Embed Size (px)

Citation preview

Quarterly Newsletter of DMP Asset Management Ltd December 2015

Issue 20

DMP Asset Management Ltd ABN 77 145 590 316 Australian Financial Services Licence Number 383580 Level 30, 80 Collins Street, Melbourne VIC 3000 T (03) 9981 3300 F (03) 9981 3399 W www.dmpam.com.au

Quarterly Newsletter of DMP Asset Management Ltd December 2015

2

The tale of three wise men following a star, bearing gifts to present to a new born child, who we know as Jesus, in today’s world of instant communication and rapid advance of science, appears somewhat far-fetched. The fact that it took until 1452 for the Bible to be printed using mass produced movable type (the Gutenberg Bible) and therefore available for reading by a wide audience, is testimony to the type of visionary that Jesus was, that his tale could survive over so many centuries. Roll the clock forward 650 years and we are now in need for a similar visionary, or group of visionaries, to lead us over the next period – let’s settle for the next five to ten years - as we confront a confluence of events that the modern world has not witnessed before – or at least not as far as we can determine. So what is this confluence of events?

First, the end of the super-cycle in the growth in debt levels, globally, due to debt saturation in the household sector.

Second, the ageing of the population in what is commonly referred to as the developed markets.

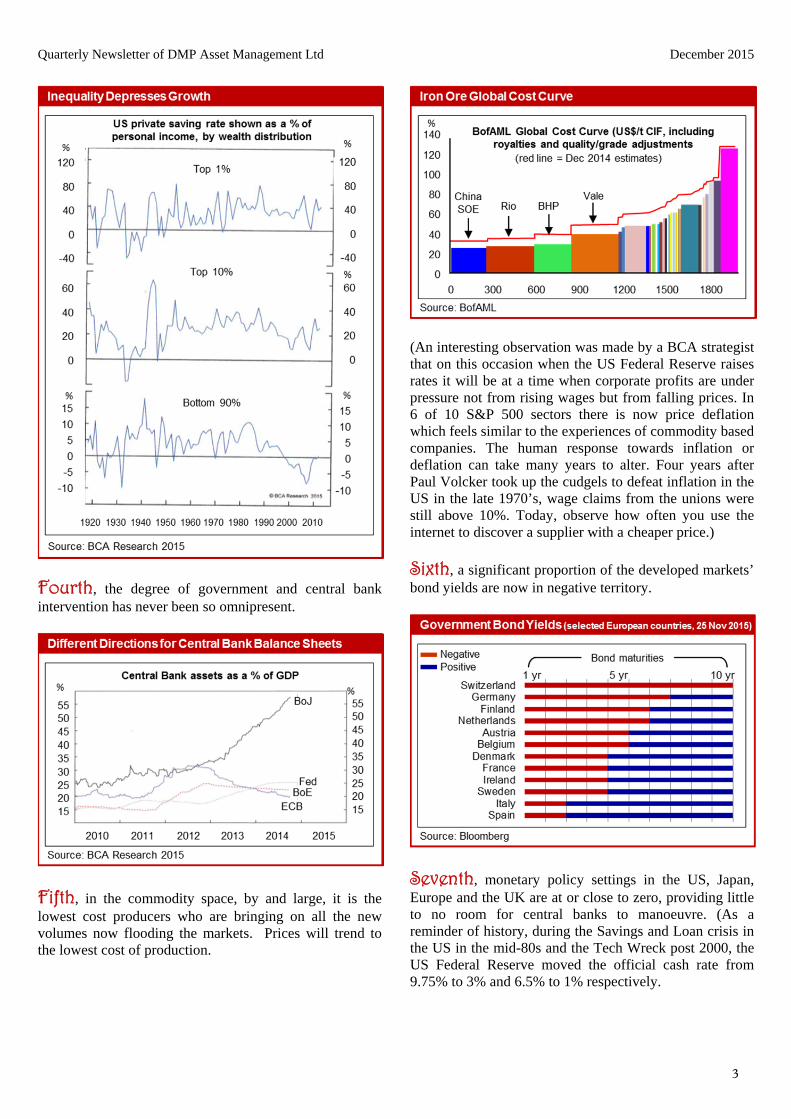

Third, the peaking, or maximum extension, of the Gini co-efficient in many economies. In layman’s terms, the gap between the “haves” and “have nots” has never been larger in modern history.

