Embed Size (px)

Citation preview

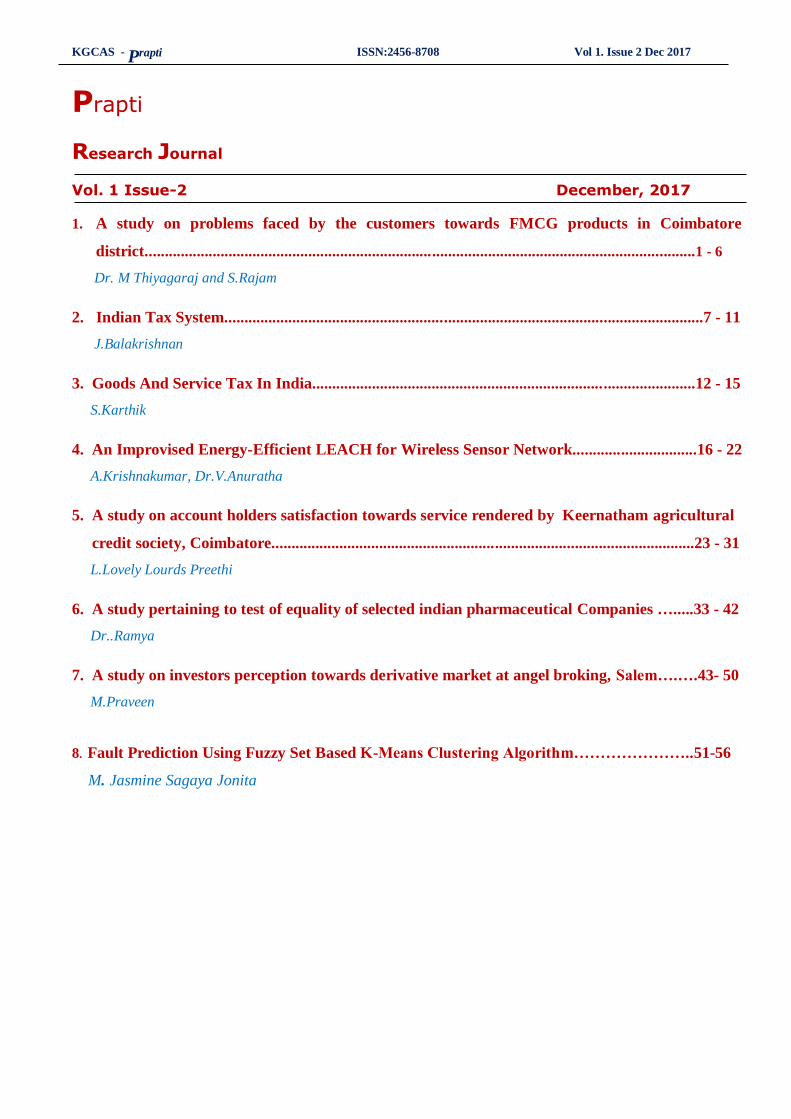

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

Prapti

Research Journal

Vol. 1 Issue-2 December, 2017

1. A study on problems faced by the customers towards FMCG products in Coimbatore

district..........................................................................................................................................1 - 6

Dr. M Thiyagaraj and S.Rajam

2. Indian Tax System........................................................................................................................7 - 11

J.Balakrishnan

3. Goods And Service Tax In India................................................................................................12 - 15

S.Karthik

4. An Improvised Energy-Efficient LEACH for Wireless Sensor Network...............................16 - 22

A.Krishnakumar, Dr.V.Anuratha

5. A study on account holders satisfaction towards service rendered by Keernatham agricultural

credit society, Coimbatore..........................................................................................................23 - 31

L.Lovely Lourds Preethi

6. A study pertaining to test of equality of selected indian pharmaceutical Companies ….....33 - 42

Dr..Ramya

7. A study on investors perception towards derivative market at angel broking, Salem….….43- 50

M.Praveen

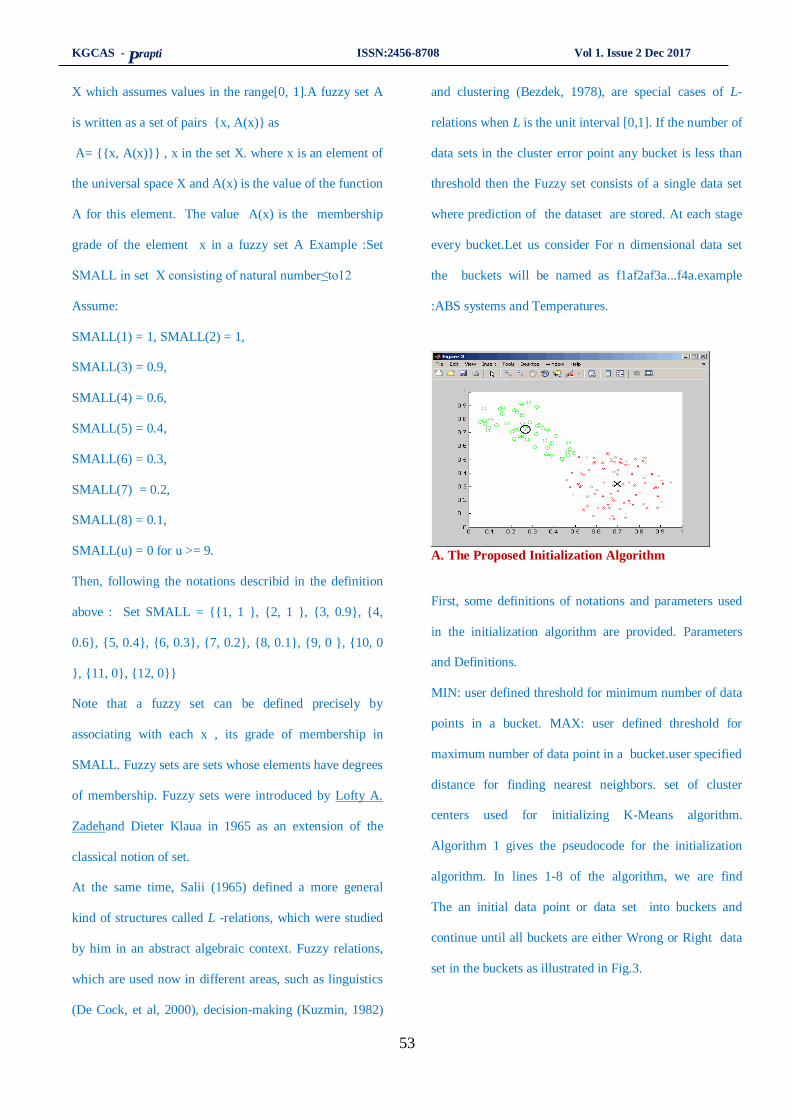

8. Fault Prediction Using Fuzzy Set Based K-Means Clustering Algorithm…………………..51-56

M. Jasmine Sagaya Jonita

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

1

A Study on Problems Faced by the Customers

towards FMCG Products in Coimbatore District Dr. M. Thiyagaraj1 , S.Rajam2

Abstract

In Indian economy, the Fast Moving Consumer Goods sector

experienced outstanding growth in the past decade. This sector

is an important contributor to India’s Gross Domestic Product.

This industry in Coimbatore district is shaping up under the

umbrella of organized sector and it is distinctly classified into

four different segments like Food and Beverage industry,

Cleaning, Disinfectants and Home Care, Personal care and

Electronics. The study is descriptive in nature both primary

and secondary data to be considered for this analysis. 750

samples are randomly selected in the rural area of Coimbatore

District and analysed for the study. Objectives are framed and

required tools to be applied for this study. Through this study

Problems towards FMCG Product have been analysed and

provide the suitable suggestions to improve the services.

Keywords: Fast Moving, Gross Domestic Product, Indian

economy, Food and Beverage, Problems.

1. INTRODUCTION

India is one of the largest economies in the world in terms

Associate Professor1,

Department of Commerce,

Dr.S.N.S Rajalaskmi Arts and Science College,

Chinavedampatti (PO). Coimbatore.

Professor2,

Department of Commerce,

Kongunadu Arts and Science College,

Kovundampalayam, Coimbatore.

of purchasing power and increasing consumer spending,

next to China.The National Council of Applied Economic

Research (NCAER) survey report says that there are 720

million consumers across the villages in rural India. Hence,

the development of the nation largely depends upon the

development of the rural population. The Indian rural

marketing environment increased the awareness along with

rise in income levels.

In Indian economy, the Fast Moving Consumer

Goods (FMCG) sector experienced outstanding growth in

the past decade. FMCG sector is an important contributor to

India’s Gross Domestic Product (GDP).

It is the fourth largest sector in the Indian economy.

This sector also creates employment for around three

million people in downstream activities, which are generally

carried out in smaller towns of rural India.

The development of consumerism in the Coimbatore

district is due to Industrialization. This increased the growth

of FMCG market in Coimbatore district. The FMCG

industry in Coimbatore district is shaping up under the

umbrella of organized sector and it is distinctly classified

into four different segments like Food and Beverage

industry, Cleaning, Disinfectants and Home Care, Personal

care and Electronics.

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

2

1.1 FAST MOVING CONSUMER GOODS (FMCG)

Products which have a quick turnover, and relatively

low cost are known as Fast Moving Consumer Goods

(FMCG). FMCG products are those that get replaced within

a year. Examples of FMCG generally include a wide range

of frequently purchased consumer products such as

toiletries, soap, cosmetics, tooth cleaning products, shaving

product and detergents, as well as other non-durables such

as glassware, bulbs, batteries, paper products, and plastic

goods.

FMCG products may also include pharmaceuticals,

consumer electronics, packaged food products, soft drinks,

tissue paper, and chocolate bars. A subset of FMCG

products is Fast Moving Consumer Electronics which

includes innovative electronic products such as mobile

phones, MP3 players, digital cameras, GPS Systems and

Laptops. These are replaced more frequently than other

electronic products. White goods in FMCG refer to

household electronic items such as Refrigerators, T.Vs,

Music Systems, etc.,

2. REVIEW OF LITERATURE

Mona Chaudhary and SnehaGhai (2014) conducted a study

to find out the perception of youngsters towards cause-

related marketing of FMCG category and its impact on their

buying behaviour. It was found that the perception of youth

was the most important aspect to contribute to the society.

The researchers appreciate the initiatives taken by the

marketers who join hands with the NGO working for a

noble cause. A well-designed cause-marketing campaign

can bring benefits to the company. It works as a great

differentiator in FMCG as there are so many similar

offerings in the market. A well-rated and effectively

communicated cause marketing campaign creates a positive

impact on buying behaviour of the young consumers in

favour of the brand.

Bloom et al. (2006) have clearly written in their

study that companies have been able to use cause-related

marketing to make a distinction of their brands from

competitors in consumers' minds and to get desirable

effects, including greater efficiency for other marketing

efforts, an ability to charge higher prices, increased market

share, greater brand loyalty and better stakeholders

management.

Cheron Emmanuel et al. (2012) carried out a study

that aimed to examine the effect of brand-cause fit and

campaign duration on company and brand image,

commercial objectives and buying intention as perceived by

Japanese consumers and aimed to evaluate the moderating

role of gender and participation in philanthropic activities

on the impact of cause-related marketing (CRM)

programmes in Japan. An experimental design was used

with 196 Japanese subjects completing a survey online.

Results showed that a high brand-cause fit was found to

elicit more positive attitudes towards the CRM programme

than campaign duration. Japanese female respondents were

showing more favourable attitudes than men, confirming

results in previous research studies conducted in the West.

Hou, Jundong et al. (2008) examined several factors

that potentially influenced a consumer's purchasing decision

to participate in cause-related marketing (CRM)

programmes in the Chinese context. This study was also

intended to test empirically the hypothesized relationship

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

3

between cause's attributes of causes and purchase intention

in such an environment. The results show that the degree of

causes participation for consumer, fit between the brand and

the cause, cause importance, congruence between the firm's

product and the cause. The cause proximity plays an

important role in consumers' attitudes towards the product.

Kalaiselvi.S (2014), conducted “A study on

consumers preference and satisfaction towards Amway

Nutrition Products with special reference to Coimbatore

city, concluded that

3. STATEMENT OF THE PROBLEM

In modern world, the consumption of FMCG

products plays an important role in our day to day life. Rural

customers are facing the problem in quality product,

availability and accessibility. Internationally the market for

FMCG products has expanded significantly during the last

decade. In recent years the demand for FMCG products is

growing among households. FMCG products are produced

by many companies and sold in their brand names. In this

situation it is required to find out and problems faced by the

consumers’.

