Embed Size (px)

Citation preview

Q2/21 Sector Report Digital Technology

Software and IT ServicesSector Focus: Application Software

Agenda

1. Introduction Page 3

2. Application Software Market

− Overview Page 5

− Valuation and M&A activity Page 10

3. IT / Software Market

− Overview Page 17

− Valuation and M&A activity Page 20

4. Introduction to IMAP and relevant expertise Page 29

5. Appendix

− Application SW: Transactions Page 34

− IT / Software: Transactions Page 37

Introduction▪ We are pleased to present the IT/ Software Report Q2 2021. This report provides insights and analysis on

current market trends, valuation developments as well as M&A dynamics within the Software and IT Services sector in Q2 2021

▪ This edition includes a special sector focus on Application software. It provides an overview of market segments, trends and players in Application software as well as data on recent M&A activity and valuations

− Overall, the horizontal application software sector has developed positively over the last twelve months; in particular, the segments "Tele- / Communication" and "SCM / Logistics" have performed strongly during the Covid pandemic. More traditional segments such as "ERP" have moved rather sideways

− Among vertical application software segments, "Energy / Mining" performed particularly well due to the accelerated digitization processes. "Healthcare" and "Finance / Insurance" recorded moderate growth, while "Real Estate / Construction" lost ground due to the implications of the Covid pandemic

Dr. Carsten LehmannManaging Partner

Martin MichalekVice President

Lennart HunoldAssociate

Nils KellerDirector

Digital technology team

Andreas WidholzPartner

Agenda

1. Introduction Page 3

2. Application Software Market

− Overview Page 5

− Valuation and M&A activity Page 10

3. IT / Software Market

− Overview Page 17

− Valuation and M&A activity Page 20

4. Introduction to IMAP and relevant expertise Page 29

5. Appendix

− Application SW: Transactions Page 34

− IT / Software: Transactions Page 37

Introduction to the Application Software Market

5

Horizontal vs. vertical application software segmentation

July 2021

Vertical Application SoftwareHorizontal Application Software

▪ Horizontal application software is used across industries and generally does not require market or industry specific customization. Examples of horizontal application software include communication, ERP, HCM, SCM, PLM or CRM applications

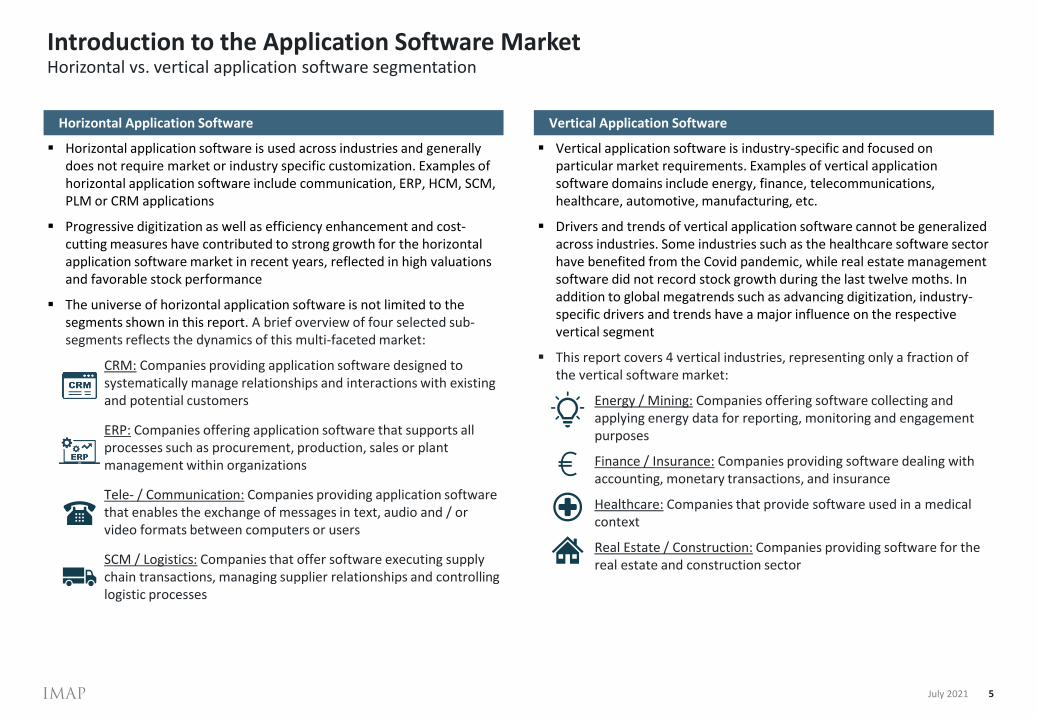

▪ Progressive digitization as well as efficiency enhancement and cost-cutting measures have contributed to strong growth for the horizontal application software market in recent years, reflected in high valuations and favorable stock performance

▪ The universe of horizontal application software is not limited to the segments shown in this report. A brief overview of four selected sub-segments reflects the dynamics of this multi-faceted market:

CRM: Companies providing application software designed to systematically manage relationships and interactions with existing and potential customers

ERP: Companies offering application software that supports all processes such as procurement, production, sales or plant management within organizations

Tele- / Communication: Companies providing application software that enables the exchange of messages in text, audio and / or video formats between computers or users

SCM / Logistics: Companies that offer software executing supply chain transactions, managing supplier relationships and controlling logistic processes

▪ Vertical application software is industry-specific and focused on particular market requirements. Examples of vertical application software domains include energy, finance, telecommunications, healthcare, automotive, manufacturing, etc.

▪ Drivers and trends of vertical application software cannot be generalized across industries. Some industries such as the healthcare software sector have benefited from the Covid pandemic, while real estate management software did not record stock growth during the last twelve moths. In addition to global megatrends such as advancing digitization, industry-specific drivers and trends have a major influence on the respective vertical segment

▪ This report covers 4 vertical industries, representing only a fraction of the vertical software market:

Energy / Mining: Companies offering software collecting and applying energy data for reporting, monitoring and engagement purposes

Finance / Insurance: Companies providing software dealing with accounting, monetary transactions, and insurance

Healthcare: Companies that provide software used in a medical context

Real Estate / Construction: Companies providing software for the real estate and construction sector

Application Software Universe

6

Overview of selected public horizontal and vertical application software players

July 2021

CRM

Mcap:

€1,271m

EV/Rev:

10.4x

EV/EBITDA:31.7x

Source: CIQ

ERP

Mcap:

€1,893m

EV/Rev:

5.4x

EV/EBITDA:15.2x

Tele- / Communications

Mcap:

€3,055m

EV/Rev:

