Embed Size (px)

Citation preview

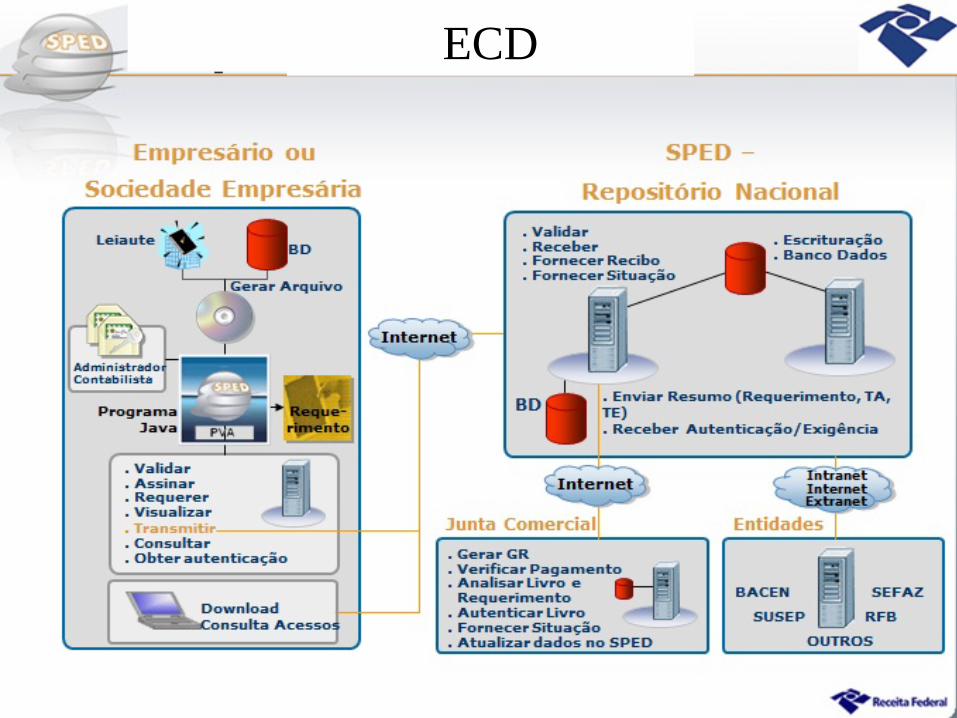

Public Digital Bookkeeping System

Newark, NJ, nov 7th, 2015

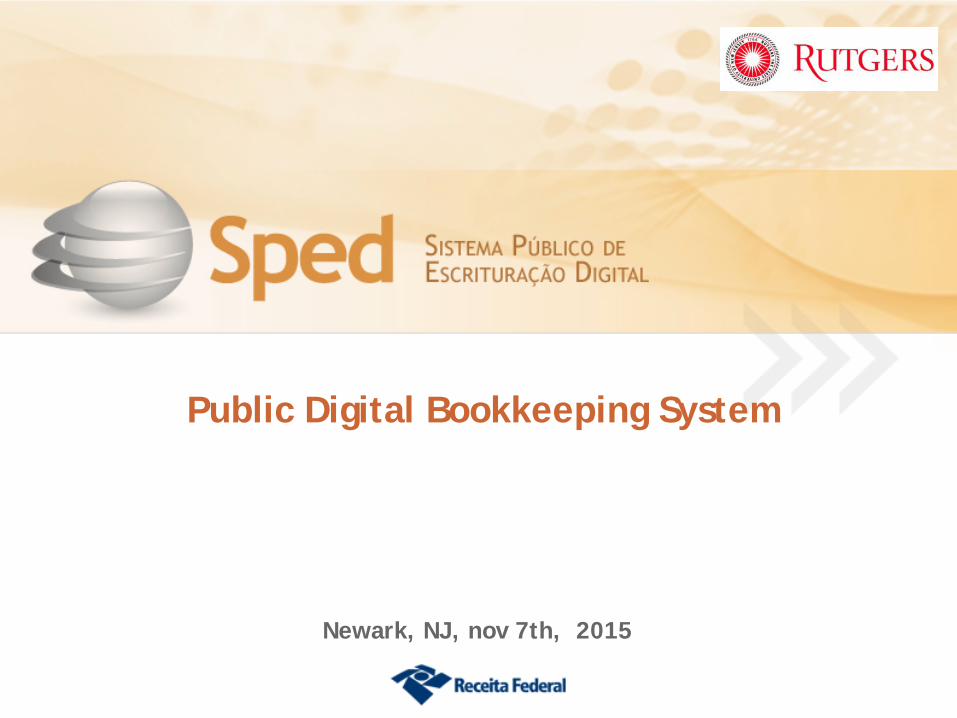

Pre-Sped: Context

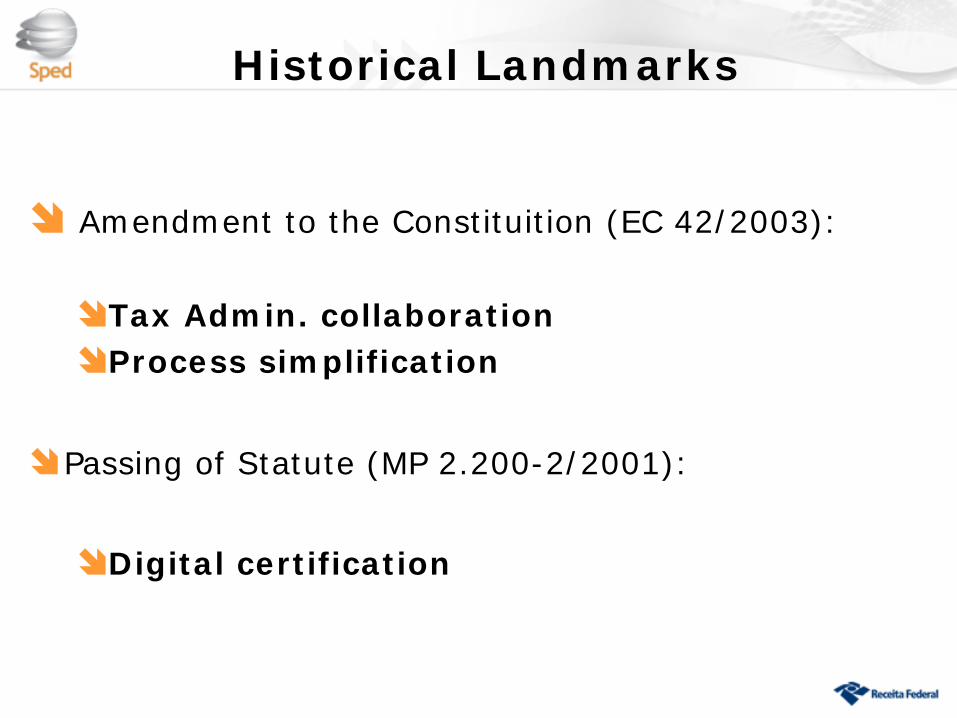

Historical Landmarks

