Embed Size (px)

Citation preview

Summer Internship 2010

i

Study on potential of Micro financing to the SHGs/VDCs through development of community finance organization (CFOs) in selected districts of MPDPIP (Project report submitted in partial fulfilment of Post Graduate Diploma in Forest Management)

Project Report

Submitted

To

Mrs. Anju Bhadoria

(Administration Coordinator)

(Panchayat and Rural Development Department, MP)

Submitted

By

Navneet Thind

IIFM Bhopal

Summer Internship 2010

i

DECLARATION BY ORGANISATION

This is to certify that the Project Report entitled “Study on potential of Micro Financing to

the SHGs/VDCs through development of community finance organization (CFOs) in

selected districts of MPDPIP” done by Ms Navneet Thind (PFM 2009-2011) for MPDPIP

is an original work. This has been carried out as Summer Internship under my guidance for

partial fulfilment of Post Graduate Diploma in Forest Management at Indian Institute of

Forest Management, Bhopal.

Place: Bhopal Mrs. Anju Bhadoria

Date: 14th June, 2010 (Administration Coordinator, MPDPIP)

Summer Internship 2010

ii

DECLARATION

I, Navneet Thind, do hereby declare that the project entitled “Study on potential of Micro

Financing to the SHGs/VDCs through development of community finance organization

(CFOs) in selected districts of MPDPIP” is an original work. The contents of this project

report reflects the work done by me during the Summer Internship component of the Post

Graduate Diploma in Forest Management of the Indian Institute of Forest Management,

Bhopal from 5th April 2009 to 11th June 2009 with MPDPIP.

Place: MPDPIP, Bhopal (Navneet Thind)

Date: 16 June 2010 PFM 2009-2011

Summer Internship 2010

iii

Contents DECLARATION BY ORGANISATION ........................................................................................... i

DECLARATION .............................................................................................................................. ii

EXECUTIVE SUMMARY ............................................................................................................... 1

ACKNOWLEDGEMENT ................................................................................................................. 3

LIST OF ACRONYMS ..................................................................................................................... 4

LIST OF TABLES ............................................................................................................................ 6

LIST OF FIGURES: .......................................................................................................................... 7

CHAPTER-1: INTRODUCTION ...................................................................................................... 8

1.1 ABOUT MPDPIP .................................................................................................................. 8

1.1.1Vision: ................................................................................................................................ 8

1.1.2 Mission: ............................................................................................................................ 8

1.1.3 About MPDPIP-I: ............................................................................................................... 9

1.1.4 About MPDPIP-II: ............................................................................................................ 10

1.1.5 About Producer companies: ............................................................................................ 10

1.2 ABOUT PROJECT: ............................................................................................................... 11

1.2.1 Background ..................................................................................................................... 11

1.2.2 Objectives: ...................................................................................................................... 13

CHAPTER-2: LITERATURE REVIEW .......................................................................................... 14

2.1 What is microfinance? ........................................................................................................... 14

2.2Various Credit Lending Models .............................................................................................. 14

2.3 The SHG model in detail ........................................................................................................ 16

2.4 SHG Bank linkage: ................................................................................................................ 17

2.5 Micro finance and SHGs in Madhya Pradesh ......................................................................... 18

2.6 Mutual Added Cooperative Society Act: ................................................................................ 20

CHAPTER-3: SHG FEDERATIONS .............................................................................................. 21

3.1 What is a SHG federation? ..................................................................................................... 21

3.2 Need of SHG Federations ...................................................................................................... 21

3.3 Evolution of SHGs and Federations ....................................................................................... 22

3.4 Objectives and Activities of Federations ................................................................................ 23

3.4.1 Financial Support Services: .............................................................................................. 23

3.4.2 Non-Financial support services ........................................................................................ 23

3.5 Indira Kranti Patham (IKP): An Example and Paradigm for the SHG Federations: ................. 24

Summer Internship 2010

iv

CHAPTER-4: RESEARCH METHODOLOGY .............................................................................. 29

4.1 Sampling: .............................................................................................................................. 29

4.2 Data Collection ...................................................................................................................... 31

4.3 Tools of Data Collection ........................................................................................................ 31

4.3.1 Questionnaire: ................................................................................................................ 31

4.3.2 Personal interviews: ........................................................................................................ 31

4.3.3 Field observation:............................................................................................................ 32

4.4 Constraints: ........................................................................................................................... 32

CHAPTER-5: FINDINGS AND ANALYSIS .................................................................................. 33

5.1 Overall status of MPDPIP-II: ................................................................................................. 33

5.2 Extent of Micro financing: ..................................................................................................... 33

5.3 Source of Income for Community members: .......................................................................... 36

5.4 Demand of loan for various activities: .................................................................................... 37

5.5 Certain Hurdles in MPDPIP-II: ................................................................................................. 38

CHAPTER-6: COMMUNITY FINANCE ORGANIZATION ......................................................... 39

6.1 What is a CFO? ..................................................................................................................... 39

6.2 Objectives of CFO: ................................................................................................................ 39

6.3 Need of CFO: ........................................................................................................................ 39

6.4 Functions of CFO: ................................................................................................................. 39

6.5 Benefits of CFO: .................................................................................................................... 40

6.6 Proposed structure of CFO: .................................................................................................... 41

6.7 Flow of Funds after Development of CFOs: ........................................................................... 42

CHAPTER 7: SUMMARY AND CONCLUSIONS ......................................................................... 44

CHAPTER 8: RECOMMENDATIONS .......................................................................................... 46

8.1 For ascertaining the Status of SHGs and VDCs to form a CFO: .............................................. 46

8.2 For development of CFOs: ...................................................................................................... 46

8.3 For a successful and more effective MPDPIP-II : ..................................................................... 47

BIBLIOGRAPHY ........................................................................................................................... 49

APPENDICES ................................................................................................................................ 51

APPENDIX I ............................................................................................................................... 51

APPENDIX-II ............................................................................................................................. 57

APPENDIX-III ............................................................................................................................ 58

Summer Internship 2010

1

EXECUTIVE SUMMARY

MPDPIP is a large poverty-alleviation programme, started in 2000, that now covers over 5000

selected villages in 14 districts of Madhya Pradesh. The MPDPIP is an ambitious project of the

Government of Madhya Pradesh aimed at combating poverty through empowering the people and by

improving the governance. It is funded by World Bank.

Initially in MPDPIP-I (2001-2008) about 3000 villages of 53 blocks of 14 districts of the State were

covered to bring change in the social and economic status of the vulnerable poor people. Members

from the targeted family formed the Common Interest Group (CIG) on the basis of common activity.

Project Facilitation Team (PFT) at a sub-block level was set up in a cluster of 30-40 villages. It was a

multidisciplinary team with experts of various subjects. Continuous training, guidance and solutions

to problems have been given by the PFT to CIGs of their working area. Village Development

Committees (VDC) were formed by organizing the members of the CIG at village level. The flow of

fund was then from project to DPSU to CIG. MPDPIP-I was quite successful in achieving its

objectives to some extent.

After completion of MPDPIP-I in 2008, the implementation of MPDPIP-II is started in 2009. It is a

five year project. It is different from MPDPIP-I in the many aspects like that in MPDPIP-I, CIGs were

formed while in MPDPIP-II, SHGs are being formed. Also there is a basic difference between the

approaches of these two phases, like in the MPDPIP-I all the money was given to CIG members as

grant but in MPDPIP no money is being provided as a grant to SHG members.

In MPDPIP-II first the SHGs are formed and then the matured SHGs are federated into next

hierarchal structure i.e. VDC, a village level organization. At least three mature SHGs are required to

form a VDC. After this when VDC gets mature enough, then a cluster level organization called CFO

is proposed to be formed that will be the federation of 30-40 VDCs at cluster level. One member of

the working committee of VDC will be a member of CFO. The total cost of project is $110 Million.

The study was aimed to provide the information about the current status of the project in two districts

i.e. Shivpuri and Rajgarh. For this purpose both the primary as well as secondary data was collected.

Both types of data was collected to assess the quantity and quality of SHGs and VDCs that were

formed before March 2010 and to know the extent of micro financing being done at the SHG and

VDC level till March 2010.To collect the primary data regarding the current status of MPDPIP-II, the

sampling was done to select the target audience. Then various tools like questionnaire, interview and

observation were used to collect the information. The target audience for the questionnaire was SHG

Summer Internship 2010

2

members and VDC members. The focus of the questionnaire was to gather the information regarding

various things like to know the background of the members, to identify their needs, to know their

expectations from the project, to know the details of their respective SHGs and VDCs, and to know

the extent of micro finance being followed at the SHG and the VDC level. The interviews were held

with the District Project Managers of the two districts and also with the PFT coordinators who were

working in the any of the two selected districts. The main focus of interview was to identify the scope

of CFOs. That means to identify whether a CFO is feasible to form and whether it will be successful.

