Embed Size (px)

Citation preview

T H E K E Y C O N C E P T :MEDICAL DEVICE OUTSOURCING

Plastics companies

27% annual increase in medtech OEMs share price

Opportunity to FocusLake Region Medical

sold for $1.7bn

Value DifferentialDiversified engineering: 9.3x

Pure play MDO: 13.0x

c.150% projected increasein the number of people aged over 60

13 of the world´s top 15 medtech OEMs Medtech OEMs

Precision engineering companies

Service companies

H 2 2 0 1 6

Strong global growth and the opportunity for Irish engineering companies to participate

Outsourcing creates new industry�

Significant M&A activity in MDO

110% 2015-2016

While metals continue to be a prominent material in the production of medical devices, a significant amount of the growth and indeed innovation in the industry is being delivered through the use of advanced polymers.

Over the past few years, polymers have been increasingly substituting traditional materials such as metals owing to their cost, biocompatibility and lightness in weight.

This trend is expected to continue due to the advancement in material science and increased safety measures for packaging.

Does this mean precision engineering businesses are going to be left behind? Absolutely not – indeed the combination of engineering skill with both materials (plastics and metals) allows companies to truly provide a comprehensive solution to their medical device clients.

MACRO OVERVIEW

The medical device industry is growing at an impressive trajectory by any standards. The global market has grown at 4.4% compound annual growth rate and is projected to continue its strong, stable improvement. A range of factors are contributing to this growth including greater healthcare access, advances in technology, the growth of the middle class in emerging markets, and an increasing and ageing population. The contribution of an aging population is significant in its own right - by 2050, it is forecast that 20% of the world’s population will be aged 60 and over (12% in 2013). Quite simply, as the population ages the demand for medical devices will increase.

So all of these favourable demand trends are wonderful if you are a Boston Scientific, Medtronic or Stryker (confirmed by their 27% share price increase over the last year) but what does it mean for the traditional engineering sector? Can plastics and precision engineering businesses ride on the coattails of this growth or, even better, transform themselves into medical device outsourcing (MDO) companies?

Although this metamorphosis will require some difficult decisions to be made in the short term, the answer is yes. Unfortunately the attractiveness of healthcare clients provides challenges. These relationships take a long time to foster because of the long lead times for product development, criticality of the underlying product and associated regulation. When you do obtain a medtech company as a customer, however, they tend to be both sticky and highly profitable.

Ageing population drives demand

Plastics or metals?

The good news for Irish engineering companies is that Ireland is one of the hotspots for global medtech companies. The statistics are compelling - thirteen of the world’s top fifteen medtech companies operate in Ireland, we are the 2nd largest exporter of medical devices in Europe and we are world beaters in certain product categories (e.g. we manufacture 80% of the world’s stents and 50% of the world’s ventilators for acute hospitals).

Ireland has been successful at attracting medtech companies for the reasons we are all familiar with (well educated, English speaking workforce, attractive corporation tax, business friendly regulation, etc). These broader incentives have been supplemented by academic and governmental supports that are extremely targetted at the sector.

One proactive example of government support is the recent establishment of CURAM, a global medical device research centre at NUI Galway. This further emphasises Ireland´s position as one of the top global medtech clusters.

Medical device hotspot

Source: United Nations Department of Economic and Social Affairs

c.150% projected increase in the number of people aged over 60

2,500

2,000

1,500

500

0

1,000

Mill

ions

of p

eopl

e

1950

1960

1970

1980

1990

2000

2010

2020

2030

2040

2050

1955

1965

1975

1985

1995

2005

2015

2025

2035

2045

c.150

% grow

th

IRELAND – A UNIQUE PLACE TO BE

Ireland: international medtech hub

This backdrop creates a relatively unique opportunity for Irish companies in the wider engineering supply chain to secure a disproportionate amount of business from this sector or indeed over time become specialists in medical devices (see case study: Creganna).

This provides the benefits of a strong growth outlook, non-cyclical demand characteristics, long term customer relationships and higher margins. These characteristics can transform not just the profitability of a business but its ultimate value to an acquirer (see valuation dynamics).

