Embed Size (px)

Citation preview

financial report

Q4 2017

DOF Subsea ASThormøhlens gate 53 C5006 BergenNORWAYwww.dofsubsea.com

Index

Financial Report 4th quarter 2017 . . . . . . . . . . . . . . . . . . .4

Financial statements 4th quarter 2017 . . . . . . . . . . . . . . .8

Consolidated statement of comprehensive income . . . . . . . . . . . 8

Consolidated statement of financial position . . . . . . . . . . . . . . . . . . 9

Consolidated statement of financial position . . . . . . . . . . . . . . . . 10

Consolidated statement of cash flows. . . . . . . . . . . . . . . . . . . . . . . . 11

Consolidated statement of changes in equity . . . . . . . . . . . . . . . . 12

Notes to the financial statements . . . . . . . . . . . . . . . . . . 14

Note 1 Management reporting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Note 2 Segment information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Note 3 Financial income and expenses . . . . . . . . . . . . . . . . . . . . . . . 17

Note 4 Tangible assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Note 5 Net interest-bearing debt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Note 6 Financial instruments and hedging activities . . . . . . . . 20

Note 7 Transactions with related parties . . . . . . . . . . . . . . . . . . . . . 21

Note 8 Investments in associates and joint ventures. . . . . . . . 21

Note 9 Events after the consolidated statement of financial position date. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Note 10 Shareholder information. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Note 11 General. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Note 12 Performance measurement definitions. . . . . . . . . . . . . 24

Supplemental information . . . . . . . . . . . . . . . . . . . . . . . . . 26

Condensed statement of comprehensive income 5 last quarters. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

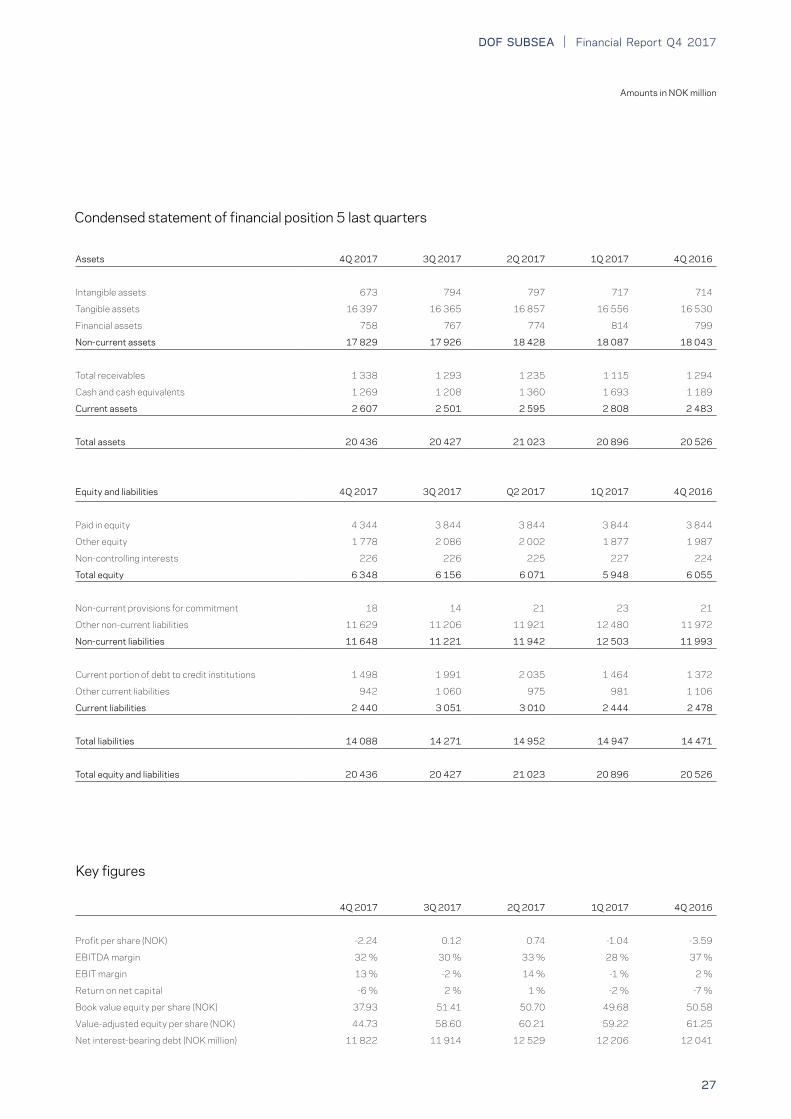

Condensed statement of financial position 5 last quarters. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

Key figures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

Financial Report Q4 2017 | DOF SUBSEA

4

HeadlinesIn the 4th quarter of 2017, DOF Subsea had an operating income of NOK 1 068 million (NOK 1 001 million in the 4th quarter of 2016) and an operating profit before depreciation of NOK 292 million (NOK 385 million including a sales gain of NOK 96 million). The operating profit was NOK 91 million (NOK 10 million) after depreciation and impairment of NOK 201 million (NOK 375 million). The net financial loss was NOK 305 million (NOK 417 million), and the loss before tax was NOK 215 million (NOK 407 million).

For 2017, the Group had an operating income of NOK 3 849 million (NOK 5 099 million) and an operating profit before depreciation of NOK 1 135 million (NOK 1 764 million including a sales gain of NOK 170 million). The operating profit was NOK 136 million (NOK 446 million) after depreciation and impairment of NOK 999 million (NOK 1 318 million). The net financial loss was NOK 259 million (NOK 179 million) giving a loss before tax of NOK 123 million (profit NOK 266 million)

During the quarter the 5-year IMR contract with Shell in Australia commenced, and in December, the Company completed a private placement of NOK 500 million towards the main shareholder, DOF ASA, increasing the number of outstanding shares from 119.7 million to 167.3 million. In connection with the private placement, the DOFSUB07 bond was extended by 2 years.

Key figures (NOK million) 4Q 2017 4Q 2016 2017 2016

Operating income 1 068 1 001 3 849 5 099

EBITDA 292 385 1 135 1 764

EBIT 91 10 136 446

Net interest-bearing debt 8 350 8 357 8 350 8 357

EBITDA proportional method 402 415 1 408 1 901

In the 4th quarter the Group has seen increased activity in both the Asia Pacific region and the North America region with increased utilisation of both personnel and assets. The activity in the Atlantic region and Brazil region was variable during the quarter giving a lower than expected utilisation of both personnel and assets. The general market conditions within our industry are still challenging, however in line with the rebound in the oil price the tendering activity has increased during the quarter for projects with start-up in 2018 and 2019.

During the quarter, the Group has seen improved performance in the Subsea/IMR Projects segment compared to 3rd quarter where the highlight was the start-up of the 5-year Shell Prelude IMR contract, and Skandi Constructor and Skandi Neptune receiving contracts within the renewables industry. In the 4th quarter, Geosea was in transit from Brazil to the North Sea, and Skandi Achiever and Skandi Vitoria were in dry-dock. In general, the idle time between projects has increased, lowering the personnel and vessel utilisation. In the quarter Geosea and

Geograph have been idle, whilst the utilisation of Skandi Niteroi has been 30%. The overall vessel utilisation for both owned and chartered-in vessels was 78% in the 4th quarter, where the uti-lisation in the Long-term Chartering segment was 87% and the utilisation in the Subsea/IMR Projects segment was 75%.

Operational events 4th quarterAs at 31 December 2017, the number of subsea employees was 1 214, and the Group’s fleet comprised 22 owned vessels, 3 chartered-in vessels and 2 newbuilds under construction, plus a fleet of 71 ROVs.

During the 4th quarter, the Asia Pacific region has conducted IMR and construction work for Shell in the Philippines, Chevron, TechnipFMC and Shell in Australia, PTSC in Vietnam and repair and installation work for PT Amman in Indonesia.

In the Atlantic region, the Group has executed engineering, survey, light construction and installation work for Eni in Angola, Conoco Phillips in Norway, TMPC in Libya and TechnipFMC in Libya, work within the renewables industry for Prysmian and Siemens and survey and positioning work for HMC.

In the North America region, the Group has conducted IMR work, installation work and ROV services for Husky Energy, Allseas, Shell, Hess and Enbridge and survey and positioning work for HMC.

In Brazil, the Group has been engaged in ROV inspection work for Petrobras. In addition, the joint venture with TechnipFMC has pro-vided pipelay services to Petrobras and McDermott/Queiroz Galvao.

During the quarter, the Group has been awarded several short-term contracts in the Subsea/IMR Projects segment where the APAC region was awarded contracts for Geotechnical services in Northern Australia utilising Skandi Hercules, and the Atlantic region was awarded contracts in the renewables industry utilising Skandi Constructor and Skandi Neptune. The North America region was awarded contracts by Allseas and Chevron utilising Skandi Achiever and Harvey Deep Sea. The JV company DOFCON Navegacao Ltda was awarded a short-term contract with McDermott utilising Skandi Niteroi.

Utilisation 4Q 2017 3Q 2017 2Q 2017 1Q 2017 4Q 2016

Long-term Chartering 87% 86% 83% 85% 95%

Subsea/IMR Projects 75% 70% 58% 57% 66%

Fleet 78% 74% 66% 65% 75%

Consolidated statement of comprehensive income and consolidated statement of financial positionIn the 4th quarter of 2017, the Group achieved an operating income of NOK 1 068 million compared to an operating income of NOK 1 001 million in the 4th quarter of 2016. The operating

Financial Report 4th quarter 2017

| Financial Report Q4 2017DOF SUBSEA

5

profit before depreciation (EBITDA) was NOK 292 million (NOK 385 million in 2016, including a sales gain of NOK 96 million). The operating profit (EBIT) was NOK 91 million (NOK 10 million). Depreciation and impairment amounted to NOK 201 million (NOK 375 million), of which NOK 64 million was impairment.

