Embed Size (px)

Citation preview

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 1

Prof. Anna Maria Variatoa.a. 2015-2016

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 2

The relevance of minskian contribution in the explanation of empirical facts: the subprime crisis

The role of FIH as a paradigm to explain macroeconomic dynamics

Is the FIH the only relevant “piece of explanation” even for Minsky himself?

Main references:

• A. Vercelli, (2010), Minsky moments, Russell chickens and grey swans: the methodological puzzles of financial instability analysis, in «Minsky, crisis and develpment», Tavasci and Toporowski (eds.) St. Martin Press, McMillan, 15-31

• A. Vercelli, (2011), A Perspective on Minsky moments, revisiting the core of the financial instabilityhypothesis, Review of Political Economy, v. 23, 49-67

• A. Variato, (2015), Can we say Minsky moment when households matter?, in «Cycles, Growth and the Great Recession», Cristini, Fazzari, Greenberg and Leoni (eds.), Routledge, London, 25-44

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 3

… to be … or not to be

Finance

Liquidity

Fragility

Endogeneity

Fairness

Uncertainty

All agents

Real effects

Money

Solvency

Stability

Exogenous shocks

Efficiency

Irreversibility

Firms

Nominal Effects

Aspects emphasized by Minsky Standard issues

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 4

Issues raised by MinskyEmpirical: Suitable for the explanation of

recent events? Yes, Yes but, No, Who cares?

From theoretical to methodological: Is the Financial Instability Hypothesis as an interpretative framework: Original? Complete? Relevant?

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 5

Part I

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 6

In order to evaluate the issue, the research questions usually evaluated are: Was the subprime crisis a Minsky Moment? Does the subprime crisis belong to the core of FIH?

Examining the existing literature one can find that the first type of question finds a different answer because: There exist different evaluations of the conditions apt to

identify a Minsky Moment (instant vs. process) (see Vercelli, 2011)

More in depth we can find different uses of the concept of time (historical vs. logical) (see Variato, 2015)

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 7

The expression ‘Minsky moment’ was coined in 1998 by PIMCO bondfund manager Paul McCulley on the occasion of the Russian debt crisis. This neologism became a fashionable catchphrase during the subprime crisis;

Point of time

• Magnus (2007a): the point where credit supply starts to dry up

• Wolf (2008): the point at which a financial mania turns into panic

Process of indeterminate length that is supposed to be short-lived, at least relatively to periods of financial tranquillity.• McCulley (2001): a self-feeding process of

debt-deflation• Lahart (2007): when over-indebted investors

are forced to sell even their solid investments

• Magnus (2007c): when lenders become increasingly cautious

• Whalen (2008): credit crunch • Davidson (2008): when the Ponzi pyramid

financial scheme collapses

Quo

tes

from

Ver

celli

201

1, p

.50

The two categories of definitions do not exclude each other since a point of time may start a process. […]More troubling is the fact that the existing definitions focus on disparate aspects of financial crises, […] playing distinctive roles in different historical episodes.

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 8

According to Variato (2015) the different interpretations given to Minsky moments relate to different notions of time

Historical time: Point of time

See Bellofiore and Halevi (2011): the point is subprime crisis

2007

Logical time:Process

See Wray (2009): the process starts as a crisis of money-manager capitalism

1997-2000

“The immediate cause of a crisis does not matter. The forces at work that led to the crisis started to operate long time before the factor triggering the occurrence of the crisis”. Tymoigne (2006)

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 9

Strongly favourableThe FIH can be extended to otherfields of economics and sciences• Regional an

internationaleconomics (Henry, 2009; Dymski, 2010)

• Macroeconomicmodeling (Barbera and Weise, 2010)

• Social science (Galbraith and Sastre, 2010)

• Method and science paradigms (Reinert, 2009)

Favourable• Emphasis on the

sufficient pieces of the minskianexplanation• Stages of capitalism:

role of interactionbetweenreal/finance/institutions; Role of policy intervention

• The nature of ceilings: institutionalnot market driven

• Wray (2009, 2011), Whalen (2008), Kregel (2010, 2010a)

Favourable but with criticism• FIH relevant, but in

need to be refined• Vercelli (2010),

(2011); • Erturk and Ozgur,

(2009), (2010);• Toporowski (2005),

(2010)

Unfavourable but FIH useful tool• Davidson (2008)• DeAntoni (2010)• Behlul (2011)• Kregel (2008)• Bellofiore and Halevi

(2011)

Who cares?Prychitko (2010): Austrian economics

The subprime crisis 2007 can beviewed as a Minsky moment?

We will deserveparticularattention to thesecontributions

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 10

Definition of Minsky momentDistinction between Minsky moment and Minsky

processContinuos time/type model where the

endogenous path of the economy is determinedby the interaction of liquidity and solvencyindicators

Policy implications

Go to the Second Part

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 11

was not triggered by over-indebted firms, but households (or banks, or other financial institutions); (almost everywhere in the literature)

was not caused by a “ponzification” of the system (that is a dynamic process where hedge units transform into speculative ones, and speculative units into Ponzi): households were not allowed to be Ponzi (ponzification of households was an effect, not a cause of the development of the crisis) (especially Davidson, but almost everywhere except Kregel);

was due to mispricing of risk (Kregel) (+ Behlul); was not due to a boom of firms’ productive investment, i.e. was not

due to profit-seeking firms, but to other profit-seeking units (again either households, or banks, or other financial institutions); (everywhere in the literature);

while implying speculative bubbles it did not lead to wage and price inflation (Bellofiore and Halevi).

This critique, also contains a twin argument which blames Minsky for excessively emphasizing the role of banks instead of other financial institutions.

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 12

… while Minsky does provide some useful insight into the financial crisis of 2008–9, the ability of his most prominent theory of financial instability—the financial instability hypothesis (FIH)—to explain current crisis is absent. (p. 137)

(…) I argue that in the decade leading up to the crisis, financial behavior at the firm level did not show a gradual and progressive deterioration toward instability—an essential requirement for a Minsky moment. (p. 137-138)

(…) Thus, the fragility of the macroeconomy in this case was not caused by the nonfarm, nonfinancial corporate sector. (p. 145)

(…) The “moment,” in a true Minskian sense, arrives after a cumulative process towards instability, the “moment” being a debt-deflation process. However, in order to arrive at that “moment,” the economy should have first moved from hedge to speculative and finally to Ponzi financing. In the current crisis, the banking system was either speculative—or Ponzi—financing from the beginning (Behlul, 2011, p. 151)

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 13

“…over the course of any expansion, the economy moves from hedge to speculative to Ponzi finance. Minsky argued that this is a necessary precondition for an unstable financial system” (Papadimitriou and Wray, 1999, p. 10, emphasis added)

(…) Consequently, with no movement from hedge to speculative to Ponzi finance, the “necessary precondition” for a Minsky moment has not been met. Instead, the current financial market problem was set off by insolvency problems of large financial market underwriters who attempted to transform illiquid noncommercial mortgages into liquid assets via securitization (Davidson 2008, p. 670).

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 14

If we consider the subprime crisis in itself, it is probably legitimate to interpret it as a “Minsky moment” followed by a “Minsky meltdown” (Roubini 2007a, 2007b; Whalen 2007; Wray 2007). Many features are in fact the same.

Our problem, however, extends beyond the episode in itself: to what extent does the subprime turmoil fit with the “core” of Minsky’s financial instability hypothesis?

I refer to the hypotheses (i) that the fundamental instability of capitalism is upward (ii) that growth endogenously leads to financial fragility and

consequently tends to be shaken by financial crises followed by debt deflations and deep depressions.

