Embed Size (px)

Citation preview

Q3 2013 Roadshow Presentation

2222

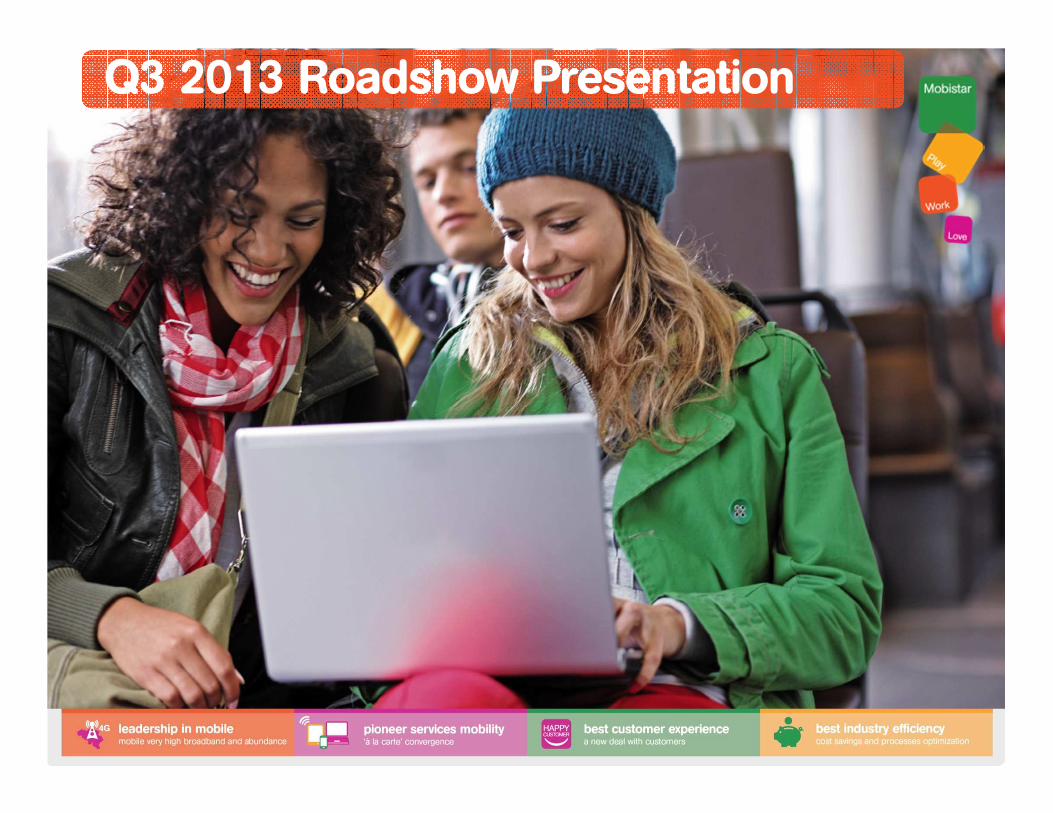

� ARPU: ARPU: ARPU: ARPU: Monthly average revenue per user is based on a rolling 12 months average taking into consideration total Incoming & outgoing revenues voice, SMS and MMM, visitor roaming ( excl.:MatMa, MVNO, IFRS, MBB )

� AUPUAUPUAUPUAUPU: Monthly average usage per user, defined as total usage for the 12 previous months divided by the weighted average number of customers

� M2MM2MM2MM2M: =Machine-to-machine = M2M cards are not included in the number of active customers

� MobileMobileMobileMobile MultimediaMultimediaMultimediaMultimedia: (MMM): Wireless high-speed internet access on handset devices

� MobileMobileMobileMobile broadbandbroadbandbroadbandbroadband (MBB): Wireless high-speed internet access through a portable modem / card, on tablets, netbooks, notebooks and laptops. (Internet Everywhere)

� MVNOMVNOMVNOMVNO: Mobile Virtual Network Operator. These are operators that do not have their own radio network and thus use the infrastructure of third-party networks.

� MTR: MTR: MTR: MTR: Mobile Termination Rate is the per minute charge paid by a telecommunications network operator when a customer makes a call to another mobile network operator

� MNPMNPMNPMNP: mobile number portability allows mobile customers to keep their mobile numbers when they change operators. The donor operator deactivates the mobile number in its information system; the recipient operator actives the same mobile number in its own

� NPSNPSNPSNPS (Net Promoter Score): A measure of customer loyalty. It is obtained by asking customers a single question on a scale of 0 to 10 where 10 is 'extremely likely' and 0 is 'not likely at all’.

� Operational Operational Operational Operational cashcashcashcash----flowflowflowflow: Corresponds to restated EBITDA minus CAPEX. Mobistar uses this indicator to measure the Group’s performance in generating cash flow from its operating activities.

DefinitionsDefinitionsDefinitionsDefinitions

3333

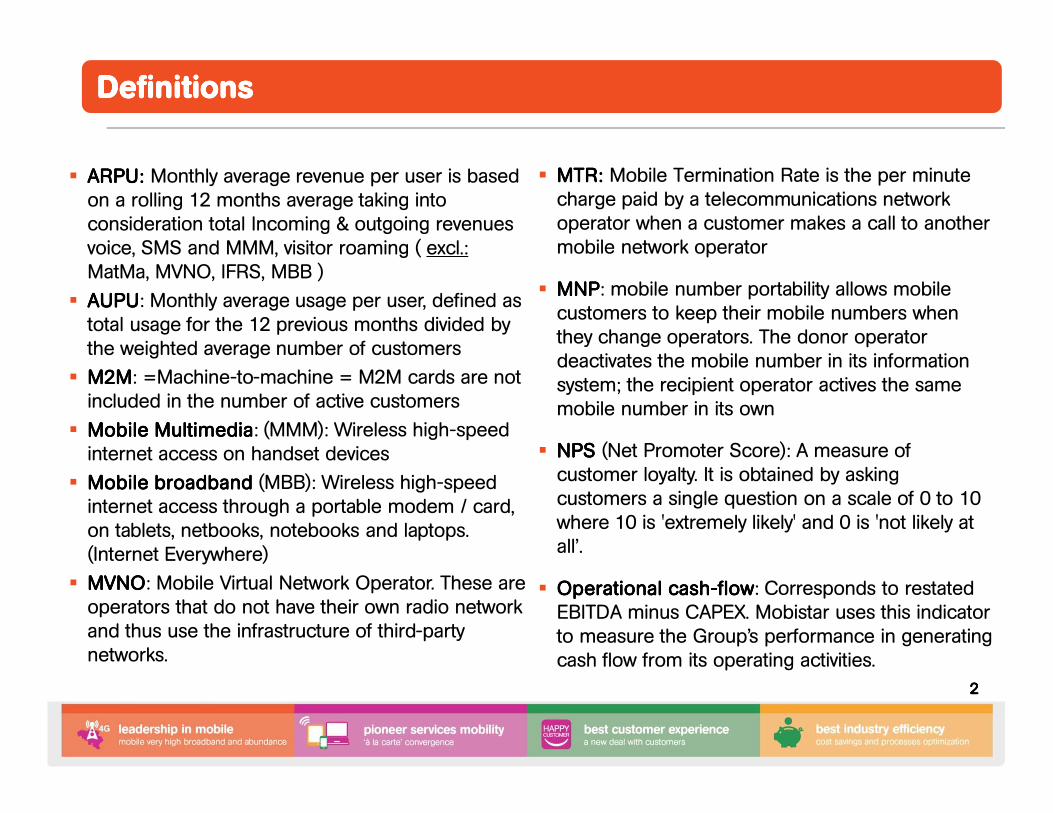

This presentation contains forward-looking statements about Mobistar, inparticular for 2013 and 2014. Although Mobistar believes these statements arebased on reasonable assumptions, these forward-looking statements are subjectto numerous risks and uncertainties, including matters not yet known to us or notcurrently considered material by us, and there can be no assurance thatanticipated events will occur or that the objectives set out will actually beachieved. Important factors that could cause actual results to differ materiallyfrom the results anticipated in the forward-looking statements include, amongothers, the impact of the price adjustments on the customer base resulting fromthe competitive pressure and the economic situation in Belgium, the accelerationof the efficiency programs which aims at a structural net savings of the cost baseof Mobistar from 30 to 50 million euro net as of 2014, the effectiveness ofMobistar convergent strategy including the success and market acceptance ofthe voice and date abundance plans, the Mobistar TV offers, the Mobistar brandand other strategic, operating and financial initiatives, Mobistar’s ability to adapt tothe on-going transformation of the telecommunications industry, regulatorydevelopments and constraints and the outcome of legal proceedings, risks anduncertainties related to business activity.

Cautionary StatementCautionary StatementCautionary StatementCautionary Statement

4444

• Key Highlights

• Operating Results

• Topics in the Spotlight

• Financial Review

• Outlook 2013

Jean Marc Jean Marc Jean Marc Jean Marc HarionHarionHarionHarionChief Executive Officer

Siddy Siddy Siddy Siddy JobeJobeJobeJobeDirector Investor Relations& Corporate Finance

Ludovic Ludovic Ludovic Ludovic PechPechPechPechChief Financial Officer

Agenda

5555

KEY QUARTERLY HIGHLIGHTSEconomic Indicators

Q3 Market Review

Company Highlights

Strategic priorities

6666

GDP growth, quarter-on-quarter Unemployment rate, monthly data

Inflation, monthly data Sectorial Surveys, Confidence Ind.

Jul-

12

Jan

-10

Mar

-11

Jul-

11

Mar

-12

No

v-1

1

Se

p-1

0

No

v-1

2

Mar

-13

May

-11

Mar

-10

May

-12

Se

p-1

3

May

-10

Jul-

10

Jan

-13

Se

p-1

2

Jan

-11

No

v-1

0

Jan

-12

Se

p-1

1

9,0%

8,5%

8,0%

7,5%

7,0%

6,5%

May

-13

Jul-

13

8,7%

7,2%7,4%

0,0%

-0,5%

0,5%

1,0%

1Q

13

0,0%

4Q

12

-0,1%

3Q

12

0,0%

2Q

12

-0,5%1

Q1

2

0,2% 0,2%

4Q

11

-0,1%3

Q1

10,0%

2Q

11

0,2%

1Q

11

0,8%4

Q1

0

0,5%

3Q

10

0,5%

2Q

10

1,0%

1Q

10

0,1%

2Q

13

Jul-

10

May

-11

Jan

-10

No

v-1

0

Mar

-12

Mar

-10

Jul-

11

No

v-1

1

Mar

-11

May

-12

1,5

2,0S

ep

-13

0,0

Se

p-1

2

May

-13

2,5

0,5

No

v-1

2

Jan

-13

Jul-

12

Mar

-13

1,0

5,0%

4,0%

3,0%

2,0%

1,0%

0,0%

May

-10

Jul-

13

Se

p-1

1

Jan

-12

Jan

-11

Se

p-1

0

1,80%

1,10%

2,1

0%

1,80%

Core inflation

Headline inflation

-30

-20

-10

0

10

20

30

40

Mar

-13

De

c-1

2

Se

p-1

2

Jun

-12

Mar

-12

De

c-1

1

Se

p-1

1

Jun

-11

Mar

-11

De

c-1

0

Se

p-1

0

Jun

-10

Mar

-10

Jun

-13

Se

p-1

3

Services

Consumers

Retail trade

Construction

Industry

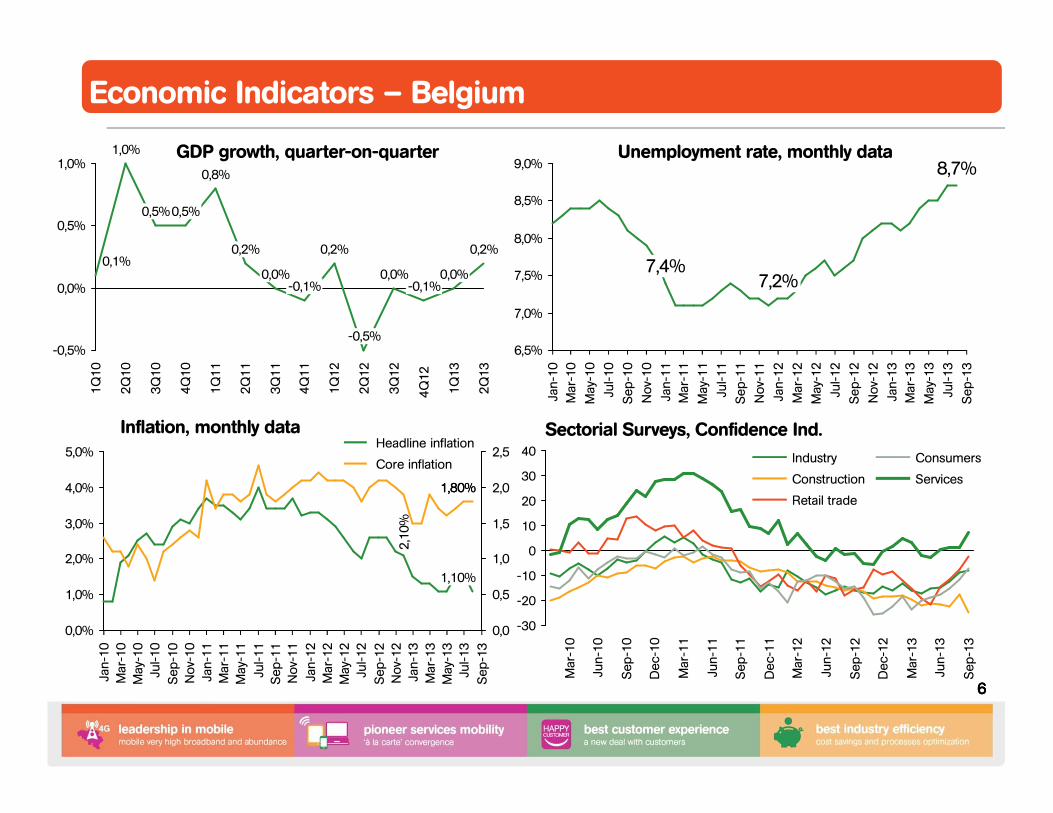

Economic Indicators – Belgium

7777

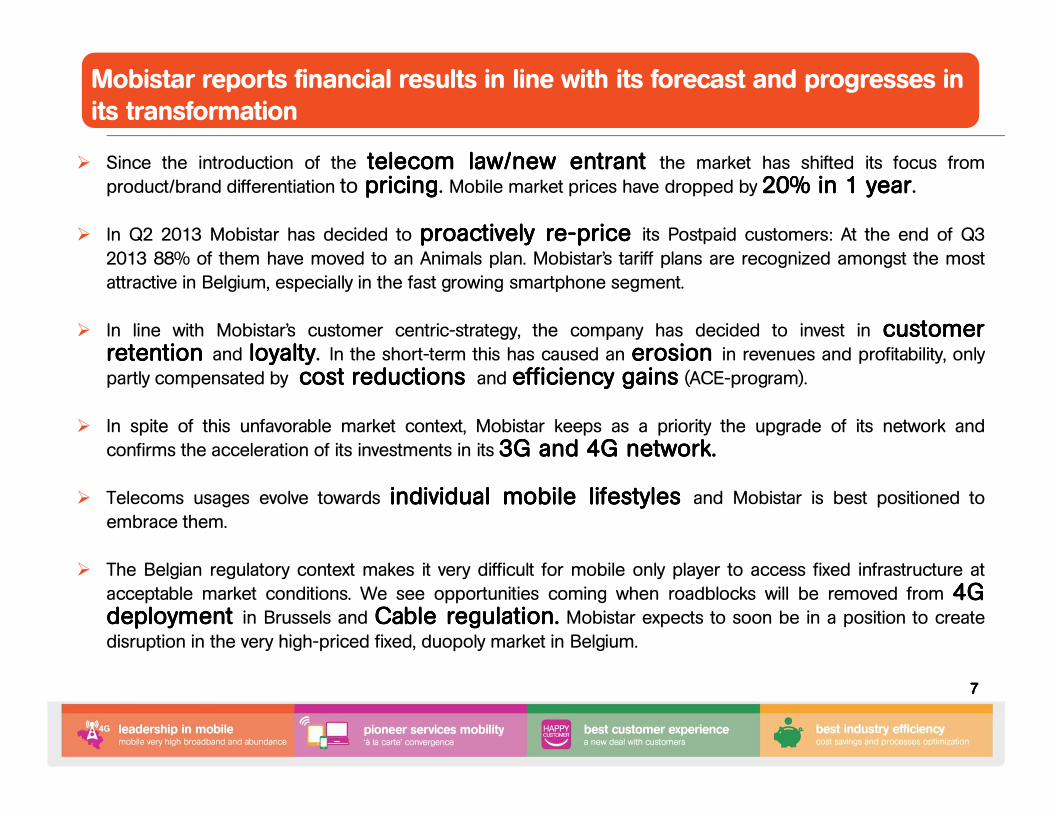

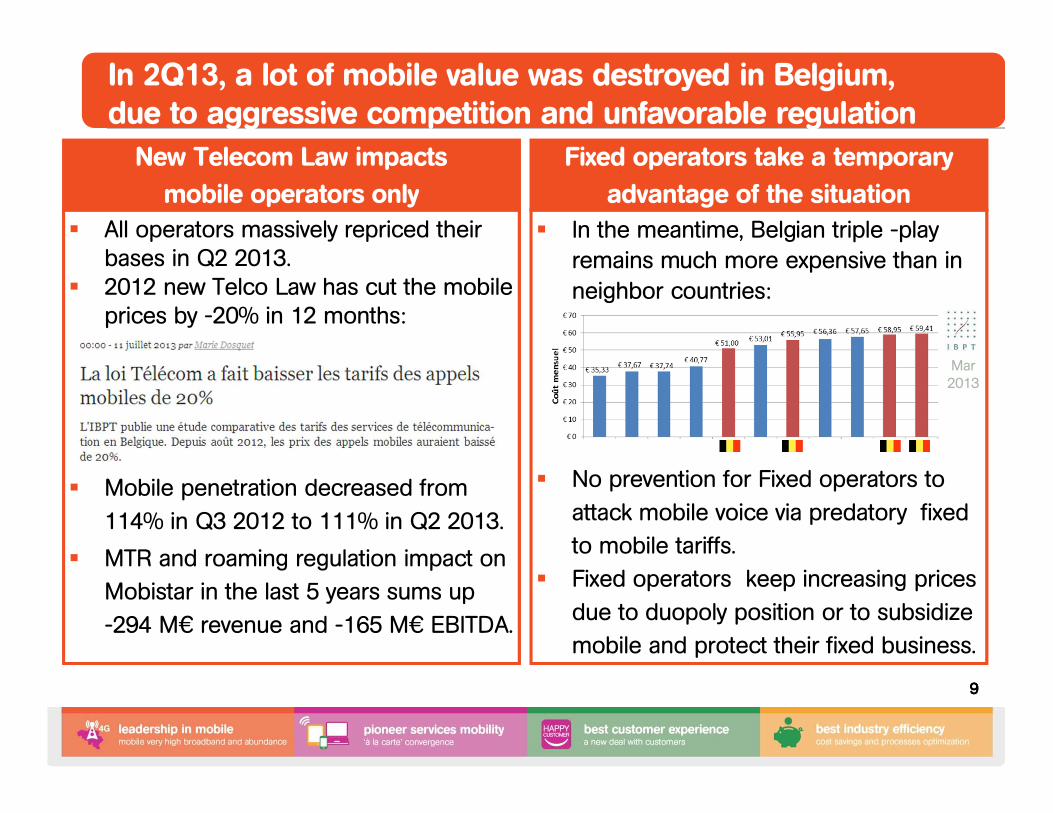

� Since the introduction of the telecomtelecomtelecomtelecom law/newlaw/newlaw/newlaw/new entrantentrantentrantentrant the market has shifted its focus from

product/brand differentiation to pricingpricingpricingpricing. Mobile market prices have dropped by 20202020%%%% inininin 1111 yearyearyearyear.

� In Q2 2013 Mobistar has decided to proactivelyproactivelyproactivelyproactively rererere----pricepricepriceprice its Postpaid customers: At the end of Q3

2013 88% of them have moved to an Animals plan. Mobistar’s tariff plans are recognized amongst the most

attractive in Belgium, especially in the fast growing smartphone segment.

� In line with Mobistar’s customer centric-strategy, the company has decided to invest in customercustomercustomercustomerretentionretentionretentionretention and loyaltyloyaltyloyaltyloyalty. In the short-term this has caused an erosionerosionerosionerosion in revenues and profitability, only

partly compensated by costcostcostcost reductionsreductionsreductionsreductions and efficiencyefficiencyefficiencyefficiency gainsgainsgainsgains (ACE-program).

� In spite of this unfavorable market context, Mobistar keeps as a priority the upgrade of its network and

confirms the acceleration of its investments in its 3333GGGG andandandand 4444GGGG networknetworknetworknetwork....

� Telecoms usages evolve towards individualindividualindividualindividual mobilemobilemobilemobile lifestyleslifestyleslifestyleslifestyles and Mobistar is best positioned to

embrace them.

� The Belgian regulatory context makes it very difficult for mobile only player to access fixed infrastructure at

acceptable market conditions. We see opportunities coming when roadblocks will be removed from 4444GGGGdeploymentdeploymentdeploymentdeployment in Brussels and CableCableCableCable regulationregulationregulationregulation.... Mobistar expects to soon be in a position to create

disruption in the very high-priced fixed, duopoly market in Belgium.

Mobistar reports financial results in line with its forecast and progresses in its transformation

8888

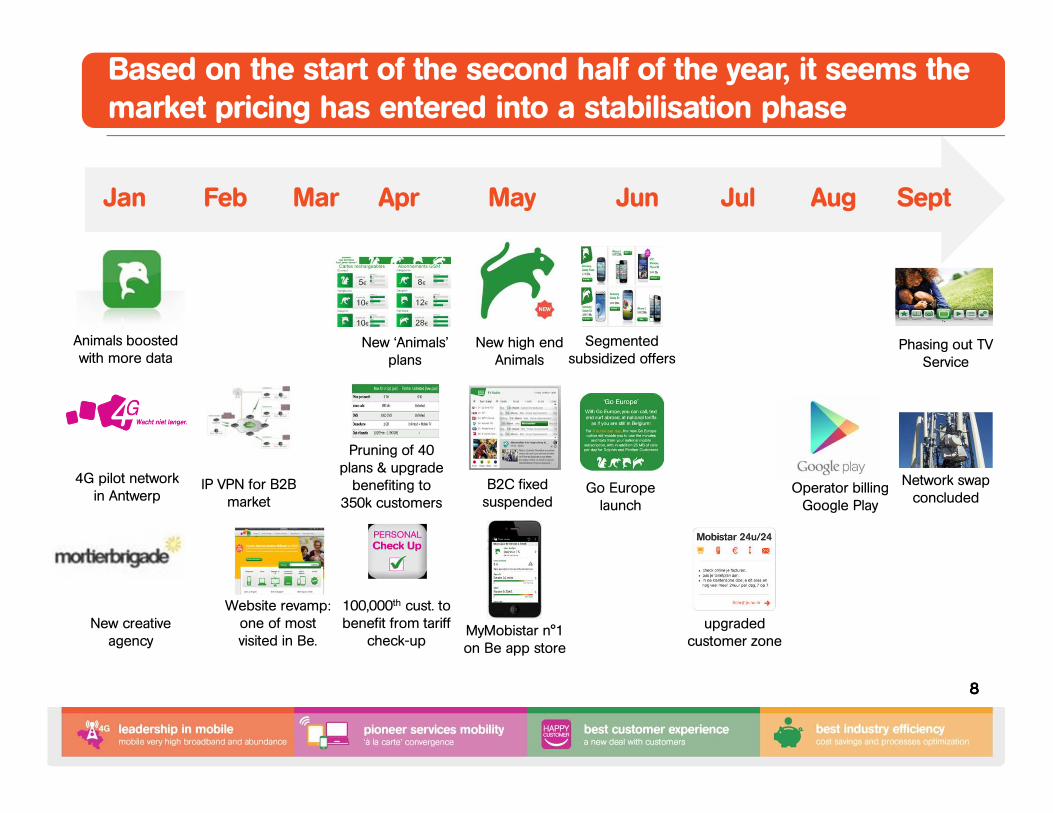

Based on the start of the second half of the year, it seems the market pricing has entered into a stabilisation phase

Apr May JunJan Feb Mar

New ‘Animals’ plans

Segmented subsidized offers

New high end Animals

Animals boostedwith more data

IP VPN for B2B market

Go Europe launch

B2C fixed suspended

Pruning of 40 plans & upgrade

benefiting to 350k customers

New creative agency

Website revamp: one of most visited in Be.

100,000th cust. to benefit from tariff

check-upMyMobistar n°1 on Be app store

4G pilot network in Antwerp

Jul Aug Sept

Network swap concluded

Phasing out TV Service

upgraded customer zone

Operator billing Google Play

� In the meantime, Belgian triple -play remains much more expensive than in

neighbor countries:

� No prevention for Fixed operators to

attack mobile voice via predatory fixed

to mobile tariffs.

� Fixed operators keep increasing prices

due to duopoly position or to subsidize

mobile and protect their fixed business.

Telco Law has cut the mobile

EBITDA.

� All operators massively repriced their bases in Q2 2013.

� 2012 new Telco Law has cut the mobile prices by -20% in 12 months:

� Mobile penetration decreased from

114% in Q3 2012 to 111% in Q2 2013.

� MTR and roaming regulation impact on

Mobistar in the last 5 years sums up

-294 M€ revenue and -165 M€ EBITDA.