Also the discussion was done regarding the proposed structure of a CFO. Based on the discussion a

structure is proposed for the CFOs in the report. Moreover the discussion was also done to establish

the relationship between the SHGs, VDCs and CFOs especially to ascertain the flow of funds between

them.

Secondary data was collected from the district offices of the both the districts i.e. Shivpuri and

Rajgarh. Although the analysis was done by considering both the types of data i.e. primary and

secondary, but conclusions drawn were mostly based on secondary data because certain limitations

were encountered while collecting the primary data, like extreme temperature, remoteness of villages

etc. Due to these reasons adequate number of target members could not be covered.

Based on the research conducted it can be concluded that, to fill the needs and demands of the

community members, some other options should be explored so that more financial assistance can be

provided to them. In this regard CFO is a good option. CFO will be the organization of 30-40 VDCs at

cluster level, which will be established when most of the proposed VDCs get formed. One member of

the working committee of VDC will be a member of CFO. CFOs will be formed when VDCs get

mature enough to sustain it. CFO will register under Mutual Added Cooperative Society Act.It may link

with private and public sector banks, NABARD, Rashtriya Mahila Kosh (RMK), venture capitals,

insurance companies and other financial institutions to provide financial services to community. After the

development of CFOs the flow of fund will be from CFO-VDC-SHG-SHG member.

The research study concludes by giving certain recommendations to make MPDPIP-II a successful

project which broadly includes to provide education and training to community members, to give more

emphasis on agriculture sector and to increase livelihood opportunities for them. Moreover in the report it

is also mentioned that formation of CFO is a good concept but it should be established at a right time,

which means when the community members become able to sustain it. Certain recommendations are also

mentioned in the end regarding the conditions which should be fulfilled by VDCs to form CFO. The most

important one is the formation of about 80-90 percent of target VDCs in a particular cluster. Apart from

these, self-dependence and decision making skills need to be developed in the members.

Summer Internship 2010

3

ACKNOWLEDGEMENT

I express my sincere gratitude to Mrs. Anju Bhadoria (Administration coordinator, MPDPIP)

and Prof. H. P. Dikshit (Director General, School of Good Governance and Policy Analysis) for

providing me an opportunity to work on this project. I am very grateful for their constant support

and guidance throughout the duration of the entire project. I express my sincere thanks to Dr. R.

B. Lal (Director, Indian Institute of Forest Management) and our present summer internship

coordinator, Mr. CVRS Vijay Kumar (Faculty, Indian Institute of forest Management) for their

guidance and support. I also express my thanks to Prof. P. K. Biswas (Faculty Indian Institute of

Forest Management, Bhopal) and Mr. Amit Singh (Microfinance Coordinator) for their

encouragement and guidance. Lastly, I thank my parents, family members and friends for their

constant support in my endeavour.

(Navneet Thind)

Summer Internship 2010

4

LIST OF ACRONYMS

ITEM NEEDED

APDPIP Andhra Pradesh District Poverty Initiative Project

APMAS Andhra Pradesh Mahila Abhivruddhi Society

APRPRP

CBO

CFO

CIF

CIG

DPMU

IKP

JLG

MFI

MIS

MPDPIP

Andhra Pradesh Rural Poverty Reduction Program

Community Based Organization

Community Finance Organization

Common Investment Fund

Common Interest Group

District Project Management Unit

Indira Kranthi Patham

Joint Liability Group

Micrifinance Institutions

Management Information System

Madhya Pradesh District Poverty Initiatives

MS

MYRADA

NABARD

NGO

NWF

PFT

PRADAN

SAPAP

SBLP

SGPA

SHG

Mandal Samakhya

Mysore Resettlement and Development Agency

National Bank for Agriculture and Rural Department

Non Governmental Organization

National Women Fund

Project Facilitating Team

Professional Assistance For Development Action

South Asia Poverty Alleviation Project

SHG-Bank Linkage Program

School of Good Governance and Policy

Analysis

Self Help Group

Summer Internship 2010

5

SME

SGSY

SPIA

UNDP

VDC

VO

ZS

Small Business Enterprises

Swaranjayanti Gram Swarojgar Yojana

Sub Project Implementing Agency

United Nations Development Programme

Village Development Committee

Village Organization

Zila Samakhya

Summer Internship 2010

6

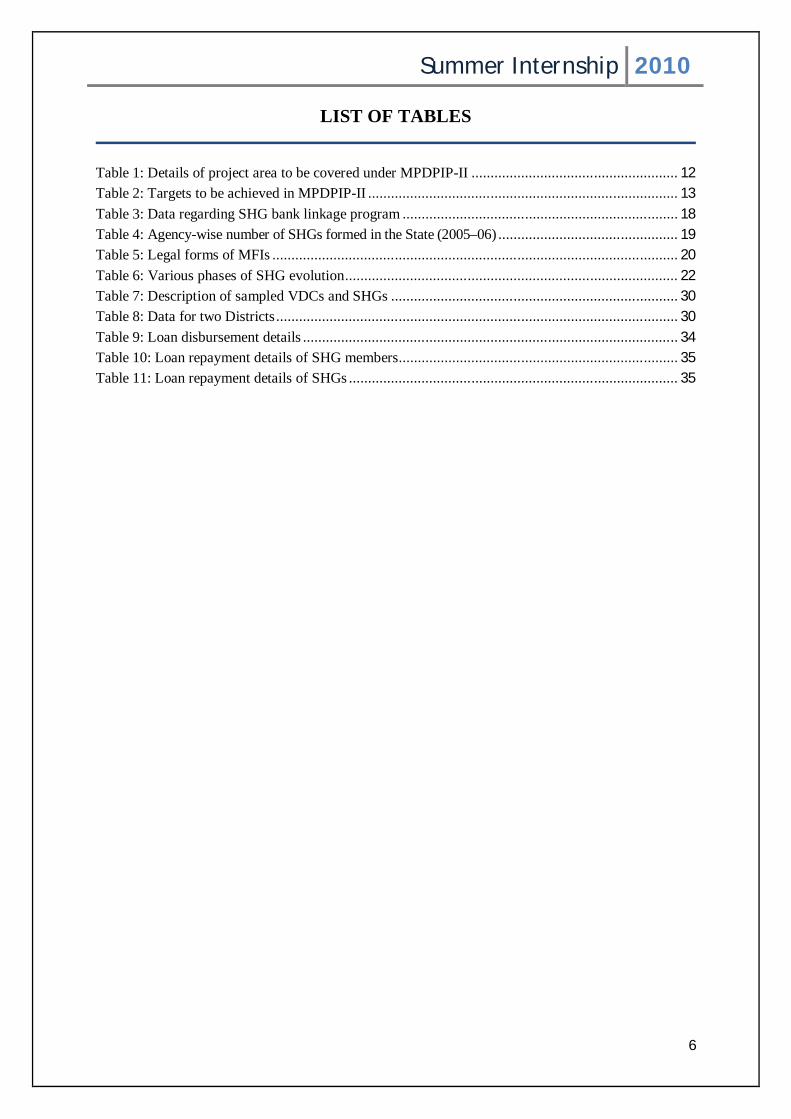

LIST OF TABLES

Table 1: Details of project area to be covered under MPDPIP-II ...................................................... 12 Table 2: Targets to be achieved in MPDPIP-II ................................................................................. 13 Table 3: Data regarding SHG bank linkage program ........................................................................ 18 Table 4: Agency-wise number of SHGs formed in the State (2005–06) ............................................... 19 Table 5: Legal forms of MFIs .......................................................................................................... 20 Table 6: Various phases of SHG evolution ....................................................................................... 22 Table 7: Description of sampled VDCs and SHGs ........................................................................... 30 Table 8: Data for two Districts ......................................................................................................... 30 Table 9: Loan disbursement details .................................................................................................. 34 Table 10: Loan repayment details of SHG members......................................................................... 35 Table 11: Loan repayment details of SHGs ...................................................................................... 35

