Embed Size (px)

Citation preview

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy

Principes de choix

de portefeuille7e édition

Christophe Boucher

1

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy

Chapitre 47e édition

La théorie Moyenne-Variance du choix de portefeuille

2

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

Part 4. Mean-Variance Portfolio Theory

3

4.1 Measuring Risk and Return

4.2 Asset Allocation with 2 Risky Assets

4.3 Introducing a Risk Free Asset and the Tobin’s Separation Theorem

4.4 Asset Allocation with N risky Assets

4.5 Portfolio Diversification

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

Preamble:

Mean/Variance Analysis Assumptions

4

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

Mean-variance is simpler

5

• Early researchers in finance, such as Markowitz and Sharpe, used just the mean and the variance of the return rate of an asset to describe it.

• Characterizing the prospects of a gamble with its mean and variance is often easier than using an NM utility function, so it is popular.

• But is it compatible with VNM theory?

• The answer is yes … approximately … under some conditions.

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

Mean-variance assumptions

6

• Investors maximise expected utility of end-of-perio d wealth

• Can be shown that above implies maximise a function of expected portfolio returns and portfolio variance p roviding

- Either utility is quadratic, or

- Portfolio returns are normally distributed (and utility is concave),

- Consider only small risks (then approximately true)

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

Mean-variance: quadratic utility

7

Suppose utility is quadratic, U(y) = ay–by2,

with some conditions on a and b

Expected utility is then

2

2

[ ( )] ( ) ( )

( ) ( ) V ar( ) .

E U y aE y bE y

aE y b E y y

= −

= − +

Thus, expected utility is a function of:

the mean: E(y),

and the variance: Var(y)

BUT not intuitive Utility function : increasing ARA

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

Mean-variance: joint normals

8

• Suppose all lotteries in the domain have normally distributed prized. (They need not be independent of each other).

• Any combination of such lotteries will also be normally distributed.

• The normal distribution is completely described by its first two moments.

• Therefore, the distribution of any combination of lotteries is also completely described by just the mean and the variance.

• As a result, expected utility can be expressed as a function of just these two numbers as well.

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

Mean-variance: small risks

9

• The most relevant justification for mean-variance is probably the case of small risks.

• If we consider only small risks, we may use a second order Taylor approximation of the NM utility function.

• A second order Taylor approximation of a concave function is a quadratic function with a negative coefficient on the quadratic term.

• In other words, any risk-averse NM utility function can locally be approximated with a quadratic function.

• But the expectation of a quadratic utility function can be evaluated with the mean and variance. Thus, to evaluate small risks, mean and variance are enough.

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

Mean-variance: small risks

10

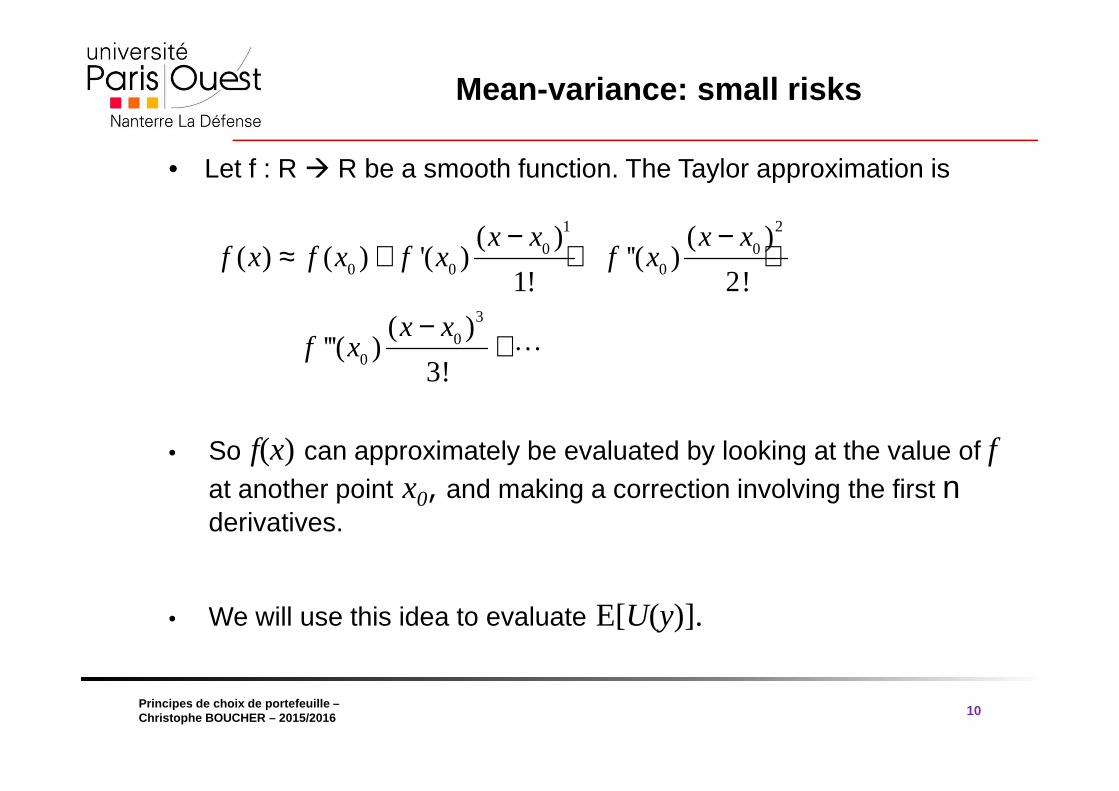

• Let f : R R be a smooth function. The Taylor approximation is

• So f(x) can approximately be evaluated by looking at the value of fat another point x0, and making a correction involving the first nderivatives.

• We will use this idea to evaluate E[U(y)].

1 2

0 00 0 0

3

00

( ) ( )( ) ( ) '( ) ''( )

1! 2!

( )'''( )

3!

x x x xf x f x f x f x

x xf x

− −≈ + + +

−+⋯

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

Mean-variance: small risks

11

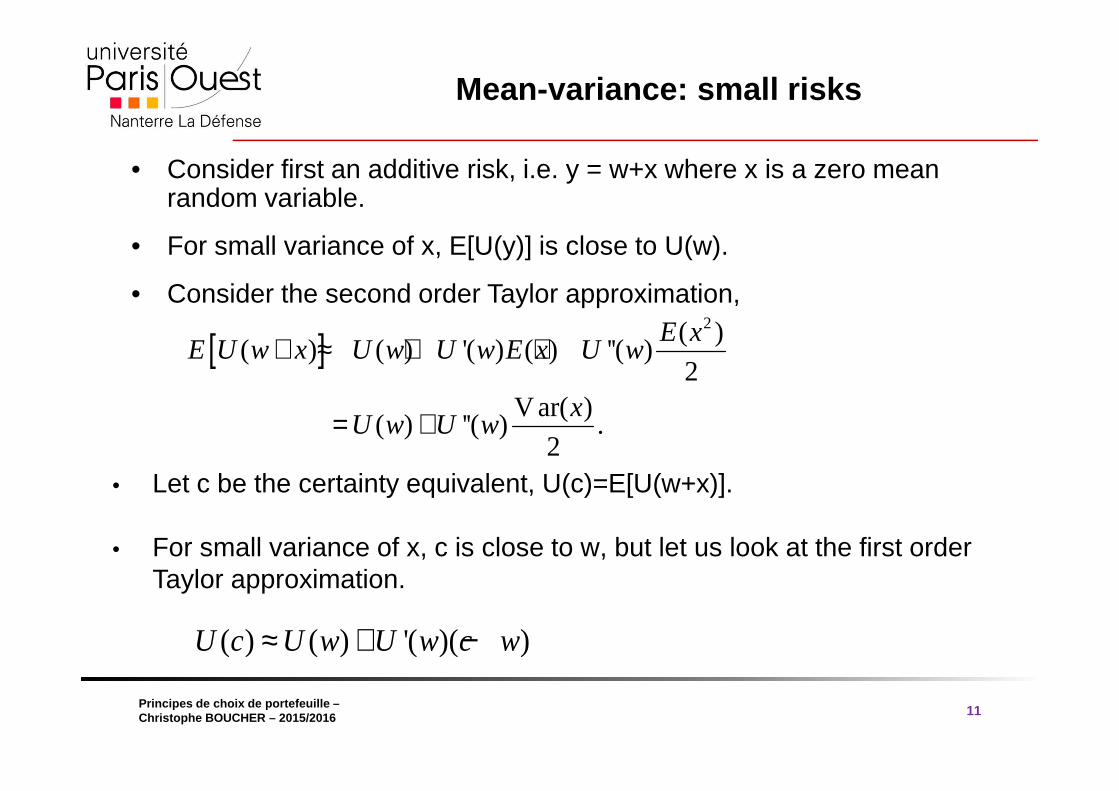

• Consider first an additive risk, i.e. y = w+x where x is a zero mean random variable.

• For small variance of x, E[U(y)] is close to U(w).

• Consider the second order Taylor approximation,

• Let c be the certainty equivalent, U(c)=E[U(w+x)].

• For small variance of x, c is close to w, but let us look at the first order Taylor approximation.

[ ]2( )

( ) ( ) '( ) ( ) ''( )2

Var( )( ) ''( ) .

2

E xE U w x U w U w E x U w

xU w U w

+ ≈ + +

= +

( ) ( ) '( )( )U c U w U w c w≈ + −

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

Mean-variance: small risks

12

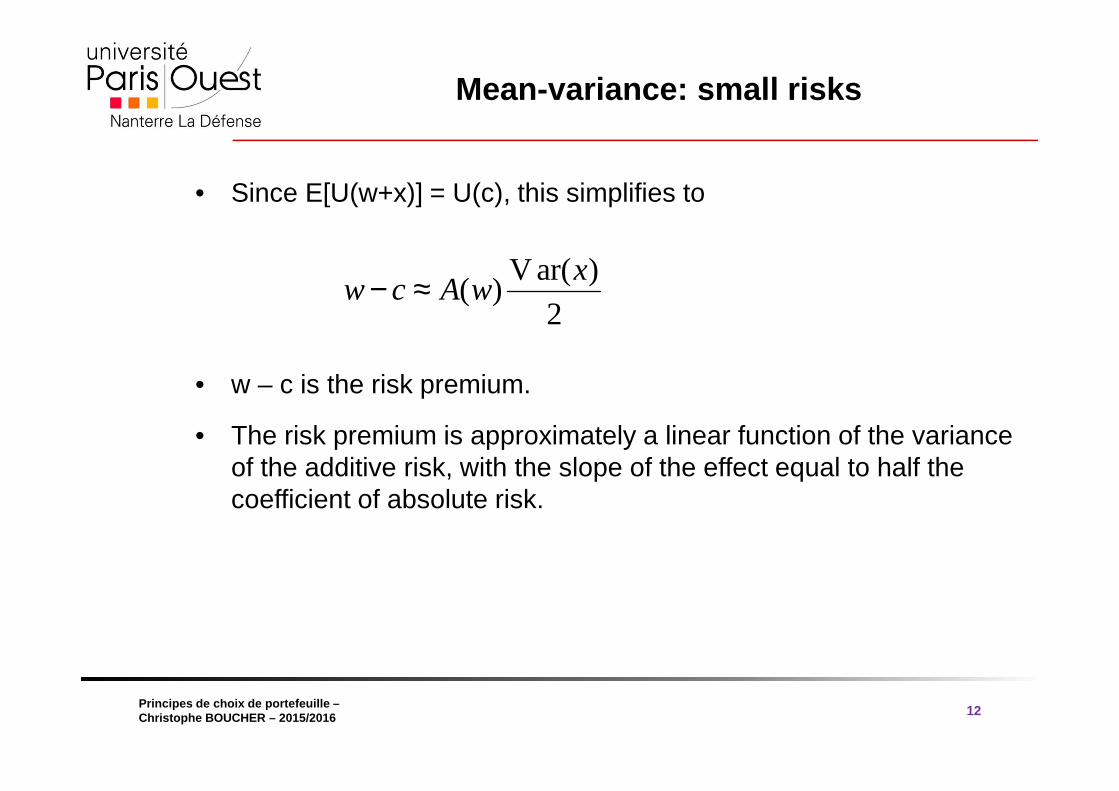

• Since E[U(w+x)] = U(c), this simplifies to

• w – c is the risk premium.

• The risk premium is approximately a linear function of the variance of the additive risk, with the slope of the effect equal to half the coefficient of absolute risk.

V ar( )( )

2

xw c A w− ≈

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

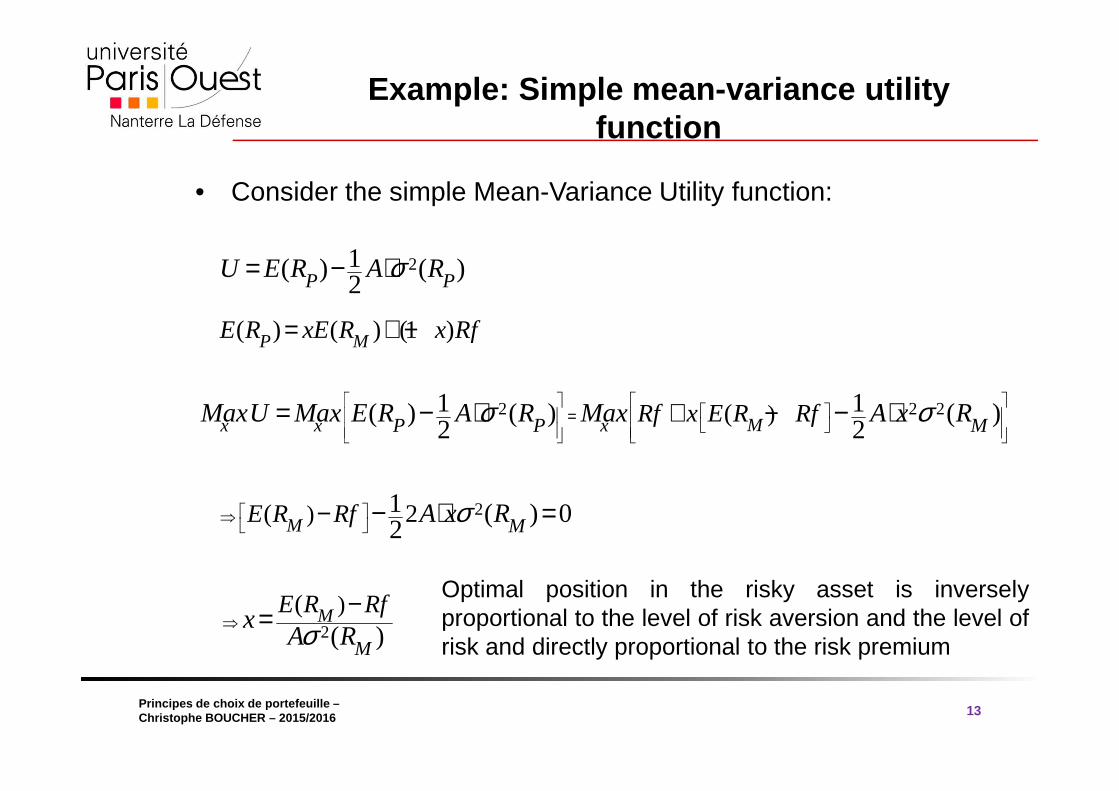

Example: Simple mean-variance utility function

13

• Consider the simple Mean-Variance Utility function:

21( ) ( )2P PU E R A Rσ= − ⋅

2 2 2)(1 1( ) ( ) ( )2 2Mx x xP P MRf x E R RfMaxU Max E R A R Max A x Rσ σ

=

+ −= − ⋅ − ⋅

( ) ( ) (1 )P ME R xE R x Rf= + −

2)( 21 ( ) 02M ME R Rf A x Rσ ⇒

− − ⋅ =

2

)(( )

M

M

E R Rfx

A Rσ⇒−=

Optimal position in the risky asset is inverselyproportional to the level of risk aversion and the level ofrisk and directly proportional to the risk premium

