Embed Size (px)

Citation preview

Sept

embe

r 20

12

RBS Treasury Guide 2012 to print.indd 1 04/09/2012 12:33

Overview Treasurers rise to unprecedented challenges 1

Legislation and regulation Navigating the regulatory landscape 3

Risk management The changing face of risk 7

Operational efficiency Managing complexity in a multi bank environment 12

Treasury centre solutions Staying agnostic 21

Efficient financing solutions Connecting the value chain 25

Accessibility All change 29

Contents

Chairman and Editor-in-chief:Padraic Fallon

Directors: Sir Patrick Sergeant, The Viscount Rothermere, Richard Ensor (managing director), Neil Osborn, Dan Cohen, John Botts, Colin Jones, Diane Alfano, Christopher Fordham, Jaime Gonzalez, Jane Wilkinson, Martin Morgan, David Pritchard, Bashar Al-Rehany

Published byEuromoney Trading Limited Nestor House, Playhouse Yard, London, EC4V 5EX

Telephone: +44 20 7779 8888Fax: +44 20 7779 8345

Editor Philip Ayers

Publisher Ash Madar

RBS Treasury Guide 2012 to print.indd 2 04/09/2012 12:33

1

Treasurers rise to unprecedented challenges

Four years into the global financial and economic crisis, corporate treasurers face an unprecedented series of challenges. The eurozone turmoil continues unabated with no clear solution in sight, creating economic uncertainty and prompting volatile markets worldwide. At the same time, financial sector regulatory reform is changing the dynamic of the banking industry beyond recognition, with significant consequences for companies.

Against this backdrop, corporate treasurers continue to astonish in terms of their ingenuity. They are being asked to do much more for the business, often without additional resources. They not only have to manage the counterparty risk that arises from working with banks but must also deal with almost unanswerable questions, such as how to respond to the imposition

of capital controls should a country leave the euro.

Even business successes – such as the huge volumes of cash being generated by many companies (but not being reinvested) or rapid growth in emerging markets – pose treasury headaches. Yields remain at historic lows, complicating the investment of surplus cash while the impact of Basel III on banks’ appetite for corpo-rate cash could exacerbate problems further. Meanwhile, rapid growth in emerging markets raises the spectre of trapped cash.

A changing landscapeIn the chapters that follow we address these and many more of the challenges that face corporate treasurers in 2012. We outline strategies for navigating the ever-changing regulatory landscape, including the newly imposed

In times of international financial turmoil, corporate treasurers continue to astonish in terms of their ingenuity. They are being asked to do much more for their businesses, often without additional resources.

RBS Treasury Guide 2012 to print.indd 1 04/09/2012 12:33

requirement for corporates based in the eurozone to be able to submit Single Euro Payments Area (SEPA) payments in XML format by February 2014 (or October 2016 for non-eurozone countries).

We also assess the relative importance of the many risks faced by companies and the crucial role the treasury plays in managing them. The eurozone crisis has once again elevated counterparty – and country – risk to the fore. However, it has also resulted in increased currency volatility, which is placing the spotlight on FX risk management. Increased growth in emerging markets further reinforces the importance, as emerging market currencies are generally more volatile than G8 currencies.

The importance of efficiency to corporates in the current environment is prompting greater ambition when they establish payment factories.

Driven by new developments in standardization, treasurers are specifying a range of requirements for next generation payment factories – such as ‘on-behalf-of’ payments and analysis of cross-border and cross-currency transactions – that simply were not feasible just a few years ago. Corporates’ appetite for bank-agnostic solutions is also spurring collaborative initiatives such as ISO 20022 Common Global Implementation (CGI) XML and electronic bank account management (eBAM).

Technology and creativity have a huge role to play in addressing the challenges faced by treasurers. Innovative solutions such as supply chain finance deliver a unique win-win-win for suppliers, buyers and banks. More importantly, they help to strengthen relationships between all parties and improve everyone’s security. Supply chain finance also has the potential to realign functions within individual companies so that purchasing, finance and sales work for a common cause and deliver maximum benefits for the company.

We hope you enjoy the chapters that follow in this Insights on transforming the Treasury and gain insights that are helpful in your day-to-day activities. The articles are designed to stimulate thought, provoke debate and inspire action.

John Owen, CEO, international banking, M&IB, RBS

RBS Treasury Guide 2012 to print.indd 2 04/09/2012 12:33

333

SEPAIn Europe, the Single Euro Payments Area (SEPA), which is for euro payments only and spans 27 EU member states, three European Economic Area member states (Iceland, Norway and Lichtenstein) Switzerland and Monaco, is now complete. However, what was thought to be primarily an interbank concern – albeit with significant implications for corporates – has now been expanded to make direct demands on companies.

“European legislation introduced at the beginning of 2012 to support SEPA – effectively to set an end date for the use of national payment instruments – has also placed a specific requirement on corporates to change their systems to ensure they can accept the ISO 2022 XML format

used in SEPA,” explains Kevin Brown, managing director, global head, transaction services product, RBS.

From February 2014, all banks operating in Europe must migrate to SEPA and the XML standard. February 2014 is also the date set for corporates based in the eurozone to be able to submit SEPA payments in XML format. However, individual countries can seek a two-year exemption from this requirement, which would (almost) bring them into line with the requirements placed on non-eurozone countries of being able to submit XML payments by October 2016.

The deadline of February 2014 places a significant burden on corporates to change their systems so that they are able to use the XML format. The impending change was flagged up last year, but was

Navigating the regulatory landscapeThe regulatory landscape – for corporates, banks and consumers – has experienced unprecedented change in the period since the onset of the financial crisis in 2008, as governments and central banks have sought to prevent a reoccurrence of the problems that caused dislocation in the financial markets and a weak macro-economic environment.

RBS Treasury Guide 2012 to print.indd 3 04/09/2012 12:33

little discussed or addressed by corporates. Consequently the relatively rapid forced migration adds significantly to business stress.

Most importantly, the deadline is too close to allow the introduction of XML to be built into the standard business cycle: ordinarily a change of this type would occur simultaneously with an upgrade of an enterprise resource planning (ERP) system, for example. However, investment decisions relating to an ERP system upgrade before February 2014 will have already been taken by corporates.

As is often the case with new European requirements, there is a lack of clarity over some important issues surrounding the change. For example, the legislation does not specify whether corporates can submit a payment file to a third party, which would then convert it to the new format. If such a thing were possible

– and there is no reason why it should not be – it raises the question of why banks cannot perform that task for corporates (as they currently do thousands of times a day).

“The objective is enshrined in law but the detail is still to be worked out,” says Brown. “Provided countries make the decision to exempt corporates until 2016, then the deadline will be achievable. There will be enough time to schedule XML into normal system upgrades.”

Basel IIINecessarily – given the nature of the financial crisis – much of the attention of regulators has been focused on banks. However, corporates should not think that new regulations, such as Basel III, which apply only to banks have no implications for them. While Basel III, and many other regulatory changes such as the UK’s individual liquidity adequacy assessment (ILAA), may make the banking system more secure, they will also have significant consequences for both the availability and the cost of a variety of financial products and services.