NOK million 4Q 2017 4Q 2016 Change %

Operating income 1 068 1 001 7%

EBITDA 292 385 -24%

EBIT 91 10 810%

Net financial loss was NOK 305 million (NOK 417 million), where NOK 194 million (NOK 193 million) was unrealised net loss on derivative instruments and currency positions. The loss before tax was NOK 215 million (NOK 407 million), and the loss for the period was NOK 375 million (NOK 430 million). Income tax expense was NOK 161 million, of which NOK 150 million was im-pairment of deferred tax assets.

The total operating income for 2017 was NOK 3 849 million (NOK 5 099 million in 2016) with an operating profit before depreciation (EBITDA) of NOK 1 135 million (NOK 1 764, in-cluding a sales gain of NOK 170 million) and an operating profit (EBIT) of NOK 136 million (NOK 446 million) after depreciation and impairment of NOK 999 million (NOK 1 318 million). The net financial loss was NOK 259 million (NOK 179 million), giving a loss before tax of NOK 123 million (profit of NOK 266 million). The loss for the period amounted to NOK 273 million (profit of NOK 155 million).

The Group’s total assets were NOK 16 738 million (NOK 16 648 million), where non-current assets amounted to NOK 14 534 million (NOK 14 479 million), including NOK 609 million (NOK 642 million) in intangible assets. Current assets were NOK 2 204 million (NOK 2 170 million), of which NOK 1 097 million (NOK 1 062 million) was cash and cash equivalents.

NOK million 31 .12 .2017 31 .12 .2016 Change %

Total assets 16 738 16 648 1%

Tangible assets 11 773 11 950 -1%

Cash and cash equivalents 1 097 1 062 3%

NIBD 8 350 8 357 -

Total equity 6 348 6 055 5%

The total equity was NOK 6 348 million (NOK 6 055 million), including non-controlling interests of NOK 226 million (NOK 224 million). Non-current liabilities were NOK 8 481 million (NOK 8 632 million). Current liabilities were NOK 1 909 million (NOK 1 961 million), of which NOK 1 191 million (NOK 1 114 million) was current portion of debt. The Group’s total equity and liabilities were NOK 16 738 million (NOK 16 648 million). The net interest-bearing debt (NIBD) was NOK 8 350 million

(NOK 8 357 million). At the end of December, the book equity ratio was 38%, and the value-adjusted equity ratio was 42%. The value-adjusted equity ratio is calculated by adjusting the book equity and total assets by excess values on all owned vessels in the Group.

Cash and cash equivalents have changed due to operating, in-vesting and financing activities. Net cash flow from operating activities in the 4th quarter was NOK -143 million (NOK 27 million). Cash flow from investing activities was NOK -5 million (NOK 759 million), of which NOK -38 million (NOK -185 million) was from investment in assets that increases or will increase ca-pacity for the Group. Cash flow from financing activities was NOK 151 million (NOK -867 million) of which NOK -305 million (NOK -869 million) was instalments and repayments on long-term inter-est-bearing debt. At the end of the 4th quarter, the Group’s cash and cash equivalents were NOK 1 097 million (NOK 1 062 million).

Debt, financing and liquidityThe Group’s current portion of debt at the end of December was NOK 1 191 million, including balloons, bond, drawn credit facilities and ordinary instalments. During the quarter no new loans were drawn, and the Group paid ordinary instalments.

The current weak market conditions have increased the risk for impairment of the Group’s non-current assets, and put pressure on the Group’s liquidity position. In December the Group completed a private placement of NOK 500 million to-wards DOF ASA, increasing the numbers of outstanding shares from 119.7 million to 167.4 million. The private placement was dependent on an extension of the remaining part of the DOFSUB07 bond of NOK 508 million from May 2018 to May 2020. In December the bondholder meeting voted in favour of extending the DOFSUB07 bond from 2018 to 2020, however with an instalment of NOK 100 million in October 2019.

Financial riskThe Group’s operating income is in NOK, USD, AUD, GBP, CAD and BRL, while the Group’s loans are distributed between NOK, USD and CAD. This exposes the Group to the risk of exchange rate fluctuations. The Group has an active exchange rate policy and uses derivatives to hedge the exchange rate exposure.

Financial Report Q4 2017 | DOF SUBSEA

6

The Group is exposed to fluctuations in interest rates. Part of the Group’s loans has fixed interest rates, reducing the exposure. The Group has an active interest rate policy and uses derivatives to hedge the interest rate exposure.

ShareholdersThe shares in DOF Subsea AS are owned by DOF ASA (64.9%), FRC Lux Holding Limited (30.6%) and Dolphin Invest 2 AS (4.5%). The number of outstanding shares is 167 352 762, with a book equity of NOK 37.93 per share.

EmployeesAt the end of 4th quarter, the number of employees in the Group was 1 214. The number does not include marine employees that are employed in DOF Management and Norskan and hired in through shipman agreements to operate and crew the vessels.

The FleetAs at end of December, the Group’s fleet comprised 22 owned vessels, 3 chartered-in vessels and 2 vessels under construction in DOFCON Navegacao Ltda, a 50/50 owned joint venture with TechnipFMC.

The BacklogAs at end of December, the firm contract backlog amounts to NOK 16.1 billion, and including options NOK 34.3 billion. However, the Group is exposed to the short-term market con-ditions in the Subsea/IMR Projects segment. In this segment the management is working to increase the backlog and improve the utilisation of personnel and assets.

Contract Backlog*

* Contract backlog excludes master service agreements (MSAs) within the subsea/

IRM project segment. Under the MSAs only confirmed POs are accounted for.

Events after the consolidated statement of financial position dateIn January, DOF Subsea Brazil was awarded 2 new ROV con-tracts by Petrobras and an extension for 2 additional ROV’s.

In the Atlantic region, the contracts for Skandi Neptune and Skandi Constructor have been extended until the beginning of April and end of February 2018.

Skandi Skansen’s contract with TechnipFMC has been extended, and the vessel has further been awarded a new contract securing high utilisation for the vessel the first four months of the year.

In the Brazil region, Skandi Salvador has been awarded a short-term contract with Saipem.

In the Asia Pacific region, an IMR frame agreement has been extended by one year, under which Skandi Singapore has been awarded 30 days of work in Q1 2018 with potential for additional scope.

In the North America region, Harvey Deep Sea and Skandi Achiever have been awarded short-term contracts securing utilisation in Q1 2018.

Forward looking statementThe Board of Directors is satisfied with the performance in 4th quarter, however the financial numbers for 2017 are below the Board of Directors’ expectations due to one-off events in the North America region and in the Asia Pacific region.

The market has continued to be challenging, with seasonal variations in the different regions during the 4th quarter, and the Board of Directors expects the markets to continue to be challenging in 2018. A continuing weak market, both with regards to terms and margins on new contracts, could lead to reduced earnings and impairment of the vessel values for the Group. As such, the Group will continue its focus on adjusting its capacity and risk exposure to the current challenging market environment. However with oil prices stabilising above USD 60 per barrel, oil companies have increased their tendering activity which may indicate the subsea markets to gradually improve, increasing the demand for the Group’s services in the medium term. The majority of the Group’s high-end assets are committed on long-term contracts, and represents the largest portion of the Group’s backlog, including the two remaining newbuilds committed on 8-year contracts. The Board of Directors would like to thank all employees for the efforts made in 2017.

Bergen, 22 February 2018The Board of Directors of DOF Subsea AS

Contact information:Mons S. Aase, CEO +47 916 61 012Marianne Møgster +47 993 06 916

