Embed Size (px)

Citation preview

Income © Ted Whitmer, All Rights Reserved.

67"

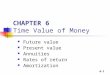

Problems

! Amortization of Tenant Finish ! Natural Break Point ! Modified Internal Rate of Return ! Value of Office ! Value of Retail ! Value of Industrial ! Partition the IRR ! Partial Interests ! Calculate Ye ! Wraparound Mortgages ! GIM vs. NIR in graph form

Amortization of Tenant Finish ! A lease is quoted at $20 PSF annually with a $10 PSF

Tenant improvement allowance. What is the equivalent rent on a 7 year lease if the tenant gets a $25 PSF tenant improvement allowance? Compute the monthly rate with a yield requirement of 9%.

! Add the .24 to 20/12 = $1.91 PSF per month

Step N I PV PMT FV

Calculate the PMT to amortize the excess TI

7 x 12 9/12 25 – 10 = 15 [.24]

Income © Ted Whitmer, All Rights Reserved.

68"

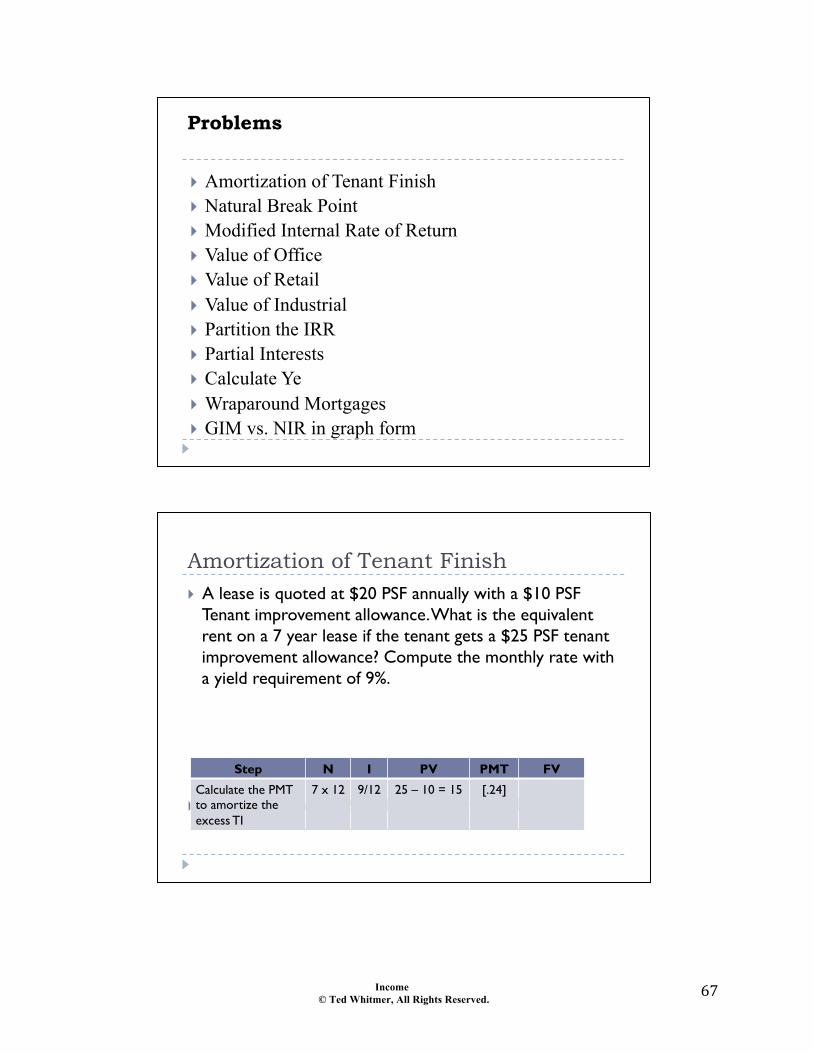

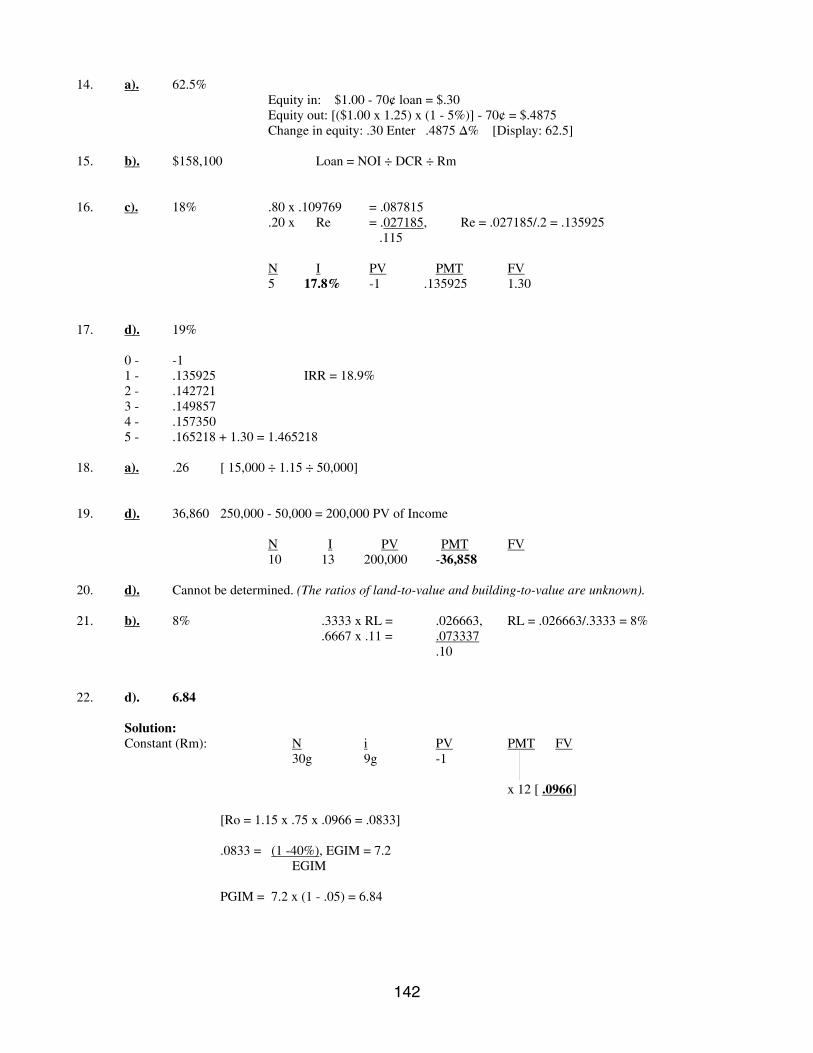

Amortization of Tenant Finish ! A lease is quoted at $20 PSF annually with a $10 PSF Tenant

improvement allowance. What is the equivalent rent on a 7 year lease if the tenant gets a $25 PSF tenant improvement allowance? Compute the monthly rate with a yield requirement of 9%. Now assume there is a 20% residual value in the excess tenant improvements at the end of the lease.

Step N I PV PMT FV

Calculate the PMT to amortize the excess TI

Amortization of Tenant Finish ! A lease is quoted at $20 PSF annually with a $10 PSF Tenant

improvement allowance. What is the equivalent rent on a 7 year lease if the tenant gets a $25 PSF tenant improvement allowance? Compute the monthly rate with a yield requirement of 9%. Now assume there is a 20% residual value in the excess tenant improvements at the end of the lease.

! Add the .22 to 20/12 = $1.87 PSF per month

Step N I PV PMT FV

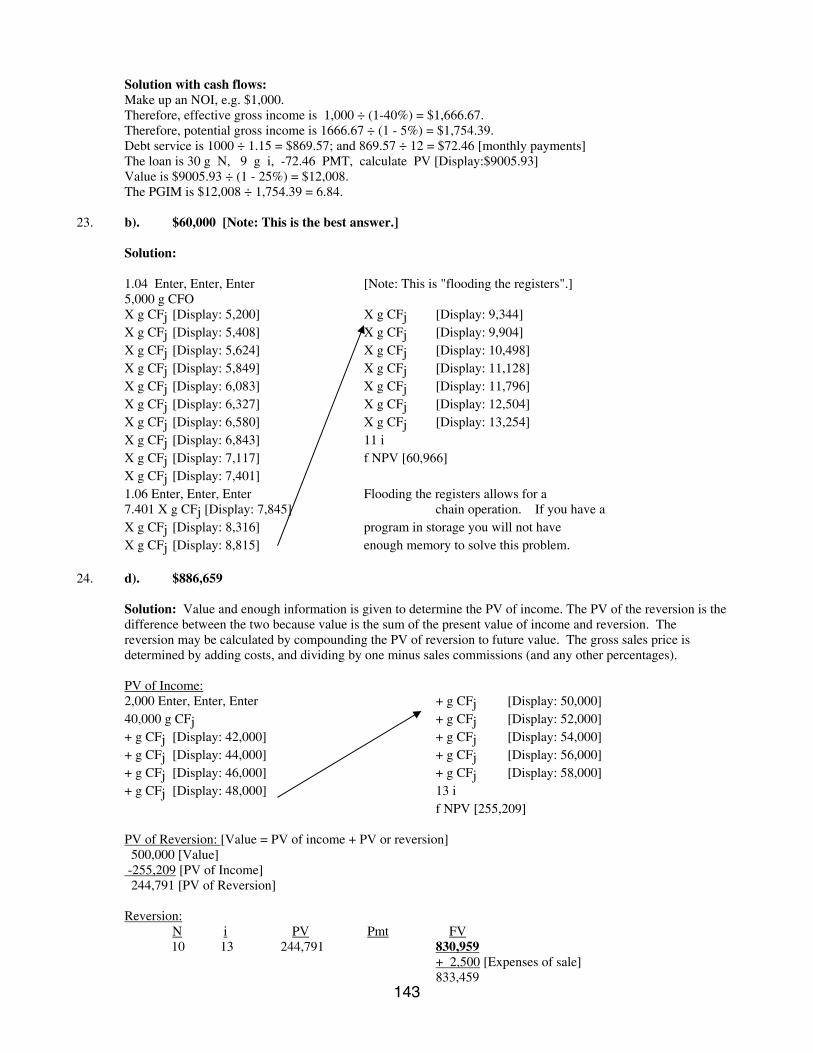

Calculate the PMT to amortize the excess TI

7 x 12 9/12 25 – 10 = -$15 [.22] 15 x 20% = $3

Income © Ted Whitmer, All Rights Reserved.

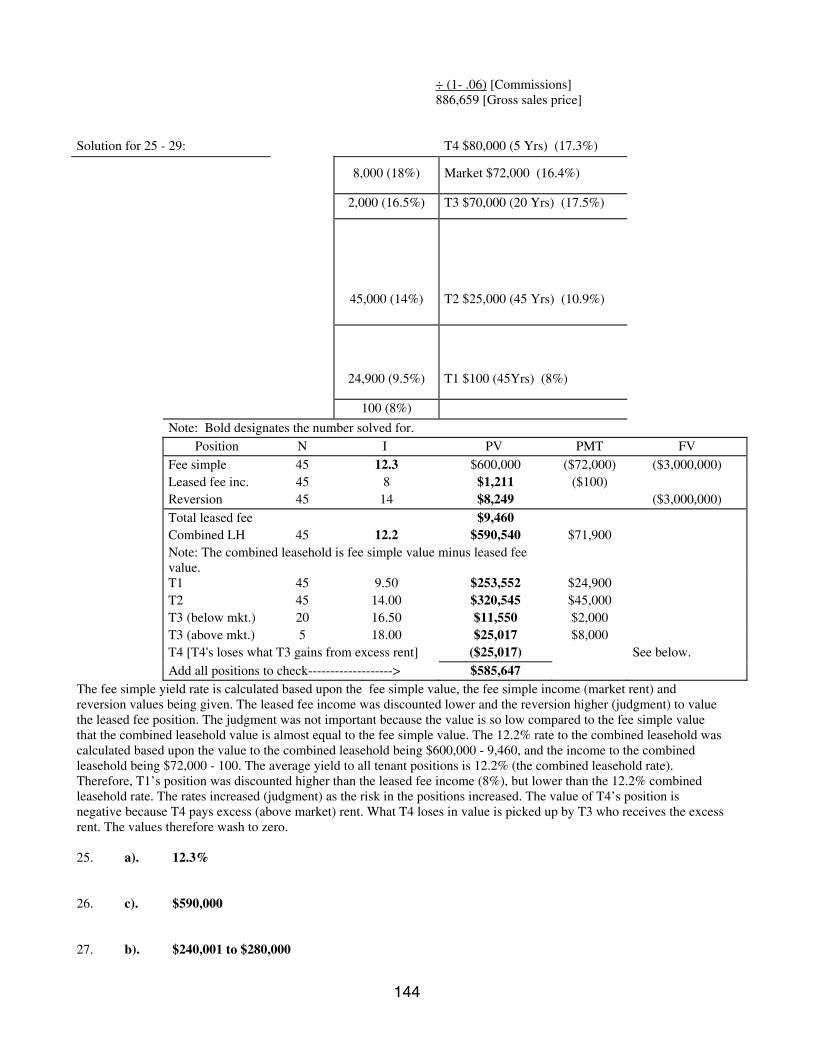

69"

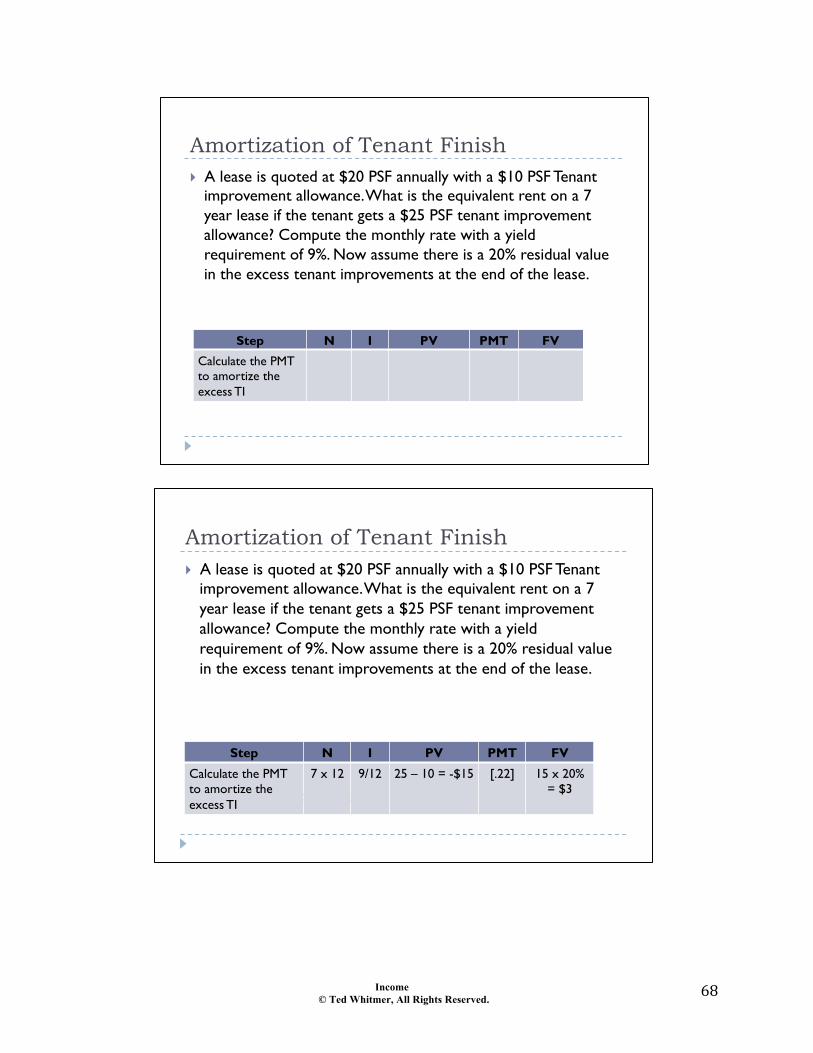

Natural Break Point ! What is the natural break point (a sales volume where

percentage rents begin) when the percentage rent is 6% and the base rent is $24,000/year?

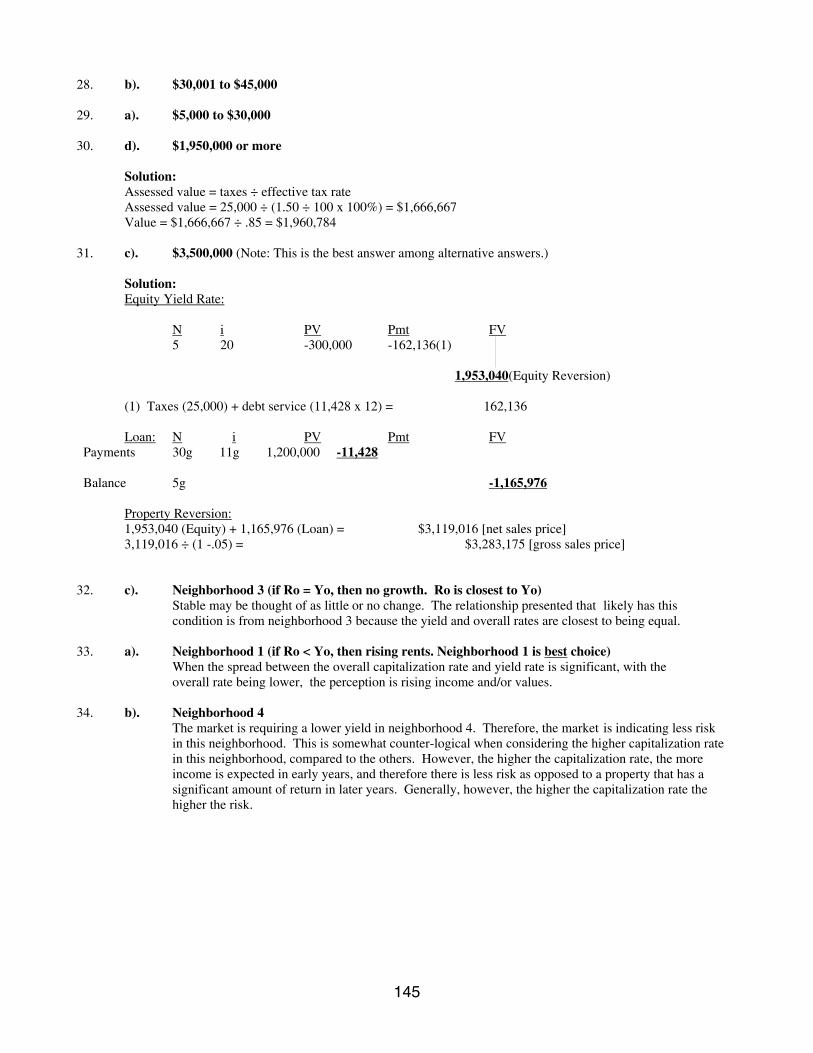

Natural Break Point

! What is the natural break point (a sales volume where percentage rents begin) when the percentage rent is 6% and the base rent is $24,000/year?

! 24,000/.06 = $400,000

! Assume sales are $500,000, the rent is $500,000 x .06 = $30,000

! Proof: Base is $24,000 + Percentage (500,000 – 400,000) x .06 = $30,000

Income © Ted Whitmer, All Rights Reserved.

70"

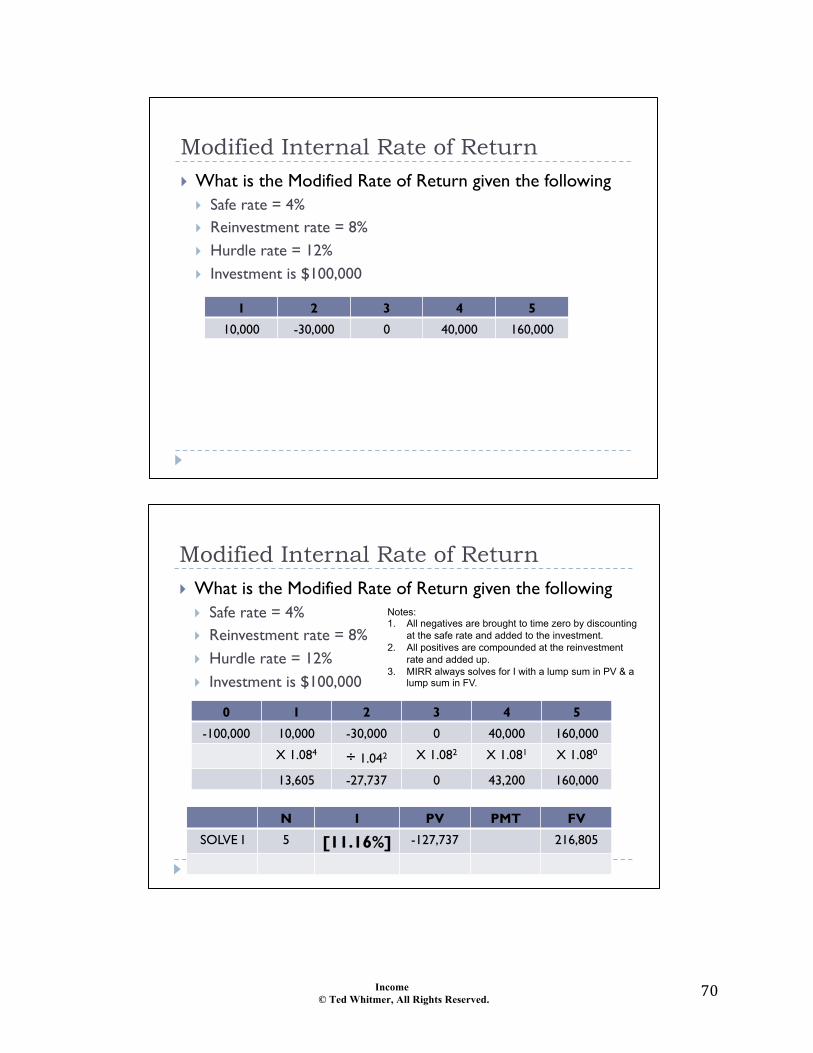

Modified Internal Rate of Return ! What is the Modified Rate of Return given the following

! Safe rate = 4% ! Reinvestment rate = 8% ! Hurdle rate = 12% ! Investment is $100,000

1 2 3 4 5

10,000 -30,000 0 40,000 160,000

Modified Internal Rate of Return ! What is the Modified Rate of Return given the following

! Safe rate = 4% ! Reinvestment rate = 8% ! Hurdle rate = 12% ! Investment is $100,000

0 1 2 3 4 5

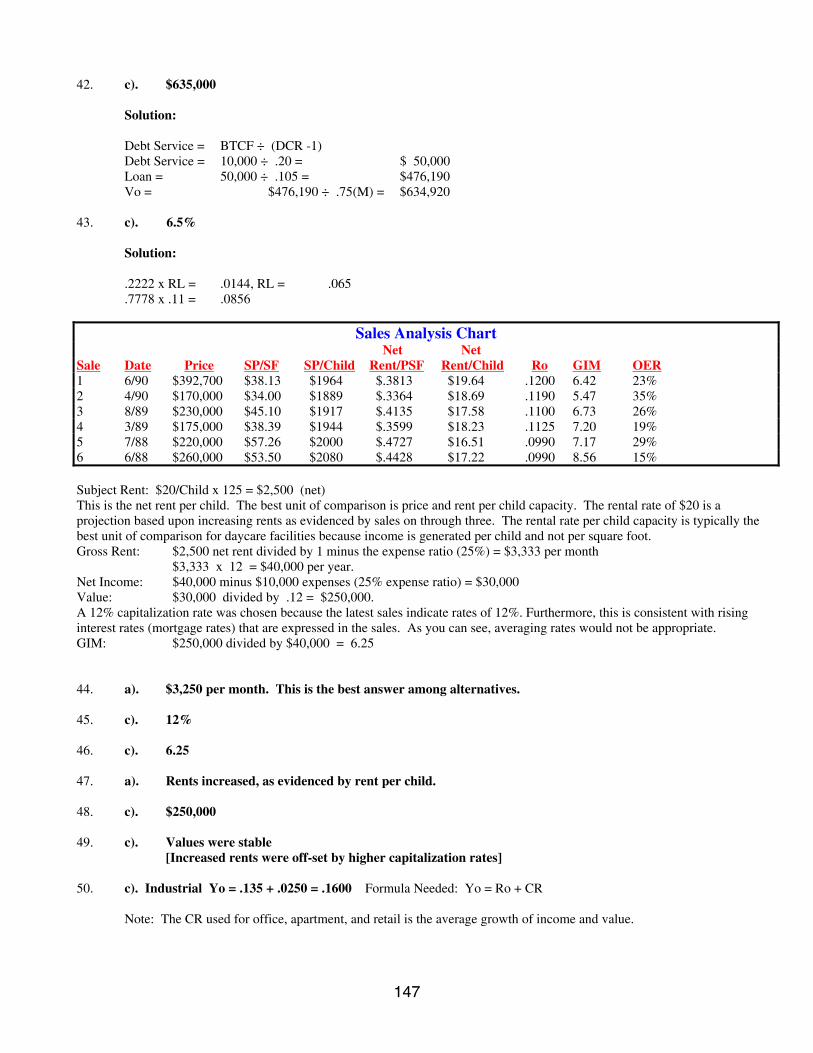

-100,000 10,000 -30,000 0 40,000 160,000

X 1.084 ÷ 1.042 X 1.082 X 1.081 X 1.080

13,605 -27,737 0 43,200 160,000

N I PV PMT FV

SOLVE I 5 [11.16%] -127,737 216,805

Notes: 1. All negatives are brought to time zero by discounting

at the safe rate and added to the investment. 2. All positives are compounded at the reinvestment

rate and added up. 3. MIRR always solves for I with a lump sum in PV & a

lump sum in FV.

Income © Ted Whitmer, All Rights Reserved.

71"

Office ! BOMA (Building Owners & Managers Association)

! Rentable is measured from inside wall of exterior walls. Use from the dominant surface (glass or sheetrock) ! Take out vertical penetrations of stairs, vents elevators but not

columns

! Usable is dominant area of interior of exterior wall to outside of hall to middle of adjacent tenant walls.

! Rentable = Usable x (1 + core, common area, add-on, load

factor) ! Usable = Rentable divided by (1 + load factor) ! Load factor = 1 – Rentable/usable

Retail ! Measured from outside ! CAM is common area maintenance. ! Percentage rents have a higher risk than base rents

Income © Ted Whitmer, All Rights Reserved.

72"

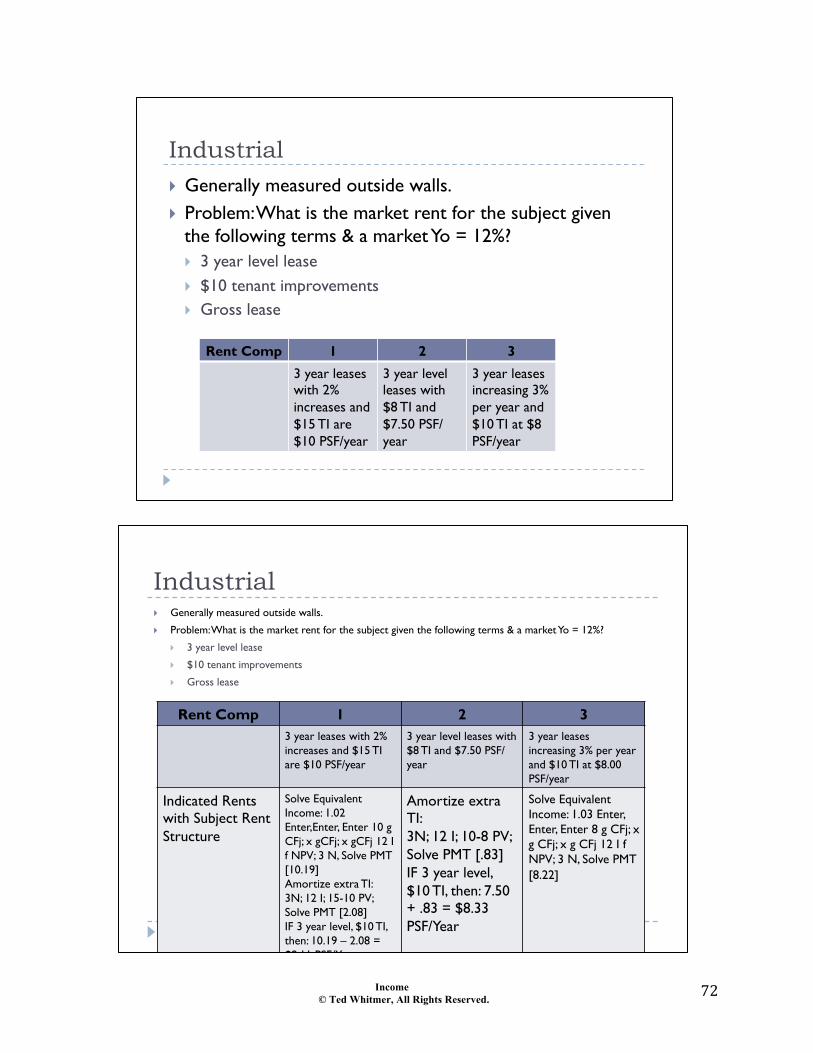

Industrial ! Generally measured outside walls. ! Problem: What is the market rent for the subject given

the following terms & a market Yo = 12%? ! 3 year level lease ! $10 tenant improvements ! Gross lease

Rent Comp 1 2 3

3 year leases with 2% increases and $15 TI are $10 PSF/year

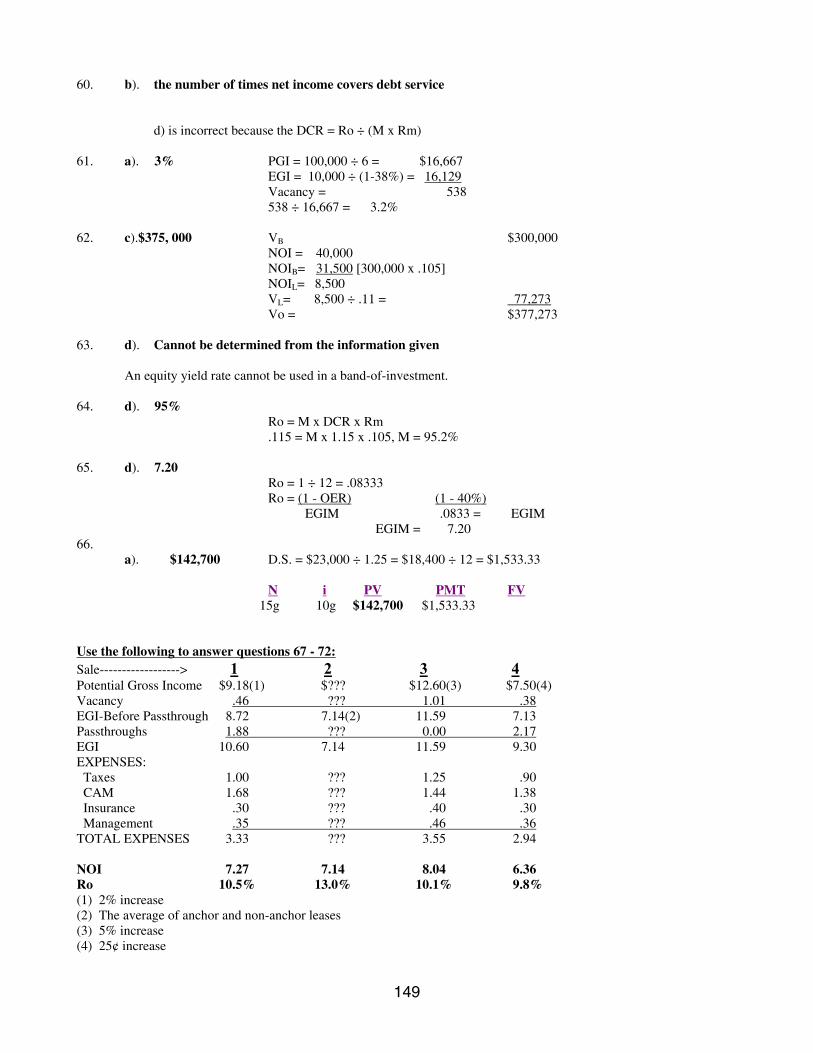

3 year level leases with $8 TI and $7.50 PSF/year

3 year leases increasing 3% per year and $10 TI at $8 PSF/year

Industrial ! Generally measured outside walls.