In particular, Basel III will change how corporate deposits held at banks are treated in terms of run-off ratio and collateralization. These changes will have significant implications in banks’ willingness to offer attractive returns on corporations’ longer-term

Kevin Brown, managing director, global head, transaction services product, RBS

RBS Treasury Guide 2012 to print.indd 4 04/09/2012 12:33

5

investment cash (unless corporates are willing to pledge to leave their cash on deposit for a minimum period – more than 90 days). As a result, numerous banks, including RBS, have recently introduced 95-day notice accounts to gain beneficial regulatory treatment and be able to reward corporates adequately.

Basel III also has implications for how intraday liquidity is priced for corporates. “There will be an increasing focus on the value of intraday liquidity, volumes over the course of a day, how it is reported, whether banks should pay for it, and whether banks should charge for it,” says Brown.

Companies’ requirements for intraday liquidity vary considerably. For example, a large company may submit thousands of payments in the morning but not receive funds until the afternoon. Under Basel III, such a pattern results in sizeable exposure for the bank that must be made transparent to regulators in terms of cost. Equally, companies that bring intraday liquidity to banks over the course of a day – those that receive payments in the morning and send them in the afternoon – may be rewarded for that.

A balanced approachThe challenge for regulators is to take a prudent approach to banks

without damaging banks’ role in the transformation of maturities - taking short-term cash and turning it into long-term investment. Such a development would adversely affect the economy by trapping liquidity and giving it no economic value.

Equally, regulators must be careful to ensure consistency of regulation – a top concern for corporates. While regulations such as SEPA should be applied in the same way across Europe in theory (or across the world, in the case of Basel III), in practice there can be significant country differences in implementation. That not only results in an unfair competitive landscape for banks but raises costs for corporates because

of the need to accommodate different rules in different locations in terms of processes and systems.

In addition, regulators must ensure that their actions do not have unforeseen consequences. For

“The deadline of February 2014 places

a significant burden on corporates to change their systems so that

they are able to use the XML format”

RBS Treasury Guide 2012 to print.indd 5 04/09/2012 12:33

example, last year a newly drafted section (1073) of the Dodd-Frank Act, which came into effect on 21 July 2010, required banks to tell consumer and small and medium enterprise clients exactly how much a recipient of their payments would receive.

Such a requirement is onerous for banks – especially those without their

own networks – because it is difficult to provide certainty regarding charges other banks will deduct. There is a risk that some banks – unable to control end-to-end costs and therefore unable to provide the level of certainty required by Dodd-Frank 1073 – may simply withdraw from providing payment services to particular countries. As a result, competition and consumer choice could suffer. While not directly impacting large companies, Dodd-Frank 1073 signals an increased level of intervention by regulators that corporates should be aware of.

However, corporates must remember that, while the changes taking place to the regulatory environment undoubtedly add complexity and may increase costs in the short-term, there are significant benefits in terms of the stability of the global financial system. Moreover, in the long-term, increased transparency could help to spur competition and lower costs.

“ The challenge for regulators is to take a prudent approach to banks without damaging banks’ role in the transformation of maturities - taking short-term cash and turning it into long-term investment”

RBS Treasury Guide 2012 to print.indd 6 04/09/2012 12:33

7

Before the financial crisis liquidity was easily – and cheaply – available from the debt markets and banks. Now, the changed financial environment has highlighted the importance of using existing cash from the business more effectively. As a consequence, cash forecasting has been a crucial risk management tool: unless treasurers know where cash is, they cannot deploy it effectively.

In addition, corporate treasurers have redoubled their efforts to optimize their liquidity structures, ensuring that their notional pooling and physical sweeping arrangements meet the requirements of the business and the realities of the markets. The goal in liquidity management is always to consolidate cash to as great an extent as possible in order to maximize value.

However, the changed financial environment has altered how corporates try to achieve that goal. For example, whereas before the crisis there was increasing talk of global mandates for treasury services, now the focus is on regional solutions to achieve diversification and limit counterparty risk. Rather than consolidating business to a single provider, an overlay structure is used to ensure that multiple providers (across different regions) deliver the control and visibility that is essential in the current volatile world.

Counterparty – and indeed country – risk management has become increasingly important as the eurozone crisis has gathered pace. “Corporates are increasingly concerned about which countries are safe to keep cash in,”

The changing face of riskThe range of risks facing corporate treasurers in the period since the financial crisis began has not changed. However, the relative importance of those risks – such as liquidity risk, counterparty risk, interest rate risk and foreign exchange risk – has inevitably altered. And the overall importance of risk management to the future stability of corporates has never been greater than it is now.

RBS Treasury Guide 2012 to print.indd 7 04/09/2012 12:33

explains Steve Everett, global head of cash management and head of transaction services product, EMEA, RBS. “Consequently, there is greater focus on daily sweeps to locations deemed to be safe, such as the Netherlands and the UK.”

The financial crisis has also increased corporates’ eagerness to have greater control over their banking relationships as a way of managing operational risk. Increasingly, companies want to be able to follow the progress of payments or queries without having to telephone a bank contact for an update. Banks such as RBS now offer visibility into their back office processes and a wide range of self-service tools and real-time information.

Interest rate and FX risk managementWhile areas of risk management – such as counterparty risk – that were of little concern to corporate treasurers just a few years ago are now paramount, other areas, such as interest rate risk management, have been less of a priority for treasurers in recent years. “In terms of using their surplus cash, clients are not remotely focused on yield,” says Everett. “Coupled with the low rate environment (in the US, UK and Europe), interest rate risk management has not been at the top of treasurers’ risk agenda.”

While the interest rate outlook in

the UK and the US is fairly certain for the foreseeable future – the Federal Reserve has said there will be no rate rises until late 2014 – the rates environment is changing elsewhere. Rates are starting to fall in emerging markets – South Africa, China, India and Brazil have all cut rates recently – and in July the European Central Bank (ECB) also lowered rates. “The ECB cut in particular is important as it takes us close to negative interest rates,” says Everett. “It remains to be seen how clients will balance the challenges of liquidity and counterparty risk against the need to achieve a positive yield.”

In contrast, FX risk management has become increasingly important for corporate treasurers as currencies have become more volatile in recent years. All cross-currency payments and collections necessarily generate FX risk. Treasurers are seeking to execute FX for cash and settlement with greater visibility in relation to the price they will pay and the risk they will take on.

The need to manage FX risk is especially important for trade. For example, a trade transaction might have a 60-day settlement time, creating a need to manage FX risk for the day of settlement. In a stable FX environment that risk might be minimal, but because of the increased volatility of the current environment there is an increased appetite for transparency and visibility of risk. “FX risk has been relatively

RBS Treasury Guide 2012 to print.indd 8 04/09/2012 12:33

9

neglected by corporate treasurers in recent years, relative to counterparty risk, for example,” says Everett. “However, as the global economy is driven increasingly by emerging markets, FX risks are becoming more important (because emerging market currencies are generally more volatile than G8 currencies) and have to be addressed.”

One currency, the Chinese renminbi, is arousing special interest. Its gradual liberalization since 2010 and the introduction of offshore settlement in Hong Kong (with the prospect of an offshore hub in London) could prove one of the most important developments in recent decades. “If you have a supply chain in China, it can make sense to settle in renminbi rather than dollars,” says Everett. “It can be a way of reducing costs and

also of eliminating FX risk. We remain in the early stages but even in 12 months volumes will have increased significantly. It’s a way for companies to get maximum benefit from the opportunities available in China.”