This gap is revealed in a stark measure when observing the savings rate in the USA between various brackets of wealth distribution.

Quarterly Newsletter of DMP Asset Management Ltd December 2015

3

Fourth, the degree of government and central bank intervention has never been so omnipresent.

Fifth, in the commodity space, by and large, it is the lowest cost producers who are bringing on all the new volumes now flooding the markets. Prices will trend to the lowest cost of production.

(An interesting observation was made by a BCA strategist that on this occasion when the US Federal Reserve raises rates it will be at a time when corporate profits are under pressure not from rising wages but from falling prices. In 6 of 10 S&P 500 sectors there is now price deflation which feels similar to the experiences of commodity based companies. The human response towards inflation or deflation can take many years to alter. Four years after Paul Volcker took up the cudgels to defeat inflation in the US in the late 1970’s, wage claims from the unions were still above 10%. Today, observe how often you use the internet to discover a supplier with a cheaper price.)

Sixth, a significant proportion of the developed markets’ bond yields are now in negative territory.

Seventh, monetary policy settings in the US, Japan, Europe and the UK are at or close to zero, providing little to no room for central banks to manoeuvre. (As a reminder of history, during the Savings and Loan crisis in the US in the mid-80s and the Tech Wreck post 2000, the US Federal Reserve moved the official cash rate from 9.75% to 3% and 6.5% to 1% respectively.

Quarterly Newsletter of DMP Asset Management Ltd December 2015

4

Eighth, after several decades of deregulation, the global financial services regulator, the Bank of International Settlements, is now determined in its desire to re-regulate the banking system to prevent any liability falling onto the taxpayer in the future in the event of GFC Mark II.

Ninth, never before has the human race been so reliant on mathematical algorithms, whether it is to manage your Facebook page or understand patterns emerging in financial markets or economies. Just don’t ask the modelers what happens when all functions within the model correlate to one or you insert a zero into the equation!

