Embed Size (px)

Citation preview

A

Study

on

(Conducted on behalf of ‘The Varachha CO-operative Bank

Ltd., Surat)

(From 1st June,2011 to10thJuly, 2011)

A Project Report submitted in partial fulfillment of the

requirements

For the award of the degree of

Submitted By:

Daya Kakadiya

MBA(Sem-2

UNDER THE GUIDANCE OF

Miss.Priyanka Parekh

Submitted To:-

1

I Daya Kakadiya here by, declare that this winter training report is

the result based on my own research & hard work or Published matter used a

reference has been duly acknowledged. Daya Kakadiya student of Sigma

Institute of Management, Vadhodiya.

Training Period from 1ST January, 2011 to 28th February, 2011 and

prepared report for the same assures that information in this report is true

and reliable.

Signature

Place:

Date:

2

I have undergone the project work at “THE VARACHHA CO-OP BANK LTD.”.

I have collected the information, which is included in this report. I take the opportunity to

express the feeling of grateful towards Gujarat Technological University for the project

work of M.B.A(Sem 2).

I also thank to Director Sir J.G and MR. RAJESH DESAI, the co-coordinator

of AMBABA COMMERCE COLLEGE & MANIBA INSTITUTE OF BUSINESS

MANAGEMENT for giving me an opportunity for project work at THE VARACHHA

CO-OP BANK LTD., and I also express my guide MR. PARESH KELAWALA for his

valuable guidance and help throughout my project.

I really and most thankful to chairman and managing director of Varachha Co-

operative Bank and mostly to A.D. Bhalani (General Manager) for allowing me to

undergo the project work at Varachha bank next and most feeling a gratitude towards

MR. PARESH KELAWALA (Punagam branch manager) and Dineshbhai, Janakbhai,

Vipulbhai, Sureshbhai, Falgunbhai, Ghanshyambhai and all the staff of bank who really

encourage me and give all information and training as not student, but as a friend. So I

again heartily thankful to all.

Yours faithfully,

Daya Kakadiya.

M.B.A.

(sem2)

TABLE OF CONTENTS

Chapter

No

Page

3

Name of The Chapter No.

Preface

Acknowledgement

Declaration

Executive Summery

1 History of Banking Industry

Introduction of bank

Definition of bank and banking

Types of banks

Structure of banking Industry

Introduction of co-operative banks

Structure of banking Co-operative

banks

2 Introduction of the Varachha Co-op.limited

History of the bank

Vital factors of the bank

Organization structure of the bank

4

Introduction of the board of directors

Different branches of the bank

Day to day operations of the bank

Different services provides by the bank

Various types of deposit account of the

bank

Bankers to the bank

Types of Loans in bank

Objectives of the bank

Contribution of bank to its shareholders

Contribution of bank its customers

Contribution of bank to its employees

Interest rates of various deposits

Interest rates of various loans

Loan recovery management

3 Research Methodology

Research problem

Objectives

5

Period of coverage

Sources of the Data

Scope of the study

Selection of sample

Important of study

Limitations of the study

Review of literature

4

Introduction of Financial Statement

analysis

Need for and meaning of financial

analysis

Objectives of financial statement

Nature of financial statement

Limitation of financial statement

Financial statement of Varachha bank

5 Tools of Financial statement analysis

Comparative financial statement

Common size financial statement

6

Trend analysis

Fund flow statement

Cash flow statement

Ratio analysis

6

Findings and suggestions

Facts and Findings

SWOT analysis of the bank

Suggestions

7 Conclusion

8 Bibliography

9 Annexure

7

1.1 INTRODUCTION OF BANK

8

banks in India were founded by Indian entrepreneurs and visionaries in the

pre-independence era to provide financial assistance to traders, agriculturists and budding

Indian industrialists. The origin of banking in India can be traced back to the last decades

of the 18th century. The General Bank of India and the Bank of Hindustan, which started

in 1786 were the first banks in India. Both the banks are now defunct. The oldest bank in

existence in India at the moment is the State Bank of India. The State Bank of India came

into existence in 1806. At that time it was known as the Bank of Calcutta. SBI is

presently the largest commercial bank in the country. The role of central banking in India

is looked by the Reserve Bank of India, which in 1935 formally took over these

responsibilities from the then Imperial Bank of India. Reserve Bank was nationalized in

1947 and was given broader powers. In 1969, 14 largest commercial banks were

nationalized followed by six next largest in 1980. But with adoption of economic

liberalization in 1991, private banking was age in allowed. The commercial banking

structure in India consists of: Scheduled Commercial Banks and Unscheduled Banks.

Scheduled commercial Banks constitute those banks, which have been included in the

Second Schedule of Reserve Bank of India (RBI) Act, 1934. RBI includes only those

banks in this schedule, which satisfy the criteria laid down vide section 42 (6) (a) of the

Act.

1949 : Enactment of Banking Regulation Act.

1955 : Nationalization of State Bank of India.

1959 : Nationalization of SBI subsidiaries.

1961 : Insurance cover extended to deposits.

1969 : Nationalization of 14 major banks.

1971 : Creation of credit guarantee corporation.

1975 : Creation of regional rural banks.

1980 : Nationalization of seven banks with deposits over 200 crore.

9

Banking during British period before independence.

Ancient Hindu scriptures provided enough evidence of the existence of money

lending business in India. Mahajans, Shroffs, Shakers, etc. were enjoyed in banking

business. In the beginning of the 18th century, the East India Company set up a few

commercial banks on modern lines. In 1970, first India bank knows as the “Bank of

Hindustan” was started and was closed down twenty years later. Later on bank of

Hindustan and Bengal Bank also came into existence in 1809. Bank of Hindustan carried

on the business till 1900. The first joint stock bank, namely the General Bank of India

was established in 1786. Later, the East India Company started three presidency banks

with government participation. These were:

1). Bank of Calcutta (1806)

2). The Bank of Bombay (1840)

3). The Bank of Madras (1843)

These banks had the financial participation by the government also.

During the 18th century, these entire banks were also opened by Agency house in

Madras and Calcutta. These entire banks failed, the need of banking regulation in India

was seriously felt. As a result companies Act, 1833 was brought into force. The impact of

the agency house got slowly reduced.

Allahbad Bank came into existence in 1865 and Alliance Bank of Simla in 1875.

The first purely Indian joint stock bank known as the Oudh Commericial Bank was set up

in 1906 encouraged the Indian entrepreneurs to start many new banks. There were as

many 648 commercial banks in India by the end of 1947. As many as 161 banks failed in

quick succession during 1913-1914 and people’s faith in the banks system was shaken.

Thus there was a great need of an institution to control and regulate banking in the

country. As a result, the reserve bank if India was established as the central bank of

country in 1935 under an act called Reserve Bank of India Act. Later on with the passage

of the banking regulation Act passed in 1949. RBI was brought under government

control. Under this act, RBL was conferred with supervision and control of the banks and

licensing powers and the authority to conduct inspections was also given to it.

10

The three presiding banks were amalgamated in 1920 and new bank called

Imperial Bank of India, this bank played an important role in the economy of the country.

After independence, it was nationalized in 1955 and renamed as the State Bank of India.

The SBI opened a large number of branches in rural and semi-urban areas. The RBI acts

as a centralized body monitoring any discrepancies and shortcoming in the system. It is

the foremost monitoring body in the Indian financial sector. The nationalized banks (i.e.

government owned banks) continue to dominate the India banking arena. Industry

estimates indicated that out of 274 commercial banks operating in India, 223 banks are in

the public sector and 51 are in the private sector. The private sector bank grid also

includes 24 foreign banks that have started their operations here.

11

1.2 Definition of Bank and Banking

Bank

Banking

12

1.3Types of Banks

3)Specialized Banks: There are specialized forms of banks catering to some special

needs with unique nature of activities.

These are ,thus ,foreign exchange bank, individual banks

13

14

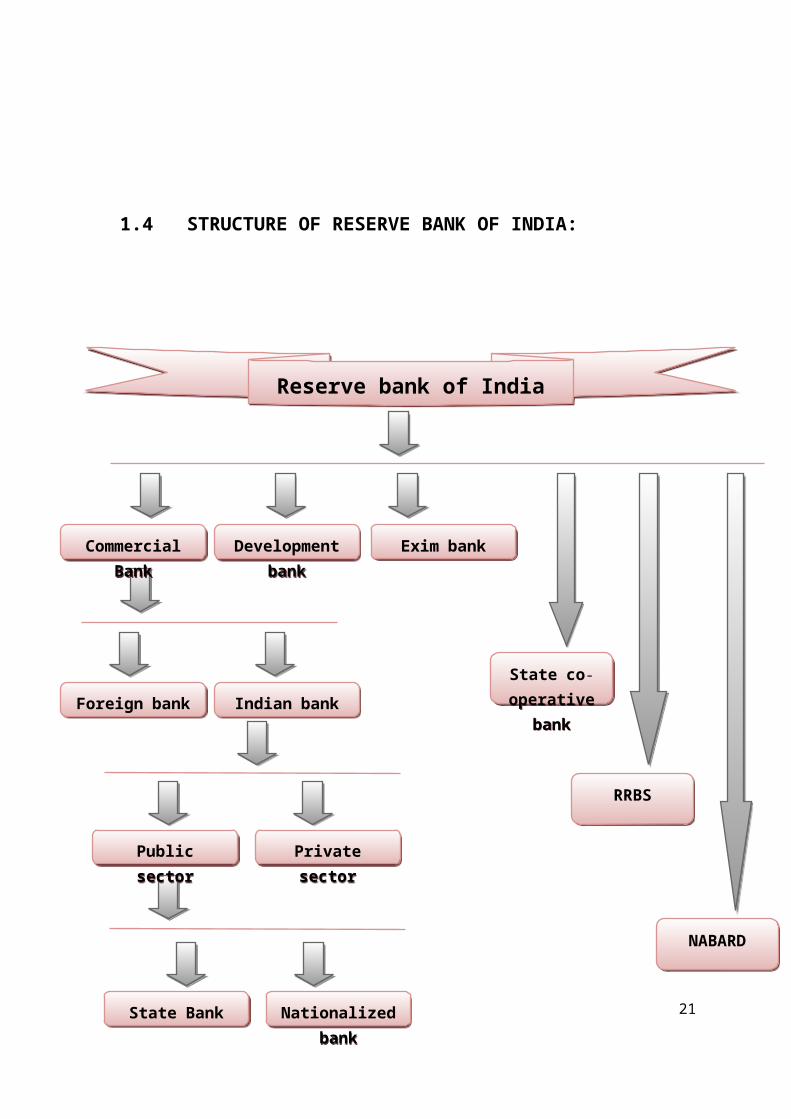

1.4 STRUCTURE OF RESERVE BANK OF INDIA:

15

Reserve bank of IndiaReserve bank of India

Indian bankIndian bank

State co-

operative

bank

State co-

operative

bank

RRBSRRBS

NABARDNABARD

Development

bank

Development

bankExim bankExim bankCommercial BankCommercial Bank

Foreign bankForeign bank

Private sectorPrivate sectorPublic sectorPublic sector

Nationalized bankNationalized bankState BankState Bank

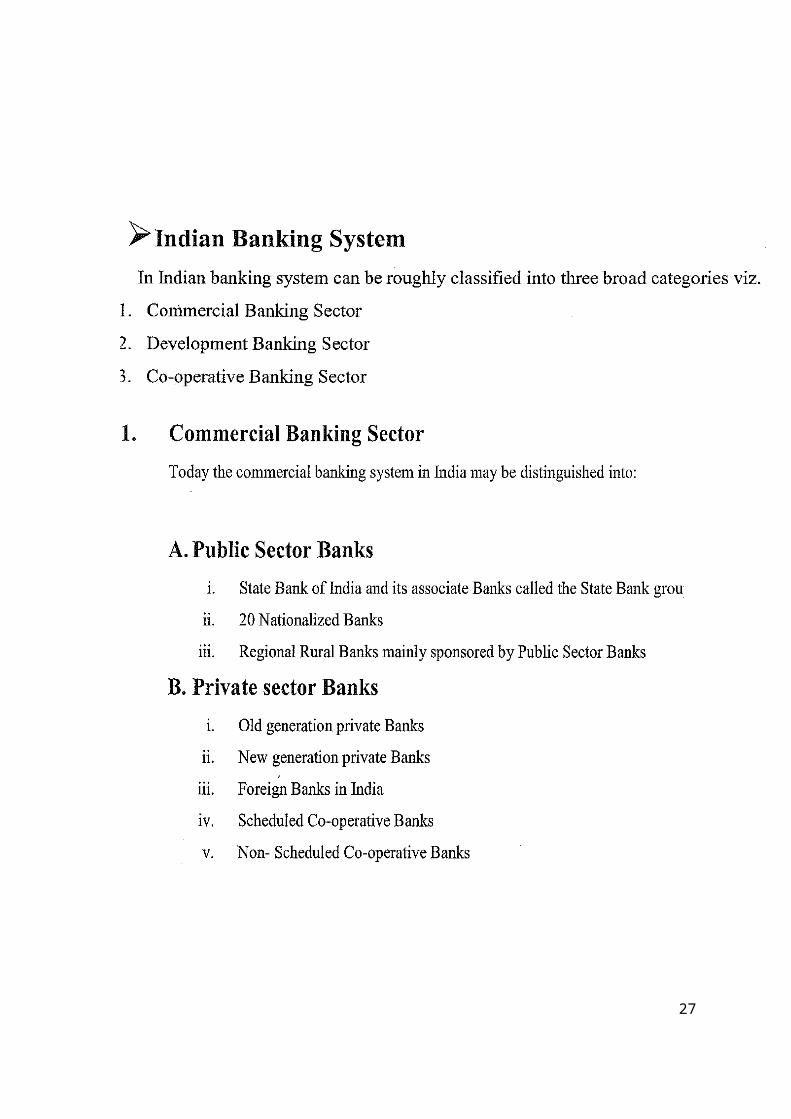

Indian banking system comprises of both organized and unorganized banks.

Unorganized banking includes indigenous bankers and village moneylenders. Organized

banking includes the followed,

Reserve bank of India (central bank)

Commercial banks

Development banks

Exim banks

Co-operative banks

Regional rural banks

Land development banks

National Bank for agriculture and rural development (NABARD)

16

1.5 Introduction of co-operative bank

MEANING OF CO-OPERATIVE BANK:

Co-operative bank are based on the value of self-responsibility,Democracy,equit and

solidarity.In the world co-operative bank activities was stated in December1844 in

Britician social development is the role aim of the Co-operative activities.

A. DEFINITION:

“Co-operation is an effective self-reliance done by organism.”

-Sir Horas Planket.

“Co-operation is the step taken for equal profit or loss under mutual

management.Management by mutually using their own resources and factors willingly.

-Herick M. T.

17

B. ORIGIN OF CO-OPERATIVE BANK:

The word of co-operative was (being) recognized in 1904 (when the co-operative

societies Act 1904 was enacted) When the co-operative credit society was passed. The

activities of co-operative was started with the main purpose of providing the advance to

the member with a low interest rates, and providing advance to farmer and lower class

and to make the people interested in savings.