Summer Internship 2010

7

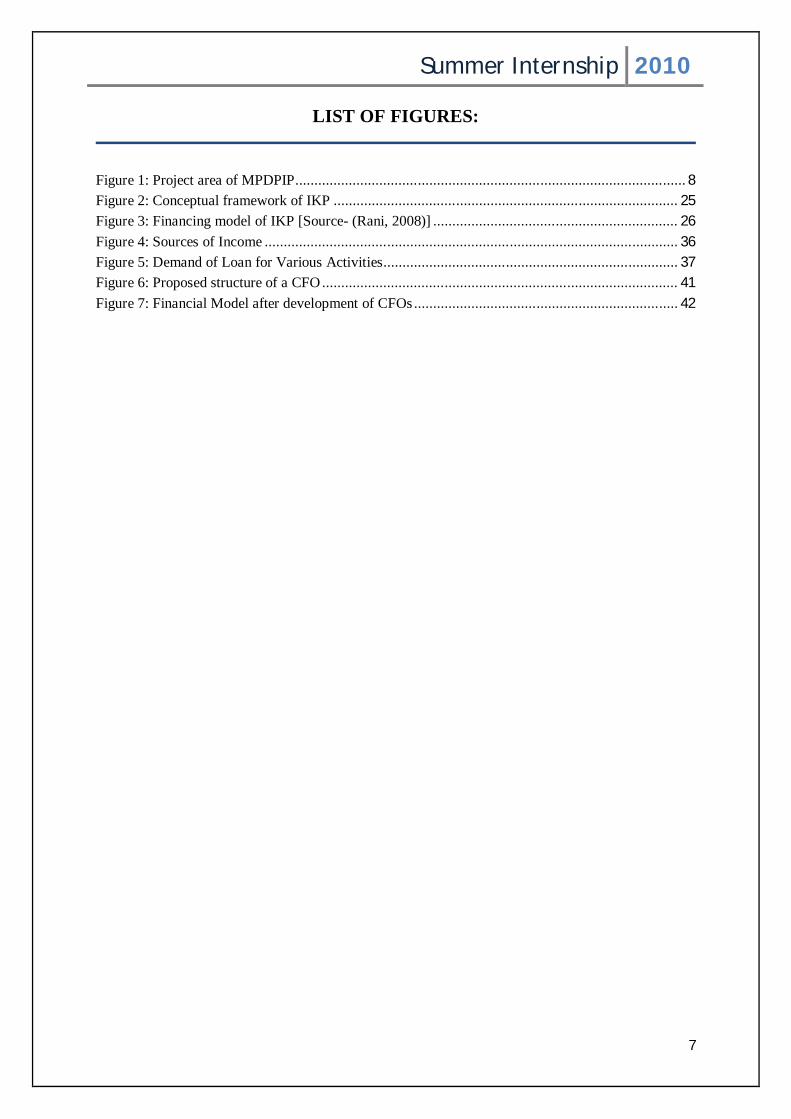

LIST OF FIGURES:

Figure 1: Project area of MPDPIP ...................................................................................................... 8 Figure 2: Conceptual framework of IKP .......................................................................................... 25 Figure 3: Financing model of IKP [Source- (Rani, 2008)] ................................................................ 26 Figure 4: Sources of Income ............................................................................................................ 36 Figure 5: Demand of Loan for Various Activities............................................................................. 37 Figure 6: Proposed structure of a CFO ............................................................................................. 41 Figure 7: Financial Model after development of CFOs ..................................................................... 42

Summer Internship 2010

8

CHAPTER-1: INTRODUCTION

1.1 ABOUT MPDPIP MPDPIP is a large poverty-alleviation programme, started in 2000, that now covers over 5000

selected villages in 14 districts of Madhya Pradesh.

Figure 1: Project area of MPDPIP

The programme works with the poorest in selected villages, after conducting a wealth ranking and

taking the villagers into confidence. In some villages, MPDPIP implements the programme directly,

with the help of 100-150 Project Facilitation Teams (PFTs) in all the fourteen districts.

1.1.1Vision:

The DPIP is an ambitious project of the Government of Madhya Pradesh aimed at combating poverty

through empowering the people and by improving the governance.

1.1.2 Mission:

MPDPIP wants to provide sustainable livelihoods to extremely poor people residing in the selected

fourteen districts of the project. It also includes establishment of self-governed community

organisations like CFOs that may become able to meet expenses of all the community members at

their own but in a sustainable manner. For this, it is essential to follow certain things like:

o To empower the active groups of disadvantaged people.

Summer Internship 2010

9

o To create income security opportunities for the rural poor

o To promot more effective and accountable village institutions including the Gram

Panchayats.

o To encourage effective demand based approaches for development.

o To enhance participation of the rural poor in economic activities.

o To do skill enhancement of the community members for taking up higher value

employment

o Increase income of the project target households through assets and market linkages.

o To organise the people into a self sustaining and self governing body.

1.1.3 About MPDPIP-I:

Madhya Pradesh District Poverty Initiatives Project (MPDPIP) was initially implemented in about

3000 villages of 53 blocks of 14 districts of the State, to bring change in social and economic status of

the vulnerable. The Project was executed from March 2001 to June 2008. It targeted the poor within a

village based on Wealth Ranking Process.

Members from the targeted family formed the Common Interest Group (CIG) on the basis of

common activity and social cohesiveness with a minimum of 5 members.

Common Interest Groups had the Liberty to select and implement the demand driven activity. These

groups were provided requisite technical support including basic infrastructure, working capital,

linkages with market and banks for successful implementation of their sub-projects.

Due to selection of similar kind of activity by the CIGs, activity based cluster has developed. In these

federations like bank, market and technical linkages have made available.

Project Facilitation Team (PFT) at a sub-block level was set up in a cluster of 30-40 villages. It was a

multidisciplinary team with experts of various subjects. Continuous training, guidance and solutions

to problems have been given by the PFT to CIGs of their working area.

To implement the sub project for the operation of the economic activity, the project transferred the

grant fund directly from District Project Support Unit to the accounts of CIGs in a single tranche. This

enabled CIGs to implement the economic activity in scheduled time qualitatively and in less cost.

Village Development Committee (VDC) has been formed by organizing the members of the CIG at

village level. VDC formed a corpus called Apna Kosh from the project fund and their regular savings.

Apna Kosh is being used for micro finance activities by the VDC.

Local Youths were provided training in various fields and have been developed as service providers.

Due to this, able persons are available at local level that are providing their services in document

maintenance, in agriculture and other land based activities, poultry, handloom, grocery and in other

service areas.

Summer Internship 2010

10

Success of the first phase is apparent through its effective evaluation and from the reports of

economic analysis of the activities. By taking benefits from the above experiences of the first phase of

the project, strategy was prepared for the implementation of the second phase of the project.

1.1.4 About MPDPIP-II:

The objective of the Second Madhya Pradesh District Poverty Initiatives Project (MP-DPIP II) is to

improve the capacity and opportunities for the targeted rural poor to achieve sustainable livelihoods.

There are four components to the project, the first component being social empowerment and

institution building. The objective of this component is to empower the poor by helping to organize

themselves into Self-Help Groups (SHG) and federate into higher levels of institutions such as Village

Development Committee (VDC), cluster-level organizations, and producer collectives and then to

federate VDCs into community finance organizations (CFOs). The second component is the

livelihoods investment support. The objective of this component is to develop the capacity of SHG to

start livelihood initiatives, and to strengthen their business operations through producer based

federations. Mechanisms to identify and support innovative approaches to help the rural poor to

organize themselves around livelihood based businesses will also be supported in this component. The

third component is the employment promotion support. The objective of this component is to enable

the project beneficiaries to capture new employment opportunities arising out of the overall growth of

the Indian economy through the establishment of a structured mechanism for skill development and

job creation. Finally, the fourth component is the project implementation support. The component will

facilitate various governance, implementation, coordination, learning, and quality enhancement efforts

in the project.

1.1.5 About Producer companies:

Apart from formation of SHGs and VDCs, MPDPIP is also facilitating the establishment of producer

companies in the project areas. The initiative of formation of producer companies was taken during

the MPDPIP-I and is continued till now. Till 2007, seventeen producers companies have been

registered in the fourteen districts where project is being implemented.

Vision: To improve rural livelihood especially of small and marginal farmers by upward integration

of their institutions with agribusiness trade and industry.

Mission: To enhance income of shareholders (small and marginal farmers) by developing dynamic

functional linkages with agribusiness trade and industry and develop support system to enable

farmers' and their institution to thrive independently in the competitive agribusiness environment.

