Embed Size (px)

Citation preview

Prestanda och karaktäristik för Grupp I-

basoljor

Henrik Marits,

Nynas AB, Naphthenics

Underhållsdagen 24 november 2015

Outline

A brief overview of base oils API Groups I to V

and their applications

A closer look at Group I base oil availability

and base oil markets drives

Some suggestions on how to secure supply of

base oils with Group I properties, now and

in the future

API classification of base oils

VI = 80-119

Sats<90% and/or S>0.03%

VI = 80-119

Sats>90% and S<0.03%

VI > 120

Sats>90% and S<0.03%

Group I

Group II

Group III

PAO Group IV

All other oils Group V

Paraffinic

Oils

Wide chemical spectrum

Narrower chemical spectrum

Specific molecule type

Group I base oils

Main base oil for 100+ years

Very suitable for

Industrial Lubricants

Hydraulic fluids

Industrial gear oils

Some metalworking applications

Straight grade heavy engine oils

Marine engine oils (high viscosity)

Greases

Process oils

Remember: “Thus, if it’s big, moves slowly under heavy load, that oil had

better be thick”

Group I – Key properties

SN 100 SN 150 SN 600 Bright Stock

Viscosity at 40°C, cSt 19-21 29-32 109-116 500

VI 95 95 95 95

Pour Point, °C -18 -15 -6 -6

Saturates, % 75-85 75-85 70-80 60-70

Noack Volatility, wt % 26-30 16-20 3 NA

Group II base oils

Group II is the new Orange

Production has exploded in the last 20 years

New main automotive engine base oil

Very dominant in North America for cars (PCMO) and trucks (HDDO)

Growing importance in Europe for trucks (HDDO)

Group II – Key properties

100 SUS 220 SUS 600 SUS

Viscosity at 40°C, cSt 19-21 42-46 109-116

VI 95-100 95-100 95-100

Pour Point, °C -18 -15 -12

Saturates, % >98 >98 >98

Noack Volatility, wt % 26-30 11-15 2-3

Group III base oils

Used for “Synthetic” engine oils, gear, transmission and hydraulic for almost

20 years

Made from slack wax, or from GTL wax, via hydro isomerization

Unlike cracking processes, that changes the properties of the fluid without

losing viscosity (cracking makes small molecules out of large ones)

Group III – Key properties

100 SUS 250 SUS

Viscosity at 40°C, cSt 19-21 47-51

VI 122-128 127-135

Pour Point, °C -15 -15

Saturates, % >98 >98

Noack Volatility, wt % 13-15 3-4

Group IV base oils- PAO

The poly-α-Olefin is a true synthetic fluid

Made from the oligomerization of 1-Decene

High VI

Low volatility

Good low temp properties

High cost

Nynas was founded in 1928

Nynas is the largest specialty oil producer in Europe

Offices in more than 30 countries around the globe

Net Sales: 3 Billion USD

Average number of employees: 1000

Refineries in Nynäshamn (SE), Gothenburg (SE), Harburg (DE),

Eastham JV (UK), Antwerp JV (BE), Isla JV (Curacao)

Base Oils

Nynas: The Different Oil Company

12% Fuel

18% Specialty oils

70% Bitumen

96% Fuel

4% Bitumen,

Specialty oils

and Lubes

Typical

oil company

Global Oil Consumption

Other Lubricants, 97%

(39 Mio tons / y)

Lubricants, 1% including

motor oils, base oils,

process oils, tyre oils

Tyre oils, 3%

(1.3 Mio tons / y)

Only 0.03% of

total global oil

demand

3.9 Billion tons / y

Source: Kline 2015

IEO-Ind. Engine Oils

GIO- General Ind. Oil

HF- Hydraulic fluids

PO- Process Oils

What is happening in the base oil market?

The base oil market is rapidly changing!

