Embed Size (px)

Citation preview

ABOUT US Visible Equity is a software development company that focuses on web-based applications for financial institutions.

Our team is comprised of experts in financial economics, mathematical and statistical modeling, and intelligent data systems. We specialize in transforming slow, expensive, and complex tasks into real time, cost effective, and simple results.

Our valuation capabilities, predictive analytics, and advanced modeling applications give you the insight and tools to effectively manage your portfolio and make better informed, data-driven decisions.

Our user friendly, web-based system merges your data with our advanced analytics and market data to produce reports and analysis that are current, relevant, and insightful.

In a nutshell, we help make the obscure visible, allowing our clients to maximize their return on equity.

For more information please visit

your website:

www.visibleequity.com

2 of 58

Fair Lending Agenda

Fair Lending The Basics Assessing Your Fair Lending Risk

Fair Lending Performance Reports Statistical Modeling

and Comparative File Reviews

Building a Fair Lending Program

3 of 58

4 of 58

Fair Lending the Basics

5 of 58

www.visibleequity.com

Fair Lending the Basics

6 of 58

Fair Lending the Basics

7 of 58

Fair Lending the Basics

Fair Lending the Basics

8 of 58

ECOA BOTH FH Act

Equal Credit Opportunity Act (ECOA) Prohibits discrimination in any aspect of a consumer credit transaction (including small businesses).

Fair Housing Act (FH Act) Prohibits discrimination in residential real estate transactions: -making loans to buy, build, repair, improve a dwelling -purchasing real estate loans -selling, brokering, or appraising residential real estate -selling or renting a dwelling

-Handicap -Race or color -Marital Status

-Familial Status -Religion -Age

-National Origin -Source of Income

-Sex

Fair Lending Laws and Prohibited Basis Groups

+ Reg B, HMDA, and CRA are related

Fair Lending the Basics

9 of 58

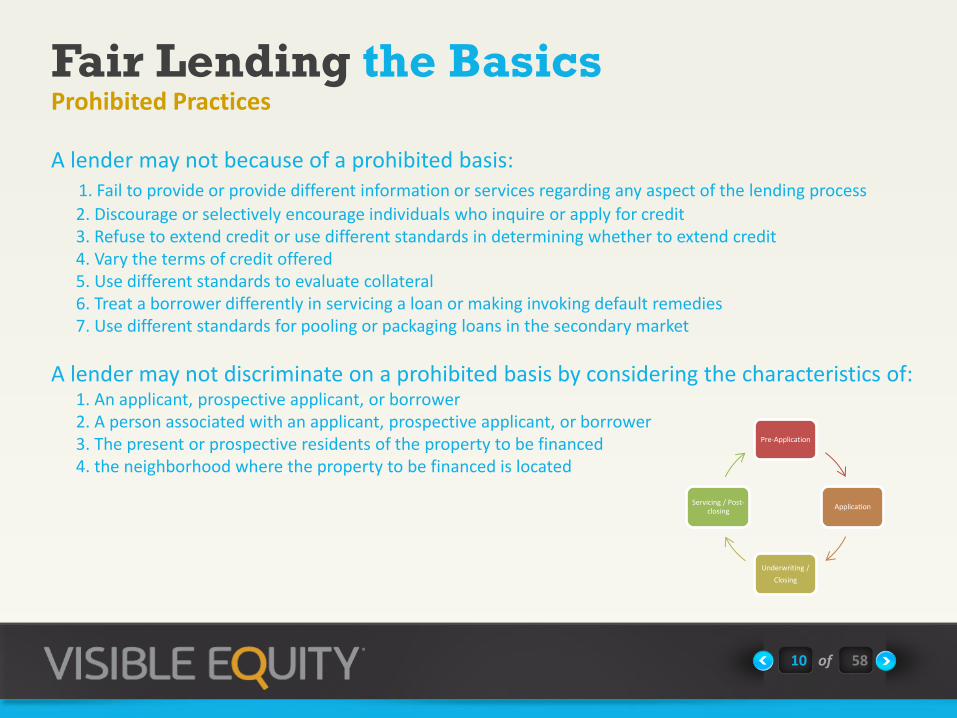

Fair Lending and The Lending Cycle

Pre-Application

Application

Underwriting /

Closing

Servicing / Post-closing

-Advertising & Market Selection -Channels -Responding to Inquiries

-Level of Assistance -Use of 3rd Parties -Initial Terms & Conditions -Approval Criteria

-Final Terms & Conditions -Appraisal Practices

-Modifications -Default Remedies

-REO

Fair Lending the Basics

10 of 58

A lender may not because of a prohibited basis: 1. Fail to provide or provide different information or services regarding any aspect of the lending process

2. Discourage or selectively encourage individuals who inquire or apply for credit 3. Refuse to extend credit or use different standards in determining whether to extend credit 4. Vary the terms of credit offered 5. Use different standards to evaluate collateral 6. Treat a borrower differently in servicing a loan or making invoking default remedies 7. Use different standards for pooling or packaging loans in the secondary market

A lender may not discriminate on a prohibited basis by considering the characteristics of: 1. An applicant, prospective applicant, or borrower 2. A person associated with an applicant, prospective applicant, or borrower 3. The present or prospective residents of the property to be financed 4. the neighborhood where the property to be financed is located

Prohibited Practices

Pre-Application

Application

Underwriting /

Closing

Servicing / Post-closing

Fair Lending the Basics

11 of 58

1. Disparate Treatment

Types of Discrimination

Treating an applicant or borrower differently due to a prohibited basis during any aspect of the lending process.

>Overt Discrimination -Lender openly discriminates on a prohibited basis (can be written or verbal)

>Comparative Evidence -Differences in treatment not fully explained by legitimate non-discriminatory factors

*Does not require evidence the lender intended to discriminate or was motivated by prejudice

2. Disparate Impact (“Effects Test”)

When an otherwise neutral policy or practice has a disproportionately negative impact on persons from a prohibited basis group. *A disparate impact claim must show the challenged policy or practice is either not justified by a valid business propose or that the business justification could be accomplished using a less discriminatory alternative.

Fair Lending the Basics

12 of 58

Discrimination?

Example 1

-For joint applicants, combine the debts and income of married joint applicants to calculate debt-to-income ratio and for unmarried joint applicants calculate an individual debt-to-income ratio for each applicant.

Yes!

Prohibited Basis: Age

Discrimination Type: Disparate Treatment-Overt

Prohibited Practice: Vary the terms of credit offered

Example 2

Credit Card Limits: -$750 for age 21-30 -$1,500 for age over 30

Yes!

Prohibited Basis: Marital Status

Discrimination Type: Disparate Treatment-Overt

Prohibited Practice: Refuse to extend credit or use different standards in determining whether to extend credit

Fair Lending the Basics www.visibleequity.com

13 of 58

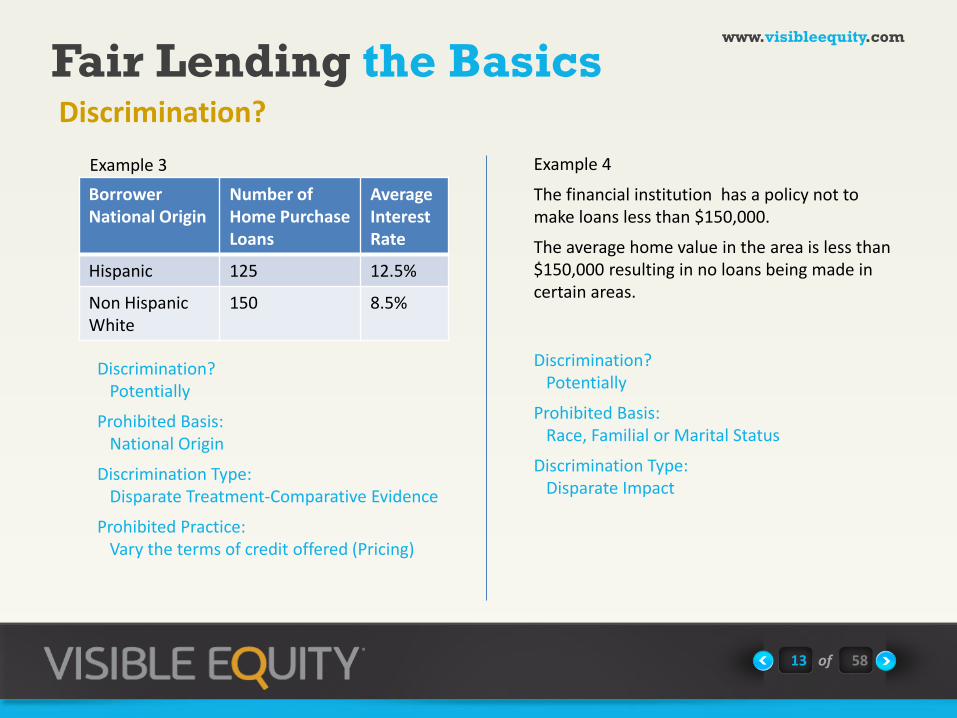

Discrimination?

Example 4

The financial institution has a policy not to make loans less than $150,000.

The average home value in the area is less than $150,000 resulting in no loans being made in certain areas.

Discrimination? Potentially

Prohibited Basis: National Origin

Discrimination Type: Disparate Treatment-Comparative Evidence

Prohibited Practice: Vary the terms of credit offered (Pricing)

Borrower National Origin

Number of Home Purchase Loans

Average Interest Rate

Hispanic 125 12.5%

Non Hispanic White

150 8.5%

Example 3

Discrimination? Potentially

Prohibited Basis: Race, Familial or Marital Status

Discrimination Type: Disparate Impact

Fair Lending the Basics

14 of 58

U.S. Department of Housing and Urban Development Office of Policy Development and Research

All Other Things Being Equal:

A Paired Testing Study of

Mortgage Lending Institutions

Final Report

April 2002

Fair Lending the Basics

15 of 58

All Other Things Being Equal:

A Paired Testing Study of

Mortgage Lending Institutions

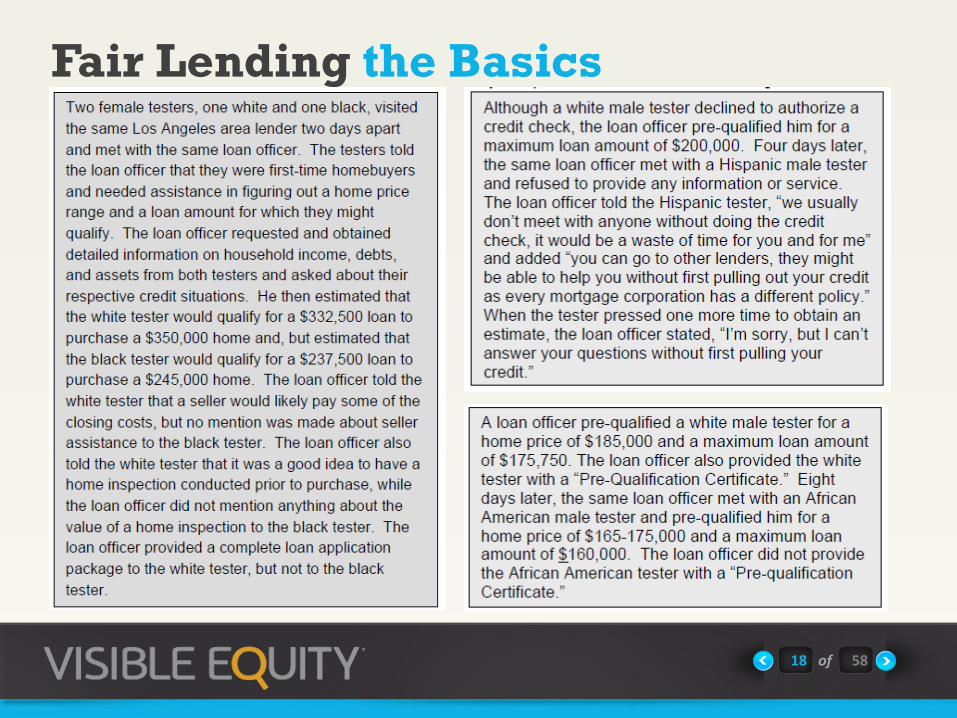

In a paired test, two individuals―one white and one minority―pose as

homebuyers and inquire about the availability and terms for home

mortgage loans. Because the two members of a tester team present

themselves as equally qualified borrowers in every respect except their

race or ethnicity, systematic differences in the treatment they receive

provide direct evidence of adverse treatment discrimination.

The Results?

Fair Lending the Basics

16 of 58

In Los Angeles -

Blacks were offered less coaching than comparable white homebuyers and were

more likely to be encouraged to consider an FHA loan.

Hispanics were denied basic information about loan amount and house price, told

about fewer products, and received less follow-up than comparable Anglo

homebuyers.

In Chicago –

Blacks were denied basic information about loan amount and house price, told about

fewer products, offered less coaching, and received less follow-up than comparable

white homebuyers.

Hispanics were quoted lower loan amounts or house prices, told about fewer

products, and offered less coaching than comparable Anglo homebuyers.

The Results

Fair Lending the Basics

17 of 58

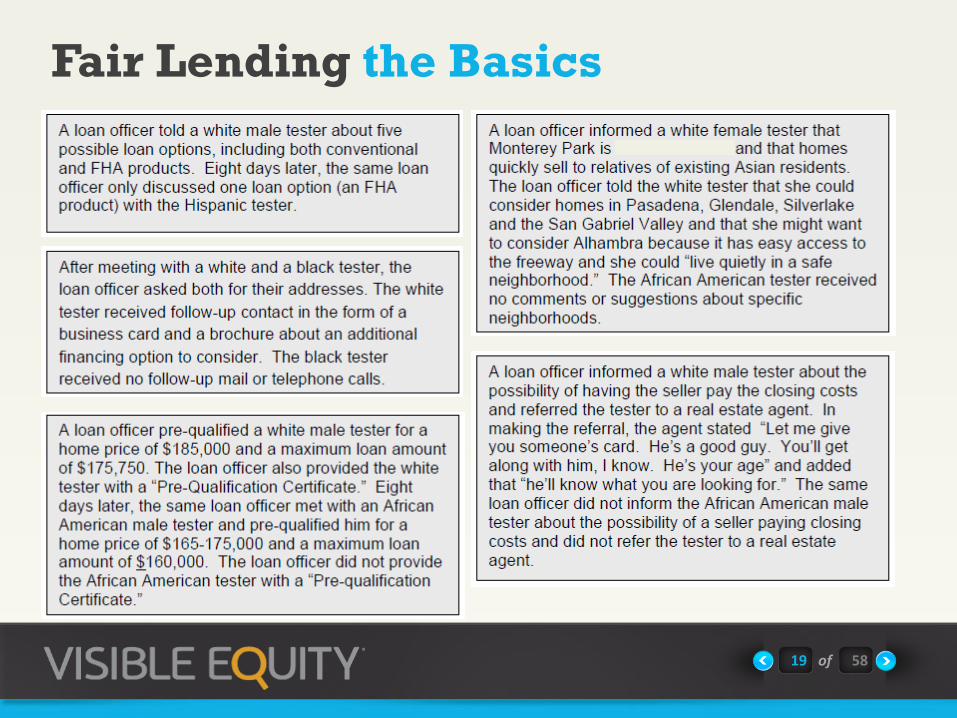

Fair Lending the Basics

18 of 58

Fair Lending the Basics

19 of 58

Fair Lending the Basics-

20 of 58

Fair Lending the Basics

21 of 58

Discrimination Type:

Disparate Treatment-Comparative Evidence (Statistical Analysis & Interviews)

Prohibited Practices:

Steering Claims (vary the terms of credit, others)

Pricing Claims (vary the terms of credit)

Findings:

African Americans 3x more likely to be put in a “subprime” product than similarly

situated white borrowers

Sources of Fair Lending Risk:

Policies and procedures inadequate

Loan officers were given discretion in setting rates, fees, and terms

Loan officers were compensated for putting buyers in higher priced loans

Bank of America Settlement ($335 M)- Accused of Discriminatory Lending (at Countrywide Home Loans)

Fair Lending Assessing Your Risk

22 of 58

The 5* Main Sources of Potential Fair Lending Risk

1. Marketing Activities

2. Discretion Permitted

3. Exceptions

4. Role of Third Parties

5. Incentives & Compensation

*In addition to overt discrimination and the technical requirements of Reg B and other fair lending

laws.

Fair Lending Assessing Your Risk

23 of 58

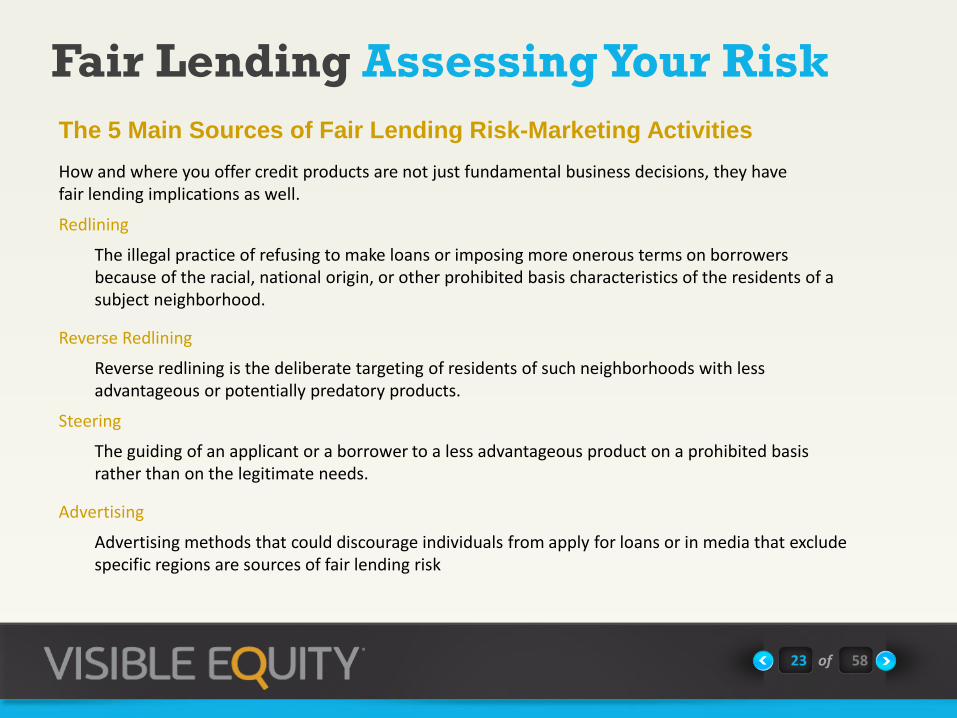

The 5 Main Sources of Fair Lending Risk-Marketing Activities

Redlining

The illegal practice of refusing to make loans or imposing more onerous terms on borrowers because of the racial, national origin, or other prohibited basis characteristics of the residents of a subject neighborhood.

Reverse Redlining

Reverse redlining is the deliberate targeting of residents of such neighborhoods with less advantageous or potentially predatory products.

Steering

The guiding of an applicant or a borrower to a less advantageous product on a prohibited basis rather than on the legitimate needs.

Advertising

Advertising methods that could discourage individuals from apply for loans or in media that exclude specific regions are sources of fair lending risk

How and where you offer credit products are not just fundamental business decisions, they have fair lending implications as well.

Fair Lending Assessing Your Risk

24 of 58

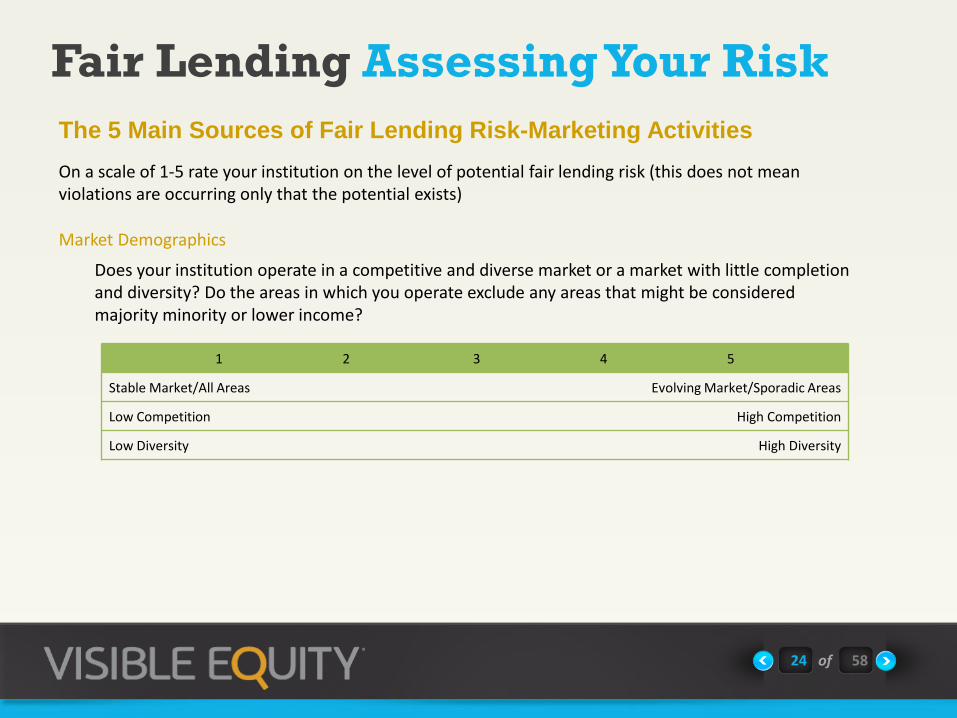

The 5 Main Sources of Fair Lending Risk-Marketing Activities

Market Demographics

Does your institution operate in a competitive and diverse market or a market with little completion and diversity? Do the areas in which you operate exclude any areas that might be considered majority minority or lower income?

On a scale of 1-5 rate your institution on the level of potential fair lending risk (this does not mean violations are occurring only that the potential exists)

1 2 3 4 5

Stable Market/All Areas Evolving Market/Sporadic Areas

Low Competition High Competition

Low Diversity High Diversity

Fair Lending Assessing Your Risk

25 of 58

The 5 Main Sources of Fair Lending Risk-Marketing Activities

Delivery Channels

Does your institution have multiple delivery channels (e.g. website, telephone, face-to-face, third parties, etc.)? Do decisions and processes related to application processing, underwriting, pricing, servicing, etc. vary by channel? Do you have “subprime” or similar subsidiaries or related businesses you refer certain applicants to?

On a scale of 1-5 rate your institution on the level of potential fair lending risk (this does not mean violations are occurring only that the potential exists)

1 2 3 4 5

Limited Channels Multiple Channels

Decisions/Processes do not vary by channel Decisions/Processes vary by channel

No Subprime Subsidiaries/Partners No Subprime Subsidiaries/Partners

Fair Lending Assessing Your Risk

26 of 58

The 5 Main Sources of Fair Lending Risk-Marketing Activities

Product Complexity Do you offer “non-traditional”, “subprime” or other products the industry would consider complex,

difficult to understand, or potentially less advantageous than traditional products?

On a scale of 1-5 rate your institution on the level of potential fair lending risk (this does not mean violations are occurring only that the potential exists)

1 2 3 4 5

Traditional Product Mix Complex and Non-traditional Product Mix

New Products Reviewed for Fair Lending Compliance New Products Not Reviewed

Advertising How complex is your advertising program? Do you advertise in multiple media platforms and/or in

multiple languages? Is your advertising constantly changing? Do you advertise exclusively in areas or through media that is targeted at areas considered majority minority or lower income? Could any of your advertising pieces be considered threatening or discouraging to a protected class?

1 2 3 4 5

Limited Advertising Extensive Advertising

No Recent Changes Constantly Changing Advertising

Broad Based Targeted

Fair Lending Assessing Your Risk

27 of 58

The 5 Main Sources of Fair Lending Risk-Marketing Activities

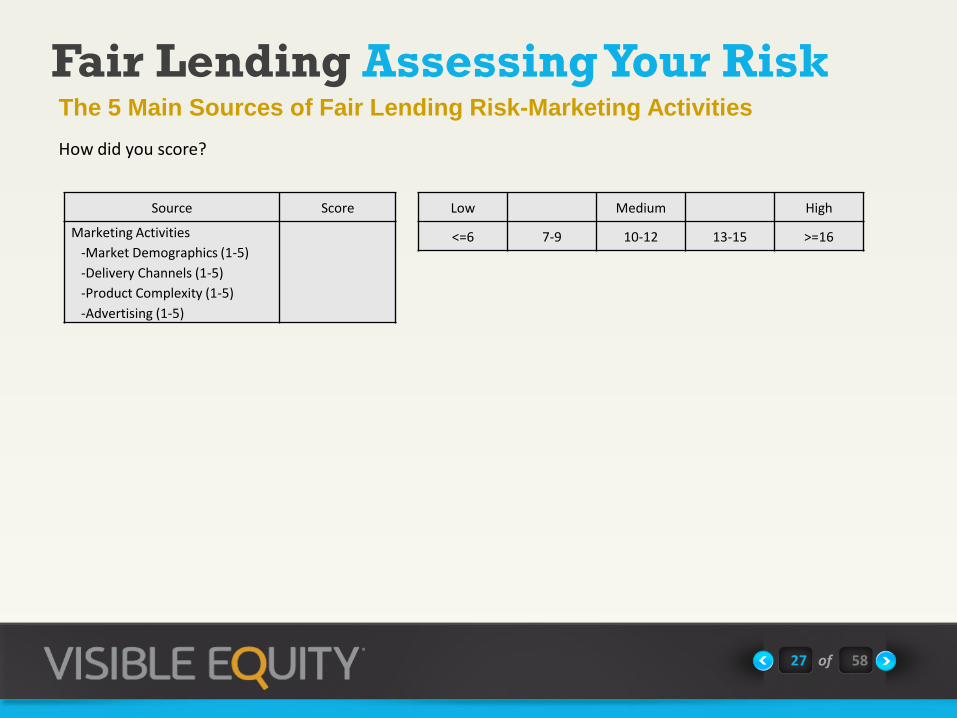

How did you score?

Source Score

Marketing Activities

-Market Demographics (1-5)

-Delivery Channels (1-5)

-Product Complexity (1-5)

-Advertising (1-5)

Low Medium High

<=6 7-9 10-12 13-15 >=16

Fair Lending Assessing Your Risk

28 of 58

The 5 Main Sources of Fair Lending Risk-Discretion Permitted

Discretion Permitted

How much discretion is permitted? Does the degree of permitted discretion vary by geography, channel, or activity? Can the exercise of discretion impact compensation? Do disparities by a prohibited basis group exist in the discretion exercised?

On a scale of 1-5 rate your institution on the level of potential fair lending risk (this does not mean violations are occurring only that the potential exists)

1 2 3 4 5

Limited and Consistent Discretion Broad and Variable Discretion

Discretion criteria is clear Discretion criteria is broad or non-existent

Discretion does not impact compensation Discretion does impact compensation

No Disparities Resulting From Exercised Discretion Unexplained Discrepancies Exists

Allowing discretion has many benefits and in fact is usually used in the favor of the applicant or borrower.

However, the level of individual discretion permitted in certain activities such as approvals or pricing increases an institution’s fair lending risk. Centralized lending operations with clear and objective non discriminatory policies and procedures that are taught, followed, and monitored significantly reduces the level of fair lending risk.

Fair Lending Assessing Your Risk

29 of 58

The 5 Main Sources of Fair Lending-Discretion Permitted

How did you score?

Source Score

Marketing Activities

Discretion Permitted

Low Medium High

<=6 7-9 10-12 13-15 >=16

1 2 3 4 5

Fair Lending Assessing Your Risk

30 of 58

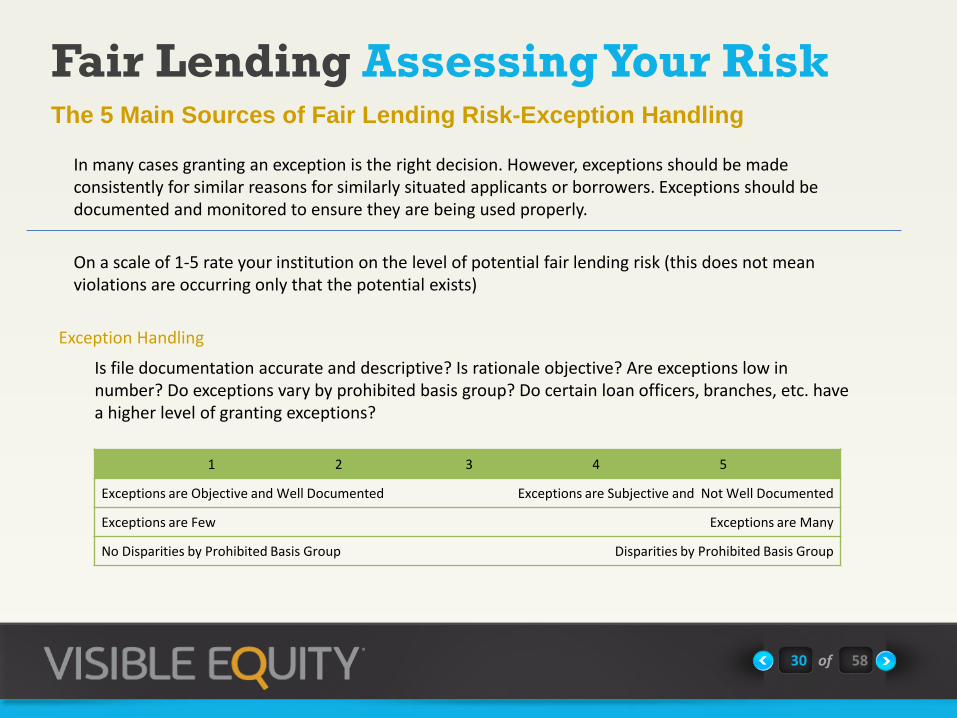

The 5 Main Sources of Fair Lending Risk-Exception Handling

Exception Handling

Is file documentation accurate and descriptive? Is rationale objective? Are exceptions low in number? Do exceptions vary by prohibited basis group? Do certain loan officers, branches, etc. have a higher level of granting exceptions?

On a scale of 1-5 rate your institution on the level of potential fair lending risk (this does not mean violations are occurring only that the potential exists)

1 2 3 4 5

Exceptions are Objective and Well Documented Exceptions are Subjective and Not Well Documented

Exceptions are Few Exceptions are Many

No Disparities by Prohibited Basis Group Disparities by Prohibited Basis Group

In many cases granting an exception is the right decision. However, exceptions should be made consistently for similar reasons for similarly situated applicants or borrowers. Exceptions should be documented and monitored to ensure they are being used properly.

Fair Lending Assessing Your Risk

31 of 58

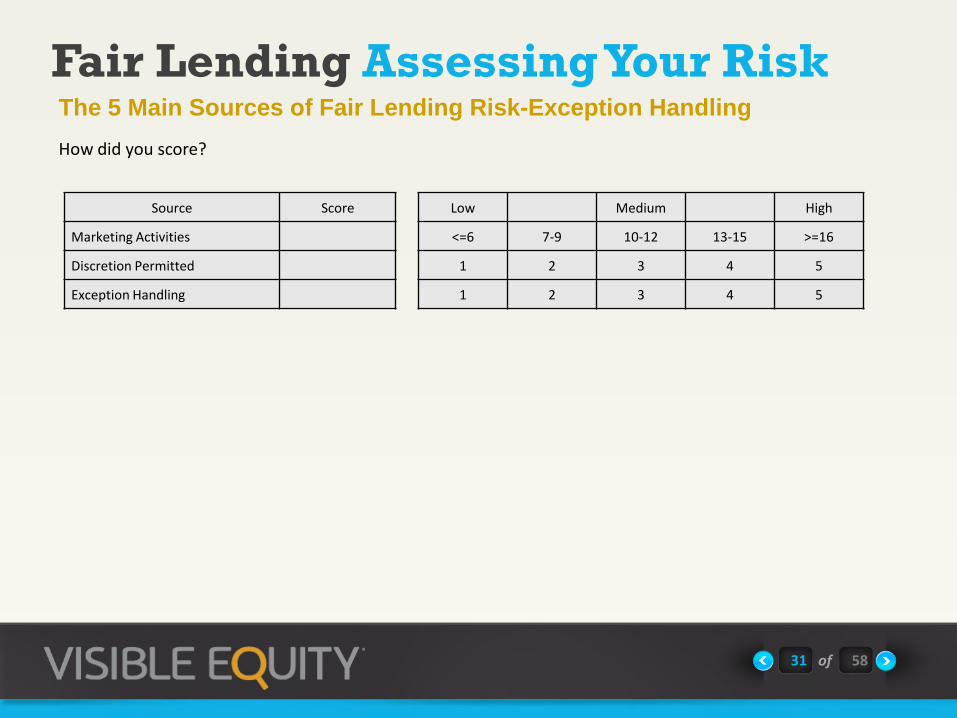

The 5 Main Sources of Fair Lending Risk-Exception Handling

How did you score?

Source Score

Marketing Activities

Discretion Permitted

Exception Handling

Low Medium High

<=6 7-9 10-12 13-15 >=16

1 2 3 4 5

1 2 3 4 5

Fair Lending Assessing Your Risk

32 of 58

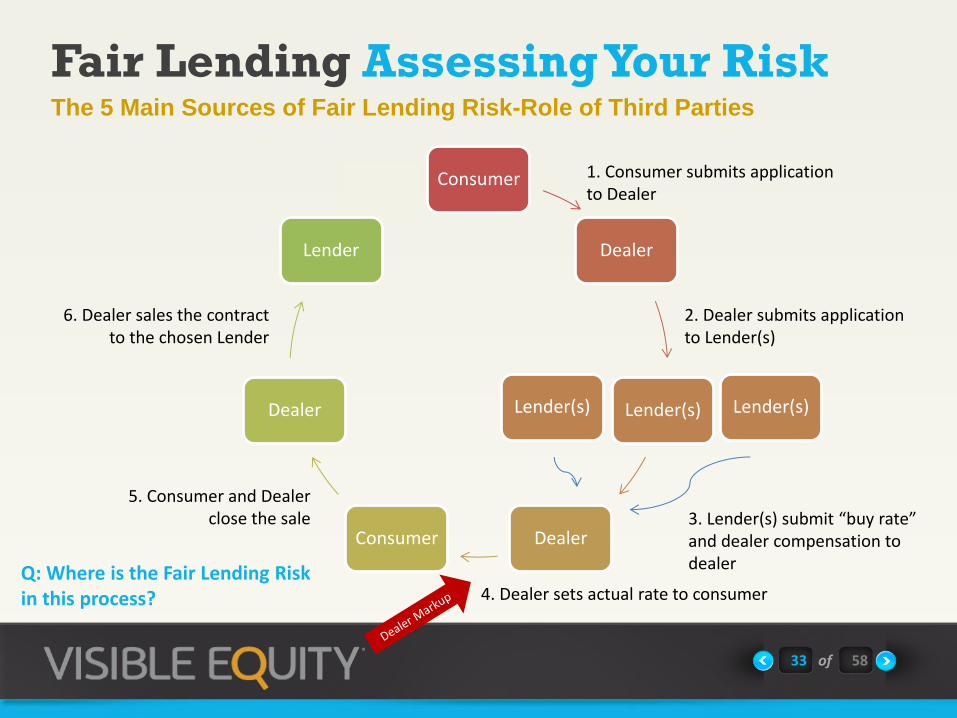

The 5 Main Sources of Fair Lending Risk-Role of Third Parties

Third party operators (TPOs) such as mortgage brokers and auto dealers offer legitimate opportunities to extend lending operations and enhance product offerings.

From a fair lending perspective TPOs are the financial institution and if any TPO does not comply with fair lending regulations the financial institution may be as culpable as if you were the initial creditor.

Fair Lending Assessing Your Risk

33 of 58

The 5 Main Sources of Fair Lending Risk-Role of Third Parties

Consumer

Dealer

Lender(s)

Dealer Consumer

Dealer

Lender

1. Consumer submits application to Dealer

2. Dealer submits application to Lender(s)

3. Lender(s) submit “buy rate” and dealer compensation to dealer

4. Dealer sets actual rate to consumer

5. Consumer and Dealer close the sale

Lender(s) Lender(s)

6. Dealer sales the contract to the chosen Lender

Q: Where is the Fair Lending Risk in this process?

Fair Lending Assessing Your Risk

34 of 58

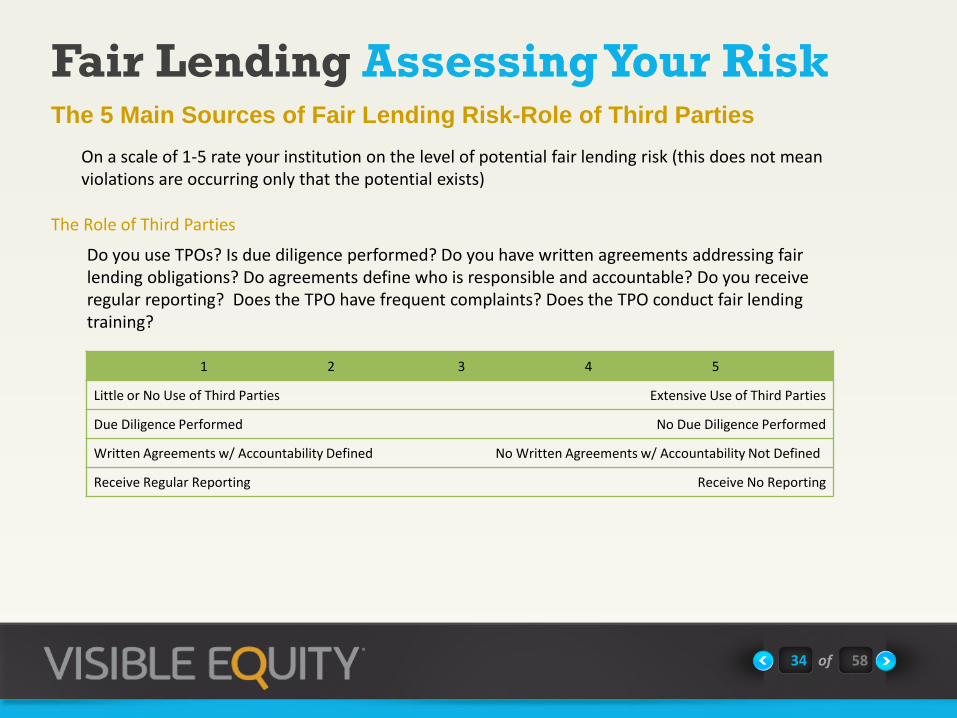

The 5 Main Sources of Fair Lending Risk-Role of Third Parties

The Role of Third Parties

Do you use TPOs? Is due diligence performed? Do you have written agreements addressing fair lending obligations? Do agreements define who is responsible and accountable? Do you receive regular reporting? Does the TPO have frequent complaints? Does the TPO conduct fair lending training?

On a scale of 1-5 rate your institution on the level of potential fair lending risk (this does not mean violations are occurring only that the potential exists)

1 2 3 4 5

Little or No Use of Third Parties Extensive Use of Third Parties

Due Diligence Performed No Due Diligence Performed

Written Agreements w/ Accountability Defined No Written Agreements w/ Accountability Not Defined

Receive Regular Reporting Receive No Reporting

Fair Lending Assessing Your Risk

35 of 58

The 5 Main Sources of Fair Lending Risk-Role of 3rd Parties (TPOs)

How did you score?

Source Score

Marketing Activities

Discretion Permitted

Exception Handling

Role of Third Parties

Low Medium High

<=6 7-9 10-12 13-15 >=16

1 2 3 4 5

1 2 3 4 5

1 2 3 4 5

Fair Lending Assessing Your Risk

36 of 58

The 5 Main Sources of Fair Lending-Incentives & Compensation

Incentives & Compensation

Are your loan officer and other decision makers compensated on loan production? Is compensation tied to higher pricing or higher fees?

On a scale of 1-5 rate your institution on the level of potential fair lending risk (this does not mean violations are occurring only that the potential exists)

1 2 3 4 5

Incentives & Compensation Not Tied to Loan

Production Incentives & Compensation Tied to Loan Production

Incentives & Compensation Not Tied to Loan Pricing

and/or Fees

Incentives & Compensation Tied to Loan Pricing and/or

Fees

Compensation tied to loan production can be a great motivator for a tough job, but it can also lead to significant fair lending issues. If loan officers or other decision makers are incented to steer borrowers into certain products disparate impact against protected groups can occur.

Fair Lending Assessing Your Risk

37 of 58

The 5 Main Sources of Fair Lending Risk-Incentives & Compensation

How did you score?

Source Score

Marketing Activities

Discretion Permitted

Exception Handling

Role of Third Parties

Incentives & Compensation

TOTAL

Low Medium-Low Medium Medium-High High

<=6 7-9 10-12 13-15 >=16

1 2 3 4 5

1 2 3 4 5

1 2 3 4 5

1 2 3 4 5

<=12 13-19 20-26 27-33 >=34

Fair Lending Assessing Your Risk

38 of 58

Fair Lending Assessing Your Risk

39 of 58

Fair Lending Performance Reports

40 of 58

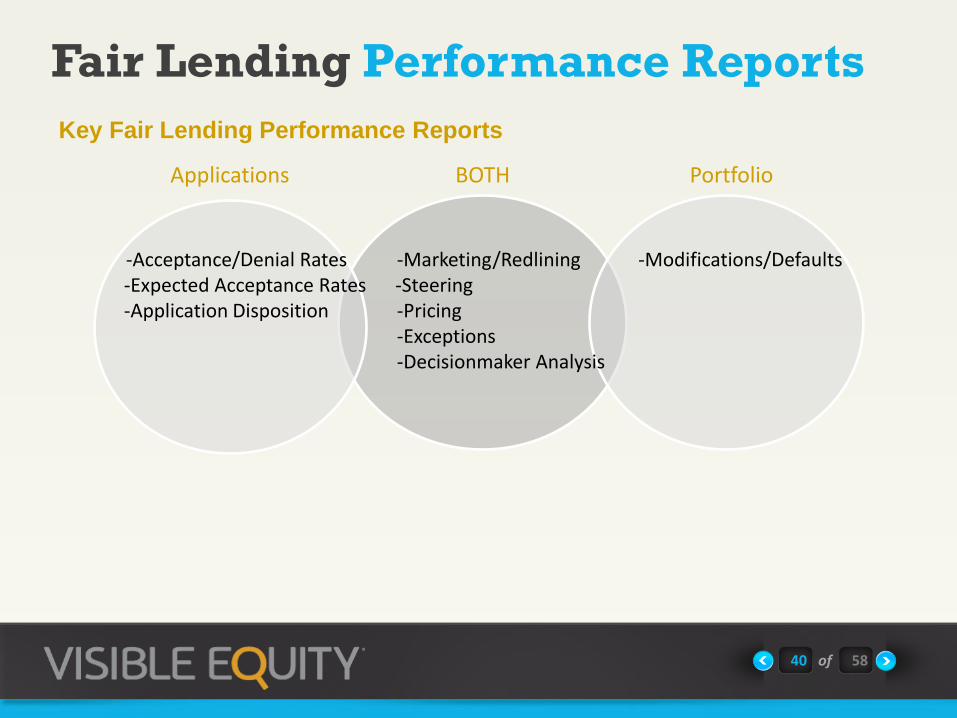

Key Fair Lending Performance Reports

Portfolio BOTH Applications

-Acceptance/Denial Rates -Marketing/Redlining -Modifications/Defaults -Expected Acceptance Rates -Steering -Application Disposition -Pricing -Exceptions -Decisionmaker Analysis

Fair Lending Performance Reports

41 of 58

Key Fair Lending Performance Reports-Application Rates

Approved

Applications

Denied

Applications Total Applications

Approval /Denial

Rates

Denial Relative

Impact

White 1000 100 1100 90.9%/9.1% 1.0

Hispanic 500 200 700 71.4%/28.6% 3.14

Black 150 150 300 50%/50% 5.5

Etc.

-Application Rates by Race/Ethnicity, Gender, Age, Marital Status, Census Tract Metric (Income, Majority Minority, Etc.

-Higher denial rates indicate potential disparate treatment.

Fair Lending Performance Reports

42 of 58

Key Fair Lending Performance Reports-Expected Approval Rates

Actual Approval

Rate

Expected

Approval Rate Status

White 92.3% 90.0% OK

Hispanic 55.0% 58.2% OK

Black 22.3% 43.4% !

Etc.

-Approval Rates by Race/Ethnicity, Gender, Age, Marital Status, Census Tract Metric (Income, Majority Minority, Etc.

-The Expected Approval Rate incorporates borrower and collateral risk. Differences are an indication of disparate treatment.

-The difference between actual and expected must be significant in terms of both statistical accuracy and magnitude.

Fair Lending Performance Reports

43 of 58

Key Fair Lending Performance Reports-Application Disposition

Total Applications Approved

Applications

Denied

Applications

Withdrawn

Applications Etc.

White 1200 1000 (83.3%) 100 (8.3%) 25 (2.0%)

Hispanic 800 500 (62.5%) 200 (25.0%) 50 (6.2%)

Black 400 150 (37.5%) 150 (37.5%) 60 (15.0%)

Etc.

-Application Disposition by Race/Ethnicity, Gender, Age, Marital Status, Census Tract Metric (Income, Majority Minority, Etc.), Etc.

-High Levels of withdrawn applications are an indicator of potential disparate treatment.

Fair Lending Performance Reports

44 of 58

Key Fair Lending Performance Reports-Marketing/Redlining

% of Loan Count % of Market Area Market Relative

Impact

Upper Income 12.5% 10% .8

Middle Income 70% 60% .86

Moderate Income 12.5% 5% .4

Low Income 5% 25% 5.0

-Applications or Loans by Race/Ethnicity, Gender, Age, Marital Status, Census Tract Metrics (Income, Majority Minority, Etc.), Etc.

-Disparities between application or portfolio mix and market area mix are an indication of potential redlining.

Fair Lending Performance Reports

45 of 58

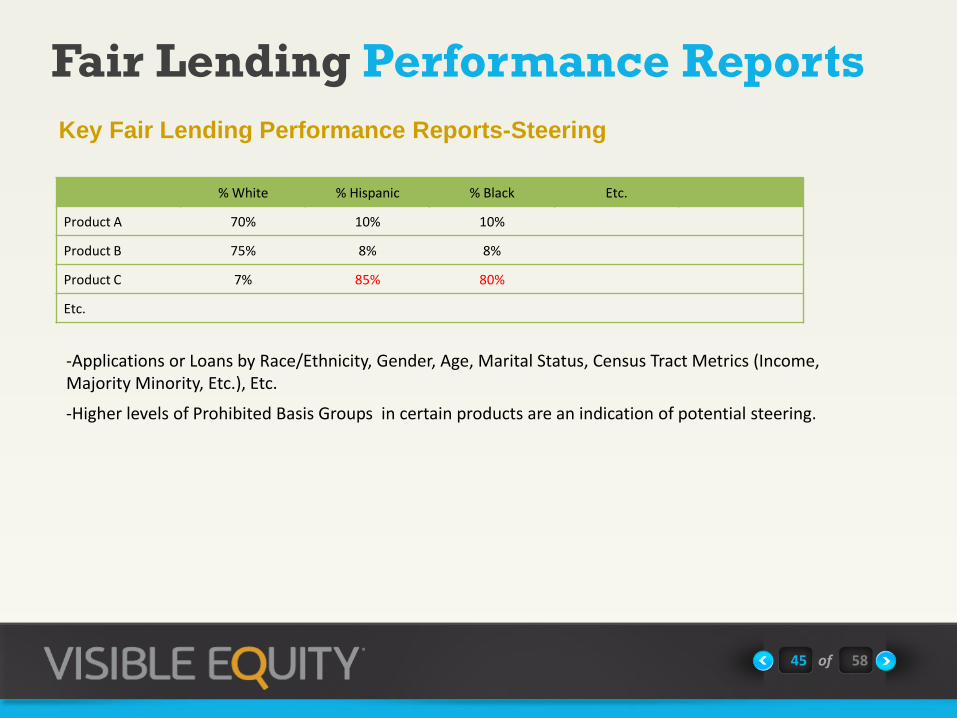

Key Fair Lending Performance Reports-Steering

% White % Hispanic % Black Etc.

Product A 70% 10% 10%

Product B 75% 8% 8%

Product C 7% 85% 80%

Etc.

-Applications or Loans by Race/Ethnicity, Gender, Age, Marital Status, Census Tract Metrics (Income, Majority Minority, Etc.), Etc.

-Higher levels of Prohibited Basis Groups in certain products are an indication of potential steering.

Fair Lending Performance Reports

46 of 58

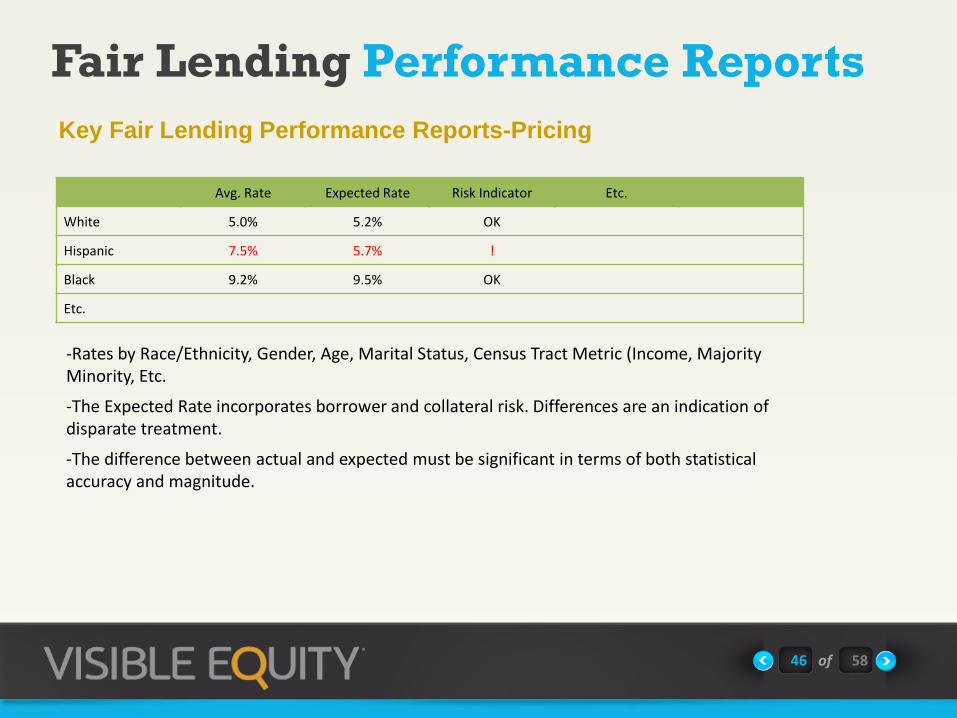

Key Fair Lending Performance Reports-Pricing

Avg. Rate Expected Rate Risk Indicator Etc.

White 5.0% 5.2% OK

Hispanic 7.5% 5.7% !

Black 9.2% 9.5% OK

Etc.

-Rates by Race/Ethnicity, Gender, Age, Marital Status, Census Tract Metric (Income, Majority Minority, Etc.

-The Expected Rate incorporates borrower and collateral risk. Differences are an indication of disparate treatment.

-The difference between actual and expected must be significant in terms of both statistical accuracy and magnitude.

Fair Lending Performance Reports

47 of 58

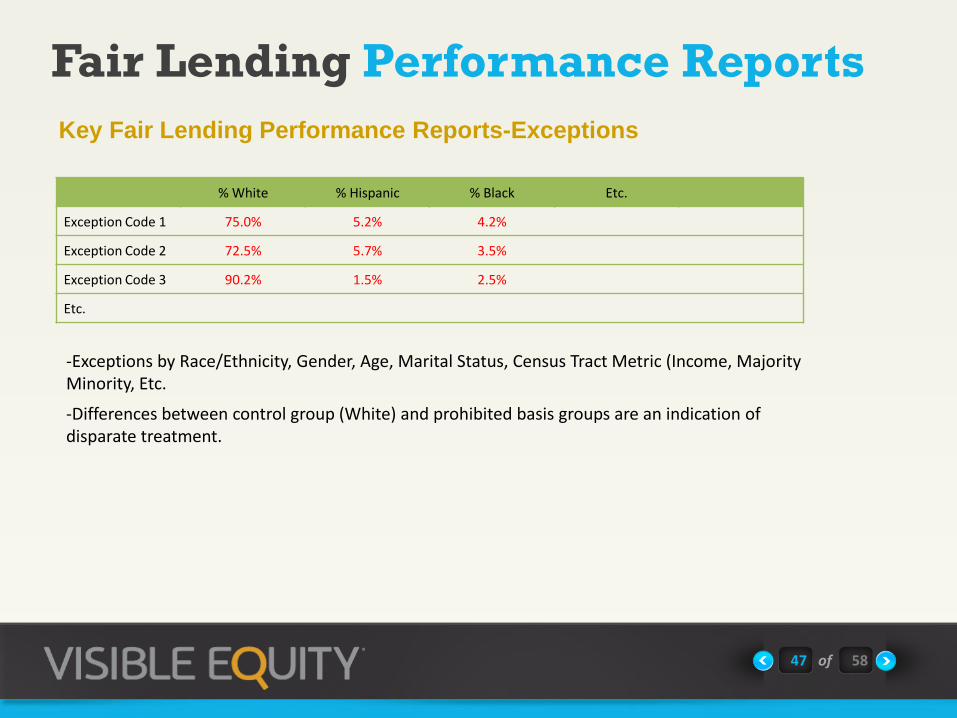

Key Fair Lending Performance Reports-Exceptions

% White % Hispanic % Black Etc.

Exception Code 1 75.0% 5.2% 4.2%

Exception Code 2 72.5% 5.7% 3.5%

Exception Code 3 90.2% 1.5% 2.5%

Etc.

-Exceptions by Race/Ethnicity, Gender, Age, Marital Status, Census Tract Metric (Income, Majority Minority, Etc.

-Differences between control group (White) and prohibited basis groups are an indication of disparate treatment.

Fair Lending Performance Reports

48 of 58

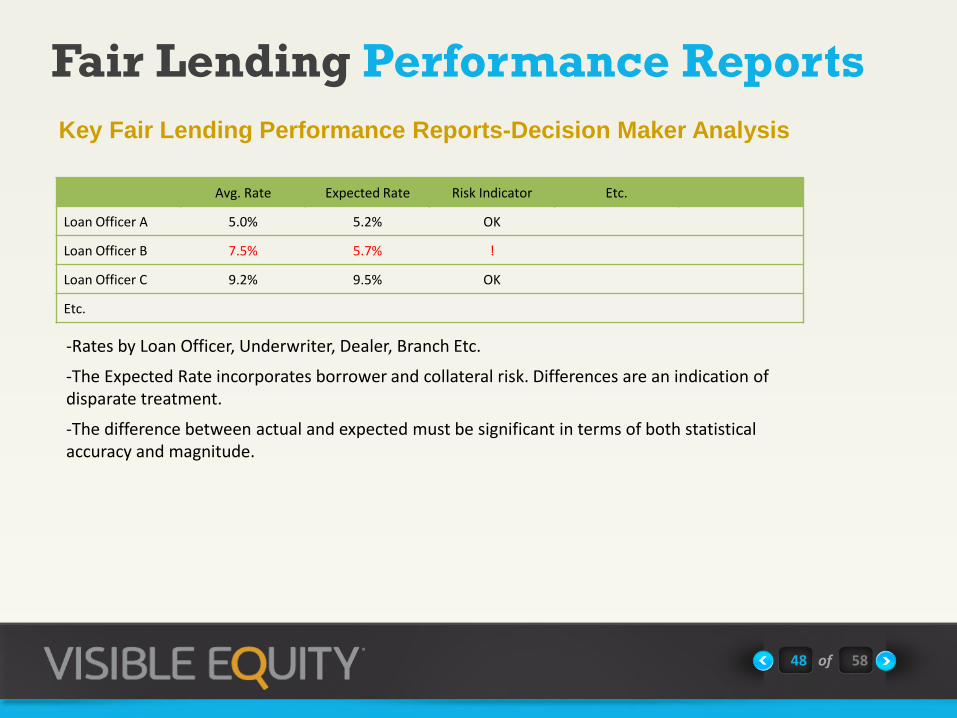

Key Fair Lending Performance Reports-Decision Maker Analysis

Avg. Rate Expected Rate Risk Indicator Etc.

Loan Officer A 5.0% 5.2% OK

Loan Officer B 7.5% 5.7% !

Loan Officer C 9.2% 9.5% OK

Etc.

-Rates by Loan Officer, Underwriter, Dealer, Branch Etc.

-The Expected Rate incorporates borrower and collateral risk. Differences are an indication of disparate treatment.

-The difference between actual and expected must be significant in terms of both statistical accuracy and magnitude.

Fair Lending Performance Reports

49 of 58

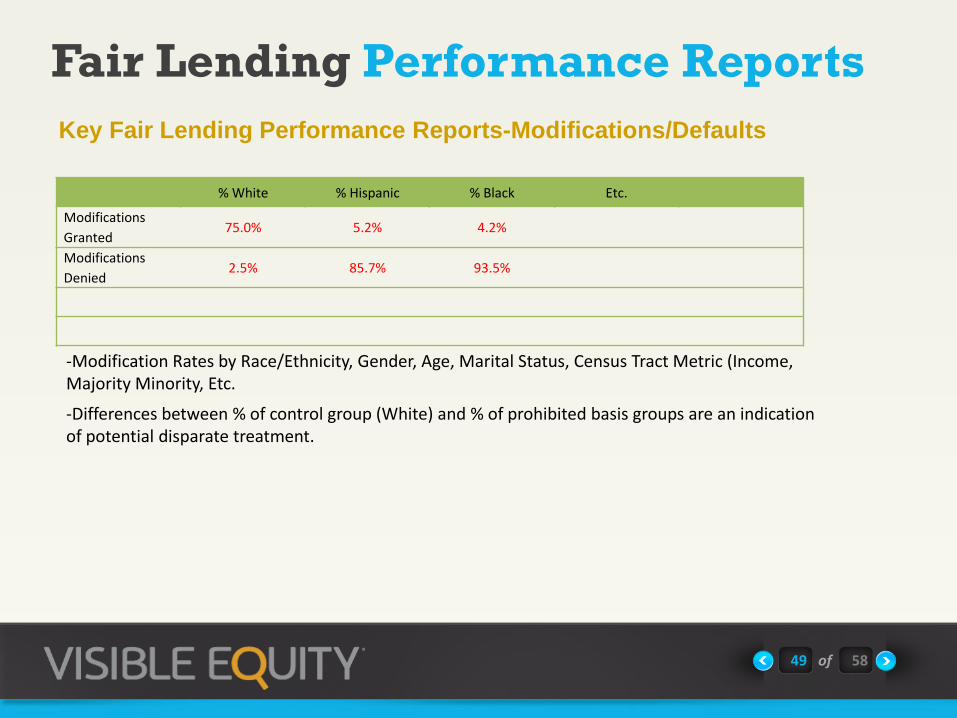

Key Fair Lending Performance Reports-Modifications/Defaults

% White % Hispanic % Black Etc.

Modifications

Granted 75.0% 5.2% 4.2%

Modifications

Denied 2.5% 85.7% 93.5%

-Modification Rates by Race/Ethnicity, Gender, Age, Marital Status, Census Tract Metric (Income, Majority Minority, Etc.

-Differences between % of control group (White) and % of prohibited basis groups are an indication of potential disparate treatment.

Fair Lending Statistical Analysis

50 of 58

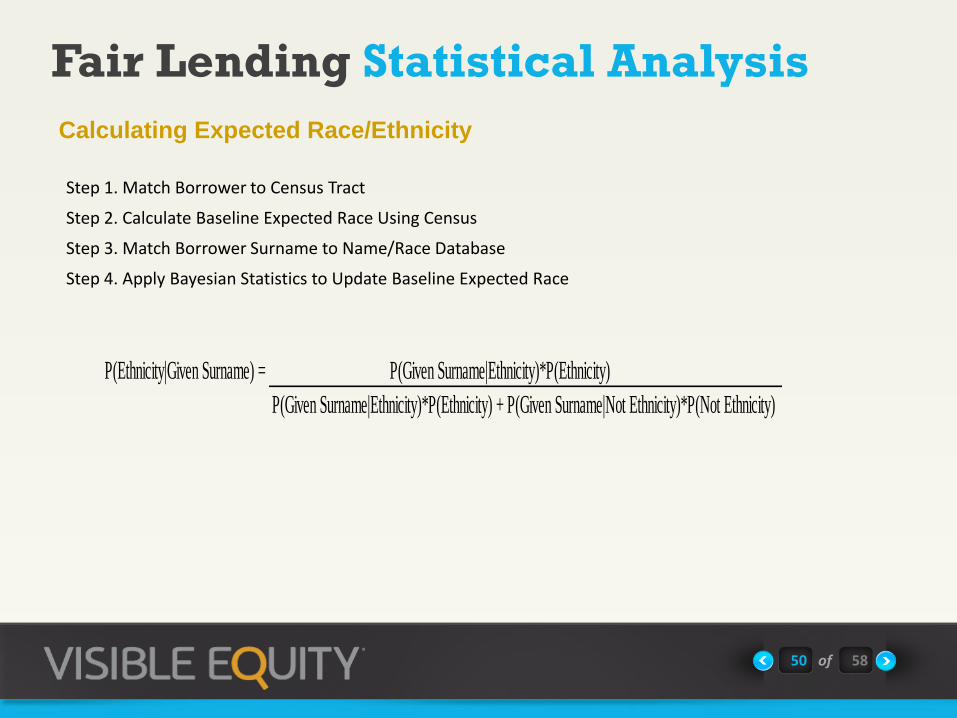

Calculating Expected Race/Ethnicity

Step 1. Match Borrower to Census Tract

Step 2. Calculate Baseline Expected Race Using Census

Step 3. Match Borrower Surname to Name/Race Database

Step 4. Apply Bayesian Statistics to Update Baseline Expected Race

P(Ethnicity|Given Surname) = P(Given Surname|Ethnicity)*P(Ethnicity)

P(Given Surname|Ethnicity)*P(Ethnicity) + P(Given Surname|Not Ethnicity)*P(Not Ethnicity)

Fair Lending Statistical Analysis

51 of 58

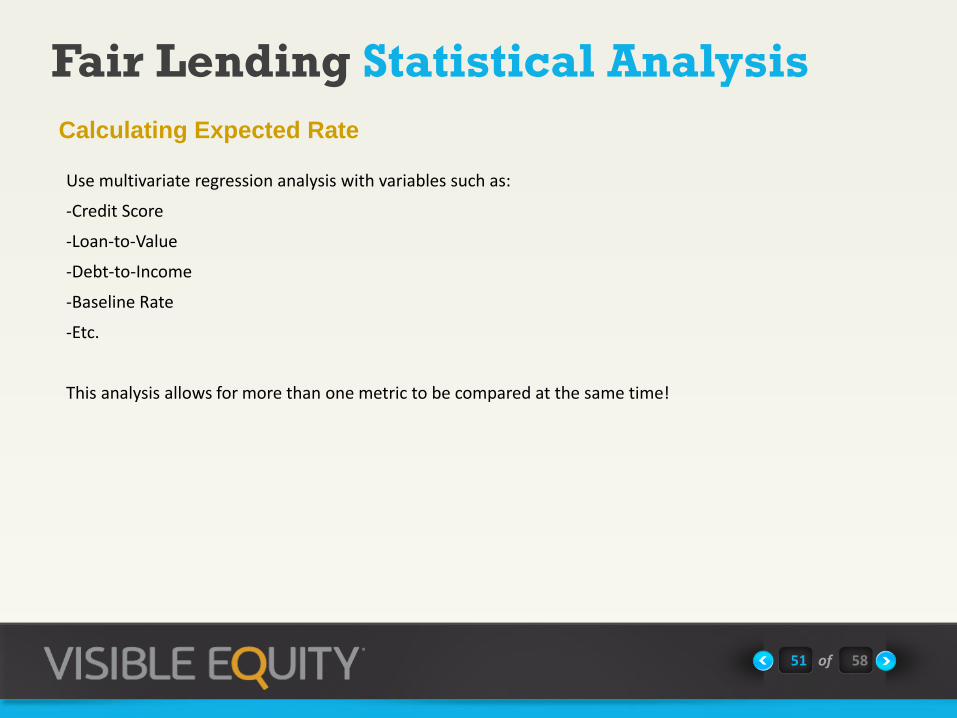

Calculating Expected Rate

Use multivariate regression analysis with variables such as:

-Credit Score

-Loan-to-Value

-Debt-to-Income

-Baseline Rate

-Etc.

This analysis allows for more than one metric to be compared at the same time!

Fair Lending Statistical Analysis

52 of 58

Comparative File Review

Use Only Marginal Transactions

Applicants that are neither clearly qualified nor clearly unqualified.

Determine Benchmark Applicant

The applicant with the least deficient reason for denial. In other words the most qualified of the denied applications for a given metric.

Compare marginal approvals with Benchmark.

If there are no approvals less qualified for a given metric then no disparate treatment exists. If there are approvals less qualified than the bench mark then potential disparate treatment exists.

Overlap Approval

An approved applicant that is no better qualified than the benchmark applicant. Note all overlap approvals and research further.

The goal of a comparative file review is to ensure all applicants received a comparable level of assistance, the credit decision for similarly situated borrowers was the same, the terms and conditions were substantially the same, and whether any remedial action is necessary.

Approve/Deny Decisions

Fair Lending Statistical Analysis

53 of 58

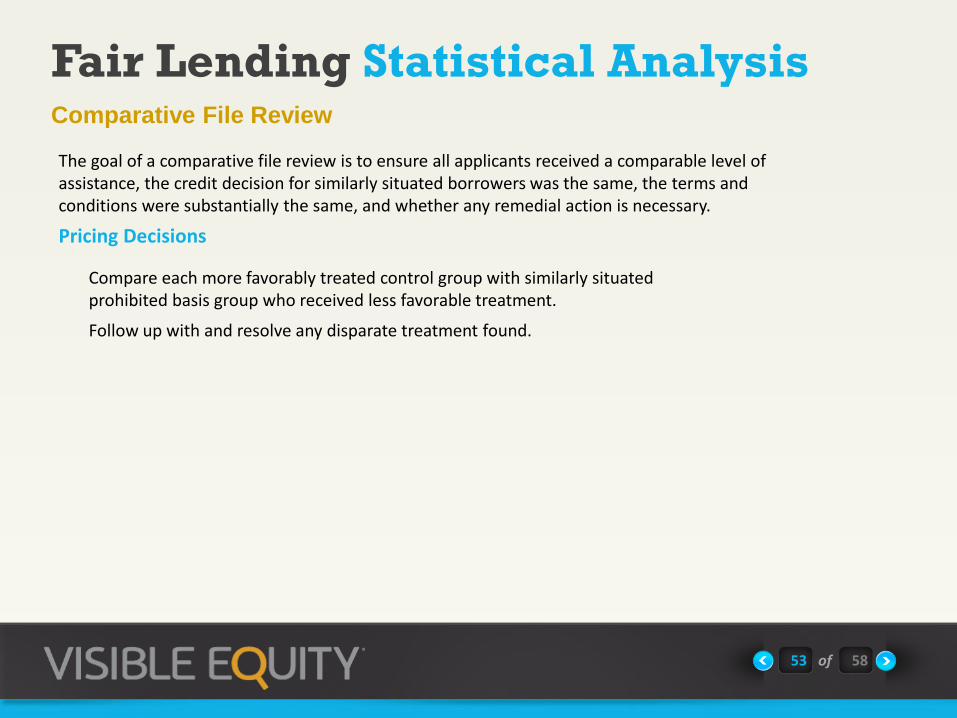

Comparative File Review

Compare each more favorably treated control group with similarly situated prohibited basis group who received less favorable treatment.

Follow up with and resolve any disparate treatment found.

The goal of a comparative file review is to ensure all applicants received a comparable level of assistance, the credit decision for similarly situated borrowers was the same, the terms and conditions were substantially the same, and whether any remedial action is necessary.

Pricing Decisions

Fair Lending Program

54 of 58

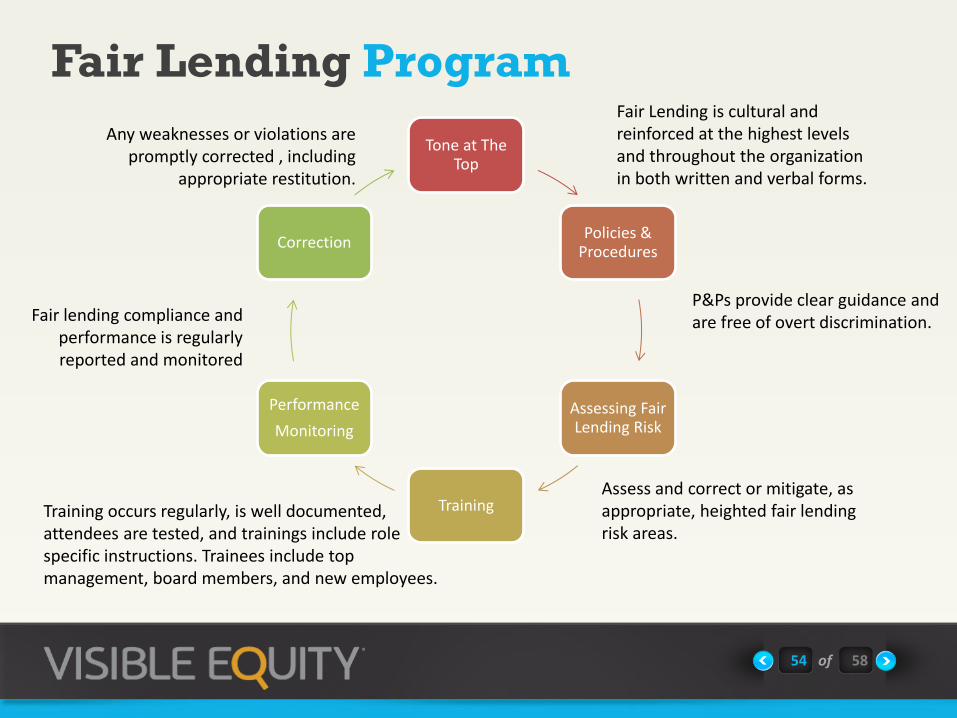

Tone at The Top

Policies & Procedures

Assessing Fair Lending Risk

Training

Performance

Monitoring

Correction

Fair Lending is cultural and reinforced at the highest levels and throughout the organization in both written and verbal forms.

P&Ps provide clear guidance and are free of overt discrimination.

Assess and correct or mitigate, as appropriate, heighted fair lending risk areas.

Training occurs regularly, is well documented, attendees are tested, and trainings include role specific instructions. Trainees include top management, board members, and new employees.

Any weaknesses or violations are promptly corrected , including

appropriate restitution.

Fair lending compliance and performance is regularly reported and monitored

Fair Lending Program

55 of 58

Financial Institutions make loans to any and all qualified borrowers using sound underwriting and pricing decisions applied consistency and equally to similarly situated borrowers without regard to any prohibited basis, such as race, gender, or age. “Fair Lending, then, is the natural state of bank (credit union) credit operations.” ABA Toolbox

Sources

56 of 58

-Visible Equity

-Comptroller’s Handbook, Fair lending, January 2010

-ABA Toolbox on Fair Lending

-Indirect Auto lending-Fair Lending Considerations, Webinar, August 6, 2013

-FDIC Presentation on Fair Lending

-NCUA, Office of Consumer Protection, Fair Lending Guide, March 2013

www.visibleequity.com

GET IN TOUCH

Address:

7070 S. Union Park Ave., Suite 260

Midvale, UT 84047

Phone:

+1 888 409 1560

Email:

facebook.com/visibleequity

twitter.com/visibleequity

57 of 58

https://www.linkedin.com/company/visible-equity

"Visible Equity makes consolidating our data and analyzing our concentration risk consistent and easy.“

Ray Wade American Airlines Credit Union

"Visible Equity realizes that all of us look at data in a different way, we all see things in a different perspective, and we're all looking at the data for different reasons. ”

Margaret Hunnicutt Landings Credit Union

“Using Visible Equity has allowed our credit union to focus on addressing potential problems rather than spending endless hours running reports and analyzing data. We continue to be impressed with the service we receive and with the functionality, accuracy, and delivery of the product. Visible Equity has been a great partner to work with for our credit union.”

Jeff Meyers Utah Community Credit Union

58 of 58