! Problem: What is the market rent for the subject given the following terms & a market Yo = 12%?

! 3 year level lease

! $10 tenant improvements

! Gross lease

Rent Comp 1 2 3 3 year leases with 2% increases and $15 TI are $10 PSF/year

3 year level leases with $8 TI and $7.50 PSF/year

3 year leases increasing 3% per year and $10 TI at $8.00 PSF/year

Indicated Rents with Subject Rent Structure

Solve Equivalent Income: 1.02 Enter,Enter, Enter 10 g CFj; x gCFj; x gCFj 12 I f NPV; 3 N, Solve PMT [10.19] Amortize extra TI: 3N; 12 I; 15-10 PV; Solve PMT [2.08] IF 3 year level, $10 TI, then: 10.19 – 2.08 = $8.11 PSF/Year

Amortize extra TI: 3N; 12 I; 10-8 PV; Solve PMT [.83] IF 3 year level, $10 TI, then: 7.50 + .83 = $8.33 PSF/Year

Solve Equivalent Income: 1.03 Enter, Enter, Enter 8 g CFj; x g CFj; x g CFj 12 I f NPV; 3 N, Solve PMT [8.22]

Income © Ted Whitmer, All Rights Reserved.

73"

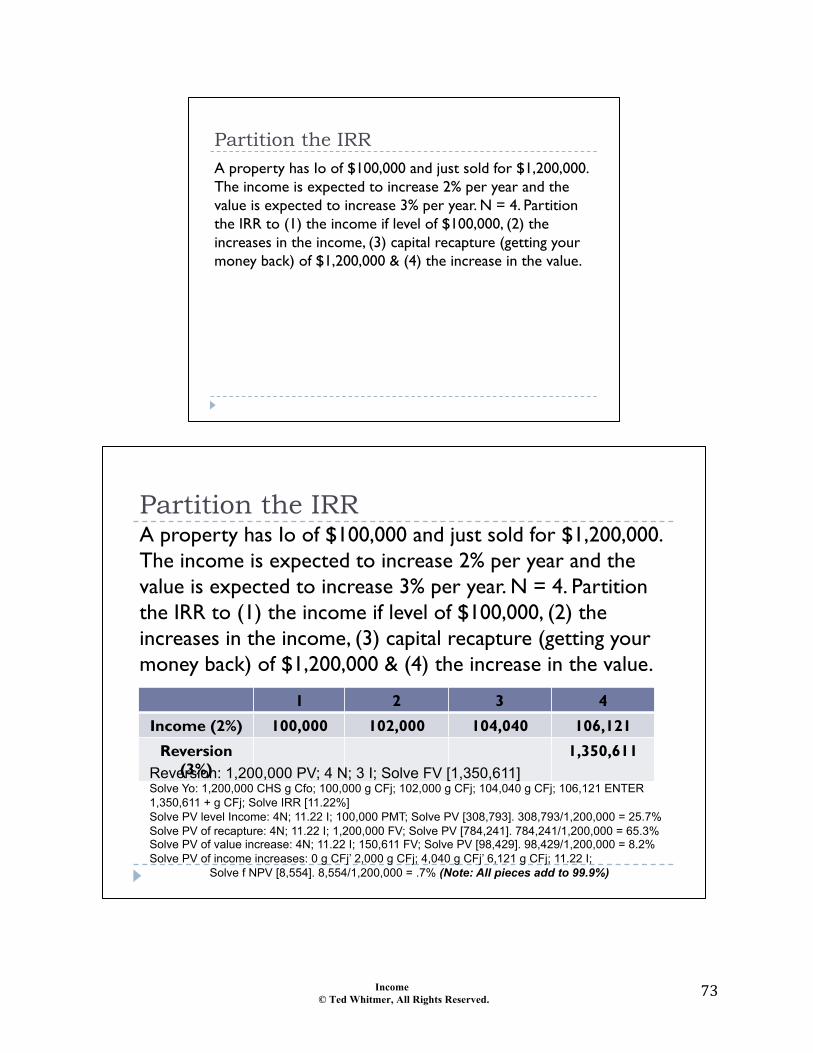

Partition the IRR A property has Io of $100,000 and just sold for $1,200,000. The income is expected to increase 2% per year and the value is expected to increase 3% per year. N = 4. Partition the IRR to (1) the income if level of $100,000, (2) the increases in the income, (3) capital recapture (getting your money back) of $1,200,000 & (4) the increase in the value.

Partition the IRR A property has Io of $100,000 and just sold for $1,200,000. The income is expected to increase 2% per year and the value is expected to increase 3% per year. N = 4. Partition the IRR to (1) the income if level of $100,000, (2) the increases in the income, (3) capital recapture (getting your money back) of $1,200,000 & (4) the increase in the value.

1 2 3 4

Income (2%) 100,000 102,000 104,040 106,121

Reversion (3%)

1,350,611 Reversion: 1,200,000 PV; 4 N; 3 I; Solve FV [1,350,611] Solve Yo: 1,200,000 CHS g Cfo; 100,000 g CFj; 102,000 g CFj; 104,040 g CFj; 106,121 ENTER 1,350,611 + g CFj; Solve IRR [11.22%] Solve PV level Income: 4N; 11.22 I; 100,000 PMT; Solve PV [308,793]. 308,793/1,200,000 = 25.7% Solve PV of recapture: 4N; 11.22 I; 1,200,000 FV; Solve PV [784,241]. 784,241/1,200,000 = 65.3% Solve PV of value increase: 4N; 11.22 I; 150,611 FV; Solve PV [98,429]. 98,429/1,200,000 = 8.2% Solve PV of income increases: 0 g CFj’ 2,000 g CFj; 4,040 g CFj’ 6,121 g CFj; 11.22 I;

Solve f NPV [8,554]. 8,554/1,200,000 = .7% (Note: All pieces add to 99.9%)

Income © Ted Whitmer, All Rights Reserved.

74"

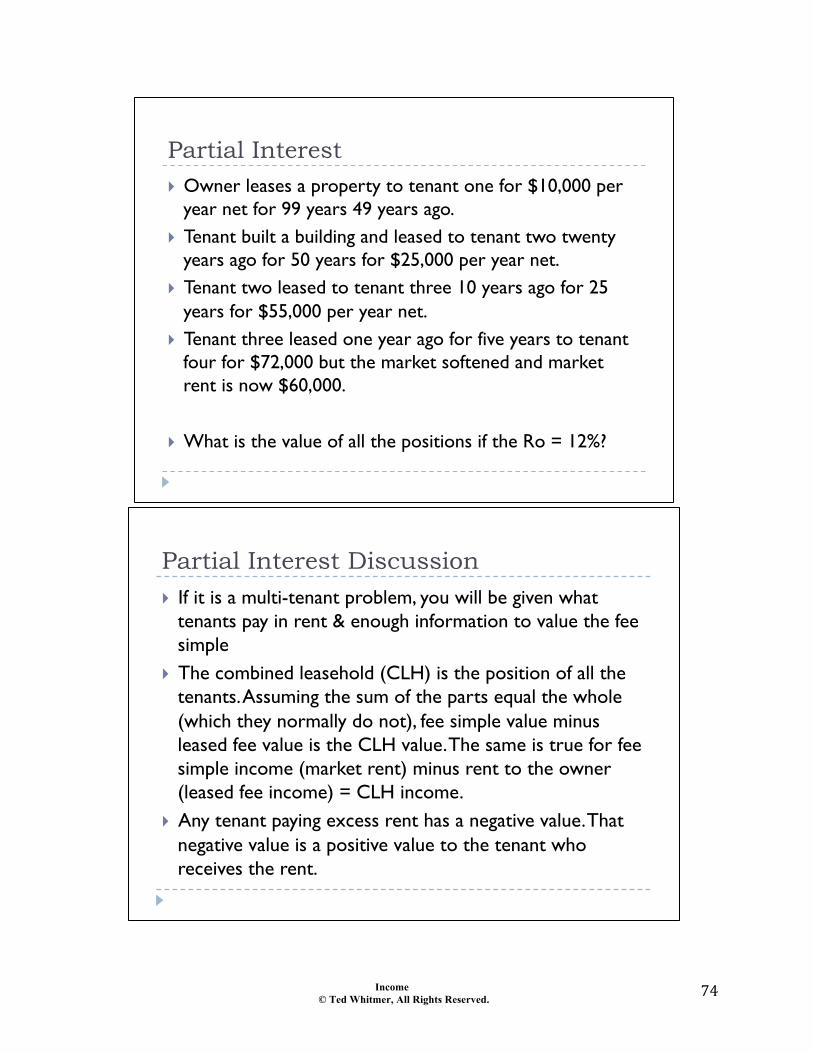

Partial Interest ! Owner leases a property to tenant one for $10,000 per

year net for 99 years 49 years ago. ! Tenant built a building and leased to tenant two twenty

years ago for 50 years for $25,000 per year net. ! Tenant two leased to tenant three 10 years ago for 25

years for $55,000 per year net. ! Tenant three leased one year ago for five years to tenant

four for $72,000 but the market softened and market rent is now $60,000.

! What is the value of all the positions if the Ro = 12%?

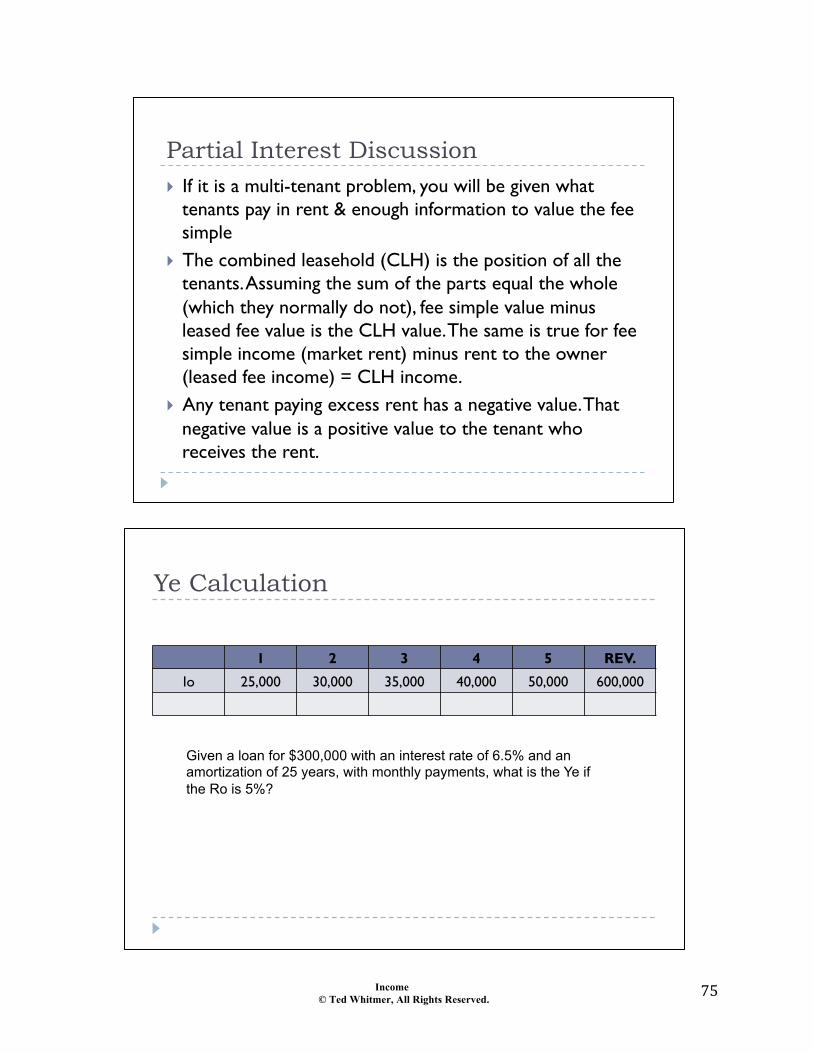

Partial Interest Discussion ! If it is a multi-tenant problem, you will be given what

tenants pay in rent & enough information to value the fee simple

! The combined leasehold (CLH) is the position of all the tenants. Assuming the sum of the parts equal the whole (which they normally do not), fee simple value minus leased fee value is the CLH value. The same is true for fee simple income (market rent) minus rent to the owner (leased fee income) = CLH income.

! Any tenant paying excess rent has a negative value. That negative value is a positive value to the tenant who receives the rent.

Income © Ted Whitmer, All Rights Reserved.

75"

Partial Interest Discussion ! If it is a multi-tenant problem, you will be given what

tenants pay in rent & enough information to value the fee simple

! The combined leasehold (CLH) is the position of all the tenants. Assuming the sum of the parts equal the whole (which they normally do not), fee simple value minus leased fee value is the CLH value. The same is true for fee simple income (market rent) minus rent to the owner (leased fee income) = CLH income.

! Any tenant paying excess rent has a negative value. That negative value is a positive value to the tenant who receives the rent.

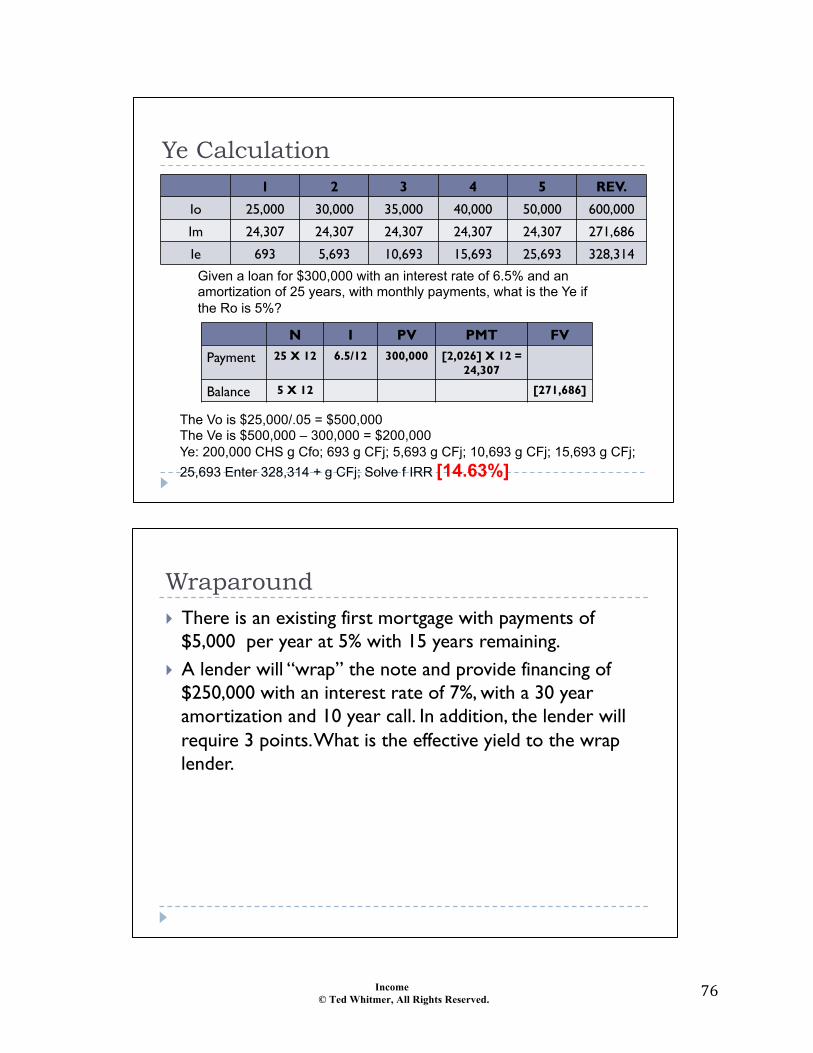

Ye Calculation

1 2 3 4 5 REV.

Io 25,000 30,000 35,000 40,000 50,000 600,000

Given a loan for $300,000 with an interest rate of 6.5% and an amortization of 25 years, with monthly payments, what is the Ye if the Ro is 5%?

Income © Ted Whitmer, All Rights Reserved.

76"

Ye Calculation 1 2 3 4 5 REV.

Io 25,000 30,000 35,000 40,000 50,000 600,000

Im 24,307 24,307 24,307 24,307 24,307 271,686

Ie 693 5,693 10,693 15,693 25,693 328,314

Given a loan for $300,000 with an interest rate of 6.5% and an amortization of 25 years, with monthly payments, what is the Ye if the Ro is 5%?

N I PV PMT FV

Payment 25 X 12 6.5/12 300,000 [2,026] X 12 = 24,307

Balance 5 X 12 [271,686]

The Vo is $25,000/.05 = $500,000 The Ve is $500,000 – 300,000 = $200,000 Ye: 200,000 CHS g Cfo; 693 g CFj; 5,693 g CFj; 10,693 g CFj; 15,693 g CFj; 25,693 Enter 328,314 + g CFj; Solve f IRR [14.63%]

Wraparound ! There is an existing first mortgage with payments of

$5,000 per year at 5% with 15 years remaining. ! A lender will “wrap” the note and provide financing of

$250,000 with an interest rate of 7%, with a 30 year amortization and 10 year call. In addition, the lender will require 3 points. What is the effective yield to the wrap lender.

Income © Ted Whitmer, All Rights Reserved.

77"

Wraparound ! There is an existing first mortgage with payments of $5,000 per year at 5% with 15 years remaining.

! A lender will “wrap” the note and provide financing of $250,000 with an interest rate of 7%, with a 30 year amortization and 10 year call. In addition, the lender will require 3 points. What is the effective yield to the wrap lender.

! The bold numbers are the solved number. First the payment of the wrap & balance were calculated. The balance of the first was calculated next along with the balloon in ten years. The points were taken care of in the last step by mulitiplying the loan times 1 – the 3 points = .97.

N I PV PMT FV

WRAP 30 7 -250,000 [20,147] Wrap

Balloon 10 [213,433]

First 15 5 [51,898] 5,000

First Balloon

10 [21,647]

Effective Yield

10 [7.98%] - [250,000(.97)– 51,898 = 190,602]

20,147 – 5,000 = 15,147

191,786

Income © Ted Whitmer, All Rights Reserved.

78"

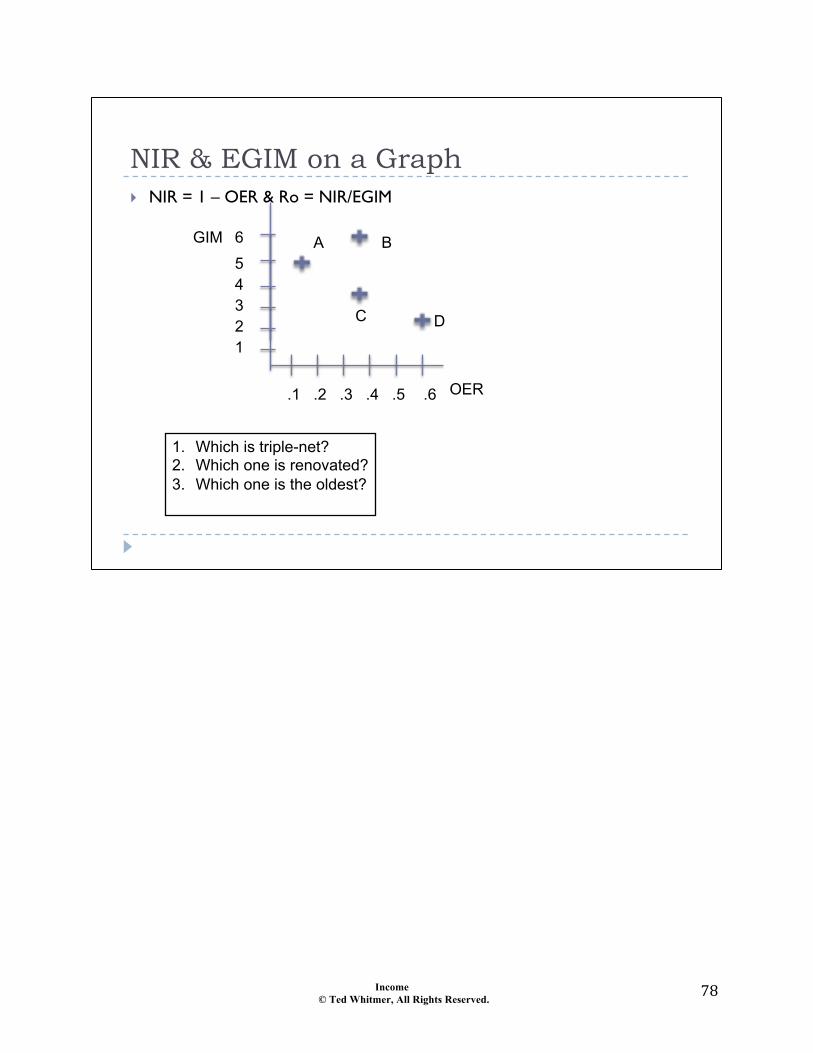

NIR & EGIM on a Graph

GIM

! NIR = 1 – OER & Ro = NIR/EGIM

OER .1 .2 .3 .4 .5 .6

1 2 3 4 5

6 A B

C D

1. Which is triple-net? 2. Which one is renovated? 3. Which one is the oldest?

Income © Ted Whitmer, All Rights Reserved.

79"

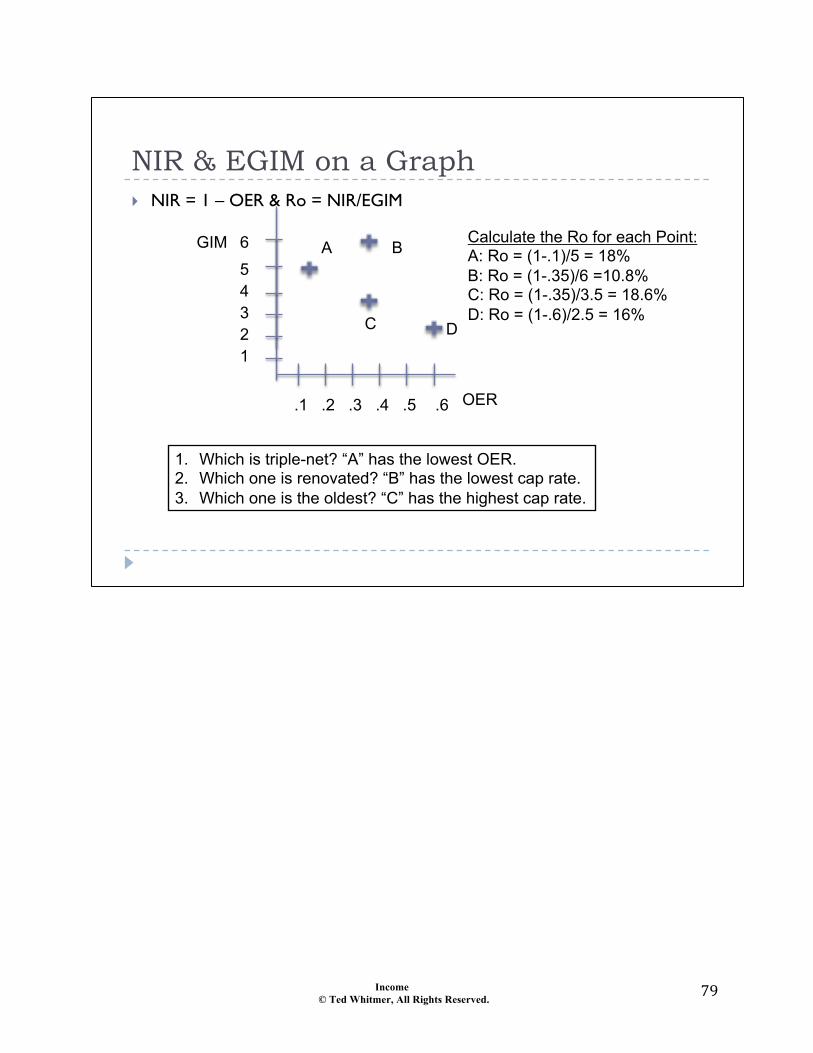

NIR & EGIM on a Graph

GIM

! NIR = 1 – OER & Ro = NIR/EGIM

OER .1 .2 .3 .4 .5 .6

1 2 3 4 5

6 A B

C D

1. Which is triple-net? “A” has the lowest OER. 2. Which one is renovated? “B” has the lowest cap rate. 3. Which one is the oldest? “C” has the highest cap rate.

Calculate the Ro for each Point: A: Ro = (1-.1)/5 = 18% B: Ro = (1-.35)/6 =10.8% C: Ro = (1-.35)/3.5 = 18.6% D: Ro = (1-.6)/2.5 = 16%

Income © Ted Whitmer, All Rights Reserved.

80"

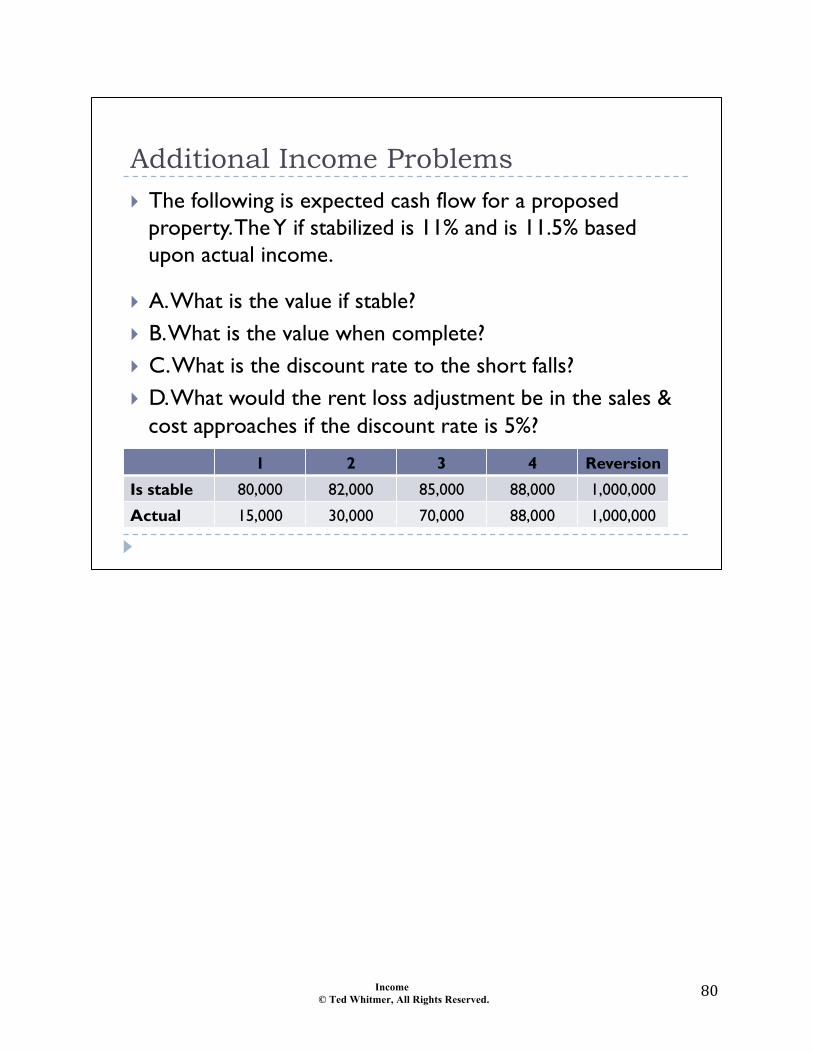

Additional Income Problems ! The following is expected cash flow for a proposed

property. The Y if stabilized is 11% and is 11.5% based upon actual income.

! A. What is the value if stable? ! B. What is the value when complete? ! C. What is the discount rate to the short falls? ! D. What would the rent loss adjustment be in the sales &

cost approaches if the discount rate is 5%?

1 2 3 4 Reversion

Is stable 80,000 82,000 85,000 88,000 1,000,000

Actual 15,000 30,000 70,000 88,000 1,000,000

Income © Ted Whitmer, All Rights Reserved.

