Embed Size (px)

Citation preview

1 Quick Success Series – Remittance & Collection

Page 1

QUICK SUCCESS SERIES

LEGAL ASPECTS OF BANKING

QUICK SUCCESS SERIES, an initiative of SBLC Deoghar to facilitate the preparation of pro-motion seeking personnel of our Bank, appears to have succeeded in its objective to a large ex-tent, as the readers are still approaching us for its revision/updation despite availability of plenty of other study materials.

We would not have been able to sustain this unique effort of ours, without the active sup-port and continuous encouragement of our DGM cum Circle Development officer Sri Bi-jayananda Padhi. We are deeply indebted to him for his co-operation and guidance. Sri Rakesh Roshan, Chief Manager (Training) ,Sri Kumar Priyank, Chief Manager (Training) Sri Sanjay Kumar Sharma,Manager (Training and Sri Jitendra Kumar Arun, Manager (Train-ing) at this SBLC have owned up this project and have taken pains to keep it relevant to the users by updating & improving it at half yearly interval.

Though every care has been taken while up-dating the contents, we request our readers to point out any lapses at the earliest. Needless to mention this book is not a substitute of cir-cular instructions issued by the Bank from time to time. For detailed guidelines please refer to Bank’s latest circulars. Soft copy of this edition is available on our ftp://10.151.51.33 in QSS folder and on SBI TIMES>PATNA CIRCLE>SBLC Deoghar site.

Team SBLC Deoghar is humbled by the re-sponse and recognition, it is receiving from the readers within and beyond the circle. We wish the readers grand success in their endeavours.

Sri Abhishek Kumar Sharma Assistant General Manager, State Bank Learning Centre, Deoghar- 814112 Phone- 06432-232895 Fax - 06432-231810 E-mail: [email protected]

Updated up to 31st October 2016

Updated By: Rakesh Roshan Chief Manager (Training), SBLC Deoghar Mobile- 9162370185 Email- [email protected]

Quick Success Series

Legal Aspects Of Banking

Updated up to 31st October 2016

2

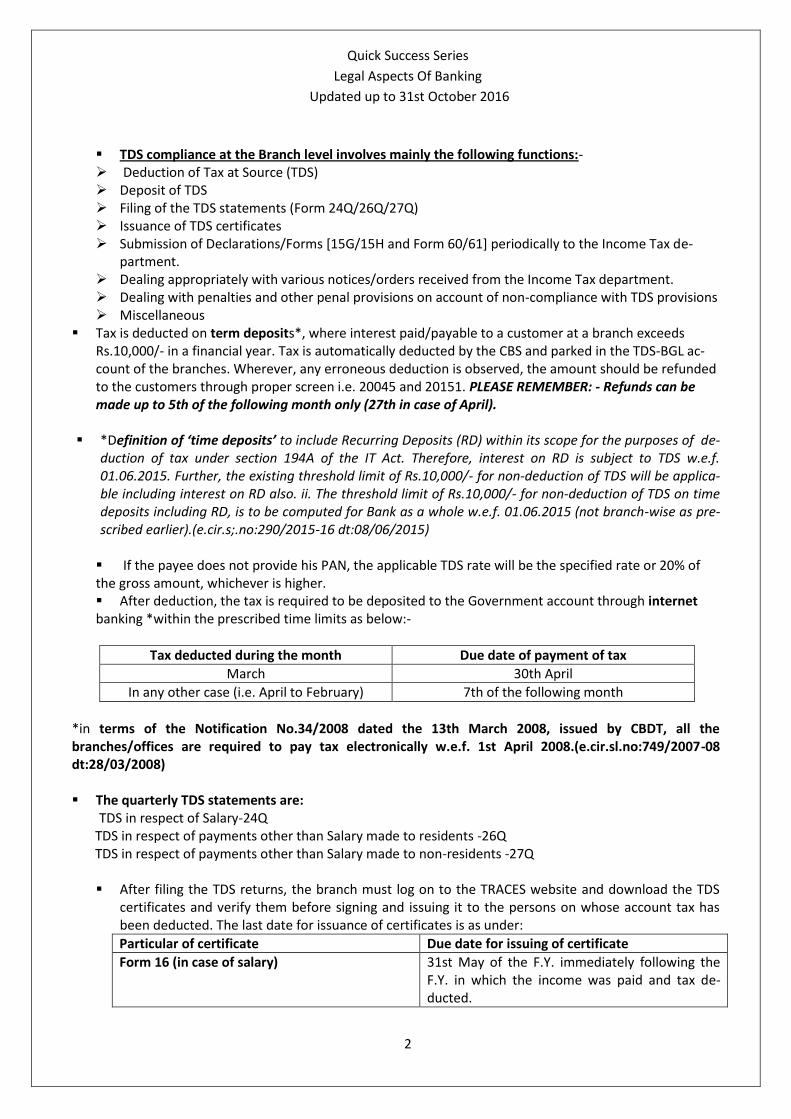

TDS compliance at the Branch level involves mainly the following functions:- Deduction of Tax at Source (TDS) Deposit of TDS Filing of the TDS statements (Form 24Q/26Q/27Q) Issuance of TDS certificates Submission of Declarations/Forms [15G/15H and Form 60/61] periodically to the Income Tax de-

partment. Dealing appropriately with various notices/orders received from the Income Tax department. Dealing with penalties and other penal provisions on account of non-compliance with TDS provisions Miscellaneous

Tax is deducted on term deposits*, where interest paid/payable to a customer at a branch exceeds Rs.10,000/- in a financial year. Tax is automatically deducted by the CBS and parked in the TDS-BGL ac-count of the branches. Wherever, any erroneous deduction is observed, the amount should be refunded to the customers through proper screen i.e. 20045 and 20151. PLEASE REMEMBER: - Refunds can be made up to 5th of the following month only (27th in case of April).

*Definition of ‘time deposits’ to include Recurring Deposits (RD) within its scope for the purposes of de-

duction of tax under section 194A of the IT Act. Therefore, interest on RD is subject to TDS w.e.f. 01.06.2015. Further, the existing threshold limit of Rs.10,000/- for non-deduction of TDS will be applica-ble including interest on RD also. ii. The threshold limit of Rs.10,000/- for non-deduction of TDS on time deposits including RD, is to be computed for Bank as a whole w.e.f. 01.06.2015 (not branch-wise as pre-scribed earlier).(e.cir.s;.no:290/2015-16 dt:08/06/2015)

If the payee does not provide his PAN, the applicable TDS rate will be the specified rate or 20% of the gross amount, whichever is higher. After deduction, the tax is required to be deposited to the Government account through internet banking *within the prescribed time limits as below:-

Tax deducted during the month Due date of payment of tax

March 30th April

In any other case (i.e. April to February) 7th of the following month

*in terms of the Notification No.34/2008 dated the 13th March 2008, issued by CBDT, all the branches/offices are required to pay tax electronically w.e.f. 1st April 2008.(e.cir.sl.no:749/2007-08 dt:28/03/2008) The quarterly TDS statements are:

TDS in respect of Salary-24Q TDS in respect of payments other than Salary made to residents -26Q TDS in respect of payments other than Salary made to non-residents -27Q

After filing the TDS returns, the branch must log on to the TRACES website and download the TDS

certificates and verify them before signing and issuing it to the persons on whose account tax has been deducted. The last date for issuance of certificates is as under:

Particular of certificate Due date for issuing of certificate

Form 16 (in case of salary)

31st May of the F.Y. immediately following the F.Y. in which the income was paid and tax de-ducted.

