Embed Size (px)

Citation preview

QUARTERLY REPORT FOR THE THREE MONTHS

ENDED 31 MARCH 2008

Quarterly report 31 March 2008

2

CONSOLIDATED FINANCIAL STATEMENTS

Quarterly report 31 March 2008

3

CONSOLIDATED INCOME STATEMENT

for the three months ended 31 March 2008

( 000) Note Q 1 2008 Q 1 2007

Revenues 1 17,990 14,366

Other income 11 -

Total revenue 18,001 14,366

Movement in work in progress, semi-finished and finished goods (2) -

Raw materials 2 (204) (221)

External services 3 (14,539) (11,478)

Rentals and leases 4 (380) (410)

Staff costs 5 (4,098) (3,496)

Amortisation and depreciation 6 (343) (170)

Capitalised internal costs 7 186 -

Impairment charges/reversal of impairment charges on non-current

assets (1) -

Other costs 8 (370) (268)

Finance income 9 299 264

Finance costs 9 (323) (128)

PROFIT/(LOSS) BEFORE TAX FROM CONTINUING

OPERATIONS (1,774) (1,541)

Taxation 10 (932) (685)

NET PROFIT/(LOSS) FROM CONTINUING OPERATIONS (2,706) (2,226)

Net profit/(loss) from discontinued operations - -

NET PROFIT/(LOSS) BEFORE MINORITY INTERESTS (2,706) (2,226)

Net profit/(loss) attributable to minority interests 60 -

NET PROFIT/(LOSS) FOR THE PERIOD ATTRIBUTABLE TO

PARENT COMPANY (2,766) (2,226)

Earnings per share 11 (0.71) (0.57)

Diluted earnings per share 11 (0.71) (0.57)

Quarterly report 31 March 2008

4

ANALYSIS OF CONSOLIDATED NET FUNDS AT 31 MARCH 2008

( 000)

31 Mar 2008 31 Dec 2007

A. Cash and cash equivalents 11,363 12,178

B. Assets held for trading 10,005 10,052

C. Liquidity (A + B) 21,368 22,230

D. Other current financial assets 2,647 2,650

E. Current bank borrowings (2) (265)

F. Current portion of non-current debt (30) (30)

G. Current financial liabilities (E + F) (32) (295)

H. Net current funds (C+D+G) 23,983 24,585

I. Non-current financial liabilities (133) (133)

L. Non-current debt (I) (133) (133)

M. Net funds (H + L) 23,850 24,452

Quarterly report 31 March 2008

5

NOTES TO THE

CONSOLIDATED

FINANCIAL STATEMENTS

Quarterly report 31 March 2008

6

BASIS OF PRESENTATION

The Acotel Group’s quarterly financial statements for the three months ended 31 March 2008 have

been prepared under international financial reporting standards (IFRS), as issued by the International

Accounting Standards Board (IASB) and endorsed by the European Union.

The financial statements also take account of the guidelines established in Annex 3D to the Regulations

for Issuers introduced by CONSOB Resolution no. 11971 of 14 May 1999 and subsequent amendments

and additions.

The accounting standards applied are consistent with those adopted for preparation of the Acotel

Group’s consolidated financial statements for the year ended 31 December 2007, integrated where

necessary by the application of standards to take account of aspects not present at that date.

The consolidated financial statements for the three months ended 31 March 2008 have been prepared

on the basis of the underlying accounting records at that date, as adjusted in accordance with the

matching principle.

Preparation of these financial statements required management to make estimates and assumptions

which, based primarily on internal records, essentially have an effect on revenues and costs that have

yet to be confirmed by customers and suppliers. Above all, turnover generated by the subsidiary,

Flycell Inc., and certain related cost items include preliminary figures and estimates that have yet to be

confirmed by the mobile transaction network provider, mBlox Inc.

Estimates and assumptions are primarily used in order to account for any refunds that may be payable

to B2C customers, and for the portion of revenues deriving from subscriptions for B2C services billed

in March 2008 and carried forward to the following accounting period.