The two theses are equally essential to Minsky’s construction. As we will see, the recent experience seems to gainsay the latter and, perhaps, also the former. (De Antoni, 2010, p. 18)

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 15

Something is missing• Critique 1: FIH deals with firms’

investment, while subprime crisiswas due to households

Something is wrong (or atleast weak)• Critique 2: FIH is too much

concerned with cycles’ ceilings, but does not explain the floors

Ponzi evils• Critique 3: The role of

heterogeneity. The «ponzification» process is reallynecessary

The role of big players• Critique 4: Do we really need the

intervention of the public authority in order to stabilize the system?

Davidson, 2008DeAntoni, 2010Behlul, 2011Kregel, 2008Bellofiore and Halevi, 2011

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 16

Research question 1: Is FIH really so much unbalancedtowards firms’ investment?

Research question 2: What kindof dynamic process is implied by

FIH? What kind of interactionbetween cycles and growth?

Research question 3: Are Ponzi units really just a particular kindof speculative ones? What is the

role of heterogeniety in the process of endogenous

instability?

Research question 4: What kindof role for big (public) players in

the economy?

We will hopefully see how the attempt to answer thesequestions leads to build a paradigm of endogenousfinancial instability. Is thisparadigm minskian?

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 17

Instabilityas an endogenous effectof economic dynamics

Real side and financial sidenot independent (money notneutral + no dichotomy) Potential conflict

micro / macro(fallacy of

composition)

Instability as a result of complex interactions between thestructure of the economy (fundamentals) and market self adjustments (instiutional intervention… sometimes for bad)

But unfortunately this is notMinskian distinctive…

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 18

Banks as representative units(answer to critique 1)

Cycles and growth are not independent

(answer to critique 2)

Ponzi units and the relevantdegree of heterogeneity(answer to critique 3)

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 19

The main reason why our economy behaves in different ways at different times is that financial practices and the structure of financial commitments change (…) The behavior and particularly the stability of the economy change as the relation of payment commitments to the funds available for payments changes and the complexity of financial arrangements evolves. (…) The evolution from financial robustness to financial fragility did not take place in a vacuum. The sources of the change can be traced to profit opportunities open to financial innovators within a given set of institutions and rules; a drive to innovate financing practices by profit-seeking households, business and bankers; and legislative and administrative interventions by governments and central bankers.

(Minsky 1986, p.197)

Uniqueness of cycles

Endogenousevolution of finance

Financial change is a complexphenomenon

Finance doesnot work alone

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 20

The minskian microfoundation: the representative agent

To analyze how financial commitments affect the economy is necessary to look at economic units in terms of cash flows. The cash-flow approach looks at all units –be they households, corporations, state and municipal governments, or even national governments – as if they were banks. (Minsky 1986, p. 198)

Capitalism may very well work best when capital assets are cheap and simple. Instability may very well be exacerbated as production becomes more capital intensive and as the relative costs and gestation periods in investment goods increase, for such in a capitalist economy financing arrangements are likely to appear in which debtors pay debts not with cash derived from income production but with cash obtained by issuing debt. We have to investigate the implications of debt and external financing of the financial structures we all know exist, for the stability of the economy. (p. 200) Same point also stated in Minsky (1964).

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 21

Onthology

the representative agent has to be understood as «the ideal, averageindividual»

so he has some features leading to the so called «homo economicus» (substantive rationality, methodological individualism, atomism…)

How far can we push the similaritybetween homo economicus and «realman»?

How far can we push the argument: we know there is a difference, anywaywe build models under the hypothesisman acts like as if he was homo economicus?

Epistemology

The representative agent is nothingbut a mere representative tool

In other words it is a «symbolic» pieceof the construction of a theory.

It is useful to represent reality but itdos not have «properties» which can be attached to the reality itself

The representative agent is the smallest microeconomic meaningfulentity; it is the first step in order to be able to build up a representation of the system.

It is one of the cornerstones of theoretical language: the representative agent stays at a letterof the alphabet as the book stays atthe system

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 22

Why the emphasis on firms’ investment?

Investment is the most unstable component of aggregate demand, and hence the most likely driver of aggregate standard fluctuations.

Investment directly connects Minsky to Keynesian tradition through the exposition of the theory of two prices. The emphasis on the theory of two prices can be view as the easiest way either to face mainstream neoclassical position, and to contrast the IS-LM reduction of Keynes.

The explanation of the FIH requires integrated real and financial sides of the economy. A financial theory of instability does not imply that the real side of the economy is obscured (almost absent) while affecting dynamics. It is not financial innovation or financial sector growth per se the vehicle towards instability, but the lack of coordination of the pace of change of finance with respect to the pace of change of real economy.

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 23

Does FIH require only instability of firms’ investment? Minsky refers to units “as banks”

Generalizing the concept of “bank” to each individual in the economic system, one discovers that the only way is related to “financial intermediation”, that is the fact that each individual may be the channel of exchange between “flows of money/liquidity today” against “money/liquidity in the future”;

nevertheless such an exchange cannot be established without the presence of capital assets which are simultaneously the mean and the end of the transfer process of liquidity through time.

In other words, financial intermediation is not a distinctive feature of a “bank” in strict sense: any individual who does not live in a never-ending present, but has to face intertemporal decisions need to face the problem to synchronize liquidity flows, and hence is compelled to behave “like a bank”.

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 24

Is the floor really missing? On the interaction between cycles and growth

The issue of cycles is of vital importance in Minsky writings. See Fazzari and Greenberg (2015), most of the joint works by Ferri and Minsky (1992), and Ferri (2010)(2013).

Cycles are symmetric (theoretically): there exist euphoric-booms, opposite to pessimistic-slumps. Why does not Minsky explore too much the slump? After Great Depression authorities have learnt how

to deal with such a problem. The so “called upward obsession” then is not an obsession at all. It is simply a claim for attention on the fact that authorities have not yet understood how dangerous can be to overlook the upward destabilizing force of finance.

If cycles and growth were independent one should not worry too much about upward instability (or downward instability as well). The consequences of the crisis, though massive and undesirable form the point of view of efficiency,

equity, distribution and social justice, would be temporary.

Minsky’s idea of the interaction between cycles and growth is that both processes are intertwined. Hence the disruptive fall-out of an euphoric-boom is especially worrisome as it contains the seed of the

worst potential negative effect on the potential long-run path of the economy (which will be captured ex-post, as an evidence of a downturn in the overall cyclical dynamics).

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 25

Standard Approach Minsky Approach

Strong independence between cyclesdeterminants and growth determinants.

Formally the two «paths» are related to different variables, usually:

Growth AS variables (technologies, labour, other resources, institutional frameworks, and their specific determinants)

Cycles AD variables (investment, consumption, public expenditure, net-exports, money demand and supply, and their specific determninants)

Usually also:

Growth long run + equilibrium path

Cycles short run + disequilibrium

Exception: Real Business Cycles long-runbecomes indistinguishable from short-run; growth = cycles; observed dynamics is an equilibrium dynamics

No point in stabilizing the economy

Because the effects of shocks are just temporary

Or for RBC, because cycles are per se an optimal answer to shocks

Cycles and growth are notindependent

Both growth and cycles can be determined by AD and AS

While maintaning the distinction: long-run «ideal» equilibrium short-run «effective»

disequilibrium

long-run asymmetrically affectedby the amplitude of cycles(downturns more effective thanupturns)

Extremely useful the role of stabilization policies as they are the theoretical safeguard towardsa sustained process of growth

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 26

The Kaleckian root of FIHLeading towards instability: the role of the growth processIf cycles and growth are not independent then the thrust towards instability is due to the growth process. Minsky states that the objective of all units is profit-seeking (not growth). In general each u

nit may obtain profit exploiting the interaction of two levers: operational and financial. The thrust towards instability is an endogenous consequence of growth, due to the fact, that, in order to seek-pr

ofits in a competitive environment, a firm which is comparatively less productive with respect to the core business, will face competition increasing leverage, hence increasing the return on “equity” and possibly overcome the result of the competitor. As the change of financial structure, during a positive phase of the cycle is much easier than the change of “core productivity”, it is quite consequential that firms, especially in the short run pursue profit-seeking through financial leverage instead of operational leverage. In the aggregate, this means increasing leverage, and accordingly increasing fragility (Minsky 1964 p. 177, and Minsky 1986 p. 213).