Mar 2013

9999

In 2Q13, a lot of mobile value was destroyed in Belgium,due to aggressive competition and unfavorable regulation

Fixed operators take a temporary

advantage of the situation

New Telecom Law impacts

mobile operators only

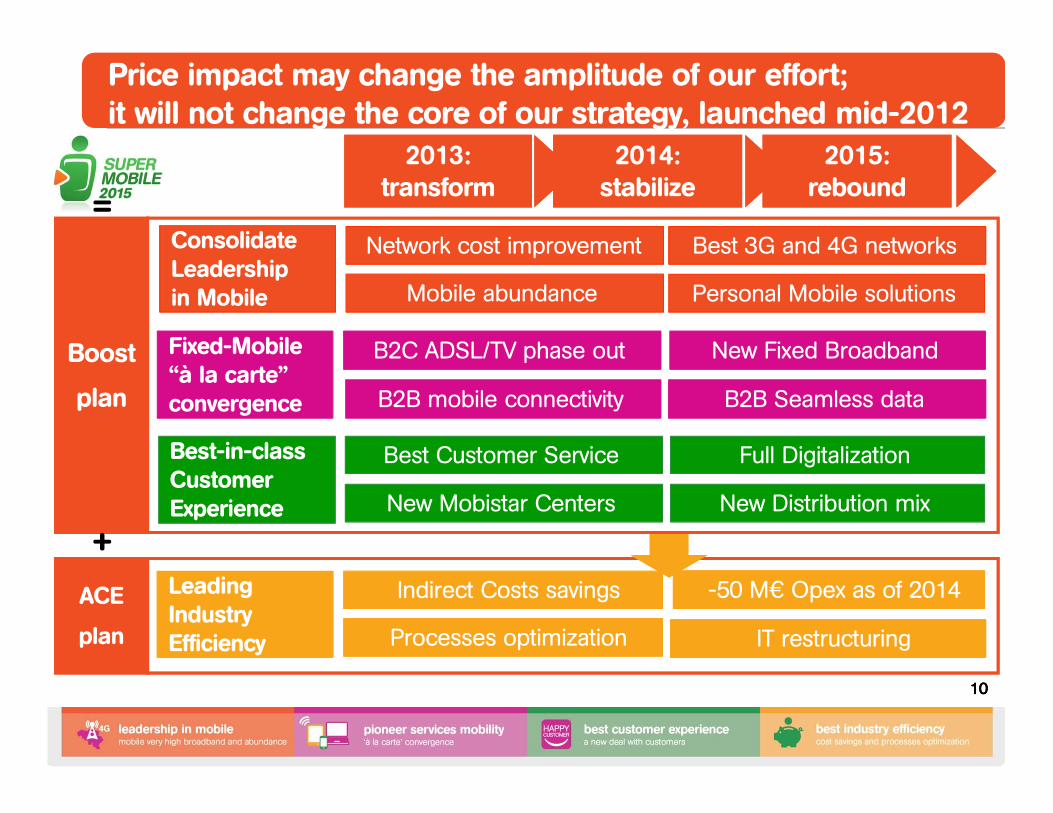

Processes optimization

-50 M€ Opex as of 2014

10101010

Price impact may change the amplitude of our effort;it will not change the core of our strategy, launched mid-2012

IT restructuring

Indirect Costs savings

Efficiency

LeadingIndustry Efficiency

Best 3G and 4G networks

Mobile abundance

Best Customer Service

New Mobistar Centers

New Fixed Broadband

B2B mobile connectivity

Network cost improvement

New Distribution mix

B2C ADSL/TV phase out

B2B Seamless data

Full Digitalization

Personal Mobile solutions

Boost

plan

ACE

plan

+

Best-in-class Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

2013:transform

2014:stabilize

2015:rebound

=

ACE 2: 50 M€ structural costs reduction secured as of 2014

11111111

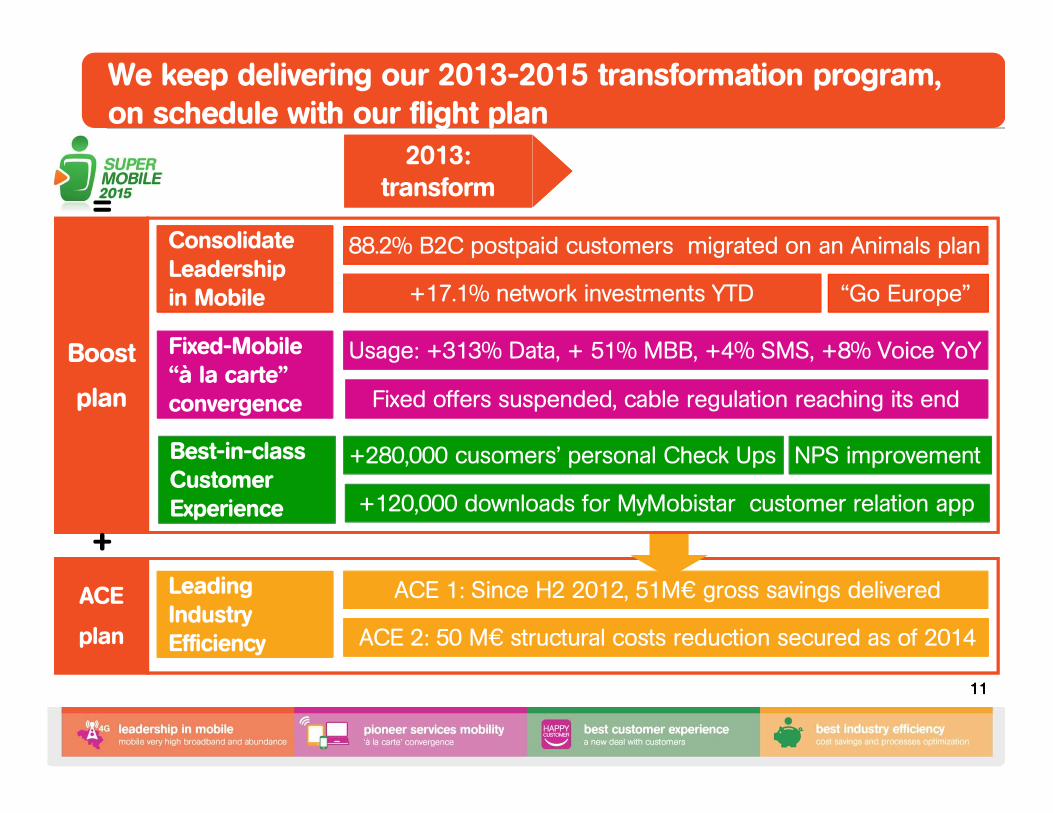

We keep delivering our 2013-2015 transformation program, on schedule with our flight plan

ACE 1: Since H2 2012, 51M€ gross savings delivered

Efficiency

LeadingIndustry Efficiency

+17.1% network investments YTD

+280,000 cusomers’ personal Check Ups

+120,000 downloads for MyMobistar customer relation app

Fixed offers suspended, cable regulation reaching its end

88.2% B2C postpaid customers migrated on an Animals plan

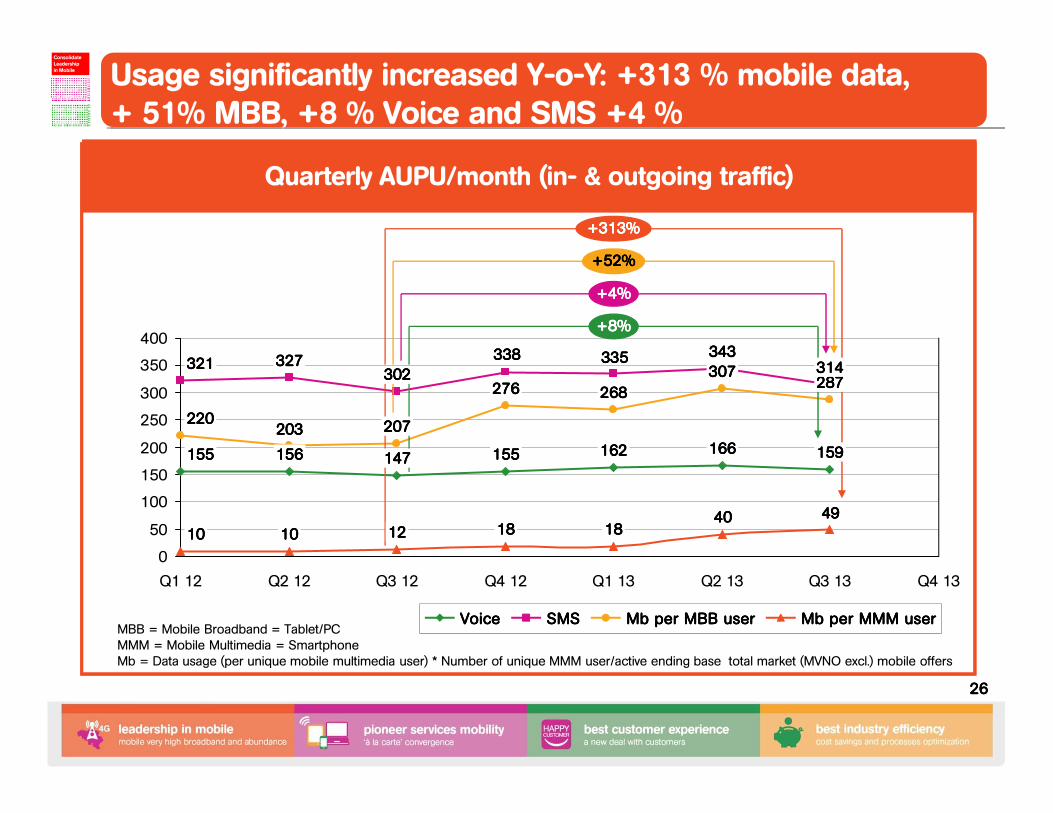

Usage: +313% Data, + 51% MBB, +4% SMS, +8% Voice YoYBoost

plan

ACE

plan

+

Best-in-class Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

2013:transform

=

NPS improvement

“Go Europe”

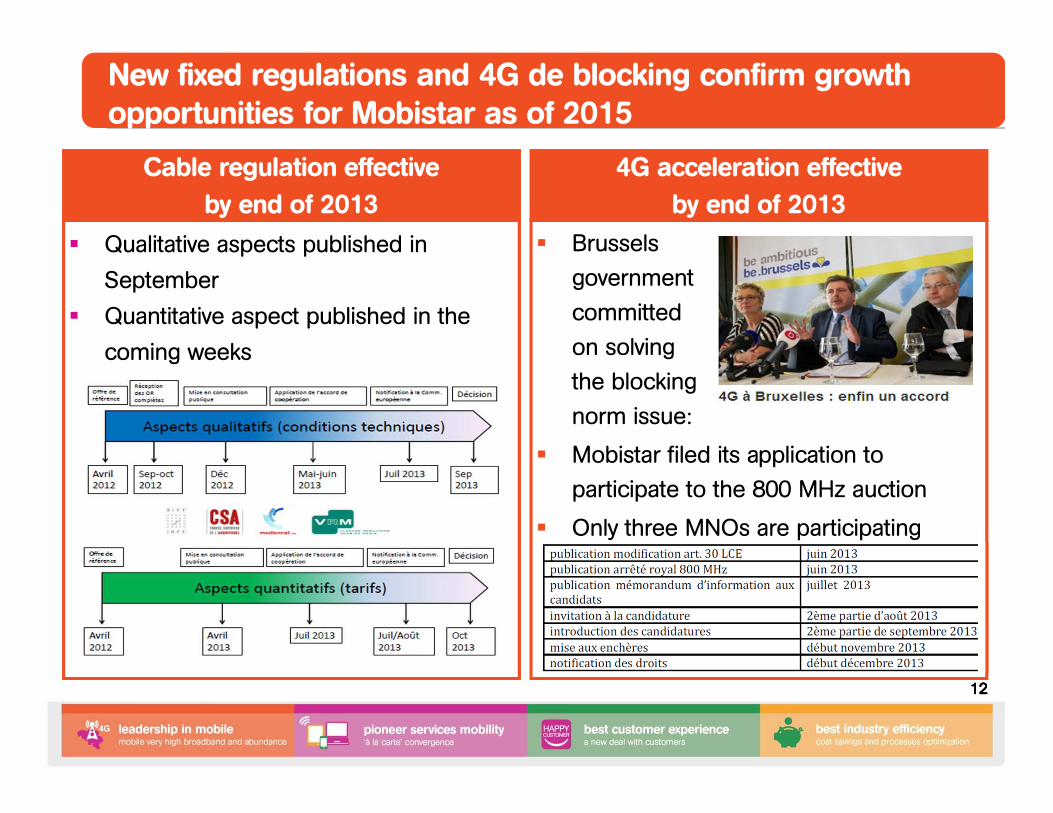

� Qualitative aspects published in

September

� Quantitative aspect published in the

coming weeks

� Brussels

government

committed

on solving

the blocking

norm issue:

� Mobistar filed its application to

participate to the 800 MHz auction

� Only three MNOs are participating

Cable regulation effective

by end of 2013

4G acceleration effective

by end of 2013

New fixed regulations and 4G de blocking confirm growth opportunities for Mobistar as of 2015

12121212

13131313

Operational UpdateMarket Dynamics

Customers, Price & Traffic Evolution

Mobile Data

B2B: M2M

Wholesale Business

14141414

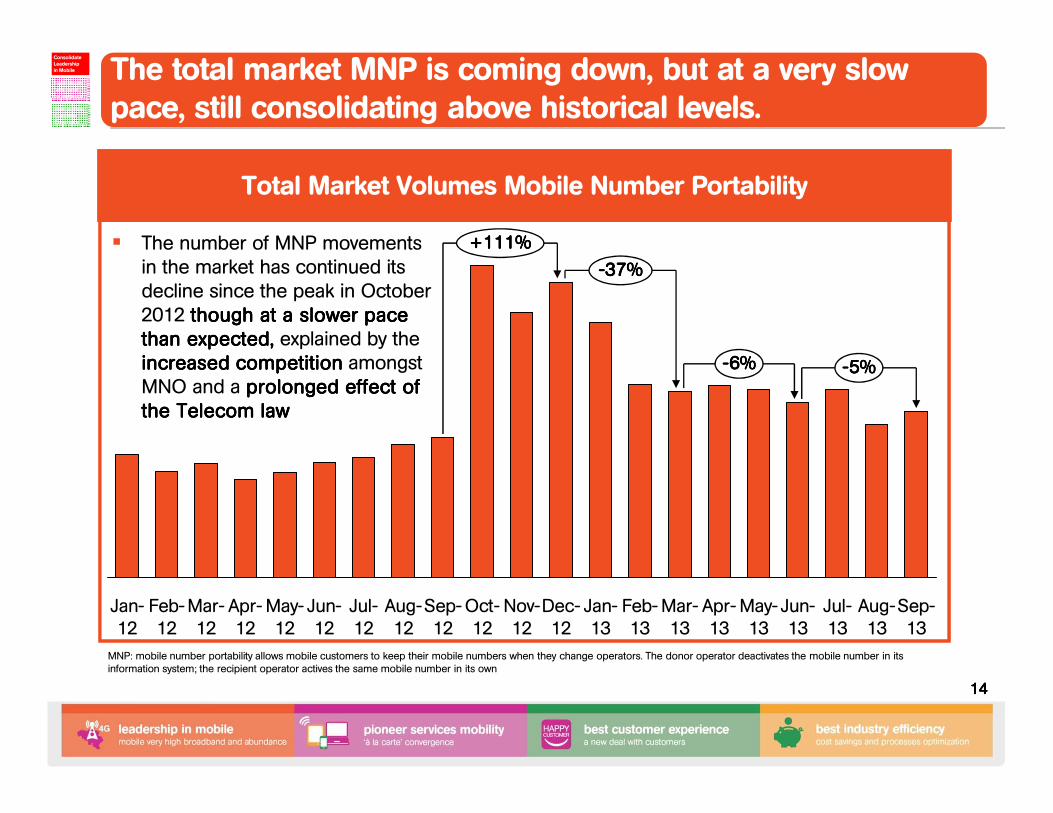

Total Market Volumes Mobile Number Portability

� The number of MNP movements in the market has continued its decline since the peak in October 2012 though at a slower pace though at a slower pace though at a slower pace though at a slower pace than than than than expected,expected,expected,expected, explained by the increased competitionincreased competitionincreased competitionincreased competition amongst MNO and a prolonged effect of prolonged effect of prolonged effect of prolonged effect of the Telecom lawthe Telecom lawthe Telecom lawthe Telecom law

MNP: mobile number portability allows mobile customers to keep their mobile numbers when they change operators. The donor operator deactivates the mobile number in its information system; the recipient operator actives the same mobile number in its own

----6%6%6%6%

+111%+111%+111%+111%

----37%37%37%37%

Sep-13

Aug-13

Jul-13

Jun-13

May-13

Apr-13

Mar-13

Feb-13

Jan-13

Dec-12

Nov-12

Oct-12

Sep-12

Aug-12

Jul-12

Jun-12

May-12

Apr-12

Mar-12

Feb-12

Jan-12

----5%5%5%5%

Best-in-class Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

The total market MNP is coming down, but at a very slow pace, still consolidating above historical levels.

15151515

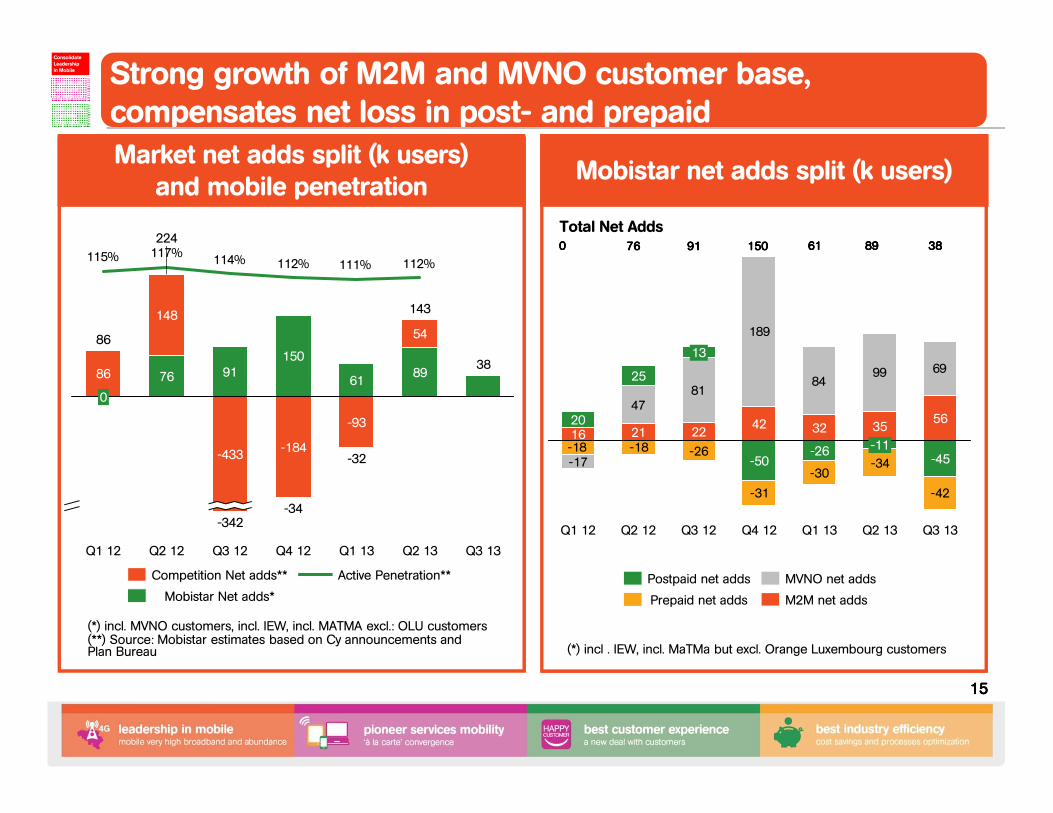

Strong growth of M2M and MVNO customer base, compensates net loss in post- and prepaid

76

38

112%111%112%114%117%115%

Q3 13Q2 13

143

89

54

Q1 13

-32

61

-93

-433

Q2 12

224

76

148

Q1 12

86

0

86

-342

Q3 12

-184

150

-34

Q4 12

91

Active Penetration**

Mobistar Net adds*

Competition Net adds**

-31

-30-34

-42

189

8499 69

-26-18-18-17

8147

Q3 13

56

-45

Q2 13

35

-11

Q1 13

32

-26

Q4 12

42

-50

Q3 12

22

13

Q2 12

21

25

Q1 12

1620

M2M net adds

MVNO net adds

Prepaid net adds

Postpaid net adds

(*) incl. MVNO customers, incl. IEW, incl. MATMA excl.: OLU customers(**) Source: Mobistar estimates based on Cy announcements and Plan Bureau (*) incl . IEW, incl. MaTMa but excl. Orange Luxembourg customers

0000 76767676 91919191 150150150150 61616161

Total Net Adds

Market net adds split (k users)and mobile penetration

Mobistar net adds split (k users)

89898989

Best-in-class Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

38383838

16161616

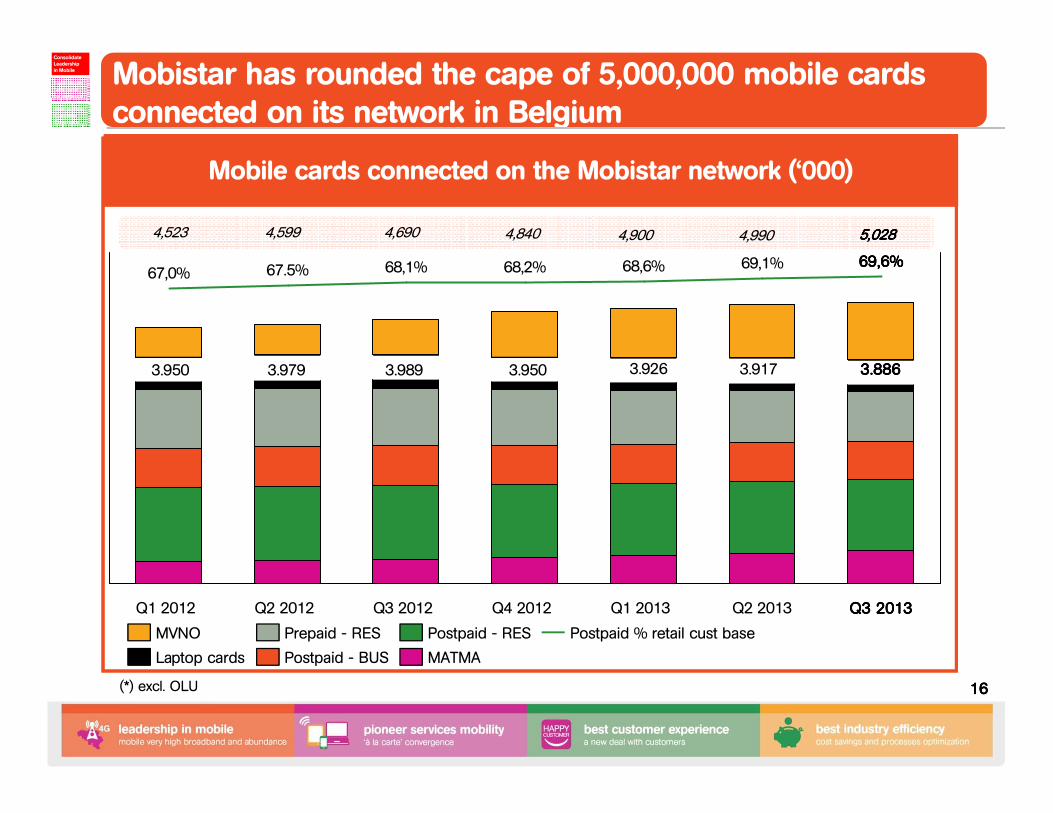

Mobistar has rounded the cape of 5,000,000 mobile cards connected on its network in Belgium

69,6%69,6%69,6%69,6%

Q3 2013Q3 2013Q3 2013Q3 2013Q2 2013

69,1%

Q1 2013

68,6%

Q4 2012

68,2%

Q3 2012

68,1%

Q2 2012

67.5%

Q1 2012

67,0%

Postpaid - RES

Postpaid - BUS

Postpaid % retail cust baseMVNO Prepaid - RES

Laptop cards MATMA

(*) excl. OLU

3.950 3.979 3.989 3.950 3.926

Mobile cards connected on the Mobistar network (‘000)

3.8863.8863.8863.886

Best-in-class Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

3.917

4,523 4,599 4,690 4,840 4,900 4,990 5,0285,0285,0285,028

April 1: continued push of Personal Check to all customers

April 16: New Animals portfolio: Postpaid review + Dolphin 12 web only

+ new High end unlimited Animals+ Prepaid Animals launched

May 7: upgrade of 350,000 old plans with new “Animals” tariff conditions

May 15: suspension of the commercialization of Fixed residential ADSL and satellite services

May 22: “iWant” tactical subsidized handset campaign

June 21: launch of Go Europe (unique roaming option)

Mobistar has invested in customer retention and loyalty,in line with its transformation strategy

17171717

Best-in-class Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

� The DNA of our customer value proposition remained unchanged.

� We observe that consumers have different lifestyles and mobility needs.

� Mobistar wants to deliver the most suitable mobility solutions to fulfill these different lifestyles, at competitive conditions.

