Embed Size (px)

Citation preview

1

Public Expenditure &

PEFA Financial Accountability

Guidelines for application of the PEFA Performance Measurement Framework at Sub

National Government Level

Volume 1 – Main Guidelines

Exposure draft

PEFA Secretariat March 2008

2

Table of Contents Abbreviations and Acronyms i

1 Introduction 2 1.1 Objective 2 1.2 Structure of the guidelines 2

2 Types of sub national government 4 2.1 Definition of a sub national entity 4 2.2 Decentralisation, Administrative, Fiscal and Political 4 2.3 Federal and Unitary States 5 2.4 Francophone and Anglophone countries 6

3 Initial planning guidelines 7 3.1 Introduction 7 3.2 Purpose of the assessment 7 3.3 Scope of the assessment 8 3.4 Selection of a representative sample 8 3.5 Assessment of multiple entities 9 3.6 Sources of information 10

4 Application of individual performance indicators 13 4.1 Introduction 13 4.2 Budget credibility 13 4.3 Budget comprehensiveness and transparency 15 4.4 Policy Based Budgeting 18 4.5 Predictability and Control in Budget Execution 19 4.6 Accounting and Reporting 22 4.7 External Audit and Scrutiny 23 4.8 Donor Practices 24 4.9 Central Government Practices 25

5 Modifications to the Performance Report 26 5.1 Executive summary and introduction 26 5.2 Country background 26 5.3 Inter governmental relationship 27 5.4 Assessment of the PFM systems, processes and institutions 28 5.5 Government reform process 29

i

Abbreviations and Acronyms

AGA Autonomous government agency CG Central Government HLG Higher level Government MDA Ministry, Department, Agency NGO Non governmental organisation PE Public Enterprise PEFA Public Expenditure and Financial Accountability PFM Public Financial Management PFM-PR PFM Performance Report PI Performance Indicator SN Sub national ToR Terms of Reference

2

1 Introduction

1.1 Objective

A sound PFM system is essential for the effective implementation of policies and achievement of intended outcomes by supporting aggregate fiscal discipline, strategic allocation of resources and efficient service delivery. Given the increasing importance of sub national government in resource allocation and service provision, the importance of an open and orderly PFM system is equally relevant at the sub national level.

The PEFA framework identifies six critical dimensions of an open and orderly PFM system. These include: budget credibility; budget comprehensiveness and transparency; policy based budgeting; predictability and control in budget execution; adequate accounting, recording and reporting and that appropriate external scrutiny and audit arrangements are operating. The Framework provides a set of 28 high-level PFM indicators to rate performance against these parameters. An additional three indicators assess the impact of donor practices on government performance.

A number of sub-national applications of PEFA have now been conducted either as part of an overall assessment of PFM in the country or as stand alone exercises for either one or more sub national entities. In order to ensure consistent and appropriate application of the indicators and a sound basis for the interpretation of the findings, the PEFA program decided to produce a set of practical and detailed guidelines for SN applications.

On the basis of assessments carried out to date, this report sets out detailed guidelines for the application of all specific indicators and individual dimensions. It provides proposals for modifications and additions to the main performance report and suggestions for sampling and aggregation of results. As far as possible, it attempts to address the wide variety of sub national government structures in existence. As with the guidelines for a central government assessment, these guidelines can be applied by the central or sub national government itself with or without external support from development partners.

1.2 Structure of the guidelines

In section 2, some background discussion is provided on the various types of sub national governments. Initial planning guidelines for the carrying out of a sub national assessment or combined or general government assessment are set out in Section 3. Individual country circumstances will need to be taken into account as to the feasibility of carrying out a combined assessment. Section 4 provides detailed guidance for the application of the individual indicators. Section 5 sets out proposed modifications and additions to the

3

performance report for both individual sub national assessments and for combined1 government reports including suggestions for the aggregation of results (where appropriate). Finally, in Annex 1, the guidelines provide a full overview of the performance indicator rating criteria and background – as included in Section 3 of the PFM Performance Measurement Framework – with highlighted changes as they refer to application at the sub-national level.

1 The term “combined government reports” has been used to cover both general government reporting

where all levels of government are assessed and those instances whereby only two of three levels have been reviewed in countries having three main levels of government.

4

2 Types of sub national government

2.1 Definition of a sub national entity

In the IMF’s GFS 2001 manual, provision is made for three levels of government: central; state, provincial, or regional; and local. The main PEFA assessment is designed to cover all central government institutions irrespective of their location. Sub national government by definition is anything below national (or central) level and thus includes the state and local government sectors. A state, province, or region is defined as “the largest geographical area into which the country as a whole may be divided for political or administrative purposes. These areas may be described by other terms, such as provinces, cantons, republics, prefectures, or administrative regions”2.

The legislative, judicial, and executive authority of local government units is defined as “being restricted to the smallest geographic areas distinguished for administrative and political purposes”. In the manual it is acknowledged that local government units may or may not be entitled to levy taxes on institutional units or economic activities taking place in their areas. It is also recognized that many are likely to be heavily dependent on grants from higher levels of government. In some cases there is also a principal: agent relationship between the central or state government and the local government institution. According to the manual, “statistics for local government may cover a wide variety of governmental units, such as counties, municipalities, cities, towns, townships, boroughs, school districts, and water or sanitation districts”.

However the manual specifies that “to be treated as institutional units, they must be entitled to own assets, raise funds, and incur liabilities by borrowing on their own account. They must also have some discretion over how such funds are spent, and they should be able to appoint their own officers independently of external administrative control.”

The exclusion of institutions with no borrowing powers is however considered to be too restrictive, for the purpose of PEFA assessments. Sub national government is therefore considered as all government entities below central government level which are involved in government activities, have their own budget, can be sued in their own right and have some form of elected/appointed body.

2.2 Decentralisation, Administrative, Fiscal and Political

The institutional structure, responsibilities, powers and characteristics of decentralized institutions vary considerably between countries. Indeed there is significant debate about the meaning of decentralization. The following terms describe the various forms of decentralization in terms of the transfer of powers.

2 GFS 2001 manual p 14

5

Fiscal decentralisation: expenditure assignment, the transfer of funds, and/or tax-raising and/or borrowing powers from higher levels to lower levels in political systems.

Administrative decentralisation (sometimes called ‘deconcentration’): the transfer of administrative powers, and sometimes administrative personnel, from higher to lower levels in political systems.

Democratic (political) decentralisation (sometimes called ‘devolution’): The transfer of funds and powers (including decision-making powers, and sometimes revenue-raising powers) from higher levels in political systems to elected bodies at lower levels.

Fiscal decentralization is clearly central to the success of democratic decentralization, SN assessments carried out to date have been for SN governments that have some degree of democratic decentralization. Fiscal deconcentration means a transfer of responsibilities, powers and resources from the central government (ministries and agencies) to field offices at the local and regional level, thereby becoming closer to the citizens while remaining a part of the central government system. Deconcentrated units (administrations déconcentrées) should therefore be covered by a central government assessment. However, difficulties in interpretation could arise in those instances where there is an appointed body not an elected body, and also for situations in which administrations déconcentrées are part of central government but central government is not, or not fully accountable for their financial activities.

2.3 Federal and Unitary States

Systems of government can be broadly divided into two types: unitary and federal. However, the distinction between a federation and a unitary state is often quite ambiguous. As illustrated in the following paragraphs, there are often similarities between and differences within the two types. A federation is generally described as a union comprising a number of partially self-governing states or regions united by a central ("federal") government. Typically the status of the component states is set out in the Constitution and may not be altered by the federal or central government. Generally, component states also have their own constitutions which can be amended without recourse to the federation. Although in conflict situations, the federal constitution normally takes precedence. A list of federal states is included in Annex 2.