Quick Success Series

Legal Aspects Of Banking

Updated up to 31st October 2016

3

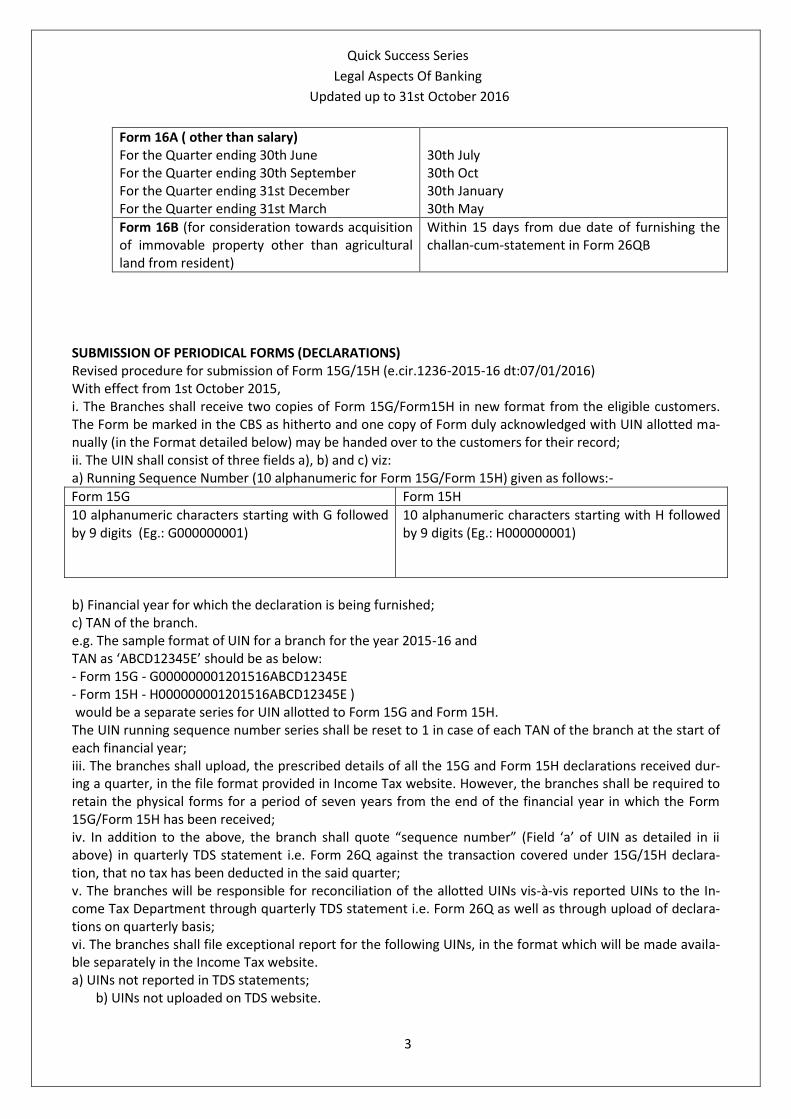

Form 16A ( other than salary) For the Quarter ending 30th June For the Quarter ending 30th September For the Quarter ending 31st December For the Quarter ending 31st March

30th July 30th Oct 30th January 30th May

Form 16B (for consideration towards acquisition of immovable property other than agricultural land from resident)

Within 15 days from due date of furnishing the challan-cum-statement in Form 26QB

SUBMISSION OF PERIODICAL FORMS (DECLARATIONS) Revised procedure for submission of Form 15G/15H (e.cir.1236-2015-16 dt:07/01/2016) With effect from 1st October 2015, i. The Branches shall receive two copies of Form 15G/Form15H in new format from the eligible customers. The Form be marked in the CBS as hitherto and one copy of Form duly acknowledged with UIN allotted ma-nually (in the Format detailed below) may be handed over to the customers for their record; ii. The UIN shall consist of three fields a), b) and c) viz: a) Running Sequence Number (10 alphanumeric for Form 15G/Form 15H) given as follows:-

Form 15G Form 15H

10 alphanumeric characters starting with G followed by 9 digits (Eg.: G000000001)

10 alphanumeric characters starting with H followed by 9 digits (Eg.: H000000001)

b) Financial year for which the declaration is being furnished; c) TAN of the branch. e.g. The sample format of UIN for a branch for the year 2015-16 and TAN as ‘ABCD12345E’ should be as below: - Form 15G - G000000001201516ABCD12345E - Form 15H - H000000001201516ABCD12345E ) would be a separate series for UIN allotted to Form 15G and Form 15H. The UIN running sequence number series shall be reset to 1 in case of each TAN of the branch at the start of each financial year; iii. The branches shall upload, the prescribed details of all the 15G and Form 15H declarations received dur-ing a quarter, in the file format provided in Income Tax website. However, the branches shall be required to retain the physical forms for a period of seven years from the end of the financial year in which the Form 15G/Form 15H has been received; iv. In addition to the above, the branch shall quote “sequence number” (Field ‘a’ of UIN as detailed in ii above) in quarterly TDS statement i.e. Form 26Q against the transaction covered under 15G/15H declara-tion, that no tax has been deducted in the said quarter; v. The branches will be responsible for reconciliation of the allotted UINs vis-à-vis reported UINs to the In-come Tax Department through quarterly TDS statement i.e. Form 26Q as well as through upload of declara-tions on quarterly basis; vi. The branches shall file exceptional report for the following UINs, in the format which will be made availa-ble separately in the Income Tax website. a) UINs not reported in TDS statements;

b) UINs not uploaded on TDS website.

Quick Success Series

Legal Aspects Of Banking

Updated up to 31st October 2016

4

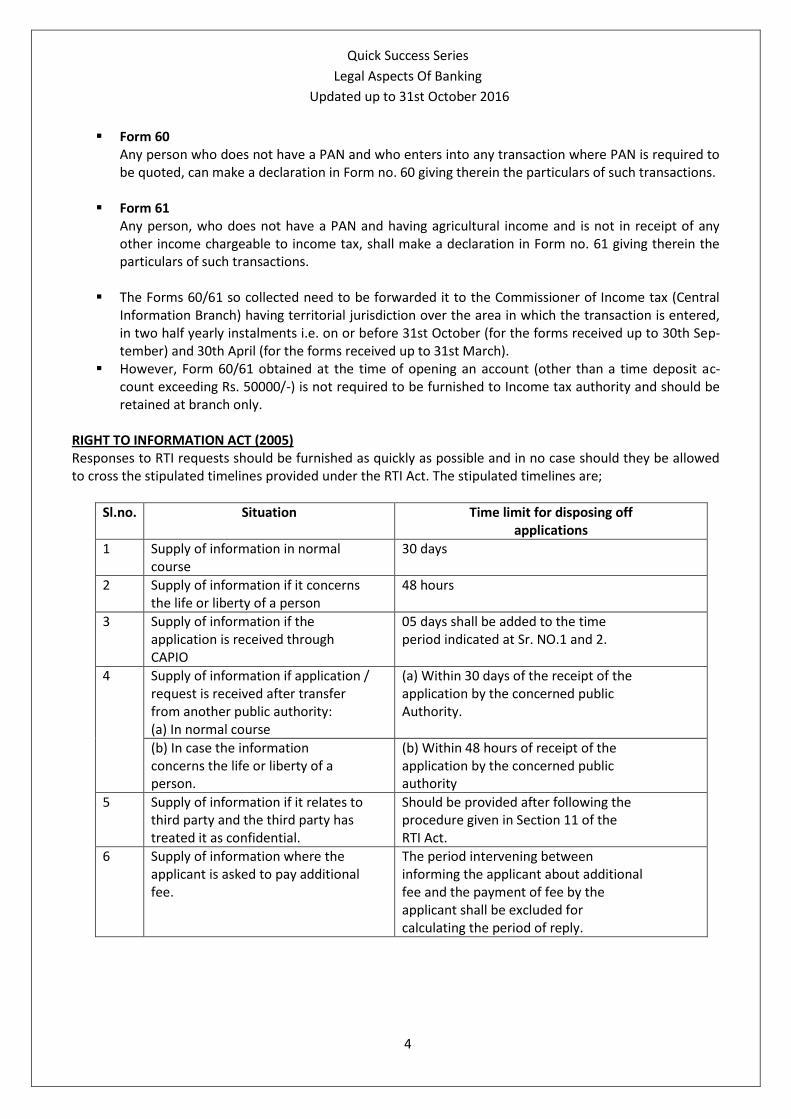

Form 60 Any person who does not have a PAN and who enters into any transaction where PAN is required to be quoted, can make a declaration in Form no. 60 giving therein the particulars of such transactions.

Form 61

Any person, who does not have a PAN and having agricultural income and is not in receipt of any other income chargeable to income tax, shall make a declaration in Form no. 61 giving therein the particulars of such transactions.