81"

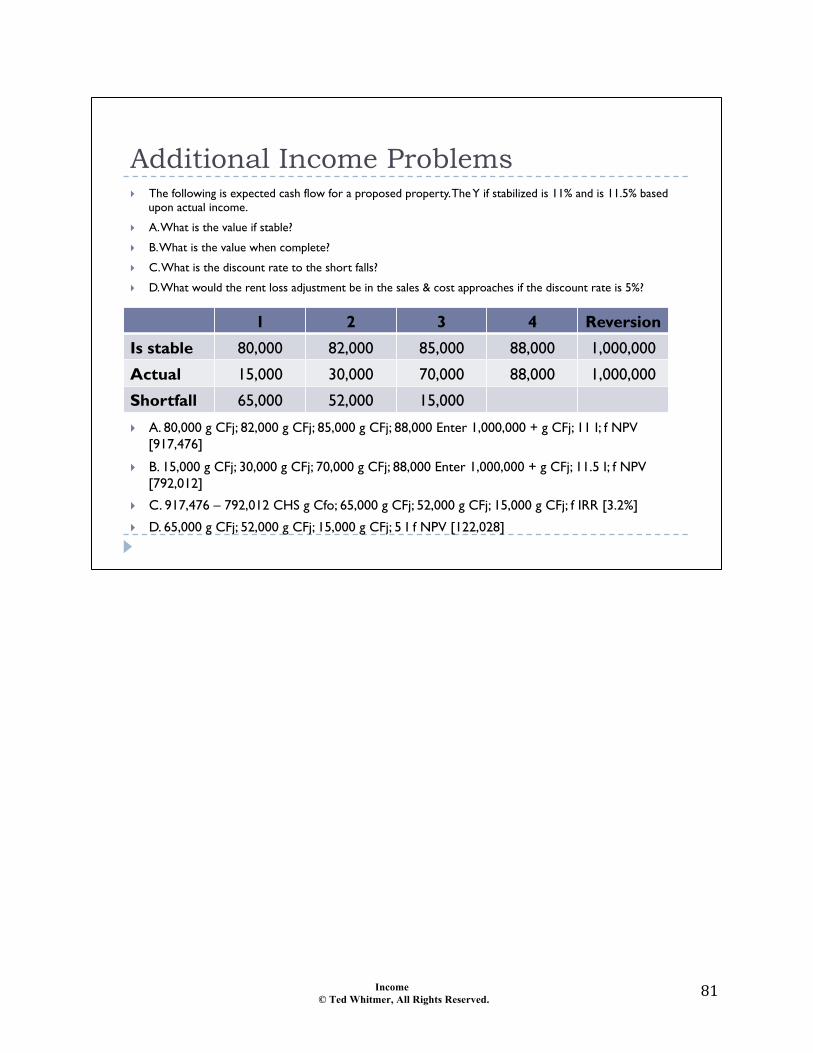

Additional Income Problems ! The following is expected cash flow for a proposed property. The Y if stabilized is 11% and is 11.5% based

upon actual income.

! A. What is the value if stable?

! B. What is the value when complete?

! C. What is the discount rate to the short falls?

! D. What would the rent loss adjustment be in the sales & cost approaches if the discount rate is 5%?

! A. 80,000 g CFj; 82,000 g CFj; 85,000 g CFj; 88,000 Enter 1,000,000 + g CFj; 11 I; f NPV [917,476]

! B. 15,000 g CFj; 30,000 g CFj; 70,000 g CFj; 88,000 Enter 1,000,000 + g CFj; 11.5 I; f NPV [792,012]

! C. 917,476 – 792,012 CHS g Cfo; 65,000 g CFj; 52,000 g CFj; 15,000 g CFj; f IRR [3.2%]

! D. 65,000 g CFj; 52,000 g CFj; 15,000 g CFj; 5 I f NPV [122,028]

1 2 3 4 Reversion

Is stable 80,000 82,000 85,000 88,000 1,000,000

Actual 15,000 30,000 70,000 88,000 1,000,000

Shortfall 65,000 52,000 15,000

Income © Ted Whitmer, All Rights Reserved.

82"

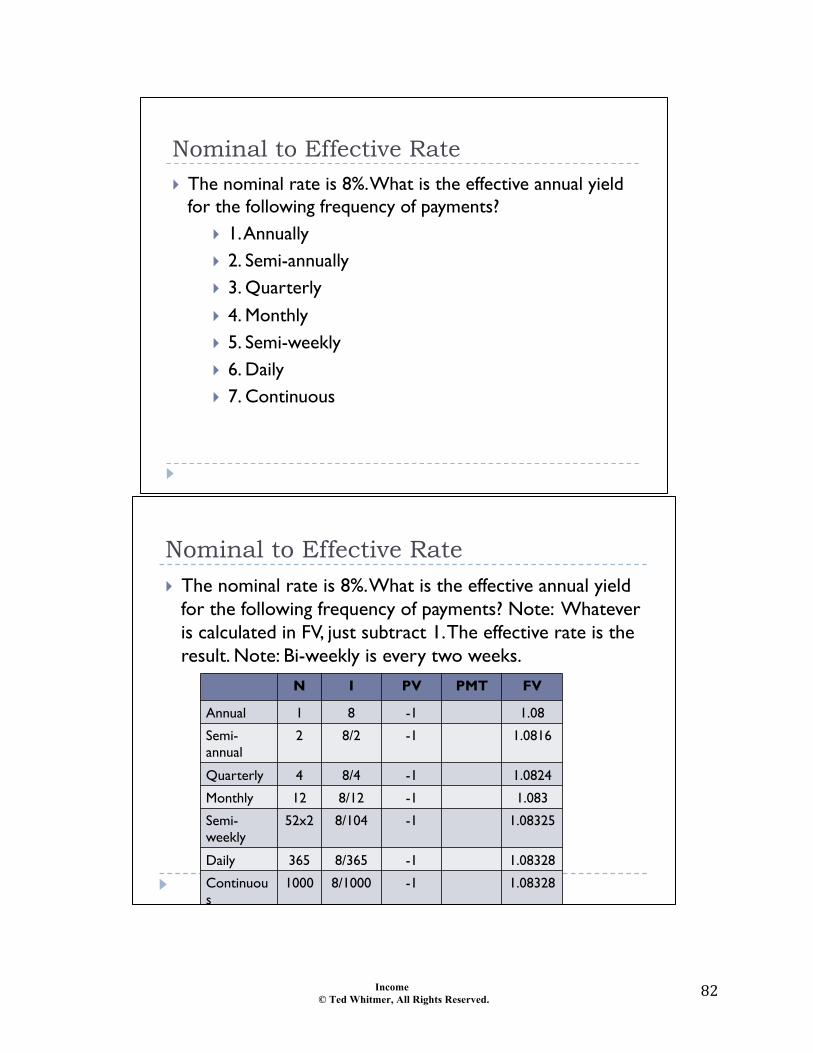

Nominal to Effective Rate ! The nominal rate is 8%. What is the effective annual yield

for the following frequency of payments? ! 1. Annually ! 2. Semi-annually ! 3. Quarterly ! 4. Monthly ! 5. Semi-weekly ! 6. Daily ! 7. Continuous

Nominal to Effective Rate ! The nominal rate is 8%. What is the effective annual yield

for the following frequency of payments? Note: Whatever is calculated in FV, just subtract 1. The effective rate is the result. Note: Bi-weekly is every two weeks.

N I PV PMT FV

Annual 1 8 -1 1.08

Semi-annual

2 8/2 -1 1.0816

Quarterly 4 8/4 -1 1.0824

Monthly 12 8/12 -1 1.083

Semi-weekly

52x2 8/104 -1 1.08325

Daily 365 8/365 -1 1.08328

Continuous

1000 8/1000 -1 1.08328

Income © Ted Whitmer, All Rights Reserved.

83"

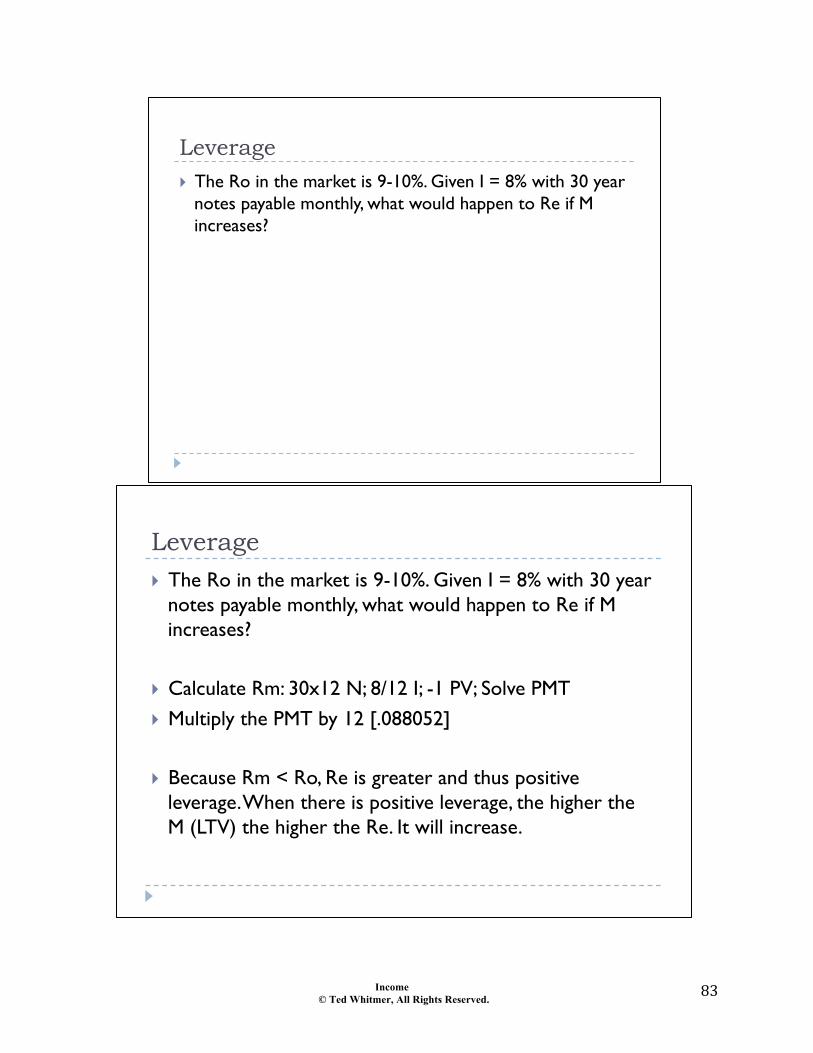

Leverage ! The Ro in the market is 9-10%. Given I = 8% with 30 year

notes payable monthly, what would happen to Re if M increases?

Leverage ! The Ro in the market is 9-10%. Given I = 8% with 30 year

notes payable monthly, what would happen to Re if M increases?

! Calculate Rm: 30x12 N; 8/12 I; -1 PV; Solve PMT ! Multiply the PMT by 12 [.088052]

! Because Rm < Ro, Re is greater and thus positive leverage. When there is positive leverage, the higher the M (LTV) the higher the Re. It will increase.

Income © Ted Whitmer, All Rights Reserved.

84"

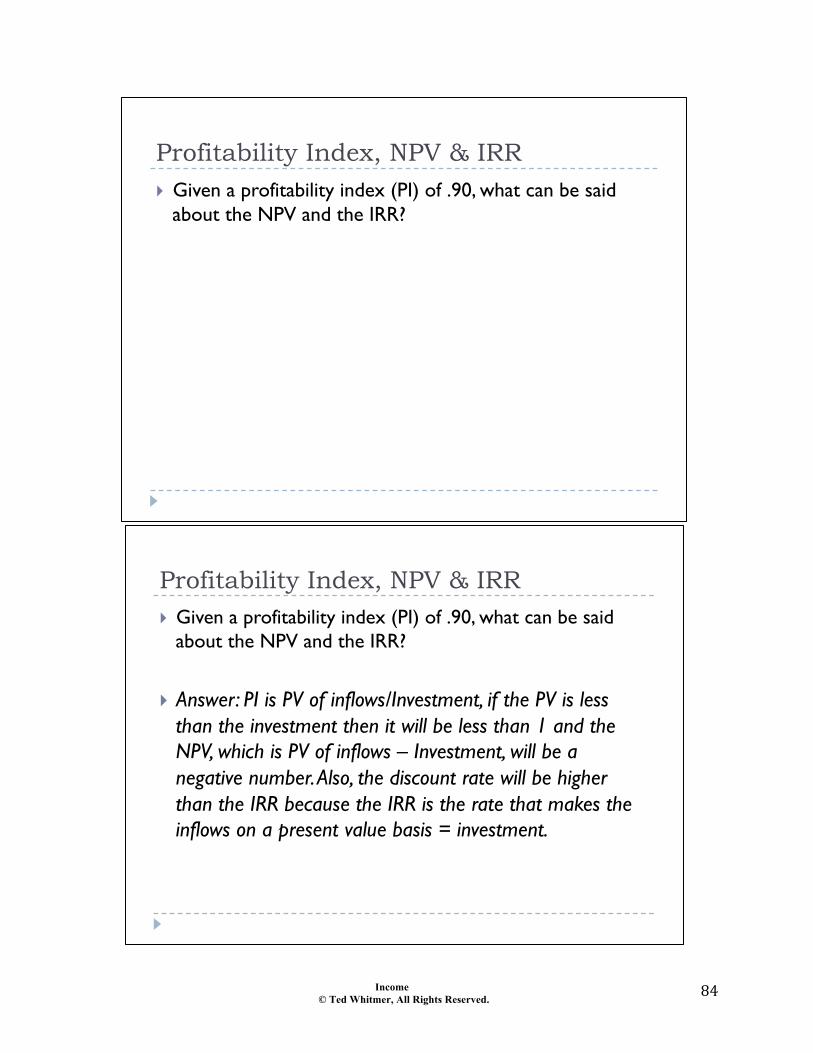

Profitability Index, NPV & IRR ! Given a profitability index (PI) of .90, what can be said

about the NPV and the IRR?

Profitability Index, NPV & IRR ! Given a profitability index (PI) of .90, what can be said

about the NPV and the IRR?

! Answer: PI is PV of inflows/Investment, if the PV is less than the investment then it will be less than 1 and the NPV, which is PV of inflows – Investment, will be a negative number. Also, the discount rate will be higher than the IRR because the IRR is the rate that makes the inflows on a present value basis = investment.

Income © Ted Whitmer, All Rights Reserved.

85"

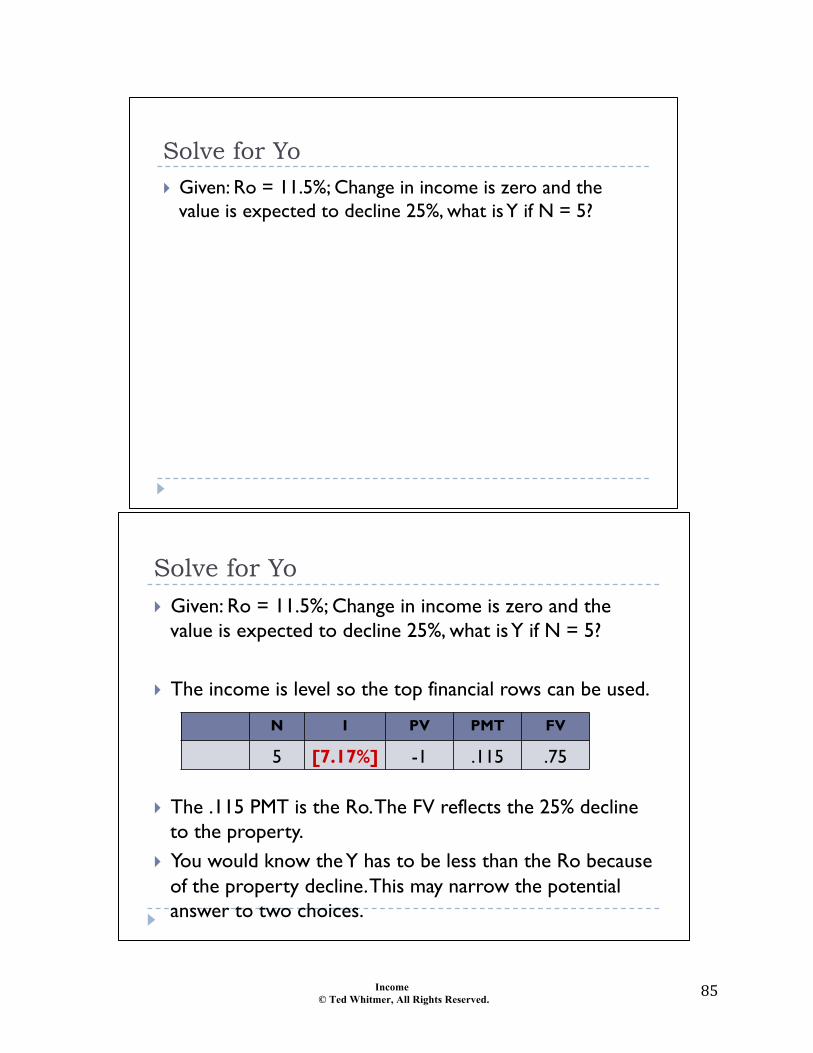

Solve for Yo ! Given: Ro = 11.5%; Change in income is zero and the

value is expected to decline 25%, what is Y if N = 5?

Solve for Yo ! Given: Ro = 11.5%; Change in income is zero and the

value is expected to decline 25%, what is Y if N = 5?

! The income is level so the top financial rows can be used.

! The .115 PMT is the Ro. The FV reflects the 25% decline to the property.

! You would know the Y has to be less than the Ro because of the property decline. This may narrow the potential answer to two choices.

N I PV PMT FV

5 [7.17%] -1 .115 .75

Income © Ted Whitmer, All Rights Reserved.

86"

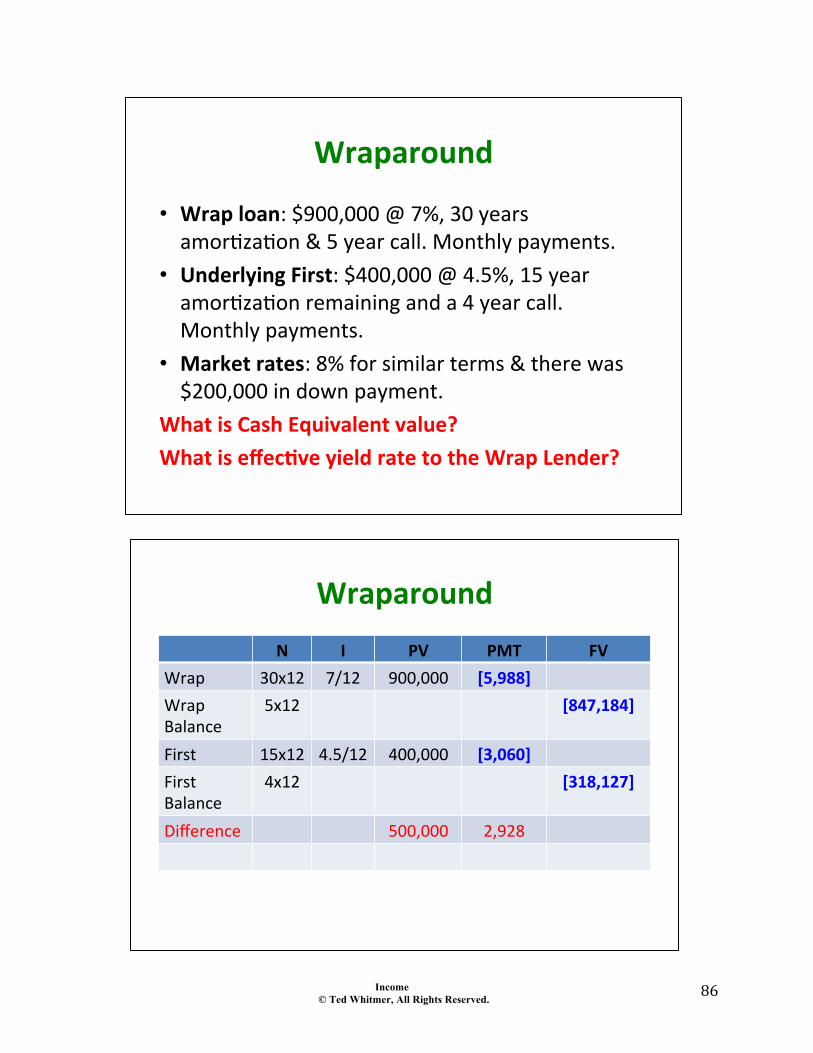

Wraparound)

• Wrap)loan:"$900,000"@"7%,"30"years"amor2za2on"&"5"year"call."Monthly"payments."

• Underlying)First:"$400,000"@"4.5%,"15"year"amor2za2on"remaining"and"a"4"year"call."Monthly"payments."

• Market)rates:"8%"for"similar"terms"&"there"was"$200,000"in"down"payment."

What)is)Cash)Equivalent)value?))What)is)effec=ve)yield)rate)to)the)Wrap)Lender?)

Wraparound!N* I* PV* PMT* FV*

Wrap! 30x12! 7/12! 900,000! [5,988]*Wrap!Balance!

5x12! [847,184]*!

First! 15x12! 4.5/12! 400,000! [3,060]*First!Balance!

4x12! [318,127]*

Difference! 500,000! 2,928!

Income © Ted Whitmer, All Rights Reserved.

87"

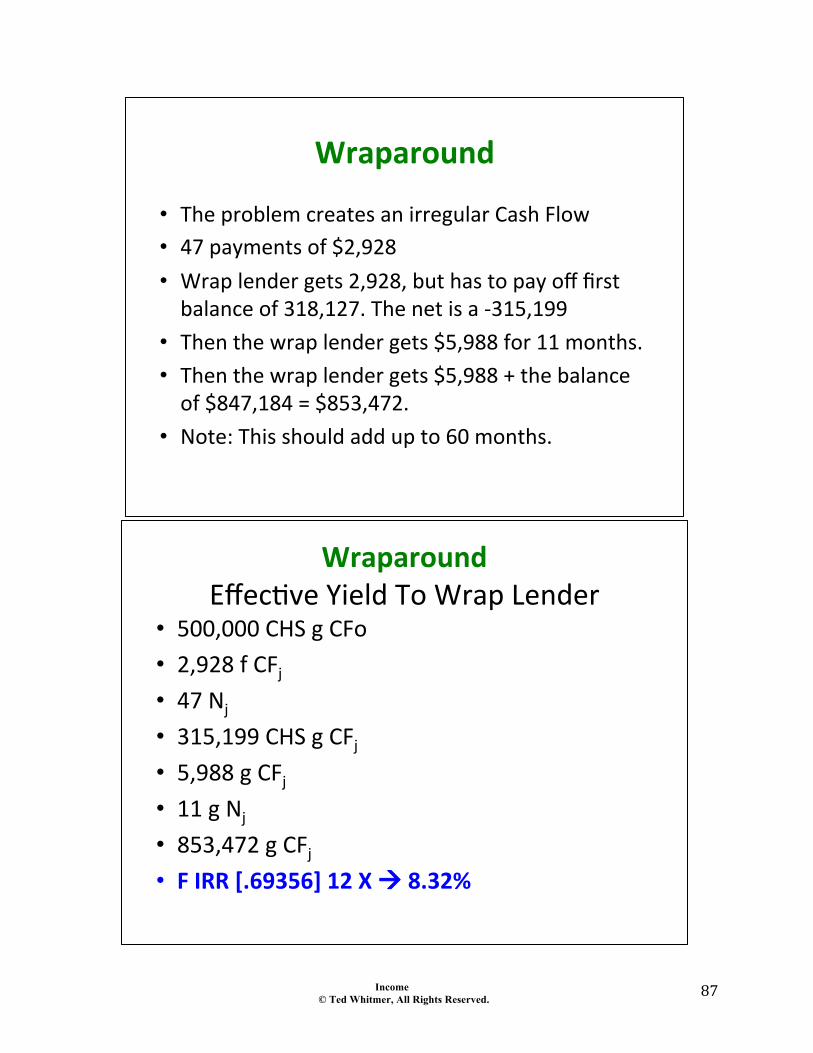

Wraparound!

• The!problem!creates!an!irregular!Cash!Flow!• 47!payments!of!$2,928!!• Wrap!lender!gets!2,928,!but!has!to!pay!off!first!balance!of!318,127.!The!net!is!a!F315,199!

• Then!the!wrap!lender!gets!$5,988!for!11!months.!• Then!the!wrap!lender!gets!$5,988!+!the!balance!of!$847,184!=!$853,472.!

• Note:!This!should!add!up!to!60!months.!

Wraparound!Effec&ve!Yield!To!Wrap!Lender!

• 500,000!CHS!g!CFo!• 2,928!f!CFj!• 47!Nj!

• 315,199!CHS!g!CFj!• 5,988!g!CFj!• 11!g!Nj!

• 853,472!g!CFj!• F*IRR*[.69356]*12*X*!*8.32%*

Income © Ted Whitmer, All Rights Reserved.

88"

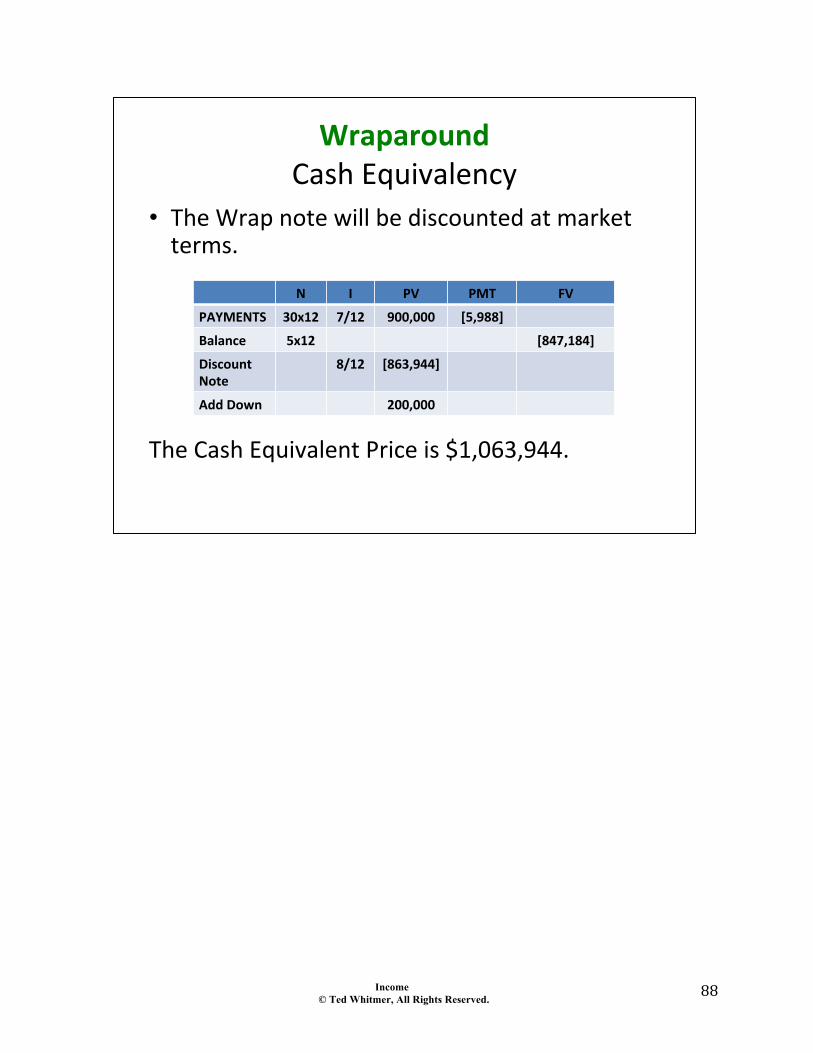

Wraparound!Cash!Equivalency!

• The!Wrap!note!will!be!discounted!at!market!terms.!!

The!Cash!Equivalent!Price!is!$1,063,944.!

N* I* PV* PMT* FV*

PAYMENTS* 30x12* 7/12* 900,000* [5,988]*

Balance* 5x12* [847,184]*

Discount*Note*

8/12* [863,944]*

Add*Down* 200,000*

Income © Ted Whitmer, All Rights Reserved.