Leadership amongst mobile customer base is Mobistar’s #1 priority

High commercial activity in Q2 2013, followed by stabilization in Q3 2013

April 1: continued push of Personal Check to all customers

April 16: New Animals portfolio: Postpaid review + Dolphin 12 web only

+ new High end unlimited Animals+ Prepaid Animals launched

May 7: upgrade of 350,000 old plans with new “Animals” tariff conditions

May 15: suspension of the commercialization of Fixed residential ADSL and satellite services

May 22: “iWant” tactical subsidized handset campaign

June 21: launch of Go Europe (unique roaming option)

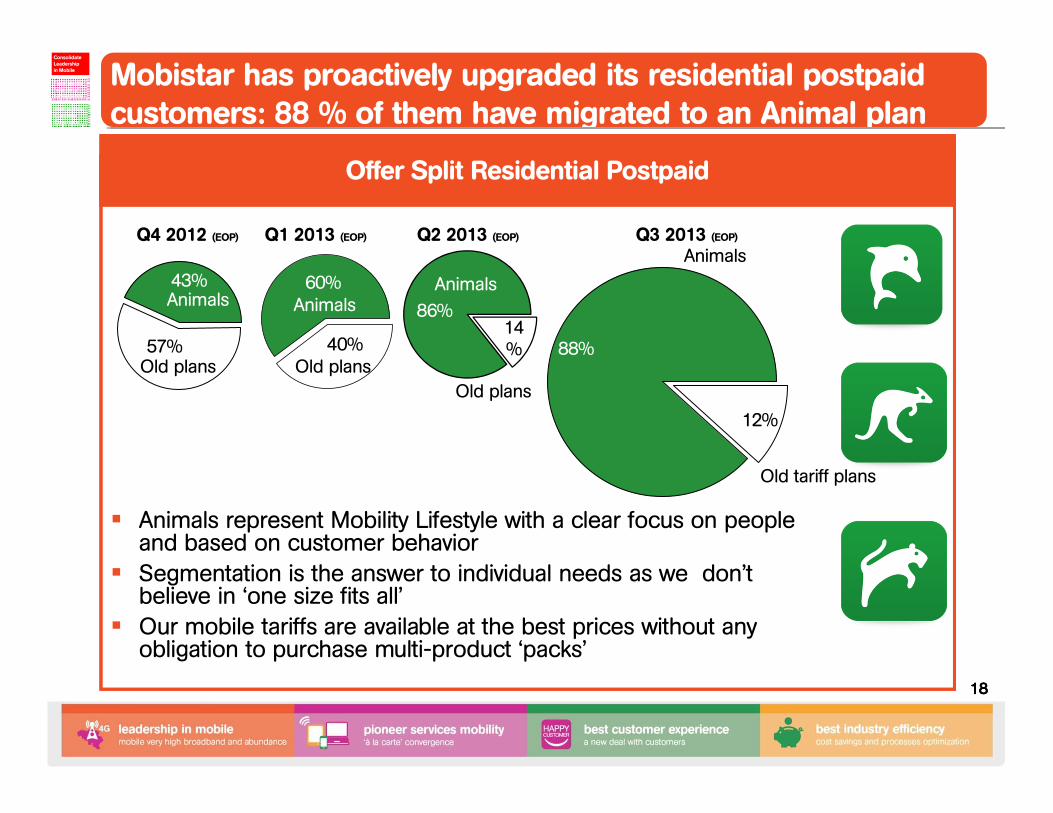

Mobistar has proactively upgraded its residential postpaid customers: 88 % of them have migrated to an Animal plan

18181818

Mobistar customers (in k customers) *Offer Split Residential Postpaid

Q4 2012 (EOP)

Animals60%

Old plans40%

Animals

Old plans

43%

57%

Q1 2013 (EOP)

� Animals represent Mobility Lifestyle with a clear focus on people and based on customer behavior

� Segmentation is the answer to individual needs as we don’t believe in ‘one size fits all’

� Our mobile tariffs are available at the best prices without any obligation to purchase multi-product ‘packs’

14%

86%

Old plans

Animals

Q2 2013 (EOP)

Best-in-class Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

12%

Old tariff plans

Animals

88%

Q3 2013 (EOP)

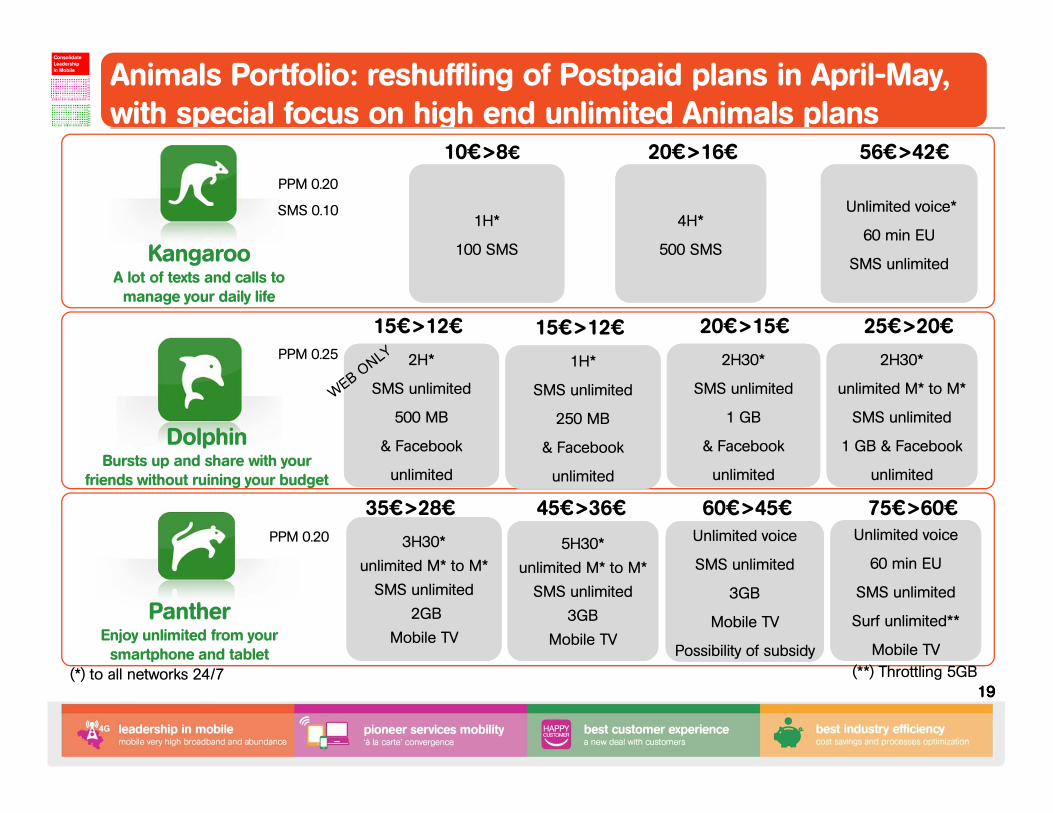

Animals Portfolio: reshuffling of Postpaid plans in April-May, with special focus on high end unlimited Animals plans

19191919

PPM 0.25

1H*

100 SMS

1H*

100 SMS

4H*

500 SMS

4H*

500 SMS

2H*

SMS unlimited

500 MB

unlimited

2H*

SMS unlimited

500 MB

unlimited

2H30*

SMS unlimited

1 GB

unlimited

2H30*

SMS unlimited

1 GB

unlimited

Unlimited voice*

60 min EU

SMS unlimited

Unlimited voice*

60 min EU

SMS unlimited

2H30*

unlimited M* to M*

SMS unlimited

1 GB & Facebook

unlimited

2H30*

unlimited M* to M*

SMS unlimited

1 GB & Facebook

unlimited

10€>8€ 20€>16€ 56€>42€

15€>12€ 20€>15€ 25€>20€

PPM 0.20 3H30*

unlimited M* to M*

SMS unlimited

2GB

Mobile TV

3H30*

unlimited M* to M*

SMS unlimited

2GB

Mobile TV

Unlimited voice

SMS unlimited

3GB

Mobile TV

Possibility of subsidy

Unlimited voice

SMS unlimited

3GB

Mobile TV

Possibility of subsidy

Unlimited voice

60 min EU

SMS unlimited

Surf unlimited**

Mobile TV

Unlimited voice

60 min EU

SMS unlimited

Surf unlimited**

Mobile TV

35€>28€ 60€>45€ 75€>60€

(**) Throttling 5GB

5H30*

unlimited M* to M*

SMS unlimited

3GB

Mobile TV

5H30*

unlimited M* to M*

SMS unlimited

3GB

Mobile TV

45€>36€

1H*

SMS unlimited

250 MB

unlimited

1H*

SMS unlimited

250 MB

unlimited

15€>12€

KangarooA lot of texts and calls to manage your daily life

DolphinBursts up and share with your

friends without ruining your budget

PantherEnjoy unlimited from your smartphone and tablet

Best-in-class Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

(*) to all networks 24/7

PPM 0.20

SMS 0.10

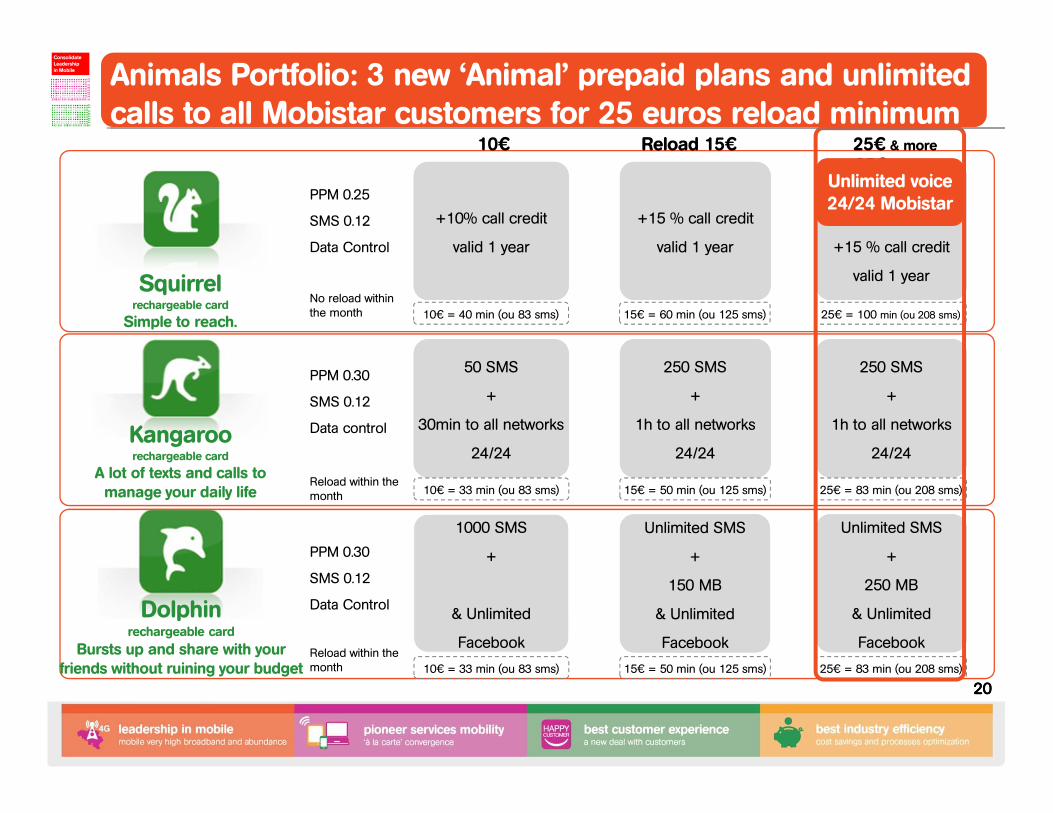

Animals Portfolio: 3 new ‘Animal’ prepaid plans and unlimited calls to all Mobistar customers for 25 euros reload minimum

20202020

25€ et plus

10€ Reload 15€

PPM 0.25

SMS 0.12

Data Control

PPM 0.30

SMS 0.12

Data Control

PPM 0.30

SMS 0.12

Data control

+10% call credit

valid 1 year

+10% call credit

valid 1 year

+15 % call credit

valid 1 year

+15 % call credit

valid 1 year

50 SMS

+

30min to all networks

24/24

50 SMS

+

30min to all networks

24/24

250 SMS

+

1h to all networks

24/24

250 SMS

+

1h to all networks

24/24

1000 SMS

+

& Unlimited

Unlimited SMS

+

150 MB

& Unlimited

Unlimited SMS

+

150 MB

& Unlimited

10€ = 33 min (ou 83 sms) 15€ = 50 min (ou 125 sms)

10€ = 33 min (ou 83 sms) 15€ = 50 min (ou 125 sms)

10€ = 40 min (ou 83 sms) 15€ = 60 min (ou 125 sms)

Squirrelrechargeable card

Simple to reach.

Kangaroorechargeable card

A lot of texts and calls to manage your daily life

+15 % call credit

valid 1 year

+15 % call credit

valid 1 year

250 SMS

+

1h to all networks

24/24

250 SMS

+

1h to all networks

24/24

Unlimited SMS

+

250 MB

& Unlimited

Unlimited SMS

+

250 MB

& Unlimited

25€ = 83 min (ou 208 sms)

25€ = 83 min (ou 208 sms)

25€ = 100 min (ou 208 sms)

Unlimited voice24/24 Mobistar

No reload within the month

Reload within the month

Reload within the month

25€ & more

Best-in-class Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

Dolphinrechargeable card

Bursts up and share with your friends without ruining your budget

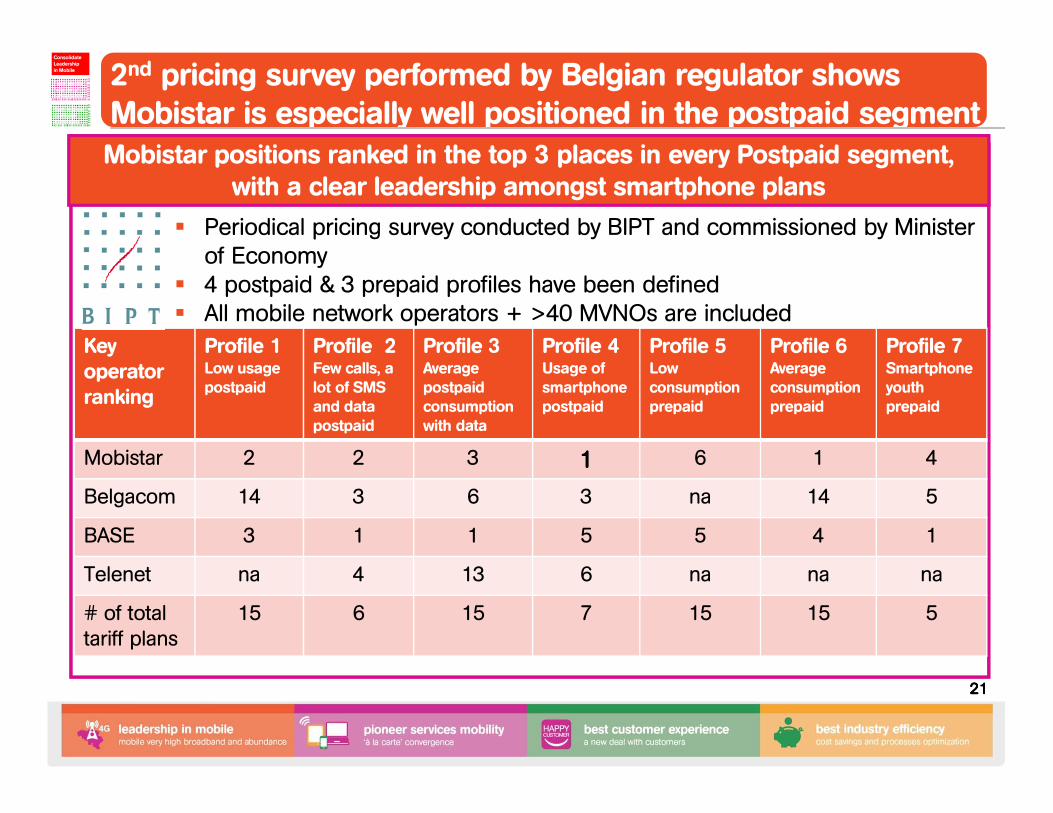

2nd pricing survey performed by Belgian regulator shows Mobistar is especially well positioned in the postpaid segment

21212121

Key operator ranking

Profile 1 Low usage postpaid

Profile 2Few calls, a lot of SMS and data postpaid

Profile 3 Average postpaid consumption with data

Profile 4 Usage of smartphone postpaid

Profile 5Low consumption prepaid

Profile 6 Average consumption prepaid

Profile 7 Smartphone youth prepaid

Mobistar 2 2 3 1111 6 1 4

Belgacom 14 3 6 3 na 14 5

BASE 3 1 1 5 5 4 1

Telenet na 4 13 6 na na na

# of total tariff plans

15 6 15 7 15 15 5

� Periodical pricing survey conducted by BIPT and commissioned by Ministerof Economy

� 4 postpaid & 3 prepaid profiles have been defined� All mobile network operators + >40 MVNOs are included

Best-in-class Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

Mobistar positions ranked in the top 3 places in every Postpaid segment,with a clear leadership amongst smartphone plans

Customer satisfaction impact� Award loyal Mobistar customers� Reduce churn in segments � Lower indirect retention cost� Lower IT costs� Create ground for new ARPU by pushing

mobile data in integrated bundlesARPU impact:� Same or lower out of bundle� Lower out-of-pocket as a first step, due to

slow AUPU elasticity to higher bundles

From old to new plans:more for same or more

2 examples of migrated tariff plans

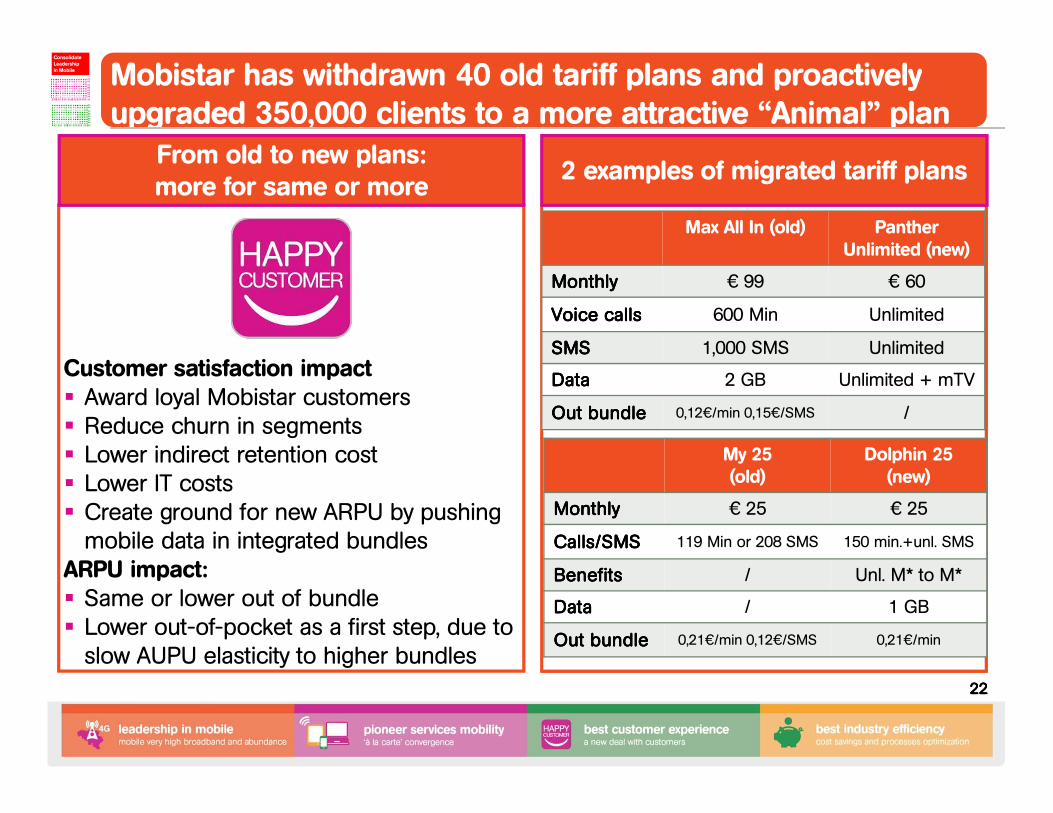

Mobistar has withdrawn 40 old tariff plans and proactively upgraded 350,000 clients to a more attractive “Animal” plan

22222222

Max All In (old) PantherUnlimited (new)

MMMMonthlyonthlyonthlyonthly € 99 € 60

Voice callsVoice callsVoice callsVoice calls 600 Min Unlimited

SMSSMSSMSSMS 1,000 SMS Unlimited

DataDataDataData 2 GB Unlimited + mTV

OutOutOutOut bundlebundlebundlebundle 0,12€/min 0,15€/SMS /

My 25(old)

Dolphin 25 (new)

MMMMonthlyonthlyonthlyonthly € 25 € 25

Calls/SMSCalls/SMSCalls/SMSCalls/SMS 119 Min or 208 SMS 150 min.+unl. SMS

BenefitsBenefitsBenefitsBenefits / Unl. M* to M*

DataDataDataData / 1 GB

OutOutOutOut bundlebundlebundlebundle 0,21€/min 0,12€/SMS 0,21€/min

Best-in-class Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

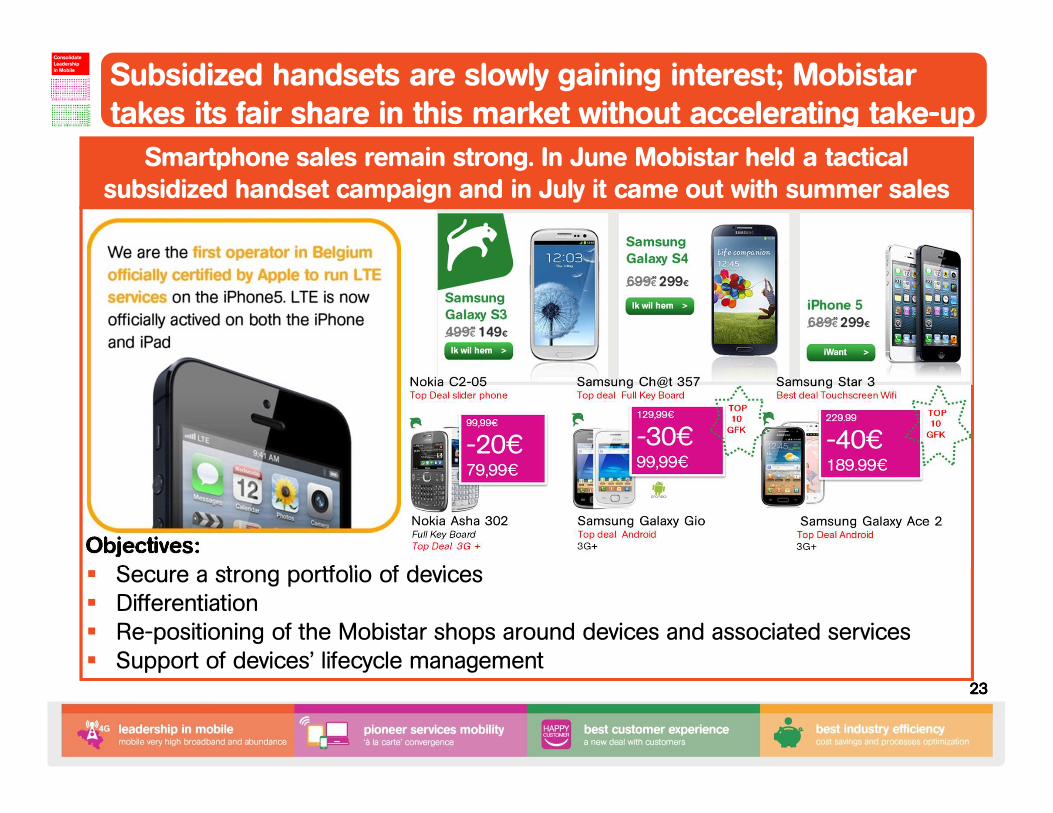

Smartphone sales remain strong. In June Mobistar held a tactical subsidized handset campaign and in July it came out with summer sales

23232323

Subsidized handsets are slowly gaining interest; Mobistartakes its fair share in this market without accelerating take-upBest-in-class

Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

Objectives:� Secure a strong portfolio of devices � Differentiation � Re-positioning of the Mobistar shops around devices and associated services � Support of devices’ lifecycle management

What � Roaming EU only� Available only on Animal TP� Calls and SMS deducted from

national bundle� Data daily bundle for Dolphin and

Panther� Unlimited options or Advantage not

includedWhy� Align with our Mobile Leadership

strategy� No more ‘bill shock’ fear restraining

usage� Anticipate roaming market evolution � Leverage on Orange Group

In June Mobistar launched Go Europe, which gives customer more peace of mind when calling, texting and surfing abroad

24242424

With Go Europe, you can call, text and surf abroad, at national tariffs

as if you are still in Belgium!

