Embed Size (px)

Citation preview

University of Mississippi University of Mississippi

eGrove eGrove

Guides, Handbooks and Manuals American Institute of Certified Public Accountants (AICPA) Historical Collection

1-1-1998

Comparing attest and management advisory services : a guide for Comparing attest and management advisory services : a guide for

the practitioner; Management advisory services special report the practitioner; Management advisory services special report

American Institute of Certified Public Accountants

Follow this and additional works at: https://egrove.olemiss.edu/aicpa_guides

Part of the Accounting Commons, and the Taxation Commons

Recommended Citation Recommended Citation American Institute of Certified Public Accountants, "Comparing attest and management advisory services : a guide for the practitioner; Management advisory services special report" (1998). Guides, Handbooks and Manuals. 157. https://egrove.olemiss.edu/aicpa_guides/157

This Article is brought to you for free and open access by the American Institute of Certified Public Accountants (AICPA) Historical Collection at eGrove. It has been accepted for inclusion in Guides, Handbooks and Manuals by an authorized administrator of eGrove. For more information, please contact [email protected].

A Management Advisory Services

Special Report

Comparing Attest and Management Advisory Services: A Guide for the Practitioner

A special report developed to aid MAS practitioners in recognizing when an engagement requires performance o f an

attest service in addition to, or instead of, management advisory services.

AICPA American Institute of Certified Public Accountants

NOTICE TO READERS

This report is issued by the American Institute of Certified Public Accountants for the information of its members and other interested parties. However, the report does not represent an official position of any of the Institute’s senior technical committees.

A Management Advisory Services

Special Report

Comparing Attest and Management Advisory Services A Guide for the Practitioner

• •

A special report developed to aid MAS practitioners in recognizing when an engagement requires performance of an

attest service in addition to, or instead of, management advisory services.

AICPA American Institute of Certified Public Accountants

Copyright © 1988 by theAmerican Institute o f Certified Public Accountants, Inc.1211 Avenue of the Americas, New York, N.Y. 10036—8775 1 2 3 4 5 6 7 8 9 0 MAS 8 9 8

Preface

The issuance of a series of binding professional standards relating to attestation engagements has created new requirements that will also affect certain MAS engagements. The attestation standards will apply to attestation services even when such services are part of an engagement to provide management advisory services.

An attest service and a management advisory service differ in purpose, structure, and reporting requirements. The appropriate professional standards need to be recognized and applied.

This MAS Special Report has been prepared to aid practitioners in determining which service to perform. Such determination is a responsibility of the practitioner, not the client, since the client will generally not be aware of the differences between the services.

MAS Practice Standards and Administration Subcommittee (1986—87)

Jacqueline L. Babicky, Chairman William E. Partin Carl M. Alongi Michael G. PershWilliam T. Cuppett Robert F. ShriverStephen D. Nadler Donald H. SweeneyJ. T. Marty O’Malley Garnett William Vining

Monroe S. Kuttner, DirectorManagement Advisory Services

Monte N. Kaplan, Technical Manager Management Advisory Services

Steven E. Sacks, Senior Technical Advisor Management Advisory Services

Libby F. Bruch, Editor/Coordinator Management Advisory Services

iii

Contents

Preface iii

Introduction 1

Attributes of Attestation Services 3

Parties Involved 3Function Performed 3Criteria Used 4Engagement Report 4

Conclusions 5

Appendix A—Comparison of Attestation Standards to MASStandards 8

Exhibit A-1—Attestation and MAS Standards 10

Appendix B—Decision Alternatives Flowchart 12

Appendix C—Engagement Examples 14

Exhibit C-1— Software Engagement 16Exhibit C-2—Business Plan Development Engagement 18Exhibit C-3—Health Care Consulting Engagement 22Exhibit C-4— Computer Feasibility and Installation Engagement 25

Appendix D—Illustrative Engagement Letter 28

Appendix E— Statement on Standards for AttestationEngagements—Attestation Standards 32

Appendix F—Statement on Standards for Attestation Engagements—Attest Services Related to MASEngagements 65

v

Introduction

The purpose of this special report is to help a practitioner1 identify when an attest service is appropriate. An attest service may be either required or desired. It may be performed instead of, or as part of, a management advisory services (MAS) engagement. Determining the appropriate service is the responsibility of the practitioner. Therefore, practitioners need to be aware of the significant differences between attest and management advisory services that will affect engagement planning and staffing, fieldwork, evaluation criteria, and reporting.

In the past, a practitioner could more readily determine the type of service to provide and apply the appropriate professional standards. Today, the issue is more complex. For example, the Statements on Standards for Attestation Engagements (SSAEs) and the Statement on Standards for Accountants’ Services on Prospective Financial Information can apply even if the described services are provided as part of a broader MAS or tax engagement. The contents of this report will be more easily understood if the reader is familiar with the SSAEs, Attestation Standards and Attest Services Related to MAS Engagements. For the convenience of readers, those standards are reprinted as appendices E and F of this report.

When is the practitioner engaged as an attester and when as an advisor? The subject matter of an engagement does not establish whether the service to be performed is an attest service, a management advisory service, or both, nor can the practitioner depend on the client to identify which service is required. The practitioner needs to explain the differences and to determine the appropriate service(s).

Determining which service(s) to provide may not be clear-cut. Unless practitioners understand the differences between attest and management advisory services, they may unintentionally propose or conduct an engagement that involves an attest service without recognizing that they need to apply different professional standards in accordance with the Statements on Standards for Attestation Engagements.

A requirement to perform an attest service can result when there is a need to provide an appropriate level of assurance on a specific written assertion,

1 Practitioner is defined in Statement on Standards for Attestation Engagements (SSAE) Attestation Standards (New York: AICPA, 1986) to include a proprietor, partner, or shareholder in a public accounting firm and any full-time or part-tim e employee of a public accounting firm, whether certified or not.

1

whether it is a client’s or another party’s assertion. The attest service will incorporate certain formalized elements not appropriate or required for management advisory services.

This report is intended to help practitioners identify the type of service needed and to comprehend, select, and apply the appropriate professional standards. It does not expand or interpret the binding professional standards for attest engagements or MAS engagements. Practitioners should understand the Statements on Standards for Attestation Engagements and the Statement on Standards for Accountants’ Services on Prospective Financial Information as well as the Statements on Standards for Management Advisory Services.

This report includes—

• A narrative discussing key attributes of attestation engagements that differ from management advisory services.

• A comparison of MAS and attestation standards (appendix A).• A flowchart that can aid in determining the applicability of MAS, attest, or

other standards (appendix B).• Examples of MAS and attest engagements to illustrate the decision-making

process delineated in the flowchart (appendix G).• An example of an engagement letter to illustrate an attest service to be

performed as part of an overall MAS engagement (appendix D).

2

Attributes of Attestation Services

A practitioner will view many of the requirements established by SSAEAttestation Standards as the same or similar to requirements in the profession’s general standards and the Statements on Standards for Management Advisory Services. However, an attest service introduces certain attributes that generally do not exist in management advisory services. These are discussed in the following paragraphs.

Parties InvolvedManagement advisory services generally involve two parties, the practitioner

and the client, and involve a service provided to a client by the practitioner that will benefit the client directly. The parties involved in an attest service are as follows:

• The asserter. An individual or organization that is responsible for a written declaration or set of related declarations taken as a whole (that is, assertions). The asserter may be a client or another party.

• The attester. An individual or organization that expresses a conclusion about the reliability of an assertion by another party. A practitioner may perform an attestation service on assertions concerning a broad range of subjects.

• The interested party. An individual or organization that may rely on both the assertion and the attester in judging the credibility of the assertion. The client or another party may be the interested party.

Function PerformedIn providing management advisory services, the practitioner is not an attester.

The practitioner’s findings, conclusions, and recommendations are the practitioner’s own assertions. In providing management advisory services, the practitioner may evaluate written assertions of others as part of the research leading to the practitioner s findings and recommendations.

2 See SSAE Attest Services Related to MAS Engagements (New York: AICPA, 1987), paragraph 5.

3

In providing attestation services, the practitioner expresses a conclusion about the reliability of a written assertion of another party to add credibility to the other party’s declarations. The practitioner, in effect, performs an independent examination or review and expresses a conclusion on what the asserter has stated, but he does not develop separate findings and conclusions of his own.

Criteria UsedManagement advisory services involve the practitioner’s application of gen

eral business principles, subjective experience, analysis, and inferences in developing conclusions and recommendations from observations (findings). An attest service requires formalized criteria. The practitioner considers whether the assertion is capable of reasonably consistent estimation or measurement using the criteria and whether competent persons using the same or similar measurement criteria should be able to obtain materially similar estimates or measurements.3

Engagement ReportIn an MAS report, which can be written or oral, the intent is to present the

client with the practitioner’s findings, conclusions, and recommendations. In an attestation report, which is defined as a written report in the attestation standards, the intent is to provide the client or other interested parties with a certain level of assurance about the reliability of specific written assertions. The contents of the attestation report focus on that sole purpose. Report requirements dealing with the presentation of assertions, levels of assurance, and distribution are prescribed in SSAE Attestation Standards.

An MAS engagement may include an attest service if the client, or the circumstance, requires the practitioner to express a conclusion about the reliability of a specific written assertion as part of the engagement.4 In such cases, due to the credibility which the practitioner’s conclusion may add, it is important that all reporting elements established in the Statements on Standards for Attestation Engagements be complied with, in keeping with the level of assurance to be provided.5 In addition, the practitioner should issue separate reports for management advisory services and attest services.6

3 See SSAE Attestation Standards, paragraph 17.

4 See SSAE Attest Services Related to MAS Engagem ents.

5 See SSAE Attestation Standards.6 See SSAE Attest Services Related to MAS Engagements, paragraph 3.

4

Conclusions

The focus of an attest service is to provide assurance on the reliability of a written assertion of another party, thus adding credibility to the written assertion. The focus of a management advisory service is to provide advice or technical assistance.

The professional requirements for an attest service differ significantly from those for a management advisory service even if one objective is similar (for example, verifying that certain software performs required functions. See appendix C, exhibit C-1.) Determining the appropriate service to provide is the practitioner’s responsibility.

The practitioner determines the type of service to provide through consultation and agreement with the client. Once established, the type of service will dictate the nature of the report to issue as well as its ultimate use. The conduct of the service provided must comply with the appropriate professional standards.

Depending on the engagement circumstances, the client may require or may voluntarily desire an attest service. In deciding whether to perform a management advisory service, an attest service, or both, the practitioner considers the following possible alternatives:

• Perform only an attest service because a written conclusion on a written assertion made by another party will be provided, the requirements of the Statements on Standards for Attestation Engagements can be met, and the practitioner believes the attest service is the appropriate service.

• Do not perform an attest service even if one is desired because the requirements established in the attestation standards cannot be met.

• Provide both attest and management advisory services (in one engagement or in separate engagements) based on the understanding with the client if the requirements of the Statements on Standards for Attestation Engagements can be met and the practitioner believes performing both services is appropriate.

• Recommend a management advisory service if the practitioner believes an attest service is not required and is not appropriate. This may be done even when a written conclusion on a written assertion is requested by the client. If the client agrees to a management advisory service, the practitioner will not provide a written conclusion on a written assertion of another party.

5

Appendices

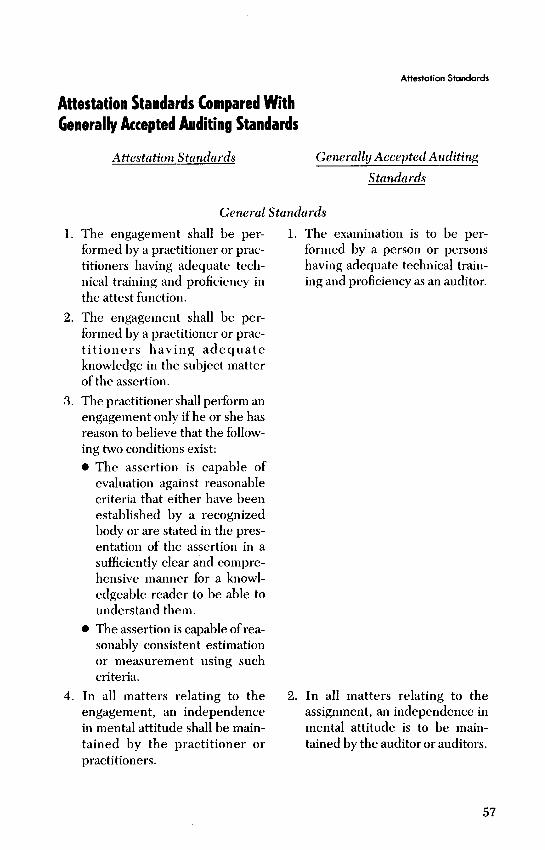

Appendix A

Comparison of Attestation Standards to MAS Standards

In differentiating between an attest service and a management advisory service, the 'practitioner needs to understand the similarities as well as the differences between attestation standards and MAS standards. Exhibit A-l facilitates a comparison of the attestation and MAS standards.

Areas o f Similarity

There are a number of important similarities between attestation standards and MAS standards. In both instances the general standards require professional competence and due professional care. They reflect the general standards in rule 201 of the AICPA’s Code of Professional Conduct, which apply to all services. The attestation standards, however, focus more specifically on proficiency in the attest function as well as adequate knowledge in the subject matter of the assertion. The two attestation standards of fieldwork that address planning and supervision of work and the sufficiency of evidential matter have very similar counterparts in the general MAS standards. However, there are differences regarding the sufficiency of evidential matter that the practitioner needs to consider.

Areas o f Difference

As the practitioner decides whether a particular engagement is an attest or MAS engagement or that an attest service is part of a larger MAS engagement, it is necessary to understand the differences in the standards to apply in each instance. First, the general attestation standards require the practitioner to be independent, whereas MAS standards specify that the practitioner need only be objective. This is an important distinction because, although independence includes objective consideration of the facts, a practitioner can be objective

8

without necessarily being independent. Second, the general attestation standards set limitations on the types of assertions that a practitioner can attest to. The classification of “assertions” is not relevant to MAS engagements. Third, MAS technical standards indicate the importance of having an oral or written understanding about the nature, scope, and limitations of the engagement and also specify the need to objectively communicate potential benefits to the client. These matters are not discussed in the attestation standards.

Attestation standards of reporting also differ from the technical standards for MAS engagements insofar as the communication of results to clients. Attestation standards of reporting specify the type of report to render to the client and require that it be in writing. MAS technical standards for communicating results, on the other hand, are much more general in nature and permit either oral or written reports.

9

Exh

ibit

A-1

Att

esta

tion

an

d M

AS

Sta

nda

rds

MA

S St

anda

rds2

Gen

eral

Sta

ndar

ds1.

Prof

essi

onal

com

pete

nce.

A m

embe

r sh

all

unde

rtake

onl

y th

ose

enga

gem

ents

whi

ch h

e or

his

firm

can

reas

onab

ly ex

pect

to

com

plet

e w

ith p

rofe

ssio

nal c

ompe

tenc

e.2.

Due

pro

fess

iona

l ca

re.

A m

embe

r sha

ll ex

erci

se d

ue p

rofe

ssi

onal

car

e in

the

perf

orm

ance

of a

n en

gage

men

t.3.

Pla

nnin

g an

d su

perv

isio

n. A

mem

ber

shal

l ade

quat

ely

plan

an

d su

perv

ise

an e

ngag

emen

t.4.

Suf

ficie

nt r

elev

ant

data

. A

mem

ber

shal

l ob

tain

suf

ficie

nt

rele

vant

dat

a to

affo

rd a

rea

sona

ble

basi

s fo

r con

clus

ions

or

reco

mm

enda

tions

in r

elat

ion

to a

n en

gage

men

t.

5. F

orec

asts

. A

mem

ber s

hall

not p

erm

it hi

s na

me

to b

e us

ed

in c

onju

nctio

n w

ith a

ny f

orec

ast

of fu

ture

tra

nsac

tions

in

a m

anne

r th

at m

ay le

ad to

the

belie

f tha

t the

mem

ber v

ouch

es

for t

he a

chie

vabi

lity

of th

e fo

reca

st.

Atte

stat

ion

Stan

dard

s1G

ener

al S

tand

ards

1. T

he e

ngag

emen

t sha

ll be

per

form

ed b

y a

prac

titio

ner o

r pra

ctit

ione

rs h

avin

g ad

equa

te te

chni

cal t

rain

ing

and

prof

icie

ncy

in th

e at

test

fun

ctio

n.2.

The

eng

agem

ent s

hall

be p

erfo

rmed

by

a pr

actit

ione

r or p

rac

titio

ners

hav

ing

adeq

uate

kno

wle

dge

in t

he s

ubje

ct m

atte

r of

the

asse

rtion

.3.

The

pra

ctiti

oner

sha

ll pe

rform

an

enga

gem

ent o

nly

if he

or

she

has

reas

on t

o be

lieve

tha

t th

e fo

llow

ing

two

cond

ition

s ex

ist:

• Th

e as

serti

on is

cap

able

of e

valu

atio

n ag

ains

t rea

sona

ble

crite

ria th

at e

ither

hav

e be

en e

stab

lishe

d by

a re

cogn

ized

bo

dy o

r ar

e st

ated

in

the

pres

enta

tion

of th

e as

serti

on i

n a

suffi

cien

tly c

lear

and

com

preh

ensiv

e m

anne

r for

a kn

owl

edge

able

rea

der

to b

e ab

le to

und

erst

and

them

.•

The

asse

rtion

is

capa

ble

of r

easo

nabl

y co

nsis

tent

est

im

atio

n or

mea

sure

men

t us

ing

such

crit

eria

.4.

In

all

mat

ters

rel

atin

g to

the

enga

gem

ent,

an i

ndep

ende

nce

in m

enta

l atti

tude

sha

ll be

mai

ntai

ned

by th

e pr

actit

ione

r or

prac

titio

ners

.5.

D

ue p

rofe

ssio

nal c

are

shal

l be

exer

cise

d in

the

perfo

rman

ce

of th

e en

gage

men

t.

10

Tec

hnic

al S

tand

ards

1. Ro

le o

f MAS

pra

ctiti

oner

. In

per

form

ing

an M

AS e

ngag

em

ent,

an M

AS p

ract

ition

er s

houl

d no

t as

sum

e th

e ro

le o

f m

anag

emen

t or t

ake

any

posi

tions

that

mig

ht im

pair

the

MAS

pr

actit

ione

r’s o

bjec

tivity

.2.

U

nder

stan

ding

with

clie

nt.

An

oral

or w

ritte

n un

ders

tand

ing

shou

ld b

e re

ache

d w

ith t

he c

lient

con

cern

ing

the

natu

re,

scop

e, a

nd l

imita

tions

of

the

MAS

eng

agem

ent

to b

e pe

rfo

rmed

.3.

C

lient

ben

efit.

Sin

ce t

he p

oten

tial

bene

fits

to b

e de

rived

by

the

clie

nt a

re a

maj

or c

onsi

dera

tion

in M

AS e

ngag

emen

ts,

such

pot

entia

l ben

efits

sho

uld

be v

iew

ed o

bjec

tivel

y an

d th

e cl

ient

sho

uld

be n

otifi

ed o

f res

erva

tions

reg

ardi

ng th

em.

In

offe

ring

and

prov

idin

g M

AS e

ngag

emen

ts, r

esul

ts s

houl

d no

t be

exp

licitl

y or

im

plic

itly

guar

ante

ed.

Whe

n es

timat

es o

f qu

antif

iabl

e re

sults

are

pre

sent

ed,

they

sho

uld

be c

lear

ly

iden

tifie

d as

est

imat

es a

nd t

he s

uppo

rt fo

r su

ch e

stim

ates

sh

ould

be

disc

lose

d.4.

C

omm

unic

atio

n of

resu

lts.

Sign

ifica

nt i

nfor

mat

ion

perti

nent

to

the

res

ults

of

an M

AS e

ngag

emen

t, to

geth

er w

ith a

ny

limita

tions

, qu

alifi

catio

ns,

or r

eser

vatio

ns n

eede

d to

ass

ist

the

clie

nt i

n m

akin

g its

dec

isio

n, s

houl

d be

com

mun

icat

ed

to th

e cl

ient

ora

lly o

r in

writ

ing.

Stan

dard

s of

Fie

ldw

ork

1. T

he w

ork

shal

l be

adeq

uate

ly p

lann

ed a

nd a

ssis

tant

s, if

any,

sh

all

be p

rope

rly s

uper

vise

d.2.

Su

ffici

ent e

vide

nce

shal

l be

obta

ined

to p

rovi

de a

reas

onab

le

basi

s fo

r the

con

clus

ion

that

is e

xpre

ssed

in th

e re

port.

Stan

dard

s of

Rep

ortin

g

1. T

he r

epor

t sha

ll id

entif

y th

e as

serti

on b

eing

repo

rted

on a

nd

stat

e th

e ch

arac

ter

of th

e en

gage

men

t.2.

The

rep

ort

shal

l st

ate

the

prac

titio

ner’s

con

clus

ion

abou

t w

heth

er t

he a

sser

tion

is pr

esen

ted

in c

onfo

rmity

with

the

es

tabl

ishe

d or

stat

ed c

riter

ia a

gain

st w

hich

it w

as m

easu

red.

3. T

he r

epor

t sh

all

stat

e al

l of

the

pra

ctiti

oner

’s sig

nific

ant

rese

rvat

ions

abo

ut t

he e

ngag

emen

t an

d th

e pr

esen

tatio

n of

th

e as

serti

on.

4. T

he r

epor

t on

an

enga

gem

ent

to e

valu

ate

an a

sser

tion

that

ha

s be

en p

repa

red

in c

onfo

rmity

with

agr

eed-

upon

crit

eria

or

on

an e

ngag

emen

t to

appl

y ag

reed

-upo

n pr

oced

ures

sho

uld

cont

ain

a st

atem

ent l

imiti

ng it

s us

e to

the

parti

es w

ho h

ave

agre

ed u

pon

such

crit

eria

or

proc

edur

es.

1 St

atem

ent

on S

tand

ards

for

Atte

stat

ion

Eng

agem

ents

, A

ttest

atio

n St

anda

rds

(New

Yor

k: A

ICPA

, 19

86).

2 St

atem

ent

on S

tand

ards

for

Man

agem

ent

Adv

isor

y Se

rvic

es N

o. 1

, D

efin

ition

s an

d St

anda

rds

for

MA

S P

ract

ice

(New

Yor

k: A

ICPA

, 19

81).

11

Appendix B

Decision Alternatives Flowchart

The decision alternatives flowchart is designed to assist practitioners in identifying when an attest service, a management advisory service, or both may be appropriate for a specific client situation. Other factors not included in the flowchart may influence the final decision.

12

Practitioner and client discuss work that is not audit, review, compilation, or tax compliance.

1. Does the anticipated work involve a review of a written assertion* of the client or another party?

2. Does the client appear to either want or need a written assurance on the reliability of the assertion as part of the practitioner’s report?

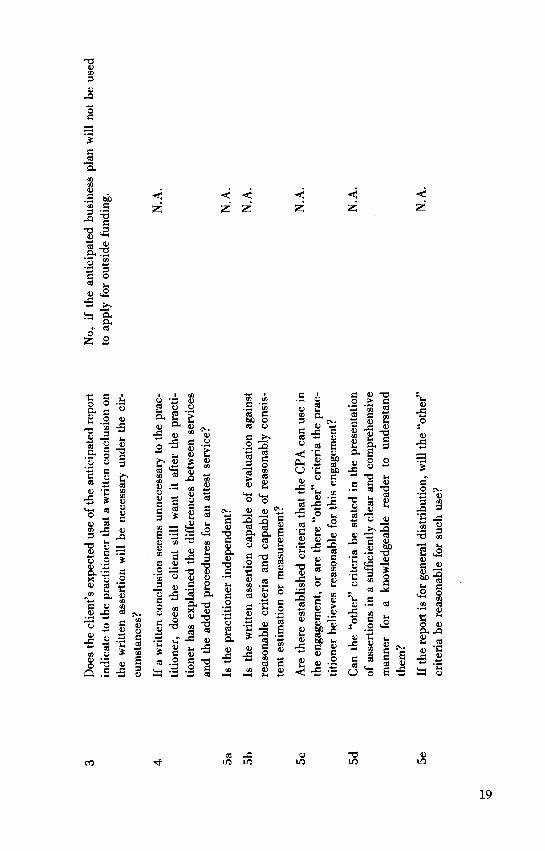

3. Does the client's expected use of the anticipated report indicate to the practitioner that a written conclusion on the written assertion will be necessary under the circumstances?

4. If a written conclusion seems unnecessary to the practitioner, does the client still want it after the practitioner has explained the differences between services and the added procedures for an attest service?

5. Does it appear that all the following attestation engagement requirements can be met?

a. Practitioner is independent.

b. The written assertion is capable of evaluation against reasonable criteria and capable of reasonably consistent estimation or measurement.

c. There are established criteria that the CPA can use in the engagement or “ other” criteria the practitioner believes are reasonable for this engagement.

d. The “ other” criteria can be stated in a presentation of assertions in a sufficiently clear and comprehensive manner for a knowledgeable reader to understand them.

e. If the report is for general distribution, the “ other” criteria will be reasonable for such use.

Attest services in accordance with the SSAE appear to be appropriate.

Attest services do not appear to be appropriate. MAS standards may apply

to other services.

Written assertions that are forecasts or projections as defined in the Statements on Standards for Accountants’ Services on Prospective Financial Information are covered by those standards and are excluded here.

13

Appendix C

Engagement Examples

The following four examples illustrate various engagement situations in which the practitioner performs either a management advisory service, an attestation service, or both.

Example 1, a software-related engagement, illustrates a situation in which the practitioner performs an attestation service by providing an appropriate level of assurance on a specific written assertion made by another party (the XYZ Software Development Corporation). Interested third parties (tax practitioners) may rely on this assertion and attestation.

Example 2, a business plan development engagement, illustrates a situation in which the practitioner initially performs a management advisory service and then provides a follow-up attest service. In the initial management advisory service, the CPA practitioner assists in gathering and analyzing financial data and developing the business plan, but the practitioner does not examine or review any evidence supporting the information furnished by Atlas Manufacturing Corporation and will not express any conclusion on its reliability.

The follow-up engagement (the presentation of a business plan to the bank) introduces a third party that will rely on the projected financial statements; therefore, the Statement on Standards for Accountants’ Services on Prospective Financial Information applies to them. A business plan development engagement can also involve an attest service if the practitioner is asked to provide a written conclusion about certain specific elements of the plan for which there are criteria and sufficient relevant data (for example, production and sales data for the previous five years).

The third example, a health care consulting engagement, illustrates a situation in which the practitioner performs both an attestation service and a management advisory service. The first part of the engagement involves an attestation service since the practitioner is required to provide the Authority with a written conclusion on a written assertion by another party (ABC Hospital) that the terms of the covenants would be met by the hospital’s performance. In the second part of the engagement, the practitioner provides consulting advice to the hospital about whether to include the covenants in the bond indenture agreement.

The final example, a computer feasibility and installation engagement, illustrates a situation in which the practitioner performs a management advisory service to help select and install a computer system and appropriate software. This case, however, introduces the possibility of the practitioner also performing an attestation service by providing written assurance that the payroll package

14

eventually selected will perform according to the vendor’s representations. Since the use of the attestation report would be internal, for the client’s use only, and the practitioner could address the client’s concern without providing a written conclusion, preparing an attestation report is based on the client’s election to proceed subsequent to the practitioner’s explanation of added professional requirements entailing added costs.

15

Exh

ibit

C-1

Sof

twar

e E

nga

gem

ent

The

XYZ

Softw

are

Dev

elop

men

t Cor

pora

tion

(her

eina

fter r

efer

red

to a

s X

YZ)

has

dev

elop

ed a

sof

twar

e pa

ckag

e to

com

plet

e Fe

dera

l Tax

Ret

urn

Form

104

0. T

he p

acka

ge i

ncor

pora

tes

the

mos

t rec

ent

chan

ges

in t

he t

ax l

aws.

XY

Z ha

s pr

epar

ed a

dra

ft of

a p

rodu

ct i

nfor

mat

ion

broc

hure

and

a d

emon

stra

tion

disk

th

at i

t wi

ll ev

entu

ally

sen

d to

acc

ount

ing

firm

s in

eve

ry s

tate

, re

gard

less

of s

ize,

as

wel

l as

to th

e m

ajor

ta

x re

turn

pre

para

tion

serv

ices

. Be

fore

com

plet

ing

the

broc

hure

, how

ever

, XY

Z ha

s en

gage

d Sm

ith, J

ones

an

d St

amps

, CP

As,

a m

ajor

acc

ount

ing

and

cons

ultin

g fir

m h

ighl

y re

gard

ed t

hrou

ghou

t th

e in

dust

ry a

s ta

x sp

ecia

lists

. Sm

ith, J

ones

and

Sta

mps

will

com

pare

the

perf

orm

ance

of t

he p

acka

ge to

XY

Z’s

asse

rtion

s m

ade

abou

t it

in t

he b

roch

ure

and

will

rep

ort

the

conc

lusi

ons.

The

firm

exp

lain

ed t

o X

YZ

man

agem

ent

that

the

repo

rt w

ould

not

incl

ude

a w

arra

nty

of p

rogr

am p

erfo

rman

ce a

s pa

rt of

the

conc

lusi

ons.

The

firm

’s re

port

will

be

incl

uded

in

the

broc

hure

.Th

e ex

ampl

e fo

llow

s th

e flo

wch

art (

from

the

appe

ndix

B p

roto

type

) to

illu

stra

te w

hy th

is e

ngag

emen

t is

an a

ppro

pria

te a

ttest

atio

n se

rvic

e.

Dec

ision

Yes

.

Yes

.

Yes

. The

repo

rt to

be

repr

oduc

ed in

the

broc

hure

wou

ld

cont

ain

writ

ten

conc

lusi

ons a

bout

the

writ

ten

asse

rtion

s of

XY

Z as

the

y ap

pear

in t

he s

oftw

are

prod

uct

info

rm

atio

n br

ochu

re.

The

repo

rt is

clea

rly th

e pu

rpos

e fo

r w

hich

the

clie

nt i

s en

gagi

ng th

e CP

A.

An

MAS

repo

rt

Step

Cr

iteria

1 D

oes

the

antic

ipat

ed w

ork

invo

lve

a re

view

of a

writ

ten

asse

rtion

of t

he c

lient

or

anot

her p

arty

?

2 D

oes

the

clie

nt a

ppea

r to

eith

er w

ant o

r nee

d a

writ

ten

assu

ranc

e on

the

rel

iabi

lity

of th

e as

serti

on a

s pa

rt of

th

e pr

actit

ione

r’s r

epor

t?3

Doe

s th

e cl

ient

’s ex

pect

ed u

se o

f the

ant

icip

ated

repo

rt in

dica

te to

the

prac

titio

ner t

hat a

writ

ten

conc

lusi

on o

n th

e w

ritte

n as

serti

on w

ill b

e ne

cess

ary

unde

r th

e ci

rcu

mst

ance

s?

16

cont

aini

ng t

he r

esul

ts o

f the

fie

ld t

ests

and

the

CPA

’s fin

ding

s an

d co

nclu

sion

s w

ould

not

be

suffi

cien

t for

the

clie

nt.

N.A

.

Ass

umed

to b

e ye

s in

this

cas

e.

Yes

, in

this

cas

e. T

he p

ract

ition

er d

eter

min

es w

heth

er

the

clai

ms

mad

e by

the

clie

nt i

n th

e br

ochu

re c

an b

e ev

alua

ted

unde

r th

e re

quire

men

ts s

et f

orth

in

the

at

test

atio

n st

anda

rds.

If ye

s, th

e se

rvic

e m

ay b

e pro

vide

d.

If n

ot,

the

atte

st s

ervi

ce m

ay n

ot b

e pe

rform

ed (

that

is,

the

CPA

can

not

issu

e a

repo

rt fo

r us

e in

the

bro

ch

ure)

.

Yes

, in

thi

s ca

se t

here

are

est

ablis

hed

crite

ria.

The

term

gen

eral

ly r

efer

s to

sta

ndar

ds s

et b

y a

regu

lato

ry

agen

cy o

r a p

rofe

ssio

nal b

ody

usin

g du

e pr

oces

s, su

ch

as A

ICPA

sta

ndar

ds.

In th

is c

ase,

IRS

regu

latio

ns p

ro

vide

the

crit

eria

.N

.A.

The

IRS

code

s ne

ed n

ot b

e st

ated

sin

ce th

ey a

re

esta

blis

hed

crite

ria.

N.A

.

4 If

a w

ritte

n co

nclu

sion

seem

s un

nece

ssar

y to

the

prac

tit

ione

r, do

es t

he c

lient

stil

l w

ant

it af

ter

the

prac

titio

ner

has

expl

aine

d th

e di

ffere

nces

bet

wee

n se

rvic

es

and

the

adde

d pr

oced

ures

for

an

atte

st s

ervi

ce?

5a

Is th

e pr

actit

ione

r in

depe

nden

t?

5b

Is th

e w

ritte

n as

serti

on c

apab

le o

f eva

luat

ion

agai

nst

reas

onab

le c

riter

ia a

nd c

apab

le o

f rea

sona

bly

cons

is

tent

esti

mat

ion

or m

easu

rem

ent?

5c

Are

ther

e es

tabl

ishe

d cr

iteria

that

the

CPA

can

use

inth

e en

gage

men

t, or

are

ther

e “o

ther

” cr

iteria

the

prac

tit

ione

r be

lieve

s re

ason

able

for t

his

enga

gem

ent?

5d

Can

the

“oth

er”

crite

ria b

e st

ated

in

the

pres

enta

tion

of a

sser

tions

in

a su

ffici

ently

cle

ar a

nd c

ompr

ehen

sive

man

ner

for

a kn

owle

dgea

ble

read

er t

o un

ders

tand

th

em?

5e

If th

e re

port

is fo

r gen

eral

dis

tribu

tion,

will

the

“oth

er”

crite

ria b

e re

ason

able

for

suc

h us

e?

17

Exh

ibit

C-2

Bu

sin

ess

Pla

n D

evel

op

men

t E

nga

gem

ent

The

clos

ely

held

Atla

s M

anuf

actu

ring

Corp

orat

ion

mak

es la

dies

’ han

dbag

s, w

alle

ts,

and

othe

r per

sona

l ac

cess

orie

s. Th

e ow

ner,

awar

e th

at h

e is

havi

ng c

ash

prob

lem

s, ha

s as

ked

CPA

Geo

rge

Han

over

for h

elp.

H

anov

er h

as a

dvis

ed t

he o

wne

r th

at c

ash

prob

lem

s ca

n of

ten

be c

orre

cted

thr

ough

a c

ombi

natio

n of

bu

dget

s, ca

sh m

anag

emen

t, an

d ou

tsid

e fin

anci

ng.

How

ever

, it

is ne

cess

ary

to d

evel

op a

bus

ines

s pl

an

to d

eter

min

e w

hat

furth

er a

ctio

ns a

re n

eede

d. T

he o

wne

r has

eng

aged

Han

over

to a

ssis

t in

dev

elop

ing

a bu

sine

ss p

lan

for

inte

rnal

use

, in

clud

ing

a fo

reca

st or

pro

ject

ion.

The

ow

ner

has

also

ask

ed H

anov

er to

as

sist

him

in

pres

entin

g th

e bu

sine

ss p

lan

to t

he b

ank

to s

ecur

e ou

tsid

e fin

anci

ng i

f it

is ne

eded

. Th

is

will

req

uire

a w

ritte

n re

port

by th

e CP

A f

or b

ank

use.

The

exam

ple

follo

ws

the

flow

char

t (fro

m th

e ap

pend

ix B

pro

toty

pe)

to il

lust

rate

why

the

enga

gem

ent i

s an

MAS

ser

vice

(pa

rt 1)

, an

d it

conf

irms

that

ano

ther

ser

vice

rel

ated

to p

rosp

ectiv

e fin

anci

al i

nfor

mat

ion

exis

ts,

as w

ell

as a

pos

sibili

ty o

f an

atte

st s

ervi

ce li

mite

d to

ele

men

ts o

f the

bus

ines

s pl

an (

part

2).

The

atte

st s

ervi

ce (

part

2) w

ould

follo

w th

e m

anag

emen

t adv

isory

ser

vice

onl

y if

the

clie

nt’s

plan

is s

ubm

itted

to

a b

ank

to o

btai

n fu

nds.

Part

1

Initi

al E

ngag

emen

t — B

usin

ess

Plan

Dev

elop

men

t

Step

C

rite

ria

Dec

isio

n

1 D

oes

the

antic

ipat

ed w

ork

invo

lve

a re

view

of a

writ

ten

No.

asse

rtion

of t

he c

lient

or

anot

her

party

?

2 D

oes

the

clie

nt a

ppea

r to

eith

er w

ant o

r nee

d a

writ

ten

No.

assu

ranc

e on

the

rel

iabi

lity

of th

e as

serti

on a

s pa

rt of

the

prac

titio

ner’s

rep

ort?

18

No,

if

the

antic

ipat

ed b

usin

ess

plan

will

not

be

used

to

app

ly f

or o

utsi

de f

undi

ng.

N.A

.

N.A

.N

.A.

N.A

.

N.A

.

N.A

.

3 D

oes

the

clie

nt’s

expe

cted

use

of t

he a

ntic

ipat

ed re

port

indi

cate

to th

e pr

actit

ione

r tha

t a w

ritte

n co

nclu

sion

on

the

writ

ten

asse

rtion

will

be

nece

ssar

y un

der

the

cir

cum

stan

ces?

4 If

a w

ritte

n co

nclu

sion

seem

s un

nece

ssar

y to

the

prac

tit

ione

r, do

es t

he c

lient

stil

l w

ant

it af

ter

the

prac

titio

ner

has

expl

aine

d th

e di

ffere

nces

bet

wee

n se

rvic

es

and

the

adde

d pr

oced

ures

for

an

atte

st s

ervi

ce?

5a

Is th

e pr

actit

ione

r in

depe

nden

t?5b

Is

the

writ

ten

asse

rtion

cap

able

of e

valu

atio

n ag

ains

tre

ason

able

crit

eria

and

cap

able

of r

easo

nabl

y co

nsis

te

nt e

stim

atio

n or

mea

sure

men

t?

5c

Are

the

re e

stab

lishe

d cr

iteria

that

the

CPA

can

use

inth

e en

gage

men

t, or

are

ther

e “o

ther

” cr

iteria

the

prac

tit

ione

r be

lieve

s re

ason

able

for

this

eng

agem

ent?

5d

Can

the

“oth

er”

crite

ria b

e st

ated

in

the

pres

enta

tion

of a

sser

tions

in a

suf

ficie

ntly

cle

ar a

nd c

ompr

ehen

sive

man

ner

for

a kn

owle

dgea

ble

read

er t

o un

ders

tand

th

em?

5e

If th

e re

port

is fo

r gen

eral

dis

tribu

tion,

will

the

“oth

er”

crite

ria b

e re

ason

able

for s

uch

use?

19

Exh

ibit

C-2

: B

usin

ess

Plan

Dev

elop

men

t E

ngag

emen

tC

ontin

ued

from

pag

e 19

Part

2

Follo

w-u

p En

gage

men

t — P

rese

ntat

ion

of B

usin

ess

Plan

to O

btai

n Fi

nanc

ing

Dec

ision

Yes

. A

third

-par

ty u

ser

of t

he b

usin

ess

plan

is

now

invo

lved

, an

d th

e St

atem

ent o

n St

anda

rds

for A

ccou

nt

ants

’ Ser

vice

s on

Pro

spec

tive

Fina

ncia

l Inf

orm

atio

n ap

pl

ies

sinc

e a

clie

nt f

orec

ast o

r pr

ojec

tion

is in

clud

ed.

If t

he p

ract

ition

er i

s al

so r

eque

sted

to

atte

st t

o ot

her

data

in

the

plan

, th

e fo

llow

ing

ques

tions

wou

ld h

ave

to b

e co

nsid

ered

.

Yes

.

Yes

. In

thi

s en

gage

men

t th

e pr

actit

ione

r is

aske

d to

at

test

to s

peci

fic q

uant

ifiab

le h

isto

rical

ele

men

ts of

the

busi

ness

pla

n (fo

r ex

ampl

e, p

rodu

ctio

n or

sal

es d

ata

for t

he p

ast f

ive

year

s). T

he p

ract

ition

er m

ust m

eet t

he

stan

dard

s fo

r evi

dent

ial m

atte

r. H

e ca

nnot

atte

st to

the

achi

evab

ility

of f

utur

e re

sults

.

Step

Cr

iteria

1 D

oes

the

antic

ipat

ed w

ork

invo

lve

a re

view

of a

writ

ten

asse

rtion

of a

clie

nt o

r an

othe

r pa

rty?

2 D

oes

the

clie

nt a

ppea

r to

eith

er w

ant o

r nee

d a

writ

ten

assu

ranc

e on

the

rel

iabi

lity

of th

e as

serti

on a

s pa

rt of

th

e pr

actit

ione

r’s r

epor

t?3

Doe

s th

e cl

ient

’s ex

pect

ed u

se o

f the

ant

icip

ated

repo

rt in

dica

te to

the

prac

titio

ner t

hat a

writ

ten

conc

lusi

on o

n th

e w

ritte

n as

serti

on w

ill b

e ne

cess

ary

unde

r th

e ci

rcu

msta

nces

?

20

N.A

.

Ass

umed

to b

e ye

s in

thi

s ca

se.

Ass

umed

to

be y

es f

or s

peci

fic e

lem

ent(s

) se

lect

ed fo

r th

e at

test

ser

vice

.

Ass

umed

to

be y

es f

or s

peci

fic e

lem

ent(s

) se

lect

ed fo

r th

e at

test

ser

vice

.

Ass

umed

to

be y

es f

or s

peci

fic e

lem

ent(s

) se

lect

ed fo

r th

e at

test

ser

vice

.

N.A

. U

se b

y th

e ba

nk is

a li

mite

d di

strib

utio

n re

quiri

ng

the

bank

’s ag

reem

ent t

o th

e cr

iteria

.

4 If

a w

ritte

n co

nclu

sion

see

ms

unne

cess

ary

to th

e pr

ac

titio

ner,

does

the

clie

nt s

till

wan

t it

afte

r th

e pr

acti

tione

r ha

s ex

plai

ned

the

diffe

renc

es b

etw

een

serv

ices

an

d th

e ad

ded

proc

edur

es f

or a

n at

test

ser

vice

?

5a

Is th

e pr

actit

ione

r in

depe

nden

t?5b

Is

the

writ

ten

asse

rtion

cap

able

of

eval

uatio

n ag

ains

tre

ason

able

crit

eria

and

cap

able

of r

easo

nabl

y co

nsis

te

nt e

stim

atio

n or

mea

sure

men

t?

5c

Are

ther

e es

tabl

ishe

d cr

iteria

that

the

CPA

can

use

inth

e en

gage

men

t, or

are

ther

e “o

ther

” cr

iteria

the

prac

tit

ione

r be

lieve

s re

ason

able

for

this

eng

agem

ent?

5d

Can

the

“oth

er”

crite

ria b

e st

ated

in

the

pres

enta

tion

of a

sser

tions

in a

suf

ficie

ntly

cle

ar a

nd c

ompr

ehen

sive

m

anne

r fo

r a

know

ledg

eabl

e re

ader

to

unde

rsta

nd

them

?5e

If

the

repo

rt is

for g

ener

al d

istri

butio

n, w

ill th

e “o

ther

”cr

iteria

be

reas

onab

le f

or s

uch

use?

21

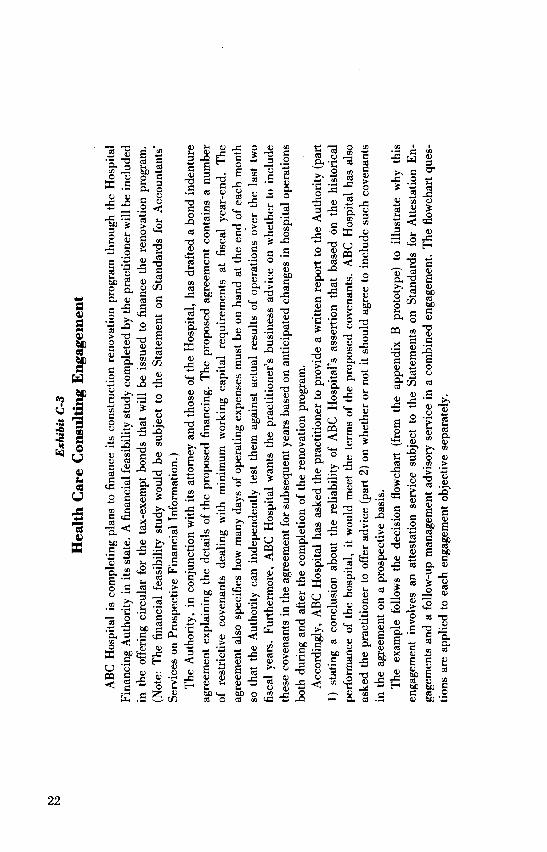

Exh

ibit

C-3

Hea

lth

Car

e C

onsu

ltin

g E

nga

gem

ent

ABC

Hos

pita

l is

com

plet

ing

plan

s to

fin

ance

its

cons

truct

ion

reno

vatio

n pr

ogra

m th

roug

h th

e H

ospi

tal

Fina

ncin

g A

utho

rity

in it

s sta

te. A

fina

ncia

l fea

sibili

ty s

tudy

com

plet

ed b

y th

e pr

actit

ione

r will

be

incl

uded

in

the

offe

ring

circ

ular

for

the

tax-

exem

pt b

onds

tha

t w

ill b

e is

sued

to

finan

ce t

he r

enov

atio

n pr

ogra

m.

(Not

e: T

he f

inan

cial

fea

sibili

ty s

tudy

wou

ld b

e su

bjec

t to

the

Sta

tem

ent

on S

tand

ards

for

Acc

ount

ants

’ Se

rvic

es o

n Pr

ospe

ctiv

e Fi

nanc

ial I

nfor

mat

ion.

)Th

e A

utho

rity,

in

conj

unct

ion

with

its

atto

rney

and

thos

e of

the

Hos

pita

l, ha

s dr

afte

d a

bond

inde

ntur

e ag

reem

ent

expl

aini

ng t

he d

etai

ls o

f the

pro

pose

d fin

anci

ng.

The

prop

osed

agr

eem

ent

cont

ains

a n

umbe

r of

res

trict

ive

cove

nant

s de

alin

g w

ith m

inim

um w

orki

ng c

apita

l re

quire

men

ts a

t fis

cal

year

-end

. Th

e ag

reem

ent a

lso s

peci

fies

how

man

y da

ys o

f ope

ratin

g ex

pens

es m

ust b

e on

han

d at

the

end

of e

ach

mon

th

so t

hat

the

Aut

horit

y ca

n in

depe

nden

tly t

est

them

aga

inst

act

ual

resu

lts o

f op

erat

ions

ove

r th

e la

st t

wo

fisca

l ye

ars.

Furth

erm

ore,

ABC

Hos

pita

l w

ants

the

prac

titio

ner’s

bus

ines

s ad

vice

on

whe

ther

to i

nclu

de

thes

e co

vena

nts

in th

e ag

reem

ent f

or s

ubse

quen

t yea

rs b

ased

on

antic

ipat

ed c

hang

es in

hos

pita

l ope

ratio

ns

both

dur

ing

and

afte

r th

e co

mpl

etio

n of

the

reno

vatio

n pr

ogra

m.

Acc

ordi

ngly

, AB

C H

ospi

tal

has

aske

d th

e pr

actit

ione

r to

prov

ide

a w

ritte

n re

port

to th

e A

utho

rity

(par

t 1)

sta

ting

a co

nclu

sion

abo

ut t

he r

elia

bilit

y of

ABC

Hos

pita

l’s a

sser

tion

that

bas

ed o

n th

e hi

stor

ical

pe

rform

ance

of

the

hosp

ital,

it w

ould

mee

t the

ter

ms

of th

e pr

opos

ed c

oven

ants

. A

BC H

ospi

tal

has

also

as

ked

the

prac

titio

ner

to o

ffer a

dvic

e (p

art 2

) on

whe

ther

or n

ot it

sho

uld

agre

e to

incl

ude

such

cov

enan

ts

in th

e ag

reem

ent o

n a

pros

pect

ive

basi

s.Th

e ex

ampl

e fo

llow

s th

e de

cisi

on f

low

char

t (fr

om t

he a

ppen

dix

B pr

otot

ype)

to

illus

trate

why

thi

s en

gage

men

t in

volv

es a

n at

test

atio

n se

rvic

e su

bjec

t to

the

Sta

tem

ents

on

Stan

dard

s fo

r A

ttest

atio

n En

ga

gem

ents

and

a fo

llow

-up

man

agem

ent a

dviso

ry s

ervi

ce in

a c

ombi

ned

enga

gem

ent.

The

flow

char

t que

stio

ns a

re a

pplie

d to

eac

h en

gage

men

t obj

ectiv

e se

para

tely

.

22

Dec

isio

n___

__Pa

rt 2

Incl

usio

n of

Cov

enan

ts in

Agr

eem

ent

(Man

agem

ent A

dvis

ory

Serv

ice)

No.

No.

Adv

ice

is re

ques

ted

on w

heth

er

or n

ot t

he h

ospi

tal

shou

ld a

gree

to

the

cove

nant

s.

N.A

.

N.A

.

(Con

tinue

d on

nex

t pag

e)

Part

1H

isto

rical

Ana

lysi

s (A

ttest

atio

n Se

rvic

e)

Yes

.

Yes

. Th

e ho

spita

l has

req

uest

ed th

e pr

actit

ione

r to

pro

vide

a le

tter t

o th

e A

utho

rity.

Yes

.

N.A

.

Step

Cr

iteria

1 D

oes

the

antic

ipat

ed w

ork

invo

lve

a re

view

of

a w

ritte

n as

serti

on o

f a

clie

nt o

r an

othe

r pa

rty?

2 D

oes

the

clie

nt a

ppea

r to

eith

er w

ant

or n

eed

a w

ritte

n as

sura

nce

on t

he

relia

bilit

y of

the

asse

rtion

as

part

of

the

prac

titio

ner’s

rep

ort?

3 Do

es th

e cl

ient

’s ex

pect

ed u

se o

f the

an

ticip

ated

re

port

indi

cate

to

th

e pr

actit

ione

r tha

t a w

ritte

n co

nclu

sion

on th

e w

ritte

n as

serti

on w

ill b

e ne

ces

sary

und

er th

e ci

rcum

stan

ces?

4 If

a w

ritte

n co

nclu

sion

seem

s un

ne

cess

ary

to t

he p

ract

ition

er,

does

th

e cl

ient

stil

l wan

t it a

fter t

he p

rac

titio

ner h

as e

xpla

ined

the

diffe

renc

es

betw

een

serv

ices

and

the

adde

d pr

oce

dure

s fo

r an

atte

st s

ervi

ce?

23

Part

2In

clus

ion

of C

oven

ants

in A

gree

men

t(M

anag

emen

t Adv

isor

y Se

rvic

e)

N.A

.N

.A.

N.A

.

N.A

.

N.A

.

Exh

ibit

C-3

: H

ealth

Car

e C

onsu

lting

Eng

agem

ent

Con

tinue

d fr

om p

age

23

____

____

____

__

Dec

isio

n

Part

1H

isto

rical

Ana

lysi

s (A

ttest

atio

n Se

rvic

e)

Ass

umed

to b

e ye

s in

this

cas

e.Y

es. T

he c

oven

ants

are

spe

cific

and

hi

stor

ical

dat

a ex

ist t

o te

st th

em.

Yes

. Th

e pr

opos

ed

cove

nant

s in

cl

ude

the

crite

ria. Yes

.

Yes

.

Step

Cr

iteria

5a

Is th

e pr

actit

ione

r in

depe

nden

t?5b

Is

the

writ

ten

asse

rtion

cap

able

of

eval

uatio

n ag

ains

t re

ason

able

crit

eria

and

cap

able

of

reas

onab

ly c

on

sist

ent e

stim

atio

n or

mea

sure

men

t?

5c

Are

the

re e

stab

lishe

d cr

iteria

tha

tth

e CP

A c

an u

se in

the

enga

gem

ent,

or a

re th

ere

“oth

er”

crite

ria th

e pr

ac

titio

ner

belie

ves

reas

onab

le f

or t

his

enga

gem

ent?

5d

Can

the

“oth

er”

crite

ria b

e st

ated

inth

e pr

esen

tatio

n of

ass

ertio

ns i

n a

suffi

cien

tly c

lear

and

com

preh

ensiv

e m

anne

r fo

r a

know

ledg

eabl

e re

ader

to

und

erst

and

them

?

5e

If th

e re

port

is fo

r ge

nera

l di

strib

utio

n, w

ill th

e “o

ther

” cr

iteria

be

rea

sona

ble

for s

uch

use?

24

Exh

ibit

C-4

Com

pu

ter

Fea

sibi

lity

an

d In

stal

lati

on E

nga

gem

ent

The

clie

nt h

as r

eque

sted

the

prac

titio

ner’s

ass

ista

nce

with

com

pute

r sy

stem

sel

ectio

n an

d in

stal

latio

n.

The

orig

inal

eng

agem

ent o

bjec

tives

wer

e to

do

the

follo

win

g:

• St

udy

the

feas

ibili

ty o

f the

com

pute

r sy

stem

.•

Hel

p pr

epar

e th

e cl

ient

’s re

ques

ts fo

r pro

posa

ls on

app

ropr

iate

sof

twar

e an

d ha

rdw

are

from

ven

dors

.•

Inst

all t

he c

hose

n sy

stem

.

No c

oncl

usio

ns o

n w

ritte

n as

serti

ons

wer

e re

quire

d fo

r th

is M

AS e

ngag

emen

t.As

the

clie

nt r

ecei

ves

the

vend

ors’

writ

ten

prop

osal

s, he

info

rms t

he p

ract

ition

er th

at h

e ha

s ex

perie

nced

m

any

prob

lem

s w

ith t

he e

xist

ing

payr

oll

syste

m a

nd r

elat

ed m

ultij

uris

dict

ion

tax

with

hold

ing.

He

stat

es

that

bef

ore

he p

urch

ases

and

ins

talls

any

sys

tem

, he

wan

ts th

e pr

actit

ione

r’s w

ritte

n as

sura

nce

that

the

so

ftwar

e ch

osen

can

per

form

pay

roll

calc

ulat

ions

and

mul

tijur

isdi

ctio

n w

ithho

ldin

g as

ass

erte

d by

the

se

lect

ed v

endo

r in

his

writ

ten

prop

osal

.Th

is re

ques

t is

an e

xpan

sion

of t

he o

rigin

al e

ngag

emen

t. Si

nce

a w

ritte

n as

serti

on o

f ano

ther

par

ty i

s in

volv

ed,

it m

ay o

r m

ay n

ot r

equi

re a

n at

test

atio

n. T

he e

xam

ple

follo

ws

the

deci

sion

flo

wch

art (

from

the

appe

ndix

B p

roto

type

) to

illus

trate

why

this

eng

agem

ent i

s an

atte

stat

ion

serv

ice

with

in a

n M

AS e

ngag

emen

t an

d ho

w th

e pr

actit

ione

r co

uld

have

arr

ived

at d

iffer

ent c

oncl

usio

ns d

epen

ding

on

the

deci

sion

mad

e by

th

e cl

ient

at s

tep

4 on

the

flow

char

t.(C

ontin

ued

on n

ext p

age)

25

Dec

ision

Yes

.

Yes

. The

clie

nt h

as re

ques

ted

the

CPA

to p

rovi

de w

rit

ten

assu

ranc

e on

a v

endo

r ass

ertio

n co

ncer

ning

pay

roll

and

mul

tijur

isdi

ctio

n w

ithho

ldin

g pr

oces

sing

.

No.

An

atte

st s

ervi

ce i

s no

t re

quire

d, b

ut t

he c

lient

ha

s re

ques

ted

it. T

he p

ract

ition

er s

houl

d ex

plai

n th

e di

ffer

ence

bet

wee

n th

e m

anag

emen

t ad

viso

ry s

ervi

ce

and

the

atte

st s

ervi

ce,

incl

udin

g th

e ad

ded

proc

edur

es

enta

iling

add

ition

al e

xpen

se to

the

clie

nt.

Yes

. If

the

clie

nt s

till d

esire

s a

writ

ten

conc

lusi

on o

n th

e ve

ndor

’s as

serti

on,

the

prac

titio

ner

may

pro

ceed

. If

not

, th

e pr

actit

ione

r m

ay p

roce

ed w

ith t

he m

anag

em

ent

advi

sory

ser

vice

orig

inal

ly r

eque

sted

. Th

e M

AS

repo

rt sh

ould

not

inc

lude

a w

ritte

n co

nclu

sion

on

the

relia

bilit

y of

the

vend

or’s

asse

rtion

s. It

may

sta

te th

at

the

reco

mm

ende

d so

ftwar

e ap

pear

s to

mee

t the

clie

nt’s

spec

ifica

tions

if t

he p

ract

ition

er’s

rese

arch

and

test

ing

so in

dica

te. (

Not

e: T

he b

alan

ce o

f thi

s exa

mpl

e as

sum

es

the

clie

nt s

till w

ants

the

atte

stat

ion.

)

Exh

ibit

C-4

: C

ompu

ter

Feas

ibili

ty a

nd I

nsta

llatio

n E

ngag

emen

tC

ontin

ued

from

pag

e 25

Step

Cr

iteria

1 D

oes

the

antic

ipat

ed w

ork

invo

lve

a re

view

of a

writ

ten

asse

rtion

of a

clie

nt o

r ano

ther

par

ty?

2 D

oes

the

clie

nt a

ppea

r to

eith

er w

ant o

r nee

d a

writ

ten

assu

ranc

e on

the

rel

iabi

lity

of th

e as

serti

on a

s pa

rt of

th

e pr

actit

ione

r’s r

epor

t?

3 D

oes

the

clie

nt’s

expe

cted

use

of t

he a

ntic

ipat

ed re

port

indi

cate

to th

e pr

actit

ione

r tha