Embed Size (px)

Citation preview

8/8/2019 Pwc Entertainment and Media Outlook 2009 2013marcel

http://slidepdf.com/reader/full/pwc-entertainment-and-media-outlook-2009-2013marcel 1/18

The Entertainment & Media Outlook: 2009 - 2013

Dublin Launch – 7 July 2009

Marcel FenezGlobal Leader, Entertainment and Media PracticePricewaterhouseCoopers

8/8/2019 Pwc Entertainment and Media Outlook 2009 2013marcel

http://slidepdf.com/reader/full/pwc-entertainment-and-media-outlook-2009-2013marcel 2/18

Slide 4

Outlook coverage

Internet Access Spending: Wired and Mobile

Internet Advertising: Wired and Mobile

TV Subscriptions and License Fees

Television Advertising

Recorded Music

Filmed Entertainment

Video Games

Consumer Magazine Publishing

Newspaper Publishing

Radio and Out-of-Home Advertising

Consumer and Educational Book Publishing

Business-to-Business Publishing

Slide 4PricewaterhouseCoopers

8/8/2019 Pwc Entertainment and Media Outlook 2009 2013marcel

http://slidepdf.com/reader/full/pwc-entertainment-and-media-outlook-2009-2013marcel 3/18

No place to hide from the digital transformation

Slide 5PricewaterhouseCoopers

8/8/2019 Pwc Entertainment and Media Outlook 2009 2013marcel

http://slidepdf.com/reader/full/pwc-entertainment-and-media-outlook-2009-2013marcel 4/18

2009-10 CAGR

Global E&M Outlook 2009-10: -1.8% CAGR, $1.4 trillion

Slide 6PricewaterhouseCoopers

North America

Latin America

Europe, Middle East,Africa (EMEA)

Asia Pacific

-4.2%

0.4%

-1.9%

1.2%

8/8/2019 Pwc Entertainment and Media Outlook 2009 2013marcel

http://slidepdf.com/reader/full/pwc-entertainment-and-media-outlook-2009-2013marcel 5/18

8/8/2019 Pwc Entertainment and Media Outlook 2009 2013marcel

http://slidepdf.com/reader/full/pwc-entertainment-and-media-outlook-2009-2013marcel 6/18