The needs of the automotive industry, driven by fuel economy legislation, is

driving the major shift away from traditional Group I base oils towards Gr. II

and Gr III

The needs of the industrial lubricant market is inconsequential to this

development

Collateral damage is caused to industrial lubricants blenders (and users), if

they cannot resolve their supply issue

Currently,

70% of Group I go into industrial lubricants

30% into automotive engine oils and

transmission fluids

Global Usage of Group I

Oils 2013 (total market

approx. 17 million tons)

Source: Kline Consulting

World Naphthenic market share:

A significant part of the global oil market The Global lubricant demand is 40 M Ton/y

Ca. 1% of the total petroleum market

Automotive Lubricants 56%

Industrial Lubricants 44 %

Global naphthenic potential:

About 10% of total base oil demand (3.6 M Ton) (Source Fuchs Petrolub AG presentation at 18th ICIS-LOR World Base Oils conference Feb 2014 in London)

Naphthenic Usage, %

Main applications of naphthenic oils (I)

Lubricant Industry (30%)

Lubricating greases

Metal Working Fluids (MWF)

As a component in other industrial

lubricants (hydraulic fluids, gear oils, etc.)

Electrical Industry (ELI) (30%)

Insulating oils for industrial transformers

Finished products for direct end use

Main applications of naphthenic oils (II)

Process oils (40%)

Adhesives and sealants

Printing inks

Battery separators

Insoluble sulfur (as oil dispersion)

Antifoams

Tyre Industry

Used as extender oil in tyre rubber

Oil extended polymers

Evolution of the global base oil pool

51%

28%

11%

1% 9%

2012

Group I

Group II

Group III

PAO

Naphthenic

44%

34%

11%

1% 10%

2014

Group I

Group II

Group III

PAO

Naphthenic

26%

48%

13%

1% 12%

2019 f’cast

Group I

Group II

Group III

PAO

Naphthenic

Source. SBA Consulting

The global base oil demand scenario is here assumed to remain around 36

M mt/pa for the period

What is driving the change?

Several supply related factors – external to the lubricant industry – have a

negative impact on Group I plants:

Mandatory clean low sulphur fuel investments

Clean base oil (low Sulfur, low polyaromatics)

Crude oil cost and availability

Refining economics

Of scale and of method/technology

“Technological paradox” Gr I more expensive to make

Thus, the Group II and III market is growing at the expenses of Group I oils,

which are required for industrial use

70% of all Group I is currently utilized for Industrial lubricants

30% remains in use in Automotive lubricants

The market will have to find a way to deal with an

unbalanced supply-demand situation

As base oils represent less than 1% of the

output of a fuel refinery, the fate of base oil

plants will mostly depend on operations

and viability of the “fuel mothership”

With a growing market and a good fit with

fuel strategies and crude flexibility, Group

II and III plants are generally in a better

position

With a shrinking market and production

cost disadvantages compared to Group II

and III, Group I plants have a more

challenging future

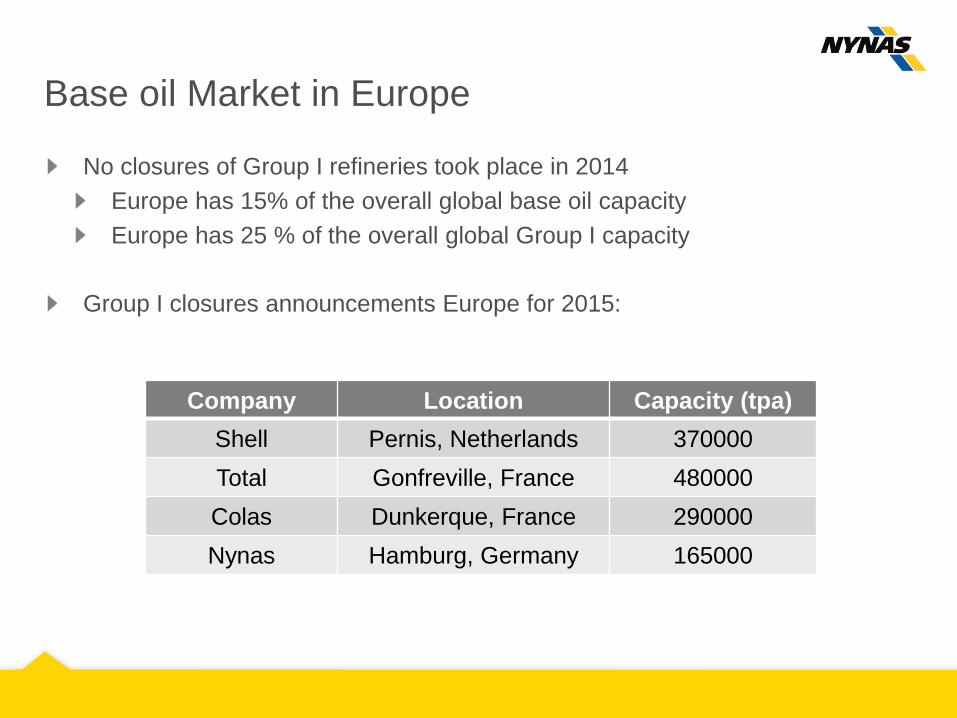

Base oil Market in Europe

No closures of Group I refineries took place in 2014

Europe has 15% of the overall global base oil capacity

Europe has 25 % of the overall global Group I capacity

Group I closures announcements Europe for 2015:

Company Location Capacity (tpa)

Shell Pernis, Netherlands 370000

Total Gonfreville, France 480000

Colas Dunkerque, France 290000

Nynas Hamburg, Germany 165000

The majority of Group I producers have an in-

house lubricant business to care for….

Lubricant producers, 89%

Non -lubricant producers, 11%

89% of the global base oil production thus originates from

producers that have an in-house lubricant business

The “collateral damage” of the paraffinic quality shift

Group II and III paraffinic oils are excellent base

stocks for the formulation of modern engine oils

However, Group II and III paraffinic oils display

lower solvency compared to Group I paraffinic

oils

Moreover, there is a limitation in the maximum

viscosity that can be reached in Group II and III

plants

Therefore, the shift from Group I to Group II and

III paraffinic oils will pose challenges to industrial

lubricant formulators, as it will lead to a loss of

solvency and viscosity range availability

The widening Solvency Gap

Solvency is an important property in most industrial

lubricant applications

In general, the base oil solvency affects the oil’s

capability of dissolving additives, oxidation products

and prevent varnish and deposit formation

In lubricating greases, the base oil solvency affects

the soap yield and the oil-soap interaction

In Metalworking fluid emulsions, the base oil

solvency affects the emulsion stability

The growing high viscosity deficiency

API group Light neutral Medium neutral Heavy neutral Brightstock

Group I 38% 13% 33% 16%

Group II 55% 25% 20% none

Group III 80% 20% none none

The ongoing shift in capacity will generate availability issues for heavy Solvent Neutrals and for Brightstock

This is already evident from the price development of Brightstock and SN 500/600 and Group II 500 SUS in markets across the regions

How is the market going to move away from Group I?

Conversion to Group II or Group III?

Conversion to Naphthenics ?

Conversion to Group II/III – Naphthenic blends?

Which are the most important base oil properties?

Viscosity (KV)

Viscosity Index (VI)

Solvency

Aniline Point (related to aromatic content)

CA Carbon Type (ASTM D 2140)

CA Carbon Type by FTIR

And, of course, availability – it must be available in the market

Solvent power / Solubility

Solvent power = The ability to solvate other molecules

Solubility = The ability of being dissolved by other molecules

From the user’s perspective, it affects:

Compatibility with polymers & resins

Pigment & filler wetting

Additive loading

Emulsion stability

Solution of impurities

Solution of oxidation products

Solvent molecule

Solute molecule

The oil solvent power in the Technical Data Sheet

Properties & Measurements:

Aniline point

Aromatic content (CA)

Naphthenic content (CN)

