Embed Size (px)

Citation preview

ICICI Securities Ltd | Retail Equity Research

Initiating Coverage

October 3, 2017

Opportunities in the pipeline…

Ratnamani Metals and Tubes (RMTL) is a leading manufacturer of

stainless steel tubes and pipes (SSTP) and carbon steel (CS) pipes. The

company’s product offerings consist of diverse grades with significant

quantum of customisation, which is the USP of the company. RMTL’s

product portfolio distinguishes it from its peers both in stainless steel and

carbon steel categories wherein the company’s products find application

in critical areas and in diverse end-user industries like oil & gas, power,

nuclear, refineries, etc. On the back of a revival of capex in key end user

industries, RMTL has undertaken capex to cater to the potential demand.

Capex revival in key user industries to provide requisite demand push

The Indian oil & gas sector is at the cusp of a capex revival on the back of

a) enhancement of domestic refining capacity and b) upgradation of

refineries to meet the BS VI standard by 2020. Furthermore, in the

medium to longer term horizon, a notable capex is planned in power

(both thermal and nuclear), fertiliser, city gas distribution (CGD), cross

country pipes lines, etc. This is expected to enhance the overall demand

for pipes. Within the SSTP segment itself, this planned aggregate capex is

likely to create an annual addressable opportunity of ~| 2400-2800 crore

for the industry. Historically, in such a niche SSTP segment, RMTL’s

domestic market share has been ~40%, thereby providing healthy

revenue visibility. Furthermore, a strong orderbook of ~|1800 crore in the

carbon steel segment augurs well for the company.

Expansion in stainless steel pipe & tube segment augurs well…

RMTL has chalked out plans to set up a hot extrusion facility for large

diameter (dia) seamless stainless steel pipes and matching cold finishing

capacity. Incremental capacity of 20000 tonnes is being set up in the

stainless steel seamless tube and pipe segment at a capex of ~| 350-400

crore and is expected to be commissioned by Q4FY19. The new facility

will be funded through internal accruals. This facility will make RMTL the

only player in India with the capability to extrude mother hollow pipes of

up to 8” in diameter against the company’s current capability of extruding

tubes up to only 2” diameter. After commissioning this new facility RMTL

will be able to manufacture large dia pipes, which will ensure import

substitution as well as further penetration of export market.

On a strong footing, recommend BUY...

Ratnamani with its competitively placed capacity is perfectly positioned to

cater to the upcoming demand. As on date, RMTL has a strong multi-year

higher order-book (~| 2100 crore, aggregate of stainless steel and carbon

steel order book), which provides a strong revenue visibility. We expect

RMTL’s topline, EBITDA and PAT to register a CAGR of 14.5%, 15.6% and

17.3% respectively during FY17-20E. We initiate coverage on the

company with a BUY rating and a target price of | 1050.

Exhibit 1: Key Financial

(Year-end March) FY16 FY17 FY18E FY19E FY20E

Total Operating Income (| crore) 1,717.7 1,411.7 1,660.5 1,898.8 2,120.0

EBITDA (| crore) 284.4 257.4 285.1 336.5 397.5

Net Profit (| crore) 163.9 144.3 158.0 193.0 232.8

EPS (|) 35.1 30.9 33.8 41.3 49.8

P/E (x) 24.8 28.2 25.7 21.1 17.5

Price/Book (x) 3.9 3.4 3.1 2.8 2.4

EV/EBITDA (x) 14.3 15.7 13.9 12.0 9.6

RoCE (%) 23.3 17.8 18.4 19.9 21.1

RoNW (%) 15.8 12.2 12.0 13.1 13.9

Source: Company, ICICIdirect.com Research

Ratnamani Metals & Tubes (RATMET) |870 Rating matrix

Rating : Buy

Target : | 1050

Target Period : 12 months

Potential Upside : 21%

Key Financials

| Crore FY17 FY18E FY19E FY20E

Revenues 1,411.7 1,660.5 1,898.8 2,120.0

EBITDA 257.4 285.1 336.5 397.5

Net Profit 144.3 158.0 193.0 232.8

EPS (|) 30.9 33.8 41.3 49.8

Valuation Summary

| Crore FY17 FY18E FY19E FY20E

P/E 28.2 25.7 21.1 17.5

Target P/E 34.0 31.0 25.4 21.1

EV/EBITDA 15.7 13.9 12.0 9.6

P/BV 3.4 3.1 2.8 2.4

RONW (%) 12.2 12.0 13.1 13.9

ROCE (%) 17.8 18.4 19.9 21.1

Stock Data

Particulars

Market Capitalisation (| crore) 4,046

Total Debt (FY17) (| crore) -

Cash & Cash Eq (FY17) (| crore) 89

EV (| crore) 3,957

52 week H/L 959 / 540

Equity Capital (| crore) 9.3

Face Value | 2

Stock Price Movement

0

200

400

600

800

1,000

0

2,000

4,000

6,000

8,000

10,000

12,000

Aug-14

Dec-14

Apr-15

Aug-15

Dec-15

Apr-16

Aug-16

Dec-16

Apr-17

Aug-17

Nifty (L.H.S) Price (R.H.S)

Source: Bloomberg, ICICIdirect.com Research

Price Performance

Return % 1M 3M 6M 12M

Ratnamani Metals 0.9 8.0 16.9 58.0

Source: ICICIdirect.com Research

Research Analyst

Dewang Sanghavi

Akshay Kadam

ICICI Securities Ltd | Retail Equity Research Page 2

Company Background

Ratnamani Metals and Tubes (RMTL) is a niche player with superior

capabilities in the domestic industrial pipes domain. The company has

stainless steel capacity of 28000 tonnes and carbon steel capacity of

350000 tonnes. RMTL manufactures a wide range of stainless steel and

carbon steel pipes and tubes, which find application in the highly

corrosive environment of end user industries like oil & gas refineries,

power, water and chemicals. The company has ~40% domestic market

share of stainless steel tubes/pipes for niche applications. The product

offering of the company have approvals from all leading industry majors

both in domestic as well as international markets.

Stainless steel division…

RMTL’s stainless steel division was established in 1985. Today, the

division consists of two state-of-the-art manufacturing facilities. One is in

Indrad while the other is in Kutch (Gandhidham), strategically located in

the vicinity of two major ports Kandla and Mundra. The stainless steel

division has an aggregate installed capacity of 28000 tonne split between

stainless steel welded tubes capacity of 20000 tonnes and stainless steel

seamless pipes of 8000 tonnes. The company also manufactures titanium

welded tubes at its Kutch facility. The product suite includes heat

exchanger tubes, instrumentation tubes and stainless steel welded and

seamless pipes. RMTL offers products in diverse grades with flexibility for

customisation. For its stainless steel segment, it has secured several

quality certifications like ISO 9001:2008, ISO 14001:2004 and OHSAS

18001:2007 under TUV. Furthermore, the company has plant specific

certifications and approvals as well from various EPC contractors, clients

and consultants.

Carbon steel division…

RMTL’s carbon steel division has an installed capacity of 350000 tonne

split between HSAW (180000 tonne), LSAW (100000 tonne) and ERW

pipes (70000 tonne) and offers pipe coating solutions as well. It has a

mobile plant for production of pipes with a capacity of 24,000 MTPA. The

mobile plant caters to customer requirement on location and can be

dismantled and erected in a short span of time. The technology enables

easy handling of pipes at site, meeting delivery schedules, cutting down

transportation cost making the project economical and viable.

Exhibit 2: Company Timeline

Source: Company, ICICIdirect.com Research

Shareholding pattern

(in % ) Q1FY18

Promoter 60.1

FII 14.7

DII 5.9

Others 19.4

FII & DII Holding

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Q4FY17

Q1FY18

%

FII DII

Export share in total revenues (FY17)

Domestic

81.5 %

Exports,

18.5 %

Source: Company, ICICIdirect.com Research

The company exports to countries such as US, UK, France,

Germany, Italy, Netherlands, Japan, South Korea and Middle East

countries.

