Embed Size (px)

Citation preview

ASIA MARKET SNAPSHOT Q 1 1 7CAPITAL MARKETS & INVESTMENT SERVICES

ASIA MARKET SNAPSHOT Q1 2017 | 3 CAPITAL MARKETS & INVESTMENT SERVICES

JEROME WRIGHT

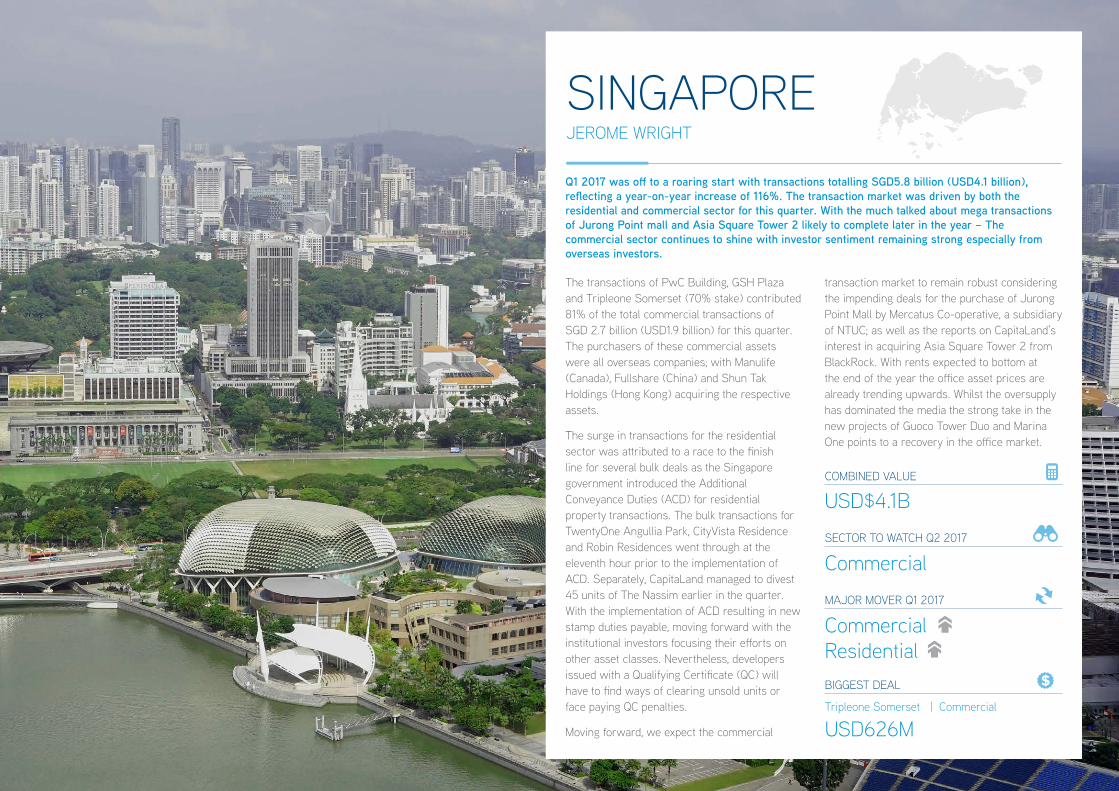

SINGAPOREQ1 2017 was off to a roaring start with transactions totalling SGD5.8 billion (USD4.1 billion), reflecting a year-on-year increase of 116%. The transaction market was driven by both the residential and commercial sector for this quarter. With the much talked about mega transactions of Jurong Point mall and Asia Square Tower 2 likely to complete later in the year – The commercial sector continues to shine with investor sentiment remaining strong especially from overseas investors.

The transactions of PwC Building, GSH Plaza and Tripleone Somerset (70% stake) contributed 81% of the total commercial transactions of SGD 2.7 billion (USD1.9 billion) for this quarter. The purchasers of these commercial assets were all overseas companies; with Manulife (Canada), Fullshare (China) and Shun Tak Holdings (Hong Kong) acquiring the respective assets.

The surge in transactions for the residential sector was attributed to a race to the finish line for several bulk deals as the Singapore government introduced the Additional Conveyance Duties (ACD) for residential property transactions. The bulk transactions for TwentyOne Angullia Park, CityVista Residence and Robin Residences went through at the eleventh hour prior to the implementation of ACD. Separately, CapitaLand managed to divest 45 units of The Nassim earlier in the quarter. With the implementation of ACD resulting in new stamp duties payable, moving forward with the institutional investors focusing their efforts on other asset classes. Nevertheless, developers issued with a Qualifying Certificate (QC) will have to find ways of clearing unsold units or face paying QC penalties.

