Embed Size (px)

Citation preview

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 1/48

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 2/48

PARTICIPANTS

� Nitin Joisor (38)

� Arun Kamat (40)

� Ravindra Korde(06).� Pratik Chheda (02).

� Shreya Vaidya(50).

� Biju kr (20).

� Deepak Sharma(24).

� Manu Sadashivan (22)

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 3/48

AGENDA

1. WHY RATIO ANALYSIS ??????

2. What is Ratio Analysis.

3. Ratio and its calculation.

4.Conclusion based on the calculations.

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 4/48

WHY & WHAT ?????????????

????????????????????

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 5/48

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 6/48

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 7/48

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 8/48

COMPLEXITY Jargons

LARGE ,SCARY ,MISLEADING,BEWILDERING NUMBERS

Eg. In 000 or millions / billions and so on..

Highly intimidating

TOO much to read , understand and

finally to decide

upon.

LOOKING AT ONE REPORT DOESNOT TELL THE WHOLE

STORY

PROBLEMS / ISSUES

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 9/48

SOLUTION:

However, through financial ratio analysis, you will be able to

work with these numbers in an organized fashion.

While earnings are important, they don't tell the whole story.

When it comes to investing, analyzing financial statement

information (also known as quantitative analysis), is one of, if not the most important element in the fundamental analysis

process.

Easy to understand and to evaluate

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 10/48

EASY investment evaluators.

Quick investment decision

making.Helps Mgmnt, Investors

:::::::::::::::::::::::::::::::::CONCLUSION : :::::::::::::::::::::::::::::::::::::::::::::::::::

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 11/48

WHAT IS

????????.

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 12/48

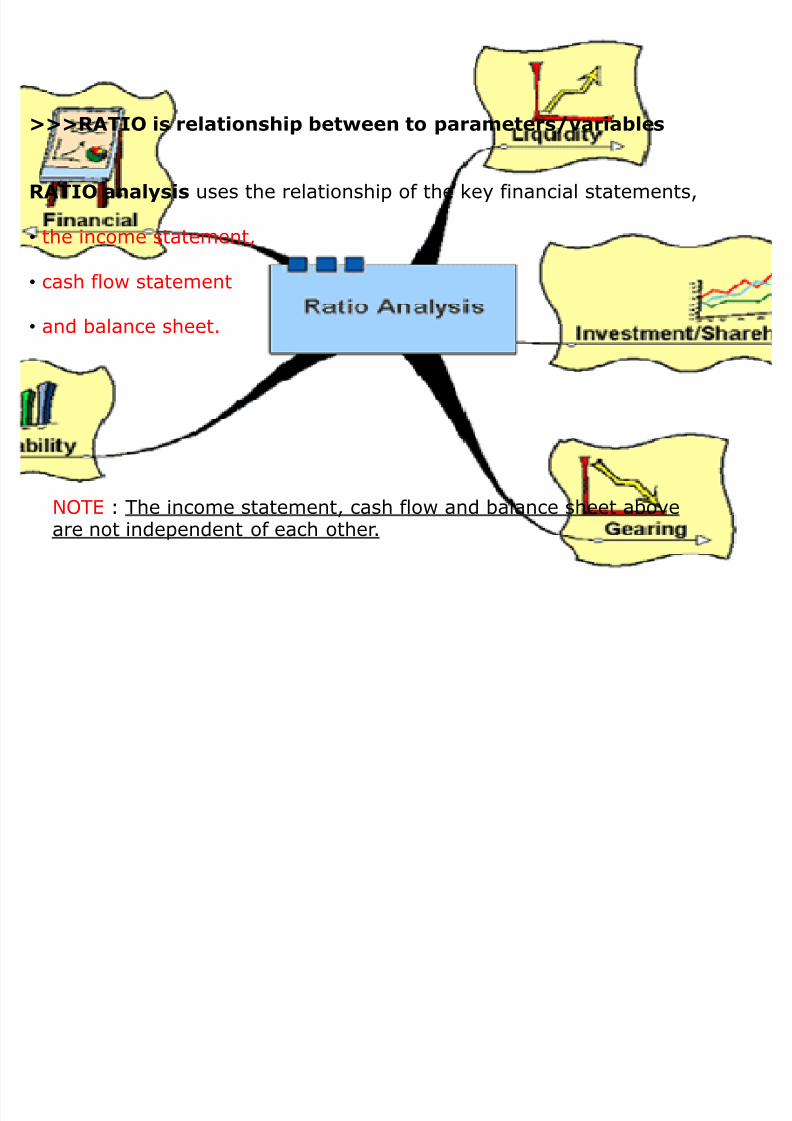

>>>RATIO is relationship between to parameters/variables

RATIO analysis uses the relationship of the key financial statements,

� the income statement,

� cash flow statement

� and balance sheet.

NOTE : The income statement, cash flow and balance sheet aboveare not independent of each other.

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 13/48

WHAT ARE 3 FINANCIAL STATEMENTS????????????????????

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 14/48

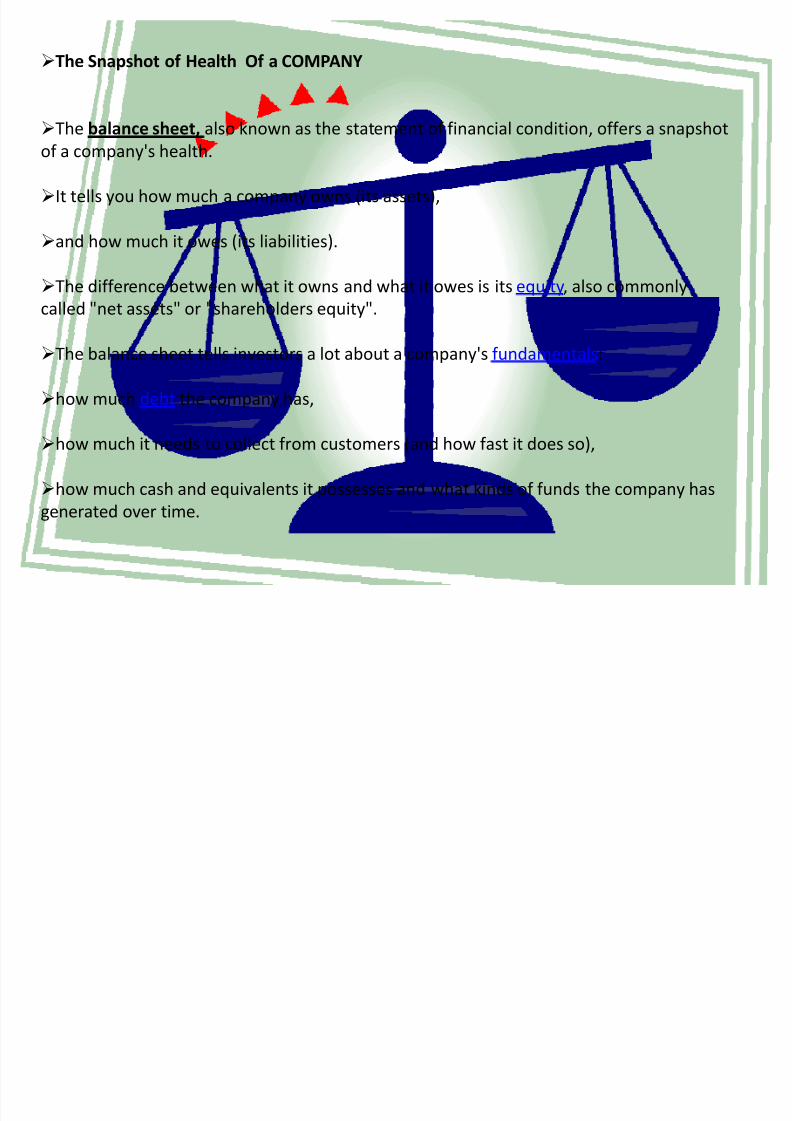

The Snapshot of Health Of a COMPANY

The balance sheet, also known as the statement of financial condition, offers a snapshot

of a company's health.

It tells you how much a company owns (its assets),

and how much it owes (its liabilities).

The difference between what it owns and what it owes is its equity, also commonly

called "net assets" or "shareholders equity".

The balance sheet tells investors a lot about a company's fundamentals:

how much debt the company has,

how much it needs to collect from customers (and how fast it does so),

how much cash and equivalents it possesses and what kinds of funds the company has

generated over time.

