Embed Size (px)

DESCRIPTION

Qatar Oil and Gas

Citation preview

Q4 2013www.businessmonitor.com

QATAROIL & GAS REPORTINCLUDES 10-YEAR FORECASTS TO 2022

ISSN 1748-4189Published by:Business Monitor International

Qatar Oil & Gas Report Q4 2013INCLUDES 10-YEAR FORECASTS TO 2022

Part of BMI’s Industry Report & Forecasts Series

Published by: Business Monitor International

Copy deadline: August 2013

Business Monitor InternationalSenator House85 Queen Victoria StreetLondonEC4V 4ABUnited KingdomTel: +44 (0) 20 7248 0468Fax: +44 (0) 20 7248 0467Email: [email protected]: http://www.businessmonitor.com

© 2013 Business Monitor InternationalAll rights reserved.

All information contained in this publication iscopyrighted in the name of Business MonitorInternational, and as such no part of thispublication may be reproduced, repackaged,redistributed, resold in whole or in any part, or usedin any form or by any means graphic, electronic ormechanical, including photocopying, recording,taping, or by information storage or retrieval, or byany other means, without the express written consentof the publisher.

DISCLAIMERAll information contained in this publication has been researched and compiled from sources believed to be accurate and reliable at the time ofpublishing. However, in view of the natural scope for human and/or mechanical error, either at source or during production, Business MonitorInternational accepts no liability whatsoever for any loss or damage resulting from errors, inaccuracies or omissions affecting any part of thepublication. All information is provided without warranty, and Business Monitor International makes no representation of warranty of any kind asto the accuracy or completeness of any information hereto contained.

CONTENTS

BMI Industry View ............................................................................................................... 7

SWOT .................................................................................................................................... 9

Industry Forecast .............................................................................................................. 10Oil And Gas Reserves ............................................................................................................................. 10

Table: Qatar Proven Oil & Gas Reserves And Total Petroleum Data, 2011-2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Table: Qatar Proven Oil & Gas Reserves And Total Petroleum Data, 2017-2022 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Oil Supply And Demand .......................................................................................................................... 13Table: Qatar Oil Production, Consumption And Net Exports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Table: Qatar Oil Production, Consumption And Net Exports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

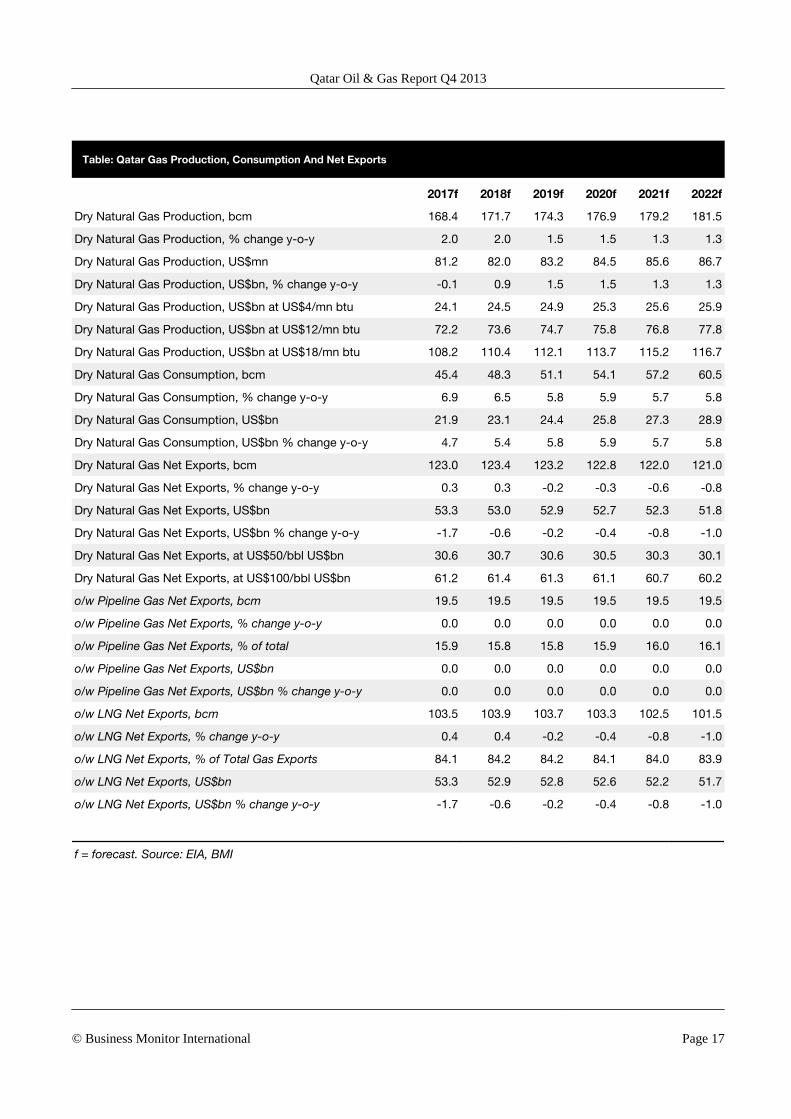

Gas Supply And Demand ......................................................................................................................... 16Table: Qatar Gas Production, Consumption And Net Exports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Table: Qatar Gas Production, Consumption And Net Exports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

LNG .................................................................................................................................................... 22Table: Qatar LNG Infrastructure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Refining And Oil Products Trade .............................................................................................................. 25Table: Qatar Refining - Production And Consumption, 2011-2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Table: Qatar Refining - Production And Consumption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Revenues/Import Costs ............................................................................................................................ 27

Key Risks To BMI's Forecast Scenario ....................................................................................................... 27

Industry Risk Reward Ratings .......................................................................................... 29Middle East - Risk/Reward Ratings ............................................................................................................. 29

Table: BMI's Middle East Oil & Gas Risk/Reward Ratings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Table: Middle East Upstream Oil & Gas Risk/Reward Rating . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

Table: Middle East Downstream Oil & Gas Risk/Reward Rating . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

Qatar - Risk/Reward Ratings ..................................................................................................................... 36

Market Overview ............................................................................................................... 38Qatar Energy Market Overview .................................................................................................................. 38

Overview/State Role ............................................................................................................................... 40

Licensing And Regulation ........................................................................................................................ 40

Government Policy ................................................................................................................................. 40

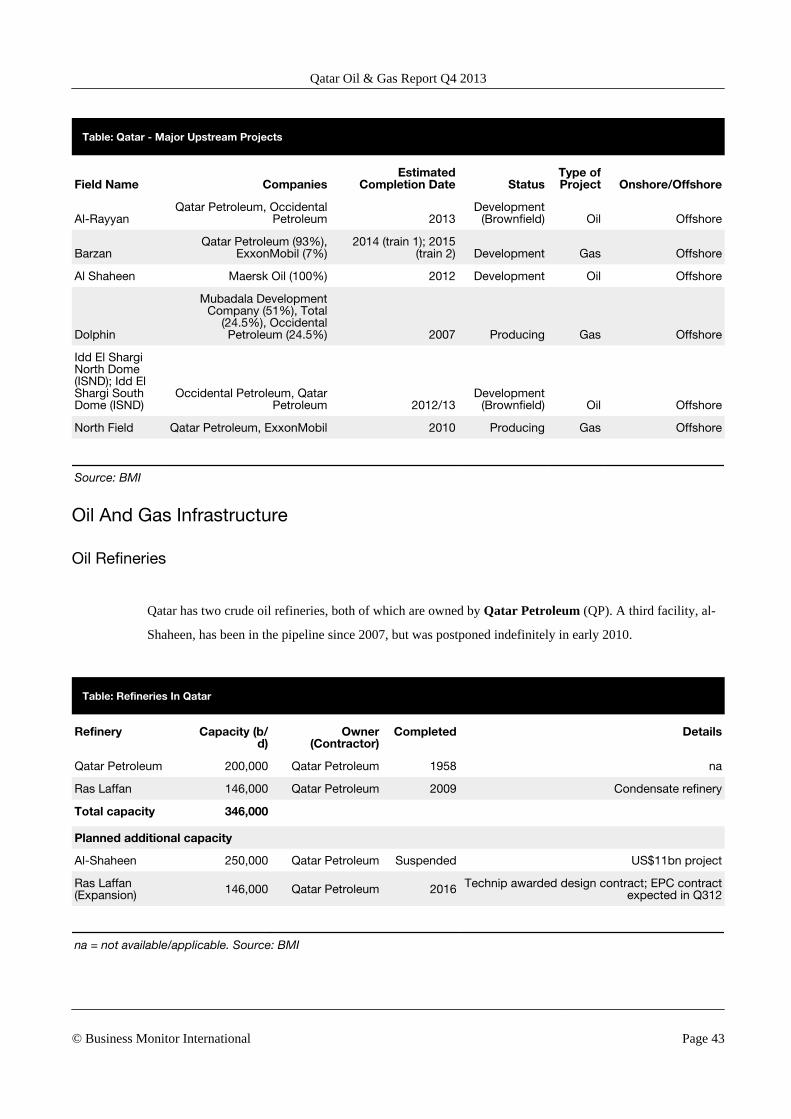

International Energy Relations ................................................................................................................. 41Table: Qatar - Major Upstream Projects . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

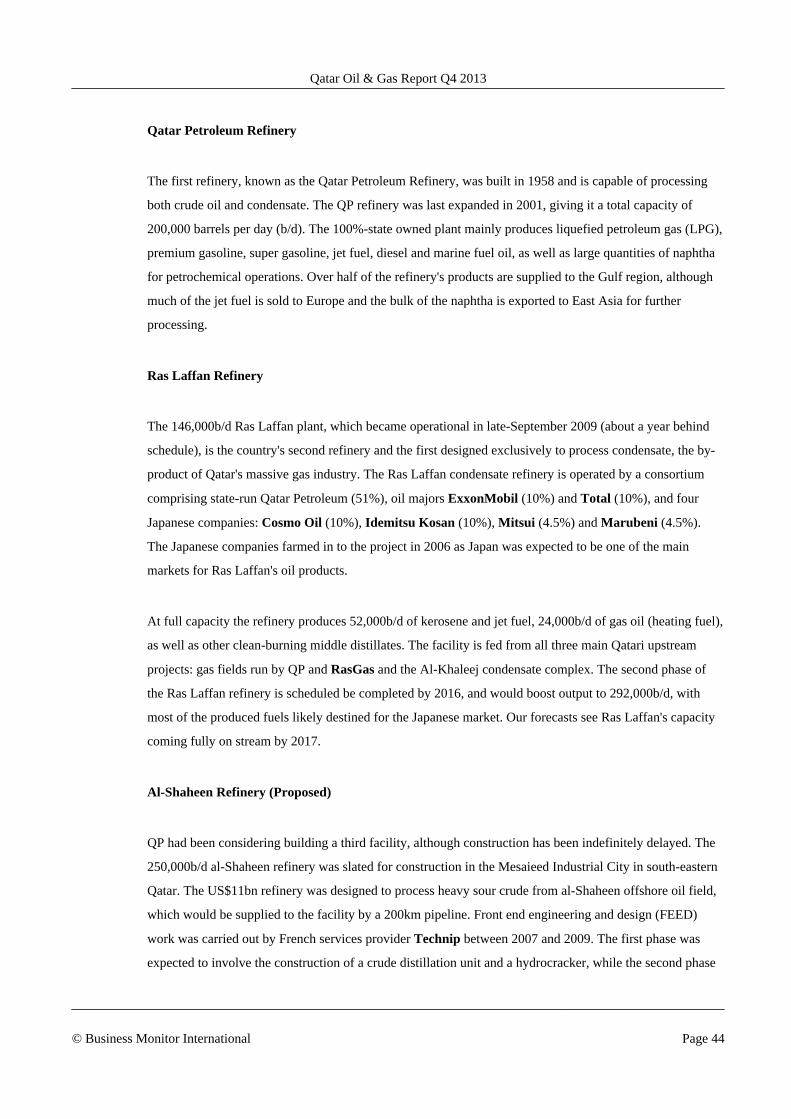

Oil And Gas Infrastructure ........................................................................................................................ 43

Oil Refineries ........................................................................................................................................ 43Table: Refineries In Qatar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

Table: GTL Plants In Qatar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

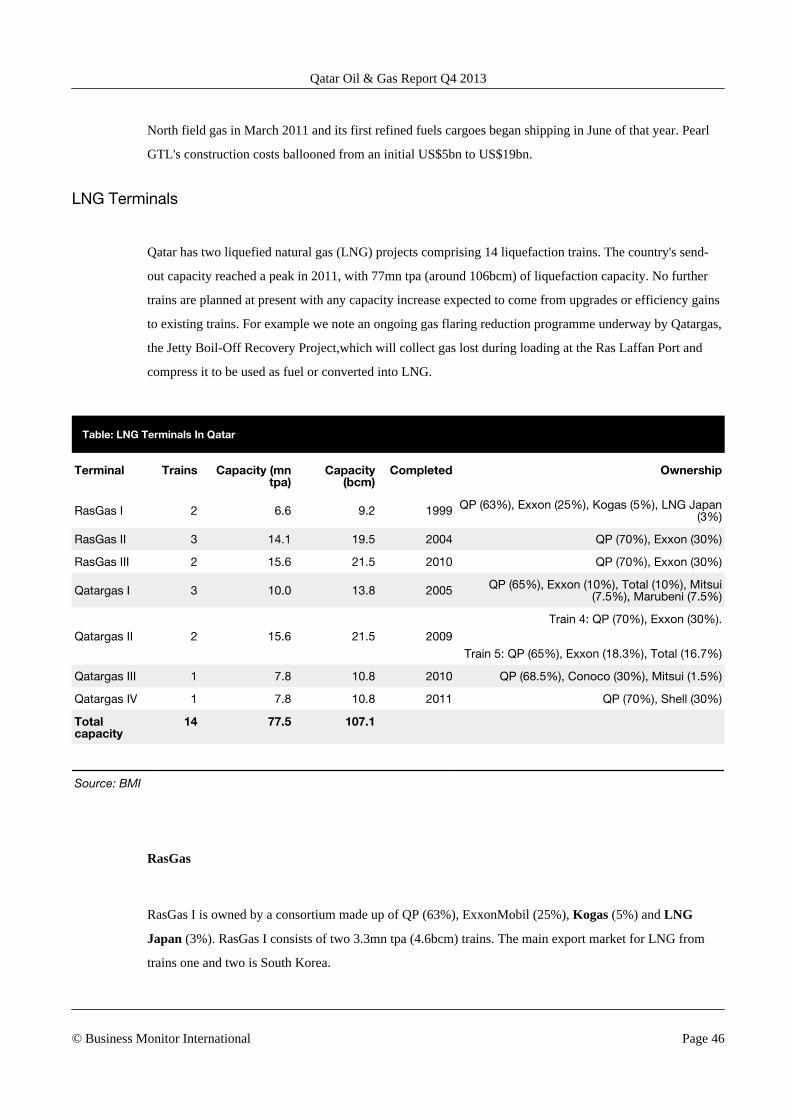

LNG Terminals ...................................................................................................................................... 46Table: LNG Terminals In Qatar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 4

Gas Pipelines ........................................................................................................................................ 48

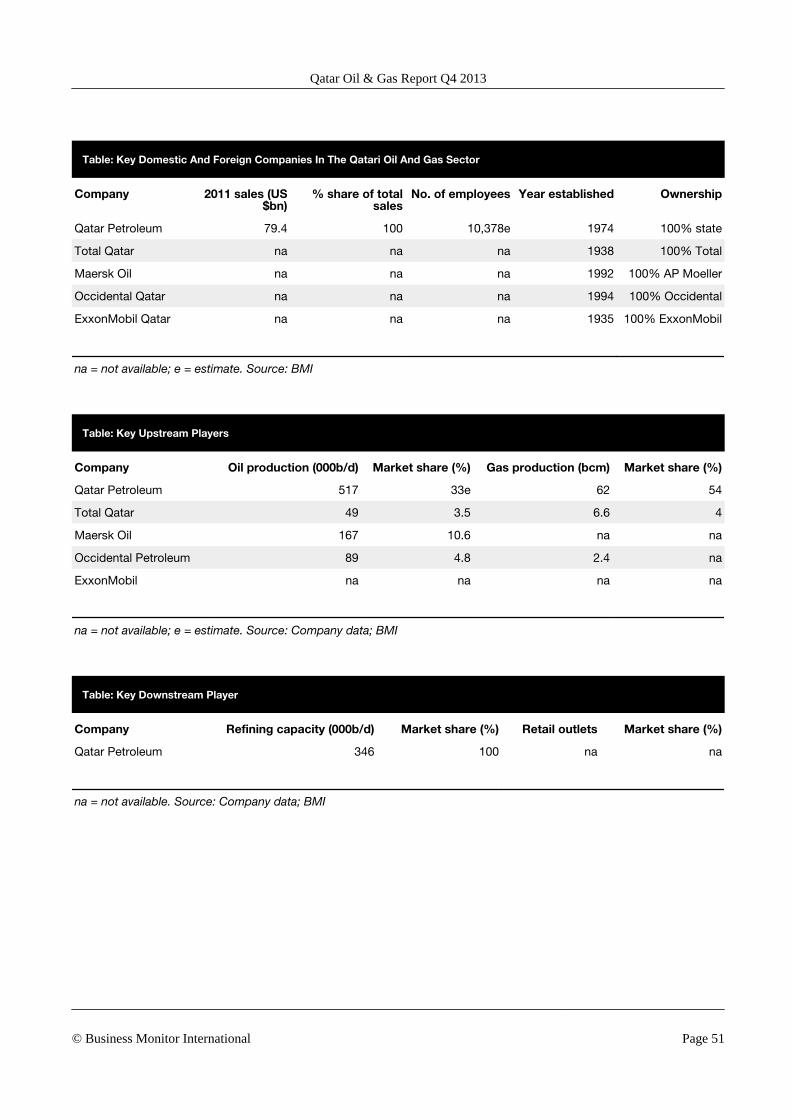

Competitive Landscape .................................................................................................... 50Executive Summary .................................................................................................................................. 50

Table: Key Domestic And Foreign Companies In The Qatari Oil And Gas Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

Table: Key Upstream Players . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

Table: Key Downstream Player . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

Company Profile ................................................................................................................ 52Qatar Petroleum ..................................................................................................................................... 52

ExxonMobil Oil Qatar .............................................................................................................................. 57

Total Qatar ............................................................................................................................................ 60

Royal Dutch Shell .................................................................................................................................... 63

Other Companies - Summary ..................................................................................................................... 66

Regional Overview ............................................................................................................ 72Middle East Energy Market Overview ......................................................................................................... 72

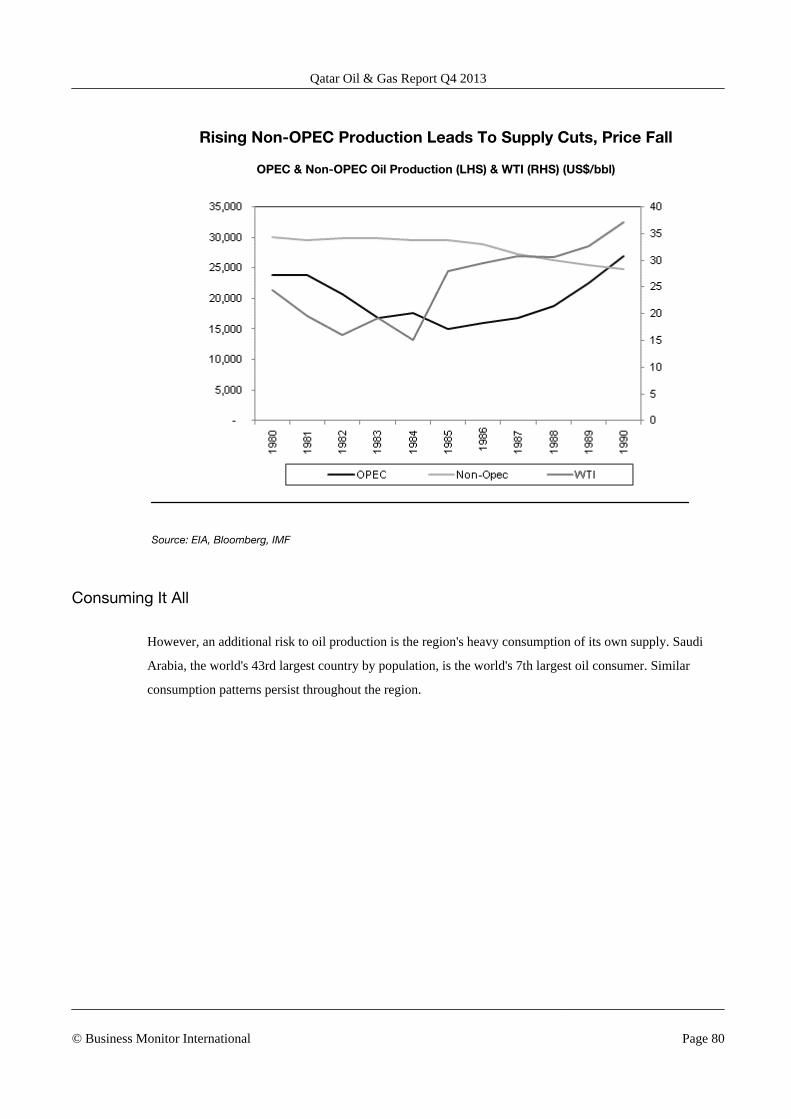

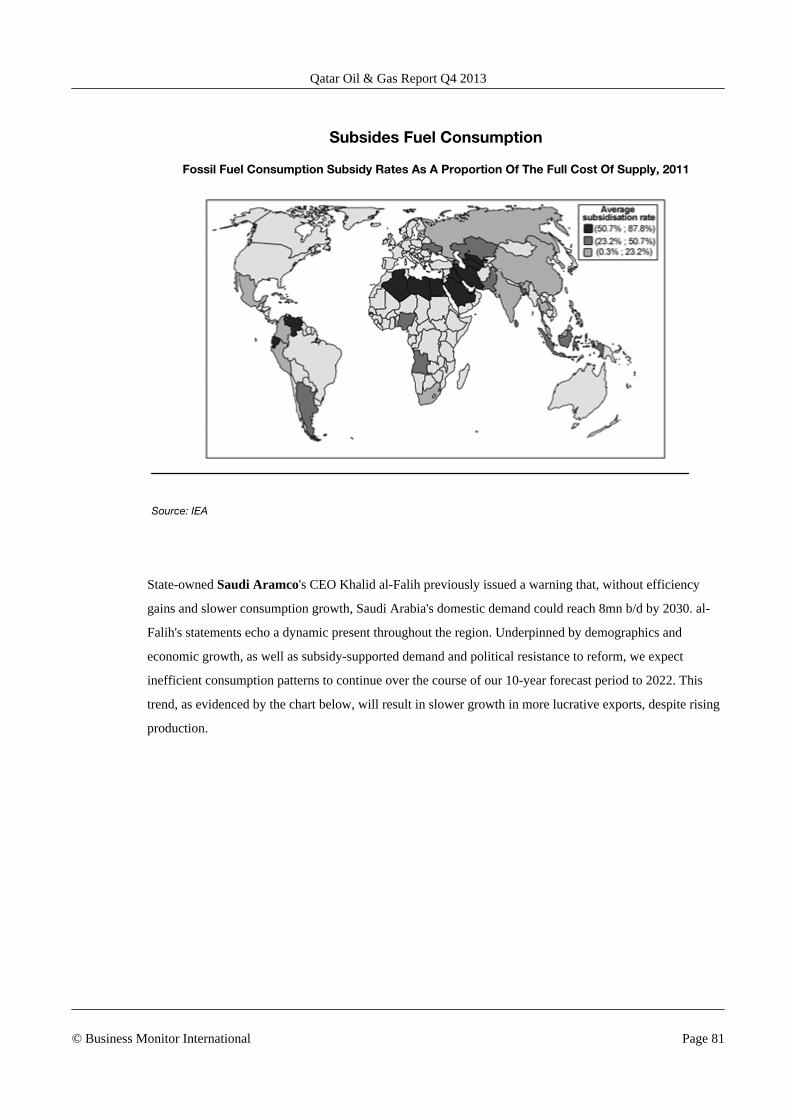

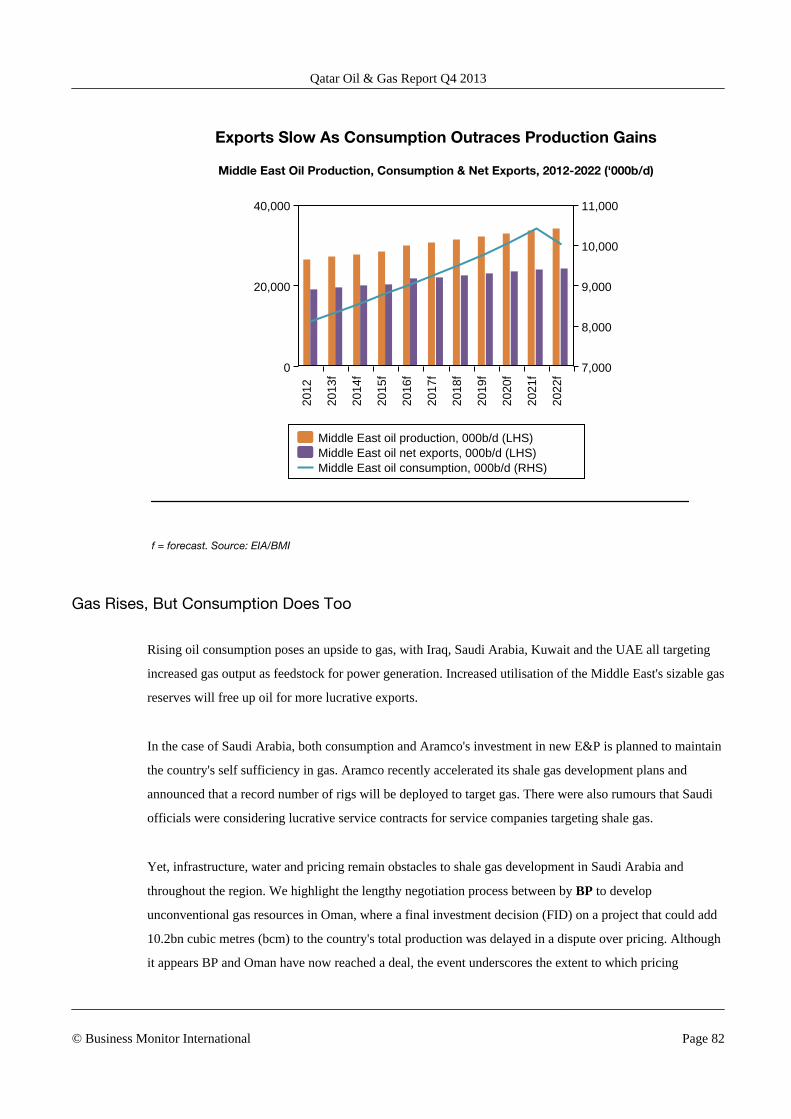

Consuming It All .................................................................................................................................... 80

