Embed Size (px)

Citation preview

ContentsWelcome 3

Australian high-density residential development 4

Lower rates, longer cycle 6

Weathering the storm 8

A perfect storm brewing 10

Builders put on notice by the regulator 12

Steps to consider when using insolvency Safe Harbour 14

Build to Rent – a compelling opportunity 16

2Property of Pitcher Partners August 2019

WelcomeAndrew Beitz Pitcher Partners, Adelaide [email protected]

At Pitcher Partners we have a passion for the property industry.We are attuned to the needs of all contributors in this complex and exciting sector – owners, developers, investors, builders, valuers, agents and of course debt/equity participants. We have a well-established and proven track record in contributing to our clients’ success based on our extensive knowledge and our intimate approach to servicing our clients.In this issue, Knight Frank takes a look at Australian high-density residential development and provides an update on the commercial property sector and the impact of the lower interest rates and slowing capital growth.

Damian Pearce, Pitcher Partners Melbourne, looks at weathering the storm and preparing for blue sky in the property development sector and preparing your business for what lies ahead.

Across in Perth, Mark Clapham from Sheffield Property shares an update on how the Perth CBD and West Perth office leasing market is recovering from the major correction that it experienced in concert with the resource downturn of 2012.

Michael Basedow, Pitcher Partners Adelaide, looks at what Safe Harbour is and the steps to consider when using insolvency safe harbour after an influx of failed builders in South Australia.

Cole Wilkinson, Pitcher Partners Brisbane shares what regulators have recently released in regards to new regulations to try and stem the steady flow of Queensland builders going under.

Finally, Brendan Jones of Pitcher Partners Sydney looks at the Build to Rent opportunity defined as multi-unit residential developments that are designed and built as long-term rental housing under a single ownership entity.

We welcome your feedback – if you have any suggestions on articles you would like us to cover in future editions please send them through to [email protected]

3 Property of Pitcher Partners August 2019

Australian high-density residential development

Michelle CiesielskiDirector Residential Research, Knight Frank [email protected]

In years gone by, grasping the performance of the Australian residential development market required three updates – the last direction of the cash rate, how much money was being borrowed to purchase residential property and the movement in the number of new residential buildings being approved. Today, the dialogue is much more complicated, and these indicators only start to scratch the surface. While the banking sector has achieved the Australian Prudential Regulation Authority (APRA) objective of cooling the residential market by creating a stricter lending environment for investors and owner occupiers, they also continue to tighten lending to developers.

This has caused many projects to be pushed back or change to an alternative use. Over the past year, this has been aided with a historic low office vacancy environment in both Sydney and Melbourne, in addition to increased competition from the hotel and student accommodation sectors.

There is no denying there has been elevated apartment stock in major Australian cities over past years, but this has also been met with reasonably strong underlying fundamentals and significant population growth.

By Knight Frank definition, high-density apartments cover projects with more than 25 apartments in a complex and more than four storeys in height. From 2015 to 2018, close to 195,650 new apartments were added to the five major cities’ apartment stock, led by Greater Sydney (90,200) and Greater Melbourne (57,700).

Knight Frank – Residential

4Property of Pitcher Partners August 2019

In total, across the five cities, there are currently 105,300 apartments under construction, with another 36,800 currently being marketed and potentially due for completion by the end of 2022. The diminishing likelihood of an additional 63,550 development approved apartments coming on line within this timeframe are continually being revised.

To arrive at this pipeline an allowance has been made to deduct the 33,100 apartments which had once launched with marketing campaigns, but now on-hold. There is a low chance these projects will come back to market and be completed by the end of 2022, given the stricter funding environment and a cooler off-the-plan new apartment market.

With these projects delaying their launch, or being removed from the pipeline altogether, most cities are positioned to absorb not only recently completed projects, but those currently under construction by 2022. There is the increasing chance many apartment markets may well be undersupplied by this time.

Major development sites suitable for high-density across Australia totalled $3.7 billion in 2018. As the market continues to correct across the major cities, the 2018 volume was 40% lower than the previous year, and less than half the volume of sales achieved in 2014.

NSW recorded the greatest volume of high-density site sales in Australia with $2.2 billion (59% of the total volume), followed by Victoria ($890 million), Queensland ($508 million) and WA ($96 million).