5.2x

EV/EBITDA:21.7x

SCM / Logistics

Mcap:

€3,020m

EV/Rev:

9.1x

EV/EBITDA:32.7x

Energy

Mcap:

€2,252m

EV/Rev:

6.4x

EV/EBITDA:23.4x

Finance / Insurance

Mcap:

€3,428m

EV/Rev:

4.5x

EV/EBITDA:19.2x

Healthcare

Mcap:

€1,862m

EV/Rev:

2.6x

EV/EBITDA:15.8x

Real Estate / Construction

Mcap:

€15,118m

EV/Rev:

13.5x

EV/EBITDA:51.4x

Note: All numbers are median figures based on 2021e

40,1

77,1

2021 2028

Global market volume (In EUR bn)

Application Software Trends

7July 2021

ERPCRM

Tele- / Communications SCM / Logistics

▪ Rising demand for cloud-based ERP applications decentralizing data access

▪ Two-tier ERP allows companies to deploy different ERP systems at the group level than at the subsidiary level

▪ ERP App Stores consolidate all business applications in one place providing quick and easy access

▪ Increasing applications of artificial intelligence within CRM (e.g., identification of patterns in customer behavior)

▪ Growing demand for mobile access to complex CRM software driven by increased adoption of telecommuting

▪ Augmented and Virtual Reality enables customers to experience products remotely before the purchase decision

▪ Improved supply chain visibility allows businesses to precisely monitor performance and increase agility

▪ Integration of blockchain technology in SCM enables companies to gain real-time ledger of transactions for all participants of their network

▪ IoT applications enhance supply chain transparency and improve the efficiency of inventory management

▪ The expansion of 5G deployment facilitates the use of highly data-demanding applications like the Internet of Things (IoT)

▪ Intelligent Automation simplifies the handling of operational tasks guaranteeing shorter waiting periods for customers and lower costs for businesses

▪ Network Virtualization allows adaptation to growing resource requirements by replacing hardware elements with software

CAGR: 9.8%

4,5

13,7

2021 2028

Global market volume (In EUR bn)

CAGR: 17.3%

40,4

82,0

2021 2028

Global market volume (In EUR bn)

1.450,5

2.095,1

2021 2028

CAGR: 10.6%

CAGR: 5.4%

Global market volume (In EUR bn)

Source: Grand View Research, Allied Market Research

Horizontal application software trends & drivers

Application Software Trends

8

Vertical application software trends & drivers

July 2021

FinancialEnergy

Healthcare

▪ IoT allows banks and financial institutions to prevent fraud and increase operational efficiency through immense data-processing capacity

▪ Cybersecurity applications not only keep customer data secure but also help businesses comply with finance regulatory standards

▪ Cloud computing stores and enables instant access to data and provides on-demand availability of computer resources

▪ Energy management software enables customers to monitor energy consumption more precisely

▪ The Internet of Energy (IoE) allows energy production to move forward more efficiently and cleanly with the least amount of waste

▪ Energy-as-a-Service (EaaS) uses a combination of AI and IoT to allow for the transition from selling electricity to selling services such as optimization of production

▪ Smart homes are systems of sensor-equipped devices gathering and analyzing data to provide a more convenient customer experience

▪ Property Management Software provides real estate owners a centralized database that can store several management tools

▪ Increasing popularity of construction management software and the application of lean management to meet requirements for large scale projects and to reduce design time

44,6

99,6

2020 2025

Global market volume (In EUR bn)

CAGR: 17.4%

62,73

104,28

2020 2025

Global market volume (In EUR bn)

94,9

138,7

2020 2025

Global market volume (In EUR bn)

CAGR: 7.9%

12,45

20,52

2021 2025

Global market volume (In EUR bn)

CAGR: 10.5%

Source: Grand View Research, Business Wire

CAGR: 10.7%

Real Estate / Construction

▪ Telemedicine enables patients to consult medical professionals remotely via virtual appointments

▪ Augmented and virtual reality allows better understanding of data and more realistic surgical training

▪ Wearable technology with companion apps enables tracking and monitoring of the personal health record

Agenda

1. Introduction Page 3

2. Application Software Market

− Overview Page 5

− Valuation and M&A activity Page 10

3. IT / Software Market

− Overview Page 17

− Valuation and M&A activity Page 20

4. Introduction to IMAP and relevant expertise Page 29

5. Appendix

− Application SW: Transactions Page 34

− IT / Software: Transactions Page 37

Stock Performance – Horizontal

10

Segmented, indexed stock performance1

July 2021

Q2 2020 – Q2 2021 indexed stock performance

1) Weighting of shares based on market capitalization

LTM Growth

+23% +10% +45% +34%

60%

80%

100%

120%

140%

160%

180%

200%

220%

240%

Date Aug-20 Sep-20 Nov-20 Dec-20 Jan-21 Mar-21 Apr-21 Jun-21

CRM / Marketing ERP Tele- / Communication SCM / Logistics

Application Software Valuation – Horizontal (I/II)

11

Median segment valuation metrics in 2021E

July 2021

EV/Revenue 2021E Revenue growth 2021E

EV/EBITDA 2021E EBITDA-margin 2021E

10,4x

5,4x 5,2x

9,1x

CRM / Marketing ERP Tele- / Communication SCM / Logistics

20%

4%

16%

11%

CRM / Marketing ERP Tele- / Communication SCM / Logistics

31,7x

15,2x

21,7x

32,7x

CRM / Marketing ERP Tele- / Communication SCM / Logistics

27%

22%

14%

25%

CRM / Marketing ERP Tele- / Communication SCM / Logistics

Application Software Valuation – Horizontal (II/II)

12

Development of the median segment valuation metrics between 2021E and 2023E

Source: CIQ July 2021

EV/Revenue 2021E-2023E Revenue growth 2021E-2023E

EV/EBITDA 2021E-2023E EBITDA-margin 2021E-2023E

10,4x

5,4x5,2x

9,1x

8,5x

5,1x 4,6x

8,2x

7,0x

4,7x4,0x

7,3x

CRM / Marketing ERP Tele- / Communication SCM / Logistics

2021E 2022E 2023E

20%

4%

16%

11%

19%

8%

14%

11%

19%

6%

15%

10%

CRM / Marketing ERP Tele- / Communication SCM / Logistics

2021E 2022E 2023E

31,7x

15,2x

21,7x

32,7x

27,9x

15,1x19,6x

30,9x

26,4x

14,1x15,8x

29,7x

CRM / Marketing ERP Tele- / Communication SCM / Logistics

2021E 2022E 2023E

27%

22%

14%

25%28%

23%

16%

24%

27%

24%

20%

28%

CRM / Marketing ERP Tele- / Communication SCM / Logistics

2021E 2022E 2023E

Stock Performance – Vertical

13

Segmented, indexed stock performance1

July 2021

Q2 2020 – Q2 2021 indexed stock performance

1) Weighting of shares based on market capitalization

LTM Growth

60%

80%

100%

120%

140%

160%

Date Aug-20 Sep-20 Nov-20 Dec-20 Feb-21 Mar-21 Apr-21 Jun-21

Energy / Mining Finance / Insurance Healthcare Real Estate / Construction

+32% +8% +12% -2%

Application Software Valuation – Vertical (I/II)