The Forms 60/61 so collected need to be forwarded it to the Commissioner of Income tax (Central

Information Branch) having territorial jurisdiction over the area in which the transaction is entered, in two half yearly instalments i.e. on or before 31st October (for the forms received up to 30th Sep-tember) and 30th April (for the forms received up to 31st March).

However, Form 60/61 obtained at the time of opening an account (other than a time deposit ac-count exceeding Rs. 50000/-) is not required to be furnished to Income tax authority and should be retained at branch only.

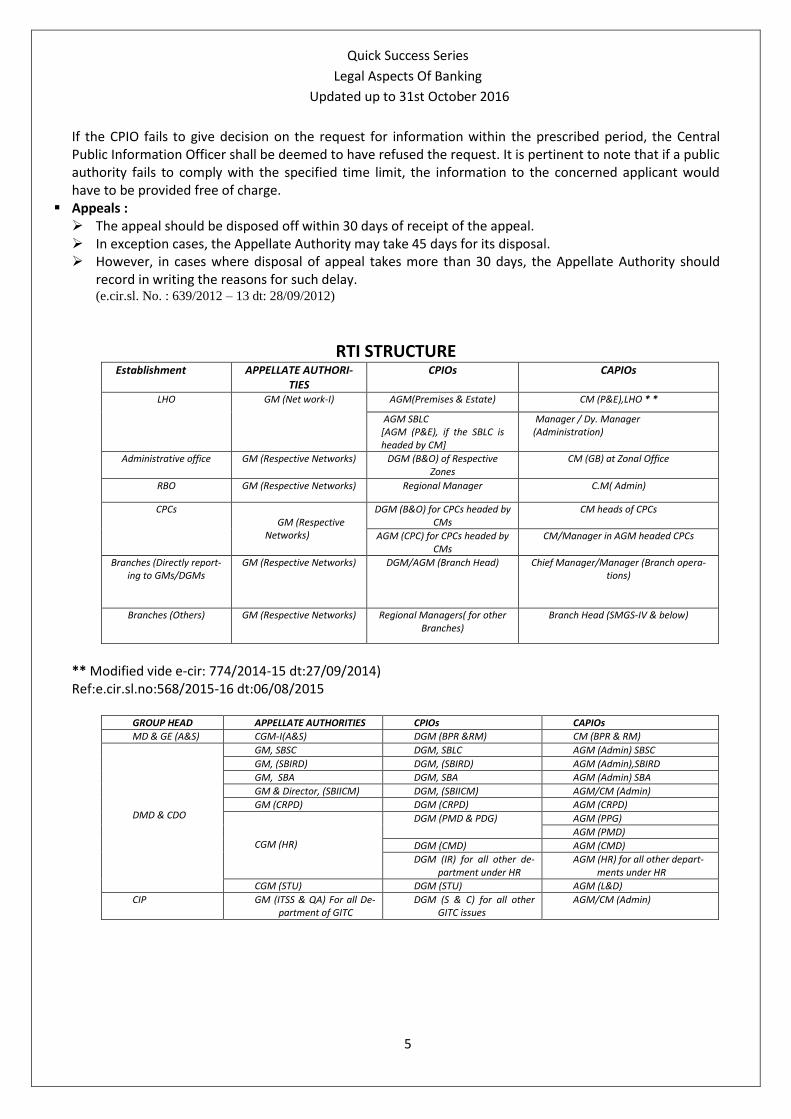

RIGHT TO INFORMATION ACT (2005) Responses to RTI requests should be furnished as quickly as possible and in no case should they be allowed to cross the stipulated timelines provided under the RTI Act. The stipulated timelines are;

Sl.no. Situation Time limit for disposing off applications

1 Supply of information in normal course

30 days

2 Supply of information if it concerns the life or liberty of a person

48 hours

3 Supply of information if the application is received through CAPIO

05 days shall be added to the time period indicated at Sr. NO.1 and 2.

4 Supply of information if application / request is received after transfer from another public authority: (a) In normal course

(a) Within 30 days of the receipt of the application by the concerned public Authority.

(b) In case the information concerns the life or liberty of a person.

(b) Within 48 hours of receipt of the application by the concerned public authority

5 Supply of information if it relates to third party and the third party has treated it as confidential.

Should be provided after following the procedure given in Section 11 of the RTI Act.

6 Supply of information where the applicant is asked to pay additional fee.

The period intervening between informing the applicant about additional fee and the payment of fee by the applicant shall be excluded for calculating the period of reply.

Quick Success Series

Legal Aspects Of Banking

Updated up to 31st October 2016

5

If the CPIO fails to give decision on the request for information within the prescribed period, the Central Public Information Officer shall be deemed to have refused the request. It is pertinent to note that if a public authority fails to comply with the specified time limit, the information to the concerned applicant would have to be provided free of charge.

Appeals : The appeal should be disposed off within 30 days of receipt of the appeal. In exception cases, the Appellate Authority may take 45 days for its disposal. However, in cases where disposal of appeal takes more than 30 days, the Appellate Authority should

record in writing the reasons for such delay. (e.cir.sl. No. : 639/2012 – 13 dt: 28/09/2012)

RTI STRUCTURE Establishment

APPELLATE AUTHORI-TIES

CPIOs CAPIOs

LHO GM (Net work-I) AGM(Premises & Estate) CM (P&E),LHO * *

AGM SBLC [AGM (P&E), if the SBLC is headed by CM]

Manager / Dy. Manager (Administration)

Administrative office GM (Respective Networks) DGM (B&O) of Respective Zones

CM (GB) at Zonal Office

RBO GM (Respective Networks) Regional Manager C.M( Admin)

CPCs GM (Respective

Networks)

DGM (B&O) for CPCs headed by CMs

CM heads of CPCs

AGM (CPC) for CPCs headed by CMs

CM/Manager in AGM headed CPCs

Branches (Directly report-ing to GMs/DGMs

GM (Respective Networks) DGM/AGM (Branch Head) Chief Manager/Manager (Branch opera-tions)

Branches (Others) GM (Respective Networks) Regional Managers( for other Branches)

Branch Head (SMGS-IV & below)

** Modified vide e-cir: 774/2014-15 dt:27/09/2014) Ref:e.cir.sl.no:568/2015-16 dt:06/08/2015

GROUP HEAD APPELLATE AUTHORITIES CPIOs CAPIOs

MD & GE (A&S) CGM-I(A&S) DGM (BPR &RM) CM (BPR & RM)

DMD & CDO

GM, SBSC DGM, SBLC AGM (Admin) SBSC

GM, (SBIRD) DGM, (SBIRD) AGM (Admin),SBIRD

GM, SBA DGM, SBA AGM (Admin) SBA

GM & Director, (SBIICM) DGM, (SBIICM) AGM/CM (Admin)

GM (CRPD) DGM (CRPD) AGM (CRPD)

CGM (HR)

DGM (PMD & PDG) AGM (PPG)

AGM (PMD)

DGM (CMD) AGM (CMD)

DGM (IR) for all other de-partment under HR

AGM (HR) for all other depart-ments under HR

CGM (STU) DGM (STU) AGM (L&D)

CIP GM (ITSS & QA) For all De-partment of GITC

DGM (S & C) for all other GITC issues

AGM/CM (Admin)