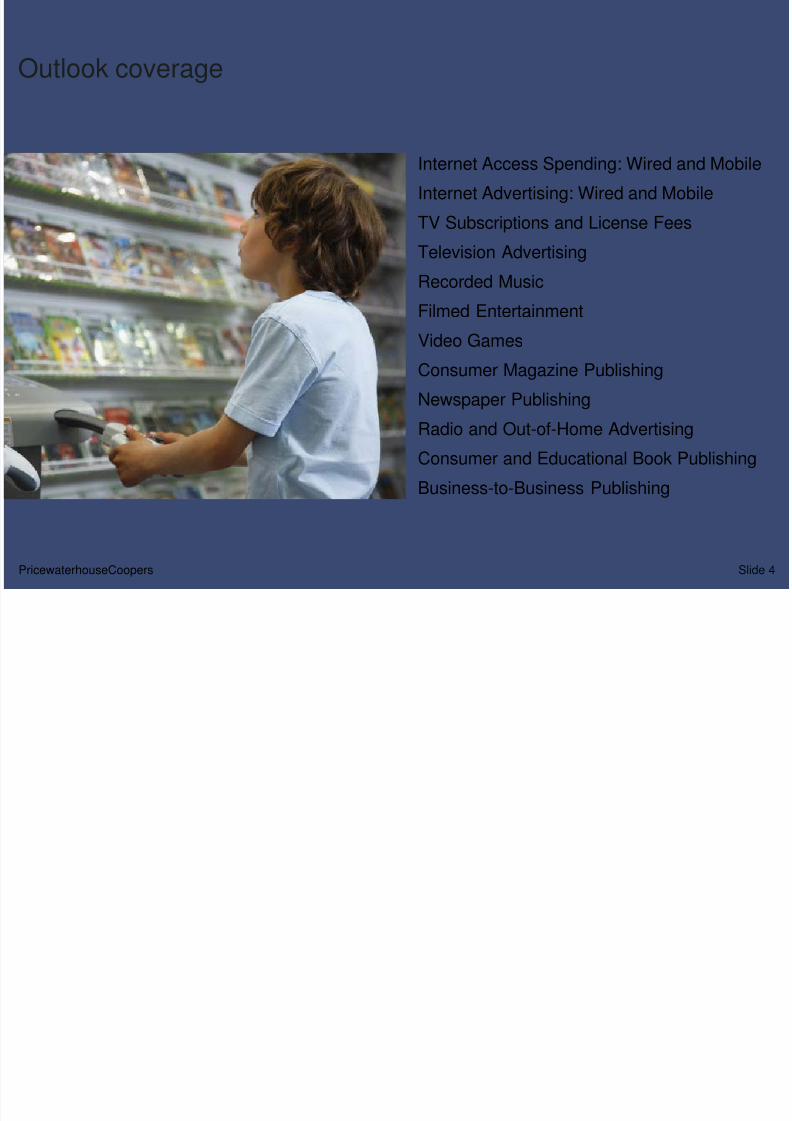

2009-13 CAGR

Global E&M Outlook 2009-2013: 2.7% CAGR, $1.6 trillion

Slide 4PricewaterhouseCoopers

North America

Latin America

Europe, Middle East,Africa (EMEA)

Asia Pacific

-4.2%

0.4%

-1.9%

1.5%

-5.1%

8.4%

-5.8%

1.7%

-1.3%

5.1%

-2.7%

4.5%

8/8/2019 Pwc Entertainment and Media Outlook 2009 2013marcel

http://slidepdf.com/reader/full/pwc-entertainment-and-media-outlook-2009-2013marcel 7/18