14

Median segment valuation metrics in 2021E

July 2021

EV/Revenue 2021E Revenue growth 2021E

EV/EBITDA 2021E EBITDA-margin 2021E

6,4x

4,6x

2,5x

13,5x

Energy / Mining Finance / Insurance Healthcare Real Estate /Construction

23,4x18,3x

15,9x

47,6x

Energy / Mining Finance / Insurance Healthcare Real Estate /Construction

12%

4%

9%

19%

Energy / Mining Finance / Insurance Healthcare Real Estate /Construction

25%22%

20%

25%

Energy / Mining Finance / Insurance Healthcare Real Estate /Construction

Application Software Valuation – Vertical (II/II)

15

Development of the median segment valuation metrics between 2021E and 2023E

Source: CIQ July 2021

EV/Revenue 2021E-2023E Revenue growth 2021E-2023E

EV/EBITDA 2021E-2023E EBITDA-margin 2021E-2023E

6,4x

4,6x2,5x

13,5x

5,6x

4,3x

2,1x

11,3x

4,9x 4,1x

2,0x

9,7x

Energy / Mining Finance / Insurance Healthcare Real Estate /Construction

2021E 2022E 2023E

23,4x

18,3x15,9x

47,6x

22,5x 16,8x

12,1x

42,4x

17,6x 15,3x10,7x

30,8x

Energy / Mining Finance / Insurance Healthcare Real Estate /Construction

2021E 2022E 2023E

25%22%

20%

25%27%

22%20%

25%

29%

23% 22%26%

Energy / Mining Finance / Insurance Healthcare Real Estate /Construction

2021E 2022E 2023E

12%

4%

9%

19%

10%8%

7%

19%

8%9%

7%

17%

Energy / Mining Finance / Insurance Healthcare Real Estate /Construction

2021E 2022E 2023E

Agenda

1. Introduction Page 3

2. Application Software Market

− Overview Page 5

− Valuation and M&A activity Page 10

3. IT / Software Market

− Overview Page 17

− Valuation and M&A activity Page 20

4. Introduction to IMAP and relevant expertise Page 29

5. Appendix

− Application SW: Transactions Page 34

− IT / Software: Transactions Page 37

▪ This section of the digital technology report provides an overview on valuation developments as well as M&A dynamics within certain sub-sectors of the IT / Software space which we have decided to summarize as follows:

Infrastructure and Cloud (Infrastructure): companies providing hardware, software or services related to running and maintaining infrastructure and cloud environments

Software as a Service (SaaS): companies following a subscription-based business model

Application software (Application): companies providing application software

SW development: companies active in software development, either as service or technology providers

IT service: companies providing a broader spectrum of IT services

Conglomerates: a collection of software and IT companies with a market cap. in excess of USD100bn

▪ IMAP Technology sector experts have advised on 170+ deals since 2015. Largest sub-sectors are Software, IT Service & Consulting, Telecommunication Services and Internet Software & Services

▪ In 2020, IMAP advised on 30 technology deals, representing 14% of IMAP total deal volume and thus the largest share of any industry

▪ Total reported deal value was approx. 2.9bn USD, leading to an average deal size of approx. 90 mn USD

▪ One third of transactions were cross-border. More than 75% of target companies were European and c. 20% North American

▪ The Technology sector is covered by c. 80 IMAP Professionals with strong networks and a global reach

Introduction | Executive Summary to the IT/Software Market

17

Overview of IMAP Germany‘s Software Industry Report

July 2021

▪ European M&A deal count continued to grow in Q2-2021 with 276 deals, representing a +81% y-o-y increase. Germany also saw a high number deals since 2018 with 40 deals in Q2-2021, a slight decrease compared to 43 deals in Q1-2021.

▪ European deal value increased to 16bn EUR in Q2, which corresponds to a fourfold increase compared to the same period a year ago. With c. 2.2bn EUR deal value in Q2-2021, German deal value decreased compared to the previous quarter, but still well above the average since 2018

▪ Average deal sizes in Europe in Q2 2021 amounted to c. 58m EUR, and c. 54m EUR in Germany

▪ Transaction valuations slightly decreased in Q2-2021, reflecting slightly lower overall valuations since the beginning of the Covid Crisis. Transaction valuations with 3.7x revenues and 14.8x EBITDA in Q2 2021 are in line with the average of the last 5 years

▪ Stock prices of Technology companies continued to increase in Q2 2021, with Application Software (+11%) and Software Development (+10%) showing the strongest quarterly growth

▪ Compared to previous quarter, relative valuations of listed companies saw an increase across all subsegments in terms of EV/EBITDA valuations, except IT Service remaining stable; a similar picture emerges for EV/Revenue multiples

▪ The IMAP Cross segment index grew by +5% in Q2 2021. Slowing stock price increases also affected overall index growth, with MSCI World, TECDAX and NASDAQ moderately increasing between 3% to 7% in Q2 2021

Introduction Executive Summary

Key Trends & Drivers

18

Global trends and drivers boost the software/ IT sector

July 2021

+22% global Cloud spending forecasted for 2021

Global end-user spending on public cloud services surged in 20/21 due to the implications of the Covid-19 pandemic; rising demand for emerging technologies such as containerization, virtualization, and edge computing as well as increasing threats from cyberattacks and the resulting rise in the importance of data security.

+19% global SaaS revenue growth between 2020 and 2021

The benefits of SaaS, such as increased agility, simplified access from any device, inherent scalability, or increased cost efficiency enable innovative companies to extend their competitive advantage and to drive performance. Demand for SaaS remains high and is driven by current trends such as AI, centralized analytics and vertical SaaS.

32 40 49 71 85 85 102 121

2015 2016 2017 2018 2019 2020 2021E 2022P

Global SaaS revenue (EUR bn)

CAGR: 21%

+10% expected CAGR in custom software development (2020-2025)

Software development is about integrating top-notch technologies and applying the latest development methods to meet customer requirements and maintain a competitive edge. In 2021, the industry is mainly driven by rising demand for advanced cybersecurity programs, artificial intelligence for improved customer experience and increasing use of IoT devices.