Generally foreign policy and national defense are the responsibility of the federal government. In terms of the distribution of other powers and responsibilities, there is no common theme. The United States Constitution provides that all powers not specifically granted to the federal government are retained by the states. Whilst, in Canada, the federal government retains all powers which the constitution does not grant to the provinces. Individual states can have equal status (symmetric federalism) or for historical or other reasons have different powers (asymmetric federalism).

In most cases, a federation is formed at two levels: the central government and the regions (states, provinces, territories). Brazil is an exception, because the 1988

6

Constitution has included the municipalities as autonomous political entities making the federation tripartite, encompassing the Union, the States, and the municipalities. The five thousand plus municipalities have their own legislative council and are autonomous and hierarchically independent from both Federal and State Government.

It is argued that “true” federal states arise because of a voluntary union between component states. However, in Argentina, Brazil, Mexico, Ethiopia, Nigeria, and with the formation of a federation in the Democratic Republic of Congo, the centre has played a part, for various reasons, in the federation’s formation.

A unitary state can have only one central tier of government, and this is often (but not always) the case for small island states. However, there are many examples of unitary states with one or more self-governing regions, some of which e.g. Spain often have greater autonomy than those of some federations. Technically it is argued that the difference between a federation and this kind of unitary state is that the autonomous status of these self-governing regions exists by the sufferance of the central government, and may be unilaterally revoked. In practice, for many countries, this is unlikely to be politically acceptable or attainable. The Republic of South Africa is another example of a unitary state with considerable powers devolved to provincial governments. In other unitary states, regional administrations are purely an extension of central government..

2.4 Francophone and Anglophone countries

At the local level, whether in a federal or unitary state, there are a number of “decentralized institutions”. District or local administration systems whereby the local office is basically “central government at the local level” are often associated with former French colonies. However, other countries including for example, Egypt and Vietnam have also traditionally had a centralized system.

At the same time, democratic decentralization is ongoing in the former French colonies of e.g. Senegal, Burkina Faso and Benin. In many Anglophone countries, the system of semi autonomous local governments has been in place for a longer time. In such cases, local authorities are legal entities, which can sue and be sued. Comparison across countries shows however that there is a multiplicity of differences between countries in how their local government sector operates. In some countries, there is a single level, in other countries e.g. Uganda, there are three levels. The extent of political decentralization also varies, some are appointed, some are elected and some are a combination of elected and appointed officials. Some local authorities have the ability to raise revenues or borrow money and have significant autonomy on how they spend their funds, whilst others have little or no real ability to do either.

7

3 Initial planning guidelines

3.1 Introduction

The strengthened approach to PFM places significant emphasis on governments playing the leadership role in PFM reform and on joint collaboration by development partners with governments and between development partners. The conduct of an assessment at a SN level requires even wider collaboration of interested parties. Individual country circumstances will dictate how these relationships are formed. Whilst grouping of countries into those with similar features e.g. federal, unitary, francophone, small island states may initially seem an appropriate course of action, in practice there are as many differences within as across these groupings. For example, small island states, include Comoros and St Kitts and Nevis (federal states), Barbados (single unitary state, no SN government), and Vanuatu (unitary state with SN government).

Indeed, it is clear from the preceding section that there are large differences in the way public sectors are structured and the way they share functions and resources across levels of government. It is therefore considered essential that the Public Financial Management Performance Report (PFM PR) sets out the legal and regulatory framework in which sub national government operates and the overall intergovernmental relationship in terms of transfers, revenue and expenditure assignments, and borrowing powers.

In addition, it will be essential to obtain a clear understanding of the institutional framework of the SN government including the administrative framework and service delivery mandate. At state level, in many cases, this will follow the legislature, cabinet and MDA structure of central government. At local authority level, there may be a number of different variations particularly in terms of the cabinet. For example, the equivalent of the cabinet may be: (i) the full council, (ii) a system of committees; (iii) a mayor elected by the electorate, with a small cabinet of councilors, (iv) a leader elected by the council, with a cabinet of councilors either selected by the leader or the full council; or (v) an elected mayor with an officer appointed by the council.

3.2 Purpose of the assessment

A PEFA assessment is designed to provide all relevant stakeholders with a high level assessment of the status of PFM in an institution or country. As noted earlier, it can be carried out by a government with or without external support. It can highlight weaknesses in the system and thus allow governments to develop remedial action plans as well as setting the platform for reform dialogue between development partners and governments. As there are clear guidelines and scoring mechanisms, initial scores can be used as a baseline and the framework can then be used to monitor the progress of reform initiatives over time. Quality assurance mechanisms mean that it can also provide information for higher level governments, taxpayers and development partners on the potential level of fiduciary risk.

8

The various reasons for carrying out a PEFA assessment are not however mutually exclusive, an assessment carried out as an input to a fiduciary risk assessment can also provide the basis for dialogue, development of an action plan and scope for capacity building assistance.

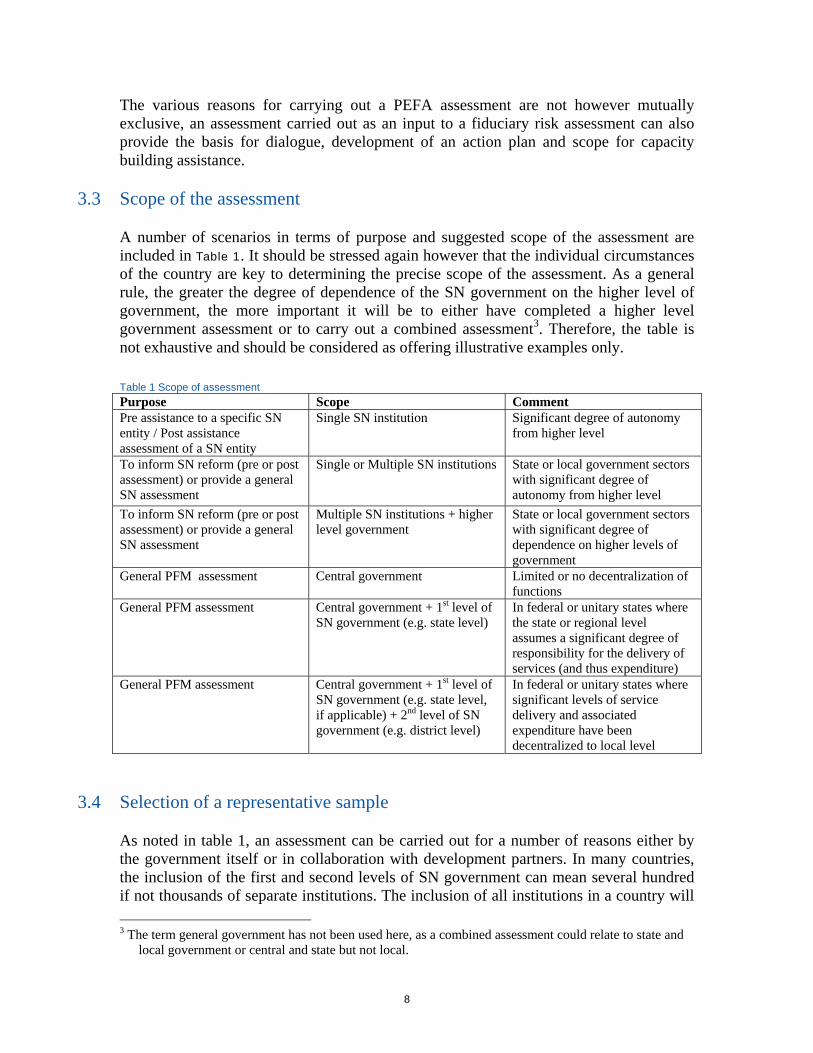

3.3 Scope of the assessment

A number of scenarios in terms of purpose and suggested scope of the assessment are included in Table 1. It should be stressed again however that the individual circumstances of the country are key to determining the precise scope of the assessment. As a general rule, the greater the degree of dependence of the SN government on the higher level of government, the more important it will be to either have completed a higher level government assessment or to carry out a combined assessment3. Therefore, the table is not exhaustive and should be considered as offering illustrative examples only.