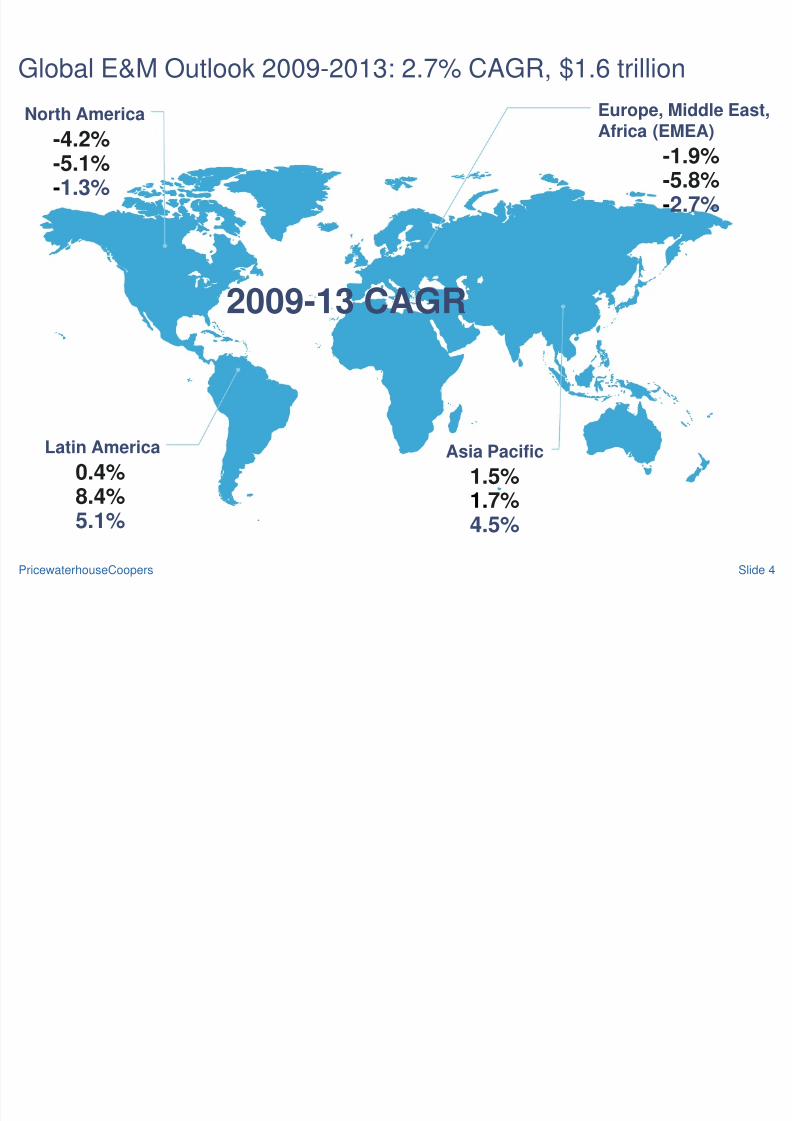

Asia Pacific E&M Outlook 2009-2013: $413 billion (4.5% CAGR)

- By Country

( % G

r o w

t h )

C h i n a

I n d i a

I n d o n e

s i a

P a k i

s t a n

V i e t n a m

A u s t r a l i a

M a l a y s i a

P h i l i p

p i n e s

S o u t h K o

r e a

T a i w a n

T h a i l a n d

0

5

10

15

20

-5

H o n g

K o n g

J a p a n

N e w

Z e a l a n d

S i n g

a p o r e

8/8/2019 Pwc Entertainment and Media Outlook 2009 2013marcel

http://slidepdf.com/reader/full/pwc-entertainment-and-media-outlook-2009-2013marcel 8/18

-10.0 -5.0

Slide 5

A fragmented road to recovery

2009-10 CAGR

2011-13 CAGR

% % % % %

2.4

2.0

3.1

1.5

2.8

8.0

5.4

-0.2

4.0

8.3

12.9

11.8

-8.8

-1.6

-4.4

-7.1

-6.2

6.6

1.9

-5.9

-5.8

3.4

0.3

5.4

0.0 5.0 10.0 15.0

B2B Publishing

Cons. & Edu. Book Pub.

Radio/Out-of-Home

Newspaper Pub.

Consumer Mag. Pub.

Video Games

Filmed Entertainment

Recorded Music

TV Advertising

TV Sub. and Lic. Fees

Internet Ad: Wired & Mobile

Internet Access

8/8/2019 Pwc Entertainment and Media Outlook 2009 2013marcel

http://slidepdf.com/reader/full/pwc-entertainment-and-media-outlook-2009-2013marcel 9/18Slide 11

Slow economy increases the speed of digital migration

Slide 8PricewaterhouseCoopers

8/8/2019 Pwc Entertainment and Media Outlook 2009 2013marcel

http://slidepdf.com/reader/full/pwc-entertainment-and-media-outlook-2009-2013marcel 10/18