+9% global IT service spending projected for 2021

The Covid pandemic has boosted digital acceptance and the transition to the cloud, driving the development of new products and services.

Growth in the IT services sector is estimated to be between 8-9% p.a. in the coming years, compared to 4-6% before COVID and will move towards digital services.

95 110 129 167 217 227 276 330

2015 2016 2017 2018 2019 2020 2021E 2022P

Cloud computing revenue (EUR bn)

CAGR: 20%

Source: Gartner, Statista

40%

44%

55%

63%

68%

Java

Python

SQL

HTML/CSS

JavaScript

Most widely utilized programming languages (2020)

780 805 824 842 929 900 978 1.061

2015 2016 2017 2018 2019 2020 2021E 2022P

Global IT services spending (EUR bn)

CAGR: 4%

Agenda

1. Introduction Page 3

2. Application Software Market

− Overview Page 5

− Valuation and M&A activity Page 10

3. IT / Software Market

− Overview Page 17

− Valuation and M&A activity Page 20

4. Introduction to IMAP and relevant expertise Page 29

5. Appendix

− Application SW: Transactions Page 34

− IT / Software: Transactions Page 37

Public Company Valuation

20

Selected public companies by sub-sector

Σ MCap:XY

∅ EV/Revenue 2020:XY

∅ EV/EBITDA 2020: XY

Infrastructure SaaS Application

Software Development IT Services Conglomerates

July 2021

MCap:

EURm 7,473

EV/Revenue:

1.3x

EV/EBITDA:10.4x

MCap:

EURm 8,445

EV/Revenue:

8.2x

EV/EBITDA:23.3x

MCap:

EURm 24,307

EV/Revenue:

3.6x

EV/EBITDA:15.8x

MCap:

EURm 12,765

EV/Revenue:

4.8x

EV/EBITDA:12.4x

MCap:

EURm 35,484

EV/Revenue:

9.7x

EV/EBITDA:28.0x

MCap:

EURm 213,250

EV/Revenue:

6.4x

EV/EBITDA:16.3x

Note: Median figures based on 2021Source: CIQ Development of respective multiple from Q1 2021 to Q2 2021

=

Stock Performance (I/II)

21

+13% +19% +28% +30% +18% +33%

Performance

Source: CIQ

Q2 2020 – Q2 2021 indexed stock performance

1) Weighting of shares based on market capitalization July 2021

Segmented, indexed stock performance1

Q1

LTM

+5% +8% +11% +10% +4% +8%

80%

90%

100%

110%

120%

130%

140%

150%

160%

Date Aug-20 Sep-20 Nov-20 Dec-20 Feb-21 Mar-21 Apr-21 Jun-21

Infrastructure SaaS Application Software Developer IT Services Conglomerates

Stock Performance (II/II)

22

Performance

Source: CIQ

Q2 2020 – Q2 2021 indexed stock performance

1) Weighting of shares based on market capitalization July 2021

Performance of the cross-segment index1 by our definition (“IMAP”) against key market indices

+33% +36% +19% +41%

Q1

LTM

+5% +7% +3% +7%

80%

100%

120%

140%

160%

180%

200%

Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21

Cross segment index MSCI World TECDAX NASDAQ

Segment Valuation (I/IV)

23

Median segment valuation metrics in 2021E

Source: CIQ July 2021

EV/Revenue 2021E Revenue growth 2021E

EV/EBITDA 2021E EBITDA-margin 2021E

4,8x

8,2x

9,7x

3,6x

1,3x

6,4x

Infrastructure &Cloud

SaaS Application SoftwareDeveloper

IT Service Conglomerates

12,4x

23,3x

28,0x

15,8x

10,4x

16,3x

Infrastructure &Cloud

SaaS Application SoftwareDeveloper

IT Service Conglomerates

8%

13%

10%

12%

7%

12%

Infrastructure &Cloud

SaaS Application SoftwareDeveloper

IT Service Conglomerates

37%

21%

33%

20%

14%

38%

Infrastructure &Cloud

SaaS Application SoftwareDeveloper

IT Service Conglomerates

Segment Valuation (II/IV)

24

Development of the median segment valuation metrics between 2021E and 2023E

Source: CIQ July 2021

EV/Revenue 2021E-2023E Revenue growth 2021E-2023E

EV/EBITDA 2021E-2023E EBITDA-margin 2021E-2023E

12,4x

23,3x

28,0x

15,8x

10,4x

16,3x

11,4x

29,3x

24,6x

14,7x

9,7x

14,9x

10,9x

24,2x21,0x

13,8x

9,3x

13,5x

Infrastructure &Cloud

SaaS Application SoftwareDeveloper

IT Service Conglomerates

2021E 2022E 2023E

8%

13%

10%

12%

7%

12%

7%

15%

12%

10%

6%

10%

7%

15%

10%

8%6%

9%

Infrastructure &Cloud

SaaS Application SoftwareDeveloper

IT Service Conglomerates

2021E 2022E 2023E

37%

21%

33%

20%14%

38%37%

21%

34%

20%15%

38%36%

22%

36%

20%

16%

37%

Infrastructure &Cloud

SaaS Application SoftwareDeveloper

IT Service Conglomerates

2021E 2022E 2023E

4,8x

8,2x

9,7x

3,6x

1,3x

6,4x

4,4x

7,1x7,7x

3,2x

1,2x

5,8x

4,2x

6,0x7,0x

3,0x

1,2x

5,3x

Infrastructure &Cloud

SaaS Application SoftwareDeveloper

IT Service Conglomerates

2021E 2022E 2023E

Segment Valuation (III/IV)

25

5-year historical development of median NTM EV/EBITDA multiple

Source: CIQ July 2021

Infrastructure Software Developer

SaaS IT Service

Application Conglomerates

Ø 11,7x

5,0x

7,0x

9,0x

11,0x

13,0x

15,0x

Jun. 16 Jun. 17 Jun. 18 Jun. 19 Jun. 20 Jun. 21

EV/EBITDA Median EBITDA

Ø 27,4x

0,0x

10,0x

20,0x

30,0x

40,0x

Jun. 16 Jun. 17 Jun. 18 Jun. 19 Jun. 20 Jun. 21

EV/EBITDA Median EBITDA

Ø 22,0x

0,0x

10,0x

20,0x

30,0x

40,0x

Jun. 16 Jun. 17 Jun. 18 Jun. 19 Jun. 20 Jun. 21

EV/EBITDA Median EBITDA

Ø 11,9x

0,0x

5,0x

10,0x

15,0x

20,0x

Jun. 16 Jun. 17 Jun. 18 Jun. 19 Jun. 20 Jun. 21

EV/EBITDA Median EBITDA

Ø 9,6x

0,0x

5,0x

10,0x

15,0x

Jun. 16 Jun. 17 Jun. 18 Jun. 19 Jun. 20 Jun. 21

EV/EBITDA Median EBITDA

Ø 18,5x

0,0x

10,0x

20,0x

30,0x

Jun. 16 Jun. 17 Jun. 18 Jun. 19 Jun. 20 Jun. 21

EV/EBITDA Median EBITDA

Segment Valuation (IV/IV)

