Embed Size (px)

Citation preview

Presentation at BVI Asset Management

Frankfurt, 1 October 2015

Peter Praet

Rubric

www.ecb.europa.eu 2

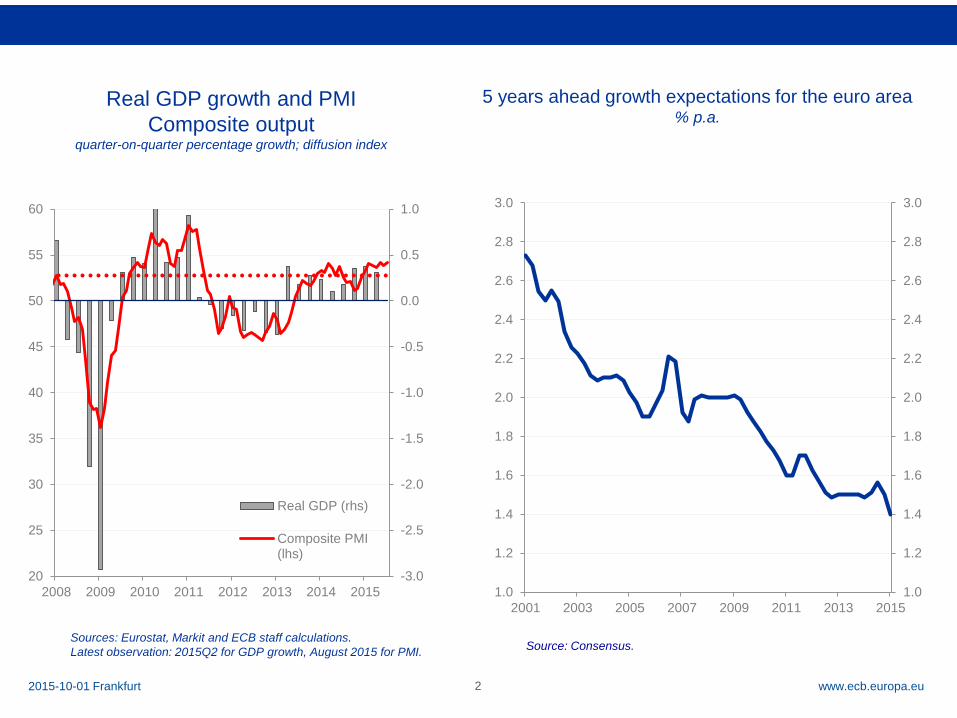

Real GDP growth and PMI

Composite output quarter-on-quarter percentage growth; diffusion index

Sources: Eurostat, Markit and ECB staff calculations.

Latest observation: 2015Q2 for GDP growth, August 2015 for PMI.

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

20

25

30

35

40

45

50

55

60

2008 2009 2010 2011 2012 2013 2014 2015

Real GDP (rhs)

Composite PMI(lhs)

2015-10-01 Frankfurt

5 years ahead growth expectations for the euro area % p.a.

Source: Consensus.

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

2001 2003 2005 2007 2009 2011 2013 2015

Rubric

www.ecb.europa.eu

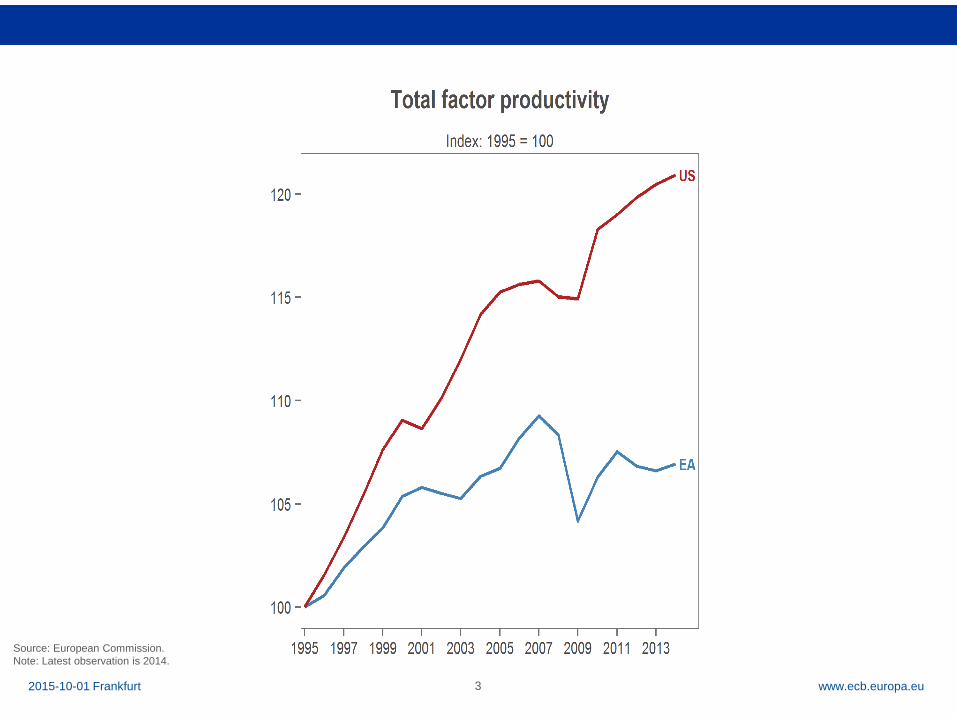

Source: European Commission.

Note: Latest observation is 2014.

3 2015-10-01 Frankfurt

Rubric

www.ecb.europa.eu

Sources: European Commission, Consensus Economics and ECB calculations.

Latest data: 2014 for GDP outcome.

Note: The dotted line represents the evolution of GDP based on private sector

expectations as measured by Consensus Economics in October 2007.

Real GDP & pre-crisis expected path index, 2006 = 100

95

100

105

110

115

120

125

2006 2007 2008 2009 2010 2011 2012 2013 2014

Actual growth

Expected growth

path in late 2007

100

105

110

115

120

125

130

135

140

1999 2002 2005 2008 2011 2014 2017

10%

Counterfactual

potential GDP

Actual GDP Potential

GDP

Source: European Commission Spring 2015 forecast, Output Gap

Working Group.

Note: counterfactual potential GDP assumes that potential GDP

continued to grow at its 2007 growth rate. I.e. it reflects the observation

that potential growth has already slowed down before the crisis.

Germany

Euro area

Spain

EA: Potential output reduction index, potential GDP in 1999=100

4 2015-10-01 Frankfurt

Rubric

www.ecb.europa.eu

Sources: European Commission and ECB calculations.

Note: 2014 partially based on forecasts. Euro area refers to euro area 12.

Equipment investment 2006=100

5

Unemployment rate % of (extended) labor force

Sources: Labour Force Survey and ECB staff calculation.

Note: Discouraged workers are inactive people who are available

but not searching a job. The extended labor force is the number of

active persons extended with the number of discouraged workers.

75

80

85

90

95

100

105

110

115

120

75

80

85

90

95

100

105

110

115

120

2006 2007 2008 2009 2010 2011 2012 2013 2014

Germany

Euro area

Spain

0

2

4

6

8

10

12

0

2

4

6

8

10

12

2005 2007 2009 2011 2013 2015

Unemployment rate

Discouraged workers

2015-10-01 Frankfurt

Rubric

www.ecb.europa.eu

Source: ECB.

Latest observation: June 2015.

Bank loans to private sector annual percentage changes

-10

-5

0

5

10

15

20

25

30

-10

-5

0

5

10

15

20

25

30

2003 2005 2007 2009 2011 2013 2015

DE ES EA

6 2015-10-01 Frankfurt

Rubric

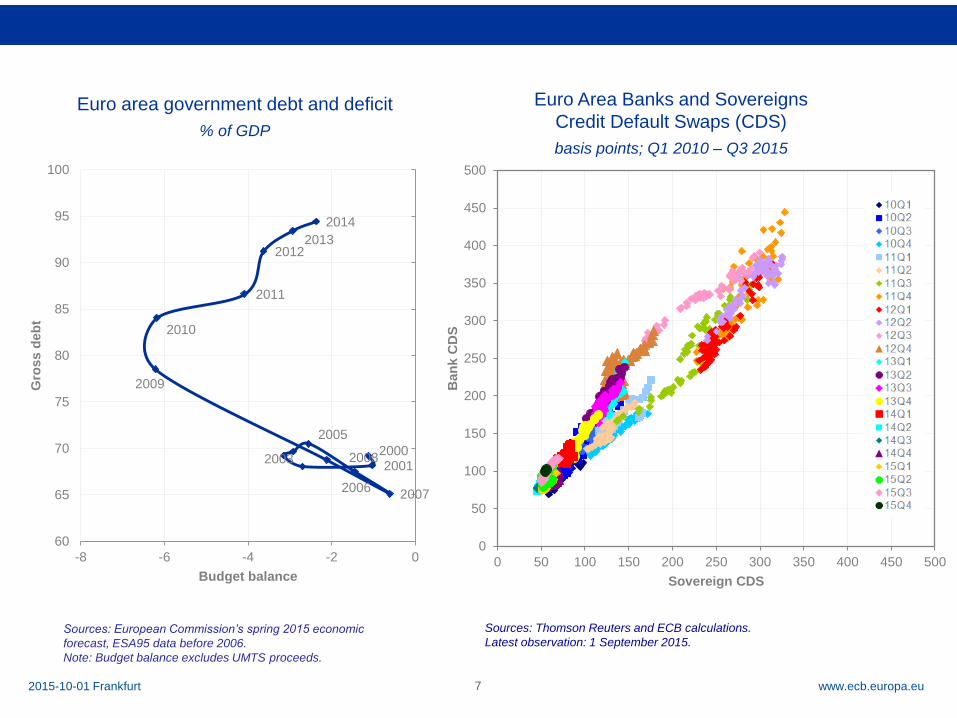

www.ecb.europa.eu 7

Sources: European Commission’s spring 2015 economic

forecast, ESA95 data before 2006.

Note: Budget balance excludes UMTS proceeds.

Euro area government debt and deficit

% of GDP

2000 2001

2003

2005

2006 2007

2008

2009

2010

2011

2012 2013

2014

60

65

70

75

80

85

90

95

100

-8 -6 -4 -2 0

Gro

ss d

eb

t

Budget balance

2015-10-01 Frankfurt

Sources: Thomson Reuters and ECB calculations.

Latest observation: 1 September 2015.

Euro Area Banks and Sovereigns

Credit Default Swaps (CDS)

basis points; Q1 2010 – Q3 2015

0

50

100

150

200

250

300

350

400

450

500

0 50 100 150 200 250 300 350 400 450 500

Ban

k C

DS

Sovereign CDS

Rubric

www.ecb.europa.eu

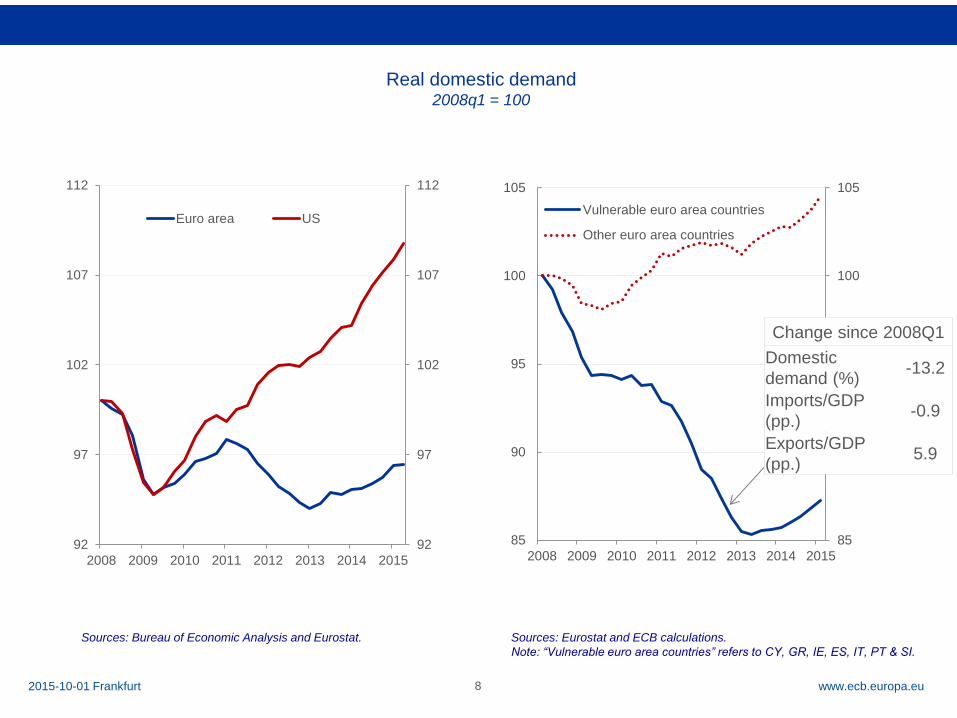

Real domestic demand 2008q1 = 100

8

Sources: Eurostat and ECB calculations.

Note: “Vulnerable euro area countries” refers to CY, GR, IE, ES, IT, PT & SI.

Sources: Bureau of Economic Analysis and Eurostat.

85

90

95

100

105

85

90

95

100

105

2008 2009 2010 2011 2012 2013 2014 2015

Vulnerable euro area countries

Other euro area countries

92

97

102

107

112

92

97

102

107

112

2008 2009 2010 2011 2012 2013 2014 2015

Euro area US

Change since 2008Q1

Domestic

demand (%) -13.2

Imports/GDP

(pp.) -0.9

Exports/GDP

(pp.) 5.9

2015-10-01 Frankfurt

Rubric

www.ecb.europa.eu 9

Price of inflation and deflation protection basis points per annum

Source: Bloomberg.

Note: Price of 0% floor and 4% cap options (year-on-year) on euro area HICP

inflation – 5Y maturity. Developments should be interpreted with caution due to

limited market liquidity. Latest observation: 2 September 2015.

0

50

100

150

200

250

300

350

400

0

50

100

150

200

250

300

350

400

2008 2009 2010 2011 2012 2013 2014 2015

Price of inflation protection

Price of deflation protection

Euro area inflation % p.a.

Source: Eurostat.

Latest observation: September 2015 (flash)

2015-10-01 Frankfurt

-0.1

0.9

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2008 2009 2010 2011 2012 2013 2014 2015

Euro Area HICP

Euro Area HICP excluding food and energy

Rubric

www.ecb.europa.eu

0

2

4

6

8

10

12

14

16

0

2

4

6

8

10

12

14

16

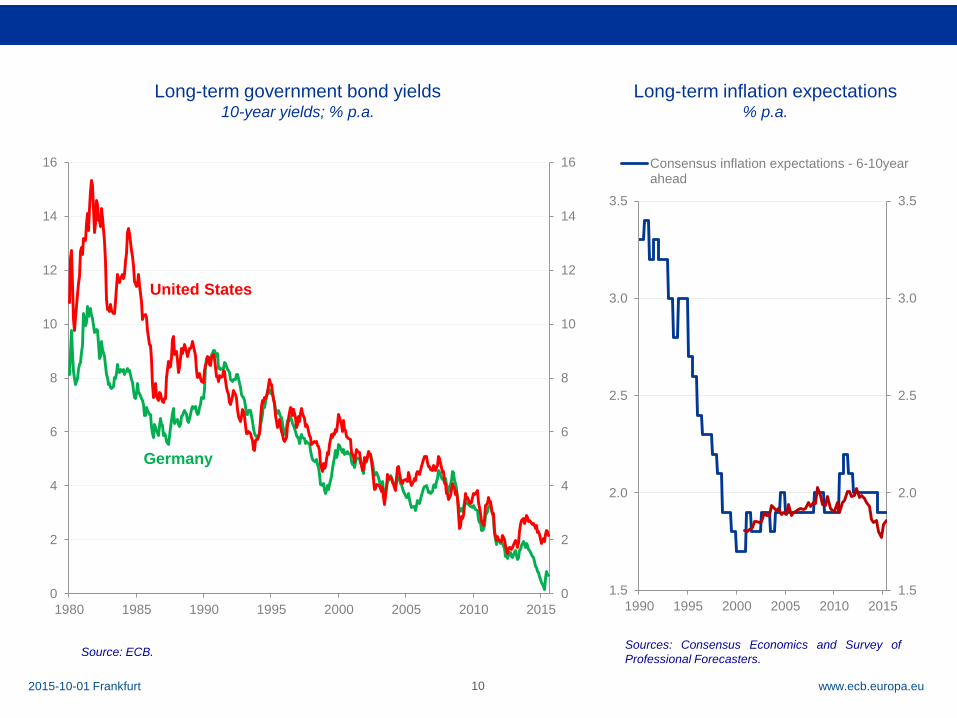

1980 1985 1990 1995 2000 2005 2010 2015

United States

Germany

10

Long-term government bond yields 10-year yields; % p.a.

Source: ECB.

2015-10-01 Frankfurt

1.5

2.0

2.5

3.0

3.5

1.5

2.0

2.5

3.0

3.5

1990 1995 2000 2005 2010 2015

Consensus inflation expectations - 6-10yearahead

Long-term inflation expectations % p.a.

Sources: Consensus Economics and Survey of

Professional Forecasters.

Rubric

www.ecb.europa.eu 11

1y1y EUR and USD OIS % p.a.

Source: Bloomberg.

2015-10-01 Frankfurt

Sources: Reuters and ECB calculations.

Note: OIS = overnight index swap.

EA: EONIA expectations based on the OIS yield curve % p.a.

-0.5

-0.3

-0.1

0.1

0.3

0.5

0.7

0.9

1.1

1.3

1.5

Jan/2013 Jul/2013 Jan/2014 Jul/2014 Jan/2015 Jul/2015

euro area

US

Forward

guidance

Narrowing of

effective corridor

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2015 2017 2019 2021 2023

Min-max range since Nov 2013 GC

Latest (25 Sep 15)

Rubric

www.ecb.europa.eu

Composite indicator of the nominal cost of bank borrowing

for non-financial corporations % p.a.

Source: ECB.

Note: The indicator for the total cost of bank borrowing is calculated by aggregating short- and long-term rates

using a 24-month moving average of new business volumes. Latest observation: July 2015.

0.0

2.0

4.0

6.0

8.0

0.0

2.0

4.0

6.0

8.0

2008 2009 2010 2011 2012 2013 2014 2015

DE ES FR EA IT

12 2015-10-01 Frankfurt

Rubric

www.ecb.europa.eu

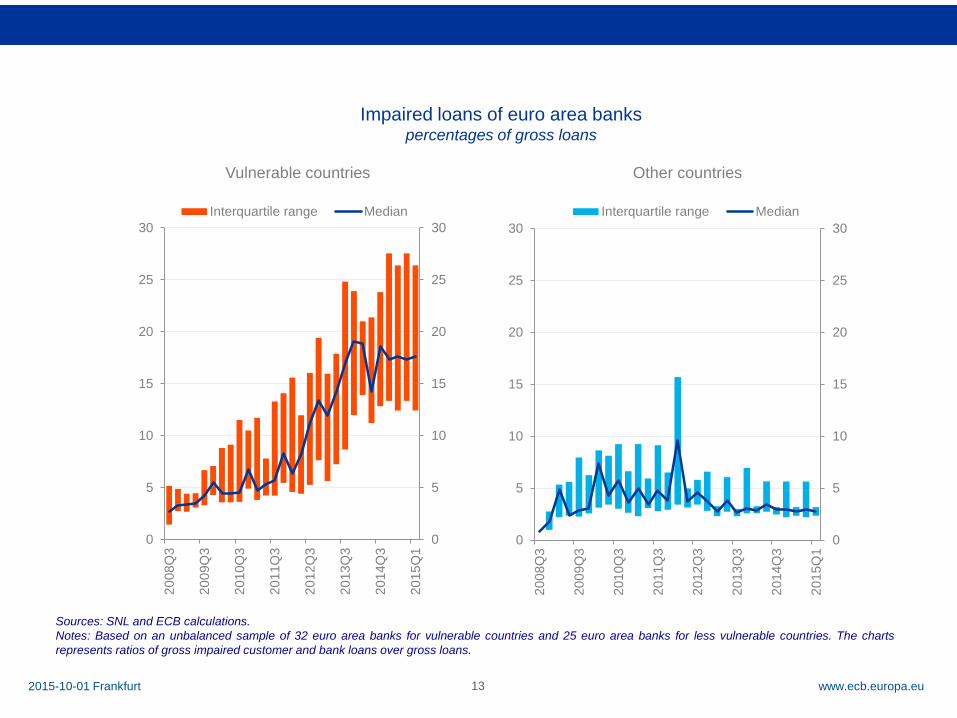

Impaired loans of euro area banks percentages of gross loans

Sources: SNL and ECB calculations.

Notes: Based on an unbalanced sample of 32 euro area banks for vulnerable countries and 25 euro area banks for less vulnerable countries. The charts

represents ratios of gross impaired customer and bank loans over gross loans.

13

0

5

10

15

20

25

30

0

5

10

15

20

25

30

20

08Q

3

20

09Q

3

20

10Q

3

20

11Q

3

20

12Q

3

20

13Q

3

20

14Q

3

20

15Q

1

Vulnerable countries

Interquartile range Median

0

5

10

15

20

25

30

0

5

10

15

20

25

30

20

08Q

3

20

09Q

3

20

10Q

3

20

11Q

3

20

12Q

3

20

13Q

3

20

14Q

3

20

15Q

1

Other countries

Interquartile range Median

2015-10-01 Frankfurt

Rubric

www.ecb.europa.eu

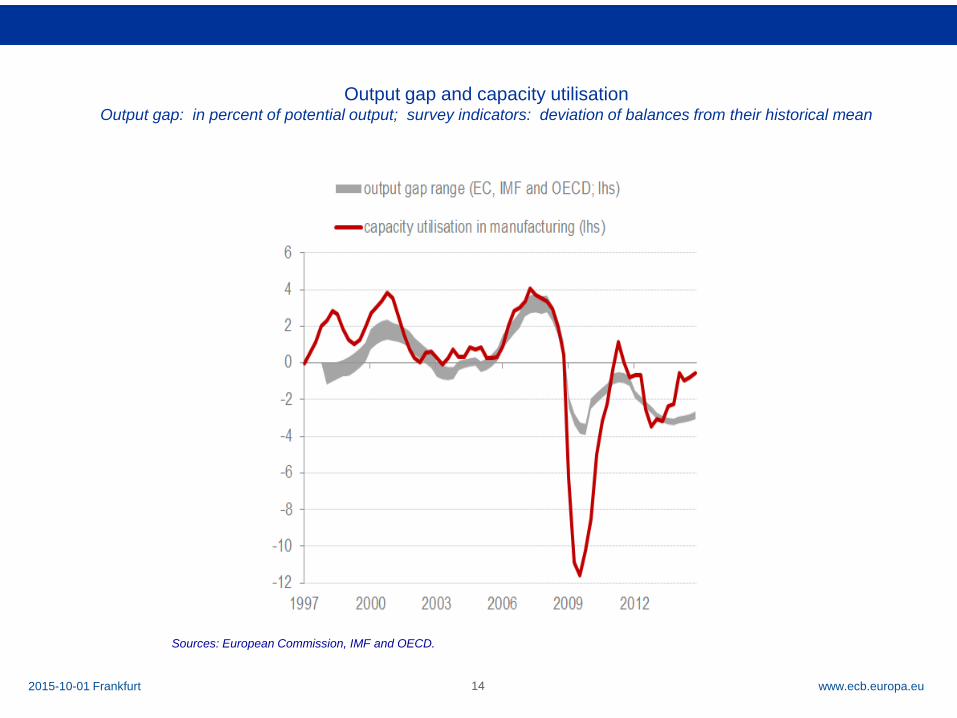

Output gap and capacity utilisation Output gap: in percent of potential output; survey indicators: deviation of balances from their historical mean

Sources: European Commission, IMF and OECD.

14 2015-10-01 Frankfurt

Rubric

www.ecb.europa.eu 15

Source: Eurobarometer ‘s 70.1, 78.2 and 81.1.

Note: Excludes response “Don’t know”.

“Generally speaking, do you think that the life of those in the EU who are children today will

be easier, more difficult, or about the same as the life of those of your own generation?”

Share of respondents in the euro area

12%

19%

67%

61%

18% 18%

0%

10%

20%

30%

40%

50%

60%

70%

80%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2012 2014 2012 2014 2012 2014

Easier More difficult Neither nor

2015-10-01 Frankfurt