Irish engineering has a head start

Hollister €80m investment in plant, employs 600 people June 2014

AbbVie €40m investment to expand manufacturing capacity January 2015

VistaMed €10m investment in a R&D facility August 2016

Moss Vision Establishing a facility to produce intraocular lenses June 2015

Teleflex Expanding its shared services and R&D facility October 2014

Bausch & Lomb €75m to increase manufacturing capacity April 2015

Stryker Building a new Surgical Innovation Centre September 2014

Medtronic €13m investment in a new manufacturing facility December 2015

Zimmer €51m manufacturing plant for orthopaedic implants January 2015

Ethicon Biosurgery €80m investment in plant April 2014

NORTH (1)

MDOs 3OEMs 1

EAST

MDOs 31OEMs 21

WEST

MDOs 31OEMs 9

Note: (1) Excludes Northern I re landSources: I r ish Medical Devices Associat ion, Col l ins McNicholas and Fora. ie

SOUTH

MDOs 21OEMs 28

MDO – Medical Device Outsourcing CompanyOEM – Medical Device Original Equipment Manufacturer

Major recent investments in Ireland

The below table shows a selection of these up and coming companies.

Irish plastics and precision engineering companies have the opportunity to shift towards the top right of the matrix by emulating the business model of the likes of Duke Empirical, Creganna and Vistamed. This is a very slow process if done organically. Ideally existing business lines should be structured in a way that they are easily divisible, such that once critical mass in medical devices is reached, other aspects could be divested.

Alternatively a proactive M&A strategy is worth considering however valuation expectations for pure play medical device outsourcing companies may make this strategy prohibitively expensive. A buy and build strategy to acquire manufacturers with diversified sector exposure may be more prudent. However, the post transaction restructuring and divestment required to be left with a medtech business of scale would be time consuming and not without risk.

MOVING UP THE MEDTECH VALUE CHAIN

Market positioning

NAME DESCRIPTION

AventaMed Device for inserting grommets

Blueacre Technology Laser systems for medical device and electronic part manufacture

Bluedrop Medical Detect foot ulcers in diabetics

Capsos Medical Treatment for unblocking arteries

NeoSurgical Products to make laparoscopic abdominal surgery safer

Neuravi Stroke therapy device

Neuromod Research and development of neuromodulation technologies

PMD Solutions Medical device manufacturers

SelfSense Technologies Teeth grinding solution

X-Bolt Orthopaedics Expanding bolt medical device for hip fracture fixation

CLASS IIIProsthetic joints Coronary stent

Basic component contract manufacture Design led contract manufacture R&D and complex manufacture

CLASS IIHypodermic needle Orthopaedic implants

CLASS INon-sterile gloves Urine bag

Irish Precision Engineering

Prod

uct r

isk

& re

gula

tion

Def

ensi

vene

ss

Profitability

Design & manufacturing complexity HIGH

HIGH

MDOs OEMs

HIGH

HIGH

Irish Plastics

Source: Key Capital research

Sources: Si l icon Republ ic and Key Capital research

While the focus of this research is on the opportunity for engineering companies in Ireland, the presence of large multinational medical device specialists has given rise to a burgeoning medtech startup sector in Ireland. These are not manufacturing businesses but pure play R&D focused companies which have been largely seeded by former executives of multinationals.

Ireland’s R&D

startups

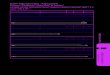

The chart shows two distinctive groups of company types within the medical devices outsourcing space; diversified engineering companies and pure play MDO companies. The pure play MDOs are showing higher valuations. Investors are willing to pay a higher premium for these

companies based on their increased profitability and stability of earnings. Medtech OEMs are less focused on cost than OEMs in some industries given the absolute requirement for quality which translates to higher margins for outsourcers.

VALUATION DYNAMICS

MDOs valued at a premium

Value vs. Profitability

EV

/201

6E E

BIT

DA

2016E EBITDA margin

20.0x

25.0x

15.0x

10.0x

5.0x

0.0x10.0% 15.0% 20.0% 25.0% 30.0%

Nolato

PSB Industries

SKF

Resilux

Integer

NordsonTeleflex

West Pharmaceutical

Masterflex

Source: Key Capital research

2016E EBITDA margin

EV/2016E EBITDA

16.3%

9.3x

21.2%

13.0x

Diversified engineering average

Pure play MDO average

There has been very significant M&A activity in the MDO

sector(1),with 21 deals announced in the first half of 2016 as compared with 10 in the same period in 2015. The sector is highly fragmented yet OEM clients are increasingly seeking partners with the breadth of product offering and scale that companies of their size and sophistication require.