26

Correlation between EV/Revenue 2022E and revenue growth 2022E

Source: CIQ July 2021

Infrastructure Software Developer

SaaS IT Service

Application Conglomerates

ADBE

BLKB

BOXDOCU

DBX

ENV

GWRENFLX PFPT

PSTG

QADA

CRMWDAY

ZEN

0,0x

5,0x

10,0x

-5,0% 0,0% 5,0% 10,0% 15,0%

EV/2

02

2E

Rev

enu

e

2022E Revenue Growth

ADBE

BLKB

BOX

DOCU

DBX

ENV

GWRE

NFLX

PFPT

PSTG

QADACRM

WDAY

ZEN

ZUO0,0x

5,0x

10,0x

15,0x

20,0x

25,0x

30,0x

0,0% 10,0% 20,0% 30,0% 40,0% 50,0%

EV/2

02

2E

Rev

enu

e

2022E Revenue Growth

ADBEANSS

ADPCSU

DSYHEXA B INTU

MSFT

OTEX

ORCLPEGA

PSAN

QADASAPSNPS

WDAY

0,0x

5,0x

10,0x

15,0x

20,0x

0,0% 5,0% 10,0% 15,0% 20,0% 25,0%

EV/2

02

2E

Rev

enu

e

2022E Revenue Growth

ACN

GIB.A

CTSHEPAM

GLOB

HCLTECH

INFY

NRO

PRGS

0,0x

5,0x

10,0x

-5,0% 0,0% 5,0% 10,0% 15,0% 20,0% 25,0% 30,0%

EV/2

02

2E

Rev

enu

e

2022E Revenue Growth

ACN

ADN1

AEIN

ATOBC8COK

CAPGIB.A

CTSH

CCC

D6H

DVTIDR

INFY

IBM

NTT

SOP

TCS

(2,0x)

0,0x

2,0x

4,0x

6,0x

8,0x

0,0% 4,0% 8,0% 12,0% 16,0%

EV/2

02

2E

Rev

enu

e

2022E Revenue Growth

GOOG.L

AMZN

AAPL

CSCO

FB

INTC

IBM

MSFT

ORCL

0,0x

5,0x

10,0x

15,0x

-5,0% -1,0% 3,0% 7,0% 11,0% 15,0% 19,0% 23,0% 27,0%

EV/2

02

2E

Rev

enu

e

2022E Revenue Growth

2.3x 1,9x 3.0x 2.5x 2,2x 2.1x 2.4x 2.4x 2,1x 1.9x 2.3x 2.7x 3.2x 3.1x 2.4x4.6x

2.8x 2.3x4.7x

3.4x 3.0x 2.6x 2.9x 2.9x 3.7x

10.6x

13.6x15.7x

11.9x 11.3x

8.9x

14.6x 15.4x

11.5x

15.3x16.4x 15.8x

17.2x16.1x 14.9x

24.7x

15.2x

11.5x

15.0x

18.9x

11.0x 10.4x

15.6x 15.1x 14.4x

13.3x

11.7x

14.7x16.0x

16.6x14.0x 14.8x

2.4x 2.3x 2.2x 2.9x 3.6x 3.0x 3.3x

Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

EV/Revenue EV/EBITDA Moving Average EV/EBITDA Moving Average EV/Revenue

Deal Dashboard

27

Application and system software market

Quarterly multiples between 2017 and Q1 2021 Europe2

Selected German transactionsEuropean M&A value in EUR bn1 German M&A value in EUR bn

European M&A Deal Count1 German M&A deal count

Source: Merger Market July 20211) Excl. German Transactions 2) Adjusted for extraordinary outliers

Selected European transactions

Buyer Target EVEV/

EBITDA

€3,183m n.a.

€1,800m n.a.

€1,395m 31.8x

€1,000m n.a.

€828m n.a.

€559m n.a.

€415m n.a.

Buyer Target EVEV/

EBITDA

€9,012m n.a.

€2,454m n.a.

€2,219m 35.5x

€140m n.a.

€95m n.a.

€50m n.a.

€22m n.a.

+others

+others

0,0

2,3

0,2 0,3 0,4 0,4

2,53,3

0,1

1,4 1,4

4,0

2,2

Q218

Q318

Q418

Q119

Q219

Q319

Q419

Q120

Q220

Q320

Q420

Q121

Q221

8

48 7

58

47

4

12 1215 16

Q218

Q318

Q418

Q119

Q219

Q319

Q419

Q120

Q220

Q320

Q420

Q121

Q221

162 135

152 161

184

170 151 183 152

196

265 267 276

Q218

Q318

Q418

Q119

Q219

Q319

Q419

Q120

Q220

Q320

Q420

Q121

Q221

11 25 26

24 26

21 22

36 18

32 33 43 40

Q218

Q318

Q418

Q119

Q219

Q319

Q419

Q120

Q220

Q320

Q420

Q121

Q221

20212015 2016 2017 2018 2019 2020

Agenda

1. Introduction Page 3

2. Application Software Market

− Overview Page 5

− Valuation and M&A activity Page 10

3. IT / Software Market

− Overview Page 17

− Valuation and M&A activity Page 20

4. Introduction to IMAP and relevant expertise Page 29

5. Appendix

− Application SW: Transactions Page 34

− IT / Software: Transactions Page 37

IMAP is specialized on mid-cap M&A transactions for privately owned companies

29

With > 200 transactions annually, we are one of the leading global M&A organizations

Execution

Dedication

Talent

Informality

Global M&A-Organization

with 60 offices in 43 countries

> 450 professionalsthereof approx. 40 in Germany

Ø > 200 deals p.a. globally

Ø 20-25 deals p.a.in Germany

c. 80% sell-side

deal value p.a.globally

c. EUR 10 bn

Ø deal value c. EUR 50 m

Managed by partners with

strong deal experience, who

are only responsible to the client

International sector teams

connected viaglobal IT platform

Regularly ranked among Top 10 M&A advisory

firms

July 2021

Our Core Values

Successful in the German market

since 1997

24Years

IMAP International Approx. 65 cross-border transactions with over 450 professionals in 43 countries completed in 2020