Viscosity

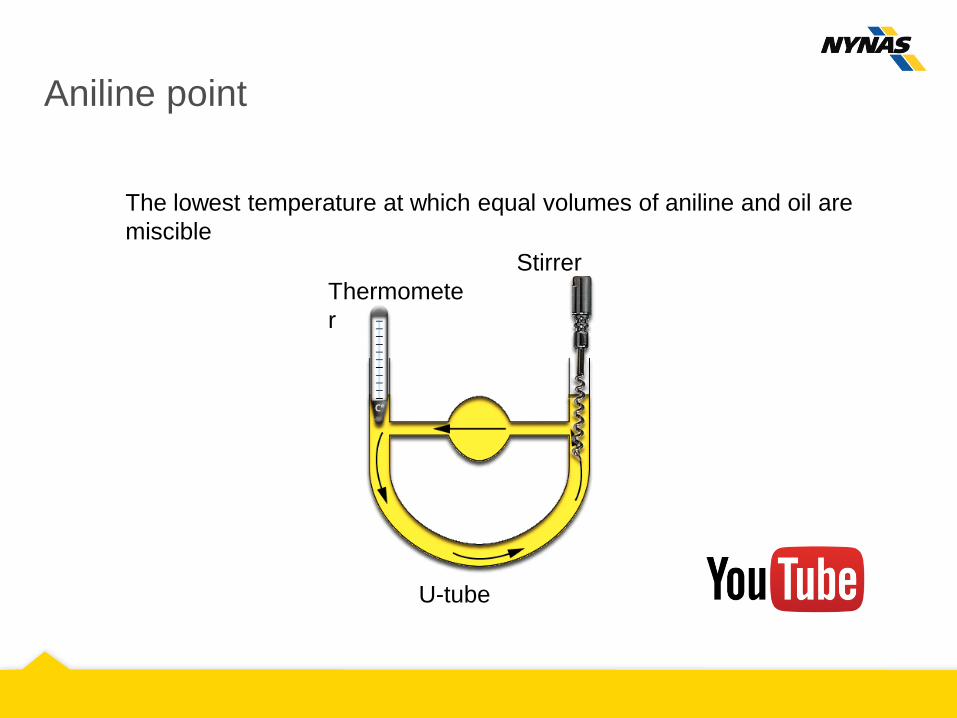

Aniline point

Thermomete

r

Stirrer

U-tube

The lowest temperature at which equal volumes of aniline and oil are

miscible

Aniline point

— 90ºC

— 80ºC

— 70ºC

— 60ºC

— 50ºC

— 40ºC

— 30ºC

— 20ºC

— 10ºC

— 0ºC

68ºC —

— 90ºC

— 80ºC

— 70ºC

— 60ºC

— 50ºC

— 40ºC

— 30ºC

— 20ºC

— 10ºC

— 0ºC

68ºC —

— 90ºC

— 80ºC

— 70ºC

— 60ºC

— 50ºC

— 40ºC

— 30ºC

— 20ºC

— 10ºC

— 0ºC

68ºC —

— 90ºC

— 80ºC

— 70ºC

— 60ºC

— 50ºC

— 40ºC

— 30ºC

— 20ºC

— 10ºC

— 0ºC

68ºC —

Aniline point

Aniline is a polar solvent

The lower the “point” temperature:

The more ”polar” the oil

The higher the solvent power

Substantial overlap between

Group I and Naphthenics

— 140ºC

— 130ºC

— 120ºC

— 110ºC

— 100ºC

— 90ºC

— 80ºC

— 70ºC

— 60ºC

— 50ºC

— 40ºC

— 30ºC

— 20ºC

Aromatic oils

Naphthenic oils

Paraffinic oils

Increasing

solvent power

CA (ASTM D 2140 method)

X

X

Increasing

solvent power

CA = 12 %

Aromatic content (CA)

Solubility comparison

Solubility comparison

Solubility comparison

Solubility comparison

Effect of CN and viscosity on solvent power

A higher naphthenic content (CN) contributes to a higher solvent power

The lower the viscosity, the higher the solvent power

Nynas Oils and Group I Replacement – the

new speciality base oil range

A new specialty base oil product range

Can be widely applied in industrial lubricant formulations

Main advantages of the New Range (NR)

Most similar (and available) product to Group I oils

High degree of flexibility in blending Optional tailor-made blends readily available

Superior low temperature performance

Main challenges vs Group I base oils

Slightly higher volatility

Lower flash point

Slightly lower VI

Lower Sulphur content

Basic requirements of the New Range

The New Range range should:

Closely match the Kinematic Viscosity (@ 40 °C) and Aniline Point of a

representative reference base oil range of Solvent Neutral (SN) Group I

paraffinic base oils

Allow industrial lubricant manufacturers to maintain key properties of their

products

Allow direct replacement, with as little re-formulation and re-working of

labels, PDS and other marketing material as possible (drop-in replacement)

…Or allow for as easy reformulation work as possible

Viscosity Range Limitations Overcome

Viscosity at 40 °C (cSt)

API Group

Group III

Group II

Group I

50 100 200 300 400 500 600 700 2500

Gr. III

Group II

Group I Viscosity at 40 °C (SUS)

7 20 40 58 80 100 115 140 500

New fluid range

Heavy Naphthenics

Bright Stock

The New Range vs. SN reference base oils

The New Range (NR) vs. SN reference base oils

NR 70 SN 70 NR 100 SN 100 NR 150 SN 150 NR 300 SN 300 NR 500 SN 500 NR 600 SN 600

Density (kg/m3) 0,873 0,849 0,867 0,859 0,871 0,868 0,886 0,876 0,889 0,879 0,876 0,880