Quick Success Series

Legal Aspects Of Banking

Updated up to 31st October 2016

6

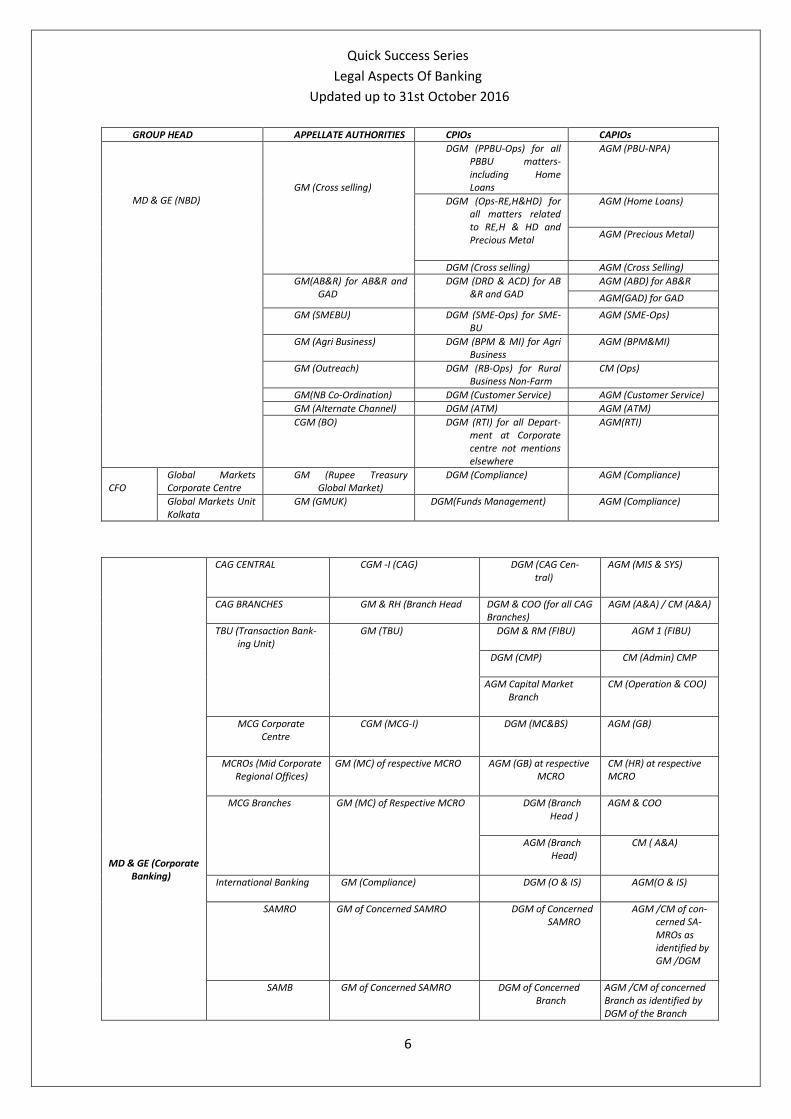

GROUP HEAD APPELLATE AUTHORITIES CPIOs CAPIOs

MD & GE (NBD)

GM (Cross selling)

DGM (PPBU-Ops) for all PBBU matters-including Home Loans

AGM (PBU-NPA)

DGM (Ops-RE,H&HD) for all matters related to RE,H & HD and Precious Metal

AGM (Home Loans)

AGM (Precious Metal)

DGM (Cross selling) AGM (Cross Selling)

GM(AB&R) for AB&R and GAD

DGM (DRD & ACD) for AB &R and GAD

AGM (ABD) for AB&R

AGM(GAD) for GAD

GM (SMEBU) DGM (SME-Ops) for SME-BU

AGM (SME-Ops)

GM (Agri Business) DGM (BPM & MI) for Agri Business

AGM (BPM&MI)

GM (Outreach) DGM (RB-Ops) for Rural Business Non-Farm

CM (Ops)

GM(NB Co-Ordination) DGM (Customer Service) AGM (Customer Service)

GM (Alternate Channel) DGM (ATM) AGM (ATM)

CGM (BO) DGM (RTI) for all Depart-ment at Corporate centre not mentions elsewhere

AGM(RTI)

CFO

Global Markets Corporate Centre

GM (Rupee Treasury Global Market)

DGM (Compliance) AGM (Compliance)

Global Markets Unit Kolkata

GM (GMUK) DGM(Funds Management) AGM (Compliance)

MD & GE (Corporate Banking)

CAG CENTRAL

CGM -I (CAG)

DGM (CAG Cen-tral)

AGM (MIS & SYS)

CAG BRANCHES

GM & RH (Branch Head

DGM & COO (for all CAG Branches)

AGM (A&A) / CM (A&A)

TBU (Transaction Bank-ing Unit)

GM (TBU)

DGM & RM (FIBU)

AGM 1 (FIBU)

DGM (CMP)

CM (Admin) CMP

AGM Capital Market Branch

CM (Operation & COO)

MCG Corporate Centre

CGM (MCG-I)

DGM (MC&BS)

AGM (GB)

MCROs (Mid Corporate Regional Offices)

GM (MC) of respective MCRO

AGM (GB) at respective MCRO

CM (HR) at respective MCRO

MCG Branches

GM (MC) of Respective MCRO

DGM (Branch Head )

AGM & COO

AGM (Branch Head)

CM ( A&A)

International Banking

GM (Compliance)

DGM (O & IS)

AGM(O & IS)

SAMRO

GM of Concerned SAMRO

DGM of Concerned SAMRO

AGM /CM of con-cerned SA-MROs as identified by GM /DGM

SAMB

GM of Concerned SAMRO

DGM of Concerned Branch

AGM /CM of concerned Branch as identified by DGM of the Branch

Quick Success Series

Legal Aspects Of Banking

Updated up to 31st October 2016

7

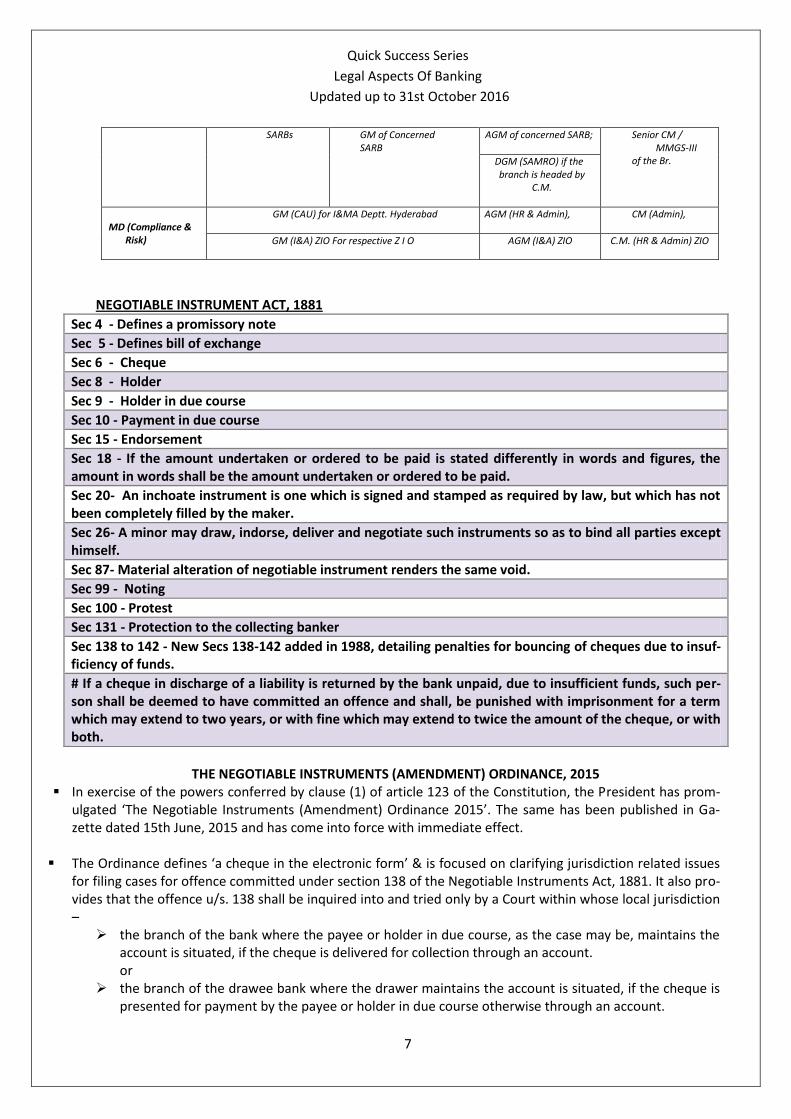

SARBs

GM of Concerned SARB

AGM of concerned SARB;

Senior CM / MMGS-III

of the Br. DGM (SAMRO) if the branch is headed by

C.M.