18

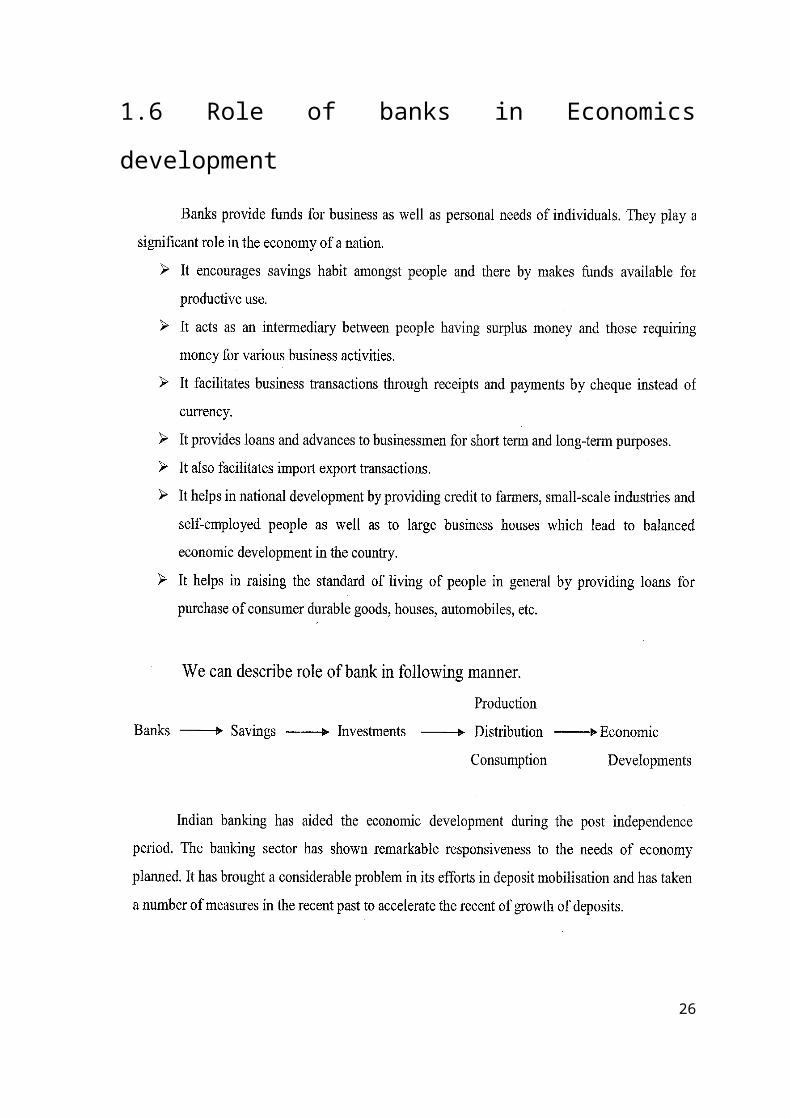

1.6 Role of banks in Economics development

19

20

21

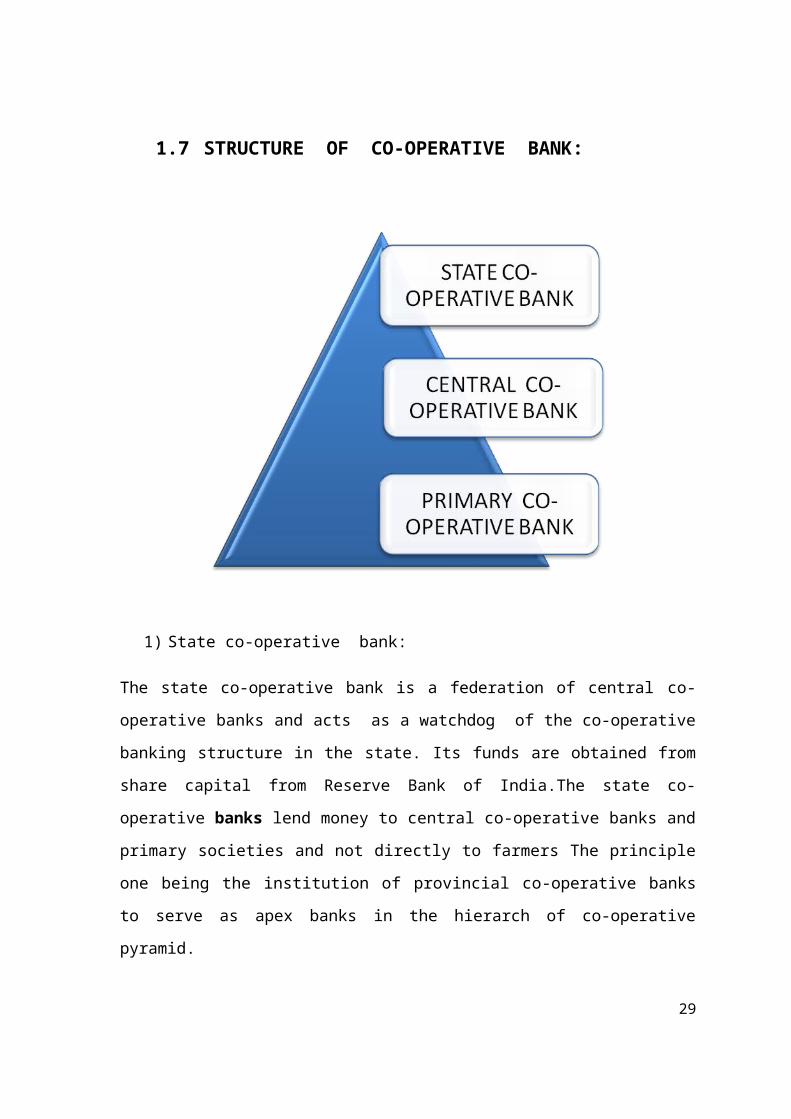

1.7 STRUCTURE OF CO-OPERATIVE BANK:

1) State co-operative bank:

The state co-operative bank is a federation of central co-operative banks and acts as a

watchdog of the co-operative banking structure in the state. Its funds are obtained from

share capital from Reserve Bank of India.The state co-operative banks lend money to

central co-operative banks and primary societies and not directly to farmers The principle

one being the institution of provincial co-operative banks to serve as apex banks in the

hierarch of co-operative pyramid.

2) central co-operative bank:

There are the federations of primary credit societies in a district and are of two types those

having a membership of primary societies only and those having a membership of societies

as well as individuals. The funds of the bank consist of share capital, deposits and

overdrafts from state co-operative banks and joint stocks. These banks finance member

22

societies within the limits of the borrowing capacity of societies. They also conduct all the

business of a ointstock bank.

3) primary co-operative bank:

Primary co-operative bank is also known as credit society. The primary co-operative credit

society is an association of borrows and number derived from the share capital and deposits

of and members and loans from central co-operative banks. The borrowing power of the

members well as of the society is fixed. The loans are given to members for the purpose of

cattle, folder fertilizer, pesticides, implements, etc

There are three types of co-operative banks and the urban co-operative bank is one type

of co-operative bank, the varachha bank is urban co-operative bank.

FUNCTION OF CO-OPERATIVE BANK:

Co-operative Banks are formed on the principle of Co-operative to Extend Credit

facilities to farmers and small scale industrial concerns and promotes in general

the habit of thrift and self help among the low and middle income groups of the

society.

Co-operative has been putting more weight on their lending activities than on

deposit mobilization.

The main function of Co-operative credit society was to provide cheap credit to

the members who are small people with small means and small needs and finance.

The Co-operative Banks have a three tier set up. The state co-operative bank,

while central district co-operative banks function at the district level and primary

credit societies work of the village level.

Co-operative banks proceed on the principle of co-operation. CO-operative Banks

maintain the cash reserve and liquid assets in relation to deposit only.

To arrange the programs regarding the Economic welfare of its members.

This bank supervises the functioning of primary credit society and gives training,

guidance and advice to the employee of credit society only.

23

24

2.1 History of varachha co-operative Bank Ltd.

THE VARACHHA CO-OP. BANK LTD.

The people in Saurashtra, located in western part of Gujarat, are always depending

upon the rain-fed cultivation. As a search for income generation in an alternate way for

their survival, they have chosen Surat city, where there is a good scope for trade in

Diamond and Textile sector. Well off people have entered into the trading sector and the

others on labour front. In a phased manner, the population of the people, involved in

diamond trade, belonging to Saurashtra increased to a sizeable extent in Surat and in

particular in the area of Varachha. It was become obvious for a necessity of a Bank for

their own people; the efforts were taken by a well known philanthropist, story writer and

columnist in local dailies, Mr. P. B. Dhakecha, founder chairman of our Bank. As such,

The Varachha Cooperative Bank Ltd., came into existence on 16th October 1995 and

Inauguration ceremony was done by on the hand of Shree Swami Sacchidanand. Some of

our directors are belonging to diamond trade, who are official site holders of getting

rough block diamonds from foreign countries. At the end of the first financial year the

number of shareholders was 4484, Share Capital 57.44 lacs, Deposits Rs.2.70 crores,

Advance Rs.2.07 crores and profit stood at 4.77 lacs.

Our Bank has gradually developed the Banking activities and at the end of 5th

year, with a network of 5 branches, the share capital and reserves raised to more than 8

crores and the deposits have crossed 100 crore mark, which is a rare phenomenon in

Cooperative Banking Sector in all over India and the number of depositors have increased

58222. The Bank has been awarded with First Prize for the best performance among all

Cooperative banks in Surat District during the FY.2000 - 01. At present the share capital

and reserves raised to nearly 40 crores. The deposit is Rs.160.70 crores Advances 78.21

25

crores. Total 7 branches and 130 staff members. In spite of run in a cooperative sector in

the year 2001, due to Madhavpura episode, the Bank has not only survived but also

developed the base without any difficulty due to confidence reposed upon by the public

with our Bank.

We have introduced the system of quick delivery of vehicle loans, with minimum

papers and documents, without any hidden charges. Other advances of our Bank have

been spread over on the following categories:

Vehicle Loan

Loan against gold ornaments

Loan on personal guarantees (Surety Loan)

Retail trade business

Professional and Self employed

Loan against Bank’s own deposits/NSC

Cash credit – hypothecation on stocks on trade

Technology Upgradation Finance (TUF) loan with subsidy

Besides the banking activity, the Bank has entered into the insurance business

arrangement with IFFCO-TOKIO. We are also having tie-up arrangements with insurance

companies on referral basis, as per RBI guidelines. We have covered with accident

insurance cover for the shareholders, depositors and borrowers of the Bank and we have

received settlement to the tune of Rs.1 crore from the insurance companies. The data

pertaining to our Bank is being sent to Reserve Bank of India, banking regulator of

the country, through e-Mail under offsite surveillance system (OSS) for the past 3 years.

Our Bank has been fully computerized banking system, right from inception and present

programme, front end Visual Basic and the back end (database) Oracle 10G Platform. We

26

are having the staff members, most of them belonging to younger generation, with

energetic and enthusiastic approach in Customer Service. The staff attendance is being

controlled under Biometric device system. CCTV system is being installed to monitor the

alertness of the entire banking activity, fitted with cameras at the vital points. Our Bank

has introduced Mobile Banking and Any Branch Banking (ABB) in the year 2007. Our

future plan is the introduction of on and off site ATMs and Core Banking System.

Other vital factors of our Bank are as follows:

One of the leading cooperative Banks in South Gujarat

Audit grade, continuously at ‘A’, from the beginning

Any Branch Banking (ABB)

CCTV system is being installed to monitor the alertness of the entire banking

activity, fitted with cameras at the vital points.

Bank has started E-payment facility for the customers of the Bank for the purpose

of payment of Income-Tax.

Personalized Cheque Book are being issued to all the customers of the Bank. -

RTGS/NEFT facility is also available.

Mobile Banking system to customers for getting various details about their

accounts like Current Balance, Cheque Return Status, FD Rates, Loan Rates,

Various Loan Schemes etc. by way of SMS.

Display/provision of VAT machine in Banking hall, for customers’ approach

Strong working capital, Deposit base and our investment assets are profit oriented

Net NPA continuously at zero percent

No default in CRR/SLR

Concurrent audit system

Implementation of Know Your Customer (KYC) policy

Teller system for payment upto Rs.20000 in CA and Rs.10000 in SB

27

Franking of adhesive stamp duty – arranged by Revenue Dept. of Gujarat State.

Besides banking, the Bank has done a little for some noble social cause, by conducting

blood donation camps. The bright wards of the shareholders are being given with

educational scholarship for their future study.

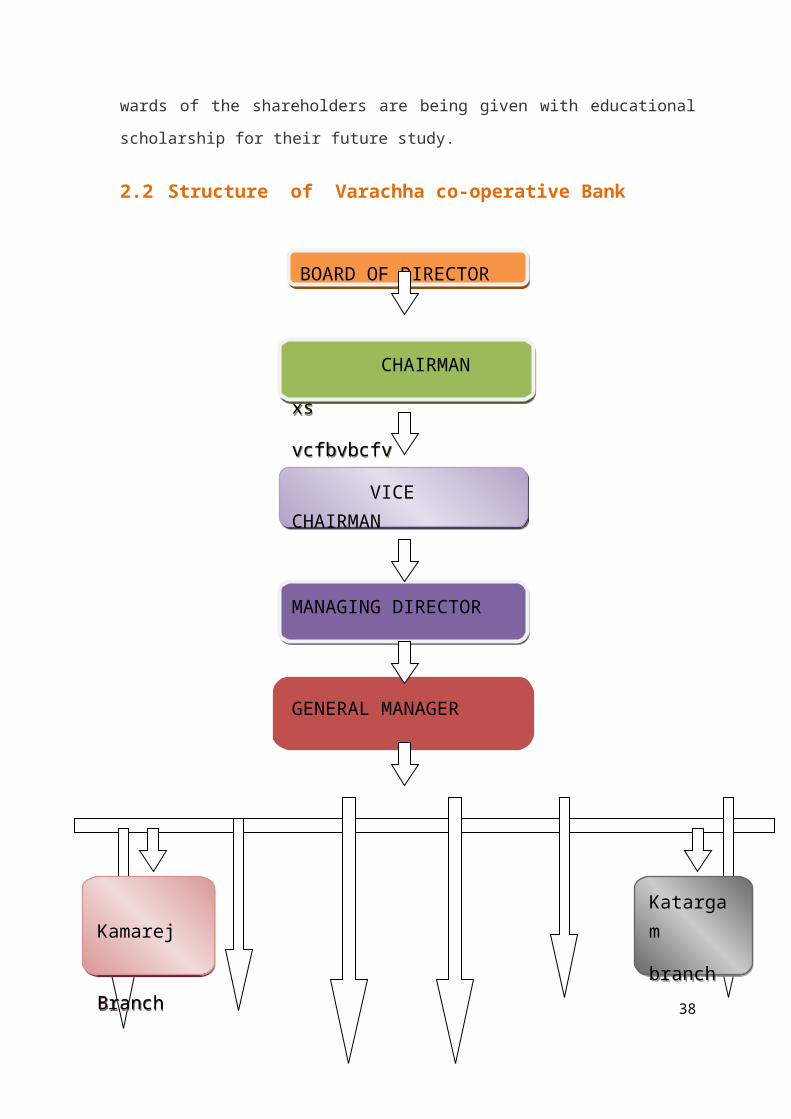

2.2Structure of Varachha co-operative Bank

28

BOARD OF DIRECTORBOARD OF DIRECTOR

CHAIRMAN

xs

vcfbvbcfv

CHAIRMAN

xs

vcfbvbcfv

VICE CHAIRMAN VICE CHAIRMAN

MANAGING DIRECTORMANAGING DIRECTOR

GENERAL MANAGER

Ring oad Branch

Ring oad Branch

Kamarej

Branch

Kamarej

Branch

Head Office

Head Office

Punagam

branch

Punagam

branch

Katargam

branch

Katargam

branch

Sachine

branch

Sachine

branch

2.3 Introduction of Board of directors

NO. NAME POSITION

1 Shree P.B.Dhankecha Est.Chairmen

2 Shree Kanjibhai R.Bhalala Chairmen

3 Shree Prabhudas T.Patel Vice Chairmen

4 Shree Bhavanbhai B.Navapara Managing Director

5 Shree Lavajibhai M.Nakarani Director

6 Shree Vallbhabhai P.Savani Director

7 Shree Kanjibhai R.Vadariya Director

8 Shree Babubhai V. Mangukiya Director

9 Shree G.R.Asodariya Director

10 Shree Jivarajbhai K.Patel Director

11 Shree Vimalaben R.Vaghani Director

12 Shree A.D.Bhalani(Head office) General Manager

13 Shree Viththalbhai B.Dhanani Assi.General Manager

29

Kadodra

branch

Kadodra

branch

Kapodra

branch branch

Kapodra

branch branch

2.4 Different branches of the Varachha Co-operative

Bank

The development of The Varachha Co- Operative Bank was continuously increasing

after two and half year from establishing of Head Office. We can know more above bank

from given a table of Branch establishment. The Varachha Cooperative Bank was not

needed take loan from government sector and other. For Developing and Vested it's branch

so progress table as under.