89"

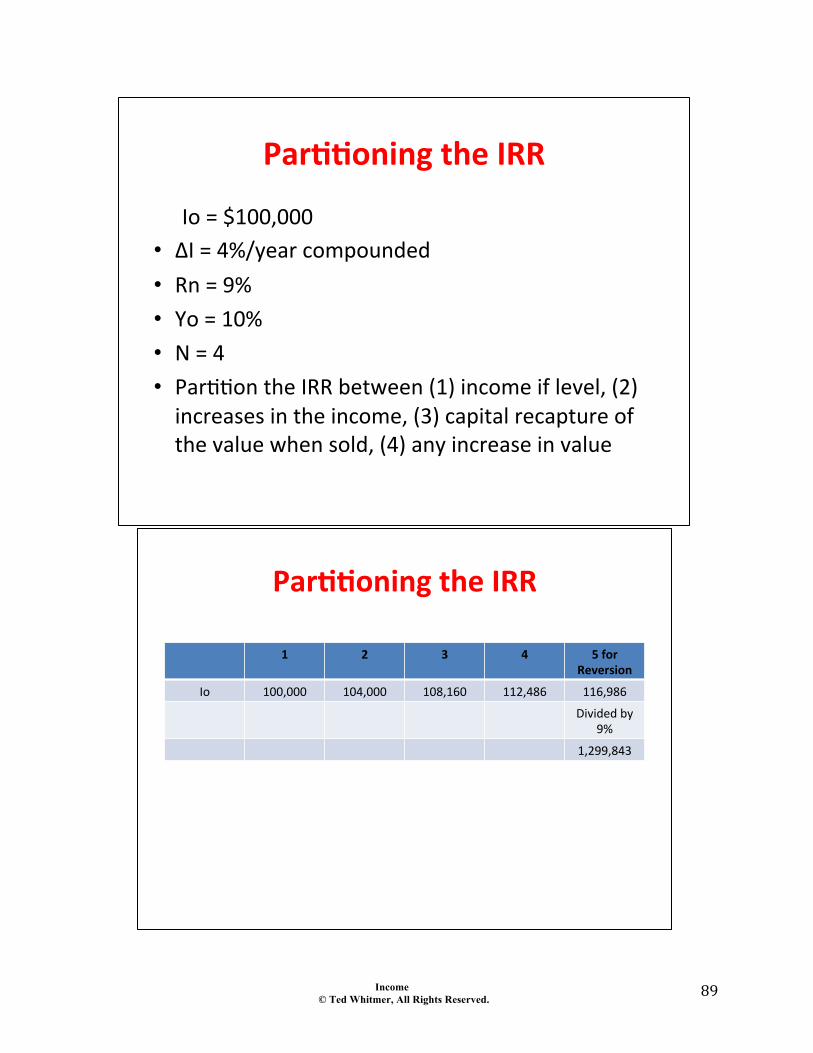

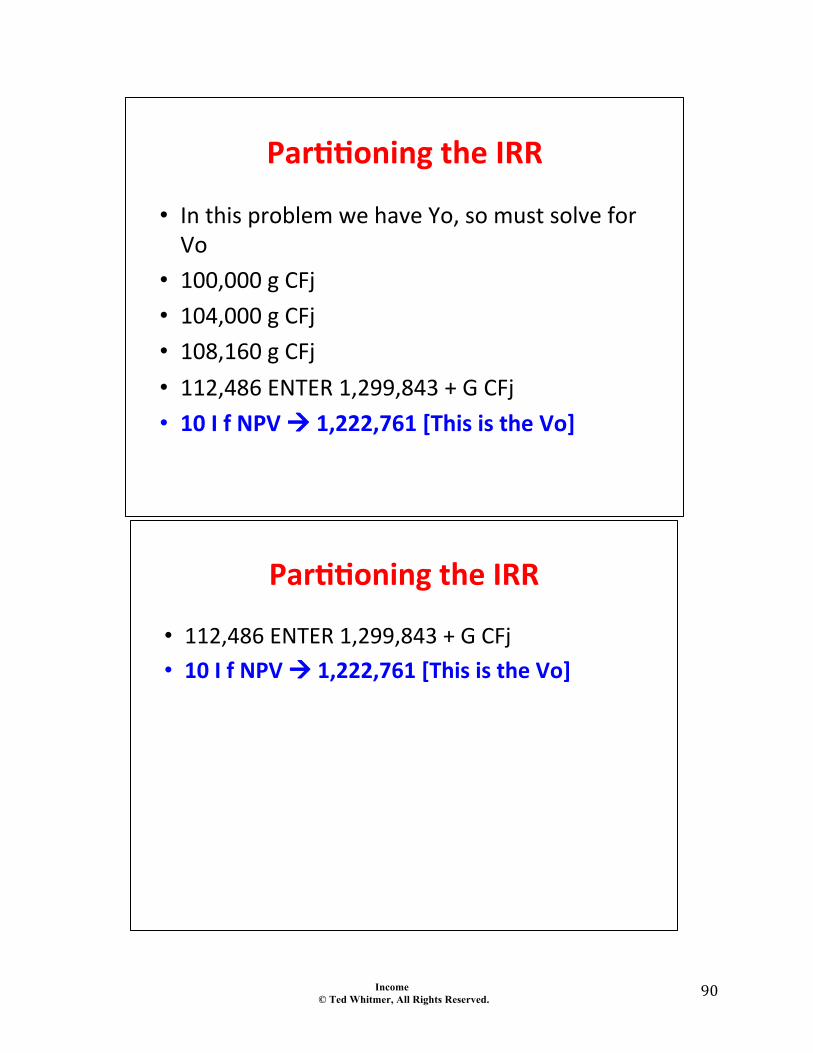

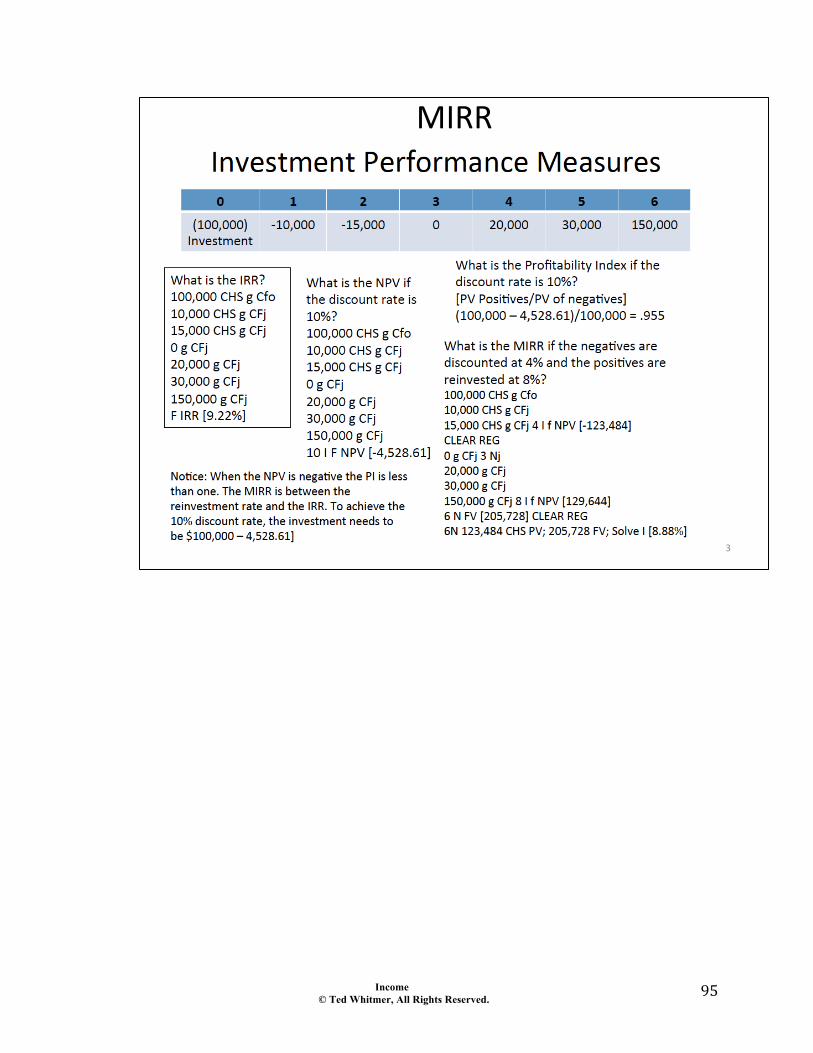

Par$$oning)the)IRR)

!Io!=!$100,000!• ΔI!=!4%/year!compounded!• Rn!=!9%!• Yo!=!10%!• N!=!4!• Par<<on!the!IRR!between!(1)!income!if!level,!(2)!increases!in!the!income,!(3)!capital!recapture!of!the!value!when!sold,!(4)!any!increase!in!value!

Par$$oning)the)IRR!

1) 2) 3) 4) 5)for)Reversion)

Io! 100,000! 104,000! 108,160! 112,486! 116,986!

Divided!by!9%!

1,299,843!

Income © Ted Whitmer, All Rights Reserved.

90"

Par$$oning)the)IRR!

• In!this!problem!we!have!Yo,!so!must!solve!for!Vo!

• 100,000!g!CFj!• 104,000!g!CFj!• 108,160!g!CFj!• 112,486!ENTER!1,299,843!+!G!CFj!• 10)I)f)NPV)!)1,222,761)[This)is)the)Vo])

Par$$oning)the)IRR!

• 112,486!ENTER!1,299,843!+!G!CFj!• 10)I)f)NPV)!)1,222,761)[This)is)the)Vo])

Income © Ted Whitmer, All Rights Reserved.

91"

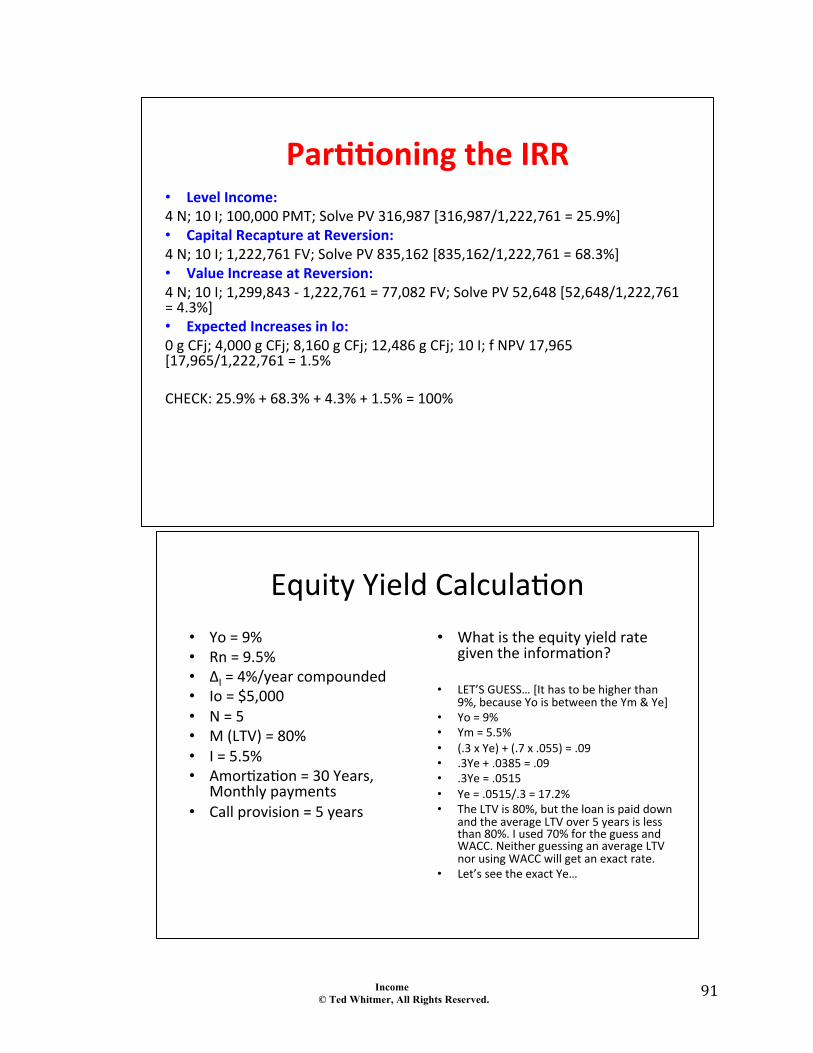

Par$$oning)the)IRR!• Level)Income:))4!N;!10!I;!100,000!PMT;!Solve!PV!316,987![316,987/1,222,761!=!25.9%]!• Capital)Recapture)at)Reversion:)4!N;!10!I;!1,222,761!FV;!Solve!PV!835,162![835,162/1,222,761!=!68.3%]!• Value)Increase)at)Reversion:)4!N;!10!I;!1,299,843!@!1,222,761!=!77,082!FV;!Solve!PV!52,648![52,648/1,222,761!=!4.3%]!• Expected)Increases)in)Io:)0!g!CFj;!4,000!g!CFj;!8,160!g!CFj;!12,486!g!CFj;!10!I;!f!NPV!17,965![17,965/1,222,761!=!1.5%!!CHECK:!25.9%!+!68.3%!+!4.3%!+!1.5%!=!100%!!!!)

Equity'Yield'Calcula/on'• Yo'='9%'• Rn'='9.5%'• ΔI'='4%/year'compounded'• Io'='$5,000'• N'='5'• M'(LTV)'='80%'• I'='5.5%'• Amor/za/on'='30'Years,'

Monthly'payments'• Call'provision'='5'years'

• What'is'the'equity'yield'rate'given'the'informa/on?'

• LET’S'GUESS…'[It'has'to'be'higher'than'9%,'because'Yo'is'between'the'Ym'&'Ye]'

• Yo'='9%'• Ym'='5.5%'• (.3'x'Ye)'+'(.7'x'.055)'='.09'• .3Ye'+'.0385'='.09'• .3Ye'='.0515'• Ye'='.0515/.3'='17.2%'• The'LTV'is'80%,'but'the'loan'is'paid'down'

and'the'average'LTV'over'5'years'is'less'than'80%.'I'used'70%'for'the'guess'and'WACC.'Neither'guessing'an'average'LTV'nor'using'WACC'will'get'an'exact'rate.''

• Let’s'see'the'exact'Ye…'

'

Income © Ted Whitmer, All Rights Reserved.

92"

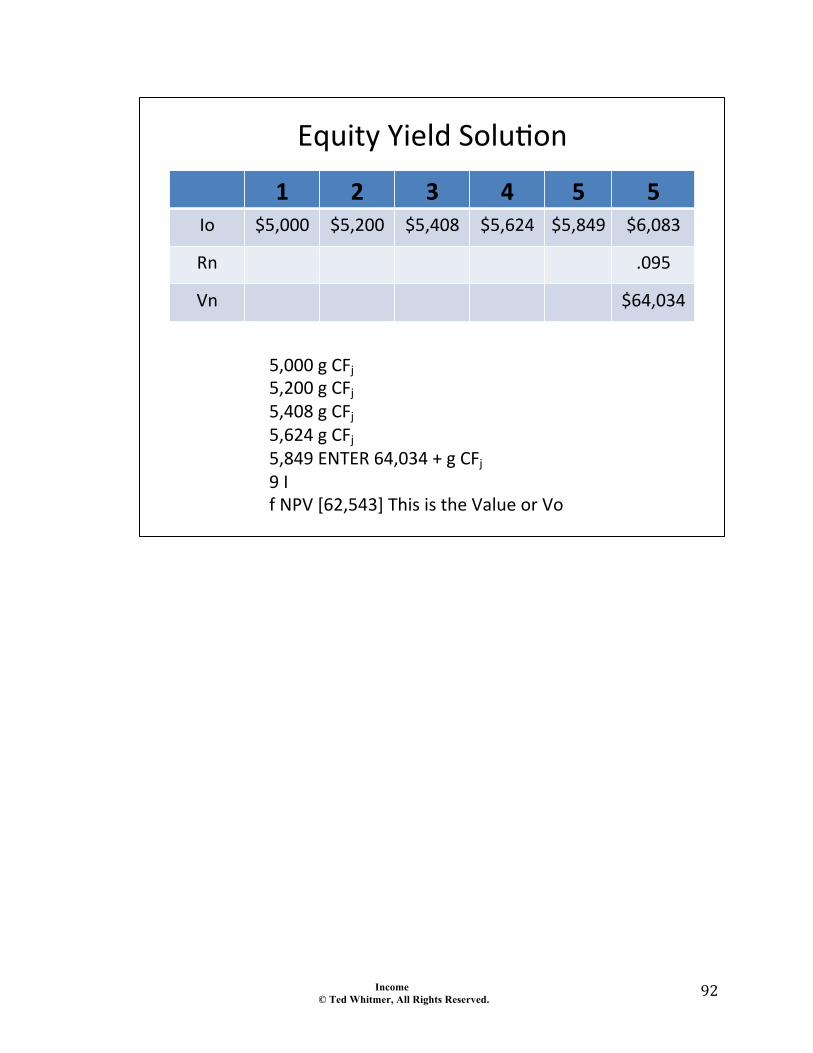

Equity'Yield'Solu.on''1" 2" 3" 4" 5" 5"

Io' $5,000' $5,200' $5,408' $5,624' $5,849' $6,083'

Rn' .095'

Vn' $64,034'

5,000'g'CFj'5,200'g'CFj'5,408'g'CFj'5,624'g'CFj'5,849'ENTER'64,034'+'g'CFj'9'I''f'NPV'[62,543]'This'is'the'Value'or'Vo'

Income © Ted Whitmer, All Rights Reserved.

93"

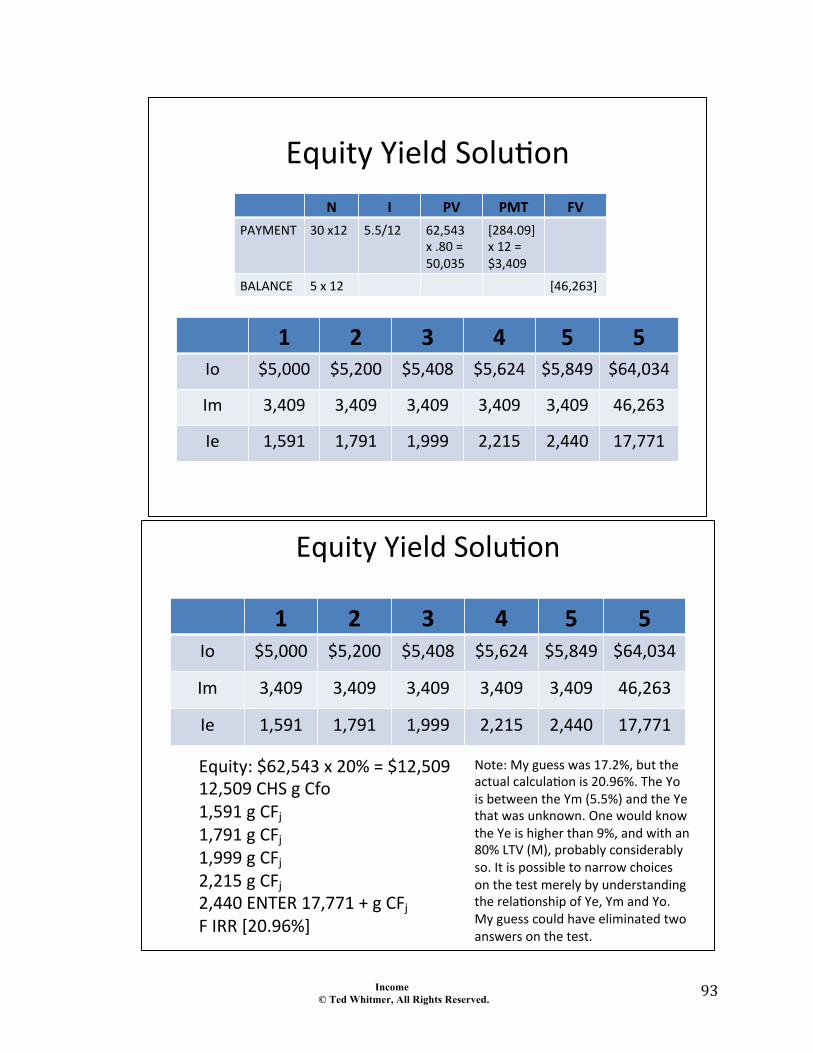

Equity'Yield'Solu.on'

1" 2" 3" 4" 5" 5"Io' $5,000' $5,200' $5,408' $5,624' $5,849' $64,034'

Im' 3,409' 3,409' 3,409' 3,409' 3,409' 46,263'

Ie' 1,591' 1,791' 1,999' 2,215' 2,440' 17,771'

N" I" PV" PMT" FV"PAYMENT' 30'x12' 5.5/12' 62,543'

x'.80'='50,035'

[284.09]'x'12'='$3,409'

BALANCE' 5'x'12' [46,263]'

Equity'Yield'Solu.on''

1" 2" 3" 4" 5" 5"Io' $5,000' $5,200' $5,408' $5,624' $5,849' $64,034'

Im' 3,409' 3,409' 3,409' 3,409' 3,409' 46,263'

Ie' 1,591' 1,791' 1,999' 2,215' 2,440' 17,771'

Equity:'$62,543'x'20%'='$12,509'12,509'CHS'g'Cfo'1,591'g'CFj'1,791'g'CFj'1,999'g'CFj'2,215'g'CFj'2,440'ENTER'17,771'+'g'CFj'F'IRR'[20.96%]''''''

Note:'My'guess'was'17.2%,'but'the'actual'calcula.on'is'20.96%.'The'Yo'is'between'the'Ym'(5.5%)'and'the'Ye'that'was'unknown.'One'would'know'the'Ye'is'higher'than'9%,'and'with'an'80%'LTV'(M),'probably'considerably'so.'It'is'possible'to'narrow'choices'on'the'test'merely'by'understanding'the'rela.onship'of'Ye,'Ym'and'Yo.'My'guess'could'have'eliminated'two'answers'on'the'test.'

Income © Ted Whitmer, All Rights Reserved.

94"

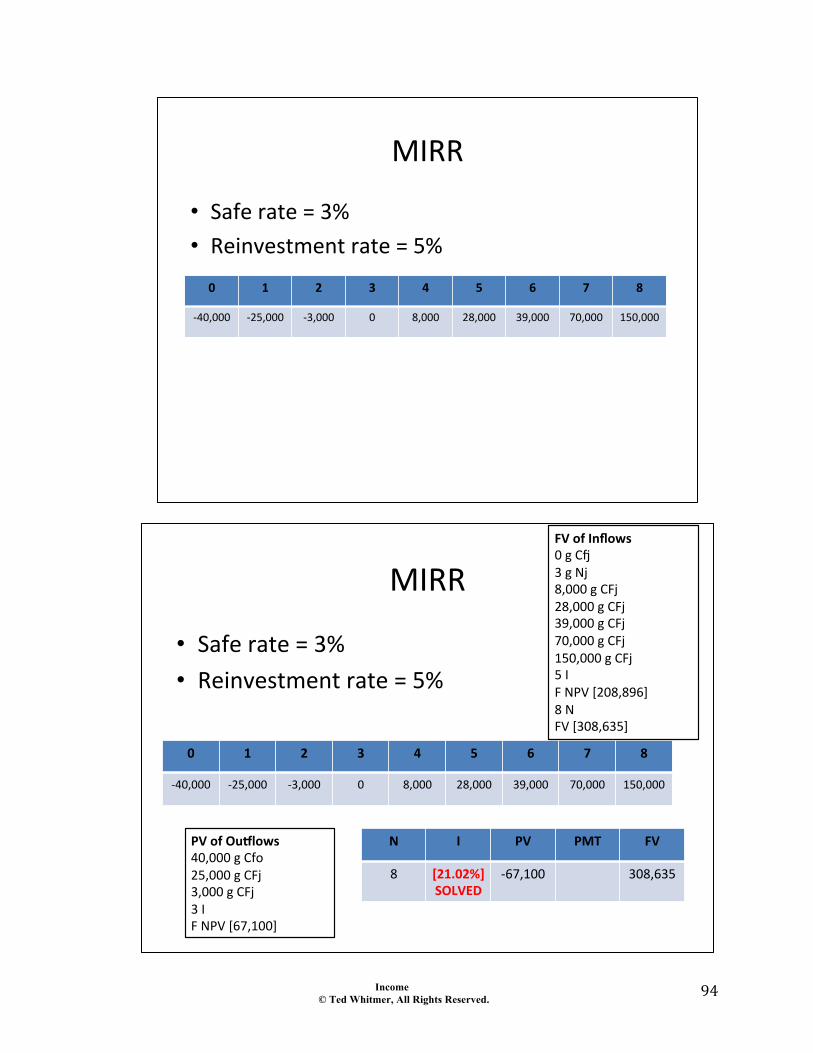

MIRR$

• Safe$rate$=$3%$• Reinvestment$rate$=$5%$

0" 1" 2" 3" 4" 5" 6" 7" 8"

440,000$ 425,000$ 43,000$ 0$ 8,000$ 28,000$ 39,000$ 70,000$ 150,000$

MIRR$

• Safe$rate$=$3%$• Reinvestment$rate$=$5%$

0" 1" 2" 3" 4" 5" 6" 7" 8"

440,000$ 425,000$ 43,000$ 0$ 8,000$ 28,000$ 39,000$ 70,000$ 150,000$

PV"of"Ou1lows"40,000$g$Cfo$25,000$g$CFj$3,000$g$CFj$3$I$$F$NPV$[67,100]$

FV"of"Inflows"0$g$CH$3$g$Nj$8,000$g$CFj$28,000$g$CFj$39,000$g$CFj$70,000$g$CFj$150,000$g$CFj$5$I$F$NPV$[208,896]$8$N$$FV$[308,635]$

N" I" PV" PMT" FV"

8$ [21.02%]"SOLVED"

467,100$ 308,635$

Income © Ted Whitmer, All Rights Reserved.

95"

MIRR$$$

3$

Income © Ted Whitmer, All Rights Reserved.

96"

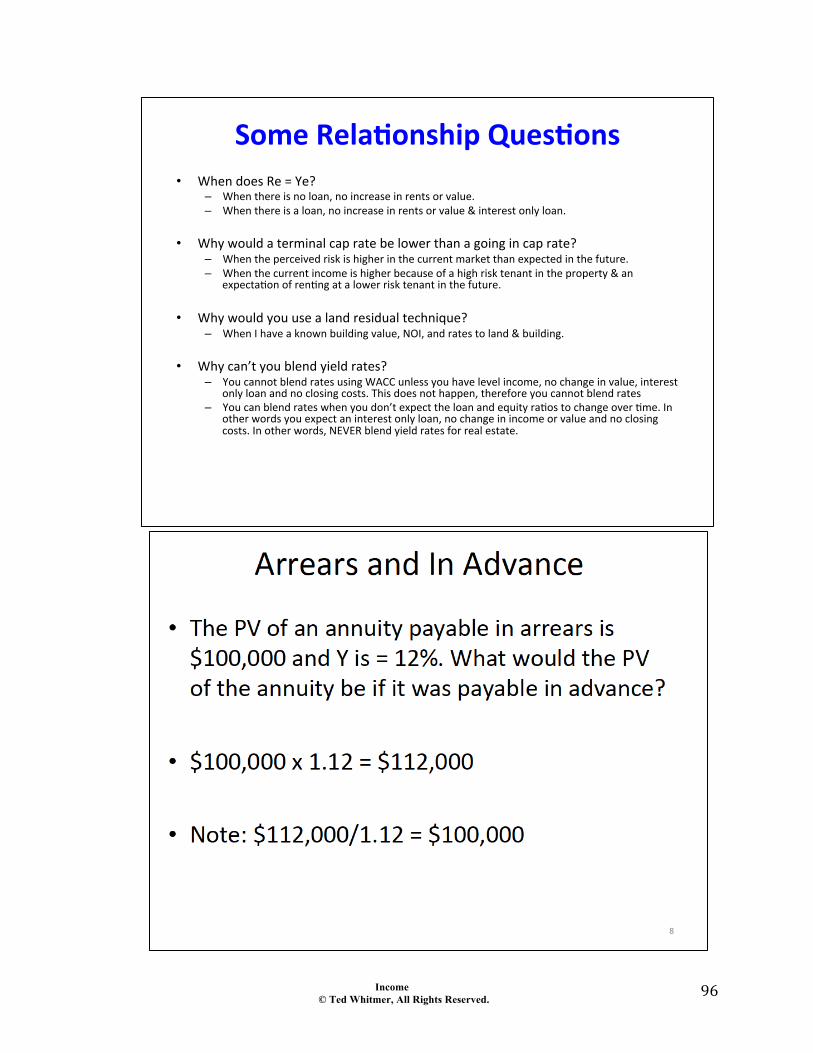

Some%Rela)onship%Ques)ons%%• When%does%Re%=%Ye?%

– When%there%is%no%loan,%no%increase%in%rents%or%value.%– When%there%is%a%loan,%no%increase%in%rents%or%value%&%interest%only%loan.%

%• Why%would%a%terminal%cap%rate%be%lower%than%a%going%in%cap%rate?%

– When%the%perceived%risk%is%higher%in%the%current%market%than%expected%in%the%future.%– When%the%current%income%is%higher%because%of%a%high%risk%tenant%in%the%property%&%an%

expectaAon%of%renAng%at%a%lower%risk%tenant%in%the%future.%%• Why%would%you%use%a%land%residual%technique?%

– When%I%have%a%known%building%value,%NOI,%and%rates%to%land%&%building.%

• Why%can’t%you%blend%yield%rates?%– You%cannot%blend%rates%using%WACC%unless%you%have%level%income,%no%change%in%value,%interest%

only%loan%and%no%closing%costs.%This%does%not%happen,%therefore%you%cannot%blend%rates%– You%can%blend%rates%when%you%don’t%expect%the%loan%and%equity%raAos%to%change%over%Ame.%In%

other%words%you%expect%an%interest%only%loan,%no%change%in%income%or%value%and%no%closing%costs.%In%other%words,%NEVER%blend%yield%rates%for%real%estate.%

8"

Income © Ted Whitmer, All Rights Reserved.

97"

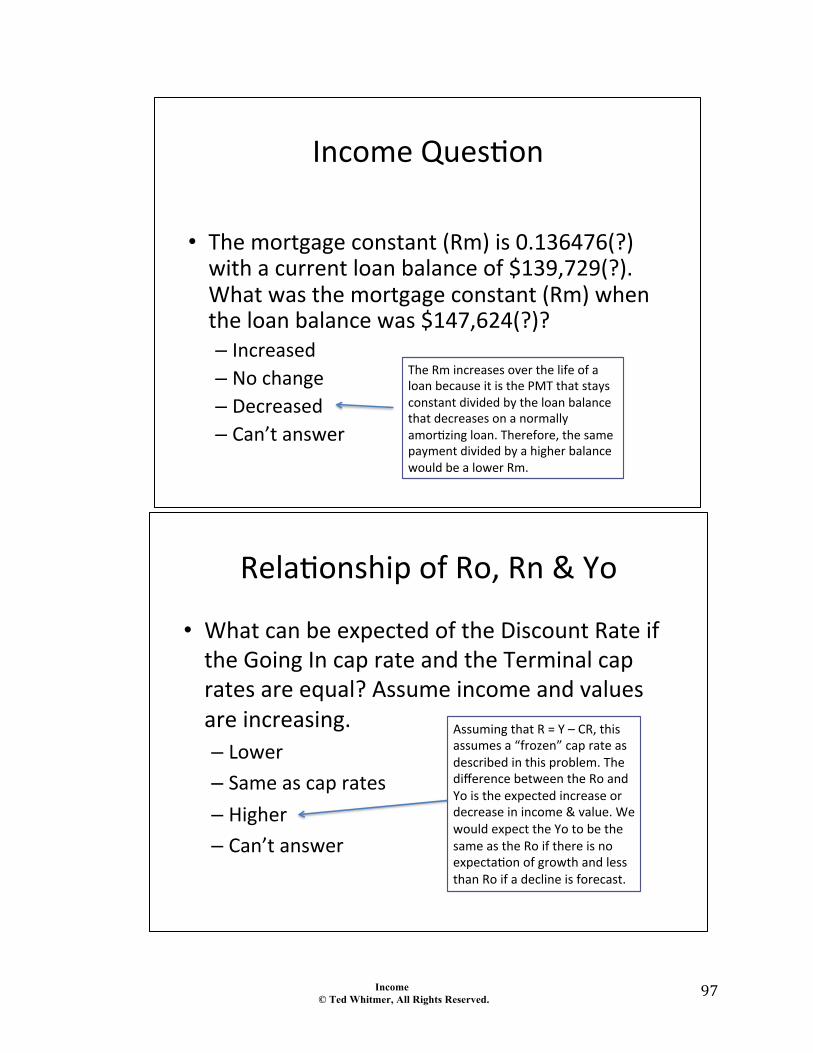

Income'Ques+on'

'• The'mortgage'constant'(Rm)'is'0.136476(?)'with'a'current'loan'balance'of'$139,729(?).''What'was'the'mortgage'constant'(Rm)'when'the'loan'balance'was'$147,624(?)?'– Increased'– No'change'– Decreased'– Can’t'answer'

The'Rm'increases'over'the'life'of'a'loan'because'it'is'the'PMT'that'stays'constant'divided'by'the'loan'balance'that'decreases'on'a'normally'amor+zing'loan.'Therefore,'the'same'payment'divided'by'a'higher'balance'would'be'a'lower'Rm.'

