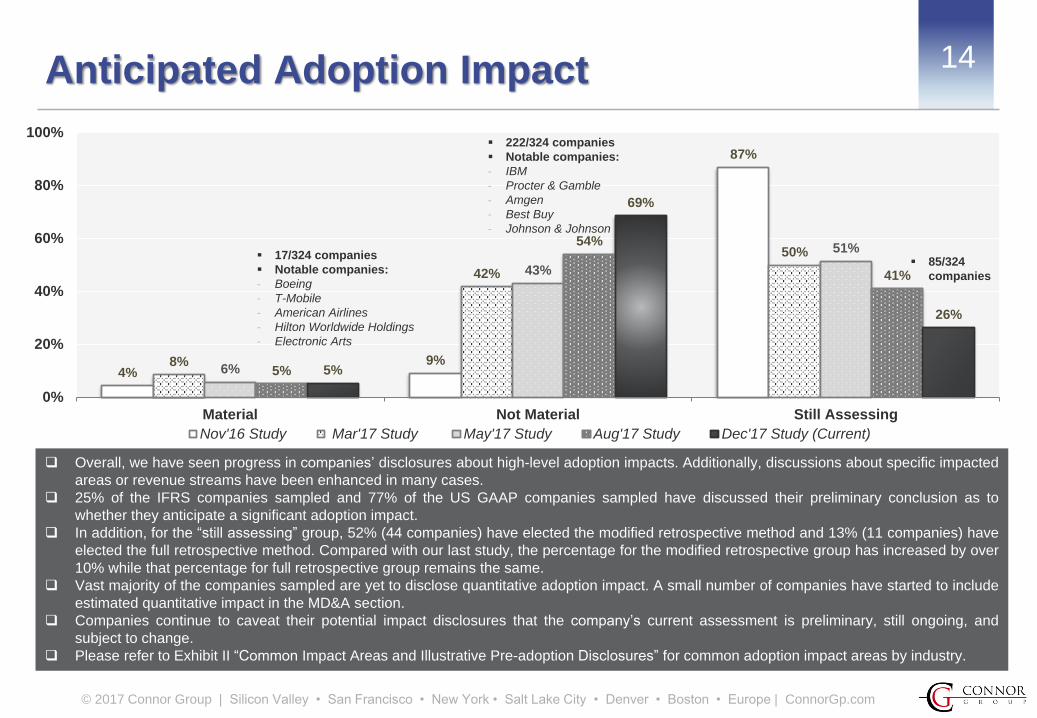

14Anticipated Adoption Impact

4%9%

87%

8%

42%

50%

6%

43%

51%

5%

54%

41%

5%

69%

26%

0%

20%

40%

60%

80%

100%

Material Not Material Still Assessing

Nov'16 Study Mar'17 Study May'17 Study Aug'17 Study Dec'17 Study (Current)

▪ 17/324 companies

▪ Notable companies:

- Boeing

- T-Mobile

- American Airlines

- Hilton Worldwide Holdings

- Electronic Arts

▪ 222/324 companies

▪ Notable companies:

- IBM

- Procter & Gamble

- Amgen

- Best Buy

- Johnson & Johnson

Overall, we have seen progress in companies’ disclosures about high-level adoption impacts. Additionally, discussions about specific impacted

areas or revenue streams have been enhanced in many cases.

25% of the IFRS companies sampled and 77% of the US GAAP companies sampled have discussed their preliminary conclusion as to

whether they anticipate a significant adoption impact.

In addition, for the “still assessing” group, 52% (44 companies) have elected the modified retrospective method and 13% (11 companies) have

elected the full retrospective method. Compared with our last study, the percentage for the modified retrospective group has increased by over

10% while that percentage for full retrospective group remains the same.

Vast majority of the companies sampled are yet to disclose quantitative adoption impact. A small number of companies have started to include

estimated quantitative impact in the MD&A section.

Companies continue to caveat their potential impact disclosures that the company’s current assessment is preliminary, still ongoing, and

subject to change.

Please refer to Exhibit II “Common Impact Areas and Illustrative Pre-adoption Disclosures” for common adoption impact areas by industry.

▪ 85/324

companies

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

Top 15 Technology Companies15

Adoption Impact

Ad

op

tio

n M

eth

od

Full

Retrospective Salesforce

Apple

Oracle Microsoft (Adopted)

Modified

Retrospective

Intel

Priceline

Alphabet (Adopted)

IBM

Accenture

Cisco Systems

Texas Instruments

Netflix

Not

Specified

NTT DoCoMo

Taiwan

Semiconductor

Manufacturing Co

Not

SpecifiedImmaterial Material

▪ Top 15 technology companies were selected based on market capitalization at the later of (a) companies’ most recent fiscal year

end or (b) June 30, 2017 (Source: MyLogIQ)

▪ 3 more companies have moved into the dot-shaded zone (right top corner) since our last study.

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

Top 15 Life Sciences Companies16

Adoption Impact

Ad

op

tio

n M

eth

od

Full

Retrospective

Modified

Retrospective

Abbott Laboratories

AbbVie

Allergan

Amgen

Celgene

Eli Lily

Gilead Sciences

Johnson & Johnson

3M

Merck

Pfizer

Medtronic

Biogen

Bristol Myers

Squibb

Not

Specified GlaxoSmithKline

Not

SpecifiedImmaterial Material

▪ Top 15 life science companies were selected based on market capitalization at the later of (a) companies’ most recent fiscal year

end or (b) June 30, 2017 (Source: MyLogIQ)

▪ 3 more companies have moved into the dot-shaded zone (top right corner) since our last study.

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

Summary of Exhibits17

Description Link

❖ Post-adoption Disclosures Examples

1. Alphabet (modified retrospective, third Form 10-Q filed after adoption) Exhibit I - 1

2. Ford (modified retrospective, third Form 10-Q filed after adoption) Exhibit I – 2

3. General Dynamics (full retrospective, third Form 10-Q filed after adoption) Exhibit I – 3

4. Workday (full retrospective, second Form 10-Q filed after adoption) Exhibit I - 4

5. Microsoft (full retrospective, first Form 10-Q filed after adoption) Exhibit I - 5

❖ Common Impact Areas and Illustrative Pre-adoption Disclosures

AA. All industries Exhibit II

A. Technology Exhibit II - A

B. Industrial products, chemicals, and manufacturing Exhibit II – B

C. Transportation and utilities Exhibit II – C

D. Life sciences (biotechnology, pharmaceuticals, medical devices) Exhibit II – D

E. Entertainment, media and communications Exhibit II – E

F. Wholesale, retail, services and other Exhibit II – F

G. Consumer products Exhibit II - G

Disclosure Example Color Legend: Adoption date or method; Adoption impact; Other Topic 606 related disclosures

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

18

Exhibit I – Post-adoption Disclosure Examples

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

19Exhibit I – Post-adoption Disclosure

Adoption of ASC Topic 606, "Revenue from Contracts with Customers"

On January 1, 2017, we adopted Topic 606 using the modified retrospective method applied to those contracts which were

not completed as of January 1, 2017. Results for reporting periods beginning after January 1, 2017 are presented under Topic

606, while prior period amounts are not adjusted and continue to be reported in accordance with our historic accounting under

Topic 605.

We recorded a net reduction to opening retained earnings of $15 million as of January 1, 2017 due to the cumulative

impact of adopting Topic 606, with the impact primarily related to our non-advertising revenues. The impact to revenues

as a result of applying Topic 606 was an increase of $10 million and $32 million for the three and nine months

ended September 30, 2017, respectively.

Revenue Recognition

Revenues are recognized when control of the promised goods or services is transferred to our customers, in an amount that

reflects the consideration we expect to be entitled to in exchange for those goods or services.

The following table presents our revenues disaggregated by revenue source (in millions, unaudited). Sales and usage-based

taxes are excluded from revenues:

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

20Exhibit I – Post-adoption Disclosure (Cont’d)

(1) As noted above, prior period amounts have not been adjusted under the modified retrospective method.

(2) Revenues include hedging gains (losses) of $105 million and $(191) million for the three months ended September 30, 2016 and 2017, respectively, and $352 million and

$29 million for the nine months ended September 30, 2016 and 2017, respectively, which do not represent revenues recognized from contracts with customers.

The following table presents our revenues disaggregated by geography, based on the billing addresses of our customers (in millions,

unaudited):

(1) Regions represent Europe, the Middle East, and Africa (EMEA); Asia-Pacific (APAC); and Canada and Latin America (Other Americas).

(2) Revenues include hedging gains (losses) for the three and nine months ended September 30, 2016 and 2017.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

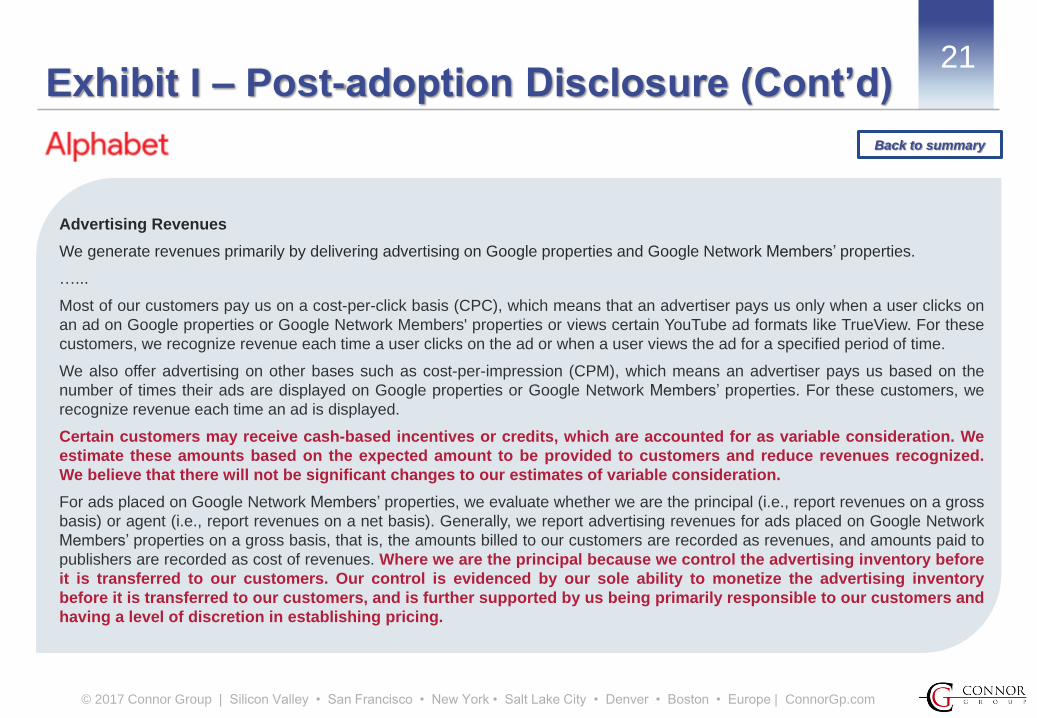

21Exhibit I – Post-adoption Disclosure (Cont’d)

Advertising Revenues

We generate revenues primarily by delivering advertising on Google properties and Google Network Members’ properties.