Head office:

Branch manager: Mr. sureshbhai d. kakadiya

Establish date: 16/10/1995

Address: affil tower: L.H.Road,surat.

Kamrej branch:

Branch manager: Mr. arvindbhai v. patel

Establish date: 7/6/1998

Address: Bhavani Complex, Kamrej Char Rasta, Surat.

Ring road branch:

Branch manager: Mr nitinbhai m.lad

Establish date: 4/7/1999

Address: first floor vankarsandh buildind opp.juss market.

30

Kadodra branch:

Branch manager: Mr dilipbhai s. bhuva

Establish date: 2/7/2000

Address: Thakorji Complex, Kadodara Char Rasta, Surat.

Kapodra branch:

Branch manager: Mr bholabhai c. sorthiya

Establish date: 28/1/2001

Katargam branch:

Branch manager: Mr. mukeshbhai p. malviya

Establish date:26/2/2001

Address: Sardar Complex, Nr. Anath Asram, Katargam Main

road ,surat.

Punagam branch:

Branch manager: Mr. pareshbhai d. kelavala

Establish date:16/10/2008,

. Address:” resma resident”,V.I.P.Road, Nr. Kenal, surat.

Sachine branch:

Branch manager:Mr. shileshbhai m. bhut

31

Address: "Visvas Bhavan" Nr. Shiddh Kutir temple,kapodra,

Varachha road,surat.

Establish date:8/5/2011

Address:c-g,12-15,c-complex laxmivila township G.I.D.C.

2.5 Services of Varachha co-operations of the bank

1) Net Banking Service

Bank Started Net Banking Service for their respective customer since 02-Oct-2009. With

help of Net Banking customer can view his/her account related information like

statement, inward clearing, outward clearing etc. from anywhere.

2) Any Branch Banking (ABB)

Customer can transact his/her account from any branches of the bank like cash receipt,

payment, transfer, balance inquiry,statement/passbook printing, deposit outward clearing

etc.

3) CCTV Monitoring

Bank’s all branches has CCTV Camera and all this connected and monitored at Head

Office. With the help of CCTV Bank is able to search any fraud with customer or

employee of the bank.

4) E-Payment Facility

Bank has started E-payment facility for the customers of the Bank for the purpose of

payment of Income-Tax.

32

5) Personalized Cheque Book

Personalized Cheque Book is being issued to all the customers of the Bank.

6) RTGS/NEFT Facility

Real Time Gross Settlement/ National Electronic Fund Transfer Facility available to the

customer of the bank. By this facility customer can transfer his balance throughout India

of any Banks, which is member of RTGS/NEFT.

7) Mobile Banking System

Now you can get the information such as Balances, Transaction Details, Cheque Status,

Deposit rates and much more… sitting at your home or office.Bank has a centralized

mobile banking facility. Through this facility customer can know his/ her balance via

SMS for getting various details about their accounts like Current Balance, Cheque Return

Status, FD Rates, Loan Rates etc. Bank also send regularly SMS to the registered

customer like cheque Inward/ Outward return details, FD rates, any event etc.

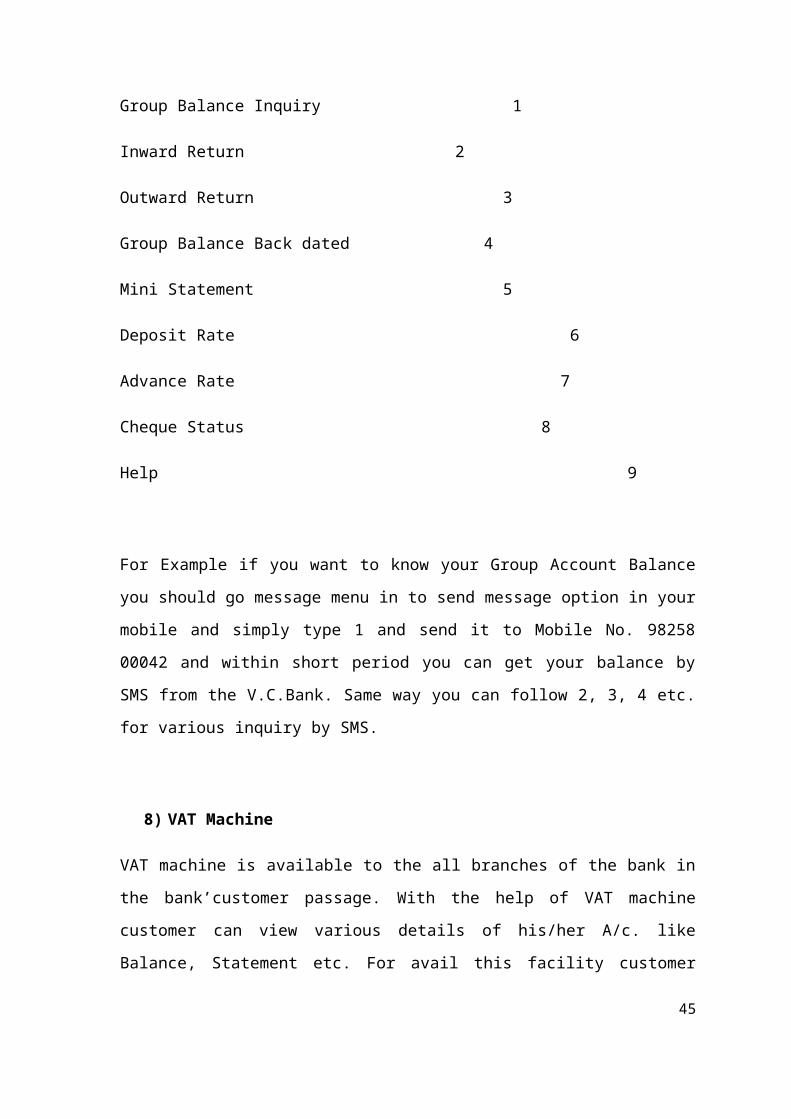

Facility

(See Example given below) Message Type

Group Balance Inquiry 1

Inward Return 2

Outward Return 3

Group Balance Back dated 4

Mini Statement 5

Deposit Rate 6

Advance Rate 7

Cheque Status 833

Help 9

For Example if you want to know your Group Account Balance you should go message

menu in to send message option in your mobile and simply type 1 and send it to Mobile

No. 98258 00042 and within short period you can get your balance by SMS from the

V.C.Bank. Same way you can follow 2, 3, 4 etc. for various inquiry by SMS.

8) VAT Machine

VAT machine is available to the all branches of the bank in the bank’customer passage.

With the help of VAT machine customer can view various details of his/her A/c. like

Balance, Statement etc. For avail this facility customer should have registered his account

with bank and get 4 digit password from the bank’s Officials.

9) Locker Facility

Locker Facility is also available at Bank’s Kamrej, Kapodra and Katargam Branches with

nominal rental. There is various types of locker followed by it’s size.

10)franking machine

franking Machine under license from Government for stamping of NonJudicial Stamp

arranged by Revenue Dept. of Gujarat State.

34

2.6 DAY TO DAY OPERATION

New account department:

New Account is opened as well as old accounts are closed in this department.

Accounts are of three types:

i. Current Account.

ii. Saving Account.

iii. Cash Credit Overdraft Account.

Daily nearly on an average about 10 to 12 current accounts and 15 to 20 saving

account are opened and 1 or 2 are closed every day the procedure for opening new

accounts in the bank starts with fill up the form given by bank. The bank has

requirements for opening a current account is two photographs of the account holder and

if the account is opened for company or firm then the photograph of the directors or

proprietors or administrator, the sign and account number of the person who wants to

open a new account in the bank and license of the firm. To open saving account only one

photograph of account holder, signature of account holder in the same bank as well as

papers or documents which give true and pair residential address such as driving license,

rationing card, light or phone bill, school living certificate etc.

The minimum balance for current account is Rs.5000 and the minimum balance

for saving account is Rs.1100. Any account holder, current or saving, can’t close his

account before completion of six months in the bank. Closing of new account is

somewhat difficult task as each and every aspect of the account is to be noted. The

charges Rs.210 are cut and remaining amount is given back to customer through the issue

of cheque book of the same amount. The cheque book of the close account is taken back

by bank is stored with the account close form. The bank provides service of cash credit

and overdraft against for the current account holders.

Issue of cheque book and pass book:

35

This is important department of the bank. In this department new passbook and

cheque book are issued. The new account department gives details of new customers and

according to that new cheque book and passbook are issued.

This department consists of only one employee who gives cheque book and passbook to

the customers. Customers who are in need of a new cheque book have to apply a day

before with a counter given in the old cheque book. For each account holder it is

compulsory to allow at least five cheques to be cleared or presented to bank for issuing a

new cheque book. Daily 70 to 75 new cheque books are issued to the customers.

As the bank is fully computerized if changes are made by customer in cheque

book, the computer will reject the cheque number because the while issuing cheque book

the number of cheque are recorded in the computer.

Draft Department:

Draft is another department of the bank. As this bank is in no co-operative sector

it has limited branches in surat. It does not have any branch in any other part of the

country. So in order to provide draft service of different cities to its customers it has

associated with certain banks.

If a customer wants a draft for Bombay, a bank must have its branch which can discount

the draft and if the bank do not have a branch than it has to joint with other bank.

Clearing Department: -

The most important department of the bank is clearing department. This

department has maximum number of employees. Nearly about seven or eight person are

continuously working in this department. Clearing per day is nearly about three or four

crores. Clearing house of all banks in surat is situated at Sate Bank of India, Nanpura,

Surat. Clearing which is collected from the clearing house is known as outward clearing.

Token Department:-

36

The next department of the bank is the Token department. It is small but

department with only one employee. The working hours of this department is from 10:00

am to 3:00 pm. Token is issued after various strict verification of cheque such as

signature amount in figure as well as in words etc. This department is small but full of

responsibility. Bank has a special service for its customers that is up to Rs.10,000 for

saving account holders and no limit for current account holders can be withdrawn directly

from the cash counts without the procedure of Toker.

Transfer Department: -

The next department is transfer. There is only one employee in this department. In

this department the cheque of the same bank is transferred from one account to other

account of customers. The entry of other department such as IBC (Inter Bill Collection)

etc. is done from this department.

2.7 VARIOUS TYPES OF DEPOSIT ACCOUNTS IN VARACHHA

BANK:-

Bank Account:

The bank accepted deposits from the public and offers facilitates to the public according

to their requirements and economic status. Though bank accepts deposits as a fund-

raising device. Its primary aim is to serve the society as financial institution and lend its

might to strengthen the capital market. Keeping all these in video a bank usually offers

three types of accounts in which it accepts deposits.

1) Fixed Time Deposit Account

2) Saving Deposit Account

3) Current Account

37

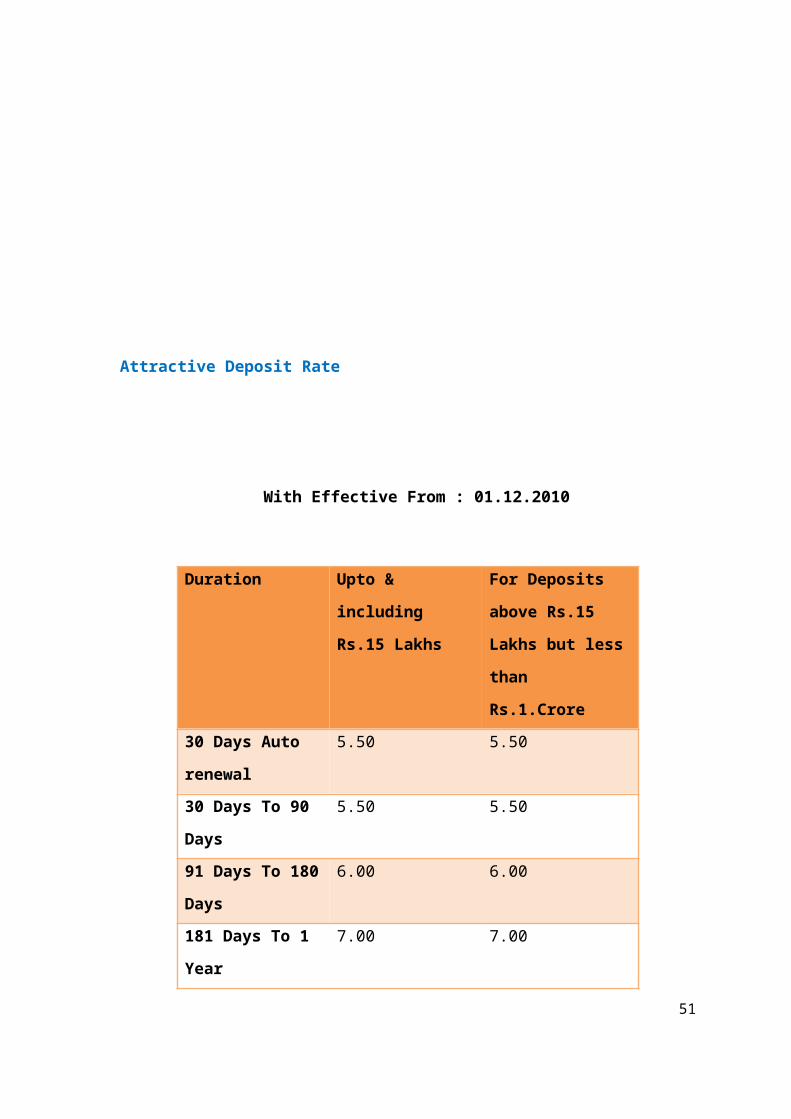

Attractive Deposit Rate

With Effective From : 01.12.2010

Duration Upto & including

Rs.15 Lakhs

For Deposits above

Rs.15 Lakhs but less

than Rs.1.Crore

30 Days Auto

renewal

5.50 5.50

30 Days To 90 Days 5.50 5.50

91 Days To 180

Days

6.00 6.00

181 Days To 1 Year 7.00 7.00

1 Year To 2 Year

Below

7.50 7.50

2 Year To 3 Year

Below

8.00 8.00

3 Year To to above 8.50 8.50

MANAGEMENT TOWARDS PROVISION FOR PROFIT

DISTRIBUTION

Net Profit

38

Deducted Provision

Reserve Fund 25 %

Share Dividend 12 %

Dividend Equalization Fund 15 %

Education Fund -

I.F.R. Reserve -

Total -

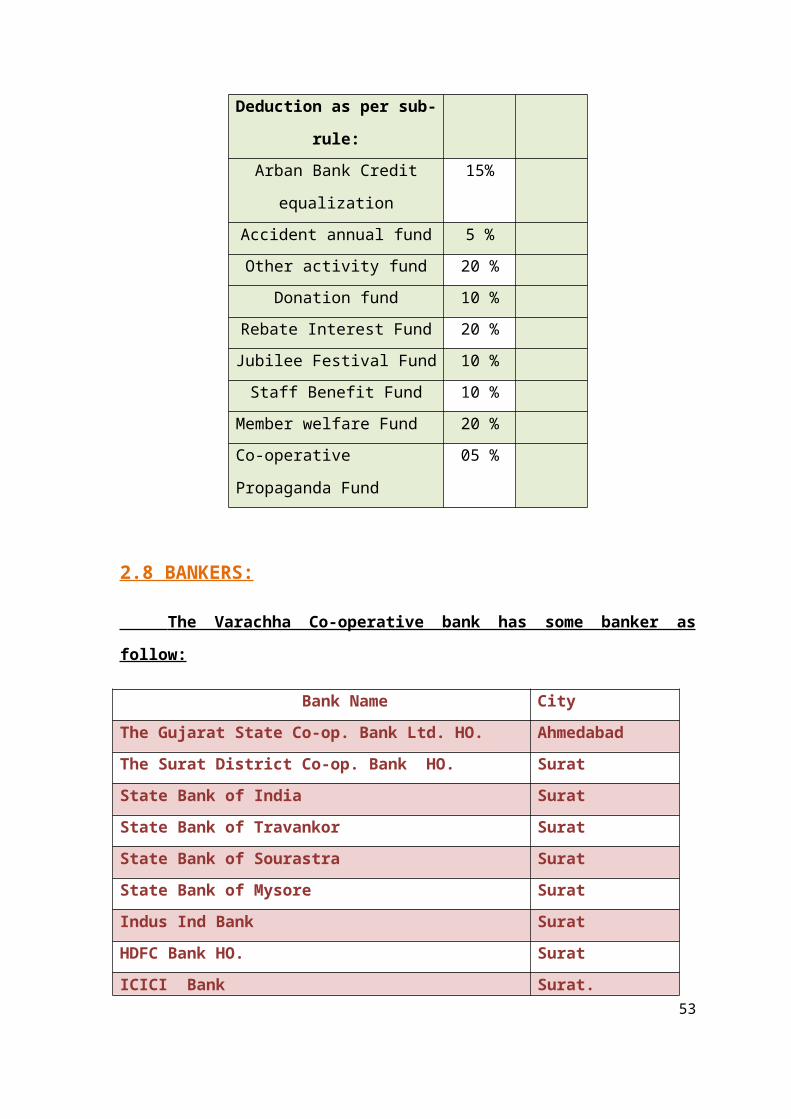

Rest Profit

Deduction as per sub-rule:

Arban Bank Credit

equalization

15%

Accident annual fund 5 %

Other activity fund 20 %

Donation fund 10 %

Rebate Interest Fund 20 %

Jubilee Festival Fund 10 %

Staff Benefit Fund 10 %

Member welfare Fund 20 %

Co-operative Propaganda Fund 05 %

2.8 BANKERS:

The Varachha Co-operative bank has some banker as follow:

Bank Name City

The Gujarat State Co-op. Bank Ltd. HO. Ahmedabad

39

The Surat District Co-op. Bank HO. Surat

State Bank of India Surat

State Bank of Travankor Surat

State Bank of Sourastra Surat

State Bank of Mysore Surat

Indus Ind Bank Surat

HDFC Bank HO. Surat

ICICI Bank Surat.

2.9 OBJECTIVES OF BANK

To give possible help and necessary guidance to members of the bank in the

conduct of business.

To do every kind of trust and agency business and particularly do the work

investment of funds, sale of properties and of recovery or acceptance of money.

To accept money document, security calculate article and goods every description

for keeping them in safe custody or for sending them from one place to other.

To act as a balancing center for surplus funds of co-operative societies.To

organize and develop co-operative societies within the district.

To redeem old debts.

To lend money on security to its members

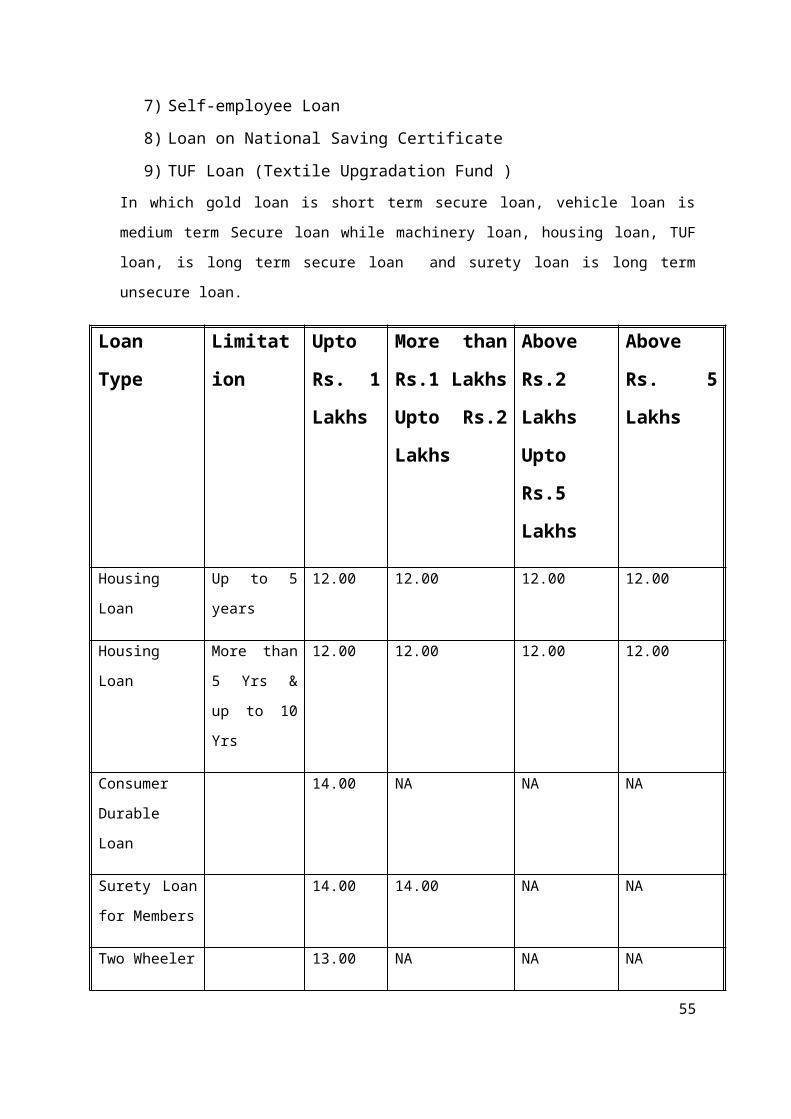

2.10 BANK PROVIDES VARIOUS TYPES OF LOANS:

1) Mortgage Loan

2) Security Loan on Bank’s Share Certificate

3) Vehicle Loan

4) Cash Credit Loan

5) Machinery Loan

6) Term Loan

40

7) Self-employee Loan

8) Loan on National Saving Certificate

9) TUF Loan (Textile Upgradation Fund )

In which gold loan is short term secure loan, vehicle loan is medium term Secure loan while

machinery loan, housing loan, TUF loan, is long term secure loan and surety loan is long term

unsecure loan.

Loan Type Limitation Upto

Rs. 1

Lakhs

More than

Rs.1 Lakhs

Upto Rs.2

Lakhs

Above

Rs.2 Lakhs

Upto Rs.5

Lakhs

Above Rs.

5 Lakhs

Housing Loan Up to 5 years 12.00 12.00 12.00 12.00

Housing Loan More than 5

Yrs & up to

10 Yrs

12.00 12.00 12.00 12.00

Consumer

Durable Loan

14.00 NA NA NA

Surety Loan for

Members

14.00 14.00 NA NA

Two Wheeler 13.00 NA NA NA

For New Cars 12.00 12.00 12.00 12.00

Cash Credit 13.00 13.00 13.00 12.00

Machinery Term

Loan

13.00 13.00 13.00 13.00

Loan Against

Gold Ornaments

11.00 NA NA NA

41

Self Employed

Loan

11.00 11.00 11.00 11.00

Machinery TUF

Loan

13.00 13.00 13.00 13.00

GOLD LOAN:

The bank gives gold loan to customers or people on pledge of ornament of gold. First

guessing the value of ornament by the goldsmith of bank. bank give gold loan for one

year and the amount of interest paid in within month and bank give loan maximum

Rs.100000/-there is no interest rebate facility not available

Document which is require in gold loan:

- photo

- Driving licenses/election card/passport (any one)

- Electricity bill/gas bill/telephone bill

- municipal tax bill

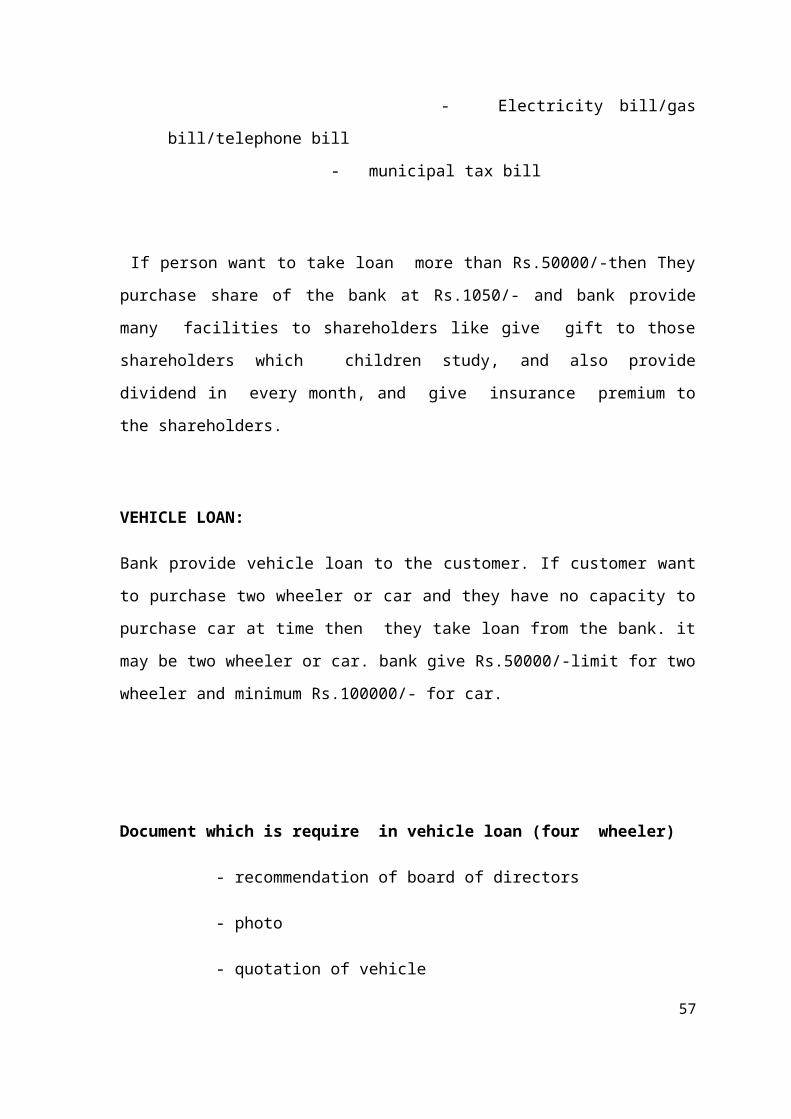

If person want to take loan more than Rs.50000/-then They purchase share of the bank at

Rs.1050/- and bank provide many facilities to shareholders like give gift to those

shareholders which children study, and also provide dividend in every month, and give

insurance premium to the shareholders.

VEHICLE LOAN:

Bank provide vehicle loan to the customer. If customer want to purchase two wheeler or

car and they have no capacity to purchase car at time then they take loan from the bank.

it may be two wheeler or car. bank give Rs.50000/-limit for two wheeler and minimum

Rs.100000/- for car.

42

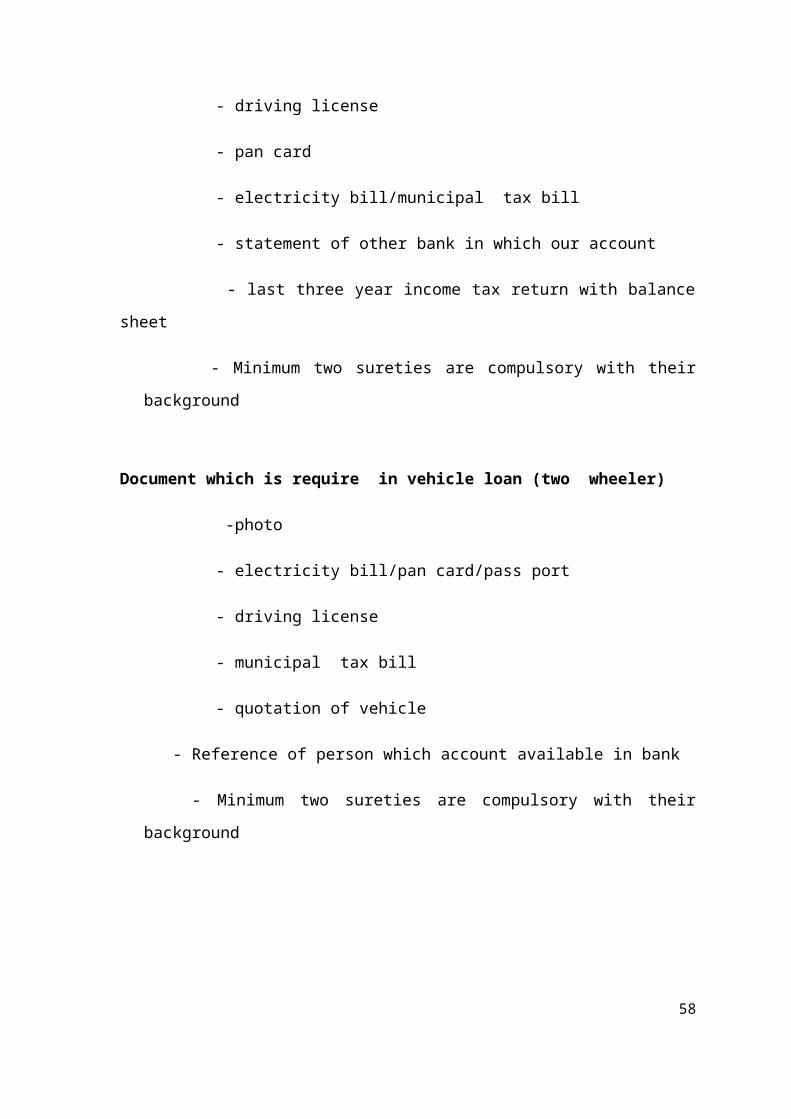

Document which is require in vehicle loan (four wheeler)

- recommendation of board of directors

- photo

- quotation of vehicle

- driving license

- pan card

- electricity bill/municipal tax bill

- statement of other bank in which our account

- last three year income tax return with balance sheet

- Minimum two sureties are compulsory with their background

Document which is require in vehicle loan (two wheeler)

-photo

- electricity bill/pan card/pass port

- driving license

- municipal tax bill

- quotation of vehicle

- Reference of person which account available in bank

- Minimum two sureties are compulsory with their background

43

SURETY LOAN:

Surety loan is given to those person who are shareholder of the bank and there account is

available from last six month. And the rate of interest is 14.00% and it is given for 5 years

if customer want to take loan for 1 year then bank also provide.

Document which is require in surety loan

- reference of director of varachha bank

- photo(2)

- electricity bill/pan card/pass port

- driving license

- municipal tax bill

- share certificate

- last three year income tax return with balance sheet

- Minimum two sureties are compulsory with their background

HOUSING LOAN :

This loan provide for construction, additions, alteration, repair of the house etc. in the

form of long-term period. Bank charge @ 12%.Bank give 1.00% rebate to those

customers who pay timely interest and Installment of the loan.