Moving forward, we expect the commercial

transaction market to remain robust considering the impending deals for the purchase of Jurong Point Mall by Mercatus Co-operative, a subsidiary of NTUC; as well as the reports on CapitaLand’s interest in acquiring Asia Square Tower 2 from BlackRock. With rents expected to bottom at the end of the year the office asset prices are already trending upwards. Whilst the oversupply has dominated the media the strong take in the new projects of Guoco Tower Duo and Marina One points to a recovery in the office market.

MAJOR MOVER Q1 2017

CommercialResidential

COMBINED VALUE

USD$4.1B

SECTOR TO WATCH Q2 2017

Commercial

BIGGEST DEAL

Tripleone Somerset | Commercial

USD626M

4 | ASIA MARKET SNAPSHOT Q1 2017 CAPITAL MARKETS & INVESTMENT SERVICES

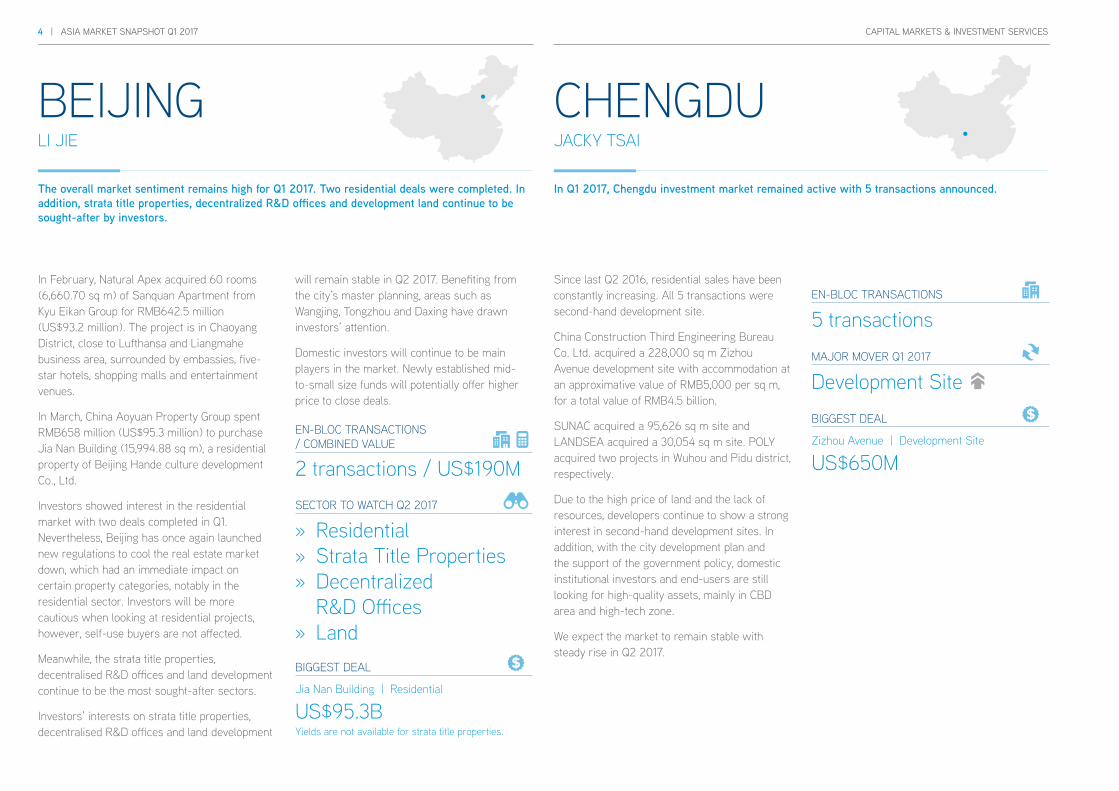

In Q1 2017, Chengdu investment market remained active with 5 transactions announced.The overall market sentiment remains high for Q1 2017. Two residential deals were completed. In addition, strata title properties, decentralized R&D offices and development land continue to be sought-after by investors.

LI JIE JACKY TSAI

CHENGDUBEIJING

In February, Natural Apex acquired 60 rooms (6,660.70 sq m) of Sanquan Apartment from Kyu Eikan Group for RMB642.5 million (US$93.2 million). The project is in Chaoyang District, close to Lufthansa and Liangmahe business area, surrounded by embassies, five-star hotels, shopping malls and entertainment venues.