The average value for a high-density site across Australia was $86,200/per apartment (excluding the CBDs across the cities) – ranging significantly from an indicative $40,000/per apartment in Greater Adelaide, to an indicative $198,300/per apartment in Greater Sydney at the end of 2018.

Greater Melbourne achieved an indicative rate of $120,400/per apartment while Greater Perth and Greater Brisbane recorded $50,700/sqm and $40,300/sqm respectively. Outside the major capital cities, Canberra and Greater Hobart achieved the highest indicative values for high-density sites at $90,000/per apartment, followed by the Gold Coast ($71,700/per apartment) and Greater Darwin ($60,000/per apartment).

The price of a new standard mainstream apartment (with two-bedrooms and two-bathrooms) averaged $8,200/sqm across Australian cities at the end of 2018. Starting from an indicative $5,500/sqm in Greater Darwin, to $9,600/sqm in Greater Melbourne; through to $13,700/sqm in Greater Sydney.

Other cities stretched between $7,000/sqm (Greater Adelaide) and $7,800/sqm (Gold Coast); with Greater Brisbane recording $7,400/sqm, Greater Hobart ($7,500/sqm), Greater Perth ($7,700/sqm) and Canberra ($7,750/sqm).

Over the coming year the residential rental vacancy rate, last recorded at 2.6% in December 2018, will be closely monitored for signs of oversupply across the major cities of Australia.

Vacancy in Greater Sydney has recently trended above 3%, although this has not yet been witnessed in Greater Melbourne. The stand-out city has been Greater Perth with 2.8% vacancy recorded at the end of 2018 – falling from the recent ceiling of 7.6% in July 2017.

KnightFrank.com.au/research Latest content in the palm of your hand

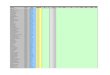

Site Sale and New Apartment Indicative Price Rates, Major Australian CitiesSites based on potential high-density development (excel. CBD) and new apartments based on standard mainstream 2bed+2bath, as at 31 Dec 2018

$15,000

$12,500

$10,000

$7,500

$5,000

For consistency across the cities, the site sales average rate/per apartment is calculated as the purchase price divided by the potential number of apartments, at the time of sale. Note: the Gold Coast new apartment rate is based on GFA.

Source: Frank Knight Research

$25,000 $50,000 $75,000 $100,000 $125,000 $150,000 $175,000 $200,000

Indicative sale price (rate/per apartment)

Indi

cativ

e ne

w a

part

men

t pric

e

(rat

e/pe

r apa

rtm

ent)

Adelaide

Brisbane

Perth

Darwin

Gold Coast

Hobart

Canberra

Melbourne

Sydney

5 Property of Pitcher Partners August 2019

Knight Frank – Commercial

Lower rates, longer cycleChris NaughtinAssociate Director Research & Consulting, Knight Frank [email protected]

Market interest rates in Australia have declined dramatically in recent months as the RBA eases monetary policy in response to the softening economic outlook. Lower interest rates will provide support to commercial property valuations at a time when capital growth is slowing and may lead to further yield compression in some markets, prolonging the property price cycle.

Capital growth moderating from elevated levelsAfter several years of strong growth in commercial property valuations, capital growth has eased since mid-2018. Capital growth, as measured by the MSCI All Property Index, slowed to 3.9% year-on-year in the March quarter 2019, from 4.6% in the December quarter 2018 and 5.5% a year ago. Capital growth for office and industrial property has moderated but remains high at 7.2% and 7.4% respectively, while the retail sector continues to struggle with subdued consumer spending and structural challenges.

Sharp downward shift in interest rates to underpin low property yields The easing in capital growth coincides with a pronounced shift to lower interest rates. Further easing by the RBA, and signals by major central banks that more accommodative policy is likely in the near future, have seen rates in short-term money markets and long-term bond yields decline dramatically. For example, yields on 10-year Australian government bonds have declined from 2.6% 12 months ago to an historic low of 1.3%, while yields on 10-year US Treasuries have fallen from 2.9% to 2% over the same period.

The change in the interest rate environment will boost demand for commercial property at a time when record low yields on some commercial property assets such as prime office property in Sydney and Melbourne have caused many to question how long the current cycle of yield compression has to run. There are several channels through which lower interest rates will support demand for commercial property assets:

Relative value: While commercial property yields are historically low, the spread between property and bond yields has widened significantly. For instance, the spread between the Sydney CBD prime office property yield and the 10-year Australian Government bond yield increased from 1.9% in the December quarter 2018 to 2.8% in the March quarter 2019.