Hence business cycles are not only generated by disappointed of expectations, or other psychological facts relating to the issue of fundamental uncertainty, but also by the different timing of evolution of the forces behind real dynamics and the forces behind financial dynamics. If finance as a destabilizing nature, the real side of the economy, without any change in expectations, may very

well trigger a downturn (just moving at a pace which is inconsistent with financial developments, and or liquidity injection into the system).

As a result the real part of the FIH is not missing, even though one may think about better refinements. See Cimoli, Dosi and Stiglitz (2009).

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 27

The assumption that Ponzi finance is nothing but a variant of speculative finance, for example, is literally stated by Prychitko (p. 205).Negative attitude towards Ponzi units: their relative incidence in the system causes increasing fragility and hence

disruptive downturns (see Galbraith and Sastre 2010, p. 268). Ponzi units are mostly connected to a behavior at least extremely

opportunistic if not openly fraudulent. As a result, representative agents, the “good” ones are not supposed to be Ponzi. Direct exposition of the idea that units are not supposed to be Ponzi can be found in

Reinert (2009, p. 8) Indirect evidence of this position can be found in Papadimitriou and Wray (1999) who

divide Minsky Moments in two phases: 1) intentional: implying the transformation of units from hedge to speculative; 2) mostly unintentional: implying the transformation from speculative to Ponzi.

Without a negative connotation of Ponzi units, the distinction of the two phases of the Minsky Moment would not require an explicit reference to the “will” of agents. In other words, if being speculative is not a fault, as it is not a fault being Ponzi, there is no need to distinguish between being speculative or Ponzi as a matter of choice, or as a consequence of an exogenous change of financial conditions.

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 28

What is a Ponzi unit?

A Ponzi-financing unit is similar to a speculative financing unit in that, for some near-term periods, the cash payment commitments exceed the expected cash receipts on account of owned assets. (…) Ponzi units capitalize interest into their liability structure. (Minsky 1986, p. 207)

The formal definition of Ponzi unit can be found in Appendix 1 Minsky (1986).

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 29

Why are we supposed to care about Ponzi units?The name Ponzi is quite unfortunate like “speculation” negative moral connotation

Furthermore Ponzi units (as well as speculation) induce higher fragility and likelihood of instability

Nevertheless Ponzi unit does not need to be “a bad” unit. The Ponzi nature Minsky attaches to agents is only related to financial conditions, not to other individual relevant features. Typical examples of Ponzi units (or actions implying that at least some individual actions follow a Ponzi scheme) are also:

a high technology firm, a chemical researcher, …, a brilliant student coming from a poor family, a government financing education, a bank financing the building of a highway.

None of the units above is bad in principle: all of them have to face decisions implying that for a quite long period of time outflows of liquidity exceeds the inflows, and the ability to pay-back the debt consequential to present liquidity unbalance is so far away in the future that such agents have to capitalize interests into their liability structure.

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 30

Can one think that Ponzi units (or situations) must be kept under control, as this is beneficial to the stability of the system?

It is true that a higher proportion of Ponzi units increases the fragility of the system, but it is on the converse true that a system without Ponzi units (like the ones just mentioned) is going to loose important growth opportunities.

So the very existence of Ponzi units creates a trade-off between stability and growth on the dynamic path of the economy.

Without an explicit acknowledgment of the particular positive nature of Ponzi units, this trade-off would be lost. loss of an existing interpretative piece of the FIH, suggestion of likely wrong economic policies (like a generalized restriction on

capital requirements in bad times, which is good for speculative units, but not for Ponzi).

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 31

About the role of big public players

One cannot answer in a definite way this question: we know that there exists state failure, not only market failure

Minsky himself was criticizing many public policies

There one has to decide «the feeling» towards policy action: Extremely positive with respect to the power of a specific action + skeptical about

the amplitude of the intervention (such neoclassical) Extremely positive with respect to the power of a specific action + positive about

the amplitude of the intervention (such neokeynesian and newkeynesian) Critical with respect to the power of a specific action + positive about the

amplitude of the intervention (such postkeynesian and swedish) Negative with respect to the power of a specific action + negative about the

amplitude of the intervention (such austrian)

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 32

Part II

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 33

Economic Methodology(philsophy of science)

Vercelli (2011) points out some methodologicalaspects related to Minsky

EconomicEpistemology

(subset of method, devoted to the building of economic theories)

Vercelli (2009, 2011) suggests his ownmodel capable to overcome supposedminskian drawbacks

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 34

Minsky often criticized because of «implicit theorizing» The theoretical idea is good as an intuition, but not fully

explained

Is this a real drawback? See Kuhn (1970) about revolutionary theories (the example of Smith

Invisible Hand, and the case of Walras and Pareto + Arrow Debreu) See Schumpeter (1954) and the role of «preanalytic visions» What is really important in Minsky «is the powerful preanalytic vision

of the working of a sophisticated financial economy…»

Hence, like in the case of smithian Invisible Hand, also FIH intuition needs to be qualified with respect to formalization: in his contributions Vercelli proposes a more complexcharacterization of financial positions

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 35

Minsky’s FIH as a perfect epitome of two metaphors: Russell’s Chickens: on the misleading role of regularities (Lucas vs.

Minsky). «It» cannot happen again. Gray Swans: on the role of universal laws they might exist but

maybe different from regularities(see the two explorations at the end of the presentation)

The pedagogical role of «birds»… Need to define the attitude towards: regularities and their

exceptions «a good economic theory is much more than «a set of instructions for building» economic models (Lucas (1981). The preanalytic vision (in the sense of Schumpeter 1954) must be general enough to help us choose the right approach for the circumstances» (Vercelli, 2009 p.5)

Need to define the attitude towards: universal laws

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 36

index of liquidity (at time t, unit i)

eit current realized outflows yit current realized inflows may be > 1

index of solvency

capitalization of expected k*itfor all the future periods within the time horizon m.

It is supposed to be less or at most equal to one. If >1 means negative net worth (virtually insolvent unless restructuring or bail-out)

The starting point is the introduction of two measures

it

itit y

ek 1* itk

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 37

Notice: • Minsky uses the same

variables in terms of differences instead of ratios.

• he does not explicitly considers solvency.

• So, in his classification, Minsky does not explicitly consider the units beyond the vertical line that are virtually insolvent.

According to Vercelli this is a crucial shortcoming of Minsky’s classification (as distressed do not necessarily disappear, and they are crucial to the representation -understanding of the dynamic process entailed by FIH).