Short-term investmentOnce operational needs are met – and assuming there is surplus cash available – treasurers are relentlessly focused on liquidity and cash preservation for their short-term investment cash. According to the survey published in July by the Association for Financial Professionals, which is funded by RBS and RBS Citizens, short-term corporate cash is increasingly moving towards banks, with bank deposits now accounting for 51% of short-term corporate investment balances. Findings from the survey show the highest level in its seven-year lifespan, nine percentage points above last year’s findings. As recently as 2006, the average allocation was 2%.

In the post crisis-period, the challenge facing corporate treasurers needing to invest short-term cash has grown significantly. There is a decreasing number of counterparties as the financial sector has consolidated while the credit quality of the remaining banks has largely declined. As a consequence, treasury policies set just a few years ago – requiring a minimum AA credit rating, for example – may no

Steve Everett, global head of cash management & head of transaction services product, EMEA, RBS

RBS Treasury Guide 2012 to print.indd 9 04/09/2012 12:33

longer be relevant. Ratings agencies have announced hundreds of ratings downgrades recently, including for many of the world’s largest banks.

At the same time, treasurers have had to contend with an environment in which banks have been flooded by cheap liquidity from central banks, in order to shore up the financial system and try to stimulate economic growth. As a consequence, banks simply do not need to attract additional liquidity and are therefore unwilling to offer attractive yields. The challenge facing corporate treasurers is exacerbated by the scale of the cash they currently hold: it is estimated that European corporates have as much as €1.3 trillion in cash while some US corporates have more cash than many asset managers (Apple is reported to have $100 billion).

While huge sums of cash may be a good problem to have, investing it is genuinely problematic in the current environment. As a result, preservation of principal is the most important priority. Yield is almost insignificant as a consideration: while good yields are available from Italian or Irish banks there is almost no interest from corporates in placing deposits with them. Instead, all attention is focused on a handful of banks deemed to be safe. In addition to the cheap liquidity they can access from central banks, they are consequently also awash with

corporate liquidity that they barely have to pay for.

Deposit paradoxAt the same time that some banks are swamped with corporate liquidity – and others are desperate to source it – new regulations such as the individual liquidity adequacy assessment (ILAA) in the UK and Basel III globally are requiring banks to hold larger liquidity buffers. As a consequence, banks have had to become more adept at valuing liquidity from different sources such as financial institutions and corporates.

The new rules mean that the value of a deposit varies considerably depending on the type of entity making it. The regulators’ assumption is that corporates move money less frequently than financial institutions and that their deposits are therefore more stable. Moreover, corporates are also likely to have operating accounts with the same bank providers, which reinforces this trend. Consequently, regulators consider corporates less likely to withdraw funds should a bank face problems, which means that their liquidity is valued more highly in terms of liquidity buffers.

However, the importance of corporate liquidity comes with a caveat: it is only valuable to banks if it is on deposit for greater than three months – at which point regulators deem it to be stable and therefore

RBS Treasury Guide 2012 to print.indd 10 04/09/2012 12:33

1111

it becomes eligible for preferential treatment as part of a liquidity buffer.

Unfortunately, corporates do not typically like to invest short-term cash for over three months; from an accounting perspective, deposits of less than three months can be counted as cash or cash equivalent and are therefore an enhancement to their liquidity.

One solution to this challenge developed by banks is the rolling 95-day notice account. Some companies have been able to account for such deposits as cash equivalent while banks can claim regulatory benefits from them. However, while meeting regulatory requirements, such accounts still present banks with a challenge. In the event of a crisis – such as a several-notch downgrade – a bank would still face an exodus of deposits after 95 days. In an ideal world, banks would like deposits of six months or longer.

Alternative solutionsBanks such as RBS have been working to develop alternative short-term investment solutions that meet corporates’ need for security while offering acceptable yields. One bespoke solution is the use of secured deposits. Banks necessarily have assets on their books that need funding. By using them as a pool of collateral it is possible to offer depositors greater security than on a regular deposit. Consequently,

corporates may be more willing to extend their deposits to six months, providing additional regulatory benefits for banks.

While the deposit is not rated (it carries only the rating of the bank offering the product) and the bank remains the counterparty, the corporate is enabled to access the pool of collateral should anything go wrong at the bank. Consequently, the risk is lower than it would be for an unsecured deposit. Typically, the deposit is over-collateralized based on the risk profile of the assets used: for example, deposits collateralized by government securities might be 101% collateralized, whereas those collateralized using asset-backed securities might be 110% collateralized. The only disadvantage of secured deposits is that the documentation is more onerous than for a traditional unsecured deposit.

Another alternative solution that might prove sufficiently attractive to corporates to encourage them to deposit cash for six months uses an existing derivatives position to deliver improved returns. If a corporate has a derivatives position, such as an FX or interest rate swap, that is out-of-the-money – they owe the bank on the contract – they can place a deposit (larger than the derivatives position) with that bank. The bank will be willing to pay a higher yield than usual because it already has exposure to the client.

RBS Treasury Guide 2012 to print.indd 11 04/09/2012 12:33

Managing complexityin a multi bank environmentWith the focus on managing risks, keeping costs down and ensuring transparency, treasurers are reviewing their payment factory plans, aided by new developments in standardization.

The current credit and risk focused climate means that managing risk and ensuring transparency, control and access to cash remain top priorities for treasurers. At the same time, the operating environment has changed. There is weak or negative growth across mature markets in Europe and the US. Corporates are faced with opportunities for expansion and divestment while customer segments and value chain opportunities in developing markets are becoming more important. All of these factors are contributing to enterprise-wide complexity, which the CFO or treasury function has to manage.

Treasury has responsibility for ensuring that control, transparency and risk management are achieved and that multiple banking, value chain and technology partners are coordinated. The most practical way to fulfil these objectives is through the creation of a shared service centre or payment factory model, which supports an enterprise-wide platform and operating structure.

Treasury and CFO functions increasingly demand an acceleration

of payment and collection factory projects or are at least reviewing their current set-ups. Such moves are driven by the continuing need to lower banking and technology costs, improve efficiency and transparency, and strengthen internal governance. They are facilitated by a number of standardization developments, which are enjoying widespread adoption.

At the same time, corporates are evaluating their counterparty risk, financial value chain risk and wallet share across their providers – to assess core strategic partnerships and to ensure that their organizations are positioned for the future.

“The level of technical specificity of this year’s regional request for proposals (RFP) is a relatively new phenomenon,” says Vanessa Manning, head, EMEA payments solutions, transactions services, RBS. “It’s being driven by a confluence of factors – new market developments in standardization of connectivity, messaging and processing techniques, and the need for international network and working capital expertise to guide entry into

RBS Treasury Guide 2012 to print.indd 12 04/09/2012 12:33

13

new markets and client segments.”Corporates are using the opportunity

of payment factory projects to assess their treasury centre or payment factory partner for the future. “At a time of great technological change, it’s important to understand which banks are participating in the creation and rollout of new interoperable standards; the agility of their deployment of new solutions and standards and their advisory services to support corporate implementation,” notes Manning.

The global adoption of the ISO 20022 XML standard – for transaction processing and account administration, reporting, electronic invoicing, FX and letter of credit confirmations – continues to fuel corporate RFPs. It is prompting companies to review their bank connectivity model and further accelerating the scalability of

payment factories. Corporates are also increasingly interested in banks’ involvement in collaborative initiatives, such as ISO 20022 XML-based Common Global Implementation (CGI) and electronic bank account management (eBAM).

