Embed Size (px)

Citation preview

MACROECONOMIC OUTLOOKPUBLISHED MAY 9, 2019 | ERIC BASMAJIAN | FATRADER.COM

MACROECONOMIC FRAMEWORK

2FATRADER.com Not For Redistribution

Secular

Economic

Trends

Business Cycle

Trends

Short-Term

Growth Cycle

Trends

10+ Year

Trends

6-10 Year

Trends

12-36

Month

Trends

SECULAR DECLINE IN NOMINAL GDP GROWTH

3FATRADER.com Not For Redistribution

Nominal GDP growth

(growth + inflation)

has been in a secular

decline since 1980.

This decline is due to

debt, demographics

and productivity

growth.

REAL GROWTH + INFLATION

4FATRADER.com Not For Redistribution

Nominal growth,

headline inflation, and

real GDP growth are

all in secular decline

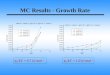

POPULATION GROWTH & PRODUCTIVITY GROWTH

5FATRADER.com Not For Redistribution

The product of

population growth and

productivity growth

comprise long-run

trend GDP growth.

POPULATION GROWTH PROJECTION

6FATRADER.com Not For Redistribution

US population growth

is projected to decline

through 2060.

A continued decline in

population growth will

drag GDP growth

lower over time.

LOWER GROWTH WILL BRING LOWER INTEREST RATES

7FATRADER.com Not For Redistribution

Over the long run,

interest rates follow

the trends in nominal

GDP growth.

As is the case in

Europe and Japan, a

continued decline in

growth will push

interest rates towards

the zero bound.

MACROECONOMIC FRAMEWORK

8FATRADER.com Not For Redistribution

Secular

Economic

Trends

Business Cycle

Trends

Short-Term

Growth Cycle

Trends

10+ Year

Trends

6-10 Year

Trends

12-36

Month

Trends

BUSINESS CYCLE TRENDS

9 Not For Redistribution

• Housing

• Durable Goods

• Automobiles

Housing, durable

goods and auto sales

are all big-ticket items

in the consumer

basket, are sensitive to

changes in interest

rates and subject to

the economic concept

of pent-up demand.

FATRADER.com

BUSINESS CYCLE TRENDS

10 Not For Redistribution

This is the third

slowdown of this

economic cycle.

The Business Cycle

Index has not

registered a sustained

negative growth rate

which would be a

major red flag in

terms of business

cycle risk.

FATRADER.com

MACROECONOMIC FRAMEWORK

11 Not For Redistribution

Secular

Economic

Trends

Business Cycle

Trends

Short-Term

Growth Cycle

Trends

10+ Year

Trends

6-10 Year

Trends

12-36

Month

Trends

FATRADER.com

GROWTH RATE CYCLE TRENDS

12 Not For Redistribution

• Employment

• Industrial Production

• Personal Income

• Consumption

As the secular trends

illustrated, growth has

been trending lower.

Within the business

cycle, growth goes

through periods of

acceleration and

deceleration.

We are currently in a

period of deceleration.

FATRADER.com

GROWTH RATE CYCLE TRENDS

13 Not For Redistribution

The US experienced a

sharp deceleration in

growth in 2015-2016

that nearly resulted in

a recession.

Today, growth, based

on the coincident

index, has

decelerated form

2.75% to 1.87%.

FATRADER.com

GROWTH RATE CYCLE TRENDS

14 Not For Redistribution

The Treasury market

follows the rate of

change in

growth/inflation.

The bond market can

often lead.

This is a coincident

index, but we have

leading indexes that

predict moves in the

coincident index.

FATRADER.com

WHERE ARE WE TODAY?

15 Not For Redistribution

Secular economic trends

point towards a long run

decline in US economic

growth prospects.

Business cycle trends

have flattened as pent-up

demand is exhausted.

After a boost from

government spending

and tax cuts, US

economic growth is

decelerating

Secular Trends ↓

Business Cycle Trends →

Growth Rate Cycle Trends ↓

FATRADER.com

ARE WE CLOSE TO A RECESSION? YES & NO.

16 Not For Redistribution

Economic growth has not

slowed sufficiently to put

the economy at risk of

recession, but it is getting

close.

Should the coincident

index continue to move

lower, sub 1.5%, the

economy becomes

vulnerable to a shock.

FATRADER.com

ARE WE CLOSE TO A RECESSION? YES & NO.

17 Not For Redistribution

Economic growth has not

slowed sufficiently to put

the economy at risk of

recession, but it is getting

close.

Should the coincident

index continue to move

lower, sub 1.5%, the

economy becomes

vulnerable to a shock.

Secular Trends ↓ +

Business Cycle Trends ↓

+ Growth Rate Cycle

Trends ↓ (Below 1.5%) +

Shock = Recession

FATRADER.com

WHY IS LOW GROWTH A PROBLEM?

18 Not For Redistribution

Eventually, a secular

decline in trend growth

becomes problematic.

For now, not many are

worried about 2% trend

growth.

Next cycle, if trend

growth moves below

1.5%, as is the case in

Japan, the economy

becomes perpetually

vulnerable to shocks and

recessions become

frequent.

FATRADER.com

MY FOCUS IS ON INTEREST RATES

19 Not For RedistributionFATRADER.com

• I prefer to overweight risk when risk assets

have performed in line or underperformed

economic growth, coupled with accelerating

business cycle trends and accelerating

growth rate cycle trends.

• I believe the highest probability bet in this

environment is for a continued decline in

interest rates.

CLOSING THOUGHTS

20 Not For Redistribution

• Secular economic trends will continue to move lower over time

• The economy is not vulnerable to a recession quite yet, but a continued

decline in economic growth will make the economy vulnerable to a

shock

• I am not betting against US stocks, but when economic growth is

decelerating, the risk of corrections increases (NYSE Composite has

not made a new high since January 2018)

• Over the next 12-36 months, my shortest timeframe, I believe we will

see lower, not higher interest rates.

FATRADER.com