Table 1 Scope of assessment Purpose Scope Comment Pre assistance to a specific SN entity / Post assistance assessment of a SN entity

Single SN institution Significant degree of autonomy from higher level

To inform SN reform (pre or post assessment) or provide a general SN assessment

Single or Multiple SN institutions

State or local government sectors with significant degree of autonomy from higher level

To inform SN reform (pre or post assessment) or provide a general SN assessment

Multiple SN institutions + higher level government

State or local government sectors with significant degree of dependence on higher levels of government

General PFM assessment Central government Limited or no decentralization of functions

General PFM assessment Central government + 1st level of SN government (e.g. state level)

In federal or unitary states where the state or regional level assumes a significant degree of responsibility for the delivery of services (and thus expenditure)

General PFM assessment Central government + 1st level of SN government (e.g. state level, if applicable) + 2nd level of SN government (e.g. district level)

In federal or unitary states where significant levels of service delivery and associated expenditure have been decentralized to local level

3.4 Selection of a representative sample

As noted in table 1, an assessment can be carried out for a number of reasons either by the government itself or in collaboration with development partners. In many countries, the inclusion of the first and second levels of SN government can mean several hundred if not thousands of separate institutions. The inclusion of all institutions in a country will 3 The term general government has not been used here, as a combined assessment could relate to state and

local government or central and state but not local.

9

be costly and is unlikely to be an efficient use of resources. In terms of PFM strengths and weaknesses, there will also often be a lot of similarities between institutions.

The best solution would be the selection of a representative sample. This solution may not necessarily be the least cost solution, either in terms of time or money, but would ensure that there is no unintended bias or lack of understanding of any differences in capacity building requirements. In the assessments carried out to date, the sample in Uganda was based on the Local Government Development Programme (LGDP) performance assessment and on geographical spread4. Whilst in Tanzania, the selection was based on two main criteria, receipt/non receipt of development funds and use/non use of the Epicor system. In Tanzania, one local government was also selected as an opposition led authority.

In choosing a more representative sample, a few of the following characteristics5 could be taken into account in the sampling process. The list is not exhaustive but provides a basis for selection and agreement by all parties:

• Population size • Levels of expenditure per capita e.g. high and low, • Economy (industrial: agricultural) or main source of revenue (e.g. oil, mining), • Organizational structure (e.g. municipal, town, district), • Rural: Urban; (if this is not adequately covered by the organizational structure,

levels of expenditure or the economy), • Political representation (government and opposition), • Accessibility to key infrastructure (e.g. roads, banks) • Manual systems or computerized systems, • Age of institution, • Extent of development partner support, and • Social or ethnic grouping.

The number of criteria for choosing the entities in the sample should be limited to a few in order to maintain clarity of what each sample entity represents and therefore how findings may be aggregated. The basis for the selection of the representative sample and the final sample should be agreed with all stakeholders.

As indicated in sub section 3.7, a significant amount of information is often available at the central level, which can be used to supplement findings from field visits and can at the same time be verified during these visits.

3.5 Composition of Assessment Teams

A number of approaches to the assessment of an entire level of SNG have been used in PEFA assessments and similar types of diagnostics. In Uganda, Nigeria and Pakistan 4 The original selection was changed by the Ministry of Local Government 5 These characteristics may not all be relevant in every country.

10

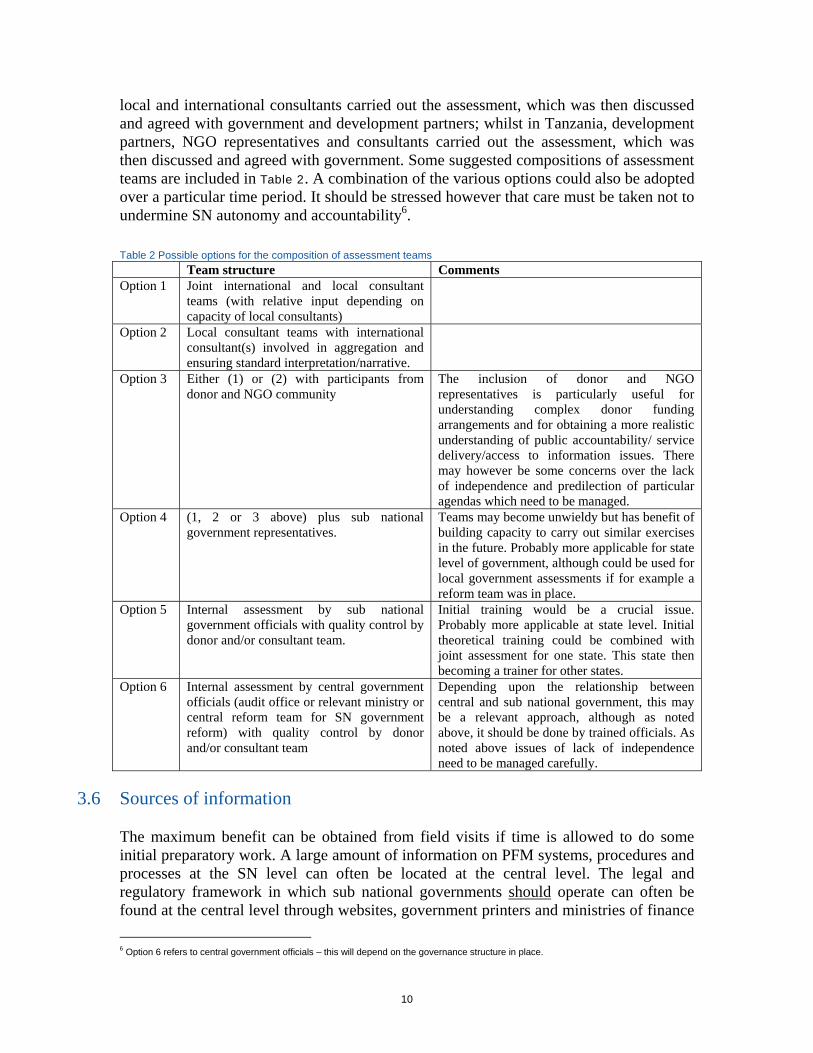

local and international consultants carried out the assessment, which was then discussed and agreed with government and development partners; whilst in Tanzania, development partners, NGO representatives and consultants carried out the assessment, which was then discussed and agreed with government. Some suggested compositions of assessment teams are included in Table 2. A combination of the various options could also be adopted over a particular time period. It should be stressed however that care must be taken not to undermine SN autonomy and accountability6.

Table 2 Possible options for the composition of assessment teams Team structure Comments Option 1 Joint international and local consultant

teams (with relative input depending on capacity of local consultants)

Option 2 Local consultant teams with international consultant(s) involved in aggregation and ensuring standard interpretation/narrative.