Document which is require in housing loan;

- recommendation of board of directors

- photo (2)

44

- driving license

- pan card

- electricity bill/municipal tax bill

- statement of other bank in which our account

- Minimum two sureties are compulsory with their background

(out of their family member)

-last three year income tax return with balance sheet etc…

CASH CREDIT LOAN:-

Bank provide cash credit facility to their customer.bank charge 13.00% interest up to

Rs.500000/-and if customer want to take more than Rs.500000/- then bank charge

12.00% interest From borrower. The customer as per his fungible or security can take a

loan up to that specified limit. The customer can withdraw money from his account,

which is called cash credit account.

MACHINERY LOAN(TUF):

TUF means Technology Upgradation Fund Under this project government has distributed

subsidy of Rs.250 million. This type of the loan is given for purchase new or secondary

textile machinery, bank grant loan up to 70% face value of bill of textile machinery. In

this scheme borrows get subsidy decided by the government. On such loan bank may

charge at the rate of 13% interests.

Loan limit Rate of interest rebate

Up to 25.00 lac 13 1

25.00 lac to 50.00 lac 13 1.5

Above 50.00 lac 13 2

45

This limit for TUF loan as well as machinery loan.

2.11SOCIAL CONTRIBUTION

Arrange blood donation camps at regular interval time to time

On 2nd October 2008 Bank has arranged Mega Blood Donation Camp and collected 2222

bottles of blood. Bank gives Rs.50000/- accident insurance cover to all the blood

donors.Again on 2nd October 2009 Bank has arranged Mega Blood Donation Camp and

collected 3456 bottles of blood. Bank gives Rs.50000/- accident insurance cover to all the

blooddonors.

Accident Insurance

Bank has taken Group Insurance Policy every year for its valued Share Holders and

Customers for Rs.50000/- to Rs.300000/- [Depending upon various accounts]. Under this

service, insurance company paid approximately Rs.1.25 Crore to its Share Holders and

Customers through bank.

Active Role in Samuh Lagna [Mass Marriage System]

Bank employees had actively participated and helpful in Mass Marriage System

organized by Saurashtra Patel Seva Samaj from time to time in various ways.

2.12 AWARDs

Surat Jilla Sahkari Sangh:- Photograph : Shield

Award received by Shri P. B.dhakecha

46

Rashtriya Vikas Ratan Gold Award:-Rashtriya

Vikas Ratan Gold Award from International Integration &

Growth.

Rashtriya Vikas Ratan Gold Award:-

Photograph : Rashtriya Vikas Ratan Gold Award Received.

The South Guj. Co-op. Bank's Association

Ltd., Surat:- Award received from The SouthGuj.

Co-op.bank's association Ltd.

47

Best Co-op. Bank in Surat Dist. for the year

2007-2008:- Best Co-op. Bank in Surat Dist. for the year

2007-2008.

Best Co-op. Bank in Surat Dist. for the year

2007-2008:- Photograph: Shield Award 2007-08

received.

Highest Blood Donation Collection Award-

2008:- Award received from Lok Samrpan Blood Bank, Surat

for Highest.

48

51

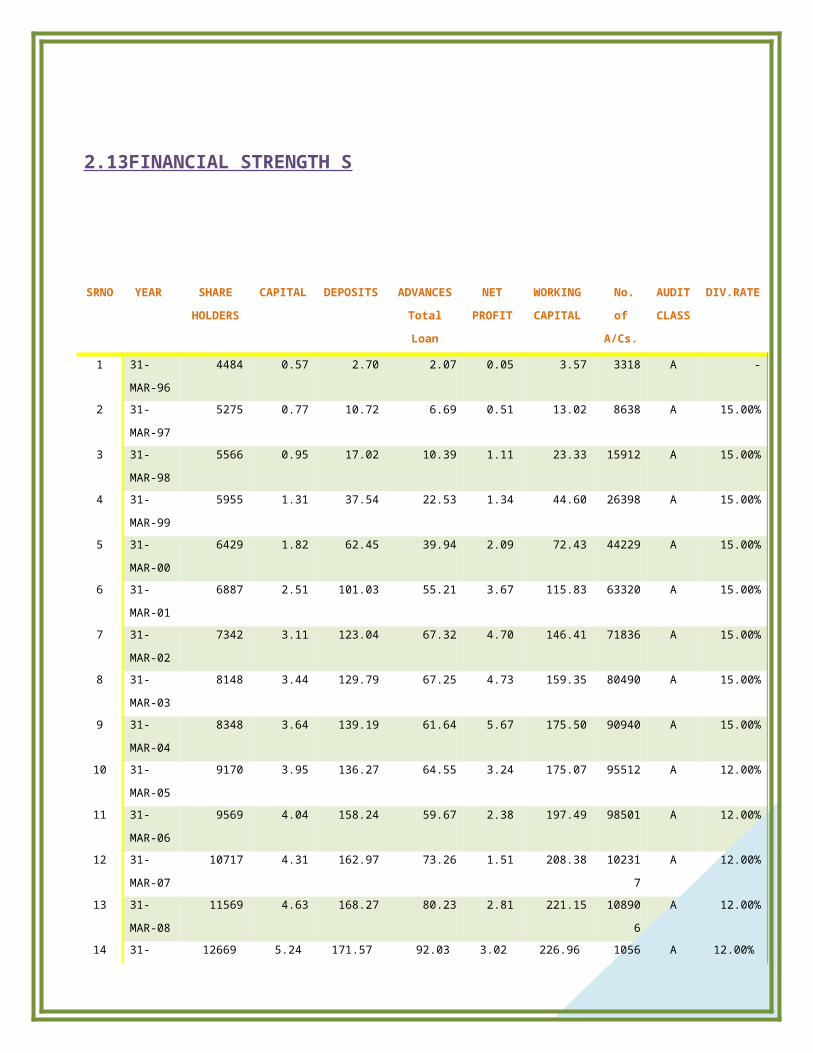

2.13FINANCIAL STRENGTH S

SRNO YEAR SHARE

HOLDERS

CAPITAL DEPOSITS ADVANCES

Total Loan

NET

PROFIT

WORKING

CAPITAL

No. of

A/Cs.

AUDIT

CLASS

DIV.RATE

1 31-

MAR-96

4484 0.57 2.70 2.07 0.05 3.57 3318 A -

2 31-

MAR-97

5275 0.77 10.72 6.69 0.51 13.02 8638 A 15.00%

3 31-

MAR-98

5566 0.95 17.02 10.39 1.11 23.33 15912 A 15.00%

4 31-

MAR-99

5955 1.31 37.54 22.53 1.34 44.60 26398 A 15.00%

5 31-

MAR-00

6429 1.82 62.45 39.94 2.09 72.43 44229 A 15.00%

6 31-

MAR-01

6887 2.51 101.03 55.21 3.67 115.83 63320 A 15.00%

7 31-

MAR-02

7342 3.11 123.04 67.32 4.70 146.41 71836 A 15.00%

8 31-

MAR-03

8148 3.44 129.79 67.25 4.73 159.35 80490 A 15.00%

9 31-

MAR-04

8348 3.64 139.19 61.64 5.67 175.50 90940 A 15.00%

10 31-

MAR-05

9170 3.95 136.27 64.55 3.24 175.07 95512 A 12.00%

11 31-

MAR-06

9569 4.04 158.24 59.67 2.38 197.49 98501 A 12.00%

12 31-

MAR-07

10717 4.31 162.97 73.26 1.51 208.38 102317 A 12.00%

13 31-

MAR-08

11569 4.63 168.27 80.23 2.81 221.15 108906 A 12.00%

14 31-

MAR-09

12669 5.24 171.57 92.03 3.02 226.96 105674 A 12.00%

15 31-

MAR-10

13566 5.91 224.16 94.89 3.15 279.11 123260 A 12.00%

51

51

3.1 Research problem:

3.2Objective of financial department:

To analyses the present financial system of The Varachha Co-Operative Bank Ltd.

To study financial strength and weakness of The Varachha Co-Operative Bank Ltd.

To get basis for financial planning, analysis and decision making through financial

information.

3.3 Period of coverage:

I have chooses the period of coverage for the financial years i.e. 2006-2007 to 2010-2011

3.4 Source of Data:

Primary data: primary data will collect through discussion with executive & staff of the

bank.

Secondary data: annual report, magazine, and data from the bank borrow itself.

3.5 Scope of the Study:

51

3.6 Research Design

There are three main types of research design

1. Exploratory design

In exploratory design the emphasis is on discovery of new ideas. The main objective of this

design is to generate new idea. The two ways of doing exploratory design is the focus group

interview & the case studies.

2. Descriptive studies

When a researcher is interested in knowing the characteristics of certain group such as age,

gender, education level, occupation, income, descriptive may be necessary. Descriptive

studies are factual and are very simple.

3. Causal design

As the name implies a causal design investigates the cause and effect relationship between

two or more variables. The two types of the causal designs are:

a) Natural experiments

b) Controlled experiments

The study report “Analysis of a financial Statement” is consider the descriptive research design.

3.7 Important of study:

51

3.8 Limitation of study:

51

3.9 Review of literature

51

51

51

4.1Introduction of Financial Statement analysis:

51

4.2 Objectives of Financial Statement:

51

4.3 Limitation of Financial Statement :

51

4.4 Financial Statement of VarachchavBank:

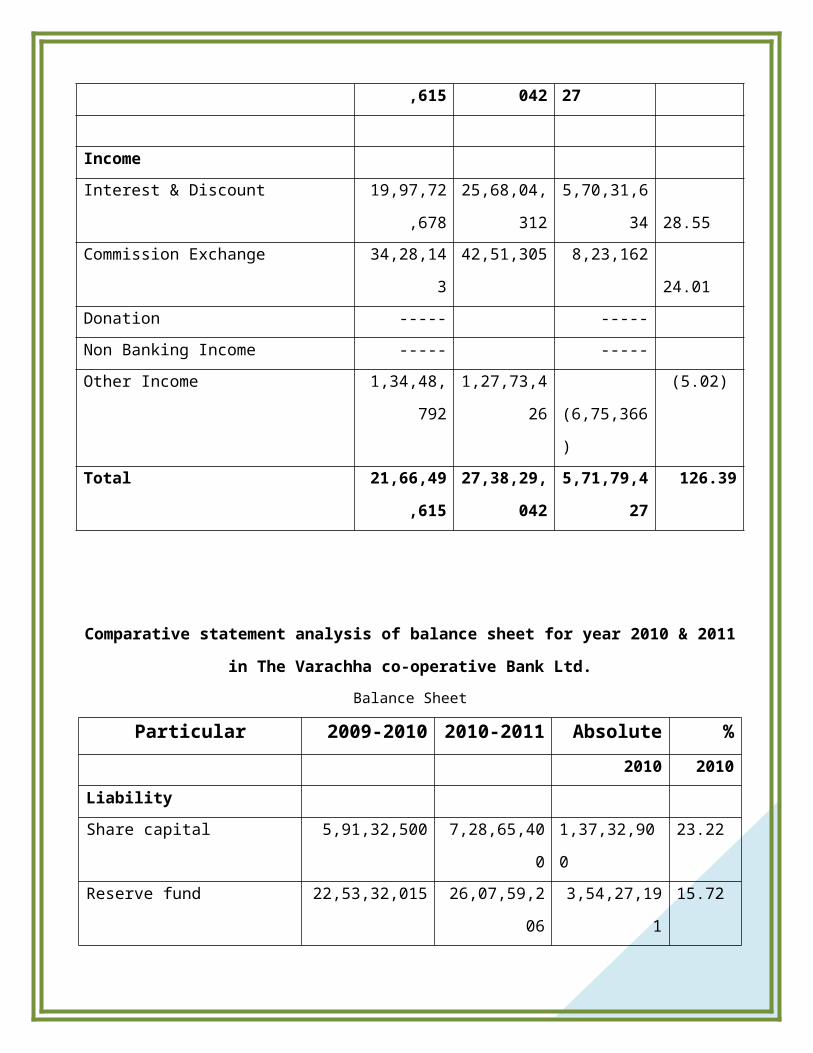

1] Profit & Loss Account:

51

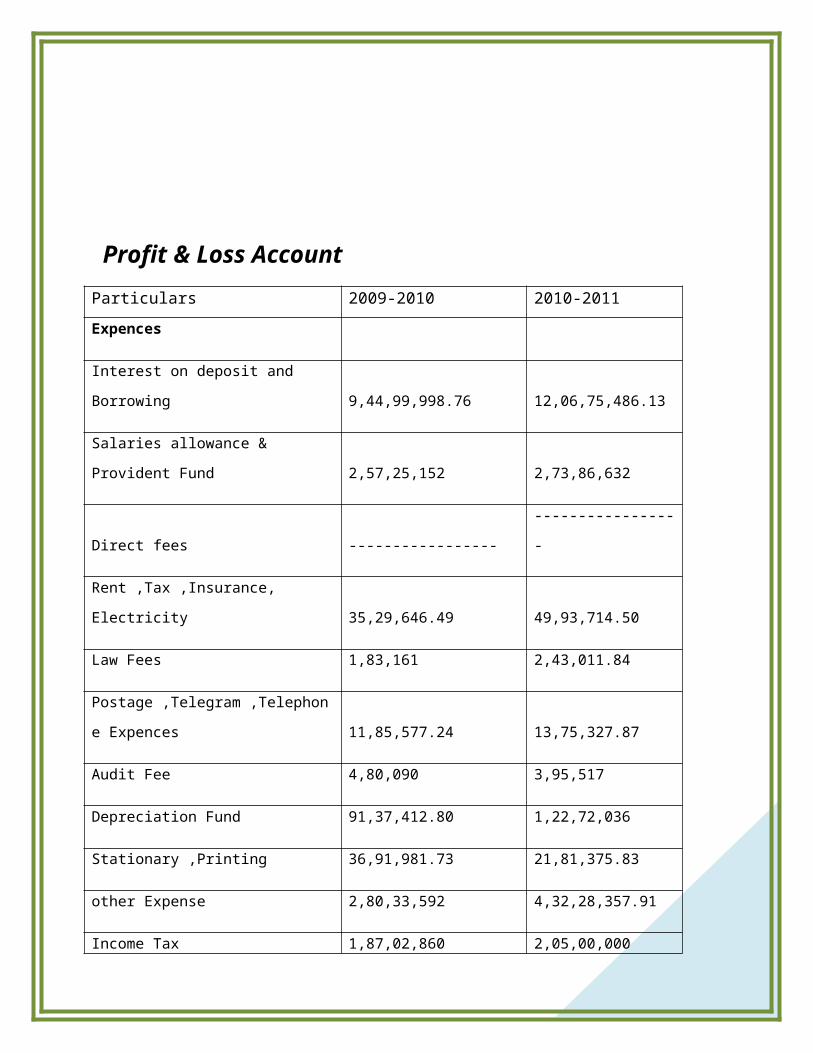

Profit & Loss Account

Particulars 2009-2010 2010-2011

Expences

Interest on deposit and Borrowing 9,44,99,998.76 12,06,75,486.13

51

Salaries allowance & Provident Fund 2,57,25,152 2,73,86,632

Direct fees ----------------- -----------------

Rent ,Tax ,Insurance, Electricity 35,29,646.49 49,93,714.50

Law Fees 1,83,161 2,43,011.84

Postage ,Telegram ,Telephone Expences 11,85,577.24 13,75,327.87

Audit Fee 4,80,090 3,95,517

Depreciation Fund 91,37,412.80 1,22,72,036

Stationary ,Printing 36,91,981.73 21,81,375.83

other Expense 2,80,33,592 4,32,28,357.91

Income Tax 1,87,02,860 2,05,00,000

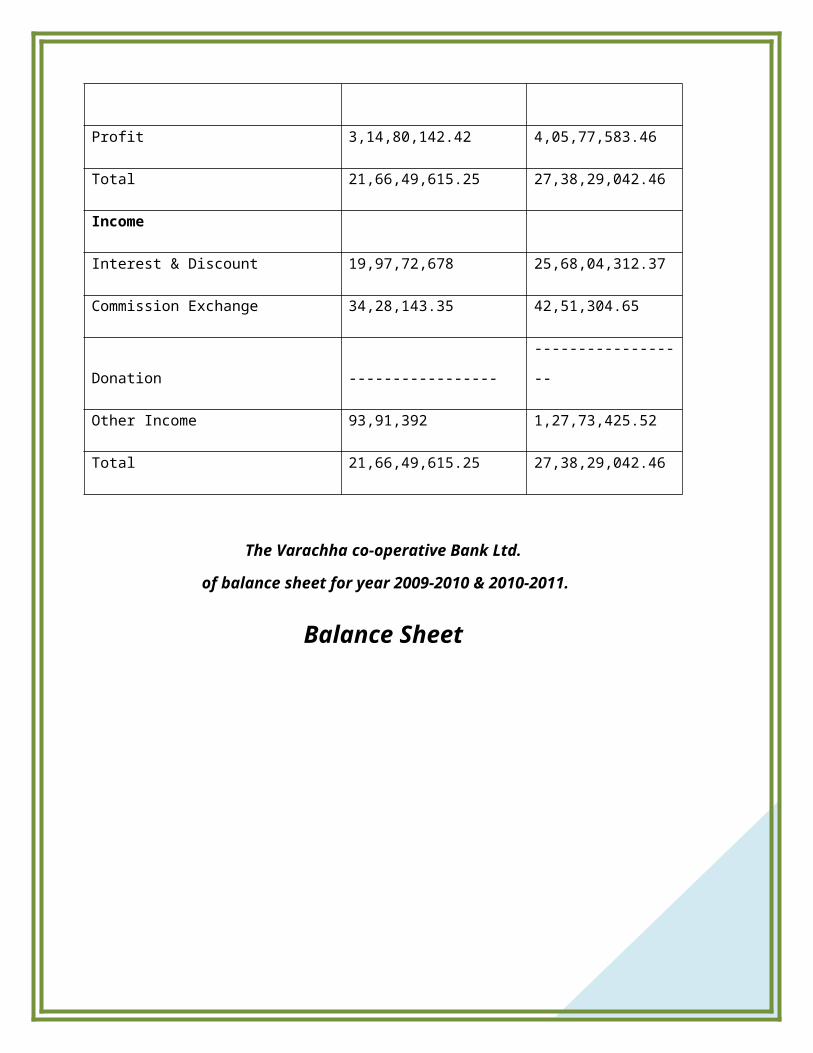

Profit 3,14,80,142.42 4,05,77,583.46

Total 21,66,49,615.25 27,38,29,042.46

Income

Interest & Discount 19,97,72,678 25,68,04,312.37

Commission Exchange 34,28,143.35 42,51,304.65

Donation ----------------- ------------------

Other Income 93,91,392 1,27,73,425.52

Total 21,66,49,615.25 27,38,29,042.46

The Varachha co-operative Bank Ltd.

of balance sheet for year 2009-2010 & 2010-2011.

Balance Sheet

51

Particular 2009-2010 2010-2011

Liability

Share capital 5,91,32,500 7,28,65,400

Reserve fund 40,99,81,617 26,07,59,206.11

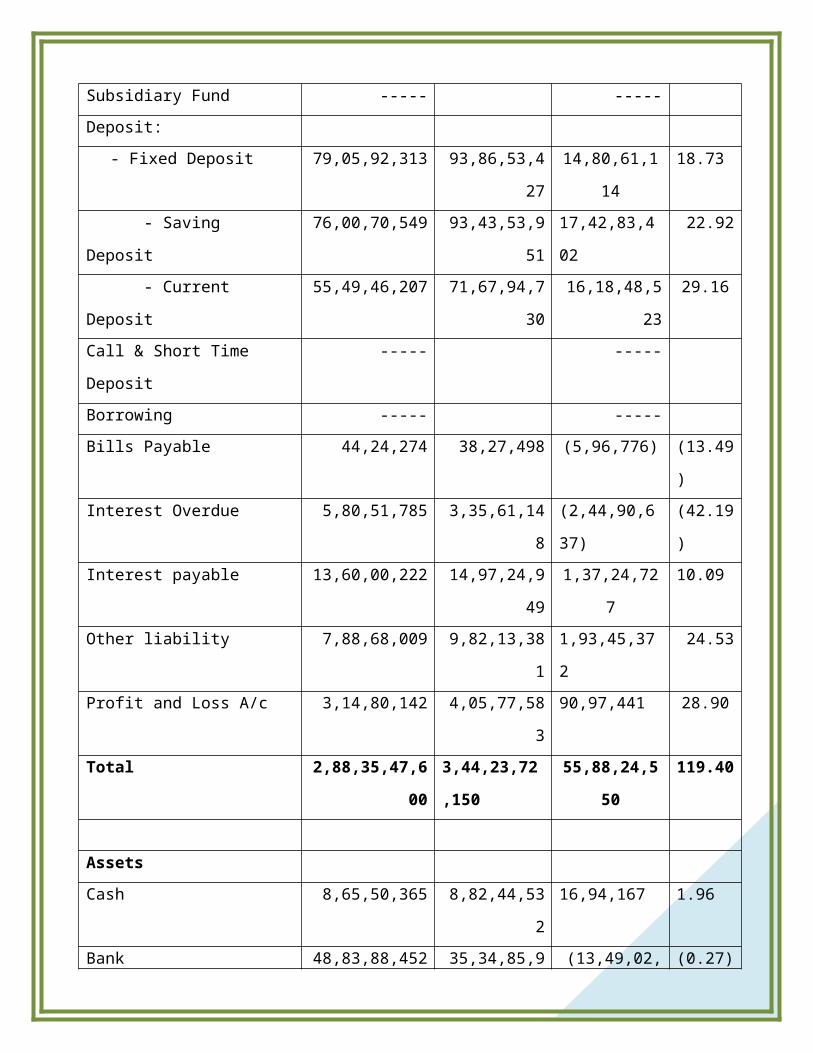

Subsidiary Fund -----

Deposit:

- Fixed Deposit 79,05,92,313 93,86,53,426.84

- Saving Deposit 76,00,70,549 93,43,53,950.77

- Current Deposit 55,49,46,207 71,67,94,729.78

Call & Short Time Deposit -----

Borrowing -----

Bills Payable 44,24,274 38,27,498

Interest Overdue 5,80,51,785 335,61,147.97

Interest payable 13,60,00,222 14,97,24,949

Other liability 7,88,68,009 9,82,13,380.70

Profit and Loss A/c 3,14,80,142 4,05,77,583.46

Total 2,88,35,47,600 3,44,23,72,149.87

Assets

Cash 8,65,50,365 8,82,44,531.98

Bank 48,83,88,452 35,34,85,910.13

Call & Short time Investment -----

Investment 117,95,03,022 1,67,11,43,767

Subsidiary Fund Invest -----

Loans and Advances

- Short term 31,56,02,553 31,43,99,482.44

- Moderate term 30,46,65,311 38,75,76,985.41

- Long term 32,85,98,967 45,68,21,245.85

Interest receivable 9,22,37,735 7,41,53,273.97

Bills Receivable 44,24,274 38,27,498

Branch adjustment -----

Building premises 2,45,05,702 3,71,90,031.97

Furniture & Fixture 1,16,70,414 1,78,92,950.86

Other Asset 4,74,00,800 3,68,36,472.26

Total 2,88,35,47,600 3,44,23,72,149.87

51

51

INRTODUCTION OF FINANCIAL DEPARTMENT:-

Meaning:-

According to Himpton John “A financial statement is an organized collection of data according to

logical and consistent accounting procedures. Its purpose is to convey an understanding of some

financial aspects of a business firm. It may show a position at a moment of time as in the case of a

balance sheet, or may reveal a series of activities over a given period of time as in the case on income

statement.”

TOOLS OF FINANCIAL STATEMENTS

As Kennedy and McMuller have,said,”The analysis and interpretation of financial statements are an

attempt to determine the significance and meaning of the financial statement data so that a forecast

may be made of the prospects for further earnings, ability to pay interest and debt maturities both

current and long term and probability of a sound dividend policy” .

51

The analysis consists of the study of inter relationship between various items comprised in

financial statements to determine whether the earnings and the financial position of the company are

satisfactory. A number of devices are used in the analysis of financial statements, some of which are

as follows:

(i) Comparative Statements

(ii) Common size statements

(iii) Trend Percentages

(iv) Cash flow Analysis

(v) Fund flow Analysis

(vi) Ratio Analysis

Comparative financial statement:

When financial statements of a few years are presented in columnar form, it indicates the trend of

changes taking place in business. The method of presenting both financial statements in columnar

form and of judging the trend of profitability and financial condition of business is known as

Comparative Statement Analysis. Generally form, though theoretically any other statement can be do

presented

If useful data is to be gathered from the analysis of financial statement, one must go beyond a single

year’s balance sheet and profit and loss account, as they suffer from following limitations.

(1) The balance sheet or profit and loss account of a single year does not show the nature and trend of

changes taking place in business.

(2) It does not give any idea about the position of incomes and expenses of current year in

comparison to those of previous year.

(3) Balance sheet of a single period fails to disclose whether the financial position of a company is

improving or deteriorating.

(4) If the reader of financial statements is interested in knowing financial and operating trends over a

period of years, it is necessary that the figures for different years, must be Presented together.

The comparative statements may also be presented in a manner that will show the percentages of

various figures with some significant item e.g. the percentage of gross profit to sales of the

previous year may be presented along with such percentage for the current year.

51

(a)Comparative Profit and Loss Accounts: The various items of profit and loss accounts may

be presented side by side which will show the trend of increasing or decreasing expenses or

incomes. Such changes may be shown in absolute figures of in percentage forms. While

examining the comparative examined.

(b) Comparative balance sheet: the change taking place in assets and liabilities over a period of

years are revealed by comparative balance sheets. Such comparative balance sheets may show

absolute figures or even percentage of various figures may be shown. Such percentages are

generally based on value of total assets.

Fund flow statement:

In a statement which shown the inflow and outflow of funds during the year, the meaning of the word

“fund” is working capital. The objective of preparing such a statement is to show to the management

and other interested parties, what funds have come into the business and how they have been applied.

A balance sheet is a static statement showing the conditions of assets and liabilities on a particular

date only. While the flow statement is dynamic statement showing changes that have taken place

during the year. E.g. if funds have been raised during the year by issuing further shares, the amount is

shown as source of funds in the statement. If any fixed asset is bought during the year, it is shown as

use or application of funds. The fund statement is therefore necessary to supplement the two basis

financial statement

This statement consist of two parts

i) Sources of Funds

ii) Application of Funds

Uses of fund flow statement

1. The fund flow statement acts as supplementary statement to the traditional financial statement

viz., balance sheet and profit and loss account

2. The funds flow statement furnishes the information about the sources from which the

company has mobilized the resources or fund during the year;

3. It also presents the detail which spell out clearly the manner in which the mobilized fund has

been utilized or employed during the year;

4. It also sheds light on the efficiency of management in the working capital management.

51

Cash flow statement:

The fund flow statement indicates changes in working capital which have taken place during the

year. But the management is more interested in the changes in cash inflow and outflow in the short

run. It is a historical statement which indicates the cash inflows and outflows during the last year and

would guide the management in framing policy regarding cash management. The cash budget shows

the projected inflows and outflows of cash for the future budget period, which the cash flow

statement is prepared on the basis of the basis of historical financial statements.

Use of cash flow statement

1. Cash flow statement facilitates to prepare sound financial policies. It also helps to evaluate the

current cash position.

2. A projected cash flow statement can be prepared in order to know the future cash position of a

concern so as to enable a firm to plan and coordinate its financial operations properly.

3. it helps the management in taking short-term financial decisions.

4. The statement explains the causes for poor cash position in spite of substantial profits in firms

by throwing light on various applications of cash made by the firm.

Common size Statements:-

Financial statements when read with absolute figures are not easily understandable. They are even

misleading the figures shown in profit & loss account and balance sheet are converted to percentage

so as to establish each element to the total figure of the statement and there statement are called

commonsize statements. When balance sheet and profit & loss account of the same concern for

several years or when balance sheet and profit & loss account of two or more than two concerns for

the same year are converted in to percentage form and presented as such, they are known as

comparative commonsize statement.

Interpretation:-

51

Profit & loss account figure is assumed to be equal to 100 and all other figure or expressed as

percentage to sales. Similarly, in balance sheet the total of assets and liability is taken as 100 and all

the figures are expressed as percentage of the total. The statement prepared is called “Commonsize

Statement.”

Trend Analysis:-

The comparative and Commonsize statements suffer from a major limitation that is absence of basic

standard to indicate whether the proportion of an item is normal or abnormal. Trend analysis

overcomes this limitation. This technique is also an important and useful of financial statement

analysis. The calculation of trend ratio involves the ascertainment of arithmetical relationship which

each item of several years to the same of base year.

This trend ratio is calculated only for some important item which can be logically converted with

other.

