Embed Size (px)

Citation preview

Private equity roundup Latin America

03Introduction

04Economic overview

06Fundraising

08 Transactions and exits

Contents10Regulatory update

11Outlook

Private equity roundup — Latin America 1

For additional information about PE investment in Latin America and other emerging economies, visit ey.com/peem.

About

Stay in touch with Private Equity at EY:• On the web at ey.com/privateequity• On Twitter at @EYPrivateEquity

Increasing macroeconomic stability in the developed markets, coupled with declining growth and geopolitical change, is leading to challenging times across many emerging markets. Despite the volatility, PE investors have remained committed, seeing opportunity in the long-term secular trends that have emerged over the last decade — namely a rising middle class, favorable demographics, low PE penetration and a lack of traditional financing infrastructure. These macro trends will continue to play out over the next decade and will continue to provide PE firms with a wide range of compelling opportunities.

EY’s Private equity roundup series delves into the drivers of fundraising, investment activity and exits across a range of developing economies, including Africa, China, India and Latin America. Our quarterly, semiannual and annual reports deliver fresh insight into the forces shaping activity, including macroeconomic trends, regulatory developments and capital markets activity.

Private equity roundup — Latin America is part of a series from EY focusing on private equity activity in the emerging markets.

Contacts:Jeff Bunder Global Private Equity Leader [email protected]

Michael Rogers Global Deputy Private Equity Leader [email protected]

Daniel Serventi South American Transaction Advisory Services Leader [email protected]

Carlos Asciutti Brazil Private Equity Leader [email protected]

Olivier Hache Mexico Transaction Advisory Services Leader [email protected]

Peter Witte Private Equity Analyst [email protected]

2 Private equity roundup — Latin America

Private equity roundup — Latin America 3

2014 was clearly a challenging year for many of the economies of Latin America. Rough winds — in the form of decreasing foreign demand, falling commodities prices and a reversal of asset flows back to the developed markets — precipitated an overall slowdown in activity across much of the region. Aggregate GDP growth rates declined on a year-over-year basis, and Brazil spent the first half of the year in recession. Many strategic investors became more cautious as the near-term outlook in many economies dimmed, while horizon risks, including a prolonged downturn in China, grew.

PE activity in the region lagged a bit in the slowdown. Investment activity lost some momentum during the year as uncertainty took hold and fundamentals deteriorated. While the value of deals increased modestly, the number of PE transactions fell 18% to 76.

However, despite the macro downturn, there remains little indication that investors are withdrawing from the region. Indeed, many seem to be doubling down. Fundraising continues to trend

higher, increasing 73%, from US$5.2b to US$9.0b, between 2013 and 2014. Moreover, nearly 60 other funds based in the region are at various stages of the fundraising process, targeting a combined US$13.5b for investment.

PE investors are confirming that the long-term thesis remains intact and are willing to weather the volatility of the market. PE investment as a percentage of GDP remains low relative to developed economies, and the region’s emerging middle class continues to represent a powerful force. Alternative sources of capital funding for SME businesses remain underdeveloped, while entrepreneurs and family owners grow increasingly accustomed to working with private equity. Indeed, many PE firms are seeing opportunity amid the volatility and the chance to put assets to work in an environment of increasingly attractive valuations. As such, while the mainstream hype surrounding Latin America may be waning, PE investors may now be seeing one of the most interesting investment climates in recent memory.

Introduction

4 Private equity roundup — Latin America

Economic overview1

While Latin America’s overall growth slowed, individual countries vary significantly, with LatAm’s two largest economies, Brazil and Mexico, currently trending in diametrically opposed directions. Mexico continues to benefit from the ongoing US recovery. Its economy is gaining traction, evidenced by higher consumer confidence and increased manufacturing output. At the end of September 2014, Mexico’s Government drafted a bill that seeks to address declining productivity in recent years and increase the country’s long-term competitiveness. The loss of productivity in recent years has been a leading drag on Mexico’s economic performance. As a result, the IMF expects Mexico’s economy to grow at a healthy 3.5% in 2015.