DOF Subsea ASThormølens gate 53 C5006 Bergen www.dofsubsea.com

| Financial Report Q4 2017DOF SUBSEA

7

Financial Report Q4 2017 | DOF SUBSEA

8

Amounts in NOK million

Financial statements 4th quarter 2017

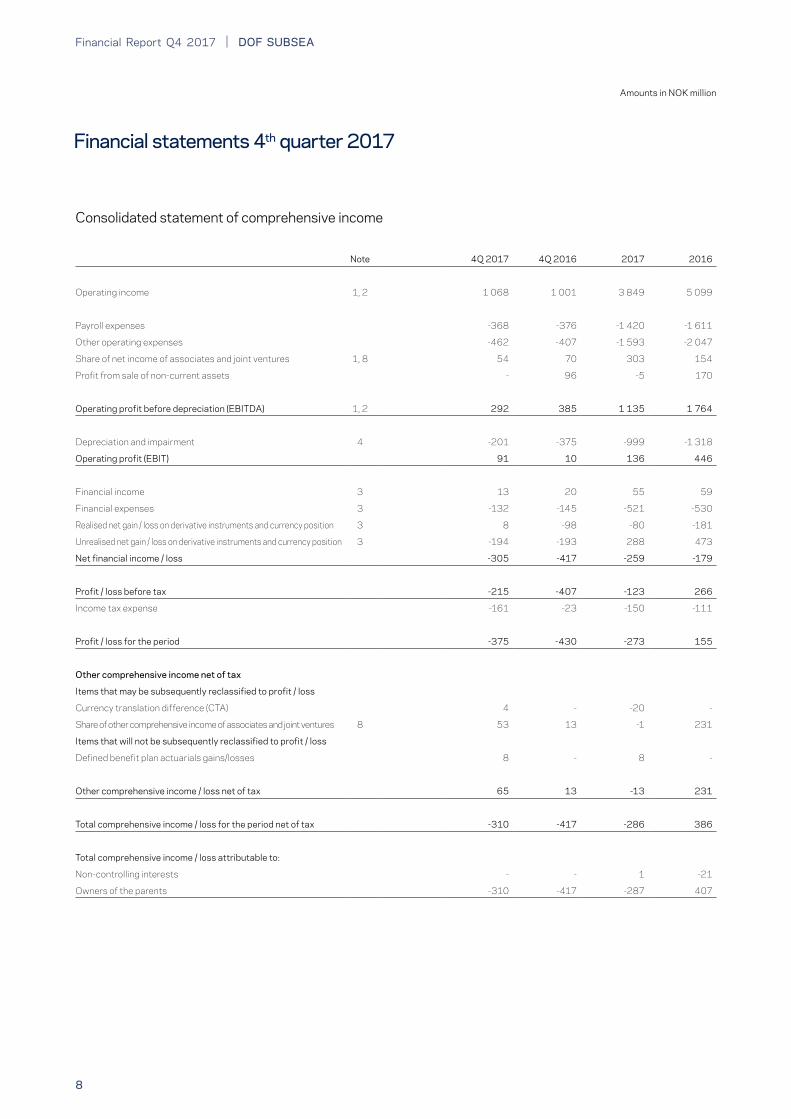

Consolidated statement of comprehensive income

Note 4Q 2017 4Q 2016 2017 2016

Operating income 1, 2 1 068 1 001 3 849 5 099

Payroll expenses -368 -376 -1 420 -1 611

Other operating expenses -462 -407 -1 593 -2 047

Share of net income of associates and joint ventures 1, 8 54 70 303 154

Profit from sale of non-current assets - 96 -5 170

Operating profit before depreciation (EBITDA) 1, 2 292 385 1 135 1 764

Depreciation and impairment 4 -201 -375 -999 -1 318

Operating profit (EBIT) 91 10 136 446

Financial income 3 13 20 55 59

Financial expenses 3 -132 -145 -521 -530

Realised net gain / loss on derivative instruments and currency position 3 8 -98 -80 -181

Unrealised net gain / loss on derivative instruments and currency position 3 -194 -193 288 473

Net financial income / loss -305 -417 -259 -179

Profit / loss before tax -215 -407 -123 266

Income tax expense -161 -23 -150 -111

Profit / loss for the period -375 -430 -273 155

Other comprehensive income net of tax

Items that may be subsequently reclassified to profit / loss

Currency translation difference (CTA) 4 - -20 -

Share of other comprehensive income of associates and joint ventures 8 53 13 -1 231

Items that will not be subsequently reclassified to profit / loss

Defined benefit plan actuarials gains/losses 8 - 8 -

Other comprehensive income / loss net of tax 65 13 -13 231

Total comprehensive income / loss for the period net of tax -310 -417 -286 386

Total comprehensive income / loss attributable to:

Non-controlling interests - - 1 -21

Owners of the parents -310 -417 -287 407

| Financial Report Q4 2017DOF SUBSEA

9

Amounts in NOK million

Consolidated statement of financial position

Assets Note 31 .12 .2017 31 .12 .2016

Tangible assets 4 11 773 11 950

Goodwill 366 373

Deferred tax asset 243 269

Investment in associates and joint ventures 1, 8 1 027 717

Non-current receivables 6 1 125 1 169

Non-current assets 14 534 14 479

Trade receivables 855 791

Other current receivables 6 252 317

Total current receivables 1 107 1 108

Restricted cash 311 305

Unrestricted cash and cash equivalents 786 757

Cash and cash equivalents 5 1 097 1 062

Current assets 2 204 2 170

Total assets 16 738 16 648

Financial Report Q4 2017 | DOF SUBSEA

10

Amounts in NOK million

Equity and liabilities Note 31 .12 .2017 31 .12 .2016

Paid-in equity 10 4 344 3 844

Other equity 1 778 1 987

Non-controlling interests 226 224

Total equity 6 348 6 055

Bond loans 5 1 914 1 297

Debt to credit institutions 5 6 518 7 208

Financial non-current derivatives 6 24 98

Other non-current liabilities 24 29

Non-current liabilities 8 481 8 632

Current portion of debt 5 1 191 1 114

Trade payables 392 500

Other current liabilities 6 325 347

Current liabilities 1 909 1 961

Total liabilities 10 390 10 594

Total equity and liabilities 16 738 16 648

Consolidated statement of financial position

| Financial Report Q4 2017DOF SUBSEA

11

Amounts in NOK million

Consolidated statement of cash flows

Note 4Q 2017 4Q 2016 2017 2016

Operating profit (EBIT) 91 10 136 446

Depreciation and impairment 4 201 374 999 1 318

Profit from sale of non-current assets - -97 5 -170

Share of net income of associates and joint ventures 1, 8 -54 -70 -302 -154

Change in trade receivables -141 -11 -64 361

Change in trade payables -10 -10 -108 -339

Changes in other working capital -142 -35 -3 21

Exchange rate effect on operating activities 55 17 -4 -62

Cash flow from operating activities - 180 659 1 423

Interest received 2 2 28 30

Interest paid -113 -154 -494 -553

Tax paid -32 -1 -50 -40

Net cash flow from operating activities -143 27 143 859

Sale of tangible assets - 938 -2 1 489

Purchase of tangible assets 4 -38 -185 -625 -479

Purchase of shares - 2 -9 -

Dividends received - - - 3

Net cash flows from other non-current receivables 32 5 -43 -249

Cash flow from investing activities -5 759 -678 763

Proceeds of interest-bearing debt -44 - 1 932 319

Instalments on interest-bearing debt -305 -869 -1 875 -2 279

Payments to non-controlling interests - 2 - -24

Share issue 500 - 500 -

Cash flow from financing activities 151 -867 558 -1 983

Net change in cash and cash equivalents 3 -81 23 -361

Cash and cash equivalents at the beginning of period 1 097 1 137 1 062 1 464

Cash and cash equivalents from merger and acquisition - - 27 -

Exchange rate effect on cash and cash equivalents -2 6 -15 -41

Cash and cash equivalents at the end of the period 1 097 1 062 1 097 1 062

Financial Report Q4 2017 | DOF SUBSEA

12

Amounts in NOK million

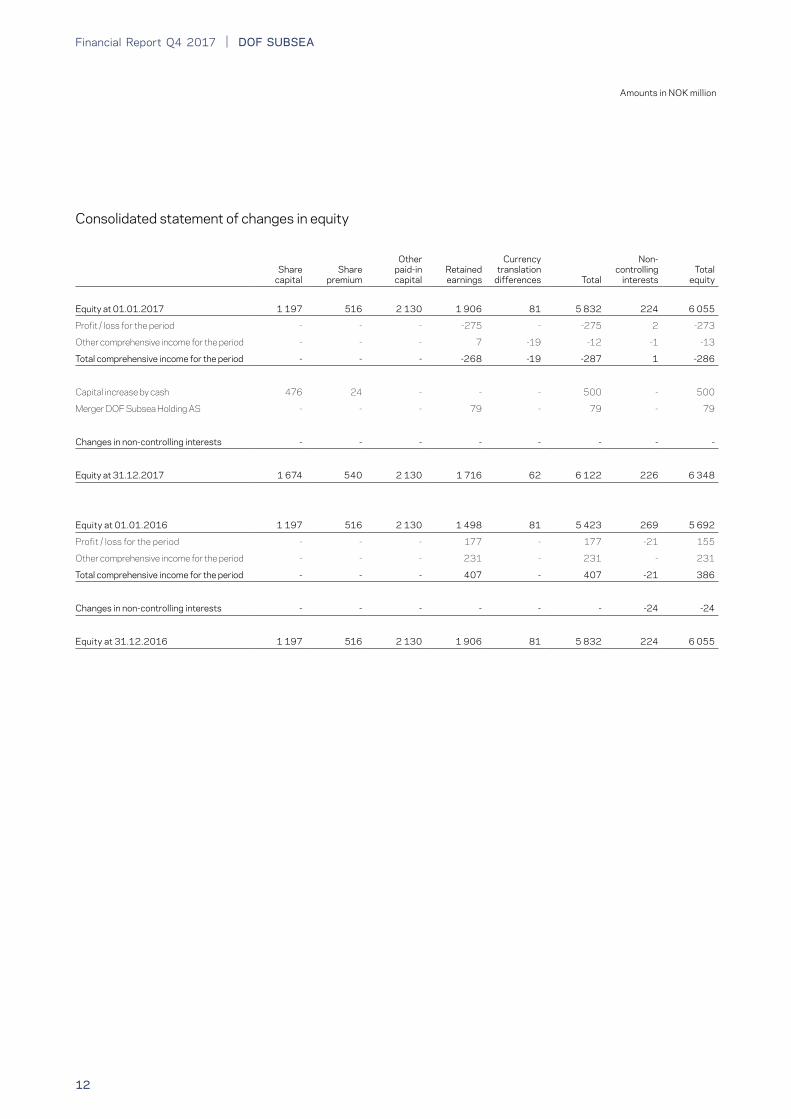

Consolidated statement of changes in equity

Share

capital

Share

premium

Other paid-in capital

Retained earnings

Currency translation

differences

Total

Non- controlling

interests

Total

equity

Equity at 01 .01 .2017 1 197 516 2 130 1 906 81 5 832 224 6 055

Profit / loss for the period - - - -275 - -275 2 -273

Other comprehensive income for the period - - - 7 -19 -12 -1 -13

Total comprehensive income for the period - - - -268 -19 -287 1 -286

Capital increase by cash 476 24 - - - 500 - 500

Merger DOF Subsea Holding AS - - - 79 - 79 - 79

Changes in non-controlling interests - - - - - - - -

Equity at 31 .12 .2017 1 674 540 2 130 1 716 62 6 122 226 6 348

Equity at 01 .01 .2016 1 197 516 2 130 1 498 81 5 423 269 5 692

Profit / loss for the period - - - 177 - 177 -21 155

Other comprehensive income for the period - - - 231 - 231 - 231

Total comprehensive income for the period - - - 407 - 407 -21 386

Changes in non-controlling interests - - - - - - -24 -24

Equity at 31 .12 .2016 1 197 516 2 130 1 906 81 5 832 224 6 055

| Financial Report Q4 2017DOF SUBSEA

13

Financial Report Q4 2017 | DOF SUBSEA

14

Amounts in NOK million

Notes to the financial statements

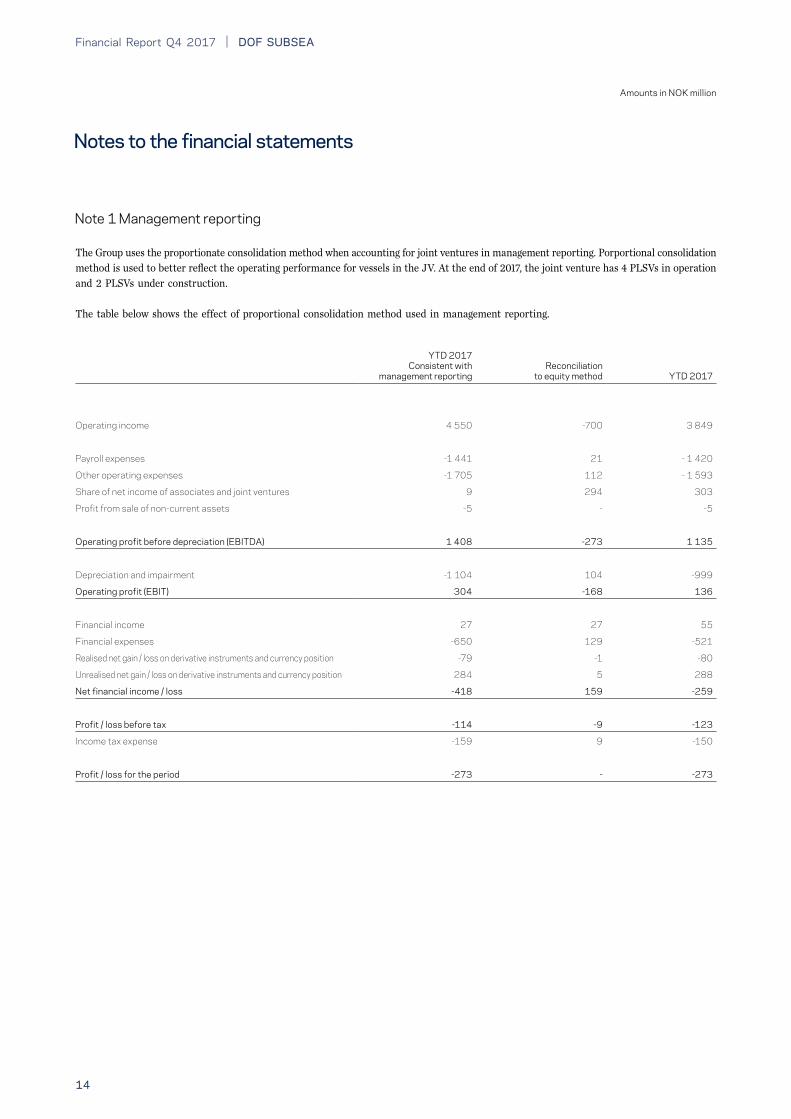

Note 1 Management reporting

The Group uses the proportionate consolidation method when accounting for joint ventures in management reporting. Porportional consolidation method is used to better reflect the operating performance for vessels in the JV. At the end of 2017, the joint venture has 4 PLSVs in operation and 2 PLSVs under construction.

The table below shows the effect of proportional consolidation method used in management reporting.

YTD 2017Consistent with

management reportingReconciliation

to equity method YTD 2017

Operating income 4 550 -700 3 849

Payroll expenses -1 441 21 - 1 420

Other operating expenses -1 705 112 - 1 593

Share of net income of associates and joint ventures 9 294 303

Profit from sale of non-current assets -5 - -5

Operating profit before depreciation (EBITDA) 1 408 -273 1 135

Depreciation and impairment -1 104 104 -999

Operating profit (EBIT) 304 -168 136

Financial income 27 27 55

Financial expenses -650 129 -521

Realised net gain / loss on derivative instruments and currency position -79 -1 -80

Unrealised net gain / loss on derivative instruments and currency position 284 5 288

Net financial income / loss -418 159 -259

Profit / loss before tax -114 -9 -123

Income tax expense -159 9 -150

Profit / loss for the period -273 - -273

| Financial Report Q4 2017DOF SUBSEA

15

Amounts in NOK million

Note 1 Management reporting (continued from previous page)

Consolidated statement of financial position

31 .12 .2017Consistent with

management reportingReconciliation

to equity method YTD 2017

Intangible assets 673 -64 609

Tangible assets 16 397 -4 624 11 773

Financial assets 759 1 393 2 152

Non-current assets 17 829 -3 295 14 534

Current assets 2 607 -403 2 204

Total assets 20 436 -3 698 16 738

Consolidated statement of financial position

31 .12 .2017Consistent with

management reportingReconciliation

to equity method YTD 2017

Total equity 6 348 - 6 348

Non-current liabilities 11 648 -3 166 8 481

Current liabilities 2 440 -532 1 909

Total liabilities 14 088 -3 698 10 390

Total equity and liabilities 20 436 -3 698 16 738

Consolidated statement of cash flows

31 .12 .2017Consistent with

management reportingReconciliation

to equity method YTD 2017

Net cash flow from operating activities 569 -426 143

Cash flow from investing activities -1 029 351 -678

Cash flow from financing activities 533 25 558

Net change in cash and cash equivalents 72 -49 23

Cash and cash equivalent at the beinning of the period 1 189 -127 1 062

Effect of merger and acquisition 27 - 27

Exchange rate effect on cash and cash equivalents -19 4 -15

Cash and Cash equivalents at the end of the period 1 269 -172 1 097

Financial Report Q4 2017 | DOF SUBSEA

16

Amounts in NOK million

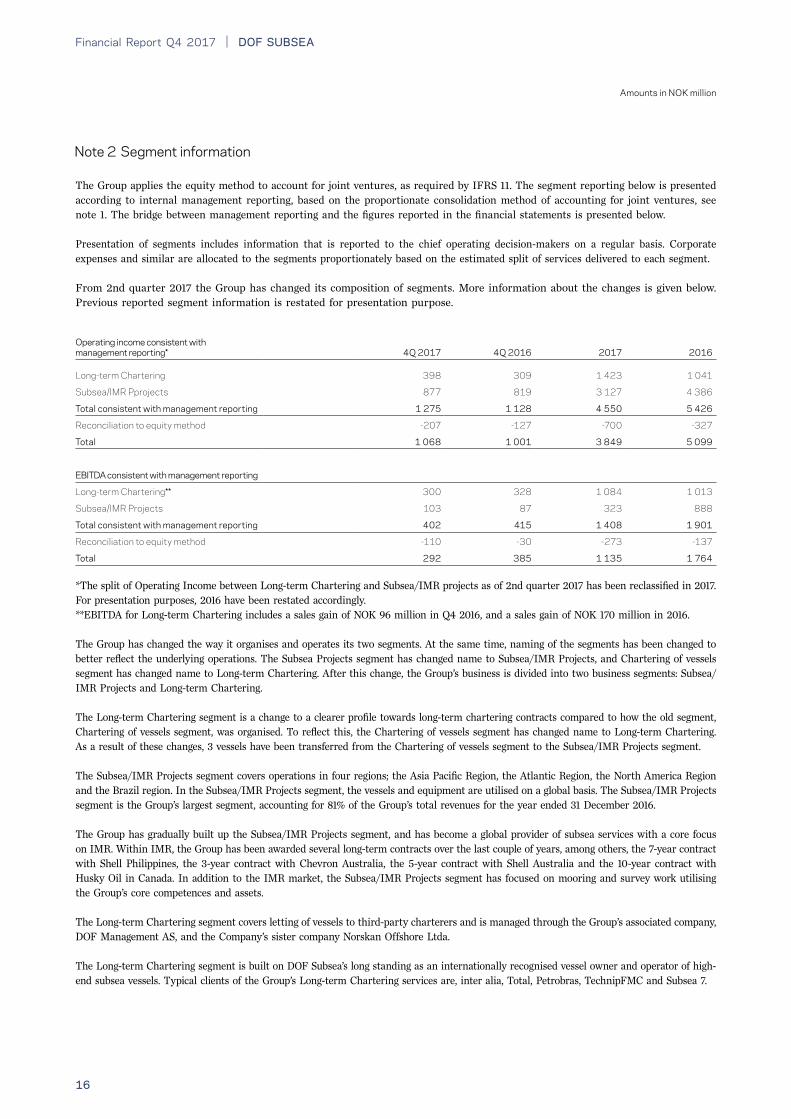

Note 2 Segment information

The Group applies the equity method to account for joint ventures, as required by IFRS 11. The segment reporting below is presented according to internal management reporting, based on the proportionate consolidation method of accounting for joint ventures, see note 1. The bridge between management reporting and the figures reported in the financial statements is presented below.