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 15/48

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 16/48

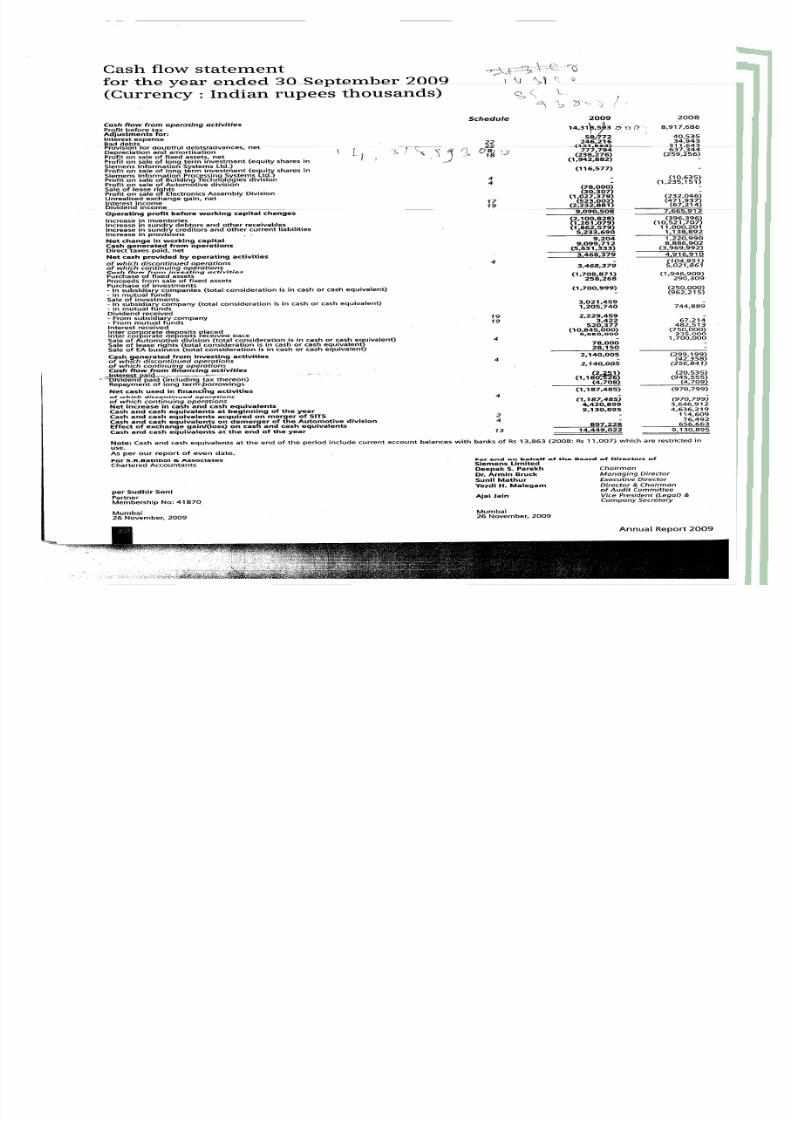

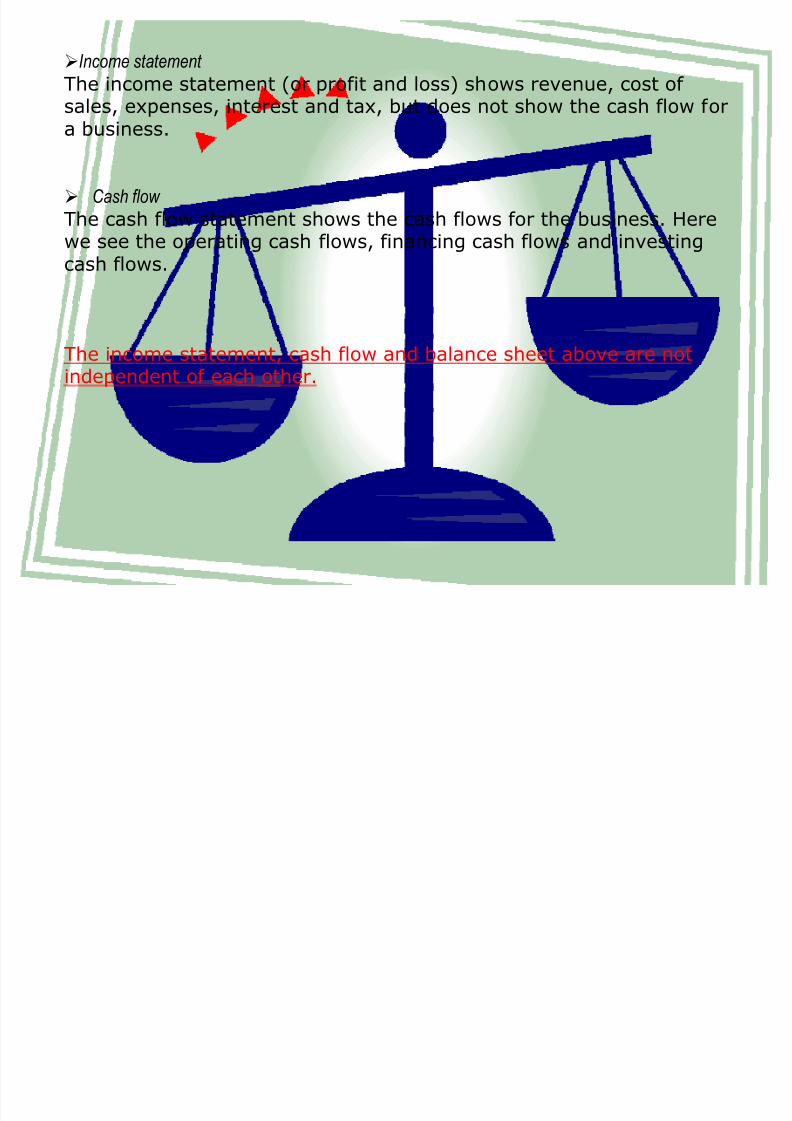

Income statement

The income statement (or profit and loss) shows revenue, cost of sales, expenses, interest and tax, but does not show the cash flow fora business.

C ash flow

The cash flow statement shows the cash flows for the business. Herewe see the operating cash flows, financing cash flows and investingcash flows.

The income statement, cash flow and balance sheet above are notindependent of each other.

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 17/48

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 18/48

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 19/48

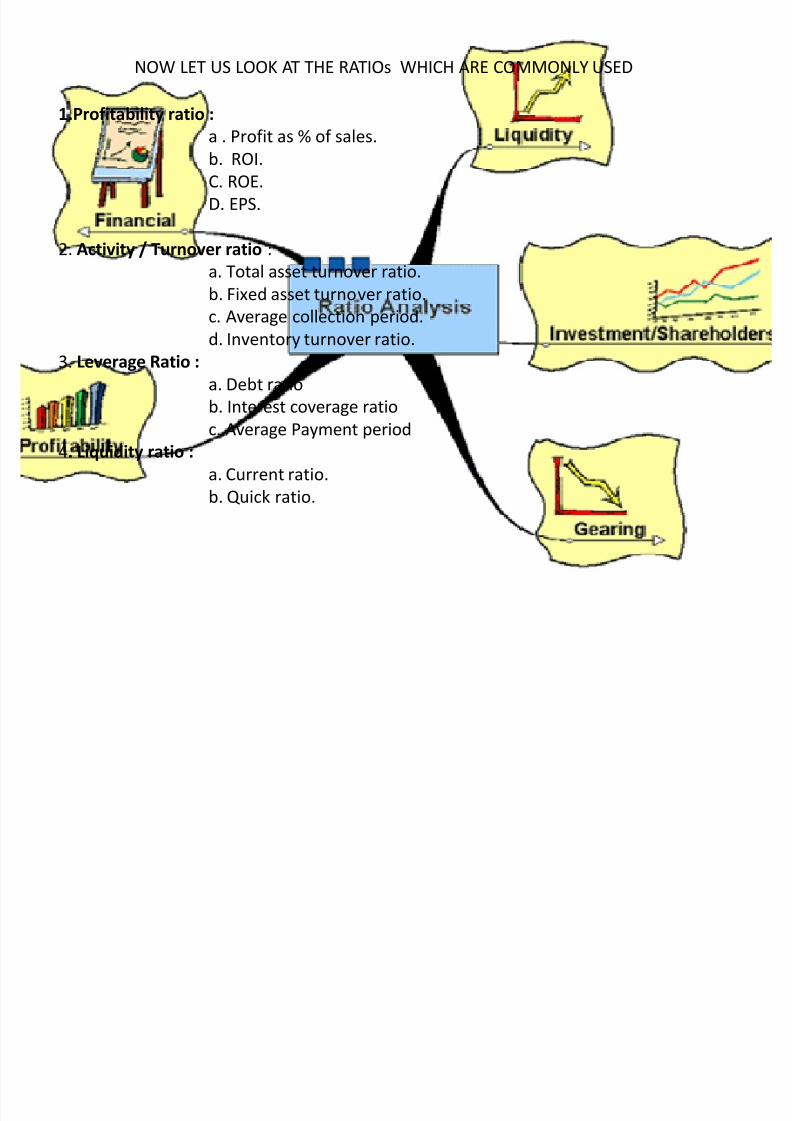

NOW LET US LOOK AT THE RATIOs WHICH ARE COMMONLY USED

1.Profitability ratio :

a . Profit as % of sales.b. ROI.

C. ROE.

D. EPS.

2. Activity / Turnover ratio :

a. Total asset turnover ratio.b. Fixed asset turnover ratio.

c. Average collection period.

d. Inventory turnover ratio.

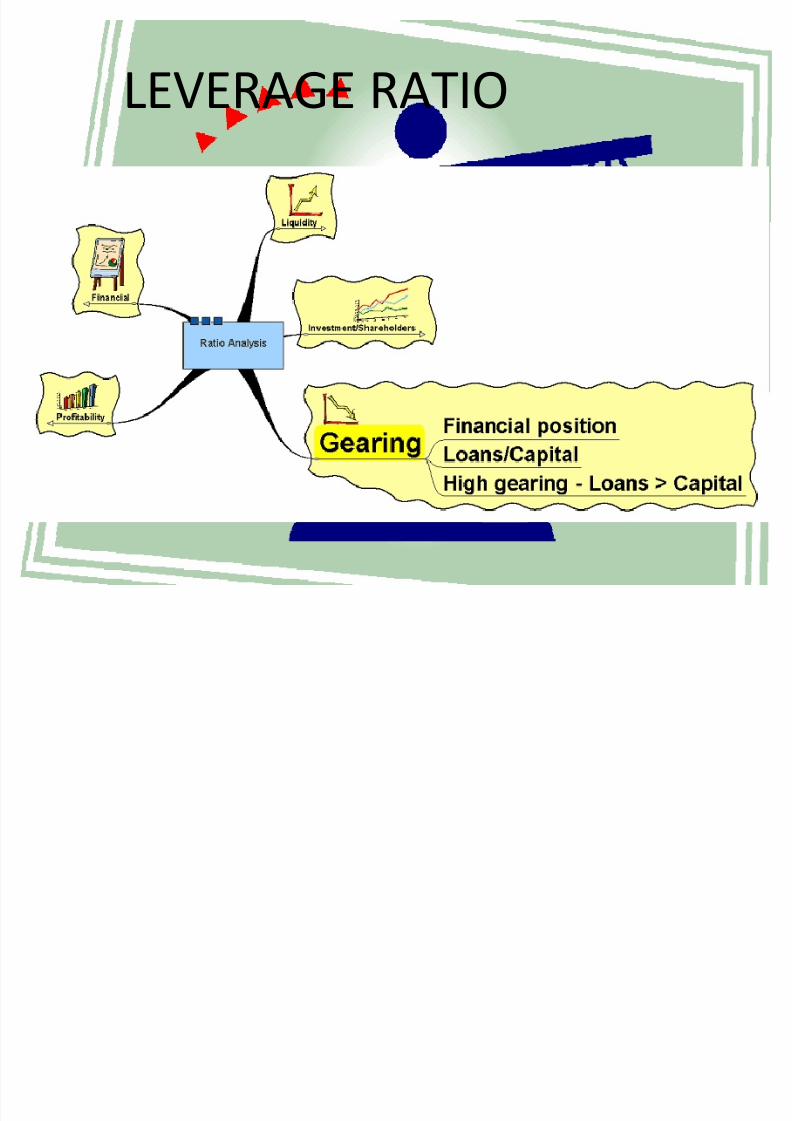

3. Leverage Ratio :

a. Debt ratio

b. Interest coverage ratio

c. Average Payment period

4. Liquidity ratio :

a. Current ratio.

b. Quick ratio.