ICICI Securities Ltd | Retail Equity Research Page 3

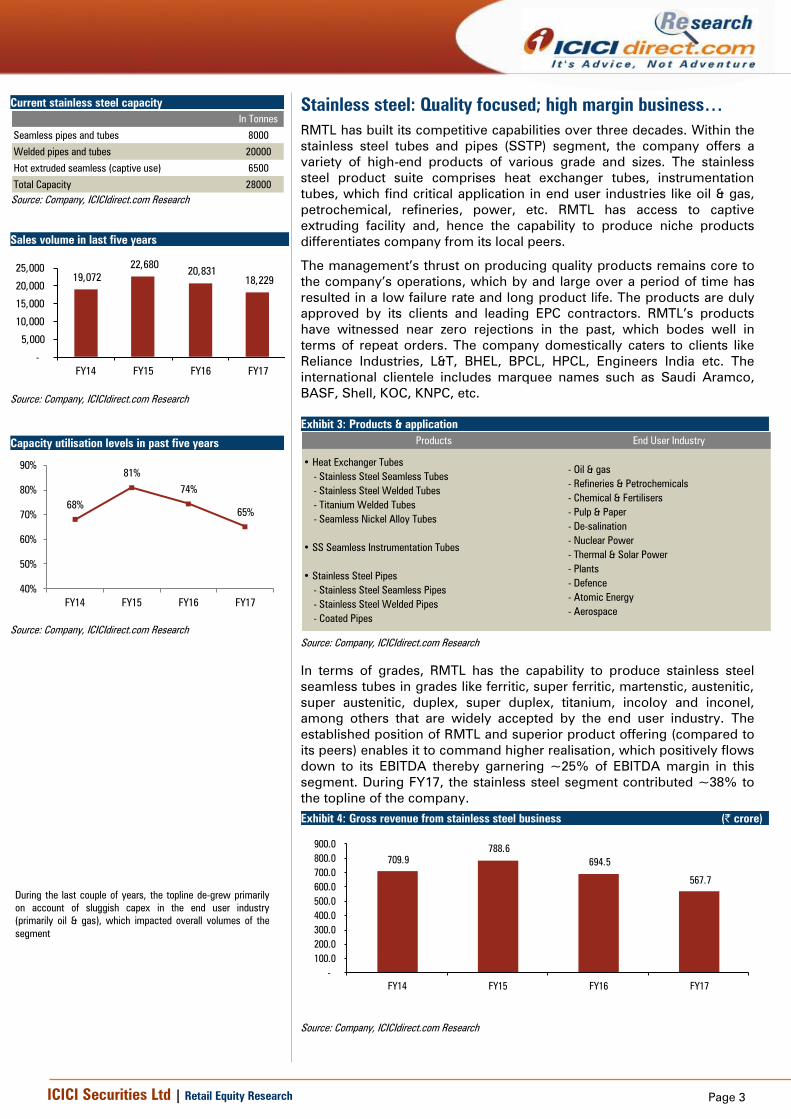

Stainless steel: Quality focused; high margin business…

RMTL has built its competitive capabilities over three decades. Within the

stainless steel tubes and pipes (SSTP) segment, the company offers a

variety of high-end products of various grade and sizes. The stainless

steel product suite comprises heat exchanger tubes, instrumentation

tubes, which find critical application in end user industries like oil & gas,

petrochemical, refineries, power, etc. RMTL has access to captive

extruding facility and, hence the capability to produce niche products

differentiates company from its local peers.

The management’s thrust on producing quality products remains core to

the company’s operations, which by and large over a period of time has

resulted in a low failure rate and long product life. The products are duly

approved by its clients and leading EPC contractors. RMTL’s products

have witnessed near zero rejections in the past, which bodes well in

terms of repeat orders. The company domestically caters to clients like

Reliance Industries, L&T, BHEL, BPCL, HPCL, Engineers India etc. The

international clientele includes marquee names such as Saudi Aramco,

BASF, Shell, KOC, KNPC, etc.

Exhibit 3: Products & application

Products End User Industry

• Heat Exchanger Tubes

- Stainless Steel Seamless Tubes

- Stainless Steel Welded Tubes

- Titanium Welded Tubes

- Seamless Nickel Alloy Tubes

• SS Seamless Instrumentation Tubes

• Stainless Steel Pipes

- Stainless Steel Seamless Pipes

- Stainless Steel Welded Pipes

- Coated Pipes

- Oil & gas

- Refineries & Petrochemicals

- Chemical & Fertilisers

- Pulp & Paper

- De-salination

- Nuclear Power

- Thermal & Solar Power

- Plants

- Defence

- Atomic Energy

- Aerospace

Source: Company, ICICIdirect.com Research

In terms of grades, RMTL has the capability to produce stainless steel

seamless tubes in grades like ferritic, super ferritic, martenstic, austenitic,

super austenitic, duplex, super duplex, titanium, incoloy and inconel,

among others that are widely accepted by the end user industry. The

established position of RMTL and superior product offering (compared to

its peers) enables it to command higher realisation, which positively flows

down to its EBITDA thereby garnering ~25% of EBITDA margin in this

segment. During FY17, the stainless steel segment contributed ~38% to

the topline of the company.

Exhibit 4: Gross revenue from stainless steel business (| crore)

709.9

788.6

694.5

567.7

-

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

FY14 FY15 FY16 FY17

Source: Company, ICICIdirect.com Research

Current stainless steel capacity

In Tonnes

Seamless pipes and tubes 8000

Welded pipes and tubes 20000

Hot extruded seamless (captive use) 6500

Total Capacity 28000

Source: Company, ICICIdirect.com Research

Sales volume in last five years

19,072

22,680 20,831

18,229

-

5,000

10,000

15,000

20,000

25,000

FY14 FY15 FY16 FY17

Source: Company, ICICIdirect.com Research

Capacity utilisation levels in past five years

68%

81%

74%

65%

40%

50%

60%

70%

80%

90%

FY14 FY15 FY16 FY17

Source: Company, ICICIdirect.com Research

During the last couple of years, the topline de-grew primarily

on account of sluggish capex in the end user industry

(primarily oil & gas), which impacted overall volumes of the

segment

ICICI Securities Ltd | Retail Equity Research Page 4

Carbon steel: Compliments the SSTP division….

RMTL through its carbon steel division manufactures all three categories –

LSAW, HSAW and ERW pipes. The primary focus is on the API grade

pipes, which find application in oil & gas pipelines, water and city gas

distribution.

The company’s manufacturing facility consists of a JCO press,

helical/spiral mills, three roll plate bending machine, inside & outside

welding lines, heat treatment furnace and all necessary testing equipment

to produce high quality pipes conforming to various international

standards. The pipes are supplied according to appropriate standards as

well as customer specifications in a large variety of steel grades and

dimensions. Specific requirements on execution, tolerances, lengths and

mechanical & chemical properties are offered on request.

Exhibit 5: Carbon steel’s division pipe wise capacity & application

Category Installed Capacity (in tonnes) Application

Spiral Pipes

- LSAW 100000 a) In-plant pipelines used in refineries & other industries

- HSAW 180000 b) Large diameter pipes for water supply & sewage

ERW Pipes 70000 a) City gas distribution pipelines

Source: Company, ICICIdirect.com Research

*Out of the 100000 tonne LSAW capacity, the company has a capacity of 60000 tonne for Circular LSAW pipes

RMTL’s technical capabilities and product approvals from key clients and

EPC contractors have enabled the company to bag orders from the likes

of L&T, NCC and other reputed EPC contractors.