Amendment to the Constituition (EC 42/2003):

Tax Admin. collaborationProcess simplification

Passing of Statute (MP 2.200-2/2001):

Digital certification

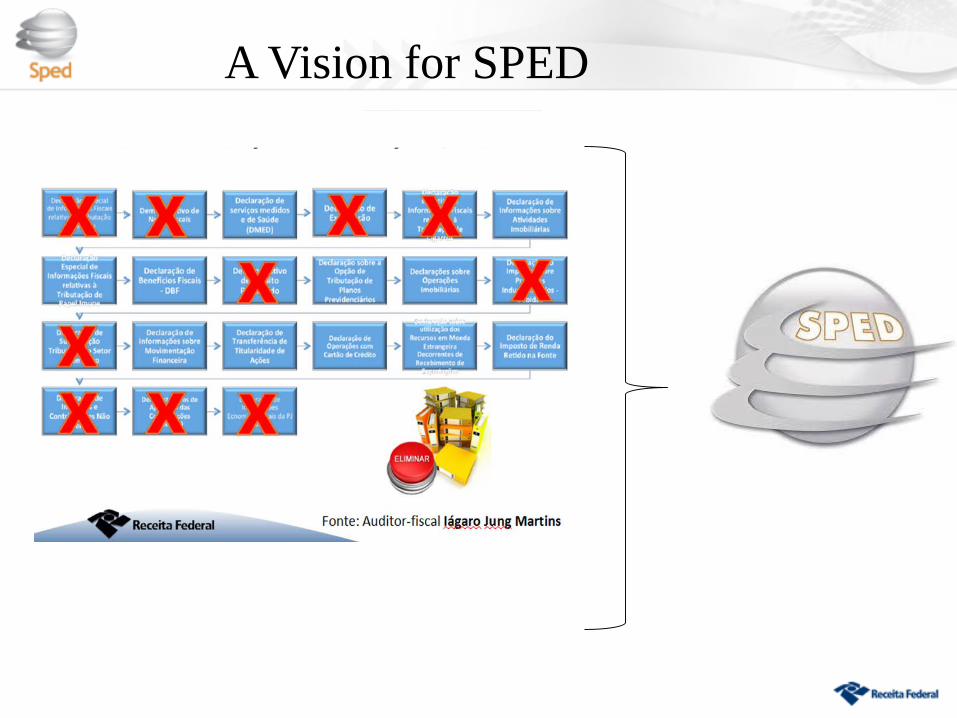

A Vision for SPED

Standardization and Simplification

Integration

Data Sharing (*)

