Embed Size (px)

Citation preview

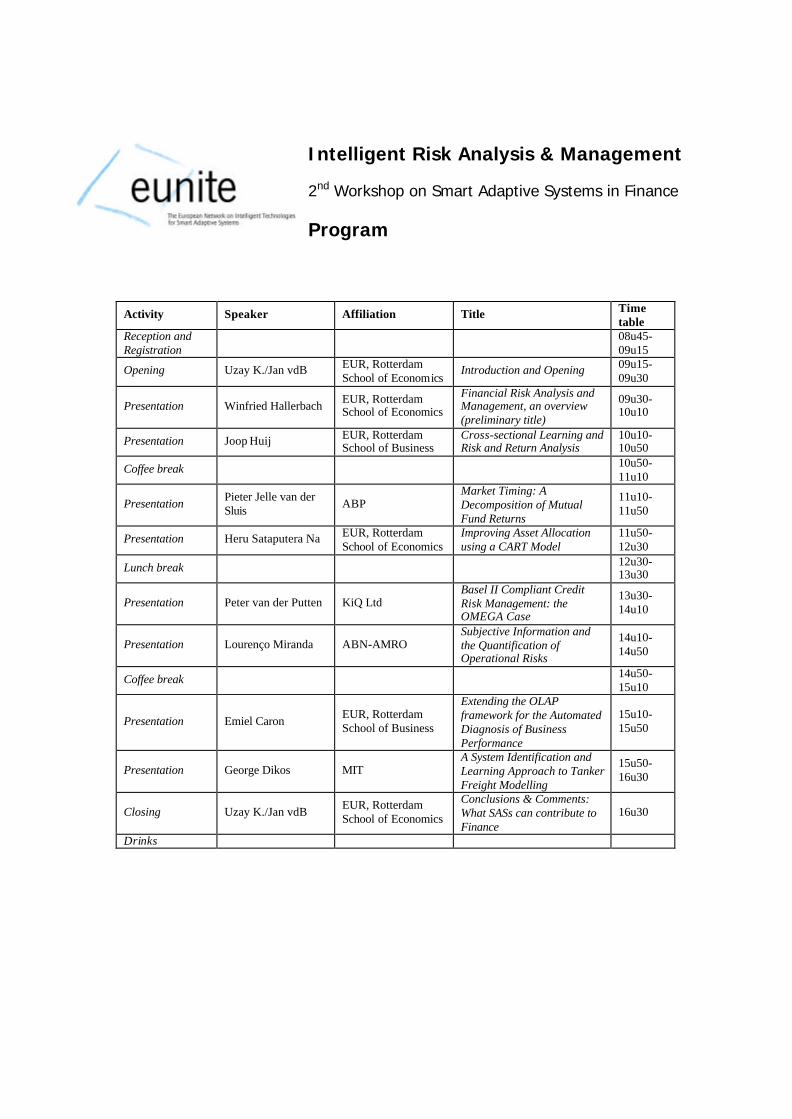

Proceedings of 2nd EUNITE Workshop on Smart Adaptive Systems in Finance

19 May 2004 Erasmus University Rotterdam, The Netherlands

Table of Contents Workshop program Call for papers 2nd EUNITE Workshop on Smart Adaptive Systems in Finance EUNITE – The European Network of Excellence on Intelligent Technologies for Smart Adaptive

Systems Abstracts of contributions Introduction and opening

by J. van den Berg, Erasmus University Rotterdam, School of Economics Financial risk analysis & management: an overview

by W. Hallerbach, Erasmus University Rotterdam, School of Economics Cross-sectional learning and risk and return analysis

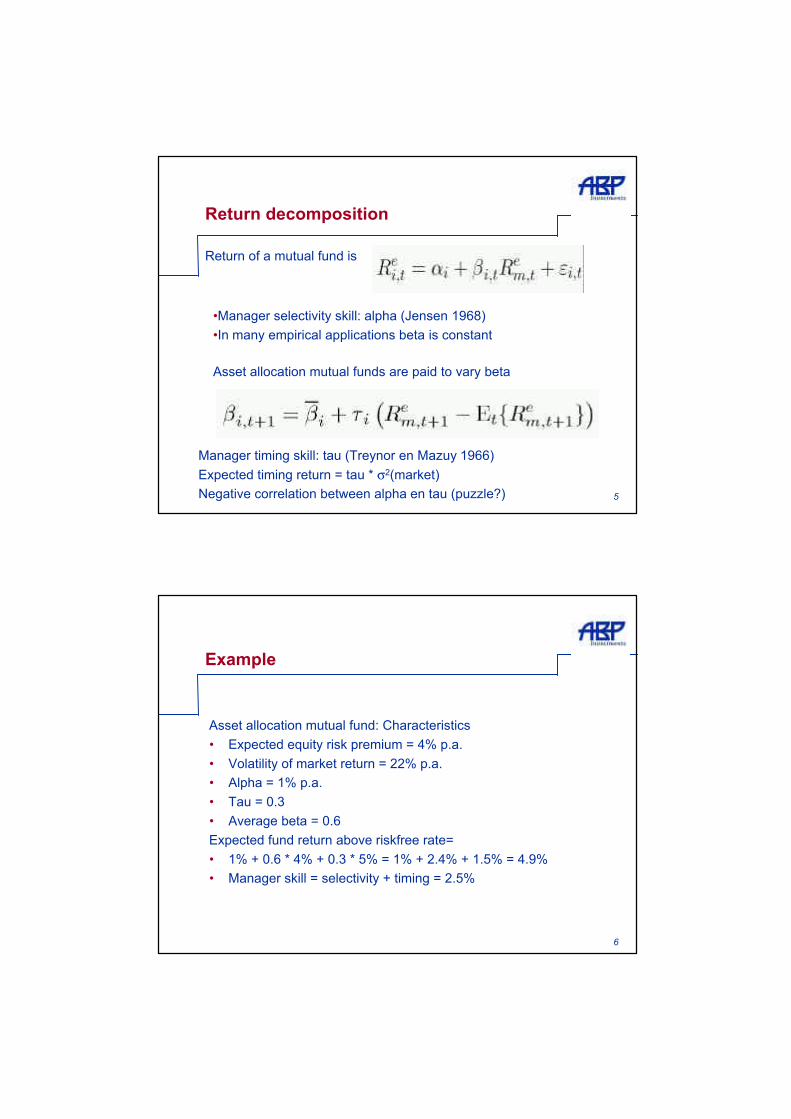

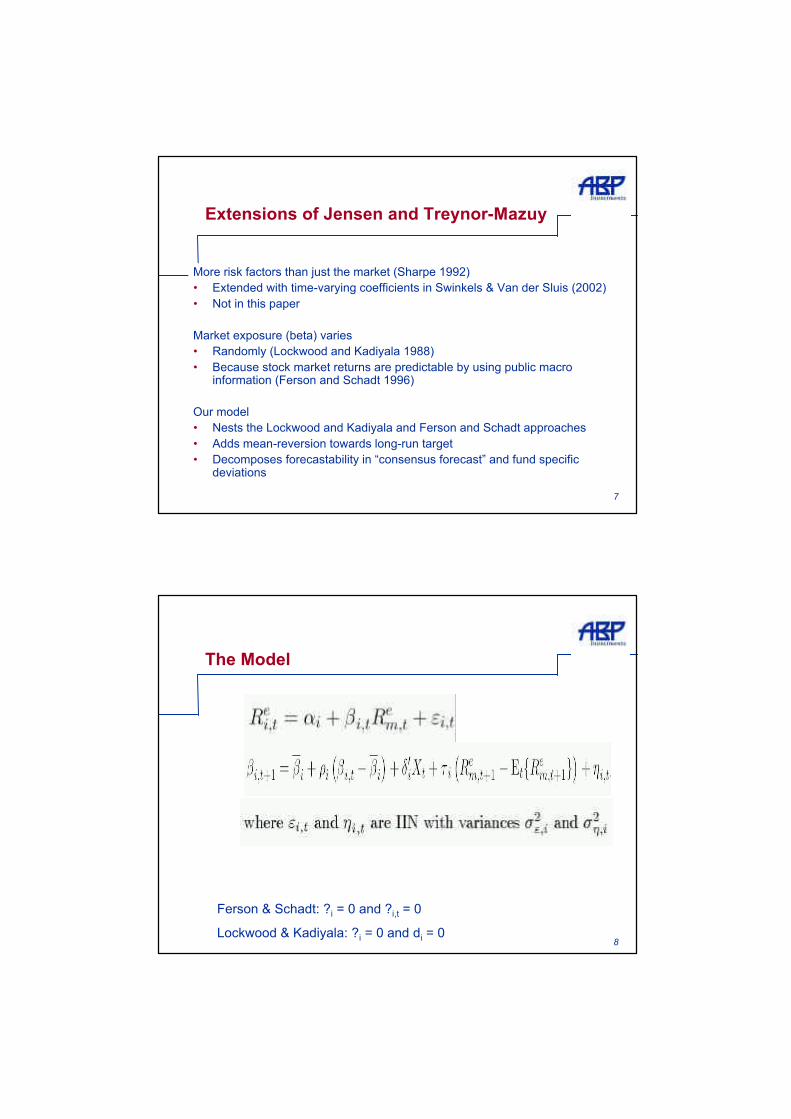

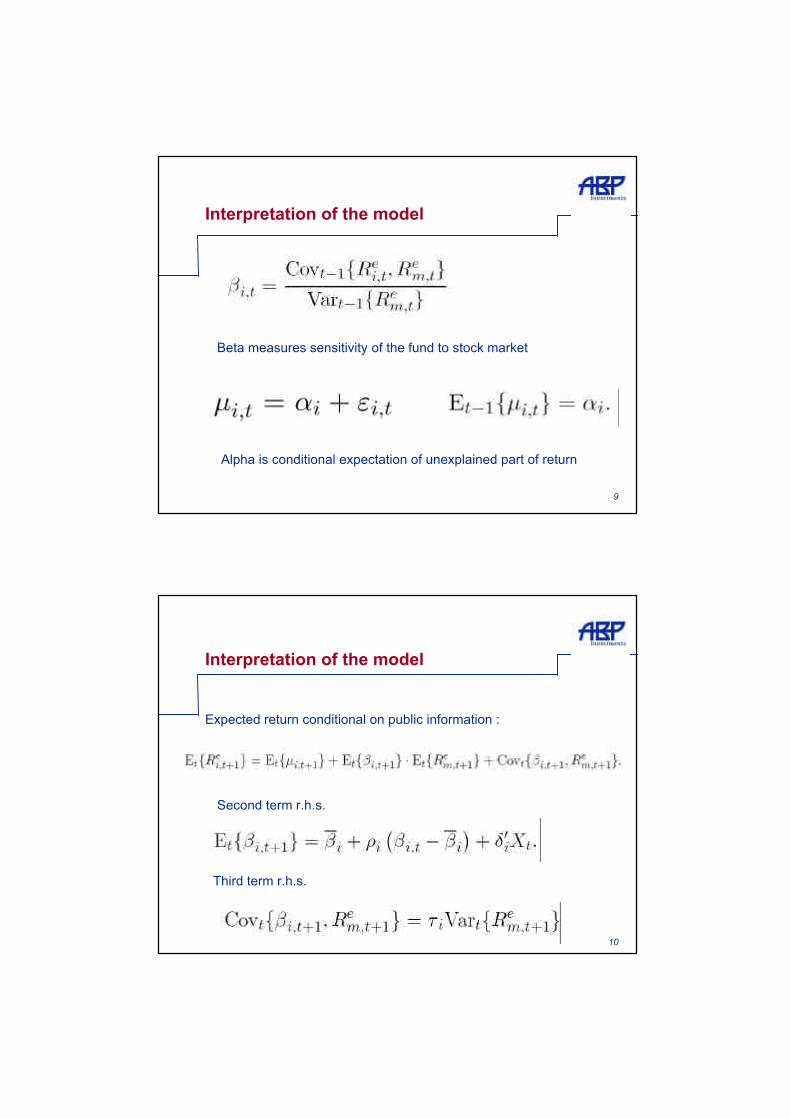

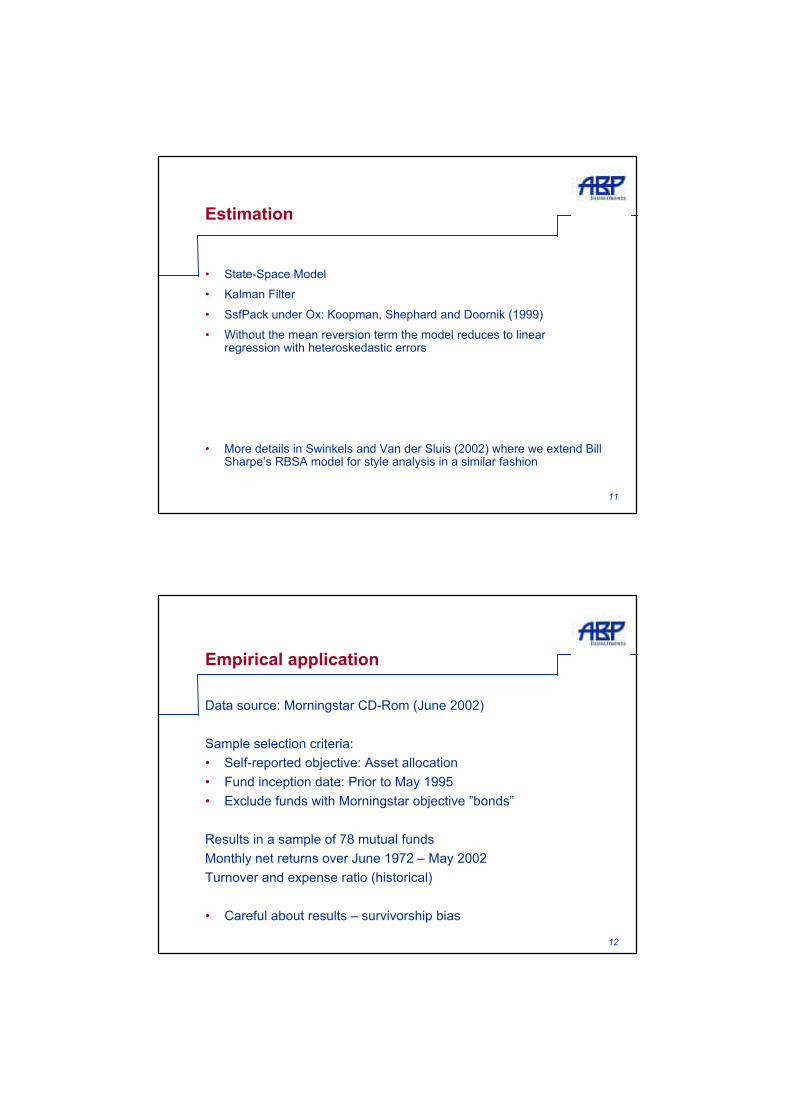

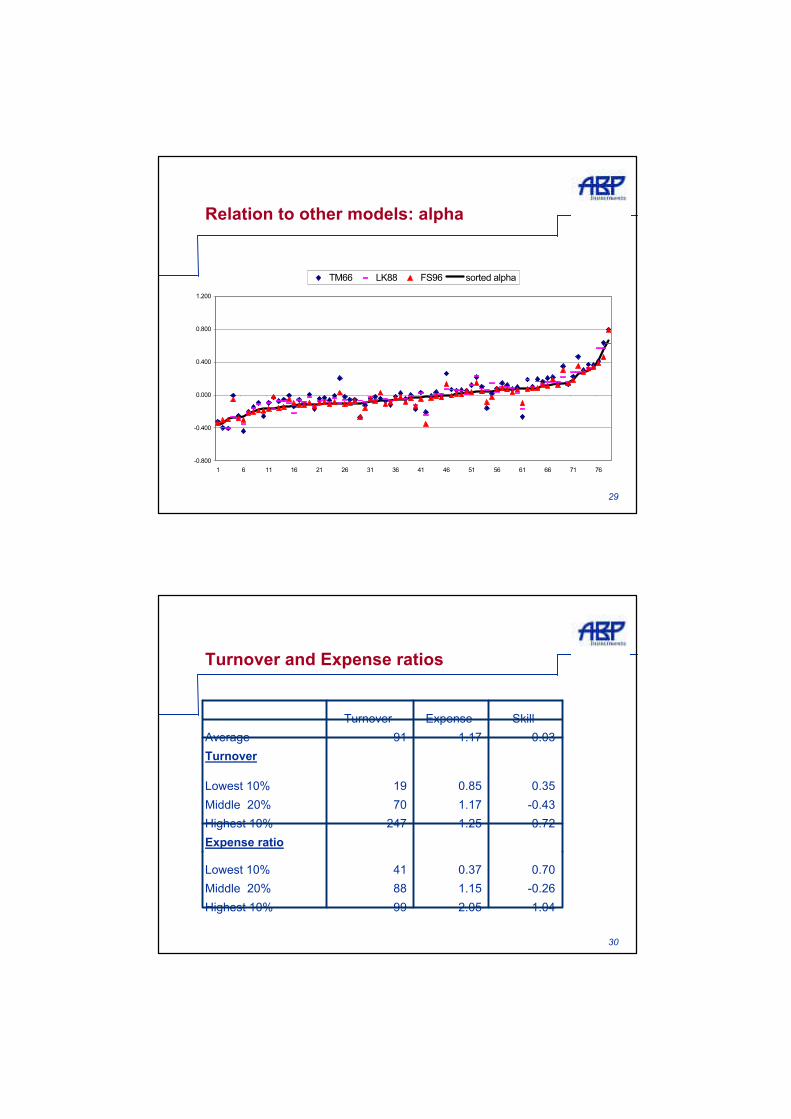

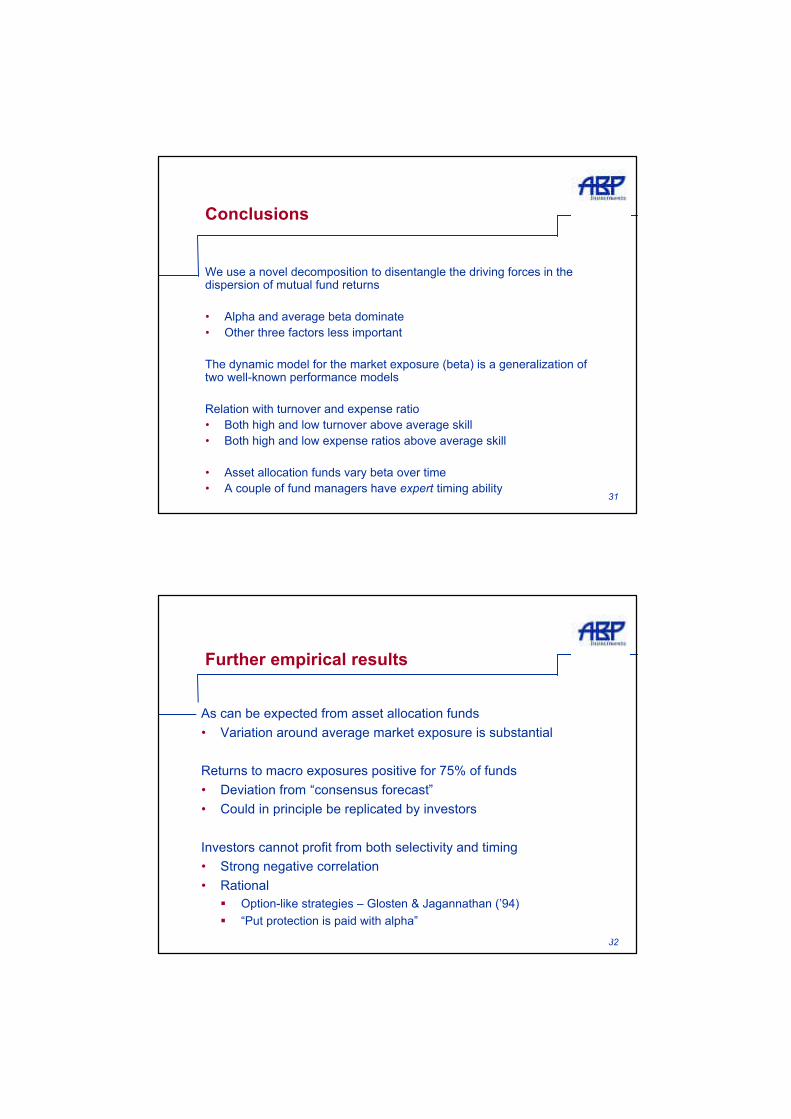

by J. Huij, Erasmus University Rotterdam, School of Business Market timing: a decomposition of mutual fund returns

by P. J. van der Sluis, ABP Improving asset allocation using a CART model

by H. S. Na, Erasmus University Rotterdam, School of Economics Basel II compliant credit risk management: the OMEGA case

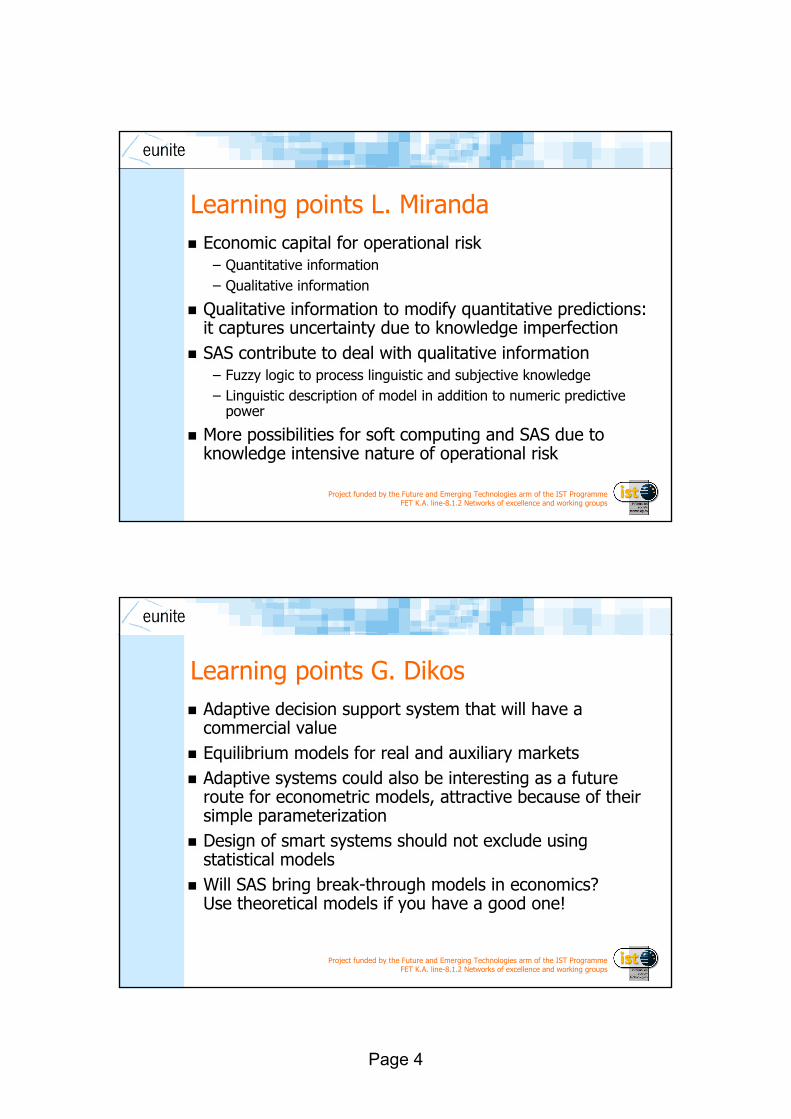

by P. van der Putten, KiQ Ltd. Subjective information and the quantification of operational risks

by L. Miranda, ABN-AMRO Bank A system identification and learning approach to tanker freight modeling

by G. Dikos, Massachusetts Institute of Technology Extending the OLAP framework for the automated diagnosis of business performance

by E. Caron, Erasmus University Rotterdam, School of Business Concluding remarks

by U. Kaymak, Erasmus University Rotterdam, School of Economics

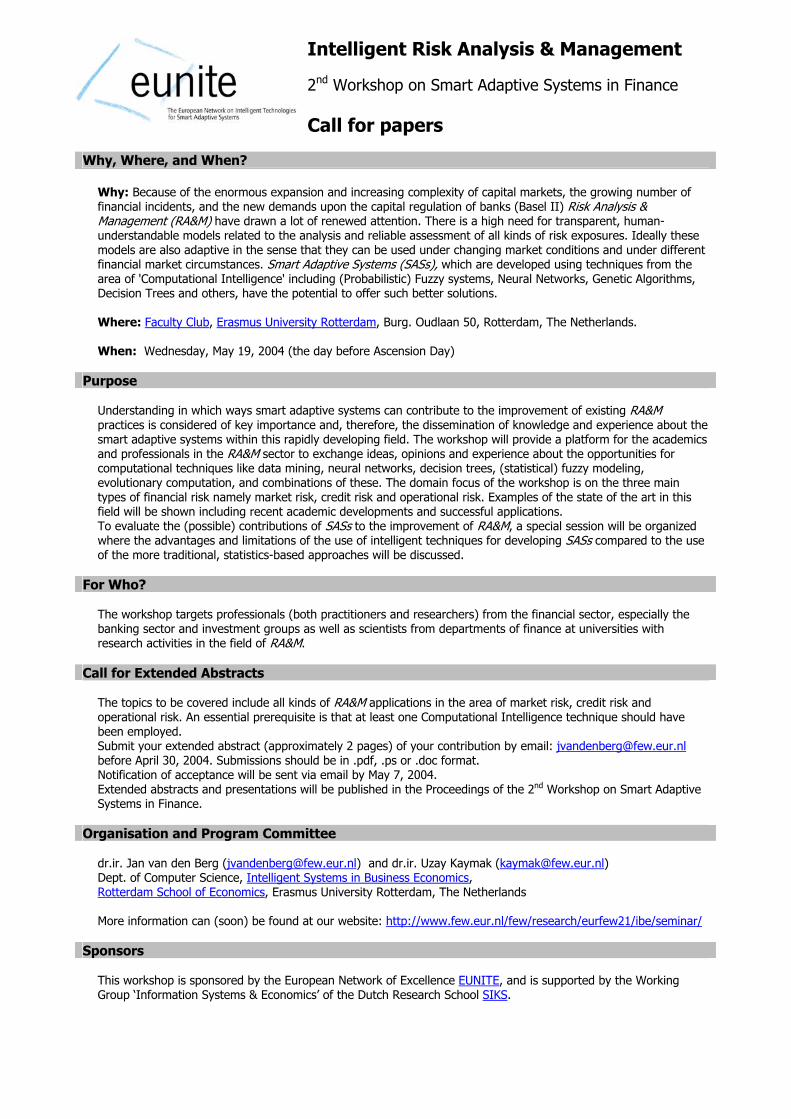

Intelligent Risk Analysis & Management 2nd Workshop on Smart Adaptive Systems in Finance Program

Activity Speaker Affiliation Title Time table

Reception and Registration

08u45- 09u15

Opening Uzay K./Jan vdB EUR, Rotterdam School of Economics

Introduction and Opening 09u15-09u30

Presentation Winfried Hallerbach EUR, Rotterdam School of Economics

Financial Risk Analysis and Management, an overview (preliminary title)

09u30- 10u10

Presentation Joop Huij EUR, Rotterdam School of Business

Cross-sectional Learning and Risk and Return Analysis

10u10-10u50

Coffee break 10u50-11u10

Presentation Pieter Jelle van der Sluis ABP

Market Timing: A Decomposition of Mutual Fund Returns

11u10-11u50

Presentation Heru Sataputera Na EUR, Rotterdam School of Economics

Improving Asset Allocation using a CART Model

11u50-12u30

Lunch break 12u30- 13u30

Presentation Peter van der Putten KiQ Ltd Basel II Compliant Credit Risk Management: the OMEGA Case

13u30- 14u10

Presentation Lourenço Miranda ABN-AMRO Subjective Information and the Quantification of Operational Risks

14u10- 14u50

Coffee break 14u50- 15u10

Presentation Emiel Caron EUR, Rotterdam School of Business

Extending the OLAP framework for the Automated Diagnosis of Business Performance

15u10- 15u50

Presentation George Dikos MIT A System Identification and Learning Approach to Tanker Freight Modelling

15u50- 16u30

Closing Uzay K./Jan vdB EUR, Rotterdam School of Economics

Conclusions & Comments: What SASs can contribute to Finance

16u30

Drinks

Intelligent Risk Analysis & Management 2nd Workshop on Smart Adaptive Systems in Finance Call for papers

Why, Where, and When?

Why: Because of the enormous expansion and increasing complexity of capital markets, the growing number of financial incidents, and the new demands upon the capital regulation of banks (Basel II) Risk Analysis &Management (RA&M) have drawn a lot of renewed attention. There is a high need for transparent, human-understandable models related to the analysis and reliable assessment of all kinds of risk exposures. Ideally these models are also adaptive in the sense that they can be used under changing market conditions and under different financial market circumstances. Smart Adaptive Systems (SASs), which are developed using techniques from the area of 'Computational Intelligence' including (Probabilistic) Fuzzy systems, Neural Networks, Genetic Algorithms, Decision Trees and others, have the potential to offer such better solutions.

Where: Faculty Club, Erasmus University Rotterdam, Burg. Oudlaan 50, Rotterdam, The Netherlands. When: Wednesday, May 19, 2004 (the day before Ascension Day)

Purpose Understanding in which ways smart adaptive systems can contribute to the improvement of existing RA&M practices is considered of key importance and, therefore, the dissemination of knowledge and experience about the smart adaptive systems within this rapidly developing field. The workshop will provide a platform for the academics and professionals in the RA&M sector to exchange ideas, opinions and experience about the opportunities for computational techniques like data mining, neural networks, decision trees, (statistical) fuzzy modeling, evolutionary computation, and combinations of these. The domain focus of the workshop is on the three main types of financial risk namely market risk, credit risk and operational risk. Examples of the state of the art in this field will be shown including recent academic developments and successful applications. To evaluate the (possible) contributions of SASs to the improvement of RA&M, a special session will be organized where the advantages and limitations of the use of intelligent techniques for developing SASs compared to the use of the more traditional, statistics-based approaches will be discussed.

For Who? The workshop targets professionals (both practitioners and researchers) from the financial sector, especially the banking sector and investment groups as well as scientists from departments of finance at universities with research activities in the field of RA&M.

Call for Extended Abstracts The topics to be covered include all kinds of RA&M applications in the area of market risk, credit risk and operational risk. An essential prerequisite is that at least one Computational Intelligence technique should have been employed. Submit your extended abstract (approximately 2 pages) of your contribution by email: [email protected] before April 30, 2004. Submissions should be in .pdf, .ps or .doc format. Notification of acceptance will be sent via email by May 7, 2004. Extended abstracts and presentations will be published in the Proceedings of the 2nd Workshop on Smart Adaptive Systems in Finance.

Organisation and Program Committee dr.ir. Jan van den Berg ([email protected]) and dr.ir. Uzay Kaymak ([email protected]) Dept. of Computer Science, Intelligent Systems in Business Economics, Rotterdam School of Economics, Erasmus University Rotterdam, The Netherlands More information can (soon) be found at our website: http://www.few.eur.nl/few/research/eurfew21/ibe/seminar/

Sponsors This workshop is sponsored by the European Network of Excellence EUNITE, and is supported by the Working Group ‘Information Systems & Economics’ of the Dutch Research School SIKS.

Page 1

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

the European Network of Excellence on Intelligent Technologies for

Smart Adaptive Systems

the European Network of Excellence on Intelligent Technologies for

Smart Adaptive Systems

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

IntroductionOn 1 January 2001, EUNITE - the European Network ofExcellence on Intelligent Technologies for Smart AdaptiveSystems - has started.

It is funded by the Future and Emerging Technologies arm of the IST Programme FET K.A. line-8.1.2 Networks of excellence and working groups

On 1 January 2001, EUNITE - the European Network ofExcellence on Intelligent Technologies for Smart AdaptiveSystems - has started.

It is funded by the Future and Emerging Technologies arm of the IST Programme FET K.A. line-8.1.2 Networks of excellence and working groups

Page 2

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Aimsto join forces within the area of Intelligent Technologies(i.e. neural networks, fuzzy systems, methods from machine learning, and evolutionary computing) for better understanding of the potential of hybrid systems and to provide guidelines for exploiting their practical implementationsand particularly,to foster synergies that contribute towards building SmartAdaptive Systems implemented in industry as well as in other sectors of the economy.

to join forces within the area of Intelligent Technologies(i.e. neural networks, fuzzy systems, methods from machine learning, and evolutionary computing) for better understanding of the potential of hybrid systems and to provide guidelines for exploiting their practical implementationsand particularly,to foster synergies that contribute towards building SmartAdaptive Systems implemented in industry as well as in other sectors of the economy.

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Integration of Intelligent TechnologiesIntelligent Hybrid Systems: Combinations of Intelligent Technologies (e.g. neuro-fuzzy, evolutionary optimised networks, etc.)

– common in theory and experimentation and less in the applicationfield

• need for guidelines regarding design, testing and assessment • need for improved understanding of the fundamental nature of

engineering systems with embedded hybrid intelligence.

Can they contribute and improve adaptivity?

Intelligent Hybrid Systems: Combinations of Intelligent Technologies (e.g. neuro-fuzzy, evolutionary optimised networks, etc.)

– common in theory and experimentation and less in the applicationfield

• need for guidelines regarding design, testing and assessment • need for improved understanding of the fundamental nature of

engineering systems with embedded hybrid intelligence.

Can they contribute and improve adaptivity?

Page 3

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Smart Adaptive SystemsAdaptivity:

A system is adaptive if it can adequately perform even in non-stationary environments, where significant smooth changes of themain data characteristics can be manifested.

Examples:monitoring systems in the presence of tool wearmedical diagnostic systems in the presence of a changing populationforecasting of dynamically changing time series

Adaptivity is also a request in the sense of portability and reusability as minimises the effort for re-development..

Example:monitoring or diagnostic systems that should run on different machines which are of similar type but each have their individual characteristics.

Adaptivity:A system is adaptive if it can adequately perform even in non-stationary environments, where significant smooth changes of themain data characteristics can be manifested.

Examples:monitoring systems in the presence of tool wearmedical diagnostic systems in the presence of a changing populationforecasting of dynamically changing time series

Adaptivity is also a request in the sense of portability and reusability as minimises the effort for re-development..

Example:monitoring or diagnostic systems that should run on different machines which are of similar type but each have their individual characteristics.

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Activities• Roadmap • Organise Conferences-Symposia-Workshops• Disseminate Feasibility and Joint case studies on

hybrid and Smart Adaptive Systems• Provide best practice guidelines - best Methodology• Learning Center• Patent support - IPR service• Benchmarking-Competitions • Scientific e-archives, e-Dictionary • Newsletter• WWW site

• Roadmap • Organise Conferences-Symposia-Workshops• Disseminate Feasibility and Joint case studies on

hybrid and Smart Adaptive Systems• Provide best practice guidelines - best Methodology• Learning Center• Patent support - IPR service• Benchmarking-Competitions • Scientific e-archives, e-Dictionary • Newsletter• WWW site

Page 4

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

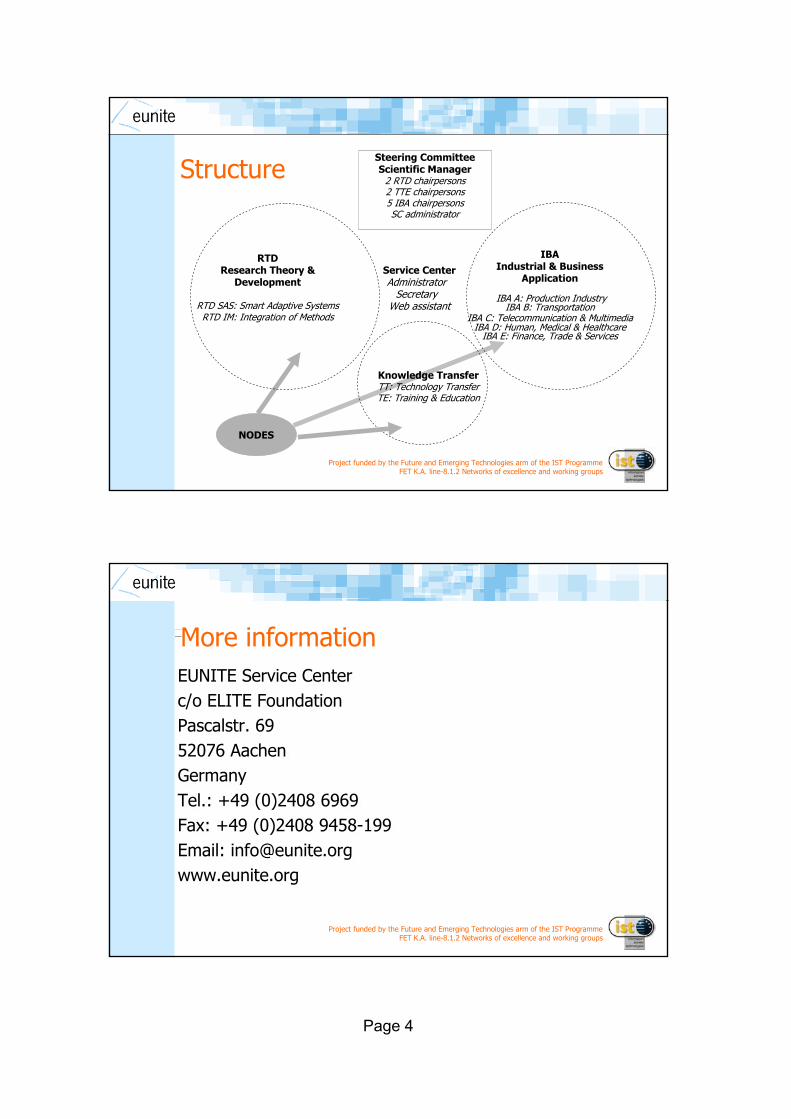

Steering CommitteeScientific Manager

2 RTD chairpersons2 TTE chairpersons5 IBA chairpersonsSC administrator

IBAIndustrial & Business

Application

IBA A: Production IndustryIBA B: Transportation

IBA C: Telecommunication & MultimediaIBA D: Human, Medical & Healthcare

IBA E: Finance, Trade & Services

Service CenterAdministrator

SecretaryWeb assistant

NODES

RTDResearch Theory &

Development

RTD SAS: Smart Adaptive SystemsRTD IM: Integration of Methods

Knowledge Transfer TT: Technology TransferTE: Training & Education

Structure

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

More informationEUNITE Service Centerc/o ELITE FoundationPascalstr. 6952076 AachenGermanyTel.: +49 (0)2408 6969Fax: +49 (0)2408 9458-199Email: [email protected]

EUNITE Service Centerc/o ELITE FoundationPascalstr. 6952076 AachenGermanyTel.: +49 (0)2408 6969Fax: +49 (0)2408 9458-199Email: [email protected]

ABSTRACTS OF CONTRIBUTIONS

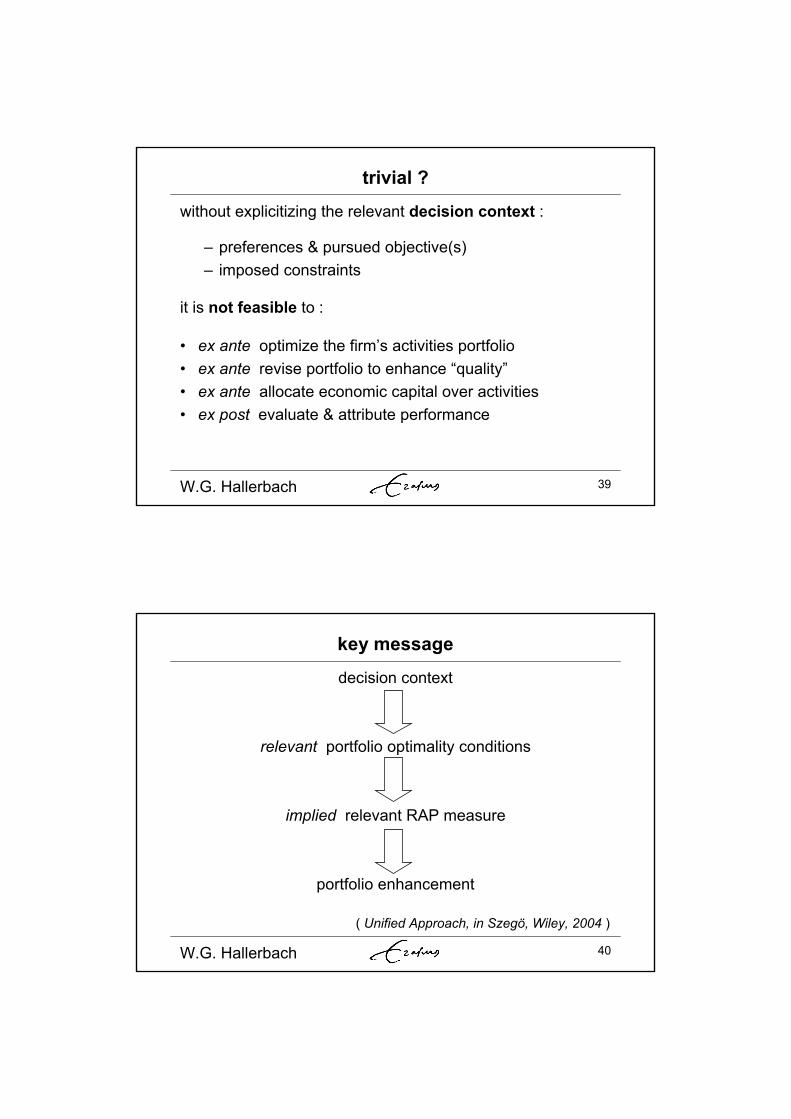

Financial Risk Analysis & Management: An Overview The globalization of business paired with rapid technological changes and increased volatility in the financial markets has changed the risk profiles of many companies dramatically. Firms have responded by embracing the concept of financial risk management. Mitigating or neutralizing excess risk exposures through hedging is widespread corporate practice nowadays. As a preamble to the various presentations today, we provide a concise overview of the various stages of the enterprise-wide risk management process, viz. risk analysis, policy formulation, implementation, and performance evaluation. We devote special attention to model risk, cognitive biases in decision making under uncertainty, and the link between the decision context and performance evaluation. ------------------------------------------------------------------------------------ Dr. Winfried G. Hallerbach Home: Hoflaan 93, NL-3062 JD Rotterdam, The Netherlands phone: +31 (10) 411-0899 Work: Dept of Finance, Erasmus University Rotterdam POB 1738, NL-3000 DR Rotterdam, The Netherlands phone: +31 (10) 408-1290 fax: +31 (10) 408-9165 e-mail: [email protected] http://www.few.eur.nl/few/people/hallerbach http://www.finance-on-eur.nl

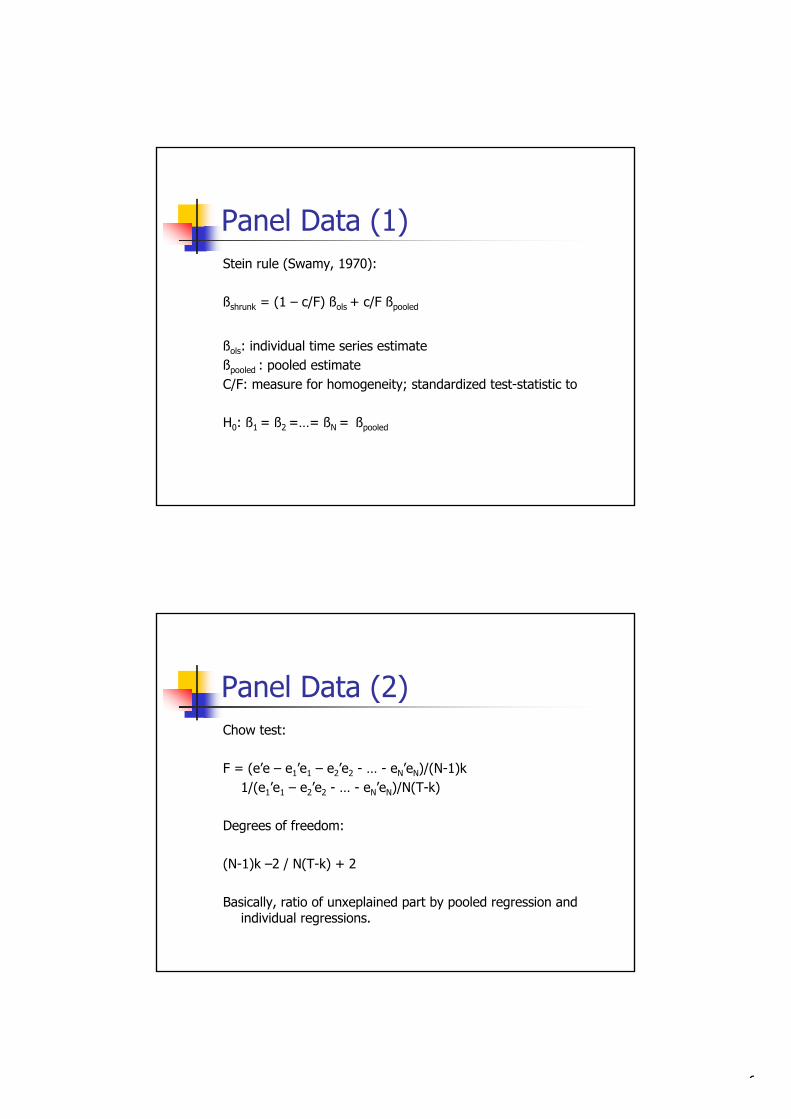

Cross-Sectional Learning and Risk and ReturnAnalysis

Joop Huij∗

May 6, 2004

Traditional estimates of risk and return measures are hampered by potentially

high levels of inaccuracy, particulary when only short horizons of monthly returns

are used. With only a small number of observations available, it is notoriously

difficult to separate skill from random luck. For example, investment funds that

are less well-diversified and have higher levels of non-systematic risk experience a

larger probability to end up with an extreme ranking because managers of these

funds typically place larger bets, i.e. run higher risks. Consequently, top and

bottom deciles in performance rankings will to a large extent be attributable to

random luck rather than managerial skill, and are therefore not very useful for

analyzing market efficiency, or fund picking purposes.

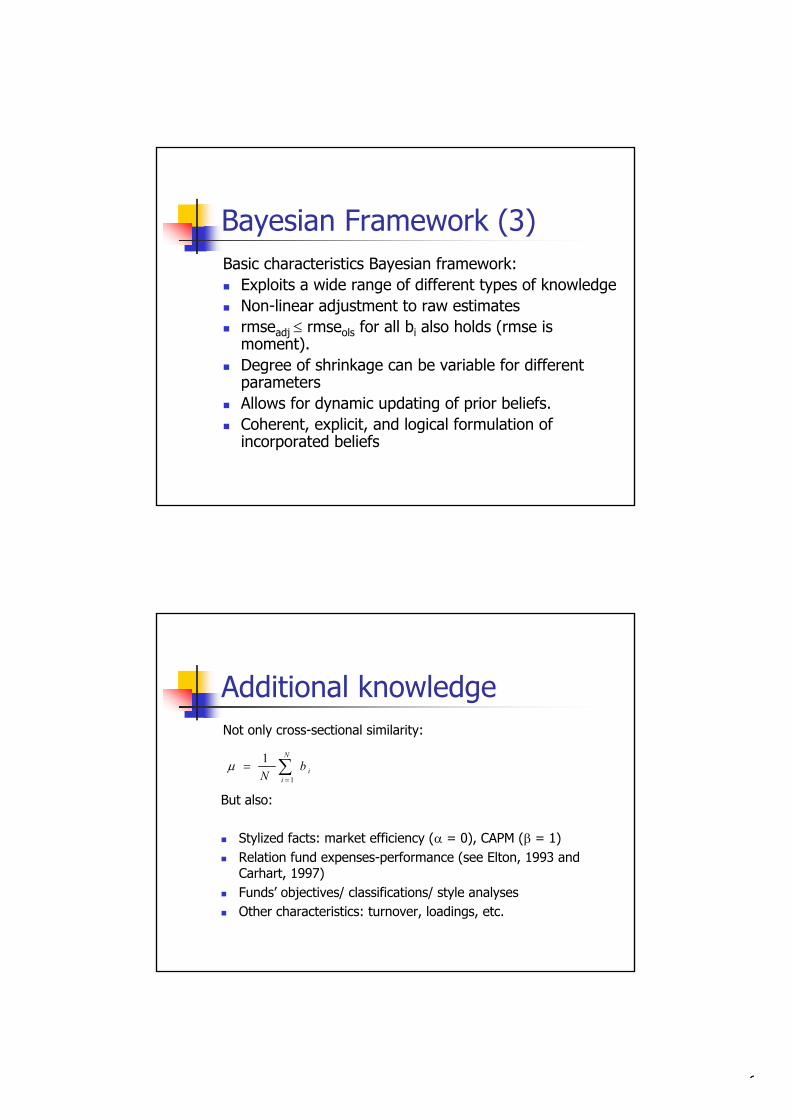

In this study, we evaluate several smart systems that not only base estimates

of risk and return measures on available returns histories, but also incorporate

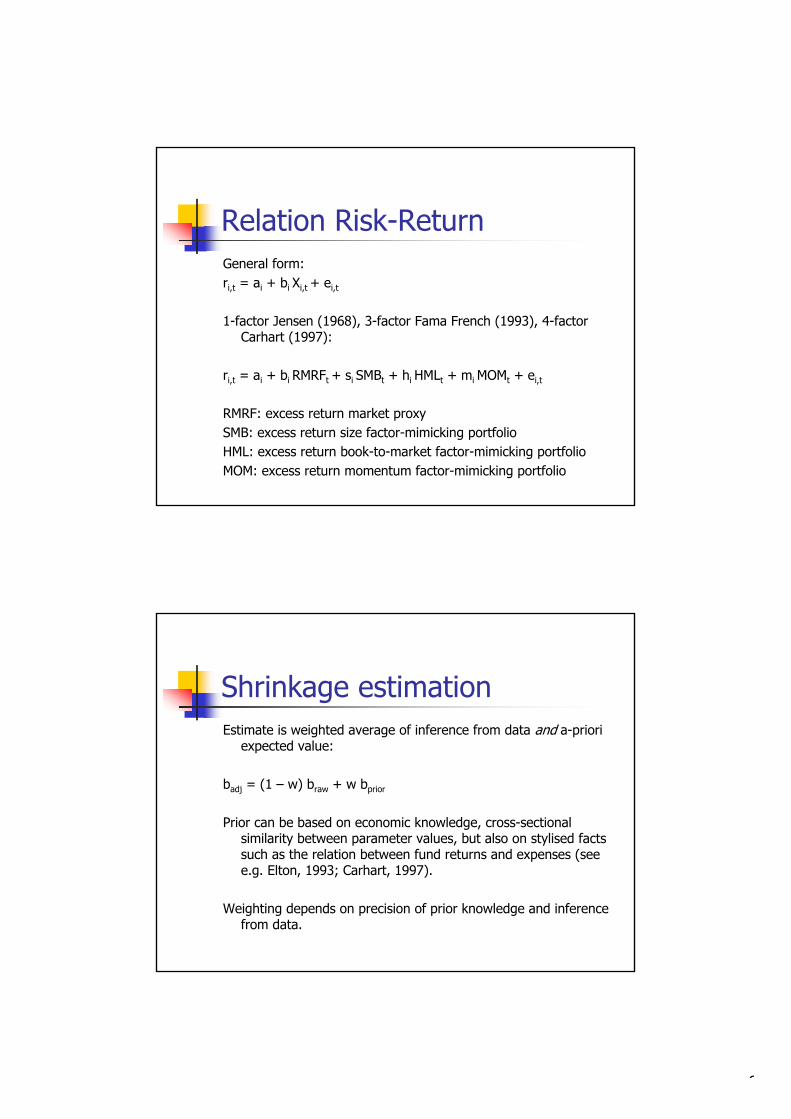

economic knowledge. For example, studies by among Elton et al. (1993) and

Carhart (1997) indicate that funds with higher fees typically underperform those

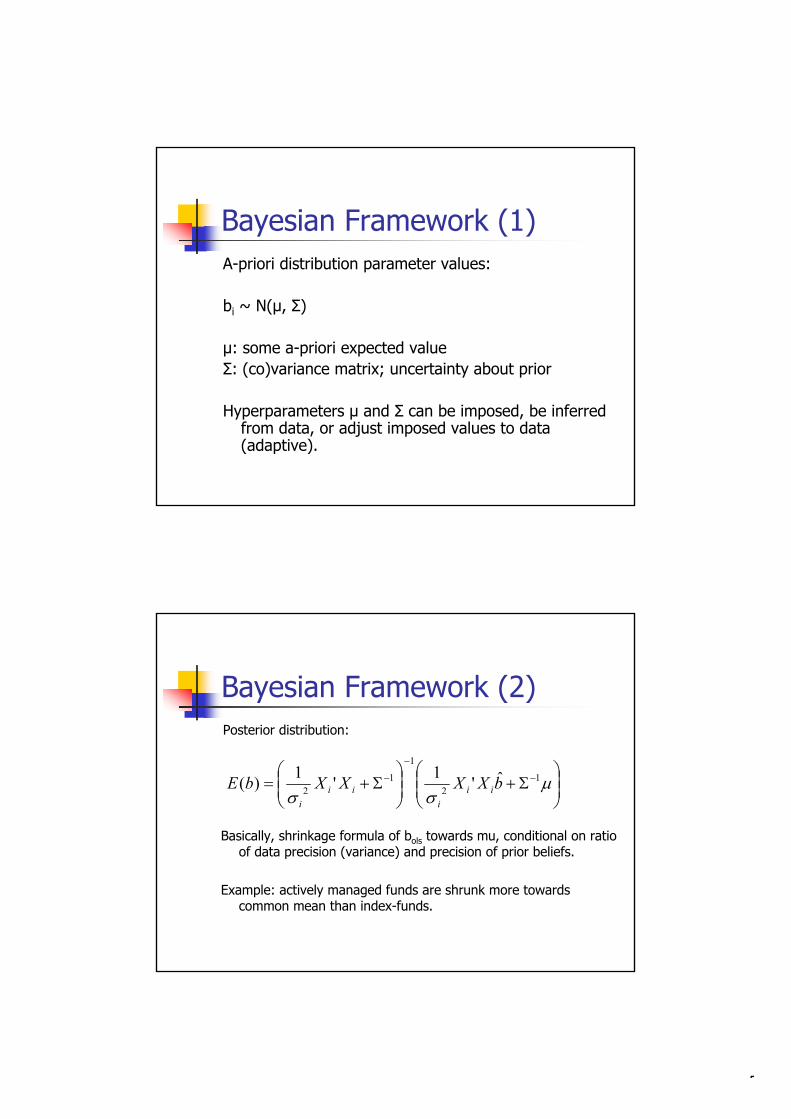

with lower fees. By means of a Bayesian framework, one could exploit prior infor-

mation related to expenses of funds, and investors’ beliefs about managerial skills

(see Baks et al. (2001), Pastor and Stambaugh (2002a,b)). In this framework,

raw performance estimates are shrunk towards the funds’ expenses conditional on

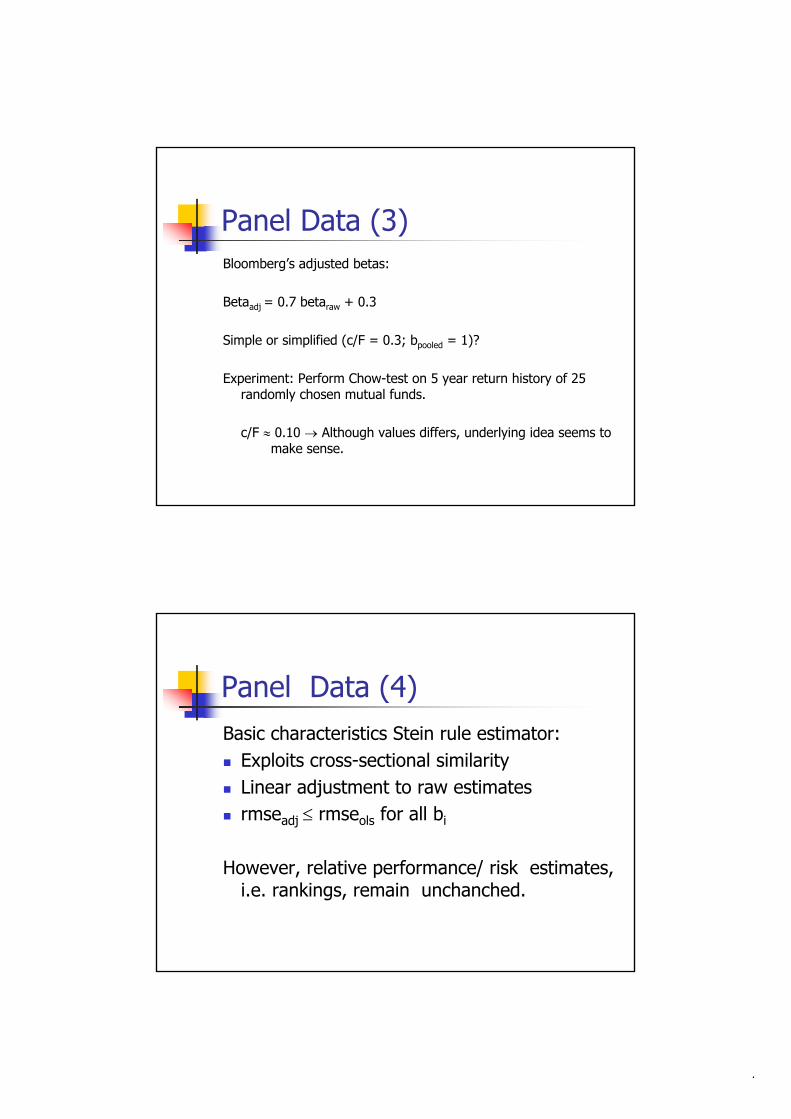

how strongly one beliefs in managerial skill. Another example are adjusted beta

estimates that are provided by commercial information services like Bloomberg.

Hereby, one exploits the knowledge that (by construction) the expected average

∗Dept. of Financial Management, Erasmus University Rotterdam, The Netherlands,[email protected].

value of betas of a cross-section of stocks is equal to one. Raw beta estimates are

then adjusted in the sense that they are shrunk towards this value of one. More

generally, the use of Bayesian shrinkage techniques can be motivated purely on

the basis of statistical arguments: When a cross-section of risk and return esti-

mates is considered, extreme values are more than average subject to positive and

negative estimation errors, respectively, and shrinking them towards an expected

value may result in more accurate inferences.

The setup of the study is as follows: First, we formulate the most general

form of the Bayesian system, and provide several applications of this framework,

e.g. CAPM, and Fama-French model (Fama and French, 1992, 1993). We then

review current literature on additional information that is incorporated in the

estimation procedure, and discuss the relative strengths and weaknesses of these

implementations. Furthermore, we extend our model so that prior beliefs become

adaptive in the sense that they can shift over time, and adjust to market dynam-

ics and structural shifts. Second, we consider a range of alternative approaches

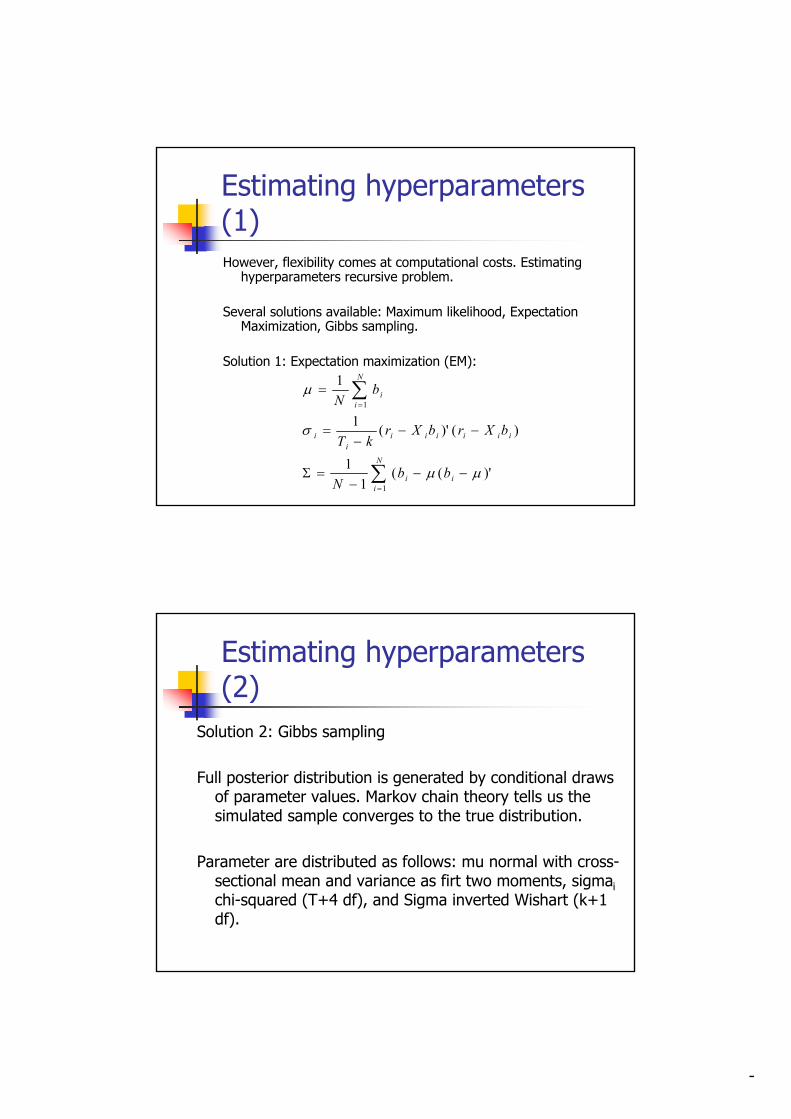

to estimate our model (hyper)parameters, including maximum likelihood, (iter-

ative) empirical Bayes, expectation maximization, and Gibbs sampling. Third,

we evaluate accuracy and ranking ability of traditional and Bayesian estimators

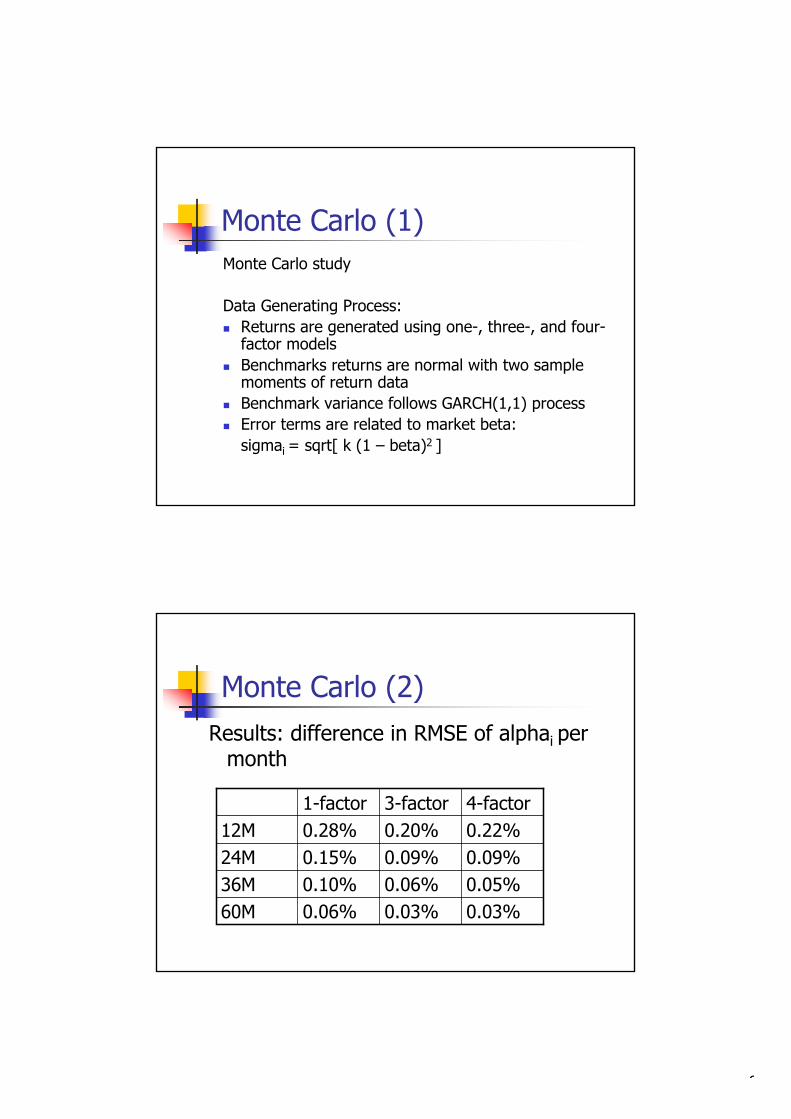

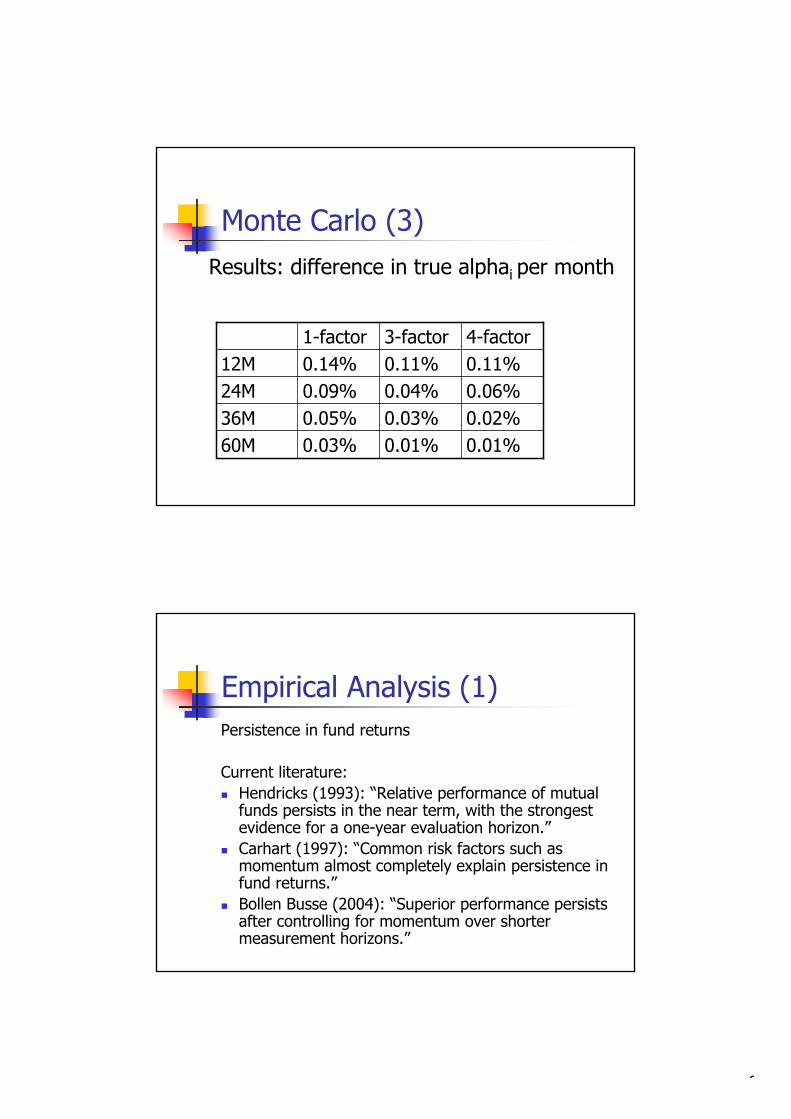

under controlled circumstances, by means of a Monte Carlo simulation. Our re-

sults demonstrate that the gains in accuracy and ranking abilities are substantial

and robust over different model specifications and measurement horizons. For ex-

ample, Bayesian alphas appear to be about 50 percent more accurate in term of

root mean squared error when evaluating a 12-month time period. Also, rankings

based on these estimates are significantly better; not only in statistical terms such

as correlation with true rankings, but also from an economic perspective in the

sense that the funds that are rated as top-performers have substantially higher

true alphas and Sharpe ratios. Finally, we apply Bayesian alphas to investigate

short-run predictability in fund returns for a large sample of US equity funds.

References

K. Baks, A. Metrick, and J. Wachter. Should investors avoid all actively managed

mutual funds? a study in bayesian performance evaluation. The Journal of

2

Finance, 56:45–85, 2001.

M. Carhart. On persistence in mutual fund performance. The Journal of Finance,

52:57–82, 1997.

E. J. Elton, M. J. Gruber, S. Das, and M. Illavka. Efficiency with costly infor-

mation: A reinterpretation of evidence from managed portfolios. The Review

of Financial Studies, 6:1–22, 1993.

E. F. Fama and K. R. French. The cross-section of expected stock returns. The

Journal of Finance, 47:427–465, 1992.

E. F. Fama and K. R. French. Common risk factors in the returns on stocks and

bonds. Journal of Financial Economics, 33:3–56, 1993.

L. Pastor and R. Stambaugh. Mutual fund performance and seemingly unrelated

assets. Journal of Financial Economics, 63:315–349, 2002a.

L. Pastor and R. F. Stambaugh. Investing in equity mutual funds. Journal of

Financial Economics, 63:351–380, 2002b.

3

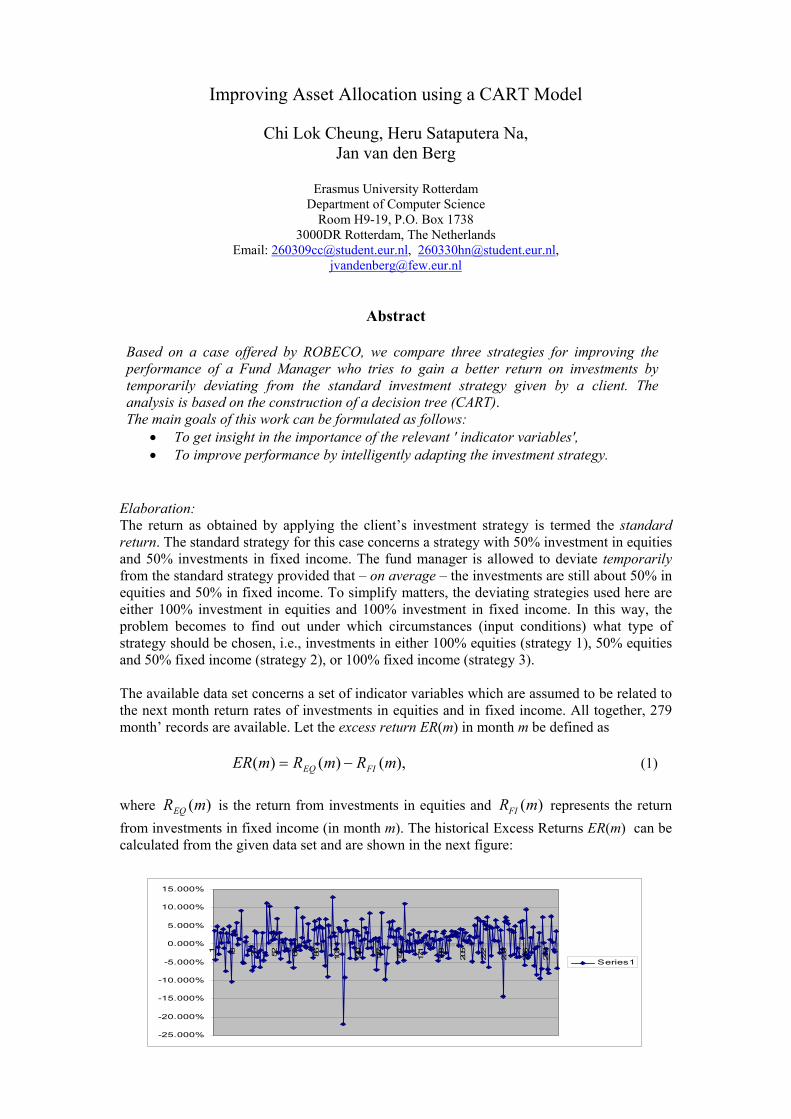

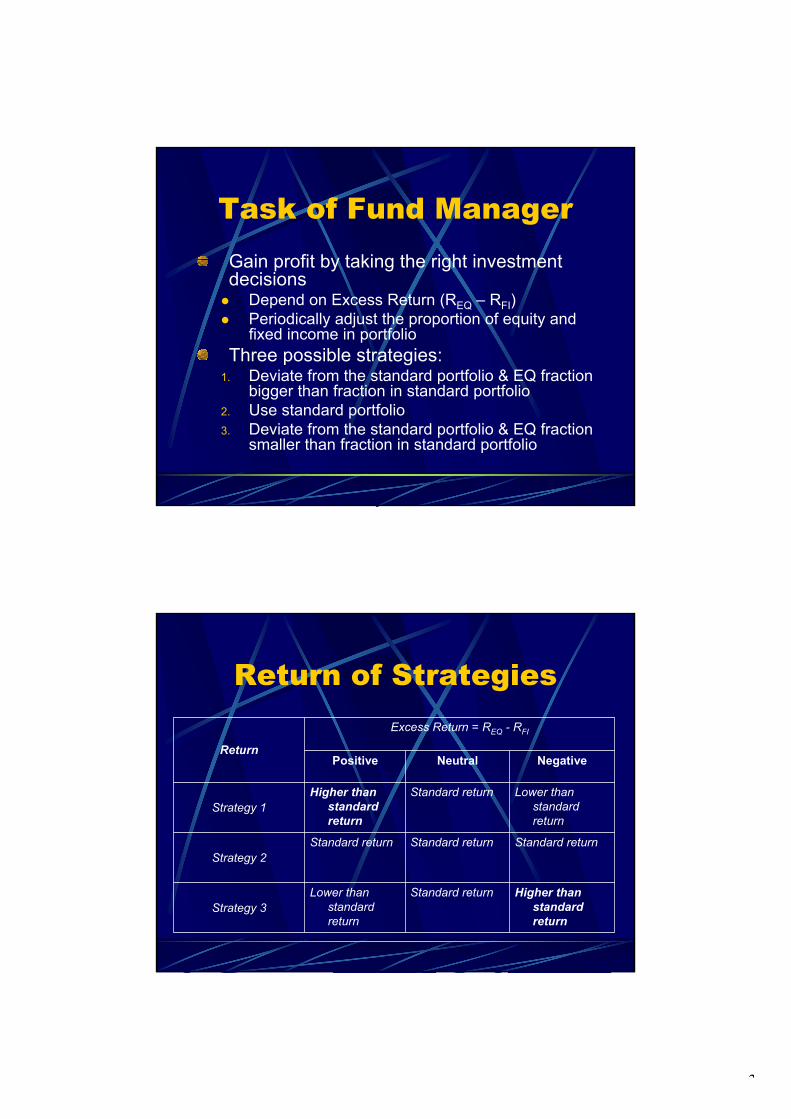

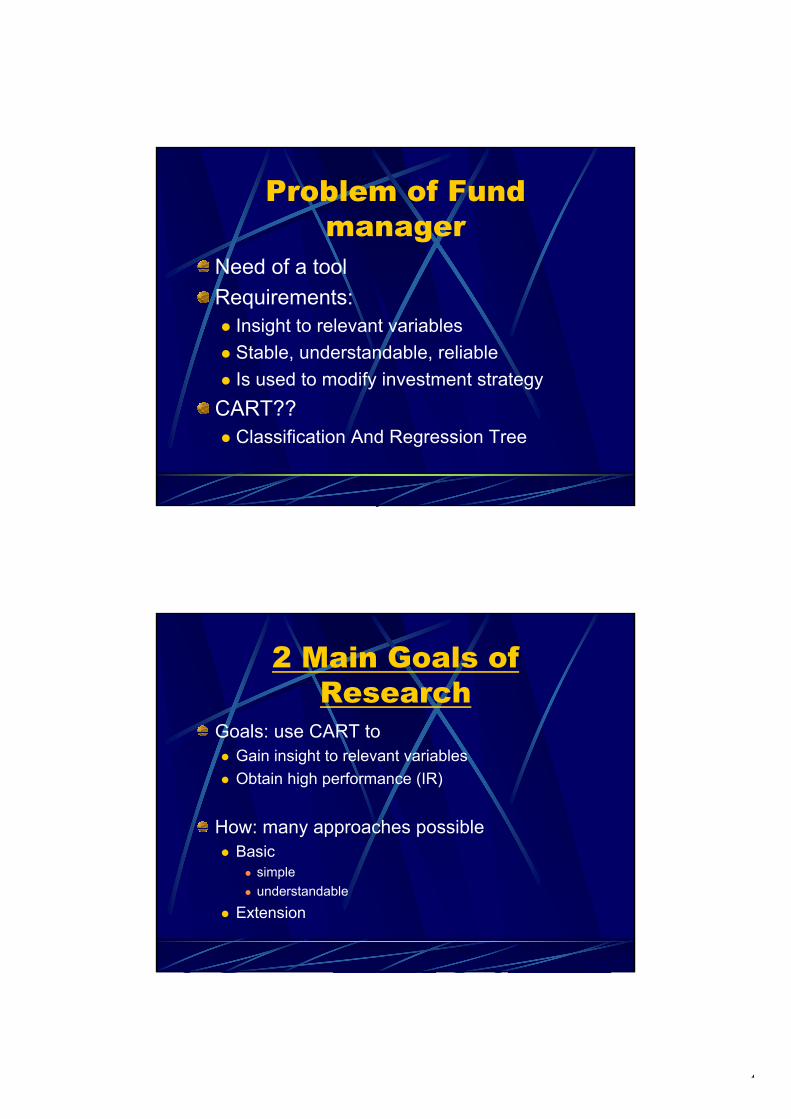

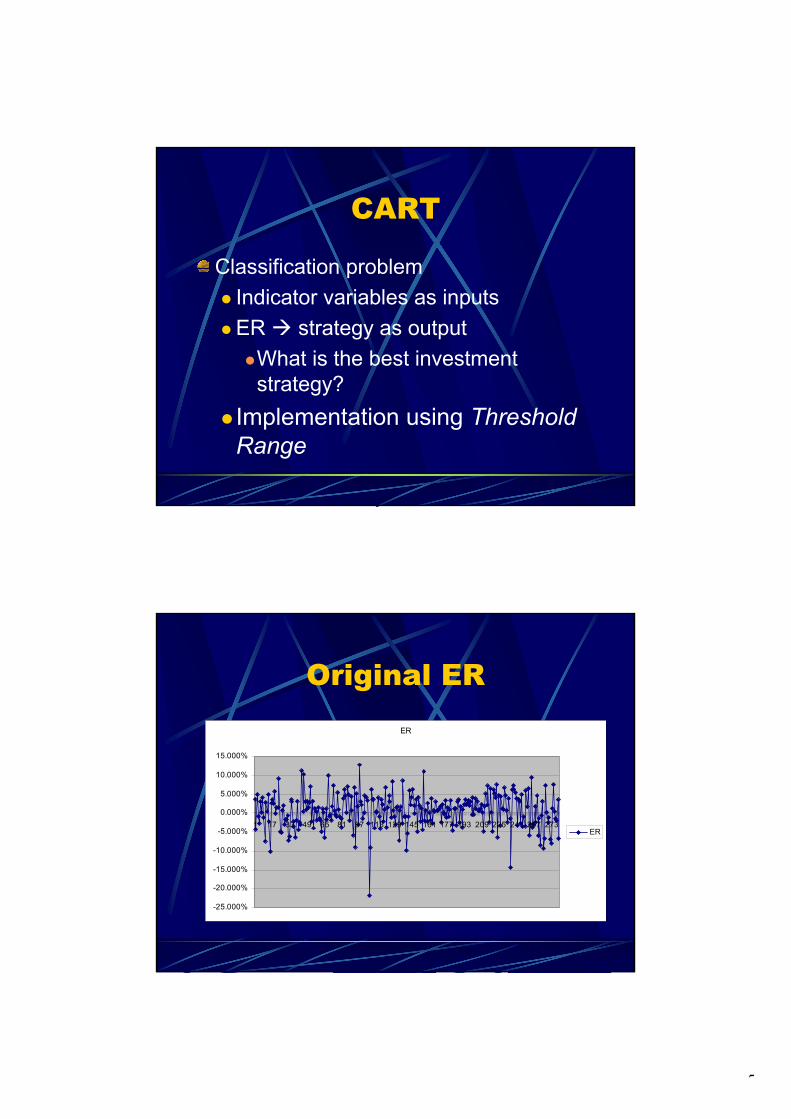

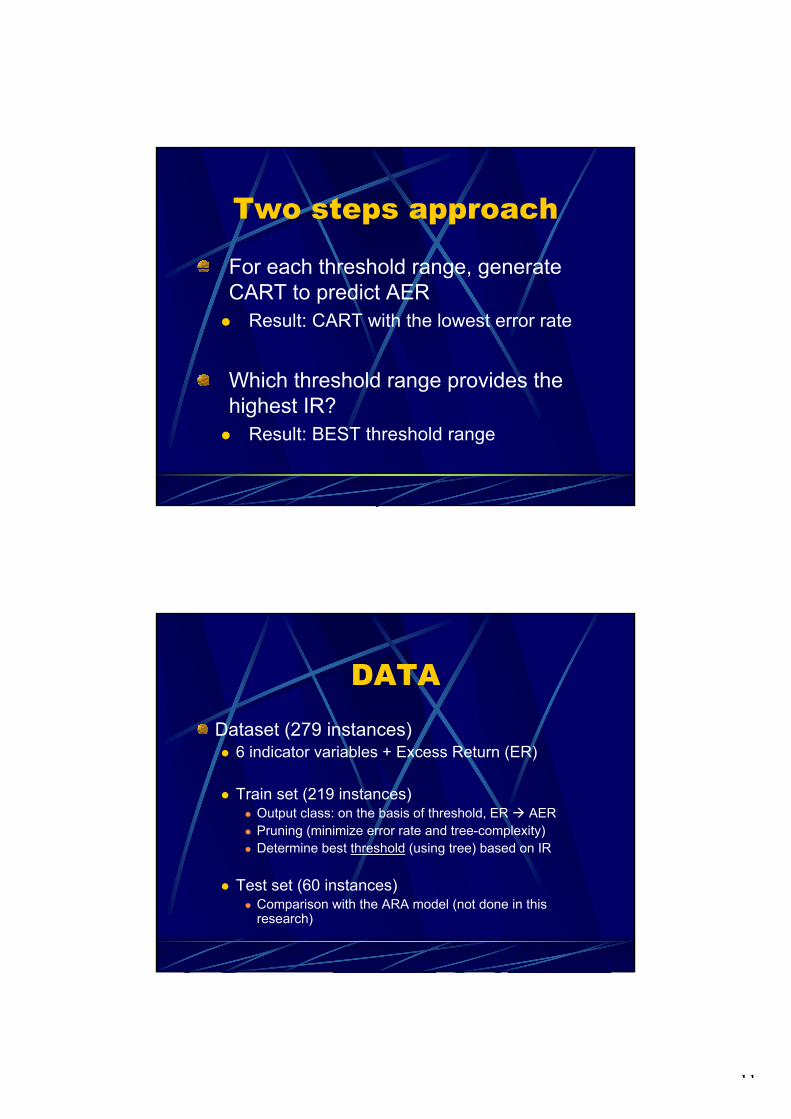

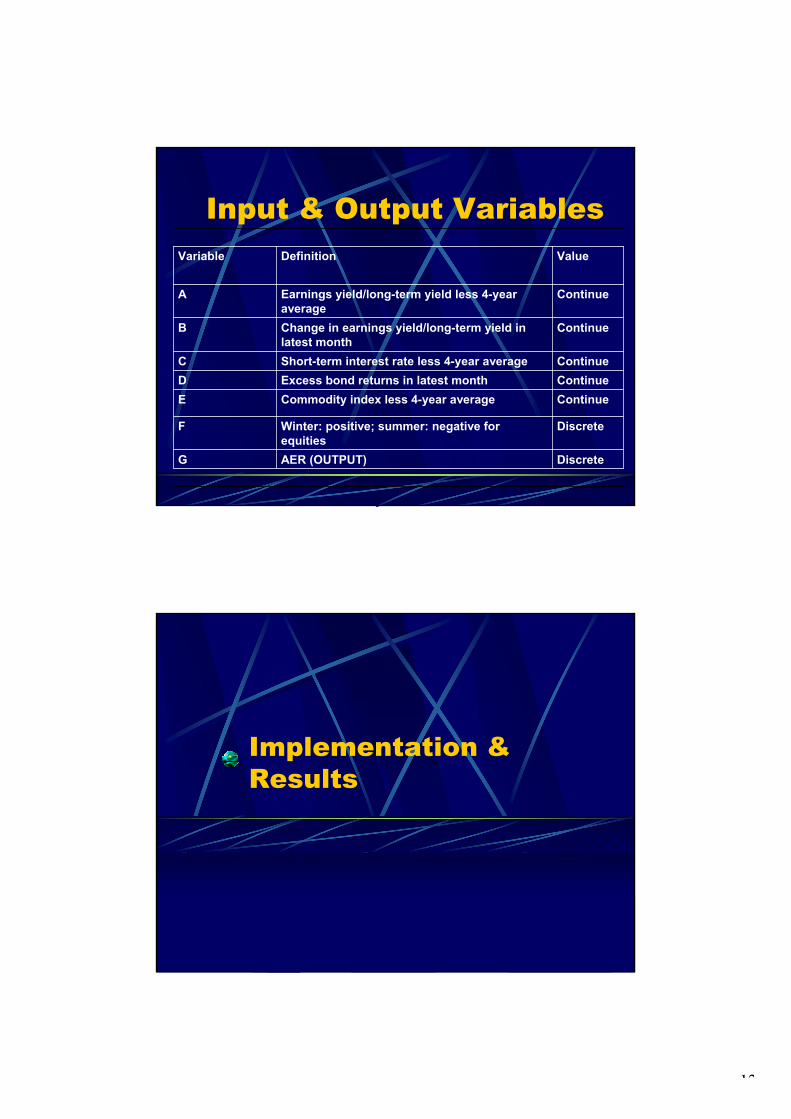

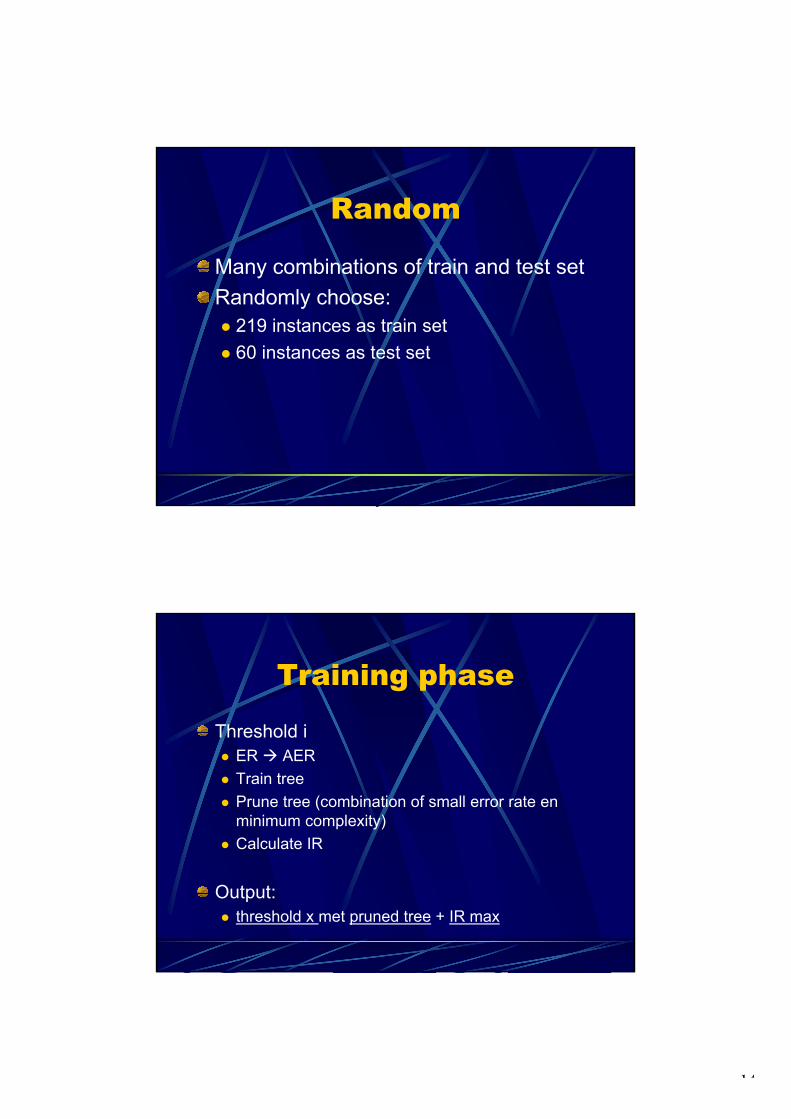

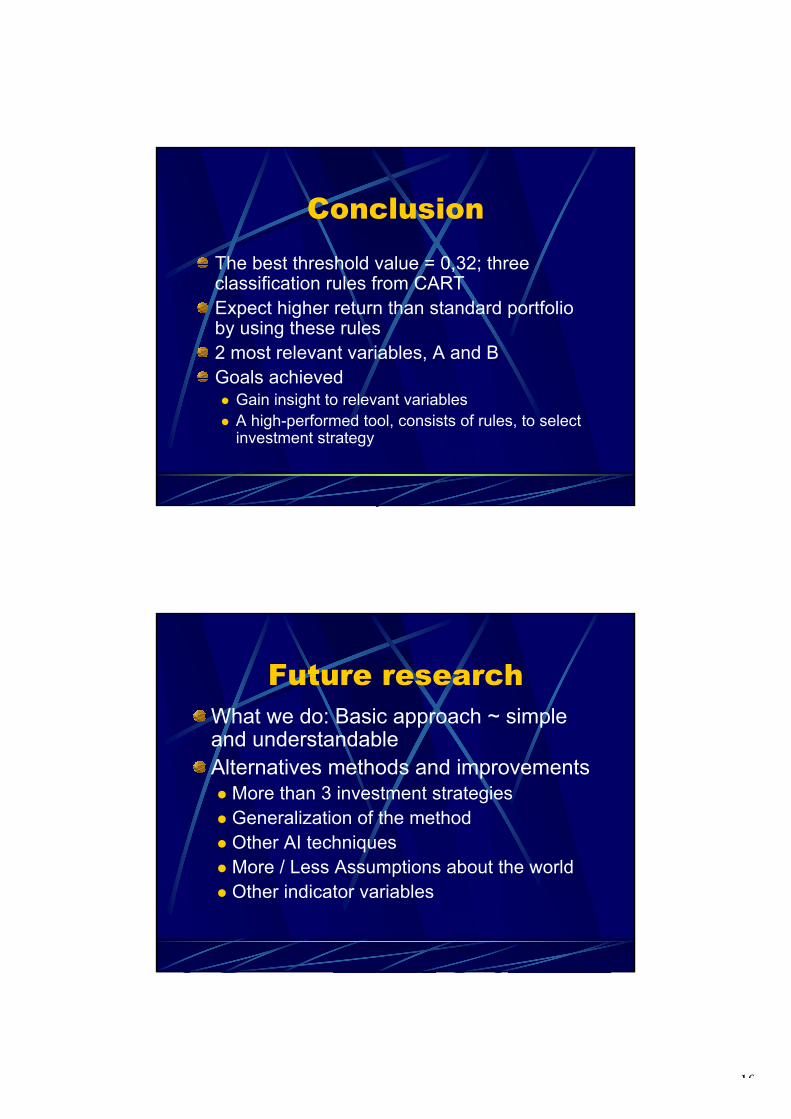

Improving Asset Allocation using a CART Model

Chi Lok Cheung, Heru Sataputera Na, Jan van den Berg

Erasmus University Rotterdam

Department of Computer Science Room H9-19, P.O. Box 1738

3000DR Rotterdam, The Netherlands Email: [email protected], [email protected],

Abstract

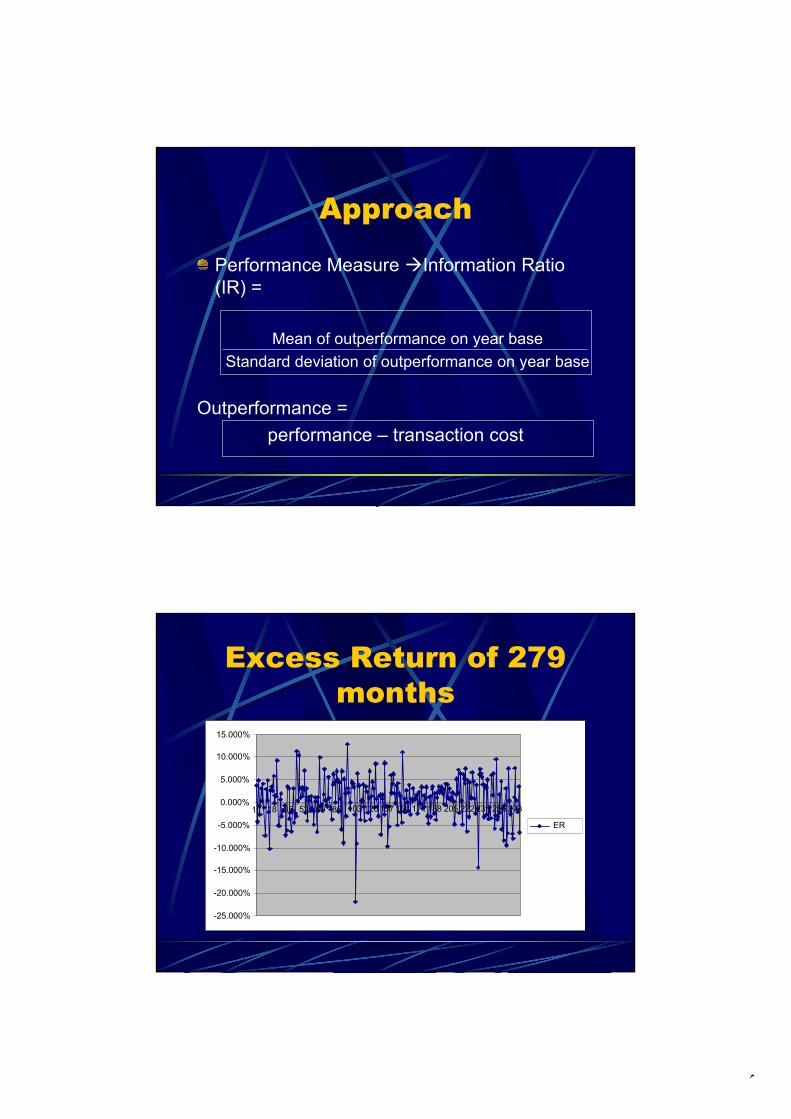

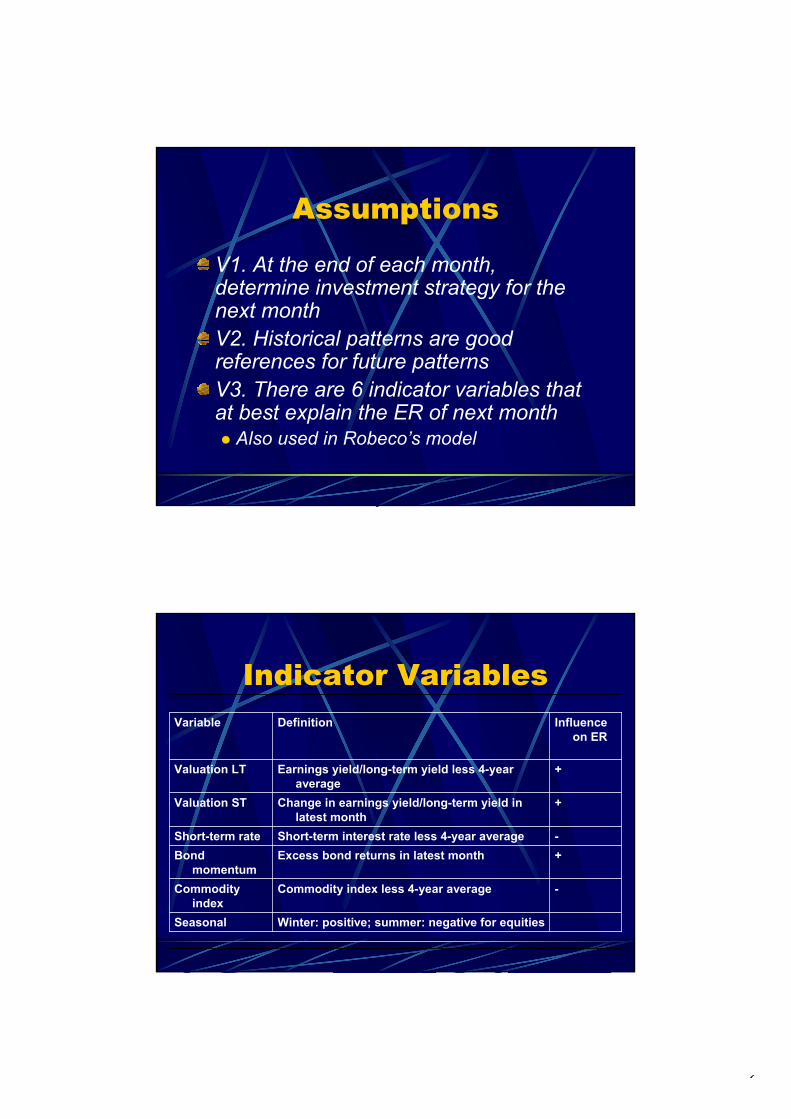

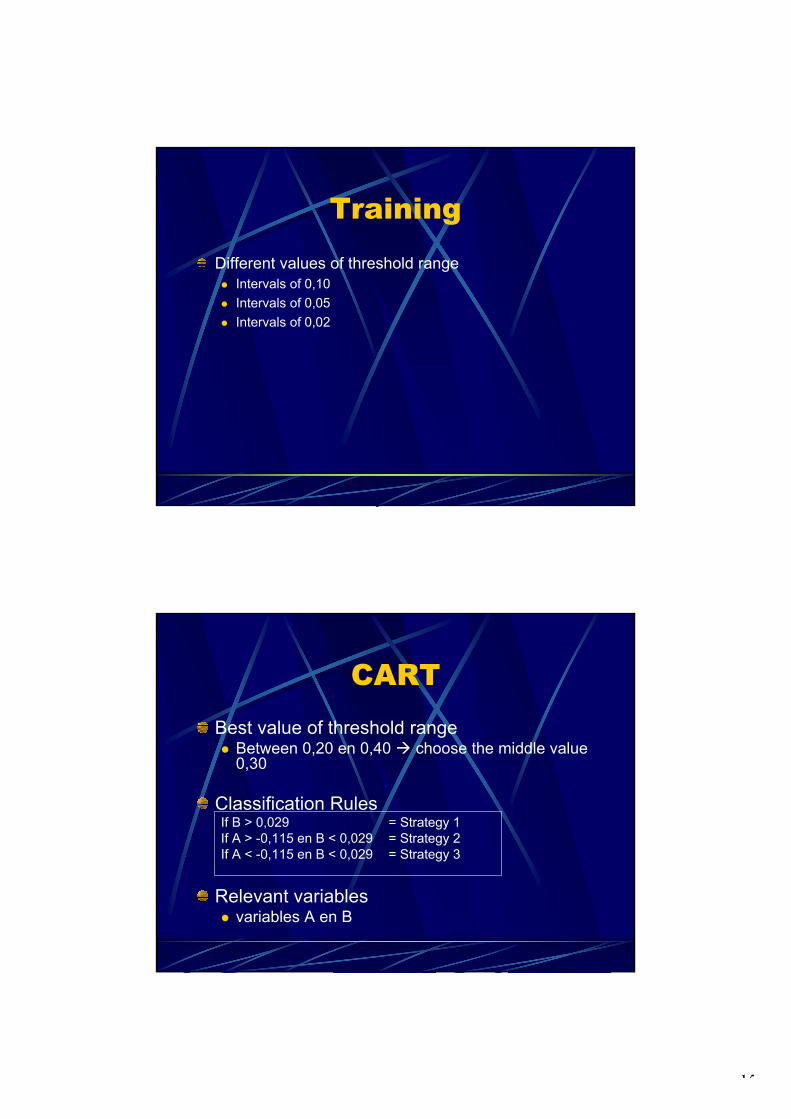

Based on a case offered by ROBECO, we compare three strategies for improving the performance of a Fund Manager who tries to gain a better return on investments by temporarily deviating from the standard investment strategy given by a client. The analysis is based on the construction of a decision tree (CART). The main goals of this work can be formulated as follows:

• To get insight in the importance of the relevant ' indicator variables', • To improve performance by intelligently adapting the investment strategy.

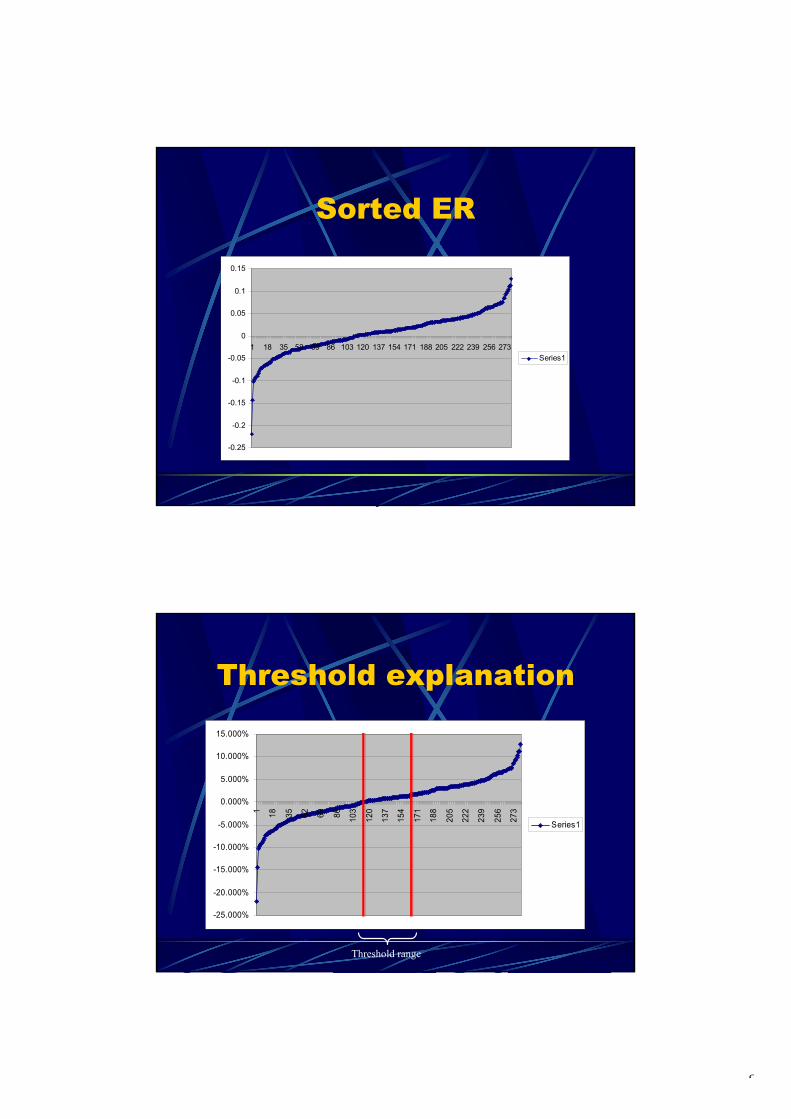

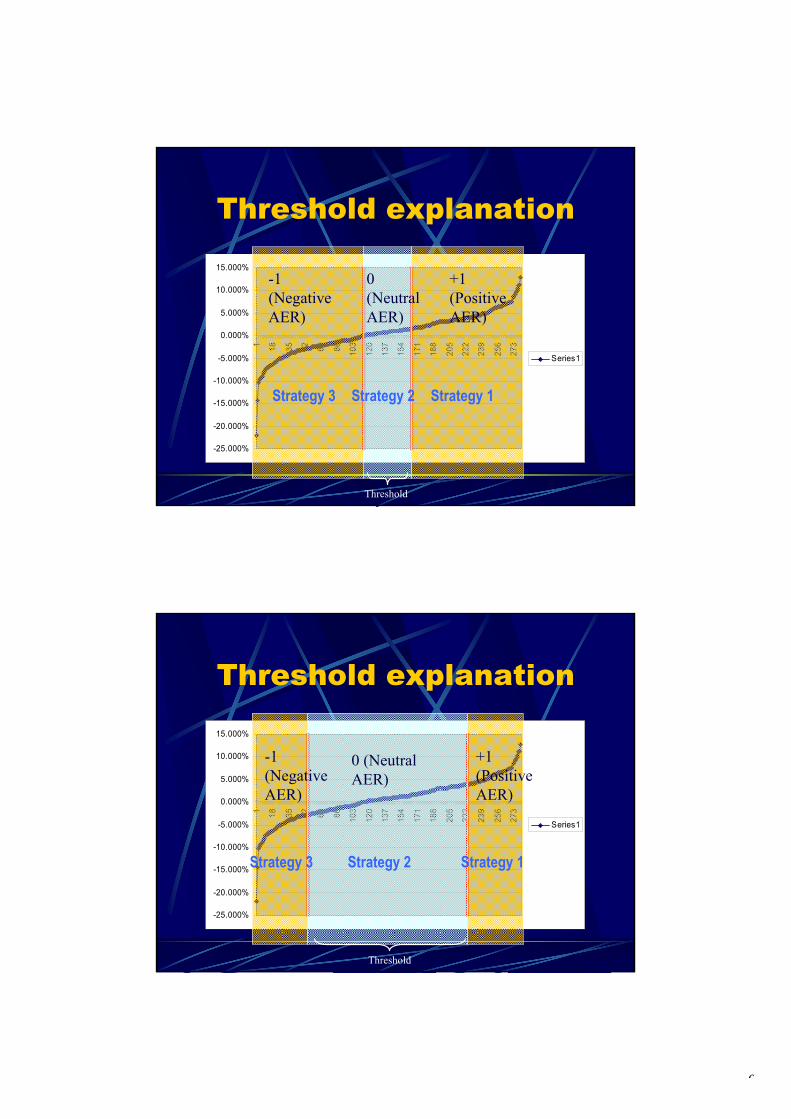

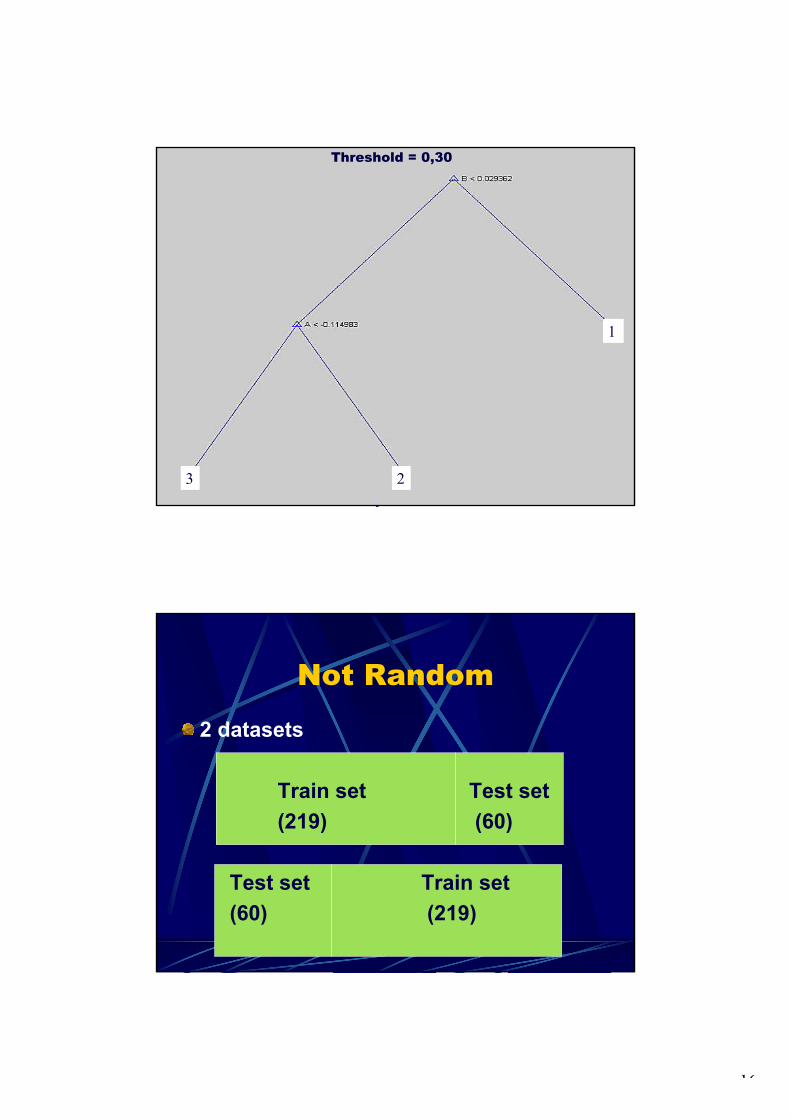

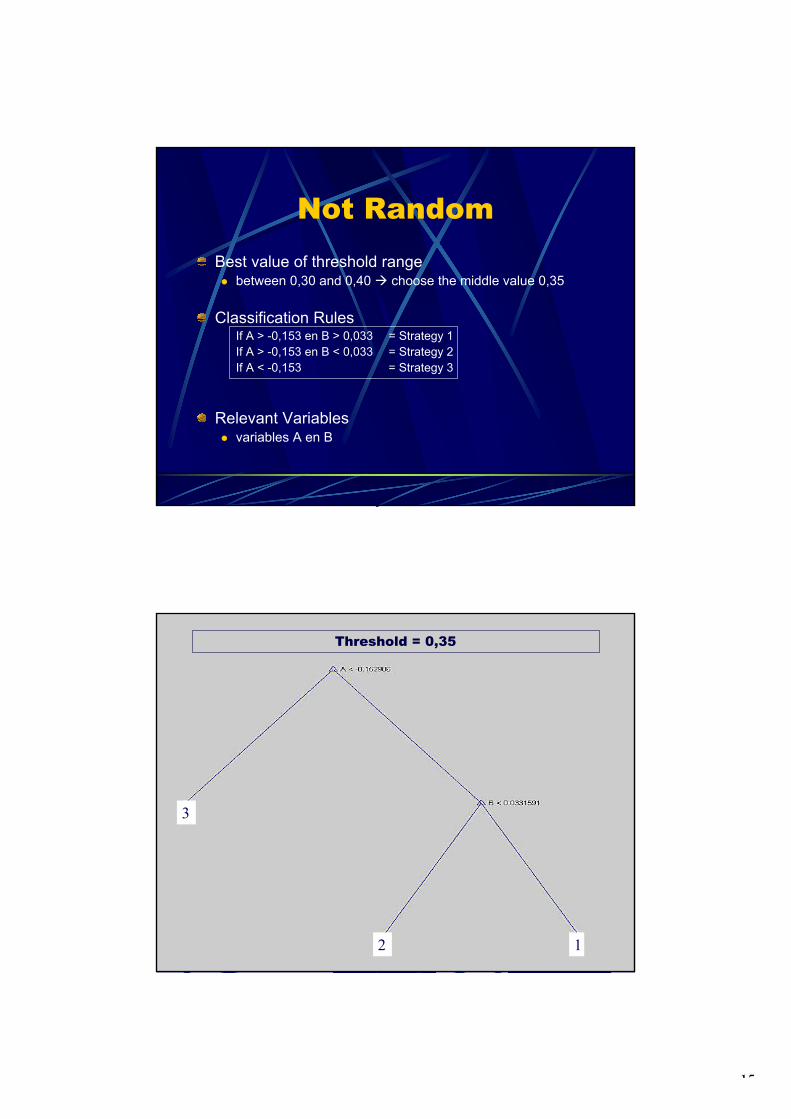

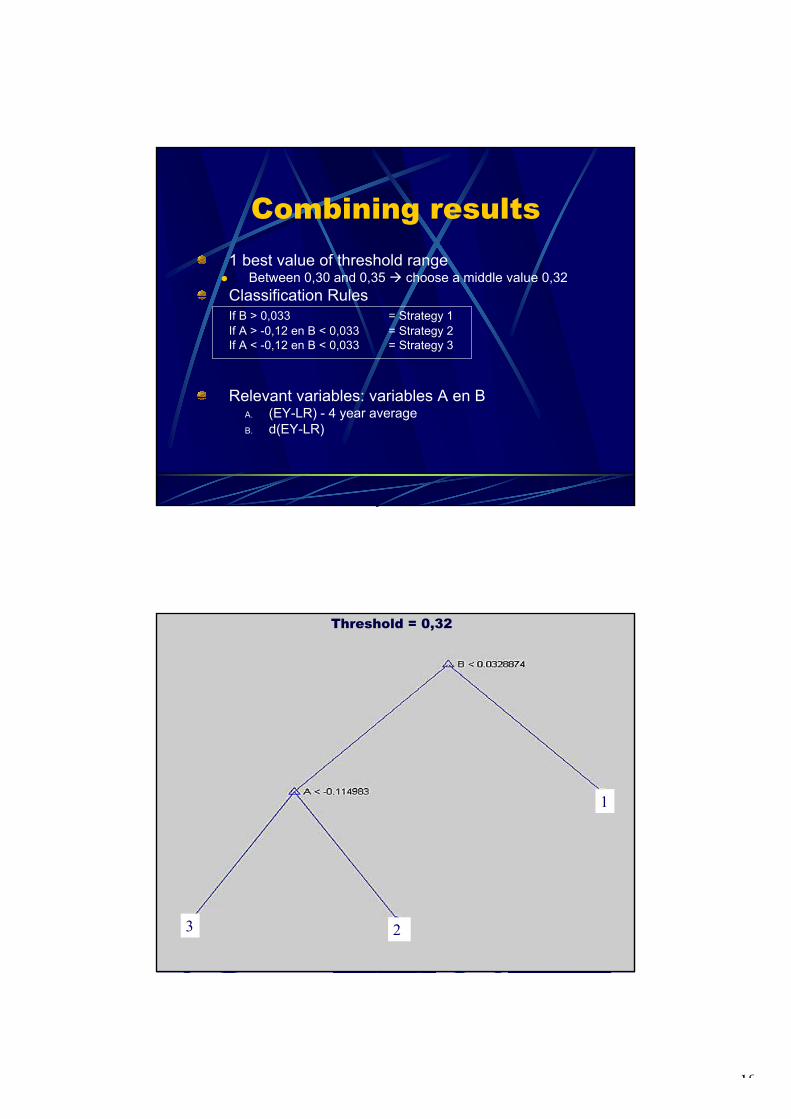

Elaboration: The return as obtained by applying the client’s investment strategy is termed the standard return. The standard strategy for this case concerns a strategy with 50% investment in equities and 50% investments in fixed income. The fund manager is allowed to deviate temporarily from the standard strategy provided that – on average – the investments are still about 50% in equities and 50% in fixed income. To simplify matters, the deviating strategies used here are either 100% investment in equities and 100% investment in fixed income. In this way, the problem becomes to find out under which circumstances (input conditions) what type of strategy should be chosen, i.e., investments in either 100% equities (strategy 1), 50% equities and 50% fixed income (strategy 2), or 100% fixed income (strategy 3). The available data set concerns a set of indicator variables which are assumed to be related to the next month return rates of investments in equities and in fixed income. All together, 279 month’ records are available. Let the excess return ER(m) in month m be defined as

),()()( mRmRmER FIEQ −= (1)

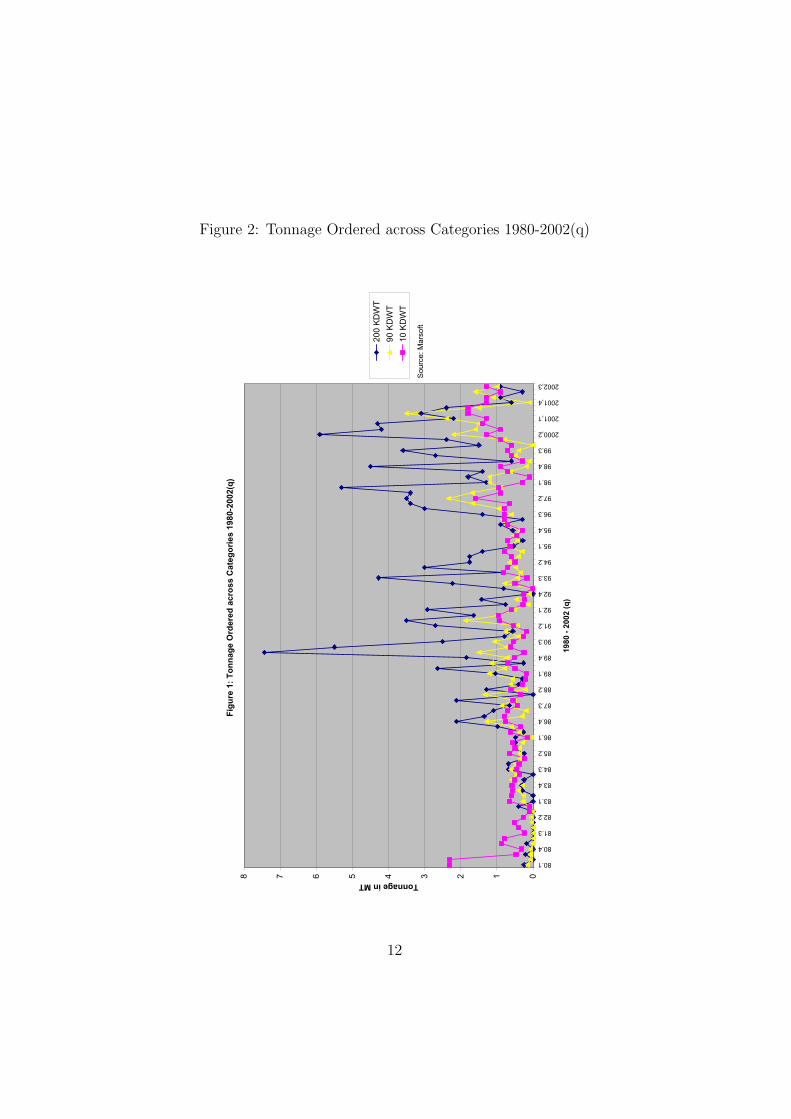

where )(mREQ is the return from investments in equities and )(mRFI represents the return from investments in fixed income (in month m). The historical Excess Returns ER(m) can be calculated from the given data set and are shown in the next figure:

-25.000%

-20.000%

-15.000%

-10.000%

-5.000%

0.000%

5.000%

10.000%

15.000%

1 18 35 52 69 86 103

120

137

154

171

188

205

222

239

256

273

Series1

In case ER(m+1) (excess return in the next month) is expected to be positive, it is reasonable to apply strategy 1, in case ER(m+1) ≈ 0, strategy 2 is most appropriate, and if ER(m+1) is negative, strategy 3 is best. To implement this idea, we have introduced a threshold range α (0 ≤ α ≤. 1) that determines two cut-off points of excess returns. The corresponding investment decision rule can be summarized as follows: If Expected ER(m+1) > (1+α)/2 Then 'Select Strategy 1', If Expected ER(m+1) < (1-α)/2 Then 'Select Strategy 3', Else 'Select Strategy 2'. E.g., if α = 0.2, the corresponding cut-off points are 0.4 and 0.6. Consequently, if the expected ER() belongs to the 40% lowest excess returns observed, strategy 3 is chosen, if it belongs to the 40% highest excess returns, strategy 1 is chosen, otherwise strategy 2 is chosen. It should be clear that the selection of the strategy to be applied (in the next month) depends on α. One of the main goals of our research efforts has been to find the optimal value of α. The optimal decision strategy has been induced from the data by trying various α-values where the CART algorithm [1] has been used in order to (a) first learn and to (b) second predict (classify) the right strategy. During the presentation, the details of the approach will be shown. In practice, changing strategy involves transaction costs that should be taken into account. These transaction actions are indeed taken into account when we calculated the performance of each system developed. In addition, 10-fold cross validation has been applied in order to investigate the stability of our approach. Results: We will conclude the presentation by showing the precise results. Among other things, we found that a threshold value of about α = 0.32 yields the expected best investment decisions. We will also show the corresponding decision trees. In the near future, all results will be discussed with the domain experts. References:

[1] Breiman, et al. (1993). Classification and Regression Trees, Chapman and Hall, Boca

Raton.

[2] Help files van Statistics Toolbox, Matlab

[3] Mitchell, T. M. (1997). Machine Learning, McGraw–Hill International Editions,

Computer Science Series, p. 63

[4] Quinlan, J. R. (1986). Induction of Decision Trees. Machine Learning, 1(1), p. 81-

106

[5] Quinlan, J. R. (1993). C4.5: Programs for Machine Learning. San Matteo, CA:

Morgan Kaufmann.

Basel II Compliant Credit Risk Management: the OMEGA Case

Peter van der Putten KiQ Ltd

& LIACS, Leiden University

Arnold Koudijs KiQ Ltd

De Lairessestraat 150 1075 HL Amsterdam,

The Netherlands {peter.van.der.putten,

arnold.koudijs, rob.walker} @ kiq.com

Rob Walker KiQ Ltd

ABSTRACT In this paper we highlight some high level requirements for adaptive modelling in a BASEL II credit risk context and highlight the OMEGA approach as a case example for BASEL II compliant risk management. We conclude with a vision on the future of adaptive ratings, models and enterprises.

Keywords Rating models, credit risk, Basel II, computational intelligence, adaptive systems

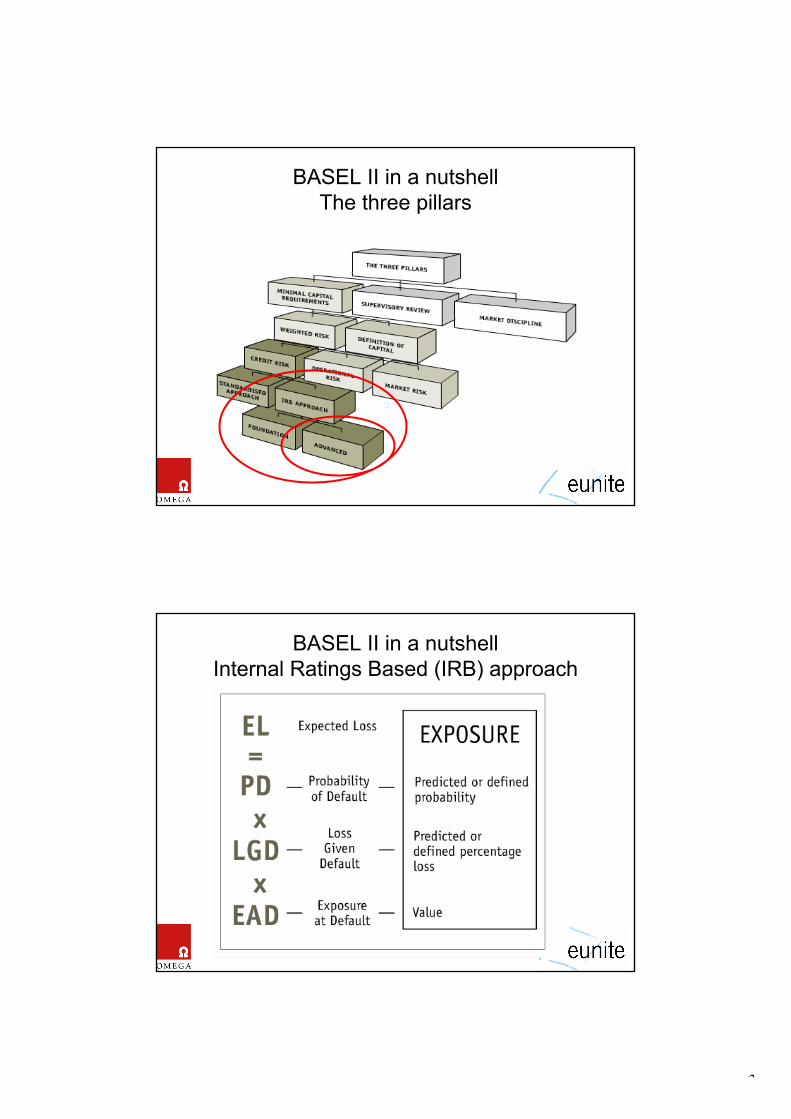

1. Introduction The new BASEL Accord (BASEL II) aims to make regulatory capital requirements more sensitive to risk to improve the overall stability of the financial market. BASEL II covers credit, market and operational risk. For calculating and managing credit risk, banks can follow the so-called Internal Ratings-Based approach (IRB), which allows calculation of risk ratings based on models developed by the bank on its own data [1].

Of course, the procedures for developing, deploying and monitoring these models must meet certain requirements, some of which are specified explicitly by BASEL II and some of which are implied by it. In section 2 we will highlight a selection of these requirements. Next, the OMEGA Active Decision Management Suite will be discussed as a case example of a state of the art solution for implementing a managed BASEL II credit risk management process (section 3). In addition we identify some opportunities that are related to BASEL II, beyond mere compliancy (section 4). Finally we specifically address some of the no-go areas and opportunities for adaptive control (section 5).

2. IRB Requirements The Internal Ratings-Based (IRB) approach depends on so-called risk components to calculate the expected loss for each exposure, which in turn sum up to the total credit risk. Basel II dictates that the capital requirements are not only based on the expected losses but also on the sophistication of the methods used to estimate these losses. The more advanced the methods used, the better a bank can do in reducing the minimum capital requirements. Expected loss is defined as

EL= PD x LGD x EAD x M (1)

with PD the probability of default, LGD the loss given default, EAD the exposure at default and M the maturity of the exposure. Typically, under the so-called IRB Foundation approach, banks provide their own estimates of PD and use supervisory estimates for other risk components – in the Advanced IRB approach all components are estimated by the bank itself.

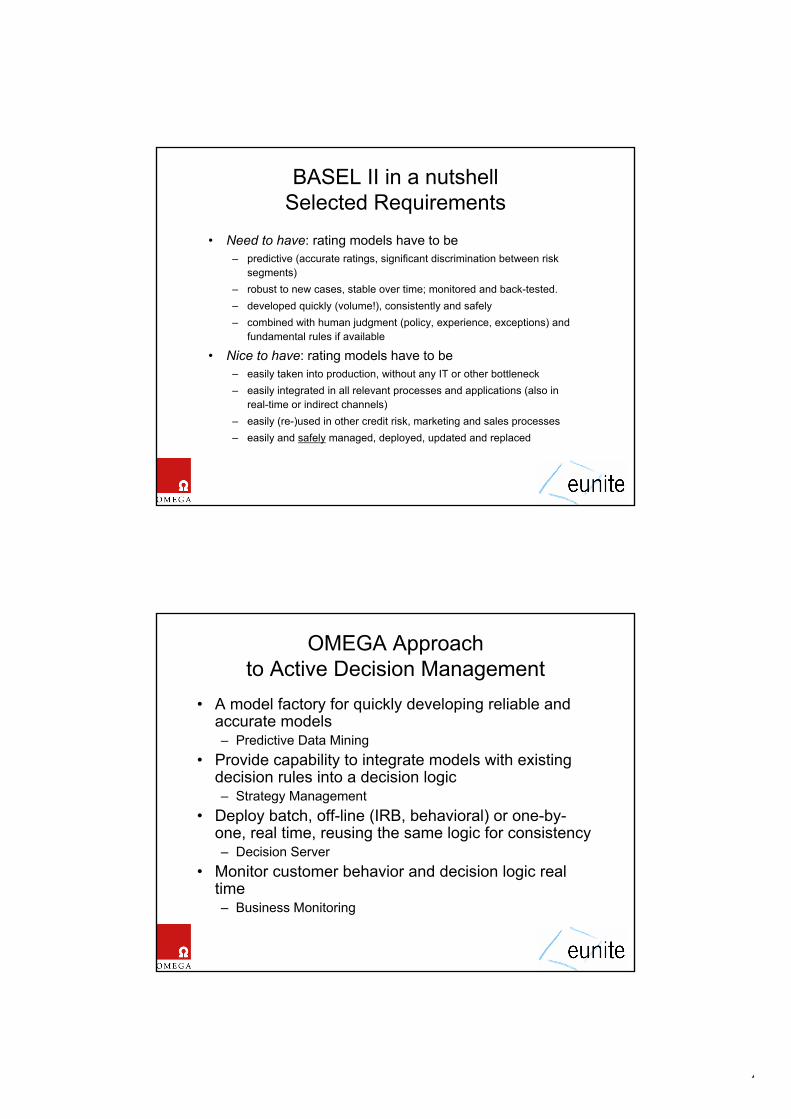

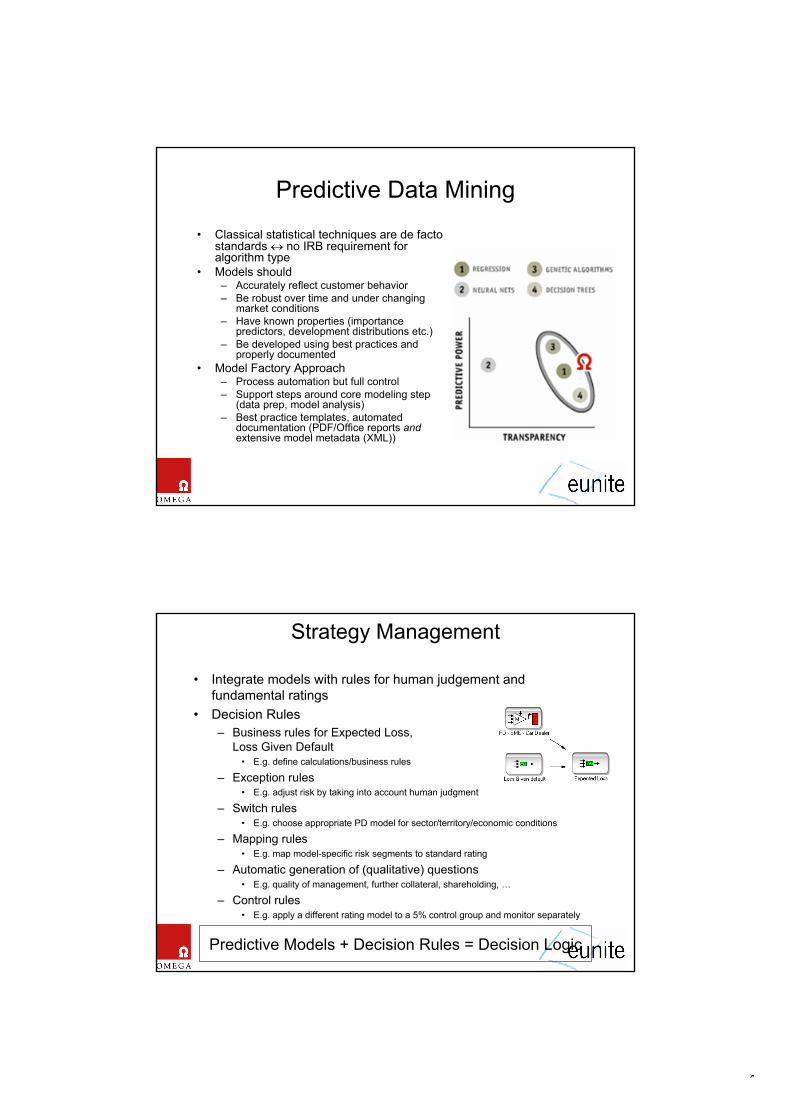

Basel compliant ratings must be calculated on the basis of at least two years of data, so the availability of historic data over that period is a must have. The data must be analyzed to calculate ratings that properly reflect the risk in a portfolio. Historically, classical statistical methods like regression are used for estimating risk components. However, the BASEL II standard does not require a specific modeling algorithm to be used, but these must meet a number of criteria. Merely being predictive is not good enough. The models must be proven to be stable under varying economic conditions and over various points in time. A priori risk assessment knowledge that may improve the bottom-up risk models must be incorporated where possible.

3. The OMEGA Approach Originally, the focus of OMEGA was purely on predictive model development for credit risk management using genetic algorithms [5]. Then OMEGA developed into a full decision management suite for optimising the entire customer relationship, including risk. OMEGA provides managed process support for the steps after a model has been developed: linking models with business rules into a decision logic, batch and real-time decision logic deployment and monitoring [2,3,4].

3.1 Model Development Process BASEL II requires that best practices for developing rating models are followed, to minimize the scope for errors and ensure consistent quality. In our opinion, the best way to ensure this is to hardcode this process in the model development tool and to provide automated support where possible, without sacrificing user control. This should not be limited to the core model algorithms, but also include project definition, data preparation and model evaluation. Because of this model factory approach, model accuracy, - robustness and process compliancy are optimized and a full audit trail to the development process can be provided. Projects can also be saved to best practice templates. As core modelling algorithms, logistic regression, additive scorecards, decision trees and genetic algorithms are available, to cover the whole spectrum between simple, understandable models and more powerful, complex models.

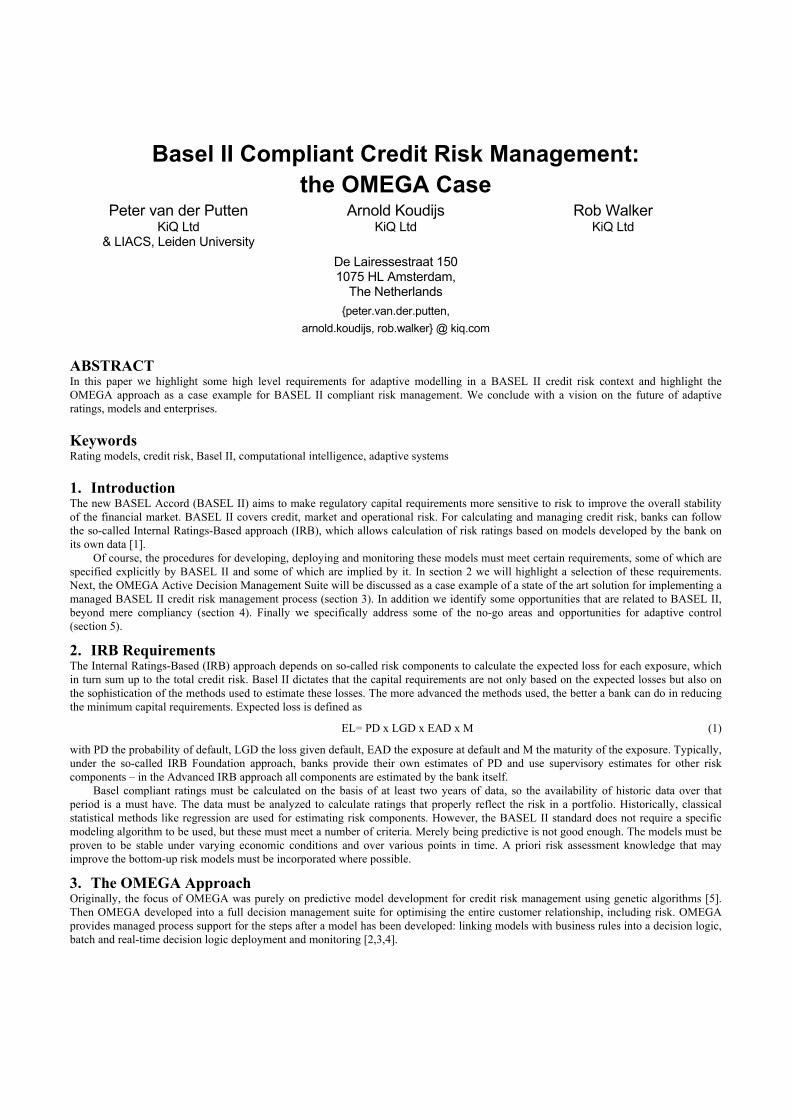

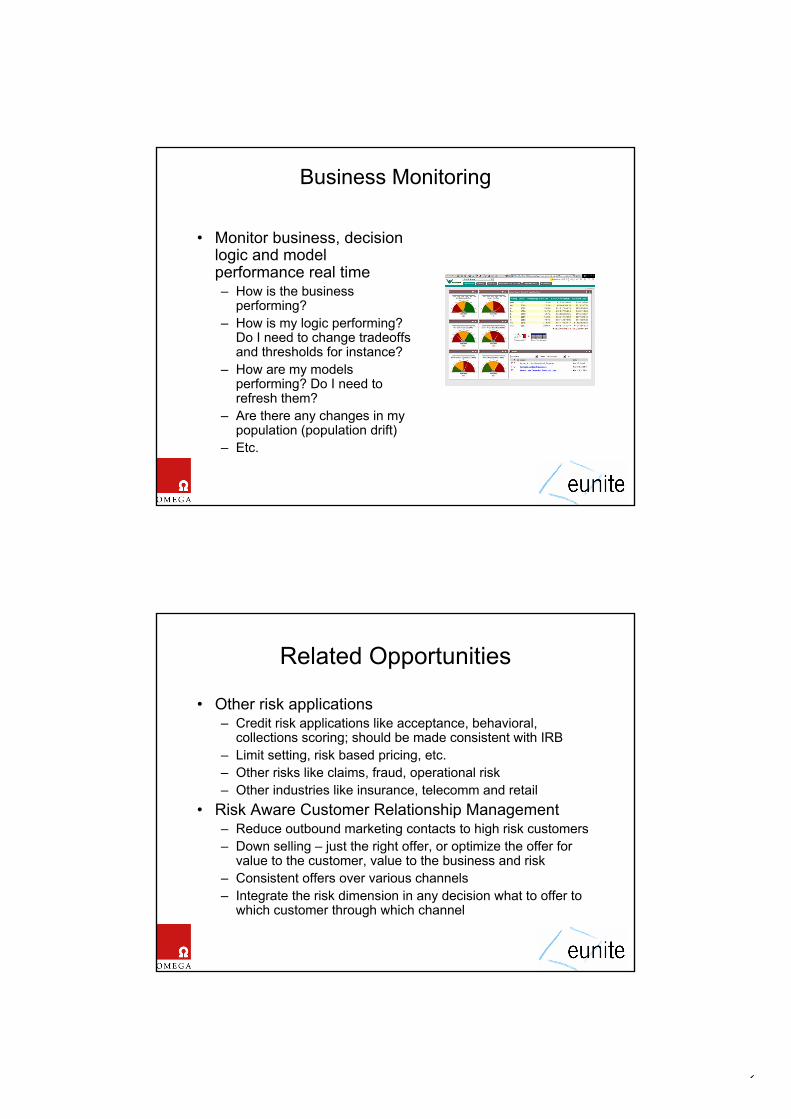

3.2 Business Policies, Rules and Strategies The OMEGA Strategy Management system allows rating models to be complemented by decision rules. This facility is typically used to express risk assessment knowledge based on information that is out of scope of the model. Examples are exceptions that lead to increase or decrease in rating or simply the implementation of core IRB formulae. Another use case would be a comprehensive rating system that requires multiple rating models. An example would be a system that rates small and medium enterprises based on several sector specific rating models, or a rating logic that combines models for different economic cycles (figure 1) [2].

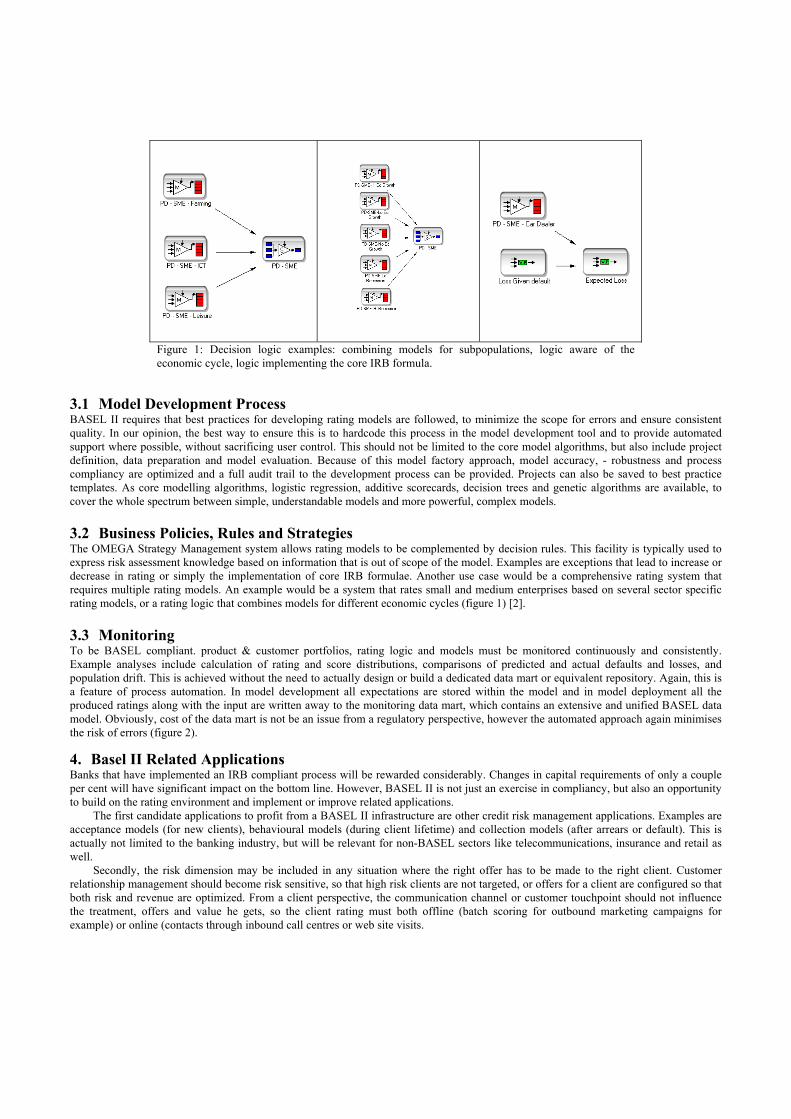

3.3 Monitoring To be BASEL compliant. product & customer portfolios, rating logic and models must be monitored continuously and consistently. Example analyses include calculation of rating and score distributions, comparisons of predicted and actual defaults and losses, and population drift. This is achieved without the need to actually design or build a dedicated data mart or equivalent repository. Again, this is a feature of process automation. In model development all expectations are stored within the model and in model deployment all the produced ratings along with the input are written away to the monitoring data mart, which contains an extensive and unified BASEL data model. Obviously, cost of the data mart is not be an issue from a regulatory perspective, however the automated approach again minimises the risk of errors (figure 2).

4. Basel II Related Applications Banks that have implemented an IRB compliant process will be rewarded considerably. Changes in capital requirements of only a couple per cent will have significant impact on the bottom line. However, BASEL II is not just an exercise in compliancy, but also an opportunity to build on the rating environment and implement or improve related applications.

The first candidate applications to profit from a BASEL II infrastructure are other credit risk management applications. Examples are acceptance models (for new clients), behavioural models (during client lifetime) and collection models (after arrears or default). This is actually not limited to the banking industry, but will be relevant for non-BASEL sectors like telecommunications, insurance and retail as well.

Secondly, the risk dimension may be included in any situation where the right offer has to be made to the right client. Customer relationship management should become risk sensitive, so that high risk clients are not targeted, or offers for a client are configured so that both risk and revenue are optimized. From a client perspective, the communication channel or customer touchpoint should not influence the treatment, offers and value he gets, so the client rating must both offline (batch scoring for outbound marketing campaigns for example) or online (contacts through inbound call centres or web site visits.

Figure 1: Decision logic examples: combining models for subpopulations, logic aware of the economic cycle, logic implementing the core IRB formula.

5. Vision for an Adaptive Future Even though statistical methods appear to be de facto standards in risk management, there are no regulatory limits to using more powerful computational learning methods like decision trees or genetic algorithms. That said, the naive idea of having completely adaptive rating systems without any human controls and checks strongly contrasts with the BASEL concept of a managed, fail safe and robust rating process.

However, increasing the adaptivity of the process as whole, within the quality constraints of BASEL II, will increase the sensitivity to risk and the agility of the enterprise. For instance, passive monitoring reporting could be turned in an active alerting environment that checks whether model inputs, outputs and actual default behaviour are still within expectations gained from historical data and challenger models. The challenger models may be developed in a more automated manner, given that these are not used for deploying ‘official’ ratings, but are just used for benchmarking purposes.

For other risk management applications such as acceptance scoring, the need to make models adaptive is of a lesser order than the need to ‘flex’ the decision logic that determines the right set of customers to be accepted, given predicted sales opportunities and risks. These tradeoff parameters can be set adaptively, depending on sales objectives, risk averseness, company policy, market and portfolio conditions. The enterprise can change any strategic objectives in the decision logic. In the truly adaptive enterprise, the decision logic governs any customer contact through any channel or touchpoint and encompasses any issue, be it risk, retention or sales. Management sets course, policy and objectives while the adaptive decision logic makes optimal decisions - the enterprise is now ready to be flown by wire [6].

6. Conclusion In this paper we have presented selected requirements for BASEL II compliant credit risk management, the OMEGA solution and our vision on the adaptive enterprise. Even though full automation is not desirable from a BASEL II point of view, there is plenty of opportunity to exploit the power of adaptivity to make enterprises more agile.

7. REFERENCES [1] Basel Committee on Banking Supervision, Overview of The New Basel Capital Accord. Third Consultative Paper (CP3), April 2003 [2] A Solution for BASEL II compliant credit risk management. KiQ Whitepaper, 2003. [3] Koudijs A., Putting Decision-Making in Consumer Credit into Action, Credit Risk International, September-October 2002, pp 25-26 [4] Van der Putten, P. Broodnodige Intelligentie voor CRM. Database Magazine nr 7, November 2002. [5] Walker R.F., Haasdijk E.W., Gerrets M.C. Credit Evaluation Using a Genetic Algorithm, in Intelligent Systems for Finance and

Business, S. In: Goonatilake & P. Treleaven (eds), John Wiley & Sons, Chichester, England, ISBN 0-471-94404-1, pp. 39-59, 1995. [6] Fly by Wire: Command and Control over Customer Interaction. KiQ Whitepaper, 2001.

Figure 2: Example of a monitoring dashboard

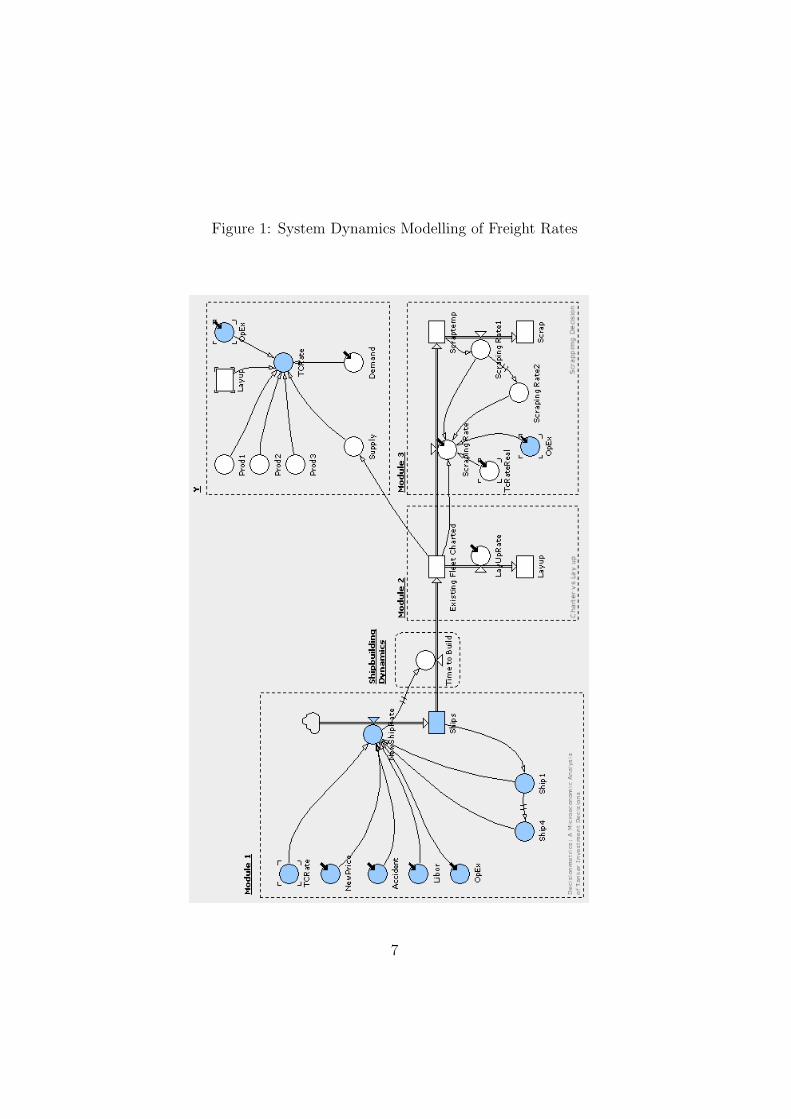

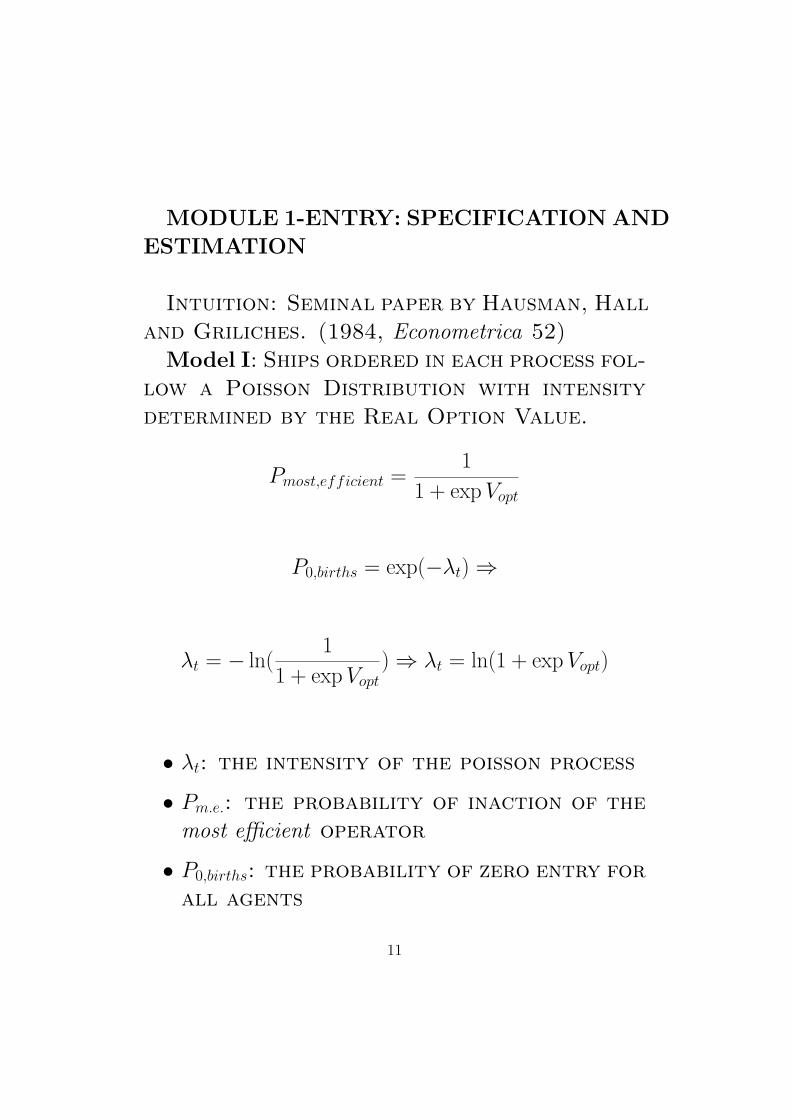

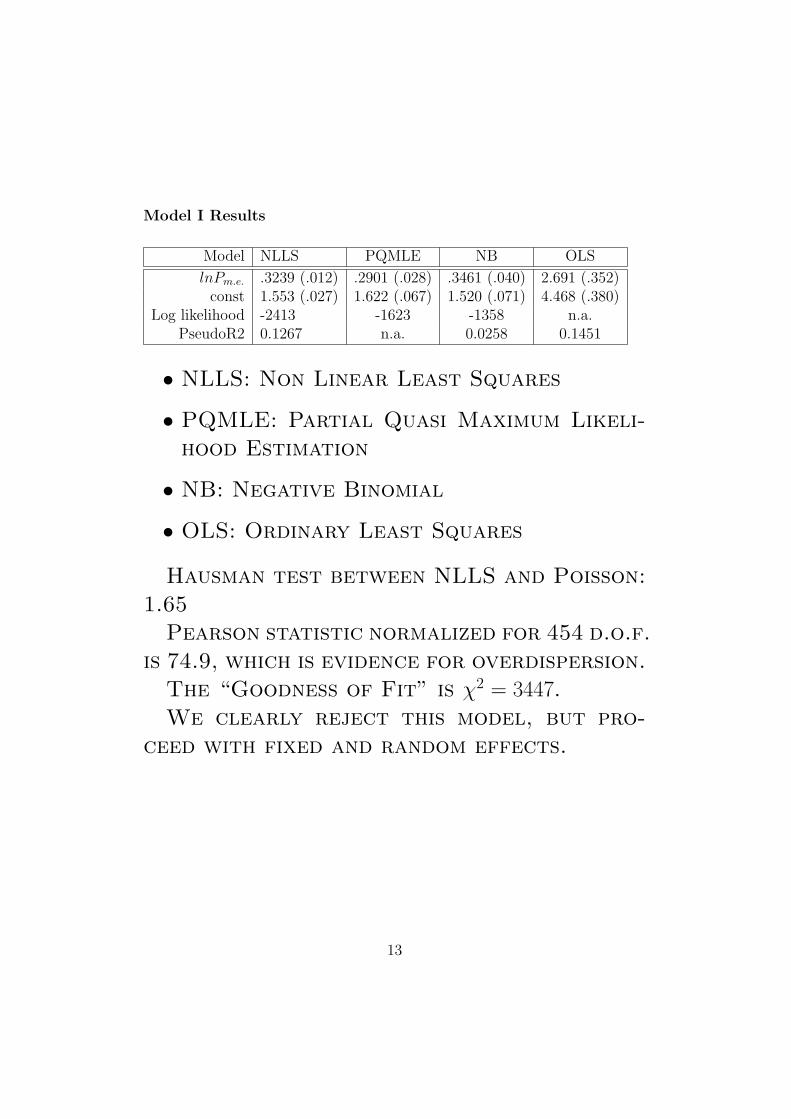

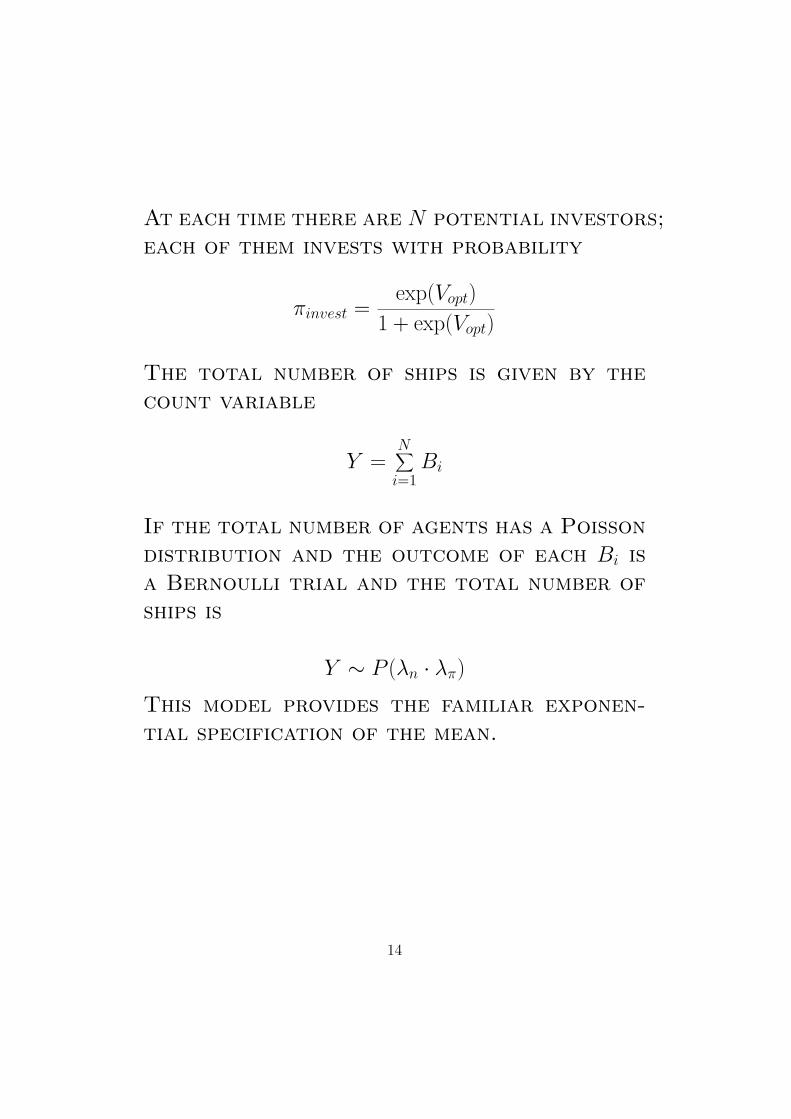

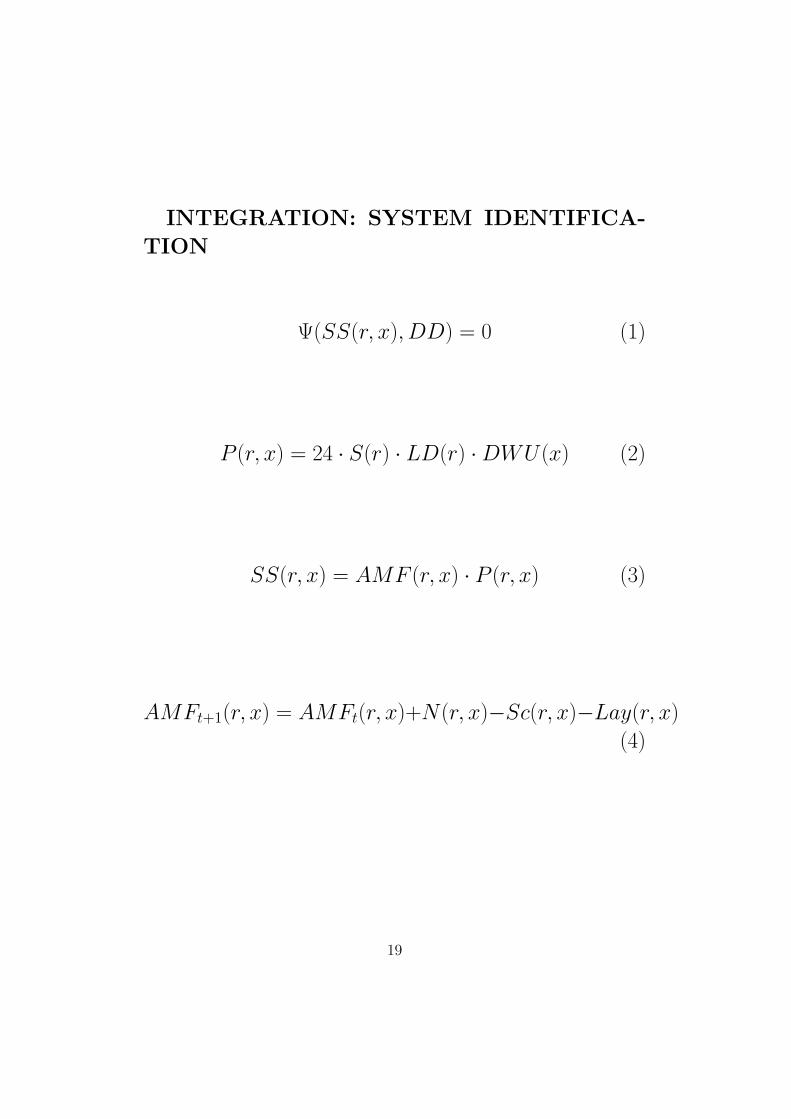

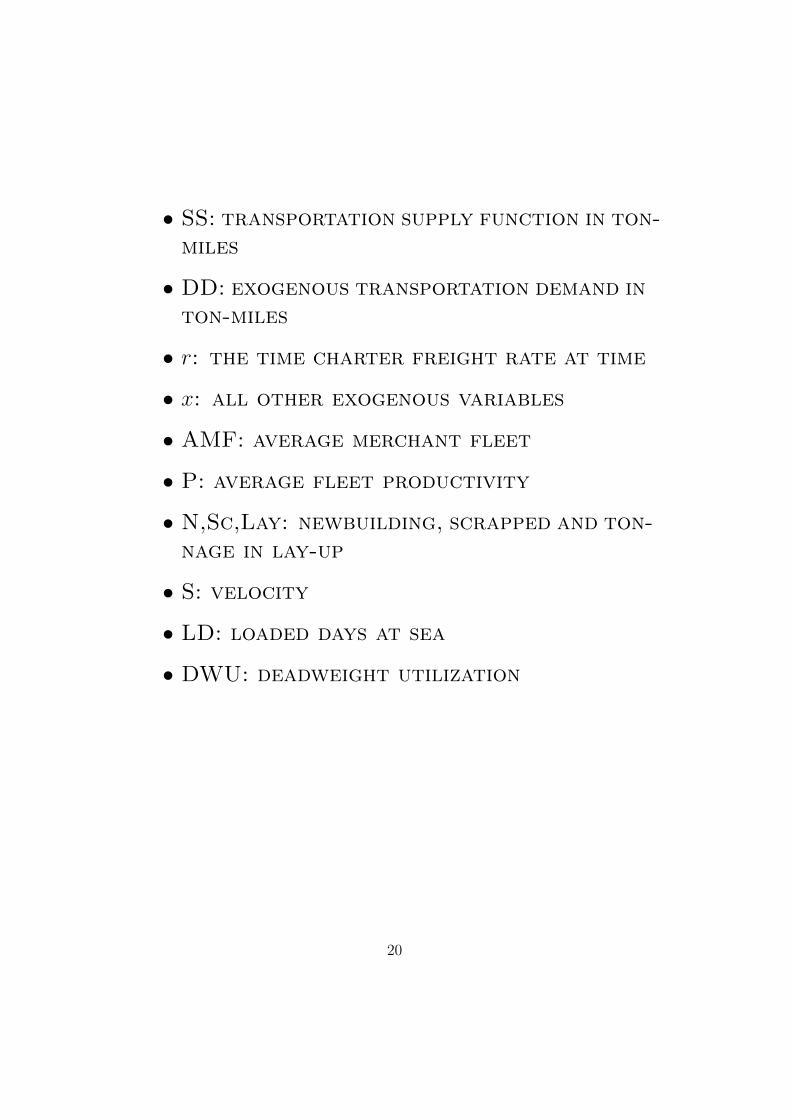

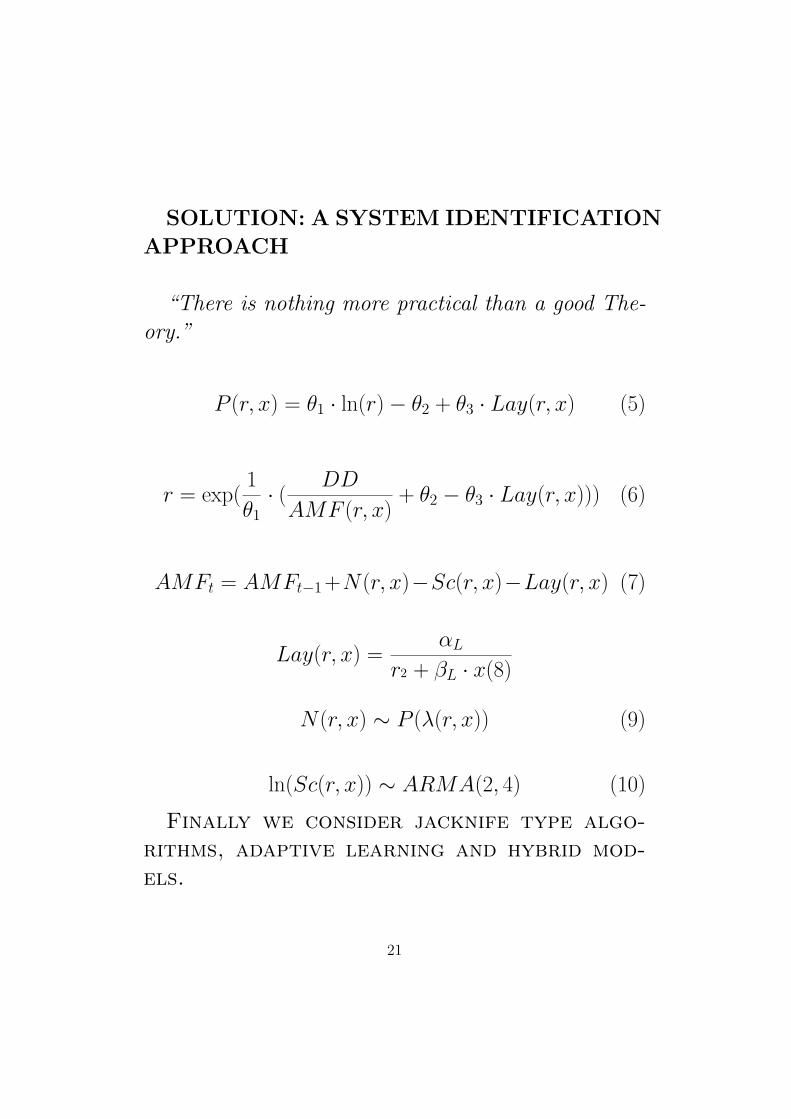

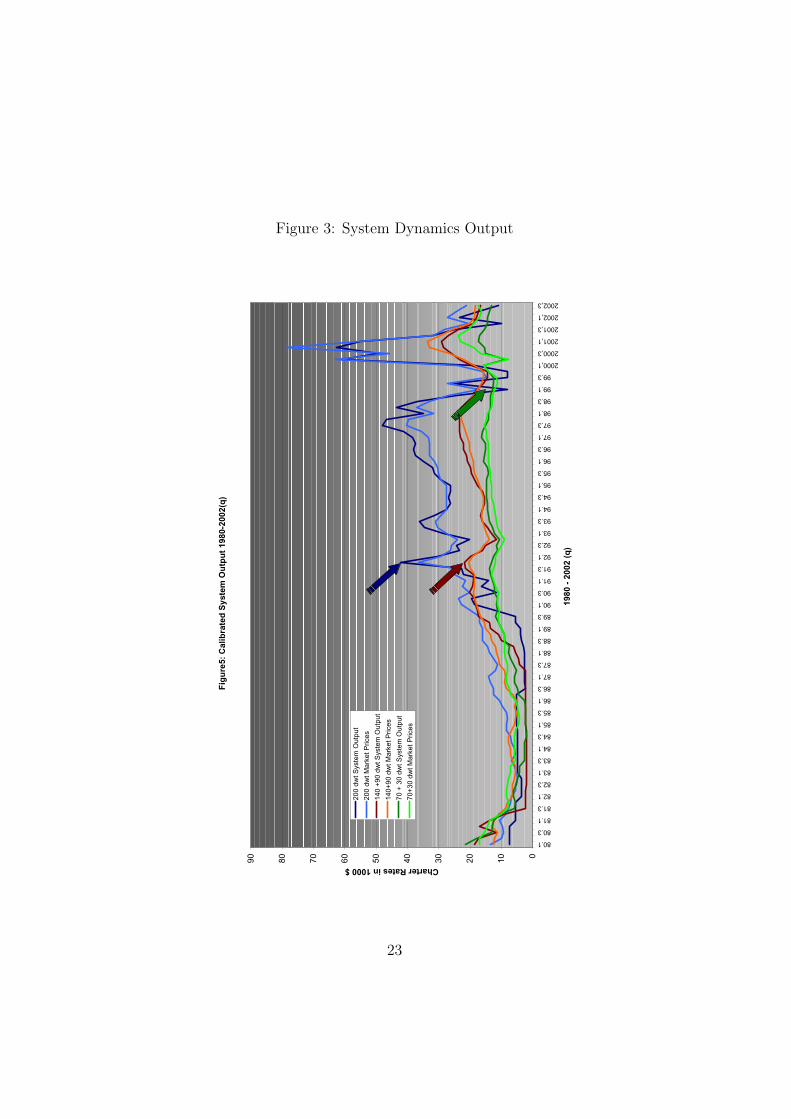

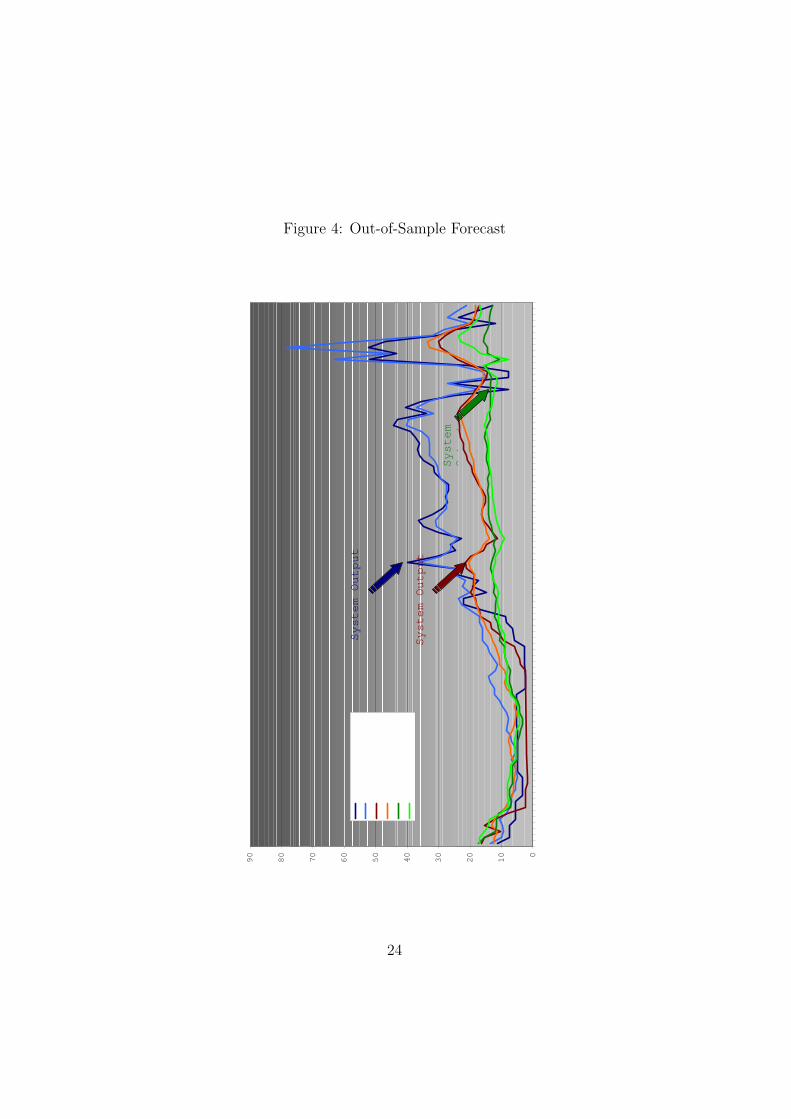

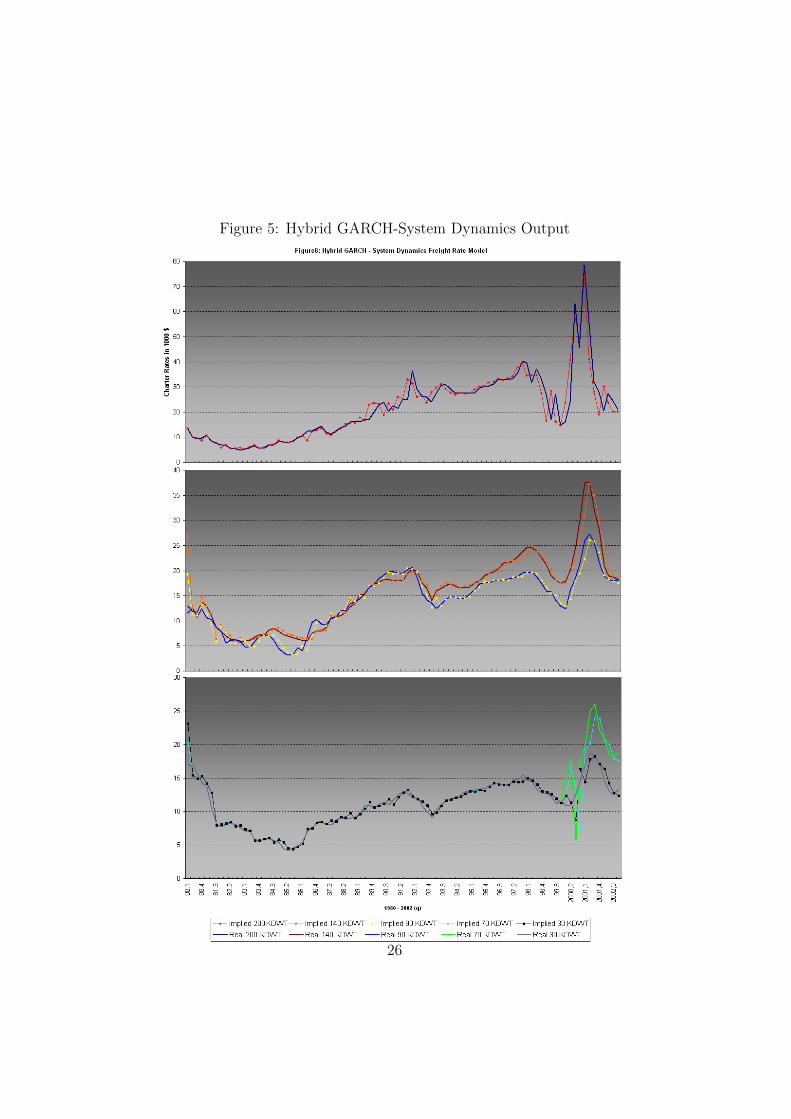

A System Identification and LearningApproach to Tanker Freight Modelling

George Dikos ∗

Massachusetts Institute of Technology

May 2, 2004

1

AbstractIn this paper we use a System Identification approach for the specification

and estimation of the evolution of freight rates for tanker carriers. Wederive the parametric form of the modules of the system from first

principles and employ Economic Theory, in order to reduce thedimensionality of the problem and allow for the control of different policies

on heterogenous agents. We aggregate actions by individual agents andform the structural equations that determine the modules of the system.

By combining statistical analysis and economic insight, we achieveidentification of the system and fully track the directional changes in freight

rates. We then proceed with performance evaluation and conclude withdiscussing dynamic learning, as well as a hybrid model that maximizes the

performance of the system, both within and out-of-sample. Finally, weaddress issues of consistency and stability of the system in a framework,

where data arrive dynamically.

1 Introduction

Two are the main objectives of this paper: We develop a structural modelfor time charter rates in the oil tanker industry, using system modellingtechniques. While pursuing this task we demonstrate how system dynamicsand system identification techniques can effectively model complex systems,where agents undertake economic actions and challenge the widespread per-ception that namely, structural models consistently under-perform statisticalmodels.

Since the seminal work of Lucas and Prescott [?] the General Equilibriumapproach has been the predominant structural model for the interaction ofeconomic agents under perfect competition. Due to the strict requirementson the rationality of agents and their ability to commit themselves to fullyrational decisions, the General Equilibrium approach has severe implicationson price dynamics, especially when we try to compute the equilibrium incomplex markets, such as the oil tanker industry. Besides the inability ofmost structural models to over-perform statistical models, economists havebeen particularly cautious with models that do no take into account the abil-ity of agents to “learn” and adapt their optimal policies dynamically. Afterwhat is formally known as Lucas’ critique [?], recursive methods have beenthe standard structural modelling technique. Besides our ultimate goal of de-

2

signing a system that will adequately explain the evolution of tanker freightrates, we go one step further and provide the necessary theoretical reasoningthat will hopefully make the case for employing system dynamics and systemidentification and estimation techniques in the process of modelling complexenvironments with interacting agents.

Before proceeding with implementing our tasks let us re-address the theo-retical issues of system modelling and their empirical relevance in the specificmarket for time charter freight rates. As we discussed earlier, there have beentwo main shortcomings that have not allowed System Identification to be-come the main device towards the modelling of complex economic systemsof interacting agents, despite the natural tendency of economic systems todeviate around a trend: On the one hand the system identification and mod-elling approach suffers inherently from Lucas’ critique [?]. Using the system,in order to account for the effect of different policies, does not take intoconsideration the adverse effects of these policies on the optimal responsesof agents and on the specific modules of the system. Furthermore, most ofthe modules employed are not derived on “first principles”, which does notallow policy makers to control for external events and furthermore does notincorporate the dynamic nature of economic systems. More specifically, themodules of the system are usually derived ad hoc and do not take into ac-count the ability of agents to learn and converge to optimal policies, underthe absence of arbitrage opportunities.

Furthermore, from an empirical point of view the models derived on theprinciples of structural systems have not been able to outperform the sta-tistical models employed in financial applications, such as the GeneralizedAuto Regressive Conditional Heteroscedastic family of models [?]. Due tothe dynamic response of agents to shifts in policy and external shocks, eco-nomic systems are time varying, which implies that even the dimension ofthe system changes over time. Non-parametric solutions may lead to a se-vere over-parametrization of the system and in some sense, if we attempt tofully identify the system non-parametrically, there is no need for economic orscientific intuition. In this paper we demonstrate that despite the fact thatany attempt to model economic systems without theory and first principlesin the background, leads to overparametrization, system theory coupled witheconomics may provide a useful alternative towards the understanding andmodelling of complex economic systems.

The paper is organized as following: We start discussing how EconomicTheory may provide helpful intuition into the case of economic systems with

3

interacting agents, whilst providing the necessary framework for a consis-tent mathematical formulation of the modules of the system, with respectto the equilibrium laws of the neoclassical economic theory. On the agentmicro-level, economics coupled with assumptions of exogeneity allow us toavoid the shortcomings of Lucas’ critique [?] and significantly reduce thedimensionality of the problem. We then proceed and re-address themathematical formulation of the System Identification problem and expandon the interrelated issues of consistency and stability. Finally, we discuss ourempirical results, regarding the modelling of time charter freight rates in thetanker industry and develop an empirical case that clearly outperforms theexisting statistical models. We conclude discussing Hybrid Models that in-tegrate both trends in modelling economic systems. Before proceeding withthese tasks we briefly introduce the tanker market industry and discuss themain characteristics of this market, such as the adverse driving forces andfeedback effects.

4

References

[1] Coyle, R. G. (1978). “A System Dynamics Case Study”. Journal of Op-erational Research 2, 2, pp. 86-96.

[2] Dikos, G. (2004). “Decisionmetrics: Dynamic Structural Estimation ofShipping Investment Decisions”. Unpublished PhD Thesis, Departmentof Ocean Engineering, Massachusetts Institute of Technology.

[3] Dixit A. and R. Pindyck (1994). “Investment under Uncertainty”.Princeton University Press.

[4] Grammenos, C. (2002).

[5] Khaled, A., AbbasMichael G. and H. Bell (1994). “System Dynamics Ap-plicability to Transportation Modelling”. Transportation Research PartA: Policy and Practice 28, 5, pp. 373-390.

[6] Sharp, J. and D.H.R. Price (1984). “System Dynamics and OperationalResearch: An Appraisal”. European Journal of Operational Research 16,pp. 1-12.

5

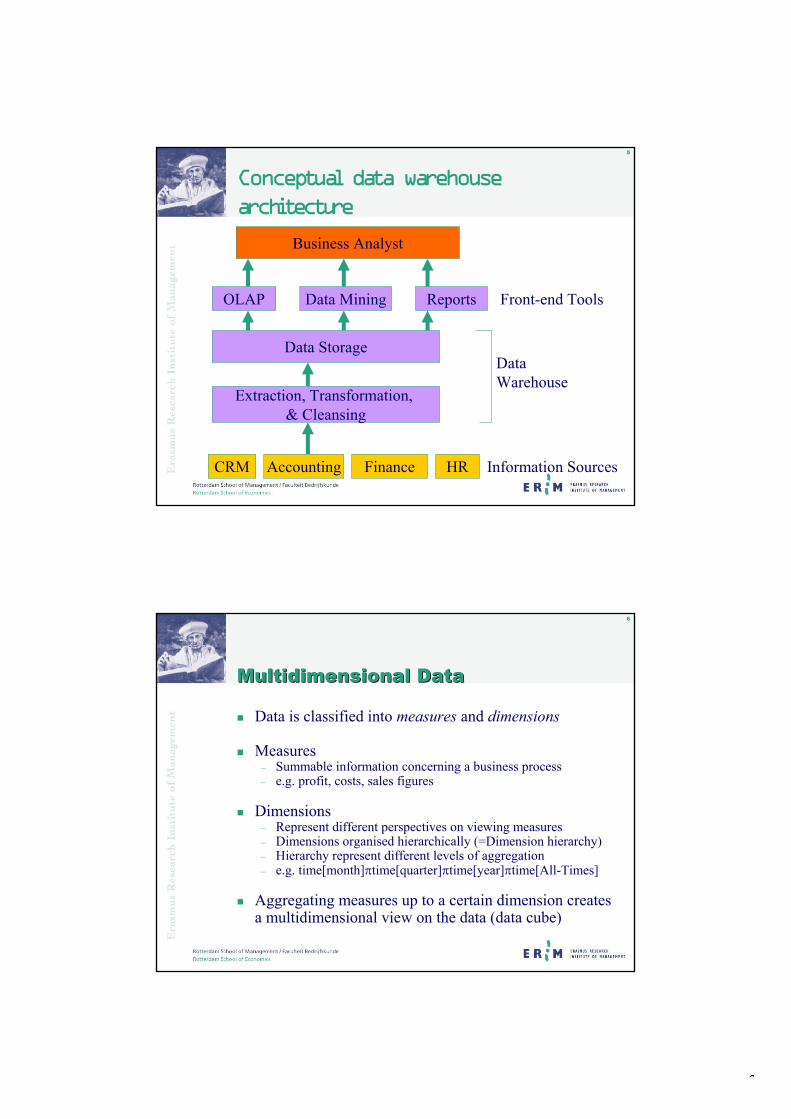

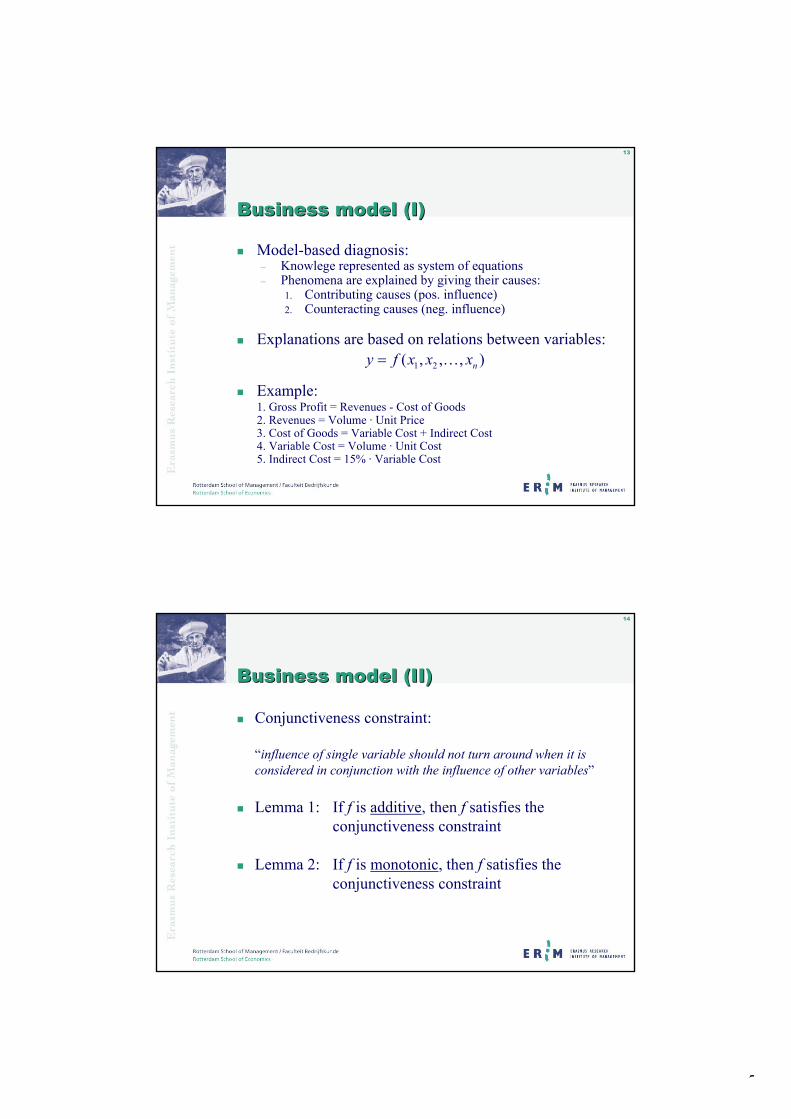

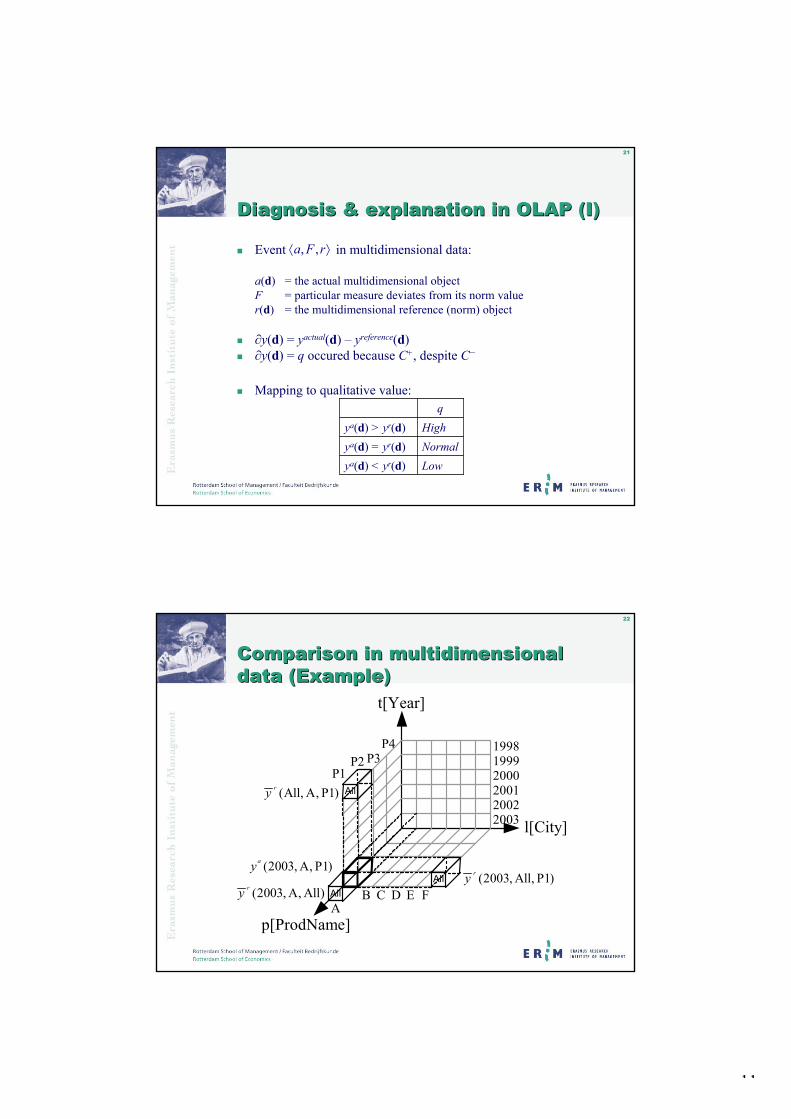

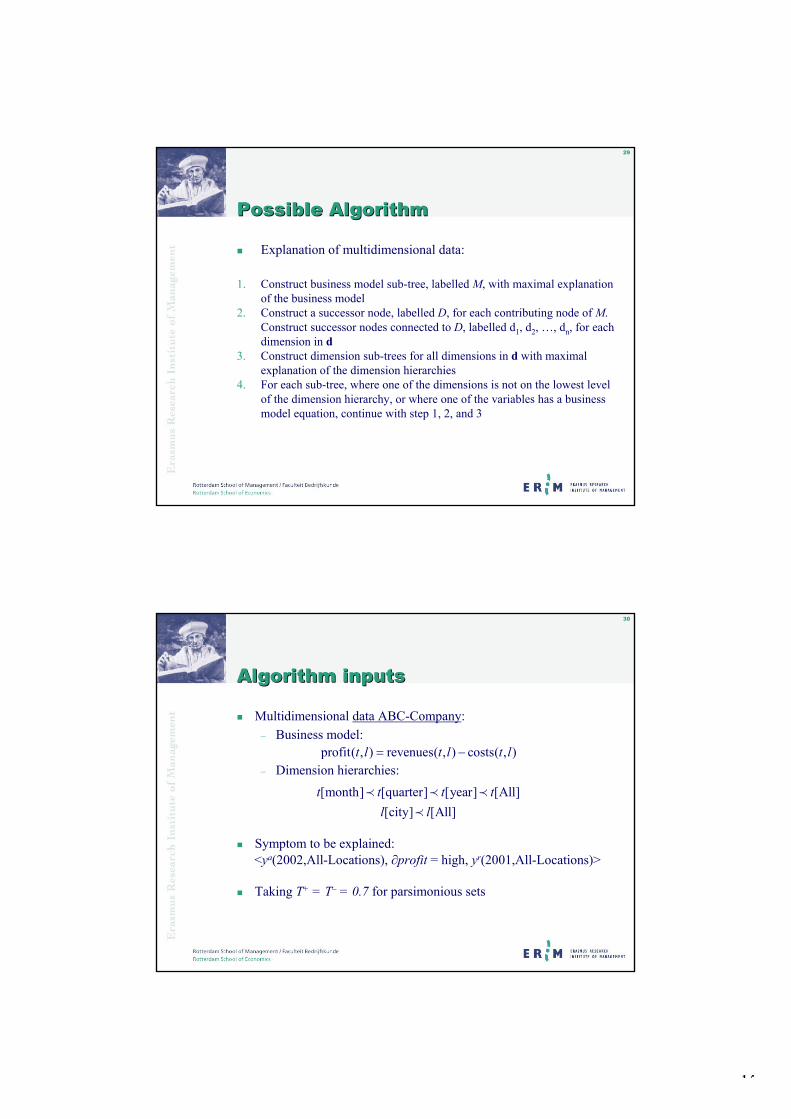

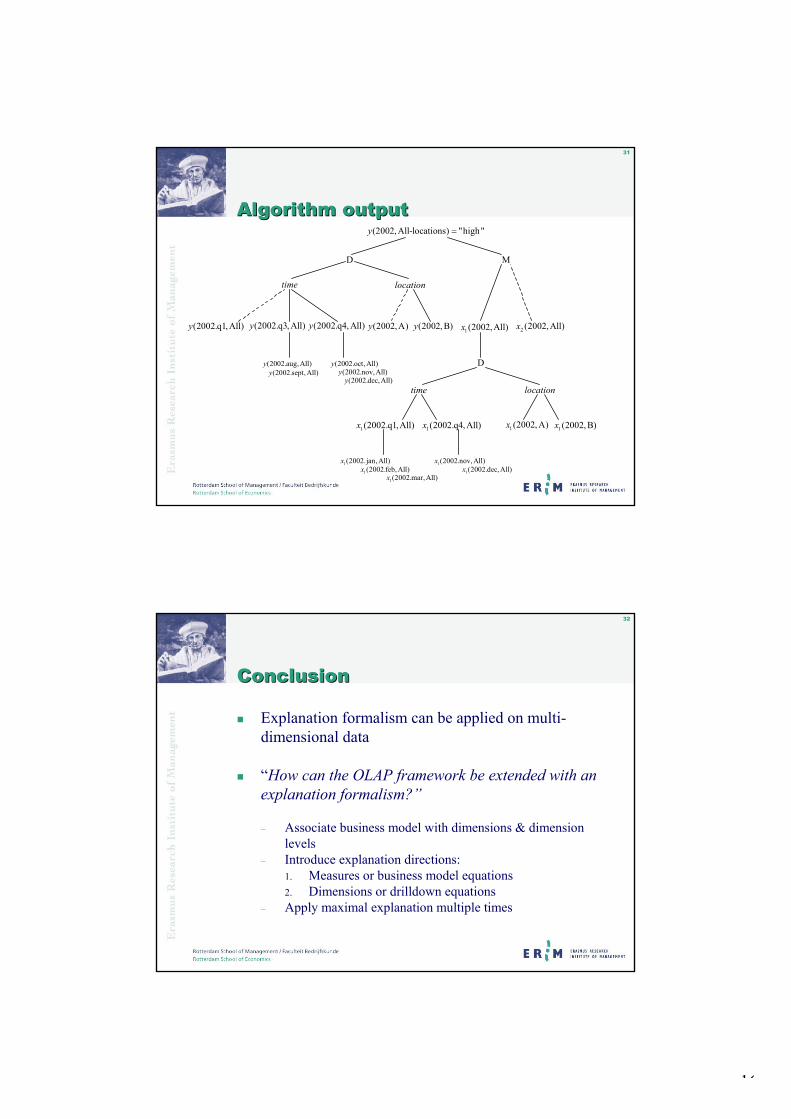

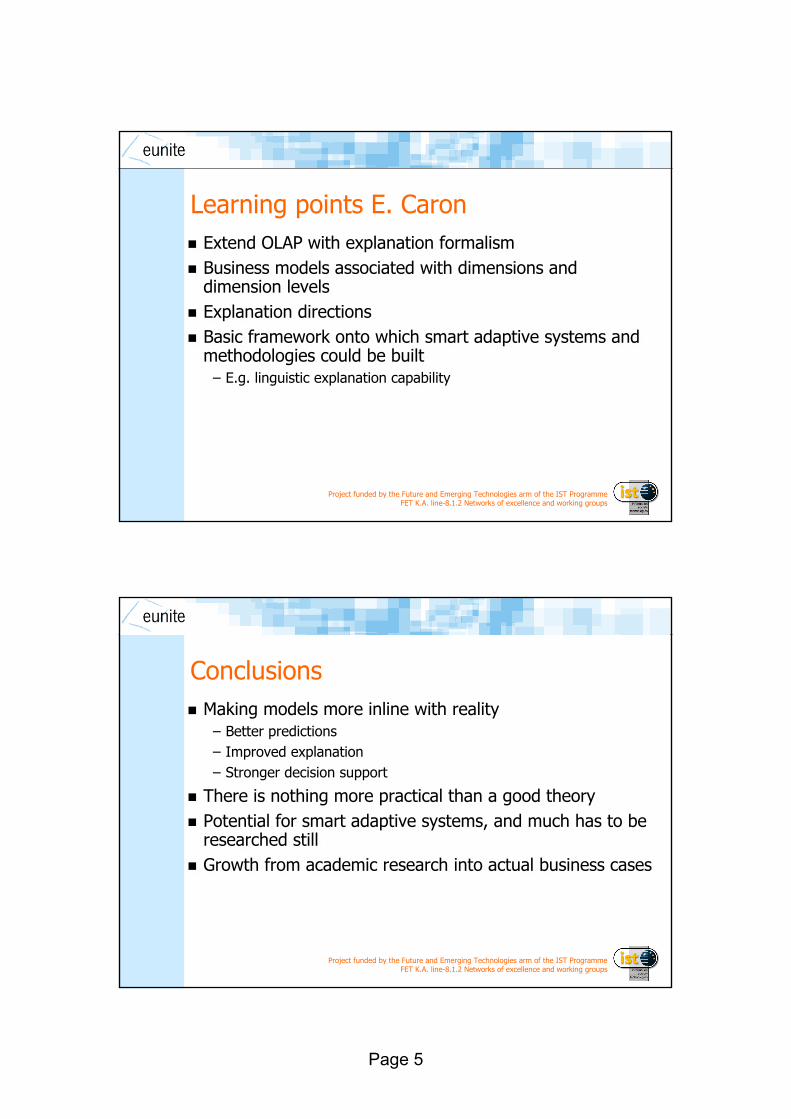

Extending the OLAP framework for the automated diagnosis of business performance

Emiel Caron1 (presenter), Hennie Daniels 1,2

1Erasmus University Rotterdam, ERIM Institute of Advanced Management Studies, PO Box 90153, 3000 DR Rotterdam, The Netherlands, phone +31 010 4082574, e-mail: [email protected]; 2Tilburg University, CentER for Economic Research, Tilburg, The Netherlands

Short abstractThe purpose of OLAP (On-Line Analytical Processing) systems is to provide a framework for the (risk) analysis of multidimensional data. Many tasks related to analysing multidimen-sional data and making business decisions are still carried out manually by analysts (e.g. financial analysts, accountants, or business managers). An important and common task in multidimensional analysis is business diagnosis. Diagnosis is defined as finding the “best” explanation of observed symptoms. Today’s OLAP systems offer little support for automated diagnosis of business performance. This functionality can be provided by extending the conventional OLAP system with an explanation formalism, which mimics the work ofbusiness decision makers in diagnostic processes. The central goal of this presentation is the identification of specific knowledge structures and reasoning methods required to construct computerized explanations from multidimensional data and business models. Recently, an explanation formalism was developed that generates explanations on the basis of simple business models. This explanation formalism serves as a starting point for more complex automated diagnosis in the OLAP framework. We propose an algorithm that generatesexplanations for symptoms in multidimensional business data. The algorithm was tested on a fictitious case study involving the comparison of financial results of a firm’s business units.

OLAP introductionDatabases systems are the core component of OLTP (On-Line Transaction Processing)systems, which support operational business processes. In general, OLTP systems are poorly suited for decision support. Efforts to extract analytical information from OLTP databases result in complex queries, multiple joins, and large computation times. To support business decision-making OLAP is a powerful and adaptive technology. OLAP is defined as “acategory of software technology that enables analysts, managers and executives to gaininsight into data through fast, consistent, interactive access to a wide variety of possible views of information that has been transformed from raw data to reflect the real dimensionality of the enterprise as understood by the user” [3].

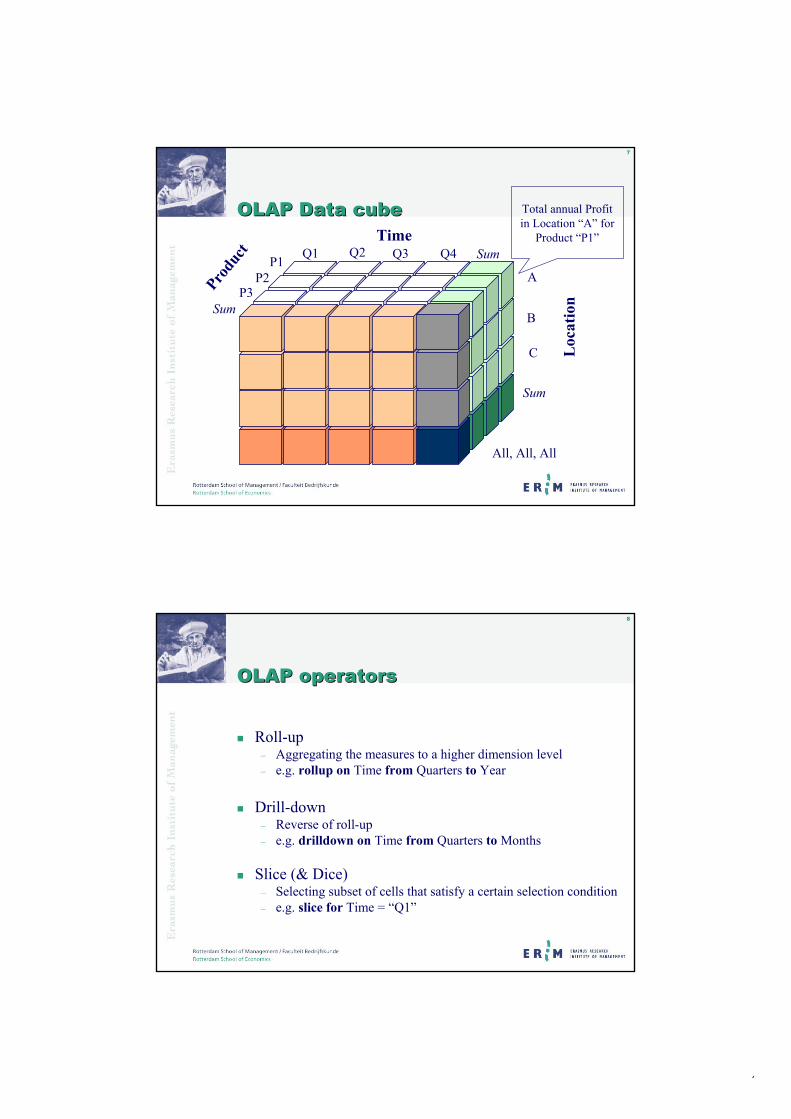

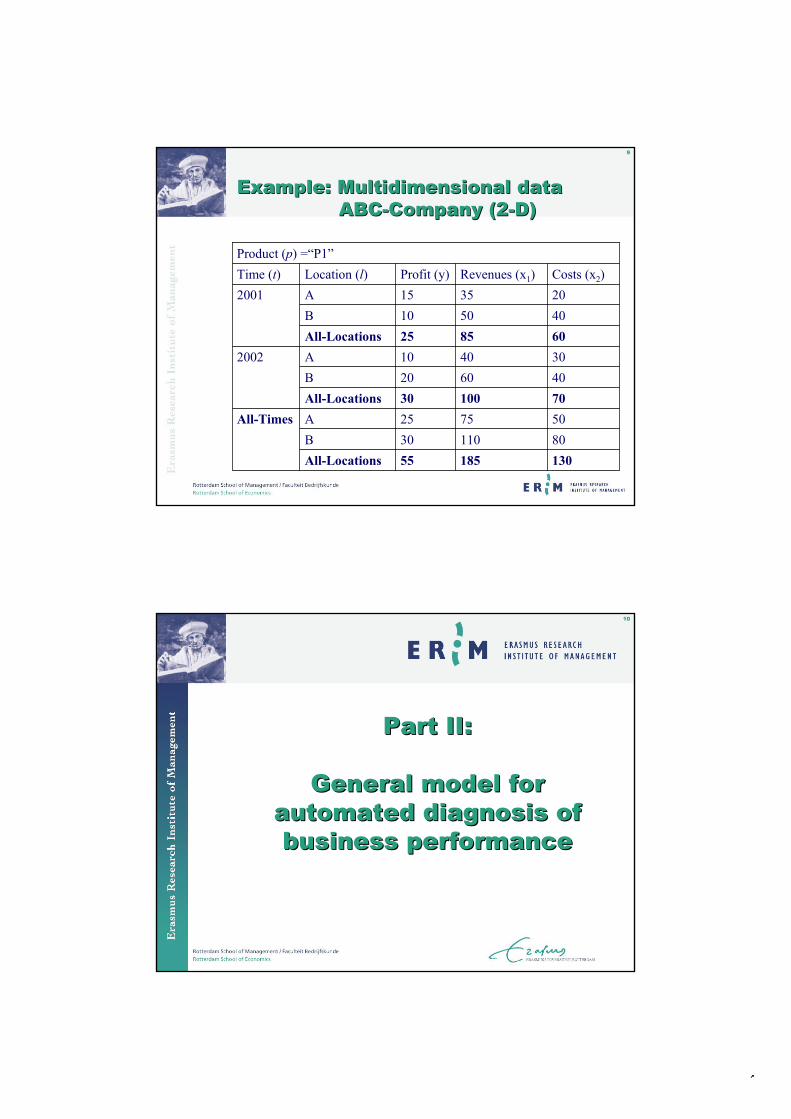

The core component of an OLAP system (or data cube) is the data warehouse, which is decision-support database that is periodically updated by extracting, transforming, and loading data from several OLTP databases. An OLAP system organizes data using the dimensional modelling approach, which classifies data into measures and dimensions.Measures or facts (e.g. sales figures, or costs) are the basic units of interest fo r analysis. Measures represent countable or summable information concerning a business process.Dimensions are the different perspectives for viewing measures. Dimensions are (can be) organised as dimension hierarchies, which offers the possibility to view measures at different dimension levels (e.g. month quarter year≺ ≺ ). The hierarchies in a dimension specify the aggregation levels.

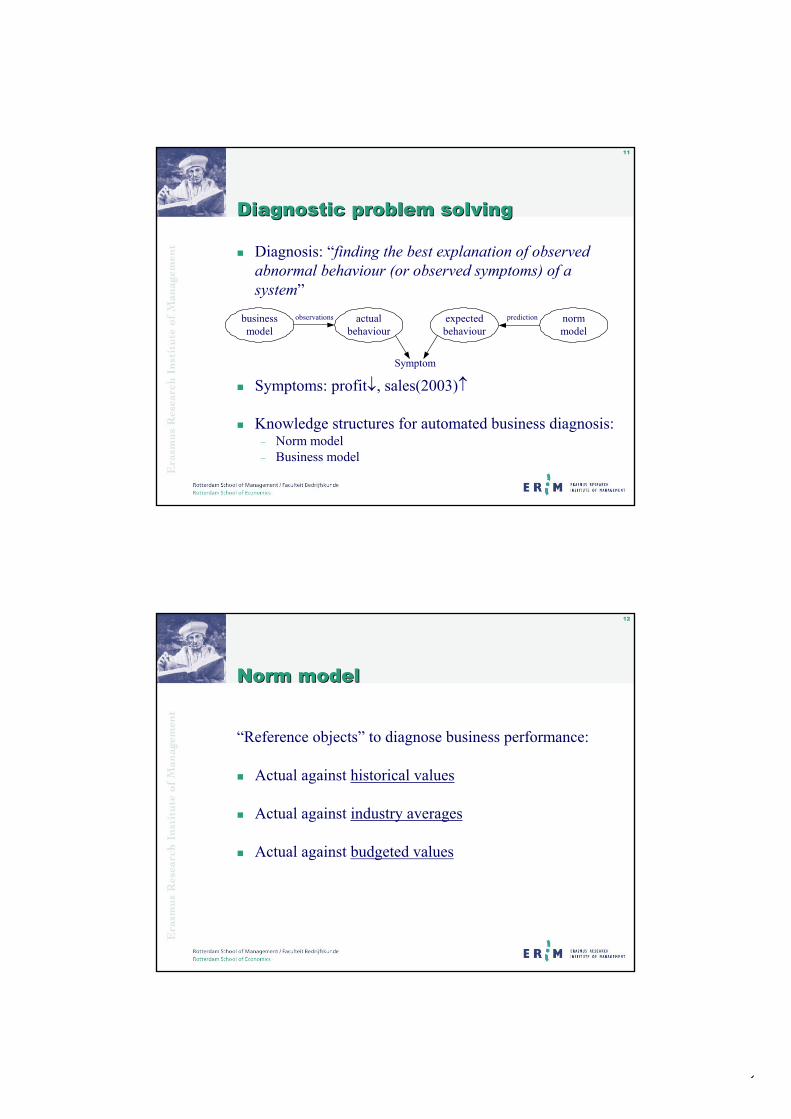

General model for automated diagnosis of business performanceThe formalisation of diagnostic problem-solving is a sub-area of Operations Research (OR) and Artificial Intelligence (AI). In [2] diagnosis is defined as finding the best explanation of

observed abnormal behaviour of a system under study. In this paper we take a model basedrather, as opposed to heuristic classification, approach to knowledge representation. Inaddition we take a causal view of explanation that is able to deal with quantitative phenomena that pervade the domain of business, finance, accounting, and logistics.

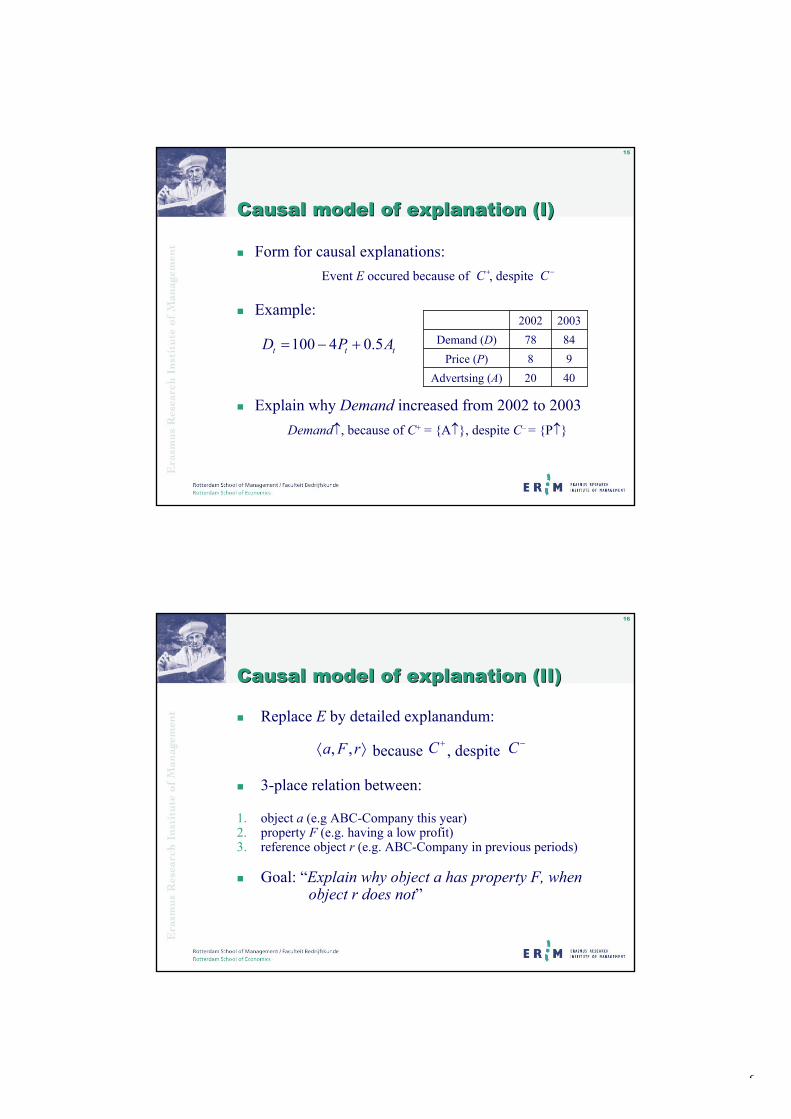

According to a causal model of explanation, phenomena (events) are explained by giving their causes. In this research paper the exposition on diagnostic reasoning and causal explanation is largely based on Feelders and Daniels’ notion of explanations [1, 2], which is again based on Humpreys’ notion of aleatory explanations. Causal influences can appear in two forms: contributing and counteracting. Therefore, Humphreys proposes the following canonical form for causal explanations:

Event E occurred because of C+ , despite C− ,

where E is the event to be explained, C+ is non-empty set of contributing causes, and C− a (possibly empty) set of counteracting causes. The explanation itself consists of the causes to which C+ jointly refers. C− is not part of the explanation of E, but gives a clearer notion of how the members of C+ actually brought about E . The event E can be specified as a variable y changing value from time t to t´.

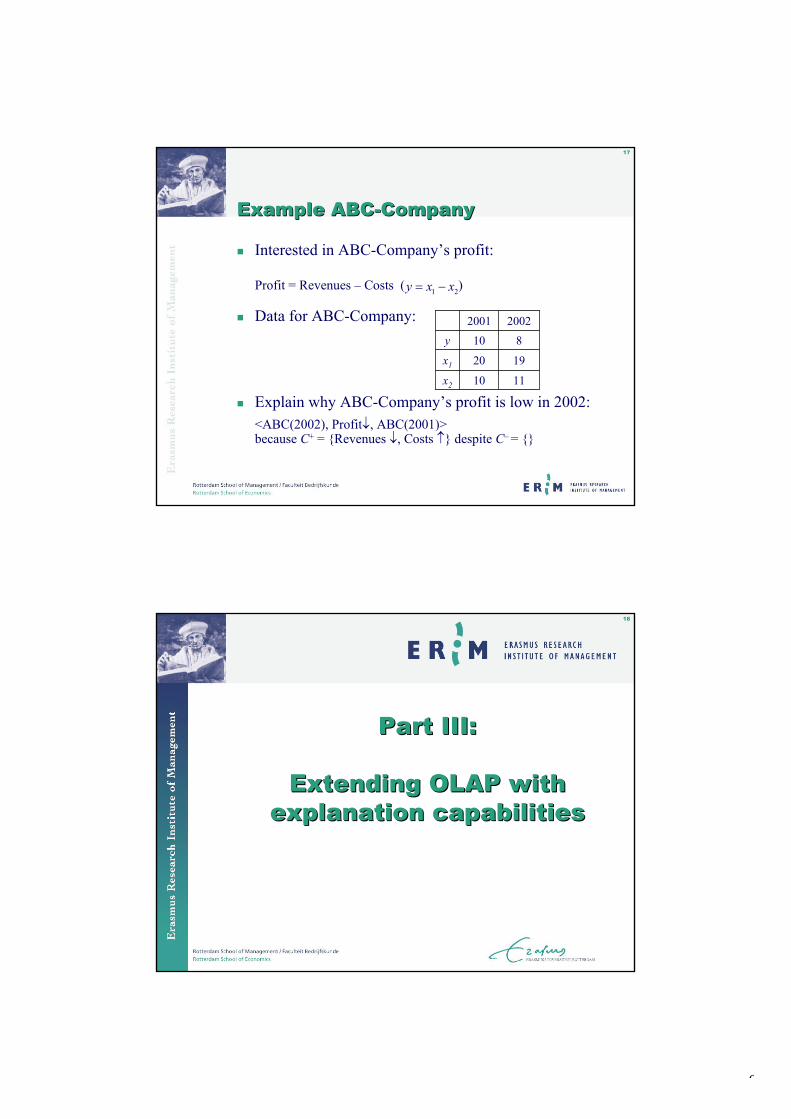

The explanandum introduced by Feelders and Daniels is a three-place relation, ,a F R⟨ ⟩ between an object a (e.g. the ABC-company), a property F (e.g. having a low profit)

and a reference class R (e.g. other companies in the same branch or industry). Here the event E is thus replaced by a more detailed explanandum. The task is not to explain why a has property F, but rather to explain why a has property F when the members of R do not . As we shall see, there are some typical ways to construct reference classes. For the purpose of explanation, the class R can often be reduced to one member r, which is in some sense the average of the class R or the ideal object. The syntax of an explanation reads:

, ,a F r⟨ ⟩ because C+ , despite C− ,

where C+ is a non-empty set of contributing causes, and C− is a (possibly empty) set of counteracting causes.

Two principal knowledge representation structures for diagnosis of business performance are identified:

• Knowledge of general laws expressing relations and variables between events: the businessmodel M. The bus iness model M represents quantitative financial and operating variablesby means of mathematical equations of the form: ( )y f= x where 1( , , )nx x=x … .

• Knowledge of the “normal” behaviour of objects: the norm model (the reference object r).Common “reference objects” for the diagnosis of business performance are, for example,historical norm values, industry averages, or plans and budgets as norm values.

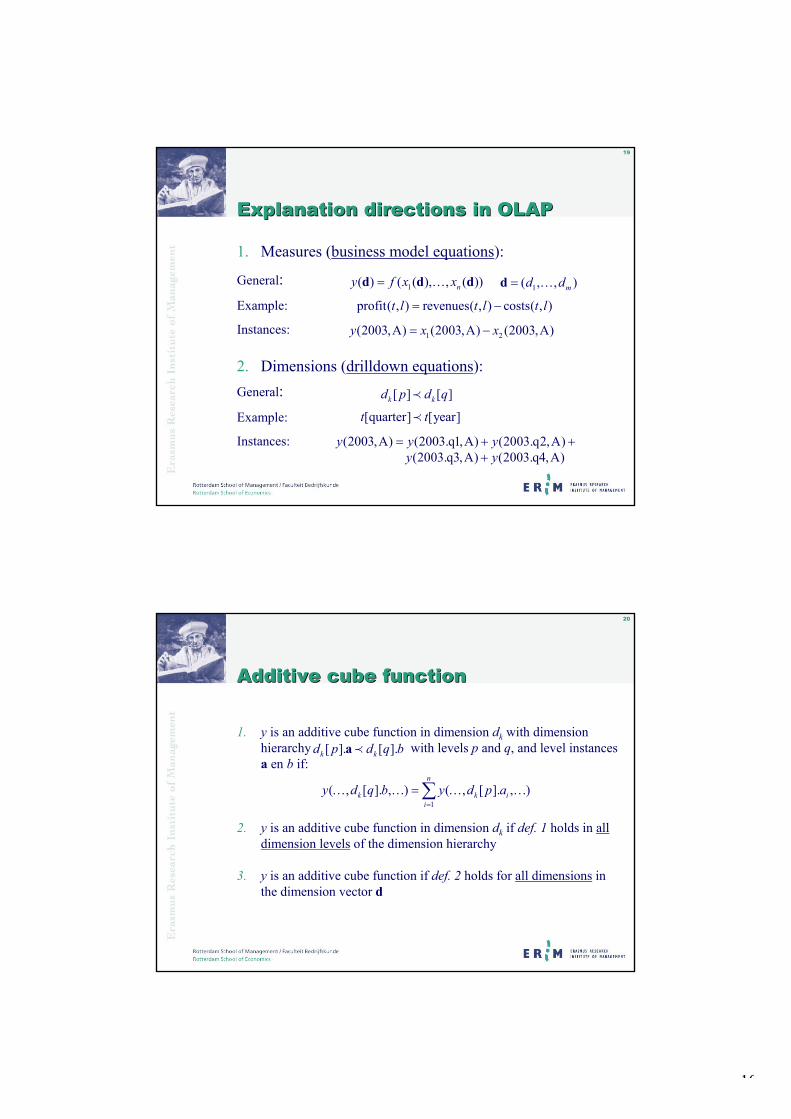

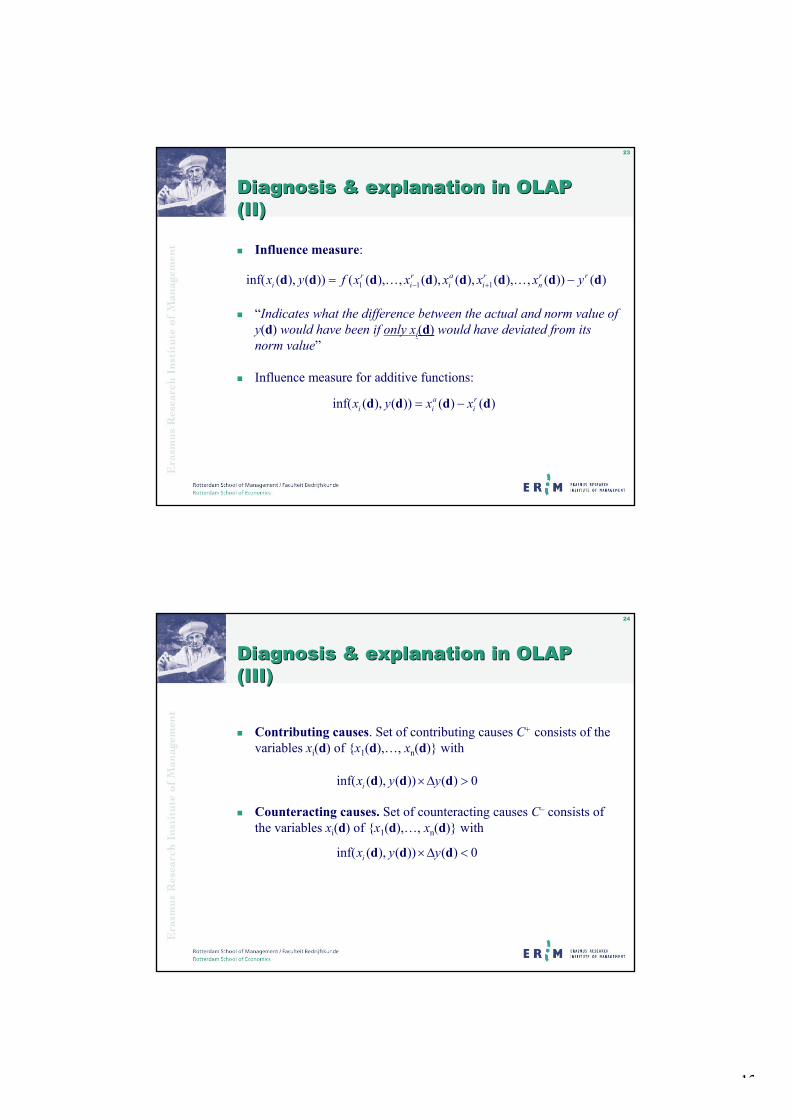

Extending OLAP with explanation capabilities We extend the method of explanation for the purpose of diagnosis of business performancewith explanation capabilities. Or stated differently we adapt the explanation model in such a way that it can deal with multidimensional financial data and can generate explanations for it.In multidimensional data there are two possible explanation directions: namely an explanation direction in the right-hand side of the business model equations (the measures) and anexplanation direction in the right-hand side of the drilldown equations (the dimensions).

To make the connection with the explanation model we have to define the actual object a and the reference object r as multidimensional objects with, for example, a time, location, or product dimension. Therefore, we associate the objects a and the reference objects r of the explanandum with the dimension vector d. In addition, the property F of the explanation model is related to the measure attribute of the multidimensional model. The actual object a(d) in combination with the property F expresses a cell of the data cube that needs to be explained. The property F in combination with the reference model r(d) expresses the cell of reference on the data cube. We are interested in explaining the difference between the actual multidimensional object and a multidimensional reference object. Consequently, we have to explain the following type of events in the data cube:

• a(d) = the actual multidimensional object;• F = a particular measure (variable) deviates from its norm value;• r(d) = the multidimens ional reference object.

We use the idea of progressive deepening in the construction of a maximal explanationalgorithm for multidimensional data. Such an algorithm is needed to create multi- levelexplanations. For diagnostic purposes it is useful to continue an explanation of ( )y q∂ =d

where { }low,highq = , by explaining the qualitative differences between the actual and norm

values of its contributing causes. This process can be continued until a contributing cause is encountered that cannot be explained:

• within the business model, because the business model equations do not contain a relation in which this contributing cause appears on the left-hand side, and

• within the dimensions, because the drilldown equations do not contain a summarization relation in which this contributing cause appears on the left-hand side.

The algorithm was tested on a fictitious case study involving the comparison of financial results of a firm’s business units.

References[1] A.J. Feelders, “Diagnostic reasoning and explanation in financial models of the firm”,

PhD thesis, University of Tilburg, (1993).[2] H.A.M. Daniels, A.J. Feelders, “Theory and methodology: a general model for

automated business diagnosis”, European Journal of Operational Research, 130: 623-637, (2001).

[3] OLAP Council, http://www.olapcounsil.org, (2000).[4] A. Datta, H.Thomas, “The cube data model: a conceptual model and algebra for on-

line analytical processing in data warehouses”, Decision Support Systems, 27 (3): 289-301, (1999).

[5] A. Shoshani, “OLAP and statistical databases: Similarities and differences”, InSixteenth ACM SIGACT SIGMOD SIGART Symp. on Principles of DatabaseSystems, pages 185-196, (1997).

PRESENTATIONS

Page 1

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

2nd Workshop Smart Adaptive Systems in Finance2nd Workshop Smart Adaptive Systems in Finance

Focus: Intelligent Risk Analysis & Management

19 May 2004

Erasmus University RotterdamThe Netherlands

Supported by

Focus: Intelligent Risk Analysis & Management

19 May 2004

Erasmus University RotterdamThe Netherlands

Supported by

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

AgendaEUNITESIKSFirst WorkshopProgram of Today

EUNITESIKSFirst WorkshopProgram of Today

Page 2

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

the European Network of Excellence on Intelligent Technologies for

Smart Adaptive Systems

the European Network of Excellence on Intelligent Technologies for

Smart Adaptive Systems

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

IntroductionOn 1 January 2001, EUNITE - the European Network of Excellence on Intelligent Technologies for Smart Adaptive Systems - has started.

It is funded by the Future and Emerging Technologies arm of the IST Programme FET K.A. line-8.1.2 Networks of excellence and working groups

On 1 January 2001, EUNITE - the European Network of Excellence on Intelligent Technologies for Smart Adaptive Systems - has started.

It is funded by the Future and Emerging Technologies arm of the IST Programme FET K.A. line-8.1.2 Networks of excellence and working groups

Page 3

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Aimsto join forces within the area of Intelligent Technologies(i.e. neural networks, fuzzy systems, methods from machine learning, and evolutionary computing) for better understanding of the potential of hybrid systems and to provide guidelines for exploiting their practical implementationsand particularly,to foster synergies that contribute towards building Smart Adaptive Systems implemented in industry as well as in other sectors of the economy

to join forces within the area of Intelligent Technologies(i.e. neural networks, fuzzy systems, methods from machine learning, and evolutionary computing) for better understanding of the potential of hybrid systems and to provide guidelines for exploiting their practical implementationsand particularly,to foster synergies that contribute towards building Smart Adaptive Systems implemented in industry as well as in other sectors of the economy

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Integration of Intelligent TechnologiesIntelligent Hybrid Systems: Combinations of Intelligent Technologies (e.g. neuro-fuzzy, evolutionary optimised networks, etc.)

– common in theory and experimentation and less in the applicationfield

• need for guidelines regarding design, testing and assessment • need for improved understanding of the fundamental nature of

engineering systems with embedded hybrid intelligence

Can they contribute and improve adaptivity?

Intelligent Hybrid Systems: Combinations of Intelligent Technologies (e.g. neuro-fuzzy, evolutionary optimised networks, etc.)

– common in theory and experimentation and less in the applicationfield

• need for guidelines regarding design, testing and assessment • need for improved understanding of the fundamental nature of

engineering systems with embedded hybrid intelligence

Can they contribute and improve adaptivity?

Page 4

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Smart Adaptive SystemsAdaptivity:

A system is adaptive if it can adequately perform even in non-stationary environments, where significant smooth changes of themain data characteristics can be manifested (robustness)

Examples:control of communication systems under changing physical conditionschanging customer preferences in an e-business environmentmedical diagnostic systems in the presence of a changing populationforecasting of dynamically changing time series

Adaptivity is also a request in the sense of portability and reusabilityas minimises the effort for re-development

Example:a financial analysis' tool developed for the European financial world can also be applied for financial markets in Asian countries

Adaptivity:A system is adaptive if it can adequately perform even in non-stationary environments, where significant smooth changes of themain data characteristics can be manifested (robustness)

Examples:control of communication systems under changing physical conditionschanging customer preferences in an e-business environmentmedical diagnostic systems in the presence of a changing populationforecasting of dynamically changing time series

Adaptivity is also a request in the sense of portability and reusabilityas minimises the effort for re-development

Example:a financial analysis' tool developed for the European financial world can also be applied for financial markets in Asian countries

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Network of Excellence

A network of institutions (universities, companies, research departments) competent and interested in a research areaThe European Commission is aiming to bring together industry and scientists and produce added value by exchanging ideas

A network of institutions (universities, companies, research departments) competent and interested in a research areaThe European Commission is aiming to bring together industry and scientists and produce added value by exchanging ideas

Page 5

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Steering CommitteeScientific Manager

2 RTD chairpersons2 TTE chairpersons5 IBA chairpersonsSC administrator

IBAIndustrial & Business

Application

IBA A: Production IndustryIBA B: Transportation

IBA C: Telecommunication & Multimedia

IBA D: Human, Medical & HealthcareIBA E: Finance, Trade & Services

Service CenterAdministrator

SecretaryWeb assistant

NODES

RTDResearch Theory &

Development

RTD SAS: Smart Adaptive SystemsRTD IM: Integration of Methods

Knowledge Transfer TT: Technology TransferTE: Training & Education

Structure

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

More information on EUNITE's activitiesEUNITE Service Centerc/o ELITE FoundationPascalstr. 6952076 AachenGermanyTel.: +49 (0)2408 6969Fax: +49 (0)2408 9458-199Email: [email protected]

EUNITE Service Centerc/o ELITE FoundationPascalstr. 6952076 AachenGermanyTel.: +49 (0)2408 6969Fax: +49 (0)2408 9458-199Email: [email protected]

Page 6

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

AgendaEUNITESIKSFirst WorkshopProgram of Today

EUNITESIKSFirst WorkshopProgram of Today

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

SIKSSIKS is the Dutch Research School for Information and Knowledge systems. It was founded in 1996 by researchers in the field of Artificial Intelligence, Databases & Information Systems and Software Engineering SIKS is an interuniversity research school that comprises 12 research groups in which currently over 270 researchers are active, including 120 Ph.D-studentsIt's Administrative University is the Free University of Amsterdam. The office of SIKS is located at Utrecht University. SIKS received its accreditation by KNAW in 1998In June 2003 SIKS was re-accreditated by KNAW for a period of 6 years.

SIKS is the Dutch Research School for Information and Knowledge systems. It was founded in 1996 by researchers in the field of Artificial Intelligence, Databases & Information Systems and Software Engineering SIKS is an interuniversity research school that comprises 12 research groups in which currently over 270 researchers are active, including 120 Ph.D-studentsIt's Administrative University is the Free University of Amsterdam. The office of SIKS is located at Utrecht University. SIKS received its accreditation by KNAW in 1998In June 2003 SIKS was re-accreditated by KNAW for a period of 6 years.

Page 7

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Scientific mission of SIKSto perform high-level fundamental and applied research inthe field of information and computing science, more particularly in the field of information and knowledge systemsto organise a high-quality four-year educational programfor its Ph.D. students, employed at 10 different Universities in the Netherlands or at leading companies in the field of ICT to facilitate and stimulate co-operation and communication between our members (Ph.D. students, research fellows, senior research fellows and associated members) and between the School and its stakeholders, including leading (industrial) companies in the field of ICT

to perform high-level fundamental and applied research inthe field of information and computing science, more particularly in the field of information and knowledge systemsto organise a high-quality four-year educational programfor its Ph.D. students, employed at 10 different Universities in the Netherlands or at leading companies in the field of ICT to facilitate and stimulate co-operation and communication between our members (Ph.D. students, research fellows, senior research fellows and associated members) and between the School and its stakeholders, including leading (industrial) companies in the field of ICT

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

New research fociAgent technology Computational Intelligence Knowledge Representation and Reasoning Web-based information systems E-business systems Human computer interaction Data management, storage and retrieval Architecture-driven system development

Agent technology Computational Intelligence Knowledge Representation and Reasoning Web-based information systems E-business systems Human computer interaction Data management, storage and retrieval Architecture-driven system development

Page 8

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

More information on SIKS

Address:

SIKSUtrecht UniversityInstitute for information and computing sciencesP. O. Box 80.0893508 TB Utrecht

Phone: +30-253-4083/1454

Fax: +30-251-3791

Email address: [email protected] site: http://www.siks.nl/

Address:

SIKSUtrecht UniversityInstitute for information and computing sciencesP. O. Box 80.0893508 TB Utrecht

Phone: +30-253-4083/1454

Fax: +30-251-3791

Email address: [email protected] site: http://www.siks.nl/

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

AgendaEUNITESIKSFirst WorkshopProgram of Today

EUNITESIKSFirst WorkshopProgram of Today

Page 9

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

First workshopFinance in generalAmsterdam, 15 November 2002Proceedings on the web

Finance in generalAmsterdam, 15 November 2002Proceedings on the web

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

AgendaEUNITESIKSFirst WorkshopProgram of Today

EUNITESIKSFirst WorkshopProgram of Today

Page 10

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

Project funded by the Future and Emerging Technologies arm of the IST ProgrammeFET K.A. line-8.1.2 Networks of excellence and working groups

ProgramShow pdf file…

Focus on Intelligent Risk Analysis & Management– statistical approaches (including the Bayesian approach)– machine learning approach (decision tree)– genetic algorithms – fuzzy logic

Other contributions using techniques from informatics– OLAP– agent-based systems

Show pdf file…

Focus on Intelligent Risk Analysis & Management– statistical approaches (including the Bayesian approach)– machine learning approach (decision tree)– genetic algorithms – fuzzy logic

Other contributions using techniques from informatics– OLAP– agent-based systems

1

Financial Risk Analysis & Management :

An Overview

Winfried G. Hallerbach

EUNITE – May 19, 2004

intelligent risk analysis & management in finance

W.G. Hallerbach 2

outline

• risk management framework

• model risk

• cognitive biases in DM under uncertainty

• decision context & performance evaluation

2

W.G. Hallerbach 3

risk management process

1. risk analysis

2. risk policy

3. implementation

4. performance evaluation

feedback

W.G. Hallerbach 4

risk analysis : risk categories

• market risks

• credit risks

• operational risks :

hardware : system / organization / technology

software : processes / procedures

wetware : control / audit / feedback / learning

( external catastrophic events )

3

W.G. Hallerbach 5

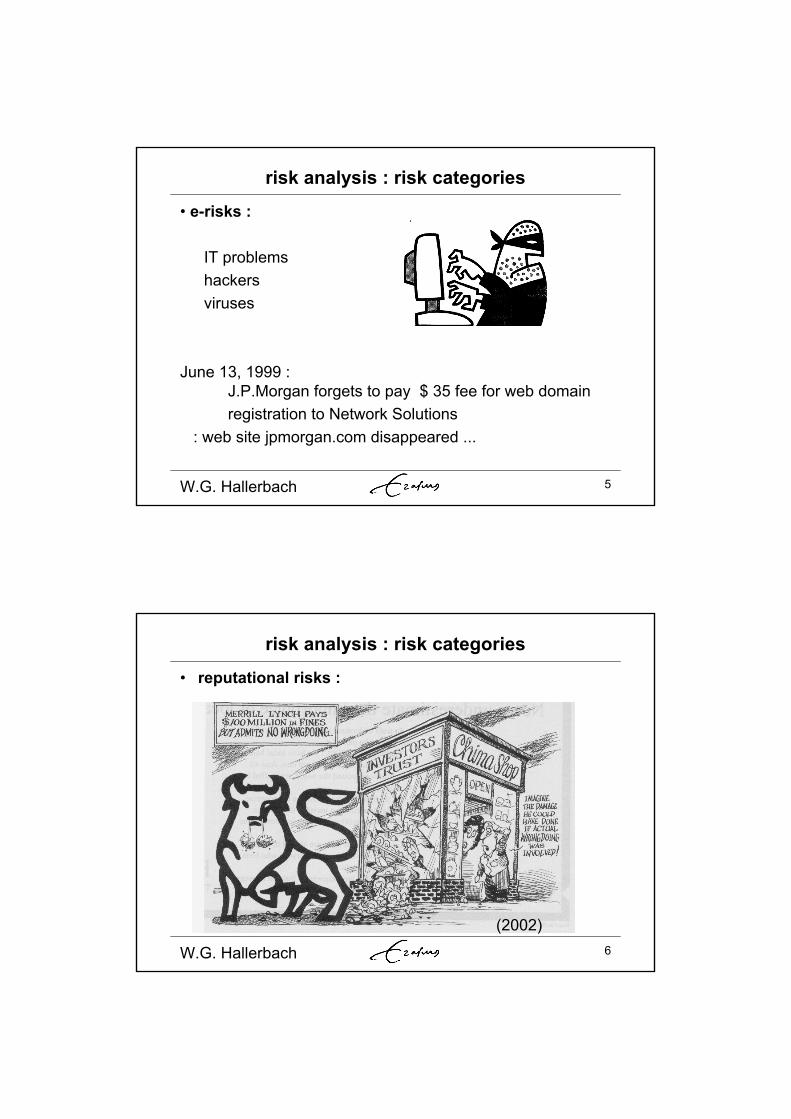

risk analysis : risk categories

• e-risks :

IT problemshackersviruses

June 13, 1999 : J.P.Morgan forgets to pay $ 35 fee for web domainregistration to Network Solutions

: web site jpmorgan.com disappeared ...

W.G. Hallerbach 6

risk analysis : risk categories

• reputational risks :

(2002)

4

W.G. Hallerbach 7

risk analysis : risk categories

• systemic risk : “financial flutter”

agency problem

moral hazard :

“lender of last resort”“too big to fail”

W.G. Hallerbach 8

risk analysis : exposure types

• transaction / tactical• economic / strategic

/ competitive

• translation

• expected• contingent• maximum

5

W.G. Hallerbach 9

risk analysis : exposure awareness (1)

W.G. Hallerbach 10

risk analysis : exposure awareness (2)

6

W.G. Hallerbach 11

risk policy

• horizon

• risk – return trade-off :

- RAROC- is risk manager biggest enemy of commercial manager ?

• “economic hedging” vs entrepreneurship

• “views” selective hedging

W.G. Hallerbach 12

diversification

7

W.G. Hallerbach 13

enterprise-wide risk management

macro view :

• netting exposures : ICT challenge

• portfolio effect : econometric challenge

• overall risk-return trade-off

• contribution to RAROC :ex anteex post

W.G. Hallerbach 14

downside & upside

upside potential vs downside risk :in Chinese :

risk :

danger opportunity

• only riskfree rate is riskfree

• profit opportunities are risky ventures

8

W.G. Hallerbach 15

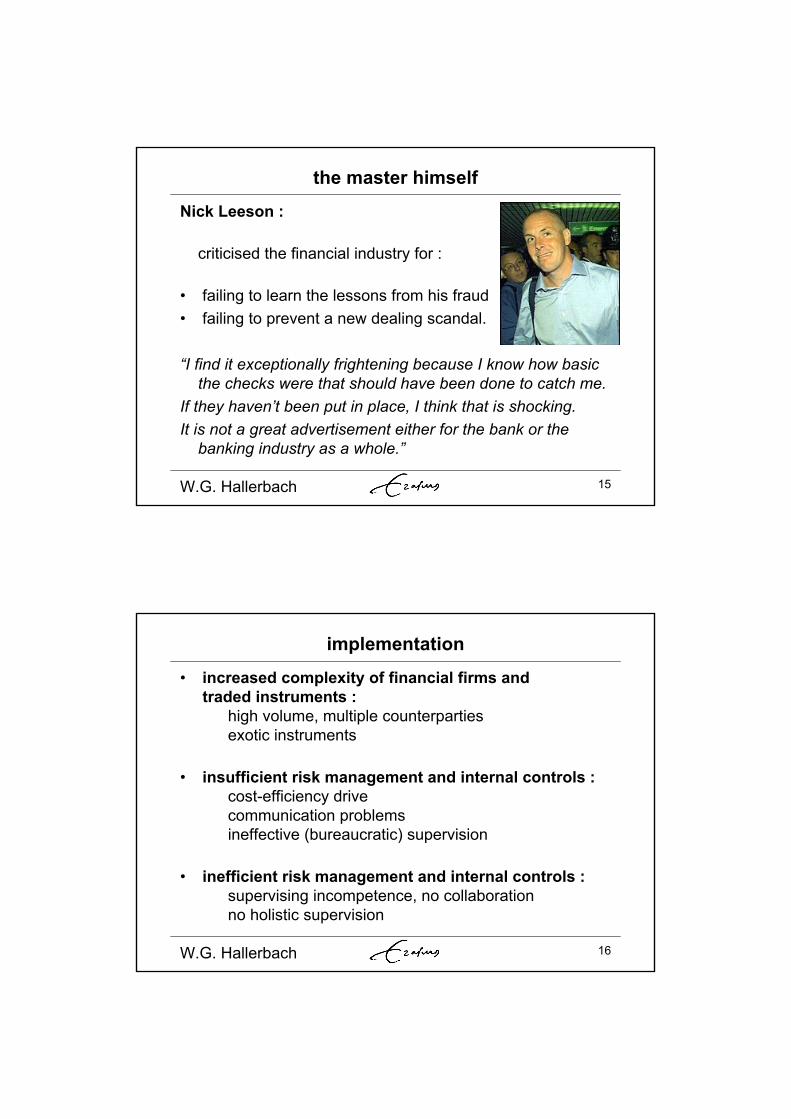

the master himself

Nick Leeson :

criticised the financial industry for :

• failing to learn the lessons from his fraud• failing to prevent a new dealing scandal.

“I find it exceptionally frightening because I know how basic the checks were that should have been done to catch me.

If they haven’t been put in place, I think that is shocking. It is not a great advertisement either for the bank or the

banking industry as a whole.”

W.G. Hallerbach 16

implementation

• increased complexity of financial firms and traded instruments :

high volume, multiple counterpartiesexotic instruments

• insufficient risk management and internal controls :cost-efficiency drivecommunication problemsineffective (bureaucratic) supervision

• inefficient risk management and internal controls :supervising incompetence, no collaborationno holistic supervision

9

W.G. Hallerbach 17

implementation

• collusion :inadequate / no separation of

functional responsibilities (front office – back office)

cover-up (protect reputation)

• agency problem :incentive system

2002 :

W.G. Hallerbach 18

communication

10

W.G. Hallerbach 19

outline

• risk management framework

• model risk

• cognitive biases in DM under uncertainty

• decision context & performance evaluation

W.G. Hallerbach 20

model risk

Emanuel Derman : “In physics, you’re playing against God; in finance, you’re playing against people.”

11

W.G. Hallerbach 21

model risk

models used for : • valuation : “mark-to-model” i.s.o. mark-to-market• risk analysis

model risk :• wrong input data : volatility• wrong parameter estimates• wrong / incomplete model• wrong implementation

garbage in – garbage out (NatWest, UBS)

W.G. Hallerbach 22

low fat modeling

no hairy hypotheses,

but

shave with Occam’s razor :

principle of parsimony

12

W.G. Hallerbach 23

Better roughly right, than exactly wrong

“The mathematics of models may be precise, but the models by definition are not…”

(Robert Merton, 1995)

“… particularly in the field of finance, what is needed are approximate answers to the precise problem rather than precise answers to the approximate problem.

(K.L. Hastie, 1982)

W.G. Hallerbach 24

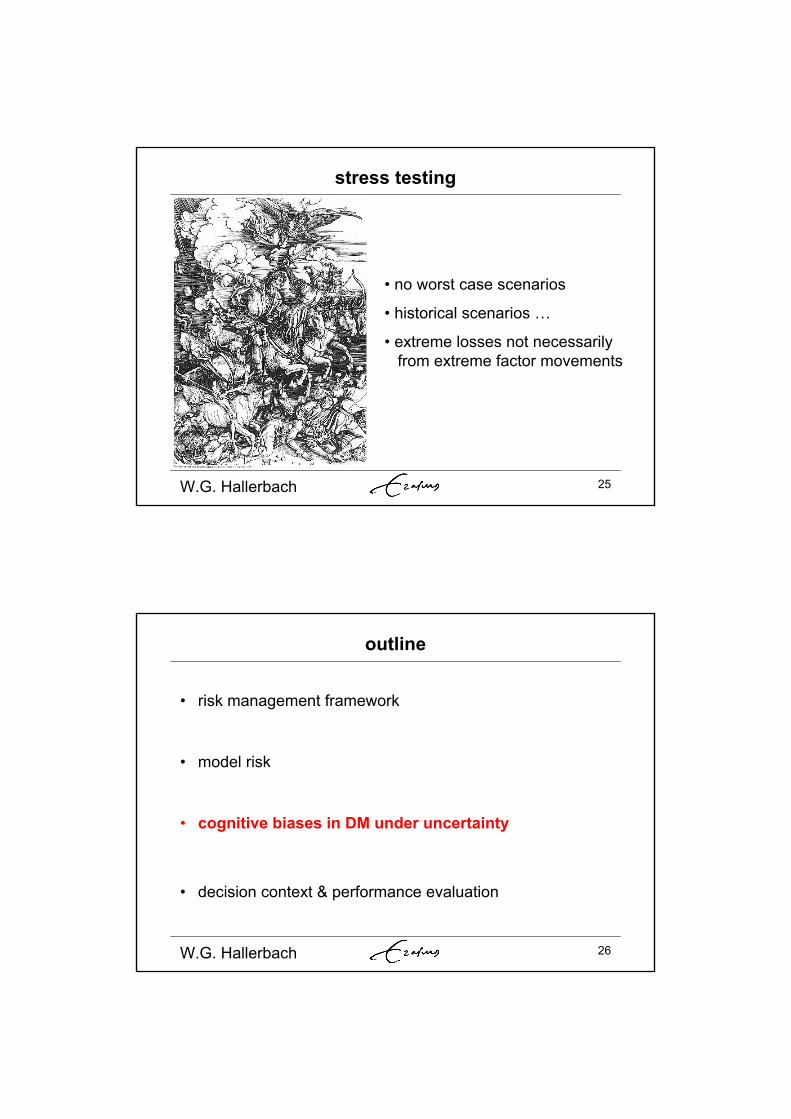

search for the Holy Scale

• speed versus accuracy • procedure risk (Beder, FAJ

1995)

• estimation risk

13

W.G. Hallerbach 25

stress testing

• no worst case scenarios

• historical scenarios …

• extreme losses not necessarily from extreme factor movements

W.G. Hallerbach 26

outline

• risk management framework

• model risk

• cognitive biases in DM under uncertainty

• decision context & performance evaluation

14

W.G. Hallerbach 27

behavioral aspects

decision-making under uncertainty :

perceptions preferences

action

• rules of thumb i.s.o. rigorous algorithms• form ànd substance of choice alternatives

W.G. Hallerbach 28

behavioral finance

The Bank of Sweden Prize in Economic Sciences in Memory of Alfred Nobel 2002

Daniel KahnemanPrinceton University, Princeton, NJ, USA b. 1934

“for having integrated insights from psychological research into economic science, especially concerning human judgment and decision-making under uncertainty”

15

W.G. Hallerbach 29

preferences : risk attitude

reference point : current (financial) situation is anchoragainst

which profit / loss is evaluated :

0 : € 100 1a : € 100

1b : € 0 50%€ 200 50%

0 : € 200 1a : € 100

1b : € 0 50%€ 200 50%

loss avoidance implies risk seeking behaviorin loss situations

W.G. Hallerbach 30

preferences : risk attitude

risk attitude even depends on context : different attitude when only formulated differently : framing :

loss :either sure 25% : 200 loss

loss of 50 òr 75% : 0 loss

cost :pay insurance

premium 50 to avoid 25% : 200 loss75% : 0 loss

16

W.G. Hallerbach 31

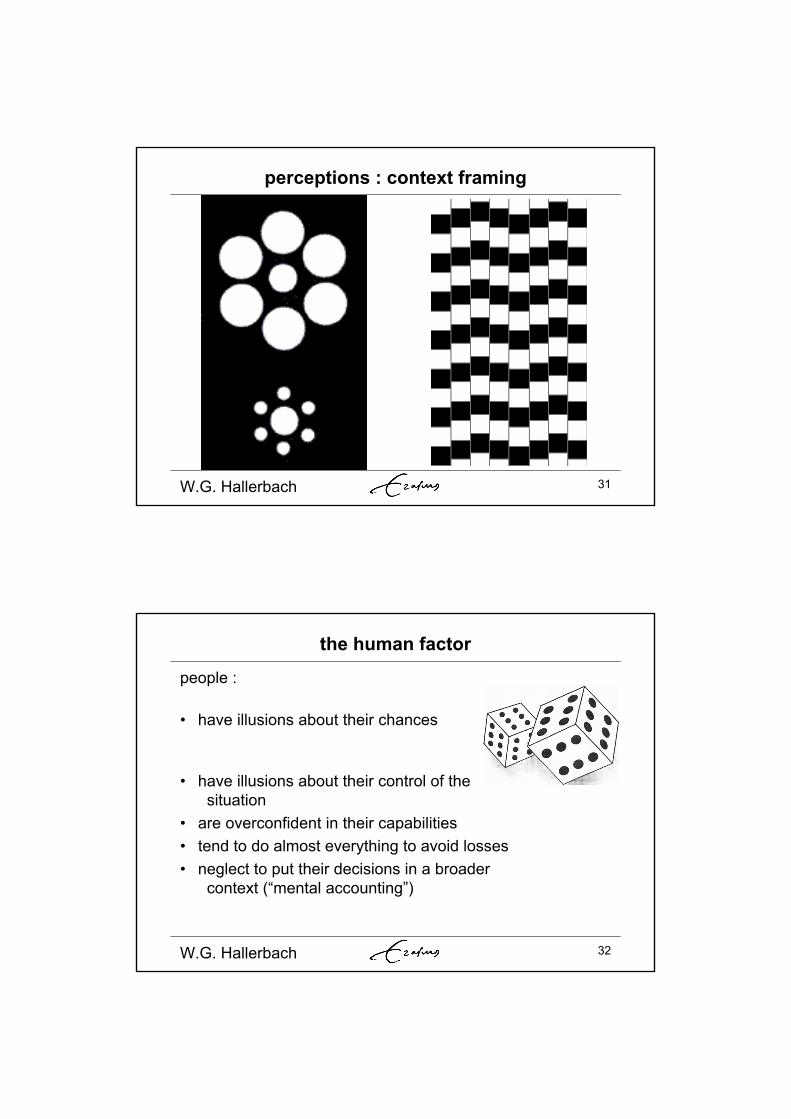

perceptions : context framing

W.G. Hallerbach 32

the human factor

people :

• have illusions about their chances

• have illusions about their control of thesituation

• are overconfident in their capabilities• tend to do almost everything to avoid losses• neglect to put their decisions in a broader

context (“mental accounting”)

17

W.G. Hallerbach 33

learning

Good judgment comes from experience. Experience comes from bad judgment.

(Walter Wriston, banker)

W.G. Hallerbach 34

outline

• risk management framework

• model risk

• cognitive biases in DM under uncertainty

• decision context & performance evaluation

18

W.G. Hallerbach 35

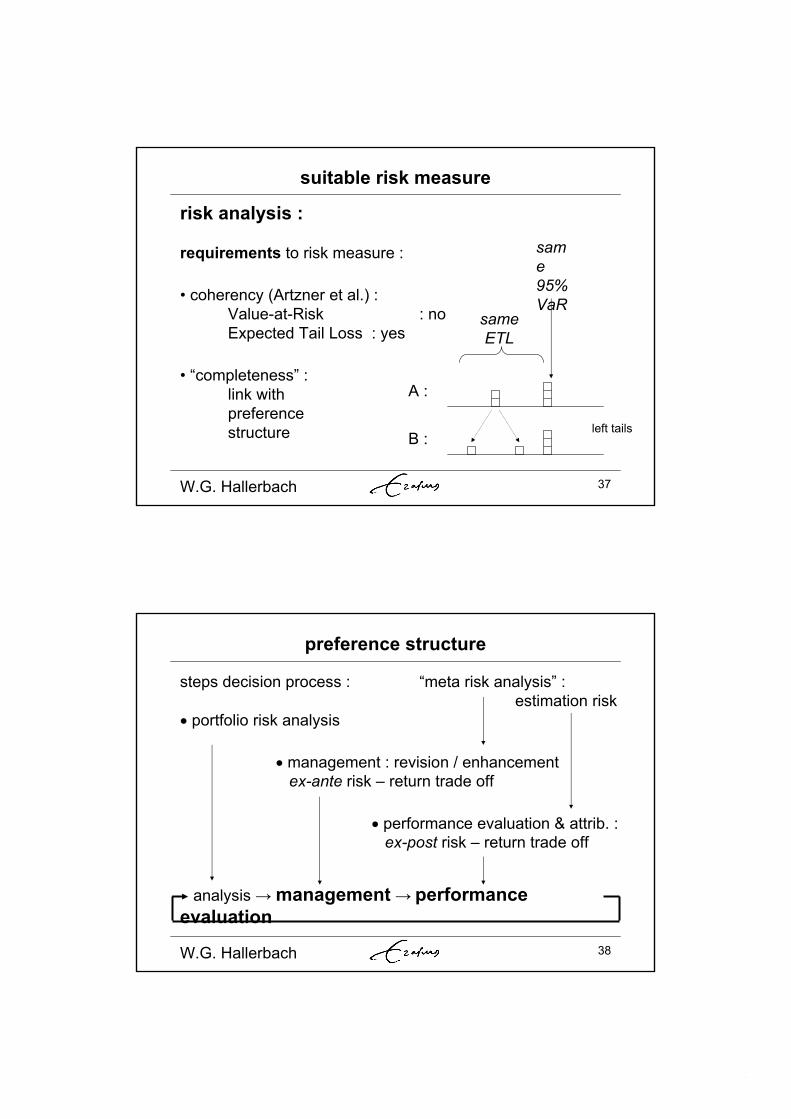

scrabble

EC W

V a R RR A P M

ROC

W.G. Hallerbach 36

“beyond” portfolio risk

risk analysis : • aggregate risk measures :

Value-at-Risk, Expected Tail Loss (Tail-VaR)

• component risk contribution : “hot spots”

• marginal risk contribution : portfolio revision

risk analysis ánd risk management( The Journal of Risk, 2002

)

19

W.G. Hallerbach 37

suitable risk measure

risk analysis :

requirements to risk measure :

• coherency (Artzner et al.) :Value-at-Risk : noExpected Tail Loss : yes

• “completeness” : link with preferencestructure

same95%VaR

sameETL

A :

B :left tails

W.G. Hallerbach 38

preference structure

steps decision process : “meta risk analysis” : estimation risk

portfolio risk analysis

management : revision / enhancementex-ante risk – return trade off