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

4.1 Measuring Risk and Return

14

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

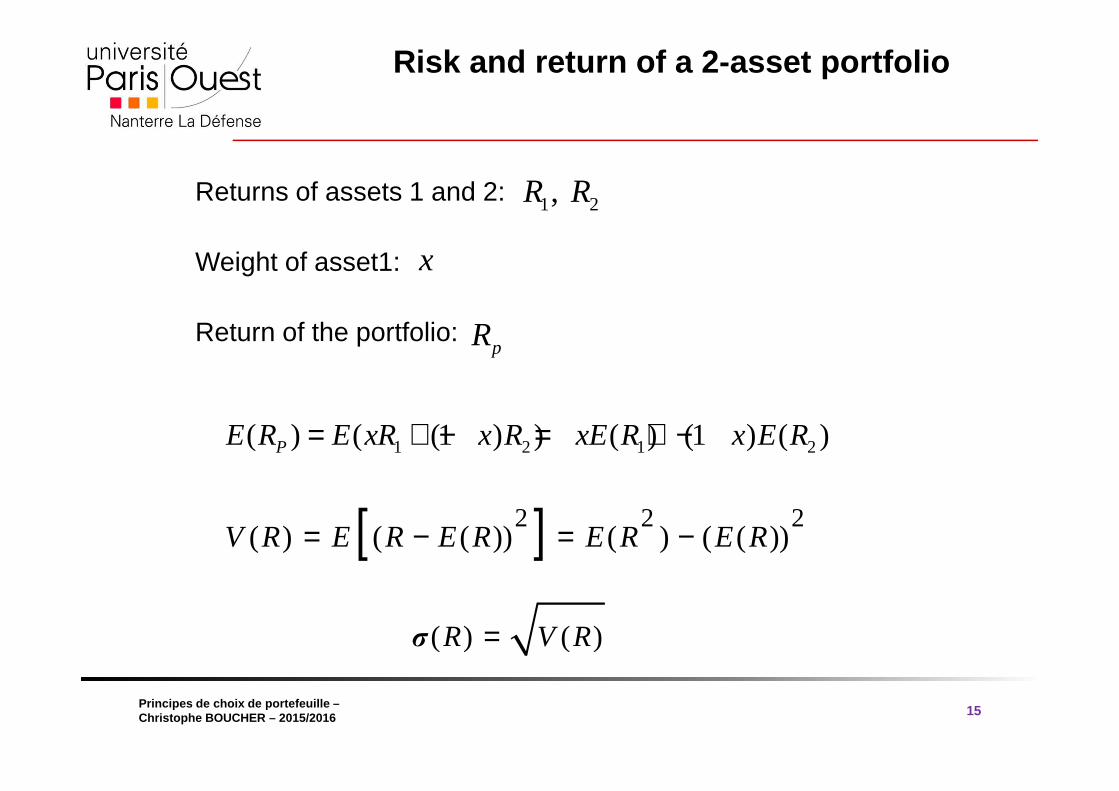

Returns of assets 1 and 2:

Weight of asset1:

Return of the portfolio:

Risk and return of a 2-asset portfolio

15

1 2, R R

x

pR

1 2 1 2( ) ( (1 ) ) ( ) (1 ) ( )PE R E xR x R xE R x E R= + − = + −

[ ]2 2 2( ) ( ( )) ( ) ( ( ))V R E R E R E R E R= − = −

( ) ( )R V Rσ =

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

Risk and return of a 2-asset portfolio

16

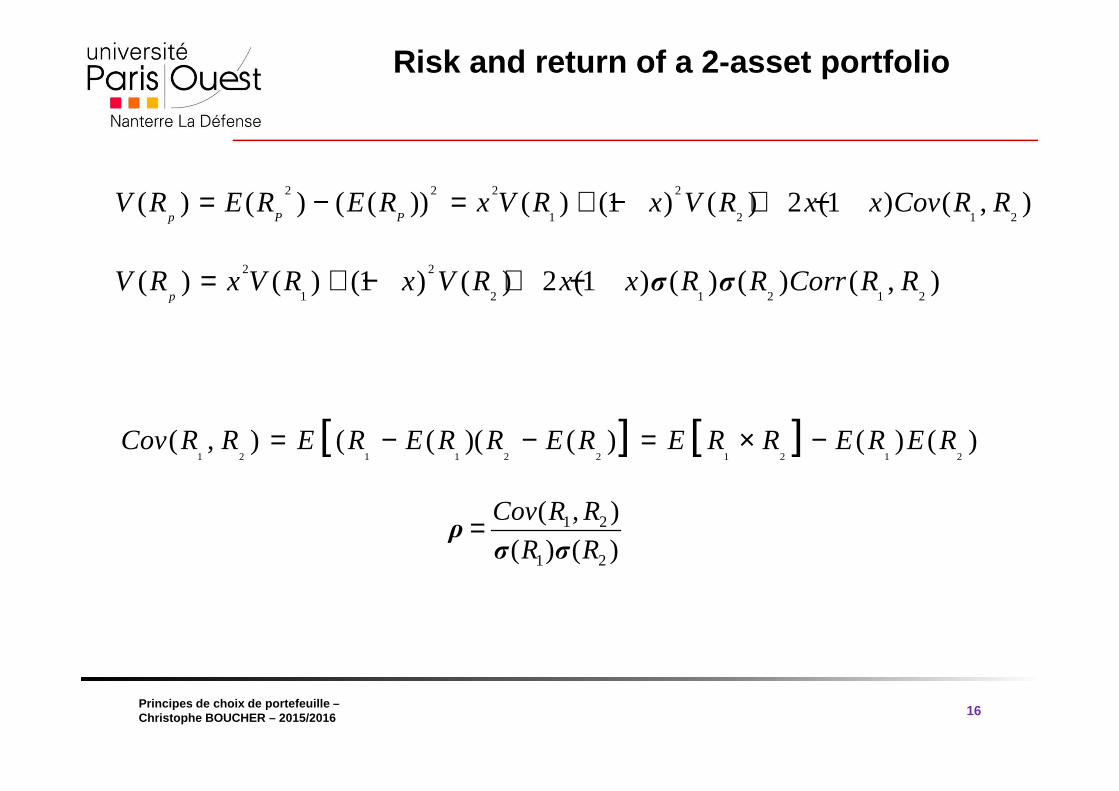

2 2 2 2

1 2 1 2( ) ( ) ( ( )) ( ) (1 ) ( ) 2 (1 ) ( , )

p P PV R E R E R x V R x V R x x Cov R R= − = + − + −

2 2

1 2 1 2 1 2( ) ( ) (1 ) ( ) 2 (1 ) ( ) ( ) ( , )

pV R x V R x V R x x R R Corr R Rσ σ= + − + −

[ ] [ ]1 2 1 1 2 2 1 2 1 2

( , ) ( ( )( ( ) ( ) ( )Cov R R E R E R R E R E R R E R E R= − − = × −

1 2

1 2

( , )

( ) ( )

Cov R R

R R=ρσ σ

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

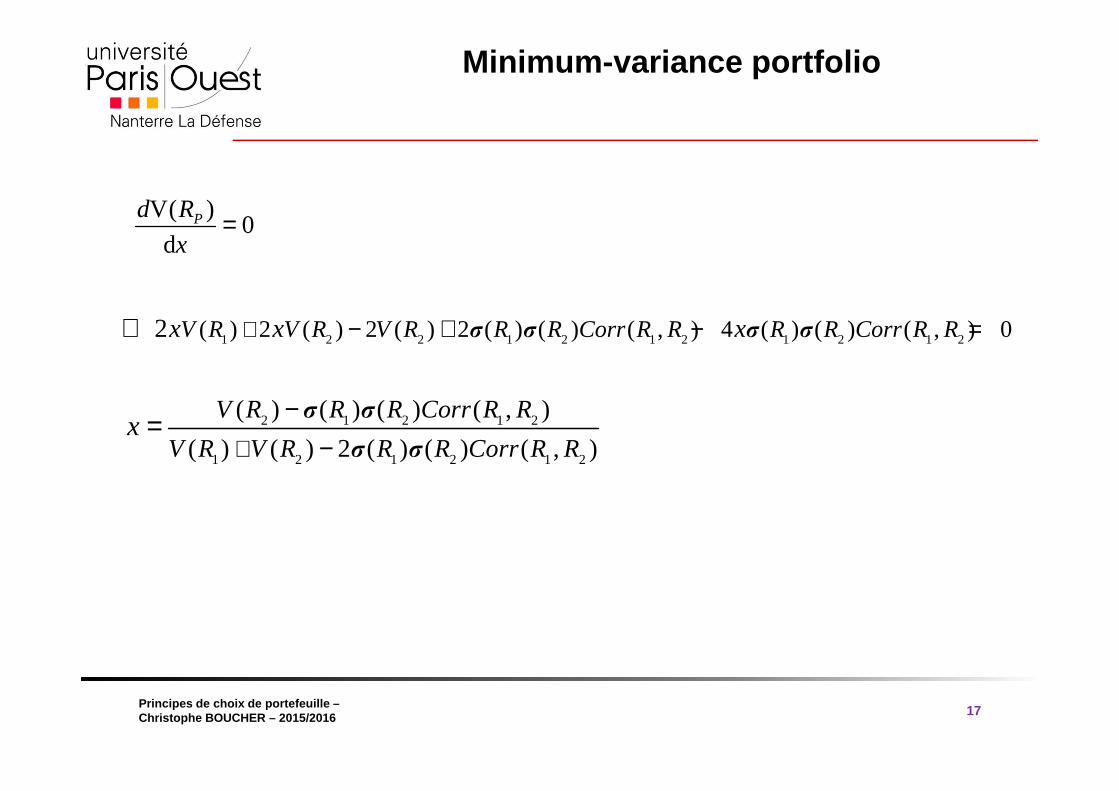

Minimum -variance portfolio

17

V( )0

dPd R

x=

1 2 2 1 2 1 2 1 2 1 2( ) 2 ( ) 2 ( ) 2 ( ) ( ) ( , ) 4 ( ) ( ) ( , ) 02 V R V R V R R R Corr R R R R Corr R Rx x xσ σ σ σ+ − + − =⇔

2 1 2 1 2

1 2 1 2 1 2

( ) ( ) ( ) ( , )

( ) ( ) 2 ( ) ( ) ( , )

V R R R Corr R R

V R V R R R Corr R Rx

σ σ

σ σ+

−−

=

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

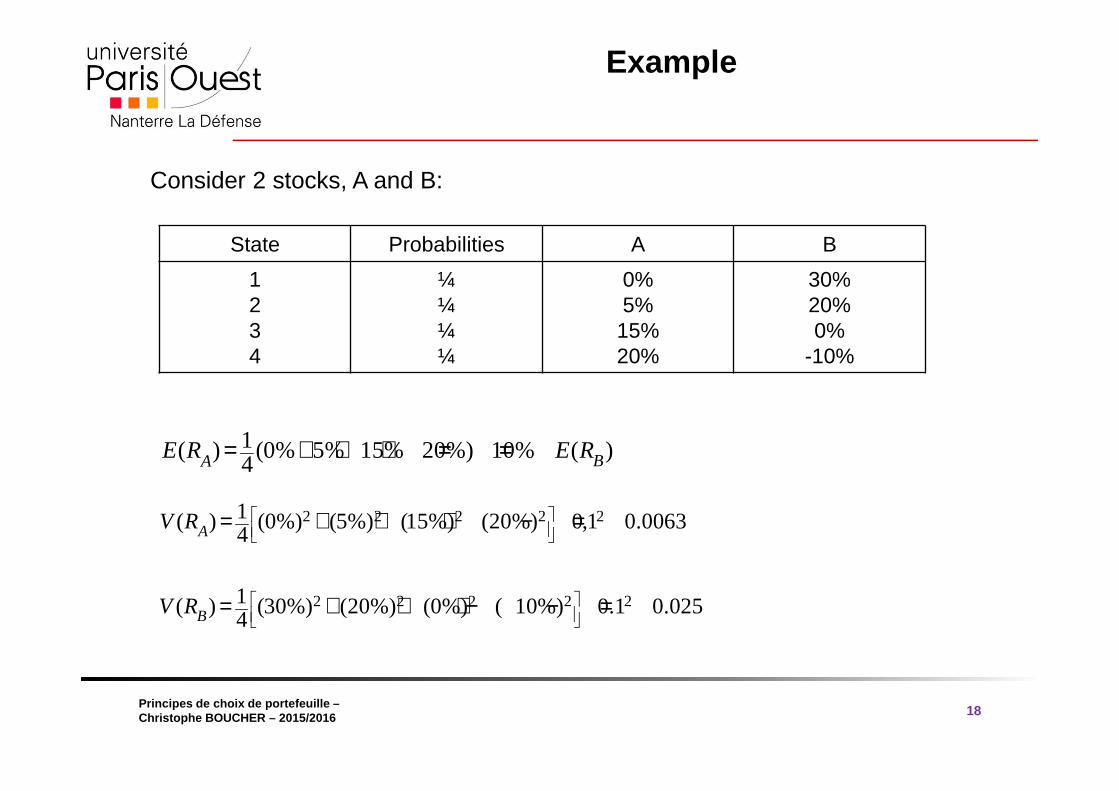

Example

18

Consider 2 stocks, A and B:

State Probabilities A B

1234

¼¼¼¼

0%5%

15%20%

30%20%0%

-10%

1( ) (0% 5% 15% 20%) 10% ( )4 BAE R E R= + + + = =

2 2 2 2 21( ) (0%) (5%) (15%) (20%) 0,1 0.00634AV R

= + + + − =

2 2 2 2 21( ) (30%) (20%) (0%) ( 10%) 0.1 0.0254BV R

= + + + − − =

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

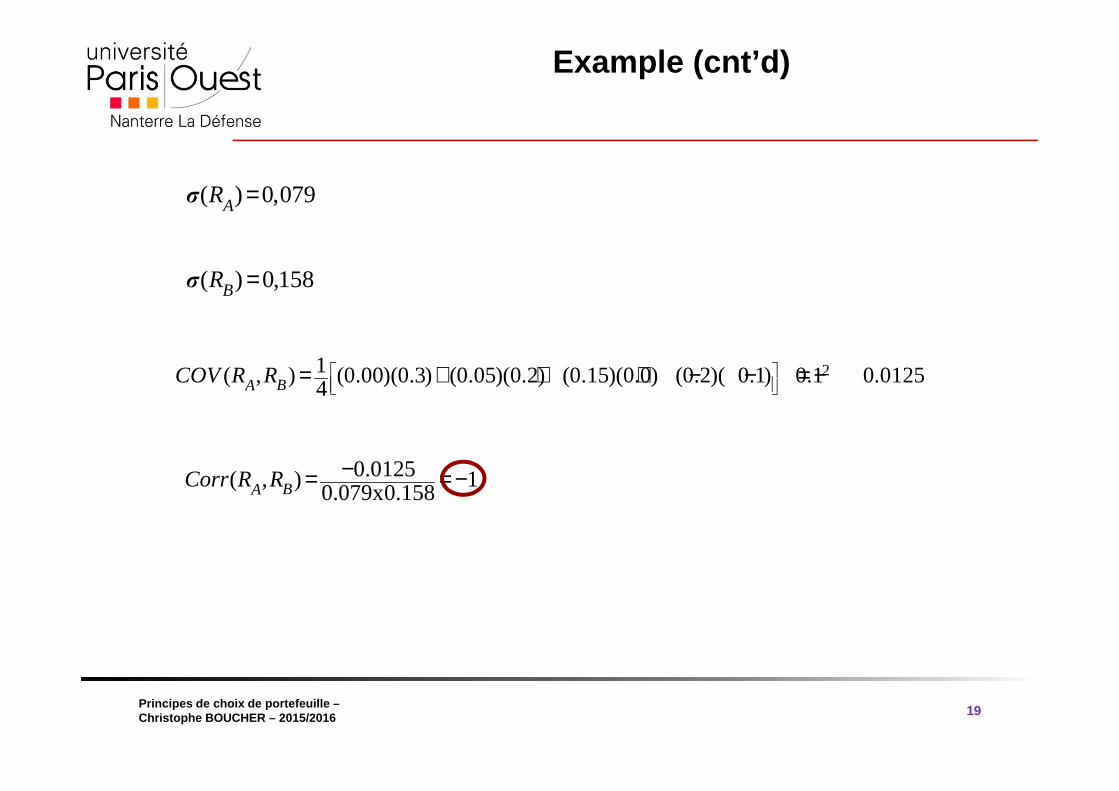

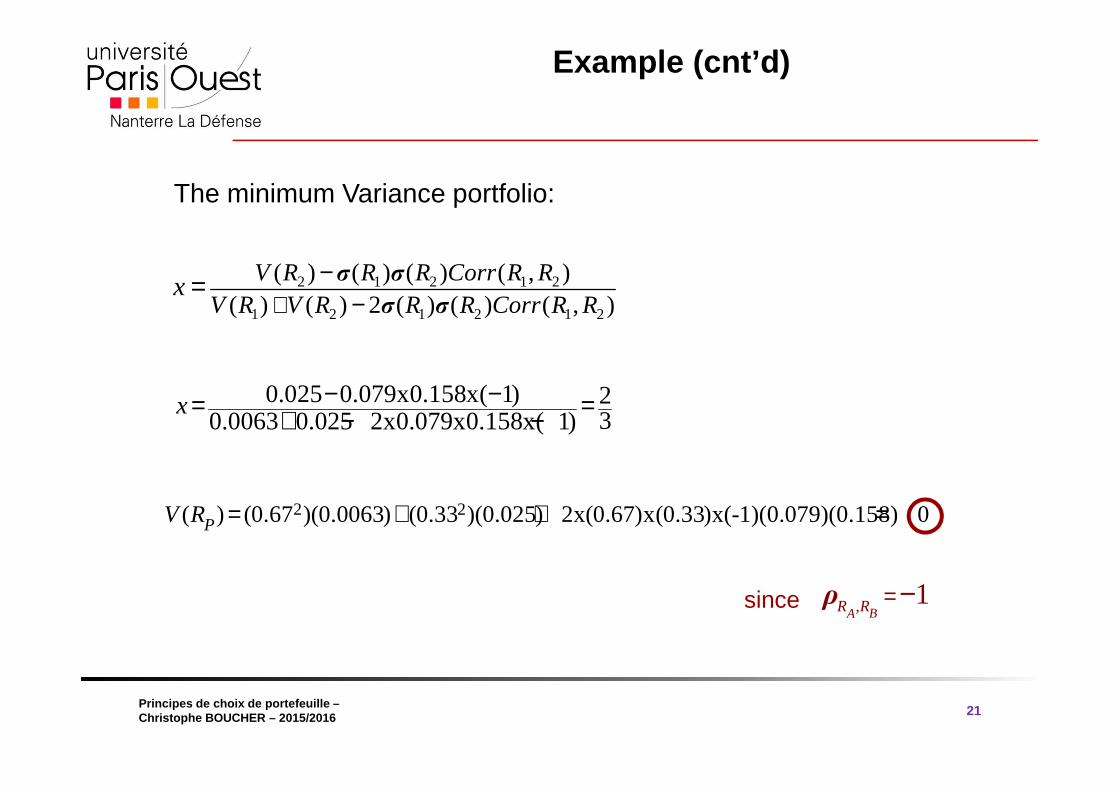

Example (cnt’d)