Exhibit 6: Industry wide end use

Industry Application

Oil and Gas Pipeline

- Cross Country Oil & Gas Pipelines

- Spur Lines

- City Gas Distribution

- High Temperature & Low Temperature Pipes

Power Plant

- Cooling Water Line & Auxiliary Cooling Water Line

- Ash Handling Line

Water & Sewerage

- Distribution and Transmission Lines for Irrigation

- Pipes for Potable Water

- Drainage Pipes

Structural Use

- Piling and Casing Pipes

- Structural Columns

Other Industrial Use

- Pipes for Fertilizer Plant

- Mining Pipes

- Dredging Pipes

- Air Duct Piping

- High Mast Pipes for Wind Mill Towers

Source: Company, ICICIdirect.com Research

Exhibit 7: Gross revenue from carbon steel pipes & coating business (| crore)

586.6

888.0

1,061.3

844.0

-

200.0

400.0

600.0

800.0

1,000.0

1,200.0

FY14 FY15 FY16 FY17

Source: Company, ICICIdirect.com Research

Sales volume in last five years

129,349

156,933

204,718

179,655

-

50,000

100,000

150,000

200,000

250,000

FY14 FY15 FY16 FY17

Source: Company, ICICIdirect.com Research

Capacity utilisation levels in last five years

37%

45%

58%

51%

25%

35%

45%

55%

65%

FY14 FY15 FY16 FY17

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 5

Investment Rationale

Capex revival in oil & gas industry to bolster demand…

The oil & gas sector accounts for a lion’s share of the revenues of the

company. The sector accounted for ~54% of FY17 revenues while the

second highest share was held by the water and infra sector accounting

for 24%. The Indian oil & gas sector is at the cusp of a capex revival on

the back of a) enhancement in domestic refining capacity and b)

upgradation of refineries to meet the BS VI standard by 2020. We believe

a capex revival in the oil & gas sector will have a positive rub-off on the

financial performance of RMTL, going forward.

Exhibit 8: Industry-wise revenue pie (FY17)

Oil & Gas, 54%

Water & Infra, 24%

Power & Nuclear,

14%

Chemicals, 4%

Others, 4%

Source: Company, ICICIdirect.com Research

Exhibit 9: Refinery capacity addition plans over next 10-12 years

In MTPA Capacity as of 2017 Capacity Addition Capacity by 2030

PSU 151 106 257

Private 85 12 97

Total 236 118 354

Source: Company, ICICIdirect.com Research

Exhibit 10: Addressable opportunity for stainless steel tubes/pipes manufacturers (| crore)

Refinery Opportunity (| Crore)

Investment

(| Crore)

Timeframe

SS Pipes &

Tubes Share

SS Pipes &

Tubes Share

Annual

Oppurtunity

RMTL's

Share

Capacity up-gradation for BS VI 20,000 3 Years 4-6% 1,050 350 140

Greenfield Capacity by 2030 315,000 10-12 Years 4-6% 15,000 400-800 160-320

Replacement Demand - 250 100

Addressable Opportunity 1000-1400 400-560

Source: Company, ICICIdirect.com Research, RMTL’s share assumed @ 40%

The oil refining industry is likely to incur notable capex, going forward,

wherein the greenfield expansion would amount to ~| 315000 crore by

2030 while upgradation of existing refineries would entail another ~|

20000 crore. With ample opportunities opening up in the near to medium

term, RMTL is poised to be a key beneficiary as stainless steel seamless

and welded tubes & pipes industry constitutes 4-6% of overall capex in

refineries and petrochemicals. We believe the company may also witness

increased orders for carbon steel pipes, which find application in oil

country tubular goods as capex from domestic exploration players

commence. RMTL is also exploring opportunities in the global oil & gas

and refineries sector, in countries like the US, Middle East, Iran, Africa and

in the Far East. Furthermore, RMTL is also tracking developments with

regard to the government’s mandate on gas imports from other

countries. The management has indicated that it will leverage the

underlying capex momentum and actively participate in procuring orders.

ICICI Securities Ltd | Retail Equity Research Page 6

Proposed capacity addition in power sector to generate healthy demand

Exhibit 11: Addressable Opportunity from Power sector

Power Plant Opportunity Investment Timeframe

SS Pipes &

Tubes Share

SS Pipes &

Tubes Share

Annual

Oppurtunity

RMTL's

Share

New Power Plant (Thermal) 50,000 5 Yrs 3-4% 1750 350 140

Old thermal power equipment

(Upgradation & Modernisation)

75,000 5-10 Yrs 3-4% 2250 450 180

Nuclear Power Plants (7000 MW) 70,000 10 Yrs 3-4% 2800 280 112

Addressable Opportunity 1080 432

Source: Company, ICICIdirect.com Research

*The modernisation plan of old thermal plant has not yet commenced. The capex for the same will be incurred over

a period of 5-10 years once the plan kicks off, RMTL’s share assumed @ 40%.

On the power front, state owned power generation authorities like NTPC

are looking to phase out old and inefficient power plants (~11000 MW) in

coming years. They are likely to replace the same with new super critical

power plants. Estimated capex for the same is likely to be ~| 50000 crore

to be done in the next five years. This presents the company with an

opportunity to supply auxiliary systems as well as boiler tubes. The new

super critical power plants are expected to work more efficiently using

less coal. Power plants would require exotic alloy such as Inconel. With

the capability to produce exotic alloys, within the next few years, RMTL’s

seamless division is poised to gain substantially from this.

Apart from setting up new thermal power plants, the Government of India

(GoI) is also planning to carry out upgradation and modernisation of its

old thermal power generating facilities. In the medium to longer term

horizon, upgradation and modernisation plans are likely to entail an

aggregate capex of ~| 75000 crore. While the upgradation and

modernisation plan is yet to commence, the annual revenue potential

from the same is at | 450 crore for the next five years. Thus, stainless

steel tubes and pipes manufacturers like RMTL are likely to benefit from

such a sizable opportunity.

Similar to thermal power, the solar power sector is likely to witness

capacity addition, going forward. The Indian government has set a target

of achieving 100 GW of solar installation by 2022 (from current capacity of

12.5 GW). The company is well placed to cater to the rising demand from

both solar and thermal power installations with the capability to produce

desired grade.

ICICI Securities Ltd | Retail Equity Research Page 7

Ten new nuclear plants to open up new demand front…

Exhibit 12: Upcoming nuclear power plants

Capacity (MW)

Kaiga, Karnataka (Unit 5 & 6) 1,400

Chutka, Madhya Pradesh (Unit 1 & 2) 1,400

Gorakhpur, Haryana (Unit 3 & 4) 1,400

Mahi Banswara, Rajasthan (Unit 1, 2, 3 & 4) 2,800

Source: Company, ICICIdirect.com Research

1) The estimated capacity of each of the facility/unit mentioned above will be ~700 MW.

2) Currently India’s nuclear power capacity stands at 6780 MW with ~22 reactors under operations

The country’s nuclear power industry is to set witness its biggest

expansion phase in the near to medium term. The Government of India

has recently approved construction of 10 new nuclear power projects

aggregating a capacity of ~7000 MW. The new reactors are of

significantly higher capacity compared to the one under operation. RMTL

stands to benefit from the same, as it has an established track record of

supplying very critical pipes to the sector (such as moderator heater tube

and instrumentation tubes). Furthermore, with products like heat

exchanger tubes, which find critical application in a nuclear power plant,

the company is well suited to cater to the upcoming demand. The

management has indicated that in the next year or two the company will

target the very large requirement of the nuclear recycle board and waste

fuel storage facilities.

