Embed Size (px)

Citation preview

PRESENTATION OF THE CMNE GROUP

LOCATION page 4

EDITORIAL page 5

CONTEXT pages 6-7

HIGHLIGHTS page 8

PROFILE AND KEY FIGURES page 9

THE CMNE GROUP pages 10-11

FINANCIAL ORGANISATIONAL CHART page 12

3

LOCATION

English Channel

North Sea NL

UK

D

Crédit Mutuel Nord Europe branches

50 kilometres

Beobank branches

Paris

Brussels

London

Amsterdam

Luxembourg

LILLE

Bruges Antwerp

Ghentd

LeuvenHasselt

LiègeWavre

Mons Namur

Arlon

Arras

Amiens

Beauvais Laon

Charleville-Mézières

Reims

Situation as at 31/12/16

ANNUAL REPORT 20164

PRES

ENTA

TIO

N

OF

THE

C

MN

E G

ROU

P

5

EDITORIAL

left: André. HALIPRÉ

right: Éric CHARPENTIER

“Development secured in all the lines of business and consolidated financial strength”

At the end of 2016, the CMNE Group posted solid results against the background of low interest rates that impact the interest margins. Its consolidated NBI and consolidated net profit amounted to €1,129 million and €205 million, down by 3.8% and 3.5% respectively. Each of the Group’s lines of business registered a sound operational performance whilst continuing its investments in the quality of service and digital transformation. Our 4,434 employees provided personalised service to 1.6 million shareholders and customers.

In balancing growth and profitability, we also bolstered our prudential capital. It amounts to €3.3 billion, up by 18% from 2015, including the impact of the first public issue of subordinated debt by the CMNE among French and European investors in September 2016 for €300 million. The overall solvency ratio stands at 20.36%, and the CET 1 capital ratio at 15.13%, beyond the regulatory requirements.

Launched in 2016, our Medium Term Plan “Vision 2020” comprises five strategic planks and is geared to improving customer satisfaction irrespective of the channel, innovating with digital technology, investing in human resources, seizing growth opportunities and generating sustainable profitability through rigorous cost, risk and capital management. The CMNE is henceforth built around three competence centres: Banking, Insurance and Asset Management.

Banking, through its networks (France, Belgium, and Business), represents 1.6 million customers. The local branches put in fine commercial performances in 2016, illustrated in particular by the success of new real estate sales. Against the background of historically low interest rates, renegotiations of loans were contained, thus preserving future margins. Moreover, the French network continued to adapt to new behaviours and expanded its offer of Internet services, through complementary physical and digital channels. In Belgium, the second domestic market of the CMNE Group, the merger of Beobank and BKCP, carried out successfully in May 2016, created a real challenger of the four players in the sector. Beobank is henceforth positioned in all the retail customer segments with a complete product offer. The Business division embarked on an operation to refocus on its territories and continued to expand in its expertise segments, such as lease finance. On the Insurance front, 2016 was marked by the implementation of Solvency 2 and the continued development of the unit-linked activity. For Asset Management, La Française confirmed its leading position in real estate and continued to develop its investment solutions whilst expanding its institutional clientele internationally. The outstanding amount of La Française now stands at nearly €60 billion at the end of the financial year.

Each of these three lines of business contributes to the fine results of the CMNE Group and the consolidation of its Euro-regional positioning as a bank-insurer. At the national level, the financial stability of the Crédit Mutuel was confirmed yet again by the stress tests conducted by the ECB, which placed it at the forefront of French banks and the leading group of European banks. The ratings by Standard & Poor’s, Fitch and Moody’s place the Crédit Mutuel group at the best level of the French banking sector.

2017 will be an even more complex and unstable year for the banking sector, on both the economic and the regulatory front. Our success requires us to continue the transformation of our customer relations model, accelerate the digitisation of our lines of business and rationalise our Group in terms of organisation and investments. In a world where everything is picking up speed, we have to capitalise on our mutualist values, while providing ever more innovative services to our customers-shareholders.

André HALIPRÉChairman

Éric CHARPENTIERGeneral Manager

PRESENTATIO

N

OF TH

E C

MN

E GRO

UP

7

In 2016, all the entities of the CMNE Group registered fine momentum in their business, continued the synergies and contributed to the Group’s overall performance.

The CMNE registered controlled development throughout 2016, thanks to the: • Diversification of the sources of revenues with insurance and asset management, the development of

non-banking commissions linked to the network activity (AFEDIM, Provol…) ;• The preservation of margins whilst remaining vigilant regarding renegotiations; • Risk control, as shown by the low cost of risk noted.

In the face of market shocks, the sound results attest to the capacities of all lines of business to structure themselves and to adapt. Combined with rigorous management, the clear strategic choices of the Medium Term Plan 2020 have made it possible to launch the first projects of said plan and to score many successes. They also prove the Group’s vitality.

The CMNE has also continued to strengthen its prudential capital which amounts to €3.3 billion (+18%), including the impact of the first public issue of a subordinated debt among French and European investors for an amount of €300 million. The overall solvency ratio stands at 20.36%, and the CET 1 capital ratio at 15.13%, beyond the regulatory requirements of the ECB.

2016 was particularly marked by the conjunction of various factors of this environment: slow growth, low interest rates, regulation and digital revolution.

Has this weighed on the activity and results of the CMNE?

The CMNE group affirmed its transformation by launching a new strategic plan for 2020 in September 2015. It wants to be known as an ambitious group, capable of taking up challenges, and has charted its directions, namely to: • Improve customer satisfaction, irrespective of the channel;• Innovate with digital technology;• Invest in human resources;• Seize growth opportunities;• Generate sustainable profitability through rigorous cost, risk and capital management.

Banking and insurance have been going through profound, rapid changes (regulation, digitisation, etc.) in a complex environment for several years.

How can the CMNE adapt to these numerous developments?

First, the CMNE has redefined its organisation which is now built around three lines of business: Banking, Insurance and Asset Management. Priorities have been clearly defined for each of these, in line with its Medium Term Plan.

Second, it has developed services geared to customer satisfaction. As proof, the Crédit Mutuel has emerged as the preferred brand of the French according to the Posternak/Ifop barometer1/Ifop and has risen to n°1 for the Banking sector in customer relations2 – distinctions that attest to the relationship of trust and confidence between the Crédit Mutuel and its customers-shareholders.

Finally, the CMNE has embarked on the digital transformation of its environment through a show of innovation and creativity. Its winning assets and achievements illustrate its dynamism, e.g.: its Customers relations Centre capable of engaging in V@D, its Internet initiatives adopted by other Crédit Mutuel branches, the development of business line laboratories, the implementation of artificial intelligence tools with the experimentation of the Watson solution in pilot local branches or the development of cooperative tools…

1 Posternak Ifop barometer /fourth quarter 20162 Survey conducted by Bearing Point and Kantar and TNS among customers from a sample of 4000 people

What are the first accomplishments that reflect this transformation of the CMNE?

2016, THE CMNE MOBILISED IN A DIFFICULT ENVIRONMENT

ANNUAL REPORT 20166

HIGHLIGHTS

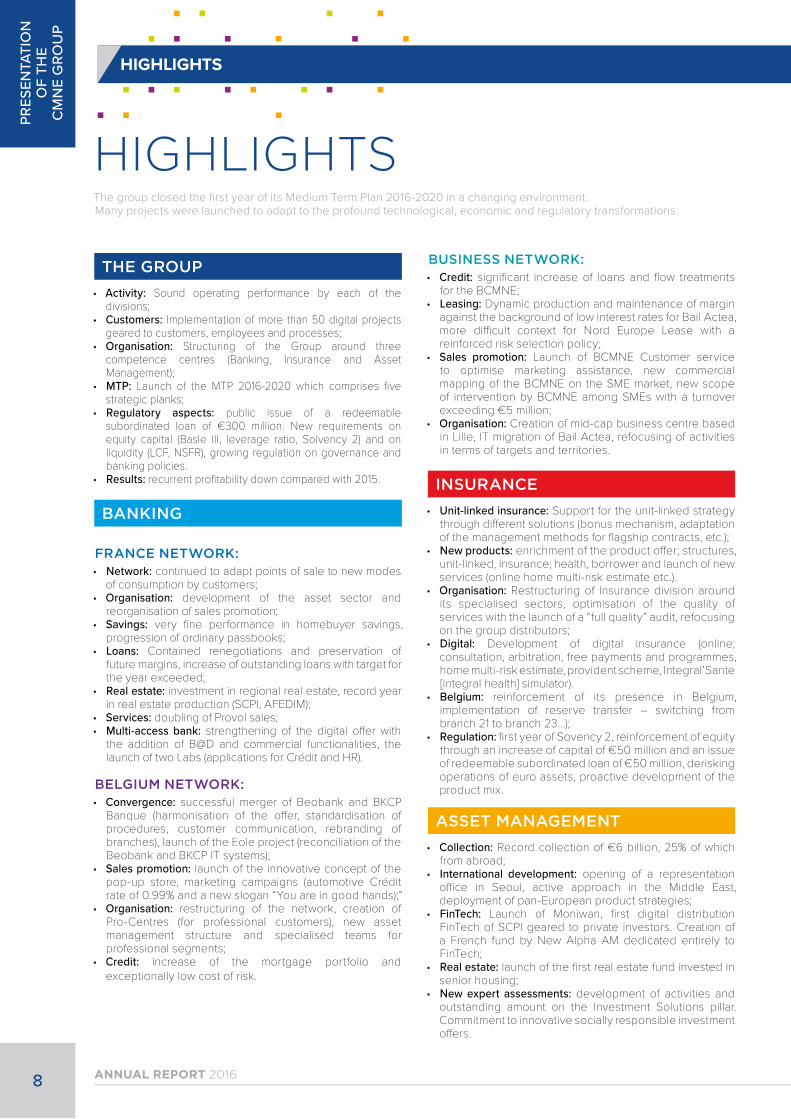

HIGHLIGHTS The group closed the first year of its Medium Term Plan 2016-2020 in a changing environment. Many projects were launched to adapt to the profound technological, economic and regulatory transformations.

THE GROUP

• Activity: Sound operating performance by each of the divisions;

• Customers: Implementation of more than 50 digital projects geared to customers, employees and processes;

• Organisation: Structuring of the Group around three competence centres (Banking, Insurance and Asset Management);

• MTP: Launch of the MTP 2016-2020 which comprises five strategic planks;

• Regulatory aspects: public issue of a redeemable subordinated loan of €300 million. New requirements on equity capital (Basle III, leverage ratio, Solvency 2) and on liquidity (LCF, NSFR), growing regulation on governance and banking policies.

• Results: recurrent profitability down compared with 2015.

BANKING

FRANCE NETWORK:• Network: continued to adapt points of sale to new modes

of consumption by customers; • Organisation: development of the asset sector and

reorganisation of sales promotion; • Savings: very fine performance in homebuyer savings,

progression of ordinary passbooks; • Loans: Contained renegotiations and preservation of

future margins, increase of outstanding loans with target for the year exceeded;

• Real estate: investment in regional real estate, record year in real estate production (SCPI, AFEDIM);

• Services: doubling of Provol sales;• Multi-access bank: strengthening of the digital offer with

the addition of B@D and commercial functionalities, the launch of two Labs (applications for Crédit and HR).

BELGIUM NETWORK: • Convergence: successful merger of Beobank and BKCP

Banque (harmonisation of the offer, standardisation of procedures, customer communication, rebranding of branches), launch of the Eole project (reconciliation of the Beobank and BKCP IT systems);

• Sales promotion: launch of the innovative concept of the pop-up store, marketing campaigns (automotive Crédit rate of 0.99% and a new slogan “You are in good hands);”

• Organisation: restructuring of the network, creation of Pro-Centres (for professional customers), new asset management structure and specialised teams for professional segments;

• Credit: increase of the mortgage portfolio and exceptionally low cost of risk.

BUSINESS NETWORK:• Credit: significant increase of loans and flow treatments

for the BCMNE;• Leasing: Dynamic production and maintenance of margin

against the background of low interest rates for Bail Actea, more difficult context for Nord Europe Lease with a reinforced risk selection policy;

• Sales promotion: Launch of BCMNE Customer service to optimise marketing assistance, new commercial mapping of the BCMNE on the SME market, new scope of intervention by BCMNE among SMEs with a turnover exceeding €5 million;

• Organisation: Creation of mid-cap business centre based in Lille, IT migration of Bail Actea, refocusing of activities in terms of targets and territories.

INSURANCE

• Unit-linked insurance: Support for the unit-linked strategy through different solutions (bonus mechanism, adaptation of the management methods for flagship contracts, etc.);

• New products: enrichment of the product offer; structures, unit-linked, insurance; health, borrower and launch of new services (online home multi-risk estimate etc.).

• Organisation: Restructuring of Insurance division around its specialised sectors, optimisation of the quality of services with the launch of a “full quality” audit, refocusing on the group distributors;

• Digital: Development of digital insurance (online; consultation, arbitration, free payments and programmes, home multi-risk estimate, provident scheme, Integral’Sante [integral health] simulator).

• Belgium: reinforcement of its presence in Belgium, implementation of reserve transfer – switching from branch 21 to branch 23…);

• Regulation: first year of Sovency 2, reinforcement of equity through an increase of capital of €50 million and an issue of redeemable subordinated loan of €50 million, derisking operations of euro assets, proactive development of the product mix.

ASSET MANAGEMENT

• Collection: Record collection of €6 billion, 25% of which from abroad;

• International development: opening of a representation office in Seoul, active approach in the Middle East, deployment of pan-European product strategies;

• FinTech: Launch of Moniwan, first digital distribution FinTech of SCPI geared to private investors. Creation of a French fund by New Alpha AM dedicated entirely to FinTech;

• Real estate: launch of the first real estate fund invested in senior housing;

• New expert assessments: development of activities and outstanding amount on the Investment Solutions pillar. Commitment to innovative socially responsible investment offers.

ANNUAL REPORT 20168

PRES

ENTA

TIO

N

OF

THE

C

MN

E G

ROU

P

9

PROFILE AND KEY FIGURES

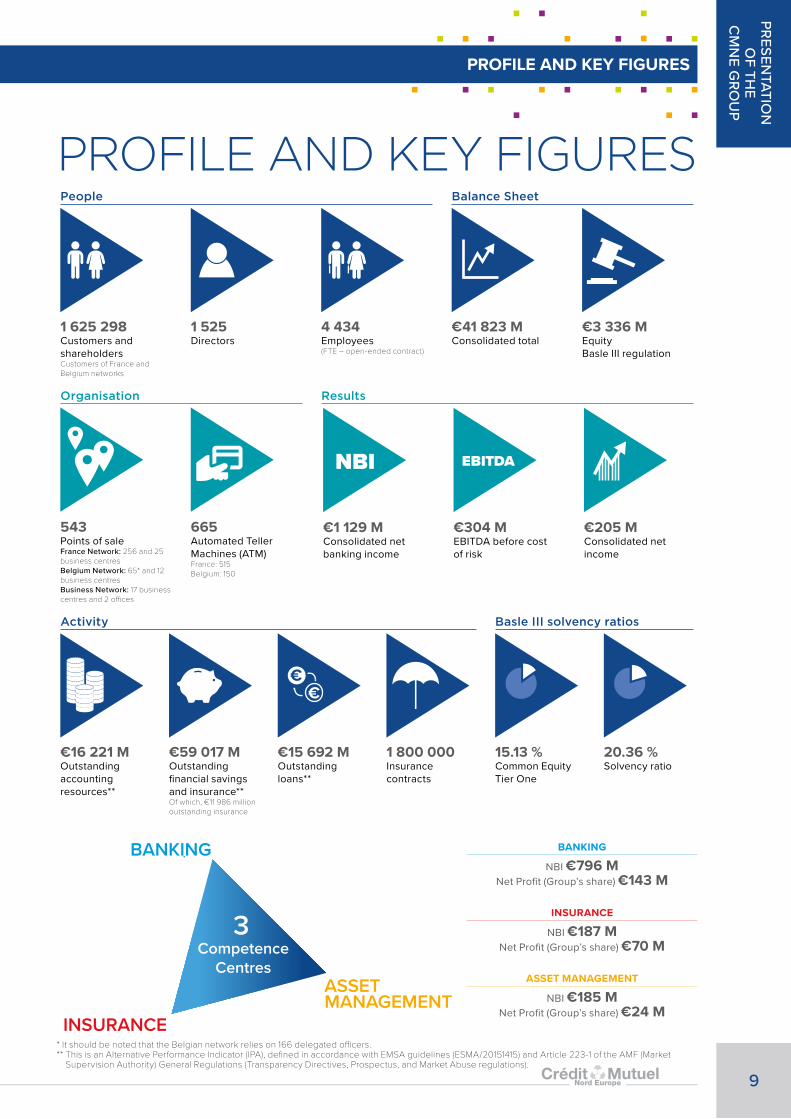

PROFILE AND KEY FIGURES People Balance Sheet

1 625 298Customers and shareholdersCustomers of France and Belgium networks

1 525Directors

4 434Employees(FTE – open-ended contract)

€41 823 MConsolidated total

€3 336 MEquity Basle III regulation

Organisation Results

NBI EBITDA

543Points of sale France Network: 256 and 25 business centres Belgium Network: 65* and 12 business centres Business Network: 17 business centres and 2 offices

665Automated Teller Machines (ATM)France: 515Belgium: 150

€1 129 MConsolidated net banking income

€304 MEBITDA before cost of risk

€205 MConsolidated net income

Activity Basle III solvency ratios

€16 221 MOutstanding accounting resources**

€59 017 MOutstanding financial savings and insurance**Of which, €11 986 million outstanding insurance

€15 692 MOutstanding loans**

1 800 000Insurance contracts

15.13 %Common Equity Tier One

20.36 %Solvency ratio

BANKING

INSURANCE

ASSETMANAGEMENT

3 Competence

Centres

BANKING

NBI €796 MNet Profit (Group’s share) €143 M

INSURANCE

NBI €187 MNet Profit (Group’s share) €70 M

ASSET MANAGEMENT

NBI €185 MNet Profit (Group’s share) €24 M

* It should be noted that the Belgian network relies on 166 delegated officers.** This is an Alternative Performance Indicator (IPA), defined in accordance with EMSA guidelines (ESMA/20151415) and Article 223-1 of the AMF (Market

Supervision Authority) General Regulations (Transparency Directives, Prospectus, and Market Abuse regulations).

PRESENTATIO

N

OF TH

E C

MN

E GRO

UP

THE CMNE GROUP

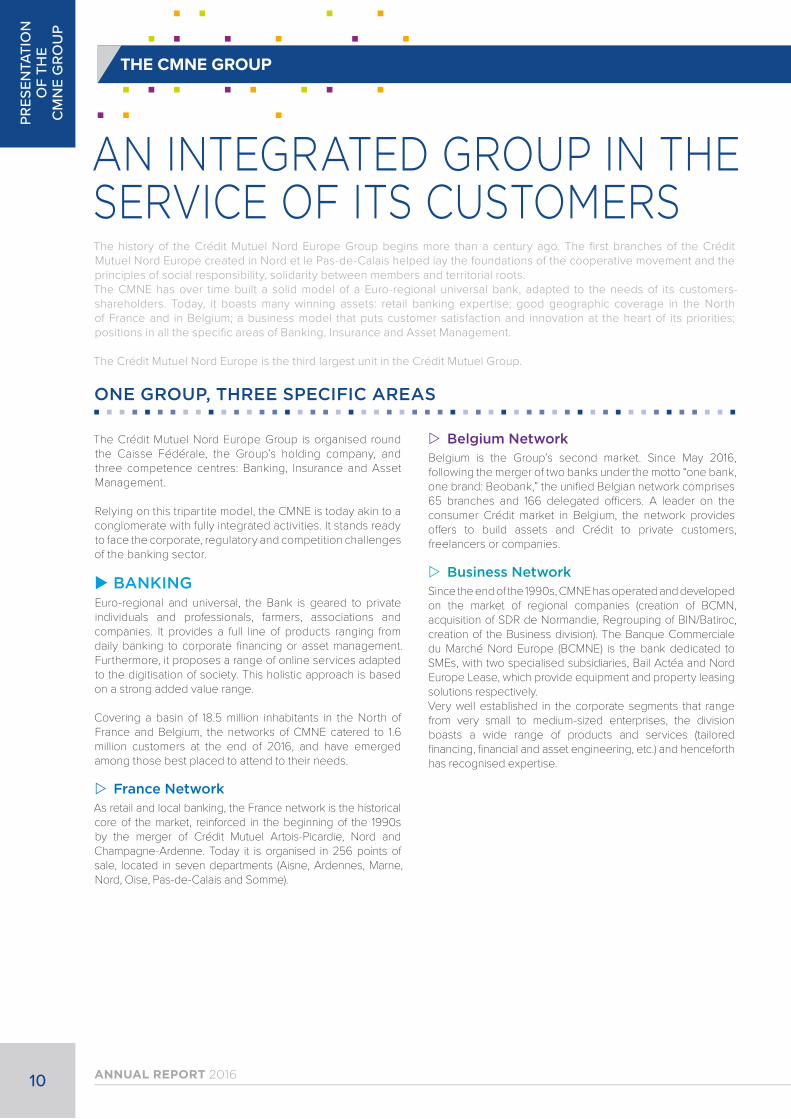

AN INTEGRATED GROUP IN THE SERVICE OF ITS CUSTOMERS The history of the Crédit Mutuel Nord Europe Group begins more than a century ago. The first branches of the Crédit Mutuel Nord Europe created in Nord et le Pas-de-Calais helped lay the foundations of the cooperative movement and the principles of social responsibility, solidarity between members and territorial roots. The CMNE has over time built a solid model of a Euro-regional universal bank, adapted to the needs of its customers-shareholders. Today, it boasts many winning assets: retail banking expertise; good geographic coverage in the North of France and in Belgium; a business model that puts customer satisfaction and innovation at the heart of its priorities; positions in all the specific areas of Banking, Insurance and Asset Management.

The Crédit Mutuel Nord Europe is the third largest unit in the Crédit Mutuel Group.

ONE GROUP, THREE SPECIFIC AREAS

The Crédit Mutuel Nord Europe Group is organised round the Caisse Fédérale, the Group’s holding company, and three competence centres: Banking, Insurance and Asset Management.

Relying on this tripartite model, the CMNE is today akin to a conglomerate with fully integrated activities. It stands ready to face the corporate, regulatory and competition challenges of the banking sector.

X BANKING Euro-regional and universal, the Bank is geared to private individuals and professionals, farmers, associations and companies. It provides a full line of products ranging from daily banking to corporate financing or asset management. Furthermore, it proposes a range of online services adapted to the digitisation of society. This holistic approach is based on a strong added value range.

Covering a basin of 18.5 million inhabitants in the North of France and Belgium, the networks of CMNE catered to 1.6 million customers at the end of 2016, and have emerged among those best placed to attend to their needs.

Z France NetworkAs retail and local banking, the France network is the historical core of the market, reinforced in the beginning of the 1990s by the merger of Crédit Mutuel Artois-Picardie, Nord and Champagne-Ardenne. Today it is organised in 256 points of sale, located in seven departments (Aisne, Ardennes, Marne, Nord, Oise, Pas-de-Calais and Somme).

Z Belgium Network Belgium is the Group’s second market. Since May 2016, following the merger of two banks under the motto “one bank, one brand: Beobank,” the unified Belgian network comprises 65 branches and 166 delegated officers. A leader on the consumer Crédit market in Belgium, the network provides offers to build assets and Crédit to private customers, freelancers or companies.

Z Business Network Since the end of the 1990s, CMNE has operated and developed on the market of regional companies (creation of BCMN, acquisition of SDR de Normandie, Regrouping of BIN/Batiroc, creation of the Business division). The Banque Commerciale du Marché Nord Europe (BCMNE) is the bank dedicated to SMEs, with two specialised subsidiaries, Bail Actéa and Nord Europe Lease, which provide equipment and property leasing solutions respectively. Very well established in the corporate segments that range from very small to medium-sized enterprises, the division boasts a wide range of products and services (tailored financing, financial and asset engineering, etc.) and henceforth has recognised expertise.

ANNUAL REPORT 201610

PRES

ENTA

TIO

N

OF

THE

C

MN

E G

ROU

P

11

LE GROUPE CMNE

X INSURANCE Created in 2004, the Nord Europe Assurances (NEA) Group is a holding which encompasses all the competencies of theCrédit Mutuel Nord Europe Group in life insurance, contingency, life, car and home insurance. The group managed to adapt on these different markets to provide a full range of products that meet specific needs: retirement savings, transfer, dependence, protection of property.

NEA comprises three life insurance companies (ACMN-Vie, North Europe Life Belgium and Nord Europe Life Luxembourg), a property and casualty insurance company (ACMN casualty), a reinsurance company (CPBK-Re) and a brokerage firm (CCMNE). They devise the insurance products on their own or in partnership with the ACM.

XASSET MANAGEMENT The third and last specific area of Crédit Mutuel Nord Europe, La Française Group, is the asset management subsidiary for third parties.

La Française is positioned as an overall asset manager, in terms of specific area and commercial coverage. It provides a full range of products and services for a diversified clientele (institutional investors, banking networks, distribution platforms, specifiers, private customers, etc.).

Created in 1975, the Group has come a long way in forty years and is now organised into four pillars: • La Française Global Asset Management:

Management and marketing of securities;• La Française Global Real Estate Investment Managers:

Management and marketing of property solutions;• La Française Global Investment Solutions:

Management and marketing of investment solutions;• La Française Global Direct Financing:

Management and marketing of financing and economic solutions.

These structures are situated mainly in France, with an office on the Boulevard Raspail in Paris. They are also established in Luxembourg, London, Frankfurt and Hong Kong, but also in Italy and Spain (representation offices). They devise financial products alone or in partnership with other affiliated management companies. For their distribution, they rely on their own networks, those of the CMNE Group or their partners (CGPI and financial networks).

PRESENTATIO

N

OF TH

E C

MN

E GRO

UP

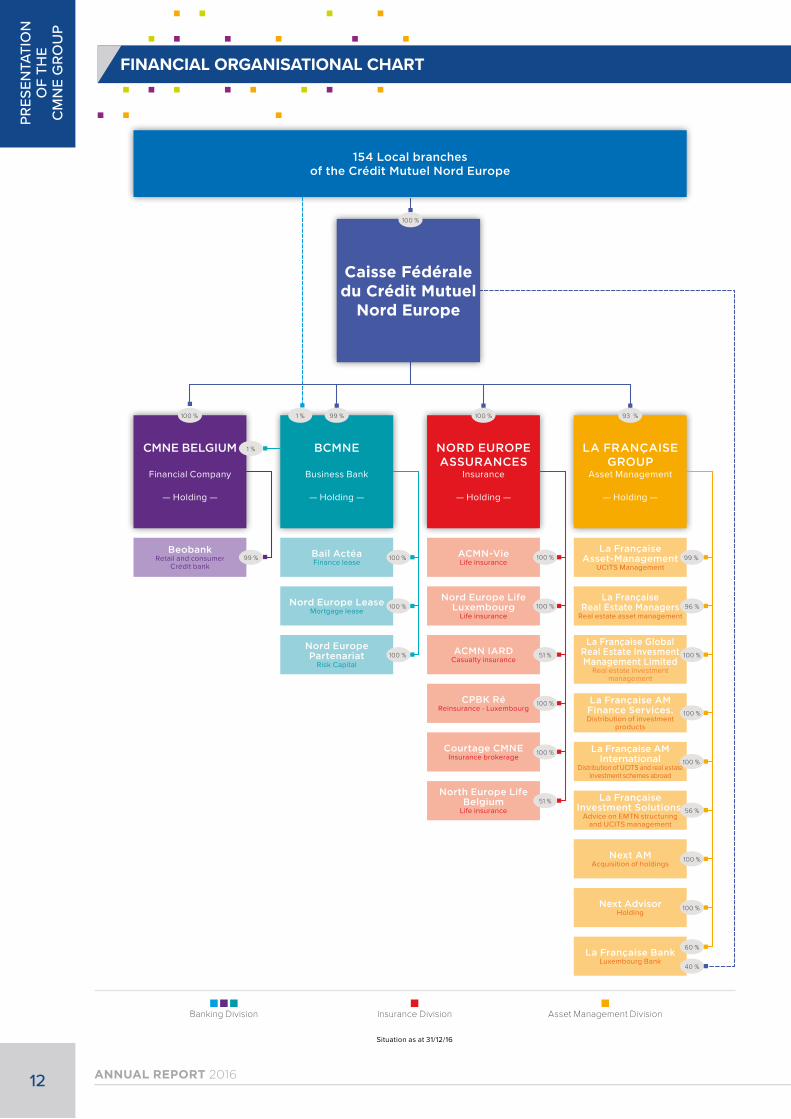

FINANCIAL ORGANISATIONAL CHART

ANNUAL REPORT 201612

PRES

ENTA

TIO

N

OF

THE

C

MN

E G

ROU

P

154 Local branches of the Crédit Mutuel Nord Europe

CMNE BELGIUM

Financial Company

— Holding —

BeobankRetail and consumer

Crédit bank Bail ActéaFinance lease

Nord Europe LeaseMortgage lease

Nord Europe Partenariat

Risk Capital

BCMNE

Business Bank

— Holding —

ACMN-VieLife insurance

CPBK RéReinsurance - Luxembourg

Nord Europe Life Luxembourg

Life insurance

Courtage CMNEInsurance brokerage

North Europe Life Belgium

Life insurance

ACMN IARDCasualty insurance

NORD EUROPE ASSURANCES

Insurance

— Holding —

La Française Asset-Management

UCITS Management

La Française AM Finance Services. Distribution of investment

products

La Française Real Estate Managers

Real estate asset management

La Française AM International

Distribution of UCITS and real estate investment schemes abroad

Next AdvisorHolding

La Française Global Real Estate InvesmentManagement Limited

Real estate investment management

La Française Investment Solutions.

Advice on EMTN structuring and UCITS management

La Française BankLuxembourg Bank

Next AMAcquisition of holdings

LA FRANÇAISE GROUP

Asset Management

— Holding —

100 %

1 %

99 %

1 %

100 % 100 % 99 %

100 % 96 %

51 % 100 %

100 %100 %

100 %

51 %

100 %

100 %

56 %

60 %

40 %

100 %

100 %

100 %

99 % 100 % 93 %

Caisse Fédérale du Crédit Mutuel

Nord Europe

100 %

Situation as at 31/12/16

Banking Division

Insurance Division

Asset Management Division