Embed Size (px)

Citation preview

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited

Prospects bright with good rabi

Key takeaways from this edition of FARM FACTS are: 1) Rabi season: Farmers’ better cash flow position aided by higher yields and increase in uptake by government agencies helped sustain rabi growth (sowing up 3% YoY). 2) Crop prices: In contrast to global prices, domestic prices are stable (ex-soybean, pulses). 3) Reservoir storage: Water level

across reservoirs above 55%, indicating timely start of kharif sowing. 4) Global commentary: Remunerative crop prices (up 30% plus) along with favourable climatic conditions across Latam driving growth.

We are confident of agri-input’s growth prospects. Forecast of ‘normal monsoon’ by Skymet and surge in crop prices remain key growth drivers.

Rabi season: Good reservoir levels sustain growth

Aided by good reservoir levels along with strong cash flow/liquidity position of

farmers with bumper kharif, the rabi season has remained healthy despite high base

of last year. Crop sowing has been at record high (up 3% YoY) with wheat driving

improvement in overall sowing. Crop prices have been a mix bag with those of key

crops wheat and maize contracting by more than 10% YoY. However, positive

highlight has been the higher procurement target set by government agencies

despite tepid prices against MSP rates. Going forward, we expect bumper

production in rabi and higher procurement by government agencies to sustain the

buoyancy in agri inputs.

Marginal rise in fertiliser volumes

Fertiliser volumes have remained stable driven by timely start to rabi season.

Improvement in crop sowing (up 3% YoY) led by good reservoir levels helped

improve demand for fertilizer. Till date, fertilizer volumes have been up 2% YoY

during Dec-Feb. Given the high base of Q3FY20, we expect industry volumes to grow

in single digit only in Q4FY21. Going forward, we expect clearance of subsidy

backlog by the government to yield better efficacy and significant reduction in

working capital requirement of fertiliser players.

Crop prices: On uptrend in global markets

Crop prices have surged more than 30% YoY. Such a spurt in agri prices is likely to

be a key positive for agri-input players such as UPL. Also, demand revival across

Latam (after weak Q3FY21) and North America bodes well.

Outlook: Positive post strong kharif

Government estimates peg kharif production at a record high of 148mt. Better crop

prices given higher procurement target along with good reservoir levels are likely

to drive rabi season despite high base of Q3FY20. Globally, remunerative crop prices

along with conducive environment conditions is like to benefit global players such

as UPL.

Top picks: UPL (BUY), Dhanuka Agritech (BUY), Coromandel International (BUY).

India Equity Research Agri Inputs March 10, 2021

FARM FACTS SECTOR UPDATE

Rohan Gupta Bharat Gupta Nihal Mahesh Jham +91 (22) 4040 7416 +91 (22) 6620 3320 +91 (22) 6623 3352 [email protected] [email protected] [email protected]