Gas Rises, But Consumption Does Too ....................................................................................................... 82

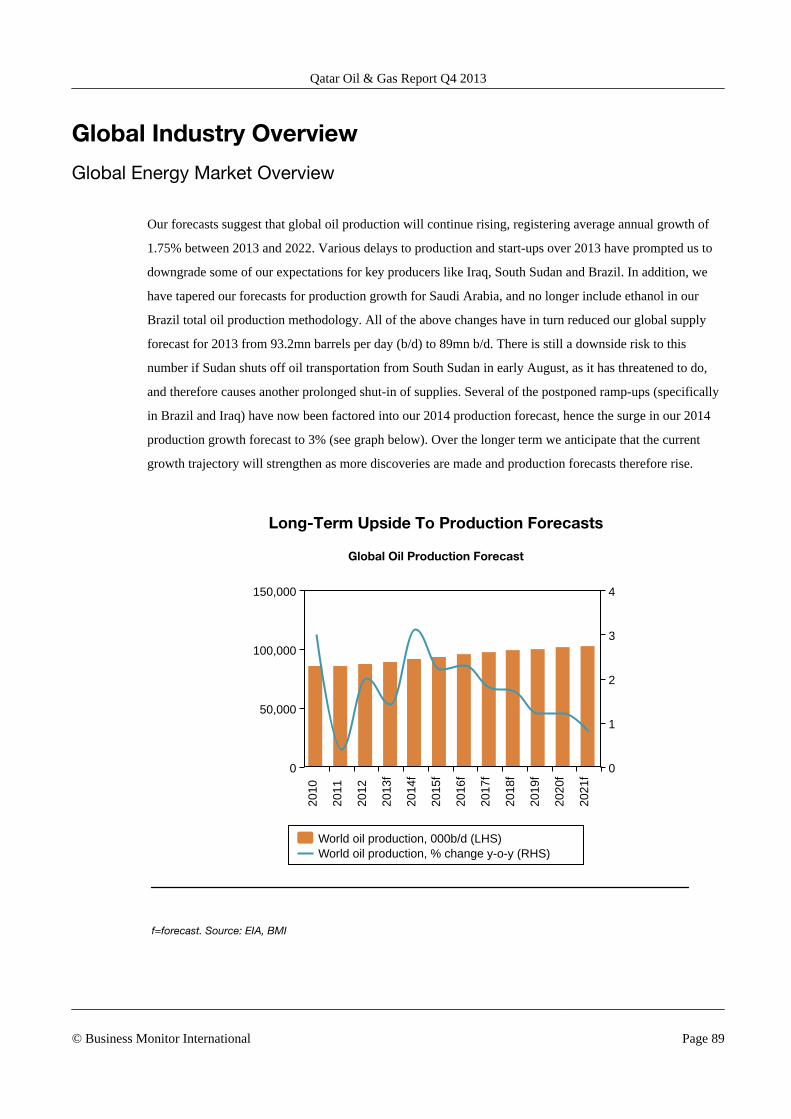

Global Industry Overview .................................................................................................. 89Global Energy Market Overview ................................................................................................................ 89

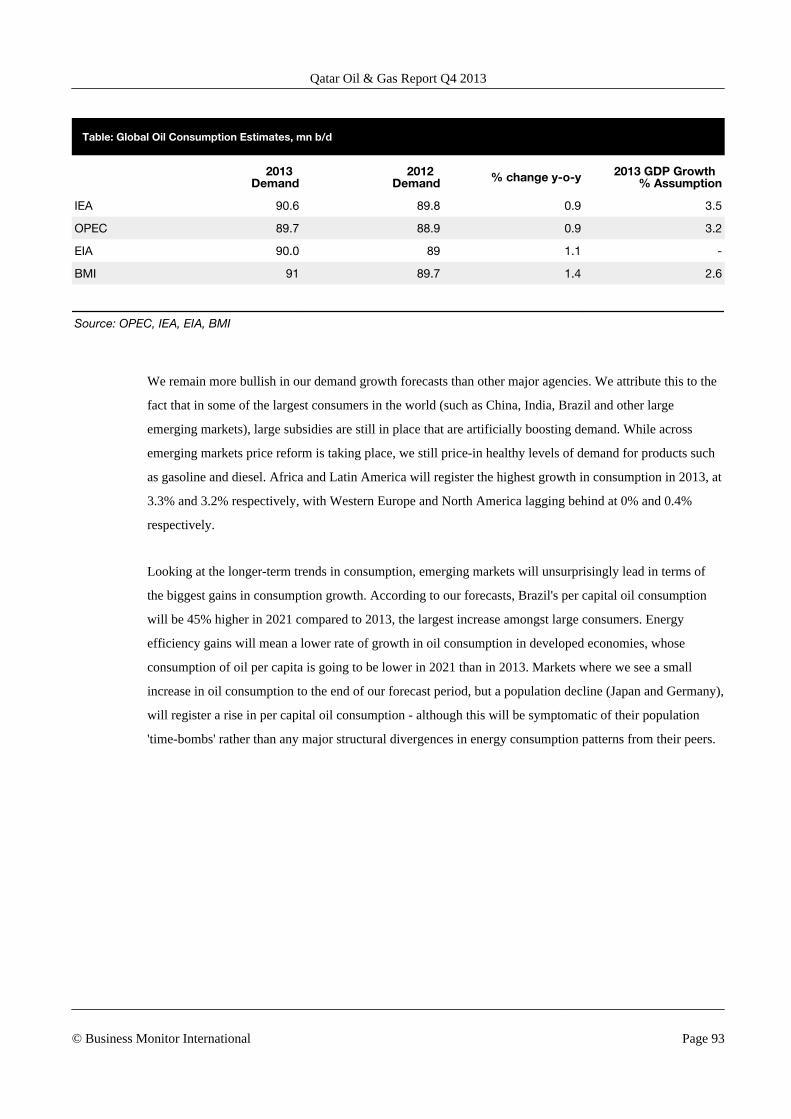

Table: Global Oil Consumption Estimates, mn b/d . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

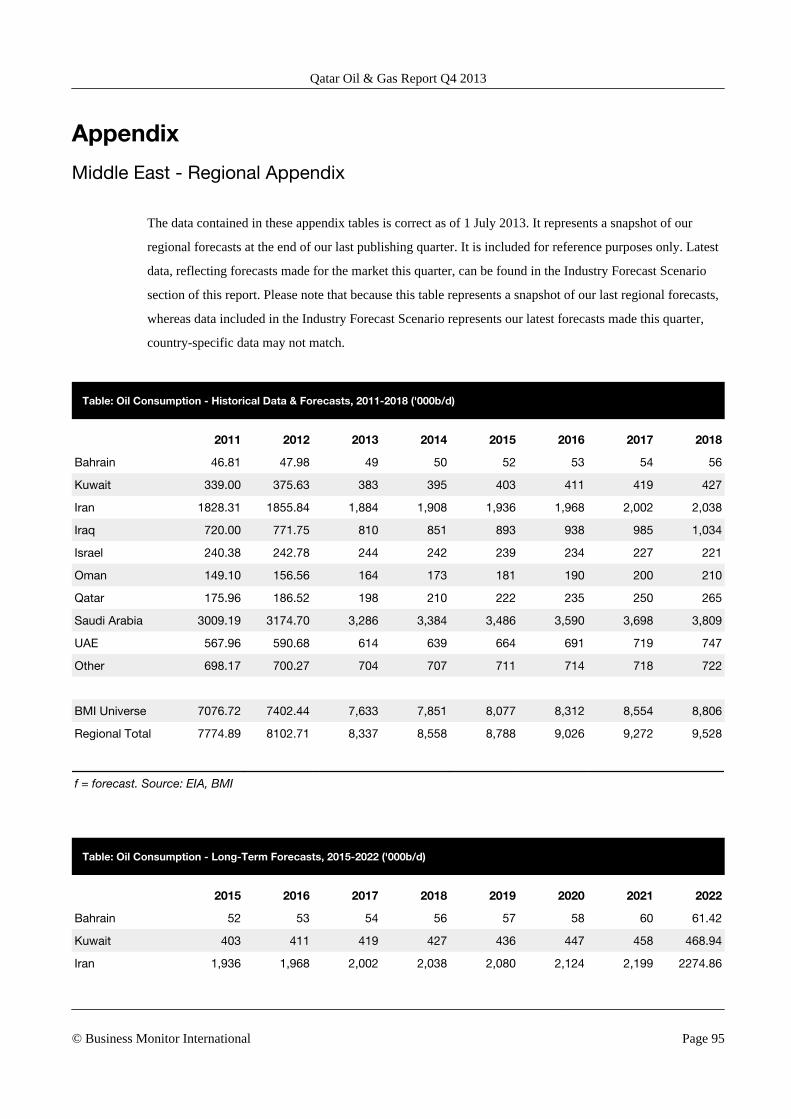

Appendix ............................................................................................................................ 95Middle East - Regional Appendix ................................................................................................................ 95

Table: Oil Consumption - Historical Data & Forecasts, 2011-2018 ('000b/d) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95

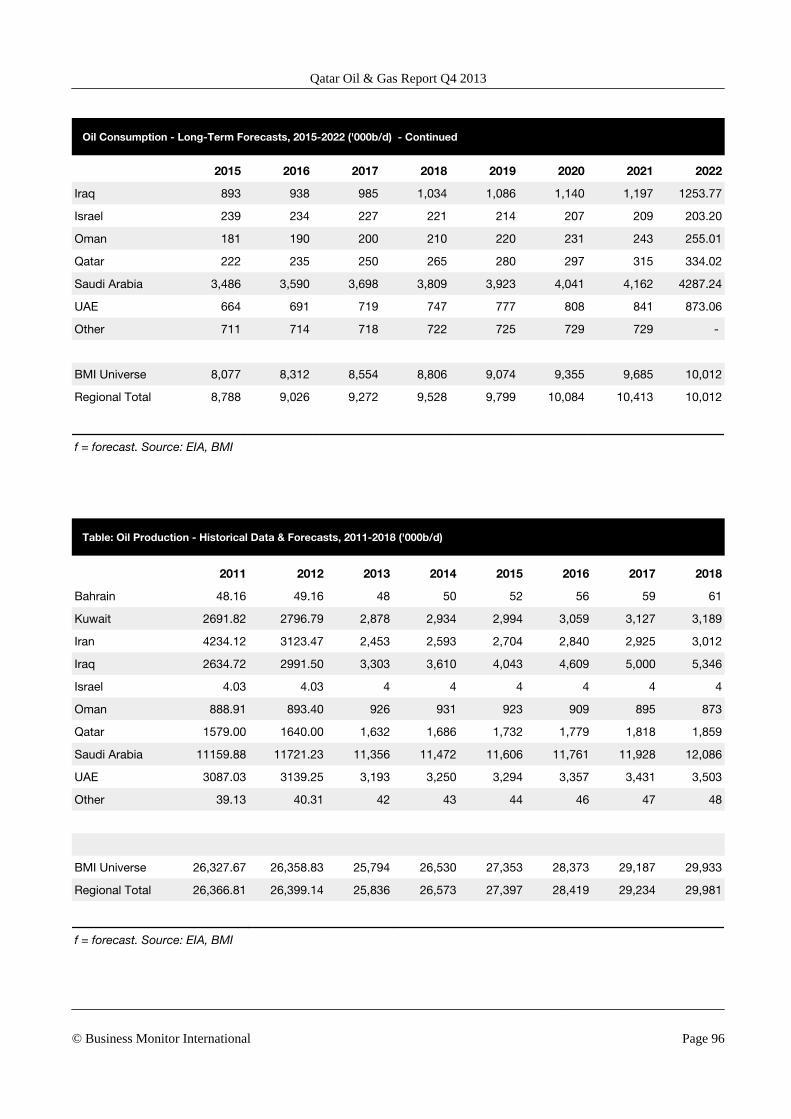

Table: Oil Consumption - Long-Term Forecasts, 2015-2022 ('000b/d) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95

Table: Oil Production - Historical Data & Forecasts, 2011-2018 ('000b/d) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

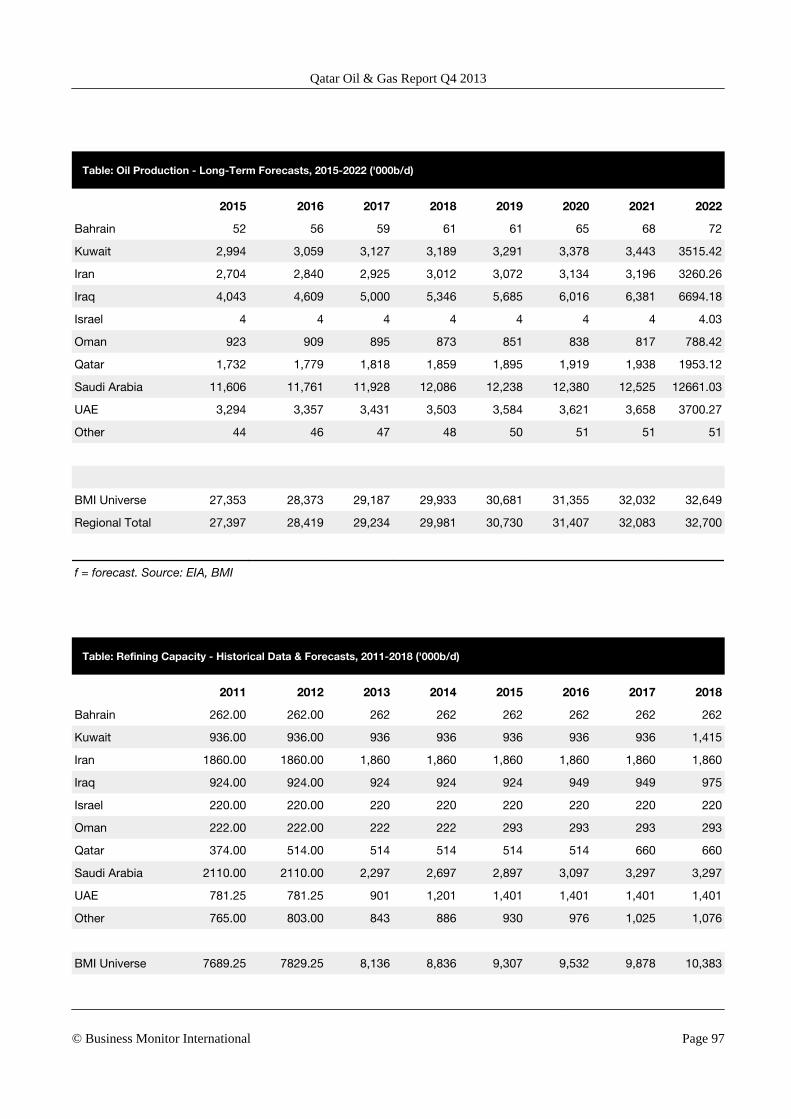

Table: Oil Production - Long-Term Forecasts, 2015-2022 ('000b/d) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97

Table: Refining Capacity - Historical Data & Forecasts, 2011-2018 ('000b/d) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97

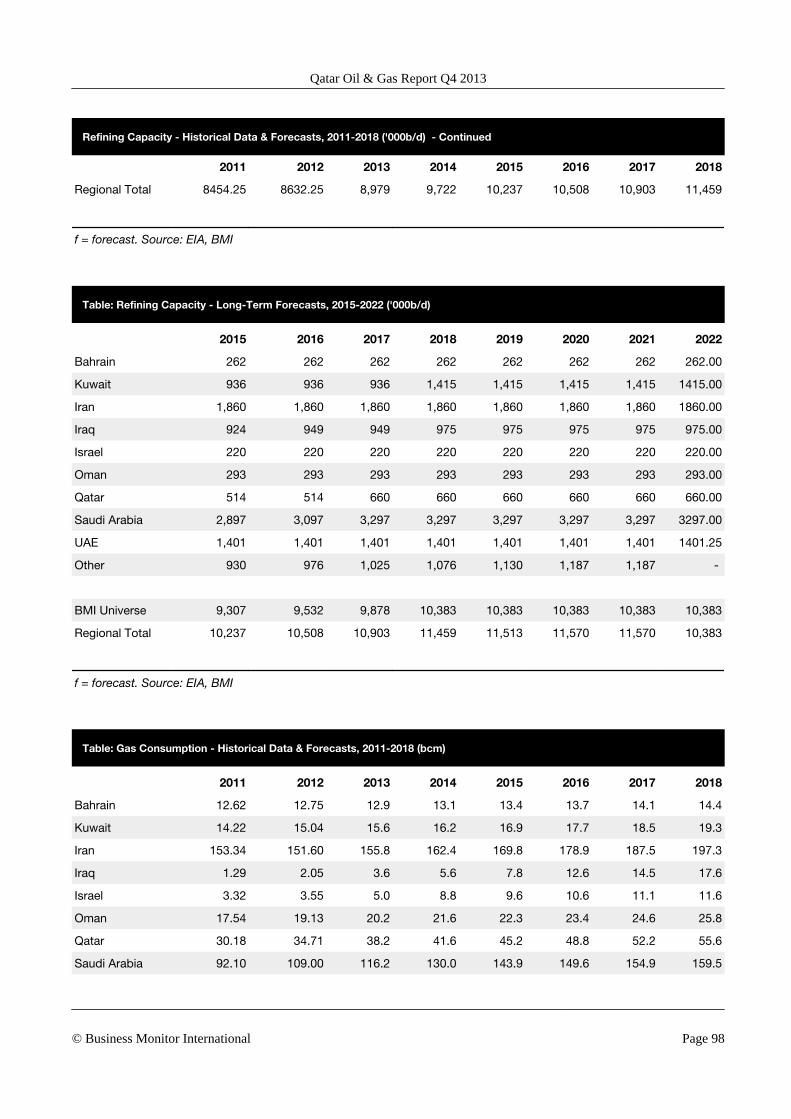

Table: Refining Capacity - Long-Term Forecasts, 2015-2022 ('000b/d) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98

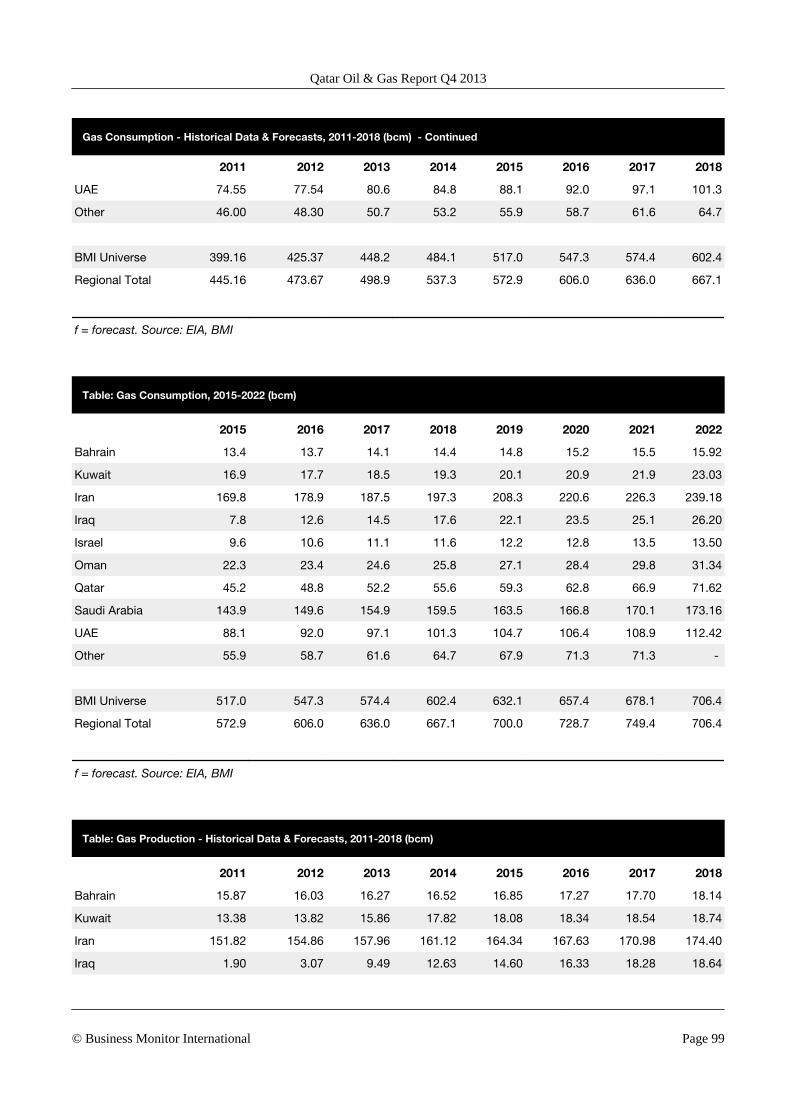

Table: Gas Consumption - Historical Data & Forecasts, 2011-2018 (bcm) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98

Table: Gas Consumption, 2015-2022 (bcm) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 99

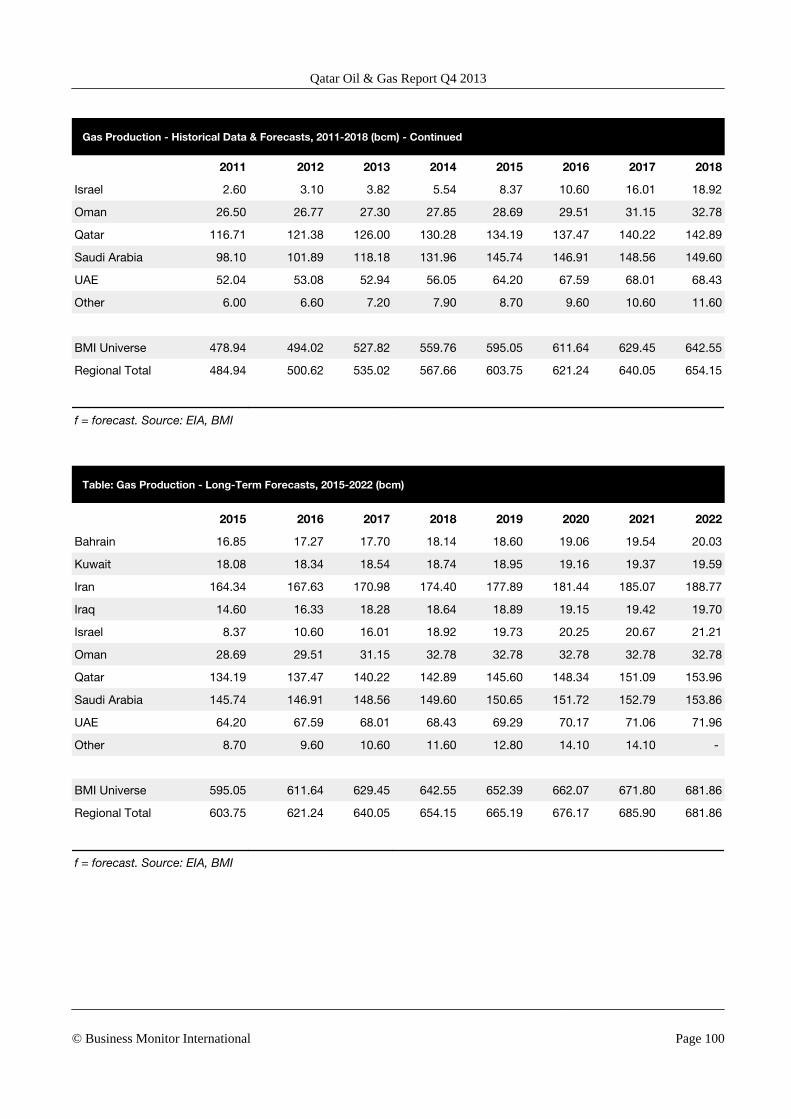

Table: Gas Production - Historical Data & Forecasts, 2011-2018 (bcm) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 99