Many of the fundamentals driving the economic upswing over the last several years deteriorated in 2014. Among them was a still-lackluster recovery in several of the developed economies, in particular Europe and Japan. While the accelerating strength of the US recovery provided a counterpoint, slowing growth in Japan and Europe had a marked impact on many LatAm economies. Indeed, the outlook for many of the region’s key trading partners remains uncertain. In the US, speculation centers on when the Fed will raise interest rates and how will it manage its now US$4.5t balance sheet. In Europe and Japan, fears linger that weak industrial production and anemic consumption growth could lead to a deflationary spiral. At the same time, China continues to rein in growth expectations, putting increased pressure on commodity prices.

Figure 1. Actual and projected GDP growth for key Latin American economies, 2013–15

Argentina Brazil Chile Colombia Mexico Paraguay Peru Venezuela

GDP growth

2013 2014E 2015E

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Economic overview

Figure 2. Actual and projected GDP growth — Latin America versus key developed and emerging markets

-1%

0%

1%

2%

3%

4%

5%

6%

7%

Advanced economies Euro area Emerging and developing Asia

Latin America andthe Caribbean

GDP growth

2013 2014E 2015E

Source: IMF — World Economic Outlook Database

Brazil will face a more challenging environment. Having just secured a second term, President Dilma Rousseff must now address policy changes regarding high inflation, government expenditures, low investment rates and sluggish employment growth. Moreover, a fresh round of corruption scandals, which includes state-backed oil producer Petrobras, threatens to derail the focus on economic growth. Indeed, President Rousseff now has a reduced majority in the legislative branch, yielding additional challenges in finding consensus for needed reforms. The current expectation is that Brazil will see growth rates of 1.4% next year, well below the 2.5% posted in 2013.

Despite Brazil’s worries, many other countries in the region remain solid, the result of market-oriented reforms and policies enacted in recent years. However, signs continue to emerge that growth for these countries is entering a more mature, less exuberant phase, in part driven by lower commodity prices. For 2015, the IMF expects stronger GDP growth for countries including Colombia, Peru, Bolivia and Paraguay.

Inflation continues to be a pervasive concern. Both Brazil and Mexico are experiencing above-target inflation and will need to tighten monetary conditions in the coming months. Argentina and Venezuela are seeing high rates of inflation coupled with negative GDP growth. In the aggregate, Latin America has a significantly higher rate of inflation than many other developing markets, including Asia, which could ultimately threaten the sustainability of growth in the region.

Table 1. Consumer price index (CPI) rates across Latin America

2013 2014E 2015EArgentina 10.6% n/a n/aBrazil 6.2% 6.3% 5.9%Chile 1.8% 4.4% 3.2%Colombia 2.0% 2.9% 2.6%Mexico 3.8% 3.9% 3.6%Paraguay 2.7% 4.8% 5.0%Peru 2.8% 3.2% 2.3%Venezuela 40.6% 64.3% 62.9%

Source: IMF — World Economic Outlook Database

Private equity roundup — Latin America 5

6 Private equity roundup — Latin America

While macroeconomic concerns took center stage in 2014, limited partners (LPs) remain focused on the longer-term outlook. To that end, the region saw its best fundraising year since 2011, with aggregate commitments reaching US$9.0b. This represents an increase of 73% from the US$5.2b raised in 2013. However, it remains well below the peak of US$17.8b raised in 2011.

The recovery in LatAm fundraising follows the global trend. Globally, PE firms closed 687 funds valued at US$444.7b in 2014, up 11% from the US$401.1b raised by 644 funds in 2013. This represents the strongest market for fundraising since the recession. It’s being driven by record liquidity in the exit market. Currently, global PE IPO exits are at record levels, and M&A exit activity is up nearly 65% by value versus last year by value. As a result, global LPs are flush with distributions and increasingly able to reallocate assets in line with their desire for greater LatAm exposure. Indeed, a survey of global LPs released earlier this year by Coller Capital and the Latin American Venture Capital Association (LAVCA) found that nearly 80% of LPs with exposure to the region expect to maintain or accelerate their commitments to Latin America over the near term.