…...

Most of our customers pay us on a cost-per-click basis (CPC), which means that an advertiser pays us only when a user clicks on

an ad on Google properties or Google Network Members' properties or views certain YouTube ad formats like TrueView. For these

customers, we recognize revenue each time a user clicks on the ad or when a user views the ad for a specified period of time.

We also offer advertising on other bases such as cost-per-impression (CPM), which means an advertiser pays us based on the

number of times their ads are displayed on Google properties or Google Network Members’ properties. For these customers, we

recognize revenue each time an ad is displayed.

Certain customers may receive cash-based incentives or credits, which are accounted for as variable consideration. We

estimate these amounts based on the expected amount to be provided to customers and reduce revenues recognized.

We believe that there will not be significant changes to our estimates of variable consideration.

For ads placed on Google Network Members’ properties, we evaluate whether we are the principal (i.e., report revenues on a gross

basis) or agent (i.e., report revenues on a net basis). Generally, we report advertising revenues for ads placed on Google Network

Members’ properties on a gross basis, that is, the amounts billed to our customers are recorded as revenues, and amounts paid to

publishers are recorded as cost of revenues. Where we are the principal because we control the advertising inventory before

it is transferred to our customers. Our control is evidenced by our sole ability to monetize the advertising inventory

before it is transferred to our customers, and is further supported by us being primarily responsible to our customers and

having a level of discretion in establishing pricing.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

22Exhibit I – Post-adoption Disclosure (Cont’d)

Other Revenues

……

As it relates to Google other revenues, the most significant judgment is determining whether we are the principal or agent for app

sales and in-app purchases through the Google Play store. We report revenues from these transactions on a net basis

because our performance obligation is to facilitate a transaction between app developers and end users, for which we

earn a commission. Consequently, the portion of the gross amount billed to end users that is remitted to app developers is not

reflected as revenues.

Arrangements with Multiple Performance Obligations

Our contracts with customers may include multiple performance obligations. For such arrangements, we allocate revenue to each

performance obligation based on its relative standalone selling price. We generally determine standalone selling prices based

on the prices charged to customers or using expected cost plus margin.

Deferred Revenues

We record deferred revenues when cash payments are received or due in advance of our performance, including amounts which

are refundable. The increase in the deferred revenue balance for the nine months ended September 30, 2017 is primarily

driven by cash payments received or due in advance of satisfying our performance obligations, offset by $779 million of

revenues recognized that were included in the deferred revenue balance as of December 31, 2016.

Our payment terms vary by the type and location of our customer and the products or services offered. The term between invoicing

and when payment is due is not significant. For certain products or services and customer types, we require payment before the

products or services are delivered to the customer.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

23Exhibit I – Post-adoption Disclosure (Cont’d)

Practical Expedients and Exemptions

We generally expense sales commissions when incurred because the amortization period would have been one year or

less. These costs are recorded within sales and marketing expenses.

We do not disclose the value of unsatisfied performance obligations for (i) contracts with an original expected length of

one year or less and (ii) contracts for which we recognize revenue at the amount to which we have the right to invoice for

services performed.

Back to summary

[Emphasis added]

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

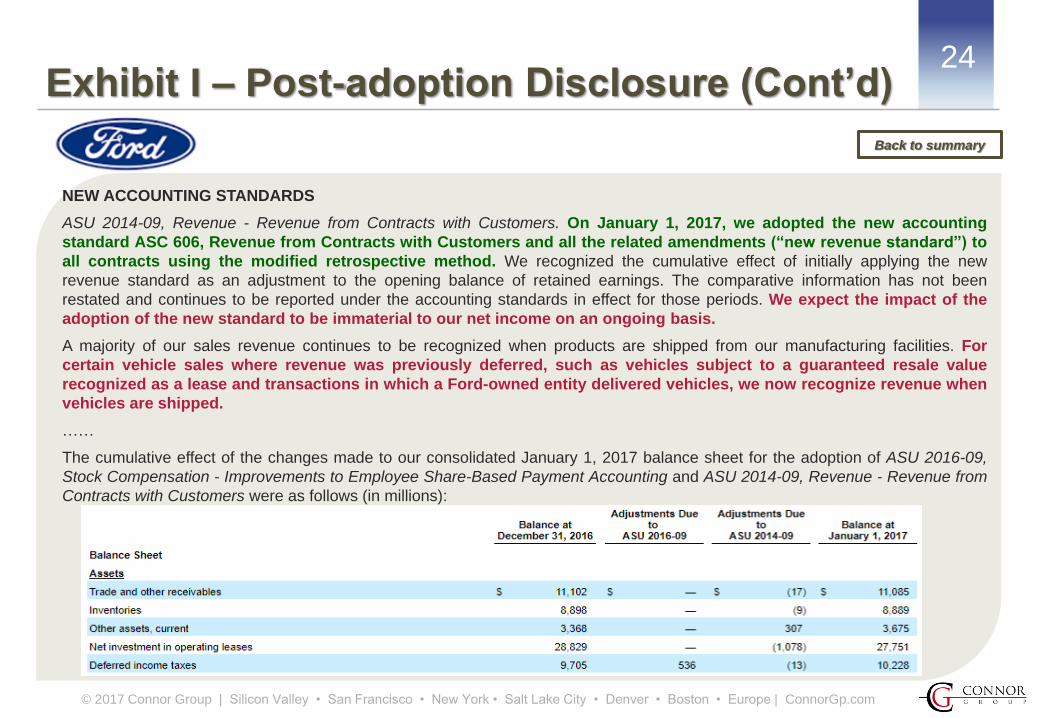

24Exhibit I – Post-adoption Disclosure (Cont’d)

NEW ACCOUNTING STANDARDS

ASU 2014-09, Revenue - Revenue from Contracts with Customers. On January 1, 2017, we adopted the new accounting

standard ASC 606, Revenue from Contracts with Customers and all the related amendments (“new revenue standard”) to

all contracts using the modified retrospective method. We recognized the cumulative effect of initially applying the new

revenue standard as an adjustment to the opening balance of retained earnings. The comparative information has not been

restated and continues to be reported under the accounting standards in effect for those periods. We expect the impact of the

adoption of the new standard to be immaterial to our net income on an ongoing basis.

A majority of our sales revenue continues to be recognized when products are shipped from our manufacturing facilities. For

certain vehicle sales where revenue was previously deferred, such as vehicles subject to a guaranteed resale value

recognized as a lease and transactions in which a Ford-owned entity delivered vehicles, we now recognize revenue when

vehicles are shipped.

……

The cumulative effect of the changes made to our consolidated January 1, 2017 balance sheet for the adoption of ASU 2016-09,

Stock Compensation - Improvements to Employee Share-Based Payment Accounting and ASU 2014-09, Revenue - Revenue from

Contracts with Customers were as follows (in millions):

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

25Exhibit I – Post-adoption Disclosure (Cont’d)

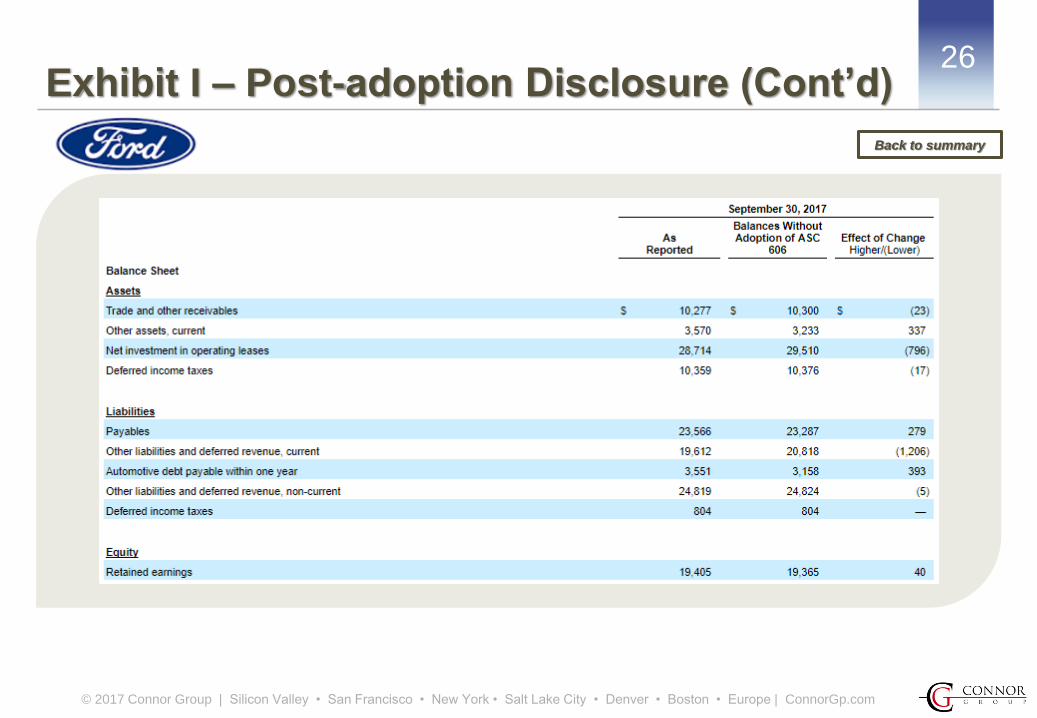

In accordance with the new revenue standard requirements, the disclosure of the impact of adoption on our consolidated income

statement and balance sheet for the periods ended September 30, 2017 was as follows (in millions):