Table: Gas Production - Long-Term Forecasts, 2015-2022 (bcm) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100

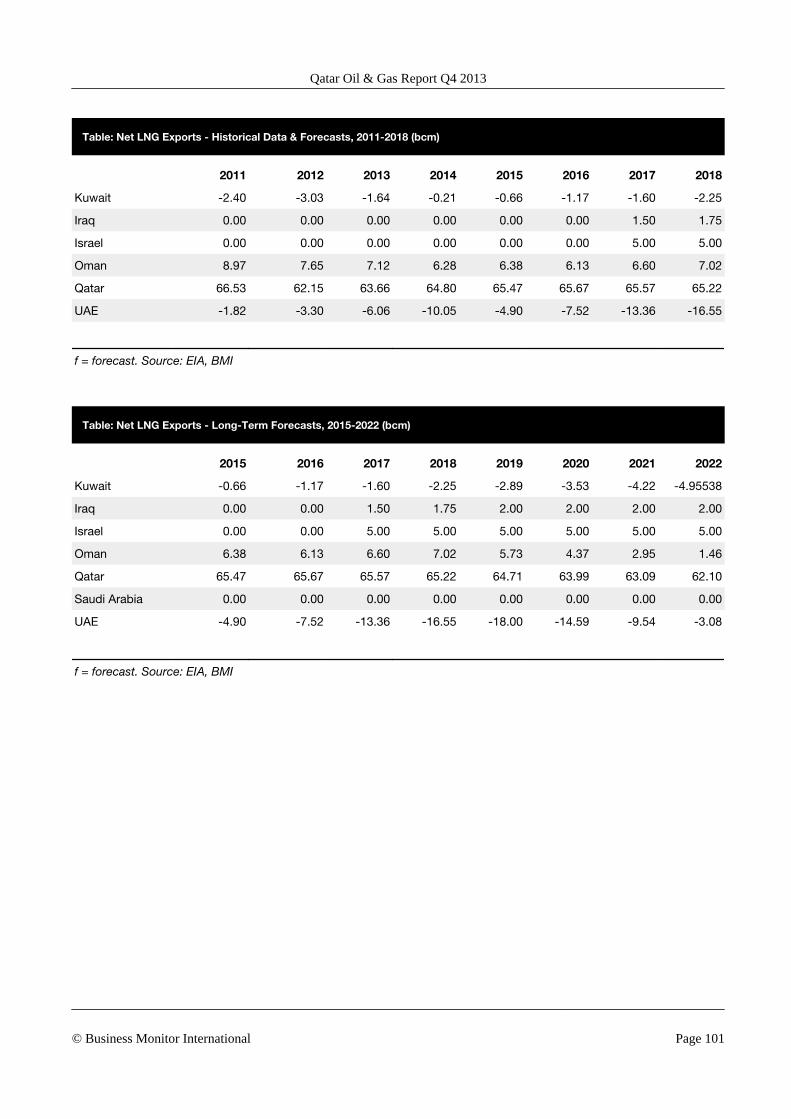

Table: Net LNG Exports - Historical Data & Forecasts, 2011-2018 (bcm) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

Table: Net LNG Exports - Long-Term Forecasts, 2015-2022 (bcm) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

Methodology .................................................................................................................... 102Oil & Gas Risk/Reward Ratings Methodology ........................................................................................... 102

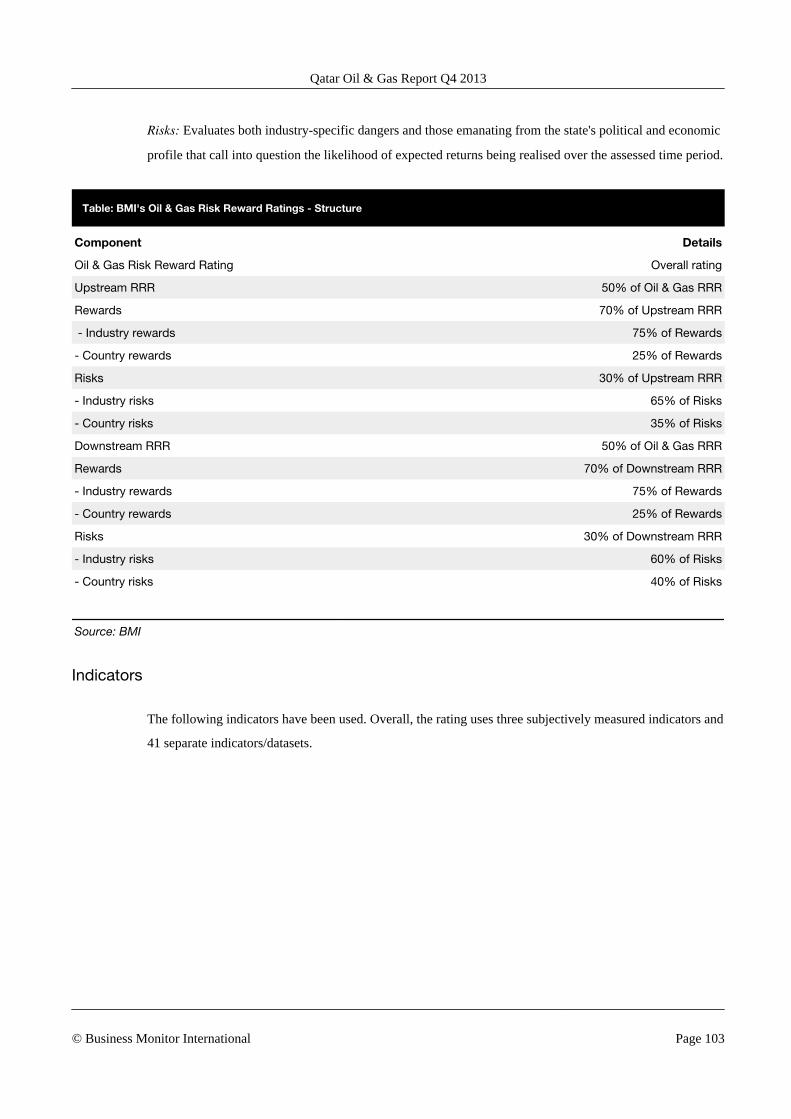

Ratings Overview ................................................................................................................................. 102Table: BMI's Oil & Gas Risk Reward Ratings - Structure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103

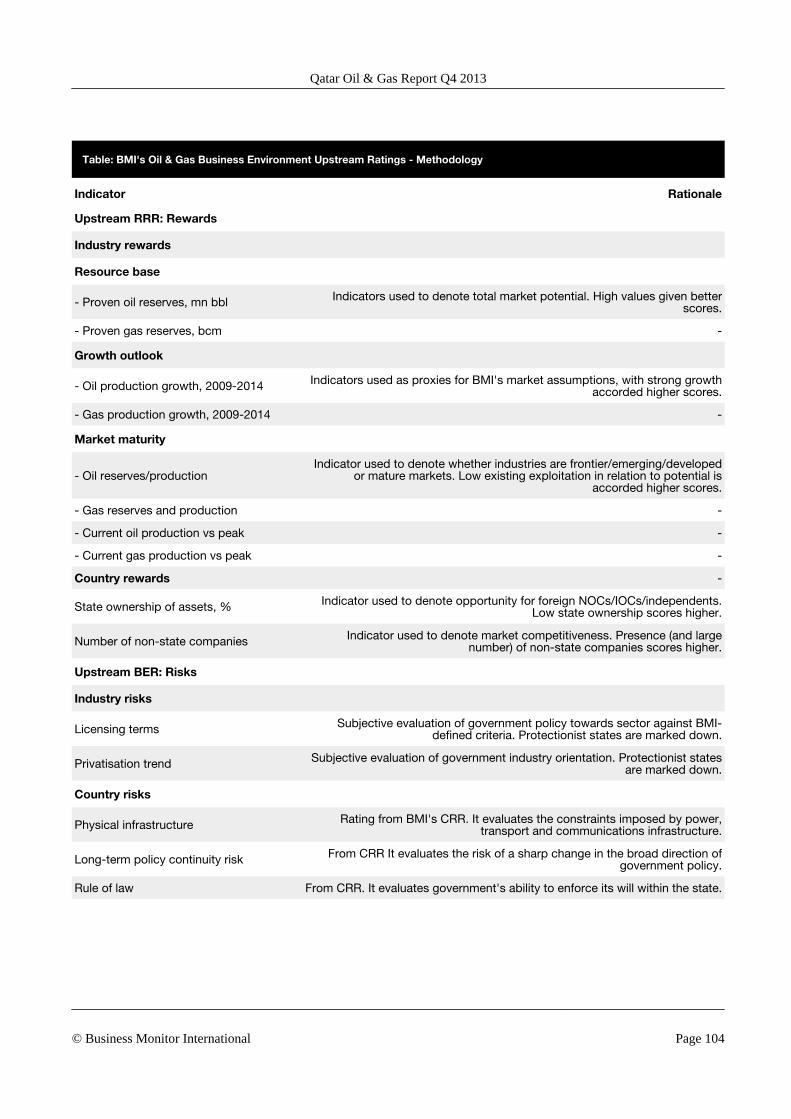

Indicators ........................................................................................................................................... 103Table: BMI's Oil & Gas Business Environment Upstream Ratings - Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 104

Oil & Gas Forecasts Methodology .......................................................................................................... 105

Energy Industry ................................................................................................................................... 106

Cross checks ....................................................................................................................................... 106

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 5

Sources .............................................................................................................................................. 107

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 6

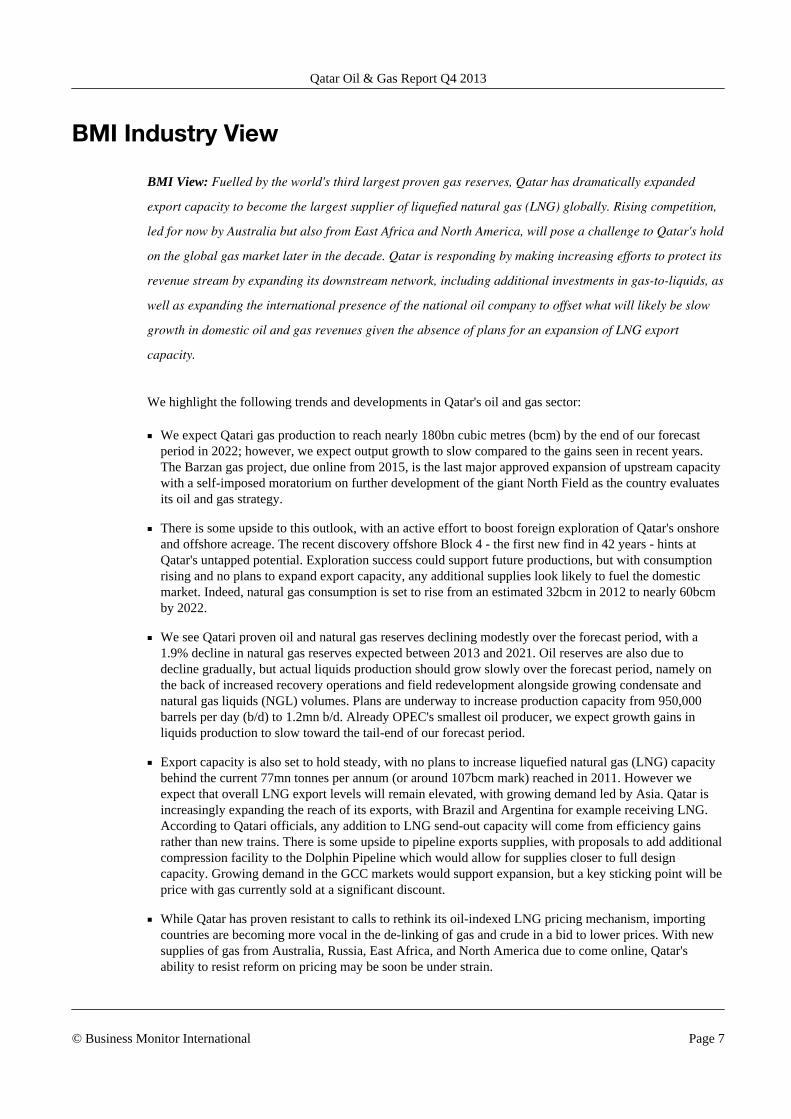

BMI Industry View

BMI View: Fuelled by the world's third largest proven gas reserves, Qatar has dramatically expanded

export capacity to become the largest supplier of liquefied natural gas (LNG) globally. Rising competition,

led for now by Australia but also from East Africa and North America, will pose a challenge to Qatar's hold

on the global gas market later in the decade. Qatar is responding by making increasing efforts to protect its

revenue stream by expanding its downstream network, including additional investments in gas-to-liquids, as

well as expanding the international presence of the national oil company to offset what will likely be slow

growth in domestic oil and gas revenues given the absence of plans for an expansion of LNG export

capacity.

We highlight the following trends and developments in Qatar's oil and gas sector:

■ We expect Qatari gas production to reach nearly 180bn cubic metres (bcm) by the end of our forecastperiod in 2022; however, we expect output growth to slow compared to the gains seen in recent years.The Barzan gas project, due online from 2015, is the last major approved expansion of upstream capacitywith a self-imposed moratorium on further development of the giant North Field as the country evaluatesits oil and gas strategy.

■ There is some upside to this outlook, with an active effort to boost foreign exploration of Qatar's onshoreand offshore acreage. The recent discovery offshore Block 4 - the first new find in 42 years - hints atQatar's untapped potential. Exploration success could support future productions, but with consumptionrising and no plans to expand export capacity, any additional supplies look likely to fuel the domesticmarket. Indeed, natural gas consumption is set to rise from an estimated 32bcm in 2012 to nearly 60bcmby 2022.

■ We see Qatari proven oil and natural gas reserves declining modestly over the forecast period, with a1.9% decline in natural gas reserves expected between 2013 and 2021. Oil reserves are also due todecline gradually, but actual liquids production should grow slowly over the forecast period, namely onthe back of increased recovery operations and field redevelopment alongside growing condensate andnatural gas liquids (NGL) volumes. Plans are underway to increase production capacity from 950,000barrels per day (b/d) to 1.2mn b/d. Already OPEC's smallest oil producer, we expect growth gains inliquids production to slow toward the tail-end of our forecast period.

■ Export capacity is also set to hold steady, with no plans to increase liquefied natural gas (LNG) capacitybehind the current 77mn tonnes per annum (or around 107bcm mark) reached in 2011. However weexpect that overall LNG export levels will remain elevated, with growing demand led by Asia. Qatar isincreasingly expanding the reach of its exports, with Brazil and Argentina for example receiving LNG.According to Qatari officials, any addition to LNG send-out capacity will come from efficiency gainsrather than new trains. There is some upside to pipeline exports supplies, with proposals to add additionalcompression facility to the Dolphin Pipeline which would allow for supplies closer to full designcapacity. Growing demand in the GCC markets would support expansion, but a key sticking point will beprice with gas currently sold at a significant discount.

■ While Qatar has proven resistant to calls to rethink its oil-indexed LNG pricing mechanism, importingcountries are becoming more vocal in the de-linking of gas and crude in a bid to lower prices. With newsupplies of gas from Australia, Russia, East Africa, and North America due to come online, Qatar'sability to resist reform on pricing may be soon be under strain.

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 7

Qatar's dependence on oil leads to high volatility in the country's export revenues. Our assumptions of

slower growth in China and persistent economic weakness in the eurozone, pose a threat to global oil

demand. At the time of writing, we are forecasting average OPEC basket oil prices to fall from US$109/bbl

in 2013 to US$101/bbl in 2014. While lower prices will result in less revenue after years of elevated prices,

large fiscal and current account surpluses, as well as a sizable foreign exchange (FX) reserves, provide the

economy with a significant buffer in the event of any short-term decline in oil prices.

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 8

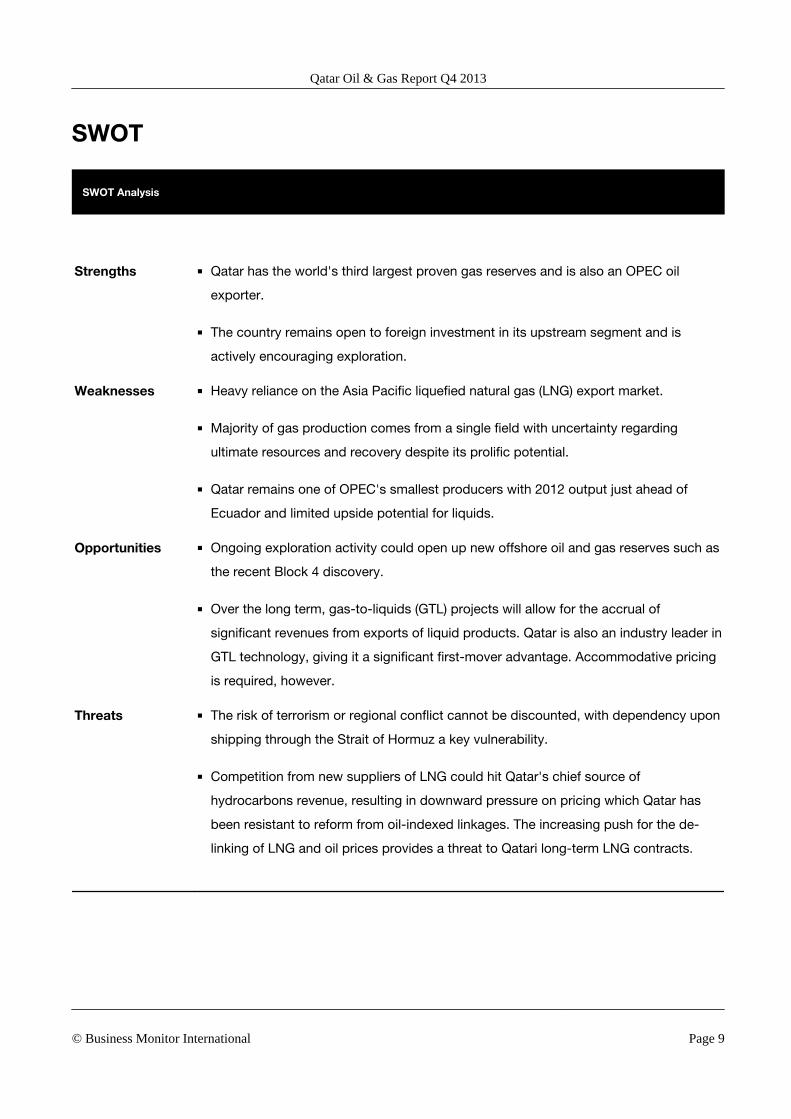

SWOT

SWOT Analysis

Strengths ■ Qatar has the world's third largest proven gas reserves and is also an OPEC oil

exporter.

■ The country remains open to foreign investment in its upstream segment and is

actively encouraging exploration.

Weaknesses ■ Heavy reliance on the Asia Pacific liquefied natural gas (LNG) export market.

■ Majority of gas production comes from a single field with uncertainty regarding

ultimate resources and recovery despite its prolific potential.

■ Qatar remains one of OPEC's smallest producers with 2012 output just ahead of

Ecuador and limited upside potential for liquids.

Opportunities ■ Ongoing exploration activity could open up new offshore oil and gas reserves such as

the recent Block 4 discovery.

■ Over the long term, gas-to-liquids (GTL) projects will allow for the accrual of

significant revenues from exports of liquid products. Qatar is also an industry leader in

GTL technology, giving it a significant first-mover advantage. Accommodative pricing

is required, however.

Threats ■ The risk of terrorism or regional conflict cannot be discounted, with dependency upon

shipping through the Strait of Hormuz a key vulnerability.

■ Competition from new suppliers of LNG could hit Qatar's chief source of

hydrocarbons revenue, resulting in downward pressure on pricing which Qatar has

been resistant to reform from oil-indexed linkages. The increasing push for the de-

linking of LNG and oil prices provides a threat to Qatari long-term LNG contracts.

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 9

Industry Forecast

Oil And Gas Reserves

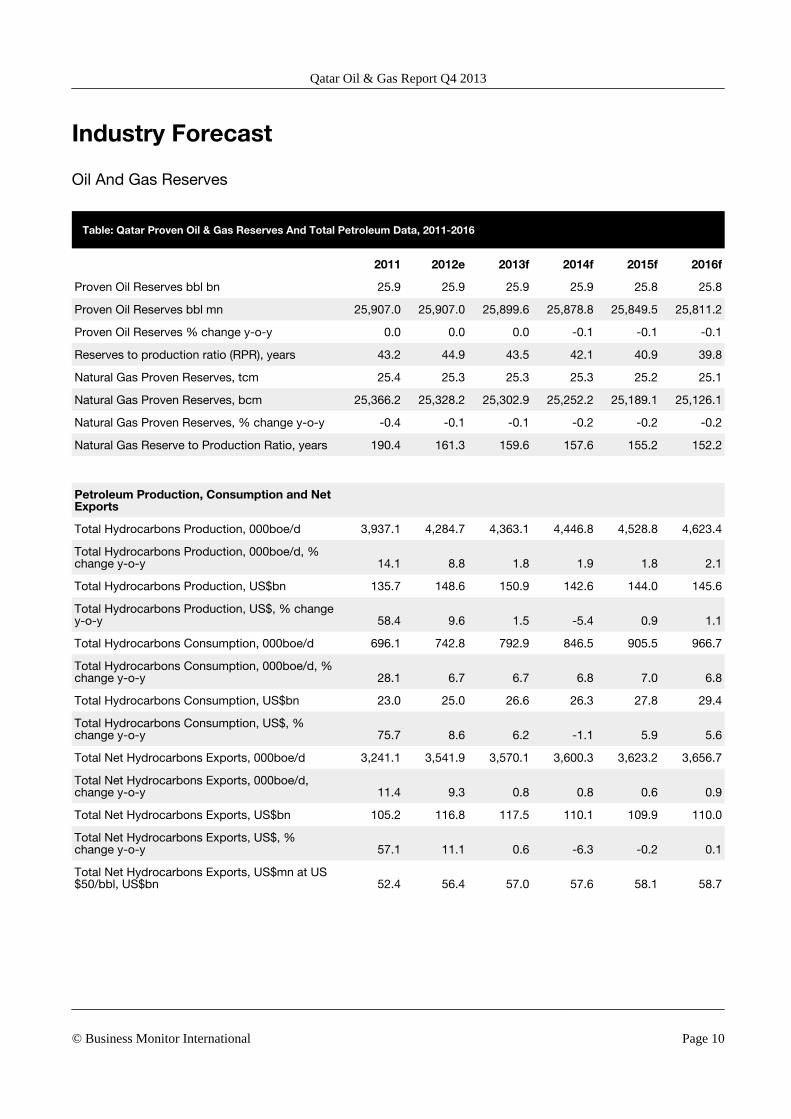

Table: Qatar Proven Oil & Gas Reserves And Total Petroleum Data, 2011-2016

2011 2012e 2013f 2014f 2015f 2016f

Proven Oil Reserves bbl bn 25.9 25.9 25.9 25.9 25.8 25.8

Proven Oil Reserves bbl mn 25,907.0 25,907.0 25,899.6 25,878.8 25,849.5 25,811.2

Proven Oil Reserves % change y-o-y 0.0 0.0 0.0 -0.1 -0.1 -0.1

Reserves to production ratio (RPR), years 43.2 44.9 43.5 42.1 40.9 39.8

Natural Gas Proven Reserves, tcm 25.4 25.3 25.3 25.3 25.2 25.1

Natural Gas Proven Reserves, bcm 25,366.2 25,328.2 25,302.9 25,252.2 25,189.1 25,126.1

Natural Gas Proven Reserves, % change y-o-y -0.4 -0.1 -0.1 -0.2 -0.2 -0.2

Natural Gas Reserve to Production Ratio, years 190.4 161.3 159.6 157.6 155.2 152.2

Petroleum Production, Consumption and NetExports

Total Hydrocarbons Production, 000boe/d 3,937.1 4,284.7 4,363.1 4,446.8 4,528.8 4,623.4

Total Hydrocarbons Production, 000boe/d, %change y-o-y 14.1 8.8 1.8 1.9 1.8 2.1

Total Hydrocarbons Production, US$bn 135.7 148.6 150.9 142.6 144.0 145.6

Total Hydrocarbons Production, US$, % changey-o-y 58.4 9.6 1.5 -5.4 0.9 1.1

Total Hydrocarbons Consumption, 000boe/d 696.1 742.8 792.9 846.5 905.5 966.7

Total Hydrocarbons Consumption, 000boe/d, %change y-o-y 28.1 6.7 6.7 6.8 7.0 6.8

Total Hydrocarbons Consumption, US$bn 23.0 25.0 26.6 26.3 27.8 29.4

Total Hydrocarbons Consumption, US$, %change y-o-y 75.7 8.6 6.2 -1.1 5.9 5.6

Total Net Hydrocarbons Exports, 000boe/d 3,241.1 3,541.9 3,570.1 3,600.3 3,623.2 3,656.7