Rela%onship,of,Ro,,Rn,&,Yo,

• What,can,be,expected,of,the,Discount,Rate,if,the,Going,In,cap,rate,and,the,Terminal,cap,rates,are,equal?,Assume,income,and,values,are,increasing.,– Lower,– Same,as,cap,rates,– Higher,– Can’t,answer,

Assuming,that,R,=,Y,–,CR,,this,assumes,a,“frozen”,cap,rate,as,described,in,this,problem.,The,difference,between,the,Ro,and,Yo,is,the,expected,increase,or,decrease,in,income,&,value.,We,would,expect,the,Yo,to,be,the,same,as,the,Ro,if,there,is,no,expecta%on,of,growth,and,less,than,Ro,if,a,decline,is,forecast.,

Income © Ted Whitmer, All Rights Reserved.

98"

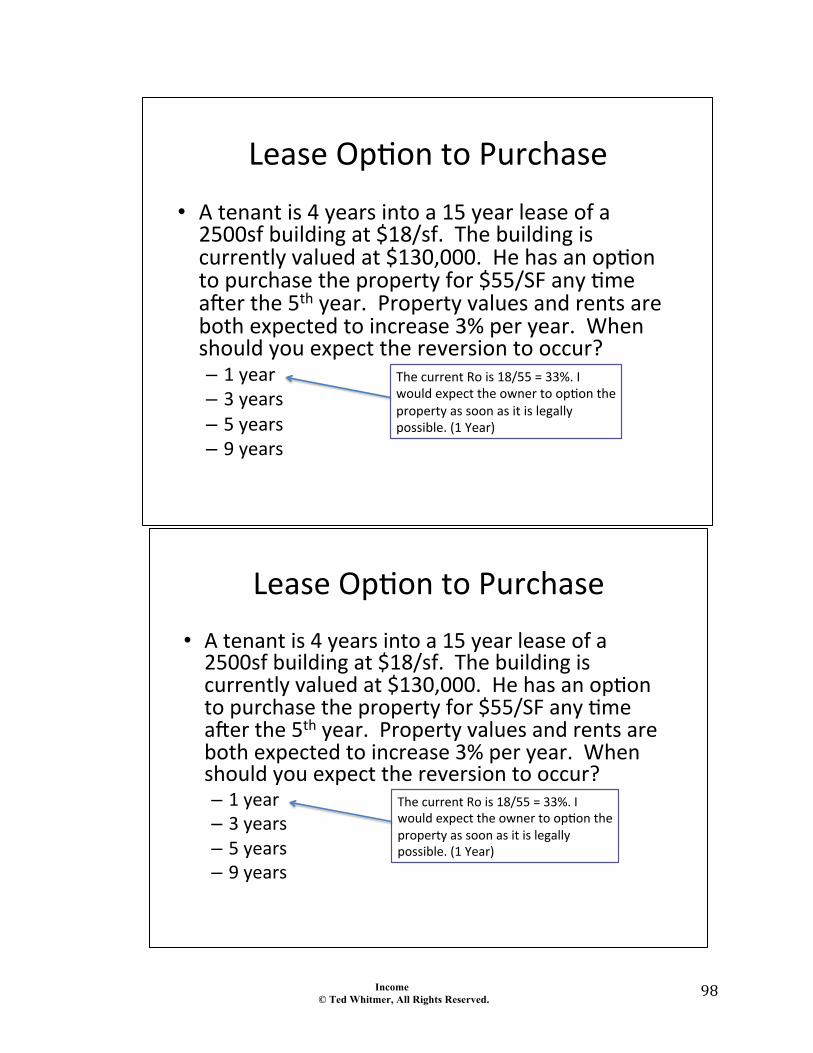

Lease%Op(on%to%Purchase%• A%tenant%is%4%years%into%a%15%year%lease%of%a%2500sf%building%at%$18/sf.%%The%building%is%currently%valued%at%$130,000.%%He%has%an%op(on%to%purchase%the%property%for%$55/SF%any%(me%aJer%the%5th%year.%%Property%values%and%rents%are%both%expected%to%increase%3%%per%year.%%When%should%you%expect%the%reversion%to%occur?%– 1%year%– 3%years%– 5%years%%– 9%years%

The%current%Ro%is%18/55%=%33%.%I%would%expect%the%owner%to%op(on%the%property%as%soon%as%it%is%legally%possible.%(1%Year)%

Lease%Op(on%to%Purchase%• A%tenant%is%4%years%into%a%15%year%lease%of%a%2500sf%building%at%$18/sf.%%The%building%is%currently%valued%at%$130,000.%%He%has%an%op(on%to%purchase%the%property%for%$55/SF%any%(me%aJer%the%5th%year.%%Property%values%and%rents%are%both%expected%to%increase%3%%per%year.%%When%should%you%expect%the%reversion%to%occur?%– 1%year%– 3%years%– 5%years%%– 9%years%

The%current%Ro%is%18/55%=%33%.%I%would%expect%the%owner%to%op(on%the%property%as%soon%as%it%is%legally%possible.%(1%Year)%

Income © Ted Whitmer, All Rights Reserved.

99"

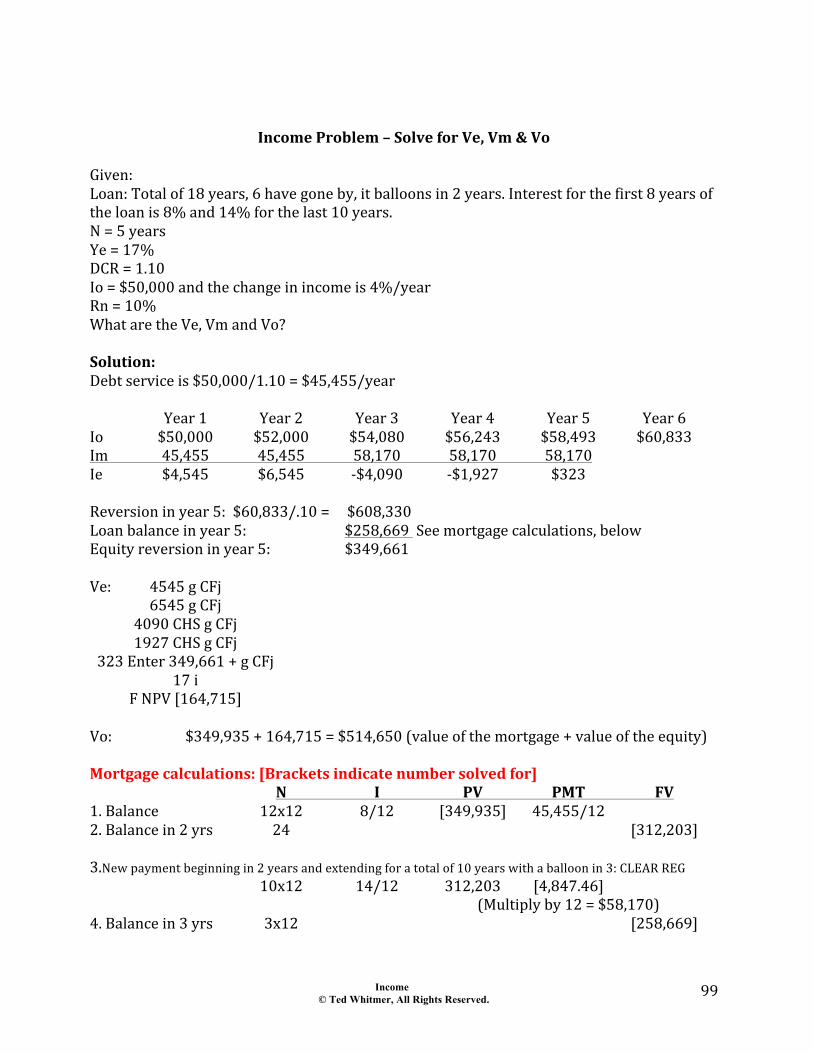

Income$Problem$–$Solve$for$Ve,$Vm$&$Vo$$

Given:"Loan:"Total"of"18"years,"6"have"gone"by,"it"balloons"in"2"years."Interest"for"the"first"8"years"of"the"loan"is"8%"and"14%"for"the"last"10"years."N"="5"years"Ye"="17%"DCR"="1.10"Io"="$50,000"and"the"change"in"income"is"4%/year"Rn"="10%"What"are"the"Ve,"Vm"and"Vo?""Solution:$Debt"service"is"$50,000/1.10"="$45,455/year""" Year"1" Year"2" Year"3" Year"4" Year"5" Year"6"Io" $50,000" $52,000" $54,080" $56,243" $58,493" $60,833"Im" 45,455" 45,455" 58,170" 58,170" 58,170" "Ie" $4,545" $6,545" V$4,090" V$1,927" $323""Reversion"in"year"5:""$60,833/.10"="""""$608,330"Loan"balance"in"year"5:" " $258,669""See"mortgage"calculations,"below"Equity"reversion"in"year"5:" " $349,661""Ve:"" 4545"g"CFj"" 6545"g"CFj"" 4090"CHS"g"CFj"" 1927"CHS"g"CFj"" 323"Enter"349,661"+"g"CFj"" 17"i"" F"NPV"[164,715]""Vo:" $349,935"+"164,715"="$514,650"(value"of"the"mortgage"+"value"of"the"equity)""Mortgage$calculations:$[Brackets$indicate$number$solved$for]$" N$ I$ PV$ PMT$ FV$1."Balance" 12x12" 8/12" [349,935]" 45,455/12"2."Balance"in"2"yrs" 24" " " " [312,203]""3.New"payment"beginning"in"2"years"and"extending"for"a"total"of"10"years"with"a"balloon"in"3:"CLEAR"REG"" 10x12" 14/12" 312,203" [4,847.46]"" " " "(Multiply"by"12"="$58,170)"4."Balance"in"3"yrs" 3x12" " " " [258,669]" ""

ProblemsIncome ApproachIncome Approach

Direct capitalizationDirect capitalizationYield capitalizationRate relationships

i l iPartial interestsMixed problem set oneMixed problem set twopMixed problem set threeAdditional problemsA Nasty hard problemA Nasty hard problem

100

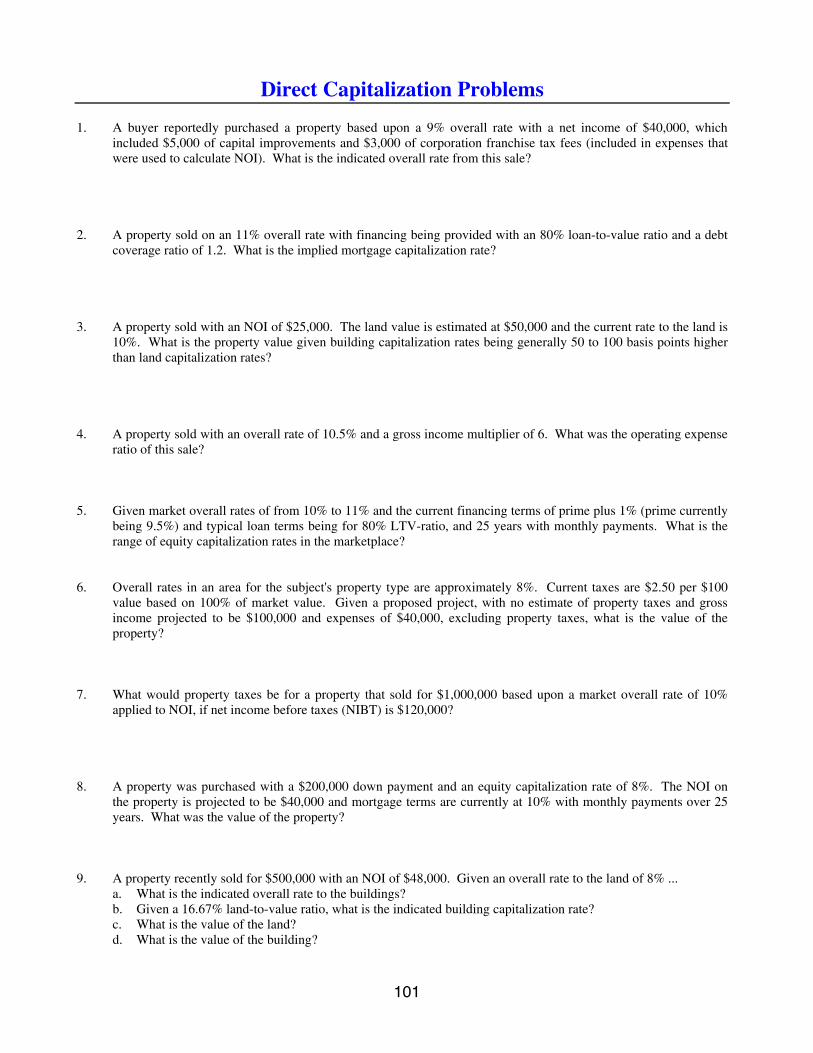

Direct Capitalization Problems 1. A buyer reportedly purchased a property based upon a 9% overall rate with a net income of $40,000, which

included $5,000 of capital improvements and $3,000 of corporation franchise tax fees (included in expenses that were used to calculate NOI). What is the indicated overall rate from this sale?

2. A property sold on an 11% overall rate with financing being provided with an 80% loan-to-value ratio and a debt

coverage ratio of 1.2. What is the implied mortgage capitalization rate? 3. A property sold with an NOI of $25,000. The land value is estimated at $50,000 and the current rate to the land is

10%. What is the property value given building capitalization rates being generally 50 to 100 basis points higher than land capitalization rates?

4. A property sold with an overall rate of 10.5% and a gross income multiplier of 6. What was the operating expense

ratio of this sale? 5. Given market overall rates of from 10% to 11% and the current financing terms of prime plus 1% (prime currently

being 9.5%) and typical loan terms being for 80% LTV-ratio, and 25 years with monthly payments. What is the range of equity capitalization rates in the marketplace?

6. Overall rates in an area for the subject's property type are approximately 8%. Current taxes are $2.50 per $100

value based on 100% of market value. Given a proposed project, with no estimate of property taxes and gross income projected to be $100,000 and expenses of $40,000, excluding property taxes, what is the value of the property?

7. What would property taxes be for a property that sold for $1,000,000 based upon a market overall rate of 10%

applied to NOI, if net income before taxes (NIBT) is $120,000? 8. A property was purchased with a $200,000 down payment and an equity capitalization rate of 8%. The NOI on

the property is projected to be $40,000 and mortgage terms are currently at 10% with monthly payments over 25 years. What was the value of the property?

9. A property recently sold for $500,000 with an NOI of $48,000. Given an overall rate to the land of 8% ... a. What is the indicated overall rate to the buildings? b. Given a 16.67% land-to-value ratio, what is the indicated building capitalization rate? c. What is the value of the land? d. What is the value of the building?

101

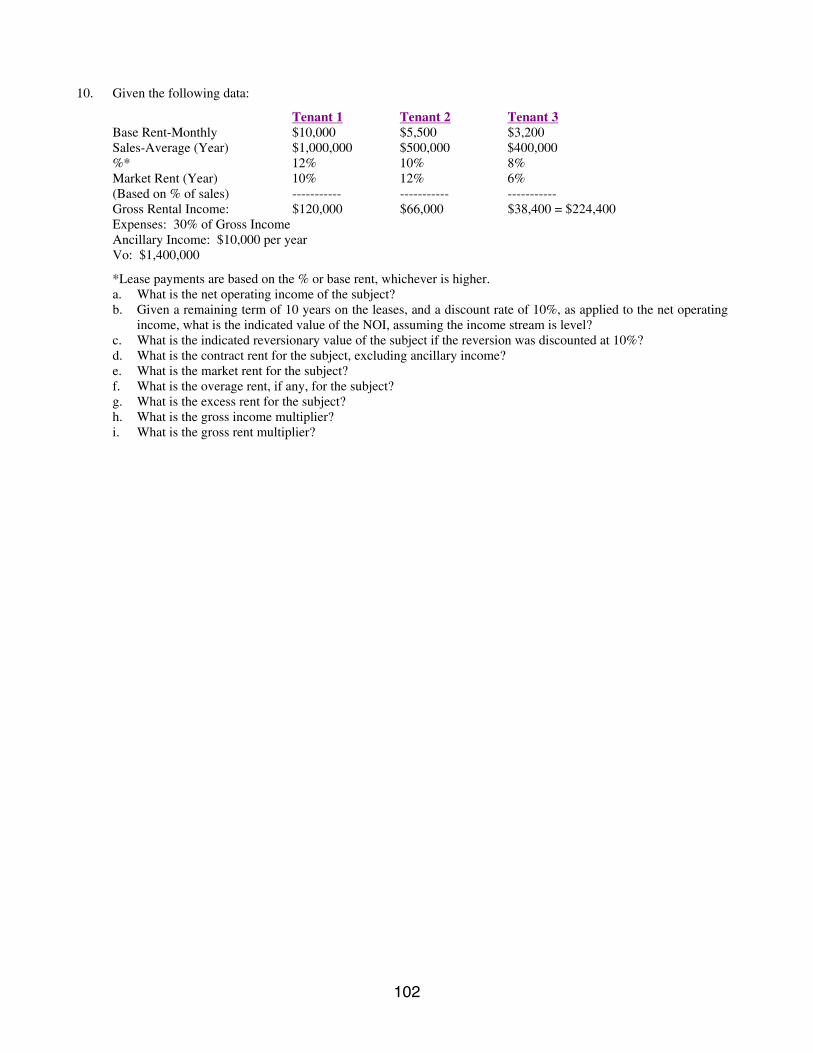

10. Given the following data:

Tenant 1 Tenant 2 Tenant 3 Base Rent-Monthly $10,000 $5,500 $3,200 Sales-Average (Year) $1,000,000 $500,000 $400,000 %* 12% 10% 8% Market Rent (Year) 10% 12% 6% (Based on % of sales) ----------- ----------- ----------- Gross Rental Income: $120,000 $66,000 $38,400 = $224,400 Expenses: 30% of Gross Income Ancillary Income: $10,000 per year Vo: $1,400,000

*Lease payments are based on the % or base rent, whichever is higher. a. What is the net operating income of the subject? b. Given a remaining term of 10 years on the leases, and a discount rate of 10%, as applied to the net operating

income, what is the indicated value of the NOI, assuming the income stream is level? c. What is the indicated reversionary value of the subject if the reversion was discounted at 10%? d. What is the contract rent for the subject, excluding ancillary income? e. What is the market rent for the subject? f. What is the overage rent, if any, for the subject? g. What is the excess rent for the subject? h. What is the gross income multiplier? i. What is the gross rent multiplier?

102

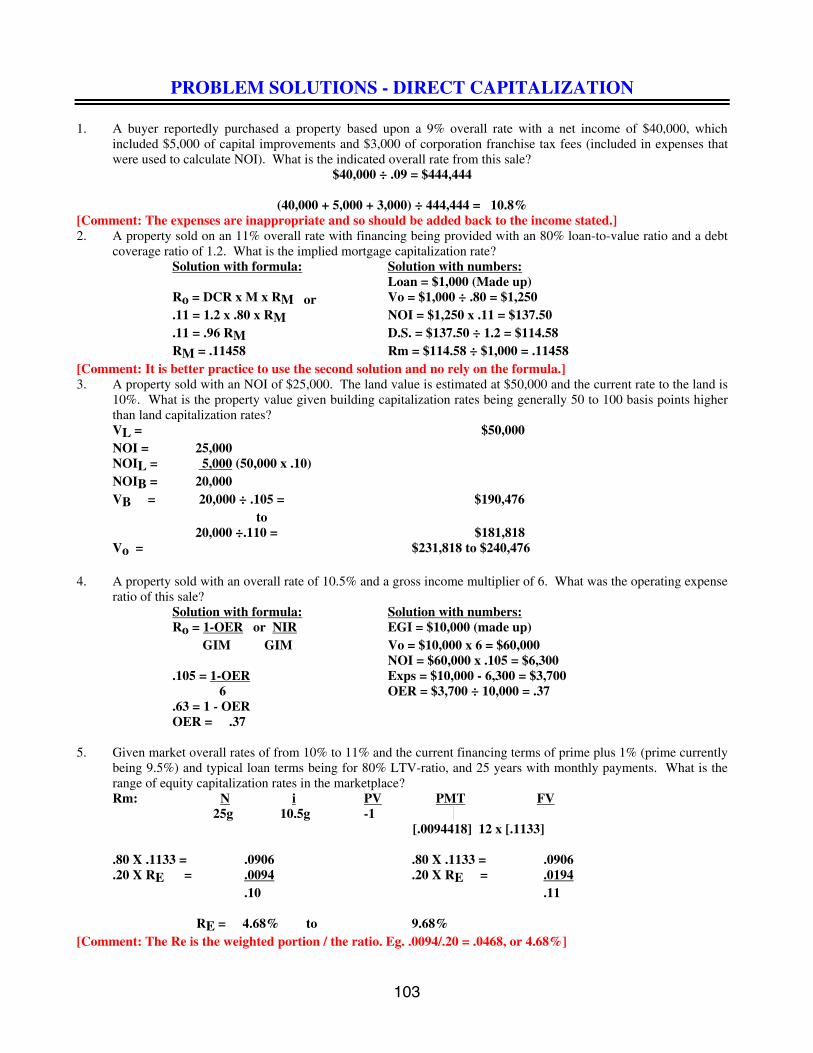

PROBLEM SOLUTIONS - DIRECT CAPITALIZATION

1. A buyer reportedly purchased a property based upon a 9% overall rate with a net income of $40,000, which included $5,000 of capital improvements and $3,000 of corporation franchise tax fees (included in expenses that were used to calculate NOI). What is the indicated overall rate from this sale?

$40,000 ÷ .09 = $444,444

(40,000 + 5,000 + 3,000) ÷ 444,444 = 10.8% [Comment: The expenses are inappropriate and so should be added back to the income stated.] 2. A property sold on an 11% overall rate with financing being provided with an 80% loan-to-value ratio and a debt

coverage ratio of 1.2. What is the implied mortgage capitalization rate? Solution with formula: Solution with numbers: Loan = $1,000 (Made up) Ro = DCR x M x RM or Vo = $1,000 ÷ .80 = $1,250 .11 = 1.2 x .80 x RM NOI = $1,250 x .11 = $137.50 .11 = .96 RM D.S. = $137.50 ÷ 1.2 = $114.58 RM = .11458 Rm = $114.58 ÷ $1,000 = .11458 [Comment: It is better practice to use the second solution and no rely on the formula.] 3. A property sold with an NOI of $25,000. The land value is estimated at $50,000 and the current rate to the land is

10%. What is the property value given building capitalization rates being generally 50 to 100 basis points higher than land capitalization rates?

VL = $50,000 NOI = 25,000 NOIL = 5,000 (50,000 x .10) NOIB = 20,000 VB = 20,000 ÷ .105 = $190,476 to 20,000 ÷.110 = $181,818 Vo = $231,818 to $240,476 4. A property sold with an overall rate of 10.5% and a gross income multiplier of 6. What was the operating expense

ratio of this sale? Solution with formula: Solution with numbers: Ro = 1-OER or NIR EGI = $10,000 (made up) GIM GIM Vo = $10,000 x 6 = $60,000 NOI = $60,000 x .105 = $6,300 .105 = 1-OER Exps = $10,000 - 6,300 = $3,700 6 OER = $3,700 ÷ 10,000 = .37 .63 = 1 - OER OER = .37 5. Given market overall rates of from 10% to 11% and the current financing terms of prime plus 1% (prime currently

being 9.5%) and typical loan terms being for 80% LTV-ratio, and 25 years with monthly payments. What is the range of equity capitalization rates in the marketplace?

Rm: N i PV PMT FV 25g 10.5g -1 [.0094418] 12 x [.1133] .80 X .1133 = .0906 .80 X .1133 = .0906 .20 X RE = .0094 .20 X RE = .0194 .10 .11 RE = 4.68% to 9.68% [Comment: The Re is the weighted portion / the ratio. Eg. .0094/.20 = .0468, or 4.68%]

103

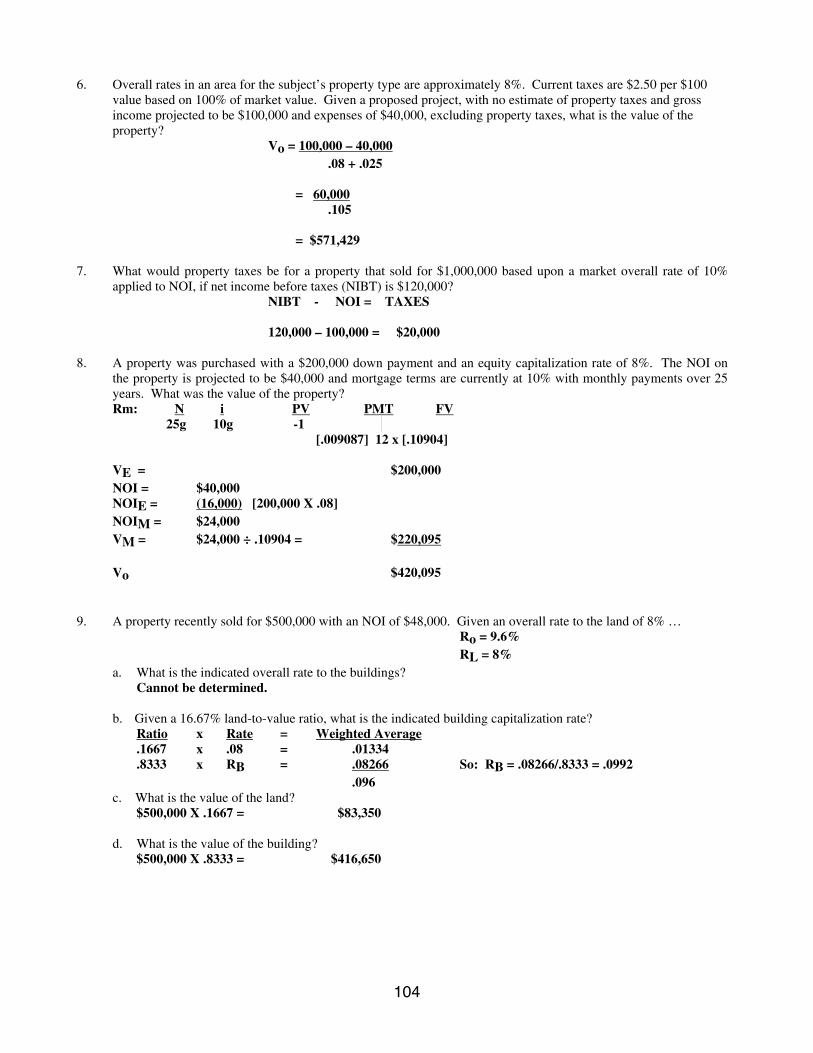

6. Overall rates in an area for the subject’s property type are approximately 8%. Current taxes are $2.50 per $100 value based on 100% of market value. Given a proposed project, with no estimate of property taxes and gross income projected to be $100,000 and expenses of $40,000, excluding property taxes, what is the value of the property?

Vo = 100,000 – 40,000 .08 + .025 = 60,000 .105 = $571,429 7. What would property taxes be for a property that sold for $1,000,000 based upon a market overall rate of 10%

applied to NOI, if net income before taxes (NIBT) is $120,000? NIBT - NOI = TAXES 120,000 – 100,000 = $20,000 8. A property was purchased with a $200,000 down payment and an equity capitalization rate of 8%. The NOI on

the property is projected to be $40,000 and mortgage terms are currently at 10% with monthly payments over 25 years. What was the value of the property?