As medtech companies increase their scale though organic investment and M&A of eye watering proportions (e.g. Medtronic’s $50bn purchase of Covidien), outsourcing companies are also engaging in consolidation. Greatbatch’s acquisition of Lake Region Medical for $1.7bn is a high profile example of a scale driven acquisition in the sector however there are a number of examples at the other end of the market where smaller companies are making strategic acquisitions to obtain both scale and expertise.

A number of these are backed by private equity firms seeking to replicate the success that Permira had with Creganna, for example the acquisition of A&E Medical Corporate by a number of private equity and investment funds.

We believe this trend of consolidation will continue as growth oriented outsourced providers seek to capitalise on favourable industry conditions and funding dynamics to acquire firms in order to expand service capabilities, geographic presence, client relationships and technical competence.

An example of an innovative use of plastics in medicine is the creation of a human skull made in the Netherlands. The plastic skull was created using advanced 3D printing technology. A 22 year old woman suffered from severe headaches that were caused by a thickening of her skull. This lead to a number of highly restrictive symptoms including loss of vision and motor control. Her essential brain functions would ultimately have ceased if a solution were not found. Surgeons were able to replace the thickened skull with an accurately fitted 3D printed plastic skull. The patient was back at work just a few months later, having made a full recovery. There are plans for other patients with similar conditions to be treated too.

M&A

CASE STUDY: CREGANNAThe transformation from precision engineering to MDO.

Creganna, the global MDO success story, originated as a small precision engineering company in Galway.

Explosion in MDO M&A activity

Innovation in practice

(1) Medical device outsourcing appl ies to industr ies that supply medical device OEMs with products and services. These can include everything f rom diversi f ied plast ics and precis ion engineer ing companies wi th some exposure to the sector and to pure play medtech contract manufactur ing businesses such as Creganna.

*We have much more data on this t ransact ion.

Founded to service a range

of precision engineering services to

multiple industries

Commenced supplying to the medical device

sector

Opens first facility

dedicated to medical device manufacturing

Divested all non-medical

device operations

to focus exclusively on

this sector

Creganna Medical Devices acquires Tactx Medical Inc.

Creganna – Tactx Medical is acquired by

Permira for €220m

Creganna – Tactx Medical acquires ABT

Medical Limited

Creganna – Tactx Medical

acquires Precision Wire Components

Inc.

TE Connectivity* acquires

Creganna – Tactx Medical for €821m with

an EV/LTM Revenue of 3.6x

1979 1998 2000 2008 2009 2010 2012 2014 2016

Source: wired.co.uk

M&A

WHAT DOES THIS ALL MEAN?

Due to improving healthcare, and advances in research and technology, there has been a marked increase in global life expectancy. This, in combination with the forecasted shift towards an increasingly ageing demographic, has and will continue to drive the demand for medical devices and has consequently increased valuations of medical devices OEMs. The increased trend from these companies to outsource manufacturing creates an opportunity to ride this growth opportunity and indeed valuation dynamics.

Irish plastics and precision engineering companies have a head start over their international peers in that they have most likely been servicing medtech companies for many years. The transition from diversified contract manufacturer to a fully-fledged MDO is not an easy one. The organic route takes time, investment and the potential sacrifice of other profitable business lines. The M&A route requires valuation discipline, patience and a willingness to take on integration risk. However for those willing to embark on this journey, there is capital available to support both strategies and the prize, as is clear from the valuation analysis, is a significant one. In Lake Region Medical and, closer to home, Creganna, roadmaps exist for success.

On the other hand if you are a potential seller, this buoyant M&A market and demand for MDOs provides an opportunity for diversified manufacturers with exposure to the medtech sector to obtain a premium valuation. This requires careful positioning and identification of the optimal international buyer – a party who sees this long term potential. We would be happy to discuss some strategic options for how both strategies can be successfully implemented.

OPPORTUNITIES✓ Long term contracts✓ High margins✓ High barriers to entry✓ High exit valuation✓ Stability of earnings✓ Counter cyclical✓ Strong growth

CHALLENGES✕ Stringent regulations

✕ High barriers to entry

✕ Increasingly complex technologies

✕ Long lead times

✕ Significant investment required

Selected M&A transactions in 2016

ANNOUNCED TARGET COUNTRY OF TARGET ACQUIRER THEME

September 16 Xeridiem Medical Devices Inc. United States PPC Industries Inc. Diversified plastics packaging company acquires MDO company

August 16 Phillips-Medisize Corporation United States Molex LLC Electronic components company acquires metal and plastics

MDO company

June 16 Tech Molded Plastics Inc. United States PRISM Plastics Inc. Precision injection moulding plastics company acquires diversified

plastics company

June 16 CEA Medical Manufacturing Inc. United States Graphic Controls Diversified manufacturing company acquires metal and plastics

MDO company

March 16 Johnson Precision Inc. United States Molded Rubber &

Plastic Corp.Plastics outsourcing company for medtech OEMs acquires plastics MDO company

March 16 Howard Precision Products Inc. United States Lampin Corporation Diversified precision engineering company acquires diversified

metal and plastics precision engineering company

February 16 A&E Medical Corporation United States Vance Street Capital

+ PE partners PE acquires metal and plastics MDO company

February 16 Peerless Injection Molding Inc. United States IRP Medical Plastics precision moulding company (medical devices) acquires

diversified precision engineering plastics company

February 16 Creganna-Tactx Medical Ireland Tyco Electronics UK

Holdings LtdDiversified engineering company acquires metal and plastics MDO company

January 16 Scientific Plastics Corporation United States Pexco LLC Diversified plastics company acquires plastics MDO company

Source: Key Capital research

IMAP BOSTONJohn [email protected]

IMAP DETROITGary N. [email protected]

IMAP CHICAGOW. Robert [email protected]

IMAP FLORIDAKurt [email protected]

IMAP IRELANDJonathan [email protected]

IMAP GERMANYChristoph [email protected]

IMAP NETHERLANDSPeer [email protected]

IMAP UKIan [email protected]

United States Europe

IMAP provides clients with access to seasoned sector experts from more than 40 independent investment banking teams in more than 65 office locations around the world.

Key Capital is the exclusive Irish member of IMAP.

ArgentinaBelgiumBosnia & HerzegovinaBrazilCanadaChileColombiaCroatiaCzech RepublicEgyptFinland

FranceGermanyHungaryIndiaIreland ItalyIvory CoastJapanMexicoMoroccoNetherlandsNorway

PeruPolandRussiaSenegalSerbiaSloveniaSpainSwedenTurkeyU.A.E.United KingdomUnited States

Jonathan Dalton Head of Corporate Finance

Telephone: + 353 1 638 3843 [email protected]

Cillian Ryan Associate

Telephone: + 353 1 638 [email protected]

Jagruti Rathod Analyst

Telephone: + 353 1 638 [email protected]

Tero Tiilikainen Director

Telephone: + 353 1 638 3833 [email protected]

Conor O'Riordan Analyst

Telephone: + 353 1 638 [email protected]

Alexandre Demenchuk Associate Director

Telephone: + 353 1 638 3846 [email protected]

KEY CAPITALHuguenot House,

St Stephen's Green, D02 NY63, Dublin, Ireland.

TEL + 353 1 638 3838

8

www.keycapital.ie

KEY CAPITAL CORPORATE FINANCE

IMAP PRECISION ENGINEERING AND MEDTECH EXPERTS

Cooper SurgicalProvider of women's health care

solutionsTrumbell, CT, United States

Acquired 100% of Equity

Laborie (Audax)Manufactures innovative medical

technologyToronto, Ontario, Canada

Acquired 100% of Business Operations of

Mediplast AB | Addtech ABMedtech wholesales

Malmö, SwedenAcquired 100% of

Business Operations of

AngioDynamics Inc. (NasdaqGS:ANGO)Provider of medical and

surgical devicesLatham, NY, United States

Acquired

Fujitsu LimitedLeading IT company

Tokyo, JapanDeveloped a Business and Capital Alliance as Partners for the Future

of Medical Care

The Pipette Company Manufacturer of micro pipettes for

the ART market Adelaide, Australia

Advised on Purchase of Company

T-DOC Company, LLC Manufacturers urology & diagnostic

products –catheters Wilmington, Delaware, United States

Advised the Seller

Fenno Medical Oy Medtech wholesales

Vantaa, FinlandAdvised on Sale of Company

Microsulis Medical Limited Provider of medical devices

Denmead, Hampshire, United KingdomAdvised the Seller

Yokogawa Medical Solutions Developer of medical equipment

Tokyo, JapanRepresented Fujitsu in this

Transaction