Total Net Hydrocarbons Exports, 000boe/d,change y-o-y 11.4 9.3 0.8 0.8 0.6 0.9

Total Net Hydrocarbons Exports, US$bn 105.2 116.8 117.5 110.1 109.9 110.0

Total Net Hydrocarbons Exports, US$, %change y-o-y 57.1 11.1 0.6 -6.3 -0.2 0.1

Total Net Hydrocarbons Exports, US$mn at US$50/bbl, US$bn 52.4 56.4 57.0 57.6 58.1 58.7

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 10

Qatar Proven Oil & Gas Reserves And Total Petroleum Data, 2011-2016 - Continued

2011 2012e 2013f 2014f 2015f 2016f

Total Net Hydrocarbons Exports, US$mn at US$100/bbl, US$bn 104.7 112.9 114.0 115.2 116.1 117.3

e/f = estimate/forecast. Source: EIA, BMI

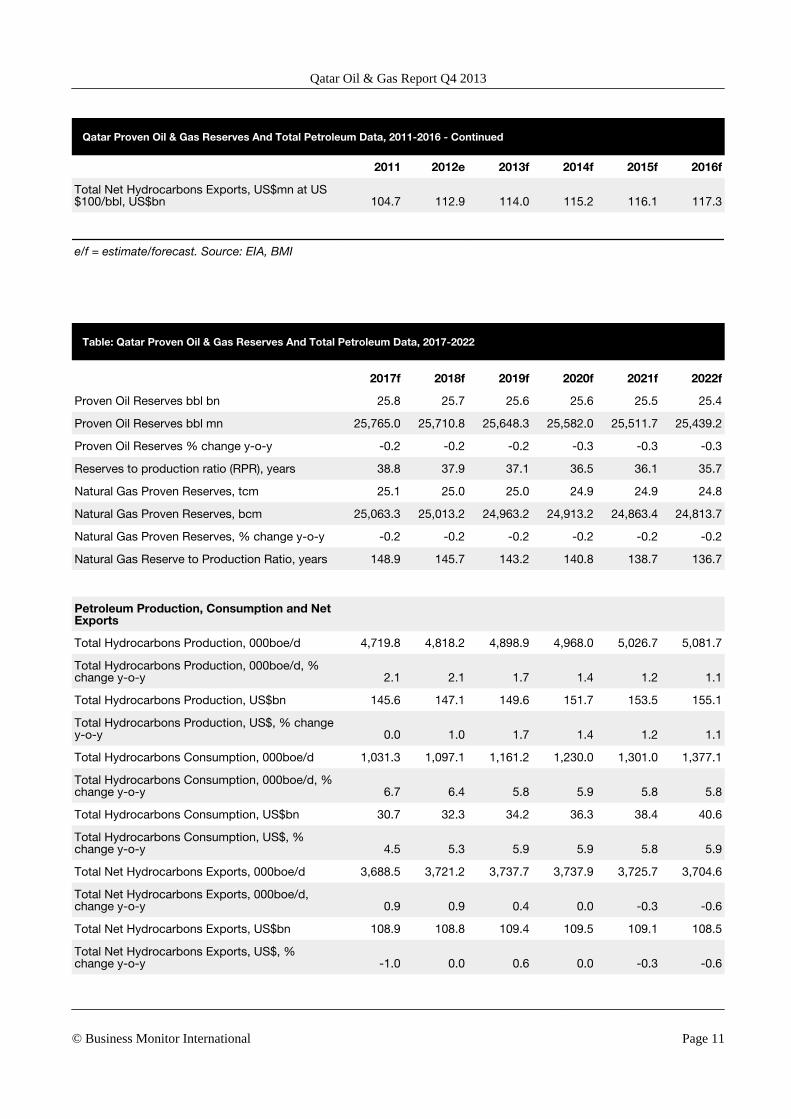

Table: Qatar Proven Oil & Gas Reserves And Total Petroleum Data, 2017-2022

2017f 2018f 2019f 2020f 2021f 2022f

Proven Oil Reserves bbl bn 25.8 25.7 25.6 25.6 25.5 25.4

Proven Oil Reserves bbl mn 25,765.0 25,710.8 25,648.3 25,582.0 25,511.7 25,439.2

Proven Oil Reserves % change y-o-y -0.2 -0.2 -0.2 -0.3 -0.3 -0.3

Reserves to production ratio (RPR), years 38.8 37.9 37.1 36.5 36.1 35.7

Natural Gas Proven Reserves, tcm 25.1 25.0 25.0 24.9 24.9 24.8

Natural Gas Proven Reserves, bcm 25,063.3 25,013.2 24,963.2 24,913.2 24,863.4 24,813.7

Natural Gas Proven Reserves, % change y-o-y -0.2 -0.2 -0.2 -0.2 -0.2 -0.2

Natural Gas Reserve to Production Ratio, years 148.9 145.7 143.2 140.8 138.7 136.7

Petroleum Production, Consumption and NetExports

Total Hydrocarbons Production, 000boe/d 4,719.8 4,818.2 4,898.9 4,968.0 5,026.7 5,081.7

Total Hydrocarbons Production, 000boe/d, %change y-o-y 2.1 2.1 1.7 1.4 1.2 1.1

Total Hydrocarbons Production, US$bn 145.6 147.1 149.6 151.7 153.5 155.1

Total Hydrocarbons Production, US$, % changey-o-y 0.0 1.0 1.7 1.4 1.2 1.1

Total Hydrocarbons Consumption, 000boe/d 1,031.3 1,097.1 1,161.2 1,230.0 1,301.0 1,377.1

Total Hydrocarbons Consumption, 000boe/d, %change y-o-y 6.7 6.4 5.8 5.9 5.8 5.8

Total Hydrocarbons Consumption, US$bn 30.7 32.3 34.2 36.3 38.4 40.6

Total Hydrocarbons Consumption, US$, %change y-o-y 4.5 5.3 5.9 5.9 5.8 5.9

Total Net Hydrocarbons Exports, 000boe/d 3,688.5 3,721.2 3,737.7 3,737.9 3,725.7 3,704.6

Total Net Hydrocarbons Exports, 000boe/d,change y-o-y 0.9 0.9 0.4 0.0 -0.3 -0.6

Total Net Hydrocarbons Exports, US$bn 108.9 108.8 109.4 109.5 109.1 108.5

Total Net Hydrocarbons Exports, US$, %change y-o-y -1.0 0.0 0.6 0.0 -0.3 -0.6

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 11

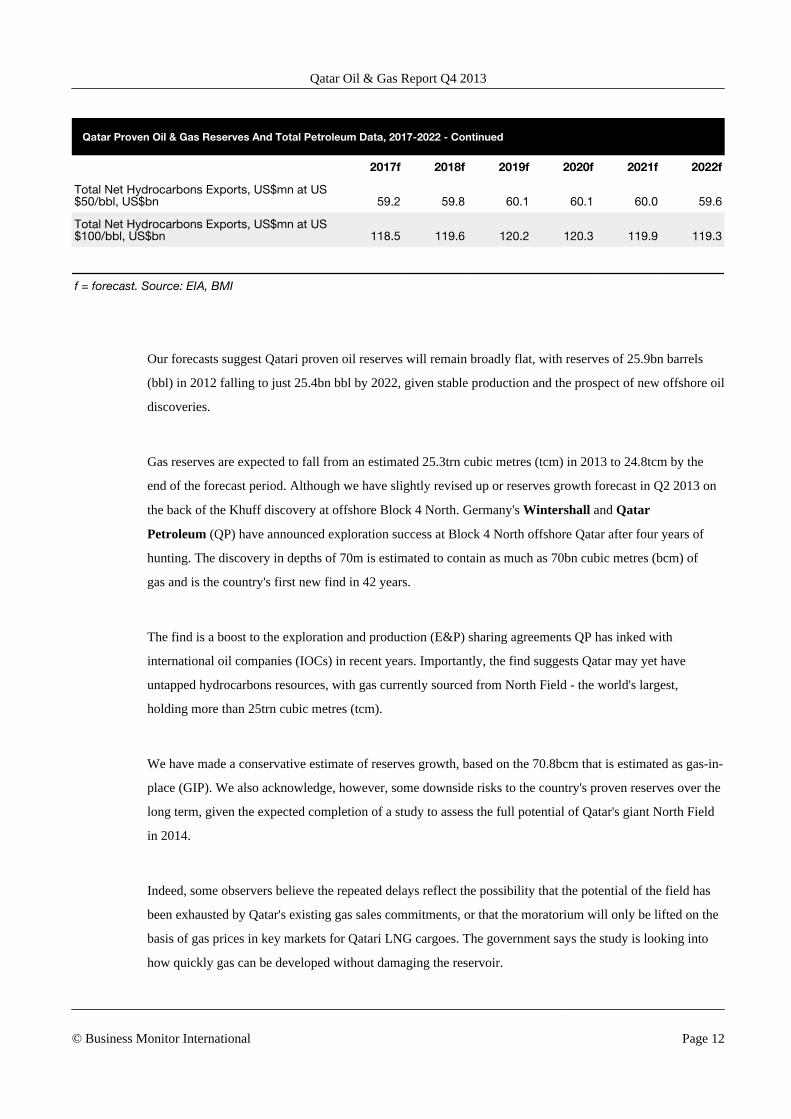

Qatar Proven Oil & Gas Reserves And Total Petroleum Data, 2017-2022 - Continued

2017f 2018f 2019f 2020f 2021f 2022f

Total Net Hydrocarbons Exports, US$mn at US$50/bbl, US$bn 59.2 59.8 60.1 60.1 60.0 59.6

Total Net Hydrocarbons Exports, US$mn at US$100/bbl, US$bn 118.5 119.6 120.2 120.3 119.9 119.3

f = forecast. Source: EIA, BMI

Our forecasts suggest Qatari proven oil reserves will remain broadly flat, with reserves of 25.9bn barrels

(bbl) in 2012 falling to just 25.4bn bbl by 2022, given stable production and the prospect of new offshore oil

discoveries.

Gas reserves are expected to fall from an estimated 25.3trn cubic metres (tcm) in 2013 to 24.8tcm by the

end of the forecast period. Although we have slightly revised up or reserves growth forecast in Q2 2013 on

the back of the Khuff discovery at offshore Block 4 North. Germany's Wintershall and Qatar

Petroleum (QP) have announced exploration success at Block 4 North offshore Qatar after four years of

hunting. The discovery in depths of 70m is estimated to contain as much as 70bn cubic metres (bcm) of

gas and is the country's first new find in 42 years.

The find is a boost to the exploration and production (E&P) sharing agreements QP has inked with

international oil companies (IOCs) in recent years. Importantly, the find suggests Qatar may yet have

untapped hydrocarbons resources, with gas currently sourced from North Field - the world's largest,

holding more than 25trn cubic metres (tcm).

We have made a conservative estimate of reserves growth, based on the 70.8bcm that is estimated as gas-in-

place (GIP). We also acknowledge, however, some downside risks to the country's proven reserves over the

long term, given the expected completion of a study to assess the full potential of Qatar's giant North Field

in 2014.

Indeed, some observers believe the repeated delays reflect the possibility that the potential of the field has

been exhausted by Qatar's existing gas sales commitments, or that the moratorium will only be lifted on the

basis of gas prices in key markets for Qatari LNG cargoes. The government says the study is looking into

how quickly gas can be developed without damaging the reservoir.

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 12

Oil Supply And Demand

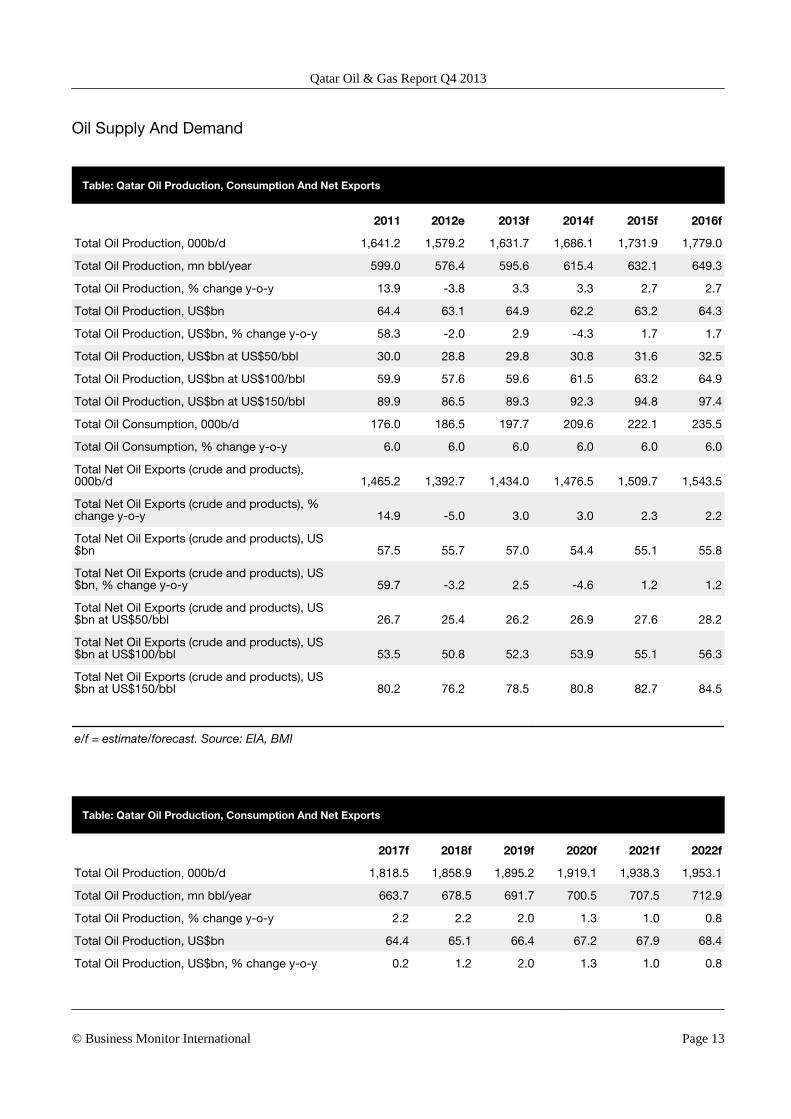

Table: Qatar Oil Production, Consumption And Net Exports

2011 2012e 2013f 2014f 2015f 2016f

Total Oil Production, 000b/d 1,641.2 1,579.2 1,631.7 1,686.1 1,731.9 1,779.0

Total Oil Production, mn bbl/year 599.0 576.4 595.6 615.4 632.1 649.3

Total Oil Production, % change y-o-y 13.9 -3.8 3.3 3.3 2.7 2.7

Total Oil Production, US$bn 64.4 63.1 64.9 62.2 63.2 64.3

Total Oil Production, US$bn, % change y-o-y 58.3 -2.0 2.9 -4.3 1.7 1.7

Total Oil Production, US$bn at US$50/bbl 30.0 28.8 29.8 30.8 31.6 32.5

Total Oil Production, US$bn at US$100/bbl 59.9 57.6 59.6 61.5 63.2 64.9

Total Oil Production, US$bn at US$150/bbl 89.9 86.5 89.3 92.3 94.8 97.4

Total Oil Consumption, 000b/d 176.0 186.5 197.7 209.6 222.1 235.5

Total Oil Consumption, % change y-o-y 6.0 6.0 6.0 6.0 6.0 6.0

Total Net Oil Exports (crude and products),000b/d 1,465.2 1,392.7 1,434.0 1,476.5 1,509.7 1,543.5

Total Net Oil Exports (crude and products), %change y-o-y 14.9 -5.0 3.0 3.0 2.3 2.2

Total Net Oil Exports (crude and products), US$bn 57.5 55.7 57.0 54.4 55.1 55.8

Total Net Oil Exports (crude and products), US$bn, % change y-o-y 59.7 -3.2 2.5 -4.6 1.2 1.2

Total Net Oil Exports (crude and products), US$bn at US$50/bbl 26.7 25.4 26.2 26.9 27.6 28.2

Total Net Oil Exports (crude and products), US$bn at US$100/bbl 53.5 50.8 52.3 53.9 55.1 56.3

Total Net Oil Exports (crude and products), US$bn at US$150/bbl 80.2 76.2 78.5 80.8 82.7 84.5

e/f = estimate/forecast. Source: EIA, BMI

Table: Qatar Oil Production, Consumption And Net Exports

2017f 2018f 2019f 2020f 2021f 2022f

Total Oil Production, 000b/d 1,818.5 1,858.9 1,895.2 1,919.1 1,938.3 1,953.1

Total Oil Production, mn bbl/year 663.7 678.5 691.7 700.5 707.5 712.9

Total Oil Production, % change y-o-y 2.2 2.2 2.0 1.3 1.0 0.8

Total Oil Production, US$bn 64.4 65.1 66.4 67.2 67.9 68.4

Total Oil Production, US$bn, % change y-o-y 0.2 1.2 2.0 1.3 1.0 0.8

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 13

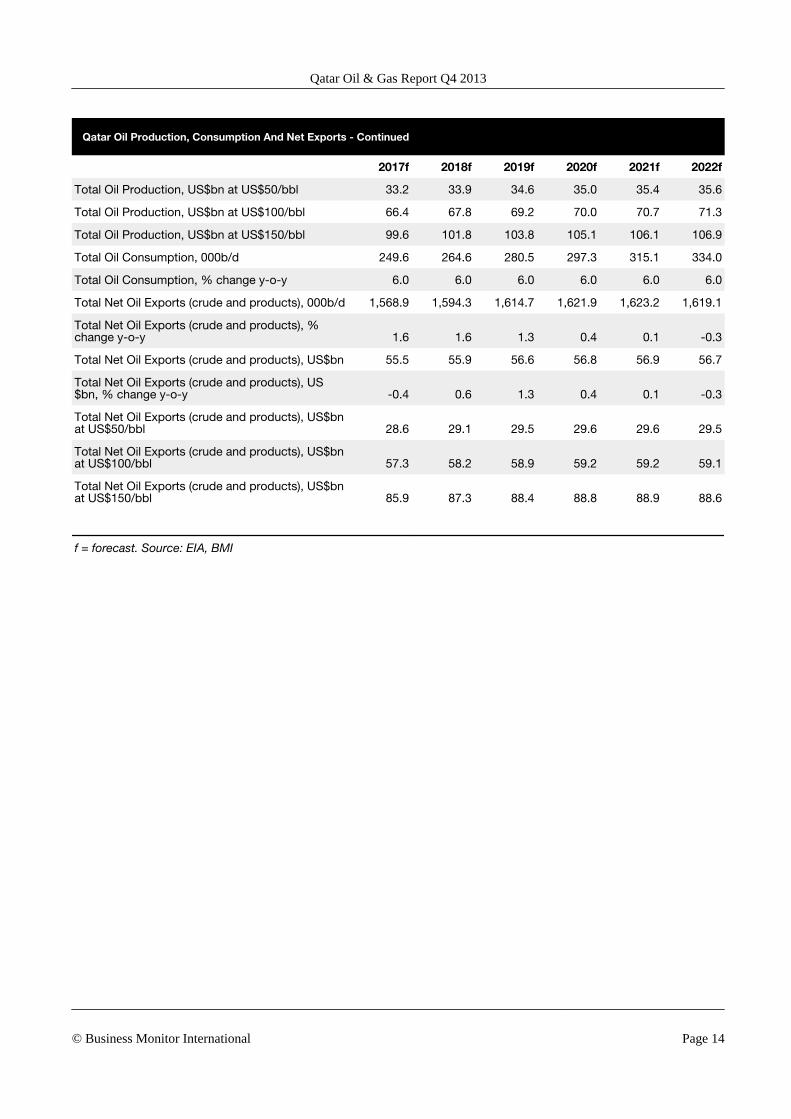

Qatar Oil Production, Consumption And Net Exports - Continued

2017f 2018f 2019f 2020f 2021f 2022f

Total Oil Production, US$bn at US$50/bbl 33.2 33.9 34.6 35.0 35.4 35.6

Total Oil Production, US$bn at US$100/bbl 66.4 67.8 69.2 70.0 70.7 71.3

Total Oil Production, US$bn at US$150/bbl 99.6 101.8 103.8 105.1 106.1 106.9

Total Oil Consumption, 000b/d 249.6 264.6 280.5 297.3 315.1 334.0

Total Oil Consumption, % change y-o-y 6.0 6.0 6.0 6.0 6.0 6.0

Total Net Oil Exports (crude and products), 000b/d 1,568.9 1,594.3 1,614.7 1,621.9 1,623.2 1,619.1

Total Net Oil Exports (crude and products), %change y-o-y 1.6 1.6 1.3 0.4 0.1 -0.3

Total Net Oil Exports (crude and products), US$bn 55.5 55.9 56.6 56.8 56.9 56.7

Total Net Oil Exports (crude and products), US$bn, % change y-o-y -0.4 0.6 1.3 0.4 0.1 -0.3

Total Net Oil Exports (crude and products), US$bnat US$50/bbl 28.6 29.1 29.5 29.6 29.6 29.5

Total Net Oil Exports (crude and products), US$bnat US$100/bbl 57.3 58.2 58.9 59.2 59.2 59.1

Total Net Oil Exports (crude and products), US$bnat US$150/bbl 85.9 87.3 88.4 88.8 88.9 88.6

f = forecast. Source: EIA, BMI

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 14

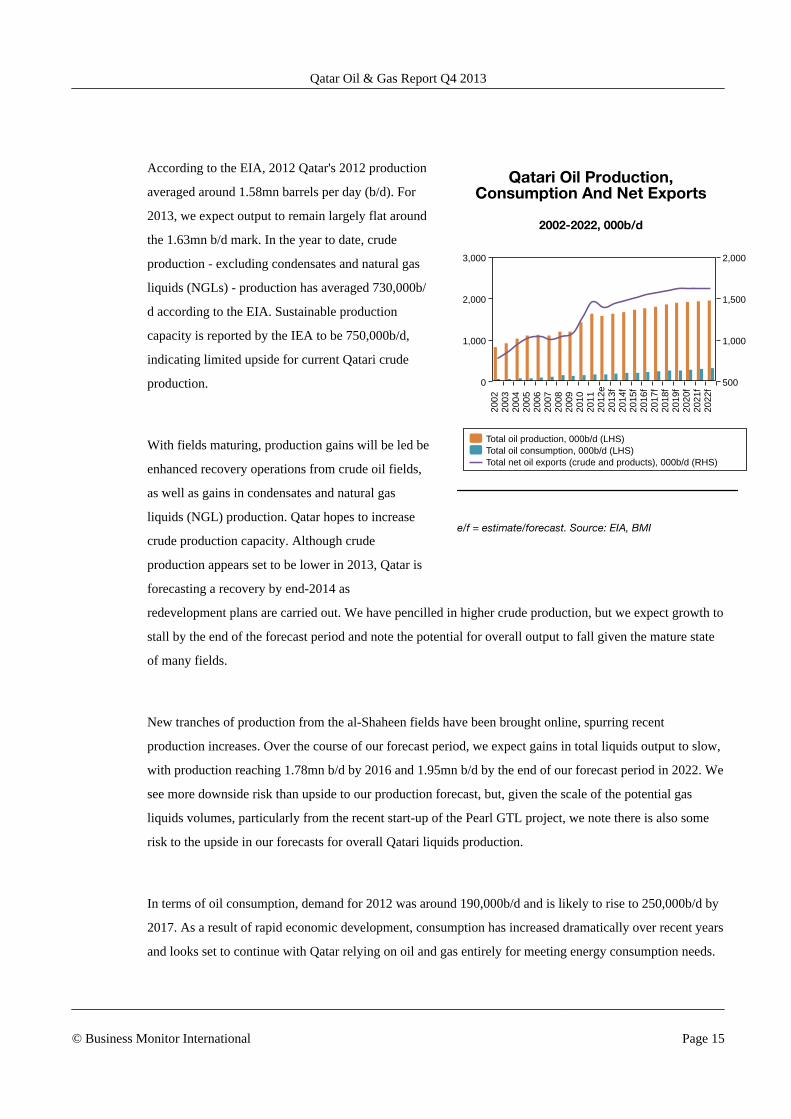

According to the EIA, 2012 Qatar's 2012 production

averaged around 1.58mn barrels per day (b/d). For

2013, we expect output to remain largely flat around

the 1.63mn b/d mark. In the year to date, crude

production - excluding condensates and natural gas

liquids (NGLs) - production has averaged 730,000b/

d according to the EIA. Sustainable production

capacity is reported by the IEA to be 750,000b/d,

indicating limited upside for current Qatari crude

production.

With fields maturing, production gains will be led be

enhanced recovery operations from crude oil fields,

as well as gains in condensates and natural gas

liquids (NGL) production. Qatar hopes to increase

crude production capacity. Although crude

production appears set to be lower in 2013, Qatar is

forecasting a recovery by end-2014 as

redevelopment plans are carried out. We have pencilled in higher crude production, but we expect growth to

stall by the end of the forecast period and note the potential for overall output to fall given the mature state

of many fields.