Fundraising2

Figure 3. Latin America fundraising, 2010–14 (in US$b)

$7.9

$17.8

$8.1

$5.2

$9.0

$-

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

$18.00

$20.00

2010 2011 2012 2013 2014

Source: Preqin

Private equity roundup — Latin America 7

According to Preqin data, despite its political and economic woes, Brazil is expected to receive nearly half of these resources. This represents a shift from 2013, when fundraising favored smaller funds, many of which were focused on the markets of Mexico, Central America and, in particular, the Andean region. However, 2014 has been driven by closings from several of the largest firms in the region, including Pátria Investimentos, which closed with US$1.8b in June after just eight months on the road; Advent International, which closed with US$2.1b after just six months on the road; Gávea Investimentos; and BTG Pactual.

Fundraising

The case for continued growth in fundraising in 2015 is strong. In 2012 and 2013, fundraising declined, as firms raised significant amounts of capital in the years prior. Now, many of the funds that closed during LatAm’s peak fundraising years are actively seeking exits for their investments, providing fresh capital for additional reinvestment and suggesting that the cycle may once again be on an upswing. Further, regulatory easing and the increased involvement of pensions in many markets represent a source of secular growth for the industry.

Table 2. Largest Latin American funds to close in 2014

Fund Type Final size (US$m)

Location focus

Advent Latin American Fund VI Buyout 2,100.00 Central and South America, particularly Argentina, Brazil, Colombia and Mexico

Pátria Brazilian Private Equity Fund V Buyout 1,800.00 South America, particularly BrazilGavea Investment Fund V Balanced 1,100.00 BrazilGLP Brazil Income Partners II Real estate 1,028.13 BrazilI Cuadrada Infrastructure Fund II Infrastructure 755.83 Mexico

8 Private equity roundup — Latin America

Transactions and exits3

While fundraising increased, PE firms were less active in acquiring companies in the region in 2014. The year saw just 76 transactions, down 18% from the 93 that were announced in 2013. Total deal value increased to US$4.3b from US$2.9b in 2013. Both years remain below the levels of activity seen in 2012, when volume reached 101 deals, totaling US$4.5b.

The first half of the year was more active than the second half, registering US$2.7b in transaction value, while the second half saw just US$1.6. Q1 2014 alone saw US$2.6 in announced deals. The three largest deals of the year happened in the first quarter. Activity slowed down in second half as a result of events including the World Cup and elections in many of the region’s countries.

Acquisitions

Figure 4. PE deal value in Latin America (in US$m)