Over the longer term horizon, there are plans to increase nuclear capacity

to 63000 MW by 2032 (India’s current installed nuclear capacity stands at

6780 MW). This provides a strong visibility to Ratnamani Metals and

Tubes as it currently has approval from Nuclear Power Corporation of

India Limited (NPCIL) for the supply of critical instrumentation seamless

tubes for primary piping of nuclear reactors

ICICI Securities Ltd | Retail Equity Research Page 8

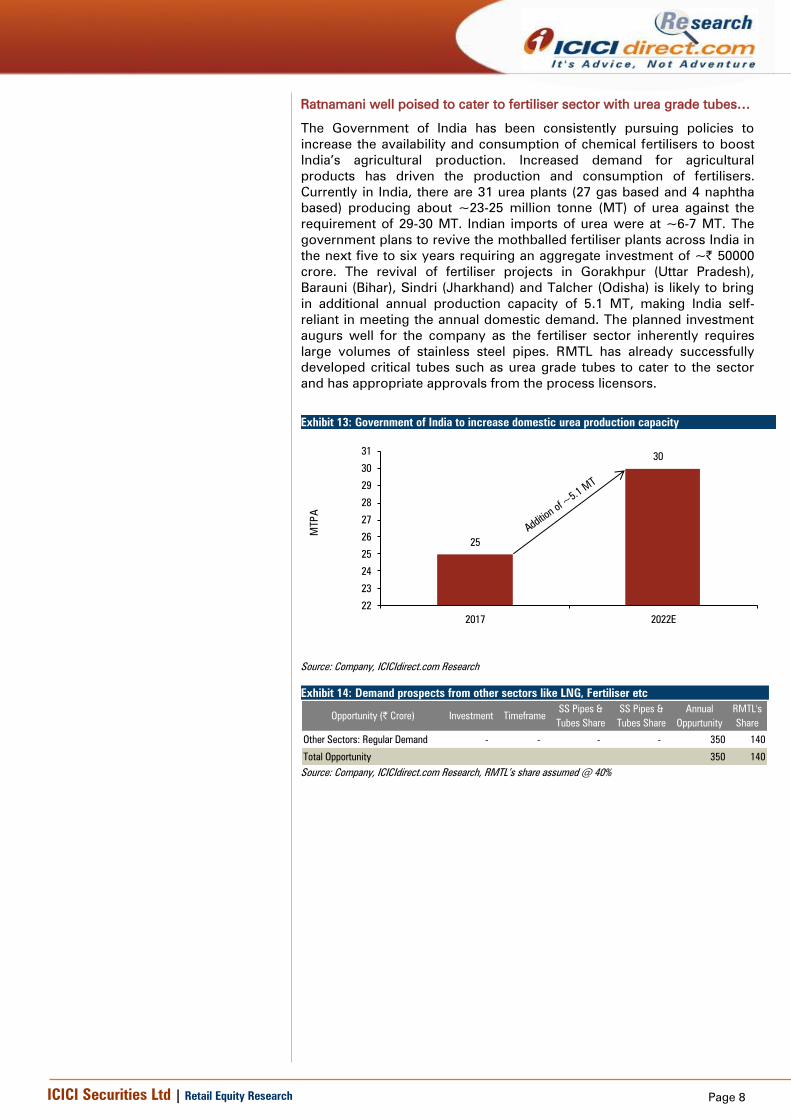

Ratnamani well poised to cater to fertiliser sector with urea grade tubes…

The Government of India has been consistently pursuing policies to

increase the availability and consumption of chemical fertilisers to boost

India’s agricultural production. Increased demand for agricultural

products has driven the production and consumption of fertilisers.

Currently in India, there are 31 urea plants (27 gas based and 4 naphtha

based) producing about ~23-25 million tonne (MT) of urea against the

requirement of 29-30 MT. Indian imports of urea were at ~6-7 MT. The

government plans to revive the mothballed fertiliser plants across India in

the next five to six years requiring an aggregate investment of ~| 50000

crore. The revival of fertiliser projects in Gorakhpur (Uttar Pradesh),

Barauni (Bihar), Sindri (Jharkhand) and Talcher (Odisha) is likely to bring

in additional annual production capacity of 5.1 MT, making India self-

reliant in meeting the annual domestic demand. The planned investment

augurs well for the company as the fertiliser sector inherently requires

large volumes of stainless steel pipes. RMTL has already successfully

developed critical tubes such as urea grade tubes to cater to the sector

and has appropriate approvals from the process licensors.

Exhibit 13: Government of India to increase domestic urea production capacity

25

30

22

23

24

25

26

27

28

29

30

31

2017 2022E

MTP

A

Source: Company, ICICIdirect.com Research

Exhibit 14: Demand prospects from other sectors like LNG, Fertiliser etc

Opportunity (| Crore) Investment Timeframe

SS Pipes &

Tubes Share

SS Pipes &

Tubes Share

Annual

Oppurtunity

RMTL's

Share

Other Sectors: Regular Demand - - - - 350 140

Total Opportunity 350 140

Source: Company, ICICIdirect.com Research, RMTL’s share assumed @ 40%

ICICI Securities Ltd | Retail Equity Research Page 9

Builds strong niche in stainless steel tubes and pipes domain…..

Ratnamani Metals and Tubes is a leading domestic player in the stainless

steel pipes and tubes segment (SS) having more than three decades of

experience in the SS production. The company has carved out a

dominant position in this segment, wherein it commands ~40% domestic

market share of stainless steel tubes/pipes for niche applications. In FY17,

this segment accounted for ~38% share in total pipe revenue of RMTL

and is mainly used for critical applications mandating a low failure rate

and long life. Hence, it is used in key industries like oil & gas,

petrochemical, refineries, thermal power, nuclear power, etc.

Within the stainless steel seamless segment, RMTL has focused on

manufacturing high value added products that are used for high end

applications while a majority of its peers are focused on low end

applications. Over the years, the company has developed expertise in

manufacturing customised stainless steel pipes, which are best in class

and tailor made to customer’s requirement. Pipes, which RMTL

manufacture, are used in a highly corrosive environment. As these pipes

also form a critical part of the process and carry a high failure cost, hence

approvals from customers are a key prerequisite of this sector. While the

approval is a key entry barrier in this segment, RMTL to its credit has

approvals from all leading industry majors thereby having an edge over

its competitors.

The entry barriers in the form of approval from clients, significant amount

of customisation, high-end products portfolio, etc, aid the company to

earn healthy margins for its SS products. The margin in the SS segment is

in the range of ~25%. Healthy margins from SS segment also support the

overall EBITDA margin of company. Consequently, this is clearly evident

in consistent & higher EBITDA margins that the company has reported in

the past. Compared to its peers, overall blended margins have

consistently been higher in the range of 16-19%.

One of the key advantages for RMTL has been its long standing

relationship with a majority of its clients that aids in procuring repeat

orders. With over three decades of experience, the company has

developed a strong client base. RMTL’s clients list ranges from private

entities like Reliance Industries, Larsen & Toubro, etc. to PSU majors like

BHEL, BPCL, HPCL, etc. Its client list also includes marquee foreign

companies such as Shell, British Petroleum, KOC, KNPC, etc.

Exhibit 15: Entry barriers in stainless steel pipes and tubes business

Competitive advantage company has over its peers

1 High capital requirement

2 Prerequisite approvals from customers & EPC contractors

3 Advanced nature of technology to offer customised products

4 High quality product with low failure rate

5 Development of strong clientele

Source: Company, ICICIdirect.com Research

Certifications and approvals

ISO 9001 : 2008 under TUV

ISO 14001 : 2004 under TUV

OHSAS 18001 : 2007 under TUV

License for API 5L, API 5LC and API 2B Monogram

ADW2 Certification under TUV

Pressure Equipment Directive [PED] under TUV

Approval by Engineers India Limited, PDIL and MECON

Approval by NPCIL for supply of critical Tubes / Pipes

NABL approval for CS Kutch facility

NORSOK approval for SS Seamless Mother hollow at Kutch

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 10

The revival in the capex cycle in the oil refinery, petrochemicals, power

and fertiliser sectors is likely to create robust demand for pipe companies,

going ahead. Expected investments in the oil & gas sector for upgrading

the current capacity and greenfield expansions could accelerate order

flows in the next few years. On the domestic front, two more greenfield

refineries in Barmer (Rajasthan) and Konkan (Maharashtra) have been

planned, which could start procurement in the next couple of years.

Further, owing to increasing urbanisation and industrialisation, the

government is focused on reviving the power sector. Considering the

significance of pipes, which RMTL has been supplying in the past two

decades, we expect it to benefit from the likely increase in order flows

from oil refinery, petrochemicals, power and fertiliser sectors, going

ahead.

Going forward, we expect a gradual improvement in the SSTP order

book, as most of the ordering for upgradation of refinery is likely to be

back-ended. Furthermore, the greenfield capex for expansion in refinery

capacity is progressing at a slower pace. The same is likely to pick up

pace over the medium to longer term horizon. We expect the capacity

utilisation (of the existing facility) to remain flattish in FY18E at 65% and

gradually improve to 75% in FY19E and further to 83% in FY20E as

traction picks up from key user industries.