New tranches of production from the al-Shaheen fields have been brought online, spurring recent

production increases. Over the course of our forecast period, we expect gains in total liquids output to slow,

with production reaching 1.78mn b/d by 2016 and 1.95mn b/d by the end of our forecast period in 2022. We

see more downside risk than upside to our production forecast, but, given the scale of the potential gas

liquids volumes, particularly from the recent start-up of the Pearl GTL project, we note there is also some

risk to the upside in our forecasts for overall Qatari liquids production.

In terms of oil consumption, demand for 2012 was around 190,000b/d and is likely to rise to 250,000b/d by

2017. As a result of rapid economic development, consumption has increased dramatically over recent years

and looks set to continue with Qatar relying on oil and gas entirely for meeting energy consumption needs.

Qatari Oil Production,Consumption And Net Exports

2002-2022, 000b/d

Total oil production, 000b/d (LHS)Total oil consumption, 000b/d (LHS)Total net oil exports (crude and products), 000b/d (RHS)

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

e20

13f

2014

f20

15f

2016

f20

17f

2018

f20

19f

2020

f20

21f

2022

f

0

1,000

2,000

3,000

500

1,000

1,500

2,000

e/f = estimate/forecast. Source: EIA, BMI

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 15

Gas Supply And Demand

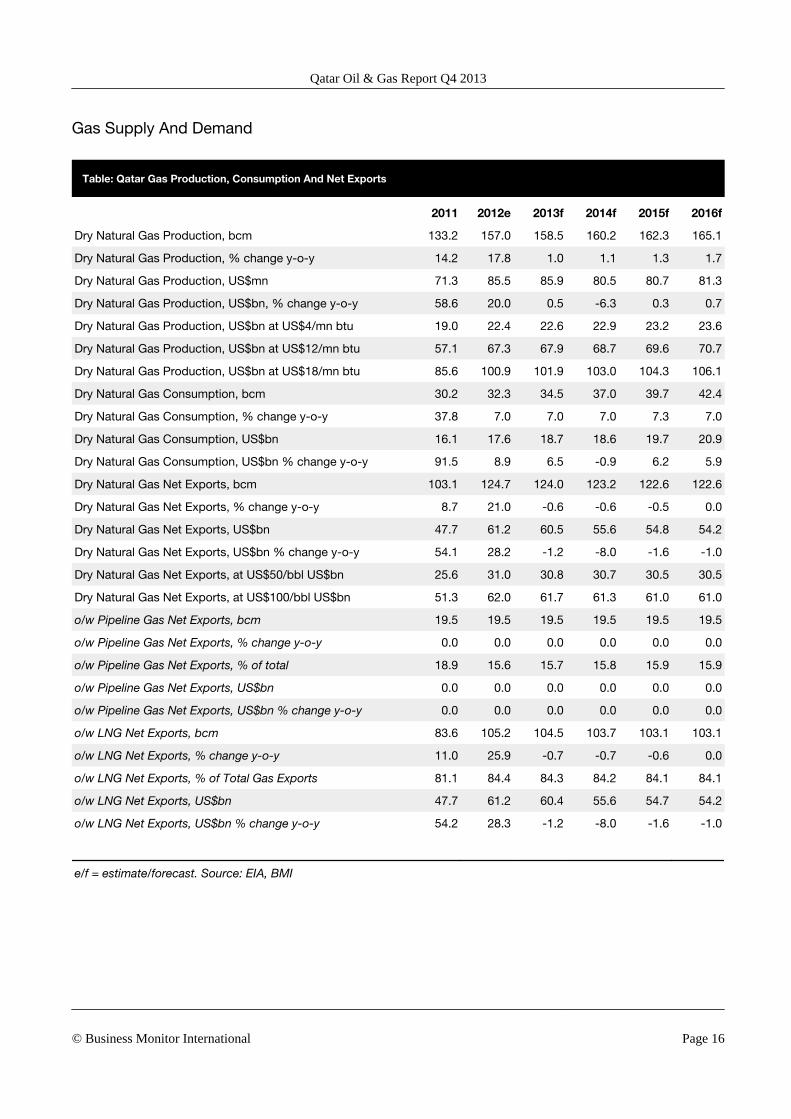

Table: Qatar Gas Production, Consumption And Net Exports

2011 2012e 2013f 2014f 2015f 2016f

Dry Natural Gas Production, bcm 133.2 157.0 158.5 160.2 162.3 165.1

Dry Natural Gas Production, % change y-o-y 14.2 17.8 1.0 1.1 1.3 1.7

Dry Natural Gas Production, US$mn 71.3 85.5 85.9 80.5 80.7 81.3

Dry Natural Gas Production, US$bn, % change y-o-y 58.6 20.0 0.5 -6.3 0.3 0.7

Dry Natural Gas Production, US$bn at US$4/mn btu 19.0 22.4 22.6 22.9 23.2 23.6

Dry Natural Gas Production, US$bn at US$12/mn btu 57.1 67.3 67.9 68.7 69.6 70.7

Dry Natural Gas Production, US$bn at US$18/mn btu 85.6 100.9 101.9 103.0 104.3 106.1

Dry Natural Gas Consumption, bcm 30.2 32.3 34.5 37.0 39.7 42.4

Dry Natural Gas Consumption, % change y-o-y 37.8 7.0 7.0 7.0 7.3 7.0

Dry Natural Gas Consumption, US$bn 16.1 17.6 18.7 18.6 19.7 20.9

Dry Natural Gas Consumption, US$bn % change y-o-y 91.5 8.9 6.5 -0.9 6.2 5.9

Dry Natural Gas Net Exports, bcm 103.1 124.7 124.0 123.2 122.6 122.6

Dry Natural Gas Net Exports, % change y-o-y 8.7 21.0 -0.6 -0.6 -0.5 0.0

Dry Natural Gas Net Exports, US$bn 47.7 61.2 60.5 55.6 54.8 54.2

Dry Natural Gas Net Exports, US$bn % change y-o-y 54.1 28.2 -1.2 -8.0 -1.6 -1.0

Dry Natural Gas Net Exports, at US$50/bbl US$bn 25.6 31.0 30.8 30.7 30.5 30.5

Dry Natural Gas Net Exports, at US$100/bbl US$bn 51.3 62.0 61.7 61.3 61.0 61.0

o/w Pipeline Gas Net Exports, bcm 19.5 19.5 19.5 19.5 19.5 19.5

o/w Pipeline Gas Net Exports, % change y-o-y 0.0 0.0 0.0 0.0 0.0 0.0

o/w Pipeline Gas Net Exports, % of total 18.9 15.6 15.7 15.8 15.9 15.9

o/w Pipeline Gas Net Exports, US$bn 0.0 0.0 0.0 0.0 0.0 0.0

o/w Pipeline Gas Net Exports, US$bn % change y-o-y 0.0 0.0 0.0 0.0 0.0 0.0

o/w LNG Net Exports, bcm 83.6 105.2 104.5 103.7 103.1 103.1

o/w LNG Net Exports, % change y-o-y 11.0 25.9 -0.7 -0.7 -0.6 0.0

o/w LNG Net Exports, % of Total Gas Exports 81.1 84.4 84.3 84.2 84.1 84.1

o/w LNG Net Exports, US$bn 47.7 61.2 60.4 55.6 54.7 54.2

o/w LNG Net Exports, US$bn % change y-o-y 54.2 28.3 -1.2 -8.0 -1.6 -1.0

e/f = estimate/forecast. Source: EIA, BMI

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 16

Table: Qatar Gas Production, Consumption And Net Exports

2017f 2018f 2019f 2020f 2021f 2022f

Dry Natural Gas Production, bcm 168.4 171.7 174.3 176.9 179.2 181.5

Dry Natural Gas Production, % change y-o-y 2.0 2.0 1.5 1.5 1.3 1.3

Dry Natural Gas Production, US$mn 81.2 82.0 83.2 84.5 85.6 86.7

Dry Natural Gas Production, US$bn, % change y-o-y -0.1 0.9 1.5 1.5 1.3 1.3

Dry Natural Gas Production, US$bn at US$4/mn btu 24.1 24.5 24.9 25.3 25.6 25.9

Dry Natural Gas Production, US$bn at US$12/mn btu 72.2 73.6 74.7 75.8 76.8 77.8

Dry Natural Gas Production, US$bn at US$18/mn btu 108.2 110.4 112.1 113.7 115.2 116.7

Dry Natural Gas Consumption, bcm 45.4 48.3 51.1 54.1 57.2 60.5

Dry Natural Gas Consumption, % change y-o-y 6.9 6.5 5.8 5.9 5.7 5.8

Dry Natural Gas Consumption, US$bn 21.9 23.1 24.4 25.8 27.3 28.9

Dry Natural Gas Consumption, US$bn % change y-o-y 4.7 5.4 5.8 5.9 5.7 5.8

Dry Natural Gas Net Exports, bcm 123.0 123.4 123.2 122.8 122.0 121.0

Dry Natural Gas Net Exports, % change y-o-y 0.3 0.3 -0.2 -0.3 -0.6 -0.8

Dry Natural Gas Net Exports, US$bn 53.3 53.0 52.9 52.7 52.3 51.8

Dry Natural Gas Net Exports, US$bn % change y-o-y -1.7 -0.6 -0.2 -0.4 -0.8 -1.0

Dry Natural Gas Net Exports, at US$50/bbl US$bn 30.6 30.7 30.6 30.5 30.3 30.1

Dry Natural Gas Net Exports, at US$100/bbl US$bn 61.2 61.4 61.3 61.1 60.7 60.2

o/w Pipeline Gas Net Exports, bcm 19.5 19.5 19.5 19.5 19.5 19.5

o/w Pipeline Gas Net Exports, % change y-o-y 0.0 0.0 0.0 0.0 0.0 0.0

o/w Pipeline Gas Net Exports, % of total 15.9 15.8 15.8 15.9 16.0 16.1

o/w Pipeline Gas Net Exports, US$bn 0.0 0.0 0.0 0.0 0.0 0.0

o/w Pipeline Gas Net Exports, US$bn % change y-o-y 0.0 0.0 0.0 0.0 0.0 0.0

o/w LNG Net Exports, bcm 103.5 103.9 103.7 103.3 102.5 101.5

o/w LNG Net Exports, % change y-o-y 0.4 0.4 -0.2 -0.4 -0.8 -1.0

o/w LNG Net Exports, % of Total Gas Exports 84.1 84.2 84.2 84.1 84.0 83.9

o/w LNG Net Exports, US$bn 53.3 52.9 52.8 52.6 52.2 51.7

o/w LNG Net Exports, US$bn % change y-o-y -1.7 -0.6 -0.2 -0.4 -0.8 -1.0

f = forecast. Source: EIA, BMI

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 17

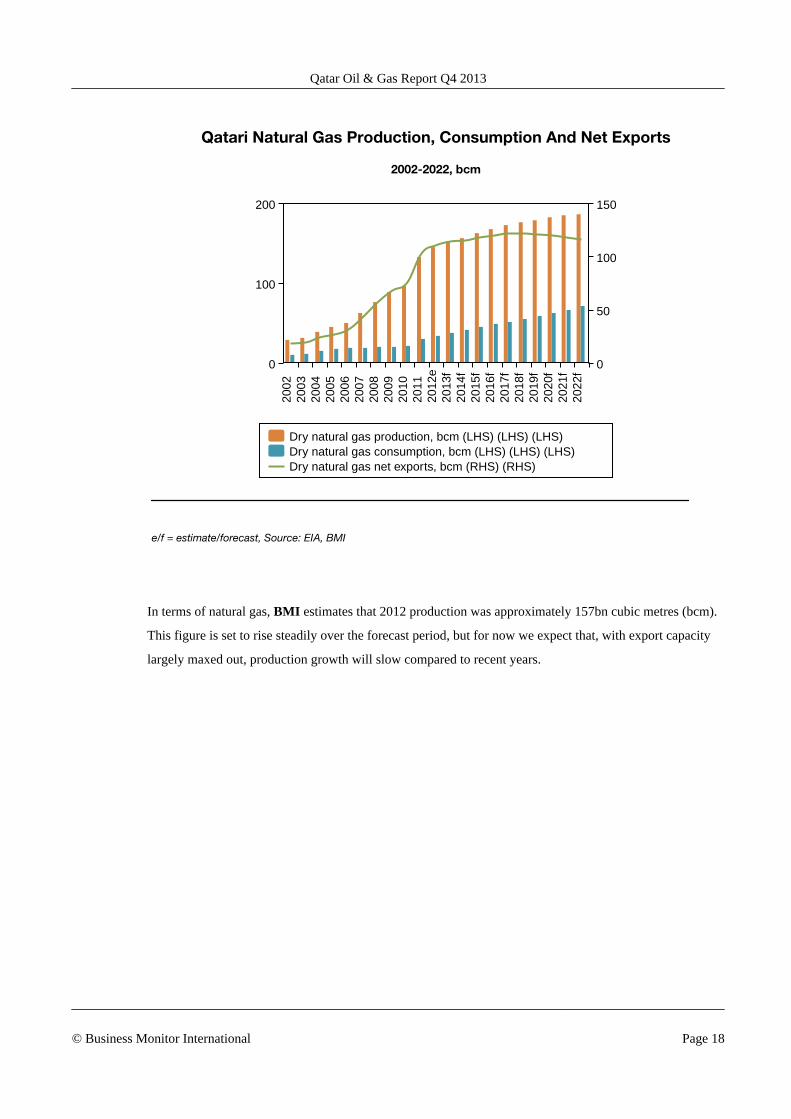

Qatari Natural Gas Production, Consumption And Net Exports

2002-2022, bcm

Dry natural gas production, bcm (LHS) (LHS) (LHS)Dry natural gas consumption, bcm (LHS) (LHS) (LHS)Dry natural gas net exports, bcm (RHS) (RHS)

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

e20

13f

2014

f20

15f

2016

f20

17f

2018

f20

19f

2020

f20

21f

2022

f

0

100

200

0

50

100

150

e/f = estimate/forecast, Source: EIA, BMI

In terms of natural gas, BMI estimates that 2012 production was approximately 157bn cubic metres (bcm).

This figure is set to rise steadily over the forecast period, but for now we expect that, with export capacity

largely maxed out, production growth will slow compared to recent years.

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 18

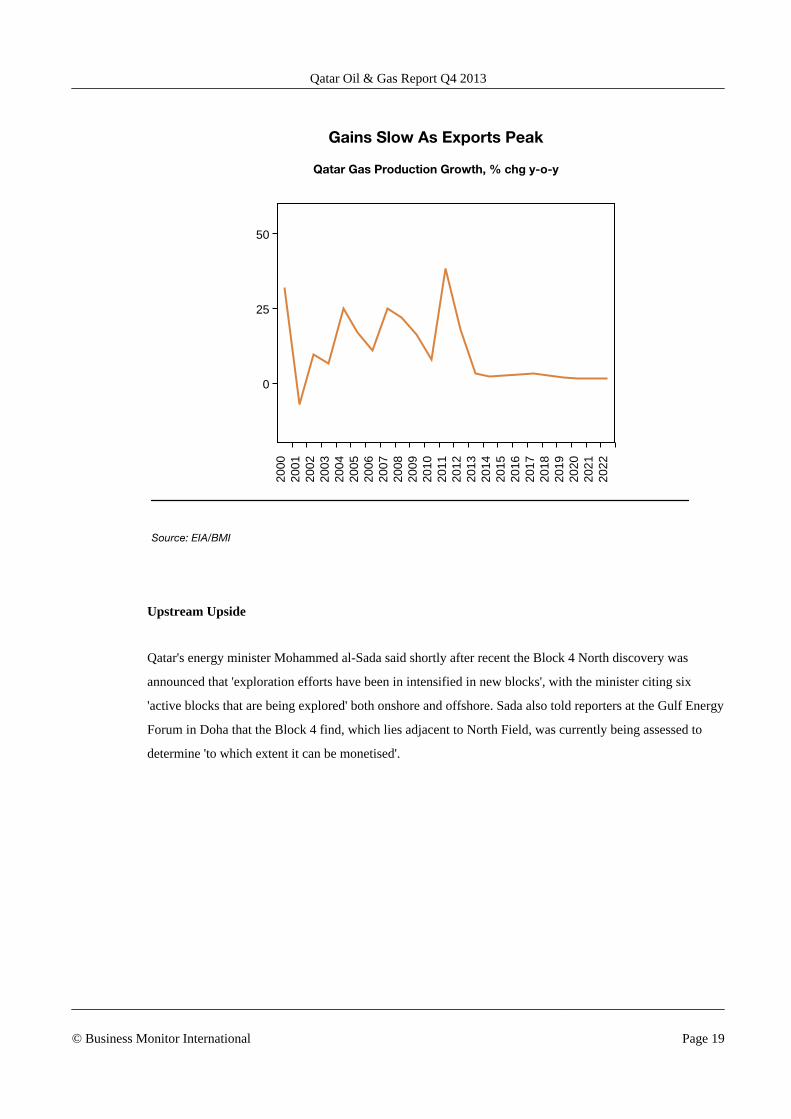

Gains Slow As Exports Peak

Qatar Gas Production Growth, % chg y-o-y

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

0

25

50

Source: EIA/BMI

Upstream Upside

Qatar's energy minister Mohammed al-Sada said shortly after recent the Block 4 North discovery was

announced that 'exploration efforts have been in intensified in new blocks', with the minister citing six

'active blocks that are being explored' both onshore and offshore. Sada also told reporters at the Gulf Energy

Forum in Doha that the Block 4 find, which lies adjacent to North Field, was currently being assessed to

determine 'to which extent it can be monetised'.

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 19

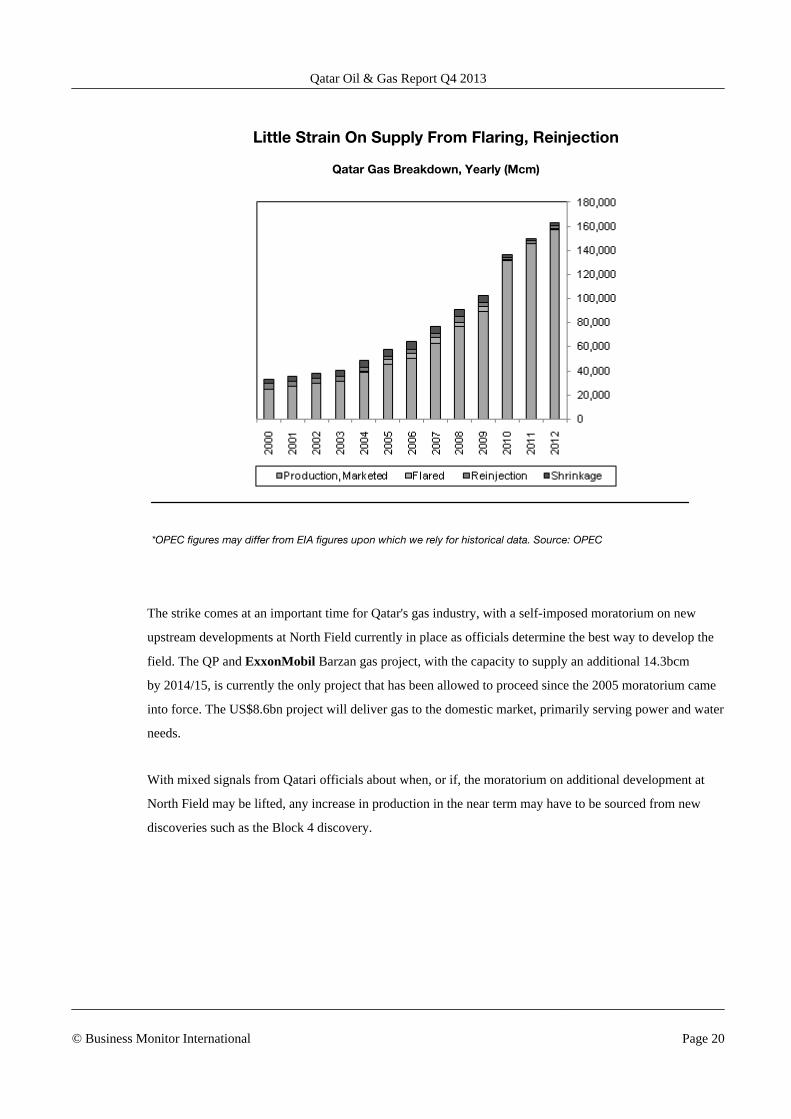

Little Strain On Supply From Flaring, Reinjection

Qatar Gas Breakdown, Yearly (Mcm)

*OPEC figures may differ from EIA figures upon which we rely for historical data. Source: OPEC

The strike comes at an important time for Qatar's gas industry, with a self-imposed moratorium on new

upstream developments at North Field currently in place as officials determine the best way to develop the

field. The QP and ExxonMobil Barzan gas project, with the capacity to supply an additional 14.3bcm

by 2014/15, is currently the only project that has been allowed to proceed since the 2005 moratorium came

into force. The US$8.6bn project will deliver gas to the domestic market, primarily serving power and water

needs.

With mixed signals from Qatari officials about when, or if, the moratorium on additional development at

North Field may be lifted, any increase in production in the near term may have to be sourced from new

discoveries such as the Block 4 discovery.

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 20

Gas Powered

Qatar Total Net Generation By Type (Twh)

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

0

25

50

75

100

125

Source: EIA/BMI/World Bank

On the other side of the ledger, gas consumption is also rising rapidly - indeed, at a much more rapid pace

than production - with power generation expansion and the start up of Pearl GTL as primary drivers. Our

consumption forecast estimates that consumption rose nearly 10% between 2011 and 2012 to reach

approximately 32bcm. This is on top of a 38% increase in natural gas consumption which occurred between

2010 and 2011. Consumption growth will continue steadily over our forecast period, reaching almost

45bcm by 2017 and 60bcm by 2022, with upside risk to these figures as new industrial projects are

announced and with limited prospects that measures could be introduced to reduce demand such as the

reform of subsides.