Summer Internship 2010

11

Main Objectives:

o To carry on the production, procurement, marketing, selling, storage, processing, packaging,

distribution and trading of all agriculture and other produce.

o Address “value chain management” in sectors like seeds, food and non-food crops, vegetables

and other perishables.

o Strengthen backward and forward linkages to “induce market driven agriculture” with

Primary Producers

1.2 ABOUT PROJECT:

1.2.1 Background

The report mainly focuses on the certain aspects of ongoing project of MPDPIP i.e. MPDPIP-

II. It aims to study the potential of micro financing to the SHGs/VDCs through development of

community finance organization (CFOs) in Shivpuri and Rajgarh districts of MP. It is also mentioned

earlier that in MPDPIP-II first the formation of SHGs takes place and then that of the VDCs.

The beneficiaries involved in this project i.e. in MPDPIP-II are mainly SHG members. They get the

required financial assistance either from their respective SHG savings or from the project fund

through VDCs. Sometimes they require more money that is beyond the scope of the project, they do

not have any resources. So the report targets to explore certain options for them in this regard. One

option is the formation of CFO. CFO is projected to be the organization of 30-40 VDC at cluster

level. Only one member of a VDC will be a part of the CFO.

Summer Internship 2010

12

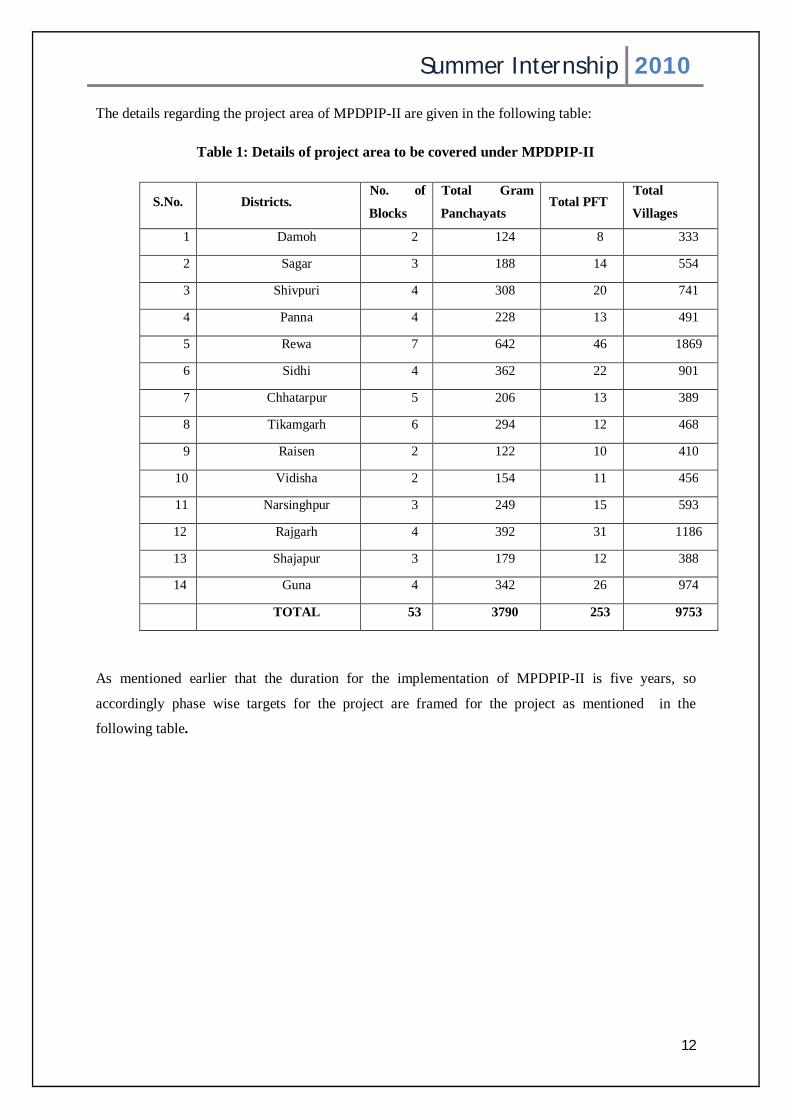

The details regarding the project area of MPDPIP-II are given in the following table:

Table 1: Details of project area to be covered under MPDPIP-II

S.No. Districts. No. of

Blocks

Total Gram

Panchayats Total PFT

Total

Villages

1 Damoh 2 124 8 333

2 Sagar 3 188 14 554

3 Shivpuri 4 308 20 741

4 Panna 4 228 13 491

5 Rewa 7 642 46 1869

6 Sidhi 4 362 22 901

7 Chhatarpur 5 206 13 389

8 Tikamgarh 6 294 12 468

9 Raisen 2 122 10 410

10 Vidisha 2 154 11 456

11 Narsinghpur 3 249 15 593

12 Rajgarh 4 392 31 1186

13 Shajapur 3 179 12 388

14 Guna 4 342 26 974

TOTAL 53 3790 253 9753

As mentioned earlier that the duration for the implementation of MPDPIP-II is five years, so

accordingly phase wise targets for the project are framed for the project as mentioned in the

following table.

Summer Internship 2010

13

Table 2: Targets to be achieved in MPDPIP-II

PARTICULARS 1st Year 2nd Year 3rd Year 4th Year 5th Year Total

Village Entry 3000 3000 3753 - - 9753

Establishment of PFT 255 - - - - 255

SHG Formation (New ) 1000 15000 12000 7000 - 35000

Restructuring of CIGs as SHGs 2000 5000 3000 1000 - 10000

VDC Formation - 2000 3000 2000 - 7000

Producer Organization

25

(existing) 0 5 5

- 35

Establishment of Ajeevika

Kendra - 600 600 300

- 1500

Skill Up grading and Training - 5000 15000 15000 5000 40000

Placement Facilitation Services 5000 20000 20000 10000 5000 60000

1.2.2 Objectives:

The deliverables for the project include:

To assess the current status of Self Help Groups and Village Development Committees and to

ascertain whether these are mature enough to form a CFO. If not then to ascertain the status

for them to form a CFO.

To propose a structure and framework for CFOs.

To establish the relationships among the SHGs, VDCs and CFOs specifically to ascertain the

fund flow between them.

To recommend the steps that the project should follow to promote CFOs.

Summer Internship 2010

14

CHAPTER-2: LITERATURE REVIEW

2.1 What is microfinance? The term refers to the provision of financial services to low-income clients, including the self-

employed.

Financial services generally include savings and credit. However, some microfinance organizations

also provide insurance and payment services.

In addition to financial intermediation, many MFIs also provide social intermediation services such as

group formation, development of self confidence, and training in financial literacy and management

capabilities among members of a group. Thus the definition of microfinance often includes both

financial intermediation and social intermediation. Microfinance is not simply banking, it is a

development tool.

Microfinance activities usually involve:

Small loans, typically for working capital.

Informal appraisal of borrowers and investments.

Collateral substitutes, such as group guarantees or compulsory savings.

Access to repeat and larger loans, based on repayment performance.

Streamlined loan disbursement and monitoring.

Secure savings products.

MFIs can be nongovernmental organizations (NGOs), savings and loan cooperatives, credit unions,

government banks, commercial banks, or nonbank financial institutions.

The people who require the micro finance are typically self-employed, low-income entrepreneurs in

both urban and rural areas. Clients are often traders, street vendors, small farmers, service providers

(hairdressers, rickshaw drivers), and artisans and small producers, such as blacksmiths and

seamstresses. Usually their activities provide them stable source of income (often from more than one

activity). Although they are poor, they are generally not considered to be the "poorest of the poor."

(Ledgerwood, 1999)

2.2Various Credit Lending Models

Microfinance institutions are one of the oldest financial institutions in the world, but like all the other

things in the world, with time they have adapted to various kinds of changes, and have started using

various credit lending models. The Microfinance community has divided itself into hierarchies. Some

of the popular microfinance credit lending models adopted across the world is:

Summer Internship 2010

15

Associations: In this type of model, a target community forges together to form an association

through which a variety of microfinance activities are carried out. The microfinance activities may

also include savings. The associations may comprise of youth, women, or be formed around cultural,

religious, or political issues.

In some of the countries a legal body can also form an association. These legal associations have

certain advantages, like collection of insurance, fees, tax breaks, and provide other protective

measures.

Community banking: This financing model considers the whole community as one unit and

facilitates the establishment of semi-formal and formal institutes through which microfinance are

administered. Usually NGOs and other similar organizations take it upon themselves to form such

institutions, and also educate the community members in diverse financial activities.