SEPA and ISO 20022 XMLSEPA migration end dates have finally been set: national instruments will cease to exist in February 2014 (or 2016 for niche products and non-euro countries). As a result, for corporates with operations in Europe, SEPA and ISO 20022 XML provide the impetus to review current technology, bank connectivity and cash management procedures, and assess centralization and optimization opportunities.

“All of our global corporate clients with European operations are getting their feet wet with ISO 20022 XML for SEPA,” says Manning. Corporates are focusing their technology and process reviews to support a like-for-like migration – transitioning current domestic and cross-border transaction types into SEPA to ensure minimal business disruption. As corporates assess the technical implementation of SEPA in their payment factory structure, it is clear from European Payments Council (EPC) statistics that the migration journey has only recently become part of corporates’ budgeting process.

Vanessa Manning, head, EMEA payments solutions, transaction services, RBS

RBS Treasury Guide 2012 to print.indd 13 04/09/2012 12:33

The majority of corporates are not SEPA-ready, so engagement with banks and specialist technology providers is increasing for the provision of enrichment, translation and validation tools to ease the time-pressure for migration by 2014. The availability of stand-alone or bank white-labelled solutions shows the changing roles of participants within the transaction services market. In particular, the solutions on offer reflect transaction banks’ desire to be more agile in deployment of time-relevant solutions and their preference for a partnered delivery rather than in-house development.

Only when corporates have migrated to SEPA will the majority consider cen-tralizing all applicable euro transactions into a single euro account structure. Some of the key obstacles for the immediate adoption of a single euro operating account remain, including:

• local central bank reporting (scheduled for elimination in 2016 under SEPA regulation);

• resident versus non-resident specifications relating to domestic ‘specials’, such as VAT, tax and social payments. Whether these payment types can be executed in SEPA or remain ‘niche’ until 2016 has yet to be determined. It will probably be detailed further in individual country migration plans,

which each national authority has until February 2013 to disclose;

• continuation of ‘niche’ products to co-exist with SEPA in the national schemes until 2016 at latest.

Among the important factors in determining the future fit of a banking provider is the technical and advisory solutions that it brings with regard to operational efficiency, especially on-behalf-of (OBO) account structures and processing for multi-currency treasury, commercial and supply chain payments and collections.

On-behalf-of payments and collectionsThe use of OBO payments and collections – which have the potential to improve operational efficiency, cost and risk management control and liquidity visibility – has become an important requirement for next-generation payment factory RFPs. Put simply, OBO payments allow multiple entities within a group to operate from one account that is controlled by the central treasury (assuming that the fiscal and legal structure of the corporate permits such an arrangement).

While the idea is simple, implemen-tation can be complex given varying tax and legislative requirements in multiple jurisdictions and lack of con-sistency across local clearing and set-

RBS Treasury Guide 2012 to print.indd 14 04/09/2012 12:33

15

tlement mechanisms to carry through the full ultimate beneficiary. In addition, the ability of banking and enterprise resource planning (ERP) providers to pass back all relevant data for recon-ciliation can add further complexity.

OBO payments have become more popular in recent years because SEPA – given its use of ISO 20022 XML – expressly enables them. Although they were previously possible, local clearing variances rendered them more difficult to implement before SEPA. Secondly, the use of XML messaging, which is the key technical

standard underpinning SEPA, has aided the uptake of OBO transactions because it supports OBO files. It provides greater certainty and security that the full invoice, ultimate ordering and beneficiary party will successfully clear and return through the payments system for enhanced straight-through processing (STP) and straight-through reconciliation (STR) by the corporate.

Thirdly, OBO payments have grown in volume because of the natural cost and efficiency benefits that they offer.

Many companies have large numbers of bank accounts at country level. Necessarily there are fees associated with keeping accounts open, but there are also costs associated with auditing accounts and maintaining their security. Rationalizing account structures can therefore reduce cost.

Finally, the availability of tools to facilitate OBO transactions has increased significantly. Now almost all vendors have an in-house banking (IHB) type that can be added easily to existing ERP systems and treasury management systems (TMS). Such

packages make it easier to manage flows internally to support delivery and receipt of OBO information to enhance corporates’ cash conversion cycle.

Streamlining cross-border and cross-currency transaction processingAs corporates increasingly focus on SEPA migration and cost reduction, there is greater analysis of their payment and collection instrument mix. This analysis includes the ratio

“At a time of great technological change, it’s important to understand which banks are participating in the creation and

rollout of new interoperable standards; the agility of their deployment of new solutions and standards and their advisory

services to support corporate implementation”

RBS Treasury Guide 2012 to print.indd 15 04/09/2012 12:33

of manual, paper-based instruments; STP and STR ratios; the percentage of high-value transactions and the cost and time criticality of those transactions. The importance of this process of analysis has been made clear in the first wave of SEPA credit transfer migrations: the majority of corporates migrated to SEPA specifically for cross-border transactions which, while accounting for less volume, are more expensive per transaction.

Corporates’ focus on lowering cross-border, cross-currency transaction costs, the desire to reduce the number of accounts held across banking providers, coupled with the requirement for transparency for all fee and FX margin agreements, has supported the growth of OBO multi-currency account solutions. Such structures enable a corporates IHB or treasury to use its centralized IHB account to transact all treasury, commercial and supplier transactions on single and multi-currency basis, secure in the knowledge that:

• transactions are routed based on the lowest available cost via the banks’ local branch, at a domestic transaction pricing level;

• corporate-specific margins for all cross-currency transactions are applied and are transparent and auditable;

• cost and control procedures maintain multi-currency accounts at a per country/per subsidiary level (where regulation and corporate governance permit); and

• FX, interest rate, supplier and other risks are centralized and managed at treasury level.

Transparency of cost and efficiency of processing are important – not just to lower costs but to benchmark banking providers. As a result, interest in Treasury Workstation Integration Standards Team (TWIST) billing, a standard that has been adopted by ISO 20022 XML this year, has also increased.

Multi-bank and ERP collaborationA crucial issue when corporates are choosing which bank to work with for their payment factory project, is the extent of individual banks’ involvement in various collaborative initiatives aimed at improving efficiency and ease of use for corporates. The most important example of these initiatives is CGI XML, which aims to streamline and standardize corporate-to-bank connectivity and messaging so that true interoperability can result.

Most of the world’s top 50 banks and leading ERP providers have now agreed standards for ISO XML implementation and an increasing

RBS Treasury Guide 2012 to print.indd 16 04/09/2012 12:33

17

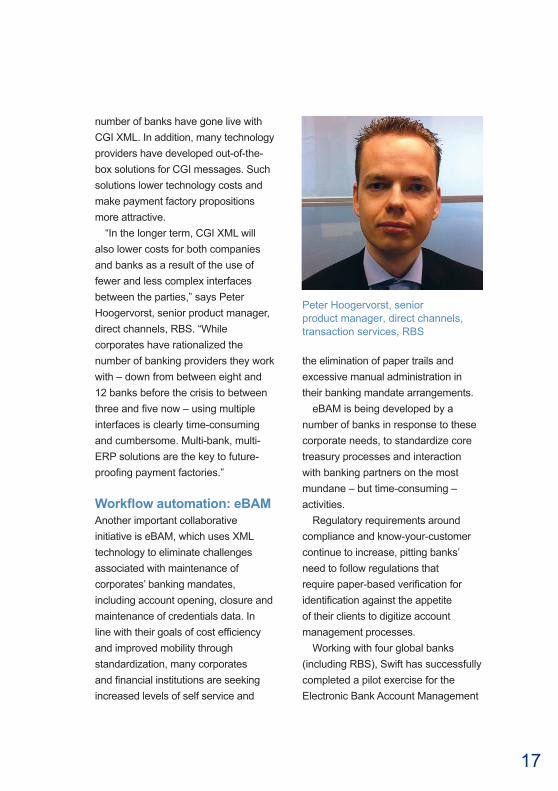

number of banks have gone live with CGI XML. In addition, many technology providers have developed out-of-the-box solutions for CGI messages. Such solutions lower technology costs and make payment factory propositions more attractive.