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 20/48

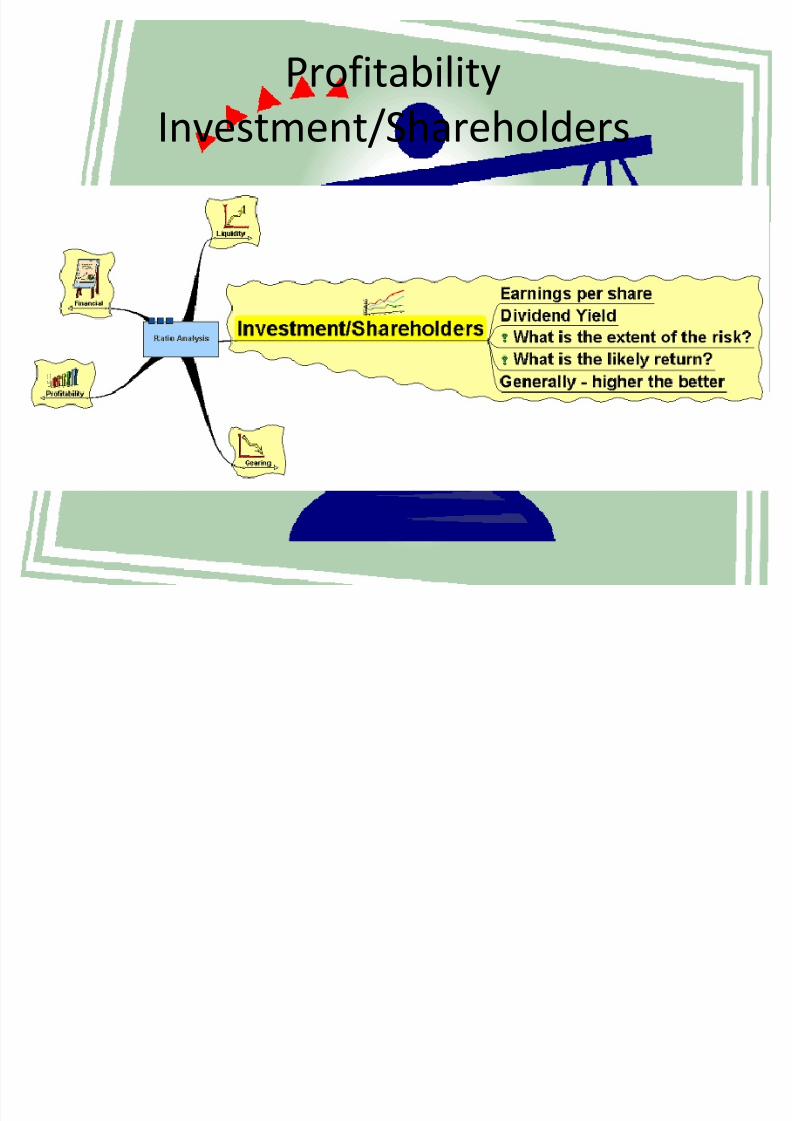

Profitability

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 21/48

Profitability

Investment/Shareholders

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 22/48

Basically, it is the amount of profit (at the gross, operating,

pretax or net income level) generated by the company as a

percent of the sales generated.

Objective analysis is to detect consistency or positive/negative

trends in a company's earnings. Positive profit margin analysis

translates into positive investment quality. To a large degree, it isthe quality, and growth, of a company's earnings that drive its

stock price.