MD (Compliance &

Risk)

GM (CAU) for I&MA Deptt. Hyderabad

AGM (HR & Admin),

CM (Admin),

GM (I&A) ZIO For respective Z I O AGM (I&A) ZIO C.M. (HR & Admin) ZIO

NEGOTIABLE INSTRUMENT ACT, 1881

Sec 4 - Defines a promissory note

Sec 5 - Defines bill of exchange

Sec 6 - Cheque

Sec 8 - Holder

Sec 9 - Holder in due course

Sec 10 - Payment in due course

Sec 15 - Endorsement

Sec 18 - If the amount undertaken or ordered to be paid is stated differently in words and figures, the amount in words shall be the amount undertaken or ordered to be paid.

Sec 20- An inchoate instrument is one which is signed and stamped as required by law, but which has not been completely filled by the maker.

Sec 26- A minor may draw, indorse, deliver and negotiate such instruments so as to bind all parties except himself.

Sec 87- Material alteration of negotiable instrument renders the same void.

Sec 99 - Noting

Sec 100 - Protest

Sec 131 - Protection to the collecting banker

Sec 138 to 142 - New Secs 138-142 added in 1988, detailing penalties for bouncing of cheques due to insuf-ficiency of funds.

# If a cheque in discharge of a liability is returned by the bank unpaid, due to insufficient funds, such per-son shall be deemed to have committed an offence and shall, be punished with imprisonment for a term which may extend to two years, or with fine which may extend to twice the amount of the cheque, or with both.

THE NEGOTIABLE INSTRUMENTS (AMENDMENT) ORDINANCE, 2015

In exercise of the powers conferred by clause (1) of article 123 of the Constitution, the President has prom-ulgated ‘The Negotiable Instruments (Amendment) Ordinance 2015’. The same has been published in Ga-zette dated 15th June, 2015 and has come into force with immediate effect.

The Ordinance defines ‘a cheque in the electronic form’ & is focused on clarifying jurisdiction related issues for filing cases for offence committed under section 138 of the Negotiable Instruments Act, 1881. It also pro-vides that the offence u/s. 138 shall be inquired into and tried only by a Court within whose local jurisdiction –

the branch of the bank where the payee or holder in due course, as the case may be, maintains the account is situated, if the cheque is delivered for collection through an account. or

the branch of the drawee bank where the drawer maintains the account is situated, if the cheque is presented for payment by the payee or holder in due course otherwise through an account.

Quick Success Series

Legal Aspects Of Banking

Updated up to 31st October 2016

8

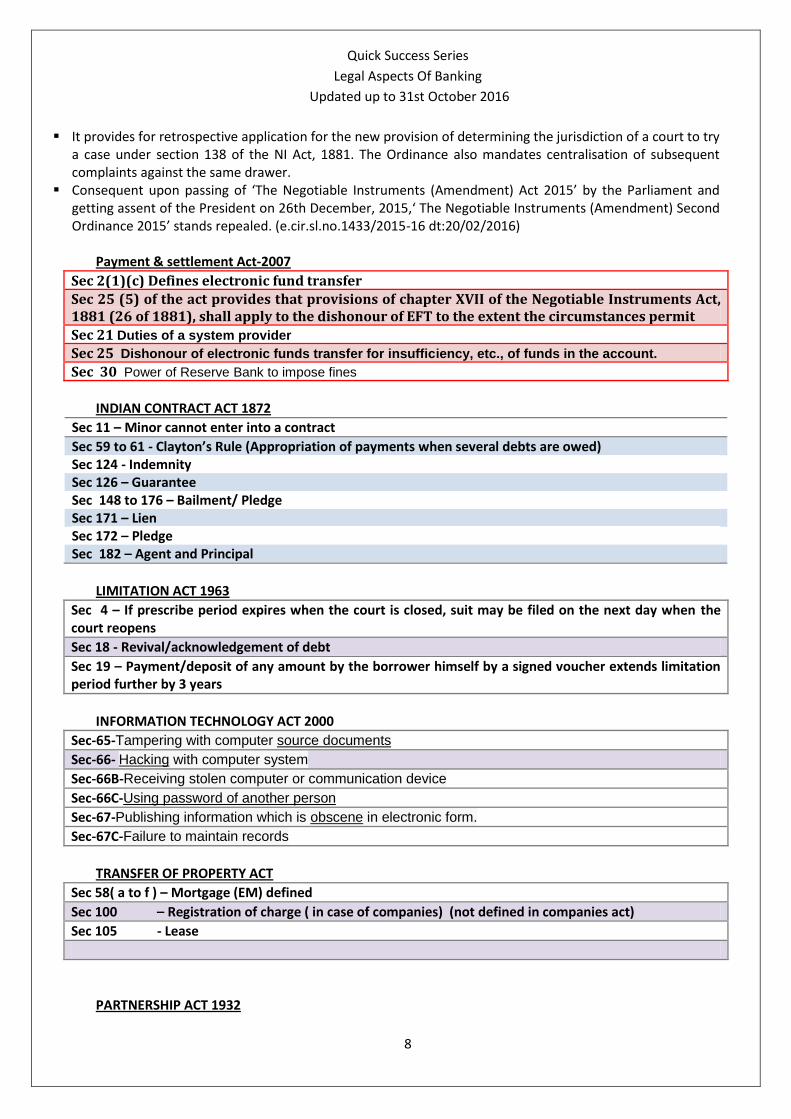

It provides for retrospective application for the new provision of determining the jurisdiction of a court to try a case under section 138 of the NI Act, 1881. The Ordinance also mandates centralisation of subsequent complaints against the same drawer.

Consequent upon passing of ‘The Negotiable Instruments (Amendment) Act 2015’ by the Parliament and getting assent of the President on 26th December, 2015,‘ The Negotiable Instruments (Amendment) Second Ordinance 2015’ stands repealed. (e.cir.sl.no.1433/2015-16 dt:20/02/2016)

Payment & settlement Act-2007

Sec 2(1)(c) Defines electronic fund transfer

Sec 25 (5) of the act provides that provisions of chapter XVII of the Negotiable Instruments Act, 1881 (26 of 1881), shall apply to the dishonour of EFT to the extent the circumstances permit

Sec 21 Duties of a system provider

Sec 25 Dishonour of electronic funds transfer for insufficiency, etc., of funds in the account.

Sec 30 Power of Reserve Bank to impose fines

INDIAN CONTRACT ACT 1872

Sec 11 – Minor cannot enter into a contract

Sec 59 to 61 - Clayton’s Rule (Appropriation of payments when several debts are owed) Sec 124 - Indemnity Sec 126 – Guarantee Sec 148 to 176 – Bailment/ Pledge Sec 171 – Lien Sec 172 – Pledge Sec 182 – Agent and Principal

LIMITATION ACT 1963

Sec 4 – If prescribe period expires when the court is closed, suit may be filed on the next day when the court reopens

Sec 18 - Revival/acknowledgement of debt

Sec 19 – Payment/deposit of any amount by the borrower himself by a signed voucher extends limitation period further by 3 years

INFORMATION TECHNOLOGY ACT 2000

Sec-65-Tampering with computer source documents

Sec-66- Hacking with computer system

Sec-66B-Receiving stolen computer or communication device

Sec-66C-Using password of another person

Sec-67-Publishing information which is obscene in electronic form.

Sec-67C-Failure to maintain records

TRANSFER OF PROPERTY ACT

Sec 58( a to f ) – Mortgage (EM) defined

Sec 100 – Registration of charge ( in case of companies) (not defined in companies act)

Sec 105 - Lease

PARTNERSHIP ACT 1932

Quick Success Series

Legal Aspects Of Banking

Updated up to 31st October 2016

9

Sec 25 – Joint and several liability of partners

Sec 30 – A minor can be admitted to the benefits of a partnership but cannot become a partner.

Sec 42 - Death, insolvency of a partner dissolves the partnership

Sec 69 – A registered firm can file a suit against others to enforce rights arising from a contract but an un-registered firm cannot. The creditors of an unregistered firm can file a suit against the firm

SBI ACT 1955

Sec 32 – Act as agent of RBI

Sec 34 1 (b) – Cannot lend against its own share

Sec 39 – Balance Sheet to be prepared as at 31st March

RBI ACT 1934

Sec 28 - Note refund rules

Sec 35- RBI can carry out inspection of any bank

Sec 42 – Schedule/Non-Schedule banks defined.