“In the longer term, CGI XML will also lower costs for both companies and banks as a result of the use of fewer and less complex interfaces between the parties,” says Peter Hoogervorst, senior product manager, direct channels, RBS. “While corporates have rationalized the number of banking providers they work with – down from between eight and 12 banks before the crisis to between three and five now – using multiple interfaces is clearly time-consuming and cumbersome. Multi-bank, multi-ERP solutions are the key to future-proofing payment factories.”

Workflow automation: eBAMAnother important collaborative initiative is eBAM, which uses XML technology to eliminate challenges associated with maintenance of corporates’ banking mandates, including account opening, closure and maintenance of credentials data. In line with their goals of cost efficiency and improved mobility through standardization, many corporates and financial institutions are seeking increased levels of self service and

the elimination of paper trails and excessive manual administration in their banking mandate arrangements.

eBAM is being developed by a number of banks in response to these corporate needs, to standardize core treasury processes and interaction with banking partners on the most mundane – but time-consuming – activities.

Regulatory requirements around compliance and know-your-customer continue to increase, pitting banks’ need to follow regulations that require paper-based verification for identification against the appetite of their clients to digitize account management processes.

Working with four global banks (including RBS), Swift has successfully completed a pilot exercise for the Electronic Bank Account Management

Peter Hoogervorst, senior product manager, direct channels, transaction services, RBS

RBS Treasury Guide 2012 to print.indd 17 04/09/2012 12:33

Central Utility (E-CU). Significant milestones were achieved to support the Swift eBAM product development life cycle, while progress was made on concepts such as use and population of a central validation database. They show great promise towards the development of a full production version of the utility.

The key is to make the utility into a working model. The ease of use for corporates is superb: the utility can offer easy access to eBAM messaging for corporates across the world. Banks and Swift now need to determine how to fund E-CU – significant investment will be required by the participating banks to develop and commercialise a go-to-market model.

At the same time as this multi-bank model is developed, banks need to continue to invest in their proprietary account management solutions in order to meet clients’ expectations. RBS, for example, has enhanced its proprietary banking tools to include intelligent e-binders, self-service real-time enquiries and investigations. “Corporates need to check that their bank is continuing to seek ways to make it accessible and intuitive to change their account parameters online for account maintenance-type activities, in addition to replicating authorization, legal or fiscal changes into their bank environment,” says Manning.

Workflow automation: electronic invoicing Electronic or e-invoicing is as important a workflow automation tool as eBAM for corporates. Ease of adoption has increased as the market has migrated to SEPA XML. In Finland, which successfully completed its migration to the SEPA in 2010, e-invoicing has been rapidly and easily adopted. The goal of the European Commission through its Digital Agenda Framework is to deliver a regulatory framework to support a pan-European standardized solution (based on ISO 20022 XML) to ensure a common EU market for commercial transaction processing and interactions. While all market participants see the value of e-invoicing (as shown by Swift’s new suite of e-invoicing and supply chain solutions) the pace at which corporates and banks can absorb and translate these multiple developments into their operating environments is relatively slow.

Multi-banked sophisticated corporate clients do not necessarily expect their banks to offer integrated e-invoicing solutions now, given that industry-based vendors have vast global supply chains and mass on-boarding models already in place. However once corporates are familiar with ISO 20022 XML as a result of SEPA, the treasury will be empowered to centralize and standardize procurement processes in a similar way so that e-invoicing can be implemented.

RBS Treasury Guide 2012 to print.indd 18 04/09/2012 12:33

19

Security and authorizationClient RFPs for next-generation payment factories in Europe have security and authorisation concerns as a top priority. Chief among developments in this area is a Swift initiative that could have significant implications for account management in the long term: 3SKey.

Many users are familiar with the use of proprietary keys or tokens to access an online portal securely. Recent technological developments have enabled the production of multi-bank token solutions. Swift, as an independent trustworthy body, administers the 3SKey solution: tokens would be transmitted to customers by banks, as before, but would be activated by Swift.

While 3SKey allows access to multiple proprietary bank portals, its real value is as a digital signature. Currently, digital signatures are bank specific. The digital signature used in 3SKey is necessarily bank-agnostic. So, provided a bank is signed up to the initiative, the token can be used to facilitate digital flow in eBAM and as a digital signature on payment files, which must be legally authorized, for multiple banks.

In the past year, 3SKey has expanded outside of its strongest market in France as increasing numbers of banks have pledged to support it. “3SKey has the potential to meet local legal requirements and

corporates’ own strict rules while still offering flexibility to customers,” says Hoogervorst. “It will allow some corporates to leapfrog their peers.” 3SKey could also have a role to play in enabling the kind of added-value functionality of a proprietary portal that many users assume they have to sacrifice to achieve bank-agnostic solutions.

Decision and execution support: advanced analytics Increasingly, corporate treasurers want enriched decision-making support tools that deliver advanced customizable analytics and core counterparty, FX and interest rate risk transparency through intuitive, user-friendly dashboards. There is an emerging trend towards risk-based exception reporting for immediate cost, margin and liquidity information rather than detailed complete transaction reports. The use of such reporting facilitates the use of treasury metrics, drives down bank fees and margins; and provides better insight on supplier or client credit quality. It also offers improved accuracy of liquidity positioning and forecasting.

Treasurers’ demand for increased, targeted information (accessible from a tablet or smart phone) is being supported not just by banks but also by Swift and payment factory technology providers. Such providers are increasingly offering greater

RBS Treasury Guide 2012 to print.indd 19 04/09/2012 12:33

functionality and analytics that take into account total financial exposure. By conveniently aggregating data in this way, payment factory technology providers in particular are helping to solve a number of multi-bank related challenges for corporates.

More generally, mobile analytics and contingency authorization options are an important consideration for corporate treasurers. Treasurers are eager to gain access to new ways of receiving payments. However, mobile payments still have security and legal issues to overcome and most countries have yet to develop a legislative and financial framework to support mobile payment clearing and settlement in real time.

Changing market participants and business modelsThe range of participants seeking to serve corporates is changing and, inevitably, so is the relationship between banks and corporates. Increasingly, providers of cloud-based solutions (such as SAP) are gaining ground with value-added services such as translation or reconciliation, so that corporates no longer have to manage such tasks themselves. Unsurprisingly, existing providers such as Swift are repositioning themselves to service this market.

The arrival of new entrants is

beneficial for corporates. Often, they are more familiar with ERP providers than they might be with Swift, for example, and therefore moving to an ERP-provided cloud-based solution could be easier and more natural. Banks are not excluded from this new relationship dynamic, and it is important that companies ask their bank providers about how they can assist in corporates’ plans in this area.