Presentation of segments includes information that is reported to the chief operating decision-makers on a regular basis. Corporate expenses and similar are allocated to the segments proportionately based on the estimated split of services delivered to each segment.

From 2nd quarter 2017 the Group has changed its composition of segments. More information about the changes is given below. Previous reported segment information is restated for presentation purpose.

*The split of Operating Income between Long-term Chartering and Subsea/IMR projects as of 2nd quarter 2017 has been reclassified in 2017. For presentation purposes, 2016 have been restated accordingly. **EBITDA for Long-term Chartering includes a sales gain of NOK 96 million in Q4 2016, and a sales gain of NOK 170 million in 2016.

The Group has changed the way it organises and operates its two segments. At the same time, naming of the segments has been changed to better reflect the underlying operations. The Subsea Projects segment has changed name to Subsea/IMR Projects, and Chartering of vessels segment has changed name to Long-term Chartering. After this change, the Group’s business is divided into two business segments: Subsea/IMR Projects and Long-term Chartering.

The Long-term Chartering segment is a change to a clearer profile towards long-term chartering contracts compared to how the old segment, Chartering of vessels segment, was organised. To reflect this, the Chartering of vessels segment has changed name to Long-term Chartering. As a result of these changes, 3 vessels have been transferred from the Chartering of vessels segment to the Subsea/IMR Projects segment.

The Subsea/IMR Projects segment covers operations in four regions; the Asia Pacific Region, the Atlantic Region, the North America Region and the Brazil region. In the Subsea/IMR Projects segment, the vessels and equipment are utilised on a global basis. The Subsea/IMR Projects segment is the Group’s largest segment, accounting for 81% of the Group’s total revenues for the year ended 31 December 2016.

The Group has gradually built up the Subsea/IMR Projects segment, and has become a global provider of subsea services with a core focus on IMR. Within IMR, the Group has been awarded several long-term contracts over the last couple of years, among others, the 7-year contract with Shell Philippines, the 3-year contract with Chevron Australia, the 5-year contract with Shell Australia and the 10-year contract with Husky Oil in Canada. In addition to the IMR market, the Subsea/IMR Projects segment has focused on mooring and survey work utilising the Group’s core competences and assets.

The Long-term Chartering segment covers letting of vessels to third-party charterers and is managed through the Group’s associated company, DOF Management AS, and the Company’s sister company Norskan Offshore Ltda.

The Long-term Chartering segment is built on DOF Subsea’s long standing as an internationally recognised vessel owner and operator of high-end subsea vessels. Typical clients of the Group’s Long-term Chartering services are, inter alia, Total, Petrobras, TechnipFMC and Subsea 7.

Operating income consistent with management reporting*

4Q 2017

4Q 2016

2017

2016

Long-term Chartering 398 309 1 423 1 041

Subsea/IMR Pprojects 877 819 3 127 4 386

Total consistent with management reporting 1 275 1 128 4 550 5 426

Reconciliation to equity method -207 -127 -700 -327

Total 1 068 1 001 3 849 5 099

EBITDA consistent with management reporting

Long-term Chartering** 300 328 1 084 1 013

Subsea/IMR Projects 103 87 323 888

Total consistent with management reporting 402 415 1 408 1 901

Reconciliation to equity method -110 -30 -273 -137

Total 292 385 1 135 1 764

| Financial Report Q4 2017DOF SUBSEA

17

Amounts in NOK million

Note 3 Financial income and expenses

4Q 2017 4Q 2016 2017 2016

Interest income 11 18 49 49

Other financial income 2 2 5 10

Financial income 13 20 55 59

Interest expenses -125 -115 -490 -484

Capitalisation of interest - - 3 -

Other financial expenses -7 -30 -34 -46

Financial expenses -132 -145 -521 -530

Net gain / loss on non-current debt 15 -92 -80 -161

Net gain / loss on operational capital -13 -9 -12 -

Net gain / loss on financial derivatives 6 2 11 -21

Net realised gain / loss on financial instruments 8 -98 -80 -181

Net unrealised gain / loss on non-current debt -145 -65 235 293

Net unrealised gain / loss on operational capital 2 5 -1 -22

Net unrealised gain / loss on financial derivatives -52 -133 54 201

Unrealised gain / loss on financial instruments -194 -193 288 473

Net financial income / loss -305 -417 -259 -179

Financial Report Q4 2017 | DOF SUBSEA

18

Amounts in NOK million

Note 4 Tangible assets

31 .12 .2017

Vessels & periodic maintenance

ROVs

Machinery & other equipment

Newbuilds

Total

Net booked value 01 .01 . 10 686 859 378 28 11 950

Additions 136 13 78 635 862

Vessel completed 498 - - -498 -

Disposals - -3 - - -3

Reclassification - 137 15 -154 -

Depreciation -328 -148 -87 - -563

Impairment -425 - - - -425

Currency translation differences -41 -2 -4 - -47

Net booked value 31 .12 . 10 525 856 381 11 11 773

31 .12 .2016

Net booked value 01 .01 . 11 990 963 455 7 13 425

Additions 380 12 73 53 517

Disposals -823 - -19 - -842

Reclassification - 43 -11 -32 -

Depreciation -335 -158 -97 - -590

Impairment -632 -5 -19 - -656

Currency translation differences 96 4 -3 - 97

Net booked value 31 .12 . 10 686 859 378 28 11 950

The challenging market conditions for offshore service vessels have continued. In the 4th quarter 2017, the Group faced lower market values for some of the Group`s vessels. Impairment indicators are observed, and an impairment test for vessels in the Group has been performed. Impairment tests are performed in line with accounting principles presented in the annual report for 2016. Impairments of NOK 64 million have been recognised in the 4th quarter of 2017. YTD 2017, the Group has recognised an impairment of NOK 425 million.

| Financial Report Q4 2017DOF SUBSEA

19

Amounts in NOK million

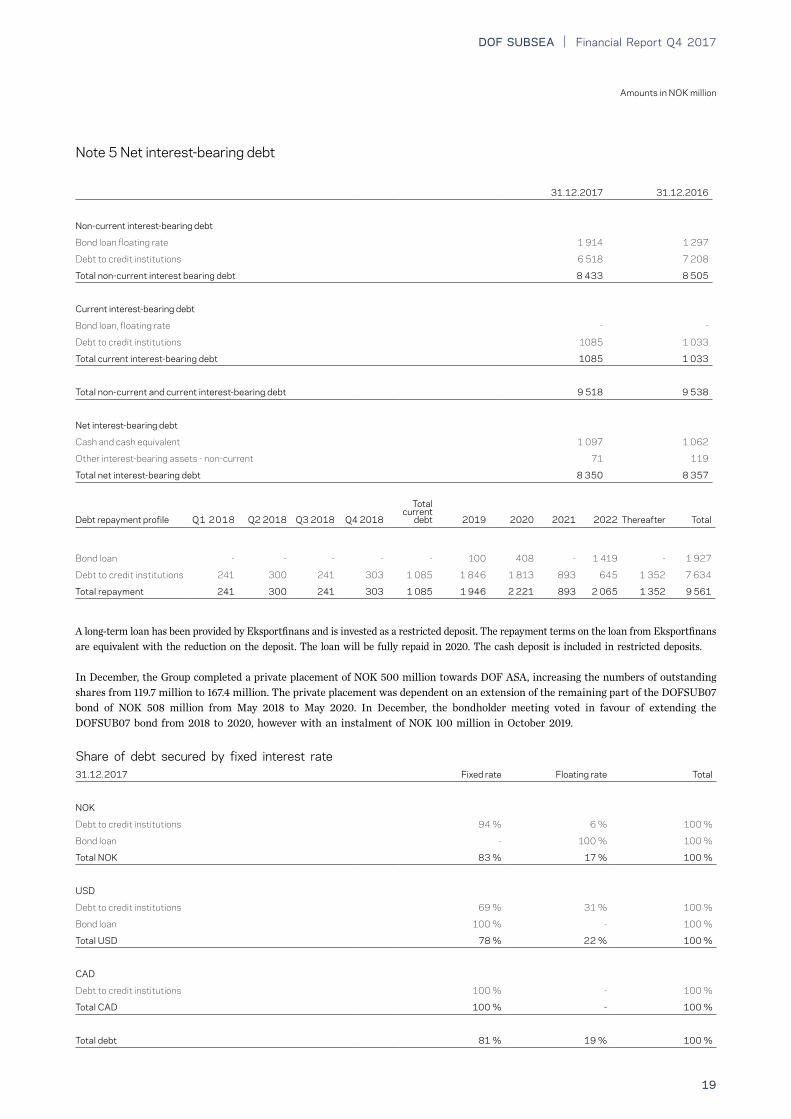

Note 5 Net interest-bearing debt

31 .12 .2017 31 .12 .2016

Non-current interest-bearing debt

Bond loan floating rate 1 914 1 297

Debt to credit institutions 6 518 7 208

Total non-current interest bearing debt 8 433 8 505

Current interest-bearing debt

Bond loan, floating rate - -

Debt to credit institutions 1085 1 033

Total current interest-bearing debt 1085 1 033

Total non-current and current interest-bearing debt 9 518 9 538

Net interest-bearing debt

Cash and cash equivalent 1 097 1 062

Other interest-bearing assets - non-current 71 119

Total net interest-bearing debt 8 350 8 357

Share of debt secured by fixed interest rate31 .12 .2017 Fixed rate Floating rate Total

NOK

Debt to credit institutions 94 % 6 % 100 %

Bond loan - 100 % 100 %

Total NOK 83 % 17 % 100 %

USD

Debt to credit institutions 69 % 31 % 100 %

Bond loan 100 % - 100 %

Total USD 78 % 22 % 100 %

CAD

Debt to credit institutions 100 % - 100 %

Total CAD 100 % - 100 %

Total debt 81 % 19 % 100 %

A long-term loan has been provided by Eksportfinans and is invested as a restricted deposit. The repayment terms on the loan from Eksportfinans are equivalent with the reduction on the deposit. The loan will be fully repaid in 2020. The cash deposit is included in restricted deposits.