For 3 euros per 3 euros per 3 euros per 3 euros per day, day, day, day, the new Go Europe option will enable you to use the minutes

and texts from your national mobile subscription, with in addition 25 MB of data per day for Dolphin and Panther Customers

Best-in-class Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

What and why“Go Europe” concept

25252525

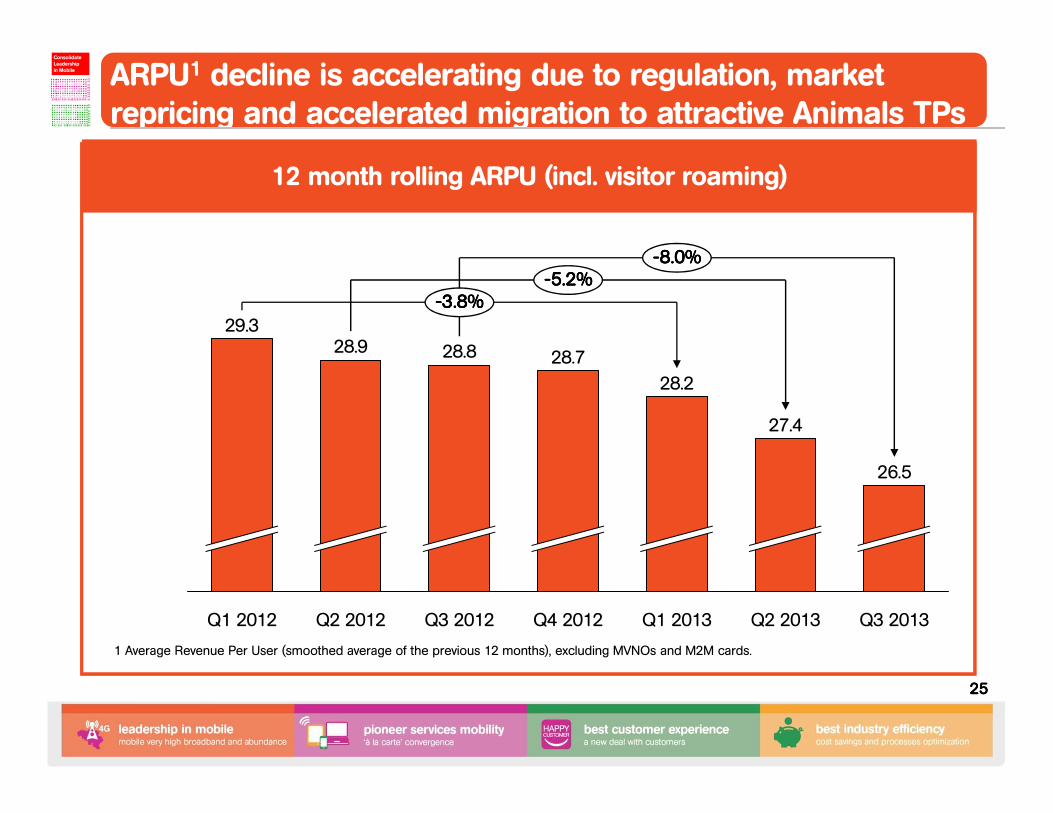

----8.0%8.0%8.0%8.0%

Q3 2013

26.5

Q2 2013

27.4

Q1 2013

28.2

Q4 2012

28.7

Q3 2012

28.8

Q2 2012

28.9

Q1 2012

----5.2%5.2%5.2%5.2%

29.3

----3.8%3.8%3.8%3.8%

ARPU1 decline is accelerating due to regulation, market repricing and accelerated migration to attractive Animals TPsBest-in-class

Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

1 Average Revenue Per User (smoothed average of the previous 12 months), excluding MVNOs and M2M cards.

12 month rolling ARPU (incl. visitor roaming)

26262626

147147147147

343343343343335335335335338338338338302302302302

203203203203

4949494940404040

0

50

100

150

200

250

300

350

400

327327327327

156156156156

Q1 12

10101010

220220220220

321321321321

155155155155

Q4 13Q2 12

10101010

+8%+8%+8%+8%

+52%+52%+52%+52%

+4%+4%+4%+4%

+313%+313%+313%+313%

Q3 13

287287287287314314314314

159159159159

Q2 13

307307307307

166166166166

Q1 13

18181818

268268268268

162162162162

Q4 12

18181818

276276276276

155155155155

Q3 12

12121212

207207207207

SMSSMSSMSSMSVoiceVoiceVoiceVoice Mb per MBB userMb per MBB userMb per MBB userMb per MBB user Mb per MMM userMb per MMM userMb per MMM userMb per MMM user

Quarterly AUPU/month (in- & outgoing traffic)

MBB = Mobile Broadband = Tablet/PCMMM = Mobile Multimedia = SmartphoneMb = Data usage (per unique mobile multimedia user) * Number of unique MMM user/active ending base total market (MVNO excl.) mobile offers

Usage significantly increased Y-o-Y: +313 % mobile data, + 51% MBB, +8 % Voice and SMS +4 %Best-in-class

Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

27272727

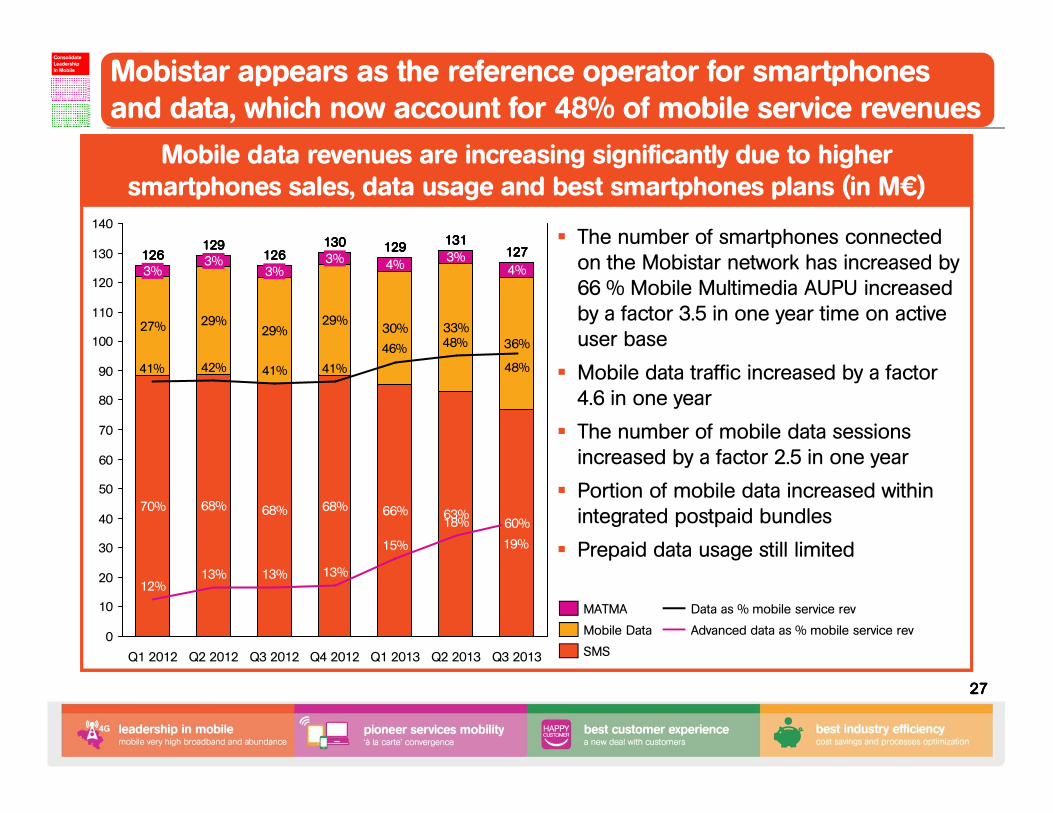

Mobile data revenues are increasing significantly due to higher smartphones sales, data usage and best smartphones plans (in M€)

48%46%

41%41%42%41% 48%

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

60%

36%

4%

Q2 2013

131131131131

18%63%

33%

3%

Q1 2013

129129129129

15%

66%

30%

4%

Q4 2012

130130130130

13%

68%

29%

3%

Q3 2013

127127127127

19%

Q3 2012

126126126126

13%

68%

29%

3%

Q2 2012

129129129129

13%

68%

29%

3%

Q1 2012

126126126126

12%

70%

27%

3%

Advanced data as % mobile service rev

Data as % mobile service rev

SMS

Mobile Data

MATMA

� The number of smartphones connected on the Mobistar network has increased by 66 % Mobile Multimedia AUPU increased by a factor 3.5 in one year time on active user base

� Mobile data traffic increased by a factor 4.6 in one year

� The number of mobile data sessions increased by a factor 2.5 in one year

� Portion of mobile data increased within integrated postpaid bundles

� Prepaid data usage still limited

Best-in-class Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

Mobistar appears as the reference operator for smartphonesand data, which now account for 48% of mobile service revenues

28282828

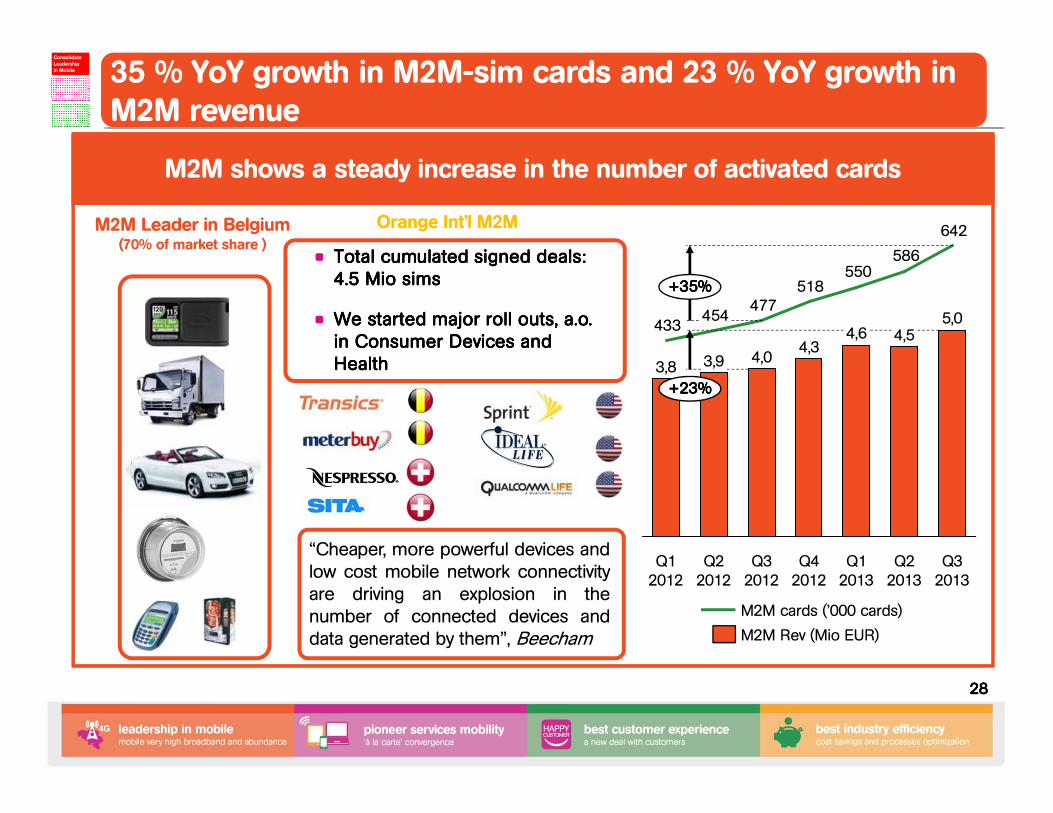

M2M Leader in Belgium (70% of market share )

Orange Int’l M2M

• Total cumulated signed deals: Total cumulated signed deals: Total cumulated signed deals: Total cumulated signed deals: 4.5 Mio 4.5 Mio 4.5 Mio 4.5 Mio simssimssimssims

• We started major roll outs, We started major roll outs, We started major roll outs, We started major roll outs, a.o.a.o.a.o.a.o.in Consumer Devices and in Consumer Devices and in Consumer Devices and in Consumer Devices and HealthHealthHealthHealth

“Cheaper, more powerful devices andlow cost mobile network connectivityare driving an explosion in thenumber of connected devices anddata generated by them”, Beecham

642

586550

518477

454433

+35%+35%+35%+35%

+23%+23%+23%+23%

Q3 2013

5,0

Q2 2013

4,5

Q1 2013

4,6

Q4 2012

4,3

Q3 2012

4,0

Q2 2012

3,9

Q1 2012

3,8

M2M Rev (Mio EUR)

M2M cards (’000 cards)

M2M shows a steady increase in the number of activated cards

35 % YoY growth in M2M-sim cards and 23 % YoY growth in M2M revenueBest-in-class

Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

29292929

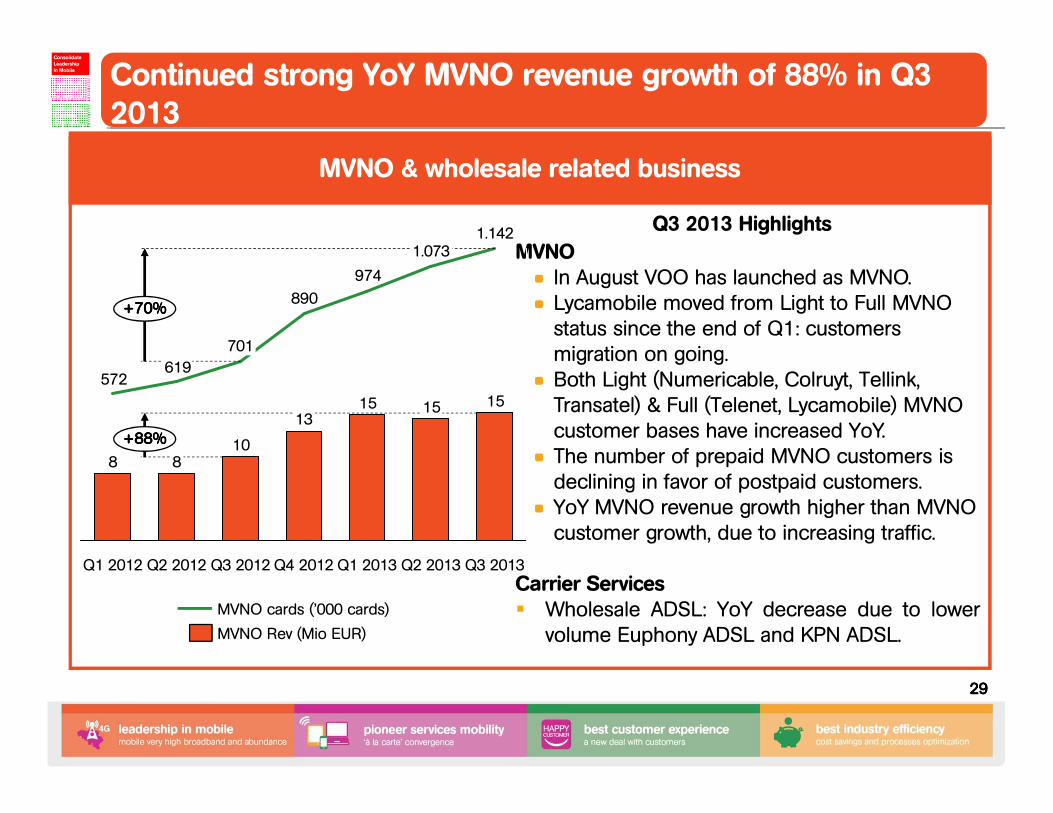

MVNO & wholesale related business

MVNO• In August VOO has launched as MVNO.• Lycamobile moved from Light to Full MVNO

status since the end of Q1: customers migration on going.

• Both Light (Numericable, Colruyt, Tellink, Transatel) & Full (Telenet, Lycamobile) MVNO customer bases have increased YoY.

• The number of prepaid MVNO customers is declining in favor of postpaid customers.

• YoY MVNO revenue growth higher than MVNO customer growth, due to increasing traffic.

Carrier Services� Wholesale ADSL: YoY decrease due to lower

volume Euphony ADSL and KPN ADSL.

151513

1088

15

974

890

619572

+70%+70%+70%+70%

+88%+88%+88%+88%

Q3 2013

1.142

Q2 2013

1.073

Q1 2013Q4 2012Q3 2012

701

Q2 2012Q1 2012

MVNO cards (’000 cards)

MVNO Rev (Mio EUR)

Q3 2013 Highlights

Continued strong YoY MVNO revenue growth of 88% in Q3 2013Best-in-class

Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

30303030

ACE

Distribution

Network

Spectrum

MTR & Roaming

Regulation

TOPICS IN THE SPOTLIGHT

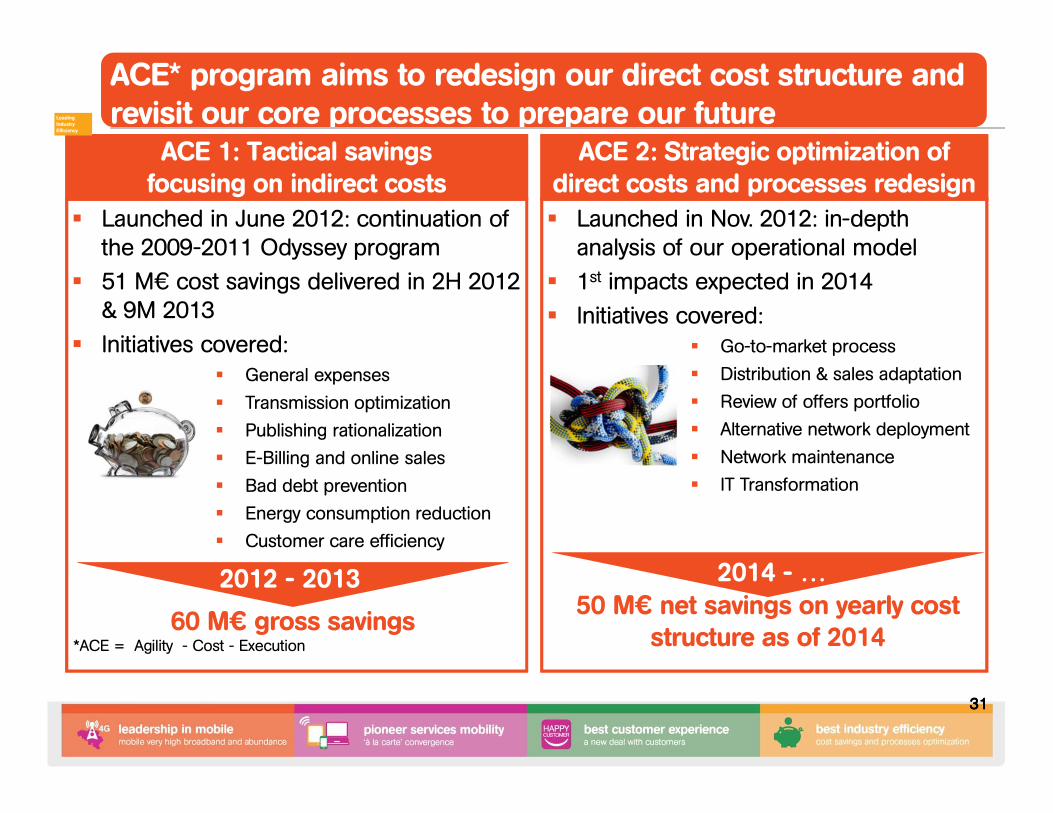

in 2H 2012

� Launched in June 2012: continuation of the 2009-2011 Odyssey program

� 51 M€ cost savings delivered in 2H 2012 & 9M 2013

� Initiatives covered:� General expenses

� Transmission optimization

� Publishing rationalization

� E-Billing and online sales

� Bad debt prevention

� Energy consumption reduction

� Customer care efficiency

31313131

� Launched in Nov. 2012: in-depth analysis of our operational model

� 1st impacts expected in 2014

� Initiatives covered:� Go-to-market process

� Distribution & sales adaptation

� Review of offers portfolio

� Alternative network deployment

� Network maintenance

� IT Transformation

direct costs and processes redesign ACE 2: Strategic optimization of

direct costs and processes redesign

2012-201350 M€ net savings on yearly cost

structure as of 201450 M€ net savings on yearly cost

structure as of 2014

2014 - …

focusing on indirect costs ACE 1: Tactical savingsfocusing on indirect costs

60 M€ gross savings60 M€ gross savings

2012 - 2013

*ACE = Agility - Cost - Execution

ACE* program aims to redesign our direct cost structure and revisit our core processes to prepare our futureLeading

Industry Efficiency

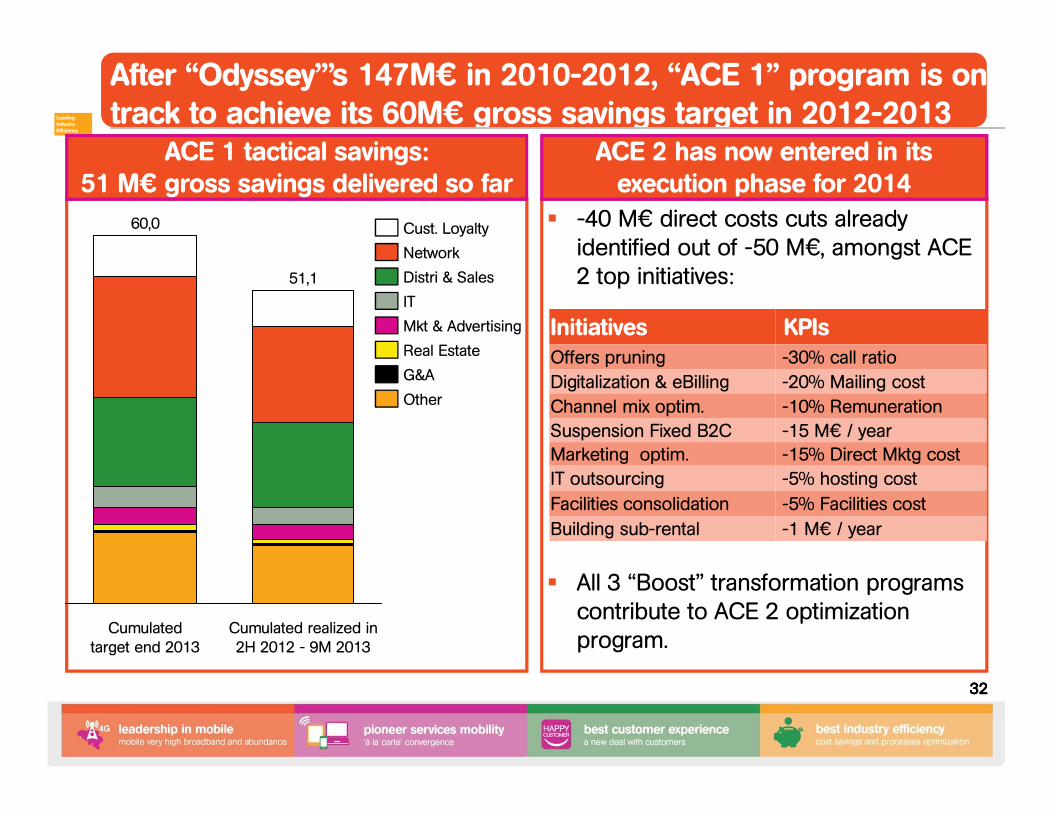

� -40 M€ direct costs cuts already identified out of -50 M€, amongst ACE 2 top initiatives:

� All 3 “Boost” transformation programs contribute to ACE 2 optimization program.

execution phase for 2014ACE 2 has now entered in its execution phase for 2014

32323232

After “Odyssey”’s 147M€ in 2010-2012, “ACE 1” program is on track to achieve its 60M€ gross savings target in 2012-2013Leading

Industry Efficiency

51 M€ gross savings delivered so farACE 1 tactical savings:

51 M€ gross savings delivered so far

Initiatives KPIsOffers pruning -30% call ratio

Digitalization & eBilling -20% Mailing cost

Channel mix optim. -10% Remuneration

Suspension Fixed B2C -15 M€ / yearMarketing optim. -15% Direct Mktg cost

IT outsourcing -5% hosting cost

Facilities consolidation -5% Facilities cost

Building sub-rental -1 M€ / year

Cumulated target end 2013

60,0

Cumulated realized in 2H 2012 - 9M 2013

51,1

Mkt & Advertising

Other

IT

Real Estate

Network

Cust. Loyalty

Distri & Sales

G&A

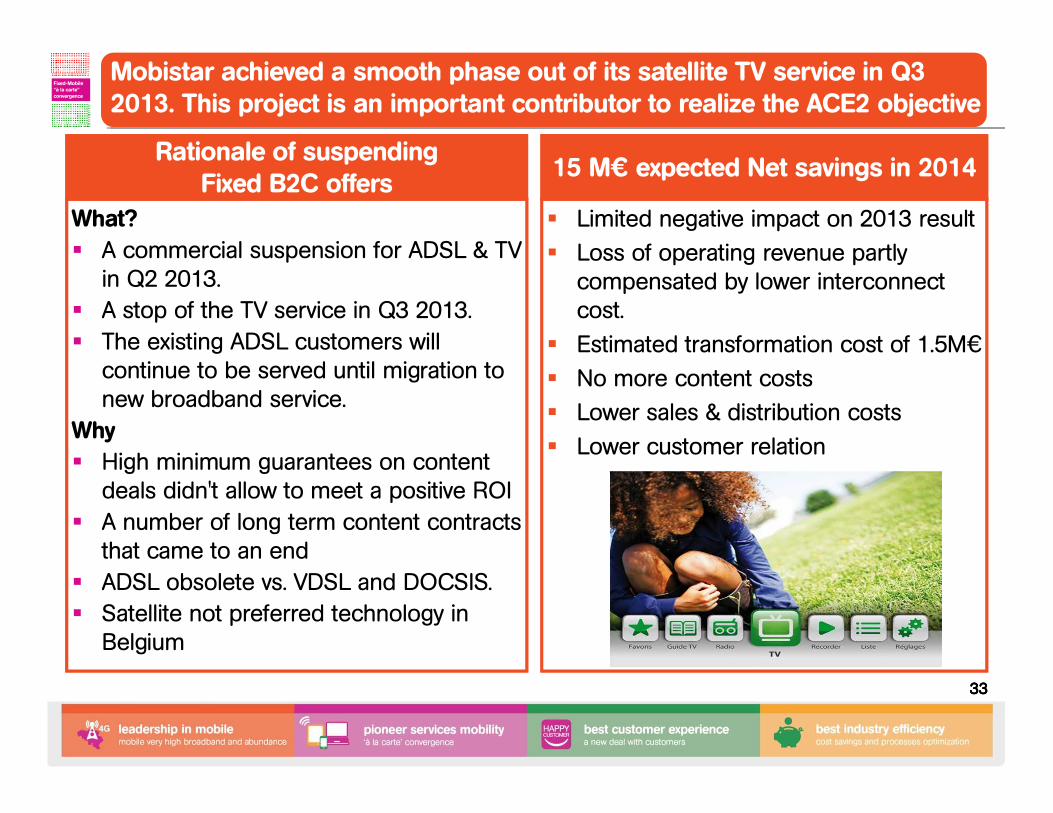

� Limited negative impact on 2013 result

� Loss of operating revenue partly compensated by lower interconnect cost.

