Embed Size (px)

Citation preview

PT. Indosat Tbk.

Full Year 2016 Results

2PT Indosat Tbk – FY 2016 Results

2016 was the year of data price warSummary

Competition in data services pricing was very though in 2016. All operators competed to offer very

cheap data services price and bundled with various trade marketing program that is very attractive

to win retailers/outlets engagement.

Hutch 3 consistently offered outlets championship/league program on a seasonal basis that was

targeting big outlet segment (wholesales) for a high revenue target with a great prize. Hutch 3

consistently offered Low price in Low quota in the beginning of 2016, then reduce the price further

in mid-2016 due to XL movement in competition.

XL surprisingly changed its move from campaigning value to offering very cheap data prices in mid-

2016. For 1 GB product XL has significantly lowered the trade price 50% in Q3 2016 compared to

the offering in beginning 2016. This was also followed by a decreasing price in 2 GB price.

XL with AXIS Brand has also conducted very significant price reduction data that offered a simple

and low quota. Axis also did a big move with lowering its 1 GB BRONET price ~50%, followed by

its 2 GB reduction. XL and Axis aggressiveness in very cheap data offers was triggering some

responds from competitors including Indosat.

Responding to tough competition, Indosat has determined its positioning in data pricing not as the

lowest price but not too far from competition.

3PT Indosat Tbk – FY 2016 Results

Facing 2017

It seems that facing 2017 all operators began to try to increase the price

of data services.

Hutch 3 has started to increase in offering its 1 GB in Feb 2017. The

same increase also happened for 2 GB package.

XL also increased its 1 GB price, followed by increasing its 2 GB price.

Indosat also has planned to increase data price as a strategic move in

improving profitability as well as strengthening Indosat positioning in the

competition.

Financial and

Operational Highlights

5

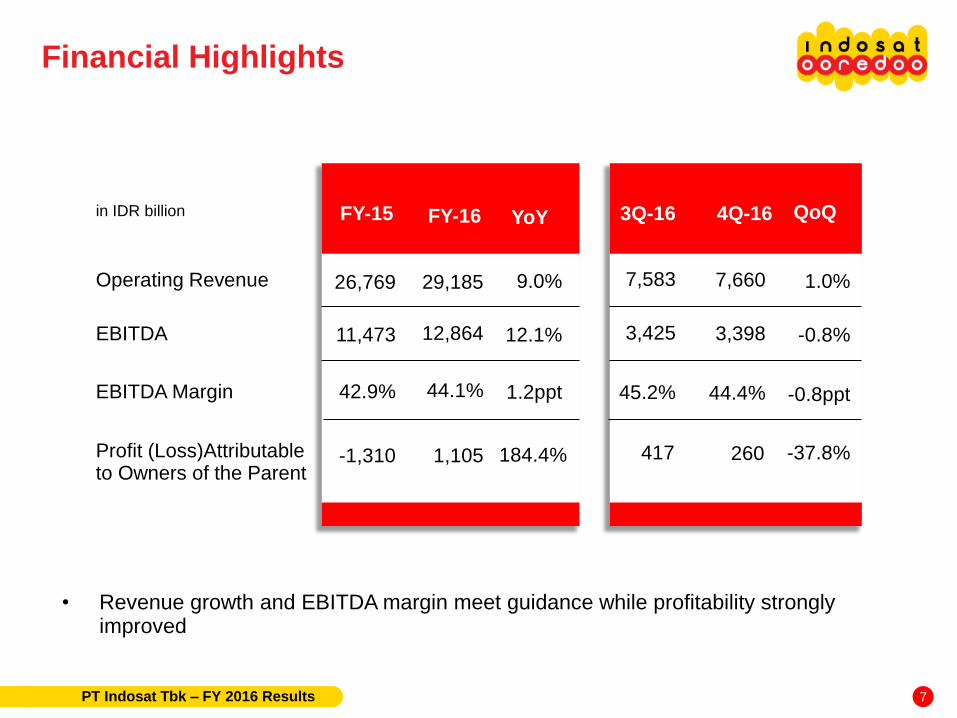

FY16 YoY Overview

Consolidated Revenue increased 9.0% from IDR 26,769 billion to IDR 29,185 billion