Co-operatives: A co-operative is an independent association of people who come together voluntarily

to meet their mutual economic, social and cultural aspirations and needs through a egalitarian

controlled enterprise. Sometimes the cooperatives also include savings activities and member-

financing as well.

Credit Unions: A credit union is a member-driven unique self-help financial institute comprising of

members of a specific group like labour unions or a social fraternity who assent to save money and

make loans to each other out of that fund at reasonable interest rates. A credit union membership is

free to all, and it follows a democratic approach in electing the director as well as the committee

representatives.

Grameen model or JLG model: The Grameen model is the most popular model which is practised

by so many MFIs all around the world. The grameen model entails that a bank unit be composed with

a field manager and a set of bank staff covering a specified area, like 15 to 20 villages. The banking

service starts when the manager and the staff familiarize themselves with the native people and

explain to them the intent, functions motives, and mode of operation. Finally, groups comprising of

five future borrowers are formed, out of which only two people get the loan initially, and if within

fifty weeks they return the principal amount along with interest, as per the banking rules, the other

members become eligible as well for taking loans. This is done, so that there is a collective liability on

the group, which serves as guarantee against the loan as risk factor is so high.

Group: This model is based on overcoming individual shortcomings by the aggregated accountability

and security engendered by the formation of a group of these individuals. This collective approach

also helps in educating and building awareness, collective negotiation powers, peer pressure etc.

Summer Internship 2010

16

Individual: This is the simplest and the oldest credit lending model where small loans are given

straight to the borrower. In most cases such loans are accompanied by socio-economic services like

education and skill development.

Intermediaries: As the name suggests this model is a ‘go-between’ organization operating between

the lender and borrower. They play a critical role of creating credit cognizance like starting savings

programs and thus raising the credibility of the borrowers to a sufficient level. These intermediaries

can be NGOs, individuals, commercial banks etc.

Non-Governmental Organizations: NGOs are very active in the field of micro-credit, be it creating

consciousness of the importance of micro-credit, or developing tools and resources to monitor and

identify righteous practices. The NGOs have also created many opportunities to help people learn all

about micro-credit practices and principles through organizing workshops, seminars, training

programs etc..

Rotating Savings and Credit Associations: A group of people join together and make periodic

cyclical contributions to a common fund that is given to a member in a lump sum. After receiving the

amount the member starts paying back by making regular contributions. Bidding or lottery makes the

decision about whom the money should go to.

Small Business Enterprises (SME): They get loans from micro-credit programs for creating

employment, increasing income etc. The micro credit is either provided directly to the SME or as a

part of a bigger SME development program.

Village Banking: This is a community based banking. In this 25-50 low income individuals who seek

self-employment come together to collect funds and give loans. The initial capital is generally arrived

from outside, but the members follow a democratic approach in operation and moral collateral for

repayment ( (Lending-models.).

2.3 The SHG model in detail

The self help group model has evolved in the NGO sector. A variety of models arise out of NGO

nurturing among which SHGs have become the most popular.

SHGs are small informal groups comprising of membership of 10-20 persons. The members of SHGs

are either exclusively male or exclusively female. The members are self selected with a liberty to

choose their group depending on their level of affinity with the other potential members. The group

meets regularly at an appointed time and place and carries out its financial transactions of savings and

Summer Internship 2010

17

credit. The roles and norms of the group are determined by the members themselves. The NGO

provides them with support services, training and developing linkages.

However, there are certain features of SHG that need to be looked into:

The group promotion process is long and the poor have to wait for long periods.

The amounts available in the beginning are very small and all the members cannot take loans

at the same time.

The functioning of the group relies completely on group dynamics which are very difficult to

build in.

Conflicts arise on seemingly trivial reasons which can lead to the break-down of the group

and it is difficult to rebuild it.

Despite these few disadvantages SHG still is a popular model for micro finance in India.

2.4 SHG Bank linkage: The SHG - Bank Linkage Programme is one of the most important and famous model for

delivering financial services to the poor in a sustainable manner (financial report).

The SHG – Bank Linkage Programme (SBLP) was started as an Action Research Project in 1989

which was the offshoot of a NABARD initiative during 1987 through sanctioning Rs. 10 lakh to

MYRADA as seed money assistance for experimenting Credit Management Groups. In the same

year the Ministry of Rural Development provided PRADAN with support to establish self-help

groups in Rajasthan.

The SBLP covered about 9.6 million persons in 2006-07, of which ninety percent were women,

and about half of them were poor. The total number of SHG members who have ever received

credit through the programme has grown to 41 million persons.

The table given below shows the Progress of SHG bank linkage program in India.

Summer Internship 2010

18

Table 3: Data regarding SHG bank linkage program

Year No. of SHG

linked

% change

over previous

year

Loan amount

in Rs. Cr.

Change over

previous year

in Rs. Cr.

% change

over previous

year

1992-03

1993-04

1994-05

1995-06

1996-07

1997-08

1998-09

1999-00

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

255

620

2,122

4,757

8,598

14,317

32,995

114,775

263,825

461,478

717,360

1,079,091

1,618,456

2,238,565

2,924,973

143

242

124

81

67

130

248

130

75

55

50

50

38

31

57

193

481

1,026

2,049

3,904

6,900

11,398

18,041

136

288

545

1,023

1,855

2,996

4,498

6,643

100

290

132

84

92

112

239

149

113

100

91

77

65

58

Source: NABARD Report 2007

2.5 Micro finance and SHGs in Madhya Pradesh Since MPDPIP-II is being implemented in the Madhya Pradesh, so it better to have detailed

understanding of microfinance and SHGs in the state, particularly in relation to each other. Various

programs have been implemented in state to encourage microfinance. Many of thes programs followed

the SHG model of microfinance. Micro finance—small credit delivered to people through a whole new

set of delivery agencies and tools, and a new set of systems and standards—has become the principal

strategy for providing credit to the poor, the small farmers, the small artisans and rural manufacturers and

service units. There are two distinct advantages that micro finance as a tool possesses in banking terms.

One is that it reduces transaction costs for delivering small credit. In case of large financial/banking

agencies, delivering small credit has high transaction costs, but micro finance cuts that out. Banks or

financial agencies deliver credit in large sums to groups which in turn make them into micro finance

whilst lending amongst themselves. The micro finance activity in MP, at present, covers more than four

lakhs SHGs formed by different organizations such as government departments, NGOs, banks and

NABARD (National Bank For Agriculture And Rural Development).Of these, the total number of SHGs

financed by banks (as on March 2005) stood at only 45105 (excluding the groups promoted under the

Summer Internship 2010

19

principal poverty alleviation scheme called the Swarnajayanti Gram Swarozgar Yojana, SGSY groups),

with a cumulative bank loan of Rs 110 crore. This enables an estimated 9.02 lakh poor households in the

state gain access to micro finance from the formal banking system. 47 NGOs have been sanctioned grant

assistance of Rs 90 lakhs for credit linkage of 6290 SHGs in 20 districts. The institutional credit for the

SHG linkage programme for 2006–07 is estimated at Rs 56.44 crore. All the 19 RRBs operating in the

state have participated in the SHG–bank linkage programme. As on 31st March 2005, RRBs had credit

linked 17678 SHGs and provided them bank loans to the tune of Rs 34.89 crore (NABARD 2006–07).

Apart from government departments, around 120 NGOs are involved in SHG promotion in 28 districts of

the state. The number of SHGs credit-linked in the state has increased from 74 SHGs with bank loans of

Rs 14.34 lakh in 1997–98 to 45105 SHGs involving bank loan of Rs 10968.74 lakh in 2004–05. These

SHGs were credit-linked by 18 CBs, 19 RRBs,and 21 DCCBs spread over all districts in MP. Although,

all the districts of MP have been covered under the SHG–bank linkage programme, there is wide

disparity across different regions ( MPDPIP implementation plan).

Table 4: Agency-wise number of SHGs formed in the State (2005–06)

S.No AGENCY NO. OF SHGs FORMED

1 Zilla Panchayat 233113

2 Rajiv Gandhi Watershed Mission 11130

3 Mahila Bal Vikas 77463

4 Padhana Badhana Andolan 63488

5 NGOs/Bank 19374

Total 404568

Both the central and state governments have been implementing a number of development schemes in

MP. Some of these schemes have a credit component, and aim at poverty alleviation by providing

affordable credit to poor households. It is envisioned that when deployed in viable enterprises (individual

as well as group-based), this financial support will reap incomes that will enable the beneficiaries to

access a basket of goods and services (including the nutritional minimum) to fulfil their basic subsistence

needs. The various schemes include Swarnajayanti Gram Swarozgar Yojana (SGSY), Pradhan Mantri

Rozgar Yojana (PMRY), Swarna Jayanti Shahri Rozgar Yojana (SJSRY), Margin Money Scheme of

Khadi Village and Industries Commission (KVIC), Special Schemes for Women and SC/STs and many

more schemes.