� Estimated transformation cost of 1.5M€

� No more content costs

� Lower sales & distribution costs

� Lower customer relation

15 M€ expected Net savings in 2014

A commercial suspension for ADSL & TV

content contracts

What?

� A commercial suspension for ADSL & TV in Q2 2013.

� A stop of the TV service in Q3 2013.

� The existing ADSL customers will continue to be served until migration to new broadband service.

Why

� High minimum guarantees on content deals didn't allow to meet a positive ROI

� A number of long term content contracts that came to an end

� ADSL obsolete vs. VDSL and DOCSIS.

� Satellite not preferred technology in Belgium

Fixed B2C offers Rationale of suspending

Fixed B2C offers

33333333

Mobistar achieved a smooth phase out of its satellite TV service in Q3 2013. This project is an important contributor to realize the ACE2 objectiveBest-in-class

Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

34343434

.be

Shop in shopDirect

Exclusive

Multibrand

Mobistar uses a balanced mix of distribution channels to address different segments of customers

Our distribution strategy has allowed Mobistar to build a very close relationship with our customers Best-in-class

Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

optimizing costs structure &revenueFuture-proof distribution requires optimizing costs structure &revenue

35353535

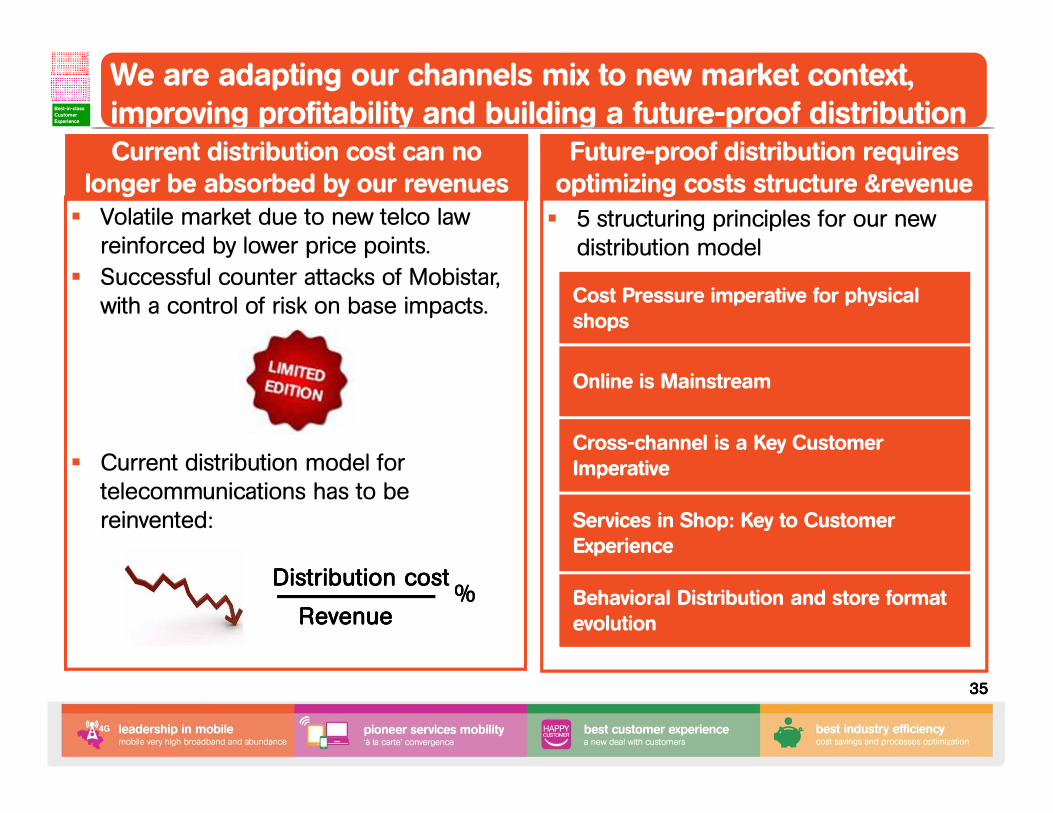

We are adapting our channels mix to new market context, improving profitability and building a future-proof distributionBest-in-class

Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

� 5 structuring principles for our new distribution model

� Volatile market due to new telco law reinforced by lower price points.

� Successful counter attacks of Mobistar, with a control of risk on base impacts.

� Current distribution model for telecommunications has to be reinvented:

longer be absorbed by our revenuesCurrent distribution cost can no

longer be absorbed by our revenues

Distribution Distribution Distribution Distribution costcostcostcost

RevenueRevenueRevenueRevenue%%%%

Cost Pressure imperative for physical shops

Online is Mainstream

Cross-channel is a Key Customer Imperative

Services in Shop: Key to Customer Experience

Behavioral Distribution and store format evolution

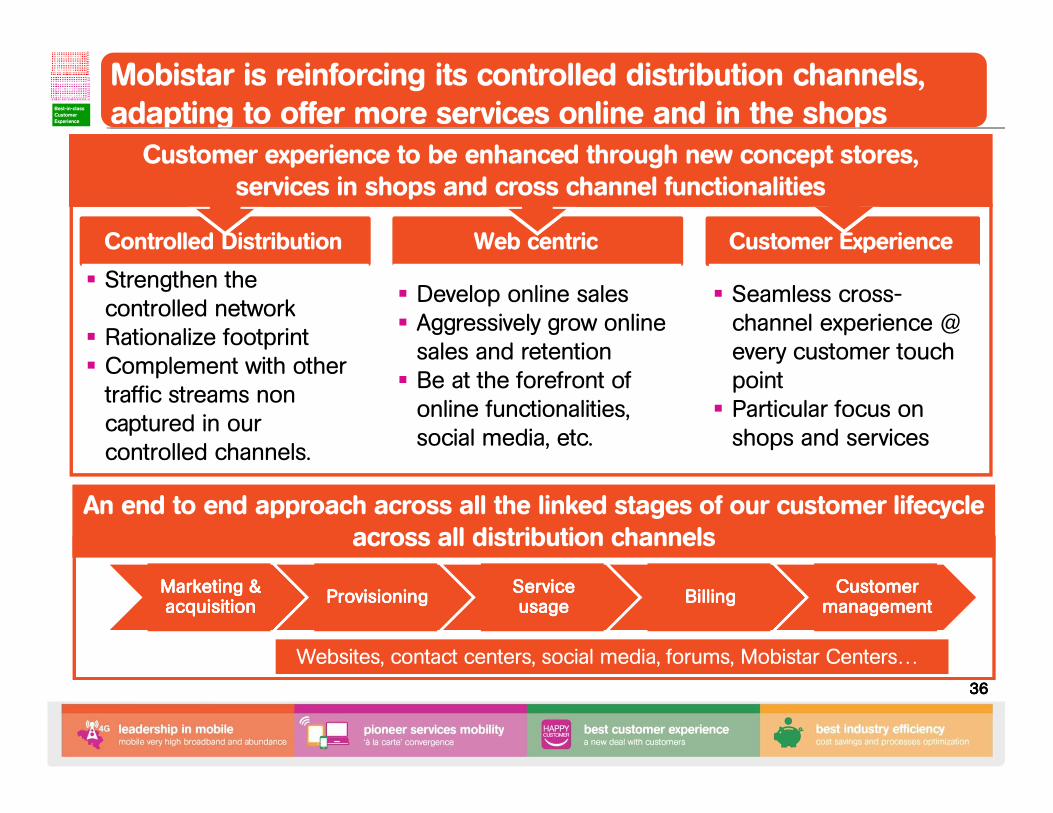

36363636

Web centricControlled Distribution Customer Experience

� Strengthen the controlled network

� Rationalize footprint� Complement with other

traffic streams non captured in our controlled channels.

� Strengthen the controlled network

� Rationalize footprint� Complement with other

traffic streams non captured in our controlled channels.

� Develop online sales� Aggressively grow online

sales and retention� Be at the forefront of

online functionalities, social media, etc.

� Develop online sales� Aggressively grow online

sales and retention� Be at the forefront of

online functionalities, social media, etc.

� Seamless cross-channel experience @ every customer touch point

� Particular focus on shops and services

� Seamless cross-channel experience @ every customer touch point

� Particular focus on shops and services

Mobistar is reinforcing its controlled distribution channels, adapting to offer more services online and in the shopsBest-in-class

Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

Customer experience to be enhanced through new concept stores, services in shops and cross channel functionalities

An end to end approach across all the linked stages of our customer lifecycle across all distribution channels

Marketing & Marketing & Marketing & Marketing & acquisitionacquisitionacquisitionacquisition

Marketing & Marketing & Marketing & Marketing & acquisitionacquisitionacquisitionacquisition

ProvisioningProvisioningProvisioningProvisioningProvisioningProvisioningProvisioningProvisioningService Service Service Service usageusageusageusage

Service Service Service Service usageusageusageusage

BillingBillingBillingBillingBillingBillingBillingBillingCustomer Customer Customer Customer

managementmanagementmanagementmanagementCustomer Customer Customer Customer

managementmanagementmanagementmanagement

Websites, contact centers, social media, forums, Mobistar Centers…

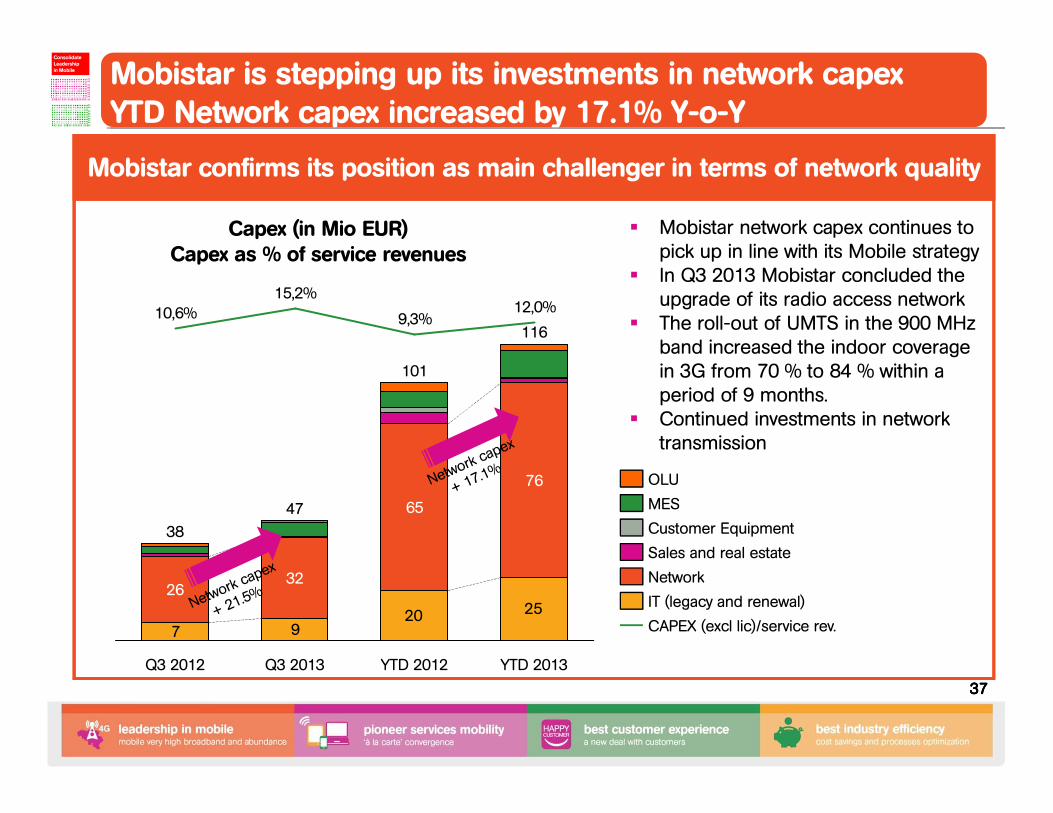

Capex (in Mio EUR) Capex as % of service revenues

Mobistar confirms its position as main challenger in terms of network quality

37373737

20 25

97

12,0%

116

YTD 2013

101

9,3%

76

Q3 2013

47

15,2%

YTD 2012

65

3226

38

Q3 2012

10,6%

Customer Equipment

CAPEX (excl lic)/service rev.

Network

Sales and real estate

OLU

MES

IT (legacy and renewal)

� Mobistar network capex continues to pick up in line with its Mobile strategy

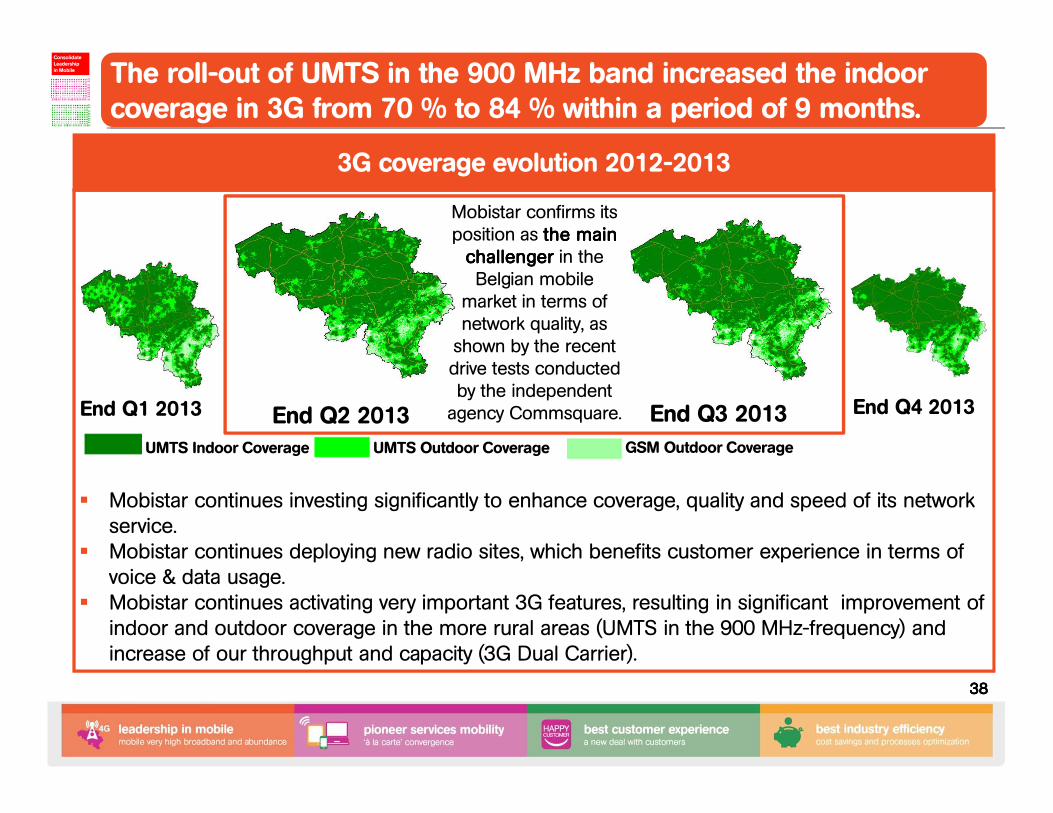

� In Q3 2013 Mobistar concluded the upgrade of its radio access network

� The roll-out of UMTS in the 900 MHz band increased the indoor coverage in 3G from 70 % to 84 % within a period of 9 months.

� Continued investments in network transmission

Mobistar is stepping up its investments in network capexYTD Network capex increased by 17.1% Y-o-YBest-in-class

Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

� Mobistar continues investing significantly to enhance coverage, quality and speed of its network service.

� Mobistar continues deploying new radio sites, which benefits customer experience in terms of voice & data usage.

� Mobistar continues activating very important 3G features, resulting in significant improvement of indoor and outdoor coverage in the more rural areas (UMTS in the 900 MHz-frequency) and increase of our throughput and capacity (3G Dual Carrier).

38383838

UMTS Indoor Coverage UMTS Outdoor Coverage GSM Outdoor Coverage

End Q2 2013

3G coverage evolution 2012-2013

End Q3 2013

Mobistar confirms its position as the main the main the main the main

challengerchallengerchallengerchallenger in the Belgian mobile

market in terms of network quality, as

shown by the recent drive tests conducted

by the independent agency Commsquare.

The roll-out of UMTS in the 900 MHz band increased the indoor coverage in 3G from 70 % to 84 % within a period of 9 months.

End Q1 2013 End Q4 2013

Best-in-class Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

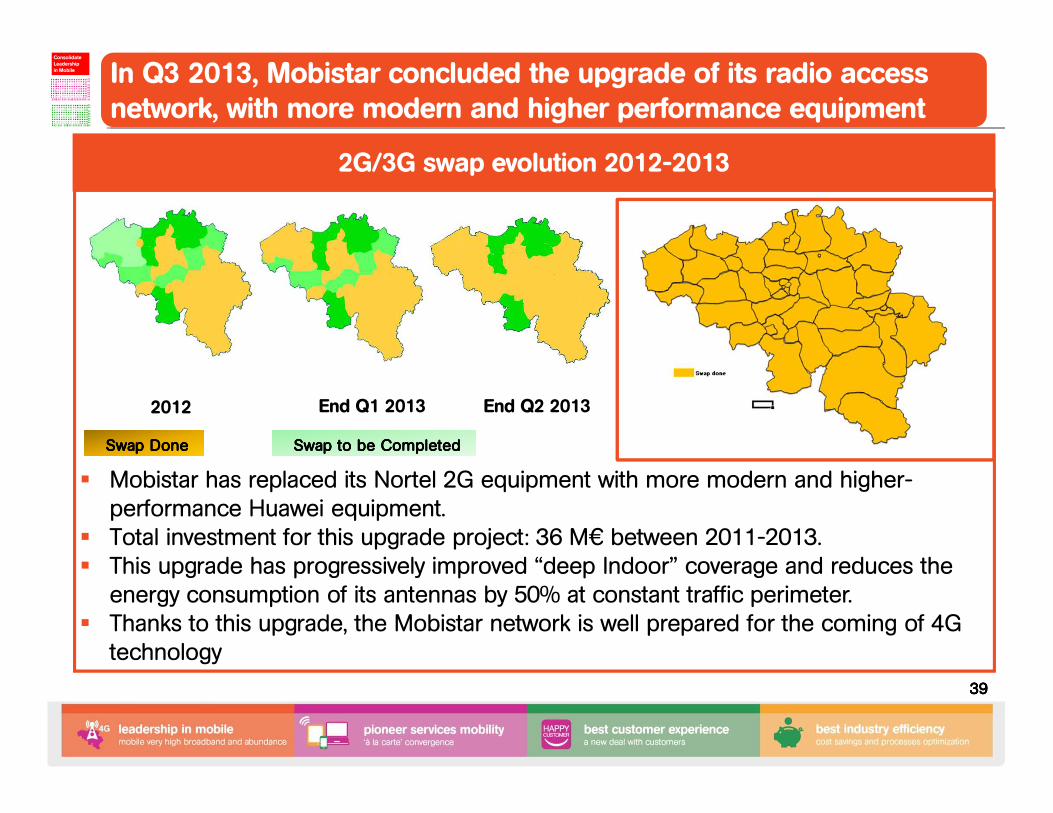

� Mobistar has replaced its Nortel 2G equipment with more modern and higher-performance Huawei equipment.

� Total investment for this upgrade project: 36 M€ between 2011-2013.� This upgrade has progressively improved “deep Indoor” coverage and reduces the

energy consumption of its antennas by 50% at constant traffic perimeter.� Thanks to this upgrade, the Mobistar network is well prepared for the coming of 4G

technology

39393939

2G/3G swap evolution 2012-2013

In Q3 2013, Mobistar concluded the upgrade of its radio access network, with more modern and higher performance equipment

SwapSwapSwapSwap DoneDoneDoneDone SwapSwapSwapSwap to be Completedto be Completedto be Completedto be Completed

2012 End Q1 2013 End Q2 2013

Best-in-class Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

40404040

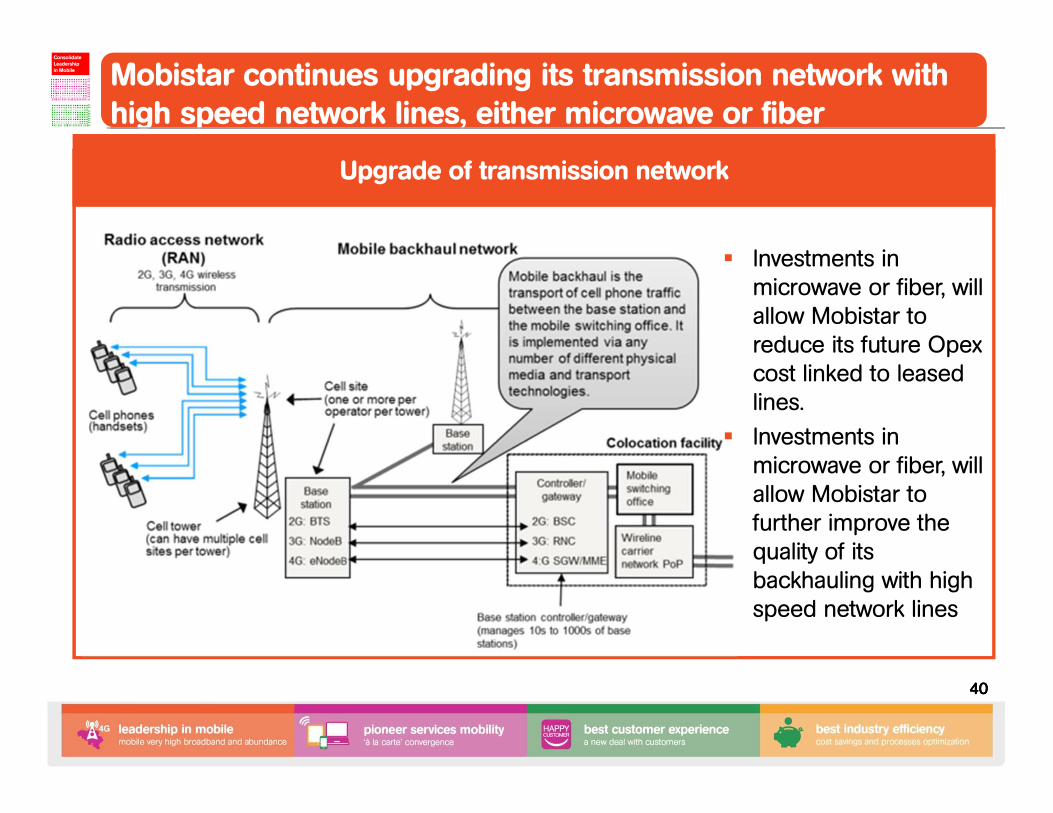

Upgrade of transmission network

� Investments in microwave or fiber, will allow Mobistar to reduce its future Opexcost linked to leased lines.

� Investments in microwave or fiber, will allow Mobistar to further improve the quality of its backhauling with high speed network lines

Mobistar continues upgrading its transmission network with high speed network lines, either microwave or fiberBest-in-class

Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

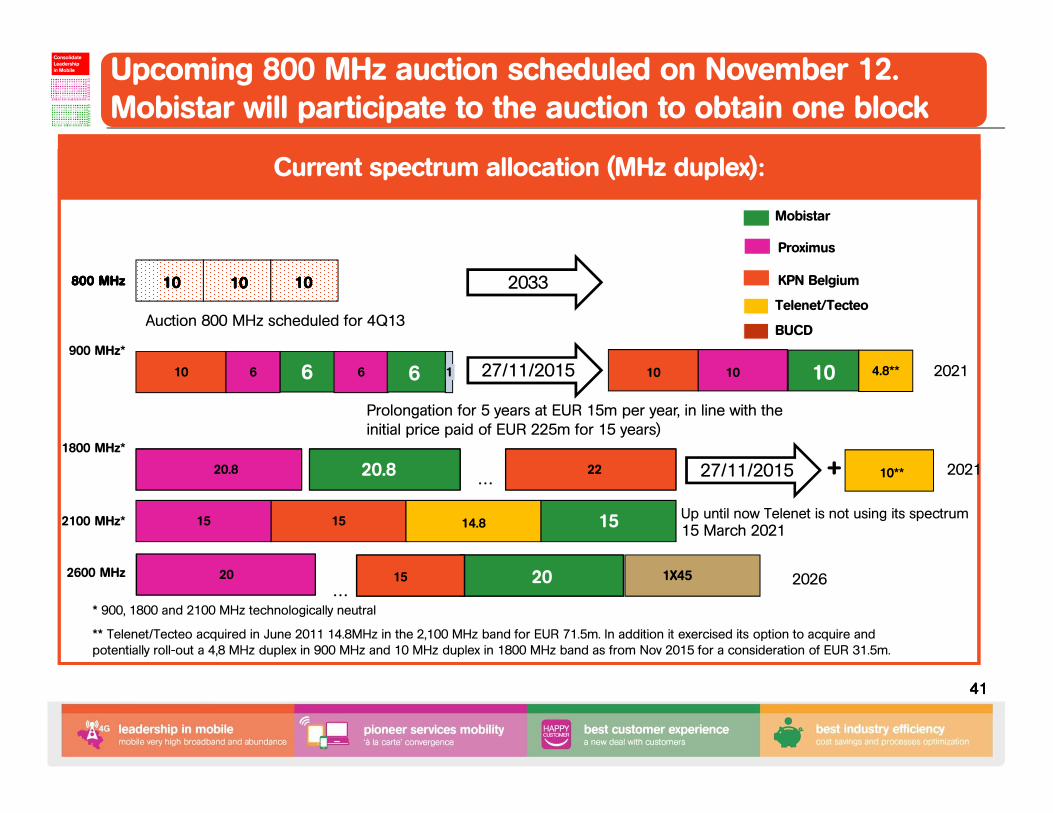

41414141

* 900, 1800 and 2100 MHz technologically neutral

** Telenet/Tecteo acquired in June 2011 14.8MHz in the 2,100 MHz band for EUR 71.5m. In addition it exercised its option to acquire and potentially roll-out a 4,8 MHz duplex in 900 MHz and 10 MHz duplex in 1800 MHz band as from Nov 2015 for a consideration of EUR 31.5m.