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 23/48

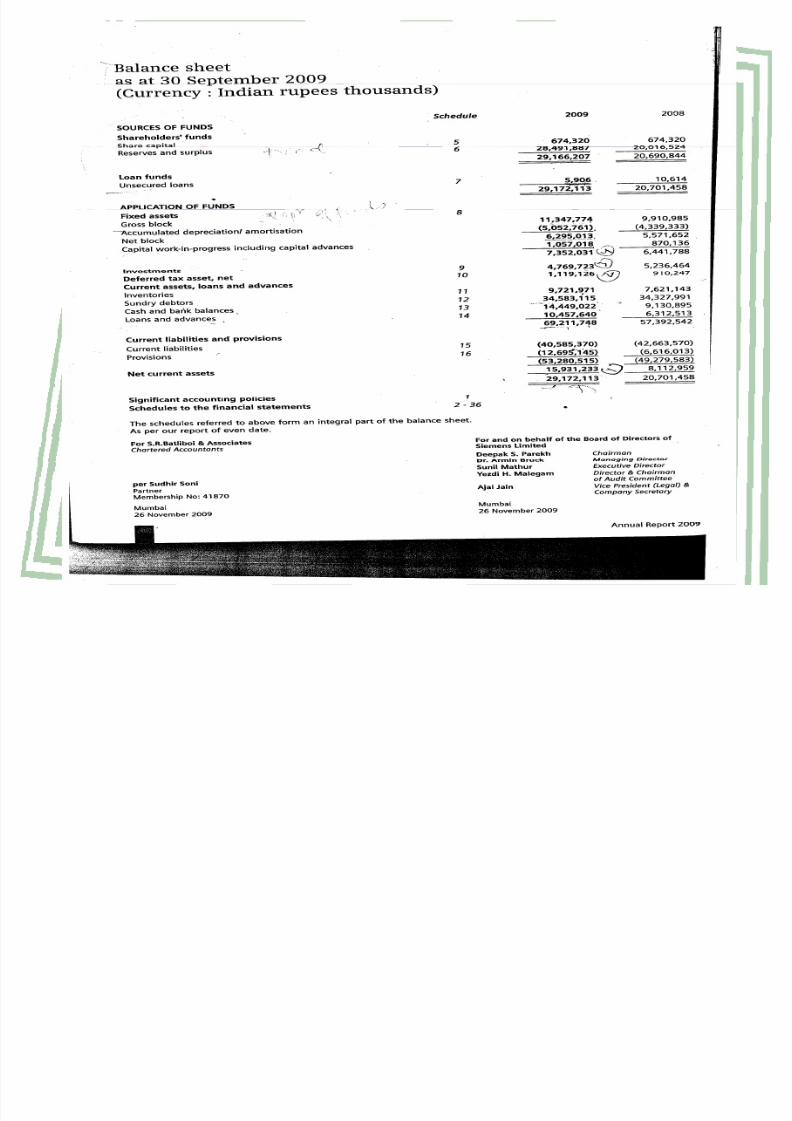

Working for SIEMENS ANNUAL REPORT -

2009

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 24/48

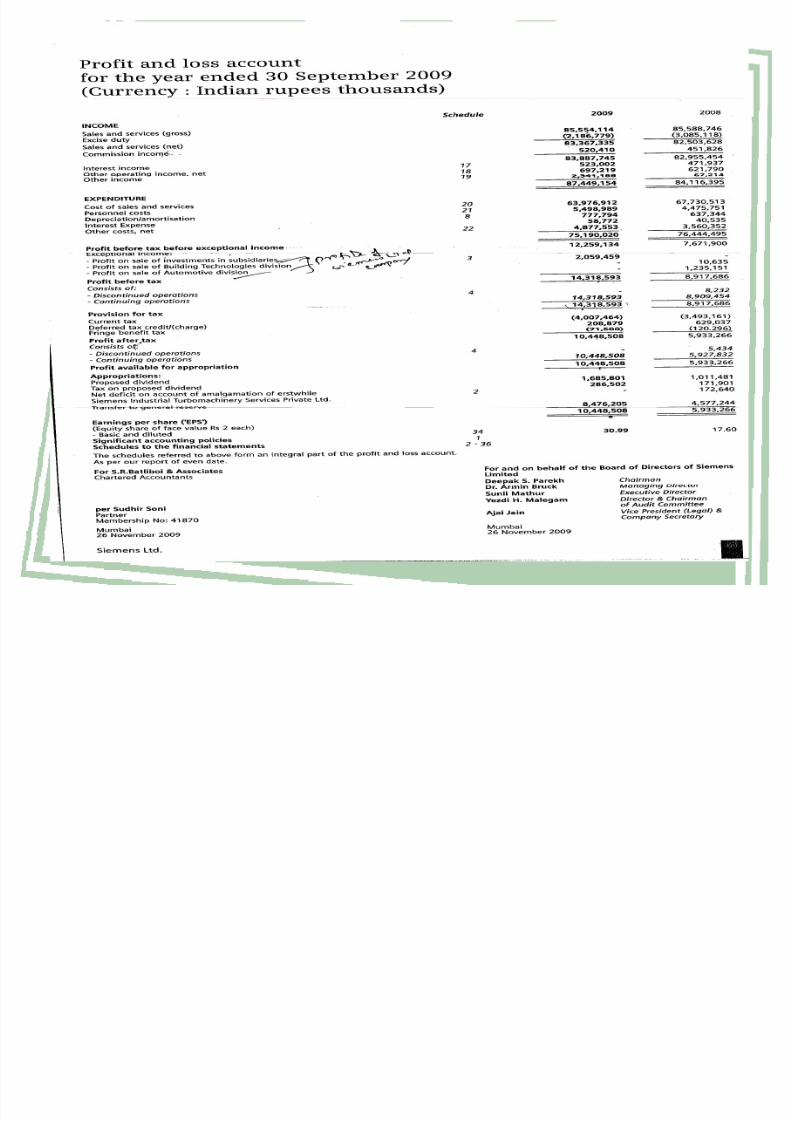

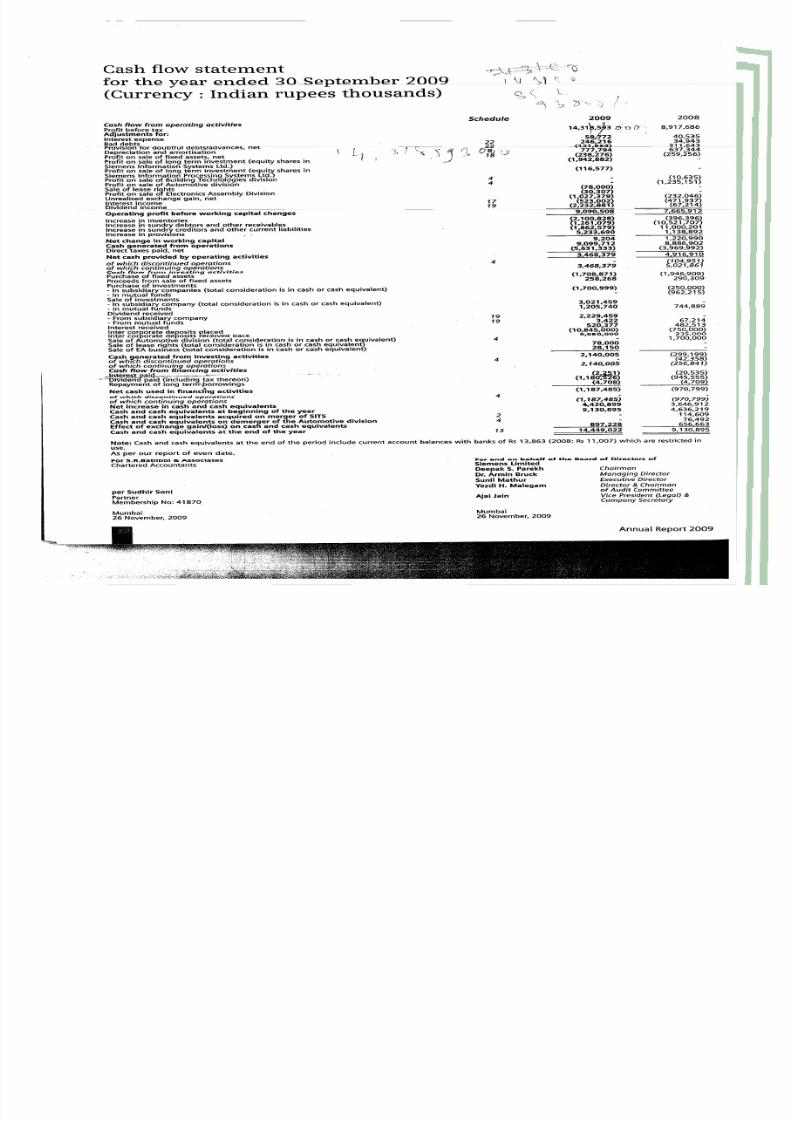

a) Profit as % of sales = Net Profit after taxes X 100

Net Salesfor the Year 2009 :- (Refer P/L A/c Report ) P961

Profit as % of sales (2009) = 10,448,508

83,367,335

: Profit as % of sale (2009) = 12.53% of Sales

for the year 2008 :- = Net Profit after taxes X100

Net Sales

Profit as % of sales (2008) = 5,933,266

82,503,628: Profit as % of sale (2008) = 7.19 % of sales

* Higher the better

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 25/48

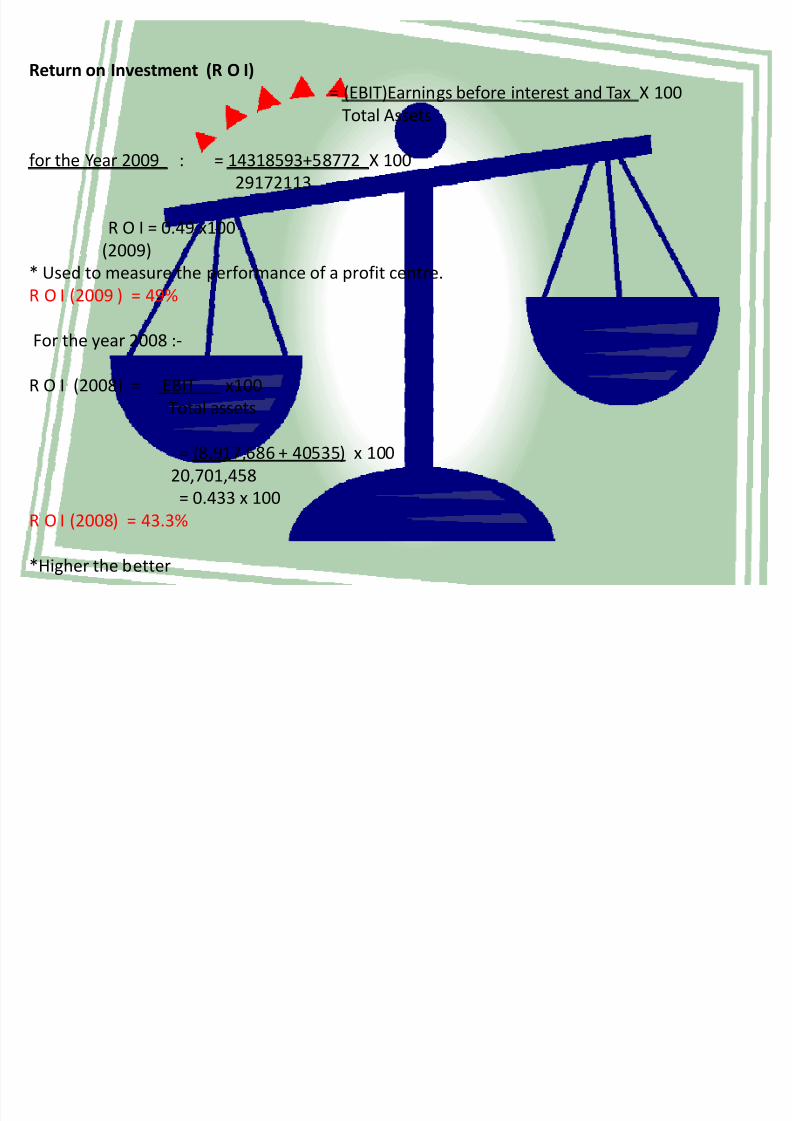

Return on Investment (R O I)

= (EBIT)Earnings before interest and Tax X 100

Total Assets

for the Year 2009 : = 14318593+58772 X 100

29172113

R O I = 0.49 x100

(2009)

* Used to measure the performance of a profit centre.R O I (2009 ) = 49%

For the year 2008 :-

R O I (2008) = EBIT x100

Total assets

= (8,917,686 + 40535) x 100

20,701,458

= 0.433 x 100

R O I (2008) = 43.3%

*Higher the better

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 26/48

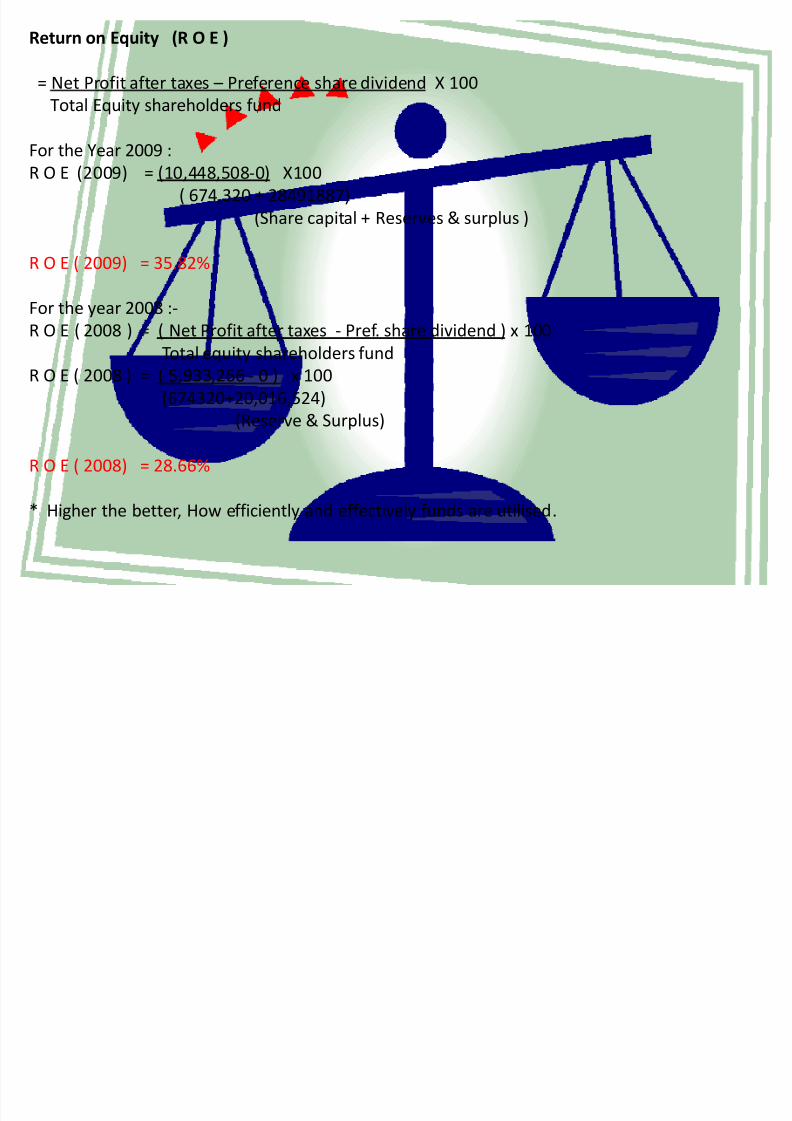

Return on Equity (R O E )

= Net Profit after taxes Preference share dividend X 100

Total Equity shareholders fund

For the Year 2009 :

R O E (2009) = (10,448,508-0) X100

( 674,320 + 28491887)

(Share capital + Reserves & surplus )

R O E ( 2009) = 35.82%

For the year 2008 :-

R O E ( 2008 ) = ( Net Profit after taxes - Pref. share dividend ) x 100

Total equity shareholders fund

R O E ( 2008 ) = ( 5,933,266 - 0 ) x 100

(674320+20,016,524)

(Reserve & Surplus)

R O E ( 2008) = 28.66%

* Higher the better, How efficiently and effectively funds are utilised.