Option 3 Either (1) or (2) with participants from donor and NGO community

The inclusion of donor and NGO representatives is particularly useful for understanding complex donor funding arrangements and for obtaining a more realistic understanding of public accountability/ service delivery/access to information issues. There may however be some concerns over the lack of independence and predilection of particular agendas which need to be managed.

Option 4 (1, 2 or 3 above) plus sub national government representatives.

Teams may become unwieldy but has benefit of building capacity to carry out similar exercises in the future. Probably more applicable for state level of government, although could be used for local government assessments if for example a reform team was in place.

Option 5 Internal assessment by sub national government officials with quality control by donor and/or consultant team.

Initial training would be a crucial issue. Probably more applicable at state level. Initial theoretical training could be combined with joint assessment for one state. This state then becoming a trainer for other states.

Option 6 Internal assessment by central government officials (audit office or relevant ministry or central reform team for SN government reform) with quality control by donor and/or consultant team

Depending upon the relationship between central and sub national government, this may be a relevant approach, although as noted above, it should be done by trained officials. As noted above issues of lack of independence need to be managed carefully.

3.6 Sources of information

The maximum benefit can be obtained from field visits if time is allowed to do some initial preparatory work. A large amount of information on PFM systems, procedures and processes at the SN level can often be located at the central level. The legal and regulatory framework in which sub national governments should operate can often be found at the central level through websites, government printers and ministries of finance 6 Option 6 refers to central government officials – this will depend on the governance structure in place.

11

or local government. In aid dependent countries, information is also available in development partner reports. Expenditure and revenue levels may also be collected by local government, interior or finance ministries7. Budgeted transfers from the higher level government should be found in their estimates, whilst actual transfers should be available from the Ministry of Finance and may be available in press releases/ websites. Information on in kind (drugs and food) transfers from the higher level to the SN level should be available at the respective ministry.

Existing state and local government reform programmes provide another good source of information on expenditure and revenue levels. In some instances, there may also be some information on the status of key PFM indicators within the reform programme documentation8. Administrators of transfer funds also retain information on SN activities.

In some countries, information on sub national government activities may also be available on websites and include estimates, financial statements, budget speeches etc. Whilst in other countries, legislation may require quite detailed reporting to the central level and therefore a significant amount of information may be available from the central ministry of finance.

Some information on donor support to SN governments should be available from in country donor groups and/or external resource departments. It will be important to understand all donor support that reaches SN governments, as it may be in the form of:

• general budget support to the state or local authority; • sector budget support provided at the central level but earmarked for state or local

government operations (e.g. additional funds to a local authority transfer fund); • sector budget support provided at the SN level but earmarked for a particular

sector e.g. health; • basket funds for sub national government operations; • basket funds for sector e.g. education which are disbursed to all levels of

government; • donor projects which cover more than one level of government e.g. water supply

and school infrastructure • specific donor project support for the sub national government level; and; • specific donor project support for the sub national government entity.

Information on PFM systems at sub national level may also be available in external audit reports from the National Audit Office, although this will depend on the structure of external audit in the country. Internal audit reports may also be available at the Ministry of Local Government, but this will again depend on the structure of internal audit in the country.

7 Although reporting to the central level may only relate to central government transfers and therefore should be treated with some caution. 8 The objectivity of these assessments may be an issue and therefore should be cross checked where possible.

12

It is recognized that information may be limited/contradictory particularly on intergovernmental transfers and local taxation issues. The above provides some guidance on the potential sources of information before visiting the SN level. Information can then be verified at that level.

13

4 Application of individual performance indicators

4.1 Introduction

Assessments carried out to date show that the whole set of indicators can be applied at the SN level, although depending on individual circumstances some indicators or dimensions may not be relevant. The proposed section on intergovernmental relationships set out in the following section should highlight those areas when an indicator or dimension is not relevant at the SN level.

Given the high degree of “central” dependence of some SN governments, some assessments that have been carried out to date have tried to assess the performance of central government. As explained in more detail in section 5, PFM outcomes at the SN level are often highly dependent on the behavior of the centre, although the PFM outcomes across the various SN institutions may differ. Whilst some aspects of the relationship are catered for in PI 8 and PI 16 in a central assessment, the monetary impact of delayed funding on SN budget performance is not specifically addressed. It is therefore recommended that consideration be given, in certain circumstances, to the addition of an additional indicator on central government (CG) practices.

The following paragraphs set out some guidelines for the application of the individual indicators and explanation/interpretation of the results, some suggestions for the additional central government assessment and some minor changes to the wording of some dimensions and scoring guidelines. For ease of use, the Annex provides an indicator by indicator guide.

As with central government assessments, scoring should be supported by source of evidence (dated where feasible). Lack of information particularly high quality data may be a problem at SN level, indeed it is often a problem for CG assessments. In these instances, as for CG, it is recommended that the lack of essential data be explained and specified and that no score be assigned. A qualitative assessment may be presented.

4.2 Budget credibility

PI-1 Aggregate expenditure out-turn compared to original approved budget.

Application. The Performance Indicators (PI) 1 can be applied with no revision. The original approved budget should be the total budget approved by the SN legislature, not the transfer approved by the national legislature. As prescribed for central assessments,

14

debt servicing (where applicable) and donor funded project expenditure9 should be excluded from the variance calculation.

Explanation. In an environment where sub national governments are highly dependent on fiscal transfers or shared revenues, local outcomes will be significantly affected by the predictability (ref: PI 8 (i) – central assessment) and timeliness of transfers (ref suggested indicator CG1). Furthermore, the ability to meet budgeted expenditures may also depend on the ability of sub national governments to access financing/debt to compensate for shortfalls in transfers and/or domestic revenues. In some cases the outcomes may also be affected by the lack of timely and accurate information on budgeted central transfers for inclusion in the SN budget process10 (ref PI 8 dim ii – central assessment). Delays in general budget support or sector budget support earmarked for sub national government activities (ref D1 -central assessment) may also be the reason for poor results. PI-2. Composition of expenditure out-turn compared to original approved budget

Application. PI 2 can be applied with no revision. Again the original approved budget should be the total budget approved by the SN legislature, including expenditure from own revenues, earmarked and non earmarked transfers from CG and budget support provided directly by donors and not limited to the transfers approved by the national legislature11. As prescribed for central assessments, debt servicing (where applicable) and donor funded project expenditure12 should be excluded from the variance calculation.

Explanation Variations in composition significantly different from those at the aggregate level may arise because of the presence of earmarked grants. For example, if earmarked grants are important for sectoral spending and these do not arrive (e.g., in health), this will impact the composition of expenditure. Lack of clarity on spending responsibilities between SN governments and deconcentrated units may also result in the payment13 of funds to sectors not in their responsibility, or to compensate for the fact that other deconcentrated sectors are not meeting local expenditure needs.

PI-3. Aggregate revenue out-turn compared to original approved budget.

Application The indicator refers to domestic revenue and says that “Accurate forecasting of domestic revenue is a critical factor in determining budget performance, since budgeted expenditure allocations are based upon that forecast”, In applying the indicator, the main question to be resolved is the precise definition of domestic revenue at the sub national government level. Transfers from donors and higher levels of government should

9 This covers all donor funded expenditure included in the budget which is not fully aligned with government procedures. General and

sector budget support should not be excluded. 10 This may occur if the FYs of donors are different from those of SNGs and/or if transfers to SN governments are changed after they have

been approved at the SN level but before they are appropriated at the national level 11 In some countries, the transfer approved by the national legislature is not the same as the amount included in the SN budget as the CG

transfer because SN budgets have to be approved prior to the approval of the national budget. 12 This covers all donor funded expenditure included in the budget which is not fully aligned with government procedures. General and

sector budget support should not be excluded. 13 If the spending is accounted for in the budget, this will not affect the budget composition, however, experience shows that it is often

outside the budget process.