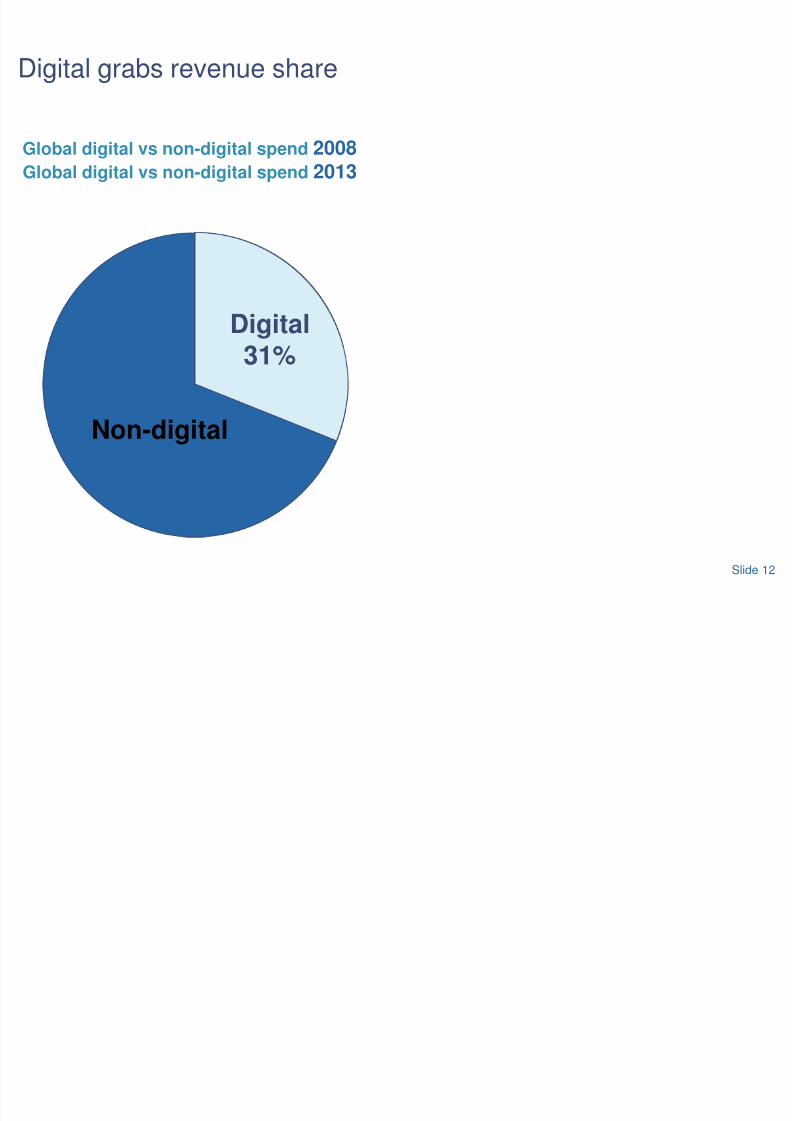

Digital grabs revenue share

Global digital vs non-digital spend 2008

Slide 12

Non-digital

Digital21%Digital31%

Global digital vs non-digital spend 2013

8/8/2019 Pwc Entertainment and Media Outlook 2009 2013marcel

http://slidepdf.com/reader/full/pwc-entertainment-and-media-outlook-2009-2013marcel 11/18Slide 12