F

FARM FACTS

Edelweiss Securities Limited

2 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

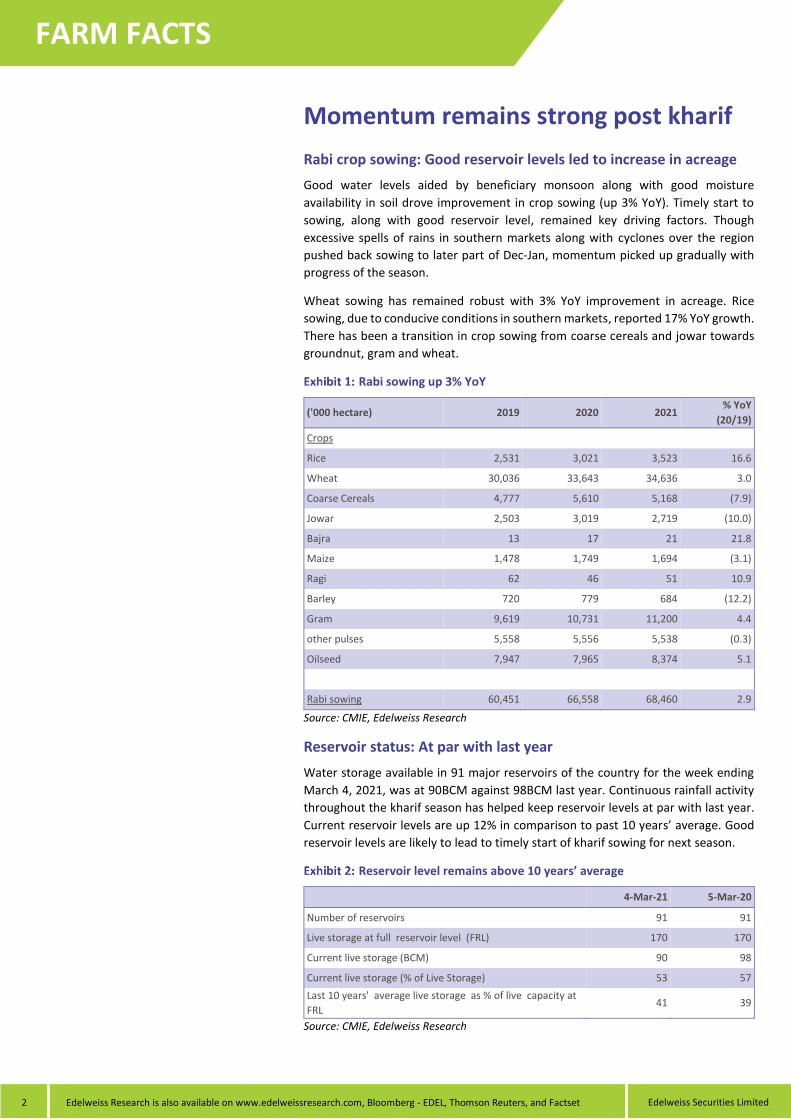

Momentum remains strong post kharif

Rabi crop sowing: Good reservoir levels led to increase in acreage

Good water levels aided by beneficiary monsoon along with good moisture

availability in soil drove improvement in crop sowing (up 3% YoY). Timely start to

sowing, along with good reservoir level, remained key driving factors. Though

excessive spells of rains in southern markets along with cyclones over the region

pushed back sowing to later part of Dec-Jan, momentum picked up gradually with

progress of the season.

Wheat sowing has remained robust with 3% YoY improvement in acreage. Rice

sowing, due to conducive conditions in southern markets, reported 17% YoY growth.

There has been a transition in crop sowing from coarse cereals and jowar towards

groundnut, gram and wheat.

Rabi sowing up 3% YoY

('000 hectare) 2019 2020 2021 % YoY

(20/19)

Crops

Rice 2,531 3,021 3,523 16.6

Wheat 30,036 33,643 34,636 3.0

Coarse Cereals 4,777 5,610 5,168 (7.9)

Jowar 2,503 3,019 2,719 (10.0)

Bajra 13 17 21 21.8

Maize 1,478 1,749 1,694 (3.1)

Ragi 62 46 51 10.9

Barley 720 779 684 (12.2)

Gram 9,619 10,731 11,200 4.4

other pulses 5,558 5,556 5,538 (0.3)

Oilseed 7,947 7,965 8,374 5.1

Rabi sowing 60,451 66,558 68,460 2.9

Source: CMIE, Edelweiss Research

Reservoir status: At par with last year

Water storage available in 91 major reservoirs of the country for the week ending

March 4, 2021, was at 90BCM against 98BCM last year. Continuous rainfall activity

throughout the kharif season has helped keep reservoir levels at par with last year.

Current reservoir levels are up 12% in comparison to past 10 years’ average. Good

reservoir levels are likely to lead to timely start of kharif sowing for next season.

Reservoir level remains above 10 years’ average

4-Mar-21 5-Mar-20

Number of reservoirs 91 91

Live storage at full reservoir level (FRL) 170 170

Current live storage (BCM) 90 98

Current live storage (% of Live Storage) 53 57

Last 10 years' average live storage as % of live capacity at

FRL 41 39

Source: CMIE, Edelweiss Research

Edelweiss Securities Limited

FARM FACTS

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 3

Fertilisers: Moderate growth volumes over Dec-Feb

Fertiliser demand has seen single digit growth over Dec-Feb (up 2% YoY). Going

forward, we expect momentum in fertiliser demand to remain positive with farmers

getting better crop prices for their produce.

Total fertiliser sales increased moderately(up 2% YoY) over Dec-Feb

(in '000 Tonnes) Feb-21 Feb-20 % YoY Jan-21 Jan-20 % YoY Dec-20 Dec-19 % YoY Nov-20 Nov-19 % YoY

DAP 463 478 (3.0) 403 340 18.5 525 665 (21.0) 1,232 1,482 (16.9)

MOP 302 237 27.2 243 176 37.9 274 177 55.1 301 217 38.4

NPKS 1,058 800 32.2 1,089 858 26.9 1,007 935 7.7 1,004 954 5.2

Urea 2,334 2,678 (12.8) 3,405 3,561 (4.4) 3,865 3,883 (0.5) 3,326 3,151 5.6

Compost 18 18 (2.6) 18 19 (4.9) 26 21 25.6 16 20 (23.2)

SSP 415 321 29.2 334 288 15.8 264 255 3.5 346 433 (20.0)

Total 4,590 4,532 1.3 5,492 5,242 4.8 5,961 5,935 0.4 6,225 6,258 (0.5)

Source: Department of Fertilizer, Edelweiss Research

Manufactured sales remained muted in Feb-21

(in '000 Tonnes) Feb-21 Feb-20 % YoY Jan-21 Jan-20 % YoY Dec-20 Dec-19 % YoY Nov-20 Nov-19 % YoY