15

clearly not be included. Own taxes and charges are related to the activities of that jurisdiction, but the situation with respect to shared revenues is more complicated. It is suggested that the portion of an SNG’s share of revenues that is collected by the sub national government be included in domestic revenue, but that the portion collected by the central government (and therefore due to SNGs) should be treated in the same way as central transfers.

In all cases, it will be important for the assessors to state clearly what has been included in own source revenue (i.e. where SNG has significant control over the rates/effort/collection receipts of a revenue) and in shared revenues (i.e. where revenue is remitted on a derivation basis, and largely beyond control of SNG.

Explanation. For many highly dependent sub national governments, domestic revenue as defined above represents a very small proportion of their total revenue base. PI 7 covers unreported local taxes and charges. Whilst central assessments of PI 8 and PI 16 comment on the existence of transparent and rule based systems, the timeliness of reliable information, and the predictability in the availability of funds for commitment of expenditure respectively, no quantitative assessment of actual variations in original transfers to actual transfers is done. It is therefore suggested that a separate indicator (CG1) is prepared in all SN government assessments where more than 10% of funding is through central transfers or shared revenues.

PI-4. Stock and monitoring of expenditure payment arrears.

Application PI 4 which assesses the stock and monitoring of expenditure payment arrears is applicable to all levels of sub national government. The definition of an arrear may be in national or local legislation, either way the narrative should clearly state the definition of the arrear used. As for the central assessment, the default would be internationally accepted business practices according to which a claim will be considered in arrears if payment has not been made within 30 days from government’s receipt of supplier’s invoice/claim (for supplies, services or works delivered), whereas the failure to make staff payroll payment or meet a deadline for payment of interest on debt immediately results in the payment being in arrears. Monitoring and elimination of stocks of arrears may be centrally directed14.

Explanation Delays in higher level transfers can result in “no fault” accumulation of arrears, if the transfers are for example directly related to salary or salary related payments. Other expenditure arrears are similar to those arising in central ministries, when purchases are made without supporting funds or as a result of court claims.

4.3 Budget comprehensiveness and transparency

PI-5. Classification of the budget.

14 In Tanzania, for example non payment of employer contributions by the SN government has been dealt

with by reducing transfers and making central payments.

16

Application PI 5 can be applied at the SN level. It is suggested however that the minimum requirements be changed slightly. The minimum requirement for a “B” is that “budget formulation and execution is based on administrative, economic and functional classification (using at least the 10 main COFOG functions), using GFS/COFOG standards or a standard that can produce consistent documentation according to those standards”. It is suggested that the phrase “using at least the 10 main COFOG functions” be modified to “(either using the main COFOG functions, to the extent that those functions are performed by the SN entity assessed or a classification that “reflects” or is “compatible” with the relevant main COFOG functions).”

Explanation Sub national governments may be required by central government to follow a different classification system. Whilst the indicator assesses against international best practice, any rules and regulations outside of the sub national government’s control should be included in the narrative.

PI-6. Comprehensiveness of information included in budget documentation.

Application This indicator refers to the annual budget and supporting documentation. When assessing PI 6 on budget documentation for sub national governments, the budget documentation referred to is that presented to the SN legislature not central government. Certain of the nine designated elements may not be relevant e.g. some macro economic assumptions e.g. exchange rates and fiscal deficit at the local government level, but could be replaced by for example inflation assumptions. It is therefore suggested that scoring of the indicator is done on a pro rata basis against the total number of relevant elements.

PI-7. Extent of unreported government operations.

Application PI 7 on unreported expenditure is applicable, but the donor element should only relate to donor funds provided directly to that level of government/entity, not that transferred from/shared with a higher level of government. As at central government level, expenditure from unreported revenue may be an issue to consider. In carrying out a combined or general government assessment, care may be needed to avoid double counting, for example road funds disburse funds to the national, regional and local level.

It is suggested that in applying dimension (i) only extra budgetary operations covered by the legally mandated expenditure assignments of SNGs. are included in the calculation. For dimension (ii), the minimum requirement for a score of “B” and “C” respectively is “ complete income/expenditure information is included in fiscal reports for all loan financed projects and at least 50% (by value) of grant financed projects” and “complete income/expenditure information for all loan financed projects is included in fiscal reports”. In many instances, loan financed support is not available directly to the SN level. It is therefore suggested that reference to loan financed projects is removed in both instances and to achieve a “B” at least 50 percent of donor-financed projects be used

17

instead, whereas to achieve a “C” at least 25% (by value) of donor15 financed projects be used instead.

Explanation As in central government assessments, there may be large amounts of revenue (e.g. school fees and hospital charges) not being reflected in the budgets and used by government entities for expenditure outside the normal control mechanisms.

PI-8. Transparency of Inter-Governmental Fiscal Relations

Application Inter governmental relations can be applied in a SN assessment but should refer to lower levels of government (where relevant) in that particular jurisdiction. For example a SN assessment at state level may look at the transfers to local governments. An assessment at local government level may look at the transfers from district to village. For dimensions (i) and (ii) in order to avoid any confusion, it is suggested that minor changes are made to the wording for example (i) Transparent and rules based systems in the horizontal allocation among lower level SN governments of unconditional and conditional transfers from the assessed level of SN government (both budgeted and actual allocations) and (ii) Timeliness of reliable information to lower level SN governments on their allocations from the SN government being assessed for the coming year. Dimension (iii), refers to general government reporting, from this perspective it is not considered to be relevant at the SN level. However an assessment of the extent to which SN governments collect information on a sectoral basis would provide useful information for any central government assessment. The dimension is therefore amended as follows “Extent to which financial information (at least on revenue and expenditure) is collected from the lower level of government and reported by the assessed SN government according to sectoral categories”.

References to central government in the minimum requirements should be modified in a similar manner to other indicators.

PI-9. Oversight of aggregate fiscal risk from other public sector entities.

Application. The application of the first dimension of this particular indicator will depend on whether the SN has responsibility for any Autonomous Government Agency (AGA) or Public Enterprise (PE). The main guidelines state that “Fiscal risks can be created by sub national government, AGAs and PEs and inter alia take the form of debt service defaulting (with or without guarantees issued by central government), operational losses caused by unfunded quasi-fiscal operations, expenditure payment arrears and unfunded pension obligations.” In most instances, reporting mechanisms for state owned or local government owned AGAs/PEs are to that level of government not to the centre16. The indicator should therefore be applied within the SN assessment. Dimension (ii) should be applied to lower levels of government within the jurisdiction of the SN entity being assessed.

15 This would then include donor financed projects irrespective of their funding mechanism. 16 There are some instances where the PE is jointly owned by central and state government, in these cases, it is recommended that the

level with the higher share ownership be the one to which the indicator is applied.

18

Interpretation Administrative controls may be in place to prevent sub national governments from accessing loan financing. This does not mean that the same restrictions will necessarily apply to borrowing by, for example state or local government owned public enterprises.