Rm: N i PV PMT FV 25g 10g -1 [.009087] 12 x [.10904] VE = $200,000 NOI = $40,000 NOIE = (16,000) [200,000 X .08] NOIM = $24,000 VM = $24,000 ÷ .10904 = $220,095 Vo $420,095 9. A property recently sold for $500,000 with an NOI of $48,000. Given an overall rate to the land of 8% … Ro = 9.6% RL = 8% a. What is the indicated overall rate to the buildings? Cannot be determined.

b. Given a 16.67% land-to-value ratio, what is the indicated building capitalization rate? Ratio x Rate = Weighted Average .1667 x .08 = .01334 .8333 x RB = .08266 So: RB = .08266/.8333 = .0992 .096 c. What is the value of the land? $500,000 X .1667 = $83,350

d. What is the value of the building? $500,000 X .8333 = $416,650

104

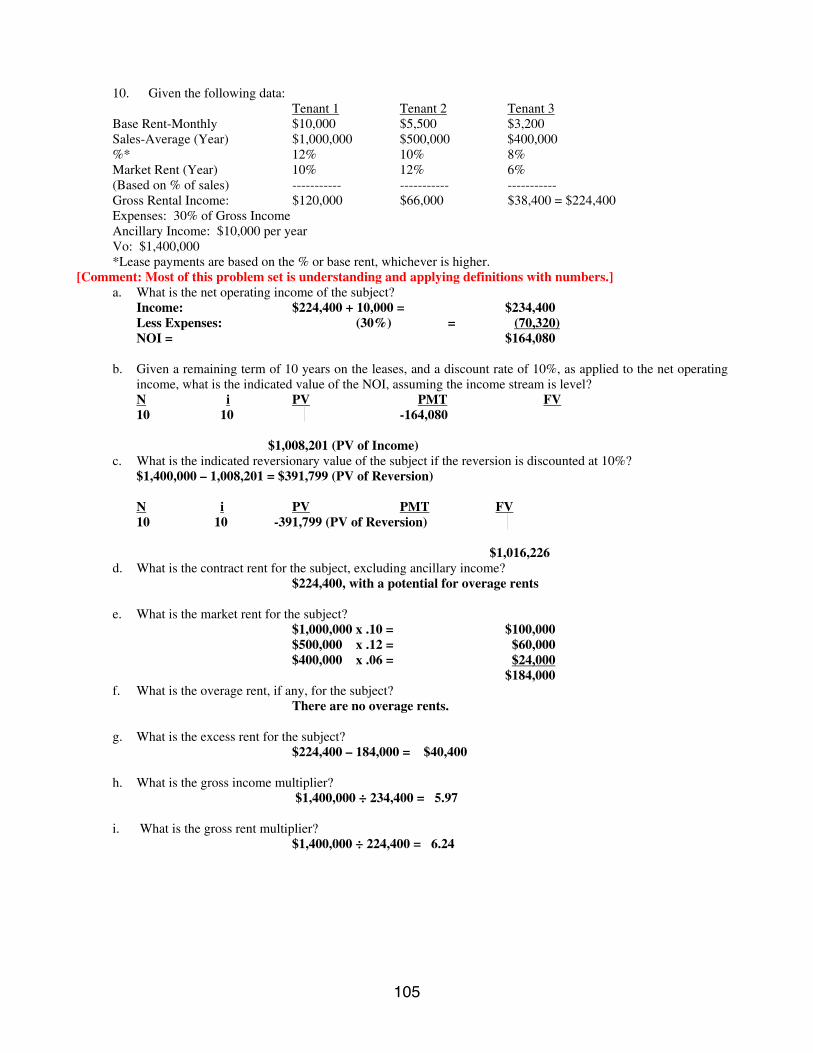

10. Given the following data: Tenant 1 Tenant 2 Tenant 3 Base Rent-Monthly $10,000 $5,500 $3,200 Sales-Average (Year) $1,000,000 $500,000 $400,000 %* 12% 10% 8% Market Rent (Year) 10% 12% 6% (Based on % of sales) ----------- ----------- ----------- Gross Rental Income: $120,000 $66,000 $38,400 = $224,400 Expenses: 30% of Gross Income Ancillary Income: $10,000 per year Vo: $1,400,000 *Lease payments are based on the % or base rent, whichever is higher. [Comment: Most of this problem set is understanding and applying definitions with numbers.]

a. What is the net operating income of the subject? Income: $224,400 + 10,000 = $234,400 Less Expenses: (30%) = (70,320) NOI = $164,080 b. Given a remaining term of 10 years on the leases, and a discount rate of 10%, as applied to the net operating

income, what is the indicated value of the NOI, assuming the income stream is level? N i PV PMT FV 10 10 -164,080 $1,008,201 (PV of Income) c. What is the indicated reversionary value of the subject if the reversion is discounted at 10%? $1,400,000 – 1,008,201 = $391,799 (PV of Reversion) N i PV PMT FV 10 10 -391,799 (PV of Reversion) $1,016,226 d. What is the contract rent for the subject, excluding ancillary income? $224,400, with a potential for overage rents

e. What is the market rent for the subject? $1,000,000 x .10 = $100,000 $500,000 x .12 = $60,000 $400,000 x .06 = $24,000 $184,000 f. What is the overage rent, if any, for the subject? There are no overage rents. g. What is the excess rent for the subject? $224,400 – 184,000 = $40,400 h. What is the gross income multiplier? $1,400,000 ÷ 234,400 = 5.97

i. What is the gross rent multiplier? $1,400,000 ÷ 224,400 = 6.24

105

PROBLEMS – YIELD CAPITALIZATION

1. Given NOI of $25,000 in year 1, a projection period of 10 years, and a yield rate of 10% … a. What is the present value (PV) of the income if the income stream is expected to continue into perpetuity? b. What is the PV of the income if the income stream is capitalized assuming the Inwood premise? c. What is the PV of the income stream assuming the Hoskold premise, and a safe rate of 5%? d. What is the PV of the income stream if expected to change in a straight-line pattern of $2,500 per year?

e. What is the PV of the income stream if expected to change at a constant ratio pattern of 5% per year?

2. Given NOI of $25,000, a projection period of 10 years and a yield of 10% … a. What is the present value of the property assuming a level income stream and no change in value over the holding

period? b. What is the present value of the property assuming a straight-line change in value of +25%, and level income? c. What is the indicated present value of the property assuming a straight-line change in value of 50% over the

holding period, and a corresponding change in income over the projection period? d. What is the income expected to be in year 3 given the above assumptions in part c.? e. What is the PV of the property assuming a change in property value of 50%, with a corresponding constant

ratio change in income and value to achieve the 50% increase over the projection period? f. What is the PV of the property assuming no change in income for the first 2 years, a 3% per year increase in

income for the next 4 years, a 5% increase per year in income over the remaining projection period and a property value change of +40% over the holding period?

3. Given an equity yield requirement of 13%, a projection period of 10 years, and an NOI of $40,000, value the

property given the following criteria … a. There is no loan, no change in property value or income expected over the projection period. b. A mortgage is available with a LTV-ratio of 70% at 10% interest for 25 years with monthly payments. c. In addition to the above mortgage, property value is expected to increase 10% over the projection period. d. In addition to the mortgage above and property increase, income is expected to increase at a rate of 5% per

year. (K-factor = 1.1982)

e. In addition to the above mortgage terms and increase in property value, income is expected to increase 40% over the projection period assuming a J-factor pattern of income. (J-factor = .352)

106

4. Identify, from the following information, which models and equations would be appropriate … a. The present value of 5 years of level lease payments given a yield rate of 12%. b. The present value of NOI in the following pattern: Year NOI 1 $10,000 2 $12,000 3 $14,000 4 $16,500 5 $19,000 c. Income and property value are expected to remain stable over the projection period. d. Income is expected to increase $500 per year, property value is expected to increase at a compound rate of

2% per year. e. Income is expected to remain level, however, the property is expected to decline in value by 10%. f. The investment rate is 12% and recapture of the investment is to be computed at 5%. 5. What do the following account for in the Ellwood Formula? a. M x P x SFF b. ∆o x SFF c. ∆IJ 6. Assuming an equity yield requirement of 15%, no mortgage, income expected to increase at a rate of 5%

per year, compounded, property value expected to increase 30% over the projection period (5 years), what is the indicated overall rate? (K-factor = 1.0902)

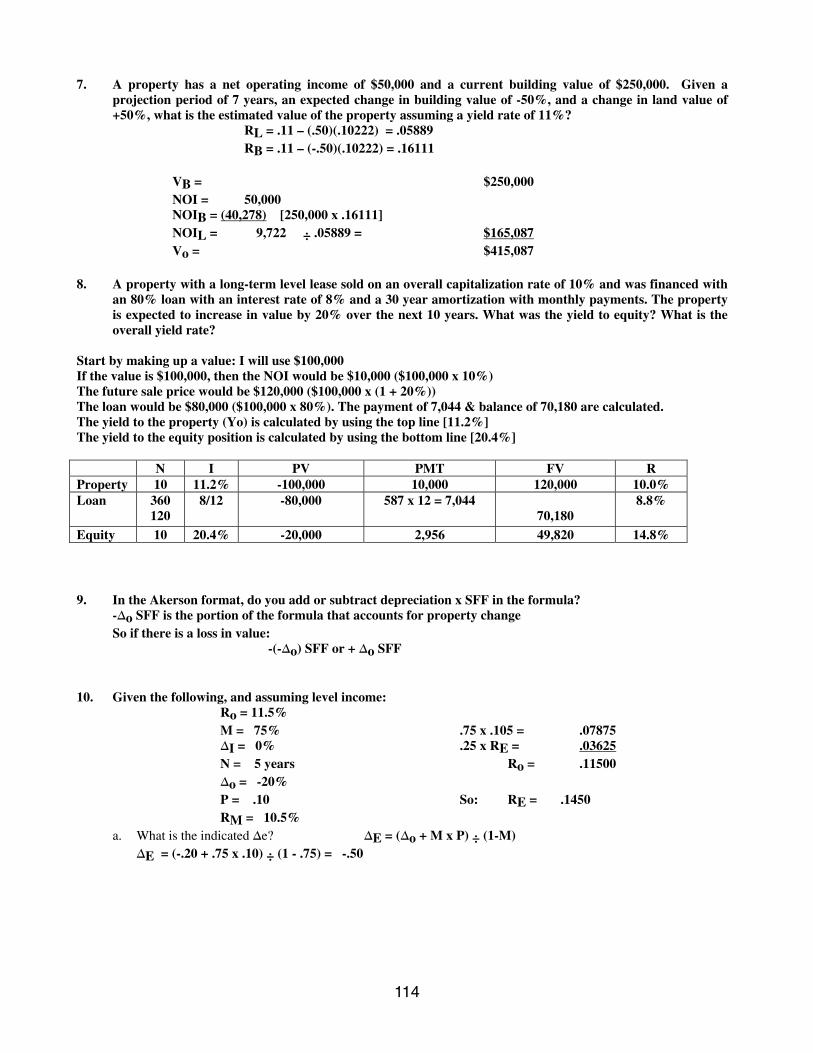

7. A property has a net operating income of $50,000 and a current building value of $250,000. Given a

projection period of 7 years, an expected change in building value of -50%, and a change in land value of +50%, what is the estimated value of the property assuming a yield rate of 11%?

8. A property with a long-term level lease sold on an overall capitalization rate of 10% and was financed with

an 80% loan with an interest rate of 8% and a 30 year amortization with monthly payments. The property is expected to increase in value by 20% over the next 10 years. What was the yield to equity? What is the overall yield rate?

9. In the Akerson format, do you add or subtract depreciation x SFF in the formula?

107

10. Given the following, and assuming level income: Ro = 11.5% M = 75% ∆I = 0% N = 5 years ∆o = -20% P = .10 RM = 10.5% a. What is the indicated ∆e?

b. What is the indicated Ye? 11. The following are the terms of a lease. The sales are $2,500,000. $20,000 base + sales in excess of percentage rent $1,000,000 2% $2,000,000 3% $3,000,000 4% a. What is the income for the above lease that is owed to the lessor? b. Assuming sales will increase at 5%/year, what is the overall property yield with overall rates ranging from

8% to 9% for sales of similar properties? What would the yield to equity be if the property were purchased for all cash?

12. Given a 10 year lease that was negotiated with $15 tenant finish, $15 psf rents and increasing 3%/year.

What would the equivalent rental rate be for a similar property, but the owner offers $20 tenant finish and a 10 year level lease? Assume Yo = 13%.

13. A property with NOI of $20,000 is expected to have a stable income for 2 years, a 5% increase in NOI

compounded each year throughout the next 3 years, and a 4% increase in NOI up through year 8. A 7 year discounted cash flow was utilized to derive a value estimate for this property. The current capitalization rate for similar properties is 12% and the terminal capitalization rate is 25 basis points higher than the current capitalization rate. Additionally, 6% expenses of sale are expected in the terminal year.

a. What is the indicated value of the subject given a discount rate of 12%?

b. What is the before tax yield to equity assuming a loan being available for 70% of value, with terms being 10.5%, for 30 years with annual payments?

c. Assuming straight-line depreciation for 31.5 years (tax depreciation), and land being 20% of total value what is the indicated after tax yield to equity if the marginal tax bracket is 28% and average taxes paid by an investor are 20%? Treat reserves for replacement as an expense.

d. Compare the value derived from the DCF, and from direct capitalization. Are they consistent?

108

14. A property with an NOI of $25,000 per year was sold based upon a 10 year projection and a discount rate applied to the NOI at 10% and the discount rate to the reversion at 12%. NOI is expected to remain level throughout the projection period.

a. What is the expected reversionary value if the value of the property is $275,000?

b. What would be the compound rate of property increase or decrease per year to indicate the future value of the property?

c. When would property increase in value over a projection period, even though NOI remains level?

d. When would it be appropriate to have a higher reversionary yield rate than the yield rate applied to NOI?

e. When would it be appropriate to have a higher yield rate to NOI than applied to the reversionary value? 15. Stock was recently purchased at $100 per share. Dividends begin at $5.00 per share and are expected to

increase by $1.00 per share per year over the next 8 years. Given an investor requirement of 14% (yield), what is the expected sales price of the stock in 8 years?

109

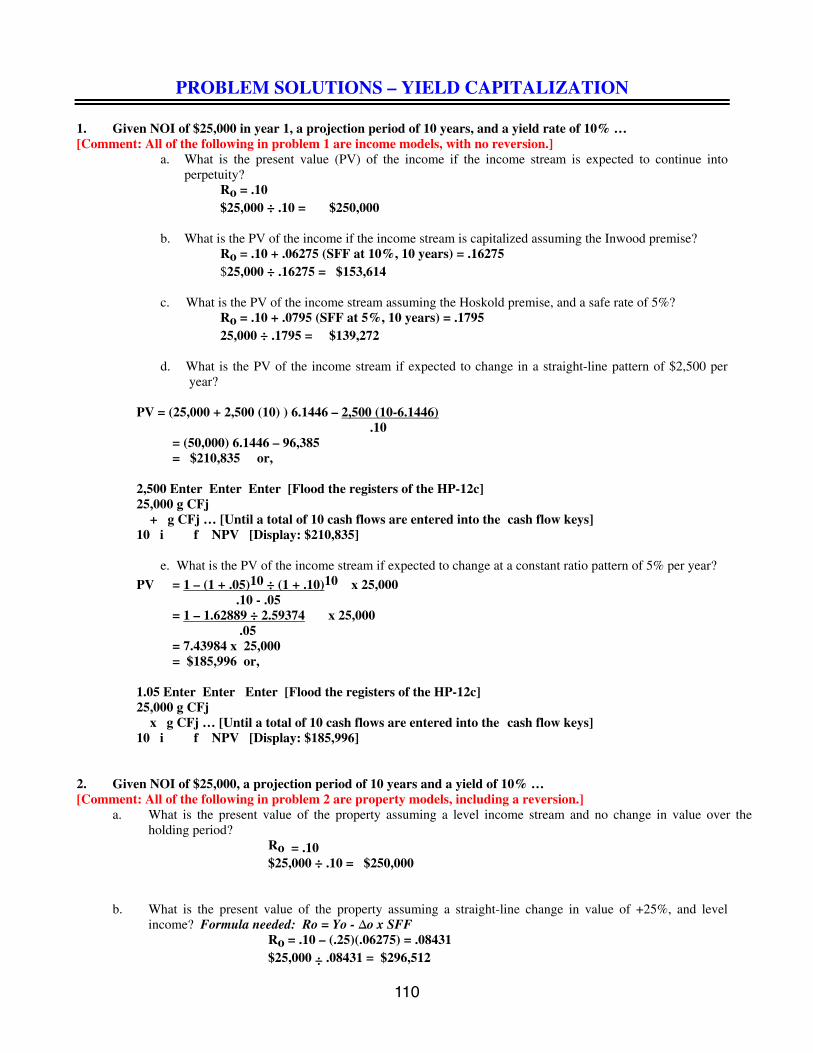

PROBLEM SOLUTIONS – YIELD CAPITALIZATION 1. Given NOI of $25,000 in year 1, a projection period of 10 years, and a yield rate of 10% … [Comment: All of the following in problem 1 are income models, with no reversion.]

a. What is the present value (PV) of the income if the income stream is expected to continue into perpetuity?

Ro = .10 $25,000 ÷ .10 = $250,000

b. What is the PV of the income if the income stream is capitalized assuming the Inwood premise? Ro = .10 + .06275 (SFF at 10%, 10 years) = .16275 $25,000 ÷ .16275 = $153,614 c. What is the PV of the income stream assuming the Hoskold premise, and a safe rate of 5%? Ro = .10 + .0795 (SFF at 5%, 10 years) = .1795 25,000 ÷ .1795 = $139,272

d. What is the PV of the income stream if expected to change in a straight-line pattern of $2,500 per year?

PV = (25,000 + 2,500 (10) ) 6.1446 – 2,500 (10-6.1446) .10 = (50,000) 6.1446 – 96,385 = $210,835 or, 2,500 Enter Enter Enter [Flood the registers of the HP-12c] 25,000 g CFj + g CFj … [Until a total of 10 cash flows are entered into the cash flow keys] 10 i f NPV [Display: $210,835]

e. What is the PV of the income stream if expected to change at a constant ratio pattern of 5% per year?

PV = 1 – (1 + .05)10 ÷ (1 + .10)10 x 25,000 .10 - .05 = 1 – 1.62889 ÷ 2.59374 x 25,000 .05 = 7.43984 x 25,000 = $185,996 or, 1.05 Enter Enter Enter [Flood the registers of the HP-12c] 25,000 g CFj x g CFj … [Until a total of 10 cash flows are entered into the cash flow keys] 10 i f NPV [Display: $185,996] 2. Given NOI of $25,000, a projection period of 10 years and a yield of 10% … [Comment: All of the following in problem 2 are property models, including a reversion.]

a. What is the present value of the property assuming a level income stream and no change in value over the holding period?

Ro = .10 $25,000 ÷ .10 = $250,000 b. What is the present value of the property assuming a straight-line change in value of +25%, and level

income? Formula needed: Ro = Yo - ∆o x SFF Ro = .10 – (.25)(.06275) = .08431 $25,000 ÷ .08431 = $296,512

110

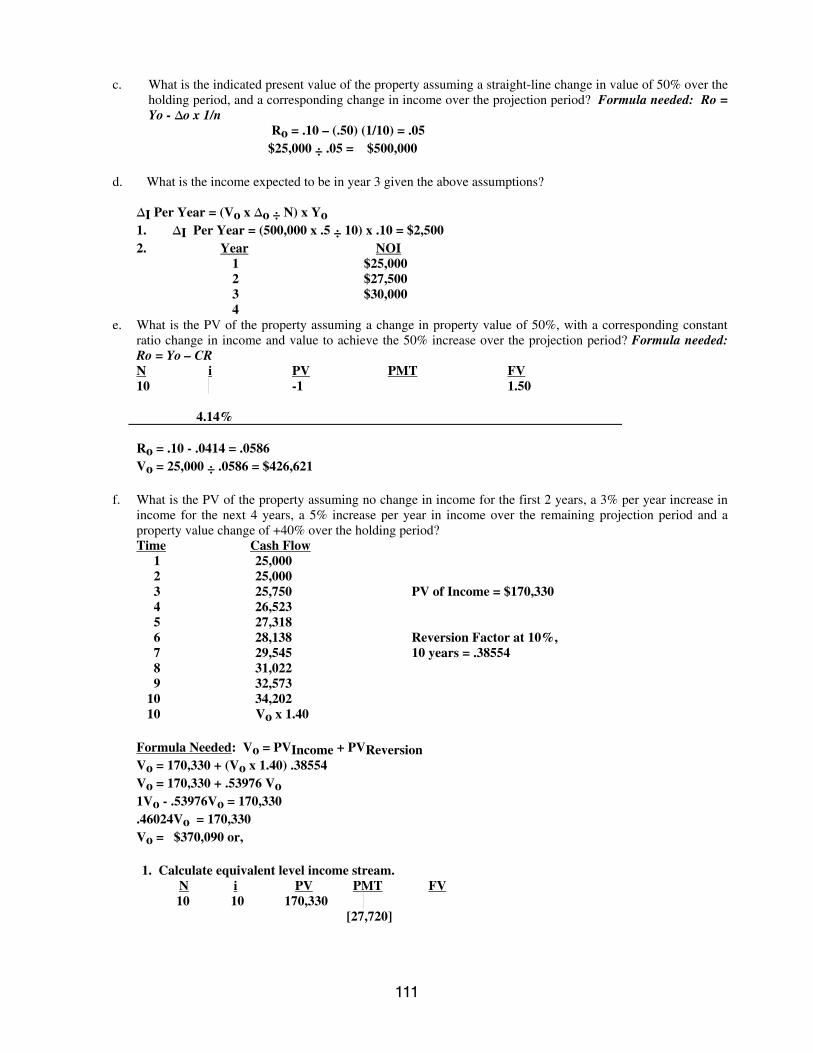

c. What is the indicated present value of the property assuming a straight-line change in value of 50% over the holding period, and a corresponding change in income over the projection period? Formula needed: Ro = Yo - ∆o x 1/n

Ro = .10 – (.50) (1/10) = .05 $25,000 ÷ .05 = $500,000

d. What is the income expected to be in year 3 given the above assumptions? ∆I Per Year = (Vo x ∆o ÷ N) x Yo 1. ∆I Per Year = (500,000 x .5 ÷ 10) x .10 = $2,500 2. Year NOI 1 $25,000 2 $27,500

3 $30,000 4

e. What is the PV of the property assuming a change in property value of 50%, with a corresponding constant ratio change in income and value to achieve the 50% increase over the projection period? Formula needed: Ro = Yo – CR

N i PV PMT FV 10 -1 1.50

4.14% Ro = .10 - .0414 = .0586 Vo = 25,000 ÷ .0586 = $426,621 f. What is the PV of the property assuming no change in income for the first 2 years, a 3% per year increase in

income for the next 4 years, a 5% increase per year in income over the remaining projection period and a property value change of +40% over the holding period?

Time Cash Flow 1 25,000 2 25,000 3 25,750 PV of Income = $170,330 4 26,523 5 27,318 6 28,138 Reversion Factor at 10%, 7 29,545 10 years = .38554 8 31,022 9 32,573 10 34,202 10 Vo x 1.40 Formula Needed: Vo = PVIncome + PVReversion Vo = 170,330 + (Vo x 1.40) .38554 Vo = 170,330 + .53976 Vo 1Vo - .53976Vo = 170,330 .46024Vo = 170,330 Vo = $370,090 or, 1. Calculate equivalent level income stream. N i PV PMT FV 10 10 170,330 [27,720]

111

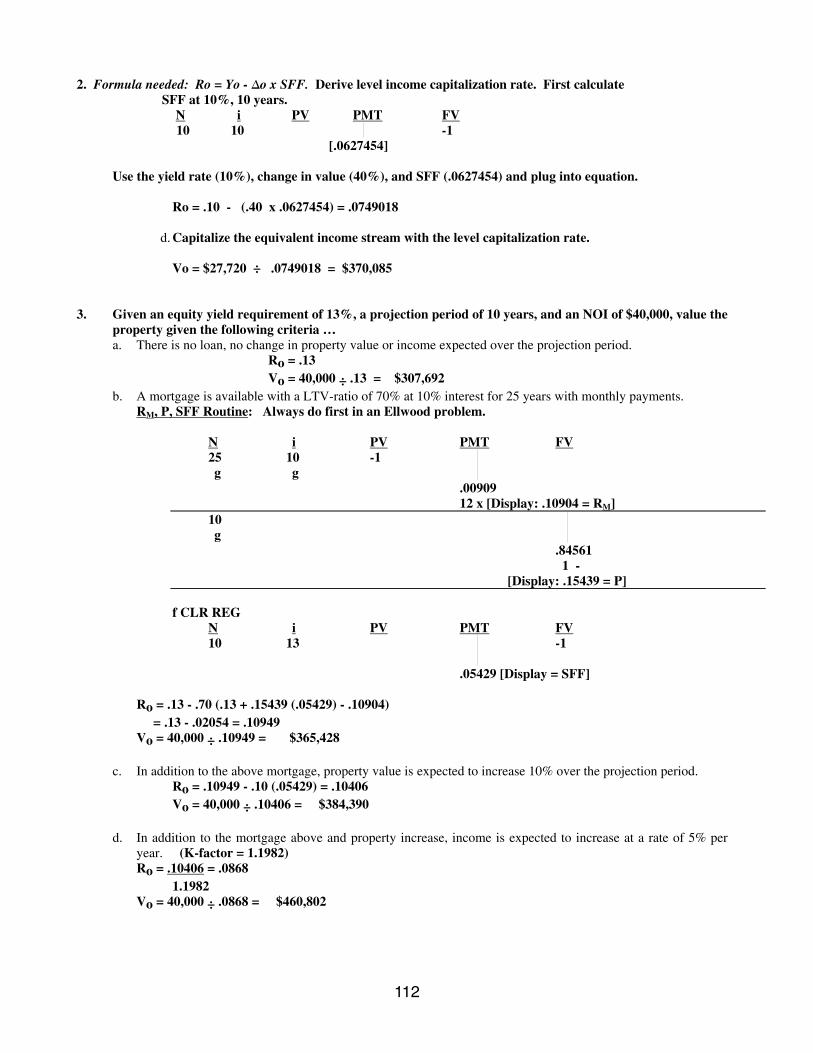

2. Formula needed: Ro = Yo - ∆o x SFF. Derive level income capitalization rate. First calculate SFF at 10%, 10 years.

N i PV PMT FV 10 10 -1 [.0627454] Use the yield rate (10%), change in value (40%), and SFF (.0627454) and plug into equation. Ro = .10 - (.40 x .0627454) = .0749018

d. Capitalize the equivalent income stream with the level capitalization rate. Vo = $27,720 ÷ .0749018 = $370,085 3. Given an equity yield requirement of 13%, a projection period of 10 years, and an NOI of $40,000, value the

property given the following criteria … a. There is no loan, no change in property value or income expected over the projection period. Ro = .13 Vo = 40,000 ÷ .13 = $307,692 b. A mortgage is available with a LTV-ratio of 70% at 10% interest for 25 years with monthly payments. RM, P, SFF Routine: Always do first in an Ellwood problem. N i PV PMT FV 25 10 -1 g g .00909

12 x [Display: .10904 = RM] 10 g .84561 1 -

[Display: .15439 = P] f CLR REG

N i PV PMT FV 10 13 -1 .05429 [Display = SFF] Ro = .13 - .70 (.13 + .15439 (.05429) - .10904) = .13 - .02054 = .10949 Vo = 40,000 ÷ .10949 = $365,428

c. In addition to the above mortgage, property value is expected to increase 10% over the projection period. Ro = .10949 - .10 (.05429) = .10406 Vo = 40,000 ÷ .10406 = $384,390 d. In addition to the mortgage above and property increase, income is expected to increase at a rate of 5% per

year. (K-factor = 1.1982) Ro = .10406 = .0868 1.1982 Vo = 40,000 ÷ .0868 = $460,802

112

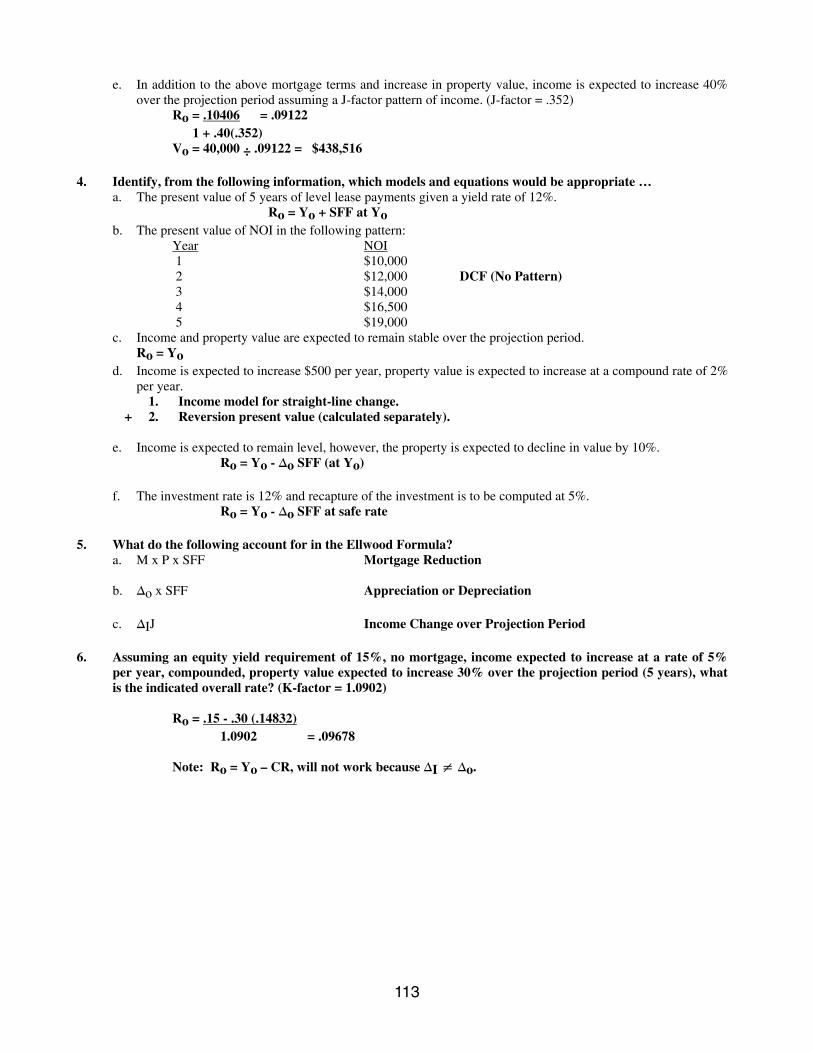

e. In addition to the above mortgage terms and increase in property value, income is expected to increase 40% over the projection period assuming a J-factor pattern of income. (J-factor = .352)

Ro = .10406 = .09122 1 + .40(.352) Vo = 40,000 ÷ .09122 = $438,516 4. Identify, from the following information, which models and equations would be appropriate … a. The present value of 5 years of level lease payments given a yield rate of 12%. Ro = Yo + SFF at Yo b. The present value of NOI in the following pattern: Year NOI 1 $10,000 2 $12,000 DCF (No Pattern) 3 $14,000 4 $16,500 5 $19,000 c. Income and property value are expected to remain stable over the projection period. Ro = Yo d. Income is expected to increase $500 per year, property value is expected to increase at a compound rate of 2%

per year. 1. Income model for straight-line change. + 2. Reversion present value (calculated separately).

e. Income is expected to remain level, however, the property is expected to decline in value by 10%. Ro = Yo - ∆o SFF (at Yo) f. The investment rate is 12% and recapture of the investment is to be computed at 5%.

Ro = Yo - ∆o SFF at safe rate 5. What do the following account for in the Ellwood Formula? a. M x P x SFF Mortgage Reduction b. ∆o x SFF Appreciation or Depreciation c. ∆IJ Income Change over Projection Period 6. Assuming an equity yield requirement of 15%, no mortgage, income expected to increase at a rate of 5%

per year, compounded, property value expected to increase 30% over the projection period (5 years), what is the indicated overall rate? (K-factor = 1.0902)

Ro = .15 - .30 (.14832)

1.0902 = .09678 Note: Ro = Yo – CR, will not work because ∆I ≠ ∆o.