Sec 42(1&6) – CRR to be maintained with RBI and it is fixed on market situations

Sec 45 – Nationalised banks can conduct Govt. business as agent of RBI

Sec 49 – Bank rate

[ A bearer draft cannot be issued ( sec 31). A fine up to the amount of the bearer draft issued may be im-posed on the bank ( sec 58 B ) ]

Sec 24- RBI issues all currency notes for denomination 2,5,10,20,50,100,500,1000,5000,10000. It has the power to direct discontinuation or non-issue of currency notes of any denomination.

BANKING REGULATION ACT 1949

Sec 6 – Forms of business a bank can transact

Sec 11 – Min paid up capital and reserves

Sec 19 – Restrictions regarding advances against shares

Sec 20 – Bank cannot grant loan against its own shares as it will amount to a reduction in its capital

Sec 24 – SLR maintenance

Sec 29 – Publication of balance sheet every year

Sec 35 – Inspection of branches by RBI

Sec 35A – Ombudsman appointed

Sec 45 –Return of paid instrument to customers

Sec 45ZA to ZF – Nomination facility

CONSUMER PROTECTION ACT (COPRA) 1986

District Forum

3 members

Term is 5 years

Claims up to Rs 20 lac

Appeal against it can be filed within 30 days

State Commission

3 members

Claims > Rs 20 lac up to Rs 100 lac

Appeal will be allowed if either 50% amount ordered by district forum or Rs Rs 25000/- whi-chever is less, is deposited

Quick Success Series

Legal Aspects Of Banking

Updated up to 31st October 2016

10

National Commission

5 members

Claims > Rs 100 lac

Appeal will be allowed if the appellate deposits 50% of the amount ordered by State Com-mission or Rs Rs 35000/- whichever is less

INCOME TAX ACT-1961

Sec 194 – TDS (Tax Deducted at Source)

Sec 269 - If the aggregate of principal of a term deposit and interest is Rs 20000/- or more then payment should not be made in cash.

Sec 271 – If violated Sec 269, the official responsible has to pay the penalty up to the amount of Term De-posit

IMPORTANT POINTS RE-LATED TO LEGAL ASPECTS

Bankers’ Books Evidence Act came into

existence in year 1891. Bankers’ books include ledgers, day books,

cash books, micro films, magnetic tapes etc.

Certified copy means a copy of any entry in the books of a bank together with a cer-tificate that it is true copy of the original entry.

Maintenance of SLR: max 40% Pursuant to the amendment of the Banking

Regulation Act, 1949, section 26A has been inserted in that Act, empowering Reserve Bank to establish a Depositor Education and Awareness Fund (the Fund). Under the provisions of this section the amount to the credit of any account in India with any bank which has not been operated upon for a period of ten years or any depo-sit or any amount remaining unclaimed for more than ten years shall be credited to the Fund, within a period of three months from the expiry of the said period of ten years.

Every scheduled commercial banks has to publish its B/S & P&L A/c as on 31.03 latest by June 30th of every year.

Garnishee order is issued under Civil Procedure code (1908) act

A complaint under Consumer Protection Act can be filed within 2 years from the

date on which the cause of action has ari-sen.

The ROC on the application of the compa-ny, on being satisfied that the company had sufficient cause for not filing particu-lars of charge within 30 days may allow registration after 30 days but within a pe-riod of 300 days from the date of creation of charge.

If the particulars of charge or for modifica-tion or satisfaction of charge are not filed within 300 days the company or any per-son interested in registration of charge can file an application to the Central Govt. for condonation of delay and extension of time for filing particulars of charges. Central Govt. can impose conditions for extension of time. IMPORTANT- It is important to note that it is imperative that charges created in favour of the Bank are regis-tered within a period of 30 days from the date of creation of charge. Otherwise it is possible that Bank may lose priority of charge created in favour of the Bank.

Reserve Bank of India vide their circular dated 07.06.2013 advised all banks to sub-ject the title deeds and other loan docu-ments in respect of all exposures of Rs 5 Crs and above to periodical legal audit and re-verification of title deeds with relevant authorities as part of regular audit exercise till the loans are fully repaid.

As per Legal Audit Plan, the Auditors for conducting the Legal Audit shall be out-

Quick Success Series

Legal Aspects Of Banking

Updated up to 31st October 2016

11

sourced and reputed Legal Firms/ Advo-cates empanelled with our Bank would carry out Legal Audit by visiting the branches where the accounts are being operated and documents are kept.

The Legal Audit shall be conducted pref-erably 3 months before the commence-ment of RFIA / Credit Audit, so that auditee branches can comply with rectification of the deficiencies pointed out. A separate Legal Audit Report Format (LARF) to be submitted by Legal Auditor has been de-signed. The format contains Value State-ments pertaining to documentation, mort-gage, charge creation, etc., corresponding to Value Statements in the existing Credit Audit Report Format (CARF).

RFIA / Credit Auditors will award scores based on the Legal Audit observations and compliances by the branch during their respective audits. The score so awarded will be integrated in the Credit Manage-ment Score of the Branch. The Legal Audit is a regulatory prescription and its progress will be reported to Bank’s ACB on quarterly basis.

Criminals Procedure Code came into existence in 1973 year.

Clayton’s Rule defines Appropriation of payments when several debts are owned. (under sec 59 to 61 of Indian Contract Act)

Quasi Contracts means Loans to minors to meet necessaries of life are binding on the minor’s estate. When the same person is the drawer

and the drawee of an instrument, the holder can treat the instrument as Bill of exchange or Promissory note ( e.g. Banker’s cheque)

Inchoate instruments means incom-plete instruments wherein some de-tails would have been left blank.

If no rate of interest is mentioned in the Promissory note intt @ 18% p.a is to be paid.

Dishonour of cheques are defined in sec 138 to 142 of NI Act.

On the dishonour of a cheque the payee must give a notice to the

drawer within 30 days days of the re-ceipt of information from the bank.

Scheduled Banks defined as The names of banks with capital and re-serves of Rs 5 lakhs and above will be included in the II schedule to the Act ( S 42)

If the aggregate of principal of a term deposit and interest is Rs 20000/- or more then payment should not be made in cash.

A minor can be admitted to the bene-fits of a partnership. (But he cannot become a partner; also documents will be signed by the guardian on minor’s behalf).

A registered partnership firm can sue third parties to enforce rights arising from a contract. An unregistered firm cannot; the creditors of an unregis-tered firm can sue the firm.

Forms of legal representation: Legal Representation is a legal decision granted on the death of a person owning property or money in order to dispose-off the said property or mon-ey. It is governed by the provisions of the Indian Succession Act, 1925. The three forms of legal representations are (a) probate (b) letter of Adminis-tration and (c) Succession certificate.

a) Probate: If the deceased has left a will, it must be first produced in a court. The court after satisfying itself that it is the last will of deceased and was duly executed, will issue a pro-bate, empowering the executor of the will to do all acts specified in the will. The executer is appointed by the per-son making the will. A copy of the will is always attached to the probate. A probate is only conclusive as to the appointment of executer and validity of the will. It applies to both movable and immovable properties. A probate issued by a High court is valid throughout India. If it is issued by a district court, the probate is valid within the state and in case the value

Quick Success Series

Legal Aspects Of Banking

Updated up to 31st October 2016

12

of property outside the state does not exceed Rs.10, 000/-, it is even valid outside the state. If a supplementary will called (a codicil) is discovered af-ter the grant of a probate, a separate probate of that codicil may be granted to the executer.

b) Letter of Administration: It is issued by a court in favour of an Adminis-trator (i) when the deceased has not left a will or (ii) when the deceased has left a will but has not named an executor, or (iii) the executor named therein refuses to act or he himself is dead .A letter of administra-tion covers not only debts due to the de-ceased and transferable securities but also all kinds of movable and immovable prop-erties. It is valid throughout India if issued by a High court. If it is issued by a District Court, it is valid within the state. However, if the value of the property outside the state does not exceed Rs.10,000/ even a letter of administration issued by a District Court is valid throughout the Country.

c) Succession Certificate: A Succession Certificate is granted when the deceased has not left any will It is issued to the legal heirs in respect of only debts and securi-ties. It is to be noted that a succession cer-tificate does not cover gold loan ornaments articles in safe deposit/safe deposit lockers etc. It is valid throughout India even if granted by a District Court. The certificate should specify the debts and securities and will be granted in a special form. The certif-icate empowers a person to whom it is granted to collect debt and securities and interest thereon.