In December, the Group completed a private placement of NOK 500 million towards DOF ASA, increasing the numbers of outstanding shares from 119.7 million to 167.4 million. The private placement was dependent on an extension of the remaining part of the DOFSUB07 bond of NOK 508 million from May 2018 to May 2020. In December, the bondholder meeting voted in favour of extending the DOFSUB07 bond from 2018 to 2020, however with an instalment of NOK 100 million in October 2019.

Debt repayment profile Q1 2018 Q2 2018 Q3 2018 Q4 2018

Total current

debt 2019 2020 2021 2022 Thereafter Total

Bond loan - - - - - 100 408 - 1 419 - 1 927

Debt to credit institutions 241 300 241 303 1 085 1 846 1 813 893 645 1 352 7 634

Total repayment 241 300 241 303 1 085 1 946 2 221 893 2 065 1 352 9 561

Financial Report Q4 2017 | DOF SUBSEA

20

Amounts in NOK million

Note 5 Interest-bearing debt (continued from previous page)

Note 6 Financial instruments and hedging activities

Financial covenantsThe Group’s long-term financing agreements include the following covenants: - The Group shall have available cash of at least NOK 500 million at all times - The Group shall have value-adjusted equity to value-adjusted assets of at least 30% - The Group shall have book equity of at least NOK 3 000 million at all times - The Group shall have positive working capital at all times, excl. short portion of debt to credit institutions - The fair value of the Group’s vessels shall always be at least 100-130% of the outstanding loan amount In addition to the above mentioned financial covenants, the loan agreements are also subject to the following covenants:- The Group’s assets shall be fully insured - There shall not be any change to classification, management or ownership of the ships without the prior written approval of the lenders- DOF ASA shall be the principal shareholder in DOF Subsea AS, and own a minimum of 50.1 % of the shares- DOF Subsea AS shall not merge or demerge activities without the prior written approval of the lenders - DOF Subsea AS shall report financial information to the lenders and Oslo Stock Exchange on a regular basis - The Group’s vessels shall be operated in accordance with applicable laws and regulations

The Group is in compliance with all covenants.

Assets

31 .12 .2017

Liabilities

Assets

31 .12 .2016

Liabilities

Non-current and current portion

Interest rate swaps - cash flow hedges 18 35 25 80

Foreign exchange contracts cash flow hedges 17 65 40 105

Total non-current and current 35 100 66 185

Non-current portion

Interest rate swaps - cash flow hedges 18 20 25 80

Foreign exchange contracts cash flow hedges 3 4 12 18

Total non-current portion 21 24 37 98

Total current portion 14 76 28 87

Committed Received

31 .12 .2017

Amount

Committed Received

31 .12 .2016

Amount

Instrument

Foreign exchange contracts, buy NOK NOK 2 225 NOK 3 214

| Financial Report Q4 2017DOF SUBSEA

21

Amounts in NOK million

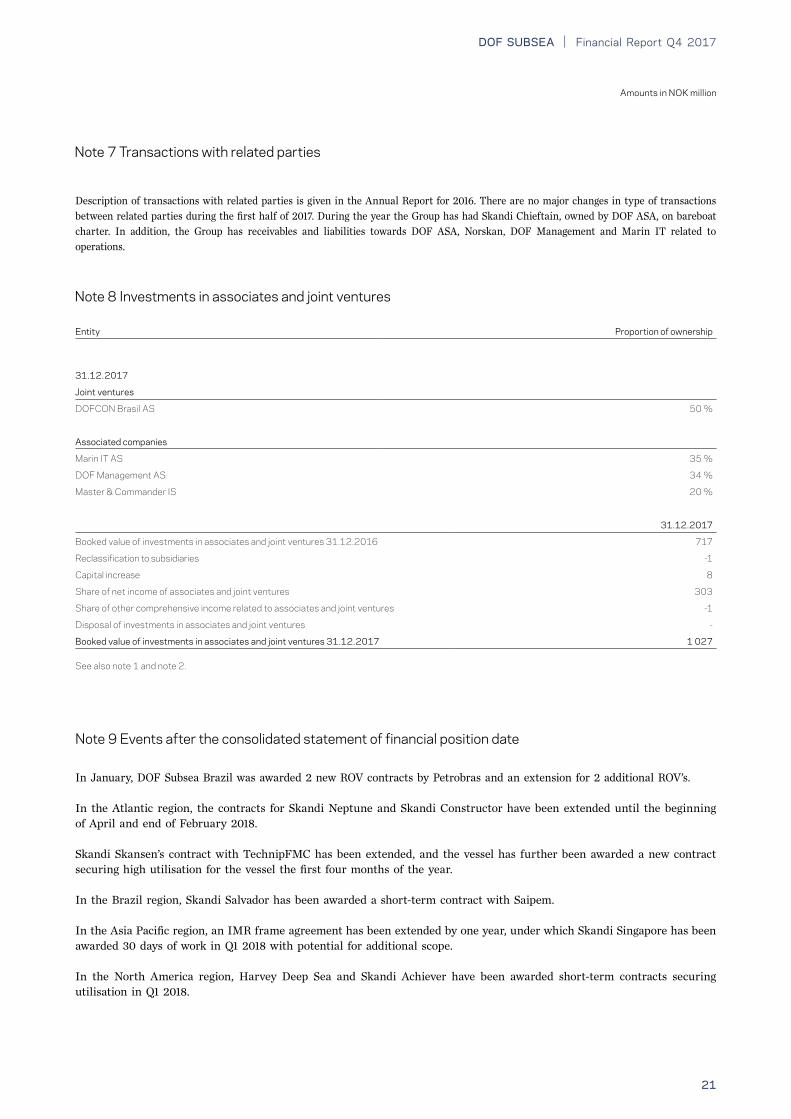

Note 8 Investments in associates and joint ventures

Entity Proportion of ownership

31 .12 .2017

Joint ventures

DOFCON Brasil AS 50 %

Associated companies

Marin IT AS 35 %

DOF Management AS 34 %

Master & Commander IS 20 %

31 .12 .2017

Booked value of investments in associates and joint ventures 31.12.2016 717

Reclassification to subsidiaries -1

Capital increase 8

Share of net income of associates and joint ventures 303

Share of other comprehensive income related to associates and joint ventures -1

Disposal of investments in associates and joint ventures -

Booked value of investments in associates and joint ventures 31 .12 .2017 1 027

See also note 1 and note 2.

Note 7 Transactions with related parties

Description of transactions with related parties is given in the Annual Report for 2016. There are no major changes in type of transactions between related parties during the first half of 2017. During the year the Group has had Skandi Chieftain, owned by DOF ASA, on bareboat charter. In addition, the Group has receivables and liabilities towards DOF ASA, Norskan, DOF Management and Marin IT related to operations.

Note 9 Events after the consolidated statement of financial position date

In January, DOF Subsea Brazil was awarded 2 new ROV contracts by Petrobras and an extension for 2 additional ROV’s.

In the Atlantic region, the contracts for Skandi Neptune and Skandi Constructor have been extended until the beginning of April and end of February 2018.

Skandi Skansen’s contract with TechnipFMC has been extended, and the vessel has further been awarded a new contract securing high utilisation for the vessel the first four months of the year.

In the Brazil region, Skandi Salvador has been awarded a short-term contract with Saipem.

In the Asia Pacific region, an IMR frame agreement has been extended by one year, under which Skandi Singapore has been awarded 30 days of work in Q1 2018 with potential for additional scope.

In the North America region, Harvey Deep Sea and Skandi Achiever have been awarded short-term contracts securing utilisation in Q1 2018.

Financial Report Q4 2017 | DOF SUBSEA

22

Amounts in NOK million

Note 10 Shareholder information

Name No . shares Shareholding Voting shares

DOF ASA 108 683 241 65 % 65 %

FRC Lux Holding Limited 51 131 358 31 % 31 %

Dolphin Invest 2 AS 7 538 163 5 % 5 %

Total 167 352 762 100 .0 % 100 .0 %

Note 11 General

This interim report has been prepared in accordance with the standard for interim reporting (IAS 34). The accounting principles and calculation methods applied for the latest published annual accounts have been applied to the quarterly financial report. Amendments and interpretations to the standards which are effective for the financial year beginning on 1 January 2017 are not material to the Group. The Financial Statement is unaudited.