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

26Exhibit I – Post-adoption Disclosure (Cont’d)

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

27Exhibit I – Post-adoption Disclosure (Cont’d)

REVENUE

The following table disaggregates our revenue by major source for the periods ended September 30, 2017 (in millions):

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

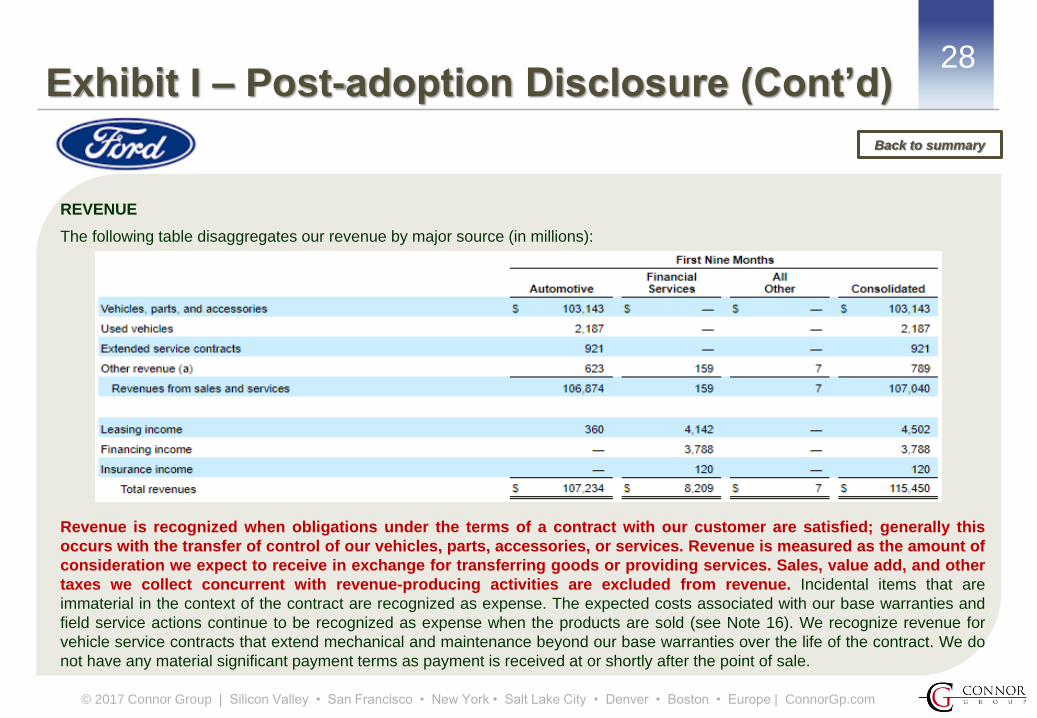

28Exhibit I – Post-adoption Disclosure (Cont’d)

REVENUE

The following table disaggregates our revenue by major source (in millions):

Revenue is recognized when obligations under the terms of a contract with our customer are satisfied; generally this

occurs with the transfer of control of our vehicles, parts, accessories, or services. Revenue is measured as the amount of

consideration we expect to receive in exchange for transferring goods or providing services. Sales, value add, and other

taxes we collect concurrent with revenue-producing activities are excluded from revenue. Incidental items that are

immaterial in the context of the contract are recognized as expense. The expected costs associated with our base warranties and

field service actions continue to be recognized as expense when the products are sold (see Note 16). We recognize revenue for

vehicle service contracts that extend mechanical and maintenance beyond our base warranties over the life of the contract. We do

not have any material significant payment terms as payment is received at or shortly after the point of sale.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

29Exhibit I – Post-adoption Disclosure (Cont’d)

REVENUE

Automotive Segment

Vehicles, Parts, and Accessories. For the majority of vehicles, parts, and accessories, we transfer control and recognize a sale when

we ship the product from our manufacturing facility to our customer (dealers and distributors). We receive cash equal to the

invoice price for most vehicle sales at the time of wholesale. When the vehicle sale is financed by our wholly-owned

subsidiary Ford Credit, the dealer pays Ford Credit when it sells the vehicle to the retail customer (see Note 8). Payment

terms on part sales to dealers, distributors, and retailers range from 30 days to 120 days. The amount of consideration we

receive and revenue we recognize varies with changes in marketing incentives and returns we offer to our customers and

their customers. When we give our dealers the right to return eligible parts and accessories, we estimate the expected

returns based on an analysis of historical experience. We adjust our estimate of revenue at the earlier of when the most

likely amount of consideration we expect to receive changes or when the consideration becomes fixed. As a result we

recognized an increase to revenue from prior periods in the third quarter of 2017 of $33 million.

Depending on the terms of the arrangement, we may also defer the recognition of a portion of the consideration received because

we have to satisfy a future obligation (e.g., free extended service contracts). We use an observable price to determine the stand-

alone selling price for separate performance obligations or a cost plus margin approach when one is not available. We

have elected to recognize the cost for freight and shipping when control over vehicles, parts, or accessories have

transferred to the customer as an expense in Cost of sales.

We sell vehicles to daily rental companies and guarantee that we will pay them the difference between an agreed amount and the

value they are able to realize upon resale. At the time of transfer of vehicles to the daily rental companies, we record the probable

amount we will pay under the guarantee to Other liabilities and deferred revenue.

Used Vehicles. We sell used vehicles both at auction and through our consolidated dealerships. Proceeds from the sale of these

vehicles are recognized in Automotive revenues upon transfer of control of the vehicle to the customer and the related vehicle

carrying value is recognized in Cost of sales.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

30Exhibit I – Post-adoption Disclosure (Cont’d)

REVENUE

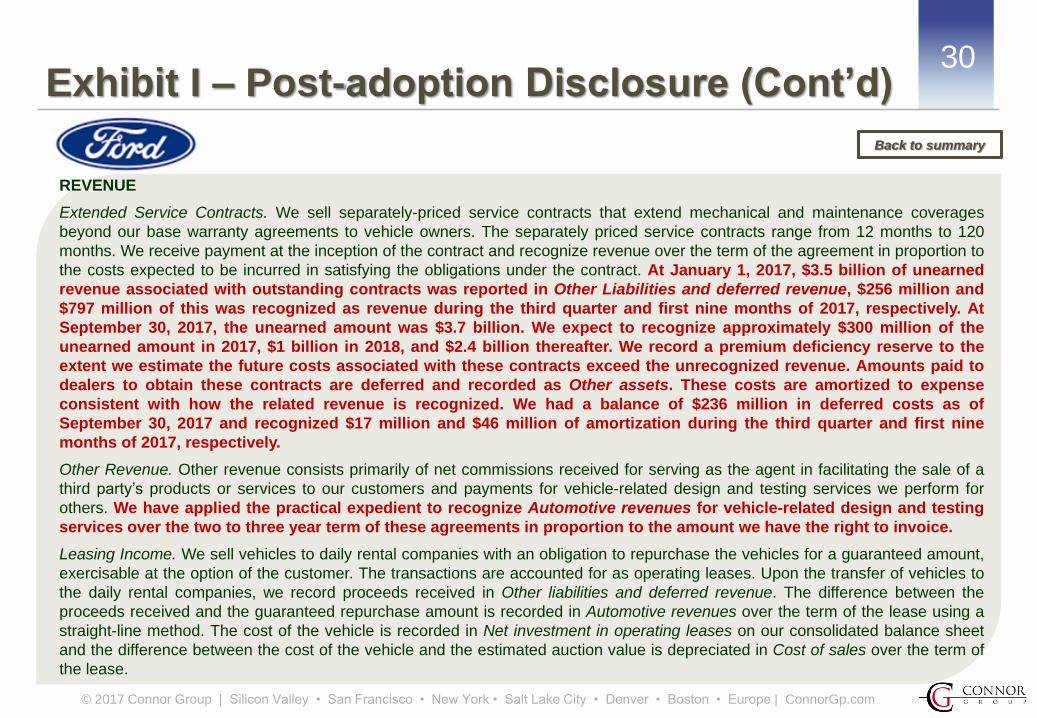

Extended Service Contracts. We sell separately-priced service contracts that extend mechanical and maintenance coverages

beyond our base warranty agreements to vehicle owners. The separately priced service contracts range from 12 months to 120

months. We receive payment at the inception of the contract and recognize revenue over the term of the agreement in proportion to

the costs expected to be incurred in satisfying the obligations under the contract. At January 1, 2017, $3.5 billion of unearned

revenue associated with outstanding contracts was reported in Other Liabilities and deferred revenue, $256 million and

$797 million of this was recognized as revenue during the third quarter and first nine months of 2017, respectively. At

September 30, 2017, the unearned amount was $3.7 billion. We expect to recognize approximately $300 million of the

unearned amount in 2017, $1 billion in 2018, and $2.4 billion thereafter. We record a premium deficiency reserve to the

extent we estimate the future costs associated with these contracts exceed the unrecognized revenue. Amounts paid to

dealers to obtain these contracts are deferred and recorded as Other assets. These costs are amortized to expense

consistent with how the related revenue is recognized. We had a balance of $236 million in deferred costs as of

September 30, 2017 and recognized $17 million and $46 million of amortization during the third quarter and first nine

months of 2017, respectively.