Summer Internship 2010

20

2.6 Mutual Added Cooperative Society Act: Since it is proposed that CFOs will be registered under the mutually added cooperative society act, so

it is essential to know the scope and other aspects of this act.

According to Act no. 30 of 1995 the mutually added cooperative society act can be defined as

“An Act to provide for the voluntary formation of cooperative societies as accountable, competitive,

self reliant business enterprises, based on thrift, self-help and mutual aid and owned, managed and

controlled by members for their economic and social betterment and for the matters connected

therewith or incidental thereto”.

The State Cooperative Acts did not provide for an enabling framework for emergence of business

enterprises owned, managed and controlled by the members for their own development. Several State

Governments therefore enacted the Mutually Aided Co-operative Societies (MACS) Act for enabling

promotion of self-reliant and vibrant co-operative Societies based on thrift and self-help. One example

of this concept is “Andhra Pradesh Mutually Aided Cooperative Societies Act 1995”. MACS enjoy

the advantages of operational freedom and virtually no interference from government because of the

provision in the Act that societies under the Act cannot accept share capital or loan from the State

Government. Many of the SHG federations, promoted by NGOs and development agencies of the

State Government, have been registered as MACS. Reserve Bank of India, even though they may be

providing financial service to its members, does not regulate MACS (APMACS Act Pdf).

MACS is a part of mutually benefit MFI. Apart from this there are two more legal forms of MFIs.

All the legal forms of MFIs are discussed in the following table (microfinance/mf_institution).

Table 5: Legal forms of MFIs

Types of MFIs Legal Acts under which Registered Not for Profit MFIs Societies Registration Act, 1860 or similar Provincial Acts

Indian Trust Act, 1882(For NGOs). Section 25 of the Companies Act, 1956 (For Non-profit Companies)

Mutual Benefit MFIs (Mutually Aided Cooperative Societies (MACS) and similarly set up institutions)

Mutually Aided Cooperative Societies Act enacted by State Government

For Profit MFIs (Non-Banking Financial Companies)

Indian Companies Act, 1956 Reserve Bank of India Act, 1934

Summer Internship 2010

21

CHAPTER-3: SHG FEDERATIONS

Since CFOs will be a federation of VDCs at cluster level and in turn a VDC is also a federation SHGs,

so it is essential to understand the various aspects of SHG federation.

3.1 What is a SHG federation? According to dictionary, the meaning of federation is an association of autonomous bodies uniting

together for a common perceived benefit. A federation is an association of primary organizations.

Primary organizations may federate to realize economies of scale or to gain strength as an interest

group.

Like in the given case VDC is a federation of SHGs that are the primary groups. A VDC is a village

level federation of SHGs. In case of CFO, VDCs will be the primary entities and a CFO will be a

cluster level federation of VDCs.

3.2 Need of SHG Federations The emergence and need of SHG federations lies in the limitations that are faced by SHGs. The

limitation of SHGs which gave rise to SHG federation is as follows:

1) Inability to take up larger issues of gender and social inequality and women empowerment,

etc: It is a well known and established fact that micro-finance is a necessary but not sufficient

condition for the promotion of livelihoods. Livelihood promotions need procurement of inputs,

organizing many support services and marketing of output. A small group of 10 to 20 members,

illiterate and uninformed, cannot take up these complex tasks.

2) Inability to Address the Larger Issues: Though SHGs have contributed to social issues like

women's mobility, interactions with the outside world, access to financial resources, and leadership

qualities, to some extent they are unable to address the issues like women empowerment and social

and gender equity.

3) Promoters Limitations: Any outside agency has limitations to get involved in community

development work perpetually and at an ever increasing scale. The limitations include staff, financial

resources, etc. Further facilitation by outside agencies is more expensive. As a result the promoters

reduce their level of support at some point of time. This results in the quality of SHGs is coming

down with age. Even in new areas, where the program is implemented in a target-oriented approach

quality is suffering.

Summer Internship 2010

22

4) Inability of Bankers to Understand and Accommodate SHGs' Needs: In many states and

regions, particularly in under serviced states, banks are unable to understand fully the commercial

importance of SHG lending and they feel that the SHG lending is being carried to fulfill the social

obligations and/ or official targets. Even, when the banks realized the potentials of SHG, they could

not attend the SHG needs as required because of staff shortage, mind set and procedural bottlenecks.

The net result of different actions of banks is that groups face three big uncertainties, viz.

• Whether they get loan or not

• Whether they get the amount requested or not

• When they get loan or how much time it takes for them to get a loan

To overcome all these shortcomings and limitations, the concept of SHG federation was evolved. The

NGO promoters initiated 'SHG federations' to provide financial and non-financial services to the

groups. They became successful to a large extent. For example UNDP’s South Asia Poverty

Alleviation Project was started in 1994 in Andhra Pradesh and was implemented in 20 mandals spread

across three districts. SHGs in each Mandal were federated into a Mandal Samakhya as a three-tier

structure of SHG-VO-MS and were registered under APMACS act. The project proved to be

extremely successful. Following the UNDP's successful piloting of SHG federation model under the

SAPAP in Andhra Pradesh, the state government adopted and improved the model in its cherished

Indira Kranti Patham (IKP). Many state governments also followed the SHG federation strategy to

promote SHGs. Federations are successful in addressing most of the above limitations faced by the

SHGs in the country. Many secondary stakeholders are coming forward to partner with them.

NABARD, through its circular dated 14th September 2007, started to provide financial support

(grants) for the promotion and strengthening of SHG federations (Reddy, et al., 2007).

3.3 Evolution of SHGs and Federations The evolution of SHG and their federation s not a onetime success, but it can be divided into six

phases.

o Many experiments were done ( like MYRADA did), several failures occurred and then , a few

grand successes were observed.

o Initially non-financial federations of about 20-30 SHGs,(managed by SHG members

themselves) were formed.

o Then some financial federations of about 100-150 SHGs in a compact area were formed that

were more professional and usually managed by hired outsiders or the NGO.

The federations are very complex to handle, so long-term training and handholding is required. The

various phases of evolution are listed below.

Table 6: Various phases of SHG evolution

Summer Internship 2010

23

[ (Karmakar, 2008) and (Reddy C. S., Seminar_Conference) ]

• Phase I: NGOs promote women SHGs as an alternative to mainstream financial services to reach un-reached

segments of society.

• Phase II: NABARD takes the lead in partnering with NGOs, particularly MYRADA, to pilot the well-

known SHG-bank linkage model.

• Phase III: State Governments, particularly in the South, take a proactive role in the promotion of SHGs in a big

way, by way of revolving loan funds and other support.

• Phase IV: SHG-Bank linkage reaches the scale of over a million bank-linked SHGs.

• Phase V: SHG federations emerge to sustain the SHG movement and to provide value-added services.

• Phase VI: SHGs and SHG federations gained widespread recognition to be partners of various mainstream

agencies such as financial institutions, corporate sector, and government

3.4 Objectives and Activities of Federations The various activities and objectives of federation can be categorised into two heads:

3.4.1 Financial Support Services: The main objective of federation is to make the required

fund available for its federated SHGs. The finance related activities may include:

a) To provide the life and loan insurance services to SHG members. To arrange these services at SHG

level is not feasible.

b) To provide credit, especially multiple credit line.

c) To provide savings facilities, especially voluntary savings.

3.4.2 Non-Financial support services: The non financial activities can include one or more of the following activities:

a) Training and hand holding in book-keeping and accounting.

b) Direct provision of accounting services.

c) Ongoing quality monitoring.

d) Periodic grading or quality assessment.

e) Annual auditing.

f) Conflict resolution and problem solving within and between groups.

g) Promoting new groups.

i) Awareness building and advocacy of social issues.

j) livelihood promotion activities if the funding is available (Ghate, 2008).

Summer Internship 2010

24

3.5 Indira Kranti Patham (IKP): An Example and Paradigm for the SHG

Federations: The concept of MPDPIP-II is new for the people of the state but a same kind of project has been

already executed in the state of Andhra Pradesh known as IKP.

The approach of MPDPIP-II is very much similar to project IKP which is being implemented in

Andhra Pradesh since year 2000.The mission and vision of both the projects are also very much same.