19

( ) 0,079AR =σ

( ) 0,158BR =σ

21( , ) (0.00)(0.3) (0.05)(0.2) (0.15)(0.0) (0.2)( 0.1) 0.1 0.01254BACOV R R

= + + + − − = −

0.0125( , ) 10.079x0.158BACorr R R −= = −

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

Example (cnt’d)

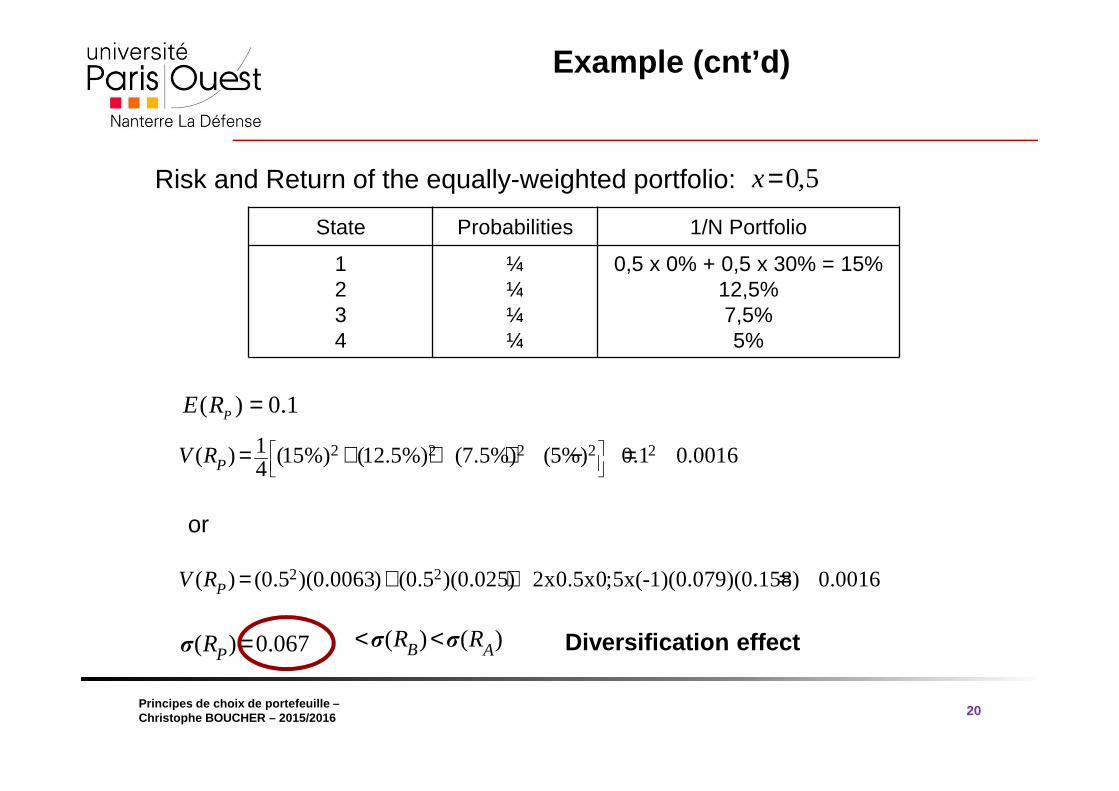

20

Risk and Return of the equally-weighted portfolio: 0,5x=

State Probabilities 1/N Portfolio

1234

¼¼¼¼

0,5 x 0% + 0,5 x 30% = 15%12,5%7,5%5%

( ) 0.1PE R =

2 2 2 2 21( ) (15%) (12.5%) (7.5%) (5%) 0.1 0.00164PV R

= + + + − =

or

2 2( ) (0.5 )(0.0063) (0.5 )(0.025) 2x0.5x0;5x(-1)(0.079)(0.158) 0.0016PV R = + + =

( ) 0.067PR =σ ( ) ( )B AR R< <σ σ Diversification effect

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

Example (cnt’d)

21

The minimum Variance portfolio:

2 1 2 1 2

1 2 1 2 1 2

( ) ( ) ( ) ( , )( ) ( ) 2 ( ) ( ) ( , )

V R R R Corr R RV R V R R R Corr R R

x+

−−

= σ σ

σ σ

0.025 0.079x0.158x( 1) 230.0063 0.025 2x0.079x0.158x( 1)

x − −= =+ − −

2 2( ) (0.67 )(0.0063) (0.33 )(0.025) 2x(0.67)x(0.33)x(-1)(0.079)(0.158) 0PV R = + + =

since , 1BAR R =−ρ

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

4.2 Asset Allocation with 2 Risky Assets

22

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

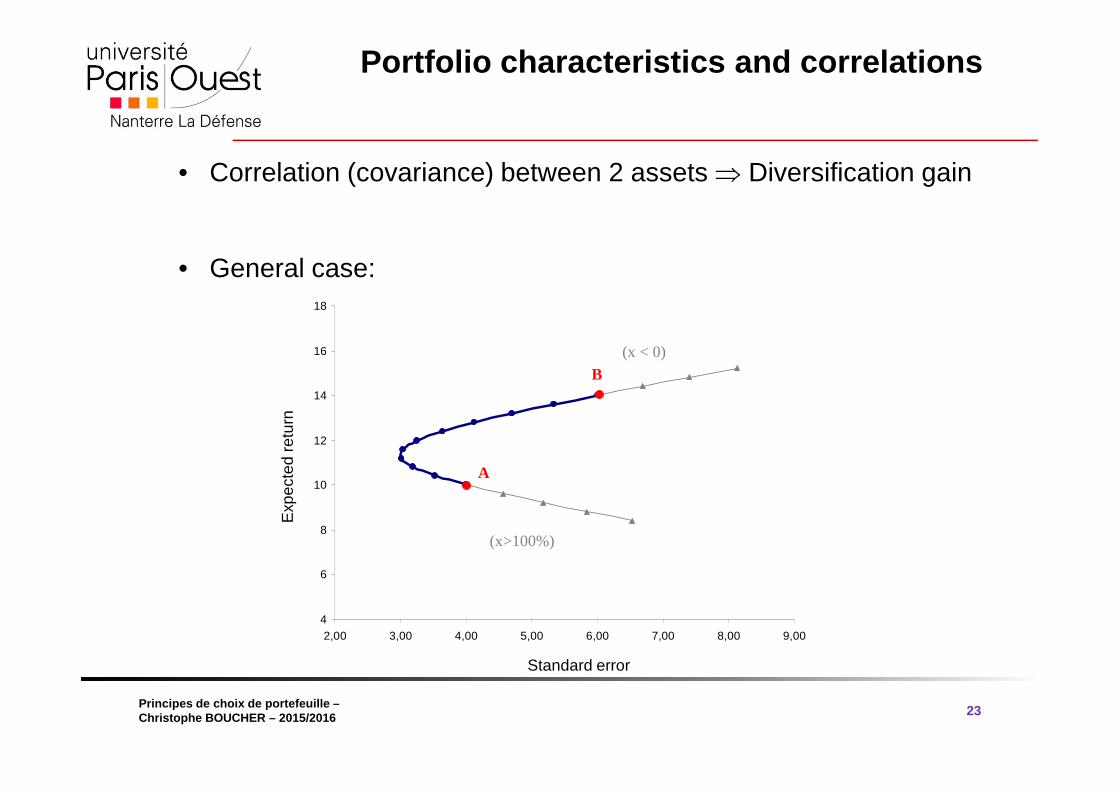

Portfolio characteristics and correlations

23

• Correlation (covariance) between 2 assets ⇒ Diversification gain

• General case:

4

6

8

10

12

14

16

18

2,00 3,00 4,00 5,00 6,00 7,00 8,00 9,00

A

B

(x>100%)

(x < 0)

4

6

8

10

12

14

16

18

2,00 3,00 4,00 5,00 6,00 7,00 8,00 9,004

6

8

10

12

14

16

18

2,00 3,00 4,00 5,00 6,00 7,00 8,00 9,00

A

B

(x>100%)

(x < 0)

Exp

ecte

d re

turn

Standard error

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

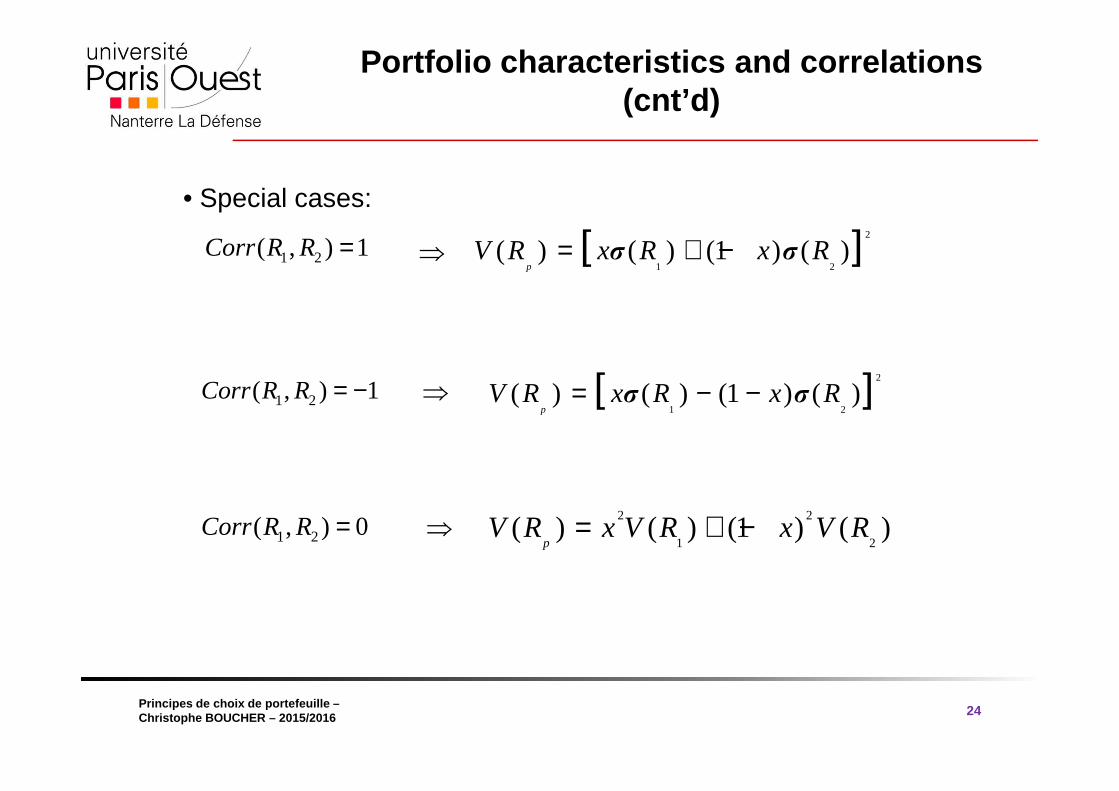

Portfolio characteristics and correlations (cnt’d)

24

• Special cases:

1 2( , ) 1Corr R R =

1 2( , ) 1Corr R R = −

1 2( , ) 0Corr R R =

[ ]2

1 2( ) ( ) (1 ) ( )

pV R x R x R= + −σ σ⇒

[ ]2

1 2( ) ( ) (1 ) ( )

pV R x R x Rσ σ= − −⇒

2 2

1 2( ) ( ) (1 ) ( )

pV R x V R x V R= + −⇒

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

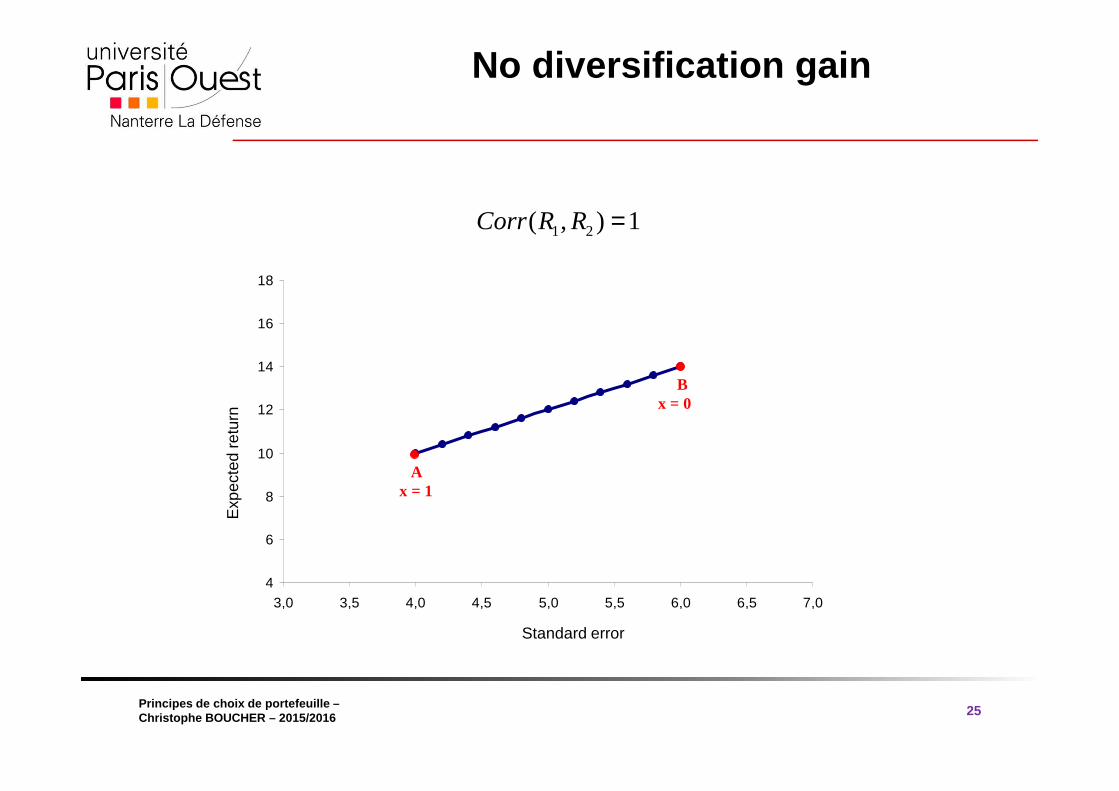

No diversification gain

25

1 2( , ) 1Corr R R =

4

6

8

10

12

14

16

18

3,0 3,5 4,0 4,5 5,0 5,5 6,0 6,5 7,0

Ren

dem

ent e

spér

é du

por

tefe

uille

(%

)