July 2021 30

Global partnership Transactions by sectors (2020 - # Deals: 218)

PublicationsInternational presence

IMAP Germany

▪ Access to local knowledge and contacts in all important international markets

▪ Proven collaboration routines according to high performance standards

▪ International sector- and project teams

▪ Integrated IT platform for collaboration and as knowledge pool for all sector specific projects

▪ Globally rotating IMAP conferences & symposia

▪ Access to all relevant national and international databases

Europe & Africa ▪ 24 offices in the EU▪ 1 office each in UK, Serbia and Bosnia and

Herzegovina▪ 9 offices in Africa▪ over 280 M&A professionals

North and South America▪ 17 offices in USA, 2 offices in Canada ▪ 1 office each in Argentina, Brazil, Chile, Colombia,

Mexico and Peru▪ over 170 M&A professionals

Asia▪ 2 offices in Japan, 1 office each in China, India and

Thailand▪ over 50 M&A professionals

14%

12%

9%

9%

7%7%6%

6%

5%

4%

21%

Technology

Industrials

Consumer & Retail

Business Services

Healthcare

Food & Beverage

Transport & Logistics

Materials, Chemicals & Mining

Building Products

Automotive

others

Q4/20 Sector Report IT / Software

2021 Sector ReportHEALTHCARE

Q1/21 Sector Report

Digital Technology

IMAP Global Technology TeamGlobally active with experienced sector experts

July 2021 31

Expert team Germany

# dealmakers: 6

International sector coverage IMAP Technology Deal Statistics

Expert team Nordics

# dealmakers: 4

Expert team BeNeLux

# dealmakers: 7

Expert team Asia

# dealmakers: 2

Expert team UK & Ireland

# dealmakers: 14

170+ deals in the technology sector since 2015

Ø 25 deals p.a.

>30% cross-border

> 70% European targets

$105mn avg. deal size in 2020

Deal split by Technology sub-sectorExpert team South America

# dealmakers: 9

Expert team France

# dealmakers: 3

Expert team S/E Europe

# dealmakers: 13

Expert team North America

# dealmakers: 10

1320

33

36

24

46

Electronic Equipment& Parts

Internet Software &Services

IT Services &Consulting

Software

TelecommunicationsServices

IMAP Germany Technology Team

Nils KellerDirector

Lennart Hunold

Martin MichalekVice President

Dr. Carsten LehmannManaging Director

Andreas WidholzPartner

July 2021 32

IMAP IT/Software DealsSelected IMAP international deals since 2018

Advisor to Lomitel

Acquired 50%

Acquired 100%

Advisor to Canorama

Acquired 100%

Advisor to Cyfrowy

Advisor to EI Towers

Acquired 100%

Advisor to neurio

Acquired 100%

Advisor to Maximum

Acquired 100%

Advisor to Cedacri

Acquired Majority Control

Advisor to Chatmeter

Strategic investmentAcquired a Minority stake

Advisor to AOEAdvisor to Promedico

Acquired Investment Interest

Advisor to Catalysts

A Portfolio Company of

Acquired 100%

Advisor to Shoper

Acquired 100%

Advisor to Highland

Acquired a Majority Stake

Advisor to Teletronika

Acquired 100%

Advisor to INOBAS

Acquired 100%

Advisor to SemVox

Acquired 100%

Advisor to Ametras

Acquired 100%

Acquired 100%

Advisor to RS Advisor to ETC

Has been acquired in an MBO from

Advisor to StratoZen

Acquired 100%

Advisor to Inovatec

Acquired Majority Control

Advisor to Vitec

Acquired 100%

Advisor to Indofin

Acquired 100%

Advisor to Awetis

Acquired 100%

Advisor to CEMA

Acquired 100%

Advisor to raynet

Has entered into a Partnership

Advisor to EXA

Acquired Majority Shares

Advisor to NBD Biblion

Acquired 100%

Advisor to Pharmagest

Acquired Investment Interest

Private Investors

Advisor to Adelis

Acquired Majority Control

Advisor to tesa scribos

Acquired 100%

Advisor to Datac

Acquired 100%

Agenda

1. Introduction Page 3

2. Application Software Market

− Overview Page 5

− Valuation and M&A activity Page 10

3. IT / Software Market

− Overview Page 17

− Valuation and M&A activity Page 20

4. Introduction to IMAP and relevant expertise Page 29

5. Appendix

− Application SW: Transactions Page 34

− IT / Software: Transactions Page 37

Selected Application Software Transactions (I/II)

34

European transactions in the last 6 months

July 2021

EV EV EV EV

Segment Date Target company Country Buyer Target Description mEUR' Revenue EBITDA EBIT

Application (horizontal;

ERP)10.06.2021

RIB Software SE (9.09% Stake)

Germany

Schneider Electric SE

Germany-based provider of technical enterprise resource planning (ERP) software solutions

222.6 8.7x 35.5x 71.2x

Application (vertical;

healthcare)03.06.2021

Babylon Healthcare Services Limited

United KingdomAlkuri Global Acquisition Corp.

UK-based company that operates a subscription based mobile healthcare application

3,182.6 48.8x n.a. n.a.

Application (vertical; finance)

03.06.2021

Invoke

FranceSagard; ISAI Gestion; Bpifrance

France-based B2B provider of software for managing financial, tax and regulatory information

50.0 2.5x n.a. n.a.

Application (vertical;

insurance)01.06.2021

wefox Germany GmbH

GermanyEurazeo; Partners Group Holding; LGT

Germany-based provider of mobile apps to compare insurances

531.6 21.0x n.a. n.a.

Application (vertical;

healthcare)01.06.2021

VISUS Health IT GmbH

Germany

CompuGroup Medical SE

Germany-based provider of picture archiving and communication systems (PACS) and healthcare content management solutions

50.0 2.7x n.a. n.a.

Application (vertical;

healthcare)25.05.2021

Metodika AB

Sweden

Carasent ASA

Sweden-based healthcare practice management software firm

10.6 3.8x 53.4x n.a.

Application (vertical;

healthcare)11.05.2021

EDL

France

Abenex Capital SA

France-based privately owned medical image software management company

100.0 6.7x 14.3x n.a.

Application (vertical;

healthcare)15.04.2021

ExtraMed Limited

United Kingdom

Alcidion Group Limited

UK-based provider of patient flow management software for the healthcare sector

6.1 0.5x n.a. n.a.

Application (horizontal;

telecom-munication)

30.03.2021

Matrix Telematics Limited

United KingdomBridges Fund Management Ltd.

UK-based fleet telematics and software provider for connected fleet technology

70.3 n.a. 15.0x n.a.