The concept of CFO in MPDPIP-II is like that of Mandal Samakhya in IKP. So to get a better

understanding of MPDPIP-II and to develop a conceptual framework for CFOs, it is good to have a

detailed study of the project IKP.

IKP is a combination of two projects:

1. Andhra Pradesh District Poverty Initiative Project (A.P.D.P.I.P) from the year 2000 to Dec 2006

(completed)

2. Andhra Pradesh Rural Poverty Reduction Programme (A.P.R.P.R.P) from the year 2002 to Sept

2009 (ongoing).

In the year 2005, the scope of the 2 projects was expanded to cover all mandals and all villages of the

state and the comprehensive programme was named as “Indira Kranthi Patham (IKP)”.

The model has been adapted from (Reddy M. S., 2007) and (Rani, 2008).

“Objective: The objective of Indira Kranthi Padham is to enable the rural poor, particularly the

poorest of the poor in AP to improve their livelihoods and quality of life by facilitating formation of

self-sustainable institutions of the poor.

Brief description of the scheme: IKP model was started in year 2000, so it now builds on more than

a decade long, state wide rural women’s self-help movement. The focus of this model is on providing

an institutional structure and developing a framework for sustaining it for comprehensive poverty

eradication. It is the single largest poverty reduction project in South Asia. The project mandate is to

build strong institutions of the poor and enhance their livelihood opportunities so that the

vulnerabilities of the poor are reduced by many times. Community Investment Fund (CIF) is the

major component of the project, which is provided to the SHGs/ VOs/ MSs to support wide range of

activities for socioeconomic empowerment of the Poor.

The project therefore helps in creating the self-managed grassroots level institutions of the poor,

namely Women thrift and credit S.H.Gs, their federations - Village Organizations (VOs) and Mandal

Samakhyas (MSs). It also takes care of many other things like:

• Support investments in sub-projects proposed by SHGs, VOs, and MSs.

• Improve access to education for girls to reduce the incidence of child labor among the poor.

• Support to disabled persons through social mobilization and access to livelihoods opportunities.

Summer Internship 2010

25

• Build capacities of established local institutions, especially the Gram Sabha/Gram Panchayat and

line departments, to operate in a more inclusive manner in addressing the needs of the poor.

• Achieve convergence of all anti-poverty programs, policies, projects and initiatives at state, district,

mandal and village levels.

Figure 2: Conceptual framework of IKP

Summer Internship 2010

26

Figure 3: Financing model of IKP [Source- (Rani, 2008)]

Community Investment Fund (CIF): The Community Investment Fund is one of the most key

components of IKP Project. CIF funds come from the SGSY scheme. Earlier CIF was also funded by

world bank when it was known as APDPIP (2000-2006).The CIF provides resources to the poor

communities for use as means to improve their livelihoods. This component supports the communities

in prioritizing livelihoods needs by investments in sub-projects proposed and implemented by the

community (SHGs / V.Os / Mandal Samakhyas (MS) and other Common interest groups). There are

three types of subprojects namely (a) Income Generation, (b) Productive physical infrastructure and

(c) Social development. The bulk of the C.I.F budget is for income generation. Out of the total IKP

project budget, CIF is the most important component that determines the level of

employment generation for the poor. CIF acts as a catalyst in capital formation at all levels including

SHG, VO and MS and offers great leverage for raising bank funds.

Under micro plan based intervention strategy, CIF is a loan from MS to VO and from VO to SHG for

implementing micro plans of SHGs, collective marketing and food security initiatives. However, it is

a grant to VO in case of implementing social development and infrastructure development activities.

District Project Management Unit (DPMU) releases the CIF to Mandal Samakhyas in installments up

to their mandal entitlement.

Summer Internship 2010

27

Organization

It is implemented by Society for Elimination of Rural Poverty (SERP), Dept of Rural Development,

Government of AP. SERP is an autonomous society registered under the Societies Act, and

implements the project through District Rural Development Agencies (DRDAs) at the District level.

Key features of the micro planning process:

• Mandal Samakhya (MS) as the Sub-project Implementing agency (SPIA) support Village

Organizations (VOs) for implementing their micro plans and assume the responsibility of appraisal,

sanction and disbursement, follow up, monitoring, recycling of recovered CIF, procurement etc.

• MS itself implement certain activities on its own which have influence on more than one village (for

example food security and marketing interventions taken up, social development activities and

Physical infrastructure created for the benefit of more than one village).

• Zilla Samakhya (ZS) is the SPIA for activities, which have influence on more than one mandal, for

example, insurance. The grassroots level organization is the SHGs. Two members from each SHG are

part of the village organization. About 200 SHGs comprise the village organization. The village

organization is at the level of the panchayat. . The village organizations are coordinated by Mandal

Mahila Samakhyas. The Mandal Mahila Samakhya is the basic financial agency. Federation of

Mandal Mahila Samakhya is the Zilla Samakhya. Some funding goes through the Zilla Samakhya but

most go through Mandal Samakhya. The Mandal Mahila Samakhya and Zilla Mahila Samakhya are

funded by DRDA for institution building. Assistant project manager is a facilitator for two Mandal

Mahila Samakhyas. The Assistant project manager also attends VOs meetings occasionally. At the

Zilla Mahila Samakhya, there is a Zilla Manager. A Community Coordinator is appointed for about

10-12 village organizations. DRDA has area coordinators or assistant project officers (APO) at the

block level. Usually about 5 Mandals are covered by the APO. The APO attends all the 5 or 6 MMS

meetings. They help in facilitating these meetings. They explain the policies and rules and also

schemes. The area coordinator who is an APO reports to the project director. The area coordinator has

an office cum residence at one of these locations.

The role of Mandal Development Officer is very limited. The community facilitator is the one who

certifies in most situations.

Services of Village Organization:

To encourage the SHGs to take up the social issues

To provide financial support to members through SHG by extending loan

To provide required technical training for livelihood activities

To identify and train personnel for SHGs & VOs for book keeping

Continuous monitoring through Committees

Summer Internship 2010

28

Services of Mandal Mahila Samakhya:

Provide CIF to VOs to implement the Micro plans of member SHGs

Capacity building activities that include organizing trainings to SHGs, VOs and staff of

CBOs

Continuous monitoring of VOs through Committees

Collaboration with Line Departments & Others

The Mandal Samakhya is responsible to develop required social capital (SHG book

keepers & Community activists identified from Community) to run the community based

organizations with the help of MS staff ” (Reddy M. S., 2007) and (Rani, 2008).

The above mentioned plan has been used to propose the structure and the functions of CFO.

Summer Internship 2010

29

CHAPTER-4: RESEARCH METHODOLOGY

4.1 Sampling: The study was conducted in the Shivpuri and Rajgarh districts of Madhya Pradesh. It was almost

impossible to cover the entire population as time was the curtailing factor, so the method of

sampling survey was employed. And according to the requirement of this study the sampling used

was multistage cluster sampling. Cluster sampling was used because population was large and

geographically dispersed. The various sampling stages are as follows:

Stage 1: Sampling Frame- Districts(14)

Stage 2: Simple Random sampling used to select the two districts.

Stage 3: Sampling frame – Blocks (4 in Shivpuri and 5 in Rajgarh)

Stage 4: Simple random sampling used to select one block from every selected district.

Stage 5: Sampling frame – PFTs or Sub Blocks (9 in Shivpuri and 14 in Rajgarh)

Stage 6: Convenient sampling used to select two PFTs or sub blocks from the selected blocks of the

selected districts.

Stage 7: Sampling Frame-SHGs/VDCs

Stage 8: Convenient sampling done to select 10 VDCs and 20 SHGs from each selected Sub blocks of

the selected blocks of the selected districts.

Stage 9: Sampling Frame-SHG/VDC Members.

Stage 10: Random Sampling used to select two or three members from the each selected SHG/ VDC

of the selected Sub blocks of the selected blocks of the selected districts.