Lower exchange rate: Lower interest rates have seen the Australian dollar depreciate against the US dollar and other major currencies, increasing the attractiveness of investment in Australia. Policy easing from other central banks, if implemented, will likely temper any further depreciation of the Australian dollar.

Reduced hedging costs: For cross-border investors, interest rate differentials between Australia and the source country play an important role in determining hedging costs. Historically, interest rates have tended to be higher in Australia than in the domicile of major cross border investors such as the US, Canada, Hong Kong and Singapore, but the recent sharp fall interest rates in Australia has reversed this dynamic, lowering hedging costs.

Lower funding costs: Lower interest rates, both in Australia and overseas, will lower funding costs for leveraged investors.

Lower interest rates will underpin demand for commercial property assets as investors continue to search for higher-yielding assets with a fixed income return component. And if favourable leasing market conditions continue, this may drive yields to even lower levels in some markets and result in a longer asset price cycle than previously anticipated.

KnightFrank.com.au/research Latest content in the palm of your hand

6Property of Pitcher Partners August 2019

Commercial property returnsTotal return, per cent change year-on-year

12

10

8

6

4

2

0

Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019

Source: MSCI

Income return

Capital return

10-year bond yieldsPer cent

3.5 0.4

3.0 0.2

2.5 0

2.0 -0.2

1.5 -0.4

1.0 -0.6

0.5 -0.8

0 -1.0

Source: Macrobond

Spread (RHS)

United States (LHS)

Australia (LHS)

JAN 2018 APR 2018 JUL 2018 OCT 2018 JAN 2019 APR 2019 JUL 2019 OCT 2019

7 Property of Pitcher Partners August 2019

Weathering the stormDamian PearceClient Director, Pitcher Partners Melbourne [email protected]

Weathering the storm and preparing for blue sky in the property development sector – preparing your business for what lies ahead. It seems there isn’t a day that passes without the media reporting on the troubles besetting the property development sector and in particular high density apartment developments. Right now the future seems more uncertain for the industry than it has been in the past, and the impact and length of changing construction cycles still tends to be underestimated. Earlier in the decade the sector kept liquidators busy in the 2012 and 2013 years as the post Global Financial Crisis stimulus launched by the Rudd-Gillard governments unwound.

It’s the grinding cyclical lag that can eventually catch up with those poorly prepared. During this period, struggling businesses, particularly builders, can encounter risks such as creditor recovery action. The ATO is proficient in winding up companies and using specific recovery powers at its disposal, and banks can get nervous. The use of bank guarantees is common to secure contracts and managing bank relationships can be uncomfortable.

Unscrupulous predatory advisors can contact vulnerable business owners and tell them what they want to hear. All too often they recommend transferring the assets, business and contracts to another company, leaving unpaid creditors wallowing in the previous shell with little hope of payment. This is known as a form of phoenixing and the construction sector has a poor reputation for this practice.

If failure ultimately occurs, builder liquidations leave directors particularly vulnerable to large personal insolvent trading claims. Combined with personal guarantees, director bankruptcy is common.

For the developer, contract clauses commonly allow them to terminate upon the liquidation of a builder (referred to as ipso facto clauses) which triggers a process of valuing unpaid works that is then combined with the bank guarantee to set-off against losses. Despite these protections, often the costs of a new builder, legal fees, interest and site security (among other costs) often leave projects in the red for the developer.

Greater support in avoiding business failure in 2019The encouraging news is that 2019 sees a different environment to previous cycles, with a combination of factors making it more encouraging for companies and directors to be proactive in avoiding collapse. Of particular note is that the legislation, banking and ATO environment is more aligned than ever in supporting robust informal workout plans to avoid business failure.

Firstly, banks have shown a willingness to work with customers in executing such plans, particularly where a reputable advisor is involved.

Secondly, the ATO is increasingly more sophisticated in conducting its due diligence in deciding and agreeing to repayment arrangements. Similarly to the banks, the ATO takes comfort where suitably qualified advisors are assisting the taxpayer in ensuring effective financial reporting and corporate governance is in place.

Thirdly, changes made to insolvency laws have been made to encourage business recovery. These include:

• For any contract commenced since 1 July 2018, the use of ipso facto clauses to terminate contracts is restricted.