4. SCOPE OF THE STUDY

The study is conducted to find out the Rural

Consumers’ problems towards the FMCG Products in

Coimbatore districts. Coimbatore is the second largest

district in the state of Tamil Nadu.

Hence the study is very essential to this particular

area and the researcher has focused on rural areas in the

Coimbatore district. To attempt the specified objectives, 750

respondents were selected.

5. OBJECTIVE OF THE STUDY

To analyze the problems faced by the consumers

while using the FMCG products.

6. RESEARCH METHODOLOGY

A pilot study was conducted with 50 consumers of

retail outlets in Coimbatore District. Interview schedules

were used as a major tool to collect first-hand information

from the sample respondents. Field survey technique was

adopted to collect information from the sample respondents.

The interview schedule has been pre-tested and

modified to suit the purposes of this study. Totally 750

respondents were taken for the study. Both primary data and

secondary data have been used in this study. The primary

data have been collected from FMCG consumers in

Coimbatore district, with the help of an Interview Schedule.

The secondary data have been drawn from different

sources like newspapers, magazines, journals, books,

websites and pamphlets. In this study Garrett Ranking

method has been used to findout the problems faced by the

customers towards FMCG products in Rural area.

7. LIMITATIONS OF THE STUDY

The geographical coverage of the study is

restricted only to rural part of Coimbatore District

and hence, the results of the study cannot be

generalized in its original form to other parts of the

state or country.

The study is confined only to the rural people who

are residing in the rural part of the Coimbatore

District. The study in confined only selected

FMCG. All the FMCG were not available in rural

areas.

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

4

8. DATA ANALYSIS AND INTERPRETATION

8.1 GARRETT’S RANKING TECHNIQUES

With the help of Garrett’s table, the percent

position estimated is converted into scores. Then for each

factor, the scores of each individual are added and then total

value of scores and mean values of score is calculated. The

factors having highest mean value is considered to be the

most important factor. In this study Garrett ranking

technique is used to know the most important problem faced

by the customers while using the FMCG products.

In this study, to know the highest problem faced by the

respondents Garrett’s ranking techniques was used. In this

study FMCG products are Classified three groups

1.Food and Bevearage

2.Personal care Products

3.Health care Products

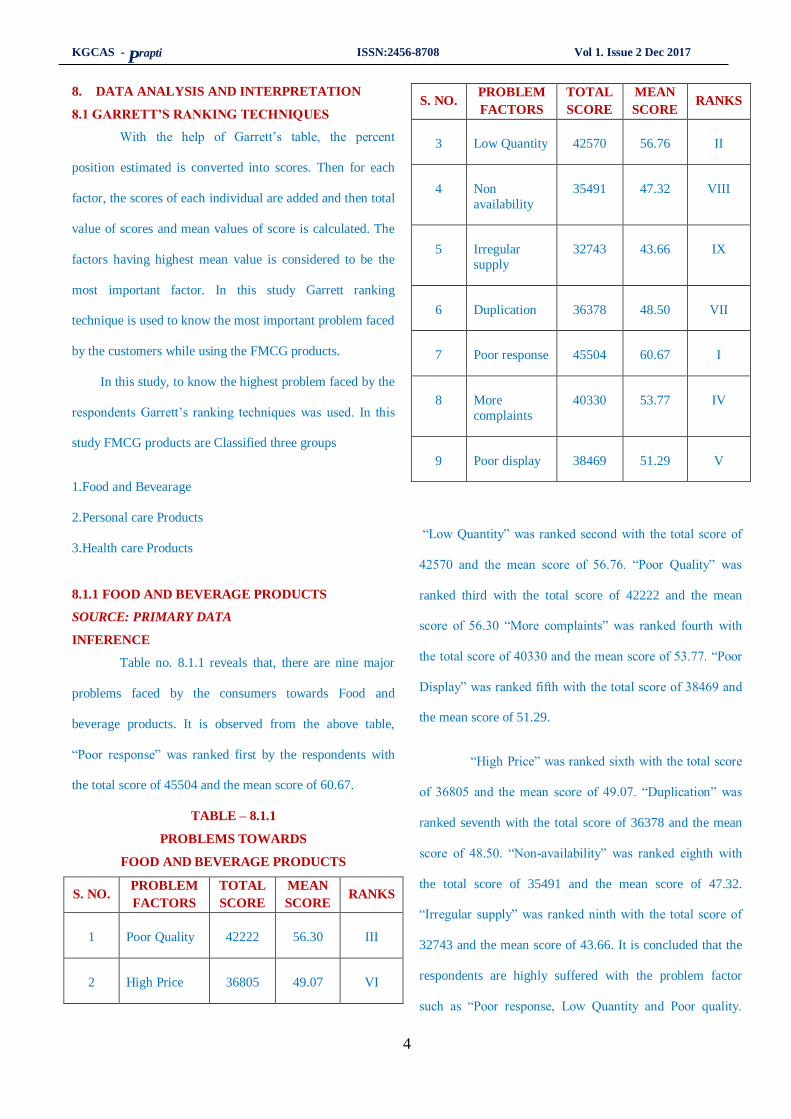

8.1.1 FOOD AND BEVERAGE PRODUCTS

SOURCE: PRIMARY DATA

INFERENCE

Table no. 8.1.1 reveals that, there are nine major

problems faced by the consumers towards Food and

beverage products. It is observed from the above table,

“Poor response” was ranked first by the respondents with

the total score of 45504 and the mean score of 60.67.

TABLE – 8.1.1

PROBLEMS TOWARDS

FOOD AND BEVERAGE PRODUCTS

S. NO. PROBLEM

FACTORS

TOTAL

SCORE

MEAN

SCORE RANKS

1 Poor Quality 42222 56.30 III

2 High Price 36805 49.07 VI

S. NO. PROBLEM

FACTORS

TOTAL

SCORE

MEAN

SCORE RANKS

3 Low Quantity 42570 56.76 II

4 Non

availability

35491 47.32 VIII

5 Irregular

supply

32743 43.66 IX

6 Duplication 36378 48.50 VII

7 Poor response 45504 60.67 I

8 More

complaints

40330 53.77 IV

9 Poor display 38469 51.29 V

“Low Quantity” was ranked second with the total score of

42570 and the mean score of 56.76. “Poor Quality” was

ranked third with the total score of 42222 and the mean

score of 56.30 “More complaints” was ranked fourth with

the total score of 40330 and the mean score of 53.77. “Poor

Display” was ranked fifth with the total score of 38469 and

the mean score of 51.29.

“High Price” was ranked sixth with the total score

of 36805 and the mean score of 49.07. “Duplication” was

ranked seventh with the total score of 36378 and the mean

score of 48.50. “Non-availability” was ranked eighth with

the total score of 35491 and the mean score of 47.32.

“Irregular supply” was ranked ninth with the total score of

32743 and the mean score of 43.66. It is concluded that the

respondents are highly suffered with the problem factor

such as “Poor response, Low Quantity and Poor quality.

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

5

These three factors are most important prblems faced by the

FMCG customer towards Food and Beverage Products.

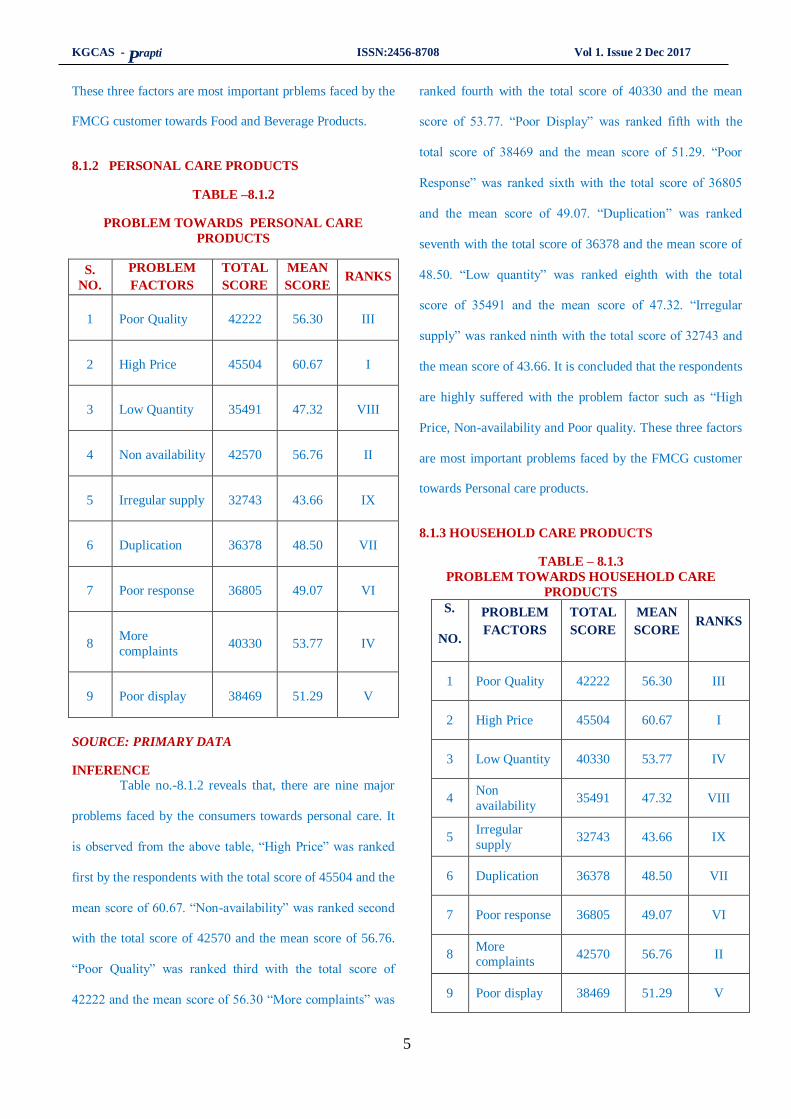

8.1.2 PERSONAL CARE PRODUCTS

TABLE –8.1.2

PROBLEM TOWARDS PERSONAL CARE

PRODUCTS

S.

NO.

PROBLEM

FACTORS

TOTAL

SCORE

MEAN

SCORE RANKS

1 Poor Quality 42222 56.30 III

2 High Price 45504 60.67 I

3 Low Quantity 35491 47.32 VIII

4 Non availability 42570 56.76 II

5 Irregular supply 32743 43.66 IX

6 Duplication 36378 48.50 VII

7 Poor response 36805 49.07 VI

8 More

complaints 40330 53.77 IV

9 Poor display 38469 51.29 V

SOURCE: PRIMARY DATA

INFERENCE

Table no.-8.1.2 reveals that, there are nine major

problems faced by the consumers towards personal care. It

is observed from the above table, “High Price” was ranked

first by the respondents with the total score of 45504 and the

mean score of 60.67. “Non-availability” was ranked second

with the total score of 42570 and the mean score of 56.76.

“Poor Quality” was ranked third with the total score of

42222 and the mean score of 56.30 “More complaints” was

ranked fourth with the total score of 40330 and the mean

score of 53.77. “Poor Display” was ranked fifth with the

total score of 38469 and the mean score of 51.29. “Poor

Response” was ranked sixth with the total score of 36805

and the mean score of 49.07. “Duplication” was ranked

seventh with the total score of 36378 and the mean score of

48.50. “Low quantity” was ranked eighth with the total

score of 35491 and the mean score of 47.32. “Irregular

supply” was ranked ninth with the total score of 32743 and

the mean score of 43.66. It is concluded that the respondents

are highly suffered with the problem factor such as “High

Price, Non-availability and Poor quality. These three factors

are most important problems faced by the FMCG customer

towards Personal care products.