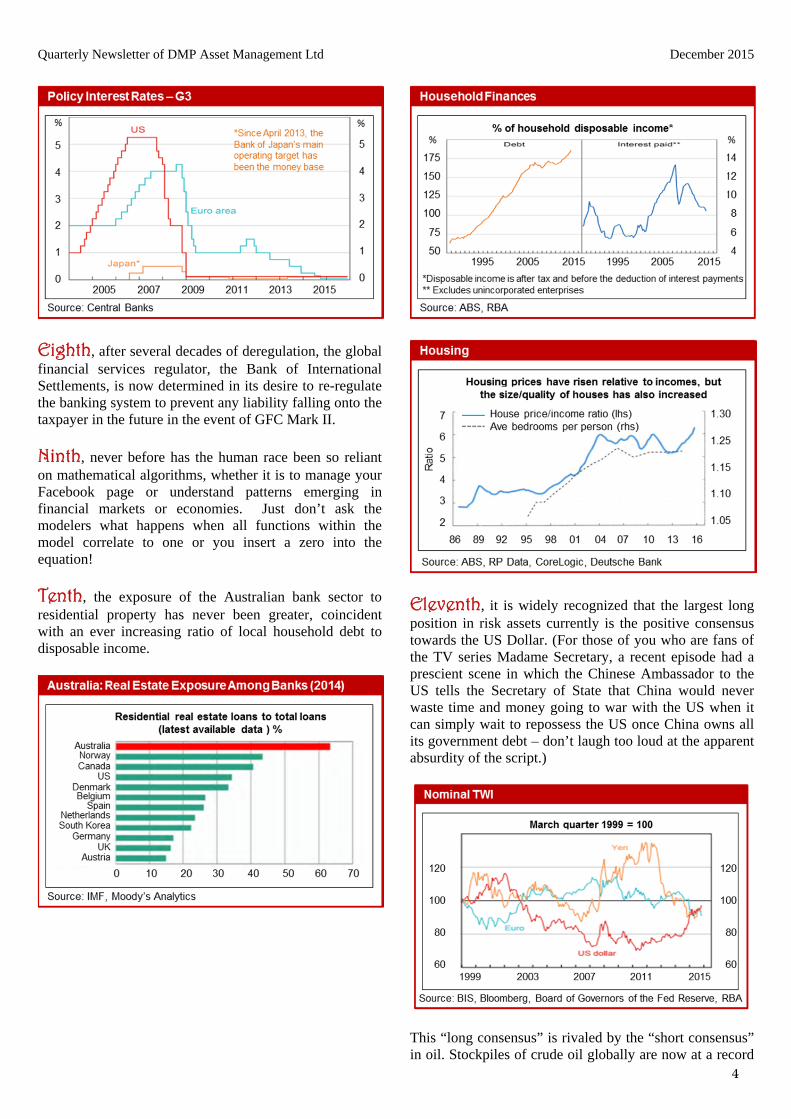

Tenth, the exposure of the Australian bank sector to residential property has never been greater, coincident with an ever increasing ratio of local household debt to disposable income.

Eleventh, it is widely recognized that the largest long position in risk assets currently is the positive consensus towards the US Dollar. (For those of you who are fans of the TV series Madame Secretary, a recent episode had a prescient scene in which the Chinese Ambassador to the US tells the Secretary of State that China would never waste time and money going to war with the US when it can simply wait to repossess the US once China owns all its government debt – don’t laugh too loud at the apparent absurdity of the script.)

This “long consensus” is rivaled by the “short consensus” in oil. Stockpiles of crude oil globally are now at a record

Quarterly Newsletter of DMP Asset Management Ltd December 2015

5

with OPEC effectively throwing in the towel at its last meeting in early December in terms of attempting to rein in member state production to support prices.

Twelfth, man has travelled further into space than ever before with the New Horizons spacecraft executing a fly-by of Pluto in July 2015, Pluto being the most distant planet in our solar system, or at least the most distant that has a name.

The Next Period So what does this mean for risk assets and, more importantly, what tactics do we as investors, need to employ to negotiate such a confluence of events and the type of investment environment that they will herald? What lies beyond Pluto? For those of our clients who were kind enough to listen to our most recent discourse entitled “Three Little Pigs” the primary message was the core drivers of performance of the equity market over the past 25-30 years are highly likely to not be the drivers over the next period (we have deliberately not defined a length, as the timing of investing is driven by valuation not a simple elapse of time). The secondary message was that we all need to get used to seeing portfolios without all/some of the household names of yesteryear in them; and the tertiary message was that yield/income will continue to be a pivotal component of total return. The Australian equity market can be broken down into four basic categories: Bank, Resource, Industrial and Income securities. The key profit/return driver for each sector can be broadly and simply defined as: Banks – Return on Equity (ROE) Resources – All in Sustaining Cost (AISC) per unit of production Industrials – Return on Invested Capital (ROIC)