In addition, certain evaluation processes, above all the most complex ones relating to the estimate of

potential impairments of fixed assets, are generally only fully carried out during preparation of the

annual financial statements, unless events or changes in circumstances indicate that there may be an

impairment requiring an immediate evaluation of any loss.

The following diagram shows the structure of the Acotel Group at 31 March 2008:

Quarterly report 31 March 2008

7

The following table provides summary information on consolidated companies held, directly or

indirectly, by Acotel Group SpA, the Parent Company.

Company Date of acquisition Group’s

interest (%)

Registered

office Share capital

Acotel SpA 28 April 2000 99.9% (4) Rome EURO 13,000,000

AEM Advanced Electronic Microsystems SpA 28 April 2000 99.9% Rome EURO 858,000

Acotel Participations S.A. 28 April 2000 100% Luxembourg EURO 1,200,000

Acotel Chile S.A. 28 April 2000 100% (5) Santiago, Chile USD 17,330

Acotel Espana S.L. 28 April 2000 100% (5) Madrid EURO 3,006

Acotel Do Brasil LTDA 8 August 2000 (1) 100% (5) Rio de Janeiro BRL 1,868,250

Jinny Software Ltd. 9 April 2001 100% (5) Dublin EURO 2,972

Millennium Software SAL 9 April 2001 99.9% (6) Beirut LBP 30,000,000

Info2cell.com FZ-LLC 29 January 2003 (3) 100% (5) Dubai DH 18,350,000

Quarterly report 31 March 2008

8

Emirates for Information Technology Co. 29 January 2003 100% (7) Amman JD 710,000

Noverca Srl 10 July 2002 (2) 100% Rome EURO 2,200,000

Flycell Inc. 28 June 2003 (1) 100% (5) Wilmington USD 10,000

Acotel Group (Northern Europe) Ltd 27 May 2004 (1) 100% Dublin EURO 101,000

Flycell Telekomunikasyon Hizmetleri A.S. 2 July 2005 (1) 99.9% (8) Istanbul TRY 50,000

Flycell Latin America Conteúdo Para

Telefonia Móvel LTDA 6 June 2006 (1) 100% (8) Rio de Janeiro BRL 250,000

Jinny Software Romania SRL 26 June 2007 (1) 100% (6) Bucharest LEI 200

Yabox LLC 24 October 2007 (1) 100% (8) Wilmington USD 1

Rawafid Information Company LLC 24 February 2008 (1) 51% (7) Riyadh SAR 500,000

(1) The date of the company’s entry into the Group coincides with its incorporation.

(2) Prior to such date the Group held 50% of the company’s share capital, posted to investments in associates.

(3) Prior to such date the Group held 33% of the company’s share capital, posted to investments in associates.

(4) AEM owns 1.92% of the share capital.

(5) Controlled via Acotel Participations S.A.

(6) Controlled via Jinny Software Ltd.

(7) Controlled via Info2cell.com FZ-LLC.

(8) Controlled via Flycell Inc.

The basis of consolidation changed during the quarter following the establishment of Rawafid

Information Company LLC by Info2cell.

Net funds at 31 March 2008 have been compared with the corresponding amount at 31 December 2007.

CONSOLIDATION PRINCIPLES

The consolidated quarterly financial statements include the financial statements of Acotel Group SpA

and those of its subsidiaries. Subsidiaries are defined as entities over which the Group has the power to

govern the financial and operating policies.

The net profit or loss of subsidiaries acquired or sold during the year is included in the consolidated

income statement from the effective acquisition date until the effective disposal date.

Profits and losses and revenues and expenses arising from intercompany transactions are eliminated.

The income statements of overseas subsidiaries based in countries outside the euro area are translated

into euros using average exchange rates for the period, as published by the Italian Exchange Office.

OTHER INFORMATION

This quarterly report is unaudited.

Quarterly report 31 March 2008

9

NOTES TO THE INCOME STATEMENT

Note 1 - Revenue

Revenue in the first quarter of 2008 amounted to 17,990 thousand euros, representing an increase of

25% on the figure for the same period of the previous year.