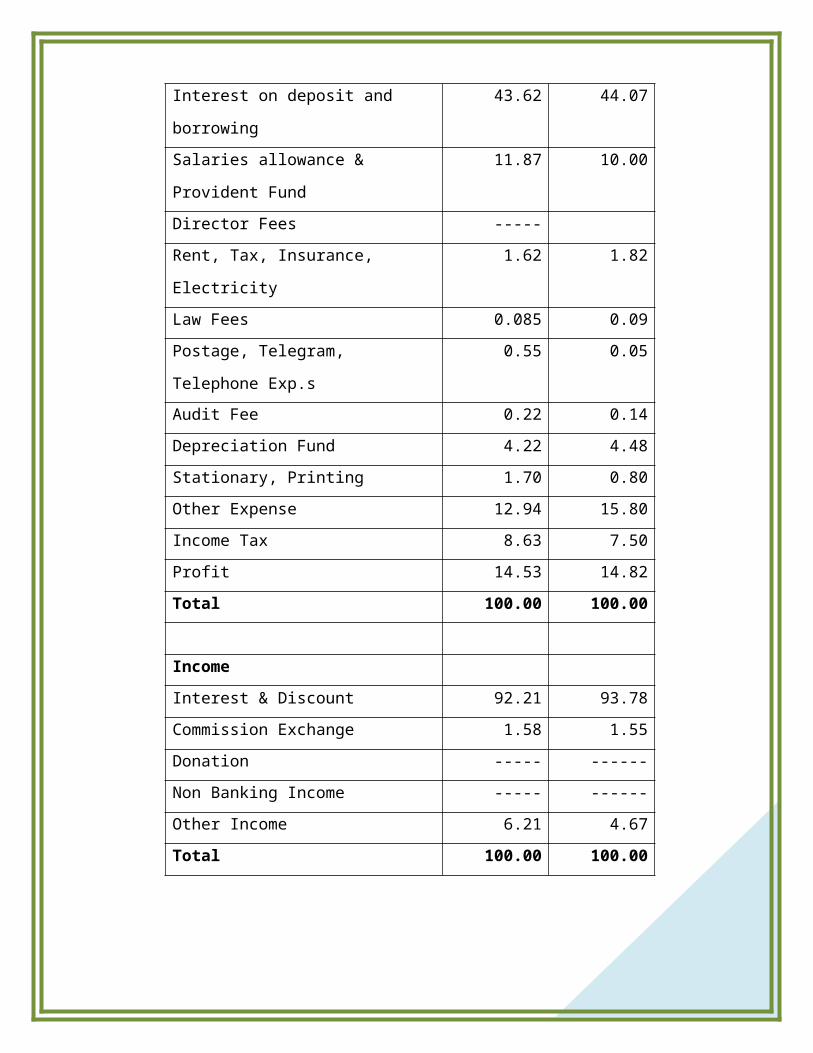

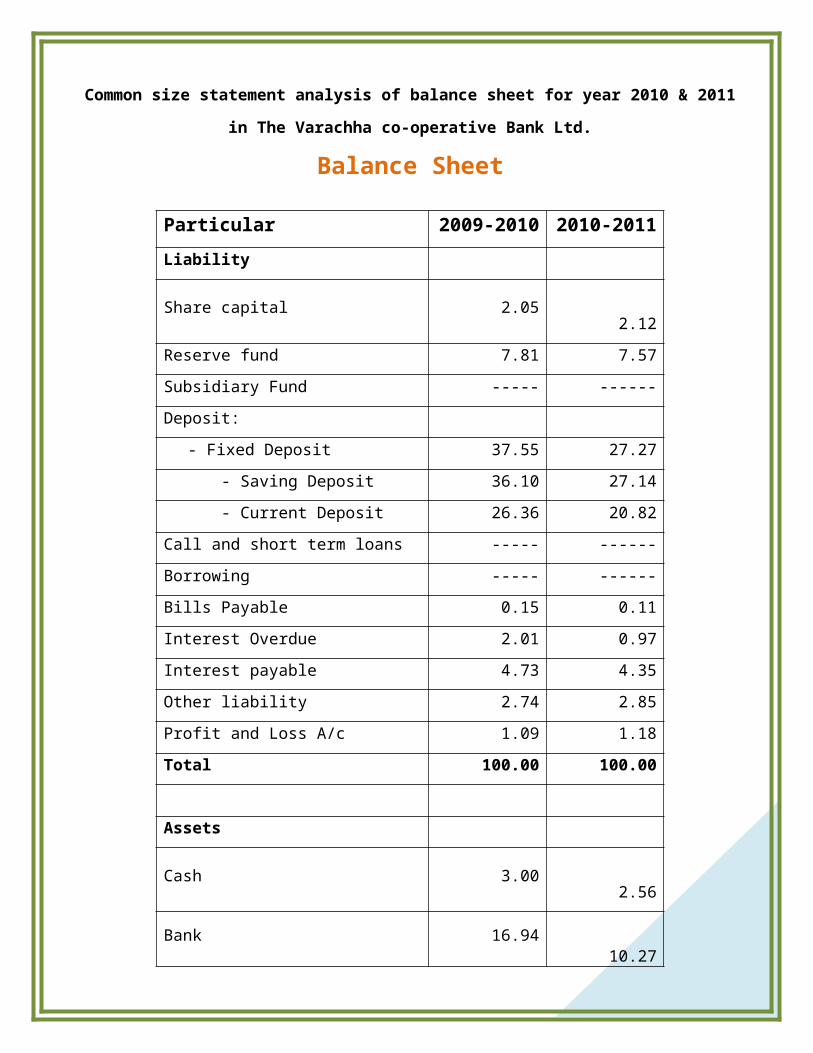

Common size statement analysis of Profit and loss account for year 2010 & 2011 in The

Varachha co-operative Bank Ltd.

Profit and loss account

Particular 2009-2010 2010-2011

Expense

Interest on deposit and borrowing 43.62 44.07

Salaries allowance & Provident Fund 11.87 10.00

Director Fees -----

Rent, Tax, Insurance, Electricity 1.62 1.82

Law Fees 0.085 0.09

Postage, Telegram, Telephone Exp.s 0.55 0.05

Audit Fee 0.22 0.14

51

Depreciation Fund 4.22 4.48

Stationary, Printing 1.70 0.80

Other Expense 12.94 15.80

Income Tax 8.63 7.50

Profit 14.53 14.82

Total 100.00 100.00

Income

Interest & Discount 92.21 93.78

Commission Exchange 1.58 1.55

Donation ----- ------

Non Banking Income ----- ------

Other Income 6.21 4.67

Total 100.00 100.00

Common size statement analysis of balance sheet for year 2010 & 2011 in The Varachha co-

operative Bank Ltd.

Balance Sheet

Particular 2009-2010 2010-2011

Liability

Share capital 2.05 2.12

Reserve fund 7.81 7.57

Subsidiary Fund ----- ------

Deposit:

- Fixed Deposit 37.55 27.27

- Saving Deposit 36.10 27.14

- Current Deposit 26.36 20.82

Call and short term loans ----- ------

Borrowing ----- ------

51

Bills Payable 0.15 0.11

Interest Overdue 2.01 0.97

Interest payable 4.73 4.35

Other liability 2.74 2.85

Profit and Loss A/c 1.09 1.18

Total 100.00 100.00

Assets

Cash 3.00 2.56

Bank 16.94 10.27

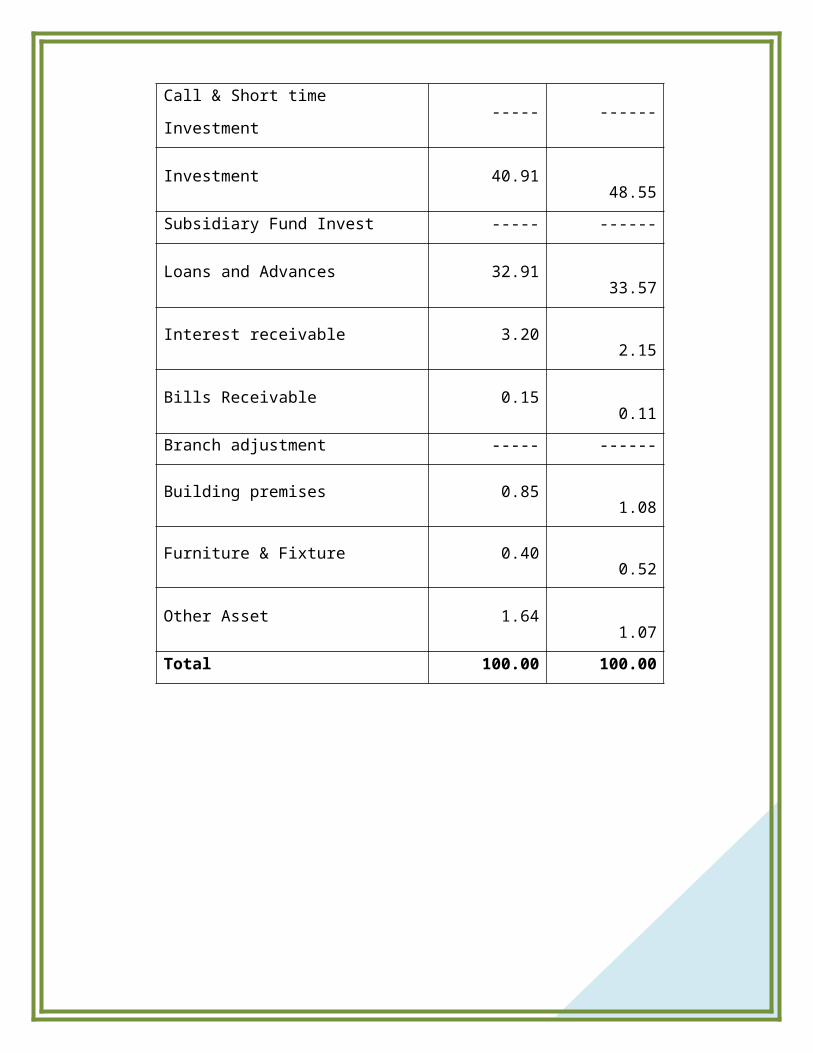

Call & Short time Investment ----- ------

Investment 40.91 48.55

Subsidiary Fund Invest ----- ------

Loans and Advances 32.91 33.57

Interest receivable 3.20 2.15

Bills Receivable 0.15 0.11

Branch adjustment ----- ------

Building premises 0.85 1.08

Furniture & Fixture 0.40 0.52

Other Asset 1.64 1.07

Total 100.00 100.00

51

Comparative statement analysis of profit and loss account for year 2010 & 2011 in The

Varachha co-operative Bank Ltd.

Profit and loss account

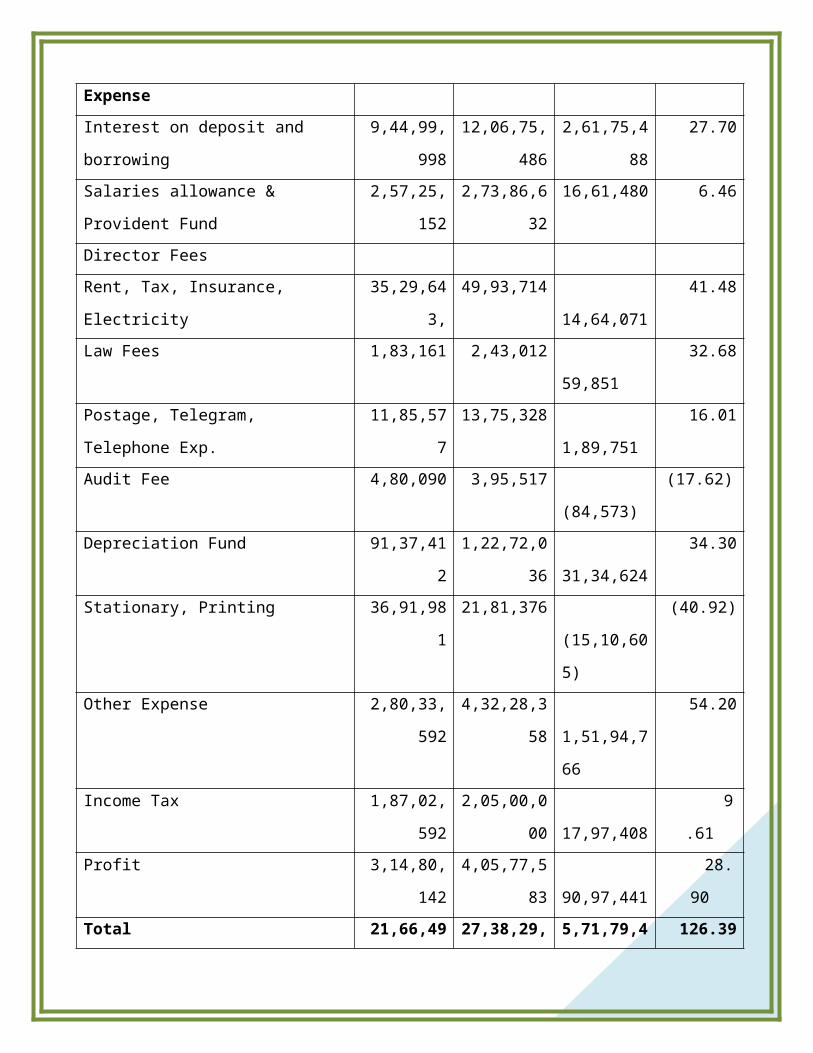

Particular 2009-2010 2010-2011 Absolute %

2010-2011 2010-2011

Expense

Interest on deposit and borrowing 9,44,99,998 12,06,75,486 2,61,75,488 27.70

Salaries allowance & Provident Fund 2,57,25,152 2,73,86,632 16,61,480 6.46

Director Fees

Rent, Tax, Insurance, Electricity 35,29,643, 49,93,714 14,64,071 41.48

Law Fees 1,83,161 2,43,012 59,851 32.68

Postage, Telegram, Telephone Exp. 11,85,577 13,75,328 1,89,751 16.01

Audit Fee 4,80,090 3,95,517 (84,573) (17.62)

51

Depreciation Fund 91,37,412 1,22,72,036 31,34,624 34.30

Stationary, Printing 36,91,981 21,81,376 (15,10,605) (40.92)

Other Expense 2,80,33,592 4,32,28,358 1,51,94,766 54.20

Income Tax 1,87,02,592 2,05,00,000 17,97,408 9.61

Profit 3,14,80,142 4,05,77,583 90,97,441 28.90

Total 21,66,49,615 27,38,29,042 5,71,79,427 126.39

Income

Interest & Discount 19,97,72,678 25,68,04,312 5,70,31,634 28.55

Commission Exchange 34,28,143 42,51,305 8,23,162 24.01

Donation ----- -----

Non Banking Income ----- -----

Other Income 1,34,48,792 1,27,73,426 (6,75,366) (5.02)

Total 21,66,49,615 27,38,29,042 5,71,79,427 126.39

Comparative statement analysis of balance sheet for year 2010 & 2011 in The Varachha co-

operative Bank Ltd.

Balance Sheet

Particular 2009-2010 2010-2011 Absolute %

2010 2010

Liability

Share capital 5,91,32,500 7,28,65,400 1,37,32,900 23.22

Reserve fund 22,53,32,015 26,07,59,206 3,54,27,191 15.72

Subsidiary Fund ----- -----

Deposit:

- Fixed Deposit 79,05,92,313 93,86,53,427 14,80,61,114 18.73

- Saving Deposit 76,00,70,549 93,43,53,951 17,42,83,402 22.92

- Current Deposit 55,49,46,207 71,67,94,730 16,18,48,523 29.16

51

Call & Short Time Deposit ----- -----

Borrowing ----- -----

Bills Payable 44,24,274 38,27,498 (5,96,776) (13.49)

Interest Overdue 5,80,51,785 3,35,61,148 (2,44,90,637) (42.19)

Interest payable 13,60,00,222 14,97,24,949 1,37,24,727 10.09

Other liability 7,88,68,009 9,82,13,381 1,93,45,372 24.53

Profit and Loss A/c 3,14,80,142 4,05,77,583 90,97,441 28.90

Total 2,88,35,47,600 3,44,23,72,150 55,88,24,550 119.40

Assets

Cash 8,65,50,365 8,82,44,532 16,94,167 1.96

Bank 48,83,88,452 35,34,85,910 (13,49,02,542) (0.27)

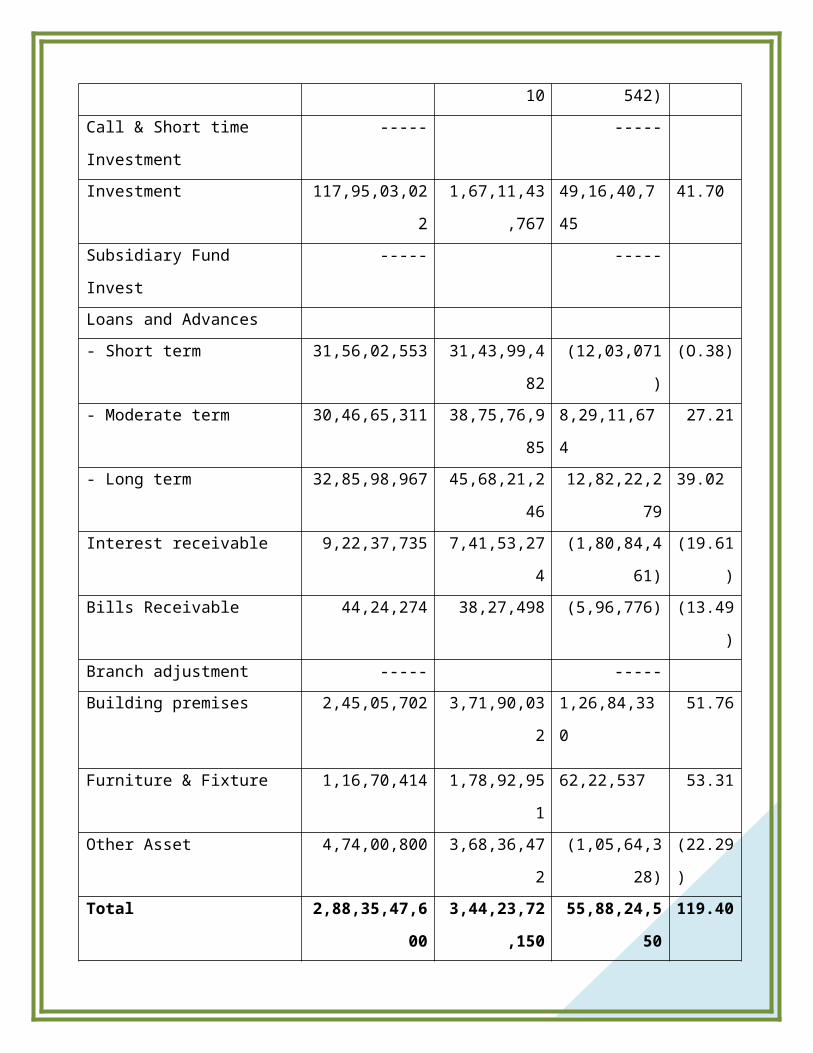

Call & Short time Investment ----- -----

Investment 117,95,03,022 1,67,11,43,767 49,16,40,745 41.70

Subsidiary Fund Invest ----- -----

Loans and Advances

- Short term 31,56,02,553 31,43,99,482 (12,03,071) (O.38)

- Moderate term 30,46,65,311 38,75,76,985 8,29,11,674 27.21

- Long term 32,85,98,967 45,68,21,246 12,82,22,279 39.02

Interest receivable 9,22,37,735 7,41,53,274 (1,80,84,461) (19.61)

Bills Receivable 44,24,274 38,27,498 (5,96,776) (13.49)

Branch adjustment ----- -----

Building premises 2,45,05,702 3,71,90,032 1,26,84,330 51.76

Furniture & Fixture 1,16,70,414 1,78,92,951 62,22,537 53.31

Other Asset 4,74,00,800 3,68,36,472 (1,05,64,328) (22.29)

Total 2,88,35,47,600 3,44,23,72,150 55,88,24,550 119.40

51

51

RATIO ANALYSIS:

A Ratio is only a comparison of the numerator with the denominator. The term ratio refers to the

numerical or quantitative relationship between two figures, and obtained by dividing the former by

the latter. Ratios are designed to show how one number is related to another. It is worked out by

dividing one number by another.