Exhibit 16: SS capacity utilisation to improve (existing facility)

65% 65%

75%

83%

50%

55%

60%

65%

70%

75%

80%

85%

FY17 FY18E FY19E FY20E

Source: Company, ICICIdirect.com, Research

** Capacity utilisation of FY20E excludes utilisation level of new facility assumed at

~10%

Exhibit 17: SS volumes to grow at CAGR of ~11.3% during FY17-20E

18,229 18,213

21,000

25,100

-

5,000

10,000

15,000

20,000

25,000

30,000

FY17 FY18E FY19E FY20E

Source: Company, ICICIdirect.com, Research, the FY20E volume includes volumes

from new facility to the tune of 2000 tonnes.

ICICI Securities Ltd | Retail Equity Research Page 11

Capacity expansion in stainless steel business augurs well

RMTL has chalked out plans to set up a hot extrusion facility for large

diameter (dia) seamless stainless steel pipes and matching cold finishing

capacity. It is setting up incremental capacity of 20000 tonnes in the

stainless steel seamless tube and pipe segment at a capex of ~| 350-400

crore. This is expected to be commissioned by Q4FY19. The new facility

will be funded through internal accruals. This facility will make RMTL, the

only player in India with a capability to extrude from mother hollow pipes

of up to 8” in diameter against the company’s current capability of

extruding tubes up to only 2” diameter. After commissioning this new

facility, the company will be able to manufacture large dia pipes, which

will ensure import substitution as well as further penetrate the export

market. Given the limited competition domestically and high entry

barriers (long gestation period and stringent approvals), the capacity

expansion in the higher margin stainless steel business is likely to

enhance the company’s market share further.

While initially the upcoming facility would have lower margins (compared

to the existing stainless steel tube and pipe operations) and utilisation

would also be subdued, over the medium to longer term horizon the

management expects the facility to ramp up to optimum utilisation levels.

Subsequently, once the new capacity is fully ramped up, on account of

improved product offering, operating margins of this segment are

expected to tread higher than that of existing stainless steel business.

Once the operation of new plant stabilises, in the long run, the expansion

is likely to augment the company’s product suite and further strengthen

its niche capability.

Ratnamani’s current facility for stainless steel seamless

tubes/pipes having a capacity of 8000 tonnes is currently

operating at ~90% utilisation levels.

ICICI Securities Ltd | Retail Equity Research Page 12

Opportunities boost RMTL’s carbon steel division…

RMTL is also engaged in the production of carbon steel pipes business. In

this segment, the company produces LSAW, HSAW, ERW and coated

pipes. Carbon steel pipes derive their major demand from four sectors –

oil & gas transportation, sewerage, water distribution and irrigation. Each

of this is witnessing a structural improvement.

According to Petroleum Planning and Analysis Cell, India’s gas pipeline

network is under penetrated and currently pegged at ~16250 km with a

capacity of ~386.53 million standard cubic metres per day (mscmd). The

government plans to further add pipeline network of ~13000 km at

various locations across India. Any positive development boosting the

gas pipeline network in the country will benefit the company in terms of

increased demand. RMTL is also closely monitoring developments with

regard to the transnational pipelines coming up like – Turkmenistan-

Afghanistan-Pakistan-India (TAPI) pipeline project, Deep Sea Natural Gas

Pipeline from Middle East (Oman) to India and Pipeline involving

Bangladesh, Myanmar and India.

Steel pipe manufacturers in India have significant prospects emerging

from city gas distribution. The Petroleum and Natural Gas Regulatory

Board is mulling inviting fresh bids for 27 geographical areas (GA) under

the fifth and the sixth bidding rounds. The Ministry of Urban Development

has also selected 20 cities to be taken up for CGD network under the

smart cities initiative round I, of which tenders for 11 cities have been

called upon. RMTL is already executing orders for the CGD network and is

continuing to bid for newer businesses.

Exhibit 18: Carbon steel capacity utilisation levels to register up-tick

51%

63% 63%

65%

50%

52%

54%

56%

58%

60%

62%

64%

66%

68%

70%

FY17 FY18E FY19E FY20E

Source: Company, ICICIdirect.com Research

Exhibit 19: CS volumes to grow at CAGR of ~8% during FY17-20E

179655

218673 218750227500

0

50000

100000

150000

200000

250000

FY17 FY18E FY19E FY20E

Source: Company, ICICIdirect.com Research

The company’s orderbook is robust at ~| 1800 crore for

carbon steel pipes

On the back of strong demand visibility, the management

is planning to expand LSAW capacity to 100000 tonne at

its Kutch facility. However, they have indicated that the

expansion plan is on the drawing board currently

ICICI Securities Ltd | Retail Equity Research Page 13

On the water supply transportation front, government schemes like

AMRUT lay emphasis on water supply and proper sewerage facility and

septage management. The government’s focus on providing increased

drinking water supply and bringing in majority of agriculture land under

irrigation provides a massive scope for growth of water carrying pipeline.

The company has recently won orders of ~| 450 crore in the water

segment under the Sauni Yojana. Sauni Yojana refers to Saurashtra

Narmada Avtaran Irrigation project, which aims to fill 115 major dams by

diverting floodwaters overflowing from the Sardar Sarovar Dam across

the Narmada River to drought prone areas. The project is set to benefit

10.22 lakh acre land through total 1126 km four link pipelines

On the back of a healthy order book, the carbon steel segment is likely to

benefit from increased execution of pipeline network in India. We expect

the carbon steel division to report capacity utilisation levels of ~55-65%

during FY18-20E. EBITDA margins of the segment are likely to be in the

range of ~12% during FY18E and FY19E.

ICICI Securities Ltd | Retail Equity Research Page 14

Healthy order book provides strong earning visibility…

Over the last couple of years, Ratnamani has consistently maintained an

aggregate order book to the tune of ~| 700-800 crore. However, recently

there healthy traction was witnessed in the carbon steel segment order

book wherein the company won large ticket size orders, which boosted

the overall order book of the company. Recent order wins have resulted

in a healthy order book of ~| 2100 crore as on September 2017,

increasing from | 830 crore in May 2017. The current order book is split

between orders of ~| 1800 crore for carbon steel pipes and ~| 300 crore

for stainless steel orders. Of the total order book, domestic orders were at

~| 1500 crore while the export order book was at | 600 crore.

Exhibit 20: Consistency in order augurs well; current o/s order book at multi-year high…

0

500

1000

1500

2000

2500

Sep-1

3

Nov-1

3

Jan-1

4

Mar-

14

May-1

4

Jul-14

Sep-1

4

Nov-1

4

Jan-1

5

Mar-

15

May-1

5

Jul-15

Sep-1

5

Nov-1

5

Jan-1

6

Mar-

16

May-1

6

Jul-16

Sep-1

6

Nov-1

6

Jan-1

7

Mar-

17

May-1

7

Jul-17

Source: Company, ICICIdirect.com Research

With early signs of a capex revival in a majority of end user industries

coupled with a diversified product portfolio and competitive positioning in

the export market, the company has been witnessing positive order

inflows in the last couple of months. In August 2017, within the carbon

steel segment, the company has order inflows both in domestic and

export markets. On the domestic front, RMTL has bagged an order from

the Sauni Yojana for supply of 80000 tonne of carbon steel coated pipes

scheduled to be completed in the next 12 months. The total size of the

above-mentioned order is to the tune of ~| 450 crore. On the exports

front, the company has bagged an order to the tune of US$29 million

(~| 184 crore) for supply of carbon steel coated pipes scheduled to be

completed by March/April 2018.

Additionally, even in July 2017, in the CS segment the company had won

export orders to the US$ 22.1 million (~| 141 crore) for supply of carbon

steel welded pipes for the oil & gas sector scheduled to be completed by

May, 2018. Domestic order wins in July 2017, comprised two new orders

for supply of HSAW pipes aggregating to | 339 crore. Of the above

mentioned order, an order of | 214 crore is scheduled to be completed by

March 2018 while an order of | 125 crore is scheduled to be completed

by May 2018.