DAP 342 387 (11.6) 308 267 15.2 376 438 (14.0) 757 893 (15.3)

MOP 196 181 7.9 151 128 18.4 149 120 23.8 162 120 34.4

NPKS 902 764 18.0 1,021 823 24.0 936 887 5.6 907 894 1.5

Urea 1,947 2,192 (11.2) 2,567 2,518 1.9 2,742 2,746 (0.2) 2,379 2,411 (1.3)

Compost 18 18 (2.6) 18 19 (4.9) 26 21 25.6 16 20 (23.2)

SSP 415 321 29.2 334 288 15.8 264 255 3.5 346 433 (20.0)

Total 3,819 3,865 (1.2) 4,400 4,044 8.8 4,494 4,467 0.6 4,566 4,771 (4.3)

Source: Department of Fertilizer, Edelweiss Research

Traded fertiliser sales increased 15% YoY in Feb-21

(in '000 Tonnes) Feb-21 Feb-20 % YoY Jan-21 Jan-20 % YoY Dec-20 Dec-19 % YoY Nov-20 Nov-19 % YoY

DAP 121 90 33.9 95 73 30.6 149 227 (34.3) 476 590 (19.3)

MOP 106 56 89.1 91 48 89.6 125 56 121.6 139 97 43.4

NPKS 156 36 332.3 68 35 95.9 71 48 47.0 97 61 59.7

Urea 387 485 (20.2) 838 1,043 (19.6) 1,123 1,136 (1.2) 948 739 28.2

Compost

SSP

Total 770 668 15.4 1,092 1,198 (8.8) 1,468 1,468 0.0 1,659 1,487 11.6

Source: Department of Fertilizer, Edelweiss Research

F

FARM FACTS

Edelweiss Securities Limited

4 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

Crop prices: Sharp increase in pulses and soybean

Crop prices have improved across the past six months. Though prices of wheat and

maize have contracted 13% and 22% YoY, respectively, those of soyabean and pulses

have seen a sharp rebound--up 17% and 15% YoY, respectively.

Crop prices remain remunerative

Price (INR/Quintal) 1 month 3 month 6 month 1 Year

Wheat 1,932 1,764 1,841 2,226

Soybean 4,562 4,165 3,726 3,909

Cotton 5,665 5,432 4,542 5,087

Tur Dal 9,321 9,304 8,405 8,124

Paddy 1,874 1,987 1,853 1,898

Sugar 3,571 3,517 3,615 3,564

Maize 1,382 1,501 1,305 1,783

( % Growth) 1 month 3 month 6 month 1 Year

Wheat (1.6) 3.0 0.8 (13.2)

Soybean 4.5 15.8 22.4 16.7

Cotton 1.5 6.7 21.6 11.4

Tur Dal 0.9 -6.4 14.0 14.7

Paddy (9.2) 2.3 (3.5) (1.3)

Sugar 2.3 (0.1) (0.8) 0.2

Maize 0.3 (4.7) 6.9 (22.5)

Source: Agmarknet, Edelweiss Research

Crop prices have remained on the soft side (ex-arhar and soybean) in comparison to

MSP. Prices of crops (Bajra, maize, ragi and jowar) across open markets/mandis have

remained nearly 20% below MSP.

MSP still remains on higher side, excluding soybean and arhar

Crop MSP Price Market Price(MP) % Change (MP/MSP)

Paddy, common 1,868 1,874 0.3

Jowar, hybrid 2,620 2,508 (4.3)

Bajra 2,150 1,431 (33.4)

Maize 1,850 1,478 (20.1)

Ragi 3,295 2,781 (15.6)

Arhar(Tur) 6,000 8,683 44.7

Groundnut in shell 5,275 5,795 9.9

Soyabean, yellow 3,880 4,896 26.2

Source: Agmarknet, Edelweiss Research

Farmers to gain from improved yield of kharif. Also, better MSP and higher

procurement by government are likely to help increase liquidity position of farmers.

As per government’s first Kharif crop estimate, overall foodgrain production is

expected to remain at 147mt (up 4% YoY).

Globally, prices have improved significantly. Prices of soybean have jumped 70%

YoY, while those of corn, cotton and wheat are up 38%, 35% and 27% YoY,

respectively. Such a spurt in crop prices is likely to result in higher cash flows for

farmers yielding strong agri-input demand globally, benefiting players such as UPL,

Bayer, Corteva, among others.