1X45

10 6 6 6

15 15 14.8 15

20.8 20.8 22

1

10101010

1800 MHz*

800 MHz800 MHz800 MHz800 MHz

900 MHz*

2100 MHz*

2600 MHz

Telenet/Tecteo

20 15

Up until now Telenet is not using its spectrum

10 1027/11/2015 10 4.8**

… 27/11/2015 10**+

…20

15 March 2021

2021

2026

2033

Prolongation for 5 years at EUR 15m per year, in line with the initial price paid of EUR 225m for 15 years)

6

Proximus

Mobistar

KPN Belgium10101010 10101010

Auction 800 MHz scheduled for 4Q13

2021

BUCD

Current spectrum allocation (MHz duplex):

Upcoming 800 MHz auction scheduled on November 12. Mobistar will participate to the auction to obtain one blockBest-in-class

Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

42424242

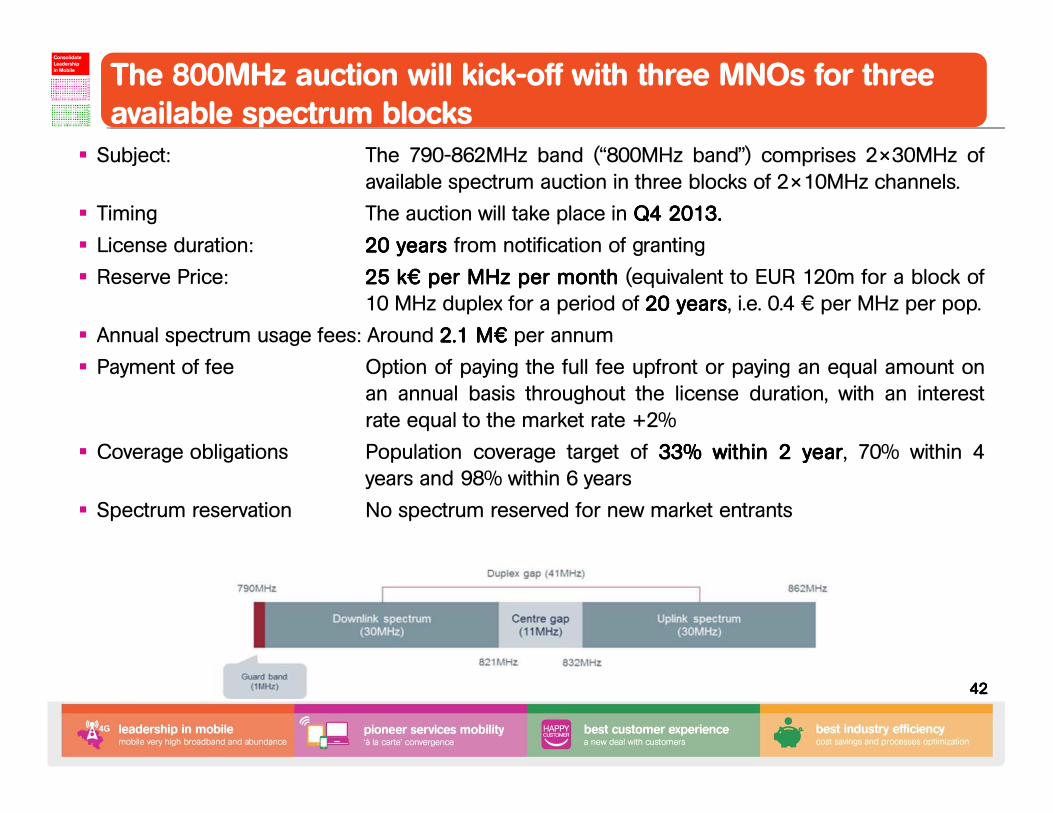

� Subject: The 790-862MHz band (“800MHz band”) comprises 2×30MHz ofavailable spectrum auction in three blocks of 2×10MHz channels.

� Timing The auction will take place in QQQQ4444 2013201320132013....

� License duration: 20202020 yearsyearsyearsyears from notification of granting

� Reserve Price: 25252525 kkkk€€€€ perperperper MHzMHzMHzMHz perperperper monthmonthmonthmonth (equivalent to EUR 120m for a block of10 MHz duplex for a period of 20202020 yearsyearsyearsyears, i.e. 0.4 € per MHz per pop.

� Annual spectrum usage fees: Around 2222....1111 MMMM€€€€ per annum

� Payment of fee Option of paying the full fee upfront or paying an equal amount onan annual basis throughout the license duration, with an interestrate equal to the market rate +2%

� Coverage obligations Population coverage target of 33333333%%%% withinwithinwithinwithin 2222 yearyearyearyear, 70% within 4years and 98% within 6 years

� Spectrum reservation No spectrum reserved for new market entrants

The 800MHz auction will kick-off with three MNOs for three available spectrum blocks Best-in-class

Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

43434343

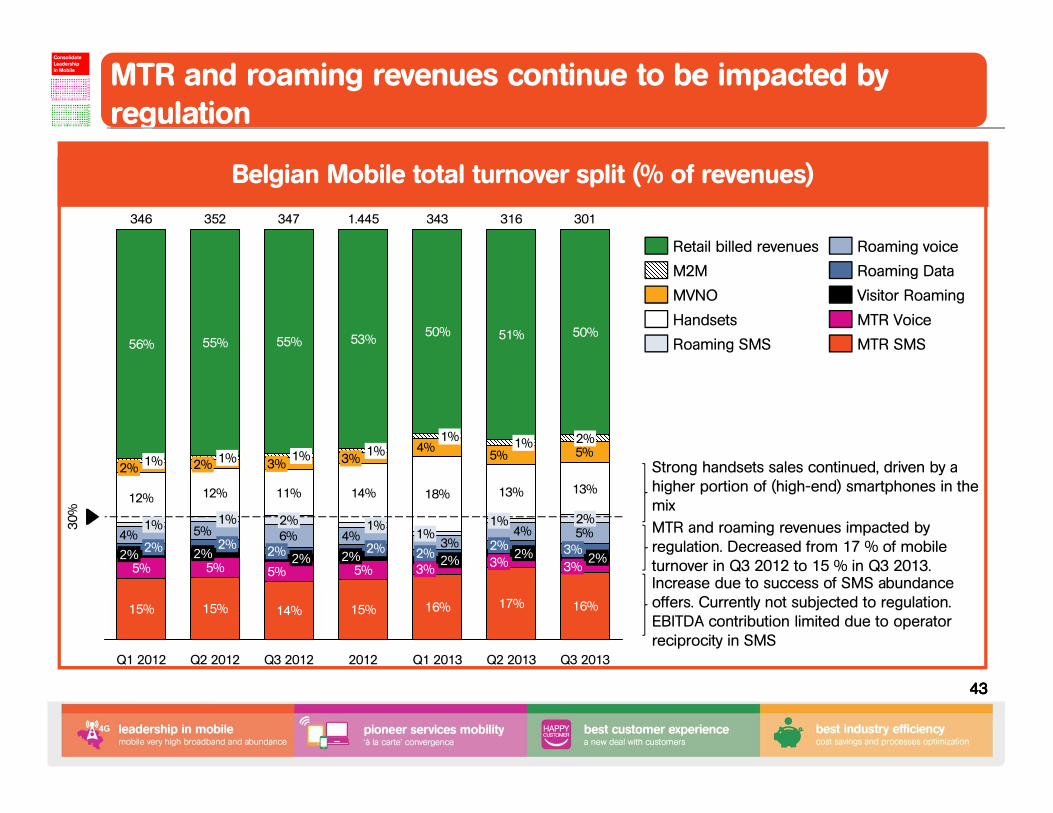

Belgian Mobile total turnover split (% of revenues)

6%

12% 12% 11% 14% 18% 13% 13%

5%4%3%

5%4% 4%

5%5%4%

50%

343

Q3 2012

347

14%

5%2%2%

2%

3%1%

55%

3%

Q1 2013

16%

2%2%

1%

1%

30

%

Q3 2013

301

16%

3%2%

3%

2%

2%

50%

Q2 2013

316

17%

3%2%

2%

1%

1%

51%

2012

1.445

15%

5%2%

2%

1%

3%1%

53%

Q1 2012 Q2 2012

15%

5%2% 2%

2%

1%

1%

56%

346

15%

5%2%

2%

1%

2% 1%

55%

352

Roaming SMS

Handsets

MVNO

M2M

Retail billed revenues

MTR SMS

MTR Voice

Visitor Roaming

Roaming Data

Roaming voice

Increase due to success of SMS abundance offers. Currently not subjected to regulation. EBITDA contribution limited due to operator reciprocity in SMS

MTR and roaming revenues impacted by regulation. Decreased from 17 % of mobile turnover in Q3 2012 to 15 % in Q3 2013.

Strong handsets sales continued, driven by a higher portion of (high-end) smartphones in the mix

MTR and roaming revenues continue to be impacted by regulationBest-in-class

Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

44444444

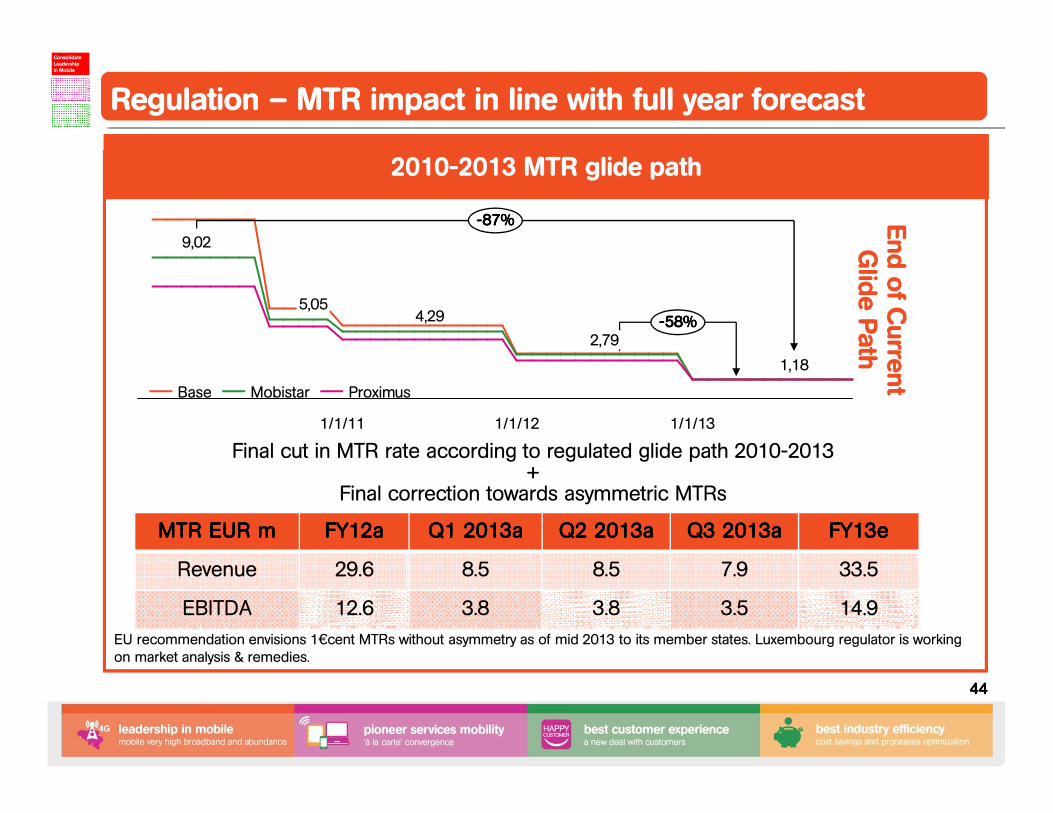

2010-2013 MTR glide path

----58%58%58%58%

----87%87%87%87%

1,18

1/1/13

2,79

1/1/12

4,29

1/1/11

5,05

9,02

ProximusMobistarBase

End ofCurrent

Glide Path

MTR EUR mMTR EUR mMTR EUR mMTR EUR m FY12aFY12aFY12aFY12a Q1 2013aQ1 2013aQ1 2013aQ1 2013a Q2 2013aQ2 2013aQ2 2013aQ2 2013a Q3 2013aQ3 2013aQ3 2013aQ3 2013a FY13eFY13eFY13eFY13e

Revenue 29.6 8.5 8.5 7.9 33.5

EBITDA 12.6 3.8 3.8 3.5 14.9

Final cut in MTR rate according to regulated glide path 2010-2013+

Final correction towards asymmetric MTRs

EU recommendation envisions 1€cent MTRs without asymmetry as of mid 2013 to its member states. Luxembourg regulator is working on market analysis & remedies.

Regulation – MTR impact in line with full year forecastBest-in-class Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

45454545

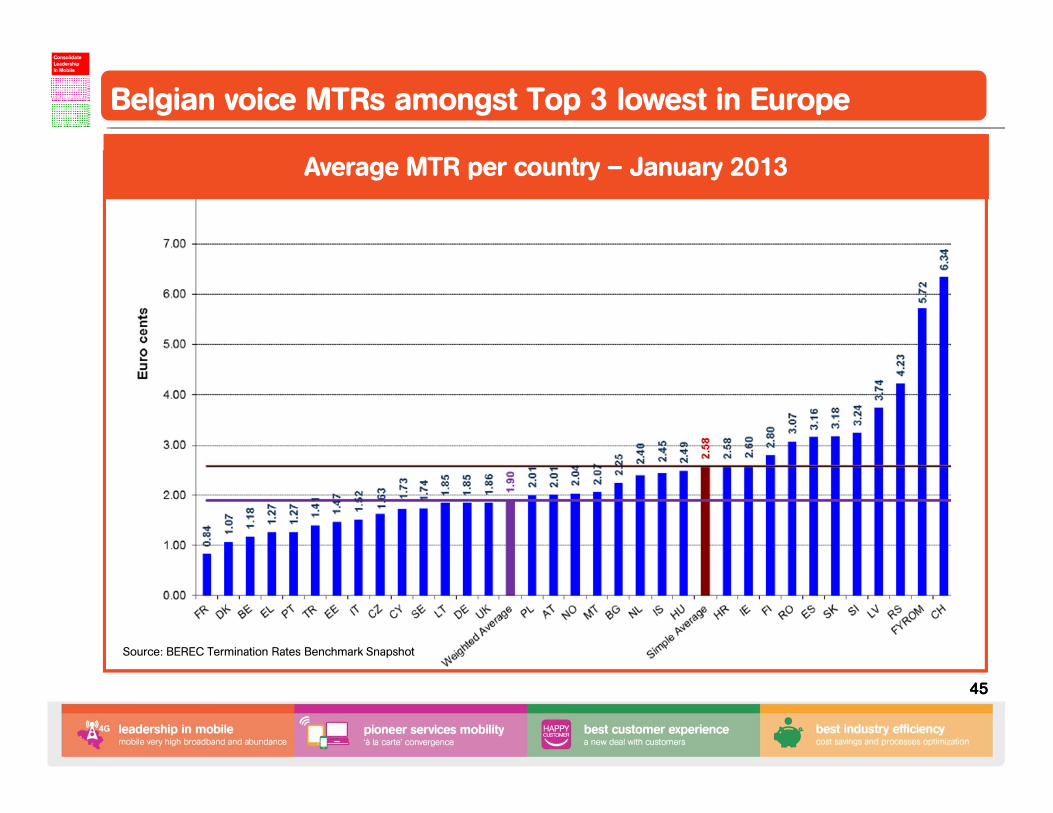

Average MTR per country – January 2013

Source: BEREC Termination Rates Benchmark Snapshot

Belgian voice MTRs amongst Top 3 lowest in EuropeBest-in-class Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

46464646

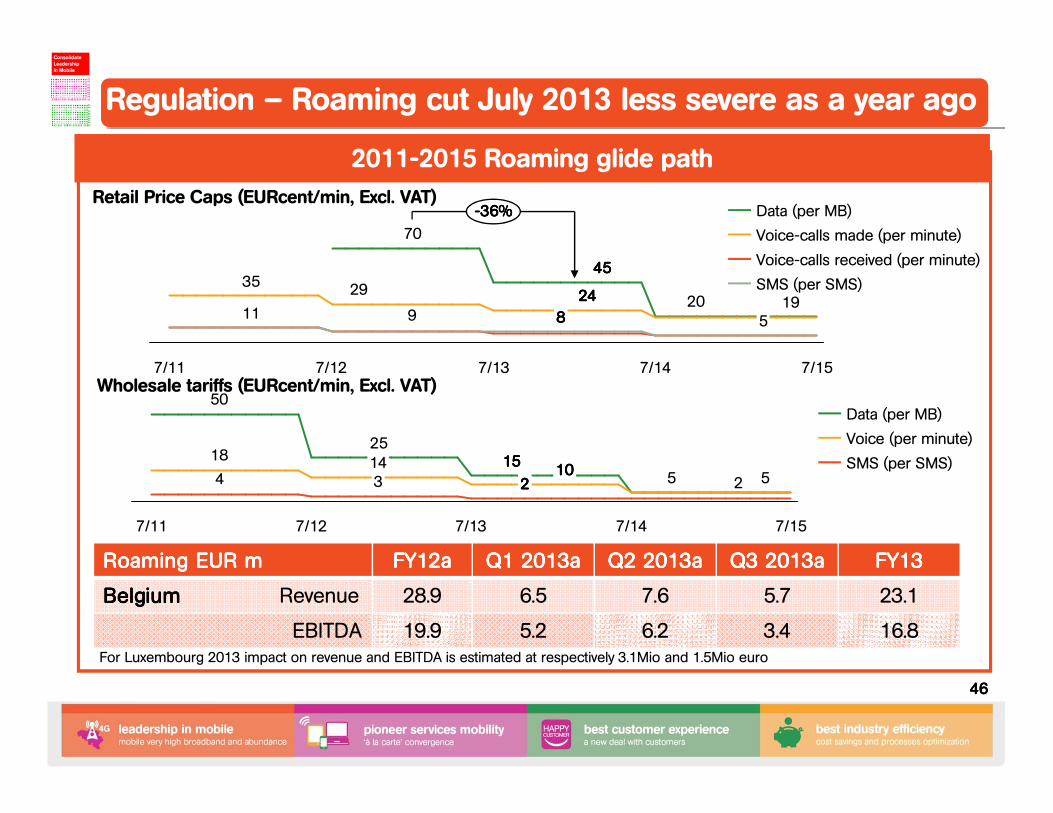

2011-2015 Roaming glide path

Roaming EURRoaming EURRoaming EURRoaming EUR mmmm FY12aFY12aFY12aFY12a Q1 2013aQ1 2013aQ1 2013aQ1 2013a Q2 2013aQ2 2013aQ2 2013aQ2 2013a Q3 2013aQ3 2013aQ3 2013aQ3 2013a FY13FY13FY13FY13

BelgiumBelgiumBelgiumBelgium Revenue 28.9 6.5 7.6 5.7 23.1

EBITDA 19.9 5.2 6.2 3.4 16.8

20

45454545

70

19242424242935

911

----36%36%36%36%

7/15

5

7/14

8888

7/137/127/11

SMS (per SMS)

Voice-calls received (per minute)

Voice-calls made (per minute)

Data (per MB)

515151515

25

50

5

18

24

7/157/14

101010102222

7/13

314

7/127/11

SMS (per SMS)

Voice (per minute)

Data (per MB)

Retail Price Caps (EURcent/min, Excl. VAT)

Wholesale tariffs (EURcent/min, Excl. VAT)

For Luxembourg 2013 impact on revenue and EBITDA is estimated at respectively 3.1Mio and 1.5Mio euro

Regulation – Roaming cut July 2013 less severe as a year agoBest-in-class Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

47474747

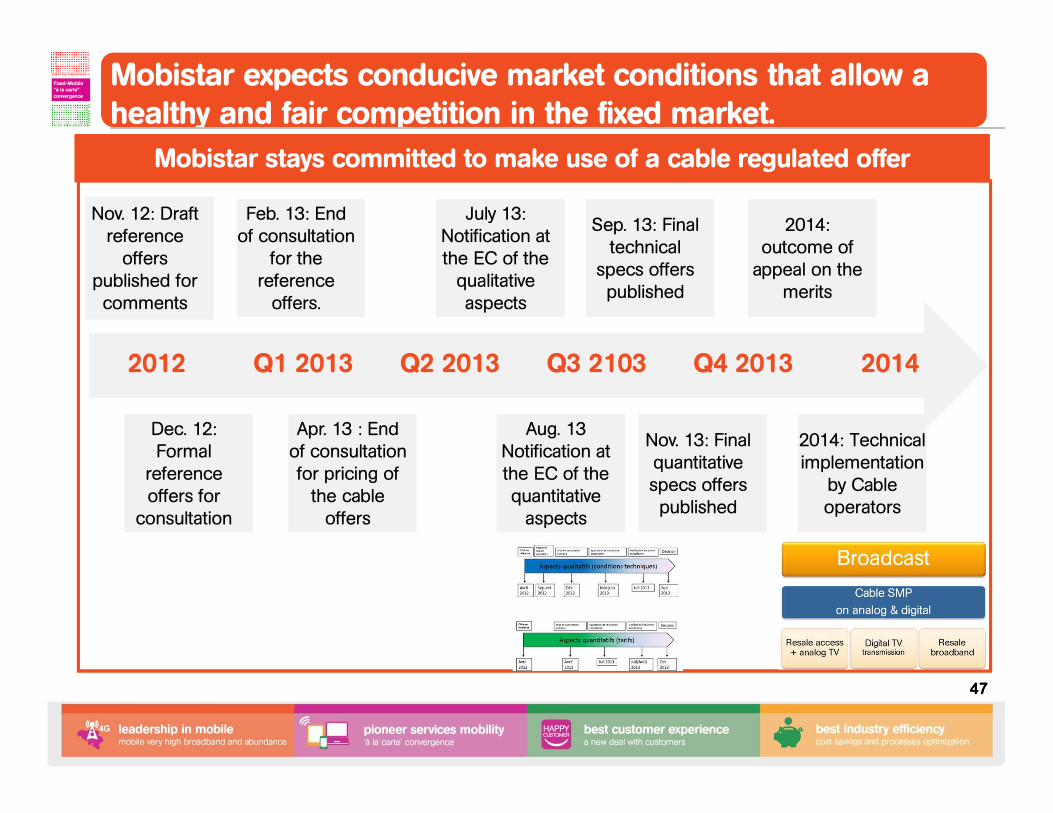

Mobistar expects conducive market conditions that allow a healthy and fair competition in the fixed market. Best-in-class

Customer Experience

ConsolidateLeadershipin Mobile

Fixed-Mobile“à la carte” convergence

Nov. 12: Draft reference

offers published for

comments

Nov. 12: Draft reference

offers published for

comments

Feb. 13: End of consultation

for the reference

offers.

Feb. 13: End of consultation

for the reference

offers.