Revenue by business segment is as follows:

( 000) Q1 2008 % Q1 2007 %

SERVICES 16,775 93.3% 13,126 91.4%

DESIGN OF ICT EQUIPMENT 760 4.2% 924 6.4%

SECURITY SYSTEMS DESIGN 455 2.5% 316 2.2%

17,990 100% 14,366 100%

SERVICES

The Services business segment includes services supplied directly to end customers (B2C) and the

activities carried out for telephone and commercial companies, and has the primary purpose of

supplying value added services and content to mobile phone users.

A breakdown of service revenues is given in the following table:

( 000) Q1 2008 Q1 2007Increase/

(Decrease)

B2C services 10,466 8,140 2,326

Network Operator services 5,245 4,475 770

Corporate services 785 165 620

Media services 279 346 (67)

Total 16,775 13,126 3,649

B2C service revenues for the first quarter of 2008 are up 28.6% on the same period of the previous

year, representing approximately 62% of total service revenues. These revenues are generated by the

US subsidiary, Flycell Inc. (7,279 thousand euros) and its direct subsidiaries, Flycell Latin America

(2,488 thousand euros) and Flycell Telekomünicasyon Hizmetleri A. (approximately 699 thousand

euros).

Revenues from the provision of Network Operator services, amounting to 5,245 thousand euros, are up

770 thousand euros (17%) on the same period of 2007. They include revenues from services rendered

by the subsidiary, Acotel SpA, to Telecom Italia, which amount to 3,200 thousand euros for the quarter,

Quarterly report 31 March 2008

10

revenues from services rendered by the Brazilian subsidiary, Acotel do Brasil, to the Brazilian

operators, TIM Celular and TIM Nordeste Telecomunicaçoes, amounting to 1,442 thousand euros, and

revenues generated by activities carried out by Info2cell for the main mobile telephony operators in the

Middle East, totalling 596 thousand euros. The increase compared with the same period of the previous

year is essentially due to the higher turnovers reported by the Brazilian and Italian subsidiaries.

Revenues from corporate services amount to 785 thousand euros and relate primarily to the services

provided by Info2cell to its Middle Eastern customers (388 thousand euros), and those supplied in Italy

by Acotel SpA, primarily to banks (378 thousand euros). The increase compared with the first quarter of

2007 (up 376%) essentially reflects higher turnover at the Italian and Middle Eastern subsidiaries.

Revenues from services provided to media companies, amounting to 279 thousand euros, are almost

entirely generated in the Middle East by the subsidiary, Info2cell (225 thousand euros), and in Italy by

Acotel SpA (44 thousand euros).

DESIGN OF ICT EQUIPMENT

Revenues from this line of business, amounting to 760 thousand euros in the first quarter of 2008, are

generated by Jinny Software on platforms, software and services supplied to mobile operators in Africa,

the Middle East, Asia, Latin America and Europe.

SECURITY SYSTEMS DESIGN

Revenues from the design of electronic security systems amount to 455 thousand euros, having risen

44% with respect to the same period of 2007. They are entirely generated by the subsidiary, AEM SpA,

which is responsible for the installation, supply, servicing and maintenance of remote surveillance

equipment installed at Italian police headquarters, at certain provincial branches of the Bank of Italy

and at certain ACEA Group companies.

A geographical breakdown of the Group’s revenue is as follows:

Quarterly report 31 March 2008

11

( 000) Q1 2008 % Q1 2007 %

NORTH AMERICA 7,279 40.5% 8,277 57.6%

ITALY 4,091 22.6% 3,615 25.1%

LATIN AMERICA 3,990 22.2% 1,349 9.4%

MIDDLE EAST 1,398 7.8% 855 6.0%

OTHER EUROPEAN COUNTRIES 768 4.3% 97 0.7%

AFRICA 358 2.0% 111 0.8%

ASIA 106 0.6% 62 0

17,990 100% 14,366 100%

The geographical revenue breakdown for the first quarter of 2008 reveals an increase in turnover in

Latin America, thanks mainly to the B2C services provided by Flycell Latin America, a direct

subsidiary of the US company, Flycell Inc., which also has control over the company’s operating

policies.