PI-10. Public Access to key fiscal information

Application This indicator applies equally to an assessment at SN level and should relate to the availability of information available to the public at the local level not information sent to central government. All six of the central assessment information requirements are applicable, although the US$100,000 for contract awards would either need to be reduced for small authorities or preferably expressed in terms of the percentage of contracts awarded e.g. the largest 60% of contracts awarded. In addition, it would be useful for information on major fees and charges to be displayed, given the importance of these at the SN level. . As in PI 23, reference to resources available to primary service delivery units should relate to those institutions which are the prime responsibility of the SN government. When carrying out a joint assessment, confusion and potential duplication should be avoided by ensuring that reference is made to service delivery units relevant to that level of government.

Given the importance of fees and charges at the SN level, it is also suggested that information on fees and charges for major services is included in the set of information requirements.

4.4 Policy Based Budgeting

PI-11. Orderliness and participation in the annual budget process

Application All three dimensions of this indicator can be applied at SN level. References to MDAs, cabinet and legislature should be interpreted in the context of the particular level of sub national government.

Explanation The requirements/actions of central government may impact adversely on sub national government performance in this indicator in a number of ways. Firstly the budget calendar may be prescribed/issued by central government, through either the Ministry of Finance or Ministry of Local Government (or its equivalent). Secondly the involvement of the Cabinet (or equivalent) in the approval of the budget ceilings may be delayed because of delays in information received on central transfers. Thirdly, national regulations may require that budgets are approved on a sequential basis central: regional and local with the associated delay in legislative approval

PI-12. Multi-year perspective in fiscal planning, expenditure policy and budgeting

Application The benefits of a multi year perspective in fiscal planning, expenditure policy and budgeting apply equally to sub national governments. The first dimension can be applied to all levels of sub national government. Depending upon the borrowing controls

19

imposed by central government, dimension (ii) on the debt sustainability analysis may not be relevant. In dimensions (iii) + (iv), it is suggested that in some countries at the local government level, local development plans17 might be substituted for sector strategies. Minimum requirements would need some minor modification to support such a change.

Interpretation Those sub national governments which are highly dependent on central transfers and/or donor support may have low scores for a number of reasons. Firstly, the ability of the SN government to prepare sound medium term forecasts will depend on good forecasts on central transfers. It will also depend in many countries on good information on CG policy. Costed sector strategies and/or local development plans also require clear delineation of responsibilities (both operational and policy development). In some countries, there is also a split between investment and recurrent responsibilities, for example school infrastructure is the responsibility of local government, but school operations are under the central Ministry of Education (and vice versa).

As at the central level, some investment projects may be donor driven without recourse to the recurrent cost implications or driven by one central ministry without due regard for the implications at local level on a different department e.g. a new health centre on road maintenance and water supply and sanitation.

4.5 Predictability and Control in Budget Execution

PI-13 Transparency of Taxpayer Obligations and Liabilities PI-14 Effectiveness of measures for taxpayer registration and tax assessment PI-15 Effectiveness in collection of tax payments

Application Clearly PI 13 – 15 will apply only to sub national governments that raise revenue through tax18 as opposed to user fees and charges. However some care does need to be taken as some charges e.g. development levy, market fee, land rent etc are not called taxes but in effect are taxes because they are compulsory and not related to a specific service or because they far exceed the cost of providing the service they are related to (ref: GFS definition of tax and non tax revenue). Application of these indicators would also not be relevant in the case of revenue sharing arrangements under which the central revenue authority collects taxes on behalf of SNs. The extent to which PI 13 – 15 can be assessed for national taxes19 which are only collected at the SN level will also need to be determined on an individual basis.

17 Local development plans referred to are not physical development plans, and sectors within those plans would need to be identifiable.

18 As for a CG assessment, assessors need to take stock of the taxes collected and to determine the major ones before they continue further data collection for the indicator assessments

19 Depending upon the allocation of powers and responsibilities set out in the legislation.

20

Interpretation. SN performance for these indicators may be influenced by national regulations and/or actions. The transparency of user fees and charges, as for the central assessment, is reviewed only by default in terms of unreported revenue (PI 7) from e.g. schools and health centres.

PI-16 Predictability in the availability of funds for commitment of expenditures

Application The need for spending ministries, departments and agencies (MDAs) to receive reliable information on availability of funds within which they can commit expenditure for recurrent and capital inputs is as relevant at the SN level. In order to avoid confusion, references to the Ministry of Finance should be changed to Ministry of Finance (or equivalent). Some care may be required in distinguishing between a finance department or treasury at SN level and a district or regional treasury which is part of the central government structure.

Interpretation. For sub national governments that are reliant on transfers, in describing PI 16, cross reference could be made to timeliness of information on allocations provided in any central government assessment (PI 8 (ii)) as this will clearly impact on the scores achieved for the first two dimensions (i) extent to which cash flows are forecast and monitored and (ii) reliability and horizon of periodic in-year information to MDAs on ceilings for expenditure commitment.

PI-17. Recording and management of cash balances, debt and guarantees

Application The relevance of the first dimension on debt management records and the third dimension on the contracting of loans and issuing of guarantees will depend upon the borrowing controls that are in place. Although some care may be needed as the regulations may not permit borrowing but the sub national government may actually have bank overdrafts and/or guarantee loans for their public enterprises. In terms of cash management, idle cash balances at the SN level are just as detrimental to overall budget performance as at central government. However, the need for a centralized system and/or physically only one bank account may not be applicable given the sophistication of many banking systems which facilitate consolidation of a multiplicity of bank accounts on a regular and timely basis. Furthermore the minimum requirement for an “A” score refers to “all” government accounts, some care will need to be taken as to the desirability of “consolidating” accounts to e.g. school or health centre level.

Explanation Bank accounts at the SN level may have been opened at the request of development partners to “safeguard” joint donor/government funds20. Banking systems at the local level particularly in remote rural areas may not allow for consolidation of numerous accounts. Any implications of having a single account for the whole of government on service delivery effectiveness at the SN level should be described.

20 This also occurs at central government level.

21

PI-18 Effectiveness of payroll controls

Application The application of this indicator will depend upon the administrative responsibility for the payroll. In those cases where the sub national government is fully responsible for its payroll, the indicator can be applied with no modifications. In some countries, central government may be responsible for the overall administration of the payroll. In these cases, only those parts of the payroll administration procedures carried out by the SN entity should be the subject of the scored assessment and the portion not covered in the assessment clearly identified in the report. For completeness, a description of the whole process and the relevant responsibilities would be useful.

PI-19 Competition, value for money and controls in procurement

Application As noted in the central government guidelines, this indicator does not look at the internal controls which are in place with respect to procurement for example; membership of tender committees, segregation of duties etc as these are covered in PI 20 on internal controls. The indicator focuses rather on the quality and transparency of the procurement regulatory framework. It is not scored as to whether regulations exist but rather whether there is adequate data/evidence to show that those regulations are complied with.

The application of the three dimensions of the indicator will therefore depend on the scope of the procurement legislation and the type of procurement oversight/reporting mechanism that is in place. In some circumstances, the results of any central government assessment may address these issues. The report text should clearly state what has been assessed. For completeness, a description of the relevant processes and responsibilities should be included.

PI-20 Effectiveness of internal controls for non-salary expenditure

Application. This indicator can be applied at all levels of sub national government.

Explanation As set out in the main guidelines to the indicator set “An effective internal control system is one that (a) is relevant (i.e. based on an assessment of risks and the controls required to manage the risks), (b) incorporates a comprehensive and cost effective set of controls (which address compliance with rules in procurement and other expenditure processes, prevention and detection of mistakes and fraud, safeguard of information and assets, and quality and timeliness of accounting and reporting), (c) is widely understood and complied with, and (d) is circumvented only for genuine emergency reasons. In relation to dimension (ii) national regulations may not have been adapted to local circumstances thus reducing their relevance and/or there may be confusion/ contradictions between local and national regulations and their jurisdiction.