In March, China Aoyuan Property Group spent RMB658 million (US$95.3 million) to purchase Jia Nan Building (15,994.88 sq m), a residential property of Beijing Hande culture development Co., Ltd.

Investors showed interest in the residential market with two deals completed in Q1. Nevertheless, Beijing has once again launched new regulations to cool the real estate market down, which had an immediate impact on certain property categories, notably in the residential sector. Investors will be more cautious when looking at residential projects, however, self-use buyers are not affected.

Meanwhile, the strata title properties, decentralised R&D offices and land development continue to be the most sought-after sectors.

Investors’ interests on strata title properties, decentralised R&D offices and land development

Since last Q2 2016, residential sales have been constantly increasing. All 5 transactions were second-hand development site.

China Construction Third Engineering Bureau Co. Ltd. acquired a 228,000 sq m Zizhou Avenue development site with accommodation at an approximative value of RMB5,000 per sq m, for a total value of RMB4.5 billion.

SUNAC acquired a 95,626 sq m site and LANDSEA acquired a 30,054 sq m site. POLY acquired two projects in Wuhou and Pidu district, respectively.

Due to the high price of land and the lack of resources, developers continue to show a strong interest in second-hand development sites. In addition, with the city development plan and the support of the government policy, domestic institutional investors and end-users are still looking for high-quality assets, mainly in CBD area and high-tech zone.

We expect the market to remain stable with steady rise in Q2 2017.

will remain stable in Q2 2017. Benefiting from the city’s master planning, areas such as Wangjing, Tongzhou and Daxing have drawn investors’ attention.

Domestic investors will continue to be main players in the market. Newly established mid-to-small size funds will potentially offer higher price to close deals.

EN-BLOC TRANSACTIONS / COMBINED VALUE

2 transactions / US$190M

EN-BLOC TRANSACTIONS

5 transactions

SECTOR TO WATCH Q2 2017

» Residential » Strata Title Properties » Decentralized R&D Offices

» LandBIGGEST DEAL

Jia Nan Building | Residential

US$95.3BYields are not available for strata title properties.