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 21

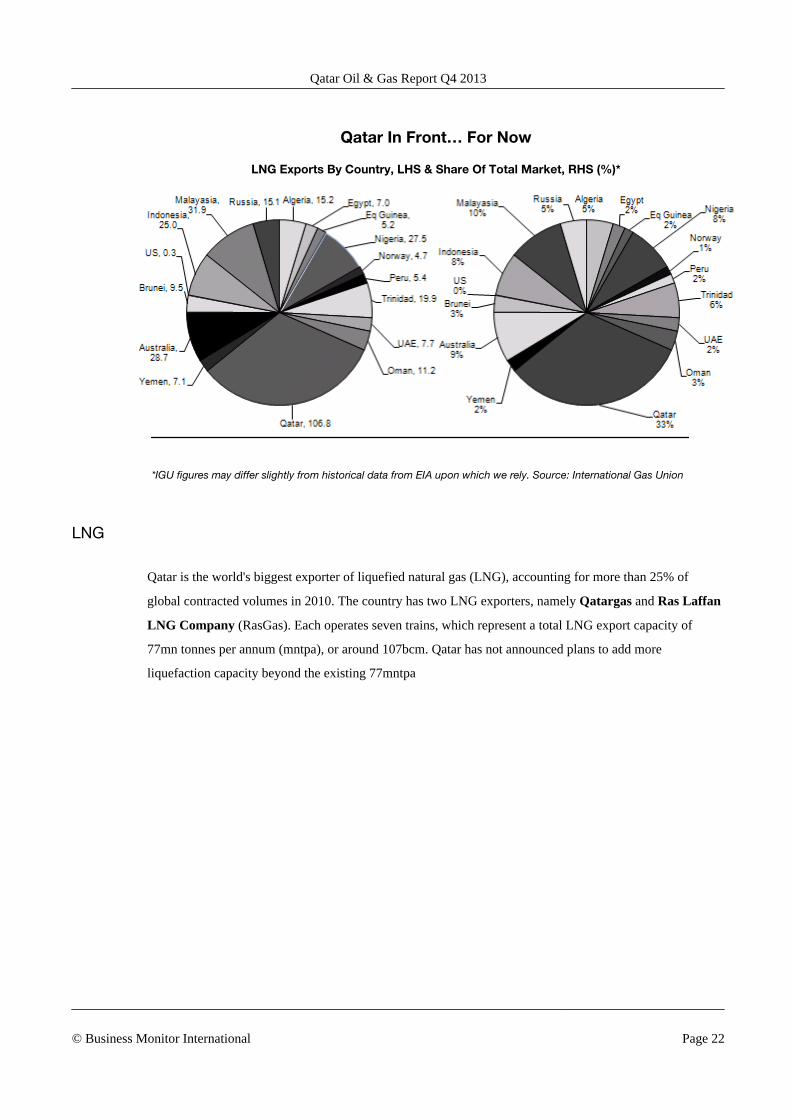

Qatar In Front… For Now

LNG Exports By Country, LHS & Share Of Total Market, RHS (%)*

*IGU figures may differ slightly from historical data from EIA upon which we rely. Source: International Gas Union

LNG

Qatar is the world's biggest exporter of liquefied natural gas (LNG), accounting for more than 25% of

global contracted volumes in 2010. The country has two LNG exporters, namely Qatargas and Ras Laffan

LNG Company (RasGas). Each operates seven trains, which represent a total LNG export capacity of

77mn tonnes per annum (mntpa), or around 107bcm. Qatar has not announced plans to add more

liquefaction capacity beyond the existing 77mntpa

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 22

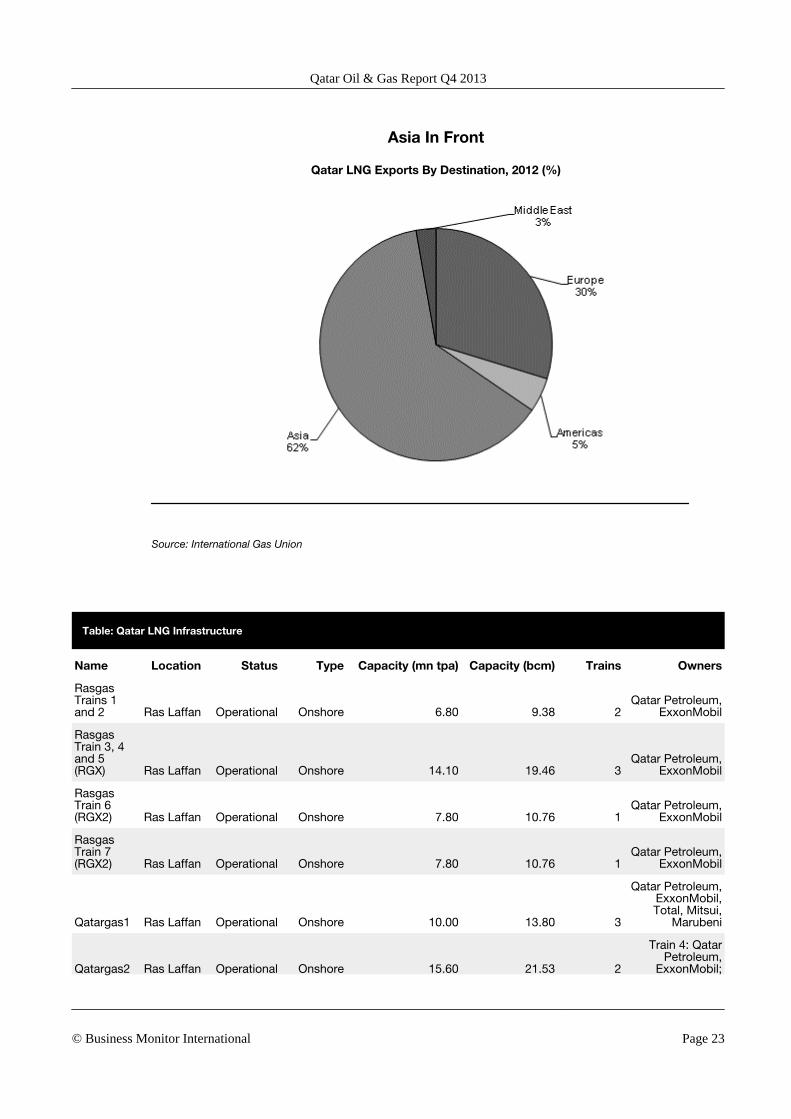

Asia In Front

Qatar LNG Exports By Destination, 2012 (%)

Source: International Gas Union

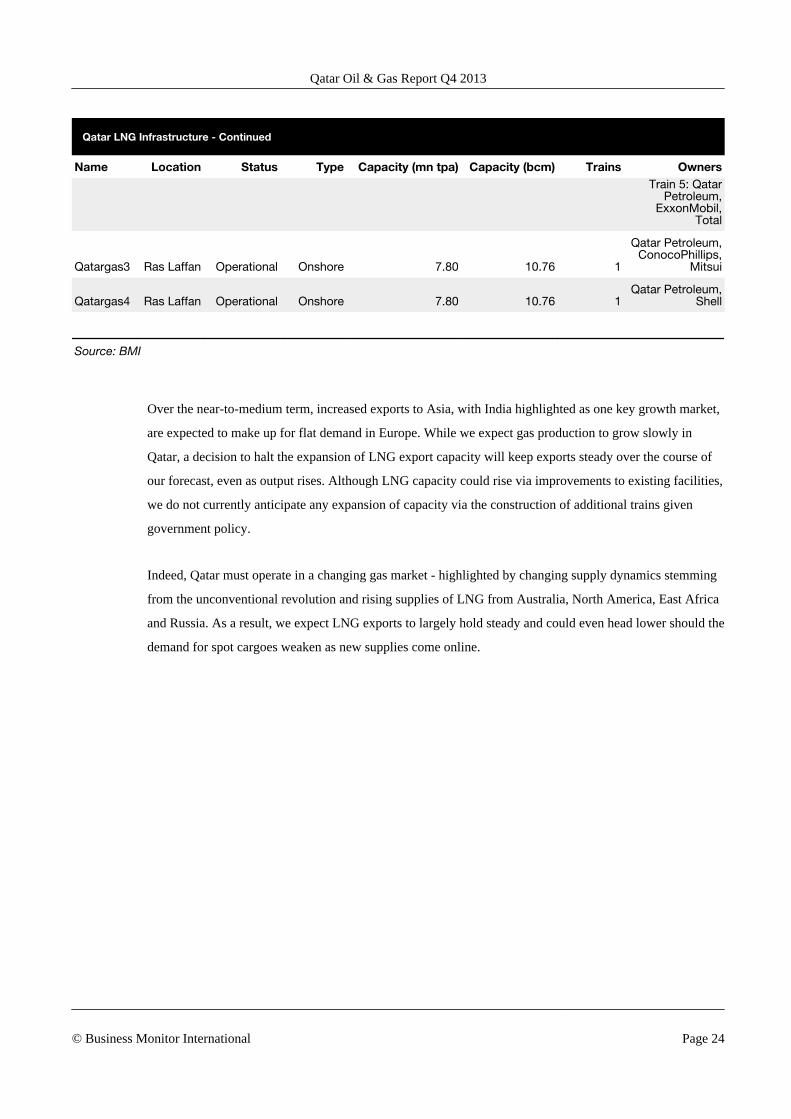

Table: Qatar LNG Infrastructure

Name Location Status Type Capacity (mn tpa) Capacity (bcm) Trains Owners

RasgasTrains 1and 2 Ras Laffan Operational Onshore 6.80 9.38 2

Qatar Petroleum,ExxonMobil

RasgasTrain 3, 4and 5(RGX) Ras Laffan Operational Onshore 14.10 19.46 3

Qatar Petroleum,ExxonMobil

RasgasTrain 6(RGX2) Ras Laffan Operational Onshore 7.80 10.76 1

Qatar Petroleum,ExxonMobil

RasgasTrain 7(RGX2) Ras Laffan Operational Onshore 7.80 10.76 1

Qatar Petroleum,ExxonMobil

Qatargas1 Ras Laffan Operational Onshore 10.00 13.80 3

Qatar Petroleum,ExxonMobil,Total, Mitsui,

Marubeni

Qatargas2 Ras Laffan Operational Onshore 15.60 21.53 2

Train 4: QatarPetroleum,

ExxonMobil;

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 23

Qatar LNG Infrastructure - Continued

Name Location Status Type Capacity (mn tpa) Capacity (bcm) Trains OwnersTrain 5: Qatar

Petroleum,ExxonMobil,

Total

Qatargas3 Ras Laffan Operational Onshore 7.80 10.76 1

Qatar Petroleum,ConocoPhillips,

Mitsui

Qatargas4 Ras Laffan Operational Onshore 7.80 10.76 1Qatar Petroleum,

Shell

Source: BMI

Over the near-to-medium term, increased exports to Asia, with India highlighted as one key growth market,

are expected to make up for flat demand in Europe. While we expect gas production to grow slowly in

Qatar, a decision to halt the expansion of LNG export capacity will keep exports steady over the course of

our forecast, even as output rises. Although LNG capacity could rise via improvements to existing facilities,

we do not currently anticipate any expansion of capacity via the construction of additional trains given

government policy.

Indeed, Qatar must operate in a changing gas market - highlighted by changing supply dynamics stemming

from the unconventional revolution and rising supplies of LNG from Australia, North America, East Africa

and Russia. As a result, we expect LNG exports to largely hold steady and could even head lower should the

demand for spot cargoes weaken as new supplies come online.

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 24

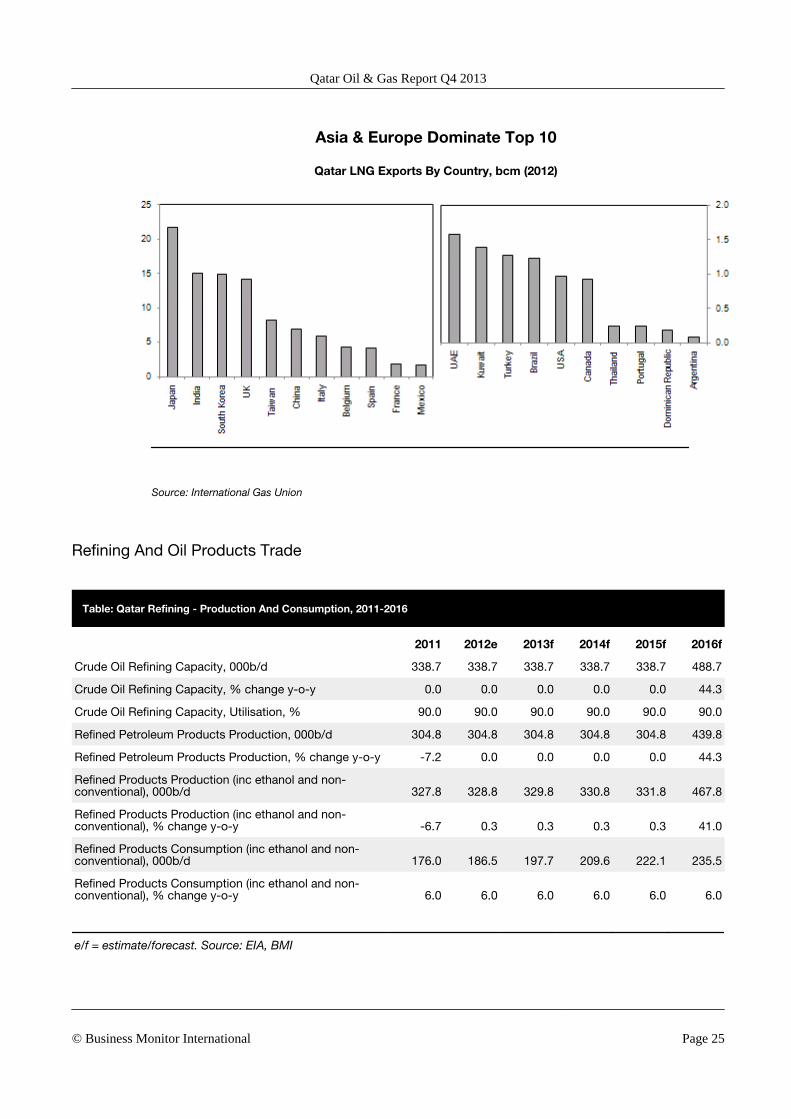

Asia & Europe Dominate Top 10

Qatar LNG Exports By Country, bcm (2012)

Source: International Gas Union

Refining And Oil Products Trade

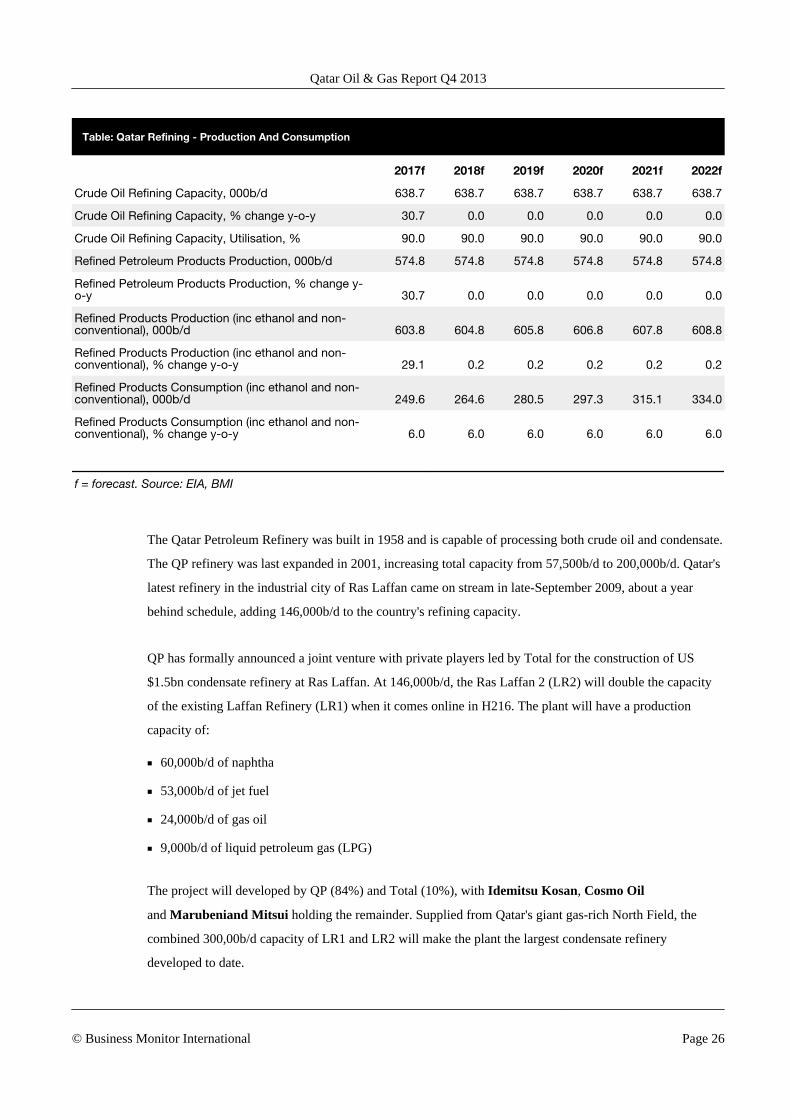

Table: Qatar Refining - Production And Consumption, 2011-2016

2011 2012e 2013f 2014f 2015f 2016f

Crude Oil Refining Capacity, 000b/d 338.7 338.7 338.7 338.7 338.7 488.7

Crude Oil Refining Capacity, % change y-o-y 0.0 0.0 0.0 0.0 0.0 44.3

Crude Oil Refining Capacity, Utilisation, % 90.0 90.0 90.0 90.0 90.0 90.0

Refined Petroleum Products Production, 000b/d 304.8 304.8 304.8 304.8 304.8 439.8

Refined Petroleum Products Production, % change y-o-y -7.2 0.0 0.0 0.0 0.0 44.3

Refined Products Production (inc ethanol and non-conventional), 000b/d 327.8 328.8 329.8 330.8 331.8 467.8

Refined Products Production (inc ethanol and non-conventional), % change y-o-y -6.7 0.3 0.3 0.3 0.3 41.0

Refined Products Consumption (inc ethanol and non-conventional), 000b/d 176.0 186.5 197.7 209.6 222.1 235.5

Refined Products Consumption (inc ethanol and non-conventional), % change y-o-y 6.0 6.0 6.0 6.0 6.0 6.0

e/f = estimate/forecast. Source: EIA, BMI

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 25

Table: Qatar Refining - Production And Consumption

2017f 2018f 2019f 2020f 2021f 2022f

Crude Oil Refining Capacity, 000b/d 638.7 638.7 638.7 638.7 638.7 638.7

Crude Oil Refining Capacity, % change y-o-y 30.7 0.0 0.0 0.0 0.0 0.0

Crude Oil Refining Capacity, Utilisation, % 90.0 90.0 90.0 90.0 90.0 90.0

Refined Petroleum Products Production, 000b/d 574.8 574.8 574.8 574.8 574.8 574.8

Refined Petroleum Products Production, % change y-o-y 30.7 0.0 0.0 0.0 0.0 0.0

Refined Products Production (inc ethanol and non-conventional), 000b/d 603.8 604.8 605.8 606.8 607.8 608.8

Refined Products Production (inc ethanol and non-conventional), % change y-o-y 29.1 0.2 0.2 0.2 0.2 0.2

Refined Products Consumption (inc ethanol and non-conventional), 000b/d 249.6 264.6 280.5 297.3 315.1 334.0

Refined Products Consumption (inc ethanol and non-conventional), % change y-o-y 6.0 6.0 6.0 6.0 6.0 6.0

f = forecast. Source: EIA, BMI

The Qatar Petroleum Refinery was built in 1958 and is capable of processing both crude oil and condensate.

The QP refinery was last expanded in 2001, increasing total capacity from 57,500b/d to 200,000b/d. Qatar's

latest refinery in the industrial city of Ras Laffan came on stream in late-September 2009, about a year

behind schedule, adding 146,000b/d to the country's refining capacity.

QP has formally announced a joint venture with private players led by Total for the construction of US

$1.5bn condensate refinery at Ras Laffan. At 146,000b/d, the Ras Laffan 2 (LR2) will double the capacity

of the existing Laffan Refinery (LR1) when it comes online in H216. The plant will have a production

capacity of:

■ 60,000b/d of naphtha

■ 53,000b/d of jet fuel

■ 24,000b/d of gas oil

■ 9,000b/d of liquid petroleum gas (LPG)

The project will developed by QP (84%) and Total (10%), with Idemitsu Kosan, Cosmo Oil

and Marubeniand Mitsui holding the remainder. Supplied from Qatar's giant gas-rich North Field, the

combined 300,00b/d capacity of LR1 and LR2 will make the plant the largest condensate refinery

developed to date.

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 26

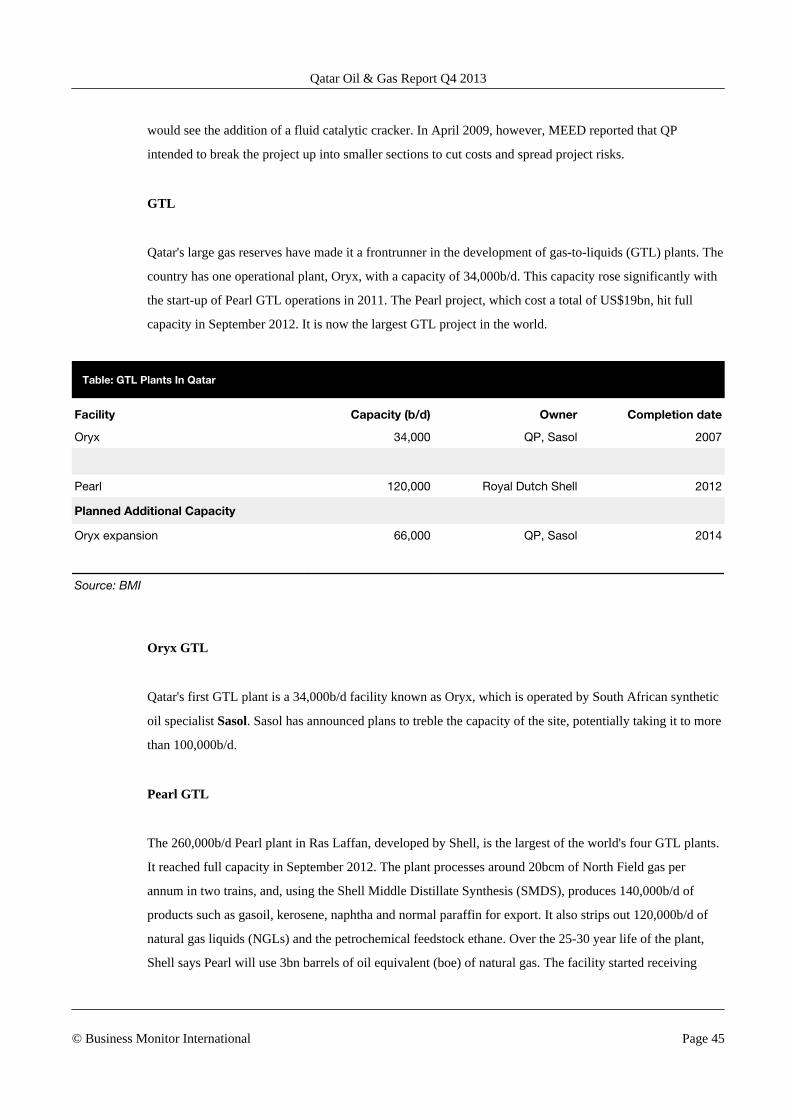

Gas-To-Liquids

Apart from the two conventional refineries, Qatar also has a 34,000b/d GTL plant known as Oryx, which is

operated by South African synthetic oil specialist Sasol. Sasol plans to treble the capacity of the site,

potentially taking it to more than 100,000b/d. The plan is feed by gas from the Al Khaleej field.

In addition, the larger Shell-operated Pearl GTL plant has the capacity to produce 140,000b/d of ultra-clean

diesel, naphtha etc, with the first train having started up in 2011 and reached full capacity in the end of

2012. The Pearl facility also produces some 120,000b/d worth of associated condensate and LPG volumes.

The plant is currently the world's largest GTL facility and is notable as the first GTL facility to integrate

upstream natural gas production with the downstream conversion facility.

The planned US$11bn al-Shaheen refinery was reported in February 2010 to be indefinitely delayed, with

re-scaling and re-tendering expected. The 250,000b/d facility was to be fed with heavy, sour crude from the

eponymous offshore oil field. GTL capacity is currently not included in our downstream forecast.

Revenues/Import Costs

Crude oil and liquids export revenues are set to fall slightly from an estimated US$56bn in 2012 to US

$55.5bn by 2017. The BMI oil price assumptions are US$109/bbl in 2013 (OPEC basket) and US$101/bbl

in 2014. By 2016, gas export revenues should have reached US$54bn. However, there is an expected

decline at the end of our forecast period, with gas export revenues dropping to US$52bn by 2022.

Key Risks To BMI's Forecast Scenario

Qatar is sensitive to oil price fluctuations, which would hit its crude export revenues. Although we do not

see it as a likely event, the possible emergence of an 'LNG glut' could hit Qatar's LNG export revenues hard,

while any increase in volume or price for pipeline exports to the UAE and Oman will boost gas revenues.

Certainly the potential increase in competition from emerging natural gas players, including those in East

Africa, could pose a long-term threat, although much of that new production is set to hit the market beyond

our forecast period.

Finally, there is increasing pressure from major LNG importing countries, namely Japan and South Korea,

which are pushing to de-link LNG contract pricing from oil prices. Qatar is strongly resisting this push;

however, as new export markets become available, the arbitrage opportunity may become too great, forcing

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 27

some contract terms and pricing mechanisms to change over the medium-to-long term. This could

potentially have a significant impact on Qatar, and particularly on Qatari fiscal accounts.

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 28

Industry Risk Reward Ratings

Middle East - Risk/Reward Ratings

BMI View: Smaller markets with strong openness to foreign investment continue to outperform those with

larger resource endowments in our overall rankings, with Israel, the UAE and Qatar outperforming

countries like Saudi Arabia. Iraq remains the country most likely to move up or down in our rankings with

both strong upside and downside risks, as the country's potential is undermined by a multitude of above-

ground woes. We also highlight Kuwait as a market at risk of continued underperformance as business

environment threats challenge both upstream and downstream performance.

The main conclusions from our Middle East Risk/Reward Ratings are:

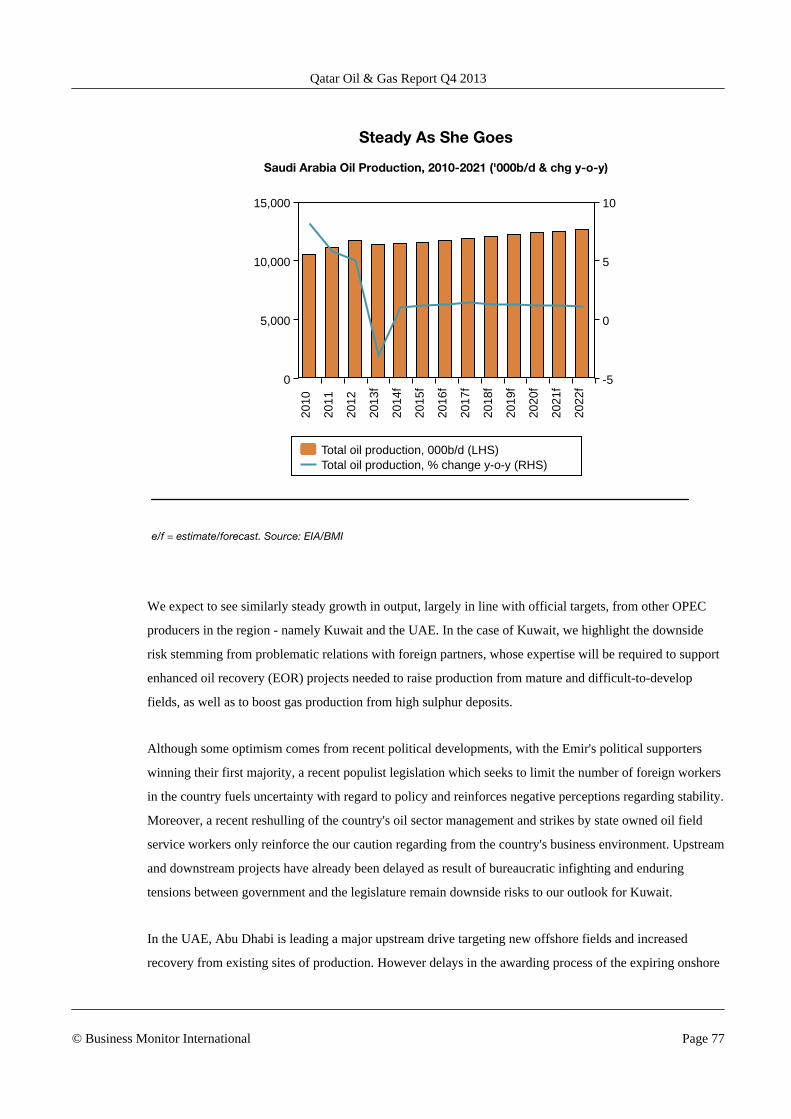

■ Scores and rankings have remained largely unchanged in our Risk/Reward Ratings (RRRs), reflecting themature status of the majority of producers in the region. In terms of production, we currently expectsteady gains in most markets over the course of our forecast period, notwithstanding the downside risksto this view. Risks stem from the ongoing disruption to traditional trade flows as growth in non-OPECproduction displaces Middle East imports in the US, and as OPEC states increasingly compete for marketshare in demand-hungry Asia.