Getting supportEstablishing a new payment factory or re-assessing a current set-up is a project that will take over a year from inception to delivery. Corporates need a strong understanding of the fiscal, legal and regulatory environments in which they operate, and how these will evolve given upcoming regulatory and market standardization developments.

Combined with inevitable enterprise-wide politics, variance in enterprise objectives, cost constraints and expertise levels, it is clear that corporates should work with their network bank provider if they want to meet their objectives in a cost effective and timely way. Only through such a consultative relationship can the effective design and deployment of a cost and control focused payment factory solution, which supports multi-bank portability, be achieved, enabling treasury and finance to focus more on value-added activities.

RBS Treasury Guide 2012 to print.indd 20 04/09/2012 12:33

21

Staying agnosticCorporates want connectivity standards that will work with any bank, enabling them to move their cash flows from one institution to another quickly and easily.

Changes in the world of bank-to-corporate connectivity take time to emerge but when they do they can rapidly gain momentum. Concern about counterparty risk has accelerated the trend towards bank-agnostic solutions as corporates and financial institutions seek ways to manage risks and streamline their operations. Corporates want a single standard that they can use with all their bank providers and have little appetite for bank-specific implementations.

“Corporates’ principal goal is to be able to move flows more easily should they need to eliminate unwanted exposure,” says Etienne Bernard, head of transaction services origination, EMEA, RBS. “The way to meet that need is through interoperability and common connectivity and security. The development of a common security tool such as 3SKey and the creation of ISO XML standards are making that goal – and the transparency and simplification it brings with it – a reality for many clients.”

Swift has enjoyed a rapid expansion of corporate users, highlighting the

growing importance of common forms of connectivity. Having been established as a bank messaging system, Swift is evolving into a financial infrastructure provider for both corporates and banks. Swift’s ambitious goal of 5,000 corporate users by 2015 – from around 900 at the end of 2011 – indicates the expectations of growth.

The drive towards bank-agnostic standards is often accelerated by corporate acquisitions or reorganizations. Such change at

“Supplier finance programmes are

changing the relationship between banks and corporates

as they have to increase connectivity to reach

a larger corporate community”

RBS Treasury Guide 2012 to print.indd 21 04/09/2012 12:33

companies is often accompanied by a renewed focus on what banks the company works with and how it connects to them. Invariably, in such circumstances, a bank-agnostic approach is adopted to improve efficiency.

Indeed, while bank-agnostic solutions have a major role to play in reducing counterparty and operational risk – because of the ability to switch providers if necessary – lowering costs is also a corporate focus. Both costs of infrastructure and costs per transaction can be lowered by using bank-agnostic solutions. Anecdotal evidence suggest that total cost per transaction can be lowered by as much as 80%.

Cost benefits are possible because bank-agnostic solutions can increase processing efficiency – through higher rates of straight-through processing – and also improve how payments are sent to reduce clearing costs. For example, transaction volumes can be split to take maximum advantage of banks’ networks and of their direct cash management connections to the corporate’s suppliers or customers. The use of SEPA instruments is also expected to be an important tool for cost reduction in the future.

New horizonsIn recent years, corporates have increasingly looked to engage with their suppliers to secure their supply

chain and support companies on which they are strategically dependent. The use of supply chain finance programmes has increased markedly in the post-financial crisis period as corporates have recognized the difficult financing conditions for the small and medium-sized companies that make up their supply chains.

Connectivity in such instances is not just a matter of corporate-to-bank links but of links between companies and their suppliers and even with their customers. The need to support suppliers is not just driven by a shortage of supplier credit but by a broader change in trade flows. The long-term trend is towards open account, which necessarily puts greater pressure on suppliers. Tools such as discounting are needed to enable that model to work in the

Etienne Bernard, head of transaction service origination, EMEA, RBS

RBS Treasury Guide 2012 to print.indd 22 04/09/2012 12:33

2323

current environment and they require connectivity.

Many banks have adapted their own proprietary platforms to become multi-bank capable. “Supplier finance programmes are changing the relationship between banks and corporates as they have to increase connectivity to reach a larger corporate community,” says Bernard.

Meanwhile, Swift’s Bank Payment Obligation (BPO), supported by the trade services utility (TSU), is also facilitating the trend of moving towards more electronic trade exchanges. The TSU is a centralized matching and workflow engine providing interbank electronic exchange of corporate purchase agreements or any related document such as commercial invoices. It uses a common connection for cash management and open account-type transactions. It significantly cuts down the transaction lifecycle and improves working capital management, while delivering security. The BPO TSU remains at a relatively early stage but for larger, more sophisticated corporates it could play an important role as a cash and trade bank-agnostic solution.

“In trade, as with cash, the flow is the commodity and the connectivity has to be efficient and secure in order to achieve corporates’ objectives,” says Bernard. “The role of banks is increasingly to add value and enhance

efficiency: that may be by developing scorecards using information associated with flows to help corporate treasuries detect scope for further improvements, or by simplifying documentation management – with uses such as electronic bank account management or by upgrading customer service allowing customers to access banks’ back-end transaction engines.”

Case study: SAPHeadquartered in Walldorf, Germany, SAP is the world’s leading provider of enterprise application software, business analytics and enterprise mobility – supporting more than 183,000 customers through 55,000 employees worldwide.

Over the past 10 years RBS has forged a close working relationship with SAP, acting as a core transaction services and hedging adviser. The bank’s role has grown as the relationship has developed and today RBS is a member of SAP’s leading group of banks that provide financial services and advice across a broad range of banking products. RBS currently runs commercial accounts for SAP across Europe, North America and the Middle East as well as settling treasury payments across eight countries. In addition RBS also operates a euro cross-border cash pool, enabling SAP to manage liquidity

RBS Treasury Guide 2012 to print.indd 23 04/09/2012 12:33

efficiently and maximize use of its working capital.

While integrating the recently acquired Sybase Corporation into SAP’s enterprise resource planning (ERP) system, SAP wanted to further improve its treasury efficiency. It decided to implement the new XML CGI formats for credit transfer and payment status, triggered by SAP’s

application, SAP Bank Communication Management for payment processes.

The new technology ensures that SAP’s overall cash management infrastructure is more flexible - while also highlighting its technical ability. The key challenge was to introduce the new formats across an established payment factory that handles thousands of daily payments for 55 subsidiaries across more than 45 countries, using the SAP standard solutions for the entire process.

Seen as an important strategic technology for SAP’s future growth, the new CGI solution ensures greater efficiencies and enables the company to operate at the lowest cost possible. RBS’s pivotal role in ensuring the success of the European roll-out has created a solid platform for full global implementation.

“ Corporates’ principal goal is to be able to move flows more easily should they need to eliminate unwanted exposure”

RBS Treasury Guide 2012 to print.indd 24 04/09/2012 12:33

25

Companies in the modern globalized environment exist to add value, through the provision of raw materials, through manufacturing processes or through the provision of services. It is a mistake to think any company exists in a vacuum – all companies are linked and those links continue to become more complex.

Traditionally, the banking industry has tended to consider suppliers, manufacturers, service providers and end customers independently. However, as working capital management has become more important to companies, the inefficiencies inherent in this approach have become more obvious.

“For example, in an interaction

between a supplier of components and a manufacturer such as an auto company, the stronger party – which might be the auto firm – can push the pressure of financing and delivery on to the supplier,” explains Dermot Canavan, regional trade product head EMEA and trade CAO, RBS. The auto company might seek to pay the supplier after 60 days rather than the current 15 days. As the supplier depends strategically on the buyer, it has to accept these terms.