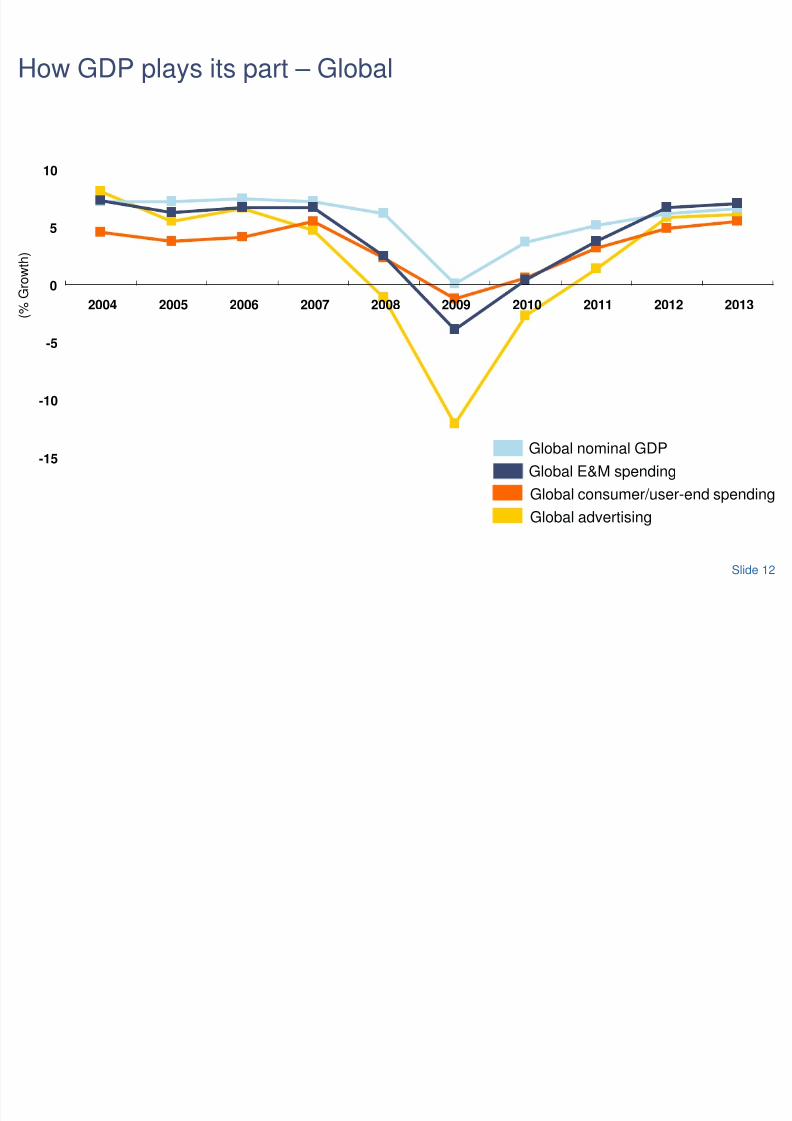

Global nominal GDP

Global E&M spending

How GDP plays its part – Global

Global consumer/user-end spending

Global advertising

( %

G r o w t h )

2009

-15

-10

-5

0

5

10

2004 2005 2006 2007 2008 2010 2011 2012 2013

8/8/2019 Pwc Entertainment and Media Outlook 2009 2013marcel

http://slidepdf.com/reader/full/pwc-entertainment-and-media-outlook-2009-2013marcel 12/18

Consumer behaviour

8/8/2019 Pwc Entertainment and Media Outlook 2009 2013marcel

http://slidepdf.com/reader/full/pwc-entertainment-and-media-outlook-2009-2013marcel 13/18

Slide 15

Digital life

Slide 15PricewaterhouseCoopers

• Always connected

• Multi-tasking• Our time vs. prime time

• Music crosses thethreshold

• Games & movies

• Interactive & social

• Informed

8/8/2019 Pwc Entertainment and Media Outlook 2009 2013marcel

http://slidepdf.com/reader/full/pwc-entertainment-and-media-outlook-2009-2013marcel 14/18

Slide 19

Digital/mobile to account for 78% of all E&M growth – Global

Total spending ondigital/mobile platforms

Other consumer/end-

user/access spending

0 100,000 200,000 300,000 400,000 500,000 600,000 700,000 800,000

2004

2005

2006

2007

2008p

2009

2010

2011

2012

2013

(US$ Millions)

8/8/2019 Pwc Entertainment and Media Outlook 2009 2013marcel

http://slidepdf.com/reader/full/pwc-entertainment-and-media-outlook-2009-2013marcel 15/18

Advertising

8/8/2019 Pwc Entertainment and Media Outlook 2009 2013marcel

http://slidepdf.com/reader/full/pwc-entertainment-and-media-outlook-2009-2013marcel 16/18

Slide 23

2013 global ad spend still trails 2007 levels

Global advertising market

( U

S $ M i l l i o n s )

400,000

425,000

450,000

475,000

500,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

8.1%

6.6%

5.5%

4.7%

1.4%

5.9%

6.1%

-1.1%

-12.1%

-2.7%

8/8/2019 Pwc Entertainment and Media Outlook 2009 2013marcel

http://slidepdf.com/reader/full/pwc-entertainment-and-media-outlook-2009-2013marcel 17/18