22

PI-21. Effectiveness of internal audit

Application This indicator can be applied at all levels of sub national government. References to central government should refer to sub national government. In some countries, internal auditors from the national treasury or central government ministries carry out compliance audits at the local level. This can confuse the situation with respect to internal or external oversight function, unless the scope of the central government internal auditors is carefully laid out. However, for PI 26 only external audit functions compatible with INTOSAI standards should be included.

In determining the time spent on systemic issues (dimension (i)) it is suggested that all “internal” audit activities are included, but an explanation of the various players and their various responsibilities are clearly described in the report.

Explanation/ Interpretation In some instances, the structure and functions of internal audit units may be centrally determined, deficiencies are therefore due to external factors outside the control of the sub national government.

4.6 Accounting and Reporting

PI-22. Timeliness and regularity of accounts reconciliation

Application: This indicator can be applied at all levels of sub national government.

PI-23 Availability of information on resources received by service delivery units.

Application This indicator can be applied at all levels of sub national government. However there could be potential overlap if carrying out a combined or general government assessment. In these cases, reference to service delivery units should be modified as follows: Collection and processing of information to demonstrate the resources that were actually received (in cash and kind) by the most common front-line service delivery units within that level of government’s responsibility, and jurisdiction. This would help highlight problems with fund flows within a level of government. At the local government level, it is suggested that the requirement for a special public expenditure tracking survey be changed to special or ad hoc report.

PI-24. Quality and timeliness of in-year budget reports.

Application This indicator can be applied to all types and levels of sub national government. In year reports should however relate to internal reports for management purposes and internal reports for the Council or other SN legislative body. Reporting to national government would be covered by PI 8 (iii) in a central government assessment. References to central government and ministry of finance should be modified as appropriate.

23

Explanation/ Interpretation In the absence of a central assessment, reporting to central government (where applicable) could also be explained, but not scored. In some instances, it may also be of relevance to note the level of reporting to all central government MDAs, as the sub national government may be required to provide similar reports to multiple entities within central government, which is neither efficient nor effective.

PI-25. Quality and timeliness of annual financial statements

Application This indicator can be applied to all types of sub national government. For small rural or semi urban local authorities some relaxation on the strict use of IPSAS may be warranted and it is suggested that appropriate national standards should be used. The definition of consolidated may also require some clarification, but should as a minimum include all ministries, departments and deconcentrated units for state level. At local government level, it should as a minimum include all departments and lower tiers (where applicable).

4.7 External Audit and Scrutiny

PI-26. Scope, nature and follow-up of external audit

Application: A high quality external audit is an essential requirement for creating transparency in the use of public funds both at the central and the SN level. Currently the minimum requirements refer only to central government entities. In applying the indicator at the SN level, the first issue to address is which audit entity has responsibility for carrying out audits at the SN level. In some countries, there may be an overlap in responsibilities/functions between the national audit office and the state audit office. This results in duplication of effort and potential gaps in review. It is suggested that the minimum requirements are modified slightly to reflect the need for clear and unambiguous responsibilities.

If a single “entity” e.g. a state government or large city council is being assessed, it is suggested that the minimum requirements for dimension (i) refer to departments in that entity. If multiple entities are being assessed for example a number of local authorities, as a sample of the local government sector, it is suggested that the minimum requirements relate to all local authorities.. Reference to the legislature in dimension (ii) should refer to that of the SN government not central government.

Explanation/ Interpretation: It will be important to document the impact of multiple audits on the integrity of the audit process.

24

PI-27 Legislative scrutiny of the annual budget law

Application The performance of the sub national government’s legislature should be assessed using this indicator. In local government in some countries, the review of fiscal policies may not be relevant in the minimum requirements for dimension (i)21.

Explanation/Interpretation The ability of the legislature to carry out its responsibilities may be impaired by central government delays in providing necessary inputs to the process. The length of delays should be explained in the narrative and/or reference made to PI 8 (ii) of a central assessment and the proposed indicator CG1.

PI-28 Legislative scrutiny of external audit reports.

Application As for PI 27, this indicator should be assessed against the activities of the SN legislature. In some countries, this task is taken over by the national legislature. Local accountability, a prime purpose of decentralisation, is then undermined. Such action should not be favourably considered. However, it is recognised that central government often provide a significant proportion of the funding to the SN level. In these cases, it is reasonable to expect that some monitoring of SN activities is requested by the national legislature. However, this should be done in a fair and transparent way and not undermine local responsibility and authority.

Explanation/Interpretation The indicator should be assessed for the SN legislature. The narrative should explain the involvement of both the SN and national legislature. In relation to the latter, the report should show how the local authorities are reviewed e.g. 100% or on a sample basis (and the basis for that sample). Any follow up actions should also be noted.

4.8 Donor Practices

D-1 Predictability of Direct Budget Support D-2 Financial information provided by donors for budgeting and reporting on

project and program aid D-3 Proportion of aid that is managed by use of national procedures.

Application These indicators are meant to capture elements of donor practices which impact the performance of the PFM system. Evidence from specific case studies, as well as other assessments, shows that all three indicators are applicable at the sub national level. However, there is potential for overlap with a central government assessment and consequently consideration should be given to carrying out a combined assessment of donor practices. If this is not feasible, it is recommended that only donor support

21 Fiscal policies may be centrally determined.

25

provided directly to the SN entity and/or SN level should be counted in an SN assessment. By making this distinction, however, it will be important to ensure that any central assessment covers the remaining donor support and a description of the findings of that assessment as far as they affect the SN level are clearly set out. This will require a clear understanding of the way that donor support is being provided and the level of alignment with local or national procedures.

4.9 Central Government Practices22

From the preceding subsections it is clear that the activities of central government impact, in the same way as donor practices, on the performance of the sub national government. This is particularly true for those sub national governments which are highly dependent on transfers from higher level. If the framework has been applied at the higher level of government indicator PI 8 (i) and (ii) refer to transparent systems and timely information, however, they do not capture the “monetary impact” of these practices. It is therefore suggested that one additional indicator is introduced. This could be used for all SN assessments, but it is suggested that it should be used for those sub- national governments that receive more than 10% of their funding from central transfers or shared revenue23 arrangements. It is suggested that this assessment is based on the indicator for direct budget support. In assessing the situation, the aggregate position should be reviewed, the situation with respect to earmarked grants, and the in-year timeliness. An draft of the proposed indicator is included as the last indicator (HLG-1) in the Annex to the guideline.

22 It should be noted that the indicator could apply to transfers from both central and state governments. 23 This definition of shared revenue should exclude that included in PI 3

26

5 Modifications to the Performance Report

5.1 Executive summary and introduction

For those countries where sub national government is highly dependent on central government, it is essential that a statement on central government practices and on the extent to which they affect PFM performance is included. This would be of relevance both in combined or separate SN assessments. The summary should also clearly show those areas where improvements can be made by the sub-national government itself and those where the SN government is unable to make changes because the area is regulated by the central government e.g. setting of national accounting standards and classification systems.. The scope of the assessment should clearly set out which institutions are covered and which are excluded. In the case of an assessment of a number of SN institutions, details of the sample and the rationale for choosing the sample should be explained. In describing the processes involved, an explanation of the method of aggregating scores should also be given if several institutions have been assessed.