Premises

Collective Construction

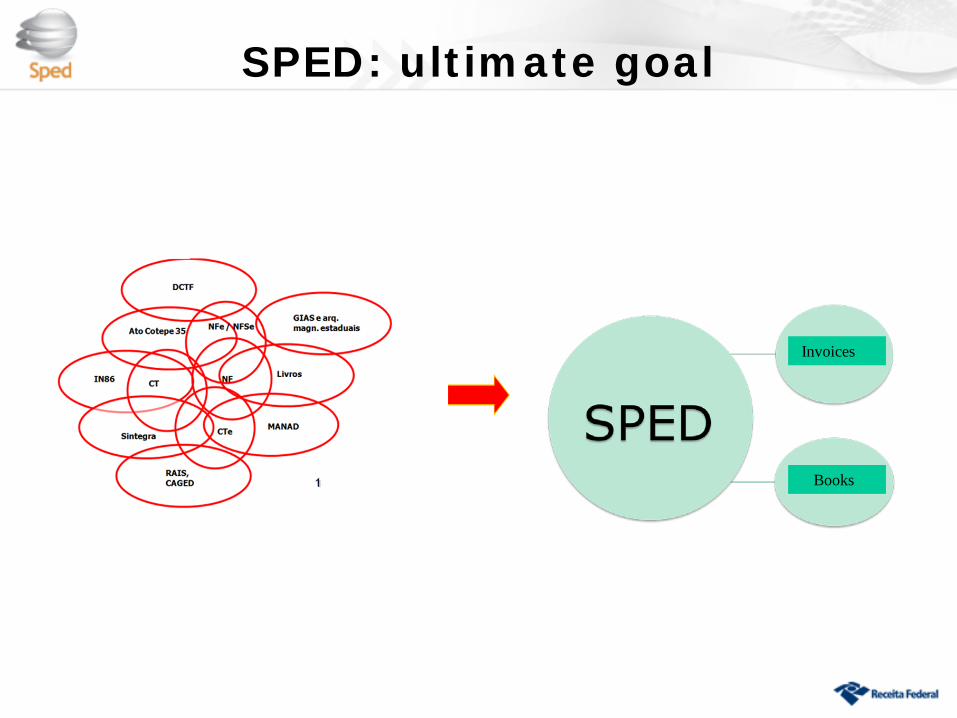

SPED: ultimate goal

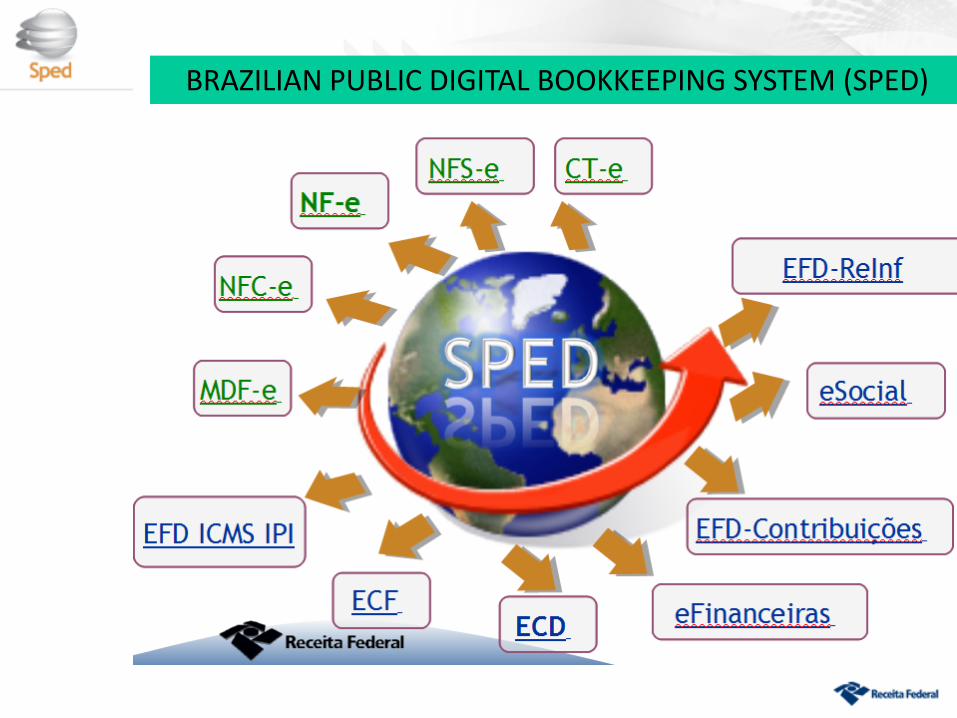

Invoices

Books

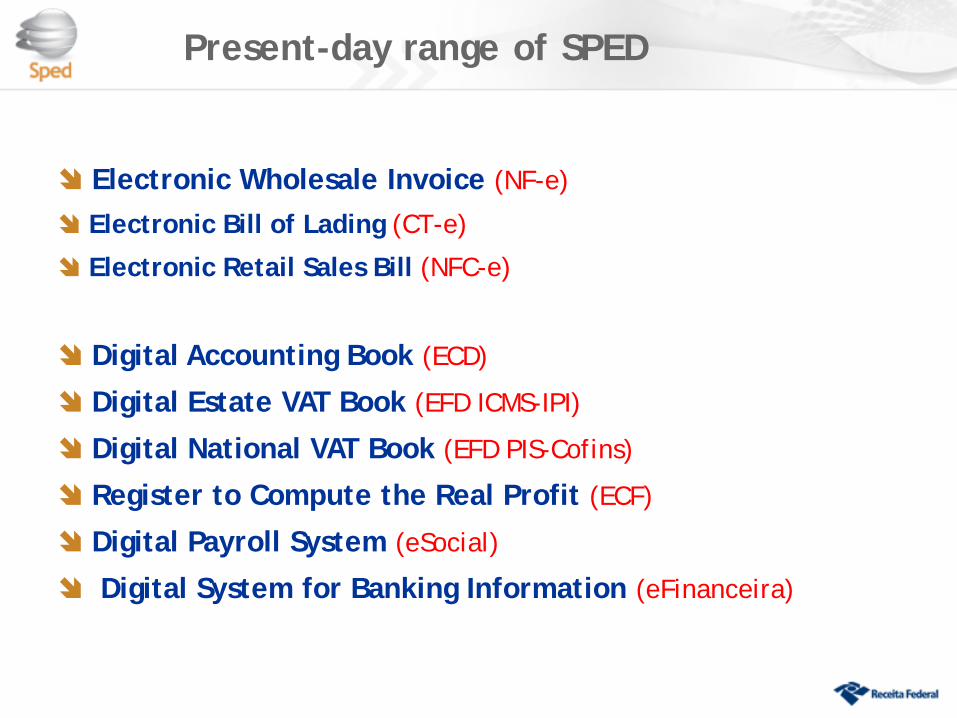

Electronic Wholesale Invoice (NF-e)

Electronic Bill of Lading (CT-e)

Electronic Retail Sales Bill (NFC-e)

Digital Accounting Book (ECD)

Digital Estate VAT Book (EFD ICMS-IPI)

Digital National VAT Book (EFD PIS-Cofins)

Register to Compute the Real Profit (ECF)

Digital Payroll System (eSocial)

Digital System for Banking Information (eFinanceira)

Present-day range of SPED

BRAZILIAN PUBLIC DIGITAL BOOKKEEPING SYSTEM (SPED)