Credit Information Companies (Regu-

lations) Act, 2005(CIC Act) and the Rules and Regulations framed there under have come into force with effect from December 14, 2006. Section 17 of the CIC (Regulations)Act, 2005 provides for collection (from members) and fur-nishing (to specified users) of credit in-formation by Credit Information Com-

panies. The CIC Act provides statutory backing for sharing of credit informa-tion by Credit Institutions with Credit Information Companies subject to con-ditions stipulated therein. Therefore with CIC Act coming into force, the “consent clause” has become redun-dant and hence the consent of the bor-rower prescribed vide Annexure- I & II of Circular No. CPP/CKG/CIR/40 dated 13.11.2002, need not be insisted upon now. (e-cir:461/2013-14 dt:03/08/2013)

Since the Govt. of India has directed the Bank to establish Facilitation cen-ters to help less conversant bidders, who intend to participate in e-auction under SARFAESI / DRT. The branches, which conduct e-auction under SAR-FAESI / DRT, should make arrange-ments for Facilitation Center to provide all information about the process of e-auction and facilitate the bidders to bid in the e -auction in a transparent man-ner.(e-cir:544/2013-14 dt:24/08/2013)

Guidelines on KYC/AML/CFT measures are issued by Reserve Bank of India un-der Section 35A of the Banking Regula-tion Act, 1949 and Rule 7 of Prevention of Money- Laundering (Maintenance of Records) Rules, 2005.

As per Rule 114B it is compulsory to quote PAN in all documents pertaining to financial transactions notified from time to time by CBDT.

Person not having the PAN are to make a declaration in form No. 60/61, giving therein the particulars of such transac-tions. Person with agricultural income and those who are not in receipt of any income chargeable to tax, have to make a declaration in Form No.61.

RBI has permitted Banks to formulate a scheme for providing services at the premises of a customer (Doorstep bank-ing) under section 23 of Banking Regula-tion act 1949.

SARFAESI-2002 Act came into force from 21st August 2002.Under the act a

Quick Success Series

Legal Aspects Of Banking

Updated up to 31st October 2016

13

secured creditor shall have the following powers:-(i) To take possession, sell or lease the secured assets (both movable and immovable assets, (ii) To take over the management of the business of the borrower, (iii) To appoint a manager, (iv) To recover any money payable by third parties to the borrower, (v) In case a joint financing under consortium or multiple lending arrangement, if 75% of the secured creditors in value agree to initiate recovery actions, the same shall be binding on all the secured creditors. Securitization: A process by which a single asset or a pool of assets are transferred from the balance sheet of the originator (bank) to a bankruptcy remote SPV (trust) in return for an im-mediate cash payment.

An entity which may be a trust, com-pany or other entity constituted or es-tablished by a ‘Deed’ or ‘Agreement’ for a specific purpose.

Minutes of the Board meetings and the memoranda are commercial confidence for the Bank and are exempted from disclosure in terms of Section 8(1)(d) of the RTI Act, 2005. (e-cir:899/2013-14 dt:07/09/2013)

The Mental Health Act, 1987 provides for a law relating to the treatment and care of mentally ill persons and to make better provision with respect to their property and affairs.

According to the said Act, “Mentally ill person” means a person who is in need of treatment by reason of any mental disorder other than mental retardation. Sections 53 and 54 of this Act provide for the appointment of guardians for mentally ill persons and in certain cases, managers in respect of their property. The prescribed appointing authorities are the district courts and collectors of districts under the Mental Health Act, 1987. (e-cir:1188/2013-14 dt:23/01/2014).

RBI has now advised that banks are insisting on guardianship certificate from all mentally ill persons. In this re-gard it is clarified that paragraph 2(iii) of our aforesaid ecircular is not intended to insist on appointment of a guardian as a matter of routine from every per-son “who is in need of treatment by reason of any mental disorder”. Branches should seek for appointment of a guardian only in such cases, where they are convinced on their own or based on documentary evidence availa-ble, that the concerned person is men-tally ill and is not able to enter into a va-lid and legally binding contract. (e-cir:1416/2015--16 dt:16/02/2016)

Major Changes Brought In By Banking

Law (Amendments) Act, 2012 The said Amendment Act has amended

the BR Act, the Banking Companies (Ac-quisition and Transfer of Undertakings) Act, 1970, the Banking Companies (Ac-quisition and Transfer of Undertakings) Act, 1980 and also made consequential amendments to certain other enact-ments including the Indian Stamp Act, 1899 and the Indian Contract Act, 1972

Amendment to Section 12 to provide for issue of preference shares:

Amendment to the said Section now enables banks to issue preference shares subject to the guidelines to be framed by RBI. However banks cannot proceed to issue preference shares and have to wait for RBI to prescribe guide-lines in respect of the same.

The amendment also provides that pro-visions of Section 87(2)(b) of the Com-panies Act, 1956 will not be applicable. Thus default in payment of dividend would not confer voting rights (in re-spect of all resolutions placed before the general meeting of the bank) to holders of preference share capital of a Bank.

The preference shareholders in a bank will continue to have power to vote in

Quick Success Series

Legal Aspects Of Banking

Updated up to 31st October 2016

14

respect of matters affecting their rights directly as provided in Section 87(2).

Banks may alter the capital clause in the Memorandum of Association such that the capital clause contains the two classes of shares viz., equity shares and preference shares.

The amendment to Section 12 also pro-vides power to RBI for increasing the ceiling on a phased manner for exercise of voting rights on poll from 10% to 26% in a bank. Earlier there was no such power and voting rights was restricted to 10% of the total voting rights.

Insertion of new Section 26A for setting up DEAF: Depositor Education and Awareness Fund: By this section, RBI has been empowered to establish Depositor Education and Awareness Fund. Funds lying in any non-operative accounts for 10 years or more or any deposits not claimed for 10 years or more in a bank now requires to be credited to the said Fund within 3 months from the expiry of 10 years.

Insertion of new Section 29A for seeking annexure of financial statements of as-sociate enterprise of the bank: This Sec-tion provides power to RBI to require a bank to annex to its financial statements or to provide separately the financial statements of any associate enterprise like holding company, subsidiary com-pany, joint venture company etc. or to cause inspection of books of accounts of such associate enterprise.

Insertion of new Section 36ACA for su-persession of powers of Board of bank: By this Section RBI has been empo-wered to supersede the powers of the Board of Directors a Bank for a period not exceeding 6 months, if affairs of a Bank is conducted in a manner detri-mental to the interests of public or its deposit holders in consultation with the Central Government. The period can be extended however not exceeding 12 months in total.

Amendments to Stamp Act, 1899 A new Section 8E is inserted in the Stamp Act, 1899 whereby any conversion of a branch of a bank in to its wholly owned subsidiary or transfer of shareholding in a bank to a holding company in terms of scheme or guidelines of the bank will not be liable to stamp duty and any in-strument transferring any property movable or immovable or any right or liability in relation to the above will also be not chargeable to duty.

Amendments to Contract Act, 1872: Section 28 of the Contract Act, 1872 declares that Agreements in restraint of legal proceedings to be void. The said Section is amended so as to exempt Guarantee Agreements executed in fa-vour of the Bank or financial institution for proper enforcement of guarantee provided to banks and their redemp-tion.

Government of India, Ministry of Fi-nance, Department of Revenue (CBDT), has issued Notification No. 63/2014, F.No.142/09/2014‐TPL dated 13th No-vember, 2014. As per the said notifica-tion, the Central Government made the amendments to the Tax Savings Bank Term Deposit Scheme, 2006. This scheme may be called the Bank Term Deposit (Amendment) Scheme, 2014.

The existing limit of Rs 1,00,000/- per financial year, in our SBI Tax Savings Scheme 2006 has been enhanced to Rs 1,50,000/- with immediate effect.