However, the extension of the terms by an additional 45 days creates inefficiency in the value chain. The buyer is effectively borrowing money from its suppliers through the extension of terms. The inefficiency occurs because the cost of funds for the supplier is higher than the cost of funds to the buyer. This increase in supplier costs is likely to be passed back to the buyer in higher prices for materials and, ultimately, that higher cost will be passed on to the end consumer.

Connecting the value chainA holistic approach to supply chain financing provides advantages and reduces inefficiencies for both buyers and suppliers.

Dermot Canavan - regional trade product head EMEA & trade CAO, RBS

RBS Treasury Guide 2012 to print.indd 25 04/09/2012 12:33

A holistic viewIn the past, banks looked separately at funding for suppliers and buyers. Now they look at the entire value chain rather than at individual custom-ers. By taking a holistic view of lend-ing across the value chain, inefficien-cies can be spotted and eliminated. In the example above, the auto firm is rated higher than the supplier and has a lower funding cost. The solution? To provide funding to the supplier but at a funding cost that reflects the rating of the buyer.

This solution provides value for both parties. The supplier might have a borrowing cost of 6% (compared to the buyer’s funding cost of just 3%) and get paid after 30 days. The buyer might want to extend its payment terms from 30 days to 60 days. Rather than paying 6% for that 60 day funding, the supplier – using supplier finance – can fund itself at 3%. Consequently, there is no additional financial disadvantage to the supplier of extending terms. While the invoice now states terms of 60 days, the bank can discount it to the supplier so it can receive payment on day zero for just 3%.

Win-win-winFor suppliers, there are multiple benefits from a supply chain finance solution. Suppliers’ credit lines are not used, which releases pressure on

their balance sheets. The solution also strengthens the strategic relationship between buyer and supplier, providing greater security. Finally, the supplier is able to agree to extended terms from the buyer at no additional cost to itself and gets a lower cost of funds than would normally be achievable.

For the buyer, the benefits are straightforward. It can extend payment terms and improve its liquidity position. Moreover, in a well-structured programme the payment is classified as a trade payable rather than a bank or capital markets debt, which helps to improve its balance sheet.

For the bank provider, supply chain finance is advantageous because it creates the opportunity for additional business. Moreover, the risk associated with lending is reduced because by establishing a

Anil Walia - head of trade and supply chain advisory, EMEA & UK, RBS

RBS Treasury Guide 2012 to print.indd 26 04/09/2012 12:33

27

supplier finance programme – with self-liquidating transactions – there is an increased incentive for the buyer to pay its invoices promptly and there is a much lower risk of payment not being made at all. “The buyer, supplier and bank all win,” notes Anil Walia, head of trade and supply chain advisory, EMEA and UK, RBS.

Supplier finance can be extended up and down the value chain without changing the relationship between parties. The only change that takes place is a greater willingness between parties to cooperate to add value. “Historically, there was little concern among buyers about where suppliers’ liquidity comes from as long as their terms were improved,” says Canavan. “Now there is recognition of the competitive benefits of engaging with suppliers through supply chain finance.”

Benefiting the entire companyIn the past, many companies adopted a silo approach to purchasing, finance and sales, with little consideration of the value chain within the company. For example, the key performance indicators (KPIs) of functions within a company may have been starkly different: the finance function may have been focused on liquidity and balance sheet management while purchasing focused on gross profit.

In practice, the misalignment of different functions’ KPIs can have a considerable negative impact. Many invoices have terms of 45 days but offer payment at 15 days with a 2% discount: a supplier that wants payment at 15 days is effectively giving up 24% a year. Given the higher cost of funding to a supplier (relative to the buyer) this is extremely inefficient. In addition, these higher costs are likely to be passed on to the buyer. The purchasing manager is happy to pay the supplier early because the gross profit target has been achieved. However, for the finance function, early repayment adversely affects the balance sheet

target: its preference would be to pay later and retain the additional 30 days’ liquidity.

Traditionally, these contradictions in KPI targets were difficult to reconcile. A more efficient way to address this situation would be to recognize that if a supplier is willing to absorb costs

“For the bank provider, supply chain finance is

advantageous because it creates the opportunity for additional business”

RBS Treasury Guide 2012 to print.indd 27 04/09/2012 12:33

of 24% a year, a better real cost for those supplies is achievable (improving gross profit and helping purchasing achieve its KPI). Furthermore, supply chain finance makes it possible to deliver liquidity to those suppliers that need it at an attractive cost. “A bank can discount invoices at a cost of just 3% a year compared to the 24% the supplier was paying previously or the 7-10%, maybe, payable through the supplier’s own lines of credit,” explains Canavan. “That differential between rates facilitates the renegotiation of the commercial contract, allowing the buyer to reduce its purchasing cost.” This way both the finance and

purchasing departments are able to achieve their performance targets.

Combating the financial crisisJust eight years ago, many of the ideas that underpin supplier finance were just that – ideas. Now many thousands of companies – both buyers and suppliers – have benefited from supply chain finance: there is conclusive proof that it works.

Indeed, supply chain finance has proved especially beneficial in the turbulent period since 2008 when many small companies have found it difficult to get liquidity from their bank providers. Inevitably, some companies have faced bankruptcy and been forced to seek protection from the courts. By using discounted receivables as part of a supplier finance solution – which can be kept out of any bankruptcy proceedings – those companies were able to continue to operate until restructuring could occur.

“ By taking a holistic view of lending across the value chain, inefficiencies can be spotted and eliminated”

RBS Treasury Guide 2012 to print.indd 28 04/09/2012 12:33

29

Treasury services and cash management are changing. The tough economic environment has increased corporates’ focus on costs and liquidity, while unprecedented regulatory change is prompting a reassessment of how banks operate in transaction banking. These powerful forces are helping to change the mindset of both corporates and banks and are resulting in new approaches that address today’s challenging conditions.

From a technological perspective, standards such as ISO 20022 XML are essential in helping banks and corporates to achieve their goals. ISO 20022 XML is spreading beyond cash management and into broader treasury functions, including trade, electronic invoicing, procurement and shared service centre functionality. As a result, corporates are able to reap the benefits of such initiatives faster and more efficiently than ever before.

At the same time, the concept of interoperability has become firmly embedded in the mindset of transaction banks. Collaborative

initiatives are at the heart of new ideas such as common security standard 3SKey, which enables bank-agnostic digital signatures, common global implementation (CGI) XML, which aims to streamline corporate-to-bank connectivity, and electronic bank account management (eBAM), which simplifies bank account management.

“The adoption of these transformational themes has three main drivers,” explains Neal Livingston, global head of transaction services origination, at RBS. The first is the economic environment, which – combined with greater regulatory pressure – is making banks focus on the sustainability of their business models and work harder to find cost and efficiency savings.

Simultaneously, the precarious economic environment is spurring the same search for efficiency among corporates. “Of course, improving efficiency related to working capital management has always been essential for treasurers, but the acuteness of the issue has been

All changePowerful forces are changing the treasury and cash management business, forcing banks to innovate and corporates to streamline their ways of doing business.

RBS Treasury Guide 2012 to print.indd 29 04/09/2012 12:33

increased by the challenges facing businesses and the broader global financial system and economy,” says Livingston. “It is absolutely critical for treasurers to strip out inefficiency and build in year-on-year productivity gains.”