• New Safe Harbour provisions provide protection to directors from insolvent trading claims where a course of action is taken that is reasonably likely to result in a better outcome than immediate liquidation or administration. Safe Harbour is not a formal insolvency process, such as liquidation, and therefore avoids (mostly) the very public process that can irreparably damage businesses.

To be effective, Safe Harbour requires prudent steps to be taken including lodging tax and BAS returns, paying employee entitlements on time and appointing an appropriately qualified entity or advisor.

Melbourne

8Property of Pitcher Partners August 2019

The path leading away from business failure is always differentIn general, every business experiences different problems and these require different solutions. At one end of the scale, some will need to take immediate steps to improve efficiencies and rationalise resources. Adopting these strategies will require time and could simply involve the cash flow assistance of negotiating temporarily relaxed payment terms with creditors.

Heading towards the other end of the scale, directors may need to downsize their operations and navigate the cost and time burdens to achieve this including redundancies, sub-leasing space and asset sales.

In both scenarios, seeking advice and acting early is crucial. When developing a plan, it should be articulated in writing and the barriers to success realistically addressed. Explaining the plan to someone impartial and trusted will help to determine what outcome is realistic. The time afforded by Safe Harbour can be used to coordinate the steps addressing cashflow needs and maintaining communication with stakeholders.

Preparing for the opportunities presented by a reboundThe following are some additional housekeeping steps to consider taking, regardless of the current position of any business in the property sector:

• Ensure bank guarantees for completed projects are returned in line with the contract.

• Carrying out your own ASIC searches on contractors can provide useful warning signs such as wind-up applications or company name changes (a common sign of phoenix activity). Wind-up documents are required to be served on the ASIC registered address of a company, as are ATO director penalty notices. Ensure these addresses are current for your companies. A Personal Properties Securities Register (PPSR) search can identify the extent businesses are engaging new suppliers and potentially not paying previous ones.

• Check your businesses’ recent financial statements and accounting records and note the existence of related party loan accounts. If an insolvency administration appointment occurs, loans owing between related parties can cause a cascading collapse.

• Review your current business structures and finance to consider:

– Are your risks and wealth adequately separated?

– Who are the directors of each company? – Which entities or individuals have provided security or guarantees to support loans?

– How can funds be accessed should cashflow become tight?

The above represents some of the broader issues being faced by distressed businesses and some mitigating actions. In reality, all of these steps should be taken by a business owner and will be beneficial in the case of a growing business. If there is one thing the GFC taught us is that recovery can be swift and those prepared for the rebound can take advantage of some fantastic opportunities.

9 Property of Pitcher Partners August 2019

A perfect storm brewing Mark ClaphamJoint Managing Director, Sheffield Property [email protected]

The Perth CBD and West Perth office leasing market is recovering quickly from the major correction that it experienced in concert with the resource downturn of 2012. Perth’s white-collar work force has reduced significantly in the period since its 2012 peak due to major mining, oil and gas projects moving from the construction to operation phase and the rapid decline in commodity prices causing some companies to cease operations. These events have led to a rapid decline in the need for office space. There was also a concurrent wave of newly built commercial office buildings which reached completion of construction at the same time with the mining downturn. The result a major oversupply in office space resulting in vacancies of circa 30%, a major discount of market rents and net incentives reached 30-year highs.

Since then, the CBD office market vacancies have dropped to approximately 18.5% in the CBD and 14.8% in West Perth earlier this year.

Nothing ever stays the same and the only consistent variable in any market is change, a perfect storm is again brewing for the Perth office market.

The largest vacancies in the Perth CBD office market over the last 12 months have been at Kings Square 1, the Quadrant at 1 William Street and 240 St Georges Terrace, all of which are now all now largely fully leased. These three buildings concluded around 75,000sqm of new leasing transactions over the last 12 months. The result of which has left the market with less than a handful of contiguous vacant floors available for lease in Prime grade office buildings.

An office tenant seeking 3,000 sqm or more of Premium or A Grade office space is now largely limited to either staying put at their existing premises and waiting for the next development cycle, or they could consider downgrading to lower A Grade and B grade office space where the vacancies still remain high at around 30%.