IFRS 15 Revenue from contracts with customers - effective from 1 January 2018The new standard is based on the principle that revenue is recognised when control of goods or service transfers to a customer - the notion of control replaces the existing notion of risks and rewards.

The Group has finalised an internal project regarding the implementation of IFRS 15 Revenue from contracts with customers. The main purpose of the project was to assess the impact of applying the new standard on the Group’s Financial Statements to ensure a good implementation process. All contracts ongoing at year-end are evaluated based on the five step model described in IFRS 15 Revenue from contracts with customers. The purpose of the evaluation was to identify the effect on the equity 1 January 2018. In addition, all types of contracts within the different revenue streams are evaluated on a general basis to determine the effects of the implementation in 2018. As part of the project the Group’s revenue streams has been categorised into the following types: Time Charter revenue and Project revenue.

Time Charter revenue is based on contracts wehre the Group delivers a vessel (including crew) to the client. During the contract period, the client decides how and when to operate the vessel. Based on existing IFRS, and after the implementation of IFRS 15 Revenue from contracts with customers, this revenue stream is recognised over time. The Time Charter revenue will be affected by the implementation of IFRS 15 Revenue from contracts with customers and the bareboat element will be recognised as lease revenue based on IFRS 16 Leases. Result of the assessment is that the timing of the revenue recognition under IFRS 15 Revenue from contracts with customers and IFRS 16 Leases will be the same as under IAS 18 Revenue and IAS 17 Leases.

Project revenue is based on operations where the Group utilises its vessels, equipment and crew to perform tailor made operations on the client’s installations, assets etc. Based on existing IFRS this revenue is recognised over time. Result of the assessment is that the timing of the revenue recognition under IFRS 15 Revenue from contracts with customers will be the same as under IAS 18 Revenue/IAS 11 Construction contracts.

A reverse merger was executed during the quarter effective 1 January 2017 between DOF Subsea AS and DOF Subsea Holding AS. This resulted in DOF Subsea Holding AS being absorbed into DOF Subsea AS, thus changes in the shareholders.

In December the Group made a private placement of NOK 500 million towards DOF ASA, increasing the numbers of outstanding shares from 119.7 million to 167.4 million.

| Financial Report Q4 2017DOF SUBSEA

23

Amounts in NOK million

Despite no change in the main recognition method, the Group has identified that the following areas might be affected going forward: - The application of IFRS 15 Revenue from contracts with customers may result in identification of several separate performance obligations, which could affect the timing of revenue recognition in relation to the separate performance obligations. - Certain costs will be recognised as a contract asset under IFRS 15 Revenue from contracts with customers with additional disclosures. Under existing IFRS, contract assets are not separated from other assets. - Parts of the Time charter revenue might be recognised as lease revenue based on IAS 17 Leases/IFRS 16 Leases.

The Group will apply IFRS 15 Revenue from contracts with customers retrospectively with the cumulative effect of initial application recognised as an adjustment to equity as of 1 January 2018. This transition method will only be applied retrospectively on contracts that are not completed by 1 January 2018. Based on the assessment the Group does not expect any adjustment to the equity as of 1 January 2018.

IFRS 9 Financial instruments - effective from 1 January 2018IFRS 9 Financial instruments addresses the classification, measurement and de-recognition of financial assets and financial liabilities and introduces new rules for hedge accounting. The Group does not use hedge accounting as of 4th quarter 2017, and the Group does not intend to use hedge accounting in 2018. The implementation might cause a minor effect on the equity as of 1 January 2018, due to the modification of the remaining part of the DOFSUB07 bond loan in December 2017. The Group does not expect any material effects on the equity as of 1 January 2018.

IFRS 16 Leases - mandatory from 1 January 2019The new standard will result in almost all leases being recognised in the statement of financial position, as the distinction between operating and finance leases is removed. Under the standard, an asset (the right to use a leased item) and a financial liability (the obligation to pay rentals) are recognised. The only exceptions of this recognition principle are short-term and low-value leases.

As of 31 December 2017, the Group has three vessels on lessee arrangements which are presented as operating leases. One of the agreements is for less than 12 months. Furthermore, the Group has and will have lease agreements on office buidlings and warehouses that will be affected by implementation of IFRS 16 Leases. Yearly lease fee for the Group’s office buildings and warehouses are approximately NOK 50 million. At the moment some lease agreements are longer than 12 months and some lease agreements are shorter than 12 months. It is expected that the composition of long- and short-term lease agreements can be changed before implementation of IFRS 16 Leases. For further information about DOF Subsea offices, see Annual Report of 2016.

For the Group as a lessor, expected impacts on revenue are related to presentation, classification and notes to the Financial Statements.

The Group does not intend to adopt the standard before its effective date, 1 January 2019.

Note 11 General (continued from previous page)

Financial Report Q4 2017 | DOF SUBSEA

24

Amounts in NOK million

Operating profit before depreciation (EBITDA)Operating profit before depreciation (EBITDA) is defined as operating profit, including profit from sale of non-current assets, before impairment of tangible and intangible assets, depreciation of tangible assets and amortisation of contract assets. EBITDA represents earnings before interest, tax, depreciation and amortisation, and is a key financial parameter for the Group. This measure is useful in evaluating operating profitability on a more variable cost basis as it excludes depreciation, impairment and amortised expenses related primarily to capital expenditures and acquisitions that occurred in the past. The EBITDA margin presented is defined as EBITDA divided by operating income.

Operating profit (EBIT)Operating profit (EBIT) represents earnings before interest and tax, and is a common non-IFRS measure to assess profitability before financial income and loss items and tax expenses.

Net interest-bearing debt Net interest-bearing debt consists of both current and non-current interest-bearing liabilities less interest bearing financial assets and cash and cash equivalents. Non-current receivables from joint ventures are not included in net interest-bearing debt. Cash and cash equivalents will include restricted cash. Current interest-bearing debt includes interest-bearing debt related to asset held for sale. Net interest-bearing debt is a measure of the Group’s net indebtedness that provides an indicator of the overall statement.

Equity ratioEquity ratio is defined as total equity divided by total assets at the reporting date.

Market valueCalculated average vessel value between two independent brokers’ estimates based on the principle of “willing buyer and willing seller”.

Vessel utilisation Vessel utilisation is a measure of the Group`s ability to keep vessels in operation and on contracts with clients, expressed as a percentage. The vessel utilisation numbers are based on actual available days, including yard-stay days for dry-docking, repairs and upgrade/conversion, transits and idle time between subsea/IMR projects and long-term chartering contracts.

Contract backlog Sum of undiscounted revenue related to secured contracts in the future and optional contract extensions as determined by the client in the future. Contract backlog excludes master service agreements (MSAs) within the Subsea/IRM Projects segment. Under the MSAs only confirmed POs are included.

Firm contract backlog Sum of undiscounted revenue related to secured contracts in the future. Secured contracts are contracts signed with clients in the past, covering future delivery of services.

Backlog optionsSum of undiscounted revenue related to optional contract extensions as determined by the client in the future.

Working capitalThe working capital position of the Group is equal to current assets less current liabilities. It is a measure of the Group’s liquidity and efficiency, and demonstrates the Group’s ability to pay its current liabilities.

Note 12 Performance measurement definitions

| Financial Report Q4 2017DOF SUBSEA

25

Financial Report Q4 2017 | DOF SUBSEA

26

Amounts in NOK million

Supplemental information

Condensed statement of comprehensive income 5 last quarters

4Q 2017 3Q 2017 2Q 2017 1Q 2017 4Q 2016

Operating income 1 275 1 093 1 199 982 1 128

Payroll expenses -381 -363 -337 -360 -376

Other operating expenses -494 -395 -466 -350 -430

Share of net income of associates and joint ventures 2 -3 3 7 -3

Profit from sale of non-current assets - - -4 -1 96

Total operating expenses -872 -762 -804 -704 -713

Operating profit before depreciation (EBITDA) 402 332 396 278 415

Depreciation and impairment -231 -352 -233 -288 -396

Operating profit (EBIT) 172 -21 163 -10 19

Financial income 5 - 15 8 14

Financial expenses -193 -151 -170 -137 -161

Realised gain / loss on financial instruments 8 24 -64 -47 -106

Unrealised gain / loss on financial instruments -195 260 136 83 -149

Net financial income / loss -374 133 -83 -93 -402

Profit / loss before tax -203 112 80 -103 -383

Tax expenses -173 26 8 -21 -47

Profit / loss for the period -375 138 88 -124 -430

The supplemental information below is presented according to internal management reporting, based on the proportionate consolidation method. Proportionate consolidation method implies full consolidation for subsidiaries, and consolidation of 50% of the comprehensive income and financial position for the joint ventures.