Application (vertical; financial)

29.03.2021

Itiviti Group AB

SwedenBroadridge Financial Solutions, Inc.

Sweden-based provider of software solutions for the financial industry in the areas of advanced trading and connectivity

2,600.0 12.5x 24.7x 50.5x

Selected Application Software Transactions (II/II)

35

European transactions in the last 6 months

July 2021

EV EV EV EV

Segment Date Target company Country Buyer Target Description mEUR' Revenue EBITDA EBIT

Application (vertical;

SCM)26.03.2021

Navis LLC

USA

Accel-KKR LLC

US-based provider of logistics supply chain execution software solutions

380.0 3.6x n.a. n.a.

Application (vertical; financial)

22.03.2021

Calypso Technology, Inc.

USA

Thoma Bravo, LLC

US-based company engaged in providing financial market software solutions

3,147.8 n.a. 37.5x n.a.

Application (horizontal;

ERP)22.03.2021

UNIT4 N.V.

NetherlandsTA Associates; Partners Group Holding

Netherlands-based provider of enterprise resource planning (ERP) and financial management software

1,678.8 4.1x 15.3x n.a.

Application (horizontal;

telecom-munication)

17.03.2021

Riaktr

BelgiumSeamless Distribution Systems AB

Belgium-based provider of big data applications and software for marketing, sales and distribution networks of telecom operators

10.4 2.1x 8.0x n.a.

Application (horizontal;

CRM)03.03.2021

Mission Labs Limited

United KingdomGamma Communications plc

UK-based software company providing solutions enhancing digital customer experiences

46.5 11.8x n.a. n.a.

Application (vertical;

healthcare)01.03.2021

The Edge Software Consultancy Ltd

United Kingdom

Instem PLC

UK-based company that develops and distributes laboratory informatics software solutions for the pharmaceutical sector

9.8 3.1x n.a. n.a.

Application (horizontal;

ERP)24.02.2021

VizuAll Inc

USAXytech Systems Corporation

US-based provider of enterprise resource planning (ERP) software for media, broadcast and transmission businesses

4.9 0.7x n.a. 12.1x

Application (vertical; energy)

15.02.2021TietoEVRY (oil and gas software business)

NorwayQuorum Business Solutions, Inc.

Norway-based company offering personnel and material logistics software and related services for the oil and gas industry

155.0 3.1x n.a. n.a.

Application (vertical;

healthcare)15.02.2021

Carmenta Public Safety AB

Sweden

CSAM Health Group AS

Sweden-based company engaged in providing software solutions for emergency response

14.9 1.8x 15.0x n.a.

Application (vertical; financial)

29.01.2021Avaloq Group AG (14% Stake)

Switzerland

JICT Co., Ltd.

Switzerland-based company that develops and provides software for core banking

278.1 3.8x 23.7x n.a.

Agenda

1. Introduction Page 3

2. Application Software Market

− Overview Page 5

− Valuation and M&A activity Page 10

3. IT / Software Market

− Overview Page 17

− Valuation and M&A activity Page 20

4. Introduction to IMAP and relevant expertise Page 29

5. Appendix

− Application SW: Transactions Page 34

− IT / Software: Transactions Page 37

EV EV EV EV

Segment Date Target company Country Buyer Target Description mEUR' Revenue EBITDA EBIT

IT Service 29.06.2021

it-novum GmbH

Germany

Allgeier SE

Germany-based company providing IT consultancy, enterprise management, and big data analytics services

22.0 n.a. 9.5x n.a.

Application 28.06.2021

Allocate Software Limited

United Kingdom

RLDatix

UK-based provider of healthcare workforce management software for workforce rostering, time and attendance, and associated compliance workflows

1,130.0 n.a. n.a. n.a.

SaaS 25.06.2021

Leviy B.V.

Netherlands

zvoove Group GmbH

Netherlands-based provider of software-as-a-service (SaaS) solutions for companies in the cleaning and facility management sector

n.a. n.a. n.a. n.a.

SaaS 25.06.2021

Rapal Oy

Finland

Orn Software AS

Finland-based real estate software-as-a-service (SaaS) company

36.8 4.5x 21.4x n.a.

Infrastructure 24.06.2021

Tink AB

Sweden

Visa Inc.

Sweden-based cloud-based open banking platform enabling banks, fintechs and startups to develop data-driven financial services

1,800.0 n.a. n.a. n.a.

Application 22.06.2021

Billage Software, S.L.

SpainPrimavera Business Software Solutions, S.A.

Spain-based company providing business management software for cloud-based CRM, task management, accounting and client billing solutions

n.a. n.a. n.a. n.a.

IT Service 18.06.2021

ANS Group Ltd

United KingdomInflexion Private Equity Partners LLP

UK-based IT systems integration company engaged in providing hardware, software, and managed services

n.a. n.a. n.a. n.a.

Application 17.06.2021

Holded Technologies S.L

Spain

Visma AS

Spain-based provider of business software solutions such as business operating systems for invoicing, project management, inventory, and accounting

120.0 n.a. n.a. n.a.

IT Service 10.06.2021datac Kommunikations-systeme GmbH

Germany

q. beyond AG

Germany-based provider of solutions for digitized working environments with Microsoft 365 and Microsoft Teams

n.a. n.a. n.a. n.a.

Application 10.06.2021RIB Software SE (9.09% Stake)

Germany

Schneider Electric SE

Germany-based provider of technical enterprise resource planning software solutions

2219.0 8.7x 35.5x 71.2x

Selected Transactions (I/IV)

37

Q2 2021 with a focus on European MidCap transactions

July 2021

EV EV EV EV

Segment Date Target company Country Buyer Target Description mEUR' Revenue EBITDA EBIT

Application 07.06.2021

Aligned Assets Limited

United Kingdom

Idox plc

UK-based company engaged in developing software solutions for location and address management

12.2 n.a. n.a. n.a.

Application 07.06.2021

Axioma Srl (65% Stake)

Italy

Zucchetti s.p.a.

Italy-based developer of ERP and management solutions for companies in the manufacturing, service, and banking sectors

n.a. n.a. n.a. n.a.

IT Service 07.06.2021

The Cloud People AS

Norway

Longship AS

Norway-based service provider for cloud-based platforms

n.a. n.a. n.a. n.a.

Application 03.06.2021Babylon Healthcare Services Limited

United KingdomAlkuri Global Acquisition Corp.

UK-based company that operates a subscription based mobile healthcare application

3,182.6 48.8x n.a. n.a.

IT Service 03.06.2021

ONI Ltd

United Kingdom

Thrive Operations, LLC

UK-based IT managed services provider owning and operating data centers

n.a. n.a. n.a. n.a.