Other Revenue. Other revenue consists primarily of net commissions received for serving as the agent in facilitating the sale of a

third party’s products or services to our customers and payments for vehicle-related design and testing services we perform for

others. We have applied the practical expedient to recognize Automotive revenues for vehicle-related design and testing

services over the two to three year term of these agreements in proportion to the amount we have the right to invoice.

Leasing Income. We sell vehicles to daily rental companies with an obligation to repurchase the vehicles for a guaranteed amount,

exercisable at the option of the customer. The transactions are accounted for as operating leases. Upon the transfer of vehicles to

the daily rental companies, we record proceeds received in Other liabilities and deferred revenue. The difference between the

proceeds received and the guaranteed repurchase amount is recorded in Automotive revenues over the term of the lease using a

straight-line method. The cost of the vehicle is recorded in Net investment in operating leases on our consolidated balance sheet

and the difference between the cost of the vehicle and the estimated auction value is depreciated in Cost of sales over the term of

the lease.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

REVENUE

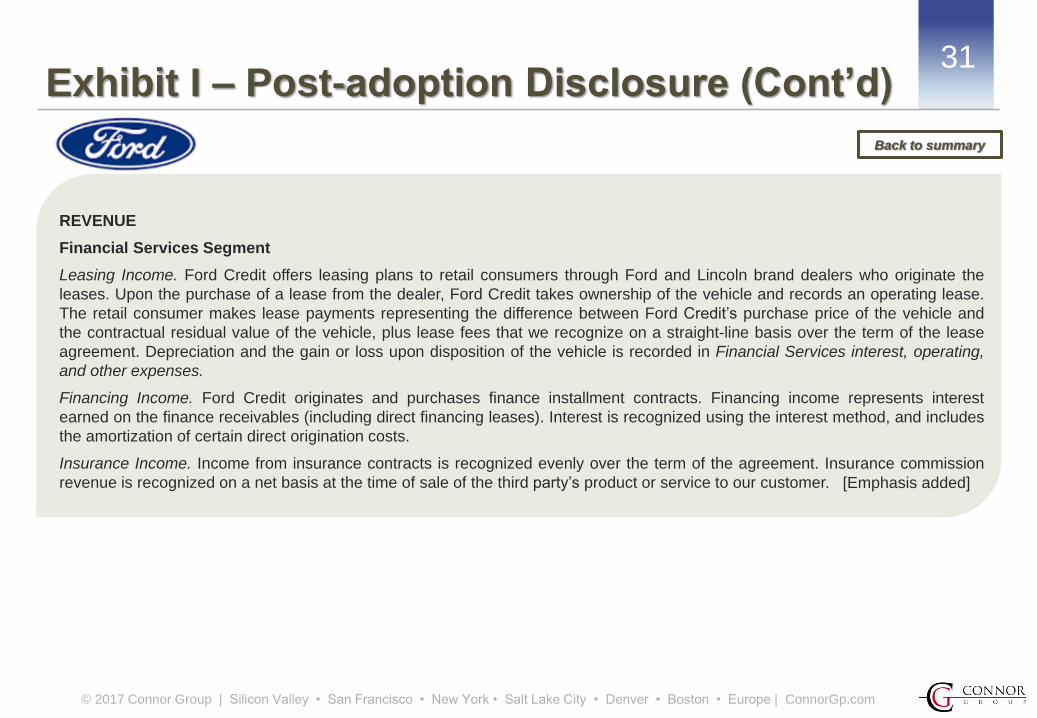

Financial Services Segment

Leasing Income. Ford Credit offers leasing plans to retail consumers through Ford and Lincoln brand dealers who originate the

leases. Upon the purchase of a lease from the dealer, Ford Credit takes ownership of the vehicle and records an operating lease.

The retail consumer makes lease payments representing the difference between Ford Credit’s purchase price of the vehicle and

the contractual residual value of the vehicle, plus lease fees that we recognize on a straight-line basis over the term of the lease

agreement. Depreciation and the gain or loss upon disposition of the vehicle is recorded in Financial Services interest, operating,

and other expenses.

Financing Income. Ford Credit originates and purchases finance installment contracts. Financing income represents interest

earned on the finance receivables (including direct financing leases). Interest is recognized using the interest method, and includes

the amortization of certain direct origination costs.

Insurance Income. Income from insurance contracts is recognized evenly over the term of the agreement. Insurance commission

revenue is recognized on a net basis at the time of sale of the third party’s product or service to our customer.

31Exhibit I – Post-adoption Disclosure (Cont’d)

[Emphasis added]

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

32Exhibit I – Post-adoption Disclosure (Cont’d)

REVENUE

The majority of our revenue is derived from long-term contracts and programs that can span several years. We account for

revenue in accordance with ASC Topic 606, Revenue from Contracts with Customers, which we adopted on January 1,

2017, using the retrospective method. See Note Q for further discussion of the adoption, including the impact on our 2016

financial statements.

Performance Obligations. A performance obligation is a promise in a contract to transfer a distinct good or service to the

customer, and is the unit of account in ASC Topic 606. A contract’s transaction price is allocated to each distinct performance

obligation and recognized as revenue when, or as, the performance obligation is satisfied. The majority of our contracts have a

single performance obligation as the promise to transfer the individual goods or services is not separately identifiable from other

promises in the contracts and, therefore, not distinct. Some of our contracts have multiple performance obligations, most commonly

due to the contract covering multiple phases of the product lifecycle (development, production, maintenance and support). For

contracts with multiple performance obligations, we allocate the contract’s transaction price to each performance obligation using

our best estimate of the standalone selling price of each distinct good or service in the contract. The primary method used to

estimate standalone selling price is the expected cost plus a margin approach, under which we forecast our expected

costs of satisfying a performance obligation and then add an appropriate margin for that distinct good or service.

Contract modifications are routine in the performance of our contracts. Contracts are often modified to account for changes in the

contract specifications or requirements. In most instances, contract modifications are for goods or services that are not distinct,

and, therefore, are accounted for as part of the existing contract.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

33Exhibit I – Post-adoption Disclosure (Cont’d)

REVENUE

Our performance obligations are satisfied over time as work progresses or at a point in time. Revenue from products and services

transferred to customers over time accounted for 70% of our revenue for the three- and nine-month periods ended October 1,

2017, and 72% and 71% of our revenue for the three- and nine-month periods ended October 2, 2016, respectively. Substantially

all of our revenue in the defense groups is recognized over time because control is transferred continuously to our

customers. Typically, revenue is recognized over time using costs incurred to date relative to total estimated costs at

completion to measure progress toward satisfying our performance obligations. Incurred cost represents work

performed, which corresponds with, and thereby best depicts, the transfer of control to the customer. Contract costs

include labor, material, overhead and, when appropriate, G&A expenses.

Revenue from goods and services transferred to customers at a point in time accounted for 30% of our revenue for the three- and

nine-month periods ended October 1, 2017, and 28% and 29% of our revenue for the three- and nine-month periods

ended October 2, 2016, respectively. The majority of our revenue recognized at a point in time is for the manufacture of

business-jet aircraft in our Aerospace group. Revenue on these contracts is recognized when the customer obtains

control of the asset, which is generally upon delivery and acceptance by the customer of the fully outfitted aircraft.

On October 1, 2017, we had $63.9 billion of remaining performance obligations, which we also refer to as total backlog.

We expect to recognize approximately 50% of our remaining performance obligations as revenue by 2018, an

additional 30% by 2020 and the balance thereafter.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

34Exhibit I – Post-adoption Disclosure (Cont’d)

REVENUE

Contract Estimates. Accounting for long-term contracts and programs involves the use of various techniques to estimate total

contract revenue and costs. For long-term contracts, we estimate the profit on a contract as the difference between the total

estimated revenue and expected costs to complete a contract and recognize that profit over the life of the contract.

Contract estimates are based on various assumptions to project the outcome of future events that often span several years. These

assumptions include labor productivity and availability; the complexity of the work to be performed; the cost and availability of

materials; the performance of subcontractors; and the availability and timing of funding from the customer.

The nature of our contracts gives rise to several types of variable consideration, including claims and award and

incentive fees. We include in our contract estimates additional revenue for submitted contract modifications or claims

against the customer when we believe we have an enforceable right to the modification or claim, the amount can be

estimated reliably and its realization is probable. In evaluating these criteria, we consider the contractual/legal basis for

the claim, the cause of any additional costs incurred, the reasonableness of those costs and the objective evidence

available to support the claim. We include award or incentive fees in the estimated transaction price when there is a basis

to reasonably estimate the amount of the fee. These estimates are based on historical award experience, anticipated

performance and our best judgment at the time. Because of our certainty in estimating these amounts, they are included

in the transaction price of our contracts and the associated remaining performance obligations.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

35Exhibit I – Post-adoption Disclosure (Cont’d)

REVENUE

As a significant change in one or more of these estimates could affect the profitability of our contracts, we review and

update our contract-related estimates regularly. We recognize adjustments in estimated profit on contracts under the

cumulative catch-up method. Under this method, the impact of the adjustment on profit recorded to date on a contract is

recognized in the period the adjustment is identified. Revenue and profit in future periods of contract performance are

recognized using the adjusted estimate. If at any time the estimate of contract profitability indicates an anticipated loss

on the contract, we recognize the total loss in the quarter it is identified.

The impact of adjustments in contract estimates on our operating earnings can be reflected in either operating costs and

expenses or revenue. The aggregate impact of adjustments in contract estimates increased our revenue, operating

earnings and diluted earnings per share as follows:

No adjustment on any one contract was material to our unaudited Consolidated Financial Statements for the three- and

nine-month periods ended October 1, 2017, and October 2, 2016.

