Embed Size (px)

Citation preview

Presented by:

Douglas Coté, CFAChief Market StrategistING Investment Management U.S.

ING Global Perspectives

Markets. Insights. Opportunities.

3Q2012for the period ended 9/30/2012

DisclosureThis presentation has been prepared by ING Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security.

Past performance is no guarantee of future results.

All of the data contained herein is as of 9/30/2012

ING Global Perspectives

Markets. Insights. Opportunities.

The Folly of Gaming Diversification

Global Perspectives on the Markets

Tectonic Shifts Impacting Global Growth

ING Global Perspectives

Markets. Insights. Opportunities.

= Global Perspectives Monthly Book page number

The Folly of Gaming Diversification

ING Global Perspectives

Markets. Insights. Opportunities.

5

Implementing an Effective Diversified Strategy

Effective Diversification

Global broad asset class expands opportunity

Intelligent risk taking with a focus on compensated risks

Adding high return assets to increase return and potentially decrease risk

Folly of Gaming Diversification

Investors try to outsmart markets

Investors abandon diversified positions to sidestep impending risks or crowd into area of strong returns

Reactionary in nature and directionally wrong

Source: ING Investment Management

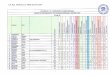

Capital Market ReturnsCapital market returns vary widely over time, making asset allocation decisions difficult and successful market timing virtually impossible.

6Note: For illustration only. Past performance is not a guarantee of future results. Investors cannot invest directly in an index. Source: FactSet, ING Investment Management.

Retirement

81

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

BC U.S. MSCI EM NAREIT/REIT MSCI EM NAREIT/REIT MSCI EM BC U.S. MSCI EM NAREIT/REIT BC U.S.

10.3% 55.8% 31.6% 34.0% 35.1% 39.4% 5.2% 78.5% 28.0% 7.8%

NAREIT/REIT R2000 MSCI EM MSCI EAFE MSCI EM MSCI EAFE T-Bill MidCap R2000 NAREIT/REIT

3.8% 47.3% 25.6% 14.0% 32.2% 11.6% 1.6% 40.5% 26.9% 4.7%

.T-Bill MidCap MSCI EAFE MidCap MSCI EAFE BC U.S. Balanced MSCI EAFE MidCap Balanced

1.7% 40.1% 20.7% 12.7% 26.9% 7.0% -22.1% 32.5% 25.5% 4.4%

MSCI EM MSCI EAFE MidCap NAREIT/REIT R2000 Balanced R2000 NAREIT/REIT MSCI EM SP500

-6.2% 39.2% 20.2% 12.2% 18.4% 6.2% -33.8% 28.0% 18.9% 2.1%

Balanced NAREIT/REIT R2000 SP500 SP500 MidCap SP500 R2000 SP500 T-Bill

-9.8% 37.1% 18.3% 4.9% 15.8% 5.6% -37.0% 27.2% 15.1% 0.0%

MSCI EAFE SP500 SP500 R2000 MidCap SP500 NAREIT/REIT SP500 Balanced MidCap

-15.7% 28.7% 10.9% 4.6% 15.3% 5.5% -37.7% 26.5% 12.1% -1.5%

MidCap Balanced Balanced Balanced Balanced T-Bill MidCap Balanced MSCI EAFE R2000

-16.2% 18.5% 8.3% 4.0% 11.1% 4.7% -41.5% 18.4% 8.2% -4.2%

.R2000 BC U.S. BC U.S. T-Bill T-Bill R2000 MSCI EAFE BC U.S. BC U.S. MSCI EAFE

-20.5% 4.1% 4.3% 3.0% 4.8% -1.6% -43.1% 5.9% 6.5% -11.7%

SP500 T-Bill T-Bill BC U.S. BC U.S. NAREIT/REIT MSCI EM T-Bill T-Bill MSCI EM

-22.1% 1.0% 1.2% 2.4% 4.3% -15.7% -53.3% 0.1% 0.1% -18.2%

NAREIT/REIT = NAREIT Equity REIT T-Bill = U.S. 30-day T-Bill BC Agg. = Barclays Capital U.S. Aggregate Bond Index