EBITDA increased 12.1% from IDR 11,473 billion to IDR 12,864 billion, EBITDA Margin reached 44.1%

Profit Attributable to Owners of The Parent increased from a loss of IDR 1,310 billion to a profit of IDR 1,105 billion

Free Cash Flow increased from IDR 1,561 billion to IDR 2,460 billion

PT Indosat Tbk – FY 2016 Results

6

4Q16 QoQ Overview

Consolidated Revenue increased 1.0% from IDR 7,583 billion to IDR 7,660 billion

EBITDA decreased 0.8% from IDR 3,425 billion to IDR 3,398 billion, EBITDA Margin reached 44.4%

Profit Attributable to Owners of The Parent decreased 37.8% from IDR 417 billion to IDR 260 billion

Free Cash Flow decreased from IDR 1,307 billion to a negative IDR186 billion

PT Indosat Tbk – FY 2016 Results

Operating Revenue

EBITDA

EBITDA Margin

Profit (Loss)Attributable to Owners of the Parent

29,185

FY-15 FY-16 YoY

9.0%

12,864 12.1%

44.1% 1.2ppt

1,105 184.4%

7,660

3Q-16 4Q-16 QoQ

1.0%

3,398 -0.8%

44.4% -0.8ppt

260 -37.8%

in IDR billion

26,769

11,473

42.9%

-1,310

Financial Highlights

7

• Revenue growth and EBITDA margin meet guidance while profitability strongly improved

7,583

3,425

45.2%

417

PT Indosat Tbk – FY 2016 Results

997909

989 1,044 1,190

286228

226238

266

in IDR billion

+1.0% QoQ+6.6% YoY

CellularFixed DataFixed Voice

+11.8% / -6.9%

+14.0% / +19.3%

-1.5% / +5.1%

QoQ / YoY

4Q-15 1Q-16

Operating Revenue Breakdown

5,904

Segment Revenue Overview

2Q-16

7,187

8

5,676

6,813

3Q-16

• Quarterly cellular revenue in 4Q-16 declined after peak season in 3Q-16• Initiative in fixed data segment to provide IT service that was launched back in 1Q-16

continued to deliver a result to support revenue growth.

4Q-16

5,914

7,129

PT Indosat Tbk – FY 2016 Results

6,301

7,583

6,204

7,660

Voice

SMS

Data

VAS

1.1%

FY-16YoY

-0.4%

46.7%

39.1%

-1.4%

4Q-16QoQ

-3.3%

3.0%

0.0%Digital business initiatives pushed VAS revenue growth

Cellular Revenue Performance

9

- Marketing initiative focus on voice service was able to generate growth in voice revenue YoY while data messaging service replaced traditional SMS.