Going forward, on the back of a diversified product portfolio, we expect

healthy inflow in order book of both carbon steel as well as stainless steel

segment. While lately the order inflow in the stainless steel segment has

been subdued, we expect the same to pick up over the next few quarters

on the back of a revival in capex of both oil & gas and power sector.

In addition to the above, the company also bagged a domestic

order for supply of 80000 tonne of carbon steel coated pipes to

be completed in the next 12 months

Out of the total order book of ~| 2100 crore, the company has

export orders to the tune of ~| 600 crore while the domestic

orderbook was at ~| 1500 crore

ICICI Securities Ltd | Retail Equity Research Page 15

Addressable opportunity for stainless steel pipes sector…

Exhibit 21: Aggregate opportunity for stainless steel tubes and pipes manufacturers

Opportunity (| Crore) Investment Timeframe

SS Pipes &

Tubes Share

SS Pipes &

Tubes Share

Annual

Oppurtunity

RMTL's

Share

Refining: Capacity up-gradation for BS VI 20,000 3 Years 4-6% 1,050 350 140

Refining: Greenfield Capacity by 2030 315,000 10-12 Years 4-6% 15,000 400-800 160-320

Refining: Replacement Demand - - - - 250 100

Power: New Power Plants 50,000 5 Yrs 3-4% 1,750 350 140

Power: Thermal Power (Upgradation & Modernisation) 75,000 5-10 Yrs 3-4% 2250 450 180

Power: Nuclear Power Plant 70,000 10 Yrs 3-4% 2800 280 112

Other Sectors: Regular Demand (Fertiliser, LNG etc) - - - - 350 140

Total Opportunity 2430-2830 972-1132

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 16

Financials

Volume growth to accentuate revenues, going forward...

We expect RMTL’s net revenues to clock a CAGR of ~14.5% in FY17-20E

to | 2120 crore in FY20E from | 1411.7 crore in FY17 supported largely by

volume and realisation growth. We expect overall stainless steel volumes

to grow at ~11.3% CAGR in FY17-20E to 25100 tonne in FY20E from

18229 tonne in FY17.

The carbon steel division, which has been a major revenue contributor in

the past, is also likely to witness traction in order booking on the back of

increasing urbanisation, proposed pipeline gas network and government

schemes like AMRUT, which aims to clean water supply and proper

sewerage facility and septage management. We expect volumes of the

carbon steel division to increase from 179655 tonne in FY17 to 227500

tonne by FY20E clocking a CAGR of ~8.2%.

Going forward, over a long term horizon, the key trigger for the revenue

growth will be the commissioning of the proposed stainless steel

seamless tube facility by Q4FY19E, which will place Ratnamani in a sweet

spot with a revival in capex of the oil & gas sector, a key demand driver.

Exhibit 22: Expect revenues to increase at CAGR of ~14.5% in FY17-20E

1,411.7

1,660.5

1,898.8

2,120.0

-

500.0

1,000.0

1,500.0

2,000.0

2,500.0

FY17 FY18E FY19E FY20E

Source: Company, ICICIdirect.com Research

EBITDA to grow at CAGR of 15.6% in FY17-20E, margins set to increase...

On an absolute basis, EBITDA of the company is expected to grow at a

CAGR of ~15.6% in FY17-20E. We expect the company to report EBITDA

margins of 17.2% in FY18E, 17.7% in FY19E and 18.8% in FY20E. The

increasing contribution from stainless steel segment is expected to

accentuate the EBITDA and EBITDA margins, going forward.

Exhibit 23: EBITDA & EBITDA margins

257

285

337

398 18.2

17.2

17.7

18.8

16.0

16.5

17.0

17.5

18.0

18.5

19.0

-

50

100

150

200

250

300

350

400

450

500

FY17 FY18E FY19E FY20E

LHS : EBITDA (| Crore) RHS: EBITDA Margin (%)

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 17

PAT to grow at a CAGR of ~17.3% during FY17-20E

The PAT has increased from | 111.4 crore in FY12 to | 144.0 crore in

FY17. Going forward, PAT is expected to replicate the growth that is

witnessed in EBITDA. The company is likely to report a PAT of | 233 crore

in FY20E, clocking a CAGR of ~17.3%.

Exhibit 24: PAT & PAT margin trend, going forward...

144 158

193

233

10.2 9.5 10.2

11.0

8.5

9.0

9.5

10.0

10.5

11.0

11.5

-

50

100

150

200

250

300

FY16 FY17 FY18E FY19E

LHS : PAT (| Crore) RHS: PAT Margin (%)

Source: Company, ICICIdirect.com Research

Free cash flow generation…

The capex at its stainless steel seamless facility is estimated at ~| 350-

400 crore. The management has guided that capex would be funded

through internal accruals. The company’s networth as on March 31, 2017

was at | 1186.9 crore. Thus, with a strong networth base and healthy cash

flow generation capability, we believe the company will comfortably

undertake the proposed modest capex without stretching the balance

sheet as such. Going forward, we expect RMTL to generate a healthy FCF

of | 230 crore in FY20E.

RoCE, RoE to increase steadily...

Prudent capital allocation has been a key quality of the management. The

company meticulously increased its capacity over the years and has

concurrently been creating value for its stakeholders. This is evident from

the superior return ratio (RoCE and RoE) of the company. We have a

positive view on management’s ability to maximise the stakeholder

returns. We expect the RoCE and RoE to improve further to ~21% and

~15% by FY20E, respectively, from that of 18% and 13% in FY17.

Exhibit 25: RoCE & RoE trend

17.8 18.4

19.9

21.1

12.2 12.0

13.1

13.9

10.0

12.0

14.0

16.0

18.0

20.0

22.0

FY17 FY18E FY19E FY20E

ROCE ROE

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 18

Risk & Concerns

Any slowdown or trimming of proposed capex in oil & gas sector…

The oil & gas sector is by far the largest contributor to the revenue pie of

the company, contributing ~54%. During the last couple of years, a

slowdown in the oil & gas sector on account of falling crude oil prices had

resulted in sluggish capex thereby impacting the order book of the

company. With revival in the capex of the oil & gas sector, RMTL is in a

sweet spot to capitalise on the opportunity. However, any delay, deferral

or trimming of the capex is likely to result in lower volumes and revenues

for the stainless steel segment, thereby impacting the overall revenue

growth as well as profitability of the company.

Volatility in prices of raw material…

Nickel, a key input for manufacturing stainless steel, is up ~24% YTD.

This is likely to alter the cost dynamics of stainless steel producers and

lead to an increase in stainless steel prices. Coils, plates and ingots of

various grades of stainless steel and carbon steel are key raw material

inputs for the company. The company procures raw material from players

like Outokumpu, Arcelor group, SEAH Steel, and SMST etc. Any volatility

in raw material prices coupled with the company’s inability to pass it on to

its customers may have a material impact on the profitability of RMTL.

Suboptimal utilisation of new facility…

Initially, we expect the upcoming facility to report sub-optimal utilisation

levels and lower margin profile (compared to the existing stainless steel

tube and pipes operation). However, with the gradual ramping up of the

facility, utilisation levels are expected to reach their optimum, thereby

unlocking its true potential. The new capacity once ramped up will

enhance the company’s product offering and thereby its market share.

However, any under-utilisation of new capacity will drag the profitability

of the division, thereby materially impacting the overall EBIDTA and PAT

of the company.

Delay in project execution, approvals from clients for new facility…

Any delay in project completion beyond the estimated timeline of

Q4FY19E, may lead to cost and time overrun for the company.

Furthermore, the company would also require fresh approvals from the

end user for its new capacity. Any hindrance in approval from the

clientele is likely to adversely impact the volumes of the new facility,

thereby impacting its overall operational and financial performance.