MSCI EM = MSCI Emerging Markets - Net R2000 = Russell 2000 Index Balanced = 60% S&P 500, 40% BC Aggregate

Midcap = Russell Midcap Index SP500 = S&P 500 MSCI EAFE = MSCI EAFE USD

Index Wgt Sep-12 QTR YTD 2011 2010 2009 2008 2007 1 year 3 years 5 years 10 years

Equity

S&P 500 10% 3.1 6.4 16.4 2.1 15.1 26.5 (37.0) 5.5 30.2 13.2 1.1 8.0

S&P Midcap 10% 2.5 5.4 13.8 (1.7) 26.6 37.4 (36.2) 8.0 28.5 14.3 3.8 10.8

S&P Smallcap 10% 2.7 5.4 13.8 1.0 26.3 25.6 (31.1) (0.3) 33.4 15.1 3.3 10.7

Global REITs 10% 2.6 6.1 22.1 (8.1) 20.0 41.3 (48.9) (4.7) 30.4 11.9 (2.5) 8.9

EAFE 10% 3.6 7.0 10.6 (11.7) 8.2 32.5 (43.1) 11.6 14.3 2.6 (4.8) 8.7

Emerging Mkts 10% 6.4 7.0 7.7 (22.7) 9.8 93.5 (59.3) 59.1 12.4 0.3 (4.7) 21.0

Average 3.5 6.2 14.1 (6.9) 17.7 42.8 (42.6) 13.2 24.9 9.6 (0.6) 11.3

Fixed Income

Corporate 10% 1.1 3.8 8.7 8.1 9.0 18.7 (4.9) 4.6 10.8 9.1 8.1 6.6

U.S. Treasury 20+ 10% (1.4) 0.1 4.3 33.8 9.4 (21.4) 33.7 10.2 6.3 12.2 11.3 7.9

Global Aggregate 10% 1.6 3.3 4.8 5.6 5.5 6.9 4.8 9.5 5.1 5.0 6.2 6.4

High Yield 10% 1.5 4.5 12.1 5.0 15.1 58.2 (26.2) 1.9 19.4 12.9 9.3 11.0

Average 0.7 2.9 7.5 13.2 9.8 15.6 1.9 6.5 10.4 9.8 8.7 8.0

60/40 Portfolio 2.4 4.9 11.4 1.1 14.5 31.9 (24.8) 10.5 19.1 9.7 3.1 10.0

Global Perspectives Model AllocationReturns for a globally diversified strategy over the last 10 years refute the notion of a “lost decade”.

7

Overview

The Global Perspectives Model includes 10 asset classes, equally weighted: S&P500, S&P400 Midcap, S&P600 Smallcap, MSCI U.S. REIT Index, FTSE NA REIT Index, MSCI EAFE Index, MSCI BRIC Index, Barclays Capital (BC) U.S. Corporate Bonds, BC U.S. Treasury Bonds, BC Global Aggregate Bonds, BC U.S. High Yield Bonds. Returns are annualized for periods longer than 1 year. Source: FactSet, FTSE NAREIT, ING U.S. Investment Management.

5

Global Perspectives on the Market

ING Global Perspectives

Markets. Insights. Opportunities.

9

Global Perspectives on the Markets Fundamentals: primary driver of markets

– Advancing Corporate Profits

– Broadening Manufacturing

– Consumer Strength Underestimated

– Developing Economies Drive Global Growth

Global Risks: secondary driver unless a breach occurs

– European Debt Crisis

– U.S. Debt and Growth Crisis

– China Hard Landing

– Commodities Bubble

9

Overview

Advancing Corporate Earnings

10Source: Factset, ING Investment Management

Since 1999 the market’s price return is negative, but earnings have grown 250% — from $39 to $97 in 2011 — and are on track to reach $105 by the end of 2012.