Ratio analysis is an important and age old technique of financial analysis. Ratios are relative form of

financial data and very useful technique to cheque upon the efficiency of firm. Some ratios indicate

trend or progress or downfall of the firm.

MEANING OF RATIO:-

51

A ratio is only a comparison of the numerator with the denominator. The tern ratio reefers to the

numerical or quantitative relationship between two figures and obtained by dividing the former by the

latter.

Ratio analysis is an important and age old technique of financial analysis. The data given in financial

statements ratio are relative form of financial data and very useful techniques to cheek upon the

efficiency of a firm. Some ratio indicates the trend or progress or downfall of the firm.

Classification of Ratios:-

Ratio can be classified into different categories depending upon the basic of classification as under:

Profit & Loss Account Ratio:-

In this ratio accumulated on the basis of all items of the profit & loss account only Ex. Net profit

ratio, operating profit ratio, expenses ratio.

Balance sheet Ratio:-

In this ratios calculated on the basis of the figures of balance sheet only.Ex. Current ratio, liquid ratio,

debt-equity ratio, proprietary ratio.

Composite Ratio or inter statement ratio:

In this ratio is the based on figures of profit & loss account as well as balance sheet.Ex. Fixed assets

turnover ratio.

IMPORTANCE OF RATIO ANALYSIS:

Aid to measure general Efficiency: ratios enable the mass of accounting data to be summarized and

simplified. They act as an index of the efficiency of the enterprise. As such they serve as an

instrument of management control.

Aid to measure financial solvency: ratios are useful tools in the hands of management and other

concerned to evaluate the firm’s performance over a period of time by comparing the present ratio

with the past ones. They point out firm’s liquidity position to meet its short term obligations and long

term solvency.

51

Facilitate decision-making: it throws light on the degree of efficiency of the management and

utilization of the assets and that is why it is called surveyor of efficiency. They help management in

decision-making.

Aid in intra firm comparison: intra firm comparisons are facilitated. It is an instrument for

diagnosis of financial health of an enterprise. It facilitates the management to know whether the

firm’s financial position is improving or deteriorating by setting a trend with the help of ratios.

Evaluation of efficiency: ratio analysis is an effective instrument which, when properly used, is

useful to assess important characteristics of business liquidity, solvency, profitability etc. a study of

these aspects may enable conclusions to be drawn relating to capabilities of business.

effective tool: ratio analysis helps in making effective control of the business measuring

performance, control of cost etc, effective control is the keynote of better management. Ratio ensures

secrecy.

LIMITATION OF RATIO ANALYSIS:

Ratio analysis a widely used tool of financial analysis, it is because ratios are simple and easy to

understand. But they must be used very carefully. They suffer from various limitations:

Differences in Definitions: Comparisons are made difficult due to differences in definitions of

various financial terms. Lack of standard formula for working out ratios makes it difficult to compare

them. They are worked out on the basis of different items in different industries.

Limitation of accounting records: ratio analysis is based on financial statements which are

themselves subject to limitations. Thus, ratios calculated on the figures given in the financial;

statements, also suffers from similar limitations.

Qualitative factors are ignored: ratios are tools of quantitative analysis only and normally

qualitative factors which may generally influence the conclusions derived are ignored while

computing ratios.

51

Limited use of single ratio: a single ratio would not be able to convey anything. Ratios can be useful

only when they are computed in a sufficient large number. If too many ratios are calculated, they are

likely to confuse instead of revealing meaningful conclusions.

Background is overlooked: when inter-firm comparison is made, they differ substantially in age,

size, nature of product etc. when an inter-firm comparison is made, these factors are not considered.

Therefore, ratio analysis cannot give satisfactory results.

Arithmetical Window dressing: window-dressing means manipulation of account in a way so as to

conceal vital facts and present the statements in a way to show better position than what it actually is.

By doing so, it is possible to cover up bad financial position. Therefore, ratios based on such figures

are not reliable.

Lack of proper standards: it is very difficult to ascertain the standard ratio in order to make proper

comparison. Because, it differs from firm to firm, industry to industry. Apart from this, it may have

happened that in one firm, a current of 2:1 is found to be quite satisfactory, whereas in another firm

2.5:1 may be unsatisfactory. Again, a high current ratio may not necessarily mean liquid position

when current assets large inventory or inventory consisting of obsolete items.

CURRENT RATIO:

Meaning:

Current ratio is the most common ratio for measuring liquidity. Being related to working capital

analysis it is also called the working capital ratio. Current ratio expresses relationship between current

assets and current liabilities

Purpose:

The current ratio of a firm measures in short term solvency. i.e. its ability to meet short term

obligation. As a measure of short term current financial liquidity.

It is calculated by dividing current asset by current liabilities

Current Ratio = Current assets

Current Liabilities

51

Current Ratio : = 71,90,01,628 2,14,97,10,680

1,59,23,61,046 1,93,64,75,655

= 0.45 =1.11

Particulars 2009-10 2010-2011

Current Asset

Cash 8,65,50,366 8,82,44,531

Bank 48,83,88,452 35,34,85,910

Advance -----

Other Asset 4,74,00,800 3,68,36,472

Bills Receivable 44,24,274 38,27,498

Interest 9,22,37,736 1,67,11,43,767

Total 71,90,01,628 2,14,97,10,680

Current Liability

Bills Payable 44,24,274 38,27,498

Interest Payable 13,60,00,222 14,97,24,949

Saving Deposit 76,00,70,549 93,43,53,950

Current Deposit 55,49,46,207 71,67,94,730

Interest Overdue 5,80,51,785 335,61,148

Other Liability 7,88,68,009 9,82,13,380

Total 1,59,23,61,046 1,93,64,75,655

51

Interpretation:

here, it shows that the bank has been decrease in 2010 current ratio is 0.45:1 to in 2011 current ratio

is 1.11 which is not satisfactory so, can be Improved by better turnover and profit.

CASH POSITION RATIO:

Meaning:

It is a variation of quick ratio. When liquidity is highly restricted in terms of cash and cash

equivalent, this ratio should be relationship between cash and near cash items on the one hand.

Purpose:

The purpose of computing the ratio to measure e more rigorous of a firm’s liquidity position.

Particulars 2009-2010 2010-2011

Cash 8,65,50,365 8,82,44,532

Marketable Securities 117,95,03,022 1,67,11,43,767

Total 1,26,60,53,387 1759388300

51

Current Liabilities 1,59,23,61,046 1,93,64,75,655

Cash Position Ratio = Cash + Marketable Securities

Current Liabilities

= 1,26,60,53,388 = 1,75,93,88,300

1,59,23,61,046 1,93,64,75,655

= 0.80 = 0.91

PROPRIETARY RATIO:

Meaning:

This relates the shareholders fund to total assets. It is a variant of the debt equity ratio. This ratio

shows the long term or future solvency of the business. It is calculated by dividing shareholders funds

by the total asset.

Purpose:

51

The purpose of proprietary ratio is indicate available to creditors and general financial strength of the

firm.

Proprietary Ratio= Shareholders Fund

Total Asset

Particulars 2009-2010 2010-2011

Shareholders Fund

Capital 5,91,3,2500 7,28,65,400

Reserve 9,65,59,375 10,49,50,670

Subsidiary Fund ----- --------

P&L Account 3,14,80,142 4,05,77,583

Total 53,20,74,401

Total Asset 2,88,35,47,600

Proprietary Ratio = 32,64,98,777 53,20,74,401

2,26,90,56,555 2,88,35,47,600

= 0.14:1 0.18:1

51

Interpretation:

The proprietary ratio is increase by 0.13:1 to 0.17:1 in the 2010 which is shown by the general

strength of the bank or company. It is very important to creditors as it helps them to find out the

proportion of shareholders funds in the total assets used in the business. In this ratio is always down

from the good position and low ratio indicate greater risk to creditors. A ratio below 50% may be

alarming for the creditors and heavily lose for company and its account is liquidation.

DEBT EQUITY RATIO:

Meaning:

The financing of total asset of a business concern is done by owner’s equity as well as outside debts.

This ratio indicates the relative proportions of debt and equity in financing the asset of a firm.

It is also known as external internal equity ratio. Debt equity ratio is determined to ascertain

soundness of the long term financial policies of a company.

Debt Equity Ratio = Long Term Debt

Shareholders Fund

51

Particulars 2009-2010 2010-2011

Long Term Debt

Fixed Deposit 79,05,92,313

Other Borrowing -----

Total 79,05,92,313

Shareholders Fund 46,91,14,117

Debt Equity Ratio:

= 57, 90, 47,751 = 79,05,92,313

43,10,13,335 46,91,14,117

= 1.34 = 1.69

Interpretation:

51

Debt equity ratio has been increase in year 2009 to 2010 that is 11.05 and 13.37 respectively. It

indicates the margin of safety to long term creditors. A high ratio shows the claim of creditors is

greater than those of owners.

SOLVENCY RATIO:

Meaning: It is also known as debt ratio. It is difference of 100 and proprietary ratio. This

ratio is found out between total asset and external liabilities of the company.

Purpose:

This generally refers to the capacity or ability of the business to meet its short term and long term

obligations. If a company in a position to pay its long term liabilities easily it is said to possess long

term solvency.

Solvency Ratio = Outside Liabilities

Total Asset

= Total Liability – Shareholder Fund

Total Assets

Particulars 2009-2010 2010-2011

Outside Liability

Total Liabilities 2,88,35,47,600

Shareholders Fund 9,06,12,642

Total 2,79,29,34,958

Total Asset 2,88,35,47,600

Solvency Ratio: = 2,18,64,17,069 = 2,79,29,34,958

2,26,90,56,555 2,88,35,47,600

51

= 0.96:1 = 0.97:1

Interpretation:

In this ratio total assets are for more than external liabilities the company is treated solvent. In

solvency ratio in 2009, 0.976% decrease in 2010 0.979:1 it means that outside liability is always less

than total assets.

NET PROFIT RATIO:

Meaning:

It is also called net profit to sales ratio (= profit margin). The profit margin is indicative of

management’s ability to operate the business with sufficient success not only to recover from revenue

of the period, the expense of operating the business and the cost of borrowed fund.

Purpose:

51

this ratio is used to measure the overall profitability and hence it is very useful to proprietors. It is an

index of efficiency and profitability when used with gross profit ratio and operational efficiency of

the concern.

Net Profit Ratio = Net Sales X 100

Net Profit

Particulars 2009-2010 2010-2011

Net Sales

Interest Receivable 9,22,37,735

Commission 34,28,143

Total 9,56,65,878

Net Profit 3,14,80,142

Net Profit Ratio:

= 3,02,24,486 = 3,14,80,142

7,55,32,888 9,56,65,878

= 40.02 = 32.91

51

Interpretation:

In this ratio, in 2009, 40.02% and 2010 decrease in 2010, 32.91%. It is more useful for the further

condition of the firm.

Expenses Ratio:

This ratio indicates the efficiency or otherwise in the incurrence of administrative expense. It

is expressed as a percentage.

The purpose of this ratio is that income is rise than expenditure it is also raised.

Particular 2009-2010 2010-2011

Total expenses

Staff, salaries, allowance 2,57,25,152

Director fees -

Legal fees 1,83,161

Rent, tax, insurance 35,29,646

Postage, telegram 11,85,577

Audit fees 4,80,090

Stationary, printing 36,91,981

Other expenses 2,80,33,593

Total 6,28,29,199

Total income 21,66,49,615

Expenses ratio = Total expenses X 100

Total incomes

= 6,68,56,334 X 100 = 6,28,29,200 X 100

19,92,78,464 21,66,49,615

51

= 33.55% = 29.00%

RETURN ON EQUITY HOLDER FUND:

Meaning:

The term net profits as used here, means net income after payment of interest and tax including net

non-operating income (i.e. non-operating income minus non-operating expenses). It is the final

income that is available for distribution as dividends to shareholders. Shareholder’s funds include

both preference and equity share capital and all reserves and surplus belonging to shareholders.

Return of Share Holder equity = Net Profit X 100

Shareholders Fund

Particulars 2009-2010 2010-2011

Net Profit 3,14,80,142

Shareholders Fund 46,91,14,117

Return of Share Holder

equity:

= 3,02,24,486 = 3,14,80,142

43,10,13,335 46,91,14,117

51

=7.01% =6.71%

Interpretation:

In this ratio, in 2009, 57.66% and 2010 decrease in 2010, 53.24%. The term net profit as used here

means net income after payment of interest and tax including net non operating income. It is the final

income that is available for distribution as dividend to shareholders.

CAPITAL TURNOVER RATIO

Sometimes the efficiency and effectiveness of the operations are judged by comparing the cost of

sales or sales with amount of capital invested in the business and not with assets held in the business,

though in both cases the same result is expected. Capital invested in the business may be classified as

long term and short term capital or as fixed capital and working capital or owned capital and loaned

capital. All capital turnovers are calculated to study the uses of various types of capital.

Ratio = Net Profit

Capital Employed

Particular 2009-2010 2010-2011

Net Sales 9,56,65,878

51

Capital Employed

Equity 5,91,32,500

Reserves 40,99,81,617

Total 46,91,14,117

Return on Asset =

7,55,32,888 = 9,56,65,878

26,60,49,805 46,91,14,117

= 28.39% = 20.39%

Interpretation:

In this ratio, decrease the percentage in 2009, 28.39% to in 2010, 20.39%. Lower ratio shows lower

profit and higher ratio shows higher profit.

CREDITORS TURNOVER RATIO:

51

This is also known as accounts payable or creditors velocity. Creditors turnovers indicates the number

of times the payable rotate in a year. It signifies the credit period enjoyed by the firm paying

creditors. Accounts payable include sundry creditors and bills payable.

Ratio = Creditors + Interest payable + bills payable

Interest on deposit and borrowing

Creditor turnover ratio: = 1,72,06,78,495 = 2,10,56,09,070

10,68,37,058 13,60,00,222

= 16.11 = 15.48

Particular 2009-2010 2010-2011

Creditors

Fixed Deposit 79,05,92,313

Saving Deposit 76,00,70,549

Current Deposit 55,49,46,207

Bills payable 44,24,274