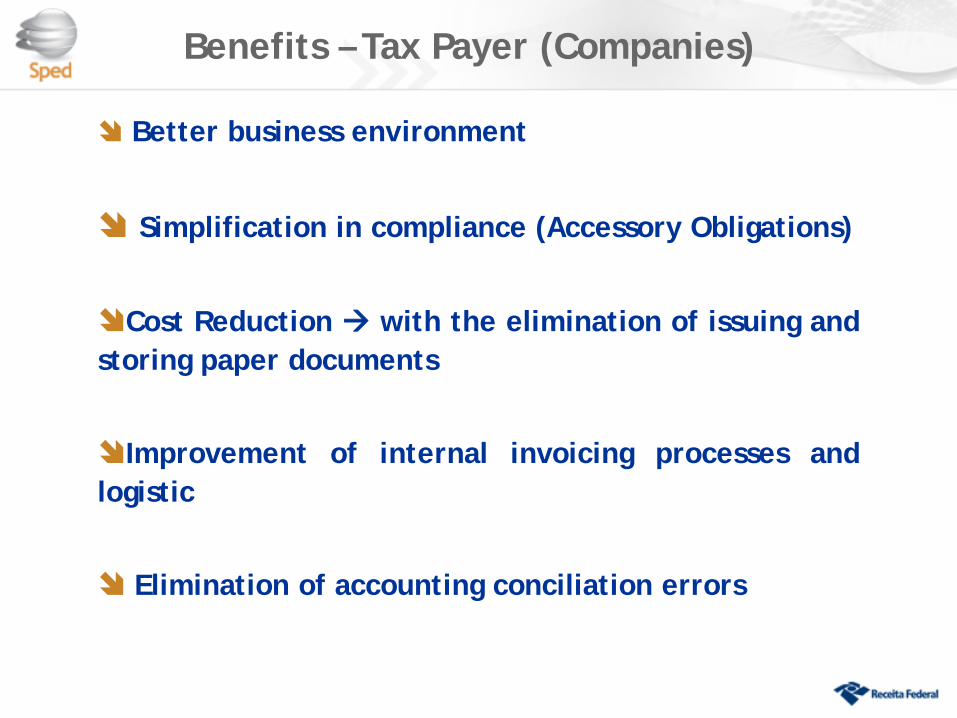

Better business environment

Simplification in compliance (Accessory Obligations)

Cost Reduction with the elimination of issuing andstoring paper documents

Improvement of internal invoicing processes andlogistic

Elimination of accounting conciliation errors

Benefits – Tax Payer (Companies)