Note 2 – Raw materials

The cost of raw materials during the quarter, amounting to 204 thousand euros, refers principally to the

purchase of materials for the construction of telecommunications and security systems by Jinny

Software Ltd (112 thousand euros) and AEM SpA (79 thousand euros).

Note 3 - External services

The cost of external services for the first quarter of 2008 amounts to 14,539 thousand euros, compared

with 11,478 thousand euros in the same period of 2007. The increase, which is closely linked to

revenue growth, essentially reflects the business model adopted by Flycell Inc. and its direct

subsidiaries, Flycell Latin America and Flycell Telekomünicasyon Hizmetleri A. . to develop business

in their principal markets. This entails substantial promotional costs (5,761 thousand euros out of a

Group total of 5,934 thousand euros) in order to raise market awareness of their services and increase

their customer base, and significant costs (4,581 thousand euros) charged by telephone operators and

mobile transaction network providers for transport and collection services.

In addition to the above costs, the most significant items regard the cost of acquiring content from

external content providers (1,566 thousand euros), the fees paid to marketing, administrative, legal and

technical consultants by Group companies in the course of business (422 thousand euros), travel

expenses (383 thousand euros) and, finally, the cost of purchasing SMS packages from mobile

operators (344 thousand euros).

Other cost items, in order of importance, regard the fees paid to governance bodies (162 thousand

euros), the cost of taking part in exhibitions and fairs (142 thousand euros), telephone expenses (131

thousand euros), and the cost of connecting to terrestrial and satellite transmission networks used to

supply value added services (114 thousand euros).

Quarterly report 31 March 2008

12

The balance reflects overheads (utilities, management and maintenance of the Group’s operating

properties, insurance, etc.) incurred by the Group in its day-to-day operations.

Note 4 – Rentals and leases

The cost of rentals and leases, amounting to 380 thousand euros, mainly includes rentals on offices

occupied by Group companies.

Note 5 - Staff costs

Staff costs include:

( 000) Q1 2008 Q1 2007Increase/

(Decrease)

Salaries and wages 3,217 2,714 503

Social security contributions 556 457 99

Staff termination benefits 54 62 (8)

Finance costs (12) (6) (6)

Other costs 283 269 14

4,098 3,496 602

Total

The number of staff by category at 31 March 2008, with a comparison of the average numbers for the

first quarters of 2008 and 2007, is reported in the following schedule:

At 31 Mar 2008 Average Q1 2008 Average Q1 2007

Managers 19 19 19

Supervisors 28 28 33

White- and blue-collar staff 322 315 257

Total 369 362 309

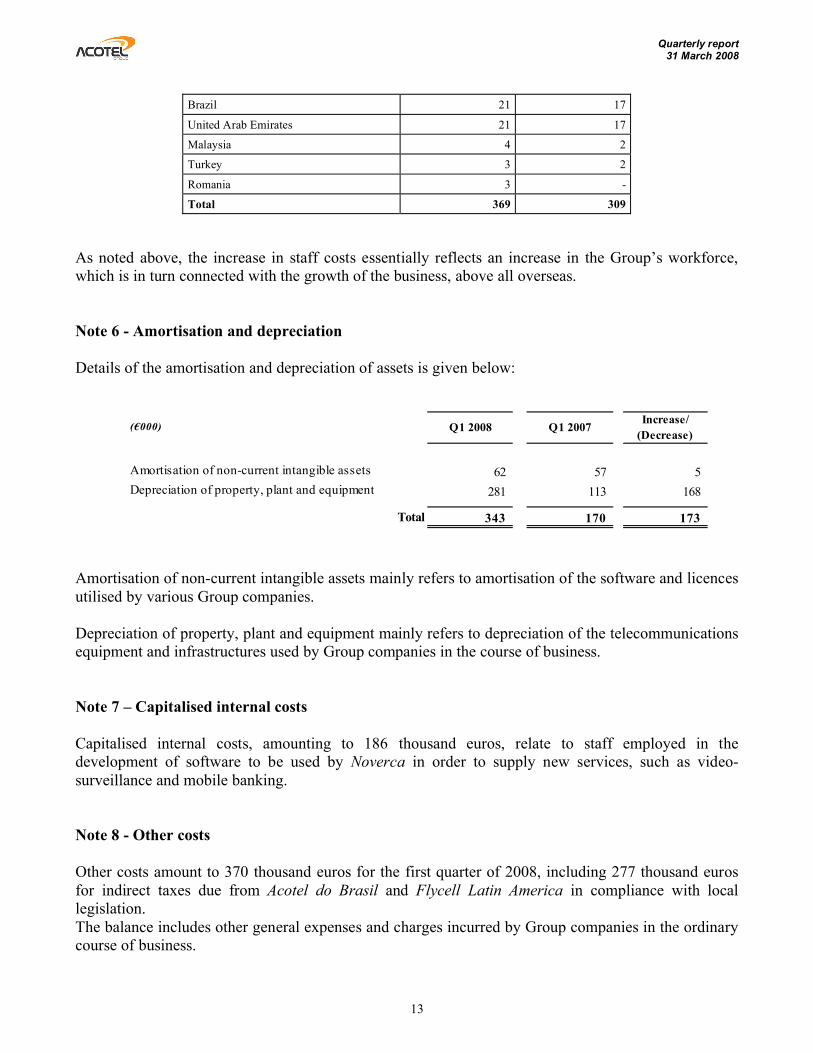

The geographical distribution of the Group’s staff is shown below.

At 31 Mar 2008 At 31 Dec 2007

Italy 99 92

Lebanon 69 57

USA 61 44

Jordan 60 53

Ireland 28 25

Quarterly report 31 March 2008

13

Brazil 21 17

United Arab Emirates 21 17

Malaysia 4 2

Turkey 3 2

Romania 3 -

Total 369 309

As noted above, the increase in staff costs essentially reflects an increase in the Group’s workforce,

which is in turn connected with the growth of the business, above all overseas.

Note 6 - Amortisation and depreciation

Details of the amortisation and depreciation of assets is given below:

( 000) Q1 2008 Q1 2007Increase/

(Decrease)

Amortisation of non-current intangible assets 62 57 5

Depreciation of property, plant and equipment 281 113 168

Total 343 170 173

Amortisation of non-current intangible assets mainly refers to amortisation of the software and licences

utilised by various Group companies.

Depreciation of property, plant and equipment mainly refers to depreciation of the telecommunications

equipment and infrastructures used by Group companies in the course of business.

Note 7 – Capitalised internal costs

Capitalised internal costs, amounting to 186 thousand euros, relate to staff employed in the

development of software to be used by Noverca in order to supply new services, such as video-

surveillance and mobile banking.

Note 8 - Other costs

Other costs amount to 370 thousand euros for the first quarter of 2008, including 277 thousand euros

for indirect taxes due from Acotel do Brasil and Flycell Latin America in compliance with local

legislation.

The balance includes other general expenses and charges incurred by Group companies in the ordinary

course of business.

Quarterly report 31 March 2008

14

Note 9 - Finance income and costs

Net finance costs of 24 thousand euros break down as follows:

( 000) Q1 2008 Q1 2007

Interest income from investments 201 207

Interest income on bank deposits 21 39

Foreign exchange gains 43 13

Other interest income 34 5

Total finance income 299 264

Interest expense and bank charges (47) (25)

Foreign exchange losses (264) (91)

Other interest expense (12) (12)

Total finance costs (323) (128)

Net finance income/(costs) (24) 136

Interest income from investments includes gains on investment of the Group’s liquidity in short-term

instruments.

The balance of foreign exchange gains and losses reflects the impact of closing exchange rates on the

value of intercompany loans originally disbursed in dollars.

Note 10 - Taxation

Taxation for the period, amounting to 932 thousand euros, reflects estimated income taxes and deferred

tax assets and liabilities recognised by Group companies.