Any protectionist measures in key geographies to impact exports…

Globally, to protect the domestic manufacturing industry, a majority of

countries have resorted to protectionist measures (like anti-dumping duty,

countervailing duty) against cheap imports (e.g. steel). RMTL has a

significant presence in the international markets, with ~18% revenues

coming from exports. Any protectionist measures adopted in key

geographical areas with regard to stainless steel are likely to have an

impact on the company’s export volumes and thereby its revenues.

ICICI Securities Ltd | Retail Equity Research Page 19

Valuation & Outlook

Ratnamani Metals and Tubes Limited (RMTL) have over three decades,

meticulously carved out a niche for itself in the stainless steel pipes and

tubes industry. The company has set up competitive capabilities for

products, which find critical application in end user industries like oil &

gas, refineries, power, nuclear and water. RMTL is capable of providing

customised products as per requirements while concurrently adhering to

quality standards, which mandate a low failure rate. Quality standards and

prerequisite approvals are key entry barriers in the stainless steel pipes

domain, as they find application in critical processes and carry high failure

cost. To its credit, the company has obtained approvals from all leading

industry majors thereby having an edge over its competitors. Thus, RMTL

commands a market share of ~40% in the niche stainless steel industrial

pipes domain.

The revival in capex in the end user industry such as oil & gas, refineries,

power and nuclear brightens the prospects of the stainless steel pipes

and tubes. In anticipation of such positive demand prospects, the

company is expanding its niche capability in the stainless steel seamless

pipes by setting up a facility of ~20000 tonnes. Going forward,

commissioning of this particular facility by the end of Q4FY19 will be a

key trigger for revenue growth, which will place the company in a sweet

spot with the said revival in capex. RMTL’s well established track record

makes it a formidable player to cater to the upcoming demand scenario.

RMTL’s carbon steel division further strengthens the company’s potential

domestically. The carbon steel division has witnessed a healthy pick-up in

order booking since Q1FY18. The company’s carbon steel pipes derive

their demand from oil & gas transportation, sewerage, water distribution

and irrigation. While the company has consistently maintained an

aggregate order book of ~| 700-800 crore, of late, the company has won

large ticket size orders boosting its order book position to ~| 2100 crore

as on August/September 2017. With healthy traction in both stainless as

well as carbon steel division and improving demand prospects, we expect

considerable orders to positively flow down in revenues as well as

profitability, going forward. We initiate coverage on the stock with a BUY

recommendation and a target price of | 1050 (average of EV/EBITDA

multiple: | 1103/share and P/E multiple: | 996 per share).

ICICI Securities Ltd | Retail Equity Research Page 20

Exhibit 26: Valuation

Valuation based on EV/EBITDA FY20E

EBITDA (| Crore) 398

Multiple (x) 12

Implied EV (| Crore) 4,770

Gross Debt (| Crore) -

Cash & Cash Eq (| Crore) 385

Implied Market Capitalisation (| Crore) 5,155

No. of Shares 4.7

Target Price (|) 1,103

Valuation based on PE Multiple FY20E

EPS 50

Multiple (x) 20

Target (|) 996

Weighted Target Price (|) 1,050

Source: Company, ICICIdirect.com Research

Exhibit 27: Two year forward EV/EBITDA

0

1000

2000

3000

4000

5000

6000

7000

8000

Apr-

09

Oct-

09

Apr-

10

Oct-

10

Apr-

11

Oct-

11

Apr-

12

Oct-

12

Apr-

13

Oct-

13

Apr-

14

Oct-

14

Apr-

15

Oct-

15

Apr-

16

Oct-

16

Apr-

17

(| C

rore

)

EV 18.0x 15.0x 12.0x 9.0x 6.0x 3.0x

Source: Company, ICICIdirect.com Research

Exhibit 28: Two year forward PE Band

0

200

400

600

800

1000

1200

1400

Oct-08

Jan-09

Apr-09

Jul-09

Oct-09

Jan-10

Apr-10

Jul-10

Oct-10

Jan-11

Apr-11

Jul-11

Oct-11

Jan-12

Apr-12

Jul-12

Oct-12

Jan-13

Apr-13

Jul-13

Oct-13

Jan-14

Apr-14

Jul-14

Oct-14

Jan-15

Apr-15

Jul-15

Oct-15

Jan-16

Apr-16

Jul-16

Oct-16

Jan-17

Apr-17

Jul-17

(|)

Price 28x 24x 20x 16x 12x 8x 4x

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 21

Annexure

Stainless steel - key product offerings

Heat exchanger tubes

A heat exchanger is a device used to transfer heat between a solid object

and a fluid, or between two or more fluids. The fluids may be separated

by a solid wall to prevent mixing or they may be in direct contact. They

are widely used in space heating, refrigeration, air conditioning, power

stations, chemical plants, petrochemical plants, petroleum refineries, and

natural gas processing and sewage treatment. The classic example of a

heat exchanger is an internal combustion engine in which a circulating

fluid known as engine coolant flows through radiator coils and air flows

past the coils, which cools the coolant and heats the incoming air.

Instrumentation Tubes

Instrumentation is measurement and control of process variables within a

production or manufacturing area. The process variables used in

industries are level, pressure, temperature, humidity, flow, pH, force,

speed, etc. Control engineering is the engineering discipline that applies

control theory to design systems with a desired behaviour.

Instrumentation tubes are used to connect various pressure gauges,

pressure switches, valves and flow monitors on industrial piping and

ventilation systems. Various types of fluids, gases pass through these

tubes at high pressure. Considering the above factors, the application of

instrumentation tubes is considered very critical. Instrumentation in

petrochemical industries basically consists of flow meters, pressure

transmitters, level sensors, temperature sensors and analysis instruments.

Stainless steel seamless pipes

In a seamless pipe, there is no welding or joints and it is manufactured

from solid round billets. The seamless pipe is finished to dimensional and

wall thickness specifications in sizes from 1/8 inch to 26 inch OD. This is

applicable for high-pressure applications like hydrocarbon industries &

refineries, oil & gas exploration and drilling, oil & gas transportation and

air and hydraulic cylinders, bearings, boilers and automobiles.

Stainless steel welded pipes

The weld procedures used depend upon the wall thickness of input raw

material for pipe manufacturing. The company has a number of tube mills

for manufacturing the stainless steel welded pipes from coils up to 18” NB

in double random length. The welding process is controlled by laser seam

tracking equipment to optimise the quality of the weld seam. The

company is capable of manufacturing pipes above 40" NB & up to 72" NB

with a combination of longitudinal/circumferential joints.

ICICI Securities Ltd | Retail Equity Research Page 22

Carbon steel - Key product offerings…

High frequency electric resistance welded pipes

RMTL has a carbon steel HF-ERW pipes capacity of 100,000 MT. HF-ERW

pipes are made from hot rolled flat steel strip, formed into tubular shape

while the longitudinal seam is welded by application of mechanical

squeezing of edges and heating edges through high frequency electric

resistance applied by induction or conduction. The weld joint is achieved

without addition of any filler metal. RMTL is capable of manufacturing as

per API 5L grade API X-80 or equivalent. In order to meet international

standard, the company has an in-house all testing facility. The product

can be manufactured in various types (circular hollow, square hollow,

rectangular hollow sections) with varied diameter range.

Submerged arc welded (SAW) pipes

A carbon steel SAW pipe manufacturing facility consists of a JCO press,

helical/spiral mills, number of three roll plate bending machine, inside &

outside welding lines, heat treatment furnace and all necessary testing

equipment to produce high quality pipes conforming to various

international standards. The facilities are capable of manufacturing pipes

in various grades.