Revenue by Category. Our portfolio of products and services consists of over 10,000 active contracts. The following series of

tables presents our revenue disaggregated by several categories.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

36Exhibit I – Post-adoption Disclosure (Cont’d)

REVENUE

Revenue by major product line was as follows:

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

37Exhibit I – Post-adoption Disclosure (Cont’d)

REVENUE

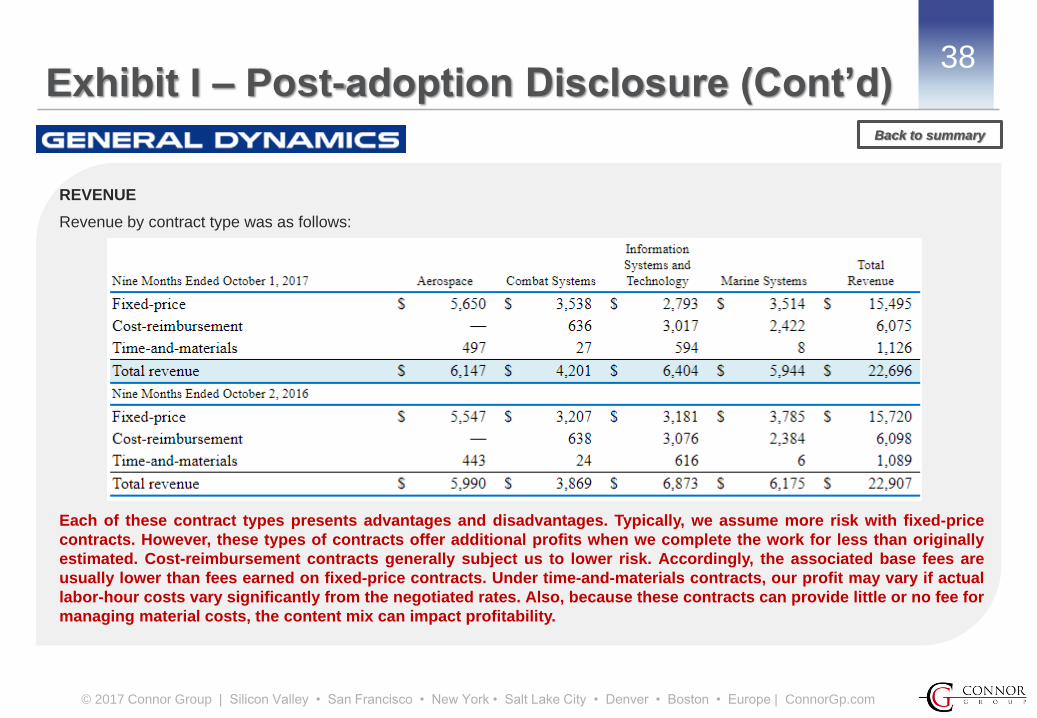

Revenue by contract type was as follows:

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

38Exhibit I – Post-adoption Disclosure (Cont’d)

REVENUE

Revenue by contract type was as follows:

Each of these contract types presents advantages and disadvantages. Typically, we assume more risk with fixed-price

contracts. However, these types of contracts offer additional profits when we complete the work for less than originally

estimated. Cost-reimbursement contracts generally subject us to lower risk. Accordingly, the associated base fees are

usually lower than fees earned on fixed-price contracts. Under time-and-materials contracts, our profit may vary if actual

labor-hour costs vary significantly from the negotiated rates. Also, because these contracts can provide little or no fee for

managing material costs, the content mix can impact profitability.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

39Exhibit I – Post-adoption Disclosure (Cont’d)

REVENUE

Revenue by customer was as follows:

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

40Exhibit I – Post-adoption Disclosure (Cont’d)

REVENUE

Revenue by customer was as follows:

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

41Exhibit I – Post-adoption Disclosure (Cont’d)

REVENUE

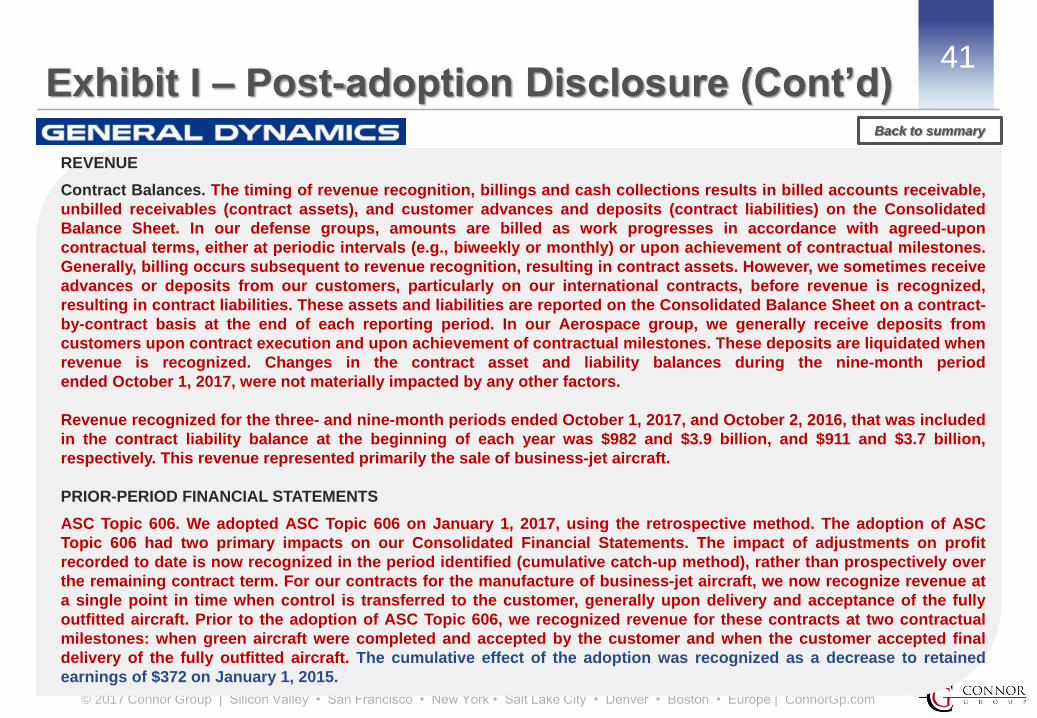

Contract Balances. The timing of revenue recognition, billings and cash collections results in billed accounts receivable,

unbilled receivables (contract assets), and customer advances and deposits (contract liabilities) on the Consolidated

Balance Sheet. In our defense groups, amounts are billed as work progresses in accordance with agreed-upon

contractual terms, either at periodic intervals (e.g., biweekly or monthly) or upon achievement of contractual milestones.

Generally, billing occurs subsequent to revenue recognition, resulting in contract assets. However, we sometimes receive

advances or deposits from our customers, particularly on our international contracts, before revenue is recognized,

resulting in contract liabilities. These assets and liabilities are reported on the Consolidated Balance Sheet on a contract-

by-contract basis at the end of each reporting period. In our Aerospace group, we generally receive deposits from

customers upon contract execution and upon achievement of contractual milestones. These deposits are liquidated when

revenue is recognized. Changes in the contract asset and liability balances during the nine-month period

ended October 1, 2017, were not materially impacted by any other factors.

Revenue recognized for the three- and nine-month periods ended October 1, 2017, and October 2, 2016, that was included

in the contract liability balance at the beginning of each year was $982 and $3.9 billion, and $911 and $3.7 billion,

respectively. This revenue represented primarily the sale of business-jet aircraft.

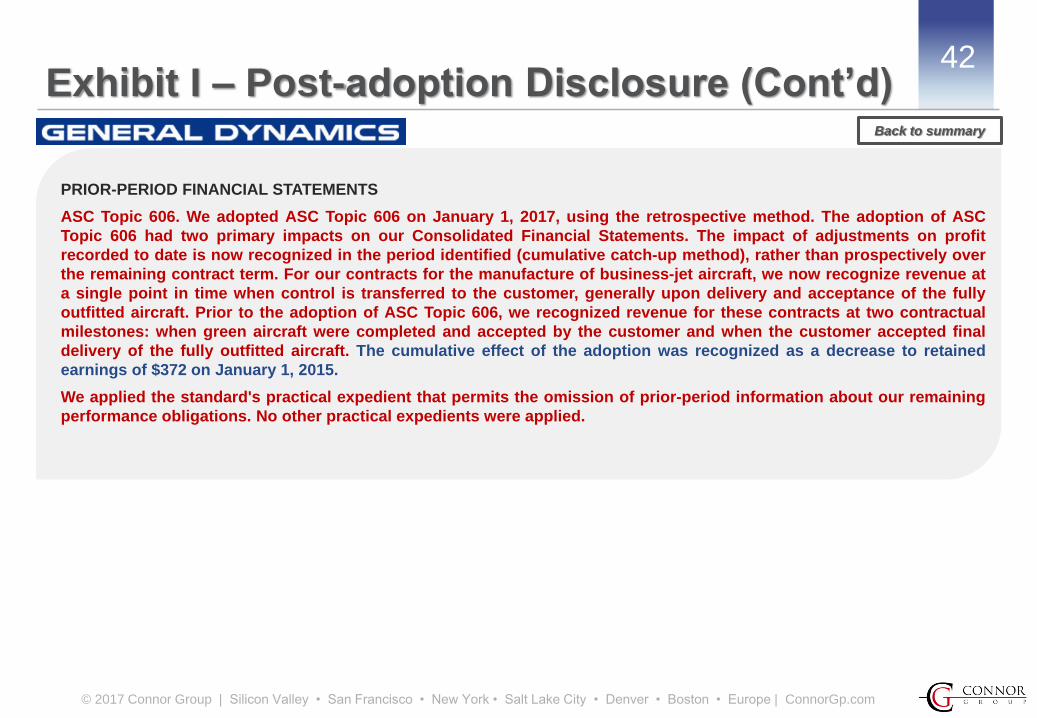

PRIOR-PERIOD FINANCIAL STATEMENTS

ASC Topic 606. We adopted ASC Topic 606 on January 1, 2017, using the retrospective method. The adoption of ASC