Note 11 - Earnings per share

The calculation of basic and diluted earnings per share is based on the following data:

Quarterly report 31 March 2008

15

( 000) Q 1 2008 Q 1 2007

Net profit/(loss) ( 000) (2,766) (2,226)

Number of shares (000)

Shares in circulation at the start of the period 3,916 * 3,916 *

Weighted average of treasury shares acquired/sold in the period - -

Weighted average of ordinary shares in circulation 3,916 3,916

Basic and diluted earnings per share ** (0.71) (0.57)

* : net of treasury shares held at the same date.

**: basic earnings for the first quarters of 2008 and 2007 coincide with diluted earnings per share

as the conditions provided for by IAS 33 do not exist.

NET FUNDS

Net funds have fallen approximately 600 thousand euros compared with 31 December 2007. This

essentially reflects the substantial cost of launching B2C services in Brazil and Turkey and VOIP

communications services in Italy under the Noverca brand.

SUBSEQUENT EVENTS

On 9 May all the corporate transactions envisaged in the agreement of 28 December 2007 between

Acotel Group SpA and Intesa SanPaolo SpA were executed. These regard:

• Intesa Sanpaolo’s acquisition of a 4.75% stake in Acotel Group via the purchase of 198,075

shares held by the Group for a total cost of 12.3 million euros (62 euros per share);

• Intesa Sanpaolo’s acquisition of a 10% interest in Noverca Srl, previously a wholly owned

subsidiary of Acotel Group, via subscription of a capital increase of 3.6 million euros. Acotel

Group has, at the same time, subscribed to a further tranche of the same capital increase,

amounting to 5.6 million euros;

• the establishment of a new company named Noverca Italia Srl, which is 66% owned by Noverca

Srl and 34% owned by Intesa Sanpaolo SpA. Noverca Srl has granted the new company

exclusive rights to use its IP platform for the provision of value added services in the Italian

market and 5 million euros in cash, whilst Intesa Sanpaolo SpA has taken part in the

establishment of Noverca Italia Srl via the injection of 13.3 million in cash;

• the election of the governance bodies of Noverca Srl and Noverca Italia Srl, and the co-option

of a Director nominated by Intesa SanPaolo SpA on to Acotel Group SpA’s Board of Dirctors.

From an industrial viewpoint, the agreement also envisages that the parties will cooperate in marketing

and commercialising Noverca Italia’s offering, on an exclusive basis for the banking sector, to the over

10 million customers of Intesa Sanpaolo SpA’s Banca dei Territori Division.

Quarterly report 31 March 2008

16

Noverca Italia Srl will operate in Italy under its own brand as a mobile virtual network operator, using

Telecom Italia SpA’s mobile network, and will offer both consumers and business customers

telecommunications services, added value IP services and electronic money and mobile banking

services to be developed jointly with Intesa Sanpaolo SpA.

Quarterly report 31 March 2008

17

DIRECTORS’ FINANCIAL AND OPERATING REVIEW

RECLASSIFIED CONSOLIDATED INCOME STATEMENT

( 000) Q1 2008 Q1 2007 Increase/Decrease % inc./(dec.)

Revenues 17,990 14,366 3,624 25%

Other income 11 - 11 -

Total revenue 18,001 14,366 3,635 25%

Gross operating profit/(loss) (1,406) (1,507) 101 7%

-7.81% -10.49%

Operating profit/(loss) (1,750) (1,677) (73) (4% )

-9.72% -11.67%

Net finance income/(costs) (24) 136 (160) (118%)

PROFIT/(LOSS) BEFORE TAX (1,774) (1,541) (233) (15% )

-9.86% -10.73%

NET PROFIT/(LOSS) BEFORE MINORITY

INTERESTS (2,706) (2,226) (480) (22% )

-15.03% -15.49%

Net profit/(loss) attributable to minority interests 60 - 60 -

NET PROFIT/(LOSS) ATTRIBUTABLE TO

PARENT COMPANY (2,766) (2,226) (540) (24% )

-15.37% -15.49%

Earnings per share (0.71) (0.57)

Diluted earnings per share (0.71) (0.57)

If compared with the results for the same period of the previous year, the Acotel Group’s results for the

first quarter of 2008 show a 25% increase in revenue and a decline in earnings.