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 27/48

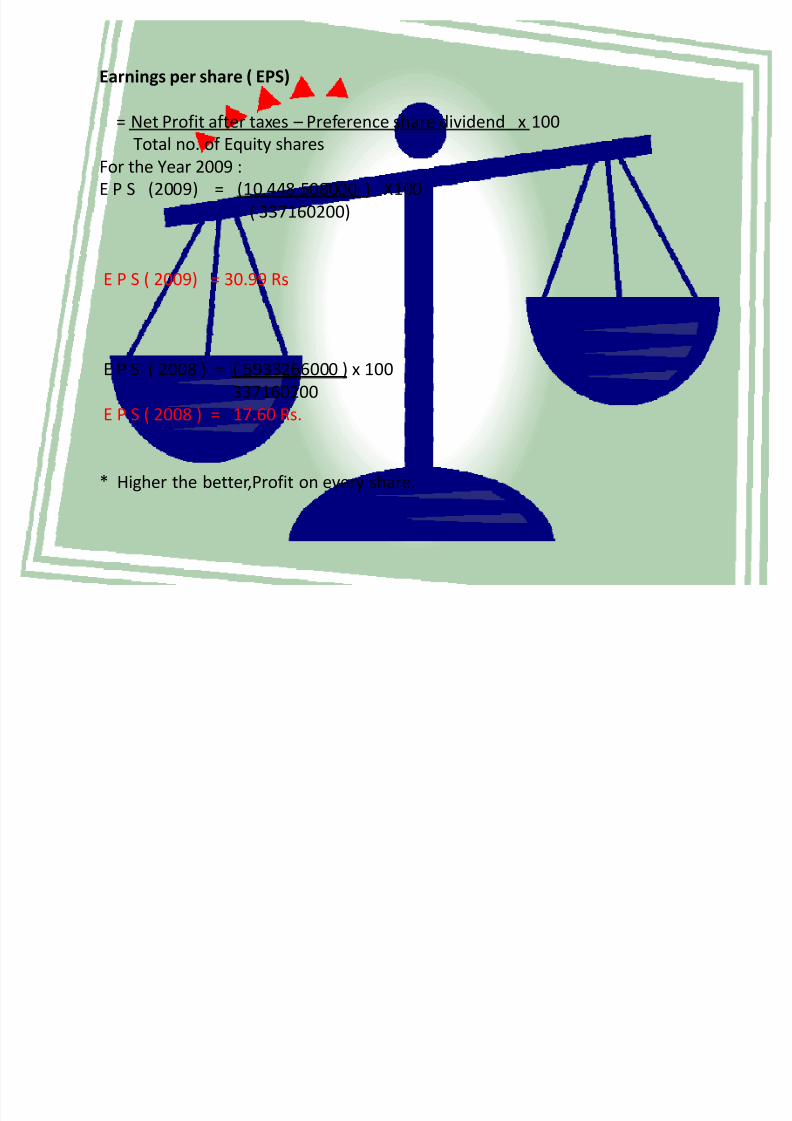

Earnings per share ( EPS)

= Net Profit after taxes Preference share dividend x 100

Total no. of Equity sharesFor the Year 2009 :

E P S (2009) = (10,448,508000 ) X100

( 337160200)

E P S ( 2009) = 30.99 Rs

E P S ( 2008 ) = ( 5933266000 ) x 100

337160200

E P S ( 2008 ) = 17.60 Rs.

* Higher the better,Profit on every share.

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 28/48

ACTIVITY / TURNOVER RATIO

*********used to find out Hidden Problems

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 29/48

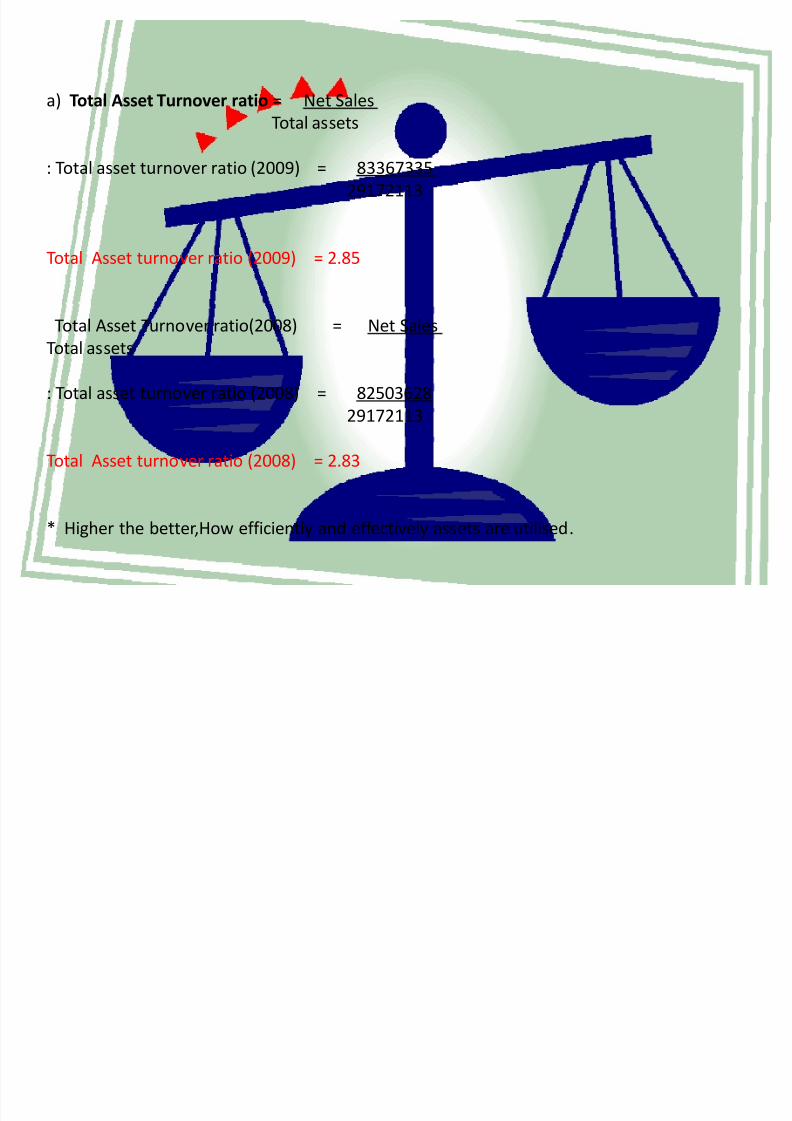

a) Total Asset Turnover ratio = Net Sales

Total assets

: Total asset turnover ratio (2009) = 83367335

29172113

Total Asset turnover ratio (2009) = 2.85

Total Asset Turnover ratio(2008) = Net Sales

Total assets

: Total asset turnover ratio (2008) = 82503628

29172113

Total Asset turnover ratio (2008) = 2.83

* Higher the better,How efficiently and effectively assets are utilised.

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 30/48

Fixed Asset Turnover ratio = Net Sales

Net fixed assets

For year 2009 :-

Fixed asset turnover ratio (2009) = 83367335

( Gross block depreciation)

= 83367335

6295013

Fixed Asset turnover ration (2009) = 13.24

Fixed Asset turnover ration (2008) = 82503628

5571652

Fixed Asset turnover ration (2008) = 14.81

* Higher the better,How efficiently and effectively fixed assets are utilised.

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 31/48

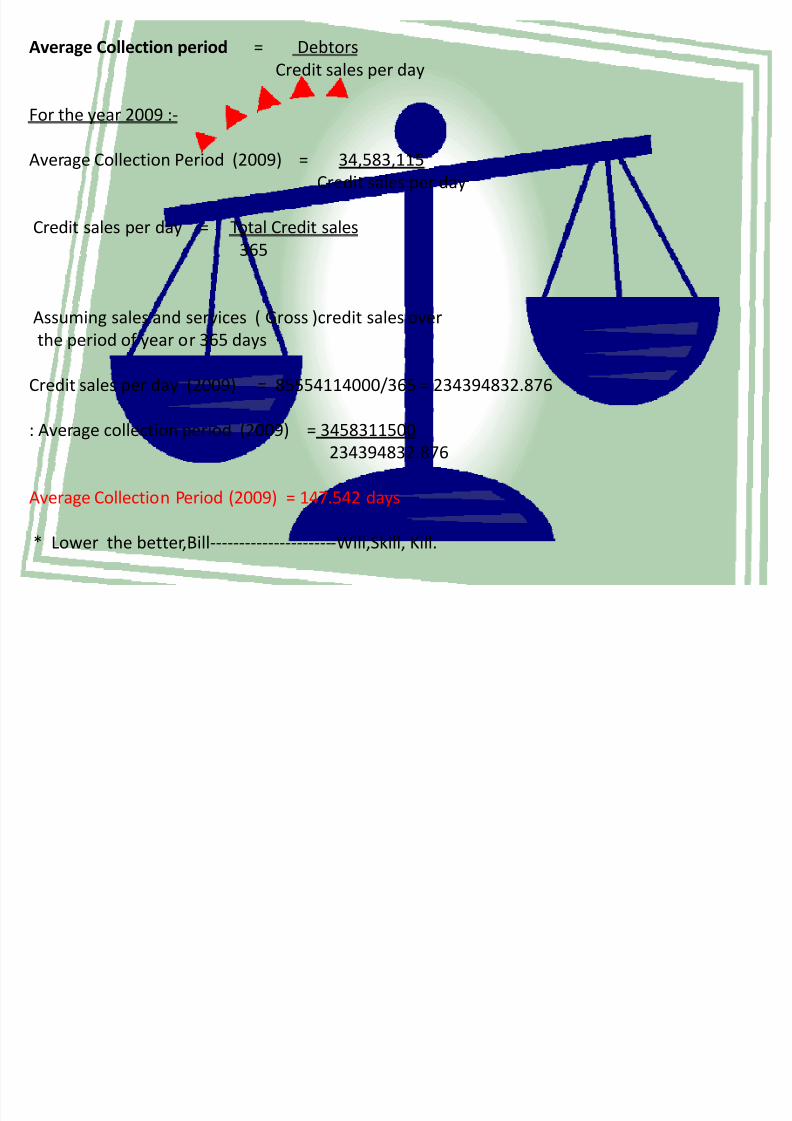

Average Collection period = Debtors

Credit sales per day

For the year 2009 :-

Average Collection Period (2009) = 34,583,115

Credit sales per day

Credit sales per day = Total Credit sales

365

Assuming sales and services ( Gross )credit sales over

the period of year or 365 days

Credit sales per day (2009) = 85554114000/365 = 234394832.876

: Average collection period (2009) = 3458311500

234394832.876

Average Collection Period (2009) = 147.542 days

* Lower the better,Bill----------------------Will,Skill, Kill.