FP COC (°C) 168 190 196 206 222 224 220 258 242 262 268 278

PP (°C) -27 -12 -24 -18 -24 -18 -21 -18 -21 -9 -15 -9

Viscosity @40 °C (cSt) 14 12 22 17 30 30 60 58 100 94 120 115

Viscosity @100°C (cSt) 3,1 2,9 4,2 3,7 5,0 5,2 7,3 7,8 10,2 10,7 12,6 12,2

VI 67 92 88 104 89 103 80 98 79 97 98 96

Aniline Pt. (°C ) 90 90 100 98 101 102 103 109 111 115 123 117

Sulfur (m-%) 0,02 0,2 0,01 0,2 0,04 0,2 0,02 0,2 0,03 0,3 0,02 0,3

CA 3 7 2 3 3 3 4 3 3 2 2 3

CN 42 27 36 32 35 33 36 32 36 31 30 29

CP 55 66 62 65 62 64 60 65 61 67 69 68

Refractive index 1,477 1,468 1,475 1,472 1,479 1,477 1,485 1,481 1,487 1,483 1,481 1,483

The New Range ISO VG vs. SN reference base oils

NR

ISO VG 32 SN 150 NR

ISO VG 46 SN 300 NR

ISO VG 68 SN 500 NR ISO VG

100 SN 600

Density (kg/m3) 0,866 0,868 0,872 0,876 0,874 0,879 0,875 0,880

FP COC (°C) 212 224 224 258 232 262 247 278

PP (°C) -18 -18 -18 -18 -18 -9 -21 -9

Viscosity @40 °C (cSt) 32 30 46 58 68 94 100 115

Viscosity @100°C (cSt) 5,3 5,2 6,7 7,8 8,75 10,7 11,1 12,2

VI 96 103 97 98 100 97 95 96

Aniline Pt. (°C ) 105 102 110 109 115 115 121 117

Sulfur (m-%) 0,02 0,2 0,02 0,2 0,02 0,3 0,02 0,3

CA 1 3 3 3 2 2 1 3

CN 31 33 31 32 31 31 31 29

CP 68 64 66 65 67 67 68 68

Refractive index 1,476 1,477 1,478 1,481 1,479 1,483 1,480 1,483

Technical evaluation of the Group I

replacement base oils

Some important base oil properties investigated

Two of the important properties of the new base oils are

Low temperature behaviour

Investigated as Pour Point measurements

Compatibility of seals and O-ring material

Examined in an elastomer material compatibility study

Some preliminary conclusions

The low temperature behaviour of the new base oils was very favourable

Low Pour Points were reached at -50% lower treat rate of Pour Point

depressant (PPD) additive

Seal materials generally changed very little when tested in the new base oils,

and compared to Group I base oil and hydraulic fluids

Small changes of rubber hardness and swelling

Hydraulic Fluids based on the new base oils

Formulation of Model Hydraulic Fluids I

Hydraulic fluids are mainly composed of

Base oils (ca 98.5%)

An additive package (anti-oxidant, anti-wear, rust & corrosion

inhibition, anti-foam) ca 1.0 %

Viscosity Index Improvers (VII) (in HV only) and Pour Point

Depressants (PPD) ca 0.5%

Viscosities (KV@ 40 °C) range from 15 cSt to 100 cSt

The largest market volumes are in ISO VG 46 and ISO VG 32

Formulation of Model Hydraulic Fluids II

We have made a series of hydraulic fluids based on the new base oil

range

All important properties measured and compared to technical

standards and existing commercially available products

Blending with existing products

All key properties were comparable

The test fluid were compatible with the existing fluids

Our screening studies support our design idea for Group I replacement

base oils

Summary

A new Group I replacement base oil range has been created

This is targeted towards industrial and metalworking lubricants

The key design parameters were viscosity and solvency

Lab trials were conducted to elucidate

PPD expression

Elastomer (seal and O-ring) material compatibility

Several model hydraulic fluids were created, and:

Benchmarked vs leading commercially

available fluids

Evaluated vs technical standards

Evaluated vs elastomer compatibility

Our lab trials and evaluations strongly

support the utilization of Nybase in hydraulic fluids

Nynas Group Head Office

P.O. Box 10700

SE-121 29 Stockholm

Sweden

Tel. +46-8-602 12 00

Fax +46-8-91 34 27