A

B

x = 1

x = 0

Exp

ecte

d re

turn

Standard error

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

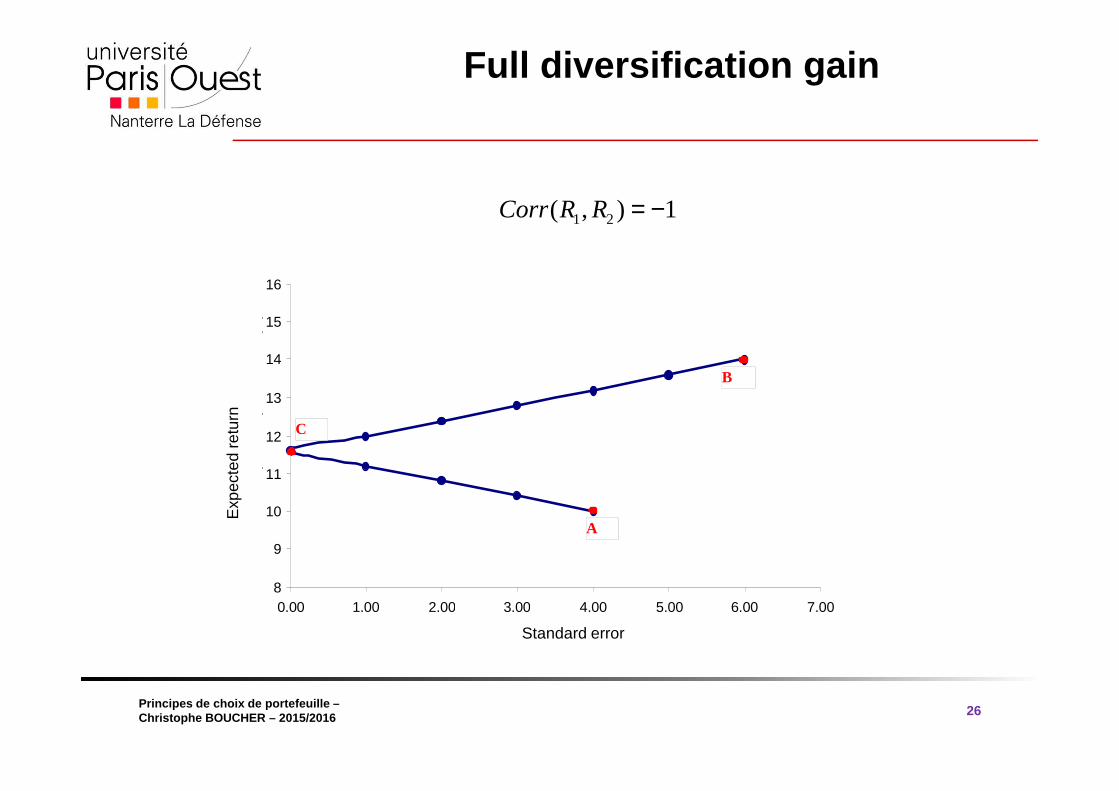

Full diversification gain

26

1 2( , ) 1Corr R R = −E

xpec

ted

retu

rn

Standard error

8

9

10

11

12

13

14

15

16

0,00 1,00 2,00 3,00 4,00 5,00 6,00 7,00Ecart type du portefeuille (%)

Ren

dem

ent e

spér

é du

por

tefe

uille

(%

)

A

B

C

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

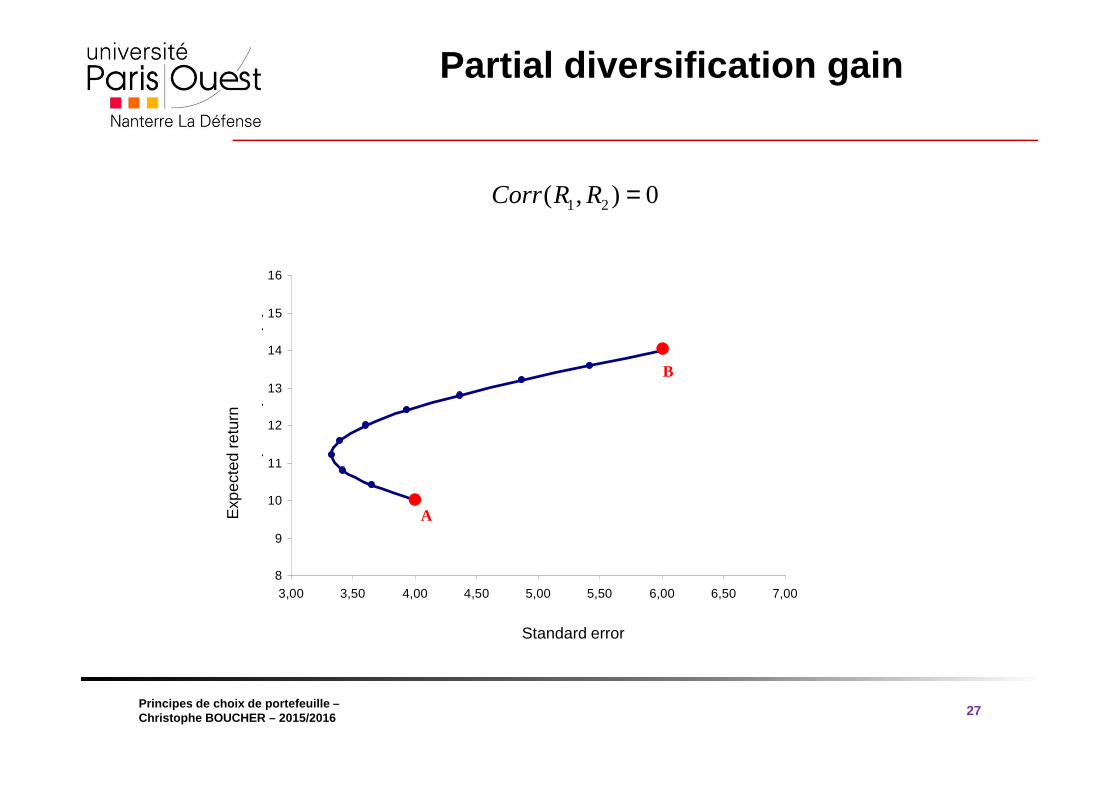

Partial diversification gain

27

1 2( , ) 0Corr R R =E

xpec

ted

retu

rn

Standard error

8

9

10

11

12

13

14

15

16

3,00 3,50 4,00 4,50 5,00 5,50 6,00 6,50 7,00

Ren

dem

ent e

spér

é du

por

tefe

uille

(%

)

A

B

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

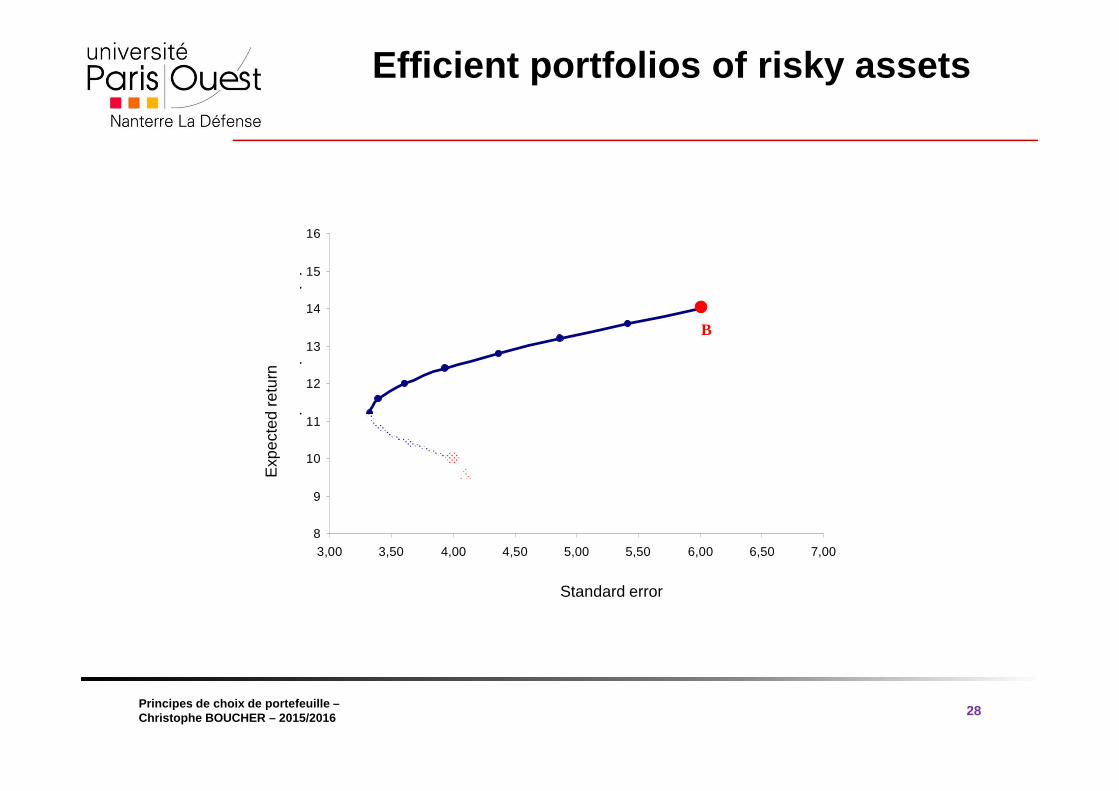

Efficient portfolios of risky assets

28

Exp

ecte

d re

turn

Standard error

8

9

10

11

12

13

14

15

16

3,00 3,50 4,00 4,50 5,00 5,50 6,00 6,50 7,00

Ren

dem

ent e

spér

é du

por

tefe

uille

(%

)

A

B

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

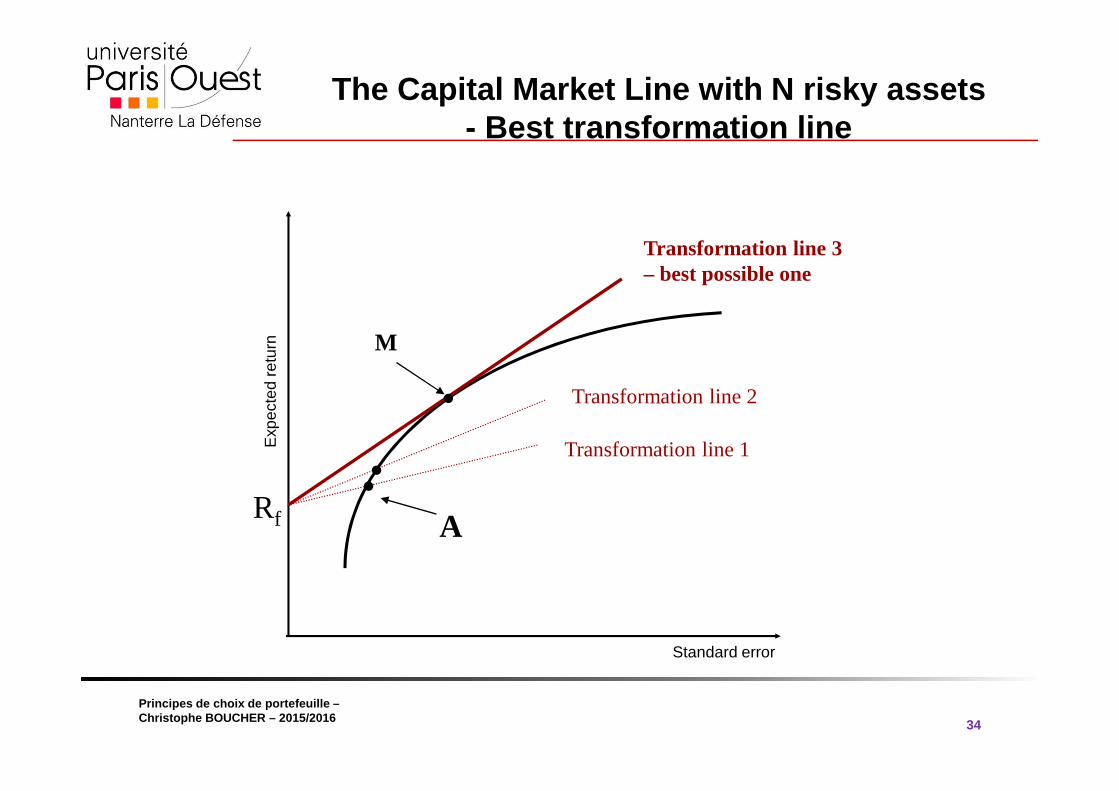

4.3 Introducing a Risk Free Asset and the Tobin’s Separation Theorem

29

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

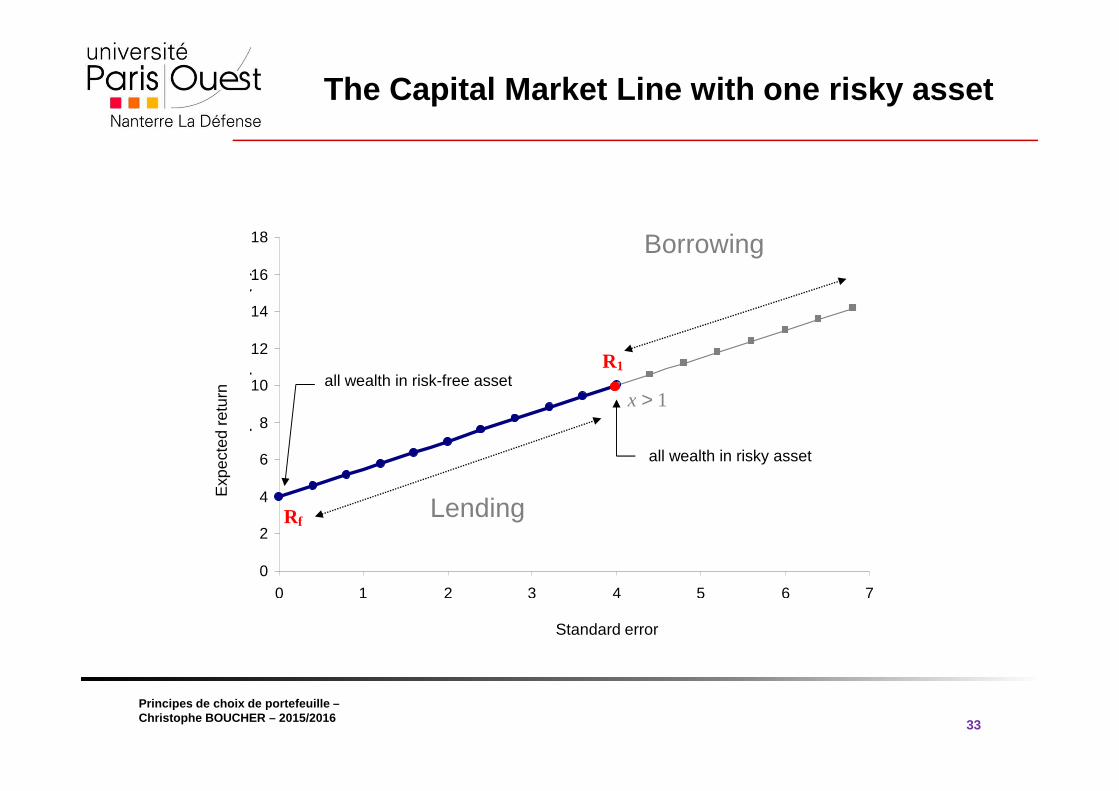

Introducing borrowing and lending:Risk free asset

30

• You are now allowed to borrow and lend at the risk free rate Rf while still investing in any SINGLE ‘risky bundle’ on the efficient frontier.

• For each SINGLE risky bundle, this gives a new set of risk return combination known as the ‘transformation line’.

• The risk-return combination is a straight line (for each single risky bundle) - transformation line.

• You can be anywhere you like on this line.