Topic 606 had two primary impacts on our Consolidated Financial Statements. The impact of adjustments on profit

recorded to date is now recognized in the period identified (cumulative catch-up method), rather than prospectively over

the remaining contract term. For our contracts for the manufacture of business-jet aircraft, we now recognize revenue at

a single point in time when control is transferred to the customer, generally upon delivery and acceptance of the fully

outfitted aircraft. Prior to the adoption of ASC Topic 606, we recognized revenue for these contracts at two contractual

milestones: when green aircraft were completed and accepted by the customer and when the customer accepted final

delivery of the fully outfitted aircraft. The cumulative effect of the adoption was recognized as a decrease to retained

earnings of $372 on January 1, 2015.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

42Exhibit I – Post-adoption Disclosure (Cont’d)

PRIOR-PERIOD FINANCIAL STATEMENTS

ASC Topic 606. We adopted ASC Topic 606 on January 1, 2017, using the retrospective method. The adoption of ASC

Topic 606 had two primary impacts on our Consolidated Financial Statements. The impact of adjustments on profit

recorded to date is now recognized in the period identified (cumulative catch-up method), rather than prospectively over

the remaining contract term. For our contracts for the manufacture of business-jet aircraft, we now recognize revenue at

a single point in time when control is transferred to the customer, generally upon delivery and acceptance of the fully

outfitted aircraft. Prior to the adoption of ASC Topic 606, we recognized revenue for these contracts at two contractual

milestones: when green aircraft were completed and accepted by the customer and when the customer accepted final

delivery of the fully outfitted aircraft. The cumulative effect of the adoption was recognized as a decrease to retained

earnings of $372 on January 1, 2015.

We applied the standard's practical expedient that permits the omission of prior-period information about our remaining

performance obligations. No other practical expedients were applied.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

43Exhibit I – Post-adoption Disclosure (Cont’d)

PRIOR-PERIOD FINANCIAL STATEMENTS

The following tables summarize the effects of adopting these accounting standards on our unaudited Consolidated Financial

Statements.

Consolidated Statement of Earnings (Unaudited)

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

44Exhibit I – Post-adoption Disclosure (Cont’d)

PRIOR-PERIOD FINANCIAL STATEMENTS

The following tables summarize the effects of adopting these accounting standards on our unaudited Consolidated Financial

Statements.

Consolidated Statement of Earnings (Unaudited)

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

45Exhibit I – Post-adoption Disclosure (Cont’d)

PRIOR-PERIOD FINANCIAL STATEMENTS

Consolidated Statement of Earnings (Unaudited)

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

46Exhibit I – Post-adoption Disclosure (Cont’d)

PRIOR-PERIOD FINANCIAL STATEMENTS

Consolidated Statement of Comprehensive Income (Unaudited)

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

47Exhibit I – Post-adoption Disclosure (Cont’d)

PRIOR-PERIOD FINANCIAL STATEMENTS Consolidated Balance Sheet (Unaudited)

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

48Exhibit I – Post-adoption Disclosure (Cont’d)

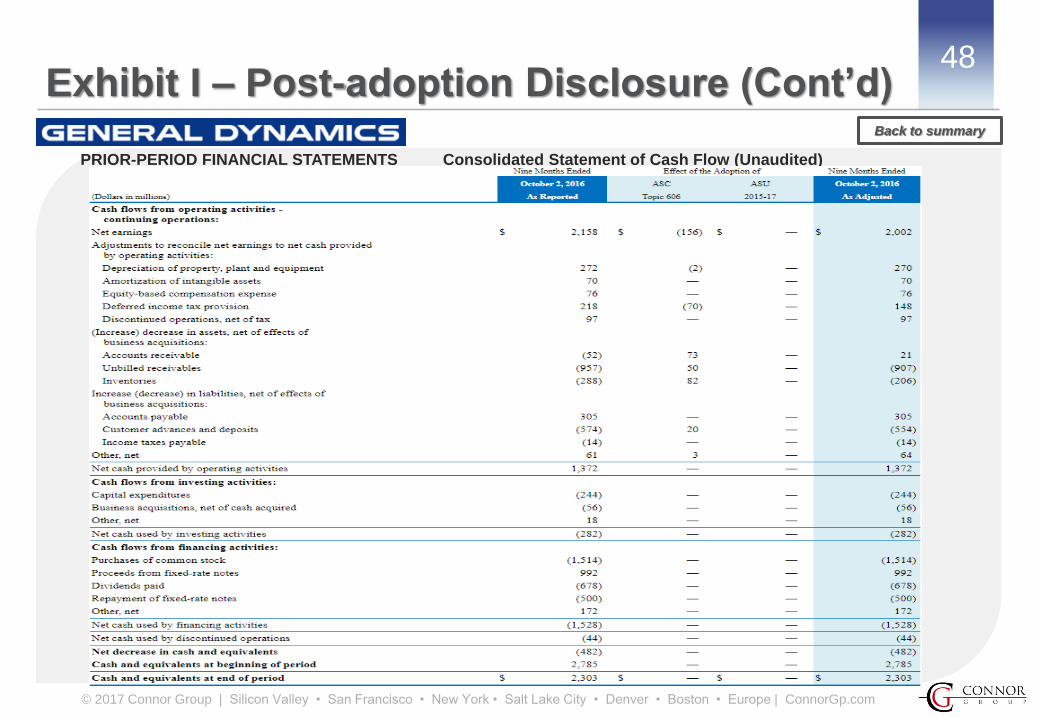

PRIOR-PERIOD FINANCIAL STATEMENTS Consolidated Statement of Cash Flow (Unaudited)

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

49Exhibit I – Post-adoption Disclosure (Cont’d)

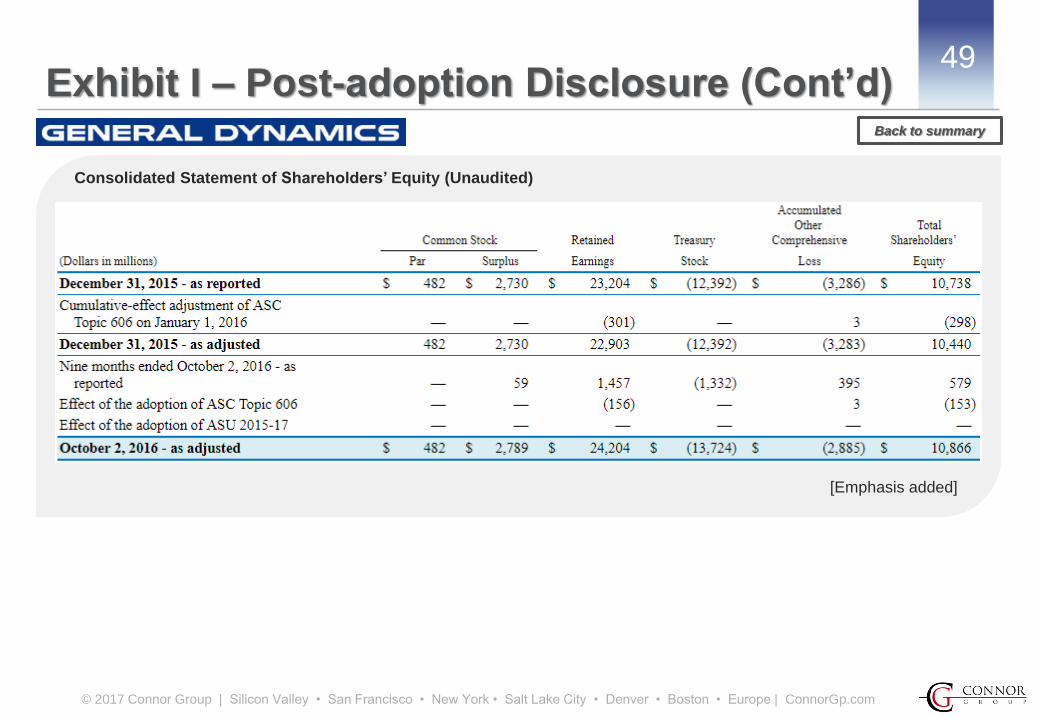

Consolidated Statement of Shareholders’ Equity (Unaudited)

Back to summary

[Emphasis added]

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

50Exhibit I – Post-adoption Disclosure (Cont’d)

…… We early adopted the requirements of the new standard as of February 1, 2017, utilizing the full retrospective method

of transition. Adoption of the new standard resulted in changes to our accounting policies for revenue recognition, trade and other

receivables, and deferred commissions as detailed below. We applied the new standard using a practical expedient where the

consideration allocated to the remaining performance obligations or an explanation of when we expect to recognize that

amount as revenue for all reporting periods presented before the date of the initial application is not disclosed.

The impact of adopting the new standard on our fiscal 2017 and fiscal 2016 revenues is not material. The primary impact

of adopting the new standard relates to the deferral of incremental commission costs of obtaining subscription contracts.