| Financial Report Q4 2017DOF SUBSEA

27

Amounts in NOK million

Condensed statement of financial position 5 last quarters

Assets 4Q 2017 3Q 2017 2Q 2017 1Q 2017 4Q 2016

Intangible assets 673 794 797 717 714

Tangible assets 16 397 16 365 16 857 16 556 16 530

Financial assets 758 767 774 814 799

Non-current assets 17 829 17 926 18 428 18 087 18 043

Total receivables 1 338 1 293 1 235 1 115 1 294

Cash and cash equivalents 1 269 1 208 1 360 1 693 1 189

Current assets 2 607 2 501 2 595 2 808 2 483

Total assets 20 436 20 427 21 023 20 896 20 526

Equity and liabilities 4Q 2017 3Q 2017 Q2 2017 1Q 2017 4Q 2016

Paid in equity 4 344 3 844 3 844 3 844 3 844

Other equity 1 778 2 086 2 002 1 877 1 987

Non-controlling interests 226 226 225 227 224

Total equity 6 348 6 156 6 071 5 948 6 055

Non-current provisions for commitment 18 14 21 23 21

Other non-current liabilities 11 629 11 206 11 921 12 480 11 972

Non-current liabilities 11 648 11 221 11 942 12 503 11 993

Current portion of debt to credit institutions 1 498 1 991 2 035 1 464 1 372

Other current liabilities 942 1 060 975 981 1 106

Current liabilities 2 440 3 051 3 010 2 444 2 478

Total liabilities 14 088 14 271 14 952 14 947 14 471

Total equity and liabilities 20 436 20 427 21 023 20 896 20 526

Key figures

4Q 2017 3Q 2017 2Q 2017 1Q 2017 4Q 2016

Profit per share (NOK) -2.24 0.12 0.74 -1.04 -3.59

EBITDA margin 32 % 30 % 33 % 28 % 37 %

EBIT margin 13 % -2 % 14 % -1 % 2 %

Return on net capital -6 % 2 % 1 % -2 % -7 %

Book value equity per share (NOK) 37.93 51.41 50.70 49.68 50.58

Value-adjusted equity per share (NOK) 44.73 58.60 60.21 59.22 61.25

Net interest-bearing debt (NOK million) 11 822 11 914 12 529 12 206 12 041

Financial Report Q4 2017 | DOF SUBSEA

28

DOF Subsea currently owns one of the largest fleet of high-end construction vessels (including newbuilds) in the world. These assets offer a versatile, new generation of high-powered and purpose-built vessels with broad offshore capabilities.

Owned vessels

Skandi Acergy

Geograph Geoholm Geosea

Geosund

Skandi Carla Skandi Constructor

Skandi Achiever

Skandi Hawk

Skandi Africa Skandi BuziosSkandi Açu

DOF Subsea vessels

| Financial Report Q4 2017DOF SUBSEA

29

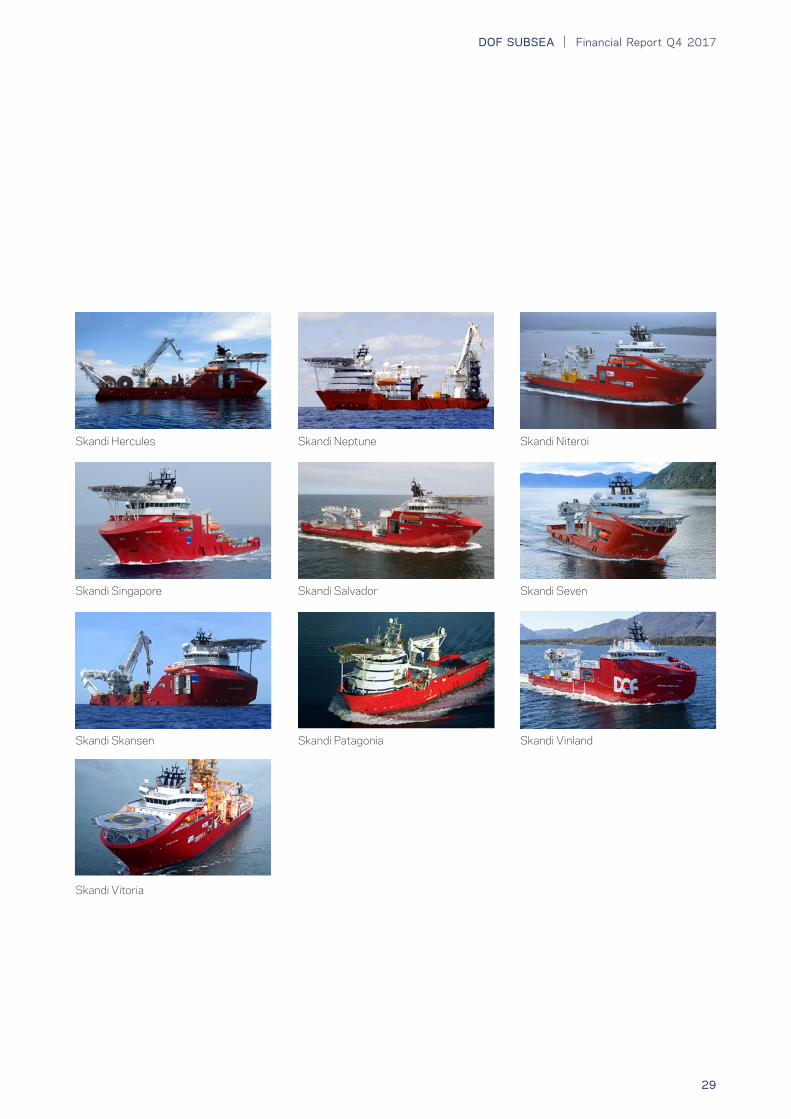

Skandi Skansen Skandi Patagonia

Skandi Vitoria

Skandi Salvador Skandi SevenSkandi Singapore

Skandi Neptune Skandi NiteroiSkandi Hercules

Skandi Vinland

Financial Report Q4 2017 | DOF SUBSEA

30

Harvey Deep Sea

DOF Subsea invests in the next generations of vessels. An ambitious Newbuild program utilises new technology and smart engineering to ensure efficient and environmentally-friendly operations in the future.

Newbuilds in joint ventures and associated companies

Chartered-in vessels

DOF Subsea charters in vessels on short and long-term contracts based on operational needs, building greater flexibility and a complementary fleet mix to meet our clients’ subsea challenges.

Skandi Olinda Skandi Recife

Skandi ChieftainSkandi Darwin

DOF Subsea vessels (continued)

AUSTRALIA

DOF Subsea Australia Pty Ltd5th Floor, 181 St. Georges TcePerth, Wa 6000 AUSTRALIAPhone: +61 8 9278 8700Fax: +61 8 9278 8799

DOF Management Australia5th Floor, 181 St. Georges TcePerth, Wa 6000 AUSTRALIAPhone: +61 3 9556 5478Mobile: +61 418 430 939

BRAZIL

DOF Subsea Brasil Serviços LtdaRua Fiscal Juca, 330 Q: W2 – L: 0001 Loteamento Novo Cavaleiros Vale Encantado – Macaé/RJ BRAZIL - CEP 27933-450 Rio address: Rua Lauro Muller 116, 17 andar Torre do Rio Sul - Botafogo Rio de Janeiro, R.J. BRAZIL - CEP: 22290-160 Phone: +55 22 2123-0100 Fax: +55 22 2123-0199

CANADA

DOF Subsea Canada26 Allstone Street, Unit 2Mount Pearl, NewfoundlandCANADA, A1N 0A4Phone: +1 709 576 2033Fax: +1 709 576 2500

SINGAPORE

DOF Subsea Asia Pacific Pte Ltd460 Alexandra Road# 15-02PSA Building, 119963SINGAPOREPhone: +65 6561 2780Fax: +65 6561 2431

GLOBAL HQ

DOF Subsea ASThormøhlensgate 53 C5006 Bergen NORWAYPhone: +47 55 25 22 00Fax: +47 55 25 22 01

NORWAY

DOF Subsea Norway ASThormøhlensgate 53 C5006 Bergen NORWAYPhone: +47 55 25 22 00Fax: +47 55 25 22 01

SEMAR ASOksenøystein 121366 Lysaker NORWAYPhone: +47 67 12 40 06Fax: +47 67 12 40 06

DOF Management ASAlfabygget5392 StorebøNORWAY

Thormøhlensgate 53 C5006 Bergen NORWAYPhone: +47 56 18 10 00Fax: +47 56 18 10 06

ANGOLA

DOF Subsea AngolaBelas Business Park-Talatona Edificio Bengo, 1º AndarSala 106/107, LuandaRepublic of AngolaPhone: +244 222 43 28 58Fax: +244 222 44 40 68Mobile: +244 227 28 00 96 +244 277 28 00 95

DOF Management Pte Ltd460 Alexandra Road# 15-02PSA Building, 119963SINGAPOREPhone: +65 6868 1001Fax: +65 6561 2431

UNITED KINGDOM

DOF Subsea UK LtdHorizons House, 81-83 Waterloo Quay Aberdeen, AB11 5DE UNITED KINGDOMPhone: +44 1224 614 000Fax: +44 1224 614 001

DOF Subsea S&P UK LtdHorizons House, 81-83 Waterloo Quay Aberdeen, AB11 5DE UNITED KINGDOMPhone: +44 1224 614 000Fax: +44 1224 614 001

CSL EngineeringHorizons House, 81-83 Waterloo Quay Aberdeen, AB11 5DE UNITED KINGDOMPhone: +44 1224 285 566Fax: +44 1224 285 599

DOF (UK) LtdHorizons House, 81-83 Waterloo Quay Aberdeen, AB11 5DE UNITED KINGDOMPhone: +44 12 24 58 66 44Fax: +44 12 24 58 65 55

USA

DOF Subsea USA Inc5365 W. Sam Houston Parkway Suite 400, Houston, Texas 77041, USAPhone: +1 713 896 2500Fax: +1 713 726 5800

DOF Subsea ASThormøhlens gate 53 C

5006 BergenNORWAY

www.dofsubsea.com

Rep

ort

desi

gn: D

OF

Cor

pora

te C

omm

unic

atio

n D

epar

tmen

t