SaaS 01.06.2021

Cloudia Oy

Finland

Mercell Holding AS

Finland-based company providing software-as-a-service (SaaS) for digital planning, sourcing, and contract and supplier management solutions

102.5 11.1x n.a. n.a.

Infrastructure 28.05.2021Cloudwurdig GmbH; Innovations ON GmbH; DI-ON.solutions GmbH

Germany; Germany; Germany

NORD Holding

Germany-based service providers and software developers engaged in supporting customers with their cloud infrastructure and developing cloud-native apps and software

n.a. n.a. n.a. n.a.

SaaS 27.05.2021

Agicap SAS

FrancePartech; BlackFin; Greenoaks

France-based developer of software-as-a-service (SaaS) platform for small and medium-sized businesses to manage and forecast their cashflow

410.0 n.a. n.a. n.a.

SaaS 27.05.2021

Dosing GmbH

Germany

Dedalus Holding S.p.A.

Germany-based provider of software-as-a-service (SaaS) medication safety solutions

n.a. n.a. n.a. n.a.

SaaS 26.05.2021

DataDome

FranceISAI Gestion, SAS; Elephant Partners

France-based publisher of the software-as-a-service (SaaS) cybersecurity solution protecting websites from bot traffic

n.a. n.a. n.a. n.a.

Selected Transactions (II/IV)

38

Q2 2021 with a focus on European MidCap transactions

July 2021

EV EV EV EV

Segment Date Target company Country Buyer Target Description mEUR' Revenue EBITDA EBIT

Application 25.05.2021

Metodika AB

Sweden

Carasent ASA

Sweden-based healthcare practice management software firm

10.6 3.8x 53.4x n.a.

Development 18.05.2021

Beecom AG

Switzerland

Eficode Oy

Switzerland-based company engaged in developing software (JSU Automation Suite for Jira Workflows)

n.a. n.a. n.a. n.a.

Development 18.05.2021

Health Solutions AB

Sweden

BCB Medical Oy

Sweden-based company engaged in software development and consultancy services within the medical sector

n.a. n.a. n.a. n.a.

Infrastructure 12.05.2021

Edgemo A/S

Denmark

Danoffice IT ApS

Denmark-based IT infrastructure provider and IT integration and consulting services specialists

n.a. n.a. n.a. n.a.

Application 12.05.2021

OneLook Systems Limited

Ireland (Republic)

VelocityEHS Holdings Inc.

Ireland-based provider of enterprise safety and risk management software solutions

n.a. n.a. n.a. n.a.

Application 12.05.2021

Terrafirma IDC Limited

United Kingdom

Dye & Durham Limited

UK-based provider of cloud-based proprietary workflow software and data insights solutions

14.0 n.a. n.a. n.a.

Application 11.05.2021

Bredana Solutions A/S

Denmark

9altitudes

Denmark-based provider of software-based enterprise resource planning and customer relationship management business solutions

n.a. n.a. n.a. n.a.

Application 11.05.2021

Omegapoint Group AB

Sweden

FSN Capital Partners AS

Sweden-based IT consulting company specialized in the field of cloud solutions

n.a. n.a. n.a. n.a.

SaaS 11.05.2021

Padam Mobility

France

Siemens Mobility GmbH

France-based technology company that provides AI-powered platforms and applications for on-demand and paratransit services

n.a. n.a. n.a. n.a.

IT Service 11.05.2021

Scandio GmbH

Germany

HiQ International AB

Germany-based digitalization consulting company focused on IT-consulting, agile software development, and cloud technology

n.a. n.a. n.a. n.a.

Selected Transactions (III/IV)

39

Q2 2021 with a focus on European MidCap transactions

July 2021

EV EV EV EV

Segment Date Target company Country Buyer Target Description mEUR' Revenue EBITDA EBIT

Development 11.05.2021

Squeed AB

Sweden

Semcon AB

Sweden-based company engaged in software development and agile change management

9.9 0.9x n.a. 7.1x

IT Service 10.05.2021

Synergics NV

Belgium

Wortell Group BV

Belgium-based provider of IT software and solutions, as well as IT consulting services

n.a. n.a. n.a. n.a.

Application 04.05.2021

Acronis International GmbH

SwitzerlandCVC Capital Partners Limited

Switzerland-based company engaged in providing cyber protection and hybrid cloud storage services

2,079.2 n.a. n.a. n.a.

SaaS 27.04.2021Userlike UG(90% Stake)

Germany

Lime Technologies AB

Germany-based software-as-a-service (SaaS) company engaged in providing customer messaging solutions

n.a. n.a. n.a. n.a.

IT Service 23.04.2021

HCS Company B.V.

Netherlands

Axxes NV

Netherland-based IT company developing software and providing IT services

n.a. n.a. n.a. n.a.

Application 22.04.2021

C4 Software BV

Netherlands

Stichting eX: plain

Netherlands-based software developer of standard course, exam and training software, tailor-made web portals and administration software for associations

n.a. n.a. n.a. n.a.

Application 15.04.2021

ExtraMed Limited

United Kingdom

Alcidion Group Limited

UK-based provider of patient flow management software for the healthcare sector

6.1 0.5x n.a. n.a.

Development 14.04.2021Evolve Technology Sweden AB

Sweden

AF Poyry AB

Sweden-based company engaged in software development and digital services in areas such as medtech, finance, retail and cyber security

12.9 1.5x n.a. n.a.

Development 08.04.2021

Copenhagen Software A/S

Denmark

IT Relation A/S

Denmark-based software development and consulting company specialized in Microsoft technologies

n.a. n.a. n.a. n.a.

Application 06.04.2021

Sage Schweiz AG

Switzerland

Infoniqa Holding GmbH

Switzerland-based business unit of a British company engaged in the development, distribution and support of business management software

45.2 1.5x n.a. 9.6x

Selected Transactions (IV/IV)

40

Q2 2021 with a focus on European MidCap transactions

July 2021

IMAP M&A Consultants AG

41

Offices

July 2021

IMAP M&A Consultants AG

Mannheim

Harrlachweg 1

68163 Mannheim

Telefon: +49 621 3286-0

Fax: +49 621 3286-100

E-mail: [email protected]

Internet: www.imap.de

Frankfurt am Main

Junghofstraße 2460311 Frankfurt am MainTelefon: +49 69 2999276-600

München

Bernhard-Wicki-Straße 380636 MünchenTelefon: +49 89 5402273-0

July 2021 42

![Georgian Banking Sector And Tbc Bank 2011 Q2[1]](https://img.pdfslide.us/doc/110x75/555c8a33d8b42a85758b45c8/georgian-banking-sector-and-tbc-bank-2011-q21.jpg)