Ponzi Speculative

Highly distressed

Hedge Distressed

1

1

Index ofliquidity

Index of solvency

Minsky’s space Vercelli’s space addition

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 38

margin of safety

Maximum value of the solvency ratio, sufficiently lower than 1 that the unit does not want to overcome

1)1(5,0

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 39

speculative

hyper-hedge hedge distressed

highly-distressedhyper-speculative

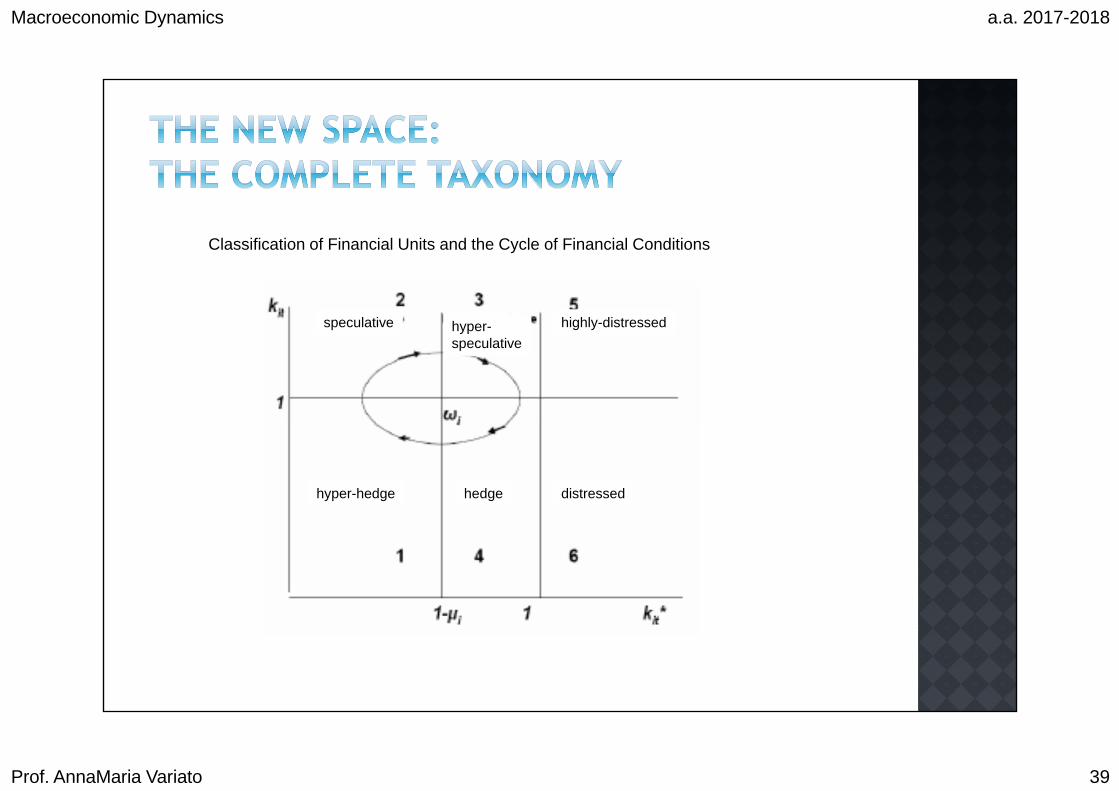

Classification of Financial Units and the Cycle of Financial Conditions

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 40

The space defined by liquidity and solvency indexes allows a representation of fluctuations

According to Vercelli the interaction between liquidity and solvency conditions is an essential component of the description of the dynamic process implied by FIH (an idea not often expressed in these terms by Minsky)

The interaction between the two indexes can be explainedin two ways:

Using an intuitive description of the phases of the cycle

Building a simple continuous-time model (Lotka-Volterra type)

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 41

Phase I: If a unit perceives to be beyond the safety margin (1-), itdecreases the illiquidity margin (1-k) in order to decrease the marginof solvency k* (look at the orbit in the figure: from area 4 towardsarea1)

Phase II: Then in the safe area of solvency, competition pushes the unitto stress the financial lever; so outflows increase faster than inflows (k increases) and likelihood to become insolvent increase, i.e. k* increases (the orbit moves: from area 4 towards area 2)

Phase III: When k overcomes the liquidity line (k>1), k* deterioratesthrough the increase of debt (the Ponzi scheme) and worsening of expectations (the orbit moves: from area 2 towards area 3 and 5 uponoccasion)

Phase IV: When liquidity barrier is hit, debt needs to be reduced, thisinduces higher liquidity (k reduces), and better expectations (increasek*) (the orbit moves: from area 3 or 5 towards area 4 via 6)

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 42

Above safety lineReduce current exposureReduce kReduce k*

Below safety lineIncrease current exposureIncrease kIncrease k*

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 43

)1(* iitiit

it kkk

1**

itiit

it kkk

Law of motion liquidity margin

Law of motion solvency margin

Speed of adjustment

• Without shocks the unit moves clockwise around a center (point in figure 1)• Shocks shift the orbit inward/outward

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 44

The term is often mentioned, but its meaning is far more controversial (Goldsmith 1982).

Vercelli defines the financial fragility of a unit as the smallest size of the shock that produces its virtual bankruptcy. Version 1: in geometric terms, the degree of financial fragility

is given by the distance between the representative point and the insolvency line (plus an infinitesimal magnitude).

Version 2: the financial fragility of a unit is given by the smallest size of the shock that would make the net worth of the unit negative.

Both definitions lead to interpret financial fragility in terms of structural instability

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 45

The aggregate level of outflows, inflows and ratios is determined by appropriate aggregation processes

The meaning of aggregation: not only a statistical device, but counterpart of a real phenomenon. The dynamic behavior of units is fairly synchronized along the financial cycle for two reasons that determine their herd-like behavior. First, the pressure of the market pushes comparable commercial units to

accept a similar risk-taking position to obtain returns not inferior to those of the other units (benchmarking).

Second, mass psychology spreads waves of optimism and pessimism that affect most units; in consequence, the perception of risk becomes insufficient in the boom and excessive in depression.

By aggregating the financial conditions of all private units Vercelli obtains a model with the same qualitative characteristics of the micro model. (think about it: no fallacy of composition?)

His aggregate model explains why in a monetary economy there is a tendency toward persistent financial fluctuations.

It is also sufficient to account for the periodic increase of financial fragility when the representative point moves clockwise in fields 2 and 3 (see figure 2).

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 46

Figure 2: Aggregate Financial Fluctuations

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 47

On general visions: Minsky’s vision is much less reductionist than most other research programs in economics: The economic system is seen as an open evolutionary system

characterized by irreversible time The system is characterized by complex dynamics so that

periods of regular behavior cannot be lightheartedly projected into the future

Technical feature: The model utilized is sufficient to generate a self-referential loop, leading easily to complex dynamics and chaos

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 48

The relevance of the equilibrium concept: Equilibrium has a role, but only as a benchmark and reference point for analyzing the complex dynamics of the system. For example, in figure 1 the point ω is an equilibrium

in the dynamic sense of the term, but this does not entail the normative overtones of conventional equilibrium modeling.

In particular, there is no reason to believe that the objective function of a unit is maximized at this point.

Not possible to assume that equilibrium states or paths are dynamically stable, nor that the dynamic system is structurally stable;

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 49

From equilibrium to the interaction between structure and dynamics: Minskyan financial instability is a combination of dynamic and structural instability Weak dynamic stability alone would be sufficient to explain

persistent financial fluctuations that periodically increase the financial fragility of units

but financial fragility should be interpreted as a measure of structural instability, i.e., the propensity of an economic unit to radically change the qualitative characteristics of its financial behavior (think about it: can this point be used in order to face Lavoie’s critique to Minsky?)