Under Topic 605, we deferred only direct and incremental commission costs to obtain a contract and amortized those

costs over the term of the related subscription contract, which was generally three years or longer. Under the new

standard, we defer all incremental commission costs to obtain the contract. We amortize these costs on a straight-line

basis over a period of benefit that we have determined to be five years or the related contractual renewal period,

depending on whether the contract is an initial or renewal contract, respectively.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

51Exhibit I – Post-adoption Disclosure (Cont’d)

We adjusted our condensed consolidated financial statements from amounts previously reported due to the adoption of

ASU No. 2014-09 and ASU No. 2016-18. Select condensed consolidated balance sheet line items, which reflect the

adoption of the new ASU’s are as follows (in thousands):

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

52Exhibit I – Post-adoption Disclosure (Cont’d)

Select unaudited condensed consolidated statement of operations line items, which reflect the adoption of the new ASUs

are as follows (in thousands except per share data):

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

53Exhibit I – Post-adoption Disclosure (Cont’d)

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

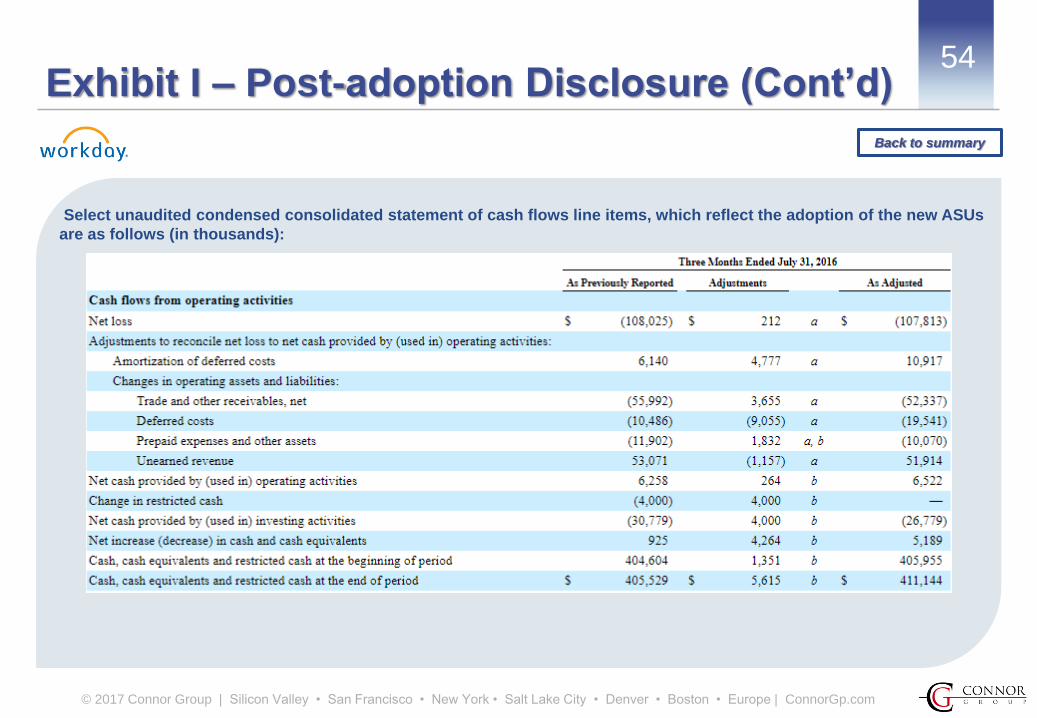

54Exhibit I – Post-adoption Disclosure (Cont’d)

Select unaudited condensed consolidated statement of cash flows line items, which reflect the adoption of the new ASUs

are as follows (in thousands):

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

55Exhibit I – Post-adoption Disclosure (Cont’d)

a. Adjusted to reflect the adoption of ASU No. 2014-09, Revenue from Contracts with Customers.

b. Adjusted to reflect the adoption of ASU No. 2016-18, Statement of Cash Flows, Restricted Cash.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

56Exhibit I – Post-adoption Disclosure (Cont’d)

Summary of Significant Accounting Policies

Revenue Recognition

We derive our revenues primarily from subscription services and professional services. Revenues are recognized when control of

these services is transferred to our customers, in an amount that reflects the consideration we expect to be entitled to in exchange

for those services.

……

Subscription Services Revenues

Subscription services revenues primarily consist of fees that provide customers access to one or more of our cloud applications for

finance, human resources, and analytics, with routine customer support. Revenue is generally recognized over time on a ratable

basis over the contract term beginning on the date that our service is made available to the customer. Our subscription contracts are

generally three years or longer in length, billed annually in advance, and non-cancelable.

Professional Services Revenues

Professional services revenues primarily consist of fees for deployment and optimization services, as well as training. The majority

of our consulting contracts are billed on a time and materials basis and revenue is recognized over time as the services are

performed. For contracts billed on a fixed price basis, revenue is recognized over time based on the proportion performed.

Contracts with Multiple Performance Obligations

Some of our contracts with customers contain multiple performance obligations. For these contracts, we account for

individual performance obligations separately if they are distinct. The transaction price is allocated to the separate

performance obligations on a relative standalone selling price basis. We determine the standalone selling prices based on

our overall pricing objectives, taking into consideration market conditions and other factors, including the value of our

contracts, the cloud applications sold, customer demographics, geographic locations, and the number and types of users

within our contracts.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

57Exhibit I – Post-adoption Disclosure (Cont’d)

Trade and Other Receivables

Trade and other receivables are primarily comprised of trade receivables that are recorded at the invoice amount, net of an

allowance for doubtful accounts, which is not material. Other receivables represent unbilled receivables related to subscription and

professional services contracts.

Deferred Commissions

Sales commissions earned by our sales force are considered incremental and recoverable costs of obtaining a contract

with a customer. Sales commissions for initial contracts are deferred and then amortized on a straight-line basis over a

period of benefit that we have determined to be five years. We determined the period of benefit by taking into

consideration our customer contracts, our technology and other factors. Sales commissions for renewal contracts are

deferred and then amortized on a straight-line basis over the related contractual renewal period. Amortization expense is

included in Sales and marketing expenses in the accompanying condensed consolidated statements of operations.

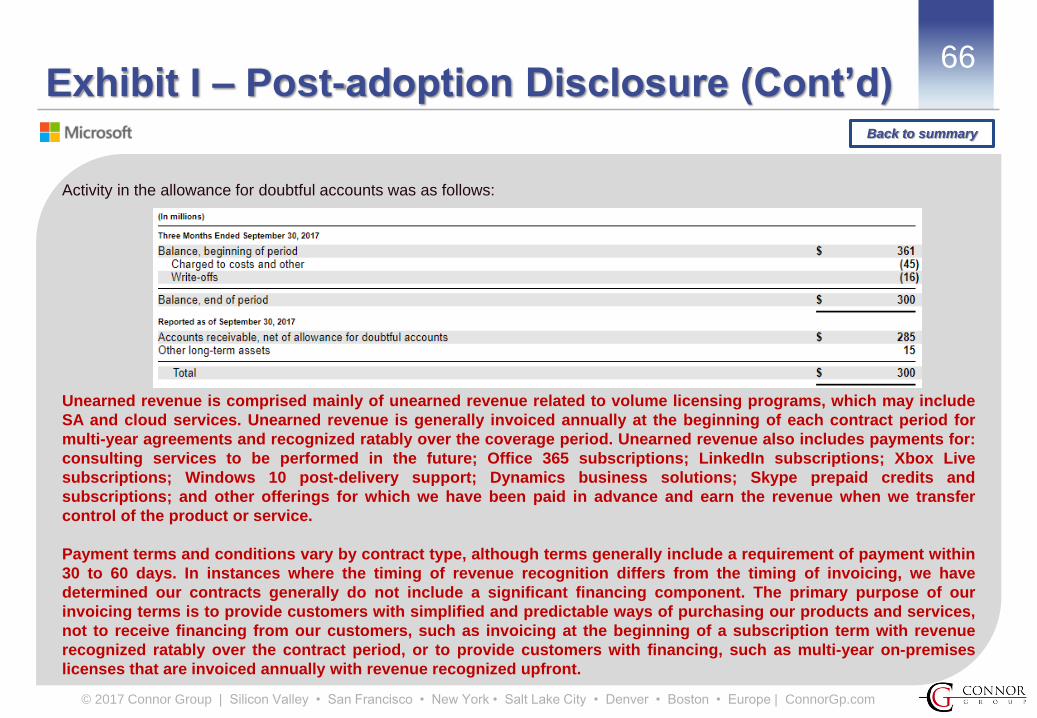

Unearned Revenue and Performance Obligations

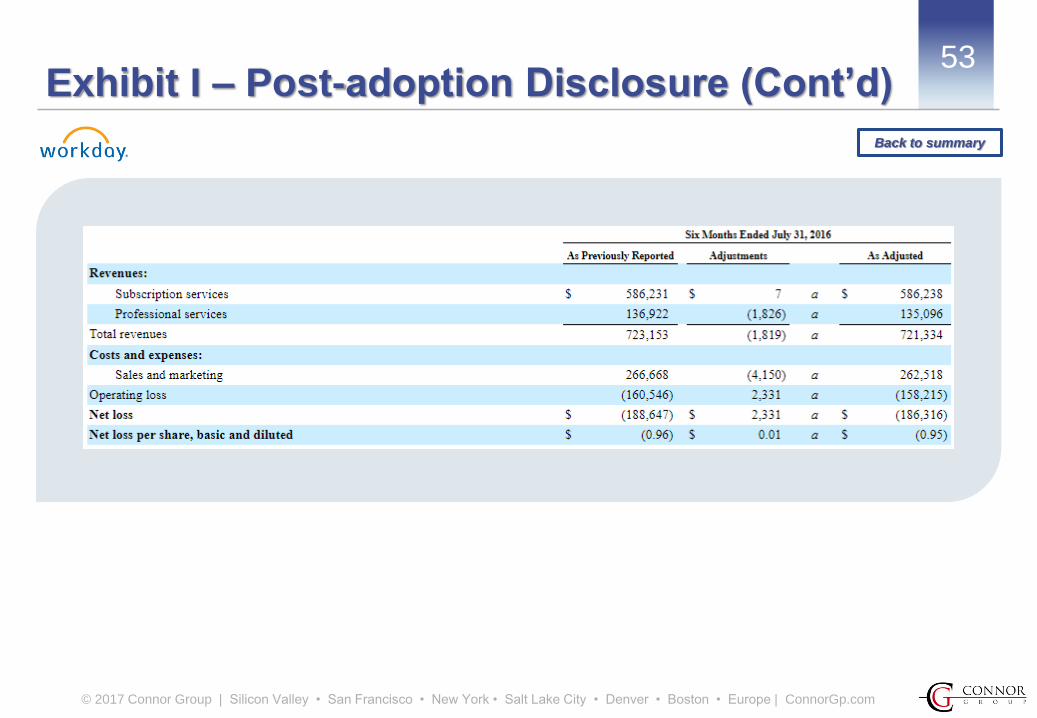

$398 million and $282 million of subscription services revenue was recognized during the three months ended July 31,

2017 and 2016, respectively, that was included in the unearned revenue balances at the beginning of the respective

periods. $759 million and $533 million of subscription services revenue was recognized during the six months ended July

31, 2017 and 2016, respectively, that was included in the unearned revenue balances at the beginning of the respective

periods. Professional services revenue recognized in the same periods from unearned revenue balances at the beginning

of the respective periods was not material.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

58Exhibit I – Post-adoption Disclosure (Cont’d)

Transaction Price Allocated to the Remaining Performance Obligations

As of July 31, 2017, approximately $4.4 billion of revenue is expected to be recognized from remaining performance

obligations for subscription contracts. We expect to recognize revenue on approximately two thirds of these remaining

performance obligations over the next 24 months, with the balance recognized thereafter. Revenue from remaining

performance obligations for professional services contracts as of July 31, 2017 was not material.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

59Exhibit I – Post-adoption Disclosure (Cont’d)

Disaggregation of Revenue

We sell our subscription contracts and related services in two primary geographical markets: to customers located in the

United States, and to customers located outside of the United States. Revenue by geography is generally based on the

address of the customer as specified in our master subscription agreement. The following table sets forth revenue by

geographic area (in thousands):

No single country other than the United States had revenues greater than 10% of total revenues for the three and six

months ended July 31, 2017 and 2016. No customer individually accounted for more than 10% of our trade and other

receivables, net as of July 31, 2017 or January 31, 2017.