PT Indosat Tbk – FY 2016 Results

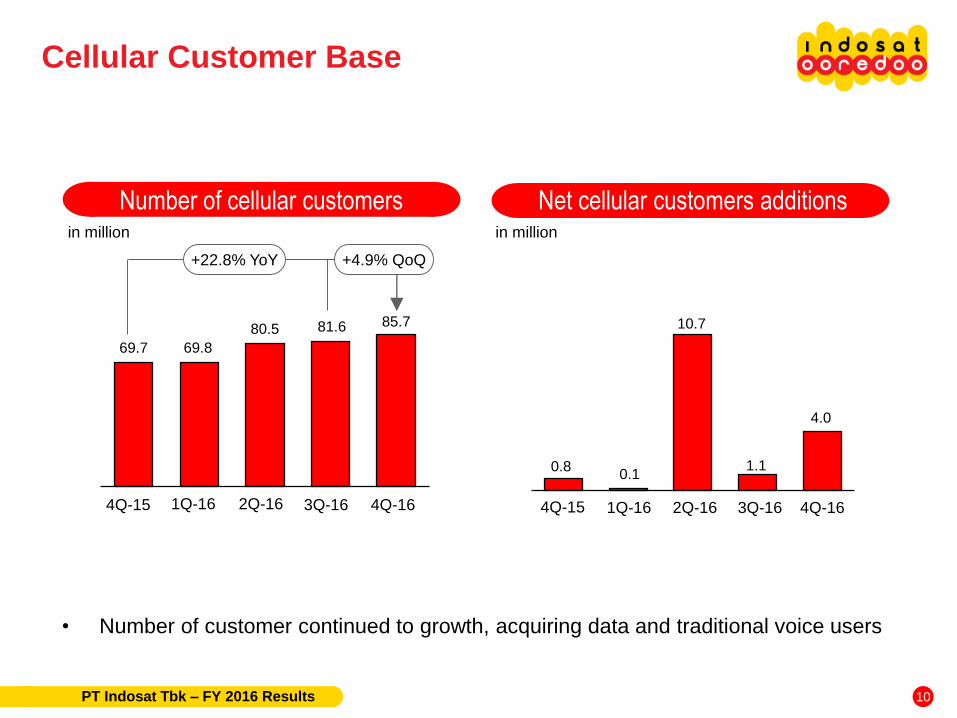

69.7 69.8

80.5 81.6 85.7

4Q-15

+22.8% YoY +4.9% QoQ

Number of cellular customersin million

4Q-15

in million

0.80.1

10.7

1.1

4.0

1Q-16 1Q-16

Net cellular customers additions

• Number of customer continued to growth, acquiring data and traditional voice users

2Q-16 2Q-16

Cellular Customer Base

10

3Q-16 3Q-164Q-16 4Q-16

PT Indosat Tbk – FY 2016 Results

ARPU and ARPM Voice Traffic and MOU

• A combination of high ARPU in Java and lower ARPU in ex-Java resulting a well managed ARPU level QoQ.

• Voice traffic maintained high coming from ex-Java area

7669 71

66 68

135 137126 124 123

15.6 14.5 15.6 16.6 16.6

+6.1% YoY

4Q-15

-0.3% QoQ

Voice Traffic

in billion minutes (Voice Traffic)

in minute/subscriber (MOU)

MOU

27.9 26.4 25.5 24.2 24.5

+1.3% QoQ-12.2% YoY

4Q-15

ARPU

in thousand IDR (ARPU)

ARPM

1Q-161Q-16 2Q-16 2Q-16

in IDR (ARPM)

ARPU maintained

11

3Q-16 3Q-164Q-16 4Q-16

PT Indosat Tbk – FY 2016 Results

Data Usage SMS Delivered

• Increase in data traffic driven by increase in number of data user and consumption per user

• SMS traffic continued to decline as trend shifting toward messaging application.

59

5255

4944

57,276 63,987

93,641

146,060

188,101

in TByte

+28.8% QoQ+228.4% YoY

4Q-15

in billion

-26.7% YoY -11.1% QoQ

1Q-16 4Q-152Q-16 1Q-16

Strong Data Usage

2Q-16

12

3Q-16 3Q-164Q-16 4Q-16

PT Indosat Tbk – FY 2016 Results

• Moderated operational expenses• Continued improvement in operational process

Cost of Service (CoS)