From the economic point of view, financial fragility cannot be interpreted correctly in terms of mere dynamic instability. It depends, however, on the dynamic instability of the cyclical path and also affects it. (think about it: it is like to say that cycles and growth are not independent?)

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 50

In the version of the FIH’s core suggested here, as in that of Minsky, a unit’s euphoria does not play a crucial role in explaining financial instability, both in its dynamic and structural sense, as the mechanism underlying financial fluctuations would produce financial instability and fragility even without euphoria. This is not to deny, however, that euphoria is typical of a sufficiently persistent boom and that its spreading encourages over-indebtedness and a more speculative stance of units, accelerating the inception of a financial crisis and aggravating its manifestations. By inserting in the model an endogenous mechanism of production of euphoria during the boom, we would make the financial fluctuations of the representative point dynamically unstable (Vercelli 2009). We prefer, however, to separate these two building blocks of financial instability because they are characterized by a different degree of regularity. The dynamic behavior of euphoria (though correlated with that of cyclical fluctuations), like all psychological phenomena, is much more irregular and is subject to sudden changes that very much depend on a host of specific factors that may vary widely from country to country and from period to period.

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 51

Possible drawback of Vercelli model recognized by Vercelli himself: The model’s conservative nature (in the dynamic sense) implies

structural instability in the strict mathematical sense: an infinitesimal perturbation would change the qualitative dynamics of the system

In the model suggested in this paper, a possible justification is that this specification somehow captures structural instability observed in the real world. We believe, following Minsky, that the crucial factor of instability of a financial system is the periodic increase in financial fragility that gradually emerges in periods of tranquility

For this to happen it suffices to assume that dynamic stability is too weak to thwart persistent fluctuations (Think about it: Vercelli as a masked “mainstream guy”?).

In addition, such a specification may be considered as an appropriate representation of what we believe to be a stylized fact: the interaction between liquidity and solvency conditions of financial units brings about persistent fluctuations that do not have an intrinsic tendency to change through time.

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 52

The role of shocks in a model of financial fluctuations. The minskyan model is in sharp contrast with the conventional view prevailing

in macroeconomics since the late 1970s. The latter is based upon the equilibrium approach worked out by Lucas in the 1970s

(Lucas 1981). In this view, business cycles are the consequence of random shocks displacing equilibrium without disrupting it.

In the first version of equilibrium business cycle Lucas considered relevant shocks as essentially monetary impulses brought about by discretionary decisions of monetary authorities.

In the early 1980s the prevailing view shifted towards the “real business cycles” approach (Kydland and Prescott 1982), where fluctuations are produced by real shocks (mainly technological impulses).

A bit later, New Keynesian economics struggled to reintroduce Keynesian features in the model, such as asymmetric information;

The ensuing “New Consensus” added real and nominal rigidities to the equilibrium approach, but did not modify it in a substantial way (Woodford 2003).

On the contrary, in a model based on the FIH, shocks are not essential in explaining persistent financial fluctuations or a financial crisis. In particular, we do not need shocks to explain the periodic increase of speculative attitudes, indebtedness, and financial fragility of most units.

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 53

The implict individual rationality: procedural rationality: We cannot assume that agents succeed in converging

instantaneously to the equilibrium position, maximizing their objective function.

This, however, does not imply sheer irrationality. A rational agent may rely on the rules of behavioral rationality adapting in the best possible way to a changing environment, taking account of the influence that may be exerted on the environment

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 54

Towards a macrofoundation of microeconomics? In the open world of FIH the relationship between microeconomics and

macroeconomics is much more complex than in conventional economics. The analysis of macroeconomic fluctuations is based on a previous analysis of a unit’s financial conditions, but is not derived from a simple linear aggregation of average behaviors.

The “stabilizing role” (?!) of aggregate conditions: The behavior of a financial unit, studied in isolation from the movement of other units, is unlikely to exhibit a very regular pattern because each unit is heavily conditioned by specific features: a certain degree of regularity and synchronization is conferred to single units by the common influence exerted on them by aggregate financial fluctuations. Summing up, a full-fledged behavioral analysis of a unit’s dynamic behavior requires

macroeconomic foundations, while the study of aggregate fluctuations has to rely on microeconomic foundations (analysis of a single unit’s financial conditions).

The interaction between micro- and macro-foundations does not involve a vicious logical circle, as it is the consequence of a real process: the financial behavior of each unit is heavily influenced by the behavior of all the other units, as expressed by aggregate indexes.

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 55

“The man who has fed the chicken every day throughout its life at last wrings its neck instead, showing that more refined views as to the uniformity of nature would have been useful to the chicken.”

Bertrand Russell – The Problems of Philosophy

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 56

On a farm, there was a flock of chickens. One chicken started talking with another, remarking ʺHow good our farmer has been to us. I think he is an awfully nice man, because he comes every morning to feed us.ʺ The other chicken nodded in agreement, adding ʺand he has been feeding each and everyone of us here every day like clockwork, every day without fail since we were all just little baby chicks.ʺ

Indeed, when queried, most of the other chickens clucked in agreement about how benevolent their farmer was. But there was one chicken, intelligent but eccentric, who countered saying ʺHow do you know he is all that good? I remember, not too long ago, that there were some older chickens who were taken away, and I havenʹt seen them since. What ever happened to them?ʺSome of the chickens may have slept a little uneasy that night, but in the morning the farmer came as usual, this time scattering even more corn around. The chickens ate this with gusto, and this dispelled any remaining doubts about the benevolence of the farmer. ʺYou see, there is nothing to worry about. Our farmer had a little extra food, so he gave it to us because he likes us! He is a good man,ʺ remarked one chicken to the others, and they all nodded in agreement, all of them, that is, except one.The intelligent but eccentric chicken became even more agitated. ʺHe is just fattening us up! We are going to be slaughtered in a weeks time!ʺ he squawked in alarm. But nobody listened. All the other chickens just thought he was a troublemaker.A week later, all the chickens were placed into cages, loaded onto a truck, and driven to the slaughterhouse.

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 57

In almost all our previous discussions we have been concerned in the attempt to get clear as to our data in the way of knowledge of existence. What things are there in the universe whose existence is known to us owing to our being acquainted with them? So far, our answer has been that we are acquainted with our sense-data, and, probably, with ourselves. These we know to exist. And past sense-data which are remembered are known to have existed in the past. This knowledge supplies our data.

But if we are to be able to draw inferences from these data -- if we are to know of the existence of matter, of other people, of the past before our individual memory begins, or of the future, we must know general principles of some kind by means of which such inferences can be drawn. It must be known to us that the existence of some sort of thing, A, is a sign of the existence of some other sort of thing, B, either at the same time as A or at some earlier or later time, as, for example, thunder is a sign of the earlier existence of lightning. If this were not known to us, we could never extend our knowledge beyond the sphere of our private experience; and this sphere, as we have seen, is exceedingly limited. The question we have now to consider is whether such an extension is possible, and if so, how it is affected.

On web march 31th 2016 source: http://www.ditext.com/russell/rus6.html

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 58

Let us take as an illustration a matter about which of us, in fact, feel the slightest doubt. We are all convinced that the sun will rise to-morrow. Why? Is this belief a mere blind outcome of past experience, or can it be justified as a reasonable belief? It is not find a test by which to judge whether a belief of this kind is reasonable or not, but we can at least ascertain what sort of general beliefs would suffice, if true, to justify the judgement that the sun will rise to-morrow, and the many other similar judgements upon which our actions are based.