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

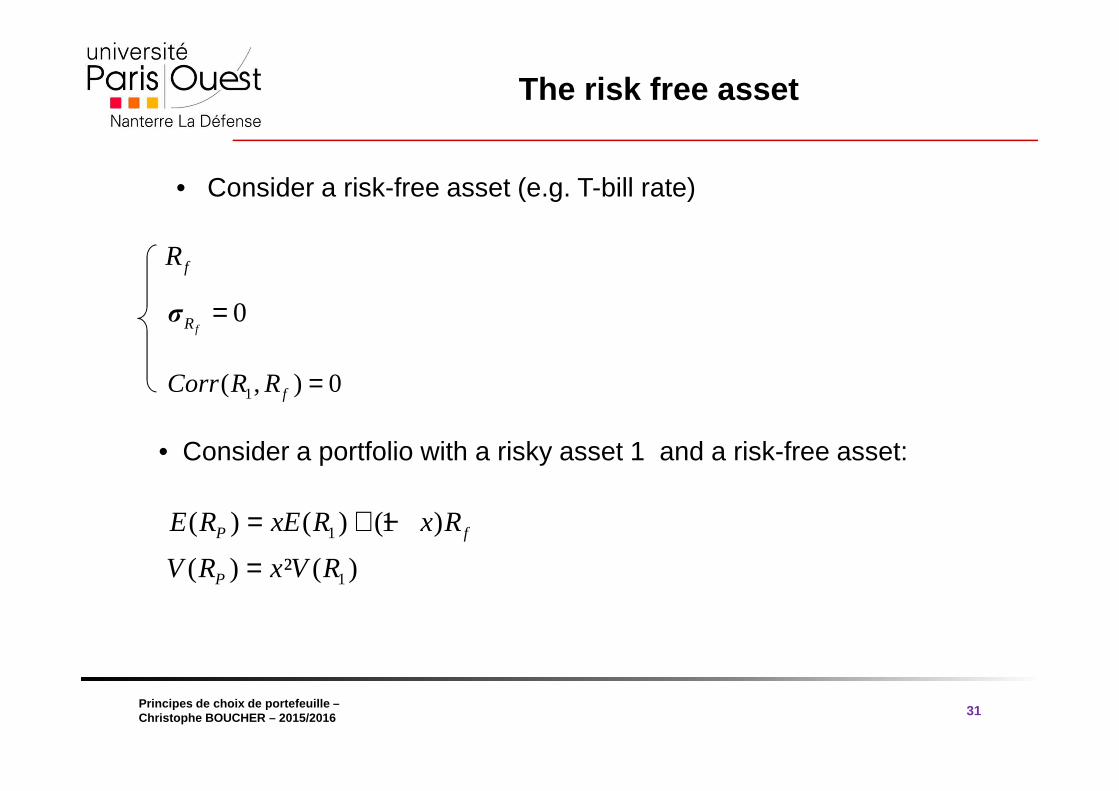

The risk free asset

31

• Consider a risk-free asset (e.g. T-bill rate)

fR

0fRσ =

1( , ) 0fCorr R R =

• Consider a portfolio with a risky asset 1 and a risk-free asset:

1

1

( ) ( ) (1 )

( ) ² ( )P f

P

E R xE R x R

V R x V R

= + −

=

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

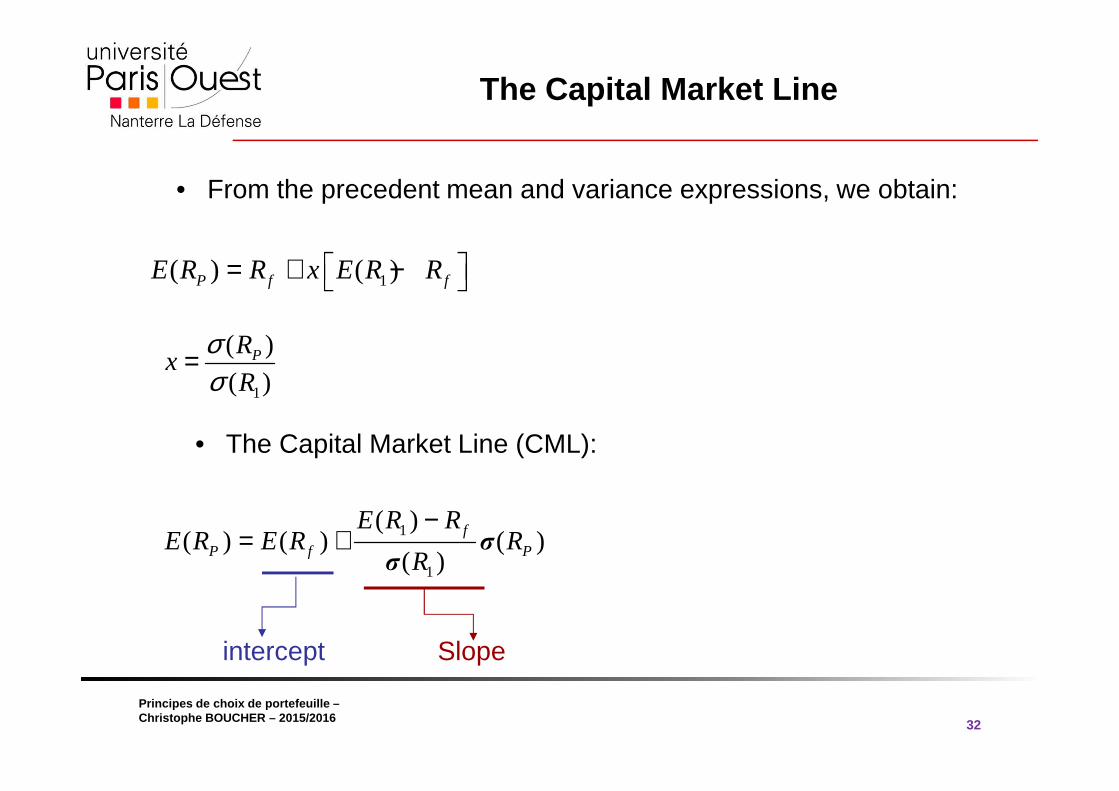

The Capital Market Line

32

• From the precedent mean and variance expressions, we obtain:

1( ) ( )P f fE R R x E R R = + −

1

( )

( )PR

xR

σσ

=

• The Capital Market Line (CML):

1

1

( )( ) ( ) ( )

( )f

P f P

E R RE R E R R

R

−= + σ

σ

Slopeintercept

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

The Capital Market Line with one risky asset

33

0

2

4

6

8

10

12

14

16

18

0 1 2 3 4 5 6 7

Ren

dem

ent e

spér

é du

por

tefe

uille

(%

)

R1

Rf

x > 1

all wealth in risky asset

Exp

ecte

d re

turn

Standard error

all wealth in risk-free asset

Lending

Borrowing

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

The Capital Market Line with N risky assets- Best transformation line

34

Exp

ecte

d re

turn

Standard error

Transformation line 1

Transformation line 2

Transformation line 3 – best possible one

Rf A

M

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

The Capital Market Line

35

Exp

ecte

d re

turn

Standard error

CML

Rf

M

Risk PremiumE(RM) – Rf

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

The CML and the separation theorem

36

• The CML dominates all other possible portfolios

• An agent invests along the CML (where ? ⇒ risk preferences)

• James Tobin’s separation theorem:

- Invest in a risky portfolio (optimal combination of risky securities)

- Borrow-lend at the risk-free rate

• Depending on your attitude toward risk: how much lend or borrow

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

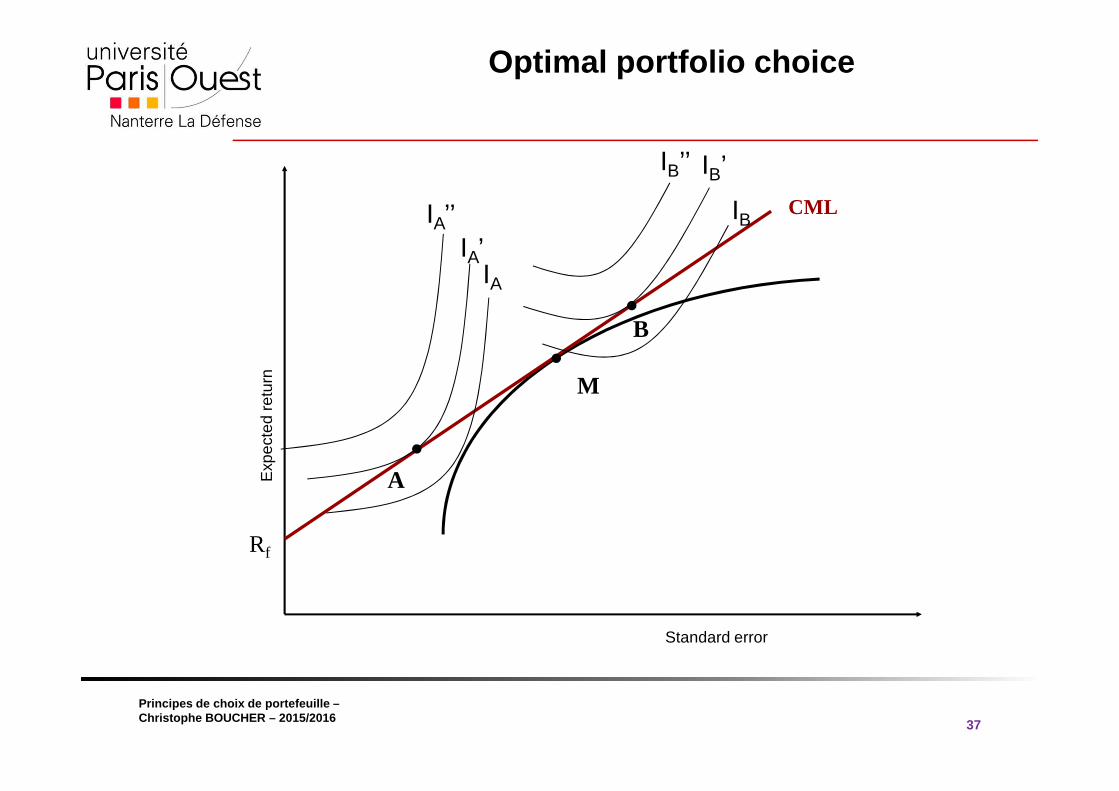

Optimal portfolio choice

37

Exp

ecte

d re

turn

CML

Rf

M

Standard error

A

B

IA’IA’’ IB

IA

IB’’ IB’

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

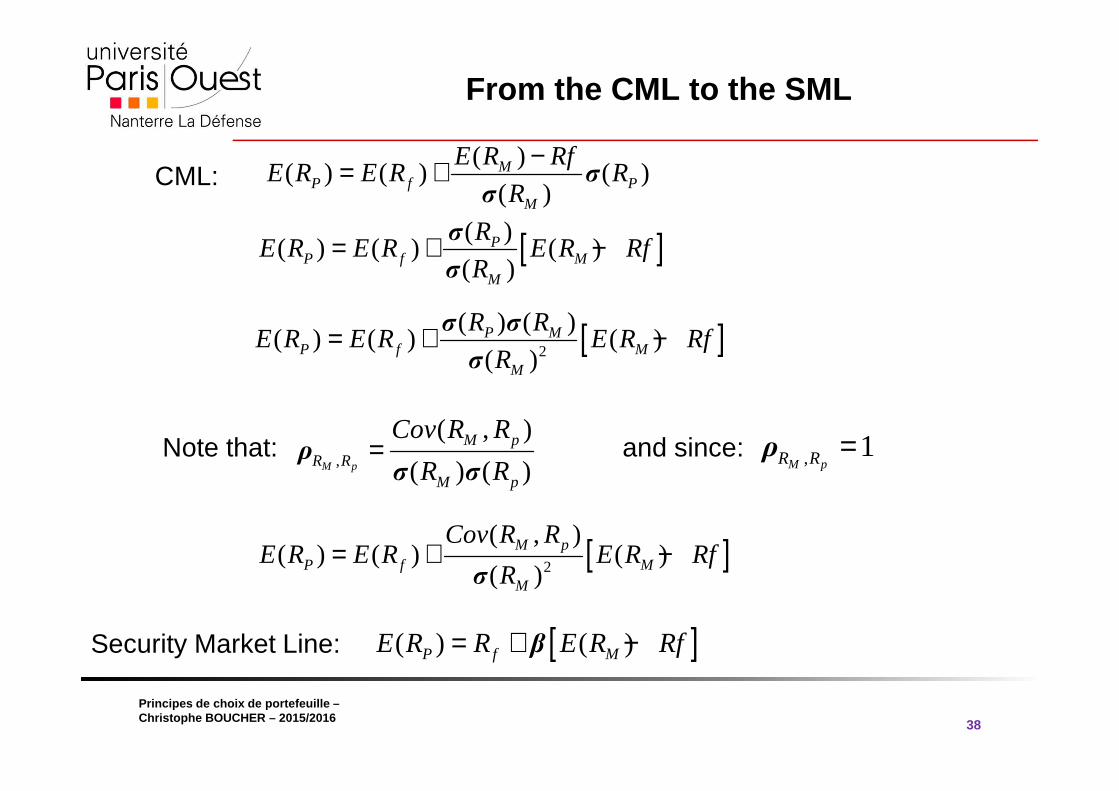

From the CML to the SML

38

( )( ) ( ) ( )

( )M

P f PM

E R RfE R E R R

R

−= + σσ

CML:

[ ]( )( ) ( ) ( )

( )P

P f MM

RE R E R E R Rf

R= + −σ

σ

Note that:,

( , )

( ) ( )M p

M pR R

M p

Cov R R

R R=ρσ σ

and since: , 1M pR R =ρ

[ ]2

( ) ( )( ) ( ) ( )

( )P M

P f MM

R RE R E R E R Rf

R= + −σ σ

σ

[ ]2

( , )( ) ( ) ( )

( )M p

P f MM

Cov R RE R E R E R Rf

R= + −

σ

Security Market Line: [ ]( ) ( )P f ME R R E R Rf= + −β

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

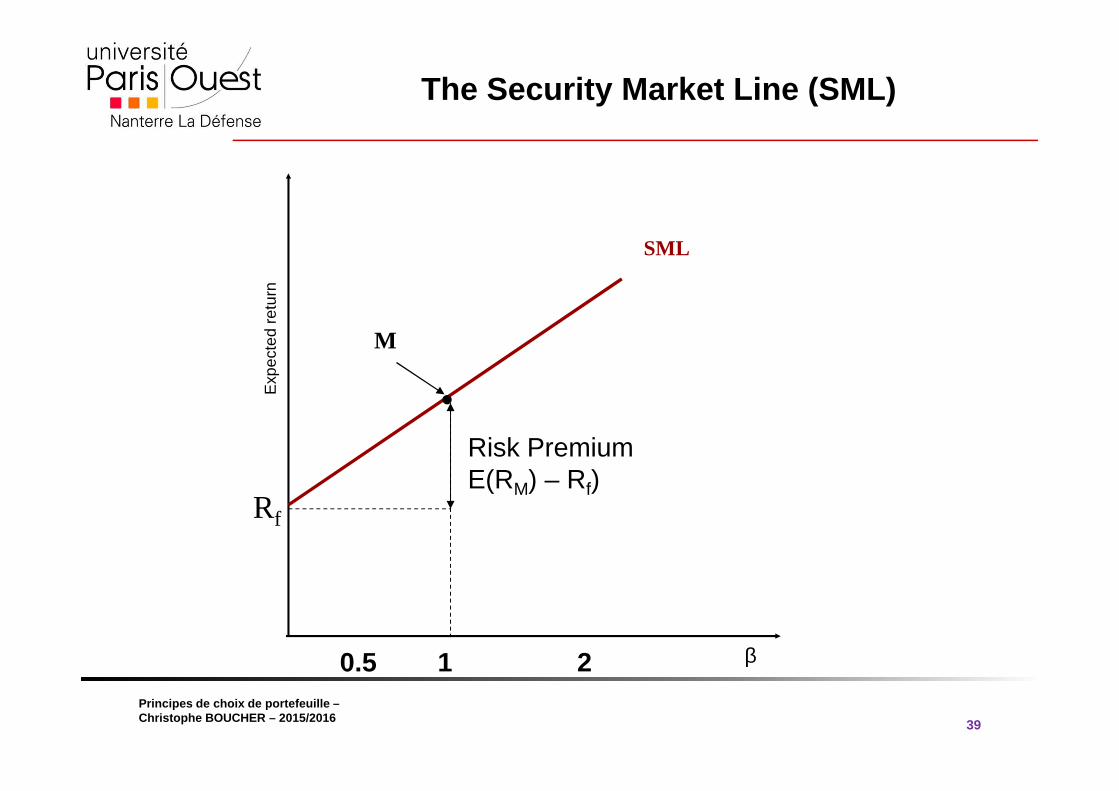

The Security Market Line (SML)

39

Exp

ecte

d re

turn

SML

Rf

M

β10.5 2

Risk PremiumE(RM) – Rf)