Revenue growth was primarily driven by the commercial activities of Flycell Inc. in Brazil and Turkey,

where it operates via its direct subsidiaries, and increased turnover at the subsidiaries, Acotel do Brasil,

Info2cell and Acotel SpA, compared with the same period of the previous year.

The decline in earnings is, on the other hand, due to the substantial cost of launching B2C services in

Brazil and Turkey which, in line with the business model adopted, involves significant promotional

expenditure to advertise the new services. Earnings were also affected by the costs relating to the

Noverca project, which has been fully described in this report.

Quarterly report 31 March 2008

18

Taking a closer look, the gross operating loss (negative EBITDA) for the quarter amounts to 1,406

thousand euros, marking a 7% improvement on the same period of 2007, when the loss was 1,507

thousand euros.

After amortisation, depreciation and impairment charges on non-current assets, the Group reports an

operating loss (negative EBIT) of 1,750 thousand euros, compared with a loss of 1,677 thousand euros

for the same period of the previous year.

After net finance costs of 24 thousand euros, estimated taxation for the period of 932 thousand euros

and profit attributable to minority interests of 60 thousand euros, the net loss attributable to the Parent

Company has widened to 2,766 thousand euros in the first quarter of 2008 compared with the net loss

for the same period of 2007, totalling 2,226 thousand euros.

OUTLOOK

Whilst information on the Group’s outlook for the year can be found in the Annual Report for the year

ended 31 December 2007, it should be remembered how the particular nature of the B2C business,

conducted primarily by the subsidiary, Flycell Inc., in the US, Brazilian and Turkish markets, means

that it alternates between periods (such as the first quarter of this year) when the focus is on driving

expansion of the customer base, involving large-scale spending on promotions, and periods when the

benefits of such spending are seen, resulting in an improvement in earnings.

DECLARATION BY THE MANAGER RESPONSIBLE FOR THE GROUP’S FINANCIAL

REPORTING PURSUANT TO THE PROVISIONS OF ARTICLE 154 BIS, PARAGRAPH

2, OF LEGISLATIVE DECREE 58/1998

The manager responsible for the Group’s financial reporting, Luca De Rita, hereby declares, pursuant

to article 154 bis, paragraph 2, of the Consolidated Law on Finance, that this consolidated quarterly

report is consistent with the underlying accounting records.

![Announces Q1 results, Limited Review Report & Financial Performance for the Quarter ended June 30, 2015 [Result]](https://img.pdfslide.us/doc/110x75/577cb2971a28aba7118c178c/announces-q1-results-limited-review-report-financial-performance-for-the.jpg)

![Announces Q1 results, Limited Review Report & Results Press Release for the Quarter ended June 30, 2015 [Result]](https://img.pdfslide.us/doc/110x75/577cb2591a28aba7118bfc8d/announces-q1-results-limited-review-report-results-press-release-for-the.jpg)

![Announces Q1 results, Limited Review Report & Earnings Release for the Quarter ended June 30, 2015 [Result]](https://img.pdfslide.us/doc/110x75/577cb2f01a28aba7118c3021/announces-q1-results-limited-review-report-earnings-release-for-the-quarter.jpg)

![Announces Q1 results & Limited Review Report for the Quarter ended March 31, 2016 [Result]](https://img.pdfslide.us/doc/110x75/577c805f1a28abe054a86957/announces-q1-results-limited-review-report-for-the-quarter-ended-march-31.jpg)

![Announces Q1 results & Limited Review for the Quarter ended June 30, 2015 [Result]](https://img.pdfslide.us/doc/110x75/577cb3191a28aba7118c3cf8/announces-q1-results-limited-review-for-the-quarter-ended-june-30-2015-result.jpg)

![Quarterly report for the first quarter (Q1) ended on June 30, 2015 [Company Update]](https://img.pdfslide.us/doc/110x75/577cb4101a28aba7118c48b3/quarterly-report-for-the-first-quarter-q1-ended-on-june-30-2015-company.jpg)