$8,944

$2,063

$4,506

$2,859

$4,281

$-

$2,000

$4,000

$6,000

$8,000

$7,000

$5,000

$3,000

$1,000

$10,000

$9,000

2010 2011 2012 2013 2014

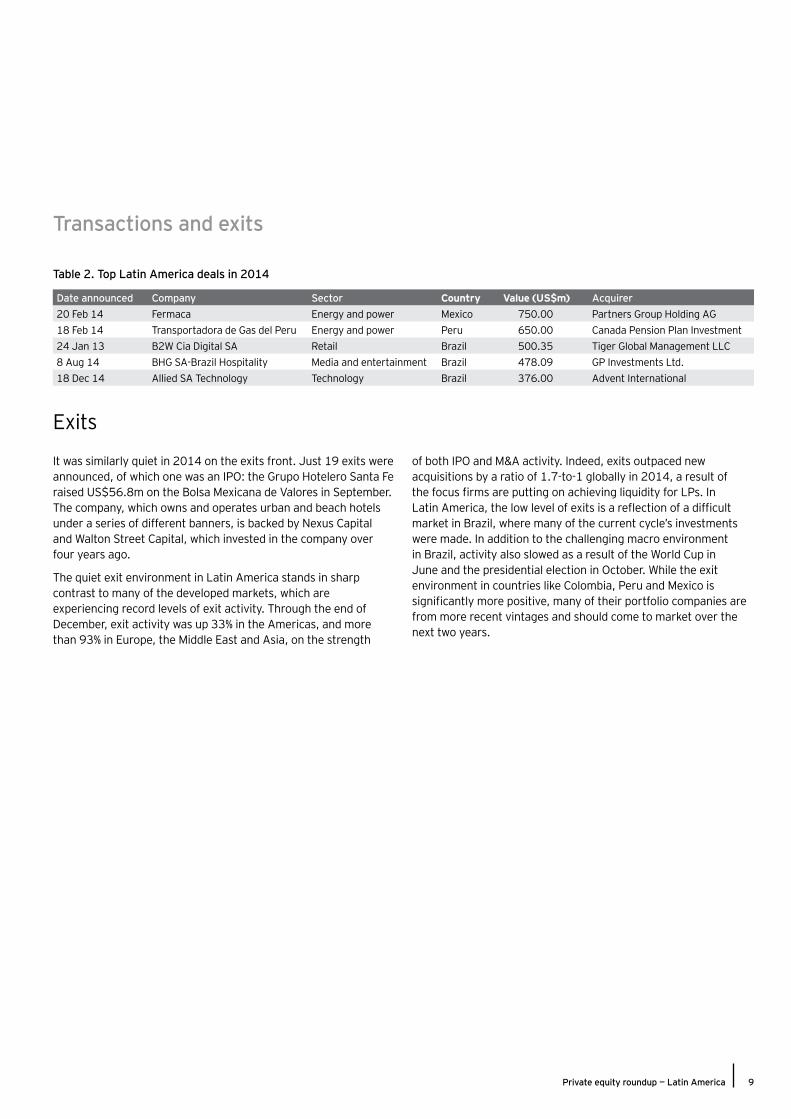

The year’s largest transaction occurred in February, when global PE firm Partners Group acquired Mexico-based Fermaca from Ospraie Management in a transaction valued at US$750m. Fermaca is a leading operator of gas infrastructure in Mexico that builds, owns and operates pipelines and other related energy assets in the country. The deal is reflective of increased interest in the oil and gas sector, and the midstream space in particular, as a result of widespread privatization efforts under way across the country.

Another significant investment in the pipeline space was the US$650m investment in Transportadora de Gas del Peru completed by the Canada Pension Plan Investment Board. It was the direct investor’s third, and largest, acquisition of shares in the company, which is the largest natural gas transporter in Peru.

While energy investments represented some of the year’s largest deals, consumer products and retail remained attractive to PE investors. In January, Tiger Global Management invested US$500.4m in e-commerce portal B2W Cia Digital SA. The company has operations across Latin America, offering nearly 40 separate categories of products and services across a range of platforms.

Private equity roundup — Latin America 9

Transactions and exits

Exits

It was similarly quiet in 2014 on the exits front. Just 19 exits were announced, of which one was an IPO: the Grupo Hotelero Santa Fe raised US$56.8m on the Bolsa Mexicana de Valores in September. The company, which owns and operates urban and beach hotels under a series of different banners, is backed by Nexus Capital and Walton Street Capital, which invested in the company over four years ago.

The quiet exit environment in Latin America stands in sharp contrast to many of the developed markets, which are experiencing record levels of exit activity. Through the end of December, exit activity was up 33% in the Americas, and more than 93% in Europe, the Middle East and Asia, on the strength

Date announced Company Sector Country Value (US$m) Acquirer20 Feb 14 Fermaca Energy and power Mexico 750.00 Partners Group Holding AG18 Feb 14 Transportadora de Gas del Peru Energy and power Peru 650.00 Canada Pension Plan Investment24 Jan 13 B2W Cia Digital SA Retail Brazil 500.35 Tiger Global Management LLC8 Aug 14 BHG SA-Brazil Hospitality Media and entertainment Brazil 478.09 GP Investments Ltd.18 Dec 14 Allied SA Technology Technology Brazil 376.00 Advent International