BIGGEST DEAL

Zizhou Avenue | Development Site

US$650M

MAJOR MOVER Q1 2017

Development Site

ASIA MARKET SNAPSHOT Q1 2017 | 5 CAPITAL MARKETS & INVESTMENT SERVICES

ANTONIO WU

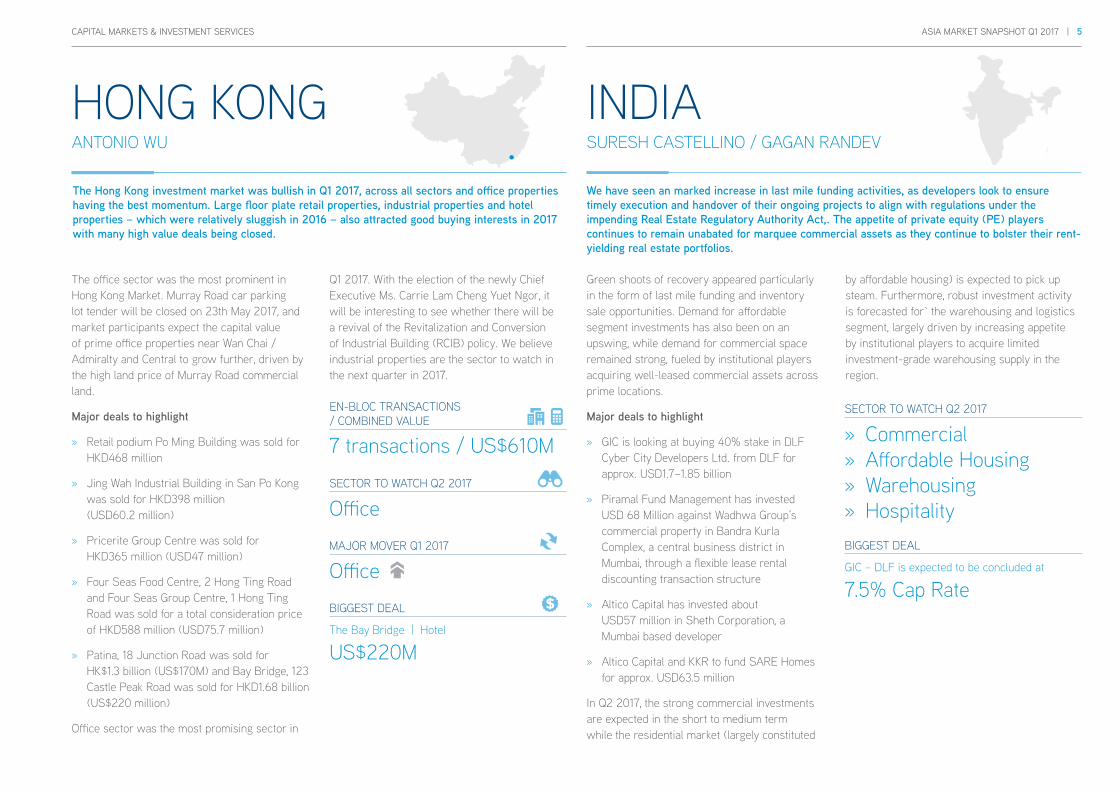

HONG KONGThe Hong Kong investment market was bullish in Q1 2017, across all sectors and office properties having the best momentum. Large floor plate retail properties, industrial properties and hotel properties – which were relatively sluggish in 2016 – also attracted good buying interests in 2017 with many high value deals being closed.

We have seen an marked increase in last mile funding activities, as developers look to ensure timely execution and handover of their ongoing projects to align with regulations under the impending Real Estate Regulatory Authority Act,. The appetite of private equity (PE) players continues to remain unabated for marquee commercial assets as they continue to bolster their rent-yielding real estate portfolios.

SURESH CASTELLINO / GAGAN RANDEV

INDIA

The office sector was the most prominent in Hong Kong Market. Murray Road car parking lot tender will be closed on 23th May 2017, and market participants expect the capital value of prime office properties near Wan Chai / Admiralty and Central to grow further, driven by the high land price of Murray Road commercial land.

Major deals to highlight

» Retail podium Po Ming Building was sold for HKD468 million

» Jing Wah Industrial Building in San Po Kong was sold for HKD398 million (USD60.2 million)

» Pricerite Group Centre was sold for HKD365 million (USD47 million)

» Four Seas Food Centre, 2 Hong Ting Road and Four Seas Group Centre, 1 Hong Ting Road was sold for a total consideration price of HKD588 million (USD75.7 million)

» Patina, 18 Junction Road was sold for HK$1.3 billion (US$170M) and Bay Bridge, 123 Castle Peak Road was sold for HKD1.68 billion (US$220 million)

Office sector was the most promising sector in

Q1 2017. With the election of the newly Chief Executive Ms. Carrie Lam Cheng Yuet Ngor, it will be interesting to see whether there will be a revival of the Revitalization and Conversion of Industrial Building (RCIB) policy. We believe industrial properties are the sector to watch in the next quarter in 2017.

EN-BLOC TRANSACTIONS / COMBINED VALUE

7 transactions / US$610M

SECTOR TO WATCH Q2 2017

Office

BIGGEST DEAL

The Bay Bridge | Hotel

US$220M

OfficeMAJOR MOVER Q1 2017

Green shoots of recovery appeared particularly in the form of last mile funding and inventory sale opportunities. Demand for affordable segment investments has also been on an upswing, while demand for commercial space remained strong, fueled by institutional players acquiring well-leased commercial assets across prime locations.

Major deals to highlight

» GIC is looking at buying 40% stake in DLF Cyber City Developers Ltd. from DLF for approx. USD1.7–1.85 billion

» Piramal Fund Management has invested USD 68 Million against Wadhwa Group’s commercial property in Bandra Kurla Complex, a central business district in Mumbai, through a flexible lease rental discounting transaction structure

» Altico Capital has invested about USD57 million in Sheth Corporation, a Mumbai based developer

» Altico Capital and KKR to fund SARE Homes for approx. USD63.5 million

In Q2 2017, the strong commercial investments are expected in the short to medium term while the residential market (largely constituted

SECTOR TO WATCH Q2 2017

» Commercial » Affordable Housing » Warehousing » Hospitality

BIGGEST DEAL

GIC – DLF is expected to be concluded at

7.5% Cap Rate

by affordable housing) is expected to pick up steam. Furthermore, robust investment activity is forecasted for` the warehousing and logistics segment, largely driven by increasing appetite by institutional players to acquire limited investment-grade warehousing supply in the region.

6 | ASIA MARKET SNAPSHOT Q1 2017 CAPITAL MARKETS & INVESTMENT SERVICES

MYANMARThe new investment law passed last November 2016 has been augmented by a set of notifications released at the end of Q1 2017, providing more detailed breakdown from the initial provisions of the law. With further reforms in the pipeline, including a new Companies Act, the overall investment environment could take a significant turn for the better in the coming quarters.