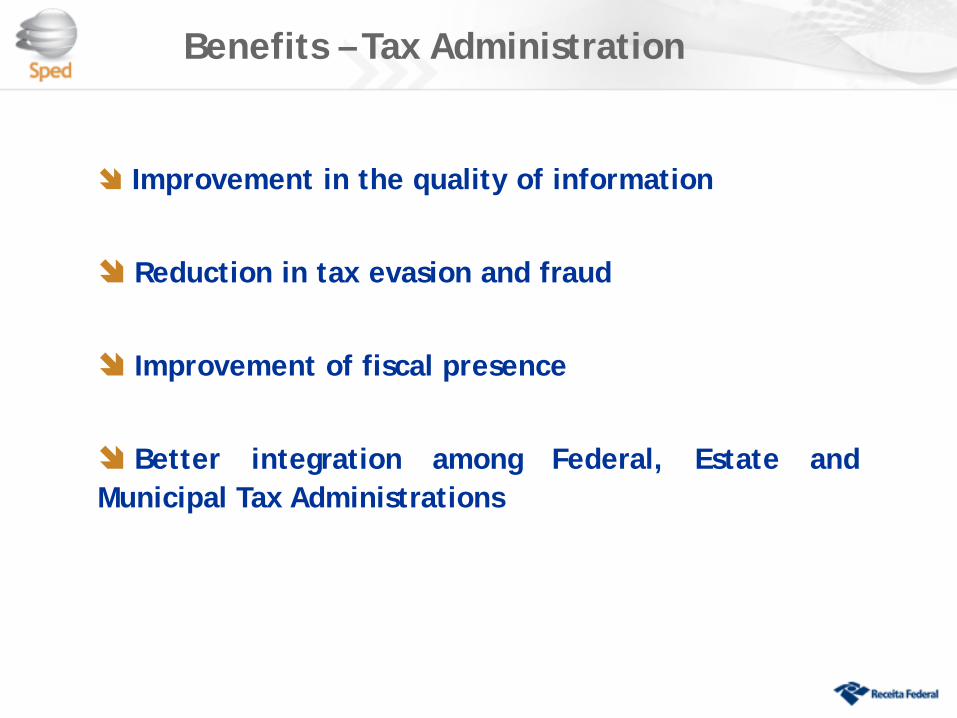

Improvement in the quality of information

Reduction in tax evasion and fraud

Improvement of fiscal presence

Better integration among Federal, Estate andMunicipal Tax Administrations

Benefits – Tax Administration

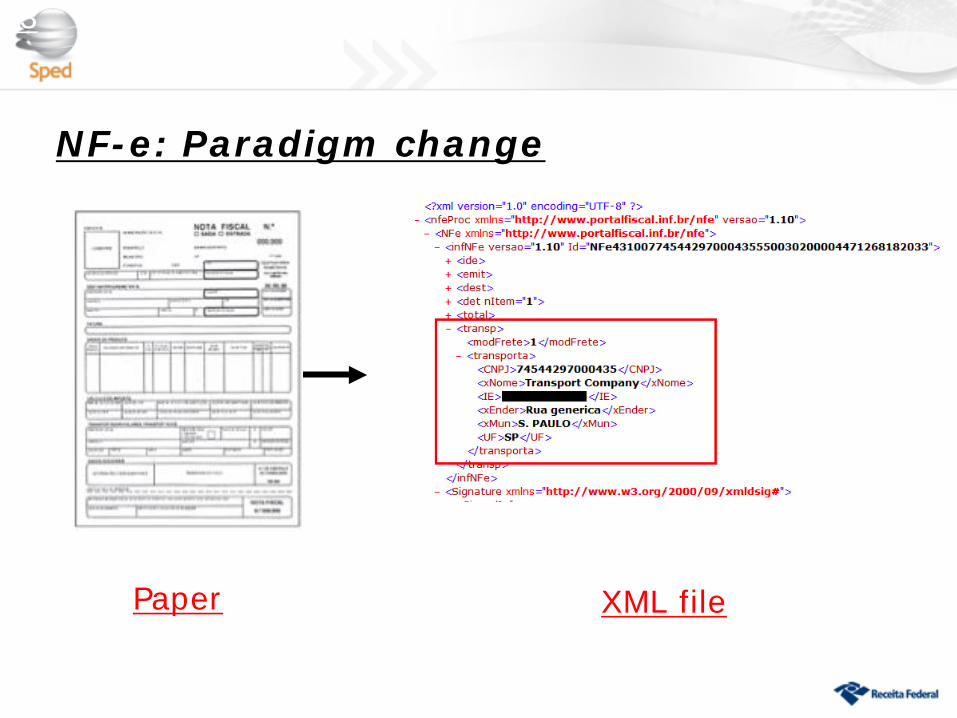

NF-e: Paradigm change

13

da emissão da nota fiscal em papel

XML filePaper

Document issued by the taxpayer on situations foreseenon the legislation, based on information and layout requiredby tax authorities.

The document is issued in order to evidence and validatea commercial transaction.

The transaction might be a sale, remittance entry or exitof goods in an establishment, among others.

The document is also issued when services are renderedby the taxpayer.

Invoice requirements are established by the threeadministrative spheres of the Brazilian government (federal,state and municipal tax authorities).

Electronic Wholesale Invoice (NF-e)

SPED – NF-e

Seller Buyer

Estate Admin: Origin Estate Admin: Destination

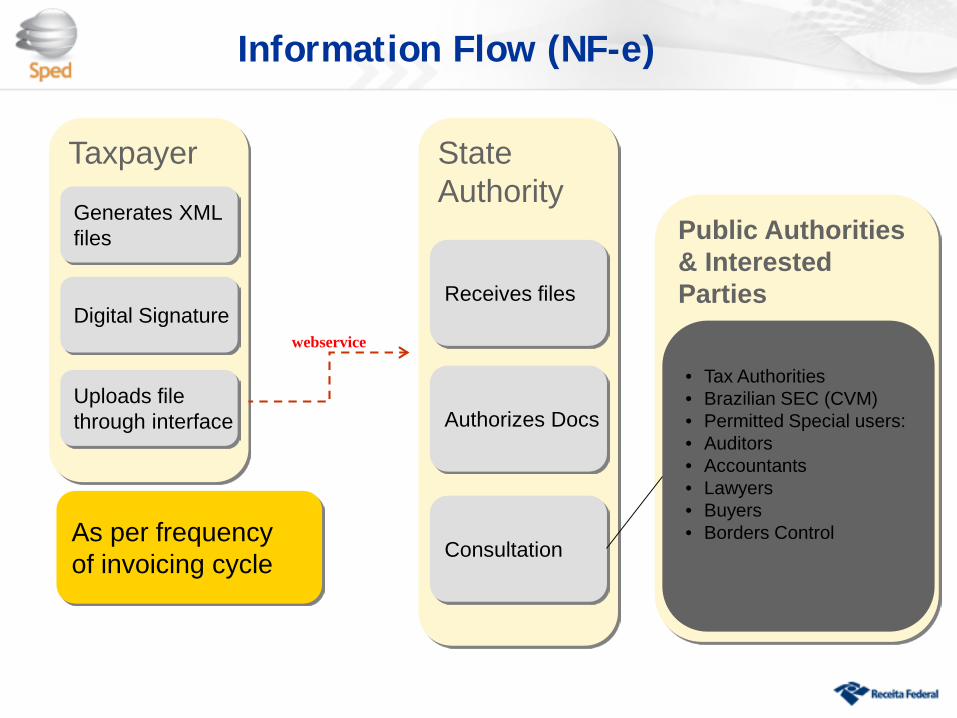

Information Flow (NF-e)

State Authority

Receives files

Authorizes Docs

Consultation

Public Authorities& Interested Parties

• Tax Authorities• Brazilian SEC (CVM)• Permitted Special users:• Auditors• Accountants• Lawyers• Buyers• Borders Control

Taxpayer

Generates XML files

Digital Signature

Uploads file through interface

As per frequency of invoicing cycle

webservice

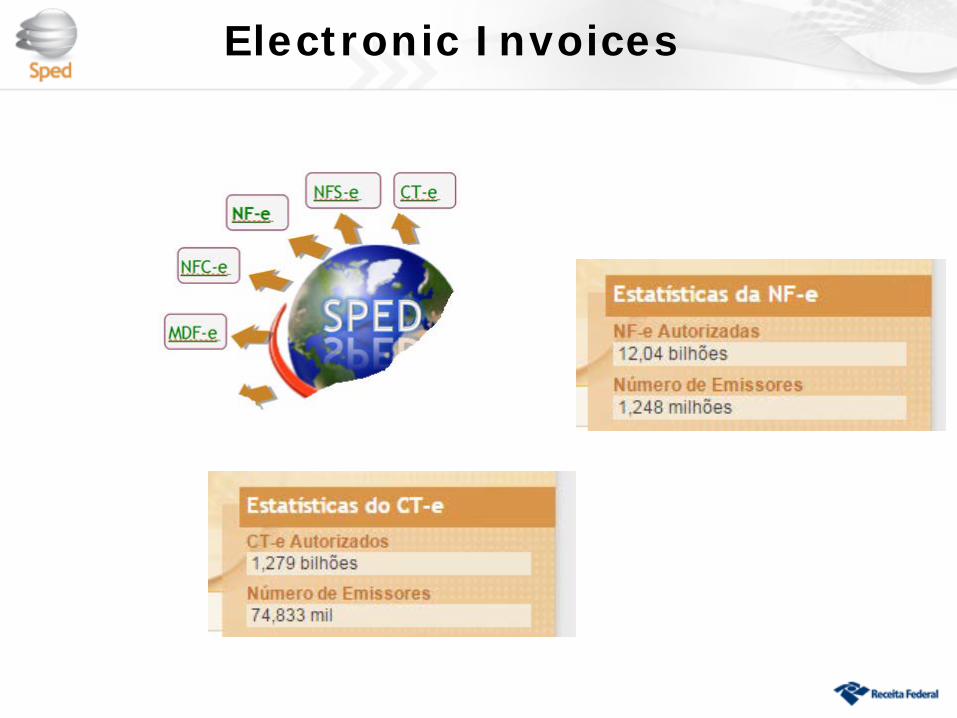

Electronic Invoices

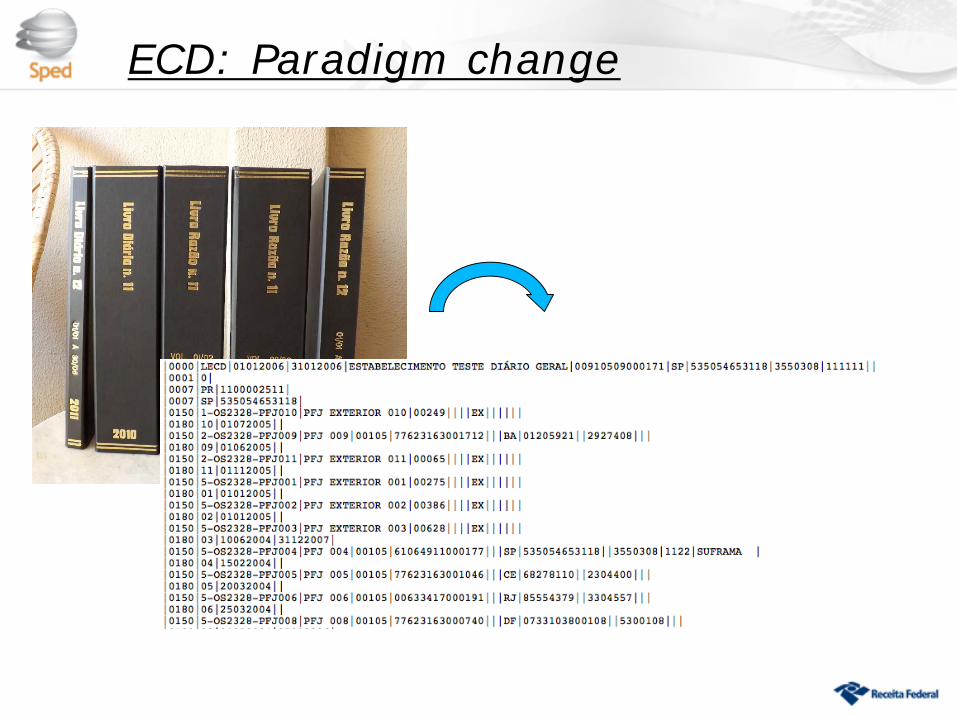

ECD: Paradigm change

Funcionalidades do SPED Contábil ECD

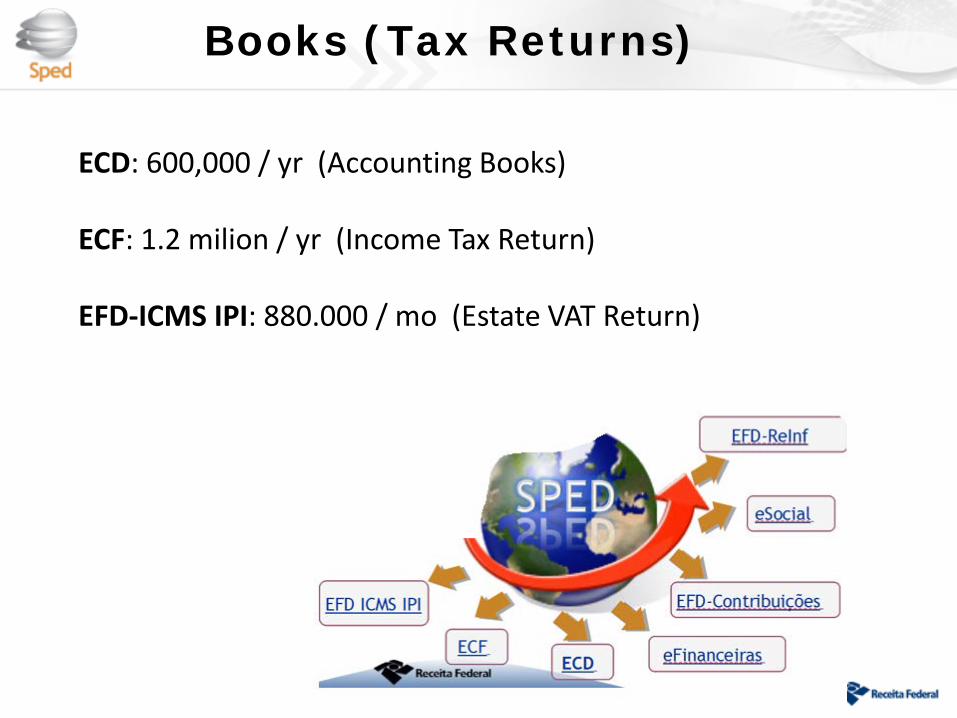

Books (Tax Returns)

ECD: 600,000 / yr (Accounting Books)

ECF: 1.2 milion / yr (Income Tax Return)

EFD-ICMS IPI: 880.000 / mo (Estate VAT Return)

Challenges&

Opportunities

eSocial

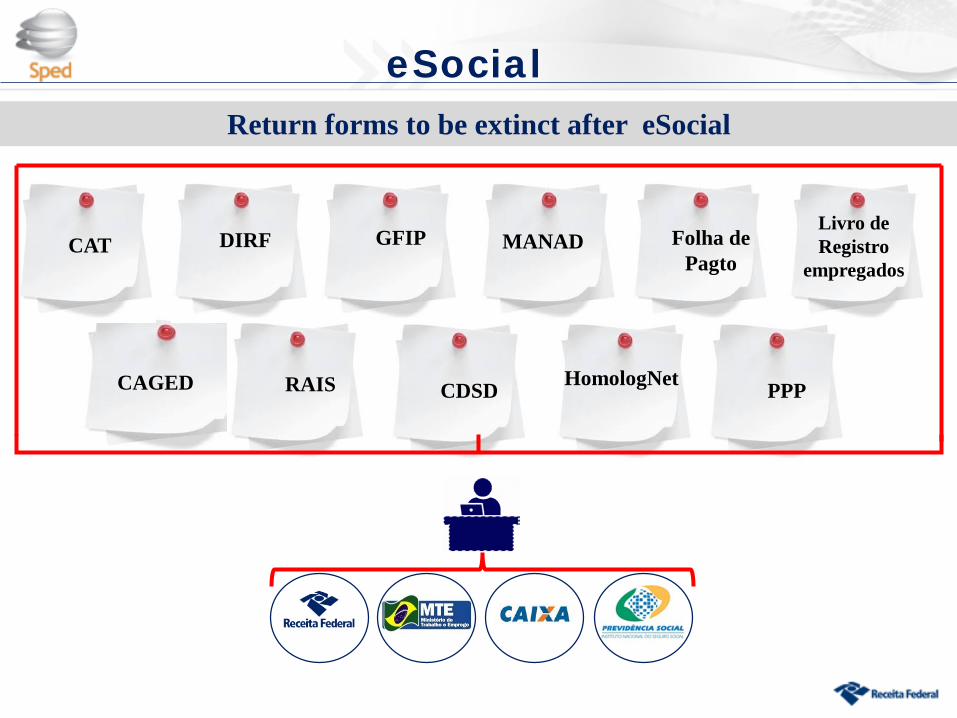

GFIP MANAD Folha dePagto

CAGED RAIS

Livro deRegistro

empregados

CDSD HomologNet PPP

DIRFCAT

Return forms to be extinct after eSocial