Table 2. Top Latin America deals in 2014

of both IPO and M&A activity. Indeed, exits outpaced new acquisitions by a ratio of 1.7-to-1 globally in 2014, a result of the focus firms are putting on achieving liquidity for LPs. In Latin America, the low level of exits is a reflection of a difficult market in Brazil, where many of the current cycle’s investments were made. In addition to the challenging macro environment in Brazil, activity also slowed as a result of the World Cup in June and the presidential election in October. While the exit environment in countries like Colombia, Peru and Mexico is significantly more positive, many of their portfolio companies are from more recent vintages and should come to market over the next two years.

10 Private equity roundup — Latin America

Regulatory update4

As the economies of Latin America continue to develop and mature, so too are regulations designed to increase the region’s attractiveness for foreign capital, including private equity investment. While a number of issues still must be addressed, among them high levels of perceived corruption and security problems in some countries, Latin America is making strides in undertaking the structural reforms necessary to attract and retain outside capital.

Perhaps the most profound of these reforms is Mexico’s continued implementation of its “Pact for Mexico.” Championed by Mexican President Peña Nieto and crossing party lines, the Pact represents a series of reforms across energy, education, labor, financial services and government that are designed to

make the country increasingly competitive internationally, and it promises to increase opportunities for a range of domestic and international investors.

In Chile, the adoption of international accounting standards for non-listed companies is a positive development for PE funds willing to invest in the local companies. Chile’s Government enacted the Single Funds Act, effective 1 May 2014, which consolidated the regulation of private equity and venture capital investment funds into a single regulatory structure. Colombia is following a similar path, and since last year it has been working to improve its regulatory framework overseeing private equity and venture capital funds.

Private equity roundup — Latin America 11

OutlookIt is a maxim of private equity that many of the best deals are made during the worst of times. While the current downturn in certain sectors of Latin America’s economy hardly qualifies as the “worst of times,” clear dislocations continue to make the operating environment increasingly challenging. Despite this, the industry has yet to see an exodus of capital. Indeed, fundraising figures and LP surveys confirm that investors continue to fund new vehicles and are maintaining or increasing their commitments.

The reasoning is clear. While cyclical volatility is increasing, the secular trends that have made the emerging markets so attractive over the last decade remain as true today as they were in 5-10 years ago: the portability of capital and labor, global demand for commodities, the rise of the middle class across the emerging markets, increased political stability, the reduction of trade barriers and other large-scale trends currently reshaping the world.

For entrepreneurs and family owners, it’s in just such challenging environments where PE’s value-add becomes its most compelling. Above and beyond simple injections of capital, the operational expertise and financial discipline that PE brings can enable savvy entrepreneurs to weather difficult macro headwinds. This was evidenced in the large number of companies that firms in the developed markets ushered through the recession to successful exits, and while the nuances of Latin America’s markets differ in significant ways, those same underlying principles — alignment of interest and good governance — will continue to work in favor of positive outcomes for current deals and continued investment across the region.

12 Private equity roundup — Latin America

Private equity roundup — Latin America 13

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

How EY’s Global Private Equity Center can help your business Value creation goes beyond the private equity investment cycle to portfolio company and fund advice. EY’s Global Private Equity Center offers a tailored approach to the unique needs of private equity funds, their transaction processes, investment stewardship and portfolio companies’ performance. We focus on the market, sector and regulatory issues. If you lead a private equity business, we can help you meet your evolving requirements and those of your portfolio companies from acquisition to exit through a highly integrated global resource of 175,000 professionals across audit, tax, transactions and advisory services. Working together, we can help you meet your goals and compete more effectively.

© 2015 EYGM Limited. All Rights Reserved.

EYG no. FR0147CSG/GSC2014/1503342ED None

In line with EY’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com/privateequity

EY | Assurance | Tax | Transactions | Advisory