Perth

10Property of Pitcher Partners August 2019

Where have all the office tenants come from that have created this change?Growth in the Engineering Services SectorA key occupier of space in Perth CBD and West Perth that service the Mining, Oil & Gas sectors is the Engineering Services sector. This sector typically occupies about 30% of the total Perth CBD and CBD Fringe office markets.

The engineering services sector acts as the bellows for the vacancy levels across Perth the office market. As the mining sector continues to improve and the oil and gas sector starts to bounce back so does the demand for office space from this sector. Large mining services contracts continue to be awarded to engineering firms on what seems to be almost on a daily basis.

Since the mining downturn in 2011 /2012, the engineering sector has undergone a major structural change, its overall occupancy footprint in the CBD reduced by around 70% over the course of 2012 to 2015. This has subsequently stabilised, the sector has grown and expanded back to 60% of the office space it previously occupied in 2012.

Tenants Migrating from the SuburbsMigrating suburban tenants have been a key contributor to falling office vacancies in the CBD & Northbridge.

Tenants have migrated from lesser quality office buildings in suburban locations, to take advantage of exceptional value lease deals in the city, and to secure an amenity, locational and building quality upgrade, all of which the CBD offers.

Looking at the letting up profile of the three largest vacancies in the Perth CBD market over the past 12 to 18 months being 240 St Georges Terrace (Circa 40,000 sqm), Kings Square 1, (Circa 21,000 sqm) and The Quadrant at 1 William Street (13,000 sqm). 240 St Georges Terrace leased circa 20% of its total vacant space to migrating suburban tenants, Kings Square 1 leased 100% of the total vacant space to migrating suburban tenants and The Quadrant at 1 William Street leased 90% of its the total vacancy to migrating suburban and CBD fringe tenants.

Flight to Quality of CBD TenantsExisting CBD office tenants took advantage of the high levels of lease incentives and reduced rentals as they made the flight to quality within the CBD from A & B Grade buildings to the Premium and A-Grade buildings.

No New SupplyThere are no new office developments of significance that are presently under construction within the Perth CBD, West Perth, East Perth or Northbridge. Given it takes somewhere between 2 to 3 years to build a new office building dependent upon its size, this provide a natural lid on vacancy levels for the next 2 to 3 years.

The only new office development about to commence construction which will have any residual vacancy to offer the market within in the Perth CBD will be the new Premium Grade Headquarters for Chevron at Elizabeth Quay, totaling approximately 50,000sqm in size of which approximately 8,000 sqm remains uncommitted. This building will be due for completion in 2023.

The lack of new supply, migrating suburban tenants, an expanding Engineering Services Sector, coupled with the flight to quality pressure created by existing CBD office tenants are all putting pressure on CBD office vacancies and rents, creating a perfect storm for rising rents and falling incentives readying the market for the next cycle of office development.

11 Property of Pitcher Partners August 2019

Steps to consider when using insolvency Safe HarbourMichael BasedowPrincipal, Pitcher Partners [email protected]

In just the last 12 months, eight South Australian residential builders have gone into Liquidation in an industry that has slowed in recent years.A number of those failures can be put down to poor management practices and a South Australian trade pool that is rapidly decreasing which, in turn, is putting pressure on quality and price.

The outcome of this activity is that once these inefficiencies of the property industry’s poor performances became structurally embedded, they would be very hard to remove down the track.

The implications of not achieving a systemic turnaround of the industry’s poor performance and effectiveness will impact South Australia’s (and Australia’s) competitiveness in all the sectors that are dependent on a better-performing, competent construction industry.

The industry is now coming under increasing competitive pressure, affecting the retention of existing jobs and the creation of new ones.

It is to that background that we should consider the signs to look for, and remedies of, an industry under pressure.

Some of the obvious signs of impending insolvency may include: • constant calls from creditors• inability to pay bills on time• increasing ATO liabilities or failed tax payment

arrangements• consistent injections of personal money into

the company • bank facilities at their limits or defaults on

bank facilities • the company is reporting continual losses• decreasing turnover or loss of a major customer• failure to prepare budgets and monitor financial

performance

There are however some actions that companies can take to protect themselves from insolvent trading (trading whilst unable to pay debts), but unfortunately business owners leave it too late to seek advice and the damage has been done.

What is Safe Harbour? Safe Harbour provisions are, if successful, protection from insolvent trading. To be successful requires a ‘course of action’ – that is ‘reasonably likely’ – to lead to a ‘better outcome’, that is better than immediate liquidation/administration.