5.2 Country background

5.2.1 SN government

In a combined report, in addition to the current sub sections on the description of the country economic background, the budgetary outcomes and the legal and institutional framework for PFM, it is suggested that an additional section is included on how sub national government operates in the country. In particular, the section should set out the following:

• The general legal and regulatory framework including specific responsibilities and any special cases (where applicable);

• The levels of SN government and the numbers of institutions at each level; • The economic and fiscal importance of the SN government sector. This

information should be available from existing reports; and • The institutional framework at the SN level as it pertains to PFM.

For assessments of multiple sub national government entities but without a central assessment, it is suggested that the current sub sections on country economic background and the legal and institutional framework for PFM are still relevant, particularly with respect to issues which would relate to service delivery at the sub national level. The sub section on budgetary outcomes could be tailored to the sub national sector and/or individual sectors within the sub national sector depending upon the availability of information.

27

For assessments that are only looking at a single entity, the country economic background will need to be tailored to that particular jurisdiction. It is also suggested that in the legal and institutional framework for PFM, specific mention should be made as to the applicability of the various national pieces of legislation (e.g. financial management, procurement etc) to the SN level or any contradictions between separate legislation. Other relevant information would include, fiscal years at SN and central government level, use of financial management systems and any administrative functions e.g. payroll carried out by central government on behalf of sub national governments.

5.3 Inter governmental relationship

The key issue that has arisen in the majority of the sub national assessments done to date is the relationship of the sub national government (state or local) with the higher level of government. It is therefore suggested that this aspect is set out in some detail in the PFM PR. Practices of the central (or higher level) government which need to be addressed in the intergovernmental relationship sub-section include: financing, revenue assignment (including which agency – central or sub-national – collects and distributes shared revenues) spending assignment, reporting and oversight and macro economic management. Even when a SN assessment is done together with a central government assessment, it is considered important that information on the following is provided:

• Type and size of fiscal transfers24 (block, earmarked), formulae and criteria used for distribution plus any in kind transfers such as drugs, food and medical supplies and revenue sharing arrangements

• Any spending directives, e.g. differences between responsibilities and spending patterns e.g. responsibilities assigned to sub national government but spending carried out by deconcentrated CG departments, or retention of transfers for higher level managed programmes;

• Reporting requirements of the SN level to the central level, oversight mechanisms in place e.g. mandate of national auditor general, monitoring/inspection/ audits by line ministries of SN activities; and

• Status of borrowing controls as to whether they are based on market discipline; rules-based controls; administrative controls; or cooperation between different levels of government.

This would supplement the results of any central assessment in relation to the clarity of inter-governmental fiscal relations (PI-8) and the comprehensiveness of fiscal risk oversight (PI-9).

24 These transfers may be direct from the ministry of finance or from other central ministries

28

5.4 Assessment of the PFM systems, processes and institutions

5.4.1 General

In stand alone or multiple SN assessments, the format of the presentation of the findings for each of the indicators can follow the format set out for the central government assessment. It is suggested that in combined or general government reports, that the narrative for the central or higher level government is presented first. In some cases, this would provide an insight into the performance of sub national government. Scores could then be presented in tabular format. In presenting assessments of multiple entities, it is suggested that an individual report, rather than an annex is prepared for each entity (as done in Nigeria, and Uganda) and a consolidated report prepared for the particular SN level. Individual reports can then be shared more easily with “local” stakeholders.

5.4.2 Aggregation of results

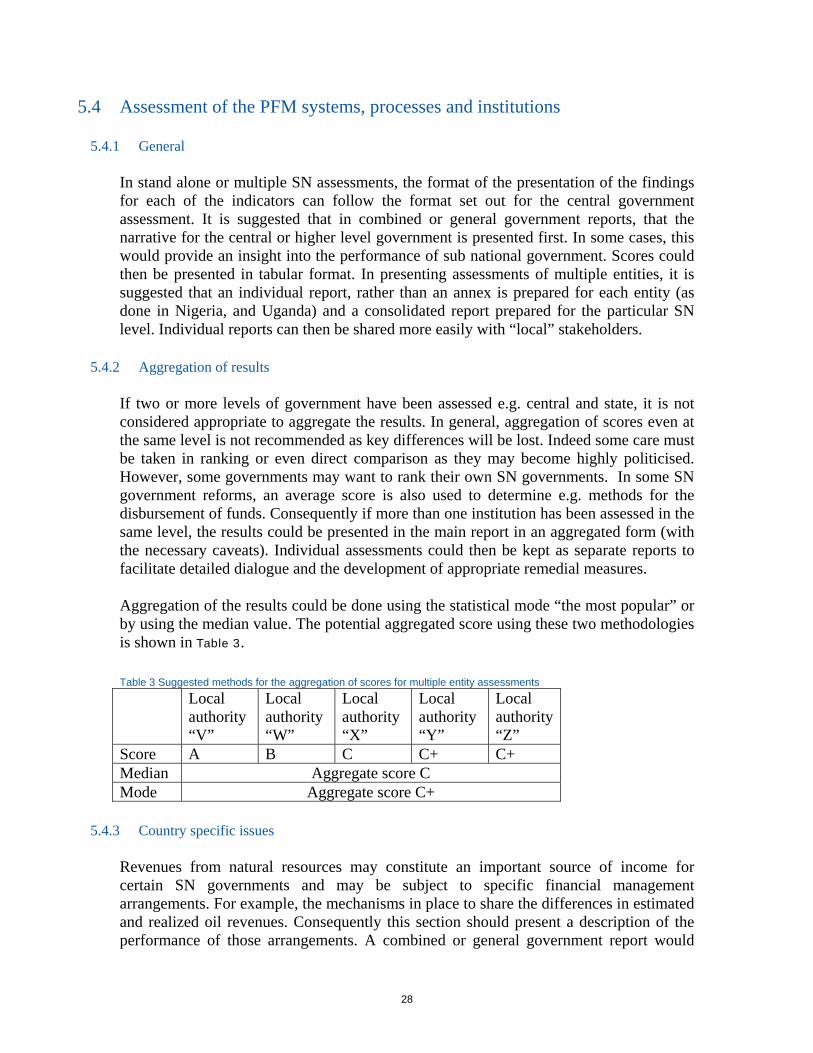

If two or more levels of government have been assessed e.g. central and state, it is not considered appropriate to aggregate the results. In general, aggregation of scores even at the same level is not recommended as key differences will be lost. Indeed some care must be taken in ranking or even direct comparison as they may become highly politicised. However, some governments may want to rank their own SN governments. In some SN government reforms, an average score is also used to determine e.g. methods for the disbursement of funds. Consequently if more than one institution has been assessed in the same level, the results could be presented in the main report in an aggregated form (with the necessary caveats). Individual assessments could then be kept as separate reports to facilitate detailed dialogue and the development of appropriate remedial measures.

Aggregation of the results could be done using the statistical mode “the most popular” or by using the median value. The potential aggregated score using these two methodologies is shown in Table 3.

Table 3 Suggested methods for the aggregation of scores for multiple entity assessments Local

authority “V”

Local authority “W”

Local authority “X”

Local authority “Y”

Local authority “Z”

Score A B C C+ C+ Median Aggregate score C Mode Aggregate score C+

5.4.3 Country specific issues

Revenues from natural resources may constitute an important source of income for certain SN governments and may be subject to specific financial management arrangements. For example, the mechanisms in place to share the differences in estimated and realized oil revenues. Consequently this section should present a description of the performance of those arrangements. A combined or general government report would

29

obviously provide a more comprehensive picture, but as noted earlier may not be practical in many countries.

5.5 Government reform process

It is suggested that this section is modified slightly to include any information on specific state or local government reform in addition to any national reform process with implications at the SN level.