113

7. A property has a net operating income of $50,000 and a current building value of $250,000. Given a projection period of 7 years, an expected change in building value of -50%, and a change in land value of +50%, what is the estimated value of the property assuming a yield rate of 11%?

RL = .11 – (.50)(.10222) = .05889 RB = .11 – (-.50)(.10222) = .16111 VB = $250,000 NOI = 50,000 NOIB = (40,278) [250,000 x .16111] NOIL = 9,722 ÷ .05889 = $165,087 Vo = $415,087 8. A property with a long-term level lease sold on an overall capitalization rate of 10% and was financed with

an 80% loan with an interest rate of 8% and a 30 year amortization with monthly payments. The property is expected to increase in value by 20% over the next 10 years. What was the yield to equity? What is the overall yield rate?

Start by making up a value: I will use $100,000 If the value is $100,000, then the NOI would be $10,000 ($100,000 x 10%) The future sale price would be $120,000 ($100,000 x (1 + 20%)) The loan would be $80,000 ($100,000 x 80%). The payment of 7,044 & balance of 70,180 are calculated. The yield to the property (Yo) is calculated by using the top line [11.2%] The yield to the equity position is calculated by using the bottom line [20.4%]

N I PV PMT FV R Property 10 11.2% -100,000 10,000 120,000 10.0% Loan 360

120 8/12 -80,000 587 x 12 = 7,044

70,180 8.8%

Equity 10 20.4% -20,000 2,956 49,820 14.8%

9. In the Akerson format, do you add or subtract depreciation x SFF in the formula? -∆o SFF is the portion of the formula that accounts for property change So if there is a loss in value: -(-∆o) SFF or + ∆o SFF 10. Given the following, and assuming level income: Ro = 11.5% M = 75% .75 x .105 = .07875 ∆I = 0% .25 x RE = .03625 N = 5 years Ro = .11500 ∆o = -20% P = .10 So: RE = .1450 RM = 10.5% a. What is the indicated ∆e? ∆E = (∆o + M x P) ÷ (1-M) ∆E = (-.20 + .75 x .10) ÷ (1 - .75) = -.50

114

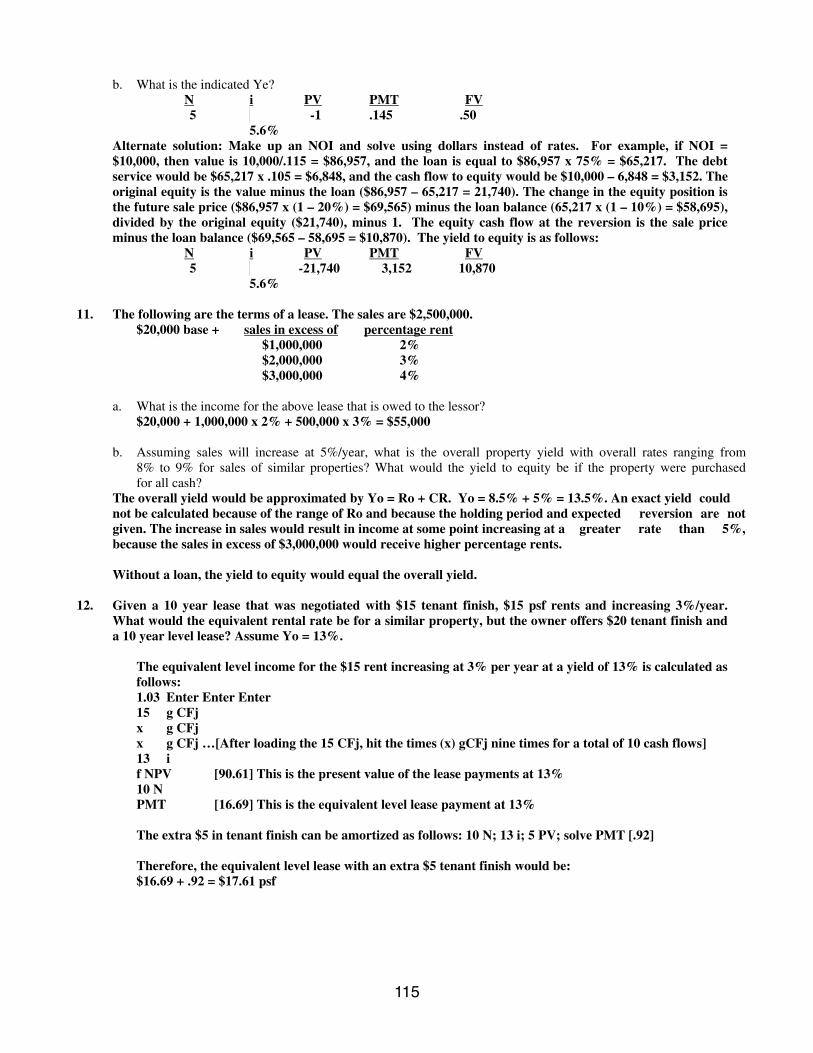

b. What is the indicated Ye? N i PV PMT FV 5 -1 .145 .50 5.6% Alternate solution: Make up an NOI and solve using dollars instead of rates. For example, if NOI =

$10,000, then value is 10,000/.115 = $86,957, and the loan is equal to $86,957 x 75% = $65,217. The debt service would be $65,217 x .105 = $6,848, and the cash flow to equity would be $10,000 – 6,848 = $3,152. The original equity is the value minus the loan ($86,957 – 65,217 = 21,740). The change in the equity position is the future sale price ($86,957 x (1 – 20%) = $69,565) minus the loan balance (65,217 x (1 – 10%) = $58,695), divided by the original equity ($21,740), minus 1. The equity cash flow at the reversion is the sale price minus the loan balance ($69,565 – 58,695 = $10,870). The yield to equity is as follows:

N i PV PMT FV 5 -21,740 3,152 10,870 5.6% 11. The following are the terms of a lease. The sales are $2,500,000. $20,000 base + sales in excess of percentage rent $1,000,000 2% $2,000,000 3% $3,000,000 4% a. What is the income for the above lease that is owed to the lessor? $20,000 + 1,000,000 x 2% + 500,000 x 3% = $55,000

b. Assuming sales will increase at 5%/year, what is the overall property yield with overall rates ranging from 8% to 9% for sales of similar properties? What would the yield to equity be if the property were purchased for all cash?

The overall yield would be approximated by Yo = Ro + CR. Yo = 8.5% + 5% = 13.5%. An exact yield could not be calculated because of the range of Ro and because the holding period and expected reversion are not given. The increase in sales would result in income at some point increasing at a greater rate than 5%, because the sales in excess of $3,000,000 would receive higher percentage rents.

Without a loan, the yield to equity would equal the overall yield. 12. Given a 10 year lease that was negotiated with $15 tenant finish, $15 psf rents and increasing 3%/year.

What would the equivalent rental rate be for a similar property, but the owner offers $20 tenant finish and a 10 year level lease? Assume Yo = 13%.

The equivalent level income for the $15 rent increasing at 3% per year at a yield of 13% is calculated as

follows: 1.03 Enter Enter Enter 15 g CFj x g CFj x g CFj …[After loading the 15 CFj, hit the times (x) gCFj nine times for a total of 10 cash flows]

13 i f NPV [90.61] This is the present value of the lease payments at 13% 10 N PMT [16.69] This is the equivalent level lease payment at 13% The extra $5 in tenant finish can be amortized as follows: 10 N; 13 i; 5 PV; solve PMT [.92] Therefore, the equivalent level lease with an extra $5 tenant finish would be: $16.69 + .92 = $17.61 psf

115

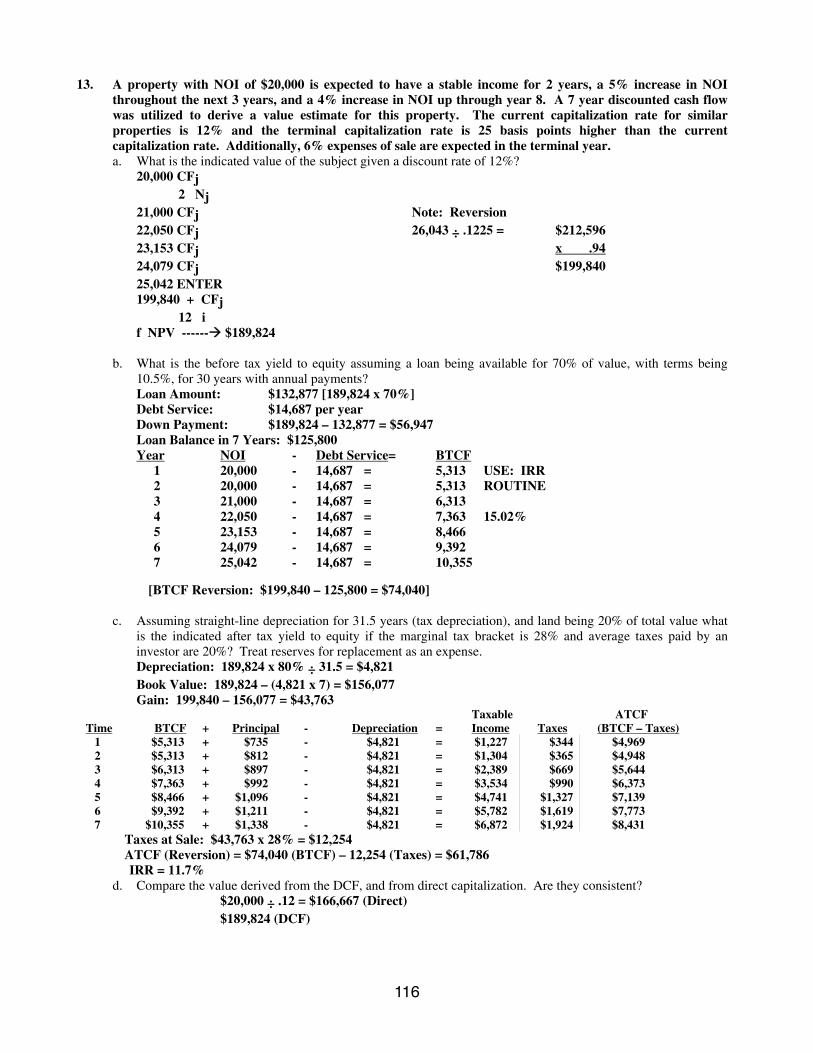

13. A property with NOI of $20,000 is expected to have a stable income for 2 years, a 5% increase in NOI throughout the next 3 years, and a 4% increase in NOI up through year 8. A 7 year discounted cash flow was utilized to derive a value estimate for this property. The current capitalization rate for similar properties is 12% and the terminal capitalization rate is 25 basis points higher than the current capitalization rate. Additionally, 6% expenses of sale are expected in the terminal year.

a. What is the indicated value of the subject given a discount rate of 12%? 20,000 CFj 2 Nj 21,000 CFj Note: Reversion 22,050 CFj 26,043 ÷ .1225 = $212,596 23,153 CFj x .94 24,079 CFj $199,840 25,042 ENTER 199,840 + CFj 12 i f NPV ------Æ $189,824

b. What is the before tax yield to equity assuming a loan being available for 70% of value, with terms being 10.5%, for 30 years with annual payments?

Loan Amount: $132,877 [189,824 x 70%] Debt Service: $14,687 per year Down Payment: $189,824 – 132,877 = $56,947 Loan Balance in 7 Years: $125,800 Year NOI - Debt Service= BTCF 1 20,000 - 14,687 = 5,313 USE: IRR 2 20,000 - 14,687 = 5,313 ROUTINE 3 21,000 - 14,687 = 6,313 4 22,050 - 14,687 = 7,363 15.02% 5 23,153 - 14,687 = 8,466 6 24,079 - 14,687 = 9,392 7 25,042 - 14,687 = 10,355 [BTCF Reversion: $199,840 – 125,800 = $74,040]

c. Assuming straight-line depreciation for 31.5 years (tax depreciation), and land being 20% of total value what is the indicated after tax yield to equity if the marginal tax bracket is 28% and average taxes paid by an investor are 20%? Treat reserves for replacement as an expense.

Depreciation: 189,824 x 80% ÷ 31.5 = $4,821 Book Value: 189,824 – (4,821 x 7) = $156,077 Gain: 199,840 – 156,077 = $43,763 Taxable ATCF Time BTCF + Principal - Depreciation = Income Taxes (BTCF – Taxes) 1 $5,313 + $735 - $4,821 = $1,227 $344 $4,969 2 $5,313 + $812 - $4,821 = $1,304 $365 $4,948 3 $6,313 + $897 - $4,821 = $2,389 $669 $5,644 4 $7,363 + $992 - $4,821 = $3,534 $990 $6,373 5 $8,466 + $1,096 - $4,821 = $4,741 $1,327 $7,139 6 $9,392 + $1,211 - $4,821 = $5,782 $1,619 $7,773 7 $10,355 + $1,338 - $4,821 = $6,872 $1,924 $8,431 Taxes at Sale: $43,763 x 28% = $12,254 ATCF (Reversion) = $74,040 (BTCF) – 12,254 (Taxes) = $61,786 IRR = 11.7%

d. Compare the value derived from the DCF, and from direct capitalization. Are they consistent? $20,000 ÷ .12 = $166,667 (Direct) $189,824 (DCF)

116

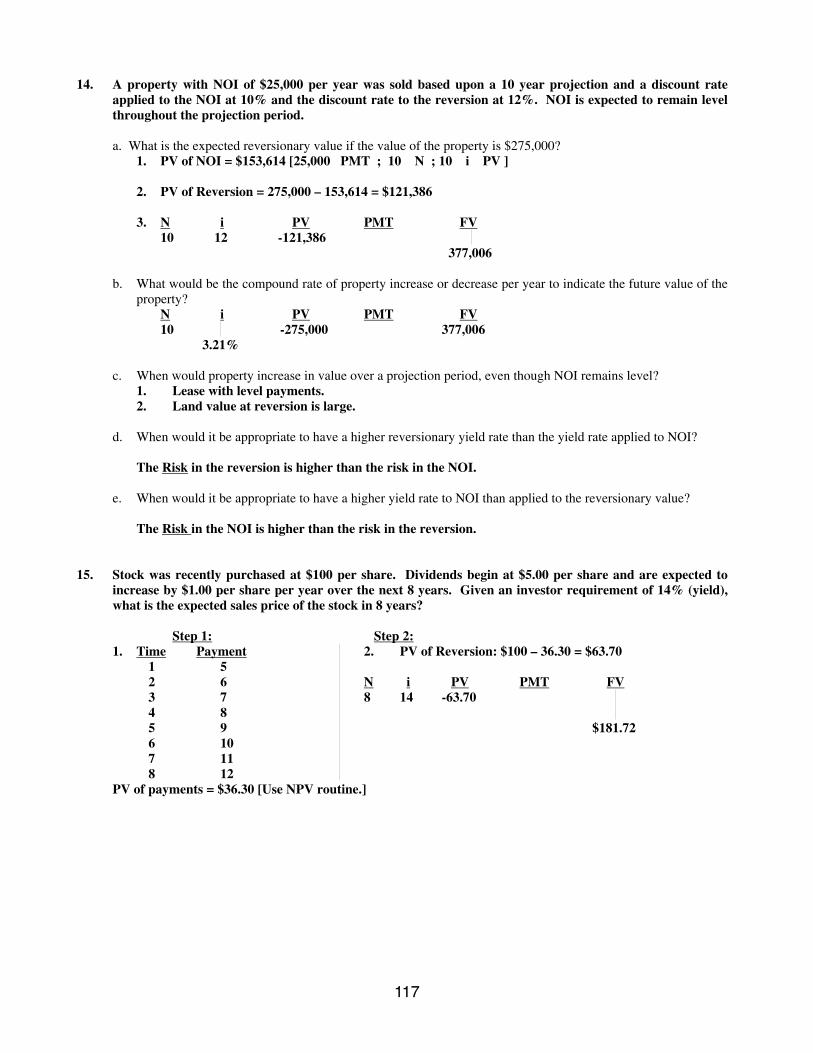

14. A property with NOI of $25,000 per year was sold based upon a 10 year projection and a discount rate applied to the NOI at 10% and the discount rate to the reversion at 12%. NOI is expected to remain level throughout the projection period.

a. What is the expected reversionary value if the value of the property is $275,000? 1. PV of NOI = $153,614 [25,000 PMT ; 10 N ; 10 i PV ] 2. PV of Reversion = 275,000 – 153,614 = $121,386 3. N i PV PMT FV 10 12 -121,386 377,006 b. What would be the compound rate of property increase or decrease per year to indicate the future value of the

property? N i PV PMT FV 10 -275,000 377,006 3.21% c. When would property increase in value over a projection period, even though NOI remains level? 1. Lease with level payments. 2. Land value at reversion is large. d. When would it be appropriate to have a higher reversionary yield rate than the yield rate applied to NOI? The Risk in the reversion is higher than the risk in the NOI.

e. When would it be appropriate to have a higher yield rate to NOI than applied to the reversionary value? The Risk in the NOI is higher than the risk in the reversion. 15. Stock was recently purchased at $100 per share. Dividends begin at $5.00 per share and are expected to

increase by $1.00 per share per year over the next 8 years. Given an investor requirement of 14% (yield), what is the expected sales price of the stock in 8 years?

Step 1: Step 2: 1. Time Payment 2. PV of Reversion: $100 – 36.30 = $63.70 1 5 2 6 N i PV PMT FV 3 7 8 14 -63.70 4 8 5 9 $181.72 6 10 7 11 8 12 PV of payments = $36.30 [Use NPV routine.]

117

PROBLEMS – RATE RELATIONSHIPS

1. Refer to the DCF problems from Yield Capitalization, problem 13.

a. Was the leverage positive or negative based upon before tax cash flows?

b. Was the leverage positive or negative, considering before tax yield rates?

c. Was the leverage positive or negative considering the after tax yield rates?

2. The present value of an ordinary annuity discounted at 12% is $50,000. What is the present value of the

lease payments if paid in advance?

3. Given two properties with income characteristics being identical except Property 1 is within an area of

higher tax rates, and very little chance of change in tax structure between the two properties… a. Would you expect the overall rates to be higher, lower or the same, when comparing property 1 to property 2? b. Would you expect the gross income multiplier to be higher, lower or the same when comparing property 1 to

property 2? 4. Given an increase in long-term interest rates, how would overall rates change? 5. Given no change in value or NOI, can the debt coverage ratio be increased? If so, how? 6. What is the indicated interest rate on a second mortgage if terms are for 20 years (annual payment), Ro =

.105, a first mortgage on the property is for 9% interest, with M = 80%, 20 years (annual payments), and RE is .06, with 10% down?

7. Given expected increases of income and value of 4% per year (to follow expected inflationary trends), and a

yield requirement of 12%, what is the indicated overall rate? 8. Given NOI of $10,500, a DCR of 1.25 and a mortgage capitalization rate of 12%, what is the indicated loan

amount?

9. Given a $50,000 loan, an NOI of $10,000 and a DCR of 1.15, what is the mortgage capitalization rate? 10. Given: M = 80% Rm = .1234 OER = 40% GIM = 6 NOI = $10,000 What is the debt service?

118

11. Given: OER = 35% DCR = 1.18 Rm = .115 M = .80 What is the GIM? 12. Given: Value = $1,000,000 Ro = .09 DCR = 1.15 Rm = .12 What is the debt service and loan amount? 13. Given: NOI = $10,000 OER = 40% (of EGI) Vacancy & collection loss = 5% What is the potential gross income?

14. What is the PGIM given an EGIM of 6 and a vacancy & collection loss of 7%?

119

PROBLEM SOLUTIONS – RATE RELATIONSHIPS 1. Refer to the DCF problems from Yield Capitalization, problem 13. a. Was the leverage positive or negative based upon before tax cash flows? RM = .1105 RM > Ro Ro = .1054 Therefore, Negative RE = .0933 [Comment: To determine the effect of leverage focus on the mortgage rate, if it is the lowest that is positive leverage. The overall rate (including yield) has to be between the equity and mortgage rates.] b. Was the leverage positive or negative, considering before tax yield rates? YM = .105 YM < Yo Yo = .120 Therefore, Positive

YE = .150 c. Was the leverage positive or negative considering the after tax yield rates? YM = .076 (.105 x (1-28%)) YM < Yo YE = .117 Therefore, Positive 2. The present value of an ordinary annuity discounted at 12% is $50,000. What is the present value of the

lease payments if paid in advance? $50,000 x 1.12 = $56,000 Please note that the “lease payments” language is a distractor. The present value of an ordinary annuity by

definition is level payments made in arrears. 3. Given two properties with income characteristics being identical except Property 1 is within an area of

higher tax rates, and very little chance of change in tax structure between the two properties... a. Would you expect the overall rates to be higher, lower or the same, when comparing property 1 to property 2? The overall rates should be equal. b. Would you expect the gross income multiplier to be higher, lower or the same when comparing property 1 to

property 2? The GIM should be lower for Property 1. 4. Given an increase in long-term interest rates, how would overall rates change? Ro = Rm x M x DCR, Rm increases so Ro increases. However, the overall rates often do not change if the reason the interest rates are higher is due

to expected inflation. Real estate is looked upon as an inflation hedge. 5. Given no change in value or NOI, can the debt coverage ratio be increased? If so, how? (1) Lower the loan-to-value ratio. (2) Lower the interest rate. (3) Extend the term of the loan.

120

6. What is the indicated interest rate on a second mortgage if terms are for 20 years, Ro = .105, a first mortgage on the property is for 9% interest, with an 80% LTV, for 20 years (annual payments), and RE is .06, with 10% down?

Rm: 20 N, 9 i, -1 PV PMT [Display: .1095465] .80 x .1095465 = .087637 .10 x Rm2 = .011363 Rm2 = 11.36% .10 x .06 = .006000 .105 N i PV PMT FV 20 -1 .1136 9.5% 7. Given expected increases of income and value of 4% per year (to follow expected inflationary trends), and a

yield requirement of 12%, what is the indicated overall rate? Ro = Yo - CR Ro = .12 - .04 = .08 8. Given NOI of $10,500, a DCR of 1.25 and a mortgage capitalization rate of 12%, what is the indicated loan

amount? ($10,500 ÷ 1.25) ÷ .12 = $70,000 Note: NOI ÷ DCR = Debt Service 9. Given a $50,000 loan, an NOI of $10,000 and a DCR of 1.15, what is the mortgage capitalization rate? (10,000 ÷ 1.15) ÷ 50,000 = .1739 10. Given: M = 80% Rm = .1234 OER = 40% GIM = 6 NOI = $10,000 What is the debt service? Ro = 1-OER 1 - .40 GIM, so 6 = .10 NOI ÷ Ro = Vo: 10,000 ÷ .10 = $100,000 Vo x M x Rm = Debt Service: $100,000 x 80% x .1234 = $9,872 or, EGI = $10,000 ÷ (1 - 40%) = $16,667 Vo = $16,667 x 6 (GIM) = $100,000 Loan = $100,000 x 80% = $80,000 Debt Service = $80,000 x .1234 = $9,872

121

11. Given: OER = 35% DCR = 1.18 Rm = .115 M = .80 What is the GIM? Solution with formulas: Solution with cash flows: Ro = DCR x Rm x M: Vo = $1,000 (made up) So, Ro = 1.18 x .115 x .80 = .10856 Loan = $1,000 x 80% = $800 Ro = NIR 1 - .35 D.S.= $800 x .115 = $92 GIM: So, .10856 = GIM NOI = $92 x 1.18 = $108.56 EGI=$108.56 ÷ (1 - 35%) = $167.02 .10856 = .65 EGIM = $1,000 ÷ $167.02 = 5.99 GIM .10856 GIM = .65 GIM = 5.99 12. Given: Value = $1,000,000 Ro = .09 DCR = 1.15 Rm = .12 What is the debt service and loan amount? Debt Service:Value x Ro ÷ DCR = 1,000,000 x .09 ÷ 1.15 = $78,261 Loan Amount:Debt Service ÷ Rm = 78,261 ÷ .12 = $652,174 13. Given: NOI = $10,000 OER = 40% (of EGI) Vacancy & collection loss = 5% What is the potential gross income? $10,000 ÷ .60 = $16,667 (EGI) $16,667 ÷ .95 = $17,544 (PGI) 14. What is the PGIM given an EGIM of 6 and a vacancy & collection loss of 7%? Solution with formula: Solution with cash flows: PGIM = EGIM x (1 - vac.) Vo = $10,000 PGIM = 6 x (1 - .07) = 5.58 EGI = $10,000 ÷ 6 = $1,666.67 PGI = $1,666.67 ÷ (1 - .07) = $1,792.11 PGIM = $10,000 ÷ $1,792.11 = 5.58

122

PROBLEM - PARTIAL INTERESTS

1. A 90 year lease was originated 55 years ago for $500 per year. Current market rent is $20,000 per year for

long-term leases, on a level basis. Tenant #1 leased to Tenant #2 for $5,000, Tenant #2 leased to Tenant #3 for $8,000, Tenant #3 leased to Tenant #4 for $12,000, Tenant #4 leased to Tenant #5 for $19,000, and Tenant #5 leased to Tenant #6 for $22,000. The market value of the property is currently $150,000 and is expected to be $500,000 at the termination of the lease.

a. What is the applicable yield rate to the fee simple?

b. What is the applicable yield rate to the reversion?

c. What is the indicated value to each of the tenant's positions? d. What is the present value of the leased fee?

123

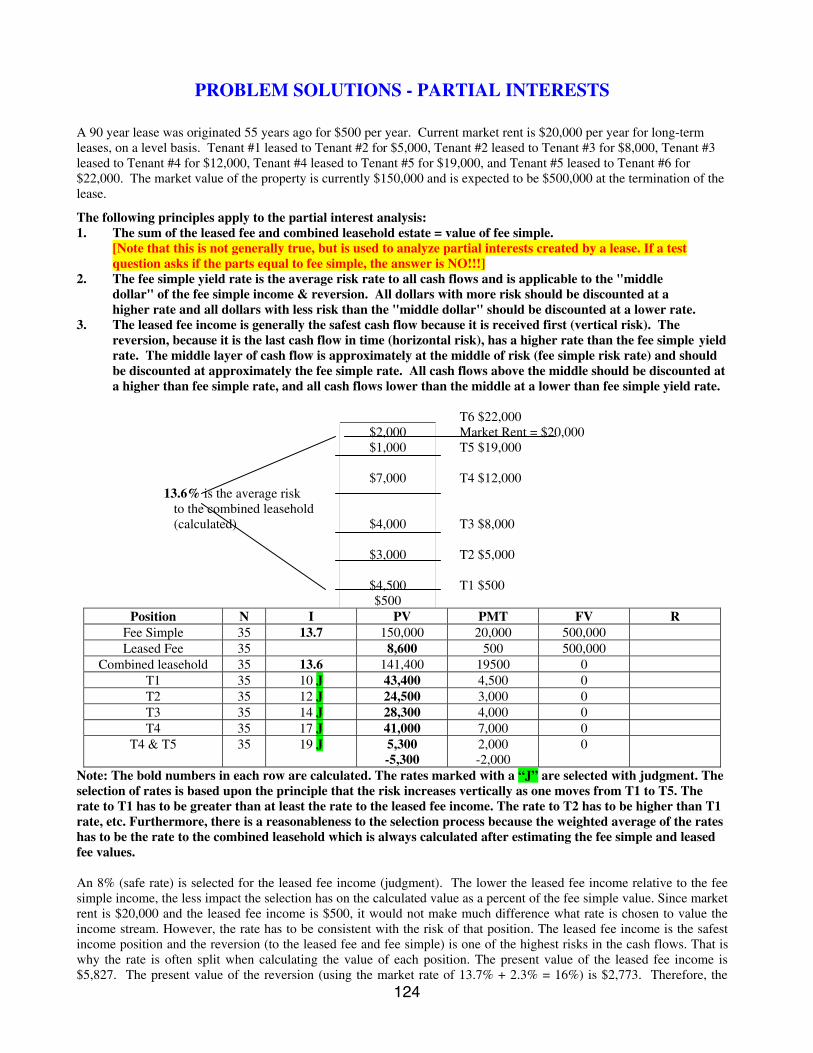

PROBLEM SOLUTIONS - PARTIAL INTERESTS

A 90 year lease was originated 55 years ago for $500 per year. Current market rent is $20,000 per year for long-term leases, on a level basis. Tenant #1 leased to Tenant #2 for $5,000, Tenant #2 leased to Tenant #3 for $8,000, Tenant #3 leased to Tenant #4 for $12,000, Tenant #4 leased to Tenant #5 for $19,000, and Tenant #5 leased to Tenant #6 for $22,000. The market value of the property is currently $150,000 and is expected to be $500,000 at the termination of the lease.

The following principles apply to the partial interest analysis: 1. The sum of the leased fee and combined leasehold estate = value of fee simple. [Note that this is not generally true, but is used to analyze partial interests created by a lease. If a test question asks if the parts equal to fee simple, the answer is NO!!!] 2. The fee simple yield rate is the average risk rate to all cash flows and is applicable to the "middle dollar" of the fee simple income & reversion. All dollars with more risk should be discounted at a higher rate and all dollars with less risk than the "middle dollar" should be discounted at a lower rate. 3. The leased fee income is generally the safest cash flow because it is received first (vertical risk). The

reversion, because it is the last cash flow in time (horizontal risk), has a higher rate than the fee simple yield rate. The middle layer of cash flow is approximately at the middle of risk (fee simple risk rate) and should be discounted at approximately the fee simple rate. All cash flows above the middle should be discounted at a higher than fee simple rate, and all cash flows lower than the middle at a lower than fee simple yield rate.