Edelweiss Securities Limited

FARM FACTS

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 5

Exhibit 8: Soybean prices surged 70% YoY

Source: Bloomberg, Edelweiss Research

Exhibit 11: Wheat prices increased 27% YoY

Source: Bloomberg, Edelweiss Research

ZZZ

Source: Bloomberg, Edelweiss Research

Exhibit 9: Corn prices up 38% YoY

Source: Bloomberg, Edelweiss Research

Exhibit 12: Cotton increased 35% YoY

Source: Bloomberg, Edelweiss Research

800

1,000

1,200

1,400

1,600

1,800

Mar

20

Jun

20

Sep

20

Dec

20

Mar

21

(USd

/bu

)

SOYBEAN FUTURE

300

375

450

525

600

675

750

Mar

20

Jun

20

Sep

20

Dec

20

Mar

21

(USd

/bu

)

CORN FUTURE May17

300

375

450

525

600

675

750

Mar

20

Jun

20

Sep

20

Dec

20

Mar

21

(USd

/bu

)

CORN FUTURE May17

50

60

70

80

90

100

Mar

20

Jun

20

Sep

20

Dec

20

Mar

21

(USd

/Lb

)

CTK1 Comdty

F

FARM FACTS

Edelweiss Securities Limited

6 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

Channel Checks: growth remains sound

Our channel checks with distributors across India highlight robustness of agri inputs.

Farmers’ cash flow position has remained strong driven by uptick in purchases done

by government agencies along with record yields of kharif. Harvest season of rabi

has started and going by current scenario, a record rabi production is anticipated.

Dealer from Madhya Pradesh

Expects sowing for kharif to start on time from June.

Farmers shifting from using SSP to DAP given lack of campaigning done by

government.

Expects corn acreage to increase going forward. Cotton acreage could see

dilution.

Farmer cash flows: Govt. has been aiding farmers in procuring higher quantum

of foodgrains at MSP. Fasal Bima money is also being given to farmers having lost

their crops during kharif.

Urea consumption is lower during kharif. Major urea consumption takes place in

rabi in MP. Soybean-urea is not required much.

DAP: INR1,185 per bag (companies have been holding inventory). Expected rise

of prices to extent of INR150/bag. However, IFFCO has said in a press release of

not increasing DAP prices.

Zinc+ boron based SSP products are available now: Usage has increased slightly.

DAP-IFFCO, GSFC, Deepak fertiliser, CHAMBAL, DCM are private players while

IFFCO is a big supplier.

Expects maize sowing to pick up in kharif. BASF, Bayer having strong portfolio in

corn herbicide, Sales likely to increase. Bayer product ‘laudis’ and BASF (synger).

Dow (delicate use increase).

Corn-fall armyworm-big issue-Sygenta-product seed treatment (40 days no

attack)-Seed treatment for cotton.

Dhanuka-Largo(Dow-delicate-Insecticide-fall armyworm)-Sales will increase.

Edelweiss Securities Limited

FARM FACTS

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 7

Global commentary: Uptick in global agri-cycle

Commentaries by global innovators highlight robustness of the agrochemical

industry in challenging times of covid-19. Nearly all companies have posted good

double-digit growth (forex adjusted) in regions of Latam, particularly Brazil. Driven

by higher channel inventory along with weather-related challenges, demand across

North America and Europe remained soft. However, good water levels across

reservoirs in South East Asia aided by normal monsoon helped companies register.

Strong growth momentum by global innovators

Companies Key Highlights (Q4CY20)

Bayer AG

Sales at Crop Science advanced by 4.3% (Fx & portfolio adj.) during Q4CY20. Sales at Fungicides rose 5% YoY, with all

regions registering growth. In Latin America company’s product Fox Xpro™ reported an increase in volumes and prices.

Normalization of weather conditions and synergy effects arising from the Bayer Plus program helped company to deliver

better in North America. Herbicide segment reported a decline of 1% YoY (Fx Adj.) due in particular to a loss of

registrations in Europe / Middle East / Africa and North America.

FMC

The revenue decrease was driven by a 5 percent FX headwind and a 3 percent volume decrease, partially offset by a 4

percent increase in pricing. Strong volume growth in EMEA and Asia was more than offset by weakness in North America

and Latin America. Sales in EMEA increased 45 percent year over year, due to a particularly strong quarter for diamide

insecticides and cereal herbicides in addition to significant pre-ordering in the UK in advance of Brexit. In Asia, revenue

increased 11 percent year over year, driven by broad volume growth in India, China, Japan and Australia. In North America,

sales decreased 34 percent year over year. The majority of this decline was due to supply chain disruptions, including COVID-

related factors associated with logistics and a U.S.-based tolling partner. The remainder of the decrease was due to reduced

volume in lower-value pre-emergent herbicides.