Safe harbour provisions are not:• a formal insolvency process• public (with a few exceptions) • binding on the ATO or other key creditors• binding on developers

Adelaide

12Property of Pitcher Partners August 2019

Steps to consider when using insolvency Safe Harbour:

Employee entitlements

Check that any outstanding employee entitlements are paid,

and that the company will be able to continue to pay employee entitlements when they are due.

Tax reporting obligations

Check that the company is meeting all its tax reporting obligations,

and ensure that systems are put in place to enable the company to

continue meeting these obligations.

Misconduct

Check that there are no outstanding issues relating to misconduct of employees and officers. Ensure employees are

complying with company policies and misconduct is identified and

dealt with appropriately.

Insurance and indemnityCheck existing policies are up-to-date and adequate.

Restructuring planDevelop a comprehensive

restructuring plan by a restructuring specialist and implement the plan.

Company debtConsider whether each new debt incurred is necessary in achieving the objectives of a plan, and that

the plan remains reasonably likely to achieve a better outcome than

the immediate appointment of an administrator or liquidator.

This is an ongoing consideration and would benefit from the

regular advice of an appropriately qualified entity (ideally, but not strictly, an insolvency expert).

Where to from here?

When owning or running a business, it can sometimes be difficult to find the time to take a step back and look at how you and your business are performing. Taking some time now to do this can save you a lot of time and heartache in the future.

13 Property of Pitcher Partners August 2019

Builders put on notice by the regulator Cole WilkinsonPartner, Pitcher Partners Brisbane [email protected]

Brisbane

Following on from changes made by the Queensland Building and Construction Commission (QBCC) in February 2018, the regulator has recently released some new regulations to try and stem the steady flow of Queensland builders going under. Some might argue the failure of some builders may have been brought forward by QBCC review and subsequent revocation of their building licence for not meeting the minimum financial requirements. The new Minimum Financial Requirements Regulation commenced on 1 January 2019 requiring QBCC licensees who hold a contractor grade licence to meet new annual financial reporting obligations. To facilitate the simple and streamlined submission of financial information eliminating the requirement to file manual submissions or emails, QBCC has launched a new online portal, ‘myQBCC’ and requires all licensees or their nominated representative to report annually to the QBCC via this portal. This now allows the QBCC to assess licensee’s financial information in real time rather than the significant time lag that occurred with manual submissions.

What is required and when?The information required will depend on the licensees’ financial category at the time of submission. For those companies whose revenue exceeds $30 million, they were required by 31 March 2019 to provide their detailed financial information for the year ended 30 June 2018 via the QBCC portal along with a full copy of their financial statements. In addition, companies are required to provide detailed information on the company’s debtors and creditors along with a completed and signed written declaration verifying the information contained in your financial statements is correct and represents a true and fair view of the financial position.

What we have seen so far is the QBCC taking swift action against high profile construction companies such as Laing O’Rourke and suspending their licence shortly after the financial information is submitted. These companies have managed to restructure their affairs to meet the requirements of the QBCC and have their licenses reinstated within a few days. However this is not before having to deal with the disruption to building programs and general business, as well as the well publicised breaches no doubt causing damage to the business’ reputation in the marketplace.

The next critical date that we will see under these regulations is the 31 December 2019 due date for reporting of financial information for the year ended 30 June 2019 by all licensees. Similarly, licensees will be required to declare that their financial information has been prepared in accordance with Australian Accounting Standards which may be different to the way many private companies prepare their accounts currently. Further the information lodged by 31 December 2019 will be in respect of the year end 30 June 2019, so careful planning and action pre 30 June 2019 may be required.

What does this mean for you?In a practical sense, what does this all mean for businesses engaged in the property and construction sector in Brisbane? We feel that there a two main risk areas that should be considered here:

If you are a current licensee Ensure you are well prepared for the new reporting requirements prior to 31 December 2019. This is earlier than many companies would have prepared their financial reports and the new regime requires stricter compliance with accounting standards. We recommend that businesses review their financial position as soon as possible so that if a restructure of the business is required, this can be done prior to the reporting deadline rather than waiting for their licence to be suspended.