It has been decided by the Compe-tent Authority that the branches should not carry out any financial transactions requested by the Non-NRI customers, too, through e-mail even if the request is made by a letter scanned as an attach-ment.(e-cir:1115/2013-14 Dt:09/01/2014) Companies Act, 2013: A statistical Snapshot

Quick Success Series

Legal Aspects Of Banking

Updated up to 31st October 2016

15

Number of schedules: 7 Number of chapters: 29 Number of sections: 470

The 2013 Act has introduced several new

concepts and has also tried to streamline many of the requirements by introducing new definitions.

A few of these significant aspects are:

One-person company: The 2013 Act

introduces a new type of entity to the ex-isting list i.e. apart from forming a public or private limited company, the 2013 Act enables the formation of a new entity a ‘one-person company’ (OPC).

An OPC means a company with only one person as its member [section 3(1) of 2013 Act].

Private company: The 2013 Act introduces a change in the definition for a private company, inter-alia, the new requirement increases the limit of the number of mem-bers from 50 to 200. [Section-2(68) of 2013 Act].

Small company: A small company has been defined as a company, other than a public company. (i) Paid-up share capital of which does not exceed 50 lakh INR or such higher amount as may be Prescribed which shall not be more than five crore INR (ii) Turnover of which as per its last profit-and-loss account does not exceed two crore INR or such higher amount as may be prescribed which shall not be more than 20 crore INR:

As set out in the 2013 Act, this sec-tion will not be applicable to the following:

• A holding company or a subsidiary com-pany • A company registered under section 8 • A company or body corporate governed by any special Act [section 2(85) of 2013 Act]

Dormant company: The 2013 Act states that a company can be classified as dormant when it is formed and registered under this 2013 Act for a future project or to hold an asset or intellectual property and has no significant accounting transaction. Such a company or an inactive one may apply to the ROC in such manner as may be prescribed for obtaining the status of a dormant com-pany. [Section-455 of 2013 Act].

Class action suits: The 2013 Act introduces a new concept of class action suits which can be initiated by shareholders against the company and auditors.

The 2013 Act increases the limit for number of directorships that can be held by an individual from 12 to 15 [section 149(1) of 2013 Act].

Key Managerial Personnel (KMP) - The Provisions relating to appointment of KMP includes (i) the Chief Executive Officer (CEO) or the managing director (MD) or the man-ager (ii) the company secretary (iii) the whole-time director; (iv) the Chief Financial Officer (CFO); and (v) such other officer as may be prescribed is applicable only for Public Limited Companies having paid up capital more than 10 crores and Private Limited Companies are exempted from ap-pointment of KMPs.

Attending at least one Board Meeting by a director in a year is a must; else he has to vacate his/her office.

Financial Year - The Companies Act 1956 Act provided companies to elect financial year. The Companies Act 2013 Act eliminates the existing flexibility in having a financial year different than 31 March. The 2013 Act provides that the financial year for all com-panies should end on 31 March, with certain exceptions approved by the National Com-pany Law Tribunal. Companies should align the financial year to 31 March within two years from 01 April 2014.

Quick Success Series

Legal Aspects Of Banking

Updated up to 31st October 2016

16

Eligibility age to become Manag-

ing Director or whole time Direc-tor - The eligibility criteria for the age limit has been revised to 21 years as against the existing re-quirement of 25 years.

Number of directorships held by

an individual - Section 165 pro-vides that a person cannot have di-rectorships (including alternate di-rectorships) in more than 20 (twenty) companies, including ten (ten) public companies.

Board meetings – At least 7 days

notice to be given for Board Meet-ing. The Board need to meet at least 4 times within a year. There should not be a gap of more than 120 days between two consecutive meetings.

Appointment of Statutory Audi-

tors- Every Listed Company can appoint an individual auditor for 5 years and a firm of auditors for 10 years. This period of 5 / 10 years commences from the date of their appointment. Therefore, those companies who have reappointed their statutory auditors for more than 5 / 10 years have to appoint another auditor in their Annual General Meeting for year 2014.

Corporate Social Responsibility

(CSR) – the company has to consti-tute a CSR committee of the Board and 2% of the average net profits of the last three financial years are to be mandatorily spent on CSR ac-tivities by an Indian company if any of the following criteria is met:

Net worth of Rs.500 crores or

Turnover of Rs. 1000 crores or

more or

Net profit of Rs. 5 crores or more Financial statements - Financial State-

ments are now defined under the Act as comprising of the following. All compa-nies (except one person Company, small company and dormant company)are now mandatorily required to maintain the following, which may not include the cash flow statement) – A balance sheet as at the end of

the financial year A profit and loss account / an in-

come and expenditure account for the financial year, as the case may be

Cash flow statement for the finan-cial year

A statement of changes in equity (if applicable)

Any explanatory note annexed to, or forming part of, any document referred to in sub-clause (i) to sub-clause (iv)

CVA: Credit valuation adjustment HPTF: High Power Task Force Committee DEAF: Depositor Education and awareness

Fund SPV: Special Purpose Vehicle RTI - QM & TS:RTI Query Management

and Tracking System FATCA: Foreign Accounts Tax Com-

pliance Act CRS: Common Reporting Standards

INDIAN STAMP ACT: VALIDITY PE-RIOD FOR USE OF STAMP PAPER: The Hon'ble Supreme Court has considered le-gal issue whether a stamp paper purchased more than six months prior to the date of execution of a document is valid or not based on the case of Thiruvengada Pillai Vs Navneethammal in WP (Civil) No 290 of 2001 decided on 19.02.2008. The Hon'ble Apex Court, while deciding the issue in af-firmative observed that the Indian Stamp Act nowhere prescribes any expiry date for use of stamp paper. The Section 54 merely

Quick Success Series

Legal Aspects Of Banking

Updated up to 31st October 2016

17

provides that a person possessing any stamp paper for which he has no imme-diate use (which is not spoiled or rendered unfit or useless) can seek refund of the val-ue thereof by surrendering such stamp pa-per to the Collector provided it was pur-chased within the period of six months next preceding the date on which it was so surrendered. The stipulation of the period of six months prescribed in Section 54 ibid is only for the purpose of seeking refund of the value of unused stamp paper, and not for the use of stamp paper, to use it within six months. Therefore, there is no impedi-ment for user of stamp paper purchased more than six months prior to the date of

execution of a document.

Lok Adalat is a forum where disputes pend-ing in the court of law, or at pre-litigation stage, are settled amicably. Lok Adalat has been given statutory status under the Legal Services Authorities Act, 1987. An award made by the Lok Adalat is deemed to be a decree of a Civil Court and is final and bind-ing on all parties. Settlement of cases through Lok Adalat has certain advantages over other methods of recovery. Monetary ceiling of cases to be referred to the Lok Adalat organized by Civil Courts is Rs. 20 lacs. Further, our branches can participate in Lok Adalats to be organised by DRTs/DRATs irrespective of the amounts involved in the cases. (Standard Operating Procedure is laid down in e.cir.845/2015-16 dt:05/10/2015) To recover Bank’s dues, suits before Civil Courts may be filed when the amount of total debt due from the borrowers is less than Rs.10 lac. Documents should not be time barred and should be in order. Civil suit is to be filed immediately on approval but in any case within a maximum period of 3 months from the date of approval. Plaint is to be signed by the authorized Branch official. Demand Draft for court fees, process fees and copying fees has to be prepared. Affidavit of Branch official has

also to be filed along with the plaint, in duplicate. The case number allotted by the Court has to be obtained from the Court by the Branch. (Standard Operating Procedure is laid down in e.cir.940/2015-16 dt:28/10/2015)

Government of India has levied Swachh

Bharat Cess @0.5% on value of all the taxable services from 15-11-2015. Effec-tive rate of service tax would be 14.5%.

GLOSSARY AGNATES A person is said to be “agnate” of another if the two are related by blood or adoption wholly through males. If there are no heirs of Class I and Class II, then upon the “ag-nates” of the deceased can claim. COGNATES One is a “Cognate” of another, if the two are related by blood or adoption, but not wholly through males. If there are no ag-nate, then upon the “Cognates” of the de-ceased can claim. CLASS I HEIRS Son, daughter, widow, mother, son/daughter of a predeceased son/daughter.Son/daughter of a prede-ceased son of a predeceased son, or widow of a predeceased son of a predeceased son. CLASS II HEIRS Father, son’s daughter’s children, daugh-ter’s grand children, children of brothers and sisters etc.