$105 per share forecasted

15

400

700

1,000

1,300

1,600

1,900

2,200

5

15

25

35

45

55

65

75

85

95

105

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

S&

P 5

00

Pric

eS&

P 5

00

EP

S

S&P 500 Index (right scale)

S&P 500 EPS (left scale)

2 2012 S&P 500 Earnings Forecast: $105

11

Advancing Corporate EarningsAccelerating and positive earnings drive markets up, and decelerating and negative earnings drive markets down, albeit with a reporting lag.

Source: Standard & Poor’s, First Call, FactSet, ING Investment Management

2012 S&P 500 Earnings Forecast: $1052012 S&P 500 Price Forecast: 1425

14

400

700

1,000

1,300

1,600

1,900

2,200

-100%

-50%

0%

50%

100%

150%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

S&

P 5

00

Pri

ce

S&

P 5

00

EP

S G

row

th

S&P 500 Index (right scale)

S&P 500 EPS growth (left scale)

2003 2004 2005 2006 2007 2008 2009 2010 2011 201230

35

40

45

50

55

60

65

Broadening ManufacturingU.S. factory activity slipped into contraction territory based on economic uncertainties in the euro zone and China and fears of the effects of the “fiscal cliff” here at home.

12

51.5

Source: Institute of Supply Management, Federal Reserve, FactSet

Expansionary (>50)

Contractionary (<50)

Economy

Non Manufacturing

551

Manufacturing

U.S. Institute for Supply Management Global Manufacturing

30

35

40

45

50

55

60

65

1998 2000 2002 2004 2006 2008 2010 2012

Euro zone PMI

Global PMI

44.0

48.4

52

2008 2009 2010 2011 20128000

10000

12000

14000

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Consumer Strength UnderestimatedRetail sales, personal consumption and personal incomes are at all time highs despite high unemployment. The consumer makes up 70% of the U.S. economy.

13Source: FactSet

$ billions $ billions

2004 2006 2008 2010 2012250

300

350

400

450

Personal Income

Personal Consumption Expenditures Retail Sales

Consumer Trends Consumer Trends

48

(25)

(20)

(15)

(10)

(5)

0

5

10

15

20

100

120

140

160

180

200

220

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

14

S&P Case-Shiller Home Price Index Home values are still 31% below 2006 levels but the 20 City Composite Index has shown recent upticks and signs of a sustainable recovery with the first year over year price increase in two years.

Source: Factset, S&P Case-Shiller, Bloomberg

Economy

Index Level

142

% 1 YR change207

58

Unemployment RateHigh unemployment may reluctantly recover as growth resumes; recent reports are somewhat mixed.

15Source: Bureau of Labor Statistics, FactSet

Economy

1964 1967 1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012

200,000

400,000

600,000

800,000

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

Unemployment Rate

Initial Unemployment Claims

000’sRecessions

55

16

Developing Economies - World GDP and Emerging Market ImportanceDespite the great recession, world GDP continued to rise due to growth in emerging markets.

0

20,000

40,000

60,000

80,000

1990 1993 1996 1999 2002 2005 2008 2011

$ trillions

Source: The World Bank Group* China, India, Russia, Brazil, Mexico, Korea, Indonesia and Taiwan

World GDP

0

10

20

30

40

50

60

70

80

1991 1995 1999 2003 2007 2011

Percent Contribution to Global Growth, PPP Basis

Global Emerging Markets Top 8*

%

U.S. + European Union + Japan

Emerging Market Importance

43

17

Developing Economies — Shanghai, China 1990

(Catherine Rampell photo)

Developing Economies — Shanghai, China, 2010

18

(Catherine Rampell photo)

19

Global Risks — European Debt CrisisPIIGS countries’ debt as a % of GDP is unsustainable.

Source: International Monetary Fund (IMF) as of 2011

Austria3% Belgium

4%Cyprus

0%

Finland2%

France21%

Germany27%

Greece3%

Ireland2%

Italy17%

Luxembourg0%

Malta0%

Netherlands6%

Portugal2%

Slovak Republic

1%Slovenia

0%

Spain12%

Euro Area 2010 GDP by Country

0

20

40

60

80

100

120

140

160

0

500

1000

1500

2000Gross Debt in Euros

(billions)Debt as % of

GDP

Euro Zone Debt

45

1964 1970 1976 1982 1988 1994 2000 2006 2012

0

20

40

60

80

100

120

20Source: Factset

Global Risks — U.S. DebtThe total federal public debt outstanding exceeds 95% of GDP (excluding Social Security and Medicare), a level that triggered the U.S. downgrade by S&P. The current U.S. deficit is over $1.4 trillion — more than 9% of GDP.