Syngenta

Syngenta reported a 12% constant currency growth with a strong performance across all markets and segments,

particularly in Brazil. In North America, sales for the H1CY20 were up 4 percent at constant exchange rates. However,

sales were impacted by cold weather and excessive rain in Q2. In Latin America, positive momentum from 2019 continued

in the first half of 2020, with strong pest pressure in Brazil and higher volumes in Argentina despite difficult economic

conditions. In Asia Pacific, sales were up by 12 percent (CER), with strong growth in Australia due to improved weather

conditions, and continued momentum from 2019 in India. Sales in Europe, Africa and the Middle East were 5 percent

higher at constant exchange rates compared with 2019. Performance was solid, particularly in South Europe, despite

COVID19 and dry weather in North-West Europe

Source: Company, Edelweiss Research

Latam drives growth momentum for global players

(% YoY Growth) LATAM EUROPE ASIA/ROW North America

Global Players

Bayer 14 (1) 7 (5)

Syngenta 32 5 12 4

FMC 4 45 11 (34)

Corteva 21 (9) 17 31

Indian Players

UPL (8) 30 21 5

Sharda Cropchem 23 30 27 31

Source: Company, Edelweiss Research

*Growth figures for Bayer, Syngenta, FMC and Corteva excludes forex impact

* Syngenta to report H2CY20 results on 20th May, 2021

* UPL and Sharda Cropchem growth includes forex impact

Fertiliser segment: Spurt in raw material prices to impact margins

Fertiliser raw material prices have bounced back during Q3FY21. Jump in phos-acid

(up 35% YoY) and ammonia (up 10% YoY) prices is likely to impact margins of

fertiliser players. While we expect companies to pass on the spurt in prices to

farmers, we expect margins to remain under pressure if companies remain

competitive in gaining market share.

F

FARM FACTS

Edelweiss Securities Limited

8 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

Phos acid prices up 35% YoY

Source: Bloomberg, Edelweiss Research

Ammonia prices up 10% YoY

Source: Bloomberg, Edelweiss Research

Exhibit 16: DAP prices up sharp 84% YoY

Source: Bloomberg, Edelweiss Research

Potash Murate prices down 14% YoY

Source: Bloomberg, Edelweiss Research

Urea prices up 36% YoY

Source: Bloomberg, Edelweiss Research

500

560

620

680

740

800

Mar-20 Jun-20 Sep-20 Dec-20 Mar-21

(USD

/Mt)

Phos acid

150

200

250

300

350

400

Mar

-19

Jun

-19

Sep

-19

Dec

-19

Mar

-20

Jun

-20

Sep

-20

Dec

-20

Mar

-21

(USD

/Mt)

Ammonia

250

350

450

550

650

750

Mar

-19

Jun

-19

Sep

-19

Dec

-19

Mar

-20

Jun

-20

Sep

-20

Dec

-20

Mar

-21

(USD

/Mt)

DAP

200

220

240

260

280

300

Mar

-20

Jun

-20

Sep

-20

Dec

-20

Mar

-21

(USD

/Mt)

Potash Murate

150

205

260

315

370

425

480

Dec-18 Mar-19 Jun-19 Sep-19 Dec-19 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21

(USD

/Mt)

Urea

Edelweiss Securities Limited

FARM FACTS

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 9

Agriculture Sector News

Dhanuka Agritech: Staying confident on strong growth in agriculture sector in India

In a detailed interview, the management of Dhanuka Agritech sounded very bullish

on the prospects of the entire agricultural space in India and also was enthused by

the developments and decisions taken by the government to aid the growth of

smaller farmers to ensure a better crop price. Dhanuka Agritech Limited is a leading

agrochemical company with a presence in herbicides, insecticides, fungicides, and

plant growth regulators /bio-stimulants market.

Dhanuka Agritech: Staying confident on strong growth in agriculture sector in India

Indian Govt. to tread cautiously in allowing nano-zinc and nano-copper crop

nutrients

The government has said that it will tread cautiously in accepting the industry’s

demand to allow nano-zinc and nano-copper in the absence of long-term data amid

global fear of allowing these as crop nutrients may lead to toxicity in the crops.The

commercial use of nano-urea was allowed in November last year that may help

improve crops yield by 18-35%.

Indian Govt to tread cautiously in allowing nano-zinc and nano-copper crop

nutrients

Govt. buys paddy worth Rs 1.26 lakh crore at MSP so far this kharif marketing

season

Procurement of Kharif paddy has increased nearly 15 per cent to 669.59 lakh tonnes

at MSP so far in the current Kharif marketing season, costing over Rs 1.26 lakh crore,

amid ongoing farmers protest against three new farm laws. Kharif Marketing Season

(KMS) starts in October. Paddy is a major Kharif (summer-sown) crop but it is also

grown in rabi (winter-sown) season.

Govt buys paddy worth Rs 1.26 lakh crore at MSP so far this kharif marketing

season

IFFCO announces “no hike” in DAP & NPK fertilizers rates

In a major move aimed at giving relief to the farmers, IFFCO announced that they

have decided not to increase the price of its DAP, NPK & NPS fertilizers, no matter

what the input cost be. Being a leader in the fertilizer price stabilization in the

country, the move is being heralded as yet another example of cooperative’s

commitment to farmers. The announcement was made on Tuesday.