It is obvious that if we are asked why we believe it the sun will rise to-morrow, we shall naturally answer, 'Because it always has risen every day'. We have a firm belief that it will rise in the future, because it has risen in the past. If we are challenged as to why we believe that it will continue to rise as heretofore, we may appeal to the laws of motion: the earth, we shall say, is a freely rotating body, and such bodies do not cease to rotate unless something interferes from outside, and there is nothing outside to interfere with the earth between now and to-morrow. Of course it might be doubted whether we are quite certain that there is nothing outside to interfere, but this is not the interesting doubt. The interesting doubt is as to whether the laws of motion will remain in operation until to-morrow. If this doubt is raised, we find ourselves in the same position as when the doubt about the sunrise was first raised.

On web march 31th 2016 source: http://www.ditext.com/russell/rus6.html

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 59

The only reason for believing that the laws of motion remain in operation is that they have operated hitherto, so far as our knowledge of the past enables us to judge. It is true that we have a greater body of evidence from the past in favour of the laws of motion than we have in favour of the sunrise, because the sunrise is merely a particular case of fulfilment of the laws of motion, and there are countless other particular cases. But the real question is: Do any number of cases of a law being fulfilled in the past afford evidence that it will be fulfilled in the future? If not, it becomes plain that we have no ground whatever for expecting the sun to rise to-morrow, or for expecting the bread we shall eat at our next meal not to poison us, or for any of the other scarcely conscious expectations that control our daily lives. It is to be observed that all such expectations are only probable; thus we have not to seek for a proof that they must be fulfilled, but only for some reason in favour of the view that they are likely to be fulfilled.

On web march 31th 2016 source: http://www.ditext.com/russell/rus6.html

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 60

Now in dealing with this question we must, to begin with, make an important distinction, without which we should soon become involved in hopeless confusions. Experience has shown us that, hitherto, the frequent repetition of some uniform succession or coexistence has been a cause of our expecting the same succession or coexistence on the next occasion. Food that has a certain appearance generally has a certain taste, and it is a severe shock to our expectations when the familiar appearance is found to be associated with an unusual taste. Things which we see become associated, by habit, with certain tactile sensations which we expect if we touch them; one of the horrors of a ghost (in many ghost-stories) is that it fails to give us any sensations of touch. Uneducated people who go abroad for the first time are so surprised as to be incredulous when they find their native language not understood.

On web march 31th 2016 source: http://www.ditext.com/russell/rus6.html

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 61

And this kind of association is not confined to men; in animals also it is very strong. A horse which has been often driven along a certain road resists the attempt to drive him in a different direction. Domestic animals expect food when they see the person who feeds them. We know that all these rather crude expectations of uniformity are liable to be misleading. The man who has fed the chicken every day throughout its life at last wrings its neck instead, showing that more refined views as to the uniformity of nature would have been useful to the chicken.

But in spite of the misleadingness of such expectations, they nevertheless exist. The mere fact that something has happened a certain number of times causes animals and men to expect that it will happen again. Thus our instincts certainly cause us to believe the sun will rise to-morrow, but we may be in no better a position than the chicken which unexpectedly has its neck wrung. We have therefore to distinguish the fact that past uniformities cause expectations as to the future, from the question whether there is any reasonable ground for giving weight to such expectations after the question of their validity has been raised.

On web march 31th 2016 source: http://www.ditext.com/russell/rus6.html

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 62

The problem we have to discuss is whether there is any reason for believing in what is called 'the uniformity of nature'. The belief in the uniformity of nature is the belief that everything that has happened or will happen is an instance of some general law to which there are no exceptions. The crude expectations which we have been considering are all subject to exceptions, and therefore liable to disappoint those who entertain them. But science habitually assumes, at least as a working hypothesis, that general rules which have exceptions can be replaced by general rules which have no exceptions. 'Unsupported bodies in air fall' is a general rule to which balloons and aeroplanes are exceptions. But the laws of motion and the law of gravitation, which account for the fact that most bodies fall, also account for the fact that balloons and aeroplanes can rise; thus the laws of motion and the law of gravitation are not subject to these exceptions.

The belief that the sun will rise to-morrow might be falsified if the earth came suddenly into contact with a large body which destroyed its rotation; but the laws of motion and the law of gravitation would not be infringed by such an event. The business of science is to find uniformities, such as the laws of motion and the law of gravitation, to which, so far as our experience extends, there are no exceptions. In this search science has been remarkably successful, and it may be conceded that such uniformities have held hitherto. This brings us back to the question: Have we any reason, assuming that they have always held in the past, to suppose that they will hold in the future?

On web march 31th 2016 source: http://www.ditext.com/russell/rus6.html

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 63

It has been argued that we have reason to know that the future will resemble the past, because what was the future has constantly become the past, and has always been found to resemble the past, so that we really have experience of the future, namely of times which were formerly future, which we may call past futures. But such an argument really begs the very question at issue. We have experience of past futures, but not of future futures, and the question is: Will future futures resemble past futures? This question is not to be answered by an argument which starts from past futures alone. We have therefore still to seek for some principle which shall enable us to know that the future will follow the same laws as the past.

The reference to the future in this question is not essential. The same question arises when we apply the laws that work in our experience to past things of which we have no experience -- as, for example, in geology, or in theories as to the origin of the Solar system. The question we really have to ask is: 'When two things have been found to be often associated, and no instance is known of the one occurring without the other, does the occurrence of one of the two, in a fresh instance, give any good ground for expecting the other?' On our answer to this question must depend the validity of the whole of our expectations as to the future, the whole of the results obtained by induction, and in fact practically all the beliefs upon which our daily life is based.

On web march 31th 2016 source: http://www.ditext.com/russell/rus6.html

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 64

It must be conceded, to begin with, that the fact that two things have been found often together and never apart does not, by itself, suffice to prove demonstratively that they will be found together in the next case we examine. The most we can hope is that the oftener things are found together, the more probable becomes that they will be found together another time, and that, if they have been found together often enough, the probability will amount almost to certainty. It can never quite reach certainty, because we know that in spite of frequent repetitions there sometimes is a failure at the last, as in the case of the chicken whose neck is wrung. Thus probability is all we ought to seek.

On web march 31th 2016 source: http://www.ditext.com/russell/rus6.html

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 65

It might be urged, as against the view we are advocating, that we know all natural phenomena to be subject to the reign of law, and that sometimes, on the basis of observation, we can see that only one law can possibly fit the facts of the case. Now to this view there are two answers. The first is that, even if some law which has no exceptions applies to our case, we can never, in practice, be sure that we have discovered that law and not one to which there are exceptions. The second is that the reign of law would seem to be itself only probable, and that our belief that it will hold in the future, or in unexamined cases in the past, is itself based upon the very principle we are examining.

The principle we are examining may be called the principle of induction, and its two parts may be stated as follows:

(a) When a thing of a certain sort A has been found to be associated with a thing of a certain other sort B, and has never been found dissociated from a thing of the sort B, the greater the number of cases in which A and B have been associated, the greater is the probability that they will be associated in a fresh case in which one of them is known to be present;

(b) Under the same circumstances, a sufficient number of cases of association will make the probability of a fresh association nearly a certainty, and will make it approach certainty without limit.