> 9.4%of GDP

> 95%of GDP

% of GDP

Debt

Deficit

$

Deficit

Debt

U.S. Government Debt Deficit Levels

61

1964 1972 1980 1988 1996 2004 2012

0

4,000,000

8,000,000

12,000,000

16,000,000

21

Global Risks — U.S. GrowthThe economy has surged after each of the past 2%+ falls in GDP (Y/Y) since 1948. The U.S. has recovered the output level it lost in the recession and has now reached new highs. Expansions historically last about five years.

Source: Bloomberg

Breakdown

Consumption: 71%Government: 20%

Investment: 12%Exports: 12%Imports: (15%)

56

(10)

(5)

0

5

10

15

20

1952 1957 1962 1967 1972 1977 1982 1987 1992 1997 2002 2007 2012$1

$2

$3

$4

$5

$6

$7

$8

$9

$10

$11

$12

2Q12 1.3%

Perc

en

t(%)

Real annualized GDP % change

Real GDP Cumulative Value starting at $1

Gro

wth

of $

1

22

Global Risks — China Hard LandingChina’s declining industrial and electricity production as well as stalled export growth raises fears about the likelihood of a “hard landing” from its enviable recent growth. China GDP growth is now reported to be 7.9%.

Source: Factset

International

Y/Y % change

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

-30

-20

-10

0

10

20

30

40

50Export Growth

Industrial Production

Electricity Production

Tectonic Shifts — TradeNew trade routes between Asian and Latin American countries — the intra-emerging market trade — are re-shaping the economic landscape

23Source: FactSet

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012(80)

(70)

(60)

(50)

(40)

(30)

(20)

(10)

0

50

100

150

200

250

Exports(right axis)

Imports(right axis)

Trade Deficit(left axis) Highest

Export Level - JUN

$185 Bil

$USD billions $USD billionsRecessions

U.S. Trade

67

24

Tectonic Shifts — TechnologyTechnological innovation is unpredictable and unstoppable, exerting a powerful influence over every sector of the market

Horn River

Montney Colorado Group

Gammon

Bakken

Laram

ide

Th

rust B

elt

Mowry

Green RiverBaxter

Mancos

McClure

Monterey

GothicHovenweep

Lewis

Mancos

Pierre

Palo Duro

Barnett

Eagle Ford

Woodford Fayetteville

Barnett/ Woodford

Laramide

Thrust Belt

Oua

chita

Thru

st B

elt

HaynesvilleBossier

Floyd/Conasauga/Neal

Ohio

Marcellus

Appal

achi

an

Thru

st B

elt

Utica

Utica Horton Bluff

Antrim

New Albany

Excello/Mulkey

Mobrara

Cane Creek

n Shale Gas Basinsn Devonian/Mississippian Shale Fairway Structural Deformation of Crust

Chattanooga

Sources of Energy in U.S. Manufacturing

Natural Gas: 27%Electricity: 13%Liquefied Petroleum: 11%Coal: 8%Fuel Oil: 2%Other : 39%

Tectonic Shift — EnergyThe abundance of natural gas in North America, as well as the ability to extract oil from shale, is changing the global energy landscape.

Note: Oil Prices are West Texas Intermediate light crude spot price (NYMEX). Source: Advanced Resources, SPE/Holditch Nov 2002 Hill 1999, Cain, 1994 Hart Publishing, 2008 modified from Ziff Energy GroupSource: U.S. Dept of Energy, FactSetSource: Census Bureau, http://upload.wikimedia.org/wikipedia/commons/b/b4/Plate_tectonics_map.gif

Economy

25

64

26

Global Perspectives on 2012

This forecast of future expectations is based on managements' current views and involves known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied.

Market & Economic Forecasts 2012

S&P 500 Index 1425

Dow Jones Index 14000

S&P Earnings Per Share 105

S&P 500 Price/Earnings Ratio 13.5

U.S. 10 Year Treasury Yield 2.86%

Inflation 2.50%

Unemployment Rate 8.00%

Crude Oil (NYM $/BBL) $80

Gold (NYM $/OZ) $1,500

U.S. GDP 2.50%

Euro GDP 0.25%

Global GDP 3.50%

G L O B A L P E R S P E C T I V E S

The Folly of Gaming Diversification

Global Perspectives on the Markets

Tectonic Shifts Impacting Global Growth

Executive Summary

Thank Youwww.INGglobalperspectives.com

ING Global Perspectives

Markets. Insights. Opportunities.

29

Barclays Capital U.S. Aggregate Bond Index is composed of U.S. securities in Treasury, Government-Related, Corporate, and Securitized sectors that are of investment-grade quality or better, have at least one year to maturity, and have an outstanding par value of at least $250 million.

Barclays Capital U.S. Corporate High-Yield Bond Index tracks the performance of non-investment grade U.S. dollar-denominated, fixed rate, taxable corporate bonds including those for which the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below, and excluding Emerging Markets debt.

Barclays Capital Global Aggregate Bond Index measures a wide spectrum of global government, government-related, agencies, corporate and securitized fixed-income investments, all with maturities greater than one year.

The Credit Suisse/Tremont Hedge Fund Index is an asset-weighted hedge fund index covering over 5000 funds with at least US$50 million under management, a 12-month track record, and audited financial statements. It is calculated net of performance fees and expenses. CS/Tremont sub-indexes track hedge fund strategies according to the methods by which fund managers seek investment opportunities such as by asset class and/or use of leverage.

Dow Jones Industrial Average is a price-weighted average computed from the stock prices of 30 large, widely held public companies in the U.S., adjusted to reflect stock splits and dividends.

FTSE NAREIT US Real Estate Index presents comprehensive REIT performance across the U.S. economy, including all commercial investment and property sectors.

FTSE EPRA/NAREIT Global Real Estate Index is designed to represent general trends in eligible real estate equities worldwide.

Index Definitions

The Chicago Board Options Exchange Volatility Index (CBOE VIX) is a measure of the implied volatility of S&P 500 index options. It is one measure of the market's expectation of volatility over the next 30 day period.

JPMorgan Emerging Markets Bond Index Plus (EMBI+) tracks total returns for actively traded emerging markets debt instruments including U.S.-dollar denominated Brady bonds, Eurobonds, and traded loans issued by sovereign entities.

MSCI EAFE Index is a free float-adjusted market capitalization weighted index designed to measure the developed markets’ equity performance, excluding the U.S. & Canada, for 21 countries.

MSCI Europe Index is a free float-adjusted market capitalization weighted index designed to measure equity performance of the developed markets in Europe consisting of 16 country indices.

MSCI Pacific Index is a free float-adjusted market capitalization weighted index designed to measure developed markets’ equity performance of the in the Pacific region consisting of 5 countries.

MSCI Emerging Markets Index is a free float-adjusted market capitalization index that measures emerging market equity performance of 22 countries.

The Municipal Bond Index is a bond index that includes investment-grade, tax-exempt, and fixed-rate bonds with long-term maturities (greater than two years) selected from issues larger than $50 million.

NASDAQ Composite Index is a market capitalization weighted index of the performance of domestic and international common stocks listed on The NASDAQ Stock Market including over 2,800 securities.

30

Index Definitions

The NCREIF (National Council of Real Estate Investment Fiduciaries) Property Index (NPI) is a market value-weighted index of total rates of return for a large pool of commercial real estate properties acquired in the private market for investment purposes. For properties with leverage, returns are reported as if there were no leverage.

Russell 3000 Index measures the performance of the largest 3000 U.S. companies representing approximately 98% of the investible U.S. equity market.

Russell 1000 Index measures the performance of the large-cap segment of the U.S. equity market and includes approximately 1000 of the largest securities based on market capitalization and representing approximately 92% of the U.S. market.

Russell 1000 Growth Index measures the large-cap growth segment of the U.S. equity market including Russell 1000 companies with higher price-to-book ratios and forecasted growth.

Russell 1000 Value Index measures the large-cap value segment of the U.S. equity market including Russell 1000 companies with lower price-to-book ratios and lower expected growth.

Russell Midcap Index measures the performance of mid-cap stocks in the U.S. equity market including 800 of the smallest securities in the Russell 1000® Index, based on market capitalization.

Russell Midcap Growth Index measures the performance of the mid-cap growth segment of the U.S. equity market including Russell Midcap Index companies with higher price-to-book ratios and forecasted growth.

Russell Midcap Value Index measures the performance of the mid-cap growth segment of the U.S. equity market including Russell Midcap Index companies with lower price-to-book ratios and forecasted growth.

Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity market including approximately 2000 of the smallest securities based on market capitalization.

Russell 2000 Growth Index measures the performance of small-cap growth stocks in the U.S. equity market including Russell 2000 companies with higher price-to-value ratios and forecasted growth.

Russell 2000 Value Index measures the performance of small-cap growth stocks in the U.S. equity market including Russell 2000 companies with lower price-to-value ratios and forecasted growth.

S&P 500 Index is a widely regarded as the best single gauge of the U.S. equities market, including 500 leading companies in major industries of the U.S. economy.

S&P/LSTA (Loan Syndications and Trading Association) Leveraged Loan Index (LLI) is a total return market value index that tracks fully funded, senior secured, first lien term loans syndicated in the U.S., as well as dollar-denominated overseas loans, including 90-95% of the institutional universe.

The S&P GICS (Global Industry Classification Standard) sectors were developed by MSCI and Standard & Poor’s to provide standardized industry definitions consisting (in the U.S.) of 10 sectors, 24 industry groups, and 68 industries.

Thomson VentureXpertTM is a database provided by Thomson Venture Economics, a leading provider of industry data about venture capital and private equity firms, which is regarded as the industry-standard source for comprehensive information on venture funds, private firms, venture-backed companies and limited partners, as well as analytics for fund statistics and performance.

U.S. Treasury Index is a component of the Barclays Capital U.S. Aggregate Index.

31

Important Disclosures

All indexes are unmanaged and an individual cannot invest directly in an index. Index returns do not include fees or expenses. Past performance is no guarantee of future results

The views and judgments expressed are those of ING Global Perspectives. They are subject to change at any time. These views do not necessarily reflect the opinions of any other firm.

All investing involves risks of fluctuating prices and the uncertainties of rates of return and yield inherent in investing. All security transactions involve substantial risk of loss.

You should consult your tax, legal, accounting or other advisors about the matters discussed herein.

As indicated on each page, some information was obtained from outside sources and is believed to be reliable, but ING does not guarantee its completeness or accuracy.

Diversification does not guarantee against a loss and there is no guarantee that a diversified portfolio will outperform a non-diversified portfolio.

PRINCIPAL RISKS: All investing involves risks of fluctuating prices and the uncertainties of rates of return and yield inherent in investing. Mutual funds are subject to market risk. Foreign Investing does pose special risks including currency fluctuation, economic and political risks not found in investments that are solely domestic. Please keep in mind, using diversification or asset allocation as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss in declining markets.Global Perspectives Market Models are tactically managed to a strategy. There is no guarantee that intended results or forecasts will be realized. Past performance is no guarantee of future results.Your clients should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. For a free copy of the Fund’s prospectus, which contains this and other information, visit us at www.inginvestment.com or call ING Investment Management at 1-800-992-0180. Please instruct your clients to read the prospectus carefully before investing.

This presentation has been prepared by ING Investment Management for informational purposes. Certain information may be received from sources ING Investment Management considers reliable; ING Investment Management does not represent that such information is accurate or complete. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change without notice. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors. ING assumes no obligation to update any forward-looking information contained in this document. ING Investment Management is not soliciting or recommending any action based on any information in this document. Past performance is no guarantee of future results.

CA:3706

32