TONY PICON

While this is still to be digested by analysts, the consensus is that the new law is an improvement from the previous investment laws and perhaps most importantly provides a unified framework covering both foreign and domestic investors.

The holding pattern remains, but the rest of the year could see take-off in market activity. Q1 2017 remained subdued for investment activity in Yangon, although the final approval of Yoma Central, a landmark 10-acre development in downtown in Q1, provided a welcome stimulus to overall real estate investment sentiment. This was after an over three-year delay due to protracted leasehold negotiations with the ministry involved. Although there is overall dissatisfaction with the pace of reforms by the year-old government led by Aung San Su Kyi, many potential investors are taking another serious look at the country. There is greater activity in market research as well as advisory sectors on specific projects prior to making firmer decisions with the industrial and logistics sector particularly active.

The issues regarding land ownership and high prices remain serious impediments for real estate investors, especially for smaller scale projects more suitable for private land plots.

Local investors also face this issue if they do not have access to their own land bank. Zoning laws in Yangon remain opaque given the various and sometimes conflicting, master plans and large infrastructure projects slated for the region. However, the overall mood is positive for Yangon as well as for the whole country.

SECTOR TO WATCH Q2 2017

Serviced Apartments

INDONESIALarge office tenants have been achieving 25–50% discounts in total packages compared to 18–24 months ago. Due to the lack of additional supply in the CBD area since last two quarters last year, the cumulative supply remained stable at 5.48 million as of Q4 2016. Asking rents continued their downward trend over the last two years with an average asking base rent in the CBD registered at IDR311,750/sq m/month representing a 6.2% decline YoY.

STEVE ATHERTON

No major investment transactions were registered since last quarter. While effective and contracted office rentals fell substantially the last two years, developers and owners have been able to hold their capital values. There is no evidence of serious price adjustments despite the oversupply and upcoming overhang. This is due to reasonably low levels of leverage and a lending system that gives the borrower more recovery time than they might get from more mature markets.

Following the completion of 19,271 apartment units during 2016, the cumulative supply of apartments in Jakarta increased by 12.3% YoY, bringing the total stock to 176,178 units. The market has yet to show a significant recovery after the government rolled out measures designed to boost the property market, including tax amnesty, a higher LTV and lower interest rates.

Besides the for-sale affordable (mid-market) apartment sector, the office sector remains the top choice of foreign investors and developers. However, finding the right entry point remains tricky as 2017 estimated new supply in the CBD is approximately just above 700,000 sq m with estimates for 2018 and 2019 well above 600,000 sq m. Considering the average annual

absorption in the range of 200,000– 300,000 sq m, we expect rents and occupancies to continue to drop.

SECTOR TO WATCH Q2 2017

Office

LogisticsMAJOR MOVER Q1 2017

ASIA MARKET SNAPSHOT Q1 2017 | 7 CAPITAL MARKETS & INVESTMENT SERVICES

The Philippine economy was one of the best performing in Asia in 2016 with 6.9% GDP growth in 2016. The real estate sector remained in a bright spot and property analysts together with industry players forecast the growth surge will spill over to Q1 2017. The government aims to spur growth further with strengthened foreign relations and increased infrastructure spending that will expand development not just in Metro Manila but also outside the country’s capital.

IEYO DEGUZMAN

PHILIPPINES

Mitsubishi Corp. in partnership with Century Properties Group Inc. (high-end developer) launched its first joint project, a 3,000-unit housing community in a 26-hectare area in Tanza, Cavite. The venture project will cater to the underserved housing demand in middle- income segment.

The office sector remained robust with Q1 2017 take up for office space driven more by non-BPO companies notably from offshore gaming companies. Over all Metro Manila vacancy is at 4% putting an upward pressure on the lease rates.

The retail sector expansion is sustained by a strong consumer-based demand (F&B, fast fashion and lifestyle shops). Developers are building branded community malls in the provincial locations to serve as a catalyst for economic growth of the area.

In the residential sector, luxury three-bedroom condominium units remain in demand amid rising vacancies in the low to mid-level condominiums. Residential capital values continue to rise as rents are slowly declining.

Sectors to watch are retail and Industrial sectors in Q2 2017. For retail, the completion of community and neighbourhood malls in the last

few quarters have provided increased consumer spending. Fast fashion and F&B are key sectors in a consumer market dominated by millennials.

Noted in the industrial sector is the growing demand for manufacturers and retailers’ distribution hub to support retail operations. The automotive industry 27* YoY growth with Toyota, Mitsubishi and Ford top performers expansion plans are in the offing. The government efforts to attract more foreign manufacturing companies are manifested by increasing interest from Japan, Korea and China.

SECTOR TO WATCH Q2 2017

» Retail » Industrial

» Retail » Office

MAJOR MOVER Q1 2017

As mentioned in Q4 2016, the Shanghai en-bloc transaction market remained active in the first quarter of 2017, with investors and corporations mainly focusing on Shanghai market. Investors accounted for 11 of the 12 transactions in Q1, with a combined transaction volume of approximately CNY21 billion (USD3 billion).

BFC, a fully integrated mixed-use complex located in the heart of the Bund Financial Belt and covering approximately 420,000 sq m with a panoramic view of Huangpu River, was the biggest transaction closed in Q1 2017. It is a 50% equity share transfer deal at a total consideration of CNY5,330 billion (USD770 million). The buyer was the domestic investor Jiaxing Shengshi Shenzhou Wenli Investment Partnership.

Office remained the major focus sector, witnessed by 7 out of 11 transactions concluded in Q1. Garden Square and No.686, Jiujiang Road were transacted in the CBD area; while Central Park, Block E of Hongqiao Green Valley Plaza, Block No.2/3/5 of Zhabei Orstar City, Tower B1 of Poly Greenland Plaza and Huangxing Mansion were transacted in DBD areas. Starcrest Corporate Plaza and Shanghai International Trade Center were transacted in the business park sector, while China Garden and Belgravia Place were transacted in the serviced apartment sector.

The investment market outlook in Q2 2017 remains optimistic. Last quarter, we forecasted a strong investors demand in assets purchase, as well as a limited number of tradable properties available in the market. Thus, we

BETTY WONG

SHANGHAI

expect a moderate increase of the capital value, and investment yields should remain stable.

EN-BLOC TRANSACTIONS

12 transactions

BIGGEST DEAL

BFC

USD$770M

MAJOR MOVER Q1 2017

Office

8 | ASIA MARKET SNAPSHOT Q1 2017 CAPITAL MARKETS & INVESTMENT SERVICES

DEREK HUANG

TAIPEIThe market continues to decline mainly due to harsh property-holding taxes as we mentioned last year. The total transaction volume in Q1 2017 was TWD21.5 billion (USD717 million), a decrease of 59% compared to Q4 2016 and a decrease of 23% compared to Q1 2016. With the market on a downturn and softening of property prices, buyers enjoyed greater bargaining power.

Occupational buyers remain active in Q1 as they now face lesser competition and can shop around. CyberPower Systems purchased an industrial office building in Neihu Technology Park for its own headquarters for TWD2.6 billion (USD87 million). Kerry TJ Logistics purchased an industrial plot in Tainan, planning to develop its logistics centre. In addition, there were several transactions for occupational purposes in decentralised areas such as Zhonghe Industrial Park and Xindian Industrial Park (both in New Taipei City).

Due to the scarcity of land in Taipei, investors are pursuing land investment opportunity at good location so long the price is right. For instance, Cathay Life Insurance purchased a commercial plot in Nanjing/Songjiang business district for TWD2.3 billion (USD77 million). Ruentex Development spent TWD3.5 billion (USD117 million) on a commercial plot in Nangang district.

As occupational buyers continue to look at office assets, we expect office will remain the most sought-after sector. Moreover, transportation infrastructures such as Taoyuan airport express-train system and new MRT lines within Taipei metropolitan are bringing growth potentials to emerging areas among the suburban area of

Taipei City, New Taipei City, and Taoyuan City.

SUNCHAI KOOAKACHAI

THAILANDThe market outlook in Q1 2017 was mostly driven by the tourism sector and government heavy spending in infrastructure aiming to boost consumer confidence in the property market. We expect private consumption to increase due to the new mass transits bidding process in Bangkok and provincial by government sector. In the investment sector, big listed residential developers are still buying prime land for new high-end projects and acquiring new assets through merge & acquisition.

The investment sector is still performing well as large listed residential developers continue to buy prime land or long lease land along mass transit routes and within the core of CBD area for new middle to high-end projects e.g. land lease deal in Ploenchit area by Raimond land, new joint venture partnership between CPN and Dusit Thani for mixed-use project worth around THB 36.7 billion on land lease in Bangkok. High-net-worth individuals and corporates continue to be pressured by low interest rates, expecting an increase in land transaction in Bangkok and its vicinities.

Demand for Grade A and B office remained strong in all main locations. Demand for residential strengthened in high-end condominium with prime location as well. Bank tight lending policy and high-household debt have kept pressuring the general market.

We expect a better market outlook in Q2 2017 with interest and inflation to remain at a low rate, and new mass transits bidding process on infrastructure projects. Due to high land prices, shortage of construction workers and still a strong tourism sector, we expect an increase in overall transactions in both land and hotel deals in Bangkok and its surrounding in the next quarter.

EN-BLOC TRANSACTIONS

1 transaction

BIGGEST DEAL

Prince Tanmei Building

2.6% yields(Assume 100% leased)

MAJOR MOVER Q1 2017

Office

BIGGEST DEAL

Amata Nakorn IE Phase 4 | Land for industrial development

US$3.1M

MAJOR MOVER Q1 2017

OfficeResidential

SECTOR TO WATCH Q2 2017

Hotels

ASIA MARKET SNAPSHOT Q1 2017 | 9 CAPITAL MARKETS & INVESTMENT SERVICES

The Vietnam economy saw a growth of 5.1% in Q1 2017, which was slightly lower than the same period last year but continued to be led by the service, industry, construction and agricultural sectors. FDI is the impressive figure to note, gaining 77.6% on last year with significant contributions from some of our key clients in Korea & Japan. Better accessibility from increased regional flight routes and the growth of airlines such as VietJet should contribute to overall number of visitors’ growth in Vietnam.

ADAM FITZPATRICK

VIETNAM

be difficult to acquire. The residential market continues to be tricky to break into for foreign investors, because of the significant competition from the major local player such as Vingroup and Novaland and the well-established regional developers such as Keppel Land and CapitaLand. Hospitality assets and land plays are likely to see significant uplift in Q2 2017.

Two large HCMC CBD office building transactions were completed in Q1 2017, both were off-market and without representation from international firms, reflecting the approach of some investors here in Vietnam. None of the buildings were Grade A or located in prime CBD, but both were reportedly sold at above market value. A major coup to highlight for Colliers is the exclusive management and leasing instruction at Deutsches Haus, a true international standard development and a key milestone for Vietnam, opening in Q3 2017.

The last quarter saw significant growth in enquiries for industrial assets and industrial land. This trend is set to continue during Q2 of 2017and reflects the growing demand from regional Industrial Park developer-owner-operators providing facilities that reflect the standard of their home nations. This demand was also driven by manufacturers and logistics firms looking to expand their regional presence, Vietnam being the preferred location. Commercial-oriented Vietnamese Industrial Zone owners will see impressive upside.

In addition to the continued growth in the industrial sector, we see all development opportunities gaining value over the next quarter as good operational assets continue to

BIGGEST DEAL

HCMC CBD Office Grade B+ c. 8%

EN-BLOC TRANSACTIONS / COMBINED VALUE

2 off market transactions / c. US$115MSECTOR TO WATCH Q2 2017

» Development Land (All) » Hospitality Assets

MAJOR MOVER Q1 2017

Industrial Land

15–16 May 2017 | Singapore

APREA ASIAPAC PROPERTY LEADERS SUMMIT 2017

This annual Summit explores the trends and drivers shaping property fundamentals and new business opportunities, as well as providing an excellent platform for business networking and relationship building with senior industry leaders.

Colliers is proud to be a Silver Sponsor, and Terence Tang, Managing Director, CMIS Asia, will be participating as a panellist in the session entitled Emerging Asset Classes on 16 May, 2:15p.m.

24–25 May 2017 | Shanghai

PERE CHINA FORUM 2017

The PERE China Forum is China’s most influential private real estate event. This year, it will be held at Wanda Reign on the Bund, and is a rare opportunity and excellent platform to connect with the most active investors from Greater China and across the globe.

Colliers is a proud sponsor of PERE China, with the below participation:

» Betty Wong, Head of CMIS, China, will be participating in the Opening Panel Discussion, What kind of investment strategies will investors put into play in 2017 and beyond? on 25 May, 9:05a.m.

» Andrew Haskins, Head of Research, Asia, will also issue a China-centric report during the event.

Colliers is also hosting an Investor Cocktail Prty on 24 May at Hotel Indigo Shanghai on the Bund which is expected to attract more than 120 top investors.

UPCOMING EVENTS

For more information on regional CMIS events, please contact Maybelyne Ng at [email protected]

Our integrated services platform of more than 120 professionals collaborate seamlessly across 39 Asian locations, to serve our clients’ multiple market requirements, tailored to their needs. The team works

to anticipate global investor trends and implications that matter most to our clients, a true partner committed to their success. When our clients

partner with us they gain access to unparalleled Asian investment insights and direct connections with key decision-makers of Asian-based investors

and property owners, allowing inroads to exclusive local opportunities.

This is the better value for our clients, in times of change.

AN INTEGRATED NETWORK: ACROSS ASIA

ASIA | INDONESIA | TAIWANBest Overall Investment Managers

THIS IS WHAT MAKES US DIFFERENT

REGIONAL BREADTHGLOBAL REACH

LOCAL DEPTH

Capital Markets & Investment Services (CMIS)

This document has been prepared by Colliers International for advertising and general information only. Colliers International makes no guarantees, representations or warranties of any kind, expressed or implied, regarding the information including, but not limited to, warranties of content, accuracy and reliability. Any interested party should undertake their own inquiries as to the accuracy of the information. Colliers International excludes unequivocally all inferred or implied terms, conditions and warranties arising out of this document and excludes all liability for loss and damages arising there from. This publication is the copyrighted property of Colliers International and/or its licensor(s). ©2016. All rights reserved.

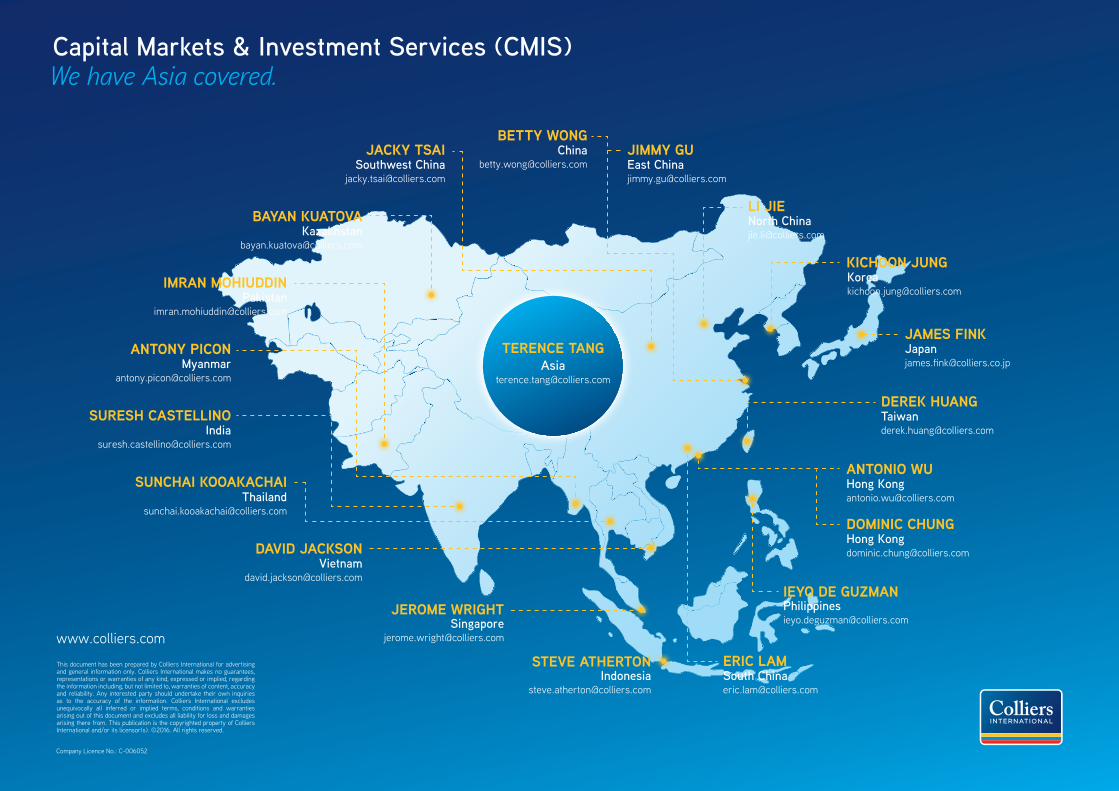

TERENCE TANGAsia

KICHOON JUNG

East [email protected]

JIMMY GUBETTY WONG

JAMES FINK

South [email protected]

ERIC LAM

SUNCHAI KOOAKACHAI Hong [email protected]

ANTONIO WU

Hong [email protected]

DOMINIC CHUNG

IEYO DE GUZMAN

DAVID JACKSON

DEREK HUANG

IMRAN MOHIUDDIN

SURESH CASTELLINO

ANTONY PICON

JEROME WRIGHT

STEVE ATHERTON

North [email protected]

LI JIEKazakhstan

BAYAN KUATOVA

Southwest [email protected]

JACKY TSAI