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

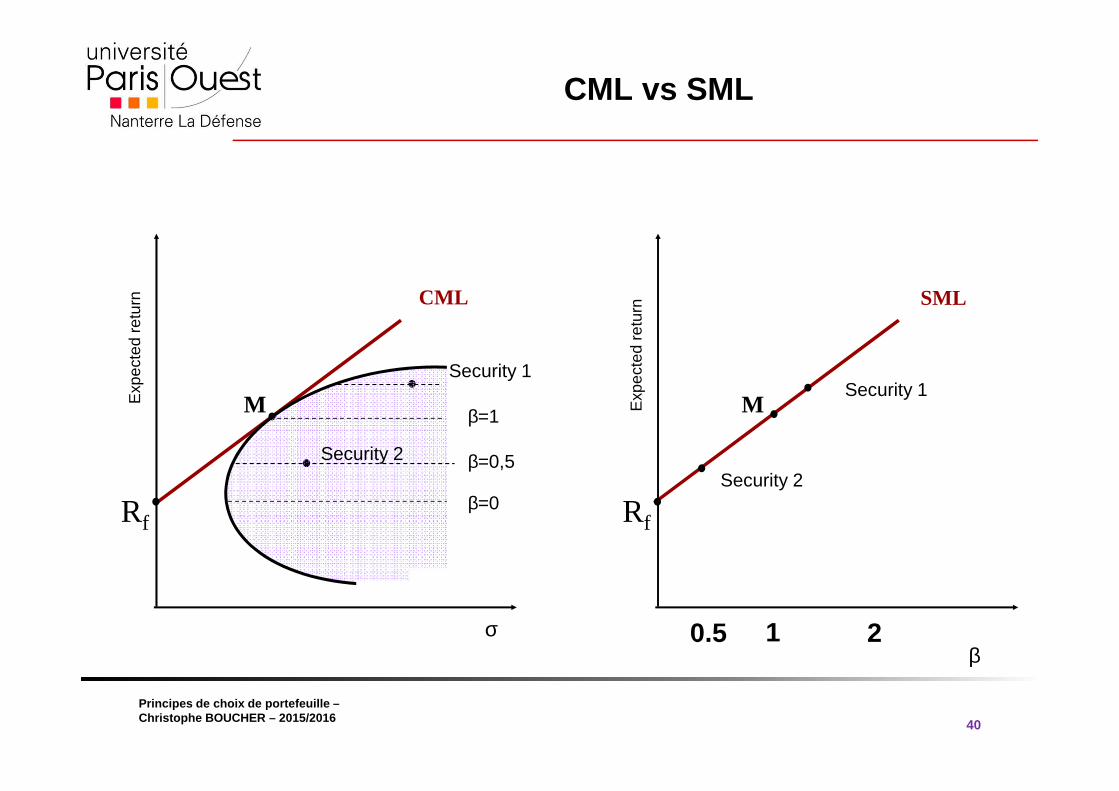

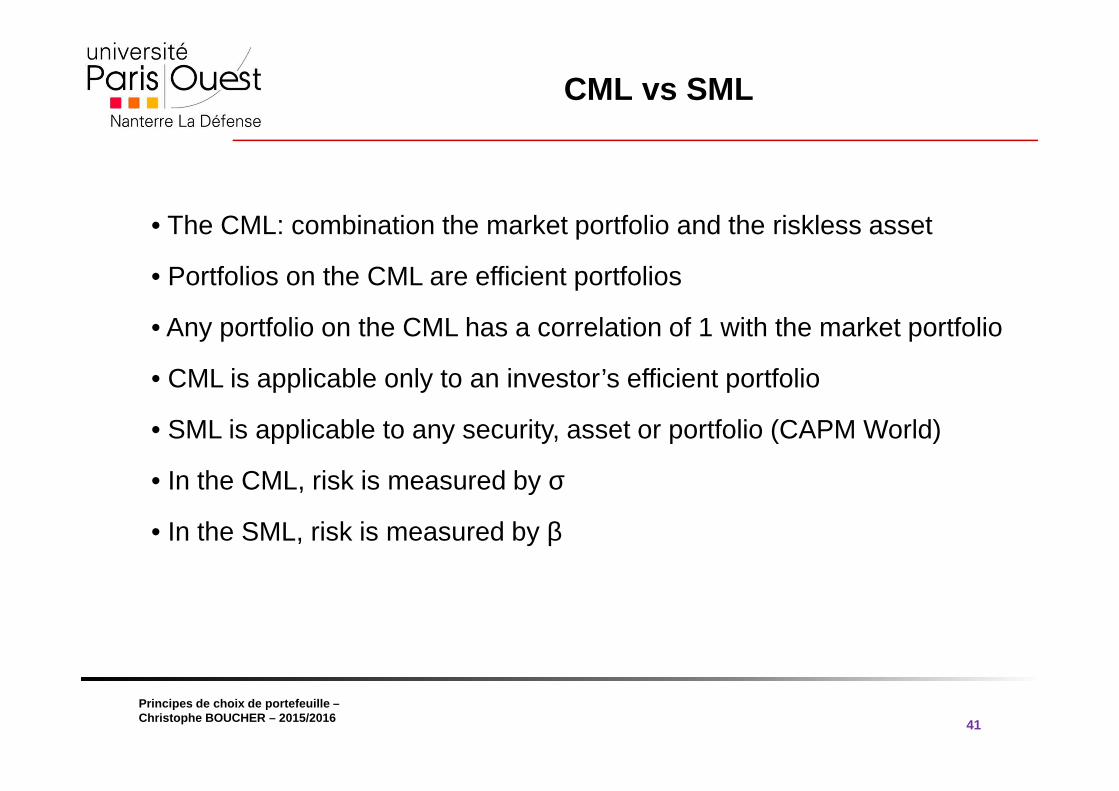

CML vs SML

40

βE

xpec

ted

retu

rn SML

Rf

M

10.5 2

Security 1

Security 2

σ

Exp

ecte

d re

turn CML

Rf

M

Security 2

Security 1

β=0

β=0,5

β=1

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

CML vs SML

41

• The CML: combination the market portfolio and the riskless asset

• Portfolios on the CML are efficient portfolios

• Any portfolio on the CML has a correlation of 1 with the market portfolio

• CML is applicable only to an investor’s efficient portfolio

• SML is applicable to any security, asset or portfolio (CAPM World)

• In the CML, risk is measured by σ

• In the SML, risk is measured by β

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

4.4 Asset Allocation with N risky Assets

42

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

Efficient portfolios

43

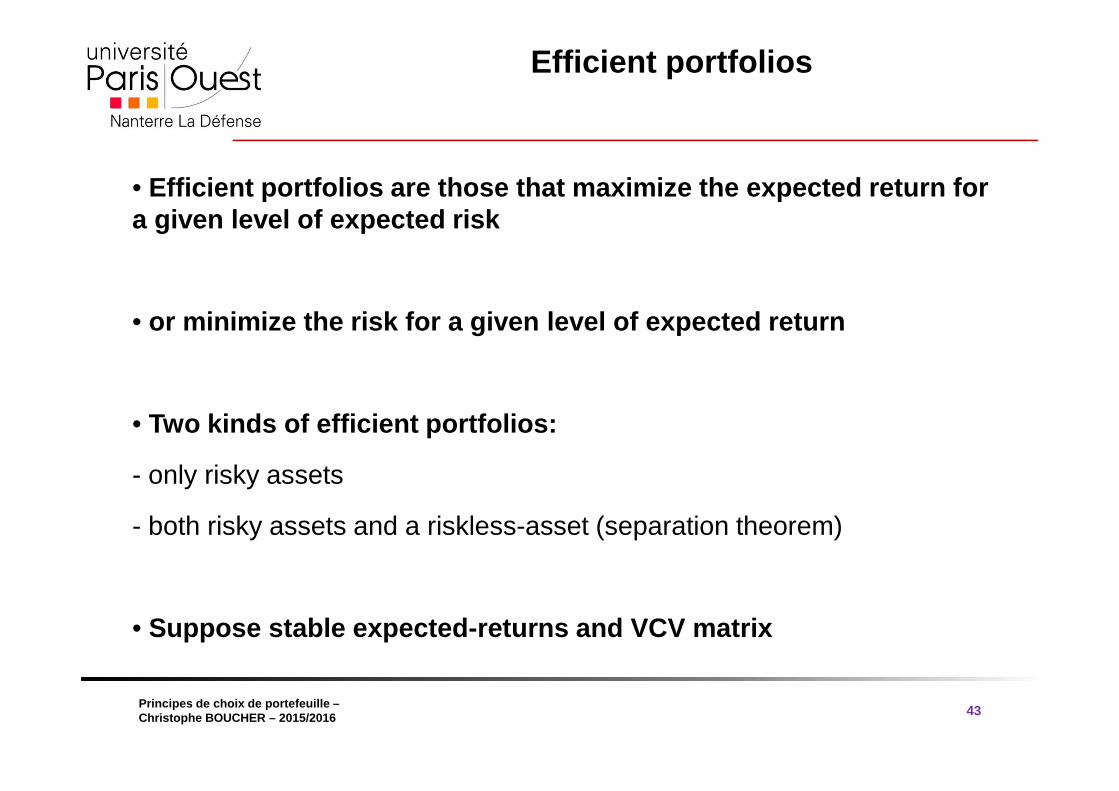

• Efficient portfolios are those that maximize the ex pected return for a given level of expected risk

• or minimize the risk for a given level of expected return

• Two kinds of efficient portfolios:

- only risky assets

- both risky assets and a riskless-asset (separation theorem)

• Suppose stable expected-returns and VCV matrix

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

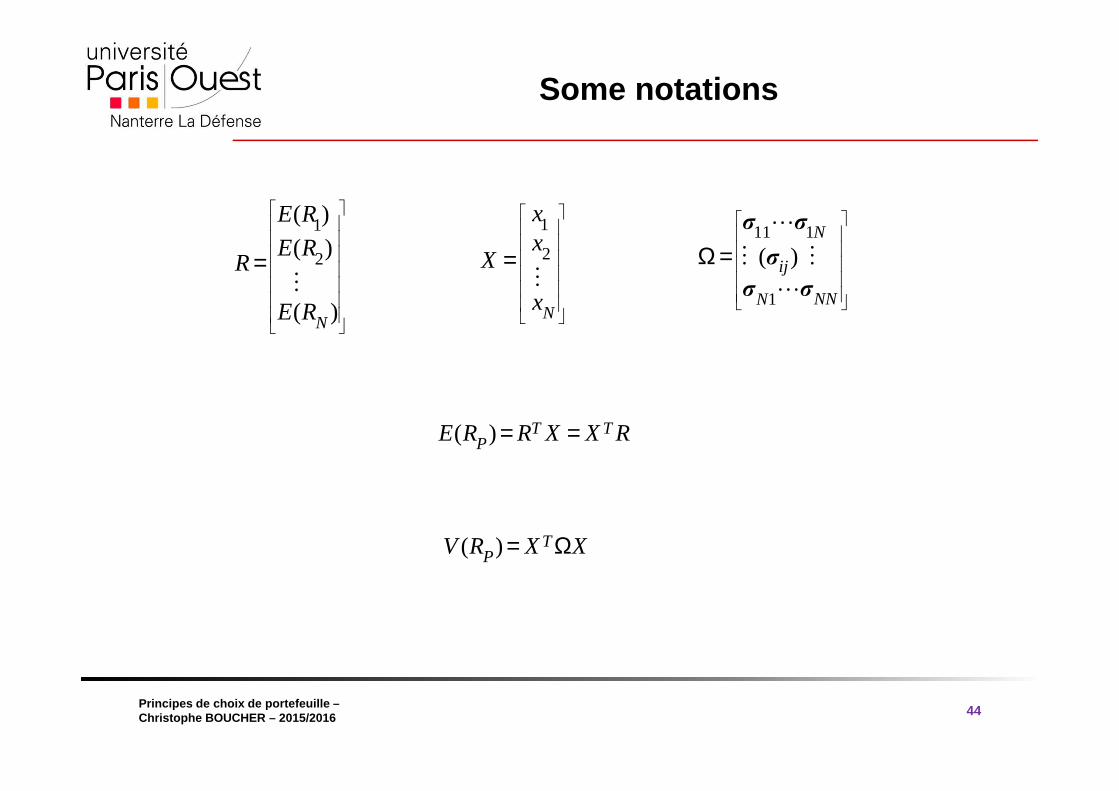

Some notations

44

1

2

( )

( )

( )N

E R

E RR

E R

=⋮

1

2

N

xx

X

x

=⋮

11 1

1

( )N

ij

NNN

Ω =⋯

⋮ ⋮

⋯

σ σ

σ

σ σ

( ) T TPE R R X X R= =

( ) TPV R X X= Ω

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

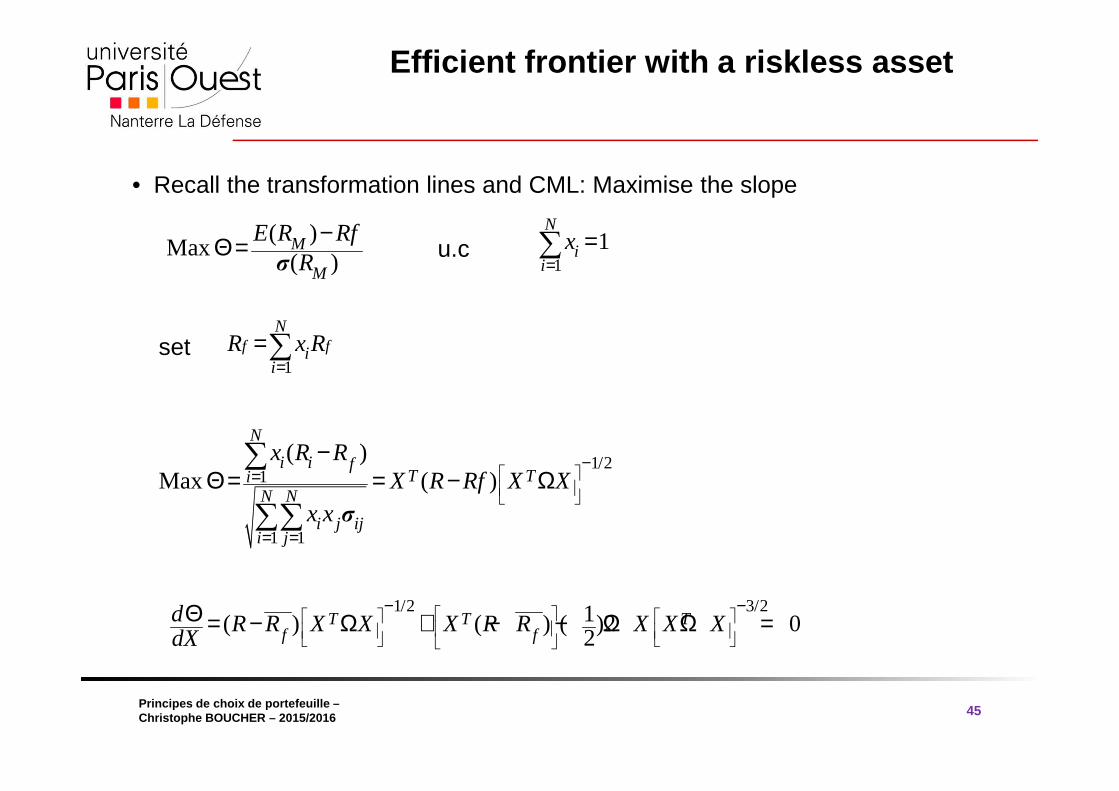

Efficient frontier with a riskless asset

45

( )Max

( )M

M

E R RfR

−Θ =σ

• Recall the transformation lines and CML: Maximise the slope

11

N

ii

x=

=∑u.c

1f f

N

ii

R x R=

=∑set

1/21

1 1

( )Max ( )

N

i i fT Ti

N N

i j iji j

x R RX R Rf X X

x x

−=

= =

−Θ = = − Ω

∑

∑∑ σ

1/2 3/21( ) ( ) ( )2 02

T T Tf f

d R R X X X R R X X XdX

− −Θ = − Ω + − − Ω Ω =

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

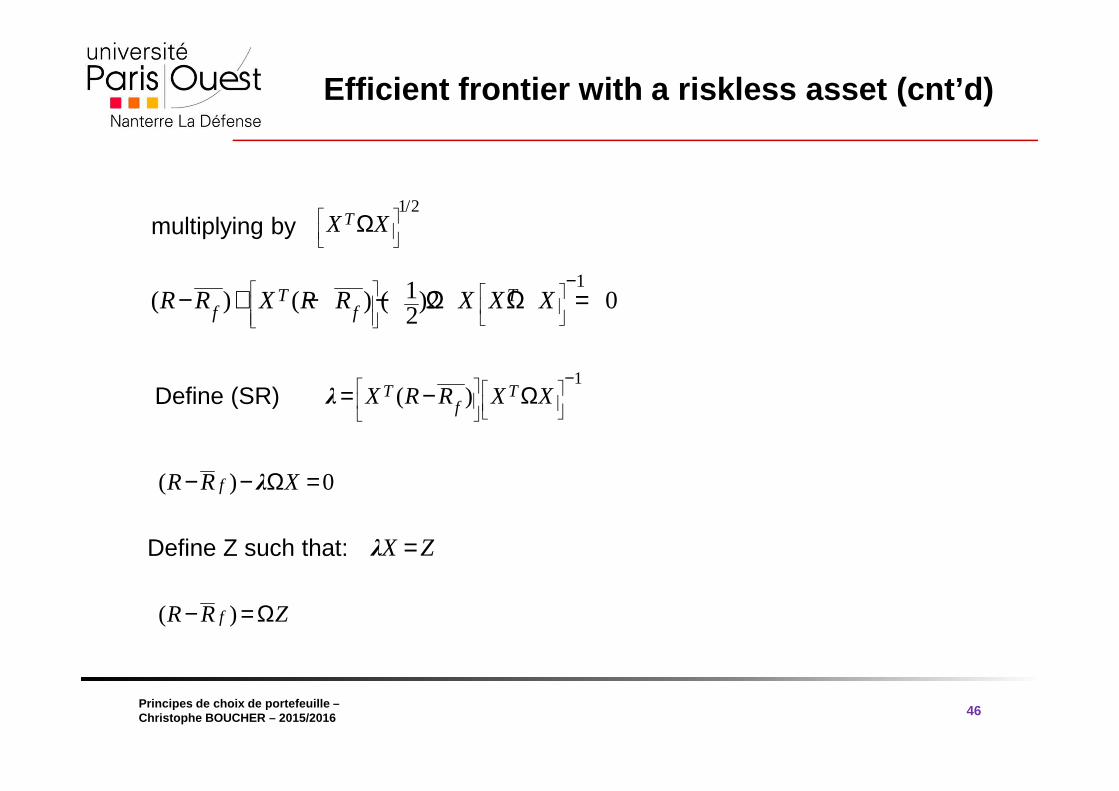

Efficient frontier with a riskless asset (cnt’d)

