Embed Size (px)

Citation preview

Product Costing in the Meat gIndustry

CMC Conference June 2012

Quebec City

2010 1 © by CSB-System AG, Kestenholz, 2010

2010 2 © by CSB-System AG, Kestenholz, 2010

That you will come away with:

An understanding of common pitfalls associated with costing decisionswith costing decisions

Profit = Price - Cost Costing methods Costing methods Net/Net or FOB Price What to consider when What to consider when

determining your costing h

2010 3 © by CSB-System AG, Kestenholz, 2010

approach

Agenda

Background (Packers & Further Processors) Background (Packers & Further Processors) Why Calculate Cost of Products? What to consider in determining Costing Approach? Types of Costing Methods

Example O / Reverse BOM/Disassemble

Cutout Analysis BOM (Hotdog) BOM (Hotdog)

Summary and Rap-up Questions

2010 4 © by CSB-System AG, Kestenholz, 2010

Q

Why Calculate Cost of Products?

Profit: Goal in business is to sell products for more than cost Effective: Ensure you are selling the right products (highest margin) Ability to analyze costs to support improvement decisions Ability to analyze costs to support improvement decisions How should we price getting new business or new product line? “What if Analysis” Management by exceptions (variance) Bench mark best practices Targets for Continuous improvement Targets for Continuous improvement

There is no right or wrong way of product costing, each company has to find the best way of costing according to

2010 5 © by CSB-System AG, Kestenholz, 2010

p y y g gtheir specific processes, customers and resources

Why Calculate Costs

Although sales increased slightly in fiscal 2010, the company’s operating results declined rapidly. PricewaterhouseCoopers attributed the decline to a numberPricewaterhouseCoopers attributed the decline to a number of factors, including insufficient pricing and higher than forecast raw material costs on certain high-volume products; higher labour costs that were incurred becauseproducts; higher labour costs that were incurred because overtime was needed to meet unforeseen customer demand; and unscheduled production shutdowns caused

2010 6 © by CSB-System AG, Kestenholz, 2010

because Colonial didn’t have cash to operate

What to consider in determining Costing Approach?Costing Approach?

Keep it simple Keep it simple Easy to understand Focused on products that effect your profits (+/-) Focused on products that effect your profits (+/-) Ensure your are capturing the true costs Ability to change quickly Ability to change quickly Support new business and new product introduction Cost Containment/ Continuous ImprovementCost Containment/ Continuous Improvement Support determining priorities (add $$ to variances) Support decision on Outsource or Make Opportunities

2010 7 © by CSB-System AG, Kestenholz, 2010

pp pp Administrative effort to maintain

Costing Methods

Standard Costing (Bill of Materials BOM) Actual/Lot Costs Ability to Bear Cutout Valuation for Packers Forecast Costing (long term contracts)

2010 8 © by CSB-System AG, Kestenholz, 2010

Standard Costing

Product costs is calculated based on BOM Product costs is calculated based on BOM (Recipes in Food Industry)

Direct costs include the raw material packaging Direct costs include the raw material, packaging and the labour cost to produce the product

Indirect costs are expressed in terms of multiplier Indirect costs are expressed in terms of multiplier factors and extras such as overhead

Standard cost is used as an average product cost Standard cost is used as an average product cost over a period of time and is followed up by comparing it with the actual cost (variance)

2010 9 © by CSB-System AG, Kestenholz, 2010

Actual/Lot Cost

Th t l h i f i di t The actual purchase price of ingredients are attributed to your finished goods

The actual yield for producing each lot provides a y p g punique cost for each lot

The commodity prices of raw ingredients can vary significantly (substitutions or force in ingredients)significantly (substitutions or force in ingredients)

In further processing operations, each lot of raw material has a different cost and when used in

d ti h b t h t h diff tproduction causes each batch to have a different cost

For Lot calculation to be efficient, it requires a

2010 10 © by CSB-System AG, Kestenholz, 2010

, qcomputer system to keep track of the product flow

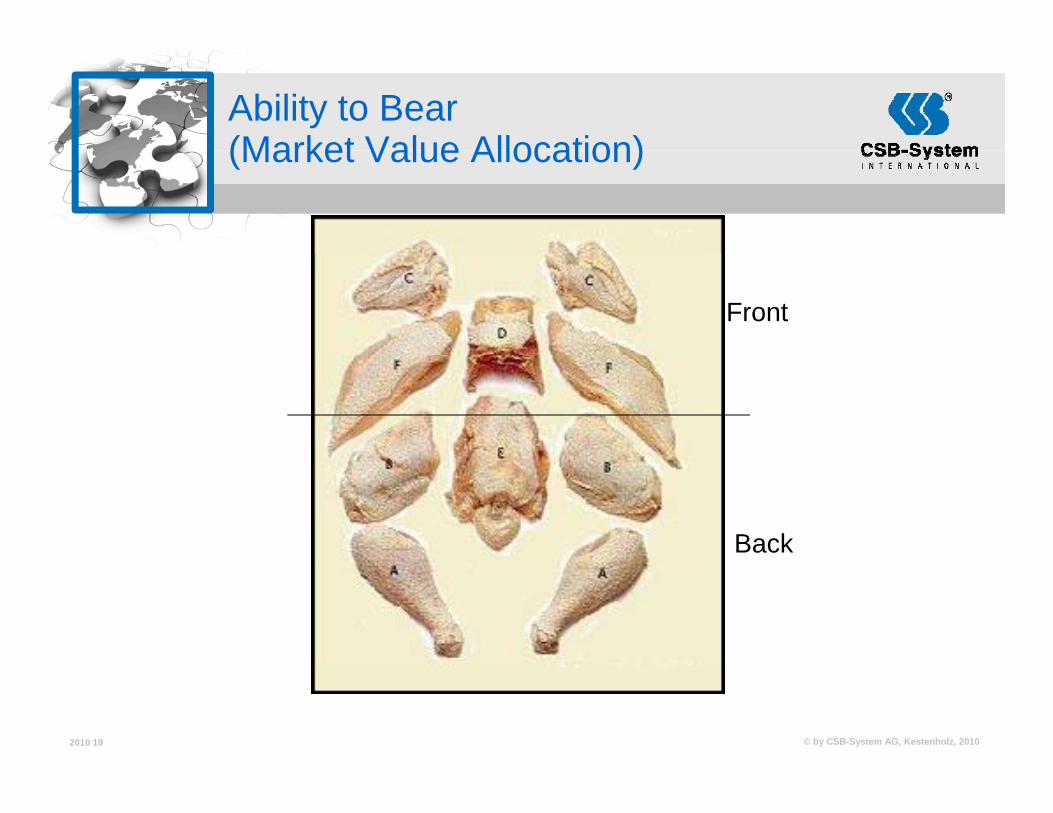

Ability to Bear(Market Value Allocation)(Market Value Allocation)

This is used by Packers or Steaking Operations This approach allocates costs in proportion to the

cost object’s ability to bear them An example the raw material cost of a carcass or

primal is the allocation to the components createdprimal is the allocation to the components created from the cutting process based on market value

The market value of the steaks are more than theThe market value of the steaks are more than the cube steaks which are more than the trim

2010 11 © by CSB-System AG, Kestenholz, 2010

Cutout Valuation (Packers)( )

This is a standard measurement in Slaughter goperations (USDA Beef and Pork Carcass Cutout)

Used by Packers as there are so many different ways of breaking up the carcass They are not ableways of breaking up the carcass. They are not able to allocate costs via traditional methods

Takes the commodity price of primals, subtracts the i t (l b ) d k i bconversion costs (labour) and packaging, by-

products to calculate the value of carcass or animal Compares calculated cutout value to actual p

purchase price of animal Value of the finished goods have little to do with the

cost to convert the animal into a finished good

2010 12 © by CSB-System AG, Kestenholz, 2010

cost to convert the animal into a finished good. Value of the finished goods is based on some external market list (USDA, Urner Barry, Chisholm)

What to consider when determining your costing approachyour costing approach

Perfection = Ideal conditions: this creates an environment of high accuracy but creates frustration as this is not realistically attainablefrustration as this is not realistically attainable

Practical = Realistic standards that employees can attainattain

Need to look at the value from capturing data, matched against the effort/cost in monitoring eachmatched against the effort/cost in monitoring each measurement to determine what level of detail you need to capture data

2010 13 © by CSB-System AG, Kestenholz, 2010

you need to capture data

Types of Costs

Variable costs Variable costs Raw materials (meat, spices, other ingredients) Packaging Packaging Landed Costs (Freight, Exchange, Duty, Broker)

Labour (different rates, and different areas)Labour (different rates, and different areas) Fixed Costs OverheadOverhead Admin. Expense

Selling & Delivery Costs

2010 14 © by CSB-System AG, Kestenholz, 2010

Selling & Delivery Costs Customer specific related costs

Labour Costs (Level of Detail)

Different Skills or Rates Different Skills or Rates Lead hand

Areas/Line where Labour is to be tracked Production task (cutting, trimming, blending,

i di i k h t )grinding, massaging, smokehouse , etc) Packaging tasks Shipping tasks

2010 15 © by CSB-System AG, Kestenholz, 2010

What can be included in OverheadWhat can be included in Overhead

Depreciation Maintenance Plant Management Energy Water Office Executive’s salaries Storage (freezer, off-site, etc)

2010 16 © by CSB-System AG, Kestenholz, 2010

Calculation of Net/Net Selling PriceFOB PriceFOB Price

Freight/Delivery Rebates and trade promotions Sales & Admin. Warehouse Allowance Brokers/Agents Commissions Commissions

These costs are normally allocated based on the customer receiving the product

2010 17 © by CSB-System AG, Kestenholz, 2010

customer receiving the product

Processes that effect Raw Material CostsCosts

Production process losses (yields) Cooler Shrink Ability to Bear (Market Value Allocation) By-Productsy Substitutions Fresh or FrozenFresh or Frozen Quality

2010 18 © by CSB-System AG, Kestenholz, 2010

Ability to Bear (Market Value Allocation)(Market Value Allocation)

Front

Back

2010 19 © by CSB-System AG, Kestenholz, 2010

Excel Ability to Bear Examples

2010 20 © by CSB-System AG, Kestenholz, 2010

Weiner Blend Process

Chop -Grind Blend

2010 21 © by CSB-System AG, Kestenholz, 2010Stuff Cook Package

Excel BOM Example 1

2010 22 © by CSB-System AG, Kestenholz, 2010

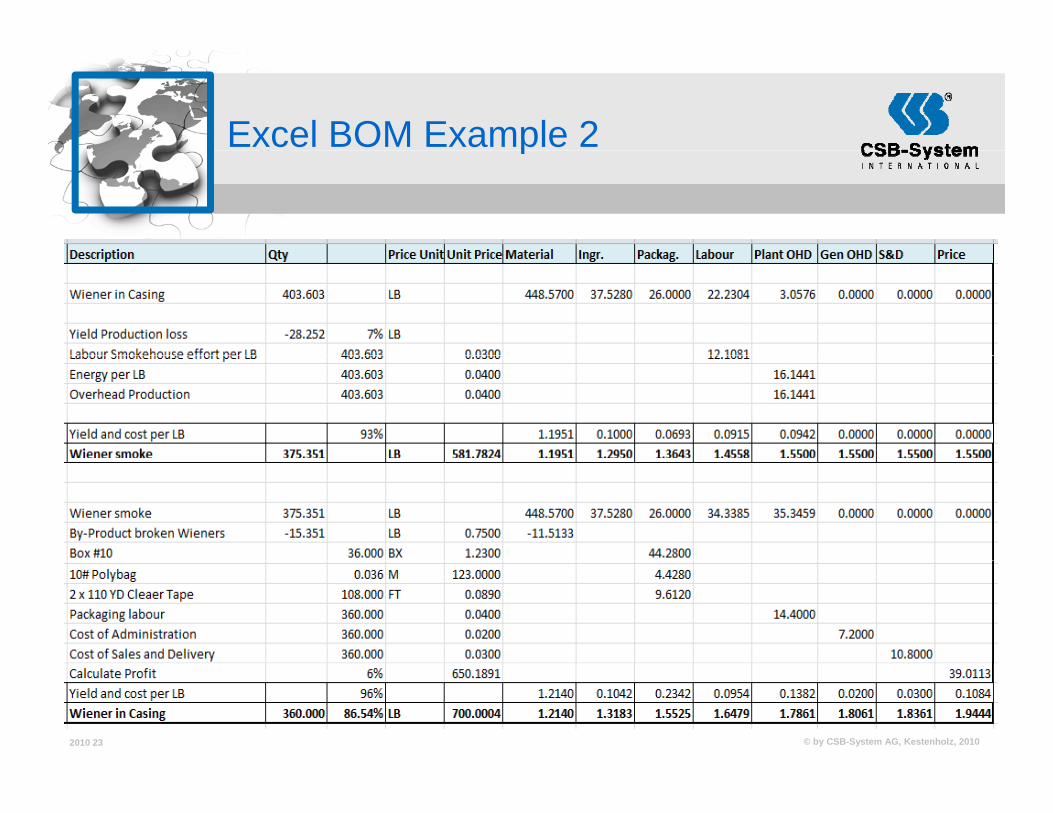

Excel BOM Example 2p

2010 23 © by CSB-System AG, Kestenholz, 2010

Excel versus IntegratedAccurate reliable DataAccurate reliable Data

D plicate entr Duplicate entry Prone to errors No or little validation Administration time consuming Limited flexibility to change Become out-dated very quickly Commodity costs change very quickly Calculation of multi methods of costing very difficult

2010 24 © by CSB-System AG, Kestenholz, 2010

g y Risk of next person not understanding the sheet

Modeling Business in an Integrated Solution

2010 25 © by CSB-System AG, Kestenholz, 2010

Summarize and Wrap-up

Manual vs. Software Application Level of detail Frequency of Updates Measure Variance Better manage costs, will protect the bottom line

(profit)

2010 26 © by CSB-System AG, Kestenholz, 2010

Contact Info

Terry McCorriston Director of Business Development CSB-System CSB System [email protected] (519) 579-7272 ext 203 www.csb.com

Q i ?Questions?

2010 27 © by CSB-System AG, Kestenholz, 2010