Slide 26

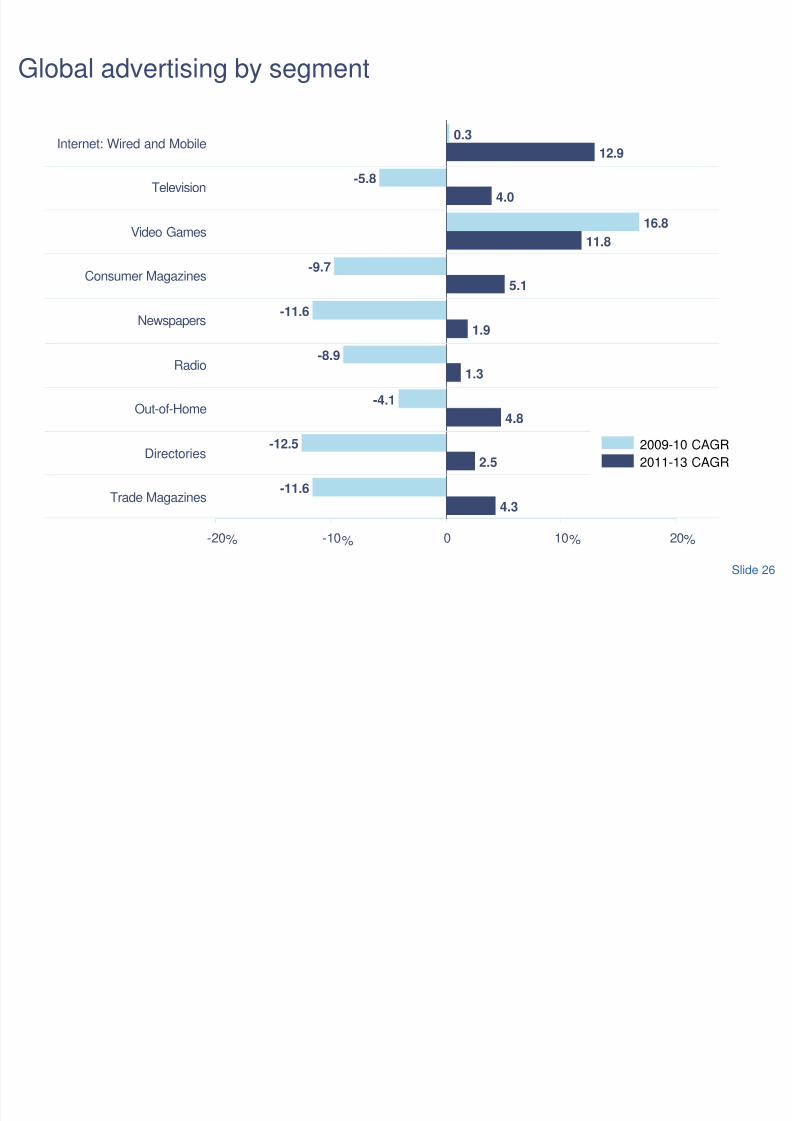

Global advertising by segment

4.3

2.5

4.8

1.3

1.9

5.1

11.8

4.0

12.9

-11.6

-12.5

-4.1

-8.9

-11.6

-9.7

16.8

-5.8

0.3

-20 -10 0 10 20

Trade Magazines

Directories

Out-of-Home

Radio

Newspapers

Consumer Magazines

Video Games

Television

Internet: Wired and Mobile

% % % %

2009-10 CAGR

2011-13 CAGR

8/8/2019 Pwc Entertainment and Media Outlook 2009 2013marcel

http://slidepdf.com/reader/full/pwc-entertainment-and-media-outlook-2009-2013marcel 18/18

Slide 20

Changing face of advertising

Slide 20PricewaterhouseCoopers

• Connected

• Mobile

• Targeted

• Interactive

• Branded content

• Fragmentation

• Cross-platform