July 13: Notification at the EC of the

qualitative aspects

July 13: Notification at the EC of the

qualitative aspects

Sep. 13: Final technical

specs offers published

Sep. 13: Final technical

specs offers published

2014: outcome of

appeal on the merits

2014: outcome of

appeal on the merits

Q3 2103 Q4 2013 20142012 Q1 2013 Q2 2013

Dec. 12: Formal

reference offers for

consultation

Dec. 12: Formal

reference offers for

consultation

Apr. 13 : End of consultation

for pricing of the cable

offers

Apr. 13 : End of consultation

for pricing of the cable

offers

Aug. 13 Notification at the EC of the

quantitative aspects

Aug. 13 Notification at the EC of the

quantitative aspects

Nov. 13: Final quantitative

specs offers published

Nov. 13: Final quantitative

specs offers published

2014: Technical implementation

by Cable operators

2014: Technical implementation

by Cable operators

Mobistar stays committed to make use of a cable regulated offer

48484848

Detailed cash flow analysis

FINANCIAL

PERFORMANCE

49494949

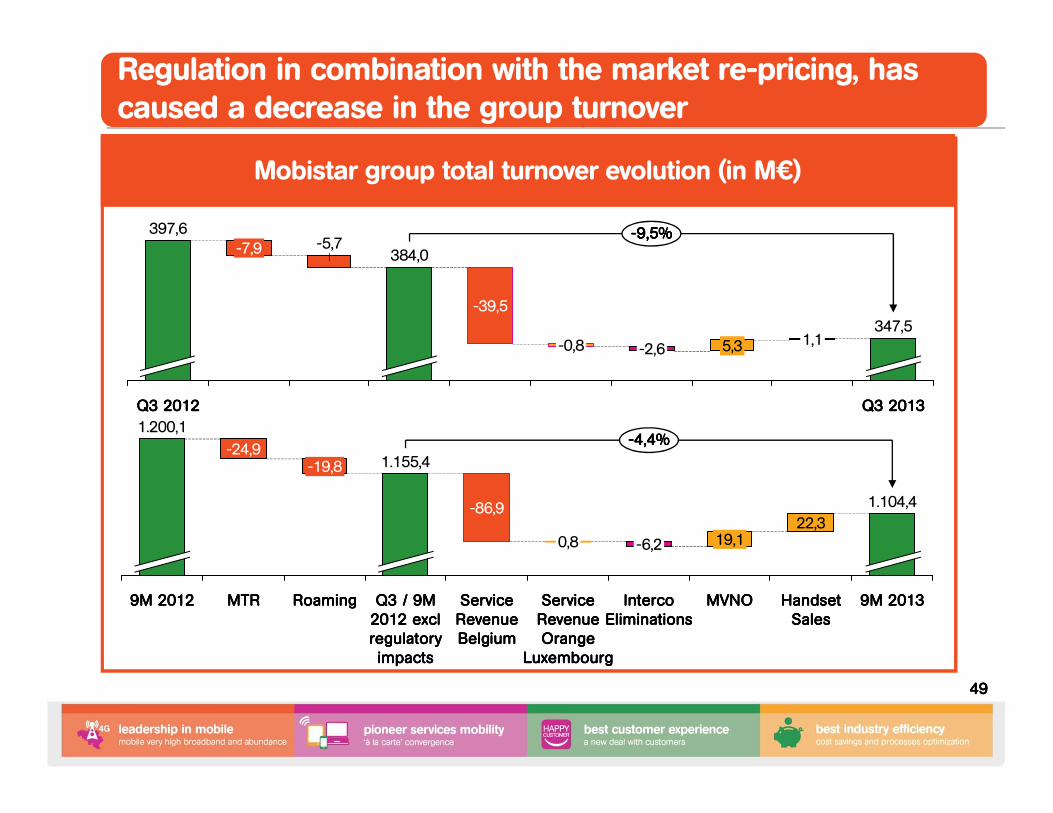

Regulation in combination with the market re-pricing, has caused a decrease in the group turnover

Mobistar group total turnover evolution (in M€)

1.200,1

-24,9

MTRMTRMTRMTR9M 20129M 20129M 20129M 2012

----4,4%4,4%4,4%4,4%

1.104,4

Handset Handset Handset Handset SalesSalesSalesSales

22,3

RoamingRoamingRoamingRoaming

-19,8

Q3 / 9M Q3 / 9M Q3 / 9M Q3 / 9M 2012 excl 2012 excl 2012 excl 2012 excl regulatory regulatory regulatory regulatory

impactsimpactsimpactsimpacts

1.155,4

-86,9

Service Service Service Service Revenue Revenue Revenue Revenue BelgiumBelgiumBelgiumBelgium

0,8

Service Service Service Service Revenue Revenue Revenue Revenue Orange Orange Orange Orange

LuxembourgLuxembourgLuxembourgLuxembourg

9M 20139M 20139M 20139M 2013

-6,2

Interco Interco Interco Interco EliminationsEliminationsEliminationsEliminations

19,1

MVNOMVNOMVNOMVNO

----9,5%9,5%9,5%9,5%397,6-5,7

Q3 2012Q3 2012Q3 2012Q3 2012

384,0

-39,5

-0,8 -2,6 5,3 1,1347,5

Q3 2013Q3 2013Q3 2013Q3 2013

-7,9

50505050

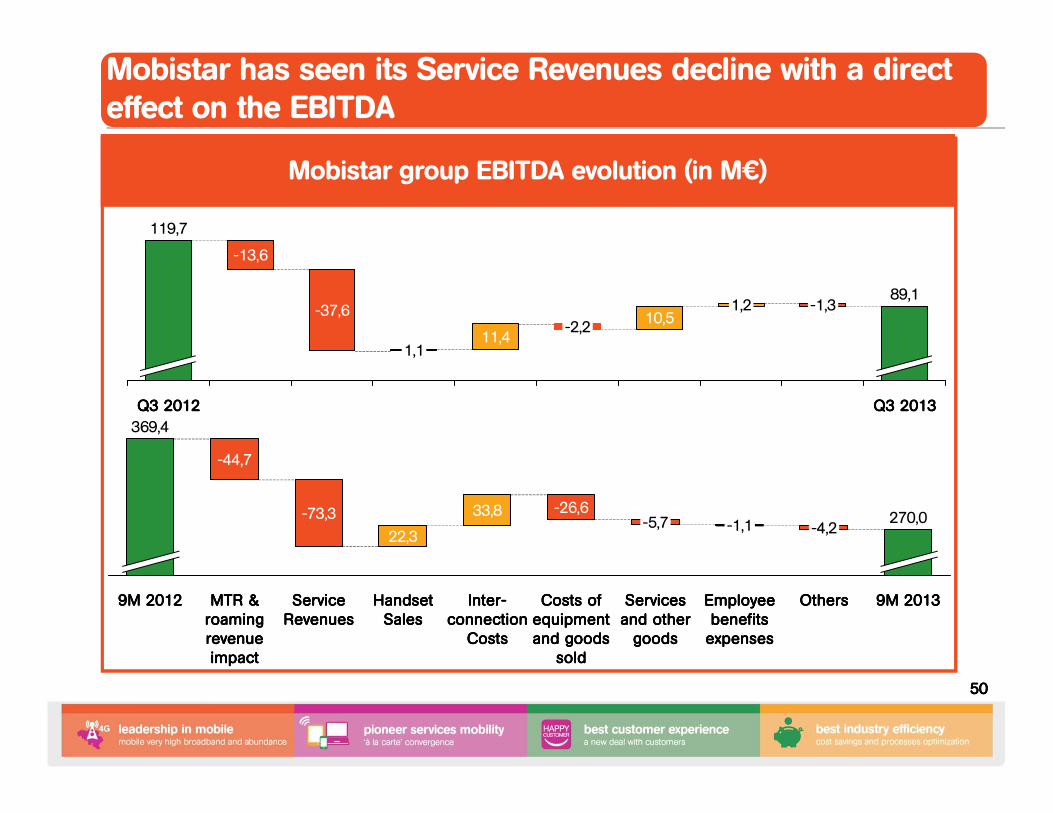

Mobistar has seen its Service Revenues decline with a direct effect on the EBITDA

Mobistar group EBITDA evolution (in M€)

9M 20139M 20139M 20139M 2013

270,0

OthersOthersOthersOthers

-4,2

Employee Employee Employee Employee benefits benefits benefits benefits

expensesexpensesexpensesexpenses

-1,1

Services Services Services Services and other and other and other and other

goodsgoodsgoodsgoods

-5,7

Costs of Costs of Costs of Costs of equipment equipment equipment equipment and goods and goods and goods and goods

soldsoldsoldsold

-26,6

InterInterInterInter----connection connection connection connection

CostsCostsCostsCosts

33,8

Handset Handset Handset Handset SalesSalesSalesSales

22,3

Service Service Service Service RevenuesRevenuesRevenuesRevenues

-73,3

MTR & MTR & MTR & MTR & roaming roaming roaming roaming revenue revenue revenue revenue impactimpactimpactimpact

-44,7

9M 20129M 20129M 20129M 2012

369,4

Q3 2013Q3 2013Q3 2013Q3 2013

89,1-1,31,2

10,5-2,2

11,41,1

-37,6

-13,6

Q3 2012Q3 2012Q3 2012Q3 2012

119,7

51515151

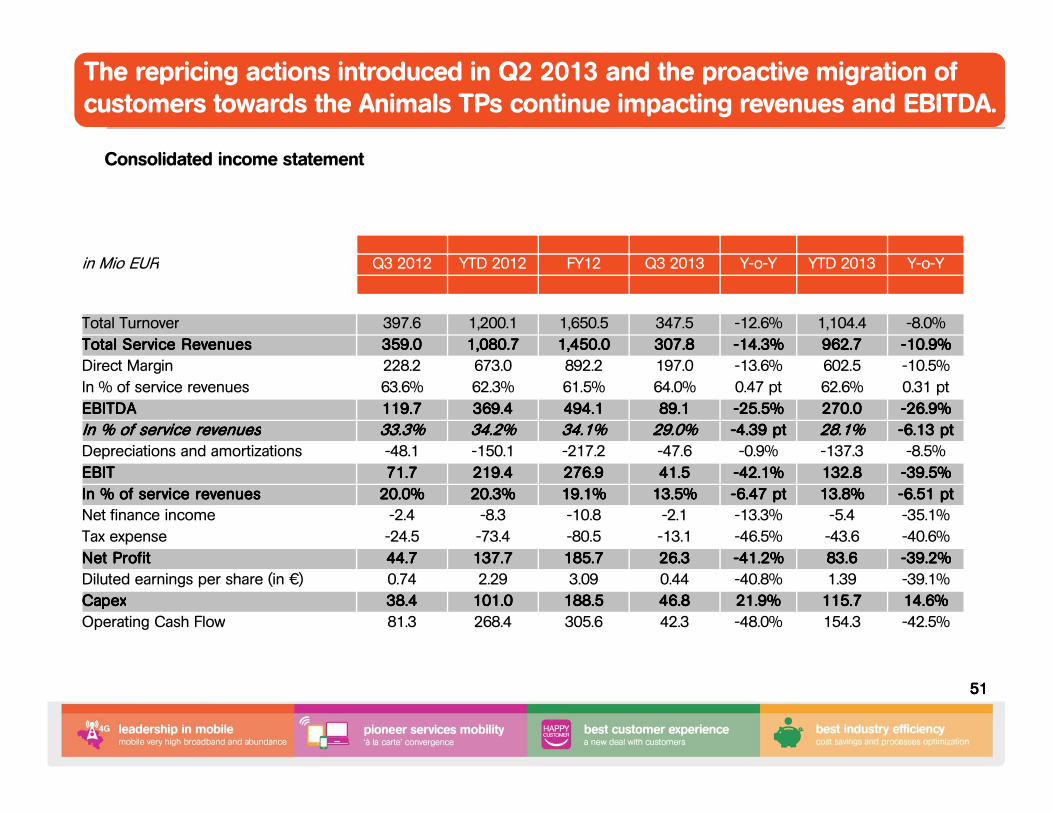

The repricing actions introduced in Q2 2013 and the proactive migration of customers towards the Animals TPs continue impacting revenues and EBITDA.

Consolidated income statement

in Mio EUR Q3 2012 YTD 2012 FY12 Q3 2013 Y-o-Y YTD 2013 Y-o-Y

Total Turnover 397.6 1,200.1 1,650.5 347.5 -12.6% 1,104.4 -8.0%

Total Service RevenuesTotal Service RevenuesTotal Service RevenuesTotal Service Revenues 359.0359.0359.0359.0 1,080.71,080.71,080.71,080.7 1,450.01,450.01,450.01,450.0 307.8307.8307.8307.8 ----14.3%14.3%14.3%14.3% 962.7962.7962.7962.7 ----10.9%10.9%10.9%10.9%

Direct Margin 228.2 673.0 892.2 197.0 -13.6% 602.5 -10.5%

In % of service revenues 63.6% 62.3% 61.5% 64.0% 0.47 pt 62.6% 0.31 pt

EBITDA EBITDA EBITDA EBITDA 119.7119.7119.7119.7 369.4369.4369.4369.4 494.1494.1494.1494.1 89.189.189.189.1 ----25.5%25.5%25.5%25.5% 270.0270.0270.0270.0 ----26.9%26.9%26.9%26.9%

In % of service revenuesIn % of service revenuesIn % of service revenuesIn % of service revenues 33.3%33.3%33.3%33.3% 34.2%34.2%34.2%34.2% 34.1%34.1%34.1%34.1% 29.0%29.0%29.0%29.0% ----4.39 pt4.39 pt4.39 pt4.39 pt 28.1%28.1%28.1%28.1% ----6.13 pt6.13 pt6.13 pt6.13 pt

Depreciations and amortizations -48.1 -150.1 -217.2 -47.6 -0.9% -137.3 -8.5%

EBITEBITEBITEBIT 71.771.771.771.7 219.4219.4219.4219.4 276.9276.9276.9276.9 41.541.541.541.5 ----42.1%42.1%42.1%42.1% 132.8132.8132.8132.8 ----39.5%39.5%39.5%39.5%

In % of service revenuesIn % of service revenuesIn % of service revenuesIn % of service revenues 20.0%20.0%20.0%20.0% 20.3%20.3%20.3%20.3% 19.1%19.1%19.1%19.1% 13.5%13.5%13.5%13.5% ----6.47 pt6.47 pt6.47 pt6.47 pt 13.8%13.8%13.8%13.8% ----6.51 pt6.51 pt6.51 pt6.51 pt

Net finance income -2.4 -8.3 -10.8 -2.1 -13.3% -5.4 -35.1%

Tax expense -24.5 -73.4 -80.5 -13.1 -46.5% -43.6 -40.6%

Net ProfitNet ProfitNet ProfitNet Profit 44.744.744.744.7 137.7137.7137.7137.7 185.7185.7185.7185.7 26.326.326.326.3 ----41.2%41.2%41.2%41.2% 83.683.683.683.6 ----39.2%39.2%39.2%39.2%

Diluted earnings per share (in €) 0.74 2.29 3.09 0.44 -40.8% 1.39 -39.1%

CapexCapexCapexCapex 38.438.438.438.4 101.0101.0101.0101.0 188.5188.5188.5188.5 46.846.846.846.8 21.9%21.9%21.9%21.9% 115.7115.7115.7115.7 14.6%14.6%14.6%14.6%

Operating Cash Flow 81.3 268.4 305.6 42.3 -48.0% 154.3 -42.5%

52525252

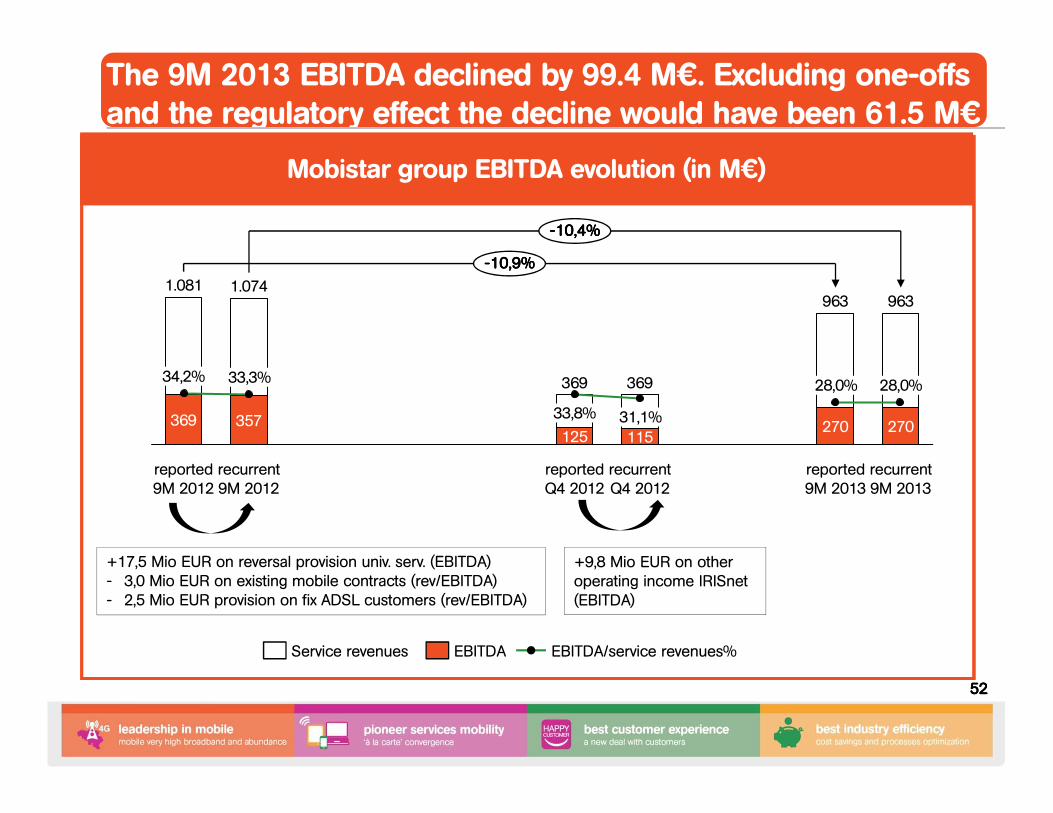

The 9M 2013 EBITDA declined by 99.4 M€. Excluding one-offs and the regulatory effect the decline would have been 61.5 M€euro

28,0%

125

1.074

270

reported 9M 2013

369

31,1%270

recurrent Q4 2012

reported Q4 2012

28,0%

115

33,8%

recurrent 9M 2012

----10,4%10,4%10,4%10,4%

369

recurrent 9M 2013

963

369

963

33,3%

357

reported 9M 2012

1.081

34,2%

----10,9%10,9%10,9%10,9%

EBITDA/service revenues%EBITDAService revenues

+17,5 Mio EUR on reversal provision univ. serv. (EBITDA)- 3,0 Mio EUR on existing mobile contracts (rev/EBITDA)- 2,5 Mio EUR provision on fix ADSL customers (rev/EBITDA)

+9,8 Mio EUR on other operating income IRISnet (EBITDA)

Mobistar group EBITDA evolution (in M€)

53535353

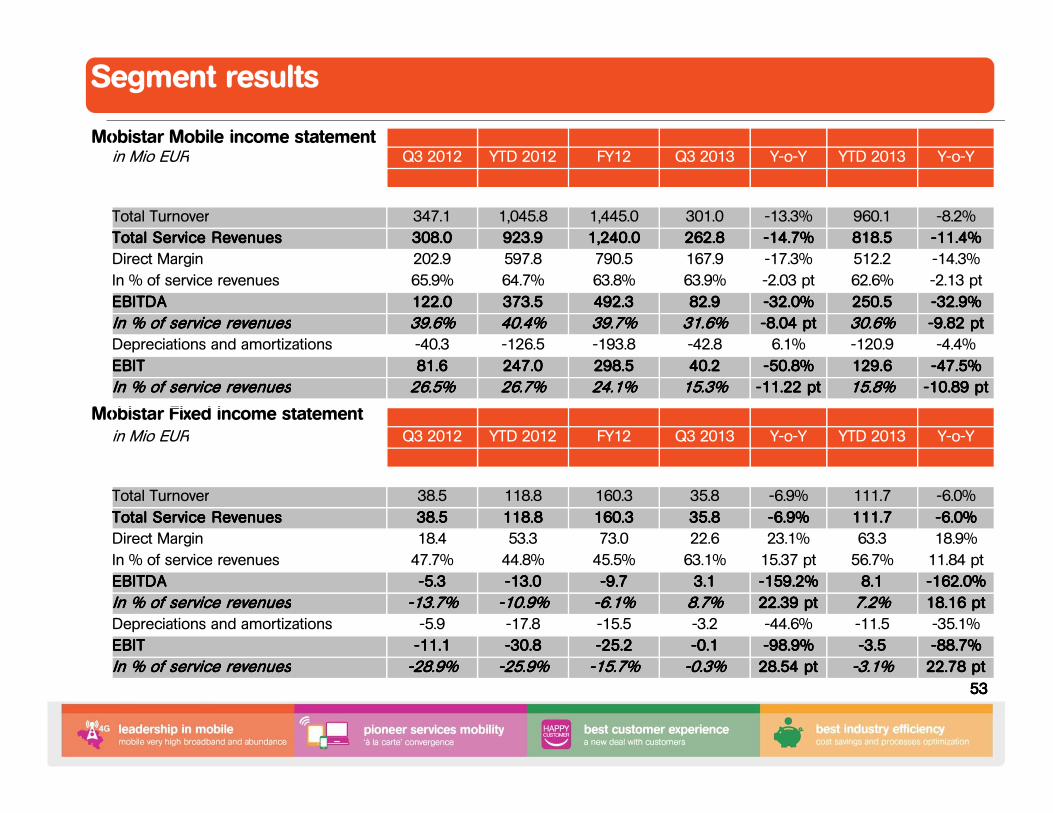

Segment results

Mobistar Mobile income statement

Mobistar Fixed income statement

in Mio EUR Q3 2012 YTD 2012 FY12 Q3 2013 Y-o-Y YTD 2013 Y-o-Y

Total Turnover 347.1 1,045.8 1,445.0 301.0 -13.3% 960.1 -8.2%

Total Service RevenuesTotal Service RevenuesTotal Service RevenuesTotal Service Revenues 308.0308.0308.0308.0 923.9923.9923.9923.9 1,240.01,240.01,240.01,240.0 262.8262.8262.8262.8 ----14.7%14.7%14.7%14.7% 818.5818.5818.5818.5 ----11.4%11.4%11.4%11.4%

Direct Margin 202.9 597.8 790.5 167.9 -17.3% 512.2 -14.3%

In % of service revenues 65.9% 64.7% 63.8% 63.9% -2.03 pt 62.6% -2.13 pt

EBITDA EBITDA EBITDA EBITDA 122.0122.0122.0122.0 373.5373.5373.5373.5 492.3492.3492.3492.3 82.982.982.982.9 ----32.0%32.0%32.0%32.0% 250.5250.5250.5250.5 ----32.9%32.9%32.9%32.9%

In % of service revenuesIn % of service revenuesIn % of service revenuesIn % of service revenues 39.6%39.6%39.6%39.6% 40.4%40.4%40.4%40.4% 39.7%39.7%39.7%39.7% 31.6%31.6%31.6%31.6% ----8.04 pt8.04 pt8.04 pt8.04 pt 30.6%30.6%30.6%30.6% ----9.82 pt9.82 pt9.82 pt9.82 pt

Depreciations and amortizations -40.3 -126.5 -193.8 -42.8 6.1% -120.9 -4.4%

EBITEBITEBITEBIT 81.681.681.681.6 247.0247.0247.0247.0 298.5298.5298.5298.5 40.240.240.240.2 ----50.8%50.8%50.8%50.8% 129.6129.6129.6129.6 ----47.5%47.5%47.5%47.5%

In % of service revenuesIn % of service revenuesIn % of service revenuesIn % of service revenues 26.5%26.5%26.5%26.5% 26.7%26.7%26.7%26.7% 24.1%24.1%24.1%24.1% 15.3%15.3%15.3%15.3% ----11.22 pt11.22 pt11.22 pt11.22 pt 15.8%15.8%15.8%15.8% ----10.89 10.89 10.89 10.89 ptptptpt

in Mio EUR Q3 2012 YTD 2012 FY12 Q3 2013 Y-o-Y YTD 2013 Y-o-Y

Total Turnover 38.5 118.8 160.3 35.8 -6.9% 111.7 -6.0%

Total Service RevenuesTotal Service RevenuesTotal Service RevenuesTotal Service Revenues 38.538.538.538.5 118.8118.8118.8118.8 160.3160.3160.3160.3 35.835.835.835.8 ----6.9%6.9%6.9%6.9% 111.7111.7111.7111.7 ----6.0%6.0%6.0%6.0%

Direct Margin 18.4 53.3 73.0 22.6 23.1% 63.3 18.9%

In % of service revenues 47.7% 44.8% 45.5% 63.1% 15.37 pt 56.7% 11.84 pt

EBITDA EBITDA EBITDA EBITDA ----5.35.35.35.3 ----13.013.013.013.0 ----9.79.79.79.7 3.13.13.13.1 ----159.2%159.2%159.2%159.2% 8.18.18.18.1 ----162.0%162.0%162.0%162.0%

In % of service revenuesIn % of service revenuesIn % of service revenuesIn % of service revenues ----13.7%13.7%13.7%13.7% ----10.9%10.9%10.9%10.9% ----6.1%6.1%6.1%6.1% 8.7%8.7%8.7%8.7% 22.39 pt22.39 pt22.39 pt22.39 pt 7.2%7.2%7.2%7.2% 18.16 pt18.16 pt18.16 pt18.16 pt

Depreciations and amortizations -5.9 -17.8 -15.5 -3.2 -44.6% -11.5 -35.1%

EBITEBITEBITEBIT ----11.111.111.111.1 ----30.830.830.830.8 ----25.225.225.225.2 ----0.10.10.10.1 ----98.9%98.9%98.9%98.9% ----3.53.53.53.5 ----88.7%88.7%88.7%88.7%

In % of service revenuesIn % of service revenuesIn % of service revenuesIn % of service revenues ----28.9%28.9%28.9%28.9% ----25.9%25.9%25.9%25.9% ----15.7%15.7%15.7%15.7% ----0.3%0.3%0.3%0.3% 28.54 pt28.54 pt28.54 pt28.54 pt ----3.1%3.1%3.1%3.1% 22.78 22.78 22.78 22.78 ptptptpt

54545454

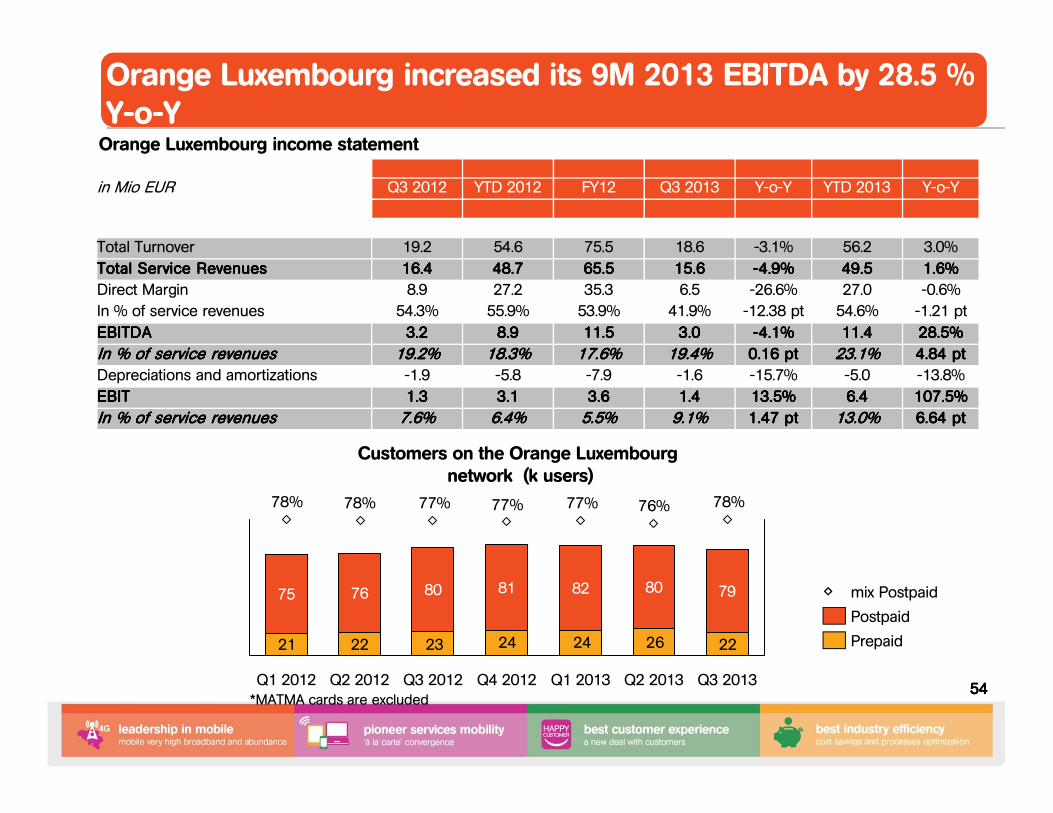

Orange Luxembourg increased its 9M 2013 EBITDA by 28.5 % Y-o-YOrange Luxembourg income statement