The second driver that is accelerating the transformation of treasury services and cash management is the increased importance of liquidity to companies and elevated concerns about counterparty risk. While counterparty risk became a crucial consideration in the wake of the collapse of Lehman Brothers and the onset of the financial crisis in 2008, the eurozone crisis has reinforced its significance – many local and regional banks in the region have huge exposures to the sovereign debt of countries perceived to be in jeopardy.

“The outflows of liquidity we have seen from the eurozone – and the concerns that such movements of cash highlight about counterparty risk – reflect the changed way in which treasurers and companies look at transaction services, where their deposits are placed and which banks form their bank group,” says Livingston. “Counterparty risk and liquidity management are now board-level concerns – they’re essential to company survival.”

The third driver accelerating the uptake of new ideas in treasury services is a renewed focus by banks on the effectiveness of their networks. Many banks have historically had large networks that were poorly connected: they failed to leverage their scale to serve clients in the best way possible. Now regulatory and competitive pressures are spurring a reassessment of the value of banks’ networks in terms of their client value proposition and a consequent right-sizing of banks’ geographic footprint. A focus on new thinking to maximize the benefits to customers is an integral part of this reassessment process.

Accelerating changeThe combined impact of the turbulent economic environment, the increased importance of liquidity and counterparty risk management and a reassessment by banks of their network and client

Neal Livingston, global head of transaction services origination, RBS

RBS Treasury Guide 2012 to print.indd 30 04/09/2012 12:33

31

proposition, is having a number of broader knock-on impacts.

The first impact is an acceleration of the pace of change in treasury services and cash management at banks. Numerous initiatives are under way at banks, with huge transformational implications. Almost all transaction banks have conducted strategy reviews that have led to reform within the business and realignment with other parts of the banking group. For instance, at RBS the former Global Transaction Services and Global Banking and Markets Divisions have been merged to create Markets and International Banking. This new division, with a new management team and risk committee, includes RBS Transactions Services, apart from RBS’s UK and US domestic franchises and brings a new approach to serving clients.

“By bringing together relationship managers and product experts – across trade, liquidity, FX and other areas – RBS is able to achieve greater efficiency and also deliver a more effective service to clients,” says Livingston. “There is no duplication of effort – or contact – between RBS and clients. They get a streamlined offering.”

A second related impact from the various forces accelerating the pace of change in cash management is a fresh approach by both treasurers and banks to working capital. “Whereas

in the past there was a tendency for credit, payments or supply chain finance to be considered separately by companies – and addressed separately by banks – the economic backdrop, and the centrality of liquidity to companies, means these themes have been merged,” says Livingston. Consequently, conversations between banks and clients now tend to be more joined-up in nature, with corporates considering working capital in a holistic way and banks looking across the value chain and product range rather than taking a silo approach.

A third impact on banks of the new environment is the need for banks to be more precise about the costs to enter – or remain – in any given geographical or product market. The tough economic environment has put pressure on banks’ revenues at a time when regulators are requiring them to hold more capital. Meanwhile, the huge weight of new regulatory requirements – from Dodd-Frank in the US to SEPA in Europe – has increased costs. Moreover, despite the best efforts of regulators, many new regulations are being introduced in different forms in different countries – increasing costs further for organizations that work in multiple countries.

One way in which banks are working to lower costs while still delivering new solutions to clients is through greater collaboration across the

RBS Treasury Guide 2012 to print.indd 31 04/09/2012 12:33

banking industry. Transaction banks will continue to compete fiercely for corporates’ business – as they should do – but there is a broad recognition that the models of the past are no longer viable. For example, in 2009, Swift launched Innotribe as an initiative to enable collaborative innovation in financial services. Participants have already put funding in place for an incubator for collaborative development projects, to enable them to be brought to market for commercial success and they have also launched a start-up competition to offer funding to companies and bring them into the financial services ecosystem.

Finally, the fourth impact resulting from the three transformational drivers is the need for banks to improve their agility. Agility does not necessarily mean being the first to implement new technologies or offer new products (although that can contribute to a bank’s agility). Instead, it is about the speed with which they can assess and address clients’ needs and the effectiveness of the solutions they offer to those clients. Agility – in the sense of bringing the relevant capability to clients in the most effective way – is a crucial source of competitive advantage for banks.

Still hurdles to overcomeDespite the power of various forces reshaping the approaches taken by

corporates and banks to treasury services and cash management, the adoption of new standards that foster collaboration and lower costs will – inevitably – continue to face hurdles.

For example, while the EU is committed to e-services and e-invoicing, the framework for such initiatives remains unclear. Similarly, there is little consensus about how to design new requirements so that industries that have already invested heavily in e-services, such as electronics, where some leading companies have an EDIFACT-based supply chain, are not forced to migrate to a new system. As a result, the move to an EU-wide e-services standard is likely to take a course similar to SEPA, with long discussions in the industry and an implementation timetable measured in decades rather than years.

Nevertheless, despite the all-too-familiar problems encountered by those in treasury services and cash management in trying to promote change, it is clear that a new attitude has taken hold at both banks and corporates. The tough economic climate requires ingenuity. Moreover, the introduction of Faster Payments in the UK – and to a lesser extent the SEPA Credit Transfer in Europe – have shown that a combination of the right regulations and the right technology can quickly deliver critical mass and savings for clients.

RBS Treasury Guide 2012 to print.indd 32 04/09/2012 12:33

No representation, warranty, or assurance of any kind, express or implied, is made as to the accuracy or completeness of the information contained in this document and RBS accepts no obligation to any recipient to update or correct any information contained herein. The information in this document is published for information purposes only. Views expressed herein are not intended to be and should not be viewed as advice or as a recommendation. You should take independent advice on issues that are of concern to you. This document does not purport to be all inclusive or constitute any form of recommendation and is not to be taken as a substitute for the recipient exercising his own judgement and seeking his own advice. This document is for your private information only and does not constitute an analysis of all potentially material issues nor does it constitute an offer to buy or sell any investment. Prior to entering into any transaction, you should consider the relevance of the information contained herein to your decision given your own investment objectives, experience, financial and operational resources and any other relevant circumstances. Neither RBS nor other persons shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary damages, including lost profits arising in any way from the information contained in this communication.

The products and services described in this document may be provided by The Royal Bank of Scotland plc, The Royal Bank of Scotland N.V. or both.

The Royal Bank of Scotland plc. Registered in Scotland No. 90312. Registered Office: 36 St Andrew Square, Edinburgh EH2 2YB. The Royal Bank of Scotland plc is authorised and regulated in the United Kingdom by the Financial Services Authority. The Royal Bank of Scotland N.V. is authorised by De Nederlandsche Bank and regulated by the Autoriteit Financiele Markten (AFM) for the conduct of business in the Netherlands.

The Royal Bank of Scotland plc is in certain jurisdictions an authorised agent of The Royal Bank of Scotland N.V. and The Royal Bank of Scotland N.V. is in certain jurisdictions an authorised agent of The Royal Bank of Scotland plc.

Copyright 2012 RBS. All rights reserved. This communication is for the use of intended recipients only and the contents may not be reproduced, redistributed, or copied in whole or in part for any purpose without RBS’s prior express consent.

RBS Treasury Guide 2012 to print.indd 33 04/09/2012 12:33

RBS Treasury Guide 2012 to print.indd 34 04/09/2012 12:33