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 32/48

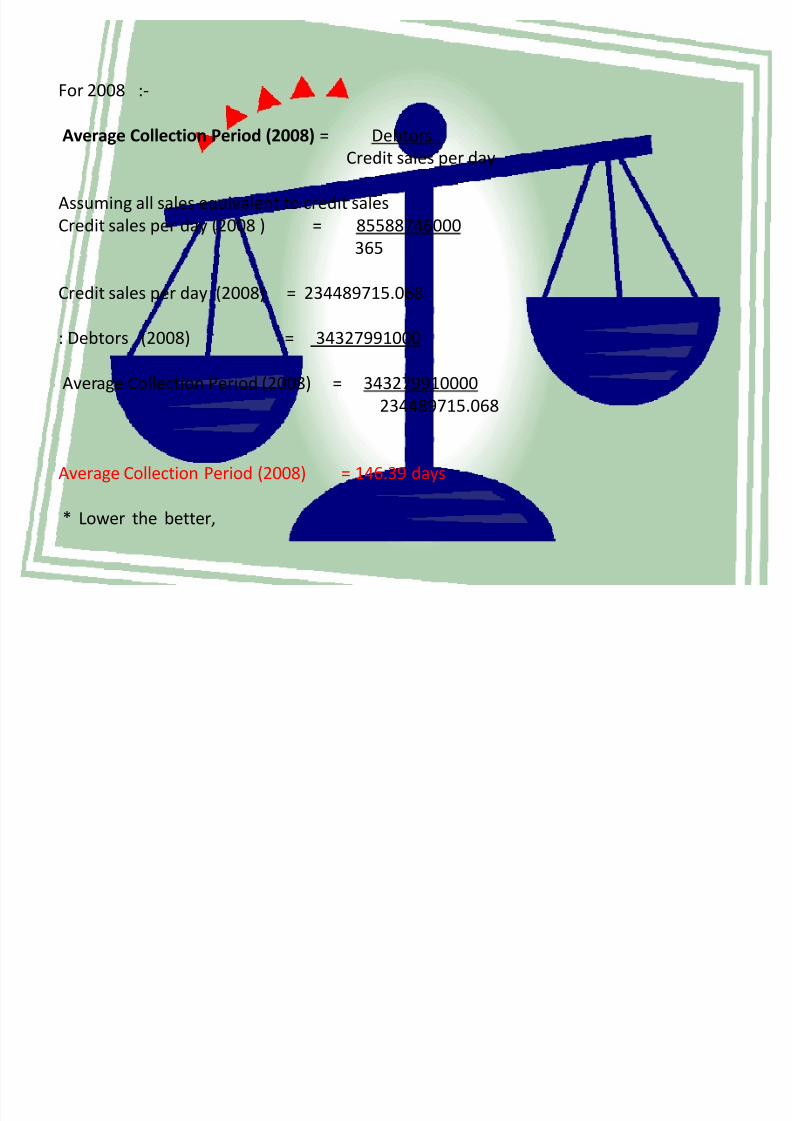

For 2008 :-

Average Collection Period (2008) = DebtorsCredit sales per day

Assuming all sales equivalent to credit sales

Credit sales per day (2008 ) = 85588746000

365

Credit sales per day (2008) = 234489715.068

: Debtors (2008) = 34327991000

Average Collection Period (2008) = 343279910000

234489715.068

Average Collection Period (2008) = 146.39 days

* Lower the better,

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 33/48

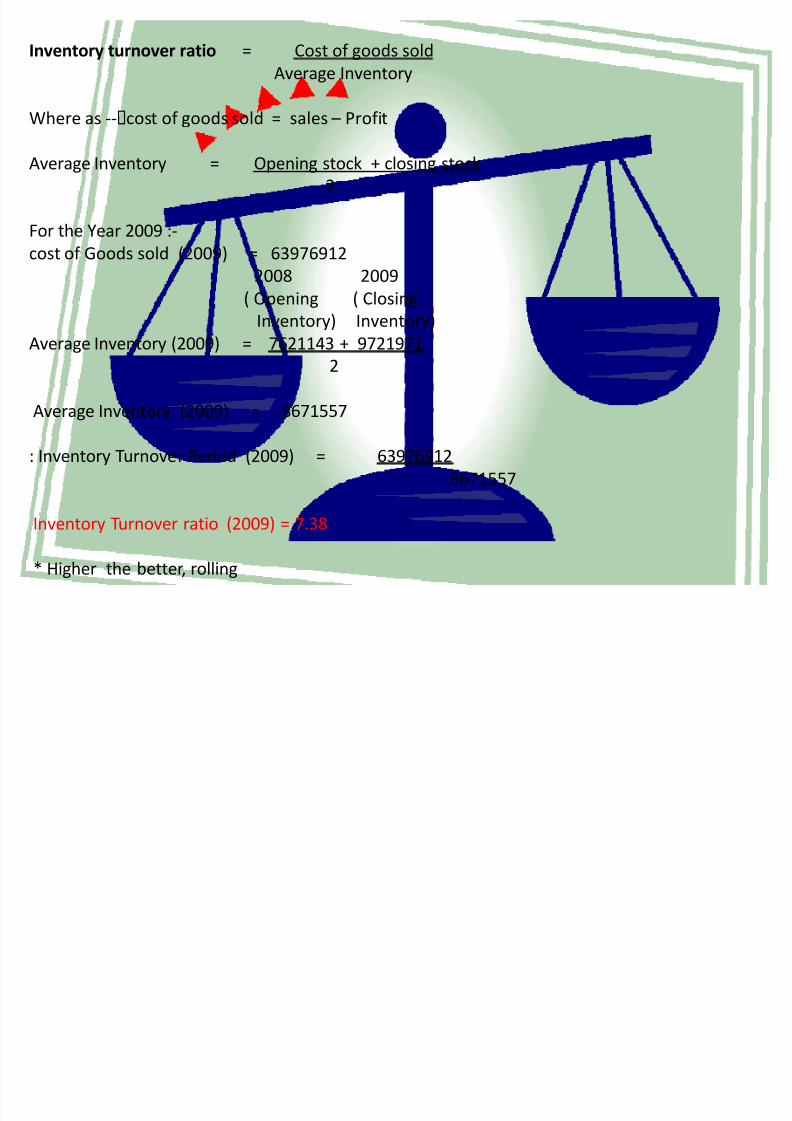

Inventory turnover ratio = Cost of goods sold

Average Inventory

Where as --cost of goods sold = sales Profit

Average Inventory = Opening stock + closing stock

2

For the Year 2009 :-

cost of Goods sold (2009) = 63976912

2008 2009( Opening ( Closing

Inventory) Inventory)

Average Inventory (2009) = 7621143 + 9721971

2

Average Inventory (2009) = 8671557

: Inventory Turnover Period (2009) = 63976912

8671557

Inventory Turnover ratio (2009) = 7.38

* Higher the better, rolling

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 34/48

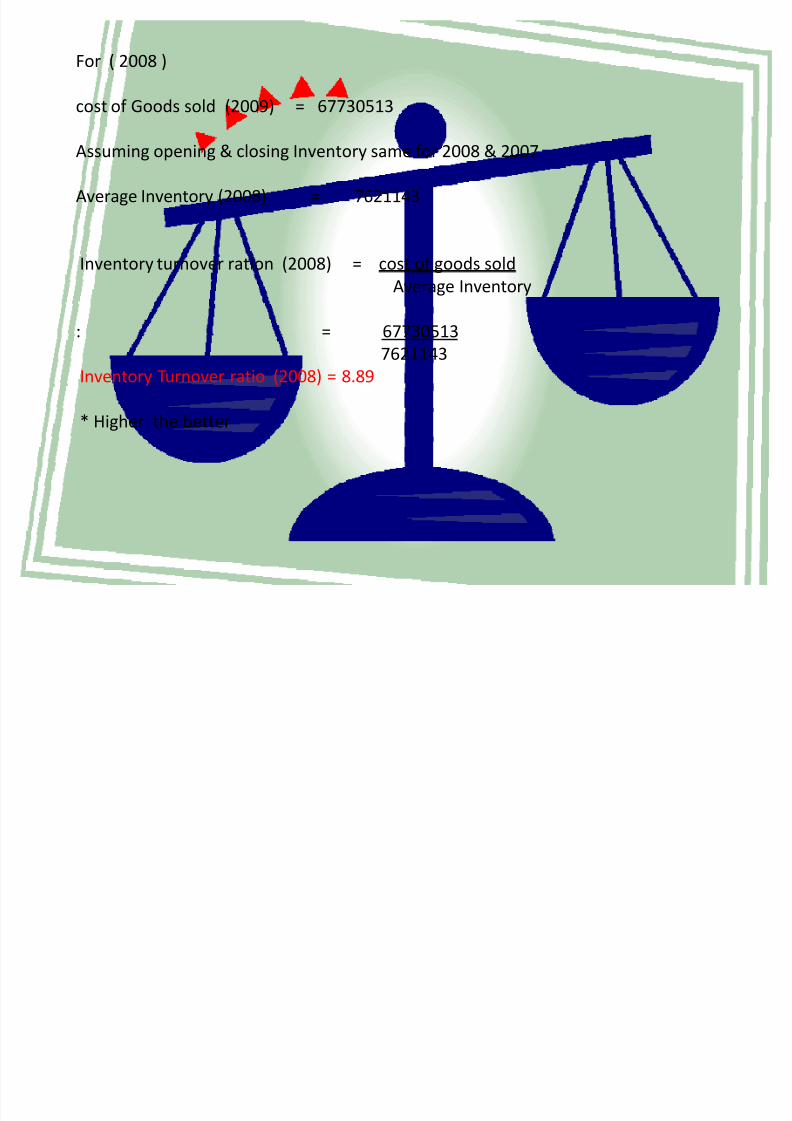

For ( 2008 )