■ The UAE has retained its top spot in our overall oil & gas RRRs. The country's relative openness toforeign investment in both the upstream and downstream segments, as well as a major investment plantargeting a sizable expansion of production capacity are among the reasons for its outperformancerelative to its peers in the region on key metrics. Nonetheless, we highlight risks to watch on the horizonfor the UAE.

■ Firstly, reports are emerging that the UAE may miss its stated target of 3.5mn barrels per day (b/d) by2017. According to officials and industry sources, the country may not reach this production level until2020. While we had priced-in delays to our output forecast, which sees production reaching 3.6mn b/donly by 2020, further setbacks may cause us to revisit this and pencil-in slower growth that could result ina fall in the UAE's upstream scores.

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 29

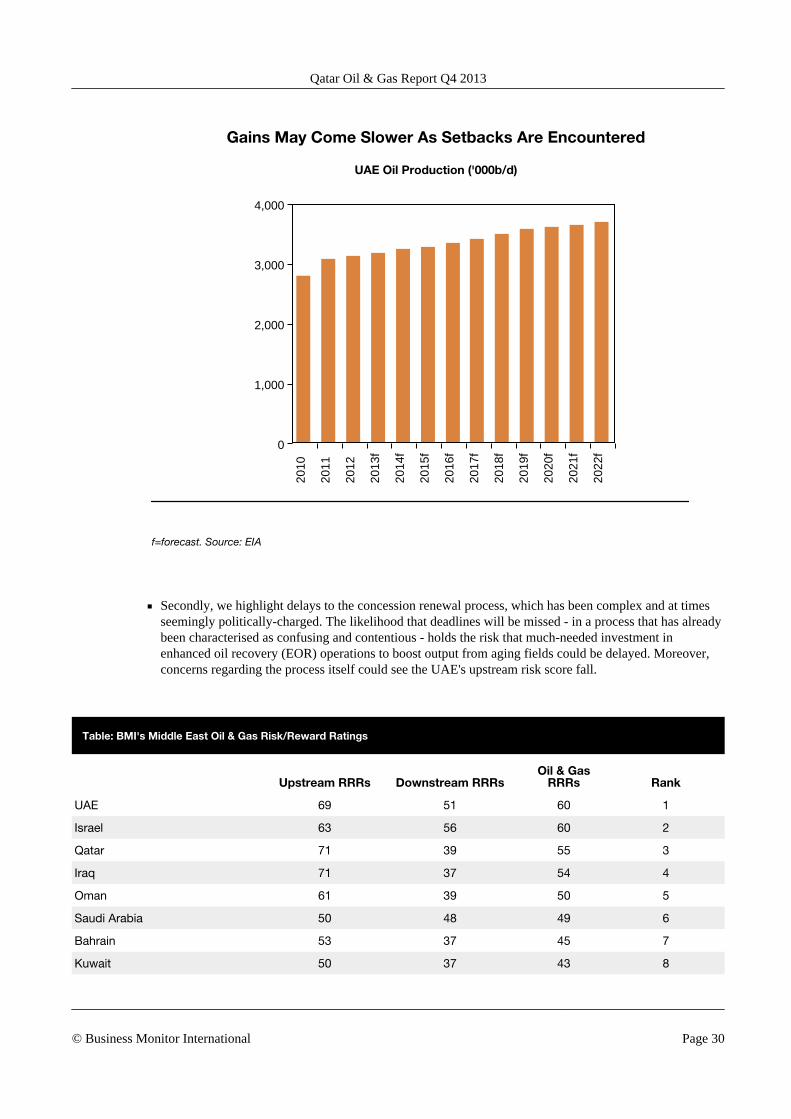

Gains May Come Slower As Setbacks Are Encountered

UAE Oil Production ('000b/d)

2010

2011

2012

2013

f

2014

f

2015

f

2016

f

2017

f

2018

f

2019

f

2020

f

2021

f

2022

f

0

1,000

2,000

3,000

4,000

f=forecast. Source: EIA

■ Secondly, we highlight delays to the concession renewal process, which has been complex and at timesseemingly politically-charged. The likelihood that deadlines will be missed - in a process that has alreadybeen characterised as confusing and contentious - holds the risk that much-needed investment inenhanced oil recovery (EOR) operations to boost output from aging fields could be delayed. Moreover,concerns regarding the process itself could see the UAE's upstream risk score fall.

Table: BMI's Middle East Oil & Gas Risk/Reward Ratings

Upstream RRRs Downstream RRRsOil & Gas

RRRs Rank

UAE 69 51 60 1

Israel 63 56 60 2

Qatar 71 39 55 3

Iraq 71 37 54 4

Oman 61 39 50 5

Saudi Arabia 50 48 49 6

Bahrain 53 37 45 7

Kuwait 50 37 43 8

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 30

BMI's Middle East Oil & Gas Risk/Reward Ratings - Continued

Upstream RRRs Downstream RRRsOil & Gas

RRRs Rank

Regional Average 61 43 52 8

NB Scores out of 100; *Higher score = lower risks. Source: BMI

■ Kuwait and Iran have swapped spots at the bottom of our overall rankings, leaving the latter in last place.This reflects the continued deterioration our outlook for Iran, as sanctions further erode the near- andlong-term competitiveness of its oil & gas sector.

■ In the case of Kuwait, the country's long-troubled business environment remains the key obstacle to itsindustry performance. Long-running disputes between the government and opposition parties in thecountry's vocal parliament have stalled key upstream and downstream projects, while regular industrialaction has further dampened its production outlook.

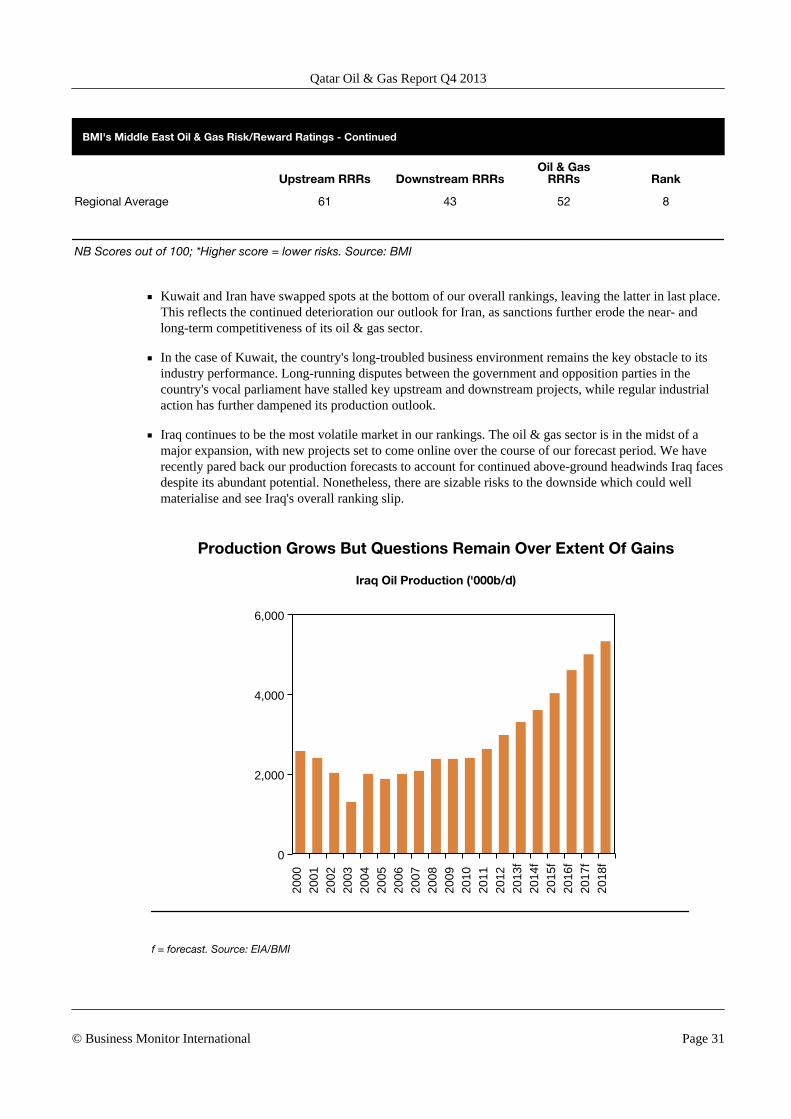

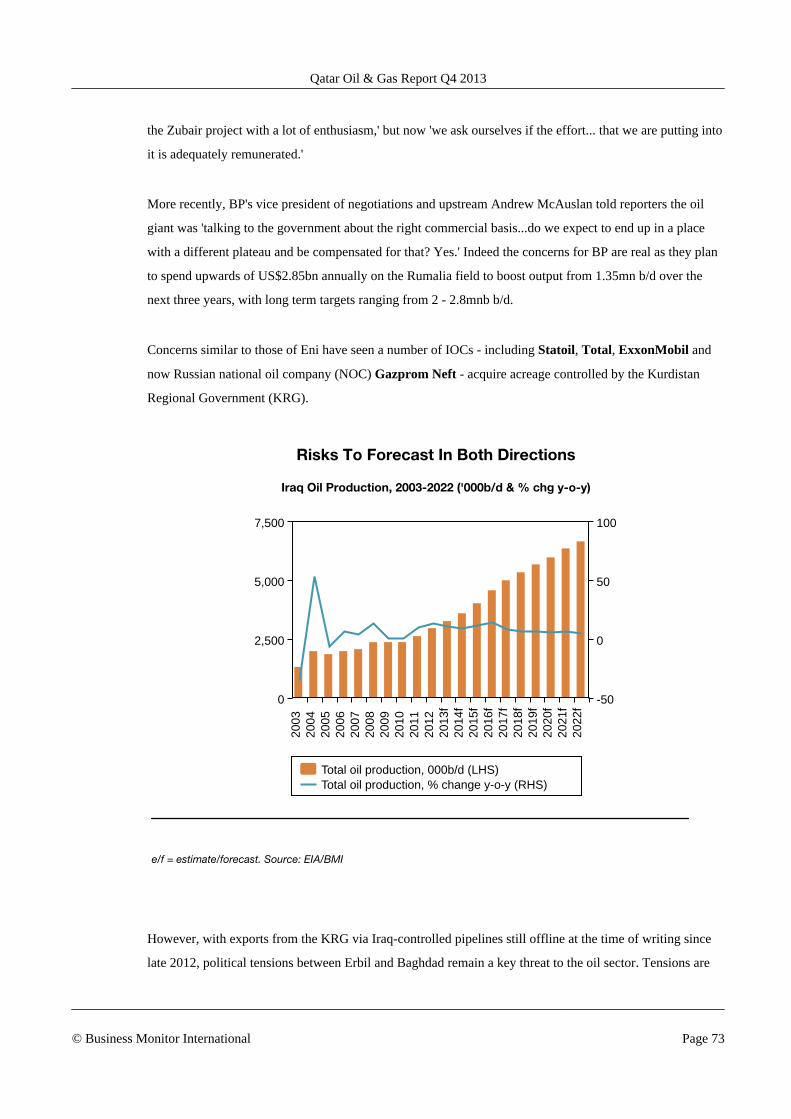

■ Iraq continues to be the most volatile market in our rankings. The oil & gas sector is in the midst of amajor expansion, with new projects set to come online over the course of our forecast period. We haverecently pared back our production forecasts to account for continued above-ground headwinds Iraq facesdespite its abundant potential. Nonetheless, there are sizable risks to the downside which could wellmaterialise and see Iraq's overall ranking slip.

Production Grows But Questions Remain Over Extent Of Gains

Iraq Oil Production ('000b/d)

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

f20

14f

2015

f20

16f

2017

f20

18f

0

2,000

4,000

6,000

f = forecast. Source: EIA/BMI

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 31

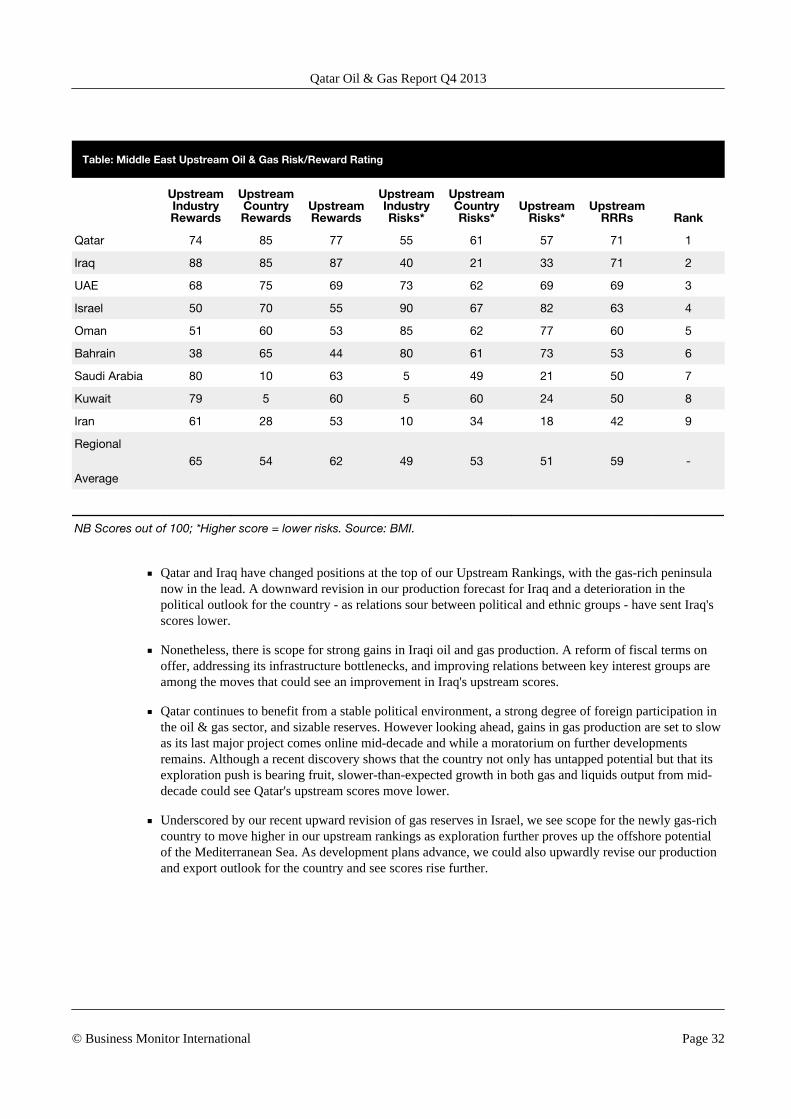

Table: Middle East Upstream Oil & Gas Risk/Reward Rating

UpstreamIndustryRewards

UpstreamCountryRewards

UpstreamRewards

UpstreamIndustryRisks*

UpstreamCountryRisks*

UpstreamRisks*

UpstreamRRRs Rank

Qatar 74 85 77 55 61 57 71 1

Iraq 88 85 87 40 21 33 71 2

UAE 68 75 69 73 62 69 69 3

Israel 50 70 55 90 67 82 63 4

Oman 51 60 53 85 62 77 60 5

Bahrain 38 65 44 80 61 73 53 6

Saudi Arabia 80 10 63 5 49 21 50 7

Kuwait 79 5 60 5 60 24 50 8

Iran 61 28 53 10 34 18 42 9

Regional

Average65 54 62 49 53 51 59 -

NB Scores out of 100; *Higher score = lower risks. Source: BMI.

■ Qatar and Iraq have changed positions at the top of our Upstream Rankings, with the gas-rich peninsulanow in the lead. A downward revision in our production forecast for Iraq and a deterioration in thepolitical outlook for the country - as relations sour between political and ethnic groups - have sent Iraq'sscores lower.

■ Nonetheless, there is scope for strong gains in Iraqi oil and gas production. A reform of fiscal terms onoffer, addressing its infrastructure bottlenecks, and improving relations between key interest groups areamong the moves that could see an improvement in Iraq's upstream scores.

■ Qatar continues to benefit from a stable political environment, a strong degree of foreign participation inthe oil & gas sector, and sizable reserves. However looking ahead, gains in gas production are set to slowas its last major project comes online mid-decade and while a moratorium on further developmentsremains. Although a recent discovery shows that the country not only has untapped potential but that itsexploration push is bearing fruit, slower-than-expected growth in both gas and liquids output from mid-decade could see Qatar's upstream scores move lower.

■ Underscored by our recent upward revision of gas reserves in Israel, we see scope for the newly gas-richcountry to move higher in our upstream rankings as exploration further proves up the offshore potentialof the Mediterranean Sea. As development plans advance, we could also upwardly revise our productionand export outlook for the country and see scores rise further.

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 32

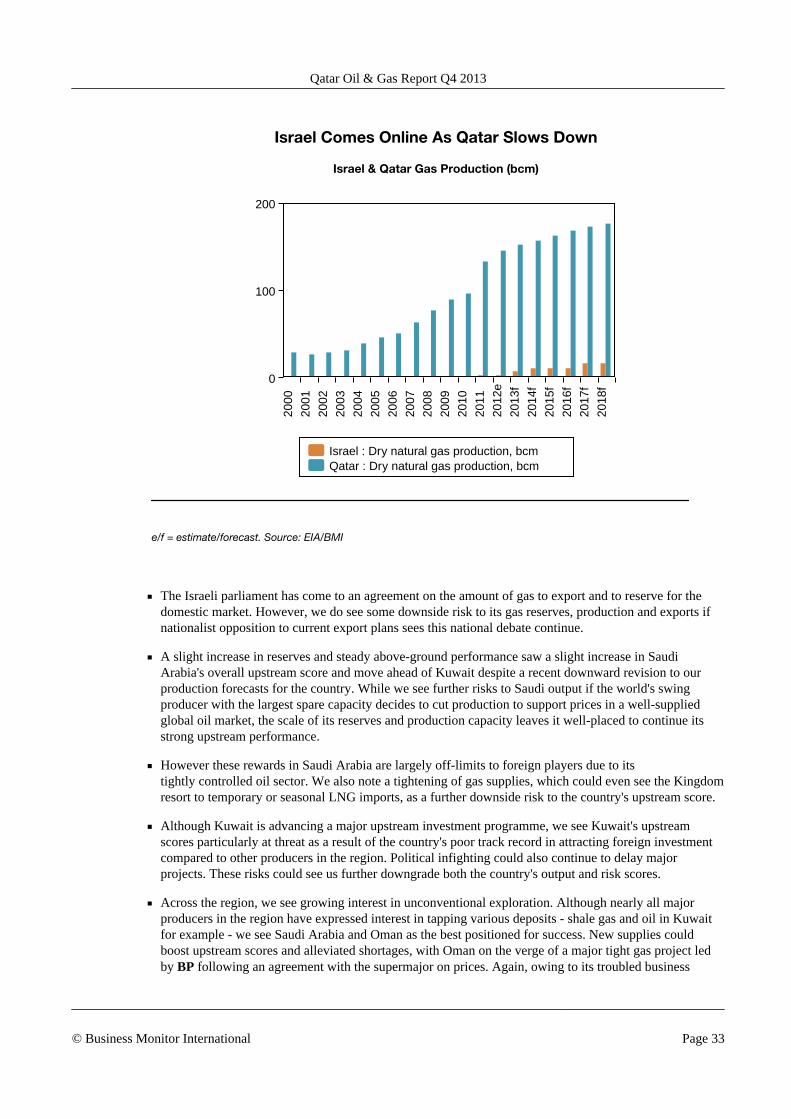

Israel Comes Online As Qatar Slows Down

Israel & Qatar Gas Production (bcm)

Israel : Dry natural gas production, bcmQatar : Dry natural gas production, bcm

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

e

2013

f

2014

f

2015

f

2016

f

2017

f

2018

f

0

100

200

e/f = estimate/forecast. Source: EIA/BMI

■ The Israeli parliament has come to an agreement on the amount of gas to export and to reserve for thedomestic market. However, we do see some downside risk to its gas reserves, production and exports ifnationalist opposition to current export plans sees this national debate continue.

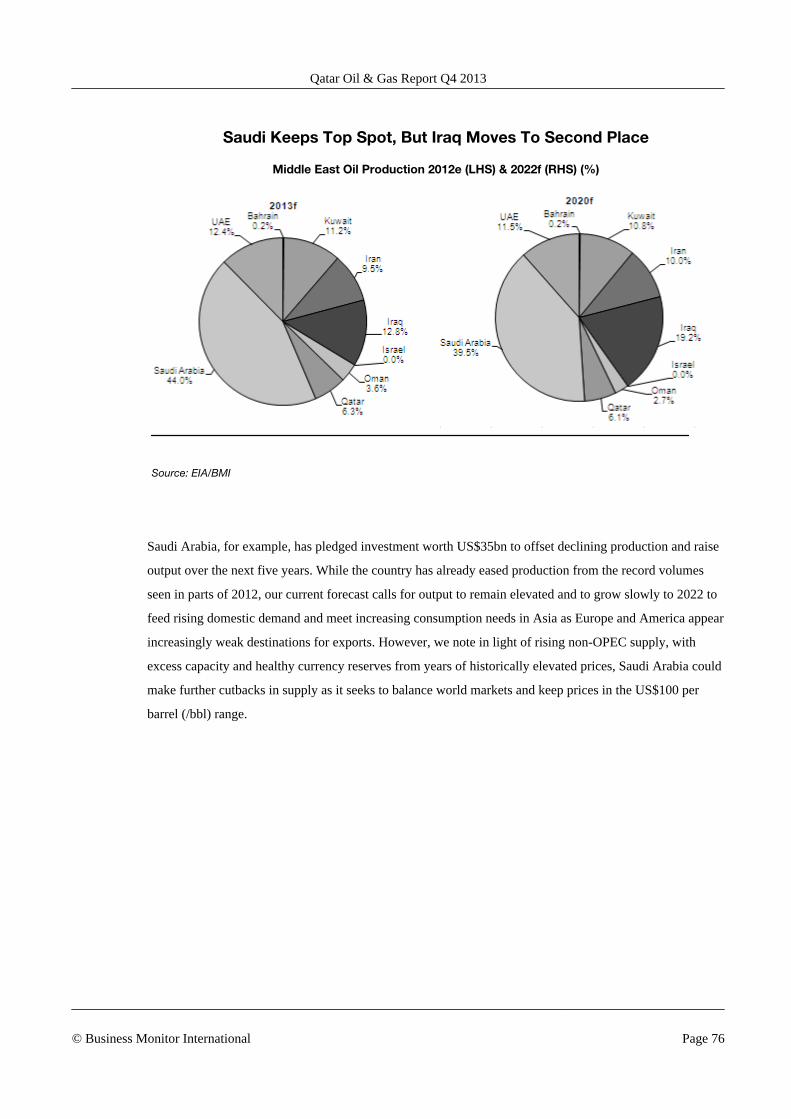

■ A slight increase in reserves and steady above-ground performance saw a slight increase in SaudiArabia's overall upstream score and move ahead of Kuwait despite a recent downward revision to ourproduction forecasts for the country. While we see further risks to Saudi output if the world's swingproducer with the largest spare capacity decides to cut production to support prices in a well-suppliedglobal oil market, the scale of its reserves and production capacity leaves it well-placed to continue itsstrong upstream performance.

■ However these rewards in Saudi Arabia are largely off-limits to foreign players due to itstightly controlled oil sector. We also note a tightening of gas supplies, which could even see the Kingdomresort to temporary or seasonal LNG imports, as a further downside risk to the country's upstream score.

■ Although Kuwait is advancing a major upstream investment programme, we see Kuwait's upstreamscores particularly at threat as a result of the country's poor track record in attracting foreign investmentcompared to other producers in the region. Political infighting could also continue to delay majorprojects. These risks could see us further downgrade both the country's output and risk scores.