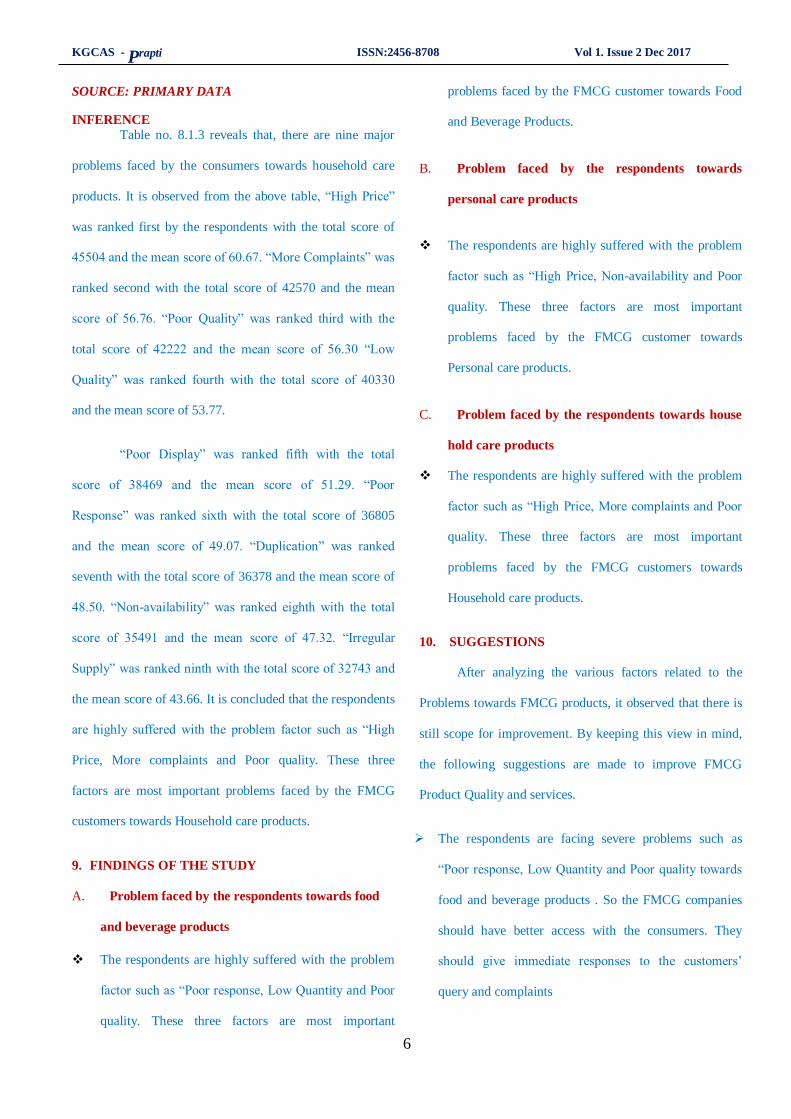

8.1.3 HOUSEHOLD CARE PRODUCTS

TABLE – 8.1.3

PROBLEM TOWARDS HOUSEHOLD CARE

PRODUCTS

S.

NO.

PROBLEM

FACTORS

TOTAL

SCORE

MEAN

SCORE

RANKS

1 Poor Quality 42222 56.30 III

2 High Price 45504 60.67 I

3 Low Quantity 40330 53.77 IV

4 Non

availability 35491 47.32 VIII

5 Irregular

supply 32743 43.66 IX

6 Duplication 36378 48.50 VII

7 Poor response 36805 49.07 VI

8 More complaints

42570 56.76 II

9 Poor display 38469 51.29 V

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

6

SOURCE: PRIMARY DATA

INFERENCE

Table no. 8.1.3 reveals that, there are nine major

problems faced by the consumers towards household care

products. It is observed from the above table, “High Price”

was ranked first by the respondents with the total score of

45504 and the mean score of 60.67. “More Complaints” was

ranked second with the total score of 42570 and the mean

score of 56.76. “Poor Quality” was ranked third with the

total score of 42222 and the mean score of 56.30 “Low

Quality” was ranked fourth with the total score of 40330

and the mean score of 53.77.

“Poor Display” was ranked fifth with the total

score of 38469 and the mean score of 51.29. “Poor

Response” was ranked sixth with the total score of 36805

and the mean score of 49.07. “Duplication” was ranked

seventh with the total score of 36378 and the mean score of

48.50. “Non-availability” was ranked eighth with the total

score of 35491 and the mean score of 47.32. “Irregular

Supply” was ranked ninth with the total score of 32743 and

the mean score of 43.66. It is concluded that the respondents

are highly suffered with the problem factor such as “High

Price, More complaints and Poor quality. These three

factors are most important problems faced by the FMCG

customers towards Household care products.

9. FINDINGS OF THE STUDY

A. Problem faced by the respondents towards food

and beverage products

The respondents are highly suffered with the problem

factor such as “Poor response, Low Quantity and Poor

quality. These three factors are most important

problems faced by the FMCG customer towards Food

and Beverage Products.

B. Problem faced by the respondents towards

personal care products

The respondents are highly suffered with the problem

factor such as “High Price, Non-availability and Poor

quality. These three factors are most important

problems faced by the FMCG customer towards

Personal care products.

C. Problem faced by the respondents towards house

hold care products

The respondents are highly suffered with the problem

factor such as “High Price, More complaints and Poor

quality. These three factors are most important

problems faced by the FMCG customers towards

Household care products.

10. SUGGESTIONS

After analyzing the various factors related to the

Problems towards FMCG products, it observed that there is

still scope for improvement. By keeping this view in mind,

the following suggestions are made to improve FMCG

Product Quality and services.

The respondents are facing severe problems such as

“Poor response, Low Quantity and Poor quality towards

food and beverage products . So the FMCG companies

should have better access with the consumers. They

should give immediate responses to the customers’

query and complaints

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

7

The respondents are facing the problem factor such as

“High Price, Non-availability and Poor quality towards

personal care products the FMCG companies are

recommended to promote FMCG in lines of pricing

strategy rather than just making low price appeals.

The respondents are highly suffered with the problem

factor such as “High Price, More complaints and Poor

quality towards house hold care products. So the

company should take necessary steps in preventing the

quality of the product.

11. CONCLUSION

The FMCG sector has had much better time in the

recent years. The FMCG market is very big in Coimbatore

Districts and it is competitive also. . In recent days we have

seen a lot of innovation in the manufacturing process and

improvement in the quality of FMCG product. With this

revolution in technology the FMCG product also increases.

Logistics companies play important role in the distribution

of FMCG. The rural people are mainly price conscious but

not so brand loyal, so they may switch to other quality

product with low price, they do not consider the taste as

important factor while making purchase decision. As well

the rural consumers are very low effect of brand ambassador

on their buying behaviour but advertisement definitely helps

them to increase their product knowledge.

12. REFERENCES

1. Dr.S.P.Gupta, Statistical Methods, Sultan Chand & Sons

Educational Publishers, New Delhi-2006.

2. J.Llian Mercer, ―Great Customer Service‖, Allen and Unwin

Publishing, New Delhi, Ed-2003.

3. Mona Chaudhary & SnehaGhai, (2014). “Perception of

Young Consumers towards Cause Marketing of FMCG

Brands”, International Journal of Sales & Marketing

Management Research and Development, Vol. 4, Issue 2,

Pp.21-26.

4. Cheron,Emmanuel; Kohlbacher, Florian; Kusuma, Kaoru,

(2012).“The effects of brand-cause fit and campaign duration

on consumer perception of cause-related marketing in

Japan”, The Journal of Consumer Marketing , Vol. 29, Issue

5 : Pp.357-368.

5. Hou, Jundong; Du, Lanying; Li, Jianfeng (2008).“Cause's

attributes influencing consumer's purchasing intention:

empirical evidence from China”, Asia Pacific Journal of

Marketing and Logistics, Vol. 20 Issue 4, Pp.363-380.

6. Kalaiselvi.S (2014), “A study on consumers preference and

satisfication towards Amway Nutrition Products with special

reference to Coimbatore city” Global Journal for Research

Analysis, Vol.3,No.10, ISSN: 2277-8160.

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

8

Indian Tax System

J.Balakrishnan

Abstract

Tax estimate the exact value to the tax payer and tax value are

collected based on the Income level of the tax payer. The

economic level are increased by the tax collection of the

government.

1. INTRODUCTION

Role of the Central and State Government

Central government of India levies taxes like as

Income tax, customs duty, service tax and central excise

duty.

State governments to levy income tax on agricultural

income, professional tax, value added tax, state excise duty,

land revenue and stamp duty. The local bodies are allowed

to collect octroi, property tax and other taxes on various

services like drainage and water supply.

Organizational Structure

The CBIT is headed by CBIT chairman and also

comprise six members. Member (Income Tax)

Member (Legislation and Computerization)

Member (Revenue)

Member (personnel & Vigilance)

Member (Investigation)

Member (Audit & Judicial)

Assistant Professor in Commerce,

Bishop Ambrose College,

Coimbatore.

The chairperson holds the rank of special Secretary to

Government of India while the members rank of additional

Secretary to Government of India.

The CBIT chairmen and members of CBIT are selected

from Indian Revenue Services (IRS), a premier civil

services of India, whose members constitute the top

management of Income Tax Department

2. OBJECTIVES OF TAXATION

The following are the main objectives of taxation.

1. Primary 2. Secondary

Primary

Raising more revenues

Preventing the concentration of wealth in a few

hands

Re-distribution of wealth for the common and social

purposes

Maintaining the welfare of the states.

Secondary

Encouraging the essential productions

Maintaining balanced economic growth

Enforcing government policy

Increasing savings and investment by public

Reduction of unemployment problems

Removal of Regional disparities among the states

Importance

There are many responsibilities of state to its

countrymen. State is represented by the government. The

government of any country performs a number of activities

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

9

in order to maintain law and order, peace and security,

satisfying with the requirement of basic needs of public

utilities. It also indicates various development programmes

and maintains diplomatic and friendly relation with other

nations in the world.

3. BENEFITS OF TAXES

Tax encourages savings and investment if a tax

payer can invest amount to his/her business and

they has to reduce in the tax payment to the

government.

Tax payer has to file tax returns, it helps when you

are in getting loan from bank.

4. ESSENTIALS OF TAX

A tax is a compulsory contribution of a person or

entity to the state as per the rules.

The tax payer does not receive direct and or special

benefit in return.

It is spent by the government for the common

interest and benefit of the people.

It is paid only by those persons and entities who

earn income exceeding a certain specified limit.

Non-Payment Penalty

Suppose the payment of tax is avoiding means the

tax payer has to pay their own money. A customer fail to

pay tax when the tax amount returns or extended and have

time to pay owe money in the same month and has to pay a

non-payment penalty equal to 0.5% of the due tax will be

levied.

Underpayment Penalty

When a customer does not make the whole

payment owed on tax and Taxes must be paid as income is

earned, and most taxpayers comply with the rule for fear

that income tax will be withheld from their pay cheques.

The independent contractors who work side jobs in

addition to their salaried employment or as full time

workers are responsible for ensuring that the tax due on

their earnings are covered through estimated tax payments.

5. TYPES OF TAXES

Two Types of taxes like

1. direct Tax and

2. Indirect Taxes

Direct Tax

Central Board of Direct Taxes (CBDT) is a part of

the Department of Revenue and it overlooks these direct

taxes.

Types of Direct Tax

Income Tax Act

Wealth Tax Act

Gift Tax Act

Interest Tax Ac:

Capital Gains Tax

Perquisite Tax

Corporate Tax – Types

Minimum Alternative Tax

Fringe Benefit Tax

Dividend Distribution Tax

Indirect Tax

Indirect Tax is depending on the goods and

services. It is differ from direct tax and it is not levied on a

person who pays them tax directly to the government.

Examples of Indirect Tax

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

10

VAT (Value Added Tax), Taxes on Imported Goods, Sales

Tax, etc.

Sales Tax

Sales tax is a tax that is levied on the sale of a

product. The product can be something that was produced in

India or imported and can even cover services rendered. The

sales tax is levied on the seller of the product who then

transfers it onto the person who buys said product with the

sales tax added to the price of the product. The limitation of

the sales tax is that it can be levied only ones for a particular

product, which means that if the product is sold a second

time, sales tax cannot be applied to it.

Service Tax

Goods sold in India is priced in the Sales tax ,so

the service tax added to services provided in India. In

budget 2015, it was announced that the service tax will be

increased from 12.36% to 14%. It is not added on goods but

on companies that provide services and is collected every

month otherwise once every quarter based on how the

services are provided. If the establishment is an individual

service provider then the service tax is paid only once the

customer pays the bills.