46

multiplying by1/2

TX X

Ω

11( ) ( ) ( )2 02

T Tf fR R X R R X X X

−− + − − Ω Ω =

1( )T T

fX R R X X

−= − ΩλDefine (SR)

( ) 0fR R X− − Ω =λ

X Z=λ

( )fR R Z− = Ω

Define Z such that:

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

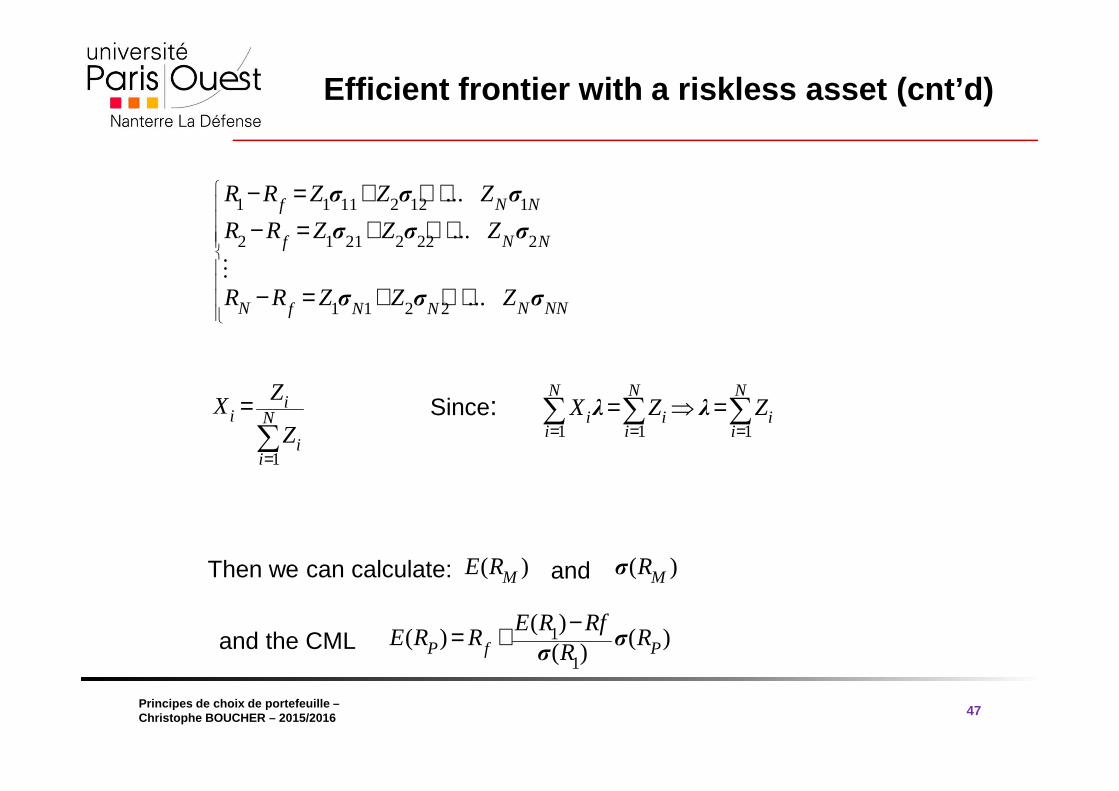

Efficient frontier with a riskless asset (cnt’d)

47

1 1 11 2 12 1

2 1 21 2 22 2

1 1 2 2

...

...

...

N Nf

N Nf

N N NNN Nf

R R Z Z Z

R R Z Z Z

R R Z Z Z

− = + + +− = + + +

− = + + +⋮

σ σ σ

σ σ σ

σ σ σ

1

ii N

ii

ZX

Z=

=∑

Since: 1 1 1

N N N

i i ii i i

X Z Z= = =

= ⇒ =∑ ∑ ∑λ λ

Then we can calculate: ( )ME R ( )MRσand

1

1

( )( ) ( )

( )P Pf

E R RfE R R R

R−= + σ

σand the CML

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

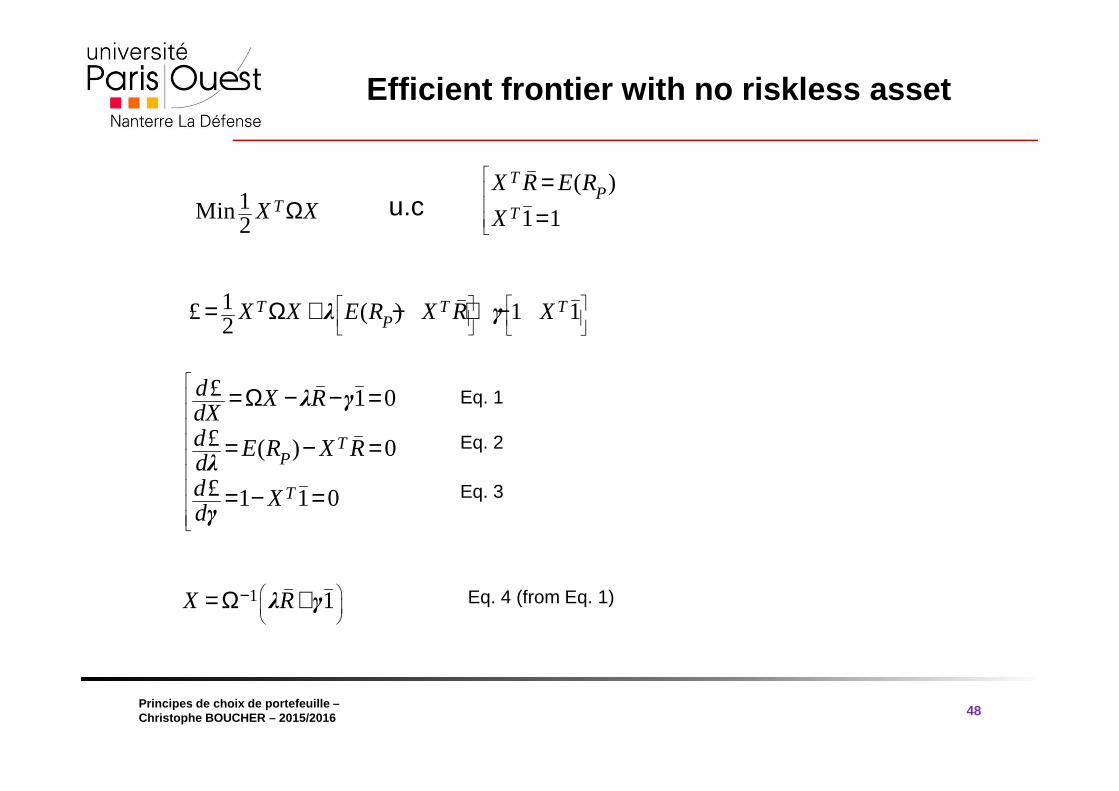

Efficient frontier with no riskless asset

48

1Min2

TX XΩ( )

1 1

TP

T

X R E R

X

==u.c

1£ ( ) 1 12

T T TPX X E R X R X

= Ω + − + −λ γ

£ 1 0

£ ( ) 0

£ 1 1 0

TP

T

d X RdXd E R X Rdd Xd

=Ω − − =

= − =

= − =

λ γ

λ

γ

1 1X R

−= Ω +λ γ

Eq. 1

Eq. 2

Eq. 3

Eq. 4 (from Eq. 1)

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

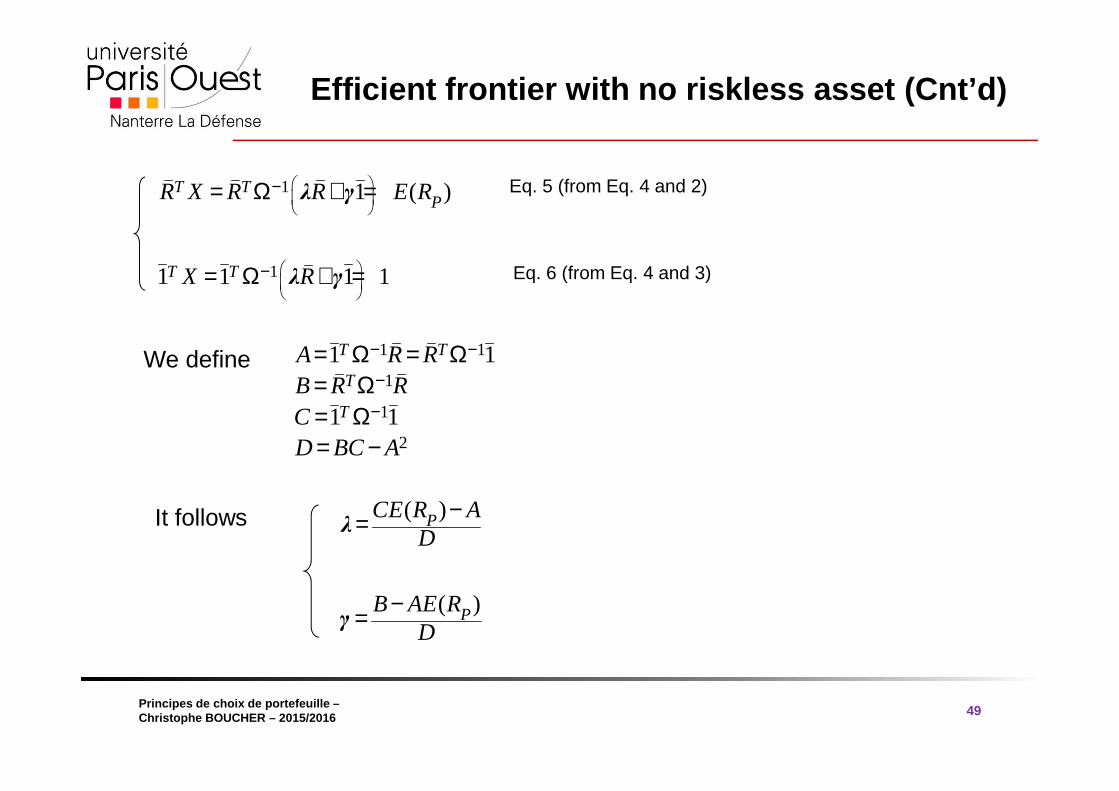

Efficient frontier with no riskless asset (Cnt’d)

49

1 1 ( )T TPR X R R E R

−= Ω + =λ γ

11 1 1 1T TX R

−= Ω + =λ γ

1 1

1

1

2

1 1

1 1

T T

T

T

A R RB R RCD BC A

− −

−

−

= Ω = Ω= Ω= Ω= −

We define

( )PCE R AD

−=λ

( )PB AE RD

−=γ

Eq. 5 (from Eq. 4 and 2)

Eq. 6 (from Eq. 4 and 3)

It follows

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

Efficient frontier with no riskless asset (Cnt’d)

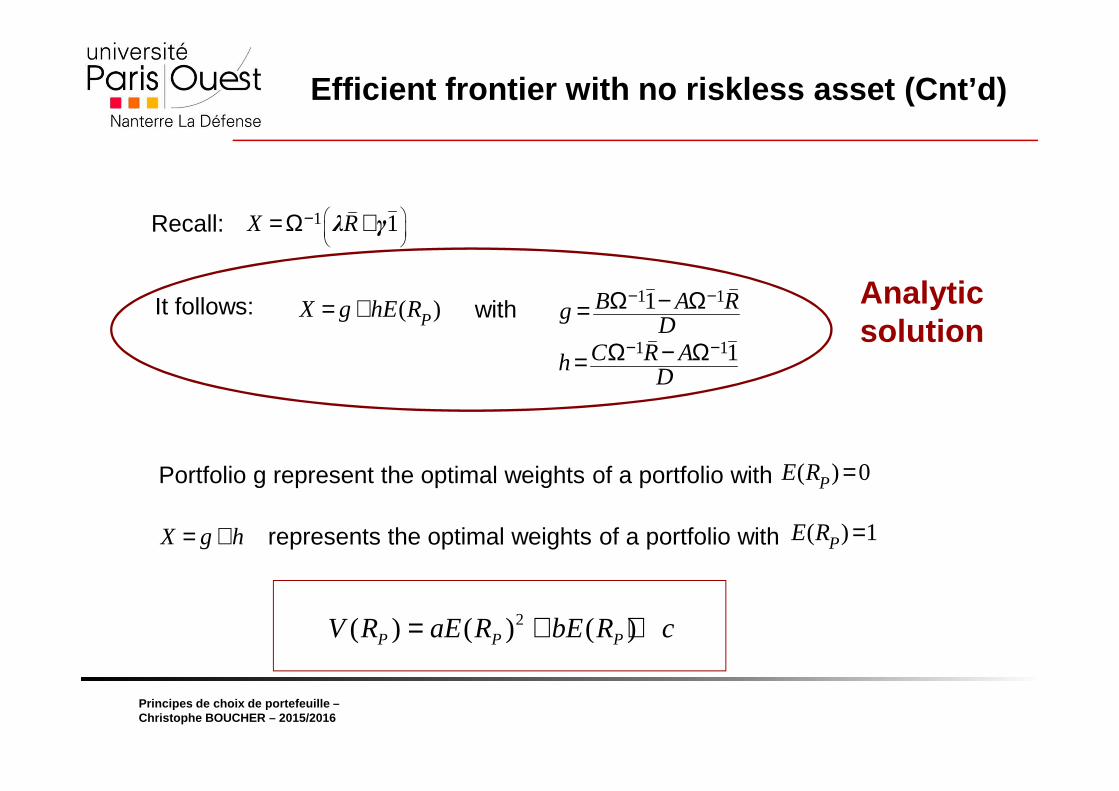

Recall: 1 1X R

−= Ω +λ γ

( )PX g hE R= + 1 1

1 1

1

1

B A RgD

C R AhD

− −

− −

Ω − Ω=

Ω − Ω=

with

Portfolio g represent the optimal weights of a portfolio with ( ) 0PE R =

X g h= + represents the optimal weights of a portfolio with ( ) 1PE R =

2( ) ( ) ( )P P PV R aE R bE R c= + +

It follows: Analytic solution

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

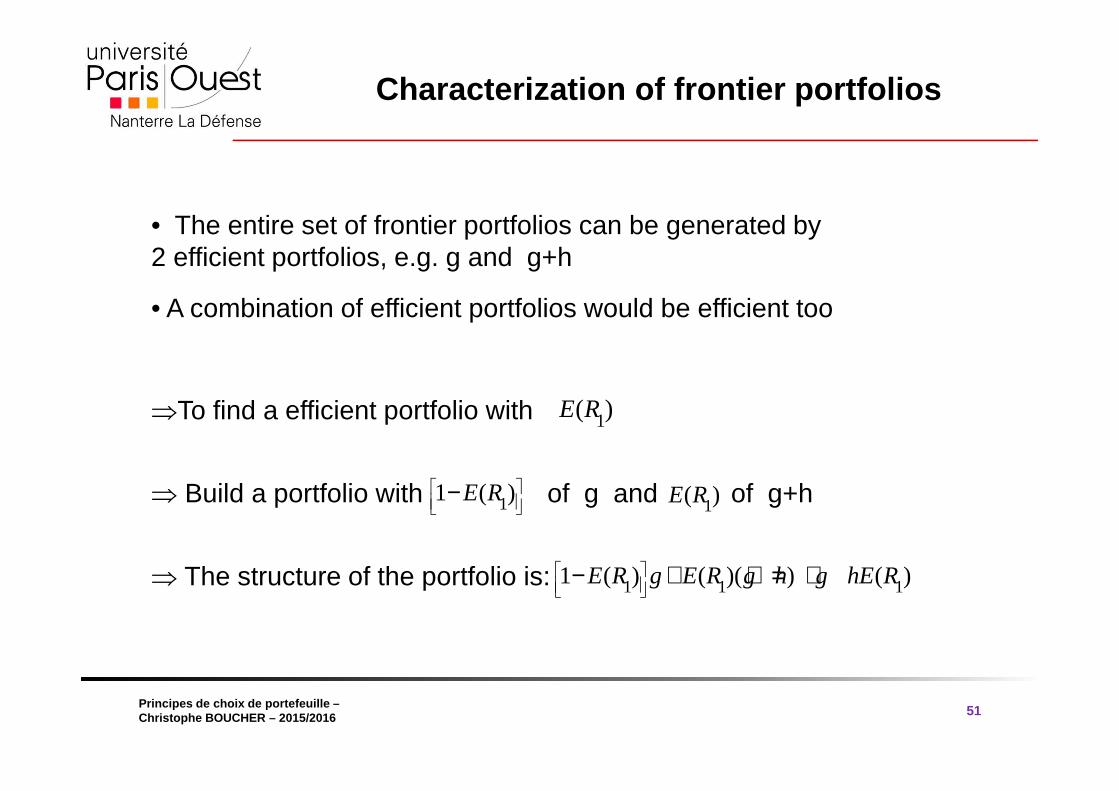

Characterization of frontier portfolios

51

• The entire set of frontier portfolios can be generated by 2 efficient portfolios, e.g. g and g+h