■ Across the region, we see growing interest in unconventional exploration. Although nearly all majorproducers in the region have expressed interest in tapping various deposits - shale gas and oil in Kuwaitfor example - we see Saudi Arabia and Oman as the best positioned for success. New supplies couldboost upstream scores and alleviated shortages, with Oman on the verge of a major tight gas project ledby BP following an agreement with the supermajor on prices. Again, owing to its troubled business

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 33

environment, we expect Kuwait to make the least progress in the region in tapping challenging anddifficult-to-recover deposits.

■ Despite its significant oil and gas reserves, above-ground obstacles in Iran will keep the country at thebottom of our rankings until sanctions are removed and badly-needed new investment and foreignparticipation returns to unlock the country's below-ground potential. While the recent election ofmoderate Hassan Rouhani could ease tensions, at present it remains near-impossible to determine if orwhen Iran's oil & gas sector could return to health.

■ Broadly speaking, despite strong hydrocarbons potential across much of the region which translates intostrong industry rewards, limits to foreign participation result in lower rewards scores while politicaluncertainty results in elevated risks in our proprietary upstream rankings.

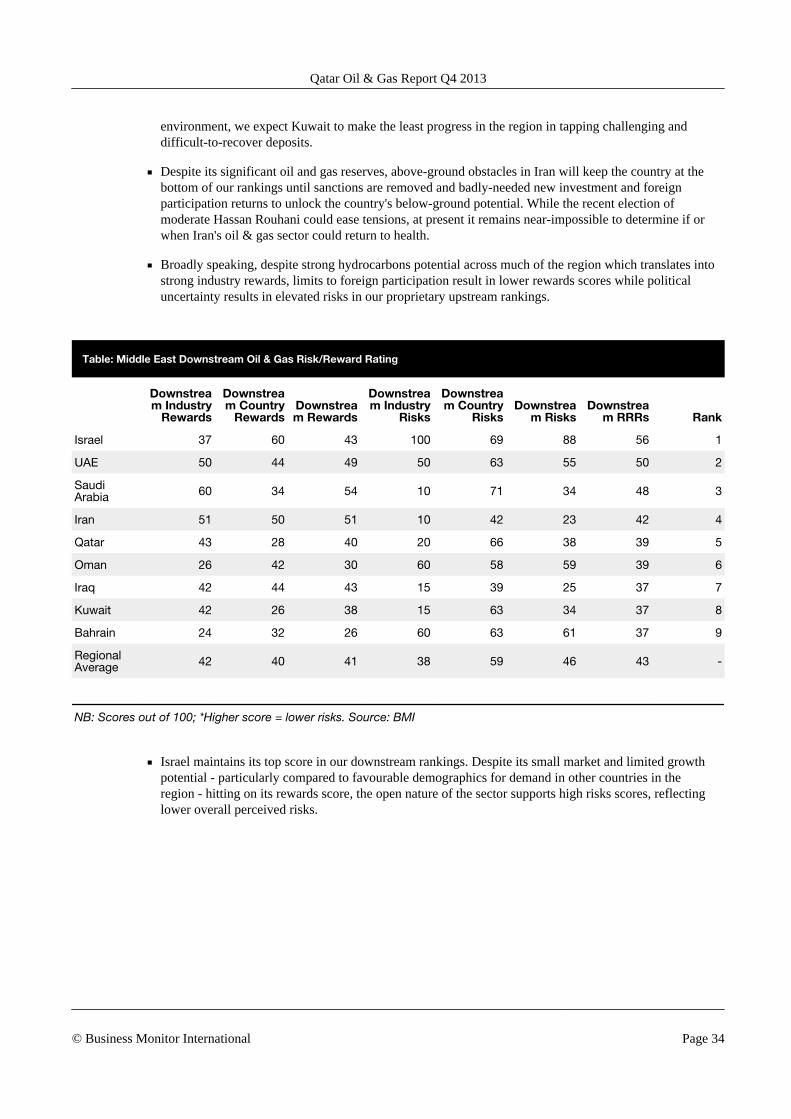

Table: Middle East Downstream Oil & Gas Risk/Reward Rating

Downstream Industry

Rewards

Downstream Country

RewardsDownstream Rewards

Downstream Industry

Risks

Downstream Country

RisksDownstrea

m RisksDownstrea

m RRRs Rank

Israel 37 60 43 100 69 88 56 1

UAE 50 44 49 50 63 55 50 2

SaudiArabia 60 34 54 10 71 34 48 3

Iran 51 50 51 10 42 23 42 4

Qatar 43 28 40 20 66 38 39 5

Oman 26 42 30 60 58 59 39 6

Iraq 42 44 43 15 39 25 37 7

Kuwait 42 26 38 15 63 34 37 8

Bahrain 24 32 26 60 63 61 37 9

RegionalAverage 42 40 41 38 59 46 43 -

NB: Scores out of 100; *Higher score = lower risks. Source: BMI

■ Israel maintains its top score in our downstream rankings. Despite its small market and limited growthpotential - particularly compared to favourable demographics for demand in other countries in theregion - hitting on its rewards score, the open nature of the sector supports high risks scores, reflectinglower overall perceived risks.

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 34

In The Lead But Below Average

Oil Consumption, % chg y-o-y

Israel: Oil consumption, % change y-o-ySaudi Arabia: Oil consumption, % change y-o-yUAE: Oil consumption, % change y-o-yMiddle East: Regional Oil consumption, % change y-o-y

2010

2011

2012

2013

f

2014

f

2015

f

2016

f

2017

f

0

25

f = forecast. Source: EIA, BMI

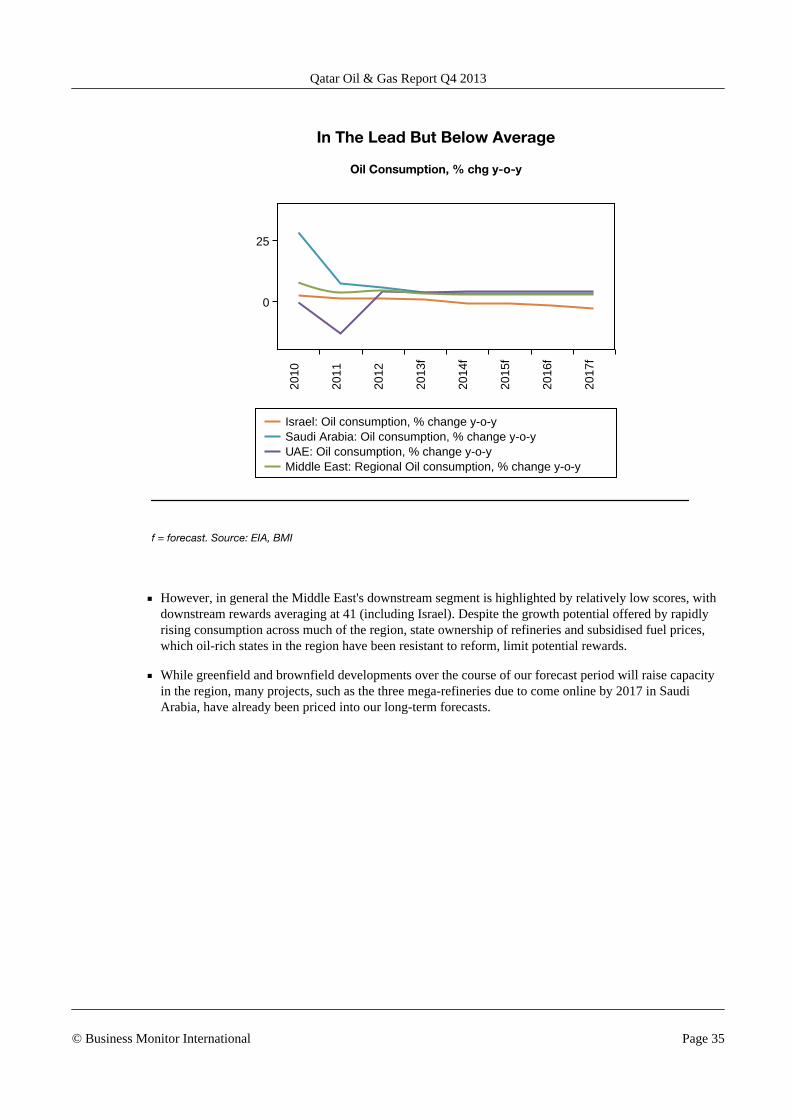

■ However, in general the Middle East's downstream segment is highlighted by relatively low scores, withdownstream rewards averaging at 41 (including Israel). Despite the growth potential offered by rapidlyrising consumption across much of the region, state ownership of refineries and subsidised fuel prices,which oil-rich states in the region have been resistant to reform, limit potential rewards.

■ While greenfield and brownfield developments over the course of our forecast period will raise capacityin the region, many projects, such as the three mega-refineries due to come online by 2017 in SaudiArabia, have already been priced into our long-term forecasts.

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 35

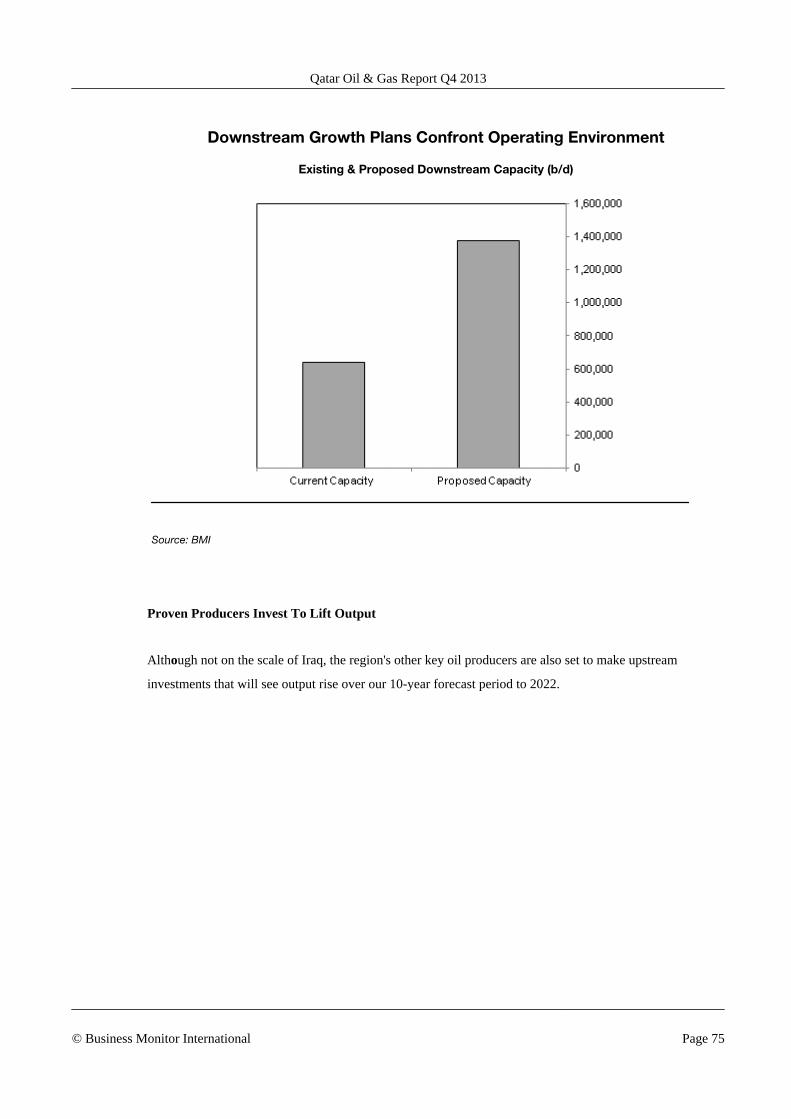

■ Where we see further upside, is Iraq, although thecountry has struggled to advance the four majordownstream projects since awarding designcontracts in 2009. This has left Iraq dependent onimports despite its growing crude oil production.Although there are incentives, we see little near-term scope for improvement in the above-groundeconomic and regulatory risks that have deterredforeign investment in refining projects to date.One project we are optimistic may advance is the300,000b/d Nassiriya plant tied to development ofa major field, though we have not pencilled-in anycapacity increase to our current forecast.

■ Although we expect capacity increases in Kuwait,we note that previous delays to the Al-Zourrefinery project - again as result of political andbureaucratic pressures - could see downwardrevisions to our projections that currently includethe 615,000b/d greenfield development as well ascapacity expansions at existing plants.

• While investment in new refineries across theregion will lift our assessment of downstreaminfrastructure and therefore ratings for eachmarket, new capacity will do little to alter thefundamentals of a tightly-regulated downstreamsegment.

Qatar - Risk/Reward Ratings

Qatar Upstream Rating

Qatar, a member of OPEC, is also the world's largest supplier of liquefied natural gas (LNG) worldwide. It

also remains one of the world's top crude oil exporters. Its significant below-ground potential, as well as its

leadership of the natural gas industry, ensures that the country will remain a key global player for the

foreseeable future. The presence of non-state competitors and relatively stable political outlook support an

attractive business environment.

Massive proven natural gas reserves and its strong gas reserves to production ratio support Qatar's role as a

key player in the sector for the foreseeable future. Its oil reserves are significant as well, although its fields

are maturing. As such, the absence of new oil discoveries will see its proven oil reserves begin to decline

over the coming decade. However, the strong presence of foreign players and positive licensing terms also

make it an attractive investment location, making its overall outlook very positive.

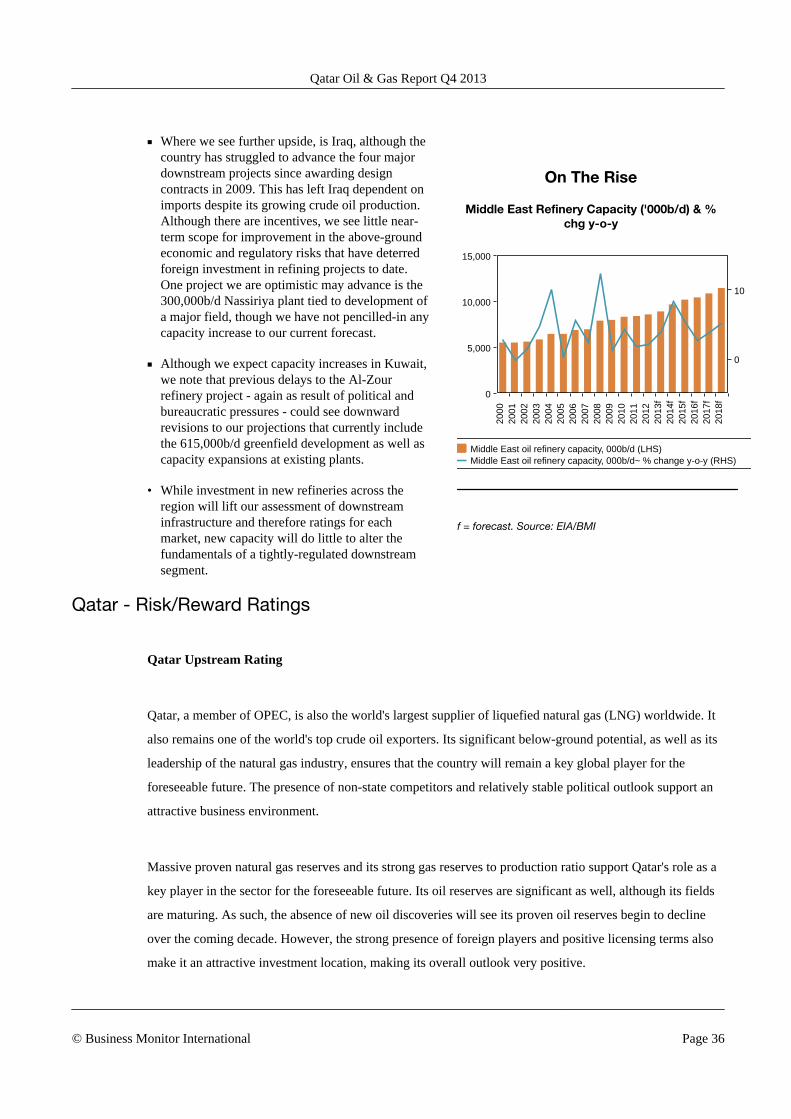

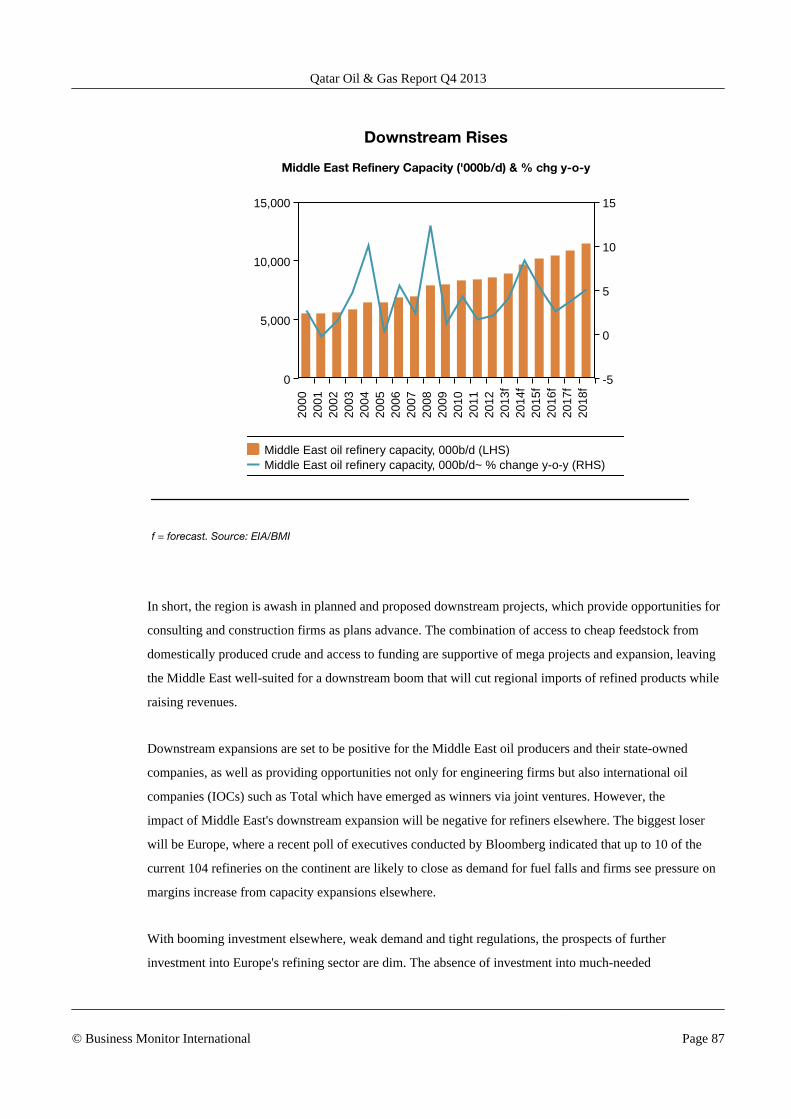

On The Rise

Middle East Refinery Capacity ('000b/d) & %chg y-o-y

Middle East oil refinery capacity, 000b/d (LHS)Middle East oil refinery capacity, 000b/d~ % change y-o-y (RHS)

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

f20

14f

2015

f20

16f

2017

f20

18f

0

5,000

10,000

15,000

0

10

f = forecast. Source: EIA/BMI

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 36

The strong likelihood of governance and policy continuity, as well as relatively low levels of corruption,

especially for the Middle East region, reduces some of the country's political risks. The country receives an

average score for physical infrastructure, although there has been additional infrastructure investment in

recent years, particularly in support of LNG exports.

Qatar Downstream Rating

Meeting rapidly growing domestic energy demand going to be critical in the years ahead, particularly in

terms of gas production which is the primary input for the country's electricity. While oil consumption

remains low relative to production, it is rising rapidly as well. The downstream segment also remains

relatively closed off to foreign investment. Planned expansions of downstream capacity could bolster

Qatar's downstream rating.

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 37

Market Overview

Qatar Energy Market Overview

Latest data from the Qatar Statistics Authority (QSA) show that the Qatari economy expanded by 6.2% in

real annual terms during Q113, decelerating slightly from growth of 7.5% and 6.6% in Q112 and Q412

respectively. The oil and gas sector continued the trend of weak growth seen since Q212, expanding by

0.8% year-on-year and remaining the worst performing sector of the economy. We expect the expansion of

the hydrocarbons sector to remain mild throughout Q413 and 2014, constrained by a small decline in oil

production and limited medium-term potential for liquefied natural gas (LNG) output growth. According to

data from the International Energy Agency, oil output averaged 0.73mn barrels per day (b/d) during the first

seven months of 2013, down by 3.0% from the same period of 2012.

The changing LNG market could push Qatar to shift strategies on gas. Firstly, we could see greater

investment in both petrochemicals and gas-to-liquids (GTL). These moves would diversify the revenue

stream away from gas and - if sufficient investment is made - could help offset any loss in profits as LNG

prices trend downward in lucrative Asian markets. Secondly, Qatar may seek alternative export

opportunities for gas; this could bring about an increase in existing pipeline connections within the Gulf

region, with countries such as Kuwait and the UAE set to see their gas import requirement rise over the

coming years.

Perhaps more boldly, Qatari officials at the Brooking Doha Energy Forum in April suggested the

development of a regional network that would link the Middle East with Southern Europe. Such a proposal

faces numerous geopolitical and financial hurdles, but given the financial resources of countries such as

Qatar, and Europe's interest in securing investment from the cash-rich region as well as reducing reliance on

Russian gas, the idea could enjoy a welcome reception.

With a moratorium on development of North Field, Qatar's energy strategy is in a period of transition.

Downstream expansion is consistent with that broader strategy as Qatar's role as the largest exporter of

LNG is increasingly under pressure from new suppliers. In response, Qatar has moved to boost cooperation

with foreign players for new discoveries, make new investment in petrochemicals and gas-to-liquids (GTL),

and boost investment abroad to capture a slice of emerging sources of new gas supplies.

An expansion of downstream capacity, although not a recent proposal, is consistent with Qatar's broader

aims to diversify and strengthen its energy position as it prepares for shifting realities on the LNG front.

Boosting refining capacity will allow Qatar to move up the value chain and capture higher revenues with

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 38

export of refined products rather than unprocessed condensate alone, which already is sold at a premium on

international markets given its suitability for both refining and as feedstock for petrochemicals.

Although LNG capacity could rise via improvements to existing facilities, we do not currently anticipate

any expansion of capacity via the construction of additional trains given government policy. Indeed,

Qatar must operate in a changing gas market - highlighted by changing supply dynamics stemming from the

unconventional revolution and rising supplies of LNG from Australia, North America, East Africa and

Russia. The anticipation of rising supplies is strengthening the hand of LNG importers, who are keen to see

prices fall from recent record highs, particularly in Asia where demand for LNG is set to grow most.

In 2012, Qatar saw talks for LNG exports to India and Pakistan enter deadlock as both governments rejected

Doha's offers based on prices that were seen as too high. Qatar, which has been resistant to altering gas

prices indexed to oil, could come under pressure as alternative supplies enter the LNG market -

especially as the Asian gas market takes tentative steps toward greater liberalisation. Japan's efforts to

introduce an LNG futures market, as well as Tokyo and Seoul's joint efforts to use their combined

purchasing power to lower prices and ensure imports are indexed to alternative benchmarks such as Henry

Hub, could place further pressure on Qatari LNG pricing.

Qatar has also announced plans to boost investment in North America. The moves seek to take advantage

of the glut of low-priced gas that is likely to transform North America from an importer into a

supplier to the global market. We believe the move will benefit not only upstream and downstream

investment in North America, but will help Qatar remain a key player in the global LNG market, even as

alternative supplies start to come online.

The response may allow Qatar to weather an environment of increased supply and even to profit from the

rise of competitors in the global market. The most recent was Qatar Petroleum International (QPI)'s

announcement that it would team-up with the UK's Centrica to spend CAN1bn (US

$976mn) on acquiring Suncor Energy's conventional natural gas assets across Alberta, north-

eastern British Colombia and southern Saskatchewan. Centrica estimates proved plus probable gas reserves

at nearly 30bn cubic meters (bcm), but contingent resources may be closer to 84bcm given prospective

but undeveloped acreage.

The acquisition will help Centrica to meet local demand via its North American subsidiary, but importantly

for Qatar, will give QPI a foothold in the Canadian gas market, where the number of planned and

proposed LNG projects is growing. Indeed, in making the move, Qatar announced this play in Canada

would be the first of numerous future investments.

Qatar Oil & Gas Report Q4 2013

© Business Monitor International Page 39

Following hot on the heels of the deal between QPI and US super major ExxonMobil to 'assess jointly

unconventional gas resources in North America and global opportunities' in LNG, Qatar should be taken at

its word. Exxon, with a significant presence in the gas and LNG market in Qatar, is now deepening its

global cooperation with Doha. The duo have already partnered on the Gulf Coast-based Golden Pass LNG

terminal, with an application currently pending with US regulators to allow exports beyond those countries

with which the US has Free Trade Agreements (FTA).

Overview/State Role

The oil and gas sector is state-controlled, with Qatar Petroleum responsible for exploration and production

(E&P). NODCO is in charge of refining and distribution. Qatargas and RasGas are responsible for the

production and marketing of LNG. The state controls virtually all aspects of the energy sector, sets policy