cost of Goods sold (2009) = 67730513

Assuming opening & closing Inventory same for 2008 & 2007

Average Inventory (2008) = 7621143

Inventory turnover ration (2008) = cost of goods sold

Average Inventory

: = 67730513

7621143

Inventory Turnover ratio (2008) = 8.89

* Higher the better

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 35/48

LEVERAGE RATIO

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 36/48

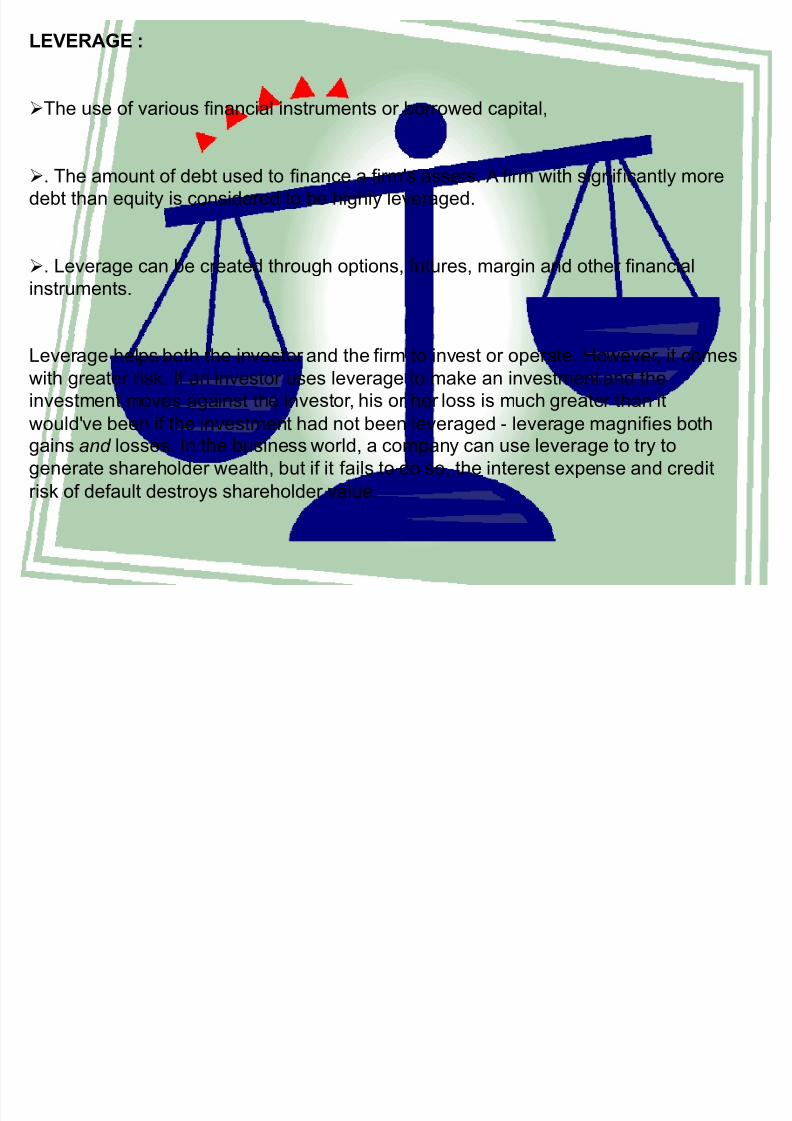

LEVERAGE :

The use of various financial instruments or borrowed capital,

. The amount of debt used to finance a firm's assets. A firm with significantly more

debt than equity is considered to be highly leveraged.

. Leverage can be created through options, futures, margin and other financial

instruments.

Leverage helps both the investor and the firm to invest or operate. However, it comes

with greater risk. If an investor uses leverage to make an investment and the

investment moves against the investor, his or her loss is much greater than it

would've been if the investment had not been leveraged - leverage magnifies bothgains and losses. In the business world, a company can use leverage to try to

generate shareholder wealth, but if it fails to do so, the interest expense and credit

risk of default destroys shareholder value.

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 37/48

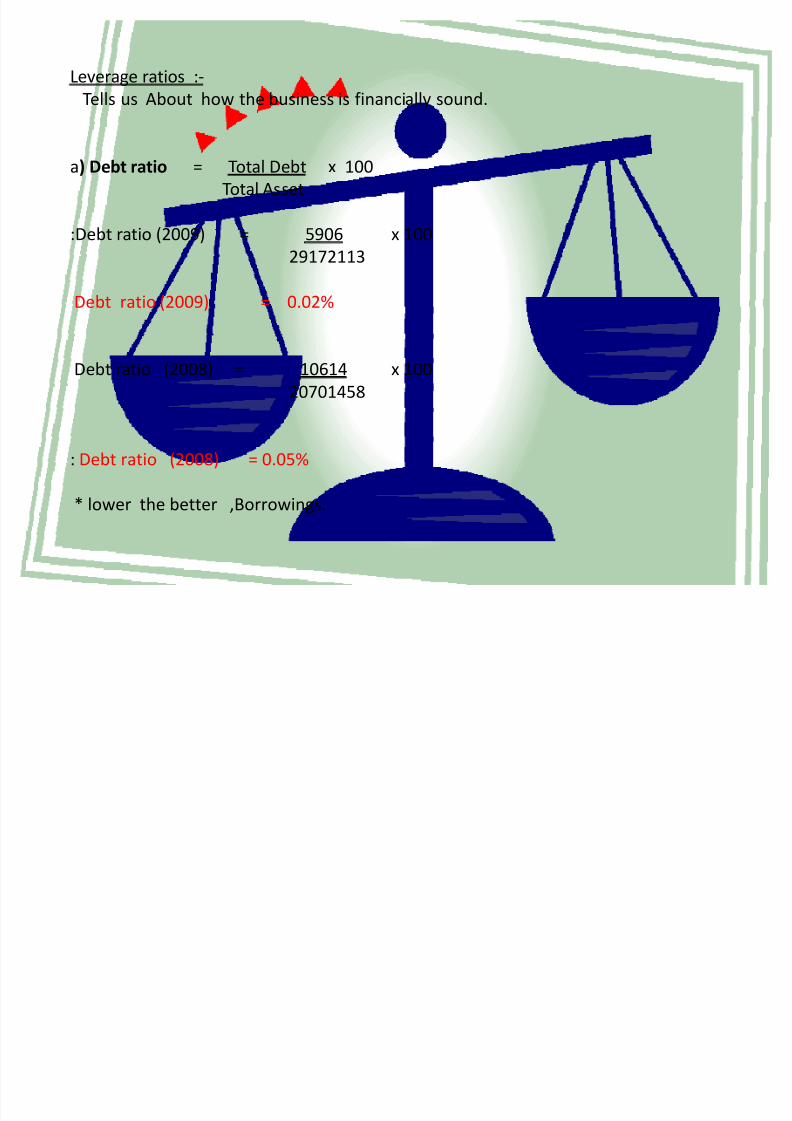

Leverage ratios :-

Tells us About how the business is financially sound.

a) Debt ratio = Total Debt x 100

Total Asset

:Debt ratio (2009) = 5906 x 100

29172113

Debt ratio (2009) = 0.02%

Debt ratio (2008) = 10614 x 100

20701458

: Debt ratio (2008) = 0.05%

* lower the better ,Borrowings.

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 38/48

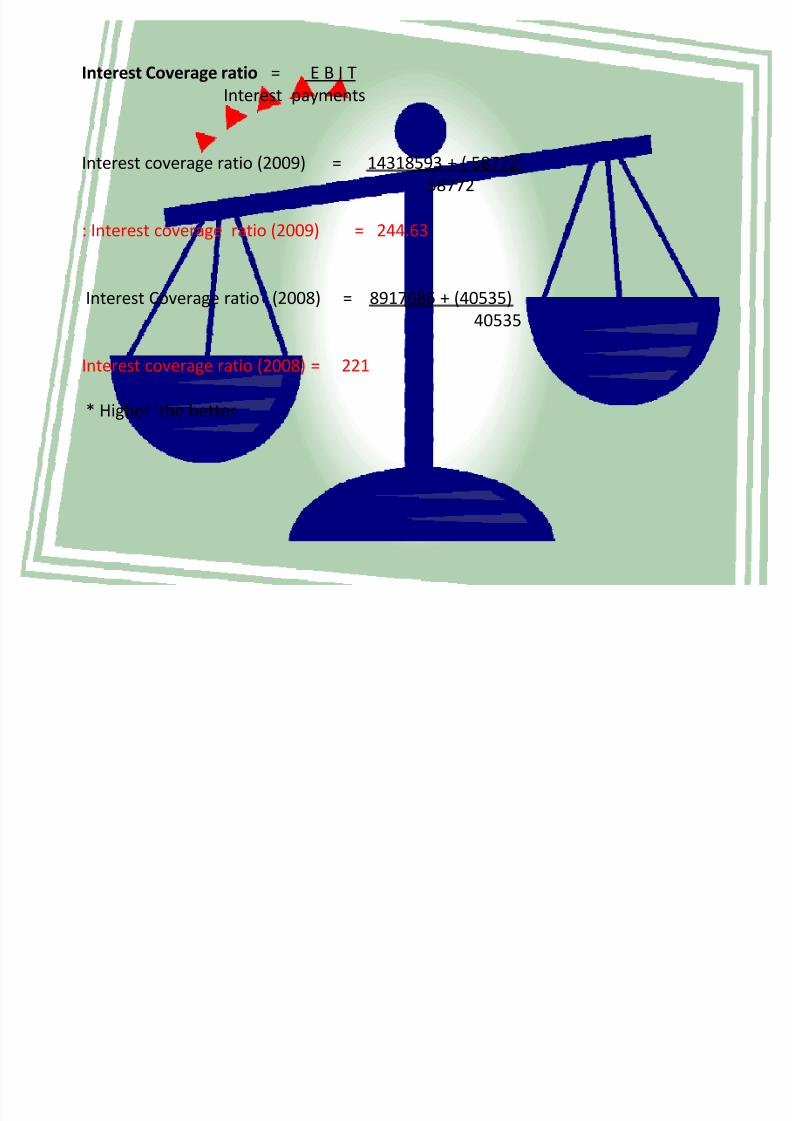

Interest Coverage ratio = E B I T

Interest payments

Interest coverage ratio (2009) = 14318593 + ( 58772)

58772

: Interest coverage ratio (2009) = 244.63

Interest Coverage ratio (2008) = 8917686 + (40535)

40535

Interest coverage ratio (2008) = 221

* Higher the better

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 39/48

Average Payment period = Creditors

Credit purchases per day

Average Payment period (2009)