IFFCO announces “no hike” in DAP & NPK fertilizers rates

UPL Announces Long-Term Collaboration With FMC Corporation for Rynaxypyr®

Active Ingredient. UPL Ltd. today announced a long-term strategic collaboration with

FMC Corporation, a leading global agricultural sciences company. The agreement

provides UPL access in key markets prior to patent expiration, to commercialize

Rynaxypyr" active, FMC's leading insecticide. As per the agreement, UPL will toll

manufacture and supply Rynaxypyr to FMC in India, and FMC will supply the active

ingredient to UPL depending on the markets.

UPL Announces Long-Term Collaboration With FMC Corporation for Rynaxypyr®

Active Ingredient

F

FARM FACTS

Edelweiss Securities Limited

10 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

Valuation of Agri-input players

EPS CAGR

Company Rating Target Multiple

FY21E

EPS

(FY19-21E)

(%) FY20 FY21E FY22E FY20 FY21E FY22E FY20 FY21E FY22E

Agri Inputs - Agrochemicals

PI Industries Hold 2,268 2,270 35x Jun23 EPS 4,729 342 50.6 30.5 68.7 44.8 36.4 38.2 31.7 25.8 18.6 23.8 23.6

Rallis India Hold 278 293 22x FY22 EPS 742 54 11.7 21.1 31.3 23.8 20.9 23.0 15.8 13.7 12.8 15.8 15.7

Dhanuka Agritech Buy 746 1,137 24x FY22 EPS 477 34 45.3 38.4 25.1 16.5 15.7 24.1 13.4 12.4 20.9 27.1 23.8

UPL Buy 615 655 8.5x Jun23 EBITDA 6,462 467 43.1 21.4 26.5 14.3 12.0 7.2 6.4 5.4 15.5 18.5 18.5

Sharda Cropchem Hold 331 337 14x FY22 EPS 411 30 24.4 11.7 18.1 13.6 13.7 8.4 5.1 4.6 12.3 14.8 13.0

Mean 24.6 34.0 22.6 19.8 20.2 14.5 12.4 16.0 20.0 18.9

Median 21.4 26.5 16.5 15.7 23.0 13.4 12.4 15.5 18.5 18.5

Agri Inputs - Fertilisers

Coromandel International Buy 786 1,004 19x FY22 EPS 3,167 229 48.9 40.9 21.6 16.1 14.9 14.5 10.2 9.2 27.7 29.0 24.7

CMP

(INR)

Mcap

(INR bn)

Target

Price

Mcap

(USD mn)

RoE (%)EV/EBITDAP/E

Edelweiss Securities Limited

FARM FACTS

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 11

DISCLAIMER Edelweiss Securities Limited (“ESL” or “Research Entity”) is regulated by the Securities and Exchange Board of India (“SEBI”) and is licensed to carry on the business of broking, depository services and related activities. The business of ESL and its Associates (list available on www.edelweissfin.com) are organized around five broad business groups – Credit including Housing and SME Finance, Commodities, Financial Markets, Asset Management and Life Insurance.

This Report has been prepared by Edelweiss Securities Limited in the capacity of a Research Analyst having SEBI Registration No.INH200000121 and distributed as per SEBI (Research Analysts) Regulations 2014. This report does not constitute an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. Securities as defined in clause (h) of section 2 of the Securities Contracts (Regulation) Act, 1956 includes Financial Instruments and Currency Derivatives. The information contained herein is from publicly available data or other sources believed to be reliable. This report is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. The user assumes the entire risk of any use made of this information. Each recipient of this report should make such investigation as it deems necessary to arrive at an independent evaluation of an investment in Securities referred to in this document (including the merits and risks involved), and should consult his own advisors to determine the merits and risks of such investment. The investment discussed or views expressed may not be suitable for all investors.

This information is strictly confidential and is being furnished to you solely for your information. This information should not be reproduced or redistributed or passed on directly or indirectly in any form to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ESL and associates / group companies to any registration or licensing requirements within such jurisdiction. The distribution of this report in certain jurisdictions may be restricted by law, and persons in whose possession this report comes, should observe, any such restrictions. The information given in this report is as of the date of this report and there can be no assurance that future results or events will be consistent with this information. This information is subject to change without any prior notice. ESL reserves the right to make modifications and alterations to this statement as may be required from time to time. ESL or any of its associates / group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. ESL is committed to providing independent and transparent recommendation to its clients. Neither ESL nor any of its associates, group companies, directors, employees, agents or representatives shall be liable for any damages whether direct, indirect, special or consequential including loss of revenue or lost profits that may arise from or in connection with the use of the information. Our proprietary trading and investment businesses may make investment decisions that are inconsistent with the recommendations expressed herein. Past performance is not necessarily a guide to future performance .The disclosures of interest statements incorporated in this report are provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. The information provided in these reports remains, unless otherwise stated, the copyright of ESL. All layout, design, original artwork, concepts and other Intellectual Properties, remains the property and copyright of ESL and may not be used in any form or for any purpose whatsoever by any party without the express written permission of the copyright holders.