22262424232221

78%76%77%77%77%78%78%

80

Q1 2013

82

Q4 2012

81

Q3 2012

80

Q2 2012

76

Q1 2012

75

Q3 2013

79

Q2 2013

mix Postpaid

Prepaid

Postpaid

Customers on the Orange Luxembourg network (k users)

*MATMA cards are excluded

in Mio EUR Q3 2012 YTD 2012 FY12 Q3 2013 Y-o-Y YTD 2013 Y-o-Y

Total Turnover 19.2 54.6 75.5 18.6 -3.1% 56.2 3.0%

Total Service RevenuesTotal Service RevenuesTotal Service RevenuesTotal Service Revenues 16.416.416.416.4 48.748.748.748.7 65.565.565.565.5 15.615.615.615.6 ----4.9%4.9%4.9%4.9% 49.549.549.549.5 1.6%1.6%1.6%1.6%

Direct Margin 8.9 27.2 35.3 6.5 -26.6% 27.0 -0.6%

In % of service revenues 54.3% 55.9% 53.9% 41.9% -12.38 pt 54.6% -1.21 pt

EBITDA EBITDA EBITDA EBITDA 3.23.23.23.2 8.98.98.98.9 11.511.511.511.5 3.03.03.03.0 ----4.1%4.1%4.1%4.1% 11.411.411.411.4 28.5%28.5%28.5%28.5%

In % of service revenuesIn % of service revenuesIn % of service revenuesIn % of service revenues 19.2%19.2%19.2%19.2% 18.3%18.3%18.3%18.3% 17.6%17.6%17.6%17.6% 19.4%19.4%19.4%19.4% 0.16 pt0.16 pt0.16 pt0.16 pt 23.1%23.1%23.1%23.1% 4.84 pt4.84 pt4.84 pt4.84 pt

Depreciations and amortizations -1.9 -5.8 -7.9 -1.6 -15.7% -5.0 -13.8%

EBITEBITEBITEBIT 1.31.31.31.3 3.13.13.13.1 3.63.63.63.6 1.41.41.41.4 13.5%13.5%13.5%13.5% 6.46.46.46.4 107.5%107.5%107.5%107.5%

In % of service revenuesIn % of service revenuesIn % of service revenuesIn % of service revenues 7.6%7.6%7.6%7.6% 6.4%6.4%6.4%6.4% 5.5%5.5%5.5%5.5% 9.1%9.1%9.1%9.1% 1.47 pt1.47 pt1.47 pt1.47 pt 13.0%13.0%13.0%13.0% 6.64 6.64 6.64 6.64 ptptptpt

55555555

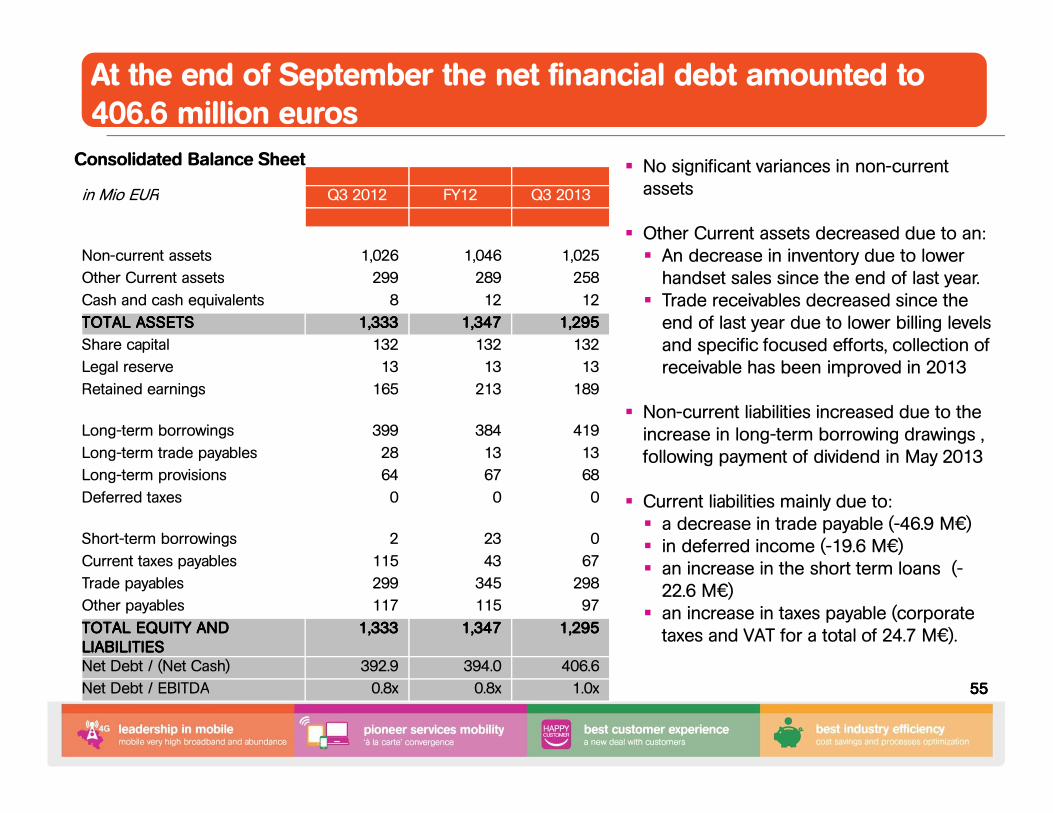

At the end of September the net financial debt amounted to 406.6 million euros

Consolidated Balance Sheet� No significant variances in non-current

assets

� Other Current assets decreased due to an:� An decrease in inventory due to lower

handset sales since the end of last year.� Trade receivables decreased since the

end of last year due to lower billing levels and specific focused efforts, collection of receivable has been improved in 2013

� Non-current liabilities increased due to the increase in long-term borrowing drawings , following payment of dividend in May 2013

� Current liabilities mainly due to:� a decrease in trade payable (-46.9 M€) � in deferred income (-19.6 M€) � an increase in the short term loans (-

22.6 M€) � an increase in taxes payable (corporate

taxes and VAT for a total of 24.7 M€).

in Mio EUR Q3 2012 FY12 Q3 2013

Non-current assets 1,026 1,046 1,025

Other Current assets 299 289 258

Cash and cash equivalents 8 12 12

TOTAL ASSETSTOTAL ASSETSTOTAL ASSETSTOTAL ASSETS 1,3331,3331,3331,333 1,3471,3471,3471,347 1,2951,2951,2951,295

Share capital 132 132 132

Legal reserve 13 13 13

Retained earnings 165 213 189

Long-term borrowings 399 384 419

Long-term trade payables 28 13 13

Long-term provisions 64 67 68

Deferred taxes 0 0 0

Short-term borrowings 2 23 0

Current taxes payables 115 43 67

Trade payables 299 345 298

Other payables 117 115 97

TOTAL EQUITY AND TOTAL EQUITY AND TOTAL EQUITY AND TOTAL EQUITY AND LIABILITIESLIABILITIESLIABILITIESLIABILITIES

1,3331,3331,3331,333 1,3471,3471,3471,347 1,2951,2951,2951,295

Net Debt / (Net Cash) 392.9 394.0 406.6

Net Debt / EBITDA 0.8x 0.8x 1.0x

56565656

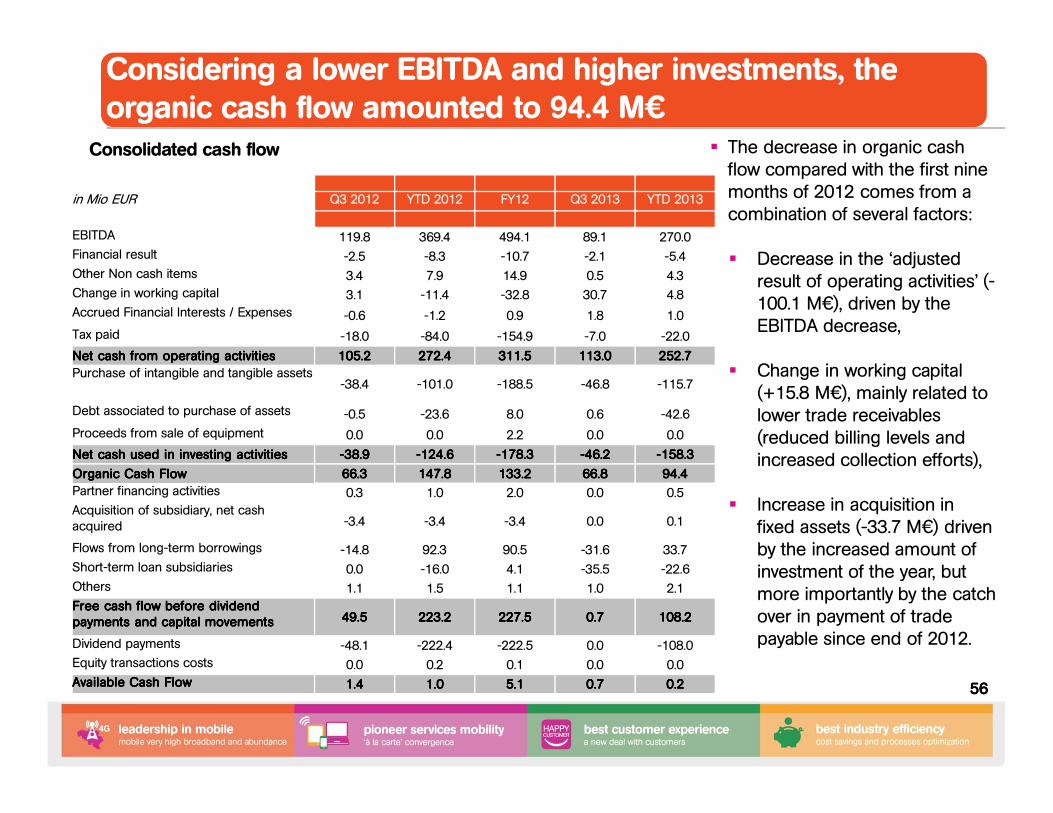

Considering a lower EBITDA and higher investments, the organic cash flow amounted to 94.4 M€

Consolidated cash flow � The decrease in organic cash flow compared with the first nine months of 2012 comes from acombination of several factors:

� Decrease in the ‘adjusted result of operating activities’ (-100.1 M€), driven by the EBITDA decrease,

� Change in working capital (+15.8 M€), mainly related to lower trade receivables (reduced billing levels and increased collection efforts),

� Increase in acquisition in fixed assets (-33.7 M€) driven by the increased amount of investment of the year, but more importantly by the catch over in payment of trade payable since end of 2012.

in Mio EUR Q3 2012 YTD 2012 FY12 Q3 2013 YTD 2013

EBITDA 119.8 369.4 494.1 89.1 270.0

Financial result -2.5 -8.3 -10.7 -2.1 -5.4

Other Non cash items 3.4 7.9 14.9 0.5 4.3

Change in working capital 3.1 -11.4 -32.8 30.7 4.8

Accrued Financial Interests / Expenses -0.6 -1.2 0.9 1.8 1.0

Tax paid -18.0 -84.0 -154.9 -7.0 -22.0

Net cash from operating activities Net cash from operating activities Net cash from operating activities Net cash from operating activities 105.2105.2105.2105.2 272.4272.4272.4272.4 311.5311.5311.5311.5 113.0113.0113.0113.0 252.7252.7252.7252.7

Purchase of intangible and tangible assets-38.4 -101.0 -188.5 -46.8 -115.7

Debt associated to purchase of assets -0.5 -23.6 8.0 0.6 -42.6

Proceeds from sale of equipment 0.0 0.0 2.2 0.0 0.0

Net cash used in investing activitiesNet cash used in investing activitiesNet cash used in investing activitiesNet cash used in investing activities ----38.938.938.938.9 ----124.6124.6124.6124.6 ----178.3178.3178.3178.3 ----46.246.246.246.2 ----158.3158.3158.3158.3

Organic Cash FlowOrganic Cash FlowOrganic Cash FlowOrganic Cash Flow 66.366.366.366.3 147.8147.8147.8147.8 133.2133.2133.2133.2 66.866.866.866.8 94.494.494.494.4

Partner financing activities 0.3 1.0 2.0 0.0 0.5

Acquisition of subsidiary, net cash acquired -3.4 -3.4 -3.4 0.0 0.1

Flows from long-term borrowings -14.8 92.3 90.5 -31.6 33.7

Short-term loan subsidiaries 0.0 -16.0 4.1 -35.5 -22.6

Others 1.1 1.5 1.1 1.0 2.1

Free cash flow before dividend Free cash flow before dividend Free cash flow before dividend Free cash flow before dividend payments and capital movementspayments and capital movementspayments and capital movementspayments and capital movements 49.549.549.549.5 223.2223.2223.2223.2 227.5227.5227.5227.5 0.70.70.70.7 108.2108.2108.2108.2

Dividend payments -48.1 -222.4 -222.5 0.0 -108.0

Equity transactions costs 0.0 0.2 0.1 0.0 0.0

Available Cash FlowAvailable Cash FlowAvailable Cash FlowAvailable Cash Flow 1.41.41.41.4 1.01.01.01.0 5.15.15.15.1 0.70.70.70.7 0.20.20.20.2

57575757

2013 Outlook

58585858

Operational cash flow **

EBITDA *

Total Turnover

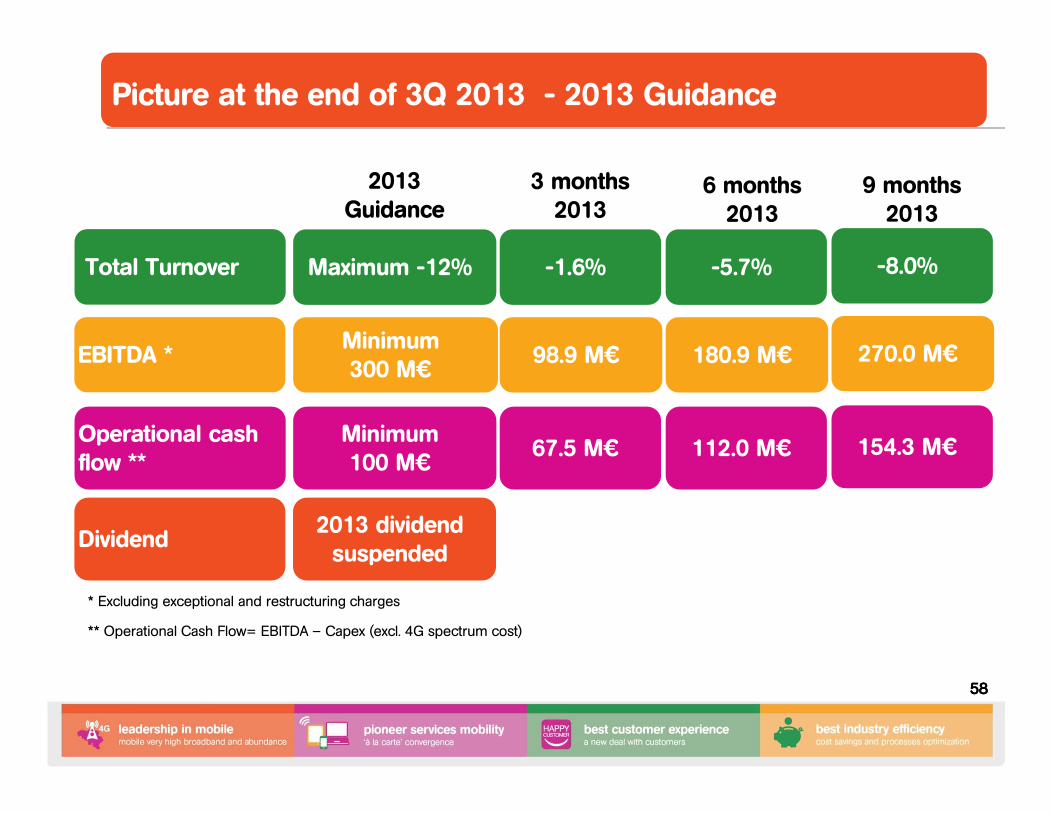

Picture at the end of 3Q 2013 - 2013 Guidance

-8.0%

154.3 M€

270.0 M€

2013 Guidance

* Excluding exceptional and restructuring charges

** Operational Cash Flow= EBITDA – Capex (excl. 4G spectrum cost)

Dividend

Maximum -12%

Minimum 100 M€

Minimum 300 M€

2013 dividend suspended

-1.6%

67.5 M€

98.9 M€

-5.7%

112.0 M€

180.9 M€

3 months 2013

6 months 2013

9 months 2013

59595959

Q&A

60606060

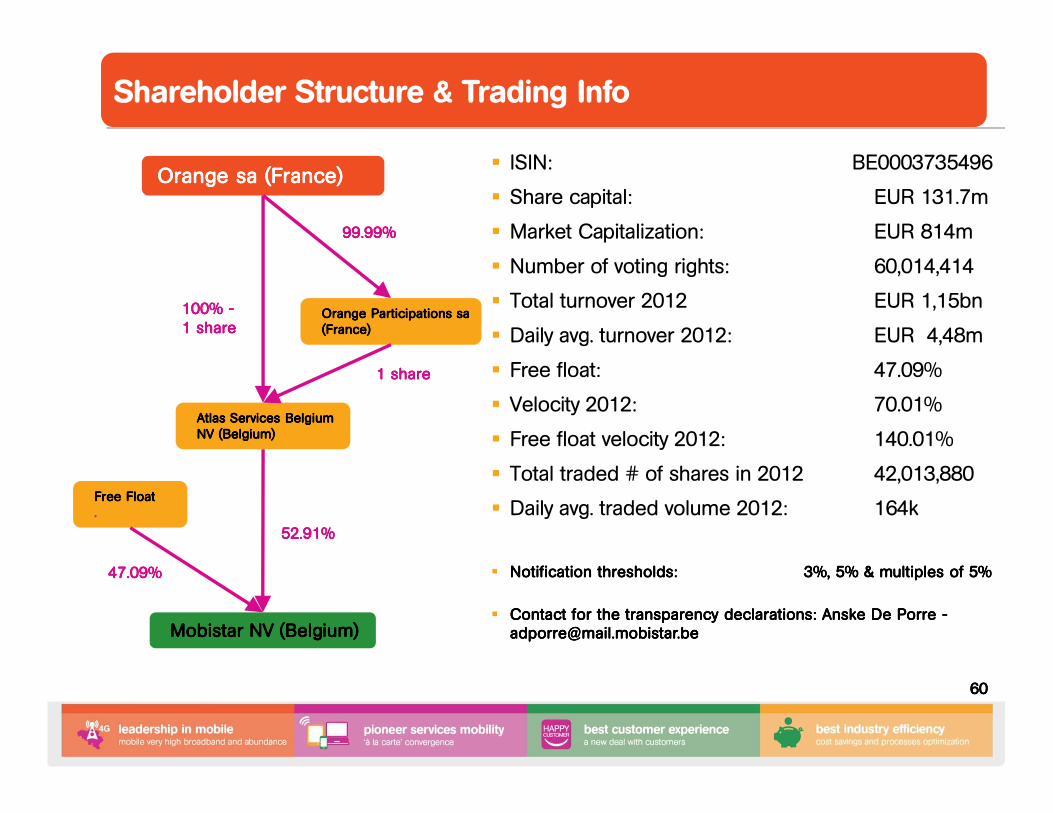

Shareholder Structure & Trading Info

Orange Orange Orange Orange sasasasa (France)(France)(France)(France)

Orange Participations Orange Participations Orange Participations Orange Participations sasasasa(France)(France)(France)(France)

Atlas Services Belgium Atlas Services Belgium Atlas Services Belgium Atlas Services Belgium NVNVNVNV (Belgium)(Belgium)(Belgium)(Belgium)

� ISIN: BE0003735496

� Share capital: EUR 131.7m

� Market Capitalization: EUR 814m

� Number of voting rights: 60,014,414

� Total turnover 2012 EUR 1,15bn

� Daily avg. turnover 2012: EUR 4,48m

� Free float: 47.09%

� Velocity 2012: 70.01%

� Free float velocity 2012: 140.01%

� Total traded # of shares in 2012 42,013,880

� Daily avg. traded volume 2012: 164k

� Notification thresholds: Notification thresholds: Notification thresholds: Notification thresholds: 3%, 5% & multiples of 5%3%, 5% & multiples of 5%3%, 5% & multiples of 5%3%, 5% & multiples of 5%

� Contact for the transparency declarations: Anske De Contact for the transparency declarations: Anske De Contact for the transparency declarations: Anske De Contact for the transparency declarations: Anske De PorrePorrePorrePorre [email protected]@[email protected]@mail.mobistar.be

Free Float Free Float Free Float Free Float . . . .

Mobistar NV (Belgium)Mobistar NV (Belgium)Mobistar NV (Belgium)Mobistar NV (Belgium)

52.91%52.91%52.91%52.91%

47.09%47.09%47.09%47.09%

99.99%99.99%99.99%99.99%

100% 100% 100% 100% ----1 share1 share1 share1 share

1 share1 share1 share1 share

61616161

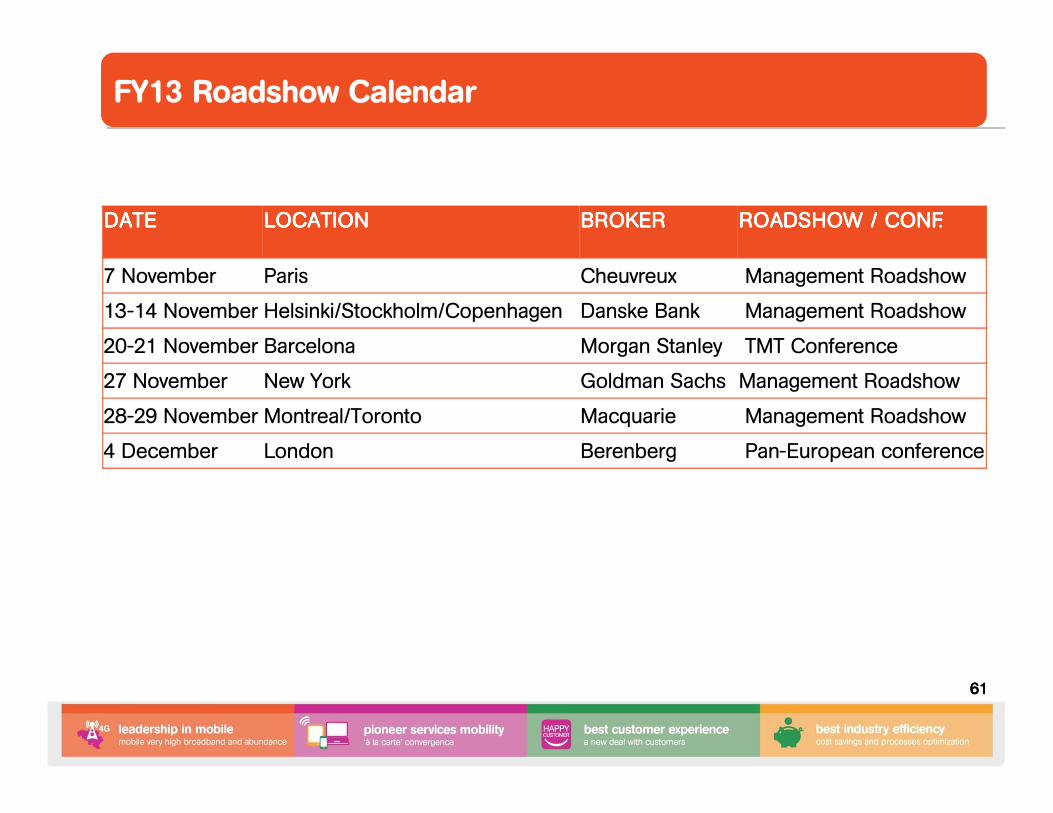

DATEDATEDATEDATE LOCATIONLOCATIONLOCATIONLOCATION BROKERBROKERBROKERBROKER ROADSHOW / ROADSHOW / ROADSHOW / ROADSHOW / CONF.CONF.CONF.CONF.

7 November Paris Cheuvreux Management Roadshow

13-14 November Helsinki/Stockholm/Copenhagen Danske Bank Management Roadshow

20-21 November Barcelona Morgan Stanley TMT Conference

27 November New York Goldman Sachs Management Roadshow

28-29 November Montreal/Toronto Macquarie Management Roadshow

4 December London Berenberg Pan-European conference

FY13 Roadshow Calendar

62626262

Visit our websites:• www.mobistar.be

• http://business.mobistar.be

• http://corporate.mobistar.be

For further questions please contact IR department

Investor Relations

Siddy JobeEmail: [email protected]

http://corporate.mobistar.be/go/en/financial_information.cfm