If you are a developer or head contractor engaging licensed contractorsThere is a risk that contractors you engage could have their licence suspended post 31 December 2019 if they don’t meet the requirements of their licence. It may be prudent to undertake checks where possible to ensure this doesn’t happen and avoid the potentially significant flow on effects to your projects.

If you have any questions regarding these changes, please contact your local Pitcher Partners and they can direct you to the appropriate person.

14Property of Pitcher Partners August 2019

Build to Rent – a compelling opportunity Dislocation in real estate markets is providing a compelling opportunity for the emergence of the nascent Build-to-Rent sector in Australia. A significant shift in the strategy and business model of developers (and local lenders) is progressively occurring in what is otherwise a very familiar proposition for global institutional investors.Whilst market sentiment and momentum has improved since the Federal election, broader economic and macro challenges are creating uncertainty for real estate investors and disrupting the property industry. Following changes to government fiscal policy and lending standards, the private residential investment market has seen volumes and activity significantly reduced over the past 2 years bringing some change to the industry.

Built-to-Rent (BTR), also commonly referred to as Multifamily in the US, is defined as multi-unit residential developments that are designed and built as long-term rental housing under a single ownership entity. Unlocking this asset class enables the development of a new market in Australia and growth in much needed housing stock of various grades at scale. BTR provides a lower risk investment opportunity that diversifies investor portfolios and provides income over a longer term.

To date however, the Australian tax system provides no great incentive to this style of development, noting that developers will not recover GST on construction and do not receive any additional tax incentives unless the product falls into the affordable housing category. There is however significant lobbying in the space, with a range of measures to ease cash flow on GST at least. It remains to be seen whether the current government has the appetite to take up these proposals.

There is currently a pipeline of over 6,000 units at different stages of development under a BTR delivery model. The current downturn in the residential market

has contributed to a material increase in interest from global institutional investors who hold significant BTR exposure (namely across North American and European jurisdictions). According to CBRE figures, investor presentations have more than tripled year on year and the number of purpose built institutional grade BTR projects under delivery has doubled. Select listed REITs have dedicated resources to this strategy though private developers are able to leverage delivery and operational efficiencies to drive returns further.

According to CBRE’s Debt & Structured Finance Director Brad Duff, “one of the critical enabling factors will be the ability to unlock a deep pool of debt capital notably from offshore non-bank lenders which are very competitive relative to local players. As the largest arranger globally CBRE has originated over US$ 26 billion in multifamily financing in 2018 alone with a very broad variety of lenders involved ranging from pension funds and life insurers to banks and alternative investment managers”.

The advisory industry consequently is gearing up for a wave of activity with CBRE extending its global know-how to the Australian market through the establishment of a dedicated BTR advisory team in country, providing key know-how ranging from commercial and financial structuring to arranging equity and debt financing as well as development and valuation assessment (a critical function to properly assess and value the long term cash flows associated with BTR projects).

Sydney

Brendan JonesPartner, Pitcher Partners [email protected]

BTR as a proportion of Industrial estate portfolios0% 5% 10% 15% 20% 25%

US

Japan

Germany

UK

Australia

Source: CBRE

15 Property of Pitcher Partners August 2019

AdelaideAndrew Beitzp. +61 8 8179 2848e. [email protected]

BrisbaneCole Wilkinsonp. +61 7 3222 8444e. [email protected]

MelbourneAndrew Clugstonp. +61 3 8610 5309 e. [email protected]

PerthLeon Mokp. +61 8 9322 2022e. [email protected]

SydneyScott McGillp. +61 2 8236 7880e. [email protected]

NewcastleGreg Farrowp. +61 2 4911 2000 e. [email protected]

pitcher.com.au

Making business personal

Adelaide Brisbane Melbourne Newcastle Perth Sydney

The material contained in this publication is general commentary only for distribution to clients of Pitcher Partners. None of the material is, or should be regarded as advice. Accordingly, no person should rely on any of the contents of this publication without first obtaining specific advice from one of the Partners of Pitcher Partners. Pitcher Partners, its Principals and agents accept no responsibility to any person who acts or relies in any way on any of the material without first obtaining such specific advice. © Pitcher Partners 2019 PrintPost Approved PP381827/ 0043

Pitcher Partners is an association of independent firms. Liability limited by a scheme approved under Professional Standards Legislation. Pitcher Partners is a member of the global network of Baker Tilly International Limited, the members of which are separate and independent legal entities.