ESL shall not be liable for any delay or any other interruption which may occur in presenting the data due to any reason including network (Internet) reasons or snags in the system, break down of the system or any other equipment, server breakdown, maintenance shutdown, breakdown of communication services or inability of the ESL to present the data. In no event shall ESL be liable for any damages, including without limitation direct or indirect, special, incidental, or consequential damages, losses or expenses arising in connection with the data presented by the ESL through this report.

We offer our research services to clients as well as our prospects. Though this report is disseminated to all the customers simultaneously, not all customers may receive this report at the same time. We will not treat recipients as customers by virtue of their receiving this report.

ESL and its associates, officer, directors, and employees, research analyst (including relatives) worldwide may: (a) from time to time, have long or short positions in, and buy or sell the

Securities, mentioned herein or (b) be engaged in any other transaction involving such Securities and earn brokerage or other compensation or act as a market maker in the financial

instruments of the subject company/company(ies) discussed herein or act as advisor or lender/borrower to such company(ies) or have other potential/material conflict of interest with

respect to any recommendation and related information and opinions at the time of publication of research report or at the time of public appearance. ESL may have proprietary long/short

position in the above mentioned scrip(s) and therefore should be considered as interested. The views provided herein are general in nature and do not consider risk appetite or investment

objective of any particular investor; readers are requested to take independent professional advice before investing. This should not be construed as invitation or solicitation to do business

with ESL.

ESL or its associates may have received compensation from the subject company in the past 12 months. ESL or its associates may have managed or co-managed public offering of securities for the subject company in the past 12 months. ESL or its associates may have received compensation for investment banking or merchant banking or brokerage services from the subject company in the past 12 months. ESL or its associates may have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past 12 months. ESL or its associates have not received any compensation or other benefits from the Subject Company or third party in connection with the research report. Research analyst or his/her relative or ESL’s associates may have financial interest in the subject company. ESL and/or its Group Companies, their Directors, affiliates and/or employees may have interests/ positions, financial or otherwise in the Securities/Currencies and other investment products mentioned in this report. ESL, its associates, research analyst and his/her relative may have other potential/material conflict of interest with respect to any recommendation and related information and opinions at the time of publication of research report or at the time of public appearance.

Participants in foreign exchange transactions may incur risks arising from several factors, including the following: ( i) exchange rates can be volatile and are subject to large fluctuations; ( ii) the value of currencies may be affected by numerous market factors, including world and national economic, political and regulatory events, events in equity and debt markets and changes in interest rates; and (iii) currencies may be subject to devaluation or government imposed exchange controls which could affect the value of the currency. Investors in securities such as ADRs and Currency Derivatives, whose values are affected by the currency of an underlying security, effectively assume currency risk.

Research analyst has served as an officer, director or employee of subject Company: No

ESL has financial interest in the subject companies: No

ESL’s Associates may have actual / beneficial ownership of 1% or more securities of the subject company at the end of the month immediately preceding the date of publication of research report.

Research analyst or his/her relative has actual/beneficial ownership of 1% or more securities of the subject company at the end of the month immediately preceding the date of publication of research report: No

ESL has actual/beneficial ownership of 1% or more securities of the subject company at the end of the month immediately preceding the date of publication of research report: No

Subject company may have been client during twelve months preceding the date of distribution of the research report.

There were no instances of non-compliance by ESL on any matter related to the capital markets, resulting in significant and material disciplinary action during the last three years except that ESL had submitted an offer of settlement with Securities and Exchange commission, USA (SEC) and the same has been accepted by SEC without admitting or denying the findings in relation to their charges of non registration as a broker dealer.

A graph of daily closing prices of the securities is also available at www.nseindia.com

Analyst Certification:

The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report.

F

FARM FACTS

Edelweiss Securities Limited

12 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

Additional Disclaimers

Disclaimer for U.S. Persons

This research report is a product of Edelweiss Securities Limited, which is the employer of the research analyst(s) who has prepared the research report. The research analyst(s) preparing the research report is/are resident outside the United States (U.S.) and are not associated persons of any U.S. regulated broker-dealer and therefore the analyst(s) is/are not subject to supervision by a U.S. broker-dealer, and is/are not required to satisfy the regulatory licensing requirements of FINRA or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject company, public appearances and trading securities held by a research analyst account.

This report is intended for distribution by Edelweiss Securities Limited only to "Major Institutional Investors" as defined by Rule 15a-6(b)(4) of the U.S. Securities and Exchange Act, 1934 (the Exchange Act) and interpretations thereof by U.S. Securities and Exchange Commission (SEC) in reliance on Rule 15a 6(a)(2). If the recipient of this report is not a Major Institutional Investor as specified above, then it should not act upon this report and return the same to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any U.S. person, which is not the Major Institutional Investor.