On web march 31th 2016 source: http://www.ditext.com/russell/rus6.html

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 66

As just stated, the principle applies only to the verification of our expectation in a single fresh instance. But we want also to know that there is a probability in favour of the general law that things of the sort A are always associated with things of the sort B, provided a sufficient number of cases of association are known, and no cases of failure of association are known. The probability of the general law is obviously less than the probability of the particular case, since if the general law is true, the particular case must also be true, whereas the particular case may be true without the general law being true. Nevertheless the probability of the general law is increased by repetitions, just as the probability of the particular case is. We may therefore repeat the two parts of our principle as regards the general law, thus:

(a) The greater the number of cases in which a thing the sort A has been found associated with a thing the sort B, the more probable it is (if no cases of failure of association are known) that A is always associated with B;

(b) Under the same circumstances, a sufficient number of cases of the association of A with B will make it nearly certain that A is always associated with B, and will make this general law approach certainty without limit.

On web march 31th 2016 source: http://www.ditext.com/russell/rus6.html

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 67

It should be noted that probability is always relative to certain data. In our case, the data are merely the known cases of coexistence of A and B. There may be other data, which might be taken into account, which would gravely alter the probability. For example, a man who had seen a great many white swans might argue by our principle, that on the data it was probable that all swans were white, and this might be a perfectly sound argument. The argument is not disproved by the fact that some swans are black, because a thing may very well happen in spite of the fact that some data render it improbable. In the case of the swans, a man might know that colour is a very variable characteristic in many species of animals, and that, therefore, an induction as to colour is peculiarly liable to error. But this knowledge would be a fresh datum, by no means proving that the probability relatively to our previous data had been wrongly estimated. The fact, therefore, that things often fail to fulfil our expectations is no evidence that our expectations will not probably be fulfilled in a given case or a given class of cases. Thus our inductive principle is at any rate not capable of being disproved by an appeal to experience.

On web march 31th 2016 source: http://www.ditext.com/russell/rus6.html

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 68

The inductive principle, however, is equally incapable of being proved by an appeal to experience. Experience might conceivably confirm the inductive principle as regards the cases that have been already examined; but as regards unexamined cases, it is the inductive principle alone that can justify any inference from what has been examined to what has not been examined. All arguments which, on the basis of experience, argue as to the future or the unexperienced parts of the past or present, assume the inductive principle; hence we can never use experience to prove the inductive principle without begging the question. Thus we must either accept the inductive principle on the ground of its intrinsic evidence, or forgo all justification of our expectations about the future. If the principle is unsound, we have no reason to expect the sun to rise to-morrow, to expect bread to be more nourishing than a stone, or to expect that if we throw ourselves off the roof we shall fall. When we see what looks like our best friend approaching us, we shall have no reason to suppose that his body is not inhabited by the mind of our worst enemy or of some total stranger. All our conduct is based upon associations which have worked in the past, and which we therefore regard as likely to work in the future; and this likelihood is dependent for its validity upon the inductive principle.

On web march 31th 2016 source: http://www.ditext.com/russell/rus6.html

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 69

The general principles of science, such as the belief in the reign of law, and the belief that every event must have a cause, are as completely dependent upon the inductive principle as are the beliefs of daily life All such general principles are believed because mankind have found innumerable instances of their truth and no instances of their falsehood. But this affords no evidence for their truth in the future, unless the inductive principle is assumed.

Thus all knowledge which, on a basis of experience tells us something about what is not experienced, is based upon a belief which experience can neither confirm nor confute, yet which, at least in its more concrete applications, appears to be as firmly rooted in us as many of the facts of experience. The existence and justification of such beliefs -- for the inductive principle, as we shall see, is not the only example -- raises some of the most difficult and most debated problems of philosophy. We will, in the next chapter, consider briefly what may be said to account for such knowledge, and what is its scope and its degree of certainty.

On web march 31th 2016 source: http://www.ditext.com/russell/rus6.html

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 70

Two Statues: An Introduction to the Philosophy of Science (Part 1-1) https://www.youtube.com/watch?v=g6p3RzMByWA&list=PL67E25537

70A6E39E

The Problem of Induction and Russell's Chicken

(Lecture 5, video #1 of 3) https://www.youtube.com/watch?v=C9GJ4965lOM

The Hypothetico-Deductive Method and The Ravens Paradox

(Lecture 5, Video 2 of 3) https://www.youtube.com/watch?v=neKF58h0Dsc

Goodman's New Riddle of Induction (Lecture 5, video #3 of 3) https://www.youtube.com/watch?v=2vviTuYhfa8

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 71

Are all swans white?

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 72

Falsifiability or refutability of a statement, hypothesis, or theory is the inherent possibility that it can be proven false. A statement is called falsifiable if it is possible to conceive of an observation or an argument which negates the statement in question. In this sense,falsify is synonymous with nullify, meaning to invalidate or "show to be false".

For example, by the problem of induction, no number of confirming observations can verify a universal generalization, such as All swans are white, since it is logically possible to falsify it by observing a single black swan. Thus, the term falsifiability is sometimes synonymous to testability. Some statements, such as It will be raining here in one million years, are falsifiable in principle, but not in practice.[1]

The concern with falsifiability gained attention by way of philosopher of science Karl Popper's scientific epistemology "falsificationism". Popper stresses the problem of demarcation—distinguishing the scientific from the unscientific—and makes falsifiability the demarcation criterion, such that what is unfalsifiable is classified as unscientific, and the practice of declaring an unfalsifiable theory to be scientifically true is pseudoscience.

(https://en.wikipedia.org/wiki/Falsifiability#Inductive_categorical_inference)

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 73

The black swan theory or theory of black swan events is a metaphor describing events that comes as a surprise and have big impacts; such events are often inappropriately rationalized after they happened with the benefit of hindsight.

The phrase "black swan" derives from a Latin expression; its oldest known occurrence is due the poet Juvenal who used the image in order to characterize extremely rare occurences: "rara avis in terris nigroque simillima cygno" ("a rare bird in the lands and very much like a black swan"). When the phrase was coined, the black swan was presumed not to exist. But the saying was rewritten after black swans were discovered in Australia.

The importance of the metaphor lies in its analogy to the fragility of any system of thought. A set of conclusions is potentially undone once any of its fundamental postulates is disproved. In this case, the observation of a single black swan would be the undoing of the logic of any system of thought, as well as any reasoning that followed from that underlying logic. ht

tps:

//en.

wik

iped

ia.o

rg/w

iki/B

lack

_sw

an_t

heor

y

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 74

The theory of black swans, in contrast, is more recent and was developed by NassimNicholas Taleb to explain:

The disproportionate role of high-profile, hard-to-predict, and rare events that are beyond the realm of normal expectations in history, science, finance, and technology.

The non-computability of the probability of the consequential rare events using scientific methods (owing to the very nature of small probabilities).

The psychological biases that blind people, both individually and collectively, to uncertainty and to a rare event's massive role in historical affairs.

Unlike the earlier and broader "black swan problem" in philosophy (i.e. the problem of induction), Taleb's "black swan theory" refers only to unexpected events of large magnitude and consequence and their dominant role in history.

Such events, considered extreme outliers, collectively play vastly larger roles than regular occurrences. More technically, in the scientific monograph 'Silent Risk', Talebmathematically defines the black swan problem as "stemming from the use of degenerate metaprobability".

http

s://e

n.w

ikip

edia

.org

/wik

i/Bla

ck_s

wan

_the

ory

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 75

Black swan events are discussed by Nassim Nicholas Taleb in his 2001 book Fooled By Randomness (on financial events). In 2007 book The Black Swan he extends the metaphor outside of financial markets.

Taleb regards almost all major scientific discoveries, historical events, and artistic accomplishments as "black swans"—undirected and unpredicted. He gives the rise of the Internet, the personal computer, World War I, dissolution of the Soviet Union, and the September 2001 attacks as examples of black swan events.