T6 $22,000 $2,000 Market Rent = $20,000 $1,000 T5 $19,000 $7,000 T4 $12,000 13.6% is the average risk to the combined leasehold (calculated) $4,000 T3 $8,000 $3,000 T2 $5,000 $4,500 T1 $500 $500

Position N I PV PMT FV R Fee Simple 35 13.7 150,000 20,000 500,000 Leased Fee 35 8,600 500 500,000

Combined leasehold 35 13.6 141,400 19500 0 T1 35 10 J 43,400 4,500 0 T2 35 12 J 24,500 3,000 0 T3 35 14 J 28,300 4,000 0 T4 35 17 J 41,000 7,000 0

T4 & T5 35 19 J 5,300 -5,300

2,000 -2,000

0

Note: The bold numbers in each row are calculated. The rates marked with a “J” are selected with judgment. The selection of rates is based upon the principle that the risk increases vertically as one moves from T1 to T5. The rate to T1 has to be greater than at least the rate to the leased fee income. The rate to T2 has to be higher than T1 rate, etc. Furthermore, there is a reasonableness to the selection process because the weighted average of the rates has to be the rate to the combined leasehold which is always calculated after estimating the fee simple and leased fee values. An 8% (safe rate) is selected for the leased fee income (judgment). The lower the leased fee income relative to the fee simple income, the less impact the selection has on the calculated value as a percent of the fee simple value. Since market rent is $20,000 and the leased fee income is $500, it would not make much difference what rate is chosen to value the income stream. However, the rate has to be consistent with the risk of that position. The leased fee income is the safest income position and the reversion (to the leased fee and fee simple) is one of the highest risks in the cash flows. That is why the rate is often split when calculating the value of each position. The present value of the leased fee income is $5,827. The present value of the reversion (using the market rate of 13.7% + 2.3% = 16%) is $2,773. Therefore, the

124

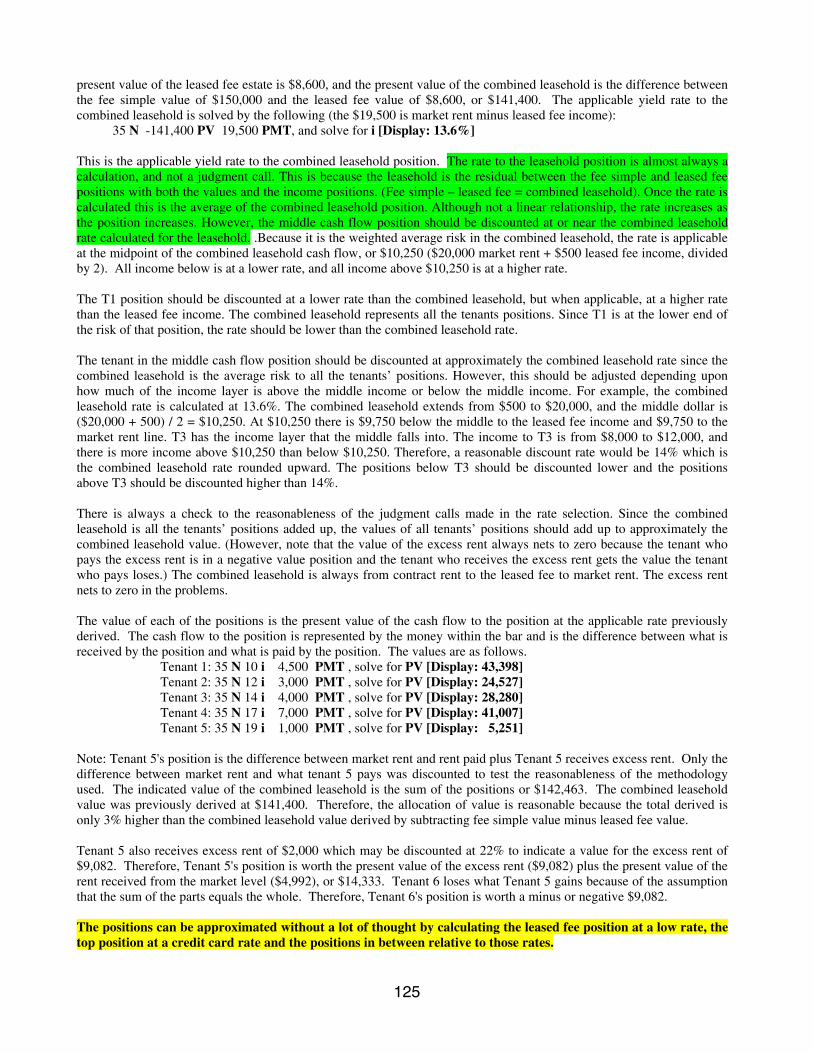

present value of the leased fee estate is $8,600, and the present value of the combined leasehold is the difference between the fee simple value of $150,000 and the leased fee value of $8,600, or $141,400. The applicable yield rate to the combined leasehold is solved by the following (the $19,500 is market rent minus leased fee income): 35 N -141,400 PV 19,500 PMT, and solve for i [Display: 13.6%] This is the applicable yield rate to the combined leasehold position. The rate to the leasehold position is almost always a calculation, and not a judgment call. This is because the leasehold is the residual between the fee simple and leased fee positions with both the values and the income positions. (Fee simple – leased fee = combined leasehold). Once the rate is calculated this is the average of the combined leasehold position. Although not a linear relationship, the rate increases as the position increases. However, the middle cash flow position should be discounted at or near the combined leasehold rate calculated for the leasehold. .Because it is the weighted average risk in the combined leasehold, the rate is applicable at the midpoint of the combined leasehold cash flow, or $10,250 ($20,000 market rent + $500 leased fee income, divided by 2). All income below is at a lower rate, and all income above $10,250 is at a higher rate. The T1 position should be discounted at a lower rate than the combined leasehold, but when applicable, at a higher rate than the leased fee income. The combined leasehold represents all the tenants positions. Since T1 is at the lower end of the risk of that position, the rate should be lower than the combined leasehold rate. The tenant in the middle cash flow position should be discounted at approximately the combined leasehold rate since the combined leasehold is the average risk to all the tenants’ positions. However, this should be adjusted depending upon how much of the income layer is above the middle income or below the middle income. For example, the combined leasehold rate is calculated at 13.6%. The combined leasehold extends from $500 to $20,000, and the middle dollar is ($20,000 + 500) / 2 = $10,250. At $10,250 there is $9,750 below the middle to the leased fee income and $9,750 to the market rent line. T3 has the income layer that the middle falls into. The income to T3 is from $8,000 to $12,000, and there is more income above $10,250 than below $10,250. Therefore, a reasonable discount rate would be 14% which is the combined leasehold rate rounded upward. The positions below T3 should be discounted lower and the positions above T3 should be discounted higher than 14%. There is always a check to the reasonableness of the judgment calls made in the rate selection. Since the combined leasehold is all the tenants’ positions added up, the values of all tenants’ positions should add up to approximately the combined leasehold value. (However, note that the value of the excess rent always nets to zero because the tenant who pays the excess rent is in a negative value position and the tenant who receives the excess rent gets the value the tenant who pays loses.) The combined leasehold is always from contract rent to the leased fee to market rent. The excess rent nets to zero in the problems. The value of each of the positions is the present value of the cash flow to the position at the applicable rate previously derived. The cash flow to the position is represented by the money within the bar and is the difference between what is received by the position and what is paid by the position. The values are as follows. Tenant 1: 35 N 10 i 4,500 PMT , solve for PV [Display: 43,398] Tenant 2: 35 N 12 i 3,000 PMT , solve for PV [Display: 24,527] Tenant 3: 35 N 14 i 4,000 PMT , solve for PV [Display: 28,280] Tenant 4: 35 N 17 i 7,000 PMT , solve for PV [Display: 41,007] Tenant 5: 35 N 19 i 1,000 PMT , solve for PV [Display: 5,251] Note: Tenant 5's position is the difference between market rent and rent paid plus Tenant 5 receives excess rent. Only the difference between market rent and what tenant 5 pays was discounted to test the reasonableness of the methodology used. The indicated value of the combined leasehold is the sum of the positions or $142,463. The combined leasehold value was previously derived at $141,400. Therefore, the allocation of value is reasonable because the total derived is only 3% higher than the combined leasehold value derived by subtracting fee simple value minus leased fee value. Tenant 5 also receives excess rent of $2,000 which may be discounted at 22% to indicate a value for the excess rent of $9,082. Therefore, Tenant 5's position is worth the present value of the excess rent ($9,082) plus the present value of the rent received from the market level ($4,992), or $14,333. Tenant 6 loses what Tenant 5 gains because of the assumption that the sum of the parts equals the whole. Therefore, Tenant 6's position is worth a minus or negative $9,082. The positions can be approximated without a lot of thought by calculating the leased fee position at a low rate, the top position at a credit card rate and the positions in between relative to those rates.

125

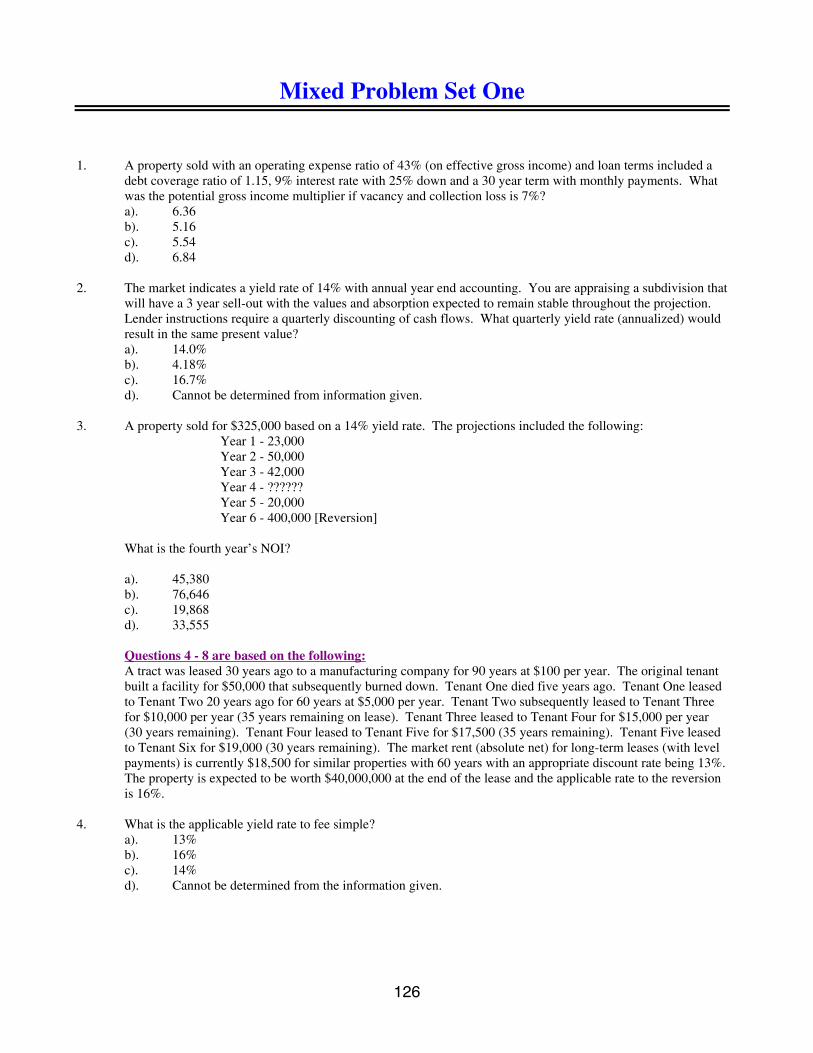

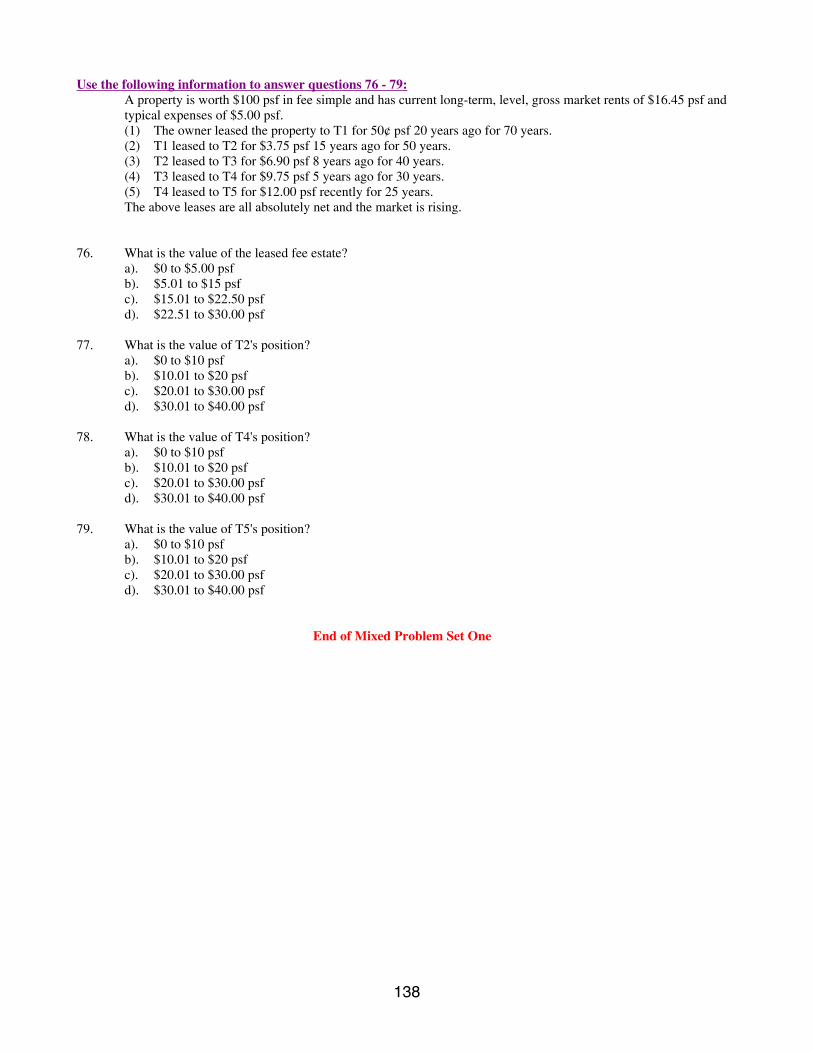

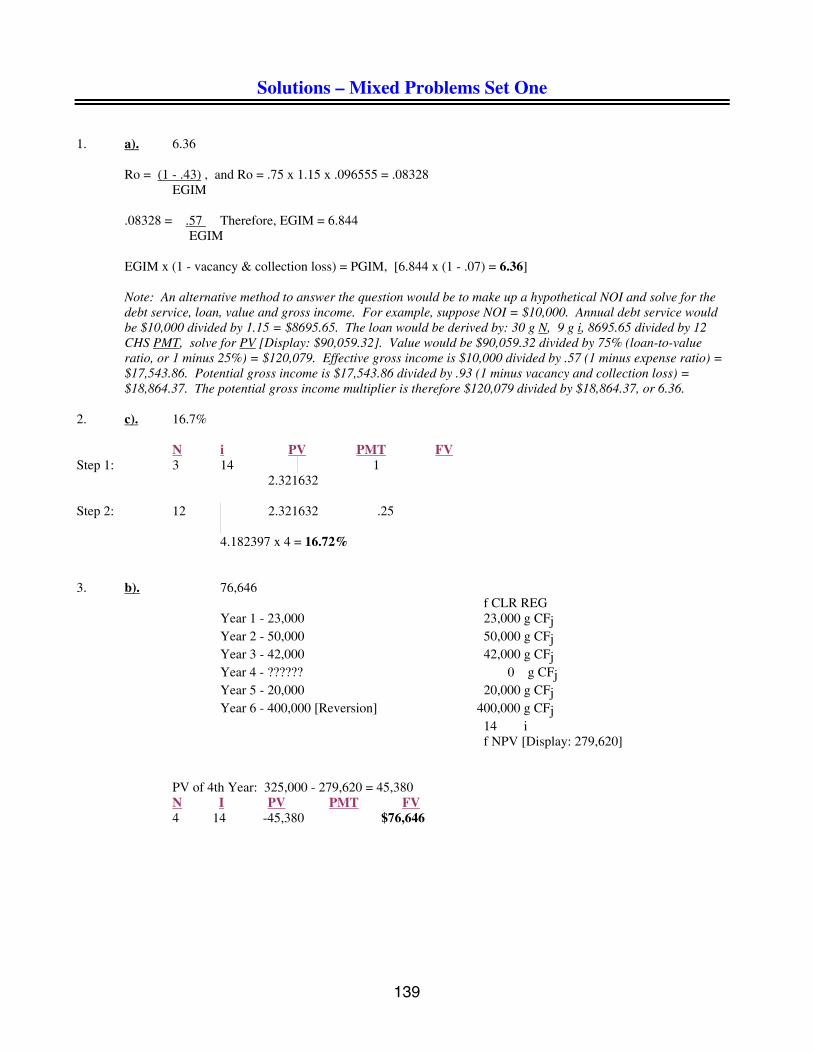

Mixed Problem Set One

1. A property sold with an operating expense ratio of 43% (on effective gross income) and loan terms included a debt coverage ratio of 1.15, 9% interest rate with 25% down and a 30 year term with monthly payments. What was the potential gross income multiplier if vacancy and collection loss is 7%?

a). 6.36 b). 5.16 c). 5.54 d). 6.84 2. The market indicates a yield rate of 14% with annual year end accounting. You are appraising a subdivision that

will have a 3 year sell-out with the values and absorption expected to remain stable throughout the projection. Lender instructions require a quarterly discounting of cash flows. What quarterly yield rate (annualized) would result in the same present value?

a). 14.0% b). 4.18% c). 16.7% d). Cannot be determined from information given. 3. A property sold for $325,000 based on a 14% yield rate. The projections included the following: Year 1 - 23,000 Year 2 - 50,000 Year 3 - 42,000 Year 4 - ?????? Year 5 - 20,000 Year 6 - 400,000 [Reversion] What is the fourth year’s NOI? a). 45,380 b). 76,646 c). 19,868 d). 33,555 Questions 4 - 8 are based on the following: A tract was leased 30 years ago to a manufacturing company for 90 years at $100 per year. The original tenant

built a facility for $50,000 that subsequently burned down. Tenant One died five years ago. Tenant One leased to Tenant Two 20 years ago for 60 years at $5,000 per year. Tenant Two subsequently leased to Tenant Three for $10,000 per year (35 years remaining on lease). Tenant Three leased to Tenant Four for $15,000 per year (30 years remaining). Tenant Four leased to Tenant Five for $17,500 (35 years remaining). Tenant Five leased to Tenant Six for $19,000 (30 years remaining). The market rent (absolute net) for long-term leases (with level payments) is currently $18,500 for similar properties with 60 years with an appropriate discount rate being 13%. The property is expected to be worth $40,000,000 at the end of the lease and the applicable rate to the reversion is 16%.

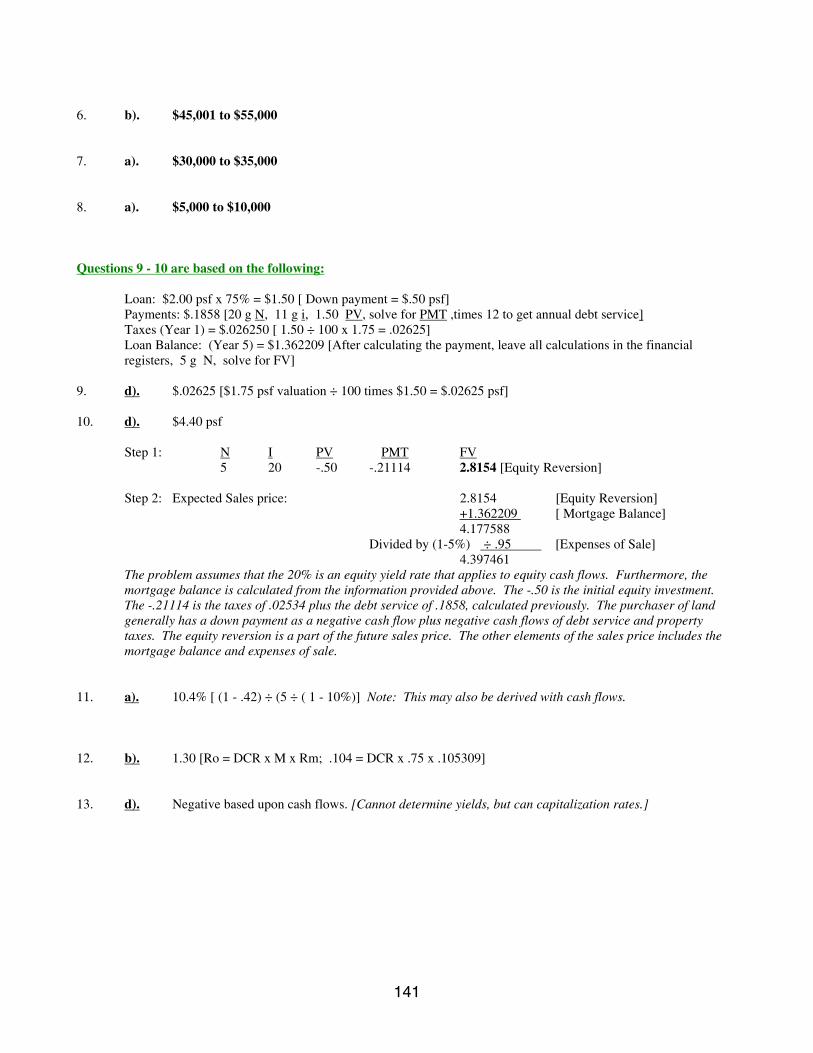

4. What is the applicable yield rate to fee simple? a). 13% b). 16% c). 14% d). Cannot be determined from the information given.

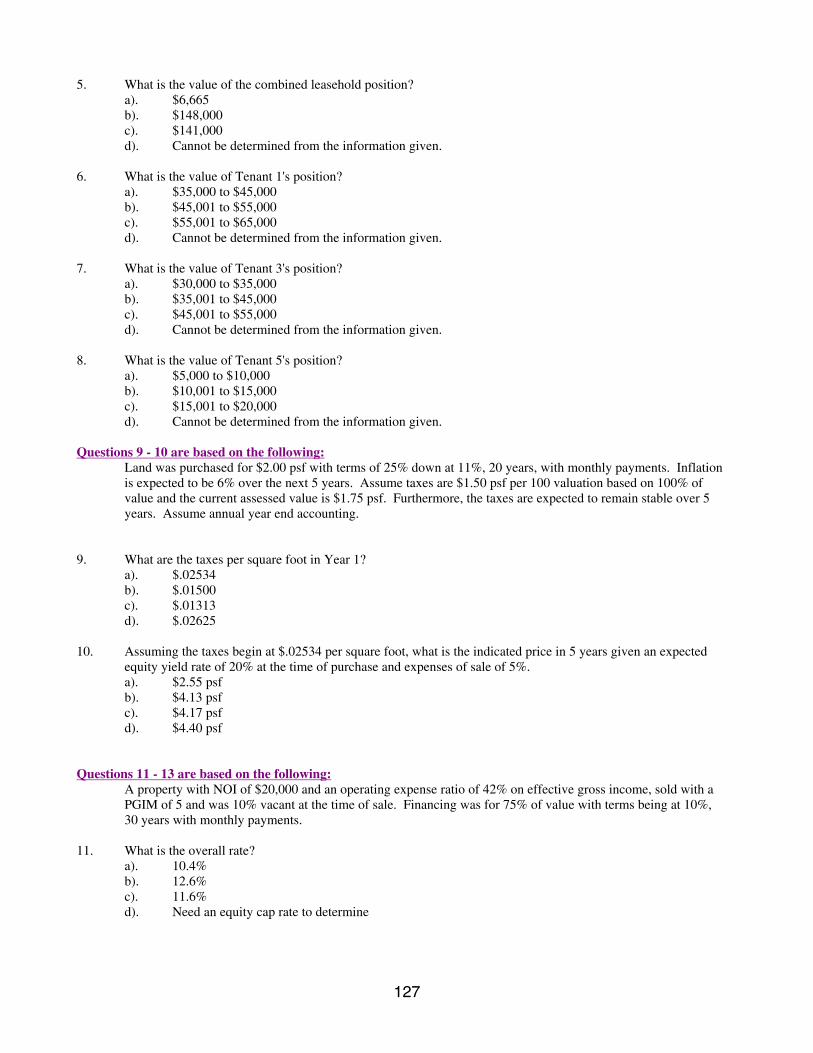

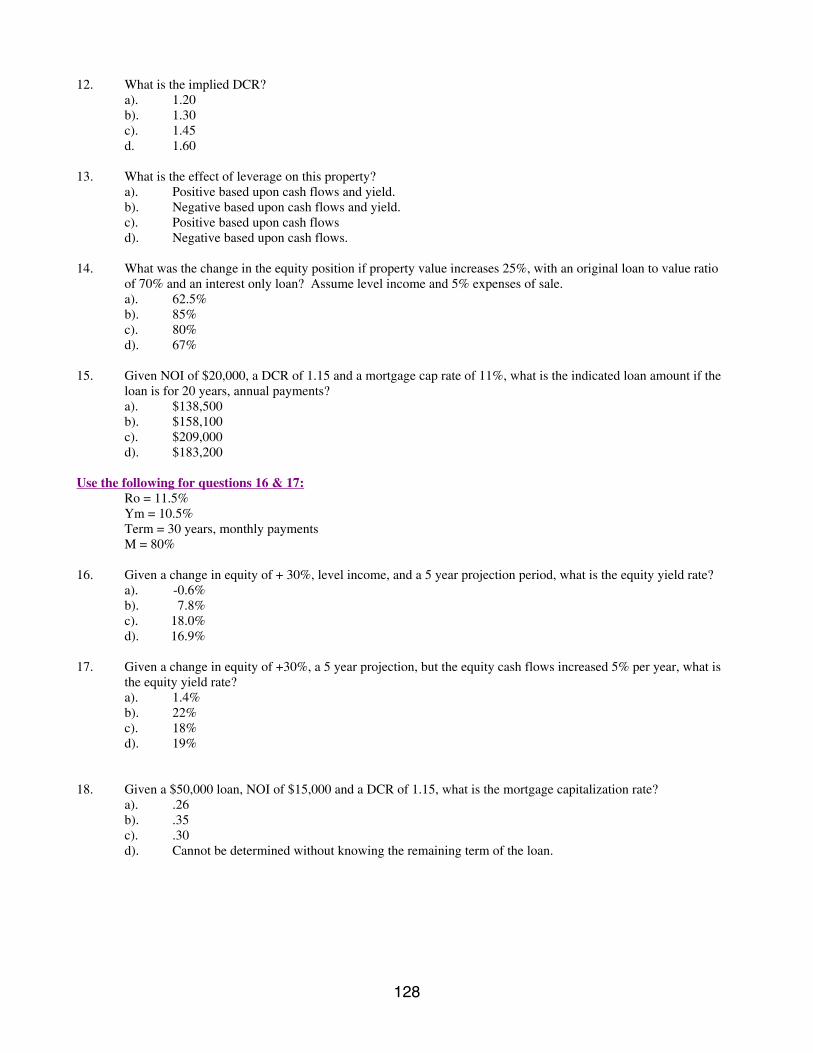

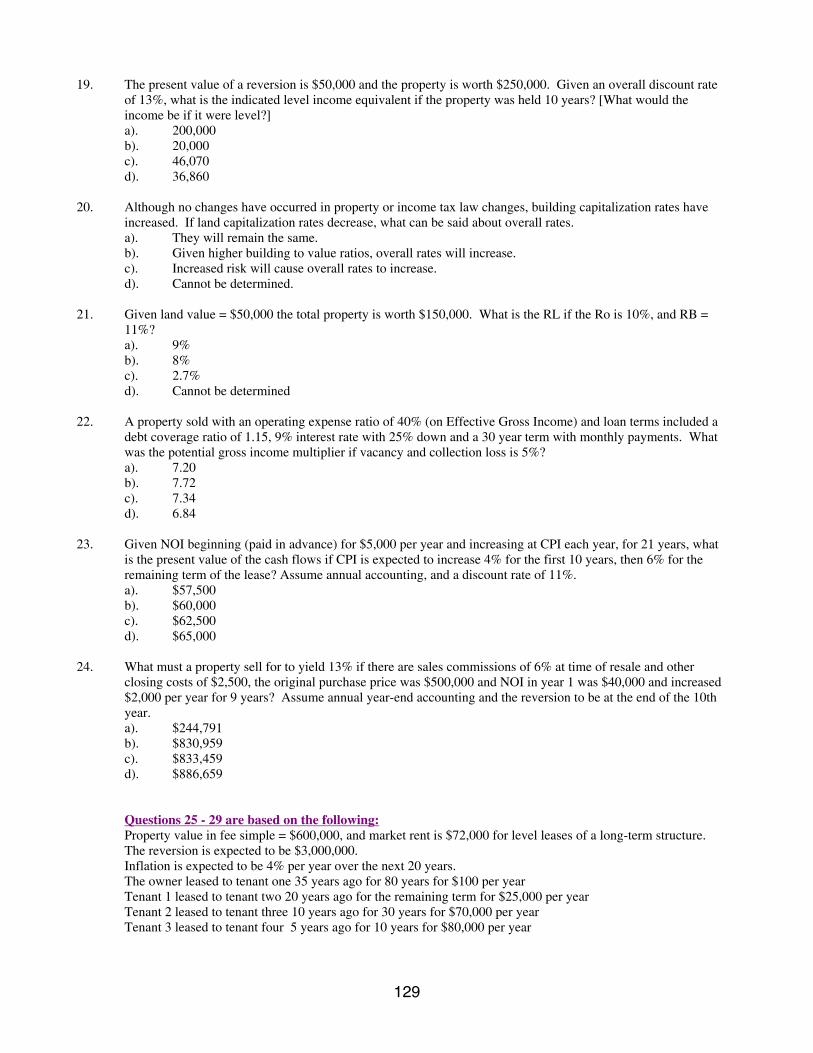

126

5. What is the value of the combined leasehold position? a). $6,665 b). $148,000 c). $141,000 d). Cannot be determined from the information given. 6. What is the value of Tenant 1's position? a). $35,000 to $45,000 b). $45,001 to $55,000 c). $55,001 to $65,000 d). Cannot be determined from the information given. 7. What is the value of Tenant 3's position? a). $30,000 to $35,000 b). $35,001 to $45,000 c). $45,001 to $55,000 d). Cannot be determined from the information given. 8. What is the value of Tenant 5's position? a). $5,000 to $10,000 b). $10,001 to $15,000 c). $15,001 to $20,000 d). Cannot be determined from the information given. Questions 9 - 10 are based on the following: Land was purchased for $2.00 psf with terms of 25% down at 11%, 20 years, with monthly payments. Inflation