The major service which comes under vicinity of

service tax are telephone, tour operator, architect, interior

decorator, advertising, beauty parlor, health center, banking

and financial service, event management, maintenance

service, consultancy service

Current rate of interest on service tax is 14.5%.

GST - Goods and Service Tax

GST is the largest reform in India’s indirect tax

structure since the market started opening up about 25 years

ago. The GST is a consumption-based tax, as it is applicable

when the consumption takes place. The GST is included on

value-added goods and services at each stage of

consumption in the supply chain. The GST payable on the

goods and services can be set off against the GST payable

on the supply of goods and services, the merchant will pay

the applicable GST rate but can claim it back through the

tax credit mechanism.

The Rajya Sabha passed the Constitutional Amendment Bill

required for introduction of GST bills on 3 August 2016

with more than two-third majority.

The IT framework and services for implementation

of the new taxation system will be managed by "Goods and

Services Tax Network (GSTN)", a non-government

company set up by the Centre and states.

GST rates in India ranges from 0% up to 50%:

which includes 0%, 5%, 12%, 18%, 28%, 29%, 31%, 43%,

45%, 48%, 50% {Additional cess includes (28%+1%),

(28%+3%), (28%+15%), (28%+17%), (28%+20%),

(28%+22%)} varying for both goods and services on 1211

items and services.

EV's (Full Electric Vehicles): 12%

Hybrid Vehicles: 43%

Value Added Tax

VAT, is a commercial tax is not applicable on

commodities that are zero rated (eg. food and essential

drugs) or those that fall under exports. The value added tax

is levied at all the stages of the supply chain, right from the

manufacturers, dealers and distributors to the end user.

The value added tax is a tax that is levied at the

discretion of the state government and not all the states

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

11

implemented it when it was first announced. The tax is

levied on various goods sold in the state and the amount of

the tax is decided by the state government itself.

Custom duty & Octroi:

When the customer purchases anything that needs

to be imported from another country, a charge is applied on

it and that is the customs duty. The custom applies to all the

products that come in via land, sea or air. Even the customer

bring in products bought in another country to India, a

customs duty can be levied on it. The use of the customs

duty is to ensure that all the goods entering the country are

taxed and paid for. Customs duty ensures that goods for

other countries are taxed.

Octroi is means to ensure that goods crossing state

borders within India are taxed appropriately. Octroi levied

by the state government and functions in much the same

way as customs duty does.

Excise duty

Central Excise Act, 1944, it imposes a duty of excise on goods manufactured or produced in India. Excise duty as a

duty or tax levied upon the manufacture or production of commodities with in the country intended for home consumption.

CENTRAL BOARD OF DIRECT TAXES

Central government of India

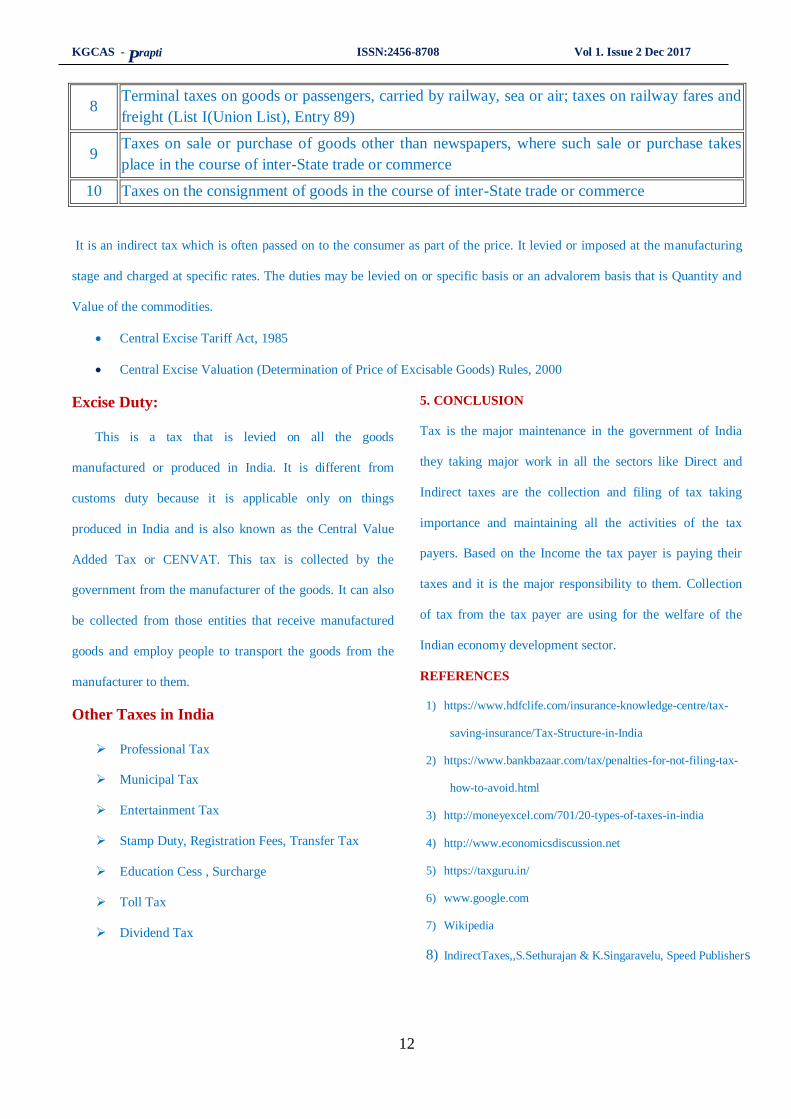

S. No. Parliament of India

1 Taxes on income other than agricultural income (List I(Union List), Entry 82)

2 Duties of customs including export duties (List I(Union List), Entry 83)

3

Duties of excise on tobacco and other goods manufactured or produced in India except (i) alcoholic liquor for

human consumption, and (ii) opium, Indian hemp and other narcotic drugs and narcotics, but including

medicinal and toilet preparations containing alcohol or any substance included in (ii). (List I(Union List), Entry

84)

4 Corporation Tax (List I(Union List), Entry 85)

5 Taxes on capital value of assets, exclusive of agricultural land, of individuals and companies,

taxes on capital of companies (List I(Union List), Entry 86)

6 Estate duty in respect of property other than agricultural land (List I(Union List), Entry 87)

7 Duties in respect of succession to property other than agricultural land (List I(Union List), Entry

88)

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

12

8 Terminal taxes on goods or passengers, carried by railway, sea or air; taxes on railway fares and

freight (List I(Union List), Entry 89)

9 Taxes on sale or purchase of goods other than newspapers, where such sale or purchase takes

place in the course of inter-State trade or commerce

10 Taxes on the consignment of goods in the course of inter-State trade or commerce

It is an indirect tax which is often passed on to the consumer as part of the price. It levied or imposed at the manufacturing

stage and charged at specific rates. The duties may be levied on or specific basis or an advalorem basis that is Quantity and

Value of the commodities.

Central Excise Tariff Act, 1985

Central Excise Valuation (Determination of Price of Excisable Goods) Rules, 2000

Excise Duty:

This is a tax that is levied on all the goods

manufactured or produced in India. It is different from

customs duty because it is applicable only on things

produced in India and is also known as the Central Value

Added Tax or CENVAT. This tax is collected by the

government from the manufacturer of the goods. It can also

be collected from those entities that receive manufactured

goods and employ people to transport the goods from the

manufacturer to them.

Other Taxes in India

Professional Tax

Municipal Tax

Entertainment Tax

Stamp Duty, Registration Fees, Transfer Tax

Education Cess , Surcharge

Toll Tax

Dividend Tax

5. CONCLUSION

Tax is the major maintenance in the government of India

they taking major work in all the sectors like Direct and

Indirect taxes are the collection and filing of tax taking

importance and maintaining all the activities of the tax

payers. Based on the Income the tax payer is paying their

taxes and it is the major responsibility to them. Collection

of tax from the tax payer are using for the welfare of the

Indian economy development sector.

REFERENCES

1) https://www.hdfclife.com/insurance-knowledge-centre/tax-

saving-insurance/Tax-Structure-in-India

2) https://www.bankbazaar.com/tax/penalties-for-not-filing-tax-

how-to-avoid.html

3) http://moneyexcel.com/701/20-types-of-taxes-in-india

4) http://www.economicsdiscussion.net

5) https://taxguru.in/

6) www.google.com

7) Wikipedia

8) IndirectTaxes,,S.Sethurajan & K.Singaravelu, Speed Publishers

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

13

Goods and Service Tax in India S.Karthik

Abstract

The Goods and service Tax plays a vital role in the

Indian economic and also this type of tax are collected from the

tax payer like business peoples when their production depend

on the tax. The goods and services are increasing the tax of the

payer get more Income and the government are also get tax

from the beneficiary.GST create a uniform market throughout

the country from multiple taxes such as excise duty, service tax

in the central level and VAT at the state level.

1. INTRODUCTION

Goods and Services Tax (GST) is an indirect tax

that will be levied on productions, sale and consumption of

goods and services. The use of the GST is that when

applicable it will abolish all indirect taxes.The present

structure of Indirect Taxes is very difficult in India and tax

rates differ from State to State.

The tax payment as ‘Entertainment Tax’ for

watching a movie. We have to pay Value Added Tax

(VAT) on purchasing goods and services. Tax like’s Excise

duties, Import Duties, Luxury Tax, Central Sales Tax, and

Service Tax. GST bring uniformity and reduce the

cascading effect of these taxes by giving input tax credit.

GST objectives:

1. Improvement in the competitiveness of the original

Assistant Professor in Commerce,

Bishop Ambrose College, Coimbatore.

Mob. No: 90037483480,

goods and services, thereby improving the GDP rate

too.

2. Availability of input credit across the value chain.

3. Decrease the complications in tax administration

and compliance.

4. Making a law involving all the tax bases, laws and

administration procedures across the country.

5. Reduce the unhealthy competition among the states

due to taxes and revenues.

6. Adaptation mechanisms and trained staff.

7. The double registration might annoy people. Also,

these registrations result in increase compliances and

cost.

8. Uninformed estimate of the exact impact of GST.

9. No proper mechanisms to control tax evasion

2. IMPORTANCE OF GOODS AND SERVICES TAX

Goods and Services Tax (GST) is an indirect tax

that will be levied on manufacture, sale and consumption of

goods and services. The importance of the GST is that when

applicable it will abolish all indirect taxes. Hence the entire

system of taxation will be simpler.

The previous Government brought a Bill in

the Lok Sabha in 2011, but failed to get it passed. The NDA

Government introduced a “slightly modified” version of the

Bill in Lok Sabha last December. It was completed on May

6, 2016 but for GST to become a reality, the Bill must be

cleared by two-thirds majority by both Houses, and ratified

by 50% of states. It is now pending in the Rajya Sabha.

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

14

The structure of Indirect Taxes is very complex

in India and tax rates differ from State to State. We payment

of ‘Entertainment Tax’ for watching a movie. We have to

pay Value Added Tax (VAT) on purchasing goods and

services. And there are Excise duties, Import Duties, Luxury

Tax, Central Sales Tax, Service Tax. GST will bring

uniformity and reduce the cascading effect of these taxes by

giving input tax credit.

GST subsumes many indirect and central levies and allows

a producer to claim credit for taxes paid on all inputs,

making production efficient. This is expected to reduce the

cost for consumers.

3. FEATURES OF GST

Subsume following indirect taxes:-

Central Excise duty,

Central Indirect Taxes

Additional duties of excise

CVD&SAD)

Excise duty levied under Medicinal and Toiletries

Preparation Act

Surcharge and Cess .

Service Tax

State Indirect Taxes

VAT/CST

Purchase tax

Entry tax

Octroi

Surcharge and Cess.

GST will have two components comprising

Central GST (CGST)

State GST (SGST)

An additional Tax of 1%

State Taxable supply of Goods by State of Origin and

it would be non CENVATABLE. The additional tax on

supply of goods shall be assigned to the States from where

such supplies originate.

All goods or services

State Excise plus VAT -Alcohol for human

consumption

Electricity Duty -Electricity

Stamp Duty plus Property Taxes -Real Estate

Petroleum Products

Codification is to be specified

It’s all goods and services in the purposed GST

structure. HSN code can be used for classification of goods

and existing accounting code can be used for classification

of services.

Removes

Effect of taxation.