Income Securities - Margin Payable over official cash rate, otherwise known as the Credit Spread (CS) For the bank sector if we are flooded with debt and the regulator requires the banks to hold more equity then we are forecasting that the ROE will fall leading to a compression in the valuation applied to banks. A cornerstone of investor portfolios for 30 years should now be seen as a source of cash for other areas of investment. The AISC of the biggest suppliers of bulk commodities and oil is currently at or below current spot prices at a time when global demand is faltering due the fact we are ageing and debt burdens suppress the propensity to spend. Resource stocks should be rented not owned for the foreseeable future. The prices of BHP, RIO and Woodside have all but given up the rally that coincided with China’s “leap” onto the world economic stage. The rule of thumb when investing in resource stocks is to sell them when they are on a forecast Price Earnings Multiple well below 10 and buy them when they are barely making any money – counter intuitive, we agree! Industrials capture many different enterprises and it is in this space that we believe portfolios need to be focused going forward. ROIC is one of the key valuation ingredients that we consider when analyzing this space. ROIC is a good indicator of management capability and strategic insight. Industrials have an advantage over resources in that they have wider opportunity and greater flexibility. A major mine development can take up to 7 years to bring into production, be very capital intensive and once you are committed then there is little ability to turn back – ask the management teams at Santos and Origin whether they think East Coast LNG is still a good idea. Given that the local equity market is dominated by the resource majors and big four banks (the Top 20 stocks account for 55% of the market capitalization) at DMP we forecast that a focal point for returns in 2016/17 will be in the middle/small segment of the market and probably be biased towards industrial related stocks with a robust/growing ROIC and a sustainable dividend yield. In line with this strategic thinking we have invested in the likes of APA Group, Challenger, Estia Health, Folkestone Education Trust and Healthscope to name a few. (As previously communicated, Mr Stephen Babidge, a small cap specialist of some 29 years has joined our team. DMP will be launching his services in the New Year and we look forward to making a presentation to you.) In line with our view that income will be a pivotal component of total return in the period ahead we have invested considerable time in understanding income securities and preference shares. The performance of these listed instruments tends to be a function of the underlying balance sheet of the issuer as well as credit spreads. Credit

Quarterly Newsletter of DMP Asset Management Ltd December 2015

6

spreads are a measurement of how far above the corresponding government bond yield a particular grade of security trades. The bigger the gap the more risk adverse investors have become and vice-versa. The last 12-18 months has been a poor period of returns from income securities and preference shares (note upward movement in spreads in graph below) but we believe that value has now returned to certain securities, ironically mainly in some of the Big Four Banks preference shares and income securities. Whilst the requirement for the banks to de-lever and hold more equity is detrimental to the valuations that their ordinary shares might trade at, the same regulatory change is beneficial to securities linked to their balance sheet security.

Post Script Over the past quarter we have fielded many enquiries about our opinion on opportunities in the agricultural sector in Australia. In the listed space the opportunities are not plentiful and where they do exist valuations can be fickle. It is important to remember that agriculture is as cyclical as resource investment and is becoming as globalized as the commodity sector. We share the enthusiasm towards the sector but not at any price. We hope that these thoughts are of interest to you, and would be more than happy to discuss them with you personally. While the confluence of events is changing the investment environment, with careful research and portfolio construction we continue to believe we can meet your investment objectives and expectations. Finally, on behalf of the crew at DMP we wish you a very happy Christmas and a safe and healthy 2016.

Harry Cator Executive Chairman

Quarterly Newsletter of DMP Asset Management Ltd December 2015

7

Quarterly Newsletter of DMP Asset Management Ltd December 2015

8

Disclaimer The information, opinions, estimates, conclusions, material and other data (the “Information”) presented in this document are provided to you for information purposes only and are not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities. Nothing in this document constitutes legal or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances, or otherwise constitutes a personal recommendation to you. The Information presented in this document has been obtained or derived from sources believed by DMP Asset Management Ltd (DMPAM) to be reliable, but DMPAM makes no representation or warranty, express or implied, as to their accuracy or completeness. To the extent permissible by law, DMPAM, its employees, agents and advisers exclude all liability for any loss or damage arising directly or indirectly as a result of any person acting or relying on the Information presented in this document. Any projections contained in this document are estimates only and may not be realised in the future. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. This document was prepared for multiple distribution and contains general securities advice only. It does not take into account the specific investment objectives, financial situation or needs of individual recipients and may not be appropriate in all circumstances. Persons relying on this Information should do so taking into consideration their specific investment objectives, financial situations and needs. Before acting on the basis of this document you are advised to contact DMPAM or an independent adviser for individual advice tailored to your personal circumstances. Finally, in accordance with the Corporations Act 2001 (Cth) please note that: (a) DMPAM may receive fees and commissions concerning any or all of the entities which are the subject of this document. Details of those fees and commissions are available on request;

and (b) DMPAM and/or its employees may hold securities or rights to take up securities or may intend to acquire securities in any or all of the entities which are the subject of this document.