Mobile plant: The company has ventured into manufacturing

pipes at the site by way of mobile plant. The mobile plant caters

to customer requirement on location. The plant can be dismantled

and re-erected within a short span. This unique feature helps in

easy handling of pipes at site, meeting delivery schedules and cut

down transportation cost, thus making the project economical

and viable

o LSAW pipes

Longitudinally welded steel pipes are used in onshore and offshore oil

and gas pipelines requiring critical service, high performance and

tight tolerances. The key differentiation between LSAW and HSAW

pipes is the welding process used in manufacturing these pipes. In

LSAW pipes, the welding is longitudinal, which means that steel (hot

rolled coil plate) is rolled into a pipe and the seam is welded

longitudinally. In the HSAW type, steel coils are welded spirally, like a

helix, so that the coil (strip) assumes the shape of a pipe. LSAW pipes

play a major role in oil & gas pipelines with features of high strength,

high quality and long distance. According to the standard of American

Petroleum Institute (API), the LSAW pipe is the only designated pipe

in large scale oil & gas transportation, especially when pipelines cross

densely populated urban areas and first & second class cities. Given

the rigorous product requirement norms, LSAW pipes garner higher

margins compared to HSAW pipes. Ratnamani’s LSAW pipes division

is likely to be see traction in orderbook through city gas distribution

opportunity.

Pipe coating solutions

Under the segment, the company provides both internal and external

pipes coating solutions. The external coatings provide anti-corrosion,

anti-abrasion protection for small and large diameter pipelines at high

operating temperatures. The internal liquid coating plant is designed to

apply a suitable spray coating on the inside surface of pipes for

transportation of oil, gas, water & any types of liquids, which facilitates

smooth improved flow and also provides corrosion protection to the

internal surface of steel pipe.

ICICI Securities Ltd | Retail Equity Research Page 23

Financial Summary

Exhibit 29: Income Statement

(Year-end March) FY17 FY18E FY19E FY20E

Total Operating Income 1,411.7 1,660.5 1,898.8 2,120.0

Growth (%) -17.8% 17.6% 14.4% 11.7%

Raw Material Expenses 880.5 1,051.6 1,201.5 1,325.0

Employee Expenses 97.8 112.2 123.4 132.5

Other Manufacturing Expenses 176.0 211.7 237.3 265.0

Total Operating Expenditure 1,154.3 1,375.4 1,562.3 1,722.5

EBITDA 257.4 285.1 336.5 397.5

Growth (%) -9.5% 10.8% 18.1% 18.1%

Interest & Finance Cost 6.1 6.0 6.3 6.7

Depreciation 59.7 63.2 64.9 80.7

Other Income 13.9 20.0 22.8 37.3

PBT before Exceptional Items 205.5 235.8 288.1 347.5

Less: Exceptional Items 0.0 0.0 0.0 0.0

PBT 205.5 235.8 288.1 347.5

Total Tax 61.2 77.8 95.1 114.7

PAT 144.3 158.0 193.0 232.8

Growth (%) -12.0% 9.5% 22.2% 20.6%

EPS 30.9 33.8 41.3 49.8

Source: Company, ICICIdirect.com Research

Exhibit 30: Balance Sheet

(Year-end March) FY17 FY18E FY19E FY20E

Equity Capital 9.3 9.3 9.3 9.3

Reserve and Surplus 1,177.6 1,305.5 1,468.5 1,671.2

Total Shareholders funds 1,186.9 1,314.9 1,477.8 1,680.6

Total Debt - - - -

Deferred Tax Liability 47.3 48.0 48.8 48.5

Other Non Current Liabilities - - - -

Source of Funds 1,234.2 1,362.9 1,526.6 1,729.1

Gross Block - Fixed Assets 919.4 967.7 992.7 1,402.7

Accumulated Depreciation 471.3 534.5 599.4 680.0

Net Block 448.1 433.2 393.3 722.7

Capital WIP 38.3 115.0 375.0 10.0

Net Fixed Assets 486.4 548.2 768.3 732.7

Investments 73.9 73.9 73.9 73.9

Inventory 339.1 409.4 468.2 522.8

Cash 14.7 100.2 37.8 237.3

Debtors 425.2 432.2 442.2 493.7

Loans & Advances & Other CA 73.6 73.2 72.9 72.8

Total Current Assets 852.7 1,015.0 1,021.1 1,326.6

Creditors 117.1 204.7 260.1 319.5

Provisions & Other CL 61.7 69.5 76.7 84.6

Total Current Liabilities 178.8 274.2 336.8 404.1

Net Current Assets 673.9 740.8 684.4 922.5

Other Assets - - - -

Application of Funds 1,234.2 1,362.9 1,526.6 1,729.1

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 24

Exhibit 31: Cash flow Statement

(Year-end March) FY17 FY18E FY19E FY20E

Profit/(Loss) after taxation 144.3 158.0 193.0 232.8

Add: Depreciation & Amortization 59.7 63.2 64.9 80.7

Net (Increase) / decrease in Current Assets (63.2) (76.9) (68.5) (106.0)

Net Increase / (decrease) in Current Liabilities (23.5) 95.5 62.6 67.3

CF from operating activities 117.3 239.8 251.9 274.8

(Inc)/dec in Investments (53.8) - - -

(Inc)/dec in Fixed Assets (52.4) (125.0) (285.0) (45.0)

Others - - - -

CF from investing activities (106.2) (125.0) (285.0) (45.0)

Inc / (Dec) in Equity Capital - - - -

Inc / (Dec) in Loans (8.9) - - -

Dividend & Dividend Tax (30.1) (30.1) (30.1) (30.1)

Others 31.8 0.8 0.8 (0.3)

CF from financing activities (7.2) (29.3) (29.3) (30.3)

Net Cash flow 3.8 85.5 (62.4) 199.5

Opening Cash 10.8 14.7 100.2 37.8

Closing Cash 14.7 100.2 37.8 237.3

Source: Company, ICICIdirect.com Research

Exhibit 32: Key Ratios

(Year-end March) FY17 FY18E FY19E FY20E

Per share data (|)

EPS 30.9 33.8 41.3 49.8

Cash EPS 43.7 47.3 55.2 67.1

BV 254.0 281.4 316.3 359.6

DPS 5.5 5.5 5.5 5.5

Cash Per Share 100.9 114.4 128.3 145.5

Operating Ratios (%)

EBITDA margins 18.2 17.2 17.7 18.8

PBT margins 14.6 14.2 15.2 16.4

Net Profit margins 10.2 9.5 10.2 11.0

Inventory days 88 90 90 90

Debtor days 110 95 85 85

Creditor days 30 45 50 55

Return Ratios (%)

RoE 12.2 12.0 13.1 13.9

RoCE 17.8 18.4 19.9 21.1

RoIC 16.7 19.3 24.4 21.4

Valuation Ratios (x)

P/E 28.2 25.7 21.1 17.5

EV / EBITDA 15.7 13.9 12.0 9.6

EV / Revenues 2.9 2.4 2.1 1.8

Market Cap / Revenues 2.9 2.4 2.1 1.9

Price to Book Value 3.4 3.1 2.8 2.4

Solvency Ratios

Debt / Equity 0.0 0.0 0.0 0.0

Debt/EBITDA 0.0 0.0 0.0 0.0

Current Ratio 4.7 3.3 2.9 2.7

Quick Ratio 2.8 1.8 1.5 1.4

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 25

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns

ratings to its stocks according to their notional target price vs. current market price and then categorises them

as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and the notional

target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk,

ICICI Securities Limited,

1st

Floor, Akruti Trade Centre,

Road No. 7, MIDC,

Andheri (East)

Mumbai – 400 093

ICICI Securities Ltd | Retail Equity Research Page 26

Disclaimer

ANALYST CERTIFICATION

We /I, Dewang Sanghavi MBA (FIN) and Akshay Kadam MBA (FIN), Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report

accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or

view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities

Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has

its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which

are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking

and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts

and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and

meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without

prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securitiesis under no obligation to update or keep the information current.

Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended

temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this

company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific

circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment

objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate

the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any

loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the

risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to

change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment

in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned

in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any

compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts

and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Dewang Sanghavi MBA (FIN) and Akshay Kadam MBA (FIN), Research Analysts of this report have not received any compensation from the companies mentioned in the report in the

preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month

preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

It is confirmed that Dewang Sanghavi MBA (FIN) and Akshay Kadam MBA (FIN), Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and

to observe such restriction.