• A combination of efficient portfolios would be efficient too

⇒To find a efficient portfolio with

⇒ Build a portfolio with of g and of g+h

⇒ The structure of the portfolio is:

1( )E R

11 ( )E R

−1( )E R

1 1 11 ( ) ( )( ) ( )E R g E R g h g hE R

− + + = +

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

3.5 Portfolio Diversification

52

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

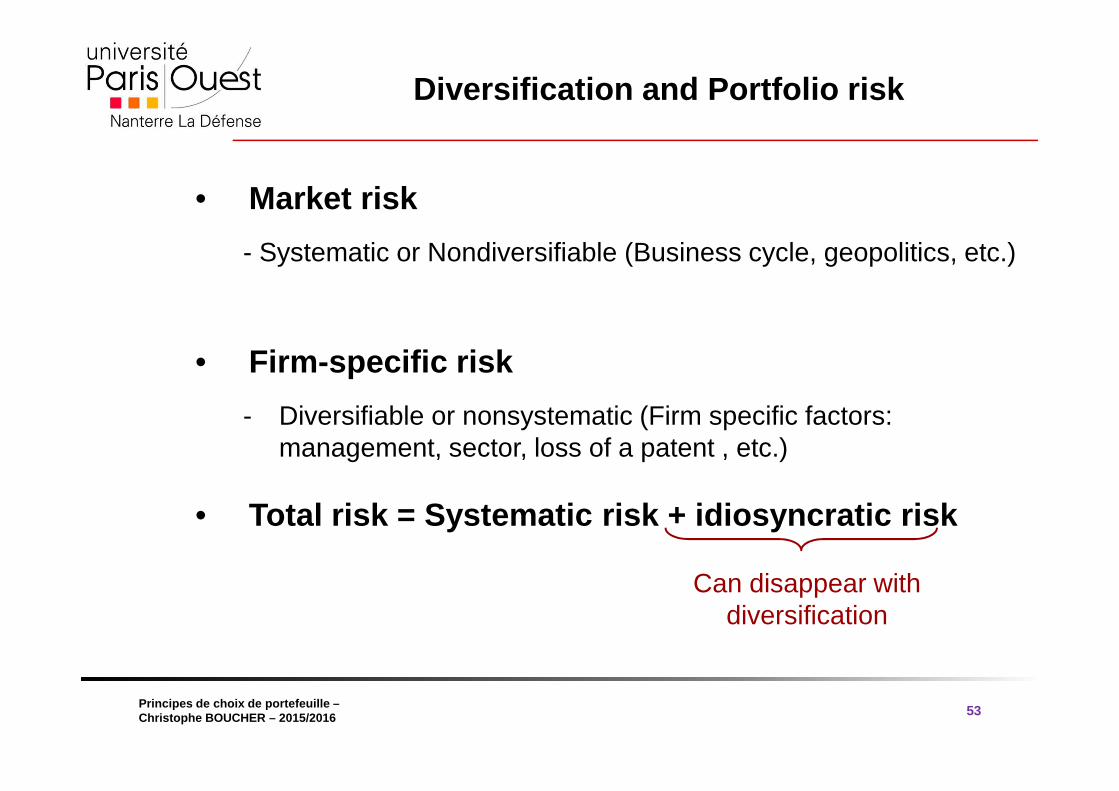

Diversification and Portfolio risk

53

• Market risk

- Systematic or Nondiversifiable (Business cycle, geopolitics, etc.)

• Firm -specific risk

- Diversifiable or nonsystematic (Firm specific factors: management, sector, loss of a patent , etc.)

• Total risk = Systematic risk + idiosyncratic risk

Can disappear with diversification

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

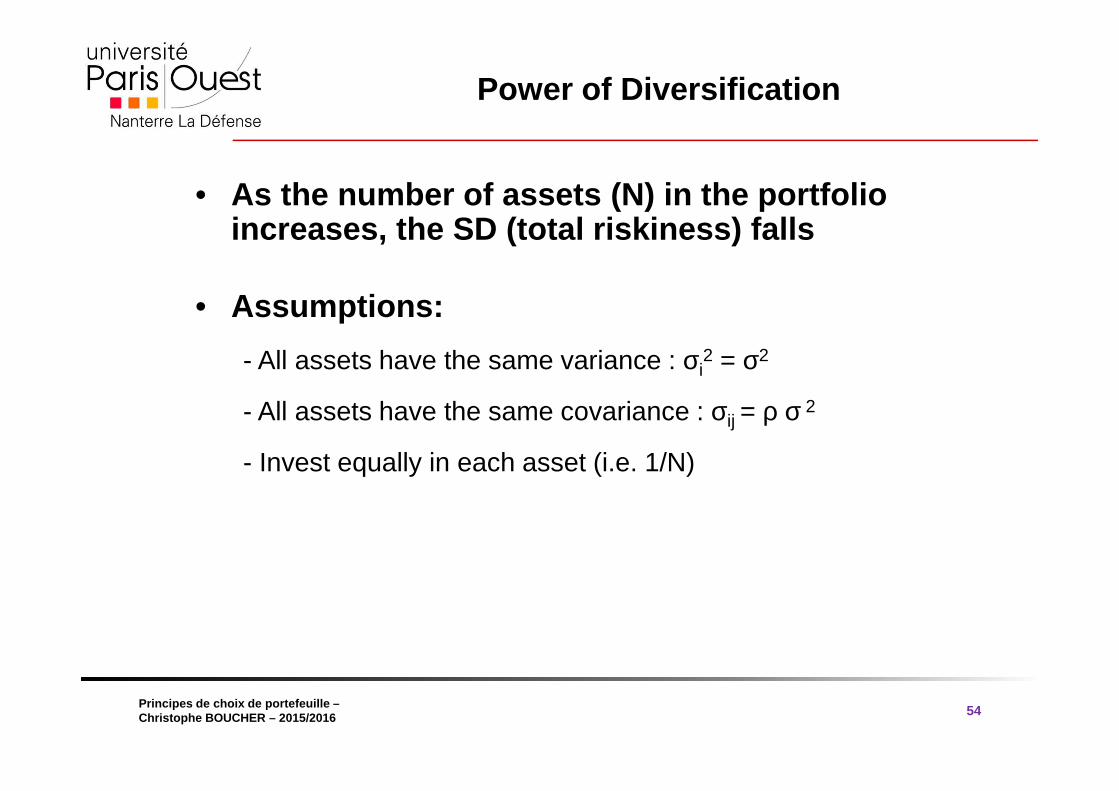

Power of Diversification

54

• As the number of assets (N) in the portfolio increases, the SD (total riskiness) falls

• Assumptions:

- All assets have the same variance : σi2 = σ2

- All assets have the same covariance : σij = ρ σ 2

- Invest equally in each asset (i.e. 1/N)

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016

Power of Diversification

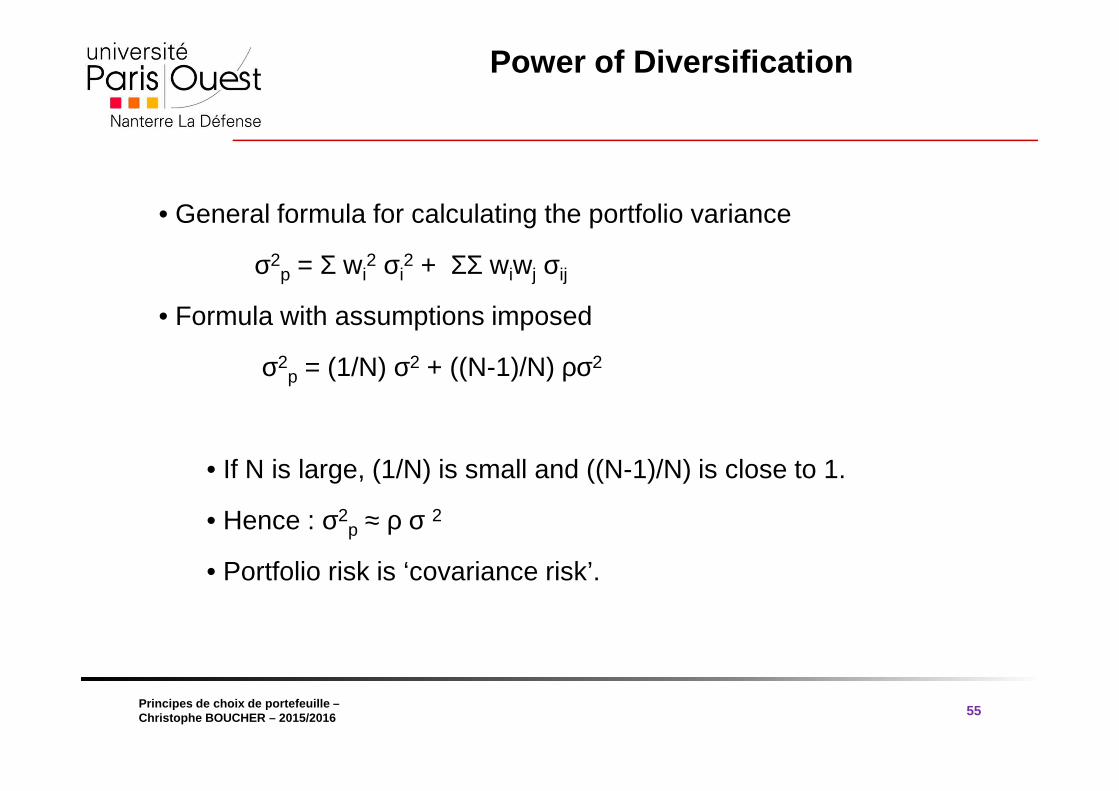

55

• General formula for calculating the portfolio variance

σ2p = Σ wi

2 σi2 + ΣΣ wiwj σij

• Formula with assumptions imposed

σ2p = (1/N) σ2 + ((N-1)/N) ρσ2

• If N is large, (1/N) is small and ((N-1)/N) is close to 1.

• Hence : σ2p ≈ ρ σ 2

• Portfolio risk is ‘covariance risk’.

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016 56

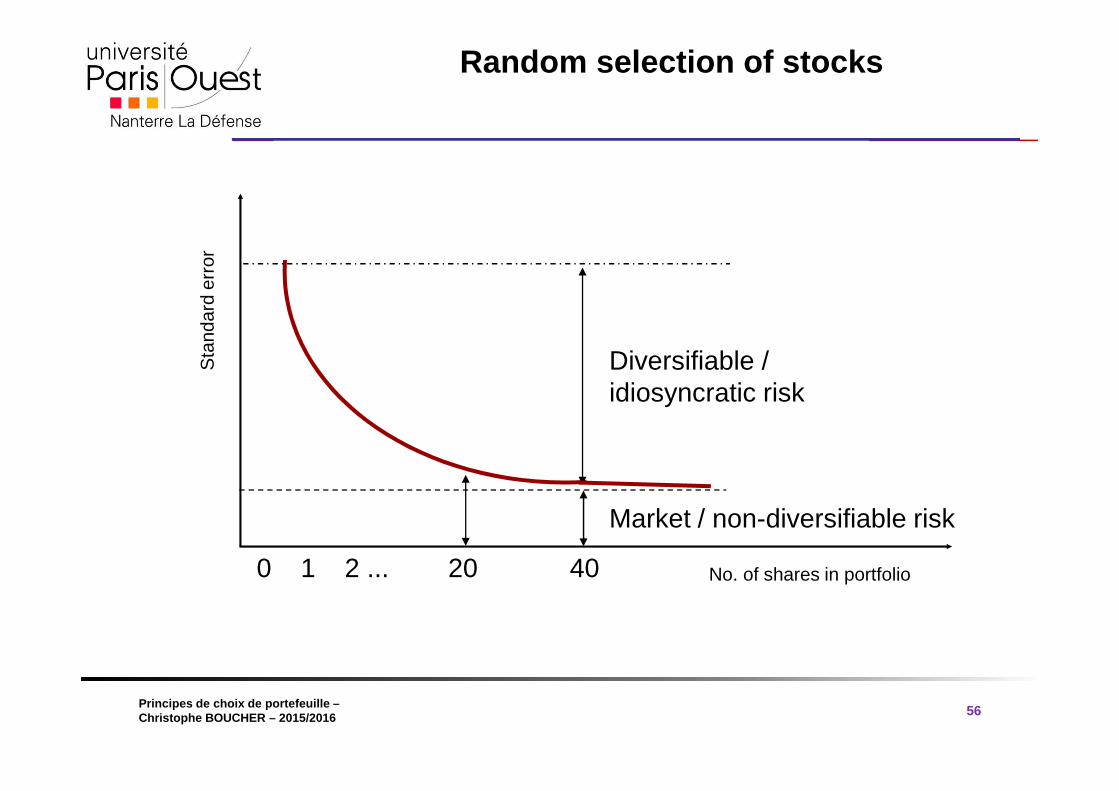

Sta

ndar

d er

ror

No. of shares in portfolio

Diversifiable / idiosyncratic risk

Market / non-diversifiable risk

20 400 1 2 ...

Random selection of stocks

® 2009 Pearson Education France

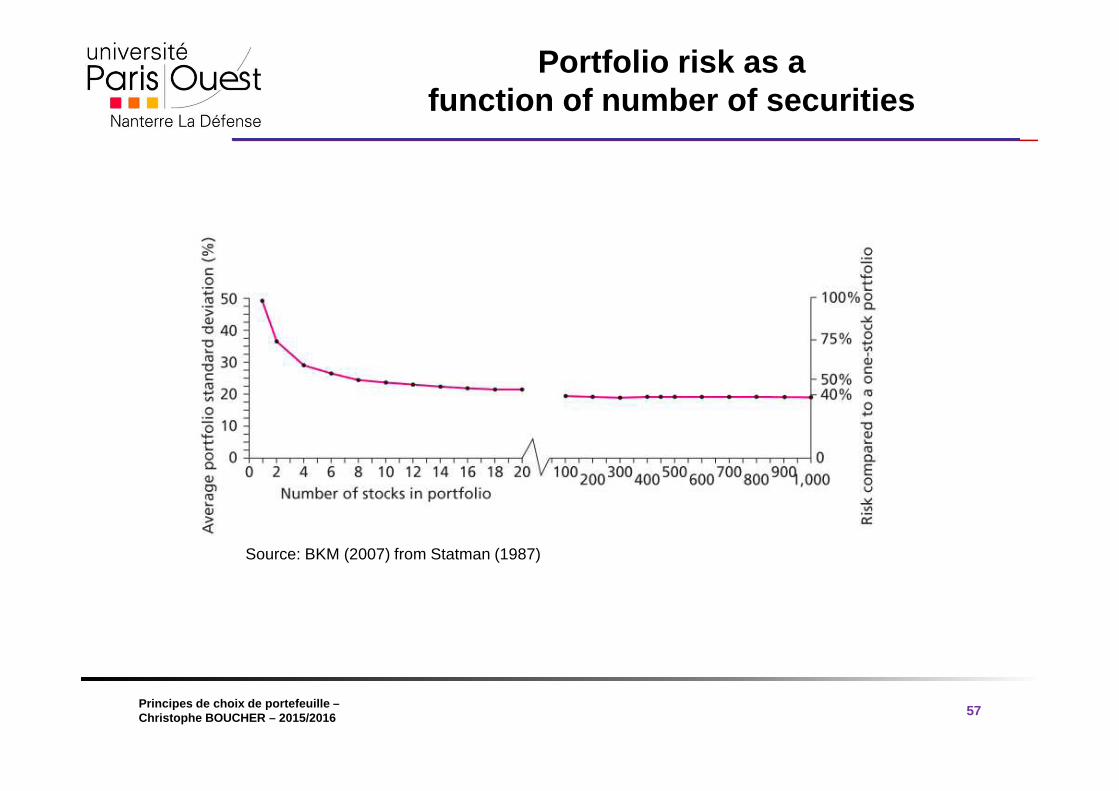

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016 57

Portfolio risk as a function of number of securities

Source: BKM (2007) from Statman (1987)

® 2009 Pearson Education France

transparents traduits par Vincent Dropsy Principes de choix de portefeuille –Christophe BOUCHER – 2015/2016 58

Thank you for your attention…

See you next week