Creditors = 654274 + 33142 + 23769726 = 24456142

Assuming all purchase to be credit

Credit Purchase per day = Total Purchases

365= 63976912000 = 175279210

365

Credit purchase period (2009) = 24456142000

175279210

Average payment period (2009) = 139.52 days

* lower the better

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 40/48

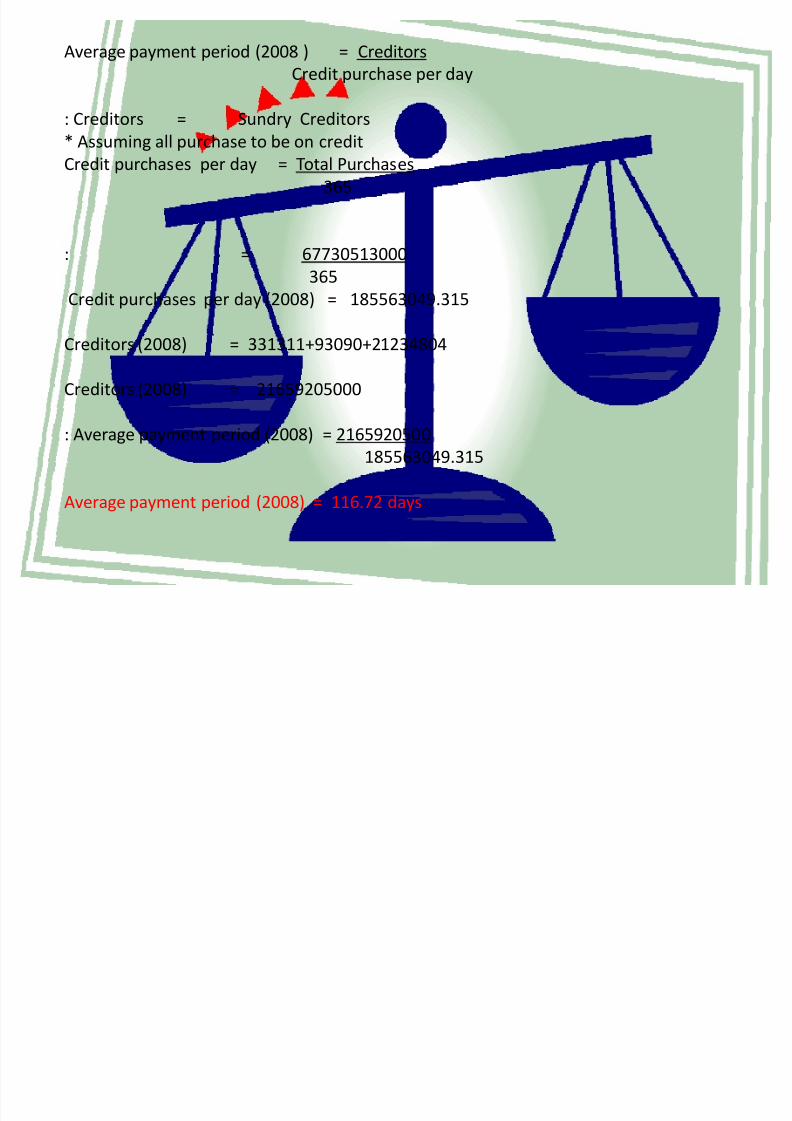

Average payment period (2008 ) = Creditors

Credit purchase per day

: Creditors = Sundry Creditors

* Assuming all purchase to be on creditCredit purchases per day = Total Purchases

365

: = 67730513000

365Credit purchases per day (2008) = 185563049.315

Creditors (2008) = 331311+93090+21234804

Creditors (2008) = 21659205000

: Average payment period (2008) = 2165920500

185563049.315

Average payment period (2008) = 116.72 days

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 41/48

Liquidity

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 42/48

LIQUIDITY RATIOS.

Liquidity ratios attempt to measure a company's ability to pay off its short-term debt

obligations.

This is done by comparing a company's most liquid assets (or, those that can be easily

converted to cash), its short-term liabilities.

In general, the greater the coverage of liquid assets to short-term liabilities the better

as it is a clear signal that a company can pay its debts that are coming due in the near

future and still fund its ongoing operations. On the other hand, a company with a low

coverage rate should raise a red flag for investors as it may be a sign that the company

will have difficulty meeting running its operations, as well as meeting its obligations.

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 43/48

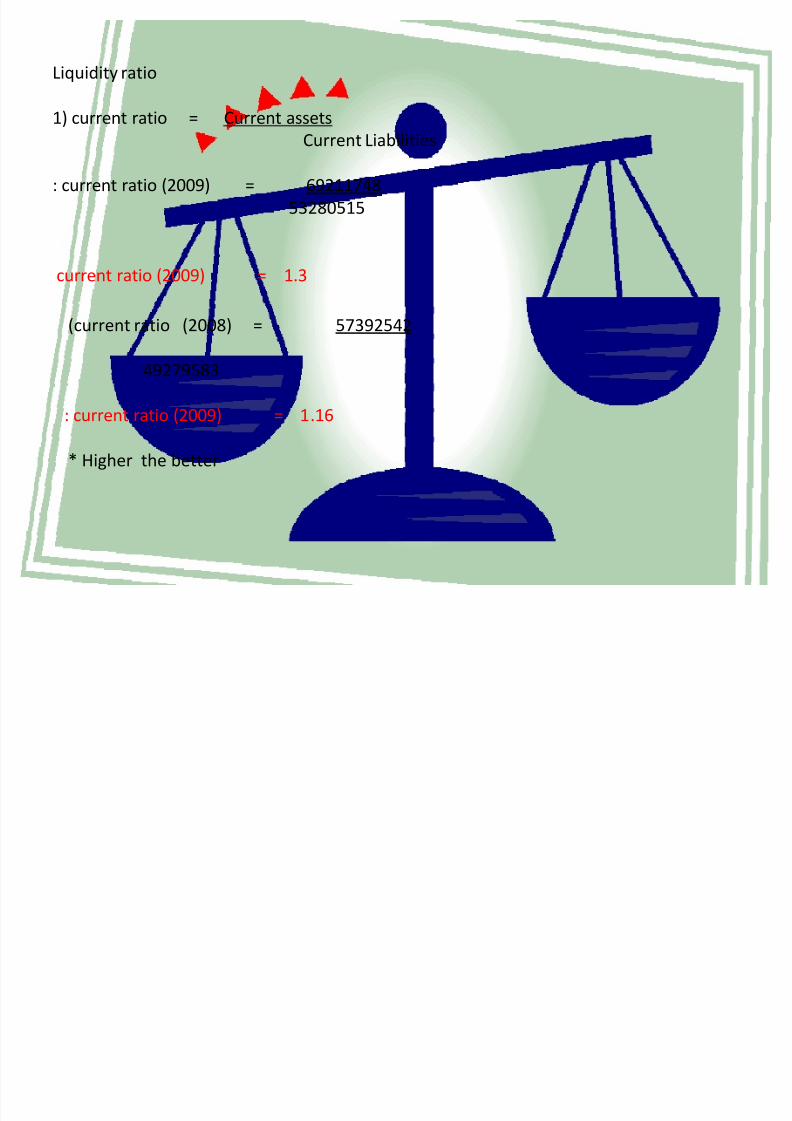

Liquidity ratio

1) current ratio = Current assets

Current Liabilities

: current ratio (2009) = 69211748

53280515

current ratio (2009) = 1.3

(current ratio (2008) = 57392542

49279583

: current ratio (2009) = 1.16

* Higher the better

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 44/48

Quick ratio : / Acid test ratio

= Current assets Inventories

Current liabilities

Quick ratio (2009) = (69211748 9721971)

53280515

= 59489777

53280515

Quick ratio (2009) = 1.12

Quick ratio (2008) = 57392542 7621143

9279583

Quick ratio (2008) = 1.01

* Higher the better

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 45/48

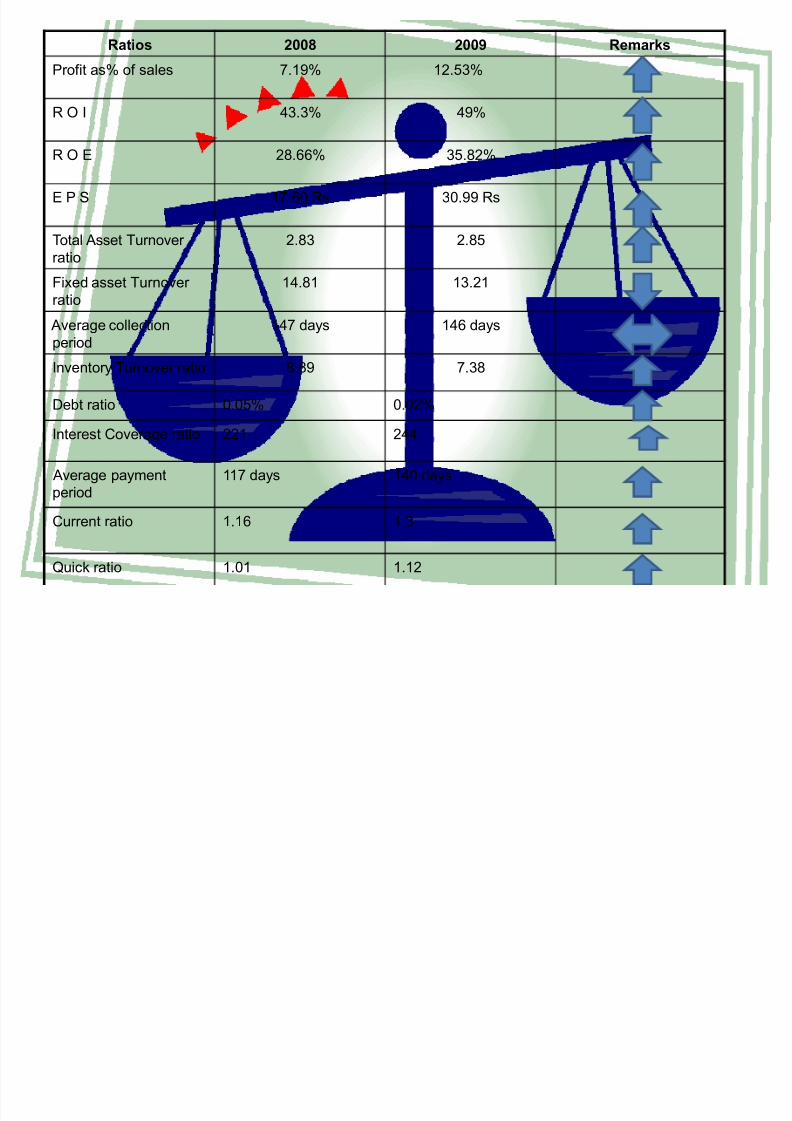

Ratios 2008 2009 Remarks

Profit as% of sales 7.19% 12.53%

R O I 43.3% 49%

R O E 28.66% 35.82%

E P S 17.60 Rs 30.99 Rs

Total Asset Turnover

ratio

2.83 2.85

Fixed asset Turnover ratio

14.81 13.21

Average collection

period

147 days 146 days

Inventory Turnover ratio 8.89 7.38

Debt ratio 0.05% 0.02%

Interest Coverage ratio 221 244

Average payment

period

117 days 140 days

Current ratio 1.16 1.3

Quick ratio 1.01 1.12

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 46/48

CONCLUSION :

After looking at the ratios calaculated in the previous

Slides , we can conclude upon

That ,The over all performance of the company has

been improved and shown consistency in the

performance for the period 2008 and 2009.

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 47/48

8/6/2019 Ratio Final Presntn 97 2003

http://slidepdf.com/reader/full/ratio-final-presntn-97-2003 48/48

THANK YOU