Depreciation and Amortization

Personnel

Marketing

as percentage of revenue

General and Administration

Total Expenses

Total Operating Expenses

Operational expenses

4Q-15

42.1%

35.1%

7.6%

6.8%

3.0%

94.7%

59.6%

13

1Q-16

40.4%

32.6%

7.8%

4.7%

3.7%

89.1%

56.5%

2Q-16

41.4%

31.3%

7.3%

4.9%

3.2%

88.1%

56.8%

PT Indosat Tbk – FY 2016 Results

3Q-16

40.6%

29.9%

6.8%

4.0%

3.5%

84.8%

54.9%

4Q-16

40.9%

29.4%

7.2%

3.5%

4.0%

85.1%

55.6%

2,906 2,961 3,0803,425 3,398

EBITDA and EBITDA margin

-0.8% QoQ+17.0% YoY

EBITDA

in IDR billion

EBITDA Margin

4Q-15

EBITDA margin in line with guidance

1Q-16

EBITDA performance

2Q-16

40.4%

14

43.5%

3Q-16 4Q-16

43.2%

PT Indosat Tbk – FY 2016 Results

45.2% 44.4%

Net profit

Improvement in operational level combinewith stable currency movement and lowUSD debt resulted positive net profit

-2,008

-1,310

1,105

+184.4% YoY+34.8% YoY

FY-16FY-15FY-14*

in IDR billion

* Restated due to implementation of PSAK 24 (revised 2013) effective 1 January 2015

Net profit

15PT Indosat Tbk – FY 2016 Results

2.73

2.42

1.84

27,346 27,72123,725

2.38

2.10

1.70

23,866 24,098 21,874

Gross debt* and gross debt/EBITDA Net debt* and net debt/EBITDA

• Currency mixed has improved and shall continue toward lower USD debt portionfollowed by further downward debt level

* IDR 4.05tn, IDR 3.97tn and IDR 3.51tn of obligation under finance lease are included in FY14, FY15 and FY16 respectively

FY-15FY-14 FY-16

-14.4% YoY

Gross Debt

in IDR billion

Gross Debt/EBITDA

FY-16FY-14 FY-15

Net Debt Net Debt/EBITDA

in IDR billion

Balance sheet

-9.2% YoY

16PT Indosat Tbk – FY 2016 Results

37.6

24.4

29.725.2

21.1 2,699

1,6632,117 1,910

1,603

Free cash flow Capex and Capex/Revenue

• Capex disbursement for FY-2016 was in line with guidance

in IDR billion

-1,392

463

8771,307

-186

4Q-15*

4Q-15

Capex

in IDR billion

Capex/Revenue1Q-16

1Q-16

2Q-16

2Q-16

Free cash flow & Capex

17

3Q-16

3Q-16

in %

4Q-16

4Q-16

* Reclassification from repayment of obligation under finance lease

PT Indosat Tbk – FY 2016 Results

Number of BTS Data User

• 4G coverage has reached 112 cities and counting• Data users are steadily growing with 1.7Gb/month usage on average.

23,596 23,714 23,793 23,859 24,042

23,730 25,068 25,816 26,273 27,724

3,361 3,544 3,724 4,080 4,717

+4.2% QoQ+11.4% YoY

3Q-16

2G3G

In million

4Q-15

52,326

1Q-16 4Q-15 1Q-16 2Q-16

34.031.2

35.139.4 40.5

+2.8% QoQ+19.1% YoY

Network & Data User

2Q-16

50,687

4G

18

3Q-164Q-16

53,333

4Q-16

PT Indosat Tbk – FY 2016 Results

54,212 56,483

Management focus

& Key updates

Management Focus

20

● Continue to transform Indosat Ooredoo to

become the leading digital telco in

Indonesia, both from a product offering

perspective as well as the way it interacts

with its stake holders

● Continue to build operational excellence

and efficiency as part of the company

culture

● To explore industry synergies to become

more efficient and effective

● To further strengthen the corporate (b2b)

offering to build a stable base through

connectivity and services.

PT Indosat Tbk – FY 2016 Results

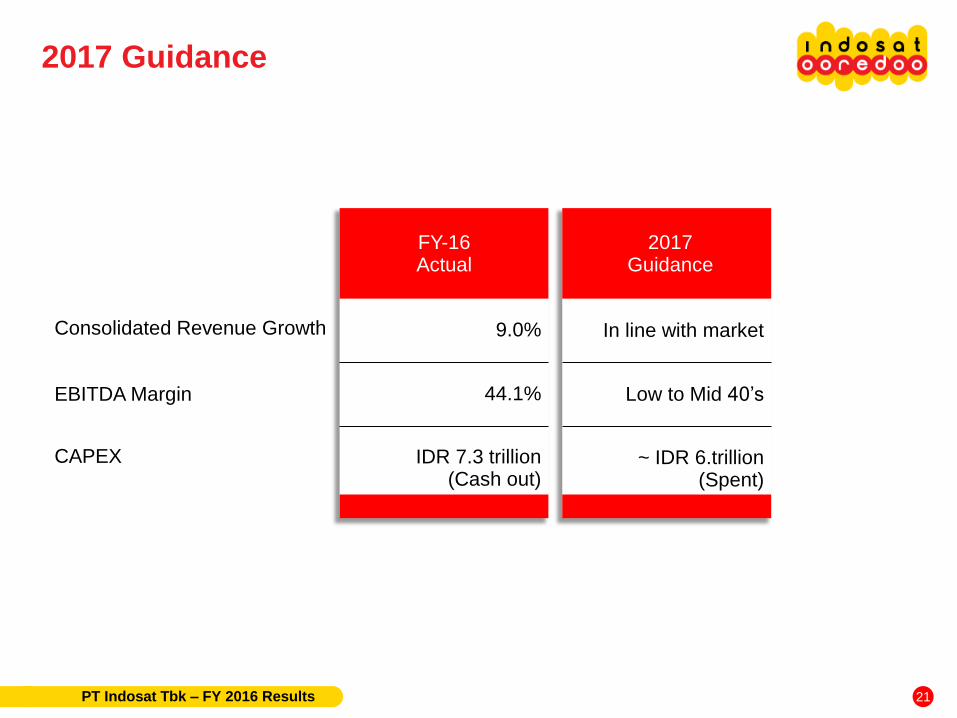

FY-16 Actual

2017 Guidance

Consolidated Revenue Growth 9.0% In line with market

EBITDA Margin 44.1% Low to Mid 40’s

CAPEX IDR 7.3 trillion(Cash out)

~ IDR 6.trillion(Spent)

2017 Guidance

21PT Indosat Tbk – FY 2016 Results

Thank YouInvestor Relations & Corporate SecretaryJl. Medan Merdeka Barat No. 21Jakarta - 10110Tel: +62 21 [email protected]

Supplemental

Information

On September 16, 2014, the South Jakarta Attorney Office (“Kejaksaan

Negeri Jakarta Selatan”), without preliminary notification, executed the

Supreme Court’s Decision on Mr. Indar Atmanto. The execution was

done based on a quotation of the Supreme Court’s Decision, which

states, among others, that (i) Mr. Indar Atmanto is found guilty and

sentenced to eight years imprisonment and charged with penalty of

Rp300,000,000,- (if the penalty is not paid, Mr. Indar Atmanto would

serve an additional six months imprisonment), and (ii) IM2 pay the

losses sustained by the State amounting to Rp1,358,343,346,674,-.

Subsequently, on January 16, 2015, Mr.Indar Atmanto and/or his lawyer

or IM2 received the document on the Supreme Court’s decision

regarding the litigation case. As of the issuance date of the consolidated

financial statements, Mr. Indar Atmanto and IM2 plan to conduct further

legal act by submitting a reconsideration request peninjauan kembali

(”PK”).

On March 16, 2015, Mr. Indar Atmanto’s submission of Judicial Review

[Peninjauan Kembali (”PK”)] was officially registered at the Corruption

Court under No. 08/AKTA.PID.SUS/PK/TPK/2015/PN.Jkt.Pst.

On November 4, 2015, the Supreme Court’s official website announced

that the Judicial Review filed by Mr. Indar Atmanto was rejected based

on Supreme Court’s decision dated October 20, 2015. However, no

detailed information regarding the exact content of such Supreme

Court’s decision was available. As of the issuance date of the interim

consolidated financial statements, the official copy of such Supreme

Court’s decision hasn’t been received.

IM2 case development

24PT Indosat Tbk – FY 2016 Results

On January 17, 2017, S&P Global Ratings affirmed its 'BB+' long-term corporate credit

rating on PT Indosat Tbk. The outlook remains positive. At the same time, they affirmed

their 'axBBB+' long-term ASEAN regional scale rating on the Indonesia-based

telecommunications company.

On 1 December 2016, PEFINDO has affirmed its “idAAA” rating for PT Indosat Tbk

(ISAT)’s Bonds VII Year 2009 Serie B of IDR600 billion and its “idAAA(sy)” rating for ISAT’s

Sukuk Ijarah IV Year 2009 Serie B of IDR172 billion that will mature on December 8, 2016.

ISAT should be able to repay the maturing Bond and Sukuk Ijarah using its internal fund.

As of September 30, 2016, it had cash and cash equivalents amounting to IDR2.4 trillion.

On 13 December 2016, Moody's Investors Service has affirmed Indosat Tbk. (P.T.)'s Ba1

corporate family rating, combines The company's standalone credit strength, which

reflects its established market position, their expectation of moderate growth in the

cellular market, and an improving macro environment. However, competition, especially in

mobile data space, will continue to pressure EBITDA margins although we expect them to

remain high for the rating level around 50%.

On 9 August 2016, Fitch Ratings Indonesia has assigned National Long-Term Ratings of

'AAA(idn)' to PT Indosat Tbk's (Indosat Ooredoo: Long-Term IDR BBB/National Rating

AAA(idn)/Stable) IDR3,172bn senior unsecured bonds and IDR288bn sukuk ijarah issues.

The issues are launched from Indosat Ooredoo's IDR9trn bond programme and IDR1trn

sukuk ijarah programme - affirmed at 'AAA(idn)' on 15 March 2016 - and are consequently

rated at the same level as the programmes.

Credit ratings

25PT Indosat Tbk – FY 2016 Results

1.88 0.27 0.27

5.94

2.56

3.62

0.95 1.10

2.08

0.12 0.36 0.81

0.26

In IDR trillion

20202019 202220182017

IDR

USD in IDR

2021 2024

* Excluding obligation under capital lease

2023

Debt maturity profile*

26PT Indosat Tbk – FY 2016 Results

2025 2026

Number of BTS

2 x 10.0

900 Mhz

2 x 7.5

2 x 7.5

Indosat

Telkomsel

XL Axiata

2 x 20.0

1800 Mhz

2 x 22.5

2 x 22.5

2 x 10.0

2100 Mhz

2 x 15.0

2 x 15.0

in Mhz

Hutchison - 2 x 10.0 2 x 10.0

2 x 2.5

850 Mhz

2 x 4.5

-

-

15.0*

2300 Mhz

15.0

-

-

* Indosat/IM2: West Java exclude Bogor, Depok & Bekasi

Spectrum overview

27

2020 2020 2020 2019 & 2026 2019Valid until

PT Indosat Tbk – FY 2016 Results

• PT Indosat Tbk ( “Indosat” or “Company” ) cautions investors that certain statements contained in this document state its management's intentions, hopes, beliefs, expectations, or predictions of the future are forward-looking statements

• The Company wishes to caution the reader that forward-looking statements are not historical facts and are only estimates or predictions. Actual results may differ materially from those projected as a result of risks and uncertainties including, but not limited to:

• The Company’s ability to manage domestic and international growth and maintain a high level of customer service

• Future sales growth

• Market acceptance of the Company’s product and service offerings

• The Company’s ability to secure adequate financing or equity capital to fund our operations

• Network expansion

• Performance of the Company’s network and equipment

• The Company’s ability to enter into strategic alliances or transactions

• Cooperation of incumbent local exchange carriers in provisioning lines and interconnecting our equipment

• Regulatory approval processes

• Changes in technology

• Price competition

• Other market conditions and associated risks

• The company undertakes no obligation to update publicly any forward-looking statements, whether as a result of future events, new information, or otherwise

Disclaimer

28PT Indosat Tbk – FY 2016 Results