Summer Internship 2010

30

Table 7: Description of sampled VDCs and SHGs

Name of

District

Name of

Block

Name of Sub-

block

Number of

VDCs

selected

Number

of SHGs

selected

Total number

of respondents

VDCs SHGs

Shivpuri Pichchore Pichchore 10 20 20 40

Bhauti 10 20 20 40

Rajgarh Biaora Barkheda 10 20 20 40

Dhakora 10 20 20 40

Total 40 80 80 160

Table 8: Data for two Districts

Particulars (Till March 2010) Shivpuri Rajgarh

Total number of VDCs formed 53 89

Total number of SHGs formed 349 771

Total number of PFTs formed 9 14

Total number of Blocks Recognized 4 5

Summer Internship 2010

31

4.2 Data Collection Data was collected from both primary and secondary sources. Primary data was collected through the

field visit to the two districts with the help of PFT members. Also the researcher interviewed and

discussed various aspects of MPDPIP-II related to microfinance with many higher and field officers

who are working in the department. PFT members and other post holders of MPDPIP-II have been

interviewed by the researcher to gain the knowledge.

Secondary data was collected through the visit to district offices and by studying various plans of

MPDPIP. Additional data was also collected by interaction with resourceful people from the

department and district office. The related documents were reviewed for collection of socio economic

data about the villagers and also of obtaining factual data about the villages. Secondary data was also

collected with the help of various resources like Google.

4.3 Tools of Data Collection Data was collected by conducting survey method using various tools like Questionnaire, Interview

and Observation. Questionnaires were designed for this purpose, which were purely close ended.

Random sampling method was used for the questionnaires to get filled. Separate questionnaires were

designed for SHGs and VDCs with required pre-testing.

4.3.1 Questionnaire:

As a part of quantitative data collection, a set of questionnaire was prepared and accordingly data

was collected from the members of SHGs and VDCs. The questionnaire was pretested and due

care was taken to wipe out all the hypothetical words and anomalies.

4.3.2 Personal interviews:

Interviews were taken to acquire information mainly from two set of people The researcher

interviewed members of PFTs, particularly Coordinator of respective PFTs to gain insight into

the issues, problems and working of SHGs and VDCs. This tool was used when direct

communication was required and where researcher can inquire respondents about the project and

its concept. The interviewees were interviewed for acquired information about the following

aspects:-

Current scenario of MPDPIP-II.

About regularity of SHG and VDC meetings.

Interloaning amongst them.

Summer Internship 2010

32

Objectives achieved till now.

Plan for future.

4.3.3 Field observation:

Observation always plays a vital role in the conduction of research. Researcher stayed at all

villages which made it easy to analyze the processing and the perception of people regarding the

project. Several meetings of SHGs and VDCs were observed in various villages and also attended

tours with PFT coordinators and members of the two districts. During this, the following aspects

of groups were studied:-

Attendance of members of the SHGs and VDCs – reasons of absence and lack of motivation.

Different activities for which the loan was required by people.

Fund flow mechanism and account maintenance.

The savings were done by SHG members and SHGs.

The expectations of the SHGs and the VDCs from the Project.

Extent of inter loaning among SHGs and VDCs.

4.4 Constraints: There were various reasons due to which adequate sampling could not be done and so a sufficient

number of target people could not be covered.

o The summer season was a big constraint due to which only limited number of SHGs and

VDCs were visited.

o The accessibility was another reason. Most of the villages were located in very remote

locations as compared to city that resulted in the field visit to few villages only. Also because

of this reasons the convenient sampling was used instead of random sampling for selecting

the villages which were to be covered.

o The lack of proper and timely conveyance also proved to be a reason.

o Time required to interact with the respondents was not sufficient as they were supposed to be

busy the whole day in their work. Sometimes they were not available even to interact. They

were free only in the morning to fill the questionnaires.

Summer Internship 2010

33

CHAPTER-5: FINDINGS AND ANALYSIS

5.1 Overall status of MPDPIP-II: Most of the SHGs and VDCs formed in MPDPIP –II are in very early phase. Many of the VDCs of

the first phase of the project are also working. The formation of various other SHGs and VDCs is also

in progress.

PFT members are there to monitor the progress of existing SHGs and VDCs and formation of new

SHGs and VDCs. They are making sure that all the members of SHGs and VDCs should understand

the basic objective of project. They also monitor that regular meeting of SHGs and VDCs should be

held.

A SHG organizes four meeting in a month, while two meeting of respective VDCs are held. If anyone

goes absent without any prior information then that member has to give Rs. Five to ten as punishment.

Various concepts of microfinance are being followed at both the levels.

5.2 Extent of Micro financing: As far as micro financing is concerned, it has been just started amongst the community members.

The members are learning and following the basic concepts of microfinance. Like the very first

concept of microfinance is savings. For the first 2-3 months after the formation of SHG, the members

follow just the practice of savings. Initially they start with a very minimal amount of Rs. 5 but after 5-

6 months they start saving Rs.10-20 per meeting. That means an SHG is able to save Rs. 400-800 in a

month. The total amount of savings varies from SHG to SHG due to varied number of members and

per SHG saving.

After 2-3 months of their formation the inter loaning among SHGs gets start. The amount of loan

taken differs from person to person. Based on the research it is found that the member have taken loan

of Rs.500-5000 from the savings as per their requirements. After 3 months, grading of SHG is done to

ensure whether it will be a feasible group in the future.

After this a seed loan of Rs 1000 is being provided to SHG members by the VDC, as per the demand.

According to the demand of SHGs, the VDCs send application for funds to district. The fund given to

VDC is grant while when it is given to SHG, it becomes a loan. A seed loan of Rs. 1000 is provided to

SHG members to check whether they are able to repay it on time. Till now most of the SHG members

have repaid their seed loans. After repayment the loan becomes a property of VDC. Now any SHG

member can take that amount as a loan. Whenever a SHG members demands for a loan it is first seen

that whether the demand can be filled from the SHG savings and then the demand goes to VDC. Only

Summer Internship 2010

34

some of the VDC have circulated the money as loan. Also every SHG transfers Rs. 50 from its saving

to Apna kosh of VDC which is also used for loaning purpose.

Till now, 90% of the SHG members who are surveyed have retuned their seed loan and now they have

applied for livelihood loan. The amount of livelihood loan depends on the demand. The demand of

loan has been forwarded to district office by VDC.

Apart from new VDCs, the SHG members are taking loans from old VDCs, if they exist in that

particular area.

The rate of interest charged by VDCs to SHGs is six percent while that of paid by SHG members is

twelve percent. The ratio of repayment till now is cent percent. All the members have repaid there

loan in between 1-6 months after taking the loan. The loan taken is generally for consumption

activities like to buy food items, medicines etc. While sometimes it was also used for income

generating activities. Sometimes it was also taken for activities like marriage and due to natural

calamities.

The following table shows the loan disbursement for the month of March in the two districts. The data

is retrieved from MIS of March month, retrieved from the two district offices of DPIP.

Table 9: Loan disbursement details

Amount of loan Shivpuri Rajgarh

Total amount of loan given to SHG by VDC (Rs.) 613750 646000

Total amount loan given to SHG member's by SHG (Rs.) 736405 529000

Summer Internship 2010

35

The loan repayment details of SHG members are given in following table:

Table 10: Loan repayment details of SHG members

From Member's to SHG (for March 2010) Shivpuri Rajgarh

Amount (principal) to be collected in current month (Rs.) 162686 131000

Actual amount collected (Principal) (Rs.) 144550 131000

Total Amount out standing (Principal) (Rs.) 591855 0

Amount in arears (Principal due but not received) (Rs.) 24636 0

Interest Amount to be collected in current month (Rs.) 7087 1687

Interest (overdue) to be collected (Rs.) 1095 0

Total interest to be collected (Rs.) 7737 1687

Actual Interest Amount Collected (Rs.) 5794 1687

Repayment Rate (%) 89% 100%

The loan repayment details of SHG are given in following table:

Table 11: Loan repayment details of SHGs

From SHG to VDC (for March 2010) Shivpuri Rajgarh

Amount (principal) to be collected in current month (Rs.) 75561 131000

Actual amount collected (Principal) (Rs.) 77810 131000

Total Amount out standing (Principal) (Rs.) 535940 0

Amount in arears (Principal due but not received) (Rs.) 3651 0

Interest Amount to be collected in current month (Rs.) 3150 843

Interest (overdue) to be collected (Rs.) -45 0

Total interest to be collected (Rs.) 3105 843

Actual Interest Amount Collected (Rs.) 3185 843

Repayment Rate (%) 100% 100%

Summer Internship 2010

36

5.3 Source of Income for Community members: Amongst the community persons surveyed, most of the members belong to agriculture based

activities. Some others were found to be labourers and only a few were from industry or marketing

activities.

Figure 4: Sources of Income

From the given pie-chart it can be easily concluded the most of the community members are

dependent on agriculture activities for their livelihood. After then it is the number of labourers which

dominates. However, more than half of the labourers are dependent on agricultural activities for their