Basics of GST – Implementation In India

Goods and services are the dual system currently India

has a taxation of, it is quite different from dual GST. Taxes

on goods are described as “VAT” Central and State level. It

has adopted value added tax with input tax credit

mechanism for the taxation of goods and services,

respectively, with limited cross-levy set-off.

4. MODELS OF GST

There are three prime models of GST:

Central (Union) Government Level only

State Government Level only

Union and State Government Levels

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

15

GST work in India:

In a first of its kind initiative, the GST will be

implemented in two components – Central GST or

CGST and State GST or SGST. This dual GST

will be levied on all the supply of goods and

services across the country.

Therefore, if there is a sale within the State, then

the both CGST and SGST will be charged.

However, if the sale is outside the State, then only

the Intra-State GST will be levied by the Centre.

CGST is doing away with indirect taxes such

Central Excise Duty, Service Tax, Addl. Customs

Duty, Special Addl. Customs Duty as well as

Addl. Excise Duty. These indirect taxes are those

that are collected by the Centre.

SGST will remove indirect taxes on goods and

services which are charged by the State such as

VAT, Entertainment Tax, Purchase Tax, Octroi,

Luxury Tax and Entry Tax.

The credits of Input Tax of CGST will be

accessible for settling the output of CGST liability

at every stage. Likewise, in the States, the credits

of SGST taken on the inputs will be made

available for clearing the output of SGST’s

liability at each stage.

GST Rates Reduced from 12% to 5% on 10-11-2017

1. Desiccated coconut

2. Narrow woven fabric including cotton newar [with no

refund of unutilised input tax credit]

3. Idli, dosa butter

4. Finished leather, chamois and composition leather

5. Coir cordage and ropes, jute twine, coir products

6. Fishing net and fishing hooks

7. Worn clothing

8. Fly ash brick

List of all Goods Covered under GST 12%

The GST Council, decision-making body for the

new tax, has fixed the tax framework under the Goods and

Services Tax (GST) which is to be rolled out this July 1.

Tax rates have been finalized for 1,211 items with a

majority of items being kept under the 18 per cent slab.

GST Rates Reduced from 18% to 12% on 10-11-

2017

1. Refined sugar & sugar cubes

2. Medicinal grade oxygen

3. Printing ink

4. Hand bags and shopping bags of jute and cotton

5. Milk

6. Hats

7. Parts of specified agricultural, horticultural,

forestry, harvesting or threshing machinery

8. Specified parts of sewing machine

9. Pasta

10. Curry paste, mayonnaise and salad dressings,

mixed condiments and mixed seasoning

11. Diabetic food

12. Spectacles frames

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

16

13. Furniture wholly made of bamboo or cane

GST Rates from 12% to 5% on 10-11-2017

1. Idli, dosa batter

2. Finished leather, chamois and composition leather

3. Coir cordage and ropes, jute twine, coir products

4. Desiccated coconut

5. Narrow woven fabric including cotton newar [with

no refund of unutilised input tax credit]

6. Fishing net and fishing hooks

5. CONCLUSION

GST plays a vital role in the Indian government

and the collection of tax amount are increase when the tax

updating coming likewise peoples get problems when

paying the GST at the same time business peoples and

trading peoples like small, medium and large all the peoples

getting affect of the GST. Government have to take step

decrees the tax amount then only the people can get wealth

in their business level.

6. REFERENCES

1. www.quora.com

2. https://gst.caknowledge.in/

3. www.google.com

4. Wikipedia

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

17

An Improvised Energy-Efficient LEACH for

Wireless Sensor Network

A.Krishnakumar1, Dr. V. Anuratha2

Abstract

Wireless Sensor Network (WSN) becomes an

emerging research area in recent years because of its easy

accessible nature. The Sensor nodes are combined to form a

cluster through which the collected information are

transferred to the Base Station (BS). The clusters are headed

by Cluster Head (CH) which is a normal sensor node.

However, the CH expends more energy level than the

member nodes for its processes which reduces the lifetime of

the network. To improvise the efficiency, the protocol

Energy-Efficient LEACH (EE-LEACH) is proposed. The CH

election is proposed in this protocol and it follows the other

activities as like as LEACH protocol. The evaluation result

shows the effectiveness of the approach used in EE-LEACH

protocol compared to the existing protocols.

1. INTRODUCTION

The sensors are attaining the peak of research in

recent period. Nowadays, the sensors are becoming an

important source in daily life which also creates the need

of developments and updates in tools and algorithms for

the sensor network. Whenever the WSN is under

discussion, the efficiency of utilising the energy (battery)

1.Krishnakumar,

Research Scholar,

2.Dr.V.Anuratha, Head,

Department of PG Computer Science,

Sree Saraswathi Thyagaraja College,

Pollachi.

of a sensor node becomes a top priority.

As long as the sensor node utilising the minimal

energy the lifetime of the network is improved. Therefore,

the energy efficiency in WSN is a serious task. The sensor

nodes are commonly deployed in an area where the human

involvements are very less. The sensor node has to collect

the information like heat, light, and so on from the

environment and forwards it to the BS. As of the dynamic

nature of the sensor nodes the node may long enough to

forward the collected data to the BS. In such situations, the

sensor node forwards the collected data to the nearby

neighbour node. The neighbour node forwards the data to

the BS or other neighbour node. Finally, the data reached

the destination. In this approach, the source sensor node

forwards the data to the neighbour node without analysing

that the node is closer to BS or not which may increase the

difficulties in reaching the data and the source node does

not consider whether the data is reached to the BS or not.

Likewise, there are some other issues which degrade the

performance of the WSN.

To resolve the above discussed issues,

Heinzelman et al., (2000) introduced Low-Energy

Adaptive Clustering Hierarchy (LEACH) protocol in

which the sensor nodes are grouped as clusters. The

clusters are formed based on probability function of

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

18

LEACH protocol. The probability function or threshold

function is detailed in Eq1.

Where T denotes threshold, n denotes number of

nodes, p denotes probability value. In LEACH the CH is

elected based on the random selection of number. Each

node chosen it value between zero (0) and one (1). Then

the node which holds lesser value than the threshold

function value is elected as CH. Suppose, more than a node

has a lesser value then the node which announces first that

it reaches the lesser value is elected as CH.

The CH then forwards the signal to its neighbour

nodes that it has been elected as CH and asks the

neighbours to join as member nodes. Also, the CH is

incharge for collecting the information from the

environment, aggregating it and forwarding to BS.

Therefore, in comparison to the member nodes the CH

needs more efficiency to complete all the tasks. The cluster

without CH or with a drained CH becomes useless until the

election of another CH. In LEACH protocol the CH is

elected in a round robin basis in which the node which is

elected as CH cannot act as CH for the next round.

LEACH follows Time Division Multiple Access (TDMA)

for round robin.

LEACH follows a convenient cluster formation,

TDMA schedule and so on however; the protocol fails in

electing energy efficient CH. To improvise the CH

election, EE-LEACH is proposed in which an efficient CH

election is attained than the existing protocols.

The section II discusses the review of literature

in which the other existing protocols are discussed. The

proposed protocol EE-LEACH is discussed in section III

where the proposed energy efficient radio model and vice-

CH election are discussed. Section IV discusses the

evaluation results of the proposed protocol and section V

concludes with conclusion and future enhancements.

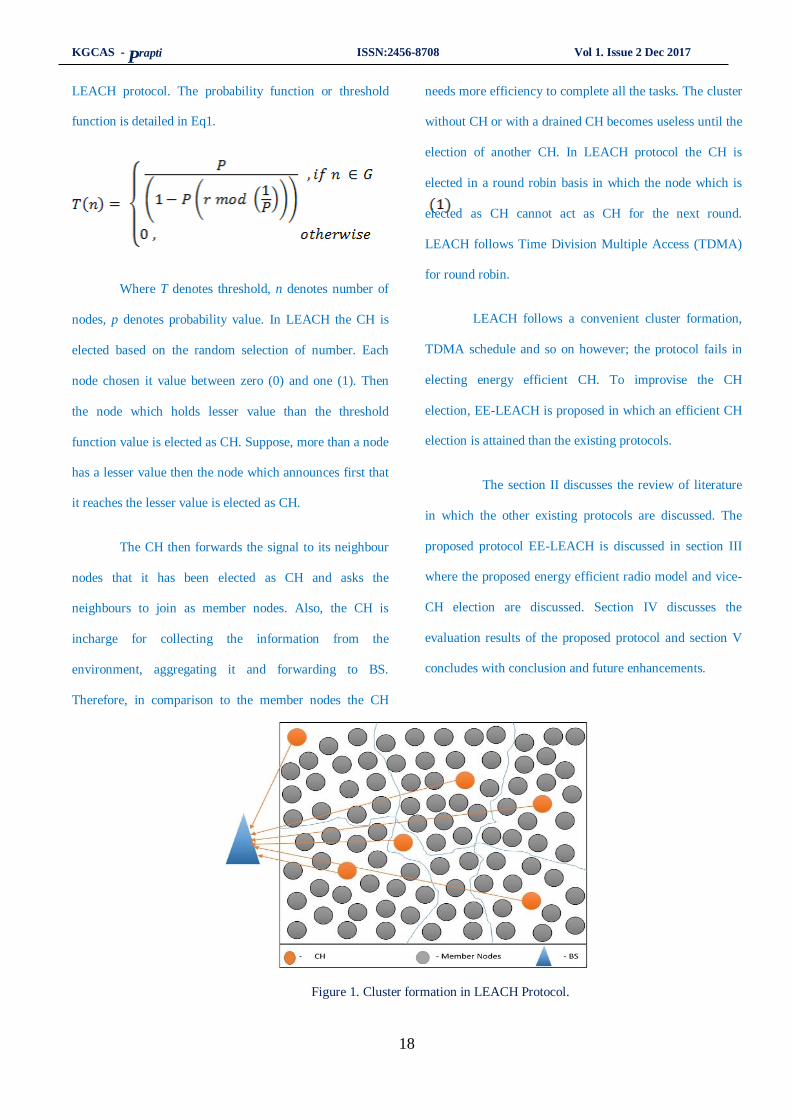

Figure 1. Cluster formation in LEACH Protocol.

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

19

Figure 1 shows the cluster formation in LEACH

protocol in which each CH forwards the collected

information from its member nodes to BS.

II. REVIEW OF LITERATURE

Al-Baz & El-Sayed (2017) proposed a new

algorithm for cluster head selection. The algorithm

selects the CH based on its distance and residual energy.

The algorithm also follows a better cluster formation

approach in which the single node cluster formations are

identified as well as rectified. However, the algorithm

lacks in improvising the network lifetime because of not

following the LEACH’s TDMA schedule. The energy

expends for the CH election may reduce because of

relaxing the TDMA schedule but still the rotation of CH

in each round improvise the lifetime and performance of

the network. The algorithm also lacks in intra cluster

communication because of maintaining the same sensor

node for collection of data from the member nodes and

forwarding to BS.

Umar et al., (2017) designs a dynamic re-

clustering LEACH protocol in which the CH is elected

in a dynamic manner. Whenever the energy of a CH

expends to a certain range then the CH election is called

on. The new CH is elected based on its residual energy.

The node which holds high energy level is elected as

CH for the next rounds. LEACH’s TDMA is remodified

according the proposed protocol. The proposed protocol

achieves energy efficiency for a small area network but

for a large area network the proposed protocol fails in

addressing the energy efficient CH election node. In

addition, the dynamic CH election needs to reform the

routing table and routing algorithm to be update fast to

maintains the connectivity which also reduces the

energy level of the CH to some extent.

Bongale et al., (2017) proposed Energy influenced

probability based LEACH protocol. The protocol elects the

CH based on the probability value of the proposed protocol.

Each sensor node is given a probability value based on the

residual energy level. The high residual energy level sensor

node is given a high probability value and low residual

energy level sensor node is assigned with a low probability

value. This probability value is assigned in each round so

that the CH node can be easily elected based on the

probability value. The probability value is also calculated

based on the expending level of energy at each round. The

sensor node which expends minimum energy is given a

higher probability than the node which expends more

energy. The protocol focused in CH election and not

consider effective cluster formation, better data

transmission and so on which drains the energy level in

ease.

Yang et al., (2017) proposed a clustering

algorithm for energy efficient management in WSN in

which the cluster formation is considered as highest

priority than the CH election. The CH is elected based

on the distance parameter and residual energy level. The

sensor node which maintains lesser distance to BS and

highest residual energy is identified and elected as CH.

The elected CH announces its election to the neighbour

nodes and asks to join. The radius which CH forwards

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

20

the message is longer than the radius of the sensor node.

Therefore, the CH can form with more number of

member nodes and reduces the election of more CH and

cluster formation. The clusters are formed with more

number of nodes which is useful in collecting the

information but it leads to data congestion. The

proposed algorithm lacks in resolving the data

congestion.

Rad et al., (2017) proposed Improved W-

LEACH routing protocol in which the LEACH

protocol’s threshold function is modified to elect the CH

based on the residual energy and the number of

neighbour nodes. The proposed protocol focused in

number of neighbours’ parameter than the residual

energy of a node. The sensor node which holds higher

number of neighbour nodes is elected as CH. This CH

election leads to drains the energy level of CH in

collecting the data form the neighbour node. The

protocol also not follows the TDMA schedule which

also drains the energy level of the sensor node in ease.

3. PROPOSED PROTOCOL

This section details the proposed protocol EE-

LEACH. This proposed protocol focused in designing the

CH election based on the residual energy of a node and

distance parameter. The distance parameter is used in two

ways to form better cluster. This proposed protocol elects

two CHs called: i) CH and ii) Vice-CH.

The CH is in charge for collection and

aggregation of information from the member nodes. As

well as, the vice-CH is in charge to forwards to collected

information to BS.

The distance parameter is considered as distance to

BS for election of CH and distance between neighbours for

election of vice- CH. The residual energy acts as same in

both elections.

1. Inter-cluster communication

The inter-cluster communication of this proposed

protocol forwards the aggregated information from

the vice-CH to the BS or to the neighbour node which

is nearer to BS. For inter-cluster communication, this

proposed protocol elects energy efficient CH using

Eq. 2 and Eq. 3.

a) Residual Energy

The residual energy is identified as in Eq. 2.

Where, present denotes the present energy level of

a node whereas preset denotes the maximum energy level

of a node.

b) Distance to BS

The distance to BS is identified as in Eq. 3.

Where, distancenode denotes distance of a node and

distancefaraway denotes distance of the faraway node

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

21

2. Intra-cluster communication

The intra-cluster communication of this proposed

protocol collects the data form the member nodes and

aggregates the data and forward it to CH by vice-CH. The

vice-CH is elected using Eq. 2 and Eq. 4.

a) Distance between neighbours

The distance between neighbours is identified as in

Eq. 4.

(4)

Where, distancenode denotes distance of a node and

distancemaximum denotes maximum distance node.

This proposed protocol elects’ CH and vice-CH as

per LEACH’s TDMA schedule. The probability

function of LEACH protocol is modified as in Eq. 5.

(inter-cluster) and Eq.6.(intra-cluster).

and

4. EVALUATION RESULTS

This Protocol EE-LEACH is proposed to achieve the energy efficiency in sensor nodes to extend the lifetime of the network.

This proposed protocol is evaluated with the existing protocol Improved_W-LEACH using Network Simulator 2 (NS2). The

simulation environment parameters are detailed in Table 1.

Table 1. Simulation Parameters

Parameters Value

Number of Nodes 100 (0-99)

Initial energy 1Joule

BS node 100

Packet size 500 bytes

Maximum

simulation time 400 seconds

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

22

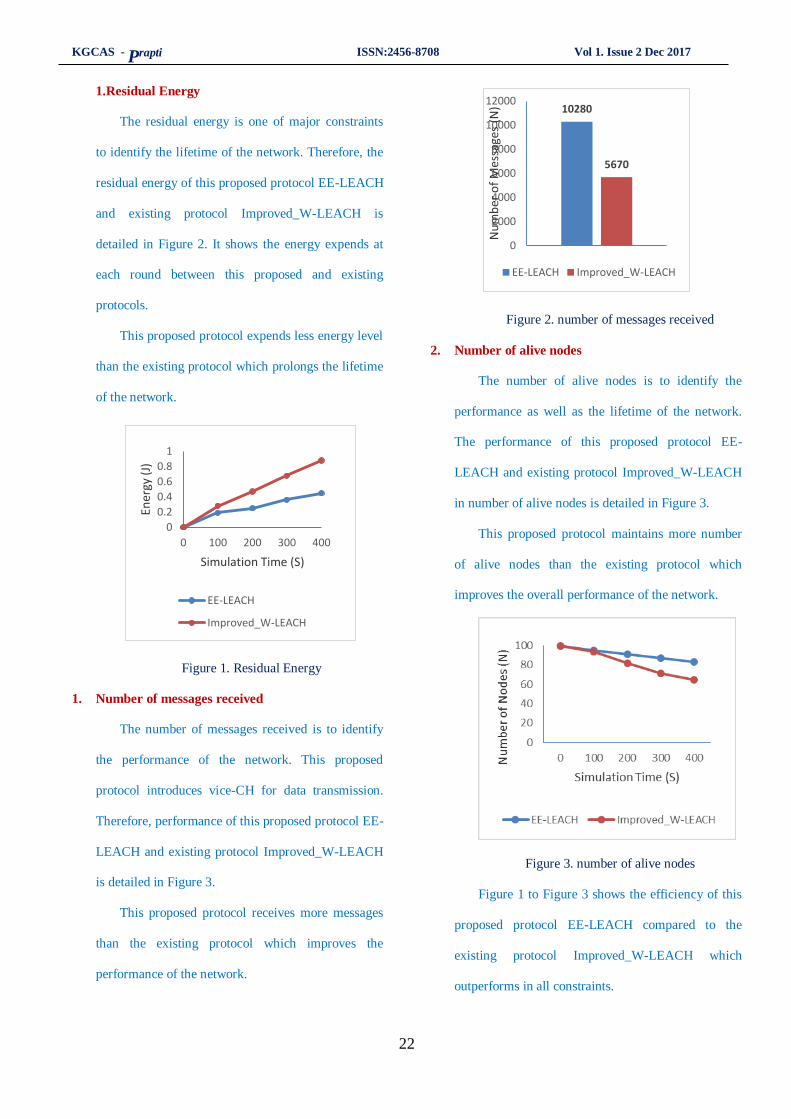

1.Residual Energy

The residual energy is one of major constraints

to identify the lifetime of the network. Therefore, the

residual energy of this proposed protocol EE-LEACH

and existing protocol Improved_W-LEACH is

detailed in Figure 2. It shows the energy expends at

each round between this proposed and existing

protocols.

This proposed protocol expends less energy level

than the existing protocol which prolongs the lifetime

of the network.

0

0.2

0.4

0.6

0.8

1

0 100 200 300 400

Ener

gy (

J)

Simulation Time (S)

EE-LEACH

Improved_W-LEACH

Figure 1. Residual Energy

1. Number of messages received

The number of messages received is to identify

the performance of the network. This proposed

protocol introduces vice-CH for data transmission.

Therefore, performance of this proposed protocol EE-

LEACH and existing protocol Improved_W-LEACH

is detailed in Figure 3.

This proposed protocol receives more messages

than the existing protocol which improves the

performance of the network.

10280

5670

0

2000

4000

6000

8000

10000

12000

Nu

mb

er o

f M

essa

ges

(N)

EE-LEACH Improved_W-LEACH

Figure 2. number of messages received

2. Number of alive nodes

The number of alive nodes is to identify the

performance as well as the lifetime of the network.

The performance of this proposed protocol EE-

LEACH and existing protocol Improved_W-LEACH

in number of alive nodes is detailed in Figure 3.

This proposed protocol maintains more number

of alive nodes than the existing protocol which

improves the overall performance of the network.

Figure 3. number of alive nodes

Figure 1 to Figure 3 shows the efficiency of this

proposed protocol EE-LEACH compared to the

existing protocol Improved_W-LEACH which

outperforms in all constraints.

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

23

V. CONCLUSION

The improvements in WSN creates the need of energy efficient CH to prolong the lifetime of the network. This

proposed protocol EE-LEACH concentrates in electing CH which carries the aggregated information to BS and this protocol

introduces the vice-CH which is concentrates in collecting and aggregating the information from the member nodes. This

approach improves the performance and prolongs the lifetime of the network. The evaluation results prove the performance

of the proposed protocol EE-LEACH. The future development is to improve the vice-CH functionalities such as cluster

formation, cluster movement and so on.

REFERENCES

1. Heinzelman, W. R., Chandrakasan, A., &

Balakrishnan, H. (2000, January). Energy-efficient

communication protocol for wireless microsensor

networks. In System sciences, 2000. Proceedings of

the 33rd annual Hawaii international conference on

(pp. 10-pp). IEEE.

2. Al‐Baz, A., & El‐Sayed, A. (2017). A new algorithm

for cluster head selection in LEACH protocol for

wireless sensor networks. International Journal of

Communication Systems.

3. Umar, S., Subbarayudu, Y., Kumar, K. K., &

Bashwanth, N. (2017). Designing of Dynamic Re-

clustering Leach Protocol for Calculating Total

Residual Time and Performance. International

Journal of Electrical and Computer Engineering

(IJECE), 7(3).

4. Bongale, A. M., Swarup, A., & Shivam, S. (2017,

February). EiP-LEACH: Energy influenced

probability based LEACH protocol for Wireless

Sensor Network. In Emerging Trends & Innovation

in ICT (ICEI), 2017 International Conference on (pp.

77-81). IEEE.

5. Yang, S. S., Shim, J. S., Jang, Y. H., Ju, Y. W., &

Park, S. C. (2017). Design of Clustering Algorithm

for Efficient Energy Management in Wireless Sensor

Network Environments. In Advanced Multimedia and

Ubiquitous Engineering (pp. 607-612). Springer,

Singapore.

6. Rad, F., Moghtaderinasab, Z., & Parvin, H. (2017).

An Improved W-LEACH Routing Protocol in

Wireless Sensor Network. Journal of Advances in

Computer Research, 8(2), 39-51.

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

24

A Study on Account Holders Satisfaction

towards Service Rendered by Keeranatham

Agricultural Credit Society, Coimbatore L.Lovely Lourds Preethi,

Abstract

Agriculture is the back bone of our country. Many

villages are based on the income they receive from agriculture

only. But for doing agriculture in now a days the villagers

don’t get much capital. For this problem the Government

started co-operative banks thought the country. The villagers

doing agriculture around the village, Keeranatham was

affected by insufficiency of finance from banks, so they

requested government to start a separate agriculture bank in

their area. As per the farmers request the government started

this bank to provide short term loans, loans with low interest,

quality seeds and good agricultural banking service to the

farmers and develop their income from agriculture.

1. INTRODUCTION

There are 4,595 Primary Agricultural Cooperative Banks at

the village level, providing short term and medium term

credit facilities to the agriculturists. These banks have

covered as on 31.3.02 85.96% of the agricultural

operational holdings in the State of which 79.57% belong to

weaker sections. Distinguishes between agricultural service

cooperatives, which provide various services to their

individually farming members, and agricultural production

cooperatives, where production resources (land, machinery)

are pooled and members farm jointly.

Assistant Professor,

Department of Commerce,

Bishop Ambrose College,

Coimbatore.

Agricultural production cooperatives are relatively rare in

the world, and known examples are limited to

collective in former socialist countries and the kibbutzim in

Israel.

The default meaning of agricultural cooperative in English

is usually an agricultural service cooperative, which is the

numerically dominant form in the world. There are two

primary types of agricultural service cooperatives, supply

cooperative and marketing cooperative. Supply cooperatives

supply their members with inputs for agricultural

production, including seeds, fertilizers, fuel, and machinery.

Marketing cooperatives are established by farmers to

undertake transformation.

The co-operative movement, which is the largest socio-

economic movement in the world, has contributed

significantly to the alleviation of poverty, creation of

productive employment as well as the enhancement of

social integration in the country. The co-operative sector is

mainly concerned with agricultural credit, marketing of

agricultural produce and distribution of fertilizers and

pesticides and other essential commodities.

SHORT-TERM LOANS

The co-operative credit institutions were evolved mainly to

check the spurious practices of the moneylenders and to

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

25

provide access to credit to various sections of the population

at reasonable rates of interest. The short term credit

structure in Tamil Nadu has a three-tier structure,

comprising of the Tamil Nadu State Apex Co-operative

Bank, (TNSCB) with 41 branches at the state level, 23

District Central Co-operative Banks (inclusive of one

Industrial Co-operative bank) with 750 branches at the

district level and around447 Primary Agricultural Credit

Societies (PACS) at the grassroot level, catering to the

needs of the farmers in 16317 villages (as on 31.3.2005).

The short term and medium term agricultural loans

provided by the Primary Agricultural Co-operative Banks

during the Tenth Five Year Plan wereRs.5043.93 crore and

Rs.291.51 crore as against the Target of Rs.7500 crore for

Short term and Rs. 625 crore for medium term respectively.

The short fallin achieving the target in short term credit

supply is mainly due to the continuous drought conditions

that prevailed in the state from 2002-03 to2004-05.

LONG TERM LOANS

The Tamilnadu Co-operative State Agriculture and

Rural Development Bank (TNSCARDB) at the state level

and Primary Co-operative Agricultural and Rural

Development banks (PCARDB) at the Taluk / Block level

constitute the two tiers of the long-term credit structure.

These banks provide loans totheir members for

operations related to agriculture and allied activities like

minor irrigation, cultivation of horticulture and Plantation

crops, poultry keeping, dairying, sheep breeding, sericulture

and purchase of tyre carts, tractors, power tillers, laying of

pipelines, construction of cattle shed, farmhouse etc, on a

schematic basis.

The Tamilnadu Co-operative State Agricultural

Rural Development Bank mobilizes the funds required for

loaning operations through floating of Special Development

Debentures. The Central, State Governments and NABARD

subscribe to these debentures.

Company Profile:

Keeranatham primary agriculture co-operative loan

society was Registered at 02.06.1930 and the bank activities

was started at 09.06.1930.

This bank functioning under the co-operative

societies act 1983 and rules 102 (8) of Tamilnadu societies

Rules 1988. The bank is placed under “B” class for the year

under Audit.

There were members 972 at the end of the year as

against 1304 at the beginning of the year. The share capital

of the members amounted to Rs 6, 30,940 againstRs ,56,405

at the beginning of the year.

The value of stock at the beginning of the year was

1,17,357.68 stock of the value of Rs 34,64,627.40 bought

during the year less purchase excluding sales return etc.

amounted to Rs 36,36,569.20. The value of closing stock at

the end of the year was 1, 4,427.47. Net profit should be

disbursed in accordance with the Act rules and by laws of

the society.

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

26

2. OBJECTIVE OF THE STUDY:

The objectives of the study are:

To study the account holders satisfaction towards

service rendered by bank.

To find out the problems related to A/c holders

To find out the influencing factors of the A/c holders

To offer suggestions to growth and development of

the bank.

3. SCOPE OF THE STUDY:

The study has been under taken:-

To assess the banks real position while providing

services to their customers.

To understand the Account holders satisfaction level

and provide solutions for their problems.

To know the real situation of the bank while

implementing new policies and loans.

To understand the Account holders expectations and

fulfill their needs from this study.

4. LIMITATIONS OF THE STUDY:

Limitations of the study are:

The respondents of this bank would not have

reveled negative issues of the bank.

The satisfaction level of the Account holders

change from time to time, Hence the result of the

project may not be applicable in the long run.

The information provided by the respondents would

be biased to certain extent.

Science most of the respondents are from rural areas

and they would not be exposed to good banking

service, hence they would think the present services

provided by this bank is the best.

5. RESEARCH METHODOLOGY:

RESEARCH DESIGN:

Research design is the basic frame work which

provides guideline for the rest of research process. It

specifies the methods of data collection and analysis. In this

study descriptive research designing is used.

DESCRIPTIVE RESEARCH DESIGN

Descriptive research design describes the Account

holder’s satisfaction towards service rendered by

Keeranatham primary agriculture bank. The main purpose

of this is to setting knowledge about to subject.

POPULATION

The population (952) specifies that the Account

holders atKeeranatham primary agriculture loan society.

SAMPLING DESIGN:

Sampling size:

This study contains 110 Account holders as

sample size.

DATA COLLECTION METHOD:

For this study two types of data were collected. One is

primary data and another One is the secondary data.

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

27

Primary data:

The Primary data were collected for the first time and

thus happen to be Original in character. Primary data were

collected through distributing questionnaire to the

respondents.

Secondary data:

The secondary data were already available in the

records of the bank. The Company profile and Account

holder’s details are secondary data of the bank.

6. STATISTICAL TECHNIQUES USED:

Percentage method:

The number of respondents of each category is

summarized to percentage for the convenience to the other

statistical tools namely pie chart, and bar Diagrams.

Chi square:

It is used to find the relationship between two

items.

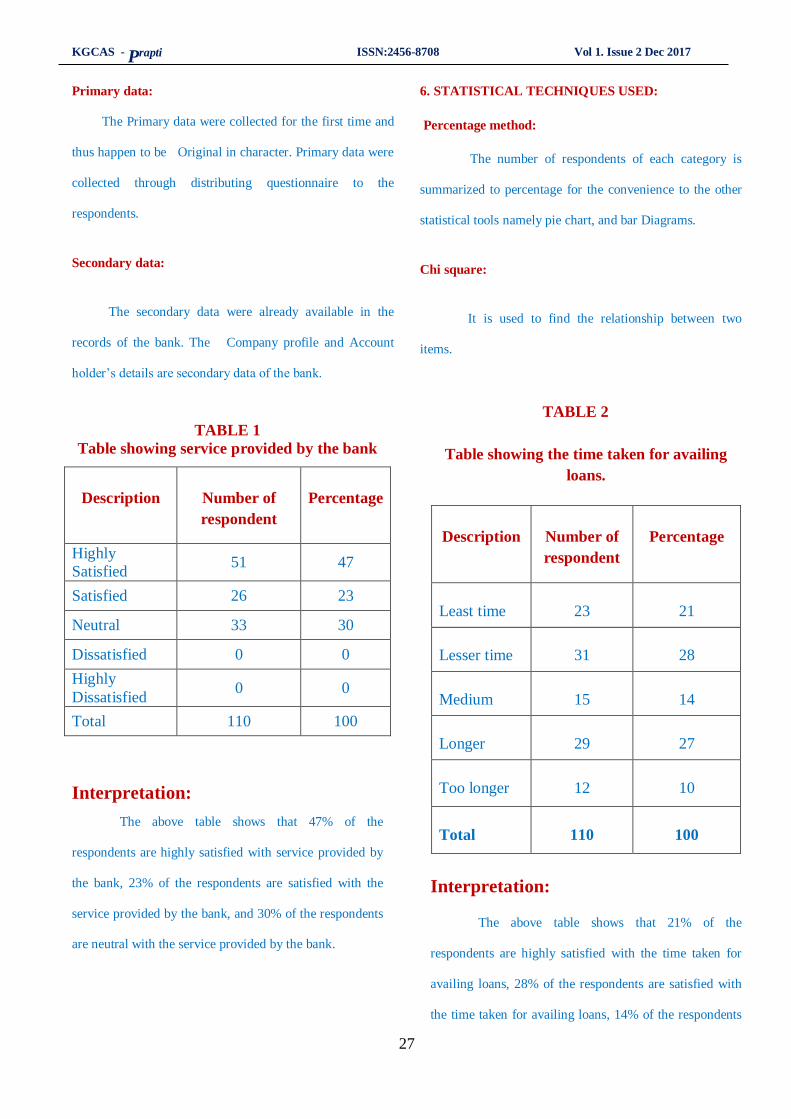

TABLE 1

Table showing service provided by the bank

Description

Number of

respondent

Percentage

Highly

Satisfied 51 47

Satisfied 26 23

Neutral 33 30

Dissatisfied 0 0

Highly

Dissatisfied 0 0

Total 110 100

Interpretation:

The above table shows that 47% of the

respondents are highly satisfied with service provided by

the bank, 23% of the respondents are satisfied with the

service provided by the bank, and 30% of the respondents

are neutral with the service provided by the bank.

TABLE 2

Table showing the time taken for availing

loans.

Description

Number of

respondent

Percentage

Least time

23

21

Lesser time

31

28

Medium

15

14

Longer

29

27

Too longer

12

10

Total

110

100

Interpretation:

The above table shows that 21% of the

respondents are highly satisfied with the time taken for

availing loans, 28% of the respondents are satisfied with

the time taken for availing loans, 14% of the respondents

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

28

are neutrally with the time taken for availing loans, 27%

of the respondents are dissatisfied with the time taken for

availing loans and 10% of the respondents are highly

dissatisfied with the time taken for availing loans from

this bank.

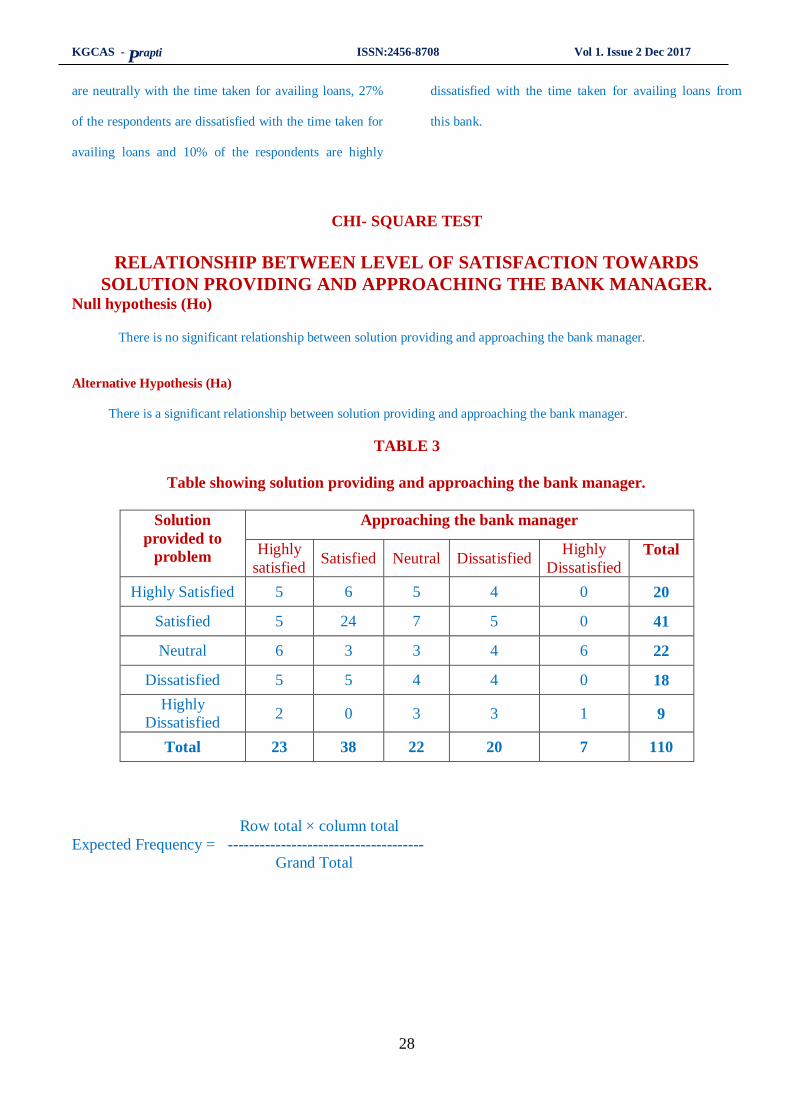

CHI- SQUARE TEST

RELATIONSHIP BETWEEN LEVEL OF SATISFACTION TOWARDS

SOLUTION PROVIDING AND APPROACHING THE BANK MANAGER. Null hypothesis (Ho) There is no significant relationship between solution providing and approaching the bank manager.

Alternative Hypothesis (Ha)

There is a significant relationship between solution providing and approaching the bank manager.

TABLE 3

Table showing solution providing and approaching the bank manager.

Solution

provided to

problem

Approaching the bank manager

Highly

satisfied Satisfied Neutral Dissatisfied

Highly

Dissatisfied

Total

Highly Satisfied 5 6 5 4 0 20

Satisfied 5 24 7 5 0 41

Neutral 6 3 3 4 6 22

Dissatisfied 5 5 4 4 0 18

Highly

Dissatisfied 2 0 3 3 1 9

Total 23 38 22 20 7 110

Row total × column total

Expected Frequency = -------------------------------------

Grand Total

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

29

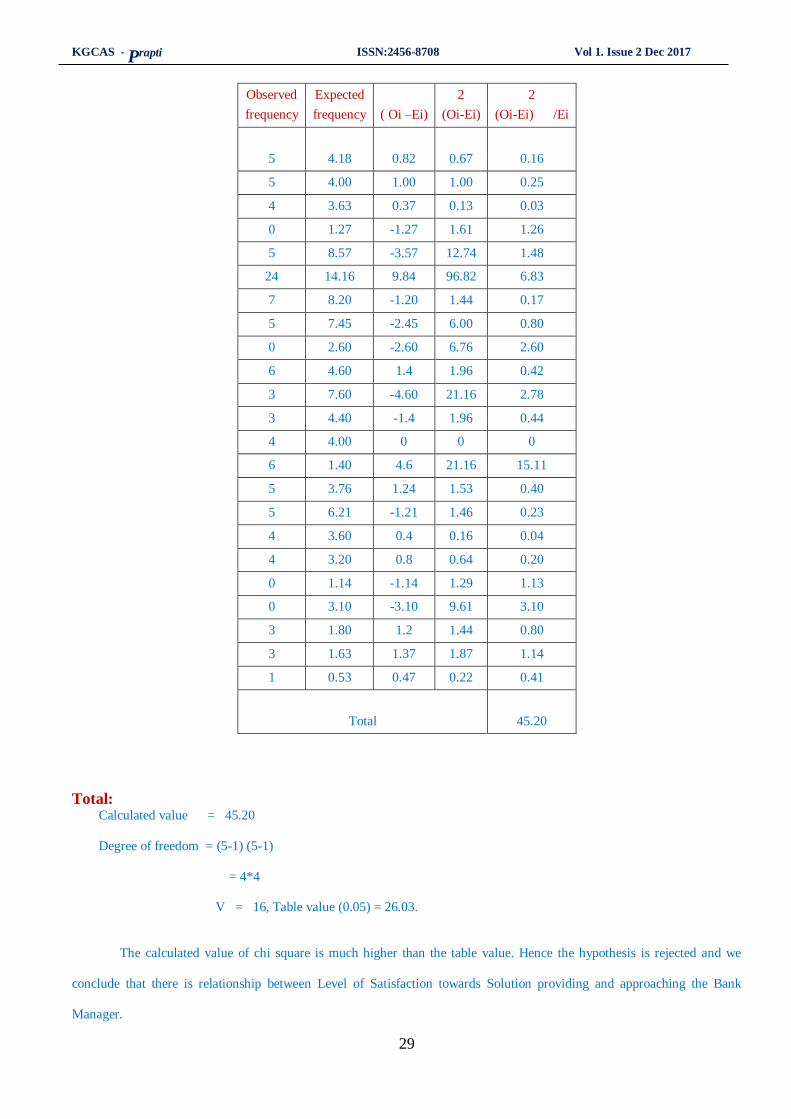

Observed

frequency

Expected

frequency

( Oi –Ei)

2

(Oi-Ei)

2

(Oi-Ei) /Ei

5

4.18

0.82

0.67

0.16

5 4.00 1.00 1.00 0.25

4 3.63 0.37 0.13 0.03

0 1.27 -1.27 1.61 1.26

5 8.57 -3.57 12.74 1.48

24 14.16 9.84 96.82 6.83

7 8.20 -1.20 1.44 0.17

5 7.45 -2.45 6.00 0.80

0 2.60 -2.60 6.76 2.60

6 4.60 1.4 1.96 0.42

3 7.60 -4.60 21.16 2.78

3 4.40 -1.4 1.96 0.44

4 4.00 0 0 0

6 1.40 4.6 21.16 15.11

5 3.76 1.24 1.53 0.40

5 6.21 -1.21 1.46 0.23

4 3.60 0.4 0.16 0.04

4 3.20 0.8 0.64 0.20

0 1.14 -1.14 1.29 1.13

0 3.10 -3.10 9.61 3.10

3 1.80 1.2 1.44 0.80

3 1.63 1.37 1.87 1.14

1 0.53 0.47 0.22 0.41

Total

45.20

Total: Calculated value = 45.20

Degree of freedom = (5-1) (5-1)

= 4*4

V = 16, Table value (0.05) = 26.03.

The calculated value of chi square is much higher than the table value. Hence the hypothesis is rejected and we

conclude that there is relationship between Level of Satisfaction towards Solution providing and approaching the Bank

Manager.

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

30

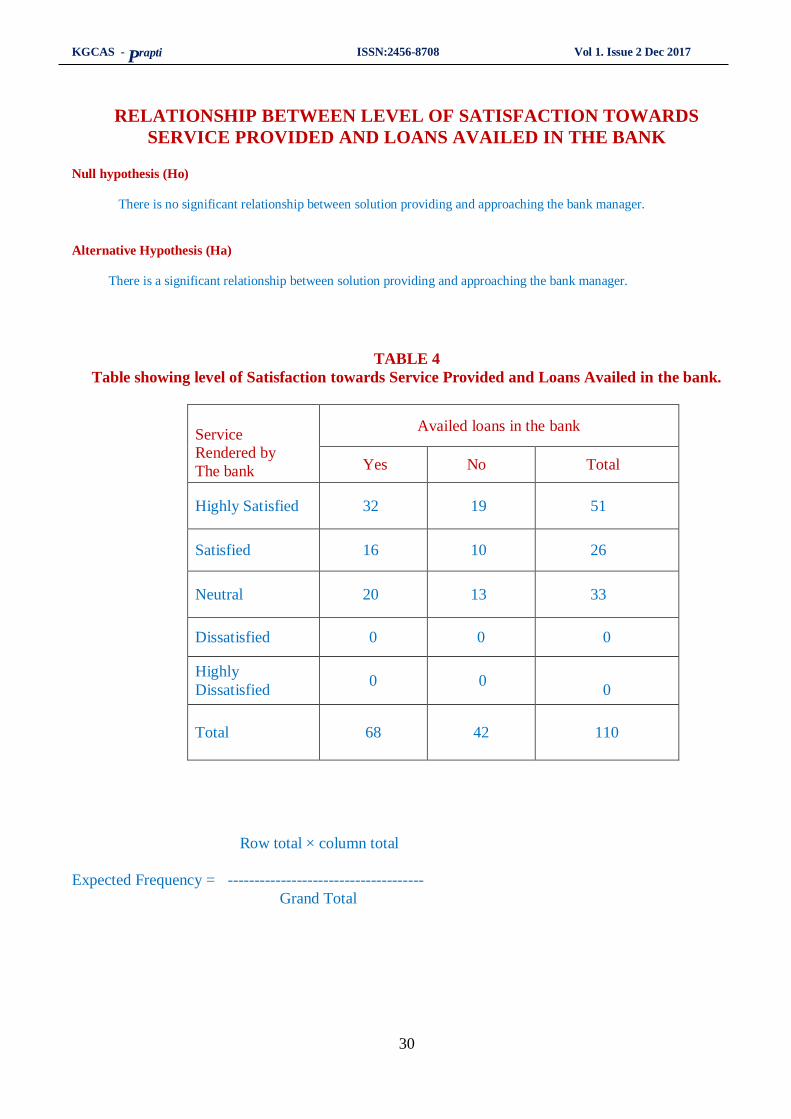

RELATIONSHIP BETWEEN LEVEL OF SATISFACTION TOWARDS

SERVICE PROVIDED AND LOANS AVAILED IN THE BANK

Null hypothesis (Ho)

There is no significant relationship between solution providing and approaching the bank manager.

Alternative Hypothesis (Ha)

There is a significant relationship between solution providing and approaching the bank manager.

TABLE 4

Table showing level of Satisfaction towards Service Provided and Loans Availed in the bank.

Service

Rendered by

The bank

Availed loans in the bank

Yes No Total

Highly Satisfied 32 19 51

Satisfied 16 10 26

Neutral 20 13 33

Dissatisfied 0 0 0

Highly

Dissatisfied 0 0

0

Total

68

42

110

Row total × column total

Expected Frequency = -------------------------------------

Grand Total

KGCAS - Prapti ISSN:2456-8708 Vol 1. Issue 2 Dec 2017

31

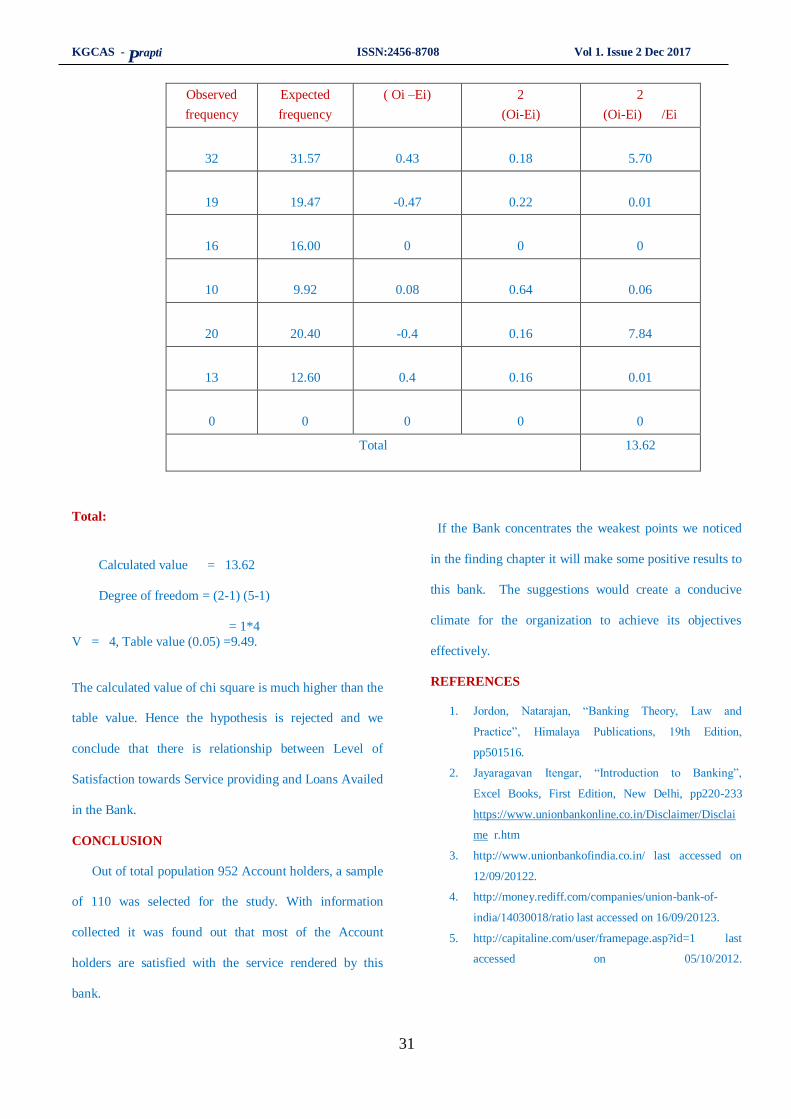

Observed

frequency

Expected

frequency

( Oi –Ei) 2

(Oi-Ei)

2

(Oi-Ei) /Ei

32

31.57

0.43

0.18

5.70

19

19.47

-0.47

0.22

0.01

16

16.00

0

0

0

10

9.92

0.08

0.64

0.06

20

20.40

-0.4

0.16

7.84

13

12.60

0.4

0.16

0.01

0

0

0

0

0

Total 13.62

Total:

Calculated value = 13.62

Degree of freedom = (2-1) (5-1)

= 1*4

V = 4, Table value (0.05) =9.49.

The calculated value of chi square is much higher than the

table value. Hence the hypothesis is rejected and we

conclude that there is relationship between Level of

Satisfaction towards Service providing and Loans Availed

in the Bank.

CONCLUSION

Out of total population 952 Account holders, a sample

of 110 was selected for the study. With information

collected it was found out that most of the Account

holders are satisfied with the service rendered by this

bank.

If the Bank concentrates the weakest points we noticed

in the finding chapter it will make some positive results to

this bank. The suggestions would create a conducive

climate for the organization to achieve its objectives

effectively.

REFERENCES

1. Jordon, Natarajan, “Banking Theory, Law and

Practice”, Himalaya Publications, 19th Edition,

pp501516.

2. Jayaragavan Itengar, “Introduction to Banking”,

Excel Books, First Edition, New Delhi, pp220-233

https://www.unionbankonline.co.in/Disclaimer/Disclai

me r.htm