Back to summary

[Emphasis added]

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

60Exhibit I – Post-adoption Disclosure (Cont’d)

……

We elected to early adopt the standard effective July 1, 2017, using the full retrospective method, which required us to

restate each prior reporting period presented. We implemented internal controls and key system functionality to enable the

preparation of financial information on adoption.

The most significant impact of the standard relates to our accounting for software license revenue. Specifically, for

Windows 10, we recognize revenue predominantly at the time of billing and delivery rather than ratably over the life of the

related device. For certain multi-year commercial software subscriptions that include both distinct software licenses and

SA, we recognize license revenue at the time of contract execution rather than over the subscription period. Due to the

complexity of certain of our commercial license subscription contracts, the actual revenue recognition treatment required

under the standard depends on contract-specific terms and in some instances may vary from recognition at the time of

billing. Revenue recognition related to our hardware, cloud offerings (such as Office 365), LinkedIn, and professional

services remains substantially unchanged.

Adoption of the standard using the full retrospective method required us to restate certain previously reported results,

including the recognition of additional revenue and an increase in the provision for income taxes, primarily due to the net

change in Windows 10 revenue recognition. In addition, adoption of the standard resulted in an increase in accounts

receivable and other current and long-term assets, driven by unbilled receivables from upfront recognition of revenue for

certain multi-year commercial software subscriptions that include both distinct software licenses and Software

Assurance; a reduction of unearned revenue, driven by the upfront recognition of license revenue from Windows 10 and

certain multi-year commercial software subscriptions; and an increase in deferred income taxes, driven by the upfront

recognition of revenue. Refer to Impacts to Previously Reported Results below for the impact of adoption of the standard

on our consolidated financial statements.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

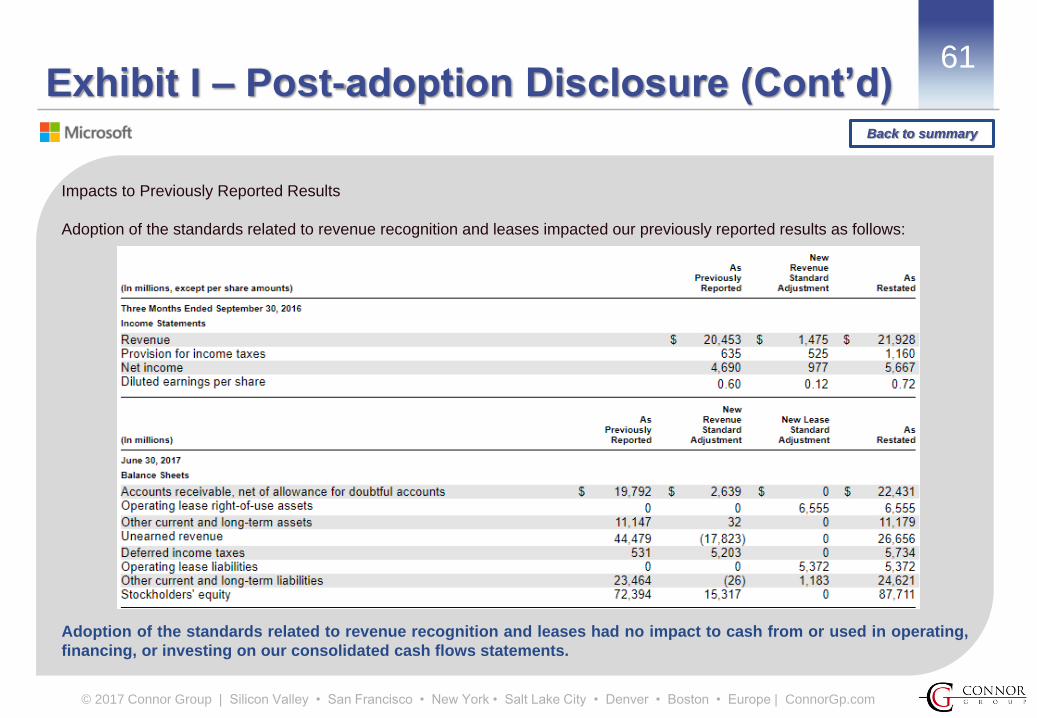

61Exhibit I – Post-adoption Disclosure (Cont’d)

Impacts to Previously Reported Results

Adoption of the standards related to revenue recognition and leases impacted our previously reported results as follows:

Adoption of the standards related to revenue recognition and leases had no impact to cash from or used in operating,

financing, or investing on our consolidated cash flows statements.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

62Exhibit I – Post-adoption Disclosure (Cont’d)

Revenue Recognition

Revenue is recognized upon transfer of control of promised products or services to customers in an amount that reflects the

consideration we expect to receive in exchange for those products or services. We enter into contracts that can include various

combinations of products and services, which are generally capable of being distinct and accounted for as separate performance

obligations. Revenue is recognized net of allowances for returns and any taxes collected from customers, which are

subsequently remitted to governmental authorities.

Nature of Products and Services

Licenses for on-premises software provide the customer with a right to use the software as it exists when made

available to the customer. Customers may purchase perpetual licenses or subscribe to licenses, which provide

customers with the same functionality and differ mainly in the duration over which the customer benefits from the

software. Revenue from distinct on-premises licenses is recognized upfront at the point in time when the software is

made available to the customer. In cases where we allocate revenue to software updates, primarily because the

updates are provided at no additional charge, revenue is recognized as the updates are provided, which is generally

ratably over the estimated life of the related device or license.

Certain volume licensing programs, including Enterprise Agreements, include on-premises licenses combined with Software

Assurance (“SA”). SA conveys rights to new software and upgrades released over the contract period and provides support,

tools, and training to help customers deploy and use products more efficiently. On-premises licenses are considered distinct

performance obligations when sold with SA. Revenue allocated to SA is generally recognized ratably over the contract

period as customers simultaneously consume and receive benefits, given that SA comprises distinct performance

obligations that are satisfied over time……

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

63Exhibit I – Post-adoption Disclosure (Cont’d)

Cloud services, which allow customers to use hosted software over the contract period without taking possession of the software,

are provided on either a subscription or consumption basis. Revenue related to cloud services provided on a subscription

basis is recognized ratably over the contract period. Revenue related to cloud services provided on a consumption

basis, such as the amount of storage used in a period, is recognized based on the customer utilization of such

resources. When cloud services require a significant level of integration and interdependency with software and the

individual components are not considered distinct, all revenue is recognized over the period in which the cloud services

are provided.

Revenue from search advertising is recognized when the advertisement appears in the search results or when the action

necessary to earn the revenue has been completed. Revenue from consulting services is recognized as services are

provided.

Our hardware is generally highly dependent on, and interrelated with, the underlying operating system and cannot

function without the operating system. In these cases, the hardware and software license are accounted for as a single

performance obligation and revenue is recognized at the point in time when ownership is transferred to resellers or

directly to end customers through retail stores and online marketplaces.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

64Exhibit I – Post-adoption Disclosure (Cont’d)

Significant Judgements

Our contracts with customers often include promises to transfer multiple products and services to a customer.

Determining whether products and services are considered distinct performance obligations that should be accounted

for separately versus together may require significant judgment. Certain cloud services, such as Office 365, depend on

a significant level of integration and interdependency between the desktop applications and cloud services. Judgment

is required to determine whether the software license is considered distinct and accounted for separately, or not

distinct and accounted for together with the cloud service and recognized over time.

Judgment is required to determine the SSP for each distinct performance obligation. We use a single amount to

estimate SSP for items that are not sold separately, including on-premises licenses sold with SA or software updates

provided at no additional charge. We use a range of amounts to estimate SSP when we sell each of the products and

services separately and need to determine whether there is a discount that needs to be allocated based on the relative

SSP of the various products and services.

In instances where SSP is not directly observable, such as when we do not sell the product or service separately, we

determine the SSP using information that may include market conditions and other observable inputs. We typically

have more than one SSP for individual products and services due to the stratification of those products and services by

customers and circumstances. In these instances, we may use information such as the size of the customer and

geographic region in determining the SSP.

Due to the various benefits from and the nature of our SA program, judgment is required to assess the pattern of delivery,

including the exercise pattern of certain benefits across our portfolio of customers.

Back to summary

© 2017 Connor Group | Silicon Valley • San Francisco • New York • Salt Lake City • Denver • Boston • Europe | ConnorGp.com

65Exhibit I – Post-adoption Disclosure (Cont’d)

Significant Judgements

Our products are generally sold with a right of return and we may provide other credits or incentives, which are