Taleb asserts (2007, chp.1):

What we call here a Black Swan (and capitalize it) is an event with the following three attributes. First, it is an outlier, as it lies outside the realm of regular expectations, because nothing in the past can convincingly point to its possibility. Second, it carries an extreme 'impact'. Third, in spite of its outlier status, human nature makes us concoct explanations for its occurrence after the fact, making it explainable and predictable.

I stop and summarize the triplet: rarity, extreme 'impact', and retrospective (though not prospective) predictability. A small number of Black Swans explains almost everything in our world, from the success of ideas and religions, to the dynamics of historical events, to elements of our own personal lives.

http

s://e

n.w

ikip

edia

.org

/wik

i/Bla

ck_s

wan

_the

ory

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 76

Taleb's black swan is different from the earlier philosophical versions of the problem, specifically in epistemology, as it concerns a phenomenon with specific empirical and statistical properties which he calls, "the fourth quadrant“ (2008).

Taleb's problem is about epistemic limitations in some parts of the areas covered in decision making. These limitations are twofold: philosophical (mathematical) and empirical (human known epistemic biases).

The philosophical problem is about the decrease in knowledge when it comes to rare events as these are not visible in past samples and therefore require a strong a priori, or an extrapolating theory; accordingly predictions of events depend more and more on theories when their probability is small. In the fourth quadrant, knowledge is uncertain and consequences are large, requiring more robustness.

http

s://e

n.w

ikip

edia

.org

/wik

i/Bla

ck_s

wan

_the

ory

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 77

According to Taleb, thinkers who came before him who dealt with the notion of the improbable, such as Hume, Mill, and Popper focused on the problem of induction in logic, specifically, that of drawing general conclusions from specific observations. The central and unique attribute of Taleb's black swan event is high profile. His claim is that almost all consequential events in history come from the unexpected — yet humans later convince themselves that these events are explainable in hindsight.

One problem, labeled the ludic fallacy by Taleb, is the belief that the unstructured randomness found in life resembles the structured randomness found in games. This stems from the assumption that the unexpected may be predicted by extrapolating from variations in statistics based on past observations, especially when these statistics are presumed to represent samples from a normal distribution. These concerns often are highly relevant in financial markets, where major players sometimes assume normal distributions when using value at risk models, although market returns typically have fat tail distributions.

http

s://e

n.w

ikip

edia

.org

/wik

i/Bla

ck_s

wan

_the

ory

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 78

Taleb said "I don't particularly care about the usual. If you want to get an idea of a friend's temperament, ethics, and personal elegance, you need to look at him under the tests of severe circumstances, not under the regular rosy glow of daily life. Can you assess the danger a criminal poses by examining only what he does on an ordinary day? Can we understand health without considering wild diseases and epidemics? Indeed the normal is often irrelevant. Almost everything in social life is produced by rare but consequential shocks and jumps; all the while almost everything studied about social life focuses on the "normal," particularly with "bell curve" methods of inference that tell you close to nothing. Why? Because the bell curve ignores large deviations, cannot handle them, yet makes us confident that we have tamed uncertainty. Its nickname in this book is GIF, Great Intellectual Fraud."

http

s://e

n.w

ikip

edia

.org

/wik

i/Bla

ck_s

wan

_the

ory

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 79

More generally, decision theory, based on a fixed universe or a model of possible outcomes, ignores and minimizes the effect of events that are "outside model".

For instance, a simple model of daily stock market returns may include extreme moves such as Black Monday (1987), but might not model the breakdown of markets following the 9/11 attacks. A fixed model considers the "known unknowns", but ignores the "unknown unknowns", made famous by a statement of Donald Rumsfeld (2002). The term "unknown unknowns" appeared in a 1982 New Yorker article on the aerospace industry, which cites the example of metal fatigue, the cause of crashes in Comet airliners in the 1950s.

Taleb notes that other distributions are not usable with precision, but often are more descriptive, such as the fractal, power law, or scalable distributions and that awareness of these might help to temper expectations.

Beyond this, he emphasizes that many events simply are without precedent, undercutting the basis of this type of reasoning altogether.

Taleb also argues for the use of counterfactual reasoning when considering risk.

http

s://e

n.w

ikip

edia

.org

/wik

i/Bla

ck_s

wan

_the

ory

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 80

A black swan is an event or occurrence that deviates beyond what is normally expected of a situation and is extremely difficult to predict; the term was popularized by Nassim Nicholas Taleb, a finance professor, writer and former Wall Street trader. Black swan events are typically random and are unexpected.

The idea of a black swan event was pioneered by the financial professional turned writer Nassim Nicholas Taleb after the results of the 2008 financial crisis. Taleb argued that black swan events are impossible to predict yet have catastrophic ramifications. Therefore, it is important for people to always assume a black swan event is a possibility, whatever it may be, and to plan accordingly. He also used the 2008 financial crisis and the idea of black swan events to point out if a broken system is allowed to fail, it actually strengthens it against the catastrophe of future black swan events.

Taleb spent 21 years on Wall Street as a quant trader, developing the computer models for financial institutions. Since that time, he has written a long-form essay broken into three books: "The Black Swan: The Impact of the Highly Improbable," "Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets" and "Antifragile: Things That Gain from Disorder." He has been a distinguished professor of risk engineering at NYU's School of Engineering and written over 45 peer-reviewed papers.

Read more: http://www.investopedia.com/terms/b/blackswan.asp

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 81

Examples of Past Black Swan Events

The financial crash of the U.S. housing market during the 2008 crisis is one of the most recent and well-known black swan events as of 2016. The effect of the crash was catastrophic and global, and only a few outliers were able to predict it happening. Also in 2008, Zimbabwe had the worst case of hyperinflation in the 21st century with a peak inflation rate of more than 79.6 billion percent. An inflation level of that amount is nearly impossible to predict and can easily ruin a country financially.

The dot-com bubble of 2001 is another black swan event that has similarities to the 2008 financial crisis. America was enjoying rapid economic growth and increases in private wealth before the economy catastrophically collapsed. Since the Internet was at its infancy in terms of commercial use, various investment funds were investing in technology companies with inflated valuations and no market traction. When these companies folded, the funds were hit hard, and the downside risk was passed onto the investors. The digital frontier was new, and therefore it was nearly impossible to predict the collapse.

As another example, the previously successful hedge fund Long Term Capital Management (LTCM) was driven into the ground in 1998 as a result of the ripple effect caused by the Russian government's debt default, something the company's computer models could not have predicted

Read more: http://www.investopedia.com/terms/b/blackswan.asp

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 82

The term "grey swan" is derived from the term black swan which was the term given by Nassim Nicholas Taleb to extremely unlikely, unforeseen risk events with a major impact.However, the slew of bad news in markets since the financial crisis suggests unexpected events with a major impact are happening increasingly frequently. This has led some analysts to start using the term grey swan to describe events that, potentially, are as catastrophic as black swan events but that are likely to happen more frequently. (http://lexicon.ft.com/Term?term=grey-swan)

An event that can be anticipated to a certain degree, but is considered unlikely to occur and may have a sizable impact on the valuation of a security or the health of the overall market if it does occur. A grey swan event is unlike a black swan event whose total impact is difficult to predict. Despite the possibility of determining the properties and potential impact of such an event, it is difficult to create precise calculations regarding the total impact.

Grey swan events, may include earthquakes and even events like the Great Depression. While analysts can look at the impacts that similar events had across history, the exact extent of damage and risk cannot be calculated. (http://www.investopedia.com/terms/g/grey-swan.asp)

Macroeconomic Dynamics a.a. 2017-2018

Prof. AnnaMaria Variato 83

Coming next: