Embed Size (px)

Citation preview

Monetary Policy Coordination

Haizhou HUANG

The Second CF40-PIIE China Economic Forum

Washington DC

October 5, 2016

2 nd Annual CF40-PIIE China Economic Forum

US and Euro Area

Slow growth, deleveraging, financial risks and low

interest rates

2

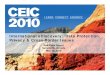

US deleverage

Source: Haver Analytics, CICC Research

40

60

80

100

120

19

90

Q1

19

91

Q1

19

92

Q1

19

93

Q1

19

94

Q1

19

95

Q1

19

96

Q1

19

97

Q1

19

98

Q1

19

99

Q1

20

00

Q1

20

01

Q1

20

02

Q1

20

03

Q1

20

04

Q1

20

05

Q1

20

06

Q1

20

07

Q1

20

08

Q1

20

09

Q1

20

10

Q1

20

11

Q1

20

12

Q1

20

13

Q1

20

14

Q1

20

15

Q1

20

16

Q1

Financial Institutions Household Government Non-financial Business

US Debt/GDP, %

3

US Monetary policy

Source: Bloomberg, CICC Research

0

3

6

9

Jan-9

1

Jan-9

2

Jan-9

3

Jan-9

4

Jan-9

5

Jan-9

6

Jan-9

7

Jan-9

8

Jan-9

9

Jan-0

0

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2

Jan-1

3

Jan-1

4

Jan-1

5

Jan-1

6

Fed funds rate target US 10-year treasury yield%

4

US Fiscal policy: expansion capped by statutory debt

limit

Source: Bloomberg, CICC Research

4

8

12

16

20

Jan-0

1

Aug-0

1

Mar-

02

Oct-

02

May-0

3

Dec-0

3

Jul-04

Fe

b-0

5

Sep-0

5

Apr-

06

Nov-0

6

Jun-0

7

Jan-0

8

Aug-0

8

Mar-

09

Oct-

09

May-1

0

Dec-1

0

Jul-11

Fe

b-1

2

Sep-1

2

Apr-

13

Nov-1

3

Jun-1

4

Jan-1

5

Aug-1

5

Mar-

16

US public debt subject to limit US statutory debt limitUS$trn

5

Valuation of US equities: stretched?

Source: Robert Shiller, CICC Research

Average=16.7

+1 stdev = 23.3

-1 stdev = 10.1

0

5

10

15

20

25

30

35

40

45

50

1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

Shiller's cyclically adjusted P/E

2000

1983

1929

1901

1921

2009

1966

1932

1937

6

Deleverage in Euro Area

Source: Haver Analytics, CICC Research

50

55

60

65

70

75

60

80

100

120

140

160

19

99

Q2

20

00

Q2

20

01

Q2

20

02

Q2

20

03

Q2

20

04

Q2

20

05

Q2

20

06

Q2

20

07

Q2

20

08

Q2

20

09

Q2

20

10

Q2

20

11

Q2

20

12

Q2

20

13

Q2

20

14

Q2

20

15

Q2

Financial Institutions Non-financial Corporations Government Household (RHS)

Euro Area Debt/GDP, %

7

Structural reforms in Euro Area are needed

Source: Wind, CEIC, CICC Research

0

5

10

15

20

25

30

2

5

8

11

14

Ja

n-0

0

Au

g-0

0

Ma

r-0

1

Oct-

01

Ma

y-0

2

De

c-0

2

Jul-

03

Fe

b-0

4

Se

p-0

4

Ap

r-0

5

No

v-0

5

Ju

n-0

6

Ja

n-0

7

Au

g-0

7

Ma

r-0

8

Oct-

08

Ma

y-0

9

De

c-0

9

Ju

l-1

0

Fe

b-1

1

Se

p-1

1

Ap

r-1

2

No

v-1

2

Ju

n-1

3

Ja

n-1

4

Au

g-1

4

Ma

r-1

5

Oct-

15

Ma

y-1

6

Eurozone Germany Italy Greece (RHS)Unemployment rate, %

8

Sovereign default risk in Euro Area: peripheral

countries’ risks are still relatively elevated

Source: Bloomberg, CICC Research

0

2

4

6

8

10

12

14

16

18

20

0.5

1.5

2.5

3.5

4.5

Jan-1

4

Mar-

14

May-1

4

Jul-14

Sep-1

4

Nov-1

4

Jan-1

5

Mar-

15

May-1

5

Jul-15

Sep-1

5

Nov-1

5

Jan-1

6

Mar-

16

May-1

6

Jul-16

Sep-1

6

Portugual Spain Italy Greece (RHS)10 year yield spread to German bunds, % (%)

9

Government debt in Euro Area: continued to

accumulate except for Germany

Source: Haver Analytics, CICC Research

20

50

80

110

140

170

200

Mar-

00

Oct-

00

May-0

1

Dec-0

1

Jul-

02

Fe

b-0

3

Sep-0

3

Apr-

04

Nov-0

4

Jun-0

5

Jan-0

6

Aug-0

6

Mar-

07

Oct-

07

May-0

8

Dec-0

8

Jul-

09

Fe

b-1

0

Sep-1

0

Apr-

11

Nov-1

1

Jun-1

2

Jan-1

3

Aug-1

3

Mar-

14

Oct-

14

May-1

5

Dec-1

5

Euro Area Germany Spain Greece ItalyGovernment debt/GDP, %

China

Deleveraging, financial risks and moderate growth

11

Financial leverage: various sectors continued

to leverage up in recent years

Source: CEIC, Haver, CICC Research

80

90

100

110

120

130

140

150

5

15

25

35

45

2007 2008 2009 2010 2011 2012 2013 2014 2015

Central Government Local Government

Household Financial Institutions

Non-financial Corporations (RHS)

China Debt/GDP, %

12

RMB still faces depreciation pressure

Source: Wind, Bloomberg, Haver, CICC Research

6.1

6.2

6.3

6.4

6.5

6.6

6.7

93

95

97

99

101

103

105

Aug-1

5

Sep-1

5

Oct-

15

Nov-1

5

De

c-1

5

Jan-1

6

Feb-1

6

Mar-

16

Apr-

16

May-1

6

Jun-1

6

Jul-16

Aug-1

6

Sep-1

6

CFETS basket

Spot USD/CNY rate, right scale

Dec 31 2014=100 USD/CNY

meansCNY depreciate

WoW: +0.3%CFETS

+0.1%USD/CNY WoW:

Sep. 19-23 Sep. 12-16

-0.2%

+0.0%

13

Rising property prices in certain cities

Source: Wind, Bloomberg, CICC Research

Beijing: 54.8

Shanghai: 49.3

Tianjin: 25.9

Chongqing: 9.1

Harbin: 8.5

Changchun: 7.3

Jilin: 6.3

Shenyang: 6.9

Yingkou: 4.9Anshan: 5.5

Hohhot: 6.4

Baotou: 4.8

Shijiazhuang: 10.3

Baoding: 8.3

Tangshan: 6.2

Handan: 5.8

Taiyuan: 8.8

Jinan: 9.3

Liaocheng: 4.7

Weifang: 4.8

Yantai: 7.3

Qingdao: 11.1

Zhengzhou: 10.3

Xi'An: 5.7

Baoji: 3.4

Lanzhou: 9.9

Yinchuan: 5.3

Xining: 7.1

Urumqi: 7.7

Hefei: 13.2

Wuhu: 6

Nanjing: 18.1

Lianyungang: 7.1

Xuzhou: 8

Hangzhou: 17.3

Ningbo: 10.4

Jinhua: 6.7

Wenzhou: 11.9Changsha: 4.7Xiangtan: 3.8

Zhuzhou: 3.9

Nanchang: 8.8

Ganzhou: 6.5

Wuhan: 10.8

Chengdu: 8.6

Guiyang: 7 Fuzhou: 15.4

Quanzhou: 8.3

Xiamen: 27.4

Guangzhou: 16.7Shantou: 10

Zhanjiang: 8.4

Haikou: 8

Nanning: 7.1

Guilin: 5.8

Liuzhou: 6.9Kunming: 6.9

Shenzhen: 35.9

Sanya: 13

Zhuhai: 13.6

Dongguan: 5.9

Dalian: 9.6

Property affordability ratio (August, 2016)

Note: 1. Affordability ratio = House price / Annual household disposal income2. Data for most cities are average prices of secondary transactions gathered from Fang.com; primary transaction prices are used if secondary transaction prices are not available; data for Beijing, Shanghai, Shenzhen, Guangzhou, Hangzhou, Nanjing and Tianjin are average prices for the city's core areas ; assume house size to be 90 sq.m3. Household disposal income = The city's disposal income per capita * average household size for the respective province; disposal income data are as of 2015 (assume disposal income to increase 10% per year if 2015's data is not available)

14

Estimated NPL: Rmb9.9~13.4trn or 9.1~12.3%

Source: CEIC, CICC Research

9,890.79.1%

5,187.14.8%

3,038.12.8%

1,531.61.4%

13,432.812.3%

5,321.04.9%

5,073.74.7%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Potential NPLs NPLs recognized NPLs resolved NPLs that can beabsorbed with existing

resources

Remaining gap

(Rmb bn)

NPLs already resolved or can be absorbed by existing financial resourcesRmb8.4trn, or 7.7%

Potential NPLsRmb9.9~13.4trn or 9.1~12.3%

NPLs recognizedRmb5.2trn or 4.8%

Remaining gapRmb1.5~5.1trnor 1.4~4.7%

15

Interest rate is around historical low, but still

have downward room if needed

Source: CEIC, CICC Research

0

2

4

6

8

10One year deposit rate One year loan rate %

16

RRR is still relatively high in historical context

Source: CIEC, CICC Research

0

5

10

15

20

25 RRR: large depository institution

RRR: small and medium depository institution

RRR

%

17

Fiscal policy: China government’s leverage is

still low

Source: BIS, CICC Research

0

50

100

150

200

250

General government debt/GDP%

18

Fiscal policy: more efforts in fiscal expansion

via higher budget deficit this year in 2016

Source: CEIC, CICC Research

-594bn

-3,000

-2,500

-2,000

-1,500

-1,000

-500

0

500

1,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2015

2016 Jan - Jul

RMB bn Cumulative fiscal balance

indicatesfiscalloosening

RMB bn Cumulative fiscal balance

indicatesfiscalloosening

RMB bn Cumulative fiscal balance

indicatesfiscalloosening

RMB bn Cumulative fiscal balance

indicatesfiscalloosening

Global Monetary Policy Coordination

Declining interest rate, expanding central bank balance

sheet and historical lessons

20

Watching for negative interest rates

Source: Bloomberg, CICC Research

1-Year 2-Year 3-Year 4-Year 5-Year 6-Year 7-Year 8-Year 9-Year 10-Year 15-Year 20-Year 30-Year

Switzerland -0.93 -0.95 -0.97 -0.90 -0.85 -0.79 -0.73 -0.66 -0.59 -0.54 -0.30 -0.19 -0.05

Japan -0.28 -0.26 -0.26 -0.25 -0.24 -0.22 -0.22 -0.19 -0.14 -0.07 0.12 0.38 0.51

Germany -0.65 -0.70 -0.71 -0.68 -0.59 -0.56 -0.50 -0.41 -0.29 -0.14 -0.01 0.21 0.42

Netherlands -0.64 -0.67 -0.66 -0.65 -0.49 -0.50 -0.41 -0.28 -0.15 -0.03 0.49

Finland -0.63 -0.66 -0.64 -0.56 -0.53 -0.45 -0.37 -0.26 -0.17 -0.02 0.25 0.51

Austria -0.58 -0.62 -0.60 -0.55 -0.50 -0.45 -0.41 -0.36 -0.09 0.07 0.01 0.49 0.74

France -0.59 -0.64 -0.61 -0.55 -0.45 -0.37 -0.30 -0.12 0.02 0.17 0.46 0.74 0.96

Belgium -0.62 -0.64 -0.59 -0.58 -0.50 -0.45 -0.36 -0.21 -0.04 0.11 0.48 0.56 1.04

Sweden -0.74 -0.67 -0.55 -0.37 -0.23 -0.07 0.14 0.68 0.98

Denmark 0.05 -0.53 -0.15 -0.39 0.31 -0.23 -0.03 0.45

Ireland -0.47 -0.45 -0.44 -0.38 0.00 -0.24 -0.12 0.09 0.24 0.34 0.68 1.16

Spain -0.26 -0.20 -0.15 -0.03 0.05 0.13 0.29 0.58 0.74 0.90 1.28 2.03

Italy -0.21 -0.11 -0.01 0.05 0.25 0.42 0.60 0.81 1.02 1.20 1.55 1.84 2.25

United States 0.57 0.75 0.86 1.12 1.39 1.57 2.30

China 2.19 2.37 2.40 2.56 2.56 2.72 2.75 2.83 2.73 3.11 3.25

21

10 year US treasury yield is 1.57% now, the lowest

level in 226 years

Source: Robert Shiller, CICC Research

0

2

4

6

8

10

12

14

16

1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

10 year US treasury yield%

Global Monetary Base Dynamics: Long View

Since 1900, it is the second time of rapid expansion of balance sheet of the

central banks of developed countries in over 100 years since the financial

crisis in 2008, and the expansion is now slowly returning to the regular level.

The data is based on the

balance sheets of the central

banks of twelve countries:

Australia, Canada, Finland,

France, Germany, Italy,

Japan, Norway, Sweden,

Switzerland, the United

Kingdom and the United

States. The data after 1999

includes the balance sheet of

the European Central Bank.

The proportion of assets of central banks in GDP

22

23

Expanding Global Monetary Base: Short View

Source: Bloomberg, CICC Research Source: Bloomberg, CICC Research

Balance Sheet: Five central total asset as of %

GDP since 2008

Balance Sheet: Five central banks total asset

since 2008

0

200

400

600

800

Jan-0

0

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2

Jan-1

3

Jan-1

4

Jan-1

5

Jan-1

6

Fed ECB BOJ PBoC BOEIndex, Jan 2007=100

0%

20%

40%

60%

80%

Jan-0

0

Jan-0

1

Ja

n-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2

Jan-1

3

Jan-1

4

Jan-1

5

Jan-1

6

Fed ECB BoJ BOE PBoCCentral bank total asset/GDP

24

Source: Bloomberg, CICC Research

Global coordination:

Plaza and Louvre Accords

0%

5%

10%

15%

20%

25%

Jan-7

1

Sep-7

1

May-7

2

Jan-7

3

Sep-7

3

May-7

4

Jan-7

5

Sep-7

5

May-7

6

Jan-7

7

Sep-7

7

May-7

8

Jan-7

9

Sep-7

9

May-8

0

Jan-8

1

Sep-8

1

May-8

2

Jan-8

3

Sep-8

3

May-8

4

Jan-8

5

Sep-8

5

May-8

6

Jan-8

7

Sep-8

7

May-8

8

Jan-8

9

US CPI YoY Fed Funds Rate

Volcker tightened monetary policy to fight against hyperinflation

Rethinking Paradigm and Drawing Blueprint

• Where are we in transition

– 1930s to 1945?

– 1970s to 1985?

– 2010s to when?

• What paradigm/anchor to switch to

– USD in Bretton Woods: BWI

– G5 + Free float exchange rate + Inflation Targeting: BWII

– Key ADs + Key EMs coalition; adopting multi objectives

(inflation, and growth and financial stability?): BWIII

25