In reliance on the exemption from registration provided by Rule 15a-6 of the Exchange Act and interpretations thereof by the SEC in order to conduct certain business with Major Institutional Investors, Edelweiss Securities Limited has entered into an agreement with a U.S. registered broker-dealer, Edelweiss Financial Services Inc. ("EFSI"). Transactions in securities discussed in this research report should be effected through Edelweiss Financial Services Inc.

Disclaimer for U.K. Persons

The contents of this research report have not been approved by an authorised person within the meaning of the Financial Services and Markets Act 2000 ("FSMA"). In the United Kingdom, this research report is being distributed only to and is directed only at (a) persons who have professional experience in matters relating to investments falling within Article 19(5) of the FSMA (Financial Promotion) Order 2005 (the “Order”); (b) persons falling within Article 49(2)(a) to (d) of the Order (including high net worth companies and unincorporated associations); and (c) any other persons to whom it may otherwise lawfully be communicated (all such persons together being referred to as “relevant persons”). This research report must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this research report relates is available only to relevant persons and will be engaged in only with relevant persons. Any person who is not a relevant person should not act or rely on this research report or any of its contents. This research report must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person. Disclaimer for Canadian Persons

This research report is a product of Edelweiss Securities Limited ("ESL"), which is the employer of the research analysts who have prepared the research report. The research analysts preparing the research report are resident outside the Canada and are not associated persons of any Canadian registered adviser and/or dealer and, therefore, the analysts are not subject to supervision by a Canadian registered adviser and/or dealer, and are not required to satisfy the regulatory licensing requirements of the Ontario Securities Commission, other Canadian provincial securities regulators, the Investment Industry Regulatory Organization of Canada and are not required to otherwise comply with Canadian rules or regulations regarding, among other things, the research analysts' business or relationship with a subject company or trading of securities by a research analyst.

This report is intended for distribution by ESL only to "Permitted Clients" (as defined in National Instrument 31-103 ("NI 31-103")) who are resident in the Province of Ontario, Canada (an "Ontario Permitted Client"). If the recipient of this report is not an Ontario Permitted Client, as specified above, then the recipient should not act upon this report and should return the report to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any Canadian person.

ESL is relying on an exemption from the adviser and/or dealer registration requirements under NI 31-103 available to certain international advisers and/or dealers. Please be advised that (i) ESL is not registered in the Province of Ontario to trade in securities nor is it registered in the Province of Ontario to provide advice with respect to securities; (ii) ESL's head office or principal place of business is located in India; (iii) all or substantially all of ESL's assets may be situated outside of Canada; (iv) there may be difficulty enforcing legal rights against ESL because of the above; and (v) the name and address of the ESL's agent for service of process in the Province of Ontario is: Bamac Services Inc., 181 Bay Street, Suite 2100, Toronto, Ontario M5J 2T3 Canada.

Disclaimer for Singapore Persons

In Singapore, this report is being distributed by Edelweiss Investment Advisors Private Limited ("EIAPL") (Co. Reg. No. 201016306H) which is a holder of a capital markets services license and an exempt financial adviser in Singapore and (ii) solely to persons who qualify as "institutional investors" or "accredited investors" as defined in section 4A(1) of the Securities and Futures Act, Chapter 289 of Singapore ("the SFA"). Pursuant to regulations 33, 34, 35 and 36 of the Financial Advisers Regulations ("FAR"), sections 25, 27 and 36 of the Financial Advisers Act, Chapter 110 of Singapore shall not apply to EIAPL when providing any financial advisory services to an accredited investor (as defined in regulation 36 of the FAR. Persons in Singapore should contact EIAPL in respect of any matter arising from, or in connection with this publication/communication. This report is not suitable for private investors.

Disclaimer for Hong Kong persons

This report is distributed in Hong Kong by Edelweiss Securities (Hong Kong) Private Limited (ESHK), a licensed corporation (BOM -874) licensed and regulated by the Hong Kong Securities and Futures Commission (SFC) pursuant to Section 116(1) of the Securities and Futures Ordinance “SFO”. This report is intended for distribution only to “Professional Investors” as defined in Part I of Schedule 1 to SFO. Any investment or investment activity to which this document relates is only available to professional investor and will be engaged only with professional investors.” Nothing here is an offer or solicitation of these securities, products and services in any jurisdiction where their offer or sale is not qualified or exempt from registration. The report also does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of any individual recipients. The Indian Analyst(s) who compile this report is/are not located in Hong Kong and is/are not licensed to carry on regulated activities in Hong Kong and does not / do not hold themselves out as being able to do so. Copyright 2009 Edelweiss Research (Edelweiss Securities Ltd). All rights reserved.

Aditya Narain

Head of Research

![Edelweiss [1]](https://img.pdfslide.us/doc/110x